14

2. FISCAL FEDERALISM: THEORY AND PRACTICE

The normative theory of public finance is largely based on Diamond and

Mirrlees (1971) model of optimal taxation and Atkinson and Stern (1974) model

of optimal public expenditures within the context of a centralized State. However,

when it comes to dealing with in a federal setup, a number of additional elements

such as intergovernmental fiscal transfers, externalities (fiscal and spatial), and

strategic interactions among governments etc., get introduced. This thus, requires

a broader framework for addressing fiscal federalism.

Fiscal federalism inter alia, plays an important role in the implementation

of core elements of the state policy. As allocation, distribution and stabilization

functions are major policy objectives of public finance (Musgrave and Musgrave,

1989), the subsequent sections in this Chapter deal with important elements of the

state policy, and the role of fiscal federalism within the overarching theoretical

framework. Assignment of responsibilities (expenditure and tax), concept of

equalization, determinants of fiscal position, strategic interactions among

constituent units, and fiscal externalities are also discussed in this Chapter. In

addition, the core issues involved in designing intergovernmental fiscal transfers

are also part of this Chapter. Some international experiences in select countries of

fiscal federalism are included as illustrations for the purpose of comparing them

with the Indian system at a later stage.

2.1 CORE ELEMENTS OF THE STATE POLICY

Mainstream public finance literature typically identifies three core

elements of the State (Kaul, 2006):

ª First, as the aggregator of national policy preferences and through the

political process implement policy initiatives (Arrow, 1963). For

efficient provision of social goods, a political process of budget

determination is resorted (Musgrave and Musgrave, 1989). As

resources are often limited, the process involves inter se prioritization

of initiatives for dealing with various issues.

ª Second, correction of market failures and promotion of desired levels

of societal or intergenerational distribution as the overall allocation

and distribution authority.

15

ª Third, based on their unique coercive powers, governments at various

levels impose taxes and collect revenue to pay for planned public

expenditures and put in place regulatory and other measures required

for the society to realize cherished policy goals.

2.2 DECENTRALIZATION VERSUS CENTRALIZATION

Determination of optimal size of jurisdiction for the various public

functions is an important concern. It is said that welfare increases through the

differentiation of public services in accordance with costs and preferences at the

appropriate governmental level. As Oates (1999) puts forth it, ‘‘... we need to

understand which functions and instruments are best centralized and which are

best placed in the sphere of decentralized levels of government’’.

Regarding the allocation function of the public sector, the principle of

fiscal decentralization has been advanced (Musgrave, 1959; Oates, 1972). The

principle of fiscal decentralization is applicable as:

1. Local governments prefer to bear the costs of financing expenditures that help

in meeting the local preferences. As preferences across regions differ, local

governments, therefore, are also in a better position to determine the

expenditure priorities of their inhabitants.

2. Local governments try to balance the benefits of public goods with the costs.

If the marginal cost of local public goods is subsidized by national

governments, local governments tend to overspend on such activities. In order

to address the problem of overspending, degree of spillovers across

jurisdictions needs to be considered.

3. On the other hand, if a public good provides benefits not only locally but also

across jurisdictions, a local jurisdiction may discount some of those benefits

and under provide for that public good. In such a case, there are two options.

Either a higher level of government may be in a better position to provide for

that public good or alternatively, it may need to subsidize local governments'

expenditures.

4. When there are economies of scale in the provision of public goods, these

services can be provided more efficiently at larger scales than in a single local

jurisdiction. In such a case, it may be more appropriate for a higher level of

government to provide for the public good.

16

5. The other side of the coin is raising of revenue. Conventional wisdom

suggests that revenues ought to be raised by taxing the most “immobile” tax

bases. Taxing a mobile factor, it can easily avoid the tax by moving outside

the relevant jurisdiction, thereby leading to a loss in revenues and causing

distortions in the economy. Generally speaking, it is easier for households,

firms, and economic entities to move within a nation than across nations, as

such these factors are less mobile from the perspective of a central

government than from that of a local government. This may be another reason

for central governments to subsidize/ compensate local governments'

expenditures on certain public goods.

6. Local governments also interact strategically, competing to attract and/or hold

a larger share of mobile tax bases. This phenomenon has been known as a

“race to the bottom”. It often leads to poorer quality of public services as

local governments collectively cut tax rates to an unviable proposition.

2.3 ASSIGNMENT OF RESPONSIBILITIES

With these initial insights now, we discuss in more detail expenditure

responsibilities, followed by tax responsibilities.

2.3.1 The Assignment of Expenditure Responsibilities

Public sector functions can be classified into three categories: the

stabilization, distribution, and allocation functions. The stabilization function

refers to smoothing business cycles, reducing inflation and unemployment,

encouraging economic growth, and obtaining other related macroeconomic

objectives. If the economic criteria for assignment are efficiency and equity, it is

typically concluded that the stabilization function should largely be performed by

the central government because the mobility of resources makes it unlikely to

pursue an effective stabilization policy by a lower level of government (Gramlich,

1987). In any case, local governments have limited powers to borrow or to issue

money curtailing any possible stabilization role by them.

Redistribution also largely, belongs to the realm of central government.

Attempts by regional governments to redistribute income are likely to be

disenchanted by the mobility of high-worth individuals and of capital, and any

such attempt to redistribute income will create distortions and inefficiencies in

geographic location (Oates, 1972). Moreover, the unequal and possibly inadequate

17

fiscal capacities of local governments also make centralization desirable on equity

grounds.

However, the allocation function, or the decision to provide kind of

services, is invariably left to local levels of government. These governments can

adapt service levels more closely to the preferences of their citizens, thereby

making available to individuals a wider range of fiscal choices than perhaps,

provided by a straight jacketed provisioning by the central government. This is the

well-known “Subsidiarity Principle”, also sometimes referred to as the

“Decentralization Theorem” (Oates, 1972, 1993, 1999).

Decentralization principle may also not be applicable where the service

has widespread spillovers. National defense is often cited as a classic example.

Environmental quality as well, falls into this category. A second exception may be

cases where provision of services involves economies of scale. An example may

be municipal solid waste: even large cities benefit from sharing a single landfill

rather than procuring their own individually, and even small towns and villages

may benefit from sharing a single conservancy service. In such cases, if there are

multiple levels of government, a middle tier may be more suitable. Alternatively,

local government may on their own form voluntary compacts. These

considerations suggest a “best practice” of assignment of expenditure

responsibilities across different levels of government. Activities such as national

defense, monetary policy, and income redistribution are appropriately assigned to

the central government; activities like police and fire protection, trash collection,

and local roads are assigned to local governments. Of course, the actual practice

on assignment of expenditure responsibilities differs somewhat from these “best

practices”. Nevertheless, despite substantial variation in expenditure assignments,

the broad principles are generally upheld in most countries.

The argument for decentralization gets further weakened in case of

economies of scale in the provision of environmental public goods and more so, if

the expenditure on these goods involves spillover effects. In this regard, consider

emissions control or pollution cleanup as a government expenditure responsibility.

Which level of government should be assigned this responsibility? Put differently,

which level of government should be assigned the responsibility for environmental

quality? Environmental quality is clearly a good that has externality – and public

good – aspects. However, there are different “types” of environmental services,

18

and the answer to the expenditure assignment question depends on the precise

value a society assigns to the environmental quality.

2.3.2 The Assignment of Tax Responsibilities

Assignment of tax responsibilities among the different levels of government is

a must to provide adequate financing for requisite expenses. Although there is

much diversity in the fiscal structures of national and local governments, here

again several general “best practices” have emerged that provide a useful point for

discussion (Musgrave, 1983; McLure, 1994; Bird, 1999):

1. Only the federal government should impose progressive income taxes.

Due to the potential mobility of factors, any attempt by local government

to redistribute income by progressive income taxes is likely to lead to the

out-migration of more mobile, higher income individuals; and thereby

leaving lesser mobile, lower income individuals to bear the burden.

Income taxes are also thought to be effective counter-cyclical instruments,

and macroeconomic goals are at best pursued by national government

policies.

2. The central government is better placed to impose taxes on the bases those

are distributed unequally across jurisdictions, and use the revenues from

such taxes to equalize fiscal capacities across different jurisdictions.

3. Local governments rely predominately, upon user charges and taxes on

immobile tax bases. In particular, user charges are used to finance goods

that provide measurable benefits to identifiable individuals within a single

jurisdiction, and taxes are used where it is difficult to identify and to

measure individual costs and benefits. The assignment of taxes should

also meet the test of administrative feasibility.

4. Local governments generally speaking, try to avoid taxes on mobile tax

bases, especially capital. As with progressive income taxes, the potential

mobility of capital or other mobile factors of production leads to out-

migration if these factors are taxed at higher-than-average tax rates. By

the same token, attempts to induce in-migration of mobile factors can lead

to a so-called “race-to-the-bottom”, as local governments compete with

each other to attract and to hold these factors by extending tax breaks and

other fiscal incentives.

19

5. Local governments need to be assigned adequate sources of revenues

consistent with their expenditure responsibilities. Local governments

ought to have some discretion over the rate of taxes to promote

accountability of local officials and to establish a link between services

demanded and the cost of service provision. Locally assigned taxes should

exhibit adequate revenue elasticity so that collections can grow with the

demand of services over time.

6. Intergovernmental transfers should be used to finance services that

generate spillovers to nearby jurisdictions as strictly local finance will

lead to inefficient provision. As a case in point, let us consider two local

jurisdictions each of which provides an impure public good (e.g., pollution

abatement) whose benefits spill over to the other jurisdiction. It could be

empirically established that each locality need to receive a subsidy (e.g., a

“conditional”, “matching”, and “open-ended” grant) on its public good

whose magnitude is equal to the marginal benefit of the externality along

the same lines of the Pigouvian tax/subsidy (Oates, 1972; Alm, 1983;

Gordon, 1983).

In practice, few countries follow rigidly these norms, although the broad

pattern of tax assignment is often consistent with these policy prescriptions. In

addition, local governments use numerous miscellaneous taxes and fees that may

be important to their finances. For example, many local governments impose taxes

on various forms of entertainment (e. g., restaurants, hotels, movies, and

gambling). Municipal governments also employ a wide variety of “nuisance”

taxes. These include license fees, and taxes on advertisements, construction

activities, non-motorized vehicles, and the like. Many of these taxes neither rate

high in terms of revenue performance, administrative ease, efficiency and

distributional effects; nor are they important sources of revenue. However, these

sundry taxes continue to be used in a routine manner.

In addition to the power of levying taxes, some of the goals of fiscal

federalism can also be achieved by tax sharing among governments, although tax

sharing does not typically give local governments any real authority in the

selection of local tax rates and therefore does not promote accountability and

efficiency in local expenditures. Surcharges have been increasingly recommended

as part of decentralization efforts around the world where it is necessary to find

some quick way to give cities a significant fiscal capacity. Of course, tax systems

20

are designed to achieve multiple objectives and a trade off is expected among

various objectives. An obvious purpose is to raise the revenues necessary to

finance government expenditures (“adequacy”), and also to ensure that the growth

in revenues is adequate to meet expenditure requirements (“elasticity”). Another

concern is to distribute the burden of taxation in a way that meets with a society’s

notions of fairness and equity. Equity is typically defined in terms of “ability to

pay” such that those with equal ability should pay equal taxes (“horizontal

equity”) and those with differential ability should pay unequal taxes (“vertical

equity”). Taxes can also be used to influence behavior of those who pay them; in

choosing taxes, a common objective is to minimize the interference of taxes in the

economic decisions of individuals and firms. It goes without saying that taxes

should be simple to administer and to comply with, as a complicated tax system

wastes the resources of both tax administrators and taxpayers.

Local tax systems in most of the countries were originally designed for a

world in which production and consumption were primarily of tangible goods, in

which the sale and consumption of these goods generally occurred in the same

location, and in which the factors of production used to make the goods were for

the most part, immobile. In such a scenario, taxation was a fairly straightforward

exercise. Sales and excise taxes were imposed by the government on the tangible

goods that were consumed in the jurisdiction in which consumption (or

production) occurred. Similarly, income and property taxes were imposed on

factors where they lived and worked without apprehension that these taxes would

drive the factors elsewhere. In making these tax decisions, a government in one

jurisdiction never felt the need to consider how its actions would affect the

governments in other jurisdictions and vice versa as tax bases were largely

immobile.

The world has now moved on from a largely immobile to highly mobile

factors of production. There is little doubt that decentralization and other

associated trends (especially competition among local governments and

“globalization”, defined loosely as increased factor mobility across jurisdictions)

had changed the ground rules. In some nations, a trend toward fiscal

decentralization has put more pressures on local tax systems, widening disparities

across regions and increasing the importance of local taxes in the choice of

location of mobile factors. In a global economy, financial capital, firms, and even

households are more mobile, making it harder for local – and even central –

21

governments to raise revenues by increased rates and broadening the base beyond

a point. For example, businesses have more flexibility in choosing where to locate

because communication and transportation costs had been slashed. Further, some

forms of production activity require little in the way of traditional capital and

labor, so that physical location becomes less important. Labor, especially skilled

labor, has become more mobile in this environment. Likewise, financial capital is

able to flow quickly across local, state and national boundaries.

Clearly, if factors of production move easily from one location to another, the

ability of a government, especially local government to tax these factors gets

greatly diminished. A government that raises its tax rates above those of other

jurisdictions risks losing its tax base to other areas. Particularly in the case of

income from capital, there is much speculation that taxation will become

increasingly problematic (Mintz, 1992). In fact, there is some empirical evidence

(even if not conclusive) that factors respond to these tax considerations (Grubert,

1998; Hines, 1999).

Increased mobility is not limited to factors of production alone. Consumers are

also able to plan their preferences according to tax considerations, and

consumption does not necessarily occur in the jurisdiction in which a taxpayer

resides. A jurisdiction that attempts to tax, say, petroleum product more heavily

than surrounding areas finds that consumers resort to purchase elsewhere.2

Similarly, individuals can now purchase many types of products over the internet

and thereby avoid paying some (or even all) sales taxes. Additionally, there has

been increased consumption of services and intangible goods (e.g., computer and

knowledge based services) that are much more difficult to tax than tangible goods.

The once-close link between the location of sales and the location of consumption

has now become quite loose.

Keeping these trends in view, the measurement, identification, and assignment

of tax bases are now much more difficult. Let us consider a typical multi-

jurisdictional business. The product that the firm makes may be designed in one or

more jurisdictions; the firm may use inputs purchased in multiple jurisdictions; the

components may be produced in several places and assembled in a still different 2 In India petroleum products are taxed differently across states, as a result it is common to observe that when tax rate is higher in a state, then consumers start to buy the products from the other states where the tax rate is lower. Recent example is the increase in sales tax rate in Delhi.

22

location; and again the final product may be sold in multiple locations. Because

the business operates in multiple jurisdictions, the firm has considerable leeway to

manipulate prices to minimize its tax liabilities. This problem is well known and

its severity has increased with the enormous expansion in the number of firms

operating in multiple jurisdictions. Likewise, consider an individual whose income

comes from multiple sources. A global income tax requires that income from these

sources be aggregated. However, it is easy for an individual to hide, say, interest

income from multiple areas. In the absence of information sharing across

governments, the ability of a local government to identify incomes from other

jurisdictions is quite limited. Similarly, a consumer can purchase goods and

services in several different ways: from traditional local merchants or from

company websites and may be able to dodge the tax authorities.

How do various local governments respond to these concerns in their tax

choices? As discussed earlier, the ability of any government to choose its tax

policies independently of those in other jurisdictions had now been greatly

curtailed. In the presence of mobile tax bases, a single government’s choice of tax

policies will have effects beyond its own borders and will be affected by the

actions of other jurisdictions. Accordingly, the analysis of tax choices by local

governments must recognize responses by other local governments in a strategic

manner. These strategic interactions can lead to a number of consequences

(intended as well as unintended) leading to overall decline of tax rates. In

particular, if tax bases can move from one jurisdiction to another, they will switch

over from high to low-tax areas.

Owners of capital, skilled labor, and consumers are also increasingly sensitive

to tax differentials in their choices of destination. As a consequence, it is argued

that governments face increased pressure to compete with one another by reducing

tax rates or by offering special tax incentives to attract and to retain tax bases. For

example, when a government reduces its tax rates on capital income, it thereby

attracts capital flows from other jurisdictions, and in doing so the government

benefits its own jurisdiction. However, such actions also impose costs on the

jurisdictions that lose factors of production, and it risks generating similar tax-

cutting responses from those governments. With tax competition, there could well

be a “race-to-the-bottom”, in which overall tax collections decline precipitously as

local governments compete to attract or to retain their tax bases. To date, however,

the evidence in this regard is mixed and inconclusive (Wilson, 1999).

23

The composition of local taxes could also change as a result of increased

difficulty in taxing mobile tax bases. The overall tax burden from income taxes on

mobile tax bases like capital and skilled labor will decline across local

governments; tax rates on these factors would also flatten and converge. In

contrast, taxes on immobile bases – unskilled labor, physical capital, and property

– in turn would increase. Consequently, local governments are likely to turn more

to environmental or “green taxes”, as well as to “sin taxes” (on alcohol, cigarettes

and lotteries) within their purview, to replace lost revenues from mobile bases.

These compositional changes imply that local tax systems are likely to

become more regressive than at present. If taxes on capital and skilled labor

decline, and if fees and charges, sin taxes, income taxes on unskilled labor all

increase, and if marginal income tax rates get flatten; local governments will find

it quite difficult to maintain progressive looking tax systems. Together with an

expected decline in overall revenues, the ability of local governments to

redistribute income to lower income individuals also gets diminished.

Not only is income tax, the form of local sales taxes is also changing. Local

(and other sub-national) governments may well decide that a destination-based

consumption tax that is collected by the federal government and distributed to

them would be preferable to further erosion in their sales tax collections.

Alternatively, they may agree among themselves to apply a uniform local sales

tax. They may even radically reform the sales tax by moving toward a

consumption-based, uniform-rate, destination-principle sales tax, as advocated by

McLure (1997) and Fox and Murray (1997), among others.

These changes suggest that local governments may attempt greater

harmonization (or at least some coordination) of their tax systems and

environmental policies, in an attempt to reduce the negative (fiscal) externalities

that one government’s decisions impose upon other governments. Such

harmonization implies convergence in tax rates across local governments, and also

in the definitions of tax bases. With harmonization, local autonomy in tax policy

obviously gets diminished (Tanzi, 1991, 1995, 2001). Central governments may

also effectively induce such harmonization through a system of intergovernmental

transfers. If local governments cannot or do not provide adequate environmental

protection, say because of competition for mobile capital or because they do not

adequately account for inter-jurisdictional environmental spillovers, central

24

governments can increase the level of protection via several instruments including

provision of matching grants (Alm, 1983; Gordon, 1983).

Whether all these changes are good or bad is obviously difficult to determine.

We have to live with them as changes are certain. Most of the previous discussion

has been focused mainly on the negative fiscal externalities of tax competition

(e.g., the race to the bottom). With greater factor and tax base mobility, local

governments have more power to influence the locational decisions of firms,

workers, and consumers. The governments that succeed in these choices will be

the ones that are able to match taxes with expenditures, able to give taxpayers the

services – including environmental protection – which individuals wish and

deserve for the taxes they pay. Previous research has focused mainly on the

negative fiscal externalities of tax competition. It is only recently that these

positive effects of tax and, especially, of expenditure competition has begun to be

considered in analytical models of local government behavior (Wilson, 1999).

Of course, complete mobility does not exist now, and is unlikely to be a reality

in the near future. However, individuals and firms do value the goods and services

that local governments provide, and they are willing to pay for them. As originally

argued by Tiebout (1956) and more recently by Zodrow and Mieszkowski (1989),

individuals will “vote with their feet” by moving to those jurisdictions in which

governments provide services that residents value. Indeed, local governments will

be required to make their communities as attractive as possible: by providing

uncongested roads, a clean environment, pleasant parks, quality schools, safe

neighborhoods, and the like, all with a tax burden that individuals deem

responsible and appropriate. Firms too, will not object because they also benefit

from safe neighborhoods and quality infrastructure, as well as from the availability

of workers who get attracted by such positivity.

To sum up this section, it is important to state that we need to have a delicate

balance between revenue and expenditure responsibilities among different tiers of

the governments that leads to a functional federal system.

2.3.3 Concept of Equalization

In many federal countries including India (Twelfth Finance Commission),

the concept of ‘equalization’ is the guiding principle for fiscal transfers as it

promotes ‘equity’ as well as ‘efficiency’ in resource use. Equalization transfers in

25

a sense, neutralize deficiency in ‘fiscal capacity’ but not in ‘revenue effort’. Under

such an approach, transfers are determined on a normative basis instead of merely

filling-up the gaps arising from the projections of revenues and expenditures based

on historical trends. As against ‘devolution of taxes’ that is more often than not is

a matter of right, ‘grants-in aid’, as more effective transfer instrument for

administrative unit specific and purpose specific targeting, are mainly used

towards achieving a degree of equalization (Shah, 2006).

2.4 DETERMINANTS OF FISCAL POSITION

Fiscal diversity is reflected in the differentials in fiscal position of various

jurisdictions, i.e., in their ability to meet the needs of their respective communities.

The ability of a jurisdiction to carry out its fiscal tasks (its fiscal position) depends

on its tax base (its capacity) relative to the outlay required for rendering public

services (its need). When jurisdictions with relatively high capacity are faced with

low needs, their fiscal position is strong and vice versa.

Available literature also mentions that a standard level of services can be

provided with a low ratio of tax revenue to tax base (a low – tax effort); meaning

thereby that a standard level of tax effort will generate a high service level relative

to need (high fiscal performance). Where the opposite holds, a high effort may be

needed to provide only a substandard performance level (Musgrave and Musgrave,

1989). In the Indian context, there is a wide variation in ‘capacity’ and ‘needs’ of

various states and union territories (UTs), making intergovernmental fiscal

transfers a delicate and sensitive political issue.

As explained above, the ‘fiscal capacity’ and ‘fiscal need’ are two

important parameters for determining fiscal position. The fiscal capacity of

jurisdiction j or Cj could be defined as

Cj = ts Bj (2.1)

where Bj is the tax base in j and ts is a standard tax rate. Cj thus measures the

revenue which j would obtain by applying that rate to its base. In real situations,

there are different bases and tax rates charged by administrative jurisdictions. On

the similar lines, we can also define the fiscal need of jurisdiction j or Nj as

Nj = ns Zj (2.2)

26

where Zj is the target population, while ns is the cost of providing a standard

service level per unit of Z. Nj thus measures the outlay in j required to secure a

standard level of performance or service. This is again oversimplification as it

allows for one service Z rather than for a mix of services, the importance of which

will vary among jurisdictions. Moreover, a detailed analysis would have to allow

for variations in n.

The fiscal position of j or Pj is defined as

Pj = Cj / Nj = ts B j /ns Zj (2.3)

Fiscal position thus equals the ratio of capacity to need. Setting P for

jurisdictions on the average equal to 1 is a necessary condition for meeting the

needs with own capacity, while a value of Pj > 1 implies a strong fiscal position

and a value of Pj < 1 a weak fiscal position. The value of P, properly defined, is

the index to which distributional weights in grant formulas are often linked.

In this discussion, the concept of ‘tax effort’ is equally important. We

define jurisdiction j’ tax effort Ej as

Ej = tj B j/ ts Bj = tj / ts (2.4)

The ratio of actual revenue in j is obtained by applying j’ tax rate tj to

what would be raised by applying ts (standard rate). This leads to the definition of

performance level Mj as

Mj = nj Zj / ns Zj = nj / ns (2.5)

or the ratio of actual outlay obtained by applying j’s outlay rate nj to that required

to meet the standard level at rate ns.

Assuming a balanced budget, we have

tj Bj=njZj (2.6)

An alternative definition of fiscal position with some mathematical

manipulation could be stated as follows:

Pj = (nj/ns ) / ( tj/ts) (2.7)

27

Fiscal position may thus be defined as the ratio of capacity to need or as the ratio

of performance to tax effort.

These concepts and problems which arise in comparing fiscal positions

both among states and among jurisdictions within states pose one of the principal

issues in fiscal federalism. They are of concern both to the federal governments,

called upon to deal with excessive differentials among states, and to state

governments, called upon to deal with excessive differentials among local

jurisdictions (Musgrave and Musgrave, 1989). ‘Fiscal need’ and ‘fiscal capacity’

of a jurisdiction are thus important concepts and in practice ‘fiscal capacity’ based

determination are preferred world over.

In the intergovernmental fiscal transfers, grant received by a jurisdiction

depends on it ‘fiscal capacity’ (Musgrave and Musgrave, 1989).

Gj = tj Bj (Bj / Ba – 1) + tj Bj (Bj /Ba - 1) (Cj / Ca – 1) (2.8)

In this formula Gj is the grant received by the jurisdiction j; Bj is the per

capita tax base and tj is the tax rate which j chooses to impose. Ba is tax base in

average jurisdiction. Cj is the cost of accomplishing a given service level in j and

Ca is the cost of doing so in the average jurisdiction. Cj may differ from Ca either

because the required resources are more or less costly or because the need is

greater in the jurisdiction j. The first term of the equation (2.8) equalizes the

revenue to be achieved from a given tax rate, while the second term equalizes the

service level to be achieved with a given outlay (Musgrave and Musgrave, 1989).

2.5 STRATEGIC INTERACTIONS

In a federal structure, lower levels of governments could be thought of as

interacting with one another along three main channels: preferences, constraints

and expectations (Revelli, 2005). According to the ‘preference interaction

hypothesis’, an action chosen by a government affects directly the preferences of

other governments as certain public services provided by a jurisdiction enter the

welfare function of other jurisdictions (Gordon, 1983). On the similar lines, in the

presence of tax base mobility, the fiscal policy by a local government affects the

budget constraints of other governments, by means of a policy – driven resource

flow (capital migration). As a result, a jurisdiction’s policy affects indirectly the

policies of other jurisdictions, giving rise to fiscal competition for mobile

28

resources (Wilson, 1999). ‘Yardstick competition theory’ based upon the existence

of an informational externality amongst neighboring jurisdictions affects the

beliefs of an electorate with respect to the competency of their own government

(Besley and Case, 1995). As a result of the information spill-over, the electorate in

a local jurisdiction learns more about the quality and efficiency of their own

incumbent in local public service provision, by using other governments’

performances as a yardstick (Besley and Smart, 2002).

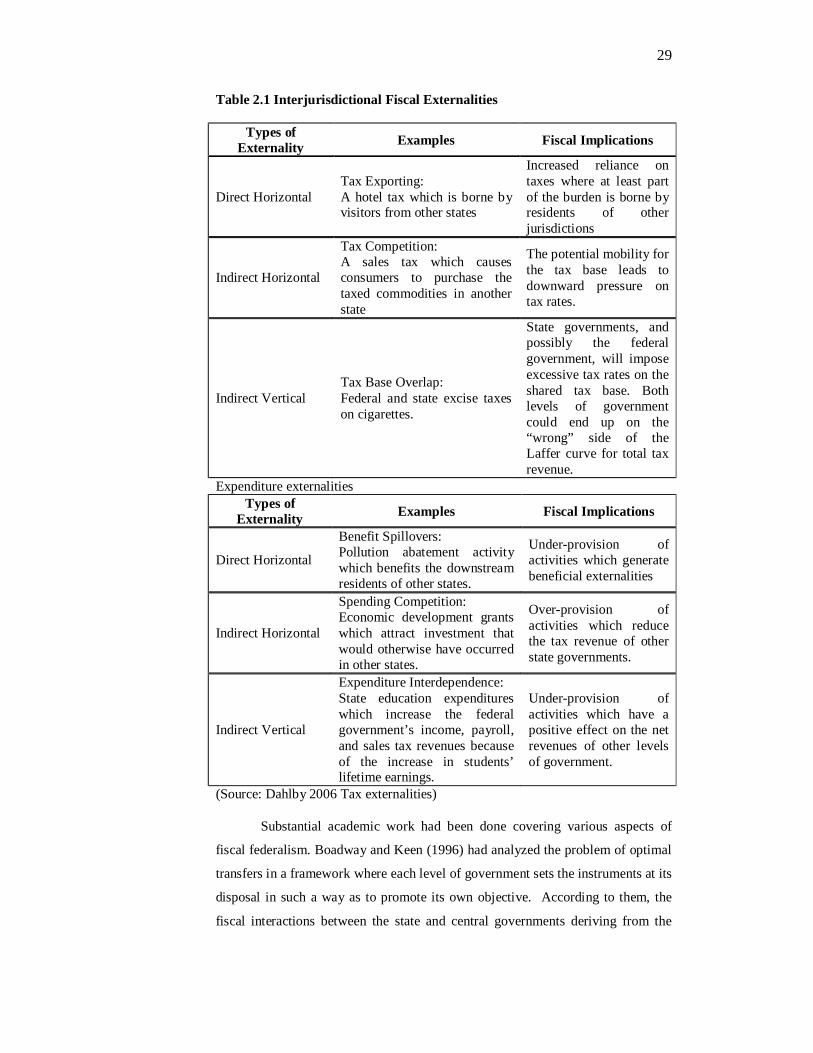

2.6 FISCAL EXTERNALITIES

Fiscal functions in a federation may lead to different types of

‘externalities’. Interjurisdictional fiscal externalities occur when a government’s

tax and expenditure decisions affect the well-being of taxpayers in other

jurisdictions either:

• Directly by changing their consumer and producer prices or their public

good provisions, or

• Indirectly by altering, the tax revenues or expenditures of other

governments.

Within the federal context, fiscal externalities could further be categorized

as ‘tax externalities’ and ‘expenditure externalities’. Coming to ‘tax externalities’,

they have been classified as ‘tax exporting’ (direct horizontal), ‘tax competition’

(indirect horizontal), and ‘tax base overlap’ (indirect vertical). On the similar

lines, there are three basic types of ‘expenditure externalities’ namely, ‘benefit

spillovers’ (direct horizontal), ‘spending competition’ (indirect horizontal), and

‘expenditure interdependence’ (indirect vertical). Table 2.1 provides us with the

types, typical examples, and their fiscal implications for both the ‘tax externalities’

and ‘expenditure externalities’ (Dahlby, 1996). Relationship between grant

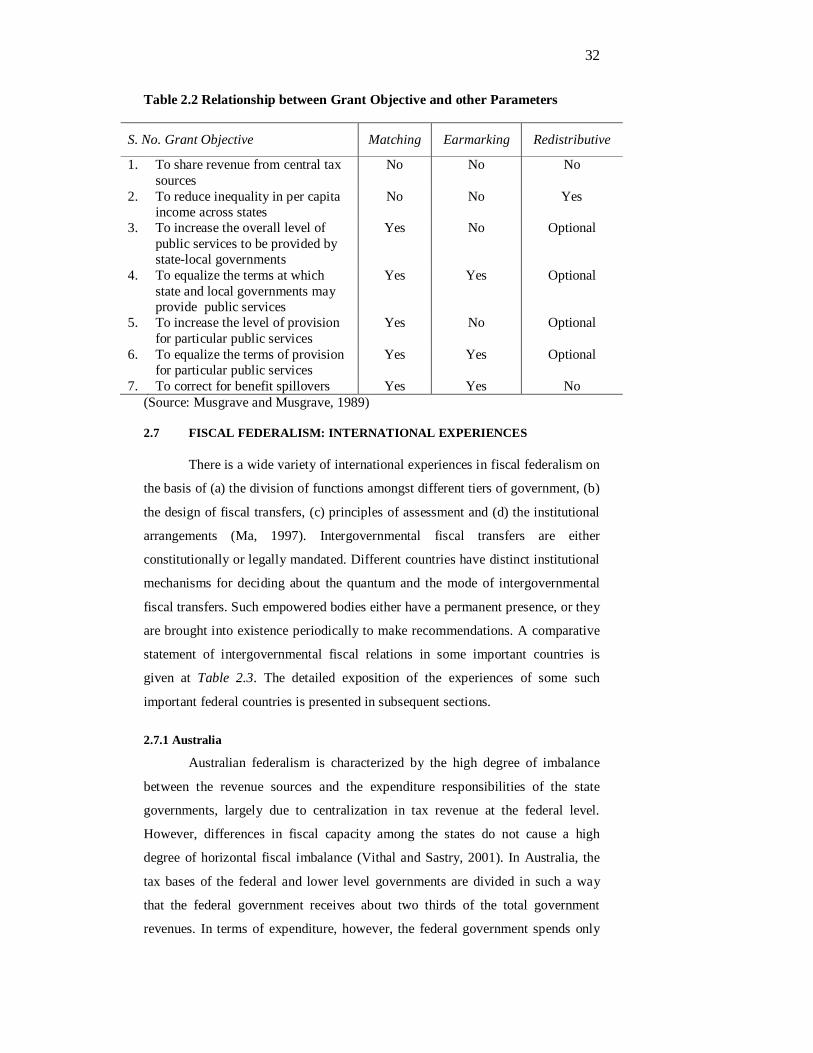

objective and other parameters such as matching, earmarking and redistribution is

captured in Table 2.2.

Given that different tiers of governments have their own tax systems and

expenditure needs, it is important to determine the optimal magnitude of transfers

between various levels of government. It is common for central governments to

transfer fiscal resources to lower-level governments in order to close a perceived

fiscal gap between the desired level of expenditures by lower-level governments

and the level of revenues that they collect.

29

Table 2.1 Interjurisdictional Fiscal Externalities

Types of Externality Examples Fiscal Implications

Direct Horizontal Tax Exporting: A hotel tax which is borne by visitors from other states

Increased reliance on taxes where at least part of the burden is borne by residents of other jurisdictions

Indirect Horizontal

Tax Competition: A sales tax which causes consumers to purchase the taxed commodities in another state

The potential mobility for the tax base leads to downward pressure on tax rates.

Indirect Vertical Tax Base Overlap: Federal and state excise taxes on cigarettes.

State governments, and possibly the federal government, will impose excessive tax rates on the shared tax base. Both levels of government could end up on the “wrong” side of the Laffer curve for total tax revenue.

Expenditure externalities Types of

Externality Examples Fiscal Implications

Direct Horizontal

Benefit Spillovers: Pollution abatement activity which benefits the downstream residents of other states.

Under-provision of activities which generate beneficial externalities

Indirect Horizontal

Spending Competition: Economic development grants which attract investment that would otherwise have occurred in other states.

Over-provision of activities which reduce the tax revenue of other state governments.

Indirect Vertical

Expenditure Interdependence: State education expenditures which increase the federal government’s income, payroll, and sales tax revenues because of the increase in students’ lifetime earnings.

Under-provision of activities which have a positive effect on the net revenues of other levels of government.

(Source: Dahlby 2006 Tax externalities)

Substantial academic work had been done covering various aspects of

fiscal federalism. Boadway and Keen (1996) had analyzed the problem of optimal

transfers in a framework where each level of government sets the instruments at its

disposal in such a way as to promote its own objective. According to them, the

fiscal interactions between the state and central governments deriving from the

30

sharing of a common tax base can lead these governments to choose policies that

are inferior, from a welfare viewpoint, to those that a unified central government

would choose.

Cremer et al. (1996) worked on informational aspects of fiscal federalism

challenging the assertion that local governments have “better information” than

central governments and that fiscal decentralization therefore facilitates efficiency

in public-sector activities. In their model of informational asymmetries between

central and lower-level governments, Cremer et al had shown that its

intergovernmental transfers and the tax system that finances them must be

incentive compatible.

Walz and Wellisch (2000) focus exclusively on horizontal interactions

analyzing tax competition for mobile capital. The allocation of both portfolio

capital and direct investment among jurisdictions depends, in general, on net-of-

tax rates of return, and individual jurisdictions may be able to stimulate local

investment through tax concessions or other fiscal incentives. Nechyba (1997)

researched on analyzing the simultaneous interaction of market and political

decision making in local public finance through a computable general equilibrium

(CGE) model. In Nechyba’s model, decision about local public good provision

are made through simple majority voting by residents, with property taxes (other

fiscal instruments) used to finance local spending.

Kappeler and Valila (2008) carried the empirical analysis of the

relationship between fiscal decentralization and the composition of public

investments. Their results suggest that decentralization increases economic

productive public investment, especially investment in public spillover goods. On

the other hand, there is no statistically significant impact of decentralization on

public investment in consumption-oriented local public goods (redistribution).

Based on the theoretical framework of fiscal federalism as discussed in this

Chapter, methodology and tools adopted by various countries in practice are dealt

with in the following section.

31 Figure 2.1 flow diagram of different types of grants deployed for intergovernmental fiscal transfers, Source: (By the author)

Grants

Specific Grants (Conditional/ earmarked)

General Grants (Unconditional/ Block)

Lumpsum Grants (Specific grants)

Matching Grants (Financial contribution)

Effort related

Non-effort related

Effort related

Closed ended

Open ended

Non-effort related

Closed ended

Open ended

Lump sum Grants (General)

Matching Grants (Financial Contribution)

Effort related

Non-effort related

Effort related

Non-effort related

Closed ended

Open ended

Closed ended

Open ended

32

Table 2.2 Relationship between Grant Objective and other Parameters

S. No. Grant Objective Matching Earmarking Redistributive

1. To share revenue from central tax sources

No No No

2. To reduce inequality in per capita income across states

No No Yes

3. To increase the overall level of public services to be provided by state-local governments

Yes No Optional

4. To equalize the terms at which state and local governments may provide public services

Yes Yes Optional

5. To increase the level of provision for particular public services

Yes No Optional

6. To equalize the terms of provision for particular public services

Yes Yes Optional

7. To correct for benefit spillovers Yes Yes No (Source: Musgrave and Musgrave, 1989)

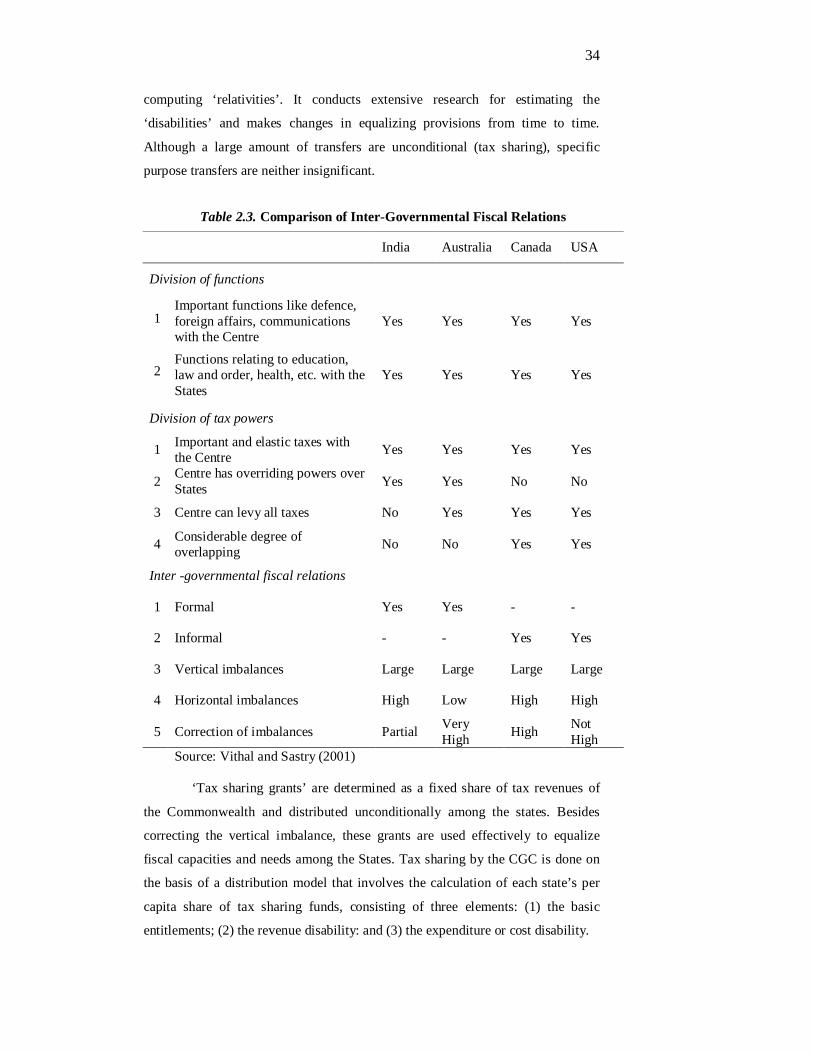

2.7 FISCAL FEDERALISM: INTERNATIONAL EXPERIENCES

There is a wide variety of international experiences in fiscal federalism on

the basis of (a) the division of functions amongst different tiers of government, (b)

the design of fiscal transfers, (c) principles of assessment and (d) the institutional

arrangements (Ma, 1997). Intergovernmental fiscal transfers are either

constitutionally or legally mandated. Different countries have distinct institutional

mechanisms for deciding about the quantum and the mode of intergovernmental

fiscal transfers. Such empowered bodies either have a permanent presence, or they

are brought into existence periodically to make recommendations. A comparative

statement of intergovernmental fiscal relations in some important countries is

given at Table 2.3. The detailed exposition of the experiences of some such

important federal countries is presented in subsequent sections.

2.7.1 Australia

Australian federalism is characterized by the high degree of imbalance

between the revenue sources and the expenditure responsibilities of the state

governments, largely due to centralization in tax revenue at the federal level.

However, differences in fiscal capacity among the states do not cause a high

degree of horizontal fiscal imbalance (Vithal and Sastry, 2001). In Australia, the

tax bases of the federal and lower level governments are divided in such a way

that the federal government receives about two thirds of the total government

revenues. In terms of expenditure, however, the federal government spends only

33

one third of the total government revenues. This means about half of the federal

government revenues are distributed through various forms of transfers to the state

and local governments (Rye and Searle, 1996).

The basic outlines of the Australian federal system empowers the

Commonwealth (Central) government with functions such as foreign affairs,

foreign trade, defence, immigration, interstate trade and commerce, currency and

banking, maritime activities, posts and telegraphs and social security payments.

The states are vested with the responsibilities of providing education, health,

public and social services. The states have also been given the control of their

local governments though some responsibilities such as maintaining the road

system, recreation and cultural services and public services such as water supply,

sewerage, garbage disposal, etc. have been delegated by them to the local

governments.

While the Commonwealth government can levy all taxes, the states have

been given concurrent powers of taxation except in the case of customs and excise

duty. The majority of state taxes are dependent upon property taxes (Vithal and

Sastry, 2001). The Australian federal system provides for correction, both of

vertical and horizontal imbalances, through tax sharing arrangements and specific

purpose grants.

The Commonwealth Grants Commission (CGC), Statutory Grants

Commissions (SGCs) and the Australian Loan Council (ALC) are the three main

institutions looking after intergovernmental fiscal relations in Australia. While the

tax sharing is distributed on the basis of relativities determined by the CGC, SGCs

administer the specific purpose grants measuring the states' fiscal capacities and

fiscal needs using broad judgments and sampling services. In addition, the ALC

raises and distributes loan funds among the States, local governments and

autonomous bodies. The Australian federal government grants to lower level

governments include general purpose grants and specific purpose grants.

The CGC has been commented by some observers as, "a model in the

international context for the objective appraisal of spending needs" (Bird, 1986).

The CGC is a statutory and permanent authority, though not a constitutional body.

Originally designed to report for special assistance by states, over the years CGC

has taken over the responsibility of recommending tax sharing grants by

34

computing ‘relativities’. It conducts extensive research for estimating the

‘disabilities’ and makes changes in equalizing provisions from time to time.

Although a large amount of transfers are unconditional (tax sharing), specific

purpose transfers are neither insignificant.

Table 2.3. Comparison of Inter-Governmental Fiscal Relations

India Australia Canada USA

Division of functions

1

Important functions like defence, foreign affairs, communications with the Centre

Yes Yes Yes Yes

2

Functions relating to education, law and order, health, etc. with the States

Yes Yes Yes Yes

Division of tax powers

1 Important and elastic taxes with the Centre Yes Yes Yes Yes

2 Centre has overriding powers over States Yes Yes No No

3 Centre can levy all taxes No Yes Yes Yes

4 Considerable degree of overlapping No No Yes Yes

Inter -governmental fiscal relations

1 Formal Yes Yes - -

2 Informal - - Yes Yes

3 Vertical imbalances Large Large Large Large

4 Horizontal imbalances High Low High High

5 Correction of imbalances Partial Very High High Not

High Source: Vithal and Sastry (2001)

‘Tax sharing grants’ are determined as a fixed share of tax revenues of

the Commonwealth and distributed unconditionally among the states. Besides

correcting the vertical imbalance, these grants are used effectively to equalize

fiscal capacities and needs among the States. Tax sharing by the CGC is done on

the basis of a distribution model that involves the calculation of each state’s per

capita share of tax sharing funds, consisting of three elements: (1) the basic

entitlements; (2) the revenue disability: and (3) the expenditure or cost disability.

35

‘Specific purpose grants’ are another important mechanism for the transfer

of resources from the Commonwealth government to state governments in

Australia. The SGC distributes general purpose grants using a comprehensive

equalization program. The ALC consisting of the Prime Minister and the State

Premiers had been created for the centralized supervision of increased capital

accounts of States and local bodies. The entire public sector borrowings in

Australia are formally subject to the control of the ALC, as to amounts, forms,

terms and conditions.

One of the most important aspects of Australian fiscal federalism is the

extent of equalization achieved through federal transfers. However, the amount

required for equalization is not very large, as the capacity differences between

different states are not very large. The two essential elements of the norms

adopted in the computation of tax relativities are: the ‘revenue disability’ and the

‘cost disability’ factors. As a result of the use of these factors, all the states are

enabled to provide such standards of public services in physical terms at least as

an average state would provide. This ensures that every citizen, irrespective of the

state of residence, is enabled to have a certain minimum standard of public

services.

2.7.2 Canada

A striking feature of the Canadian economy is the substantial inter-

Provincial and intra-Provincial variations. The essential difference between the

advanced and backward provinces in Canada is in the presence and exploitation of

natural resources. In keeping with their economic dominance, the provinces of

Quebec, Ontario and Alberta have played a major role in the development of

Canadian fiscal federalism. The specific purpose transfers from the federal

government in Canada to all ten provinces and two territories are similar. But for

equalization transfers, the territories receive more than the provinces on a per

capita basis, as the equalization scheme reflects the greater needs and costs that

arise from the territories' remoteness and sparse populations (Broadway and

Hobson, 1993).

The Canadian constitution specifies the exclusive powers of both the

National (Federal) and Provincial governments. Most of the residual powers rest

with the federal government, although matters of merely local or private nature are

assigned to the provinces. Federal power covers issues relating to the nation as a

36

whole such as internal trade, railway, harbors and canals that are the sinews of

economic development. The provinces have been given jurisdiction over

education, health, welfare, property and civil rights, and ownership and

exploitation of natural resources. Historically, the provinces have guarded their

constitutional powers and have been relatively successful in asserting their rights

to the point where Canada is considered as one of the most decentralized

federations in the world (Vithal and Sastry, 2001).

While the federal government can raise money ‘by any system or mode of

taxation’, the provinces are given access to all forms of ‘direct taxation’, to raise

revenues for provincial purpose. Both the national and provincial governments

have constitutional access to all major forms of taxation. The major taxes of the

federal government are income tax on personal and corporate incomes, succession

and estate taxes, manufacturer’s sales taxes, customs, excise taxes and duties. It

also obtains some revenues through resources rents, most notably from export tax

on oil. The main provincial taxes consist of retail sales tax on ‘tangible personal

property’ (covers all commodities), tax on personal and corporate incomes,

succession and gift tax, health and social insurance levies, and property taxes.

The result of the severe vertical and horizontal imbalances has been the

evolution of an equalizing and liberal system of federal transfers in Canada (Shah,

1995). These transfers can be broadly classified as:

(1) Statutory subsidies: The subsidies paid to each Province as part of the

terms of confederation take several forms including grants in support of

Provincial Legislature, per capita grants, debt allowances and certain

special grants.

(2) Transfer under the Federal–Provincial Fiscal Arrangements and

Established Programmes Financing Act, 1977:

(a) Equalization Payments: Equalization payments to less endowed

Provinces are made under this Act essentially to raise the fiscally

deficient governments to the average level based on the per capita

revenue potential of the province. The consequence of these

equalization payments is that the difference between the provinces

in providing public services is remarkably small considering their

capacity differences.

37

(b) Stabilization Payments: The earlier tax agreements between the

national government and the provinces assured the later a revenue

‘floor’. The 1977 financial arrangements saw the national

government surrendering to the provinces, one percentage point of

its revenue from personal income tax on a one time only basis. It

also protects each province against a reduction in revenue due to

any subsequent changes in the national personal income tax

structure.

(c) Established Programme Financing: It covers the national

government’s contribution to provinces towards the cost of three

programme areas namely, hospital insurance, medical care and post

secondary education. The national government’s contributions

under EPF are not directly related to the provincial expenditures,

but to the rate of growth of the economy.

(3) Specific Purpose Transfers: Besides the three activities which are

supported under EPF, specific matching grants are given under the

Canadian Assistance Plan (CAP), primarily to provide adequate

assistance to persons in need. The unique feature of the scheme is that the

schemes for assistance are started entirely with Provincial initiative and

federal government accommodates it. Under the CAP, the national

government meets 50 per cent of the operating costs of the programmes

in each province. The Province may itself administer the programme,

designate a municipality or make use of agencies operated by private

groups.

Besides the above, the National and Provincial governments, over the

years, share costs through conditional matching grants on a wide variety of

activities. The inter-governmental fiscal problems in the course of implementing

fiscal policy are hammered out within an elaborate structure of consultations. This

process of consultation in Canada is carried out on virtually at every level of

federal and provincial administration. The annual meetings of the First Ministers

(the Prime Ministers and the Provincial Premiers) and regular meetings of the

ministers in the many areas of inter-governmental concern provide a prime forum

for solving the problems.

38

As regards fiscal policy, the most important roles are played by the

Federal and Provincial Relations Officer (FPRO) and the Department of Finance.

The FPRO is responsible for the important meetings of the First Ministers, and

together with Department of Justice, for matters relating to the Canadian

Constitution. The Department of Finance, through its Federal Relations Division

and Social Policy branches, is responsible for the fiscal arrangements agreed to by

the National government and the Provinces. The Economic Council of Canada

contributes inputs to this consultation process through its studies and annual

reports. In the end, the inter-governmental process culminates in a Federal and

Provincial conference. In fact, the inter-governmental consultation/conference

process has been the chief architect of the fiscal arrangements and equalization

programmes affected in Canada. Availability of constitutional access to all major

forms of taxation to both Federal and Provincial governments is a notable feature

of Canadian federalism (Vithal and Sastry, 2001). There are no constitutional

solutions to the fiscal transfers in Canada; they depend on political solutions.

2.7.3 European Union

In the European Union, fiscal decentralization is connected to the term

“subsidiarity”, the roots of which are found in 20th century Catholic social

philosophy (Doring, 1997). According to the subsidiarity principle, as

consolidated and adopted by the Maastricht Treaty of 1992, public policy and its

implementation should be allocated to the smallest jurisdiction with the

competence to achieve the objectives.

The constitutional arrangements for relationships between the different

levels of government vary considerably between EU countries. Some members

are federations while many other are unitary states. Coming to the local tier of

governance, some members have ‘strong’, while others ‘weak’ and the rest have

‘intermediate’ type of local governments (CTPA, 2002). In a large number of EU

member countries, the most common categories of sub-national government

expenditure are education, health, social security and welfare, housing and

community amenities, recreation, cultural and religious affairs, and transport and

communication. But the relative importance of these items varies widely between

countries. Similarly, the relative importance of taxes, non-tax revenues and grants

also varies greatly between EU member countries. Coming to sources of revenues

39

for sub-national entities in EU member countries (CTPA, 2002), they could

broadly, be categorized as follows:

i) Taxes, which include revenue from social security contributions as well as from

taxes on income, payrolls, consumption, wealth and property, and any other

taxes.

ii) Grants, which include any non-repayable payments received from other levels

of government.

iii) Non-tax revenues, which includes any other sources of non-repayable income,

including surpluses of trading enterprises, property income, administrative

fees and charges, fines and forfeits, and contributions from both employees

and other levels of government to employee pension and welfare funds.

As a representative member country of EU, we shall now discuss salient

features of fiscal federalism in Germany in the next subsection.

2.7.4 Germany

The German federation consists of sixteen Landers with a linguistically

homogeneous population having considerable economic disparity and difference

in political cultures between the former West and East Germanies. A notable

characteristic of the German federation is the extensive constitutional and political

interlocking of the federal and state governments. The federal government has a

very broad range of exclusive, concurrent (with federal law prevailing) and

framework legislative jurisdiction. But the Landers in turn have a mandatory

constitutional responsibility for applying and administering most of these federal

laws (Watts and Hobson, 2000). Another significant feature of the German

federation is that the Landers are more directly involved in decision-making at the

federal level than the states or provinces in virtually any other federation. This is

achieved through the constitutional requirement that the second chamber, the

Bundesrat, is composed of Land first ministers and senior ministers serving as ex

officio delegates of their Land governments. The Bundesrat possesses an absolute

veto on all federal legislation affecting the Lander. This makes the Bundesrat a

key institution in the highly integrated legislature, administrative and financial

interdependence of the two orders of government.

There are two fundamental features of the distribution of powers in

Germany worthy of note. First, the Basic Law allocates legislative jurisdiction on

40

the basis of an exclusive list of federal powers and a list of concurrent powers,

with the residual power remaining with the Lander. Exclusive federal legislative

power is granted in areas which include foreign affairs and defence, citizenship

and immigration, rail and air transport, criminal policing and foreign trade. An

extensive list of areas of concurrent legislative jurisdiction includes such areas as

civil and criminal law, the regulation of nuclear energy, labour relations,

environmental protection, and road transport (Watts and Hobson, 2000).

There are also two additional special categories of concurrent powers in

the Basic Law, First, the federal government may under its ‘framework’ powers

restrict the exercise of Lander legislative authority, to a limited extent, in certain

fields. In these fields, the federal government has the right to enact framework

legislation aimed at providing a degree of uniformity of action across the

federation; within these parameters, the Lander have the right to enact customized,

detailed laws. Framework legislative fields include areas such as higher

education, nature conservation, and regional planning. Second, there is a

constitutional provision for the federal and Land governments to carry out ‘joint

tasks’ together. These areas include university construction, regional policy,

agricultural structural policy and coastal preservation, education planning and

research policy.

2.7.5 Japan

The fiscal relations between the central and local governments in Japan

are markedly a vertical financial imbalance requiring transfers from the central

government to the local governments. In Japan, there are five types of transfers

from the central government to local governments: the local allocation tax, central

government disbursement, local transfer taxes, special traffic safety

disbursements, and transfers as a substitution for fixed-assets tax (Ma, 1994;

Yonehara, 1993; Fujiwara, 1992; and Ishi, 1993). Of these transfers, the local

allocation tax and central government disbursements are the most important of the

total transfers from the central government to local governments. The local

allocation tax is allocated to local governments to equalize their fiscal capacity

and to ensure sufficient funds for the public services that local governments are

required to provide.

41

The number of central government disbursement programs covers almost

all fields of local government activities. The local transfer taxes are levied by the

central government, which imposes them as local rather than as central taxes. The

central government collects these taxes on behalf of local governments because of

the advantages in assessment and collection. The local allocation tax aims to

equalize the fiscal capacities of local governments by supplementing the shortage

of their tax revenues, thereby, enabling local governments to provide public

services at the standard level prescribed by the central government. When a local

government does not maintain the level prescribed for public services, or has paid

an excessive amount for the services, the central government may reduce the local

allocation tax for that local government. Compared to other transfer schemes, the

local allocation tax is the only equalization scheme in Japan. It is allocated both to

prefectures and municipalities in the same way.

Like many other countries, basic fiscal need is a standardized amount

necessary to provide public services at the level prescribed by the central

government in Japan. Because the cost of providing public services is affected by

various factors such as geographical, social, economic, and institutional

characteristics of each locality, modification coefficients are applied to the

equation to adjust for these factors. The unit costs are calculated each fiscal year,

taking into account the change in price levels and the change in the people's

demand for the particular public service.

2.7.6 Korea

Intergovernmental fiscal transfer in Korea is administered through five

major transfer mechanisms. They are (1) Local Shared Tax; (2) National Treasury

Subsidy; (3) Local Transfer Fund; (4) Adjustment Allocation Grant; and (5)

Provincial Government Subsidy (Kim, 1985). The first three transfers are

distributed from the central to provincial governments, while the latter two are

transfers from major cities or provinces to lower level governments.

The Local Shared Tax and National Treasury Subsidy are the traditional

means utilized by the central government to transfer certain fiscal resources to

local governments. The Local Transfer Fund, introduced in 1991, can also be

categorized as a mechanism to transfer a portion of the fiscal base of the central

government to local governments except that the transfer is made directly out of

42

national tax revenue without having the revenue accounted for first in the central

government budget. Local Shared Taxes in Korea are divided into Ordinary Local

Shared Taxes (distributed on the basis of the pre-determined equalization formula)

and Special Local Shared Taxes (allocated on the basis of special needs of local

governments).

The objective of Ordinary Local Shared Taxes is to equalize the fiscal

capacities of local governments. The equalization formula used to distribute Local

Shared Taxes in Korea calculates for each local government the standardized

fiscal needs, the standardized fiscal revenue, and their difference signifies the

standardized fiscal shortage of the local government and becomes the basis of

actual allocation of Ordinary Local Shared Taxes. The results of these calculations

and the actual allocation of Local Shared Tax among local governments are

published annually for public inspection and scrutiny. While Ordinary Local

Shared Taxes are unconditional grants to the local governments, Special Shared

Taxes are conditional grants to supplement the operation of the Ordinary Local

Shared Taxes. Korea's National Treasury Subsidies are categorical grants provided

by the central government to local governments for specific projects. National

Treasury Subsidies are classified into three categories: (a) National Treasury

Share, (b) Promotion Subsidies, and (c) Specific Grants. National Treasury Share

is provided on the matching basis for natural disaster recovery projects and other

construction projects. Promotional Subsidies are allocated to local governments to

encourage them to undertake certain projects or to provide financial assistance for

certain projects. Specific Grants are provided usually for the full cost of

administering national functions (Kim1994).

2.7.7 The United States of America

The American system of public administration is an extremely complex

governmental organism with multiple layering as the striking feature of the

American government (Vithal and Sastry, 2001). The US Constitution allocates

the functions of national importance such as defence, international relations, postal

service, space research and technology exclusively to the Federal government. In

all other areas, Federal, state and local bodies hold concurrent powers to spend

though the states have ‘reserved’ powers to organize their own governments

without national interference, legislate for health, welfare, safety and morals of

their residents and assume responsibility for and the control of local governments.

43

All governmental bodies concurrently exercise most expenditure

functions. On social insurance, the roles of the federal and state governments are

almost equal. The local governments are primarily concerned with the provision

of education, health and hospitals, housing and urban renewal services. Because of

the concurrent powers in case of almost all the important taxes, the tax system in

the US looks uncoordinated and overlapping. The only co-coordinating device, in

case of individual income tax, is the deductibility of most State and local taxes for

federal tax purposes. All the three levels of government utilize many of the same

tax sources.

There is a considerable degree of variation in terms of potential and

degree of urbanization among the state and local governments leading to the

significant fiscal disparities noticed among the states. Although concurrent

powers of taxation are vested in different levels of government, imbalance

between revenues and expenditures at lower levels of government persists in the

USA. Originally, the federal special grant programmes started as conditional

school land grants. These transfers, over the years, gave birth to cash grants for

specific purpose programmes. After the depression and the Second World War, a

number of new federal grants were initiated; as a percentage of State-local

expenditures and in terms of numbers, the federal grant programmes increased

enormously (Vithal and Sastry, 2001). Almost all these grants, except revenue

sharing grants, are conditional in nature. Basically, three kinds of instruments are

used for the transfer of resources:

(1) Categorical (Conditional) Grants: are preferred in the USA to ensure that

important public services are provided more or less uniformly across the

country. The two important types of categorical grants are:

(a) Formula based categorical grants are given to achieve the prescribed

targets on a clearly defined population of eligible recipients for whom the

grant is intended. Most grants are made only to state governments while

some are made to state and local governments or to local governments

only. The most common formula grants are in the area of ground

transportation, education, training and employment, etc.

(b) Project-based grants are used when neither a well-defined beneficiary

population nor responsible objective measures of fiscal need and capacity

44

are available. In such cases, grants are made available for particular

projects in some specified area of public service. Project grants require

competitive applications from potential recipients.

(2) Block Grants: They are provided for use in a broad functional area. The

use of the funds is largely at the recipient’s discretion. Presently there are

five block grants in the broad functional areas of community

development, partnership for health, law enforcement assistance,

comprehensive employment and training, and social services. These

grants are distributed on the basis of specific statutory-based formula,

with population and certain other indices of need being the most

prominent factors used (Vithal and Sastry, 2001).

(3) General Revenue Sharing: Under revenue sharing, funds are distributed

to the States and local bodies for general purposes. Some important

features of revenue sharing grants are: (i) they are the shares of a fixed

sum of money and do not vary with federal revenues; (ii) revenue sharing

in the US does not involve inter-state equalization; and (iii) the inclusion

of the effort component and the requirement to pass two-thirds of the

funds to local governments diminishes their importance as a means of

rectifying inter-State imbalances between own revenues and expenditures.

As taxation and expenditure decisions in the USA are shared among

diverse units of government, and different levels of government are vested with

concurrent powers, this makes an intensive inter-governmental consultation

process inevitable. Essentially, the structure of inter-governmental relations is

built on the edifice of an informal cooperative consultation process. Inter-

governmental consultations in the USA mostly result from continuous day-to-day

contacts, knowledge and evaluation by government officials at both national and

State levels. The enactment of a number of Acts has helped in evolving better

administrative procedures, brought about improvements in personnel

administration, and enabled sub-national units to obtain more than one kind of

assistance from the national government.

Each of the lower level governments also has institutional arrangements

within its governmental structure to serve a liaison and information role with

officials at the state and national levels. Inter-governmental policy-making is

45

further aided by a number of nationwide associations fostering regular

consultations and discussions among the public officials of different levels of

government (Vithal and Sastry, 2001). Institutional mechanisms, such as the

Advisory Council on Inter-governmental Relations (ACIR), helps in providing

essential inputs to the process of solving inter-governmental fiscal problems. In

spite of a long, democratic history and a multi-layered institutional framework, the

USA seems to be less federal in fiscal matters than many other countries.

The American system of revenue raising shares with the Canadian one the

range of discretion that the states have over their own taxes. Most states levy their

own corporate and personal income taxes as well as their own retail sales taxes.

Their municipalities use property taxes extensively as well as taxes on natural

resources. The federal government shares many of the same tax bases, with the

notable exception of the sales tax. It also uses the payroll tax for financing a

specific program, the Social Security system (Boadway & Watts, 2006).

In the United States the vertical fiscal gap is closed by a wide array of

conditional transfers, both block and specific. This widespread use of conditional

transfers is a relatively unique feature of the US federal system. It arises at least

partly as a device to inducing accountability in state executive branches that,

unlike in parliamentary systems, are not accountable to state legislatures.

In the United States, there is no formal system of tax harmonization. The

major taxes co-occupied by the federal and state governments are personal and

corporate income taxes. In both cases, states have their own independent systems.

Some states choose to piggyback on the federal system by basing state tax

liabilities on the federal tax base, and sometimes also the federal rate structure.

However, other states define their taxes independently. In the case of the

corporate tax, there is the additional problem that different states apply different

conventions for allocating to themselves taxable income earned by firms that

operate in more than one state. This gives rise not only to inefficiencies but also

to instances of double taxation or of non taxation of some portion of incomes.

Sales taxes are used only at the state level, and here too there is no harmonization.

State sales taxes are single staged retail taxes (for those that use this tax source),

where bases and rate structures can vary considerably across states. Thus the tax

system in the United States is highly differentiated across states, though the

46

significance of this is somewhat diminished by the fact that states collect a

relatively smaller proportion of total tax revenue than in Canada (Boadway &

Watts, 2006).

The aforesaid discussion on fiscal federalism clearly brings out a variety