1

1Q12 Earnings

Results Presentation

09/05/2012

2

This release contains forward-looking statements relating to the prospects of the business, estimates for operating and financial results, and those related to growth prospects of TPI – Triunfo Participações e Investimentos S.A. These are merely projections and, as such, are based exclusively on the expectations of the Company’s management concerning the future of the business. Such forward-looking statements depend substantially on changes in market conditions, the performance of the Brazilian economy, the sector and the international markets, and are, therefore, subject to changes without previous notice. The information is presented in proportion to the participation of Triunfo in each subsidiary. The operational numbers correspond to 100% of the business. The information includes the performance of the subsidiary Rio Verde.

Forward-Looking Statements

3

Digite aqui o Título

da Palestra

Digite aqui o Nome do Palestrante e a Data

I - Highlights

4

I – Highlights 1Q12

Net Revenue grew 21.7% compared to 1Q11, reaching R$231 million.

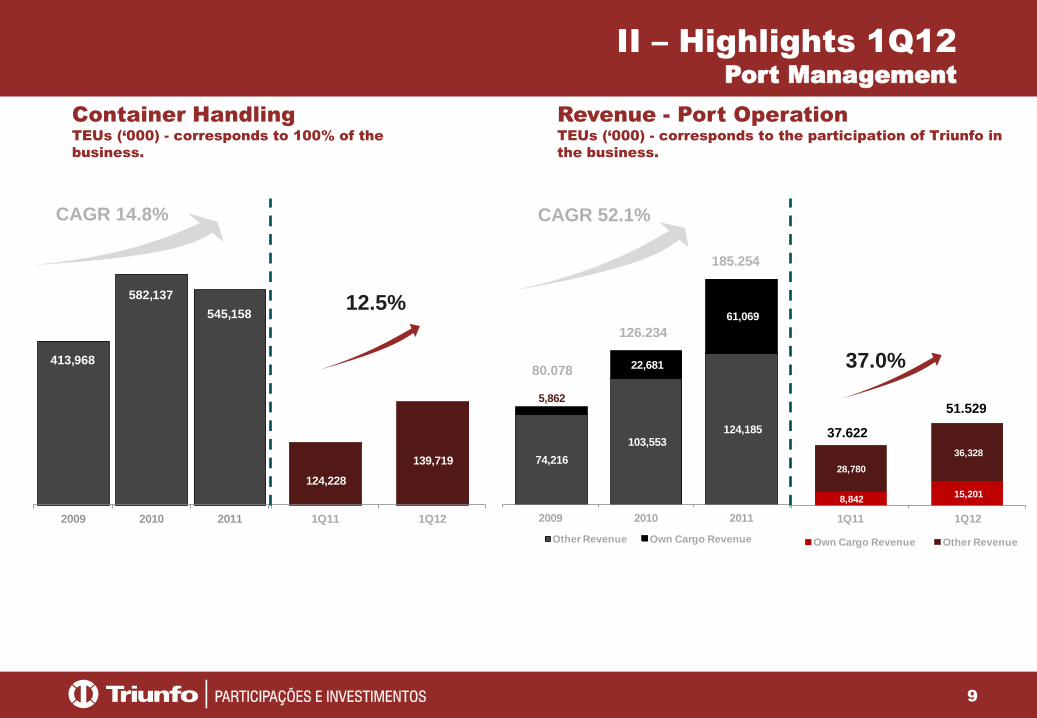

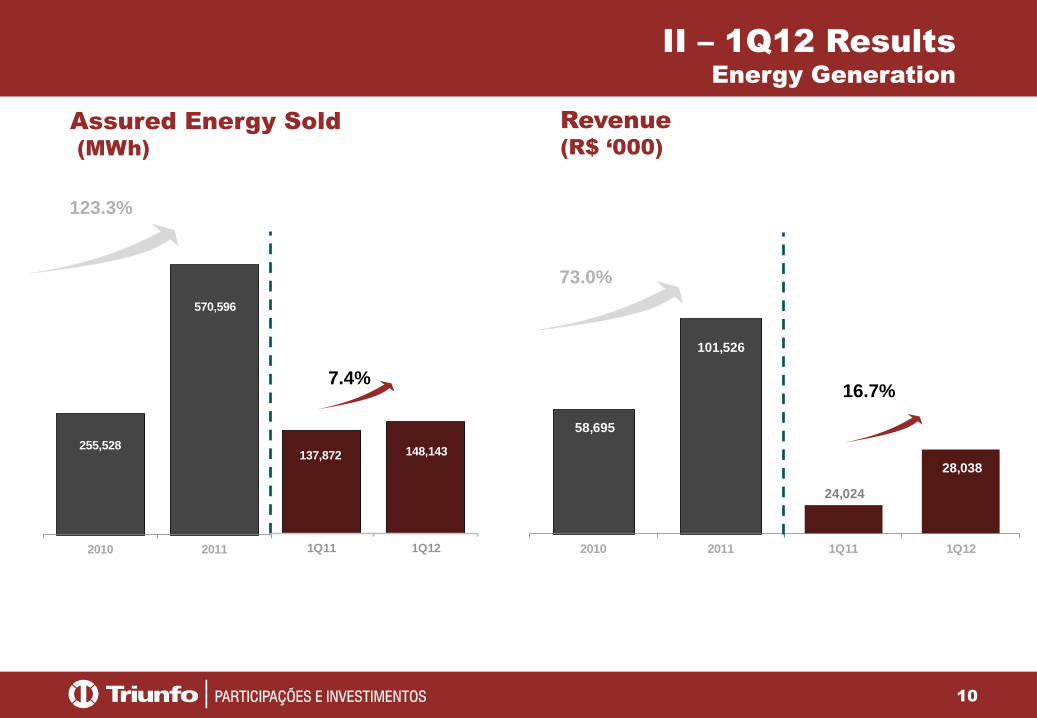

Traffic volume increased 7.6%, totaling 21.3 million equivalent vehicles. Handled container volume at Portonave reached 139,719 TEUs, 12.5% higher than 1Q11. Assured Energy Sold was 148,143 MWh, a 7.4% increase over 1Q11. From March 2012, Cabotage has been operating with a fleet of four ships, offering full service

with weekly stopovers at the terminals where it operates.

Adjusted EBITDA was R$110 million in 1Q12, 22.2% above the prior year, a margin of 54.4%, totaling

R$ 372 million LTM. Net Income in 1Q12 was R$15.0 million. The Dividend Calculation Base was R$31.9 million for the

quarter, an increase of 28.8% over the prior year, representing a dividend payout of R$ 0.055 per share.

5

I - Highlights 1Q12

In February 2012, the Company, in partnership with UTC Participações S.A and Egis Airport Operation,

won the auction for the expansion, maintenance and operation of the Campinas International Airport. The

result was ratified by the National Civil Aviation Agency (ANAC) in April.

In March 2012, the Company’s Board of Directors approved the first issuance of Promissory Notes

amounting to R$300 million with a maturity of 180 days. The use of proceeds is to pay the outstanding

balance of the 2nd debentures of the Company, and for investments in the Company and its subsidiaries.

6

Digite aqui o Título

da Palestra

Digite aqui o Nome do Palestrante e a Data

II – 1Q12 Results

7

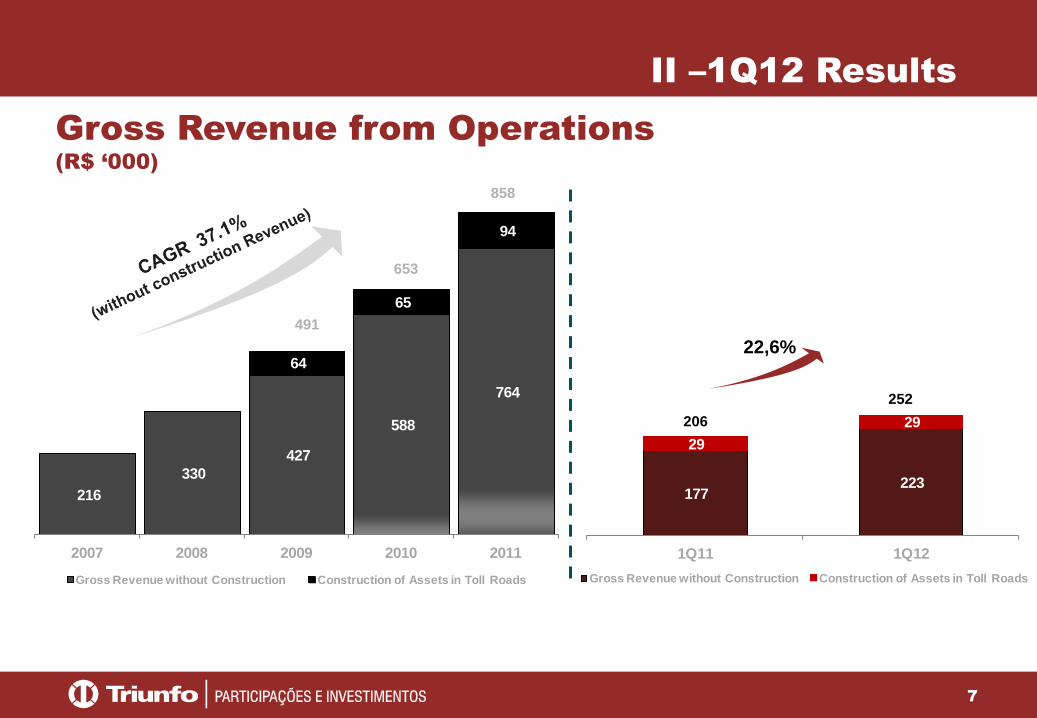

216

330

427

588

764

64

65

94

2007 2008 2009 2010 2011

Gross Revenue without Construction Construction of Assets in Toll Roads

177 223

29

29

1Q11 1Q12

Gross Revenue without Construction Construction of Assets in Toll Roads

Gross Revenue from Operations

(R$ ‘000)

22,6%

II –1Q12 Results

252

206

858

653

491

8

19,793

21,290

1Q11 1Q12

64,085

70,985

76,940

2009 2010 2011

Traffic – Equivalent Vehicles

(‘000) - corresponds to 100% of the business.

CAGR 9.6%

Revenue – Toll Roads*

(‘000) - corresponds to the participation of Triunfo in the

business.

7.6%

* It does not include revenues of construction and other revenue

114,265 128,826

1Q11 1Q12

341,940

398,206

451,196

2009 2010 2011

12.7%

II – Highlights 1Q12

Toll Roads

CAGR 14.9%

9

413,968

582,137

545,158

2009 2010 2011

124,228

139,719

1Q11 1Q12

74,216

103,553 124,185

5,862

22,681

61,069

2009 2010 2011

Other Revenue Own Cargo Revenue

8,842 15,201

28,780

36,328

1Q11 1Q12

Own Cargo Revenue Other Revenue

Container Handling

TEUs (‘000) - corresponds to 100% of the

business.

Revenue - Port Operation

TEUs (‘000) - corresponds to the participation of Triunfo in

the business.

37.0%

CAGR 14.8% CAGR 52.1%

12.5%

II – Highlights 1Q12

Port Management

185.254

126.234

80.078

51.529

37.622

10

Assured Energy Sold

(MWh)

II – 1Q12 Results

Energy Generation

Revenue

(R$ ‘000)

137,872 148,143

1Q11 1Q12

255,528

570,596

2010 2011

123.3%

7.4%

58,695

101,526

2010 2011

24,024

28,038

1Q11 1Q12

16.7%

73.0%

11

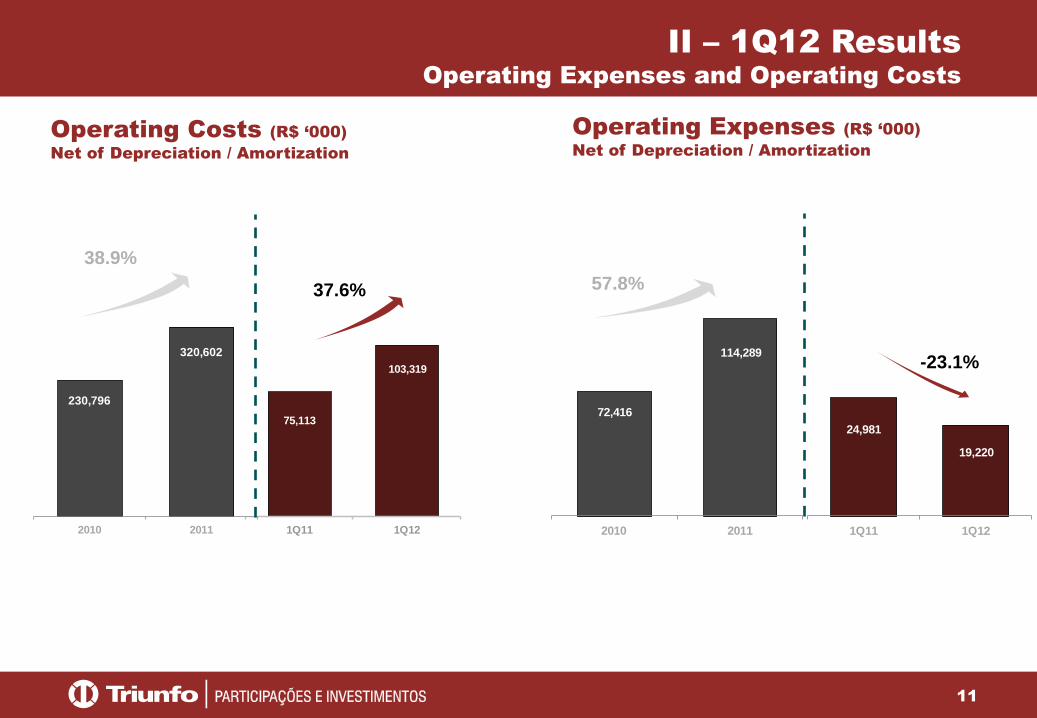

Operating Expenses (R$ ‘000)

Net of Depreciation / Amortization

II – 1Q12 Results

Operating Expenses and Operating Costs

Operating Costs (R$ ‘000)

Net of Depreciation / Amortization

75,113

103,319

1Q11 1Q12

230,796

320,602

2010 2011

24,981

19,220

1Q11 1Q12

72,416

114,289

2010 2011

37.6%

-23.1%

38.9%

57.8%

12

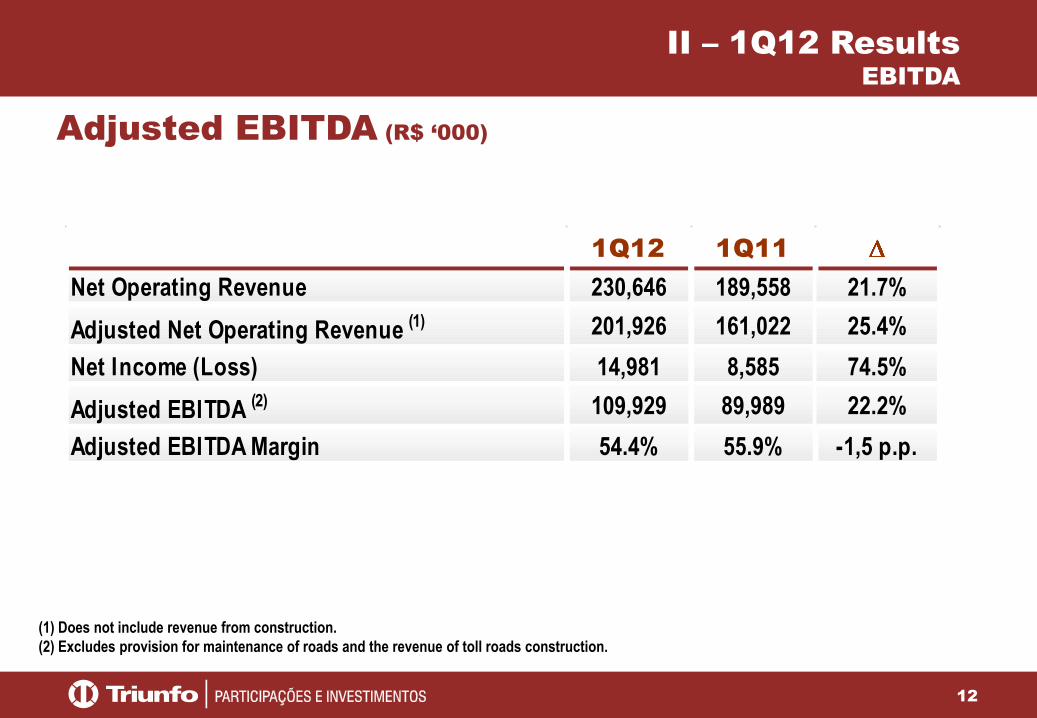

II – 1Q12 Results

EBITDA

Adjusted EBITDA (R$ ‘000)

(1) Does not include revenue from construction. (2) Excludes provision for maintenance of roads and the revenue of toll roads construction.

1Q12 1Q11

Net Operating Revenue 230,646 189,558 21.7%Adjusted Net Operating Revenue (1) 201,926 161,022 25.4%Net Income (Loss) 14,981 8,585 74.5%Adjusted EBITDA (2) 109,929 89,989 22.2%Adjusted EBITDA Margin 54.4% 55.9% -1,5 p.p.

13

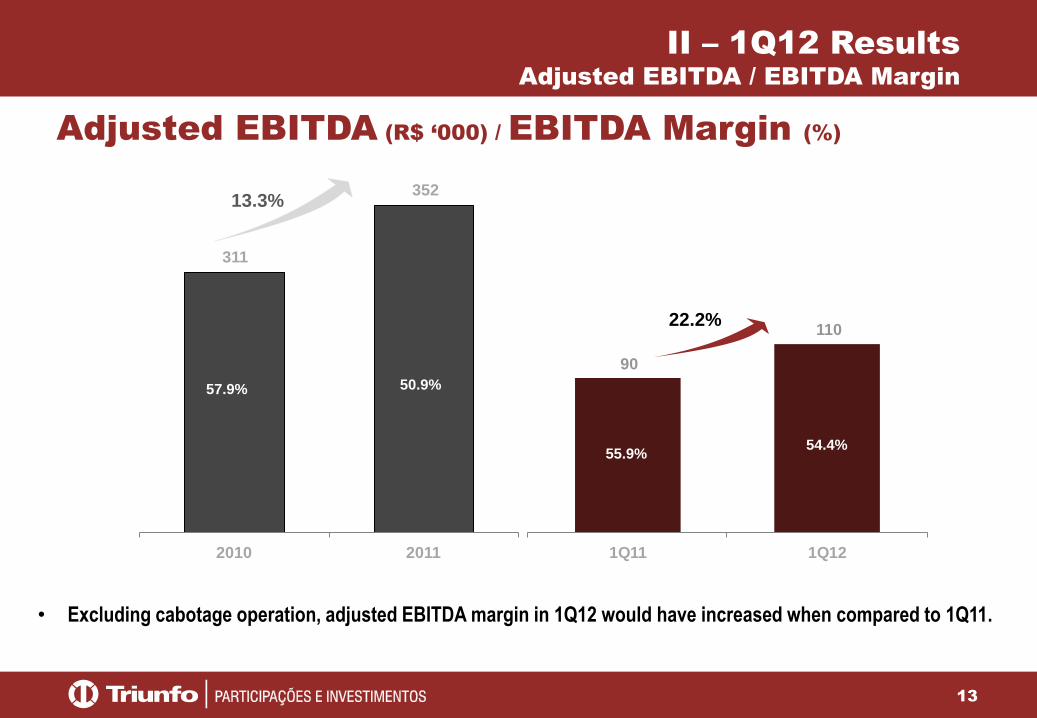

Adjusted EBITDA (R$ ‘000) / EBITDA Margin (%)

58.1%

54.8%

50.9% 57.9%

90

110

1Q11 1Q12

311

352

2010 2011

57.9% 50.9%

55.9% 54.4%

13.3%

22.2%

• Excluding cabotage operation, adjusted EBITDA margin in 1Q12 would have increased when compared to 1Q11.

II – 1Q12 Results

Adjusted EBITDA / EBITDA Margin

14

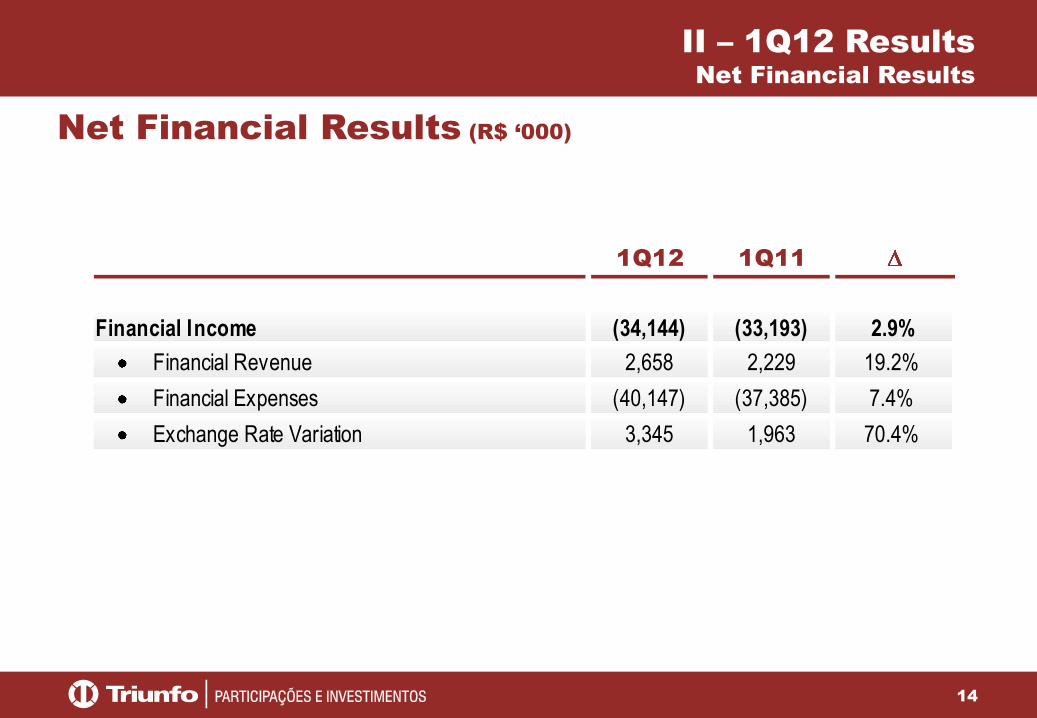

Net Financial Results (R$ ‘000)

1Q12 1Q11

Financial Income (34,144) (33,193) 2.9% Financial Revenue 2,658 2,229 19.2%

Financial Expenses (40,147) (37,385) 7.4%

Exchange Rate Variation 3,345 1,963 70.4%

II – 1Q12 Results

Net Financial Results

15

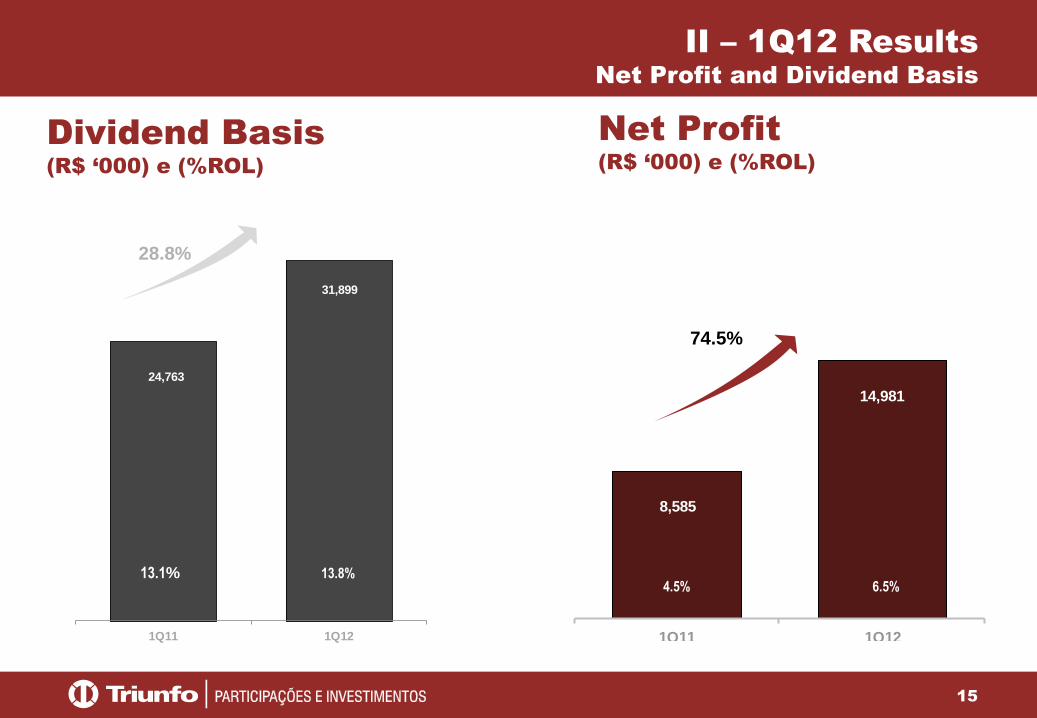

Net Profit

(R$ ‘000) e (%ROL)

II – 1Q12 Results

Net Profit and Dividend Basis

Dividend Basis

(R$ ‘000) e (%ROL)

8,585

14,981

1Q11 1Q12

24,763

31,899

1Q11 1Q12

74.5%

28.8%

6.5% 4.5% 13.8% 13.1%

16

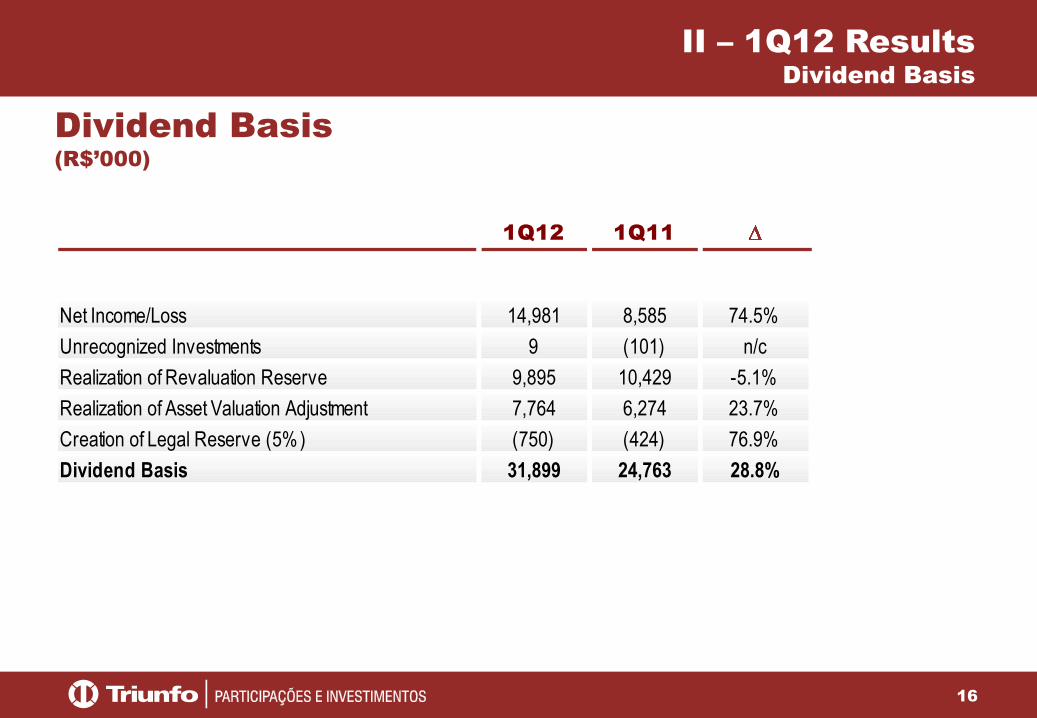

Dividend Basis

(R$’000)

1Q12 1Q11

Net Income/Loss 14,981 8,585 74.5%

Unrecognized Investments 9 (101) n/c

Realization of Revaluation Reserve 9,895 10,429 -5.1%

Realization of Asset Valuation Adjustment 7,764 6,274 23.7%

Creation of Legal Reserve (5%) (750) (424) 76.9%

Dividend Basis 31,899 24,763 28.8%

II – 1Q12 Results

Dividend Basis

17

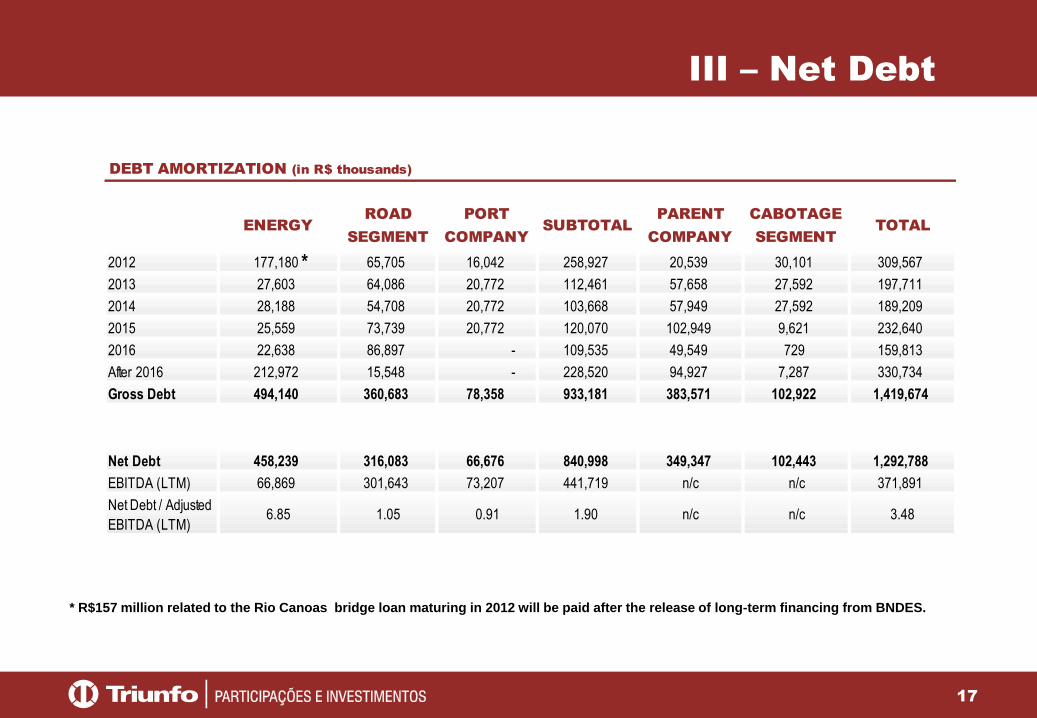

ENERGY

ROAD

SEGMENT

PORT

COMPANY

SUBTOTAL

PARENT

COMPANY

CABOTAGE

SEGMENT

TOTAL

2012 177,180 65,705 16,042 258,927 20,539 30,101 309,567

2013 27,603 64,086 20,772 112,461 57,658 27,592 197,711

2014 28,188 54,708 20,772 103,668 57,949 27,592 189,209

2015 25,559 73,739 20,772 120,070 102,949 9,621 232,640

2016 22,638 86,897 - 109,535 49,549 729 159,813

After 2016 212,972 15,548 - 228,520 94,927 7,287 330,734

Gross Debt 494,140 360,683 78,358 933,181 383,571 102,922 1,419,674

Net Debt 458,239 316,083 66,676 840,998 349,347 102,443 1,292,788EBITDA (LTM) 66,869 301,643 73,207 441,719 n/c n/c 371,891

Net Debt / Adjusted

EBITDA (LTM) 6.85 1.05 0.91 1.90 n/c n/c 3.48

DEBT AMORTIZATION (in R$ thousands)

III – Net Debt

*

* R$157 million related to the Rio Canoas bridge loan maturing in 2012 will be paid after the release of long-term financing from BNDES.

18

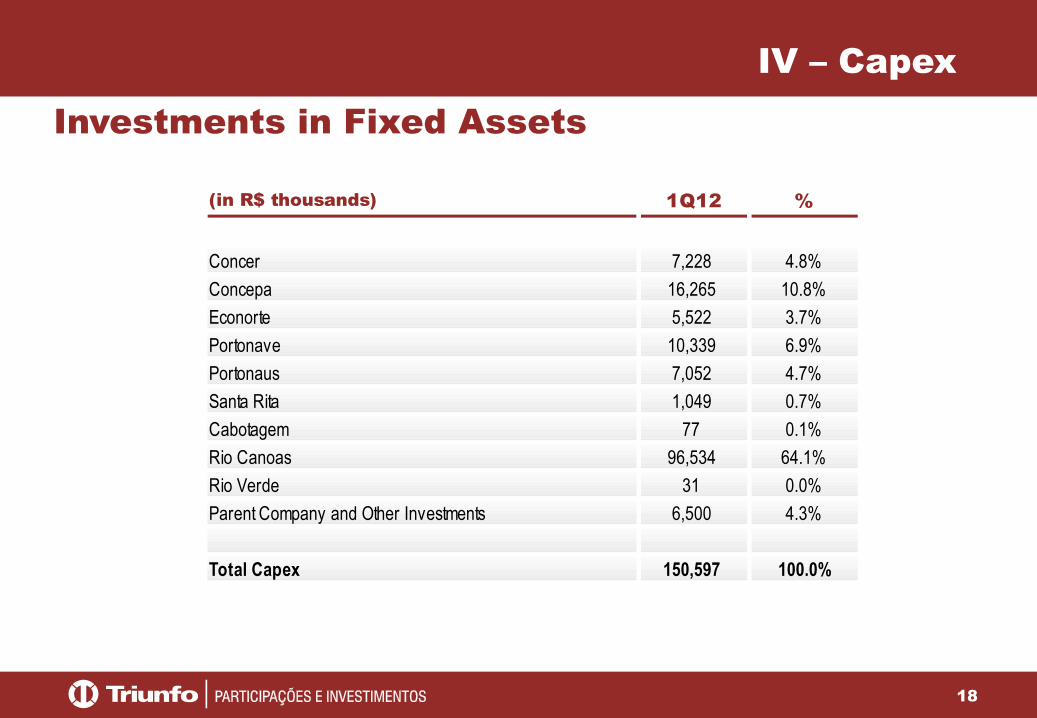

IV – Capex

Investments in Fixed Assets

(in R$ thousands) 1Q12 %

Concer 7,228 4.8%

Concepa 16,265 10.8%

Econorte 5,522 3.7%

Portonave 10,339 6.9%

Portonaus 7,052 4.7%

Santa Rita 1,049 0.7%

Cabotagem 77 0.1%

Rio Canoas 96,534 64.1%

Rio Verde 31 0.0%

Parent Company and Other Investments 6,500 4.3%

Total Capex 150,597 100.0%

19

www.tpisa.com.br

Triunfo São Paulo

Rua Olimpíadas 205 14º andar cj. 1402

CEP 04551-000 São Paulo SP BR

Fone 55 11 2169 3999

Fax 55 11 2169 3969

Rua Olimpíadas 205 14º andar cj. 1402 CEP 04551-000 São Paulo SP BR

Fone 55 11 2169 3999 Fax 55 11 2169 3939

www.triunfo.com

Recommended