Annual Report 2009

UBank Ltd.

2 / Annual Report 2009

UBank Ltd.

6 The Board of Directors’ Report to Shareholders’ General Meeting

115 Management Review of the Bank’s Financial Position and Operating Results

135 CertificationsoftheGeneralManagerandthe Chief Accountant

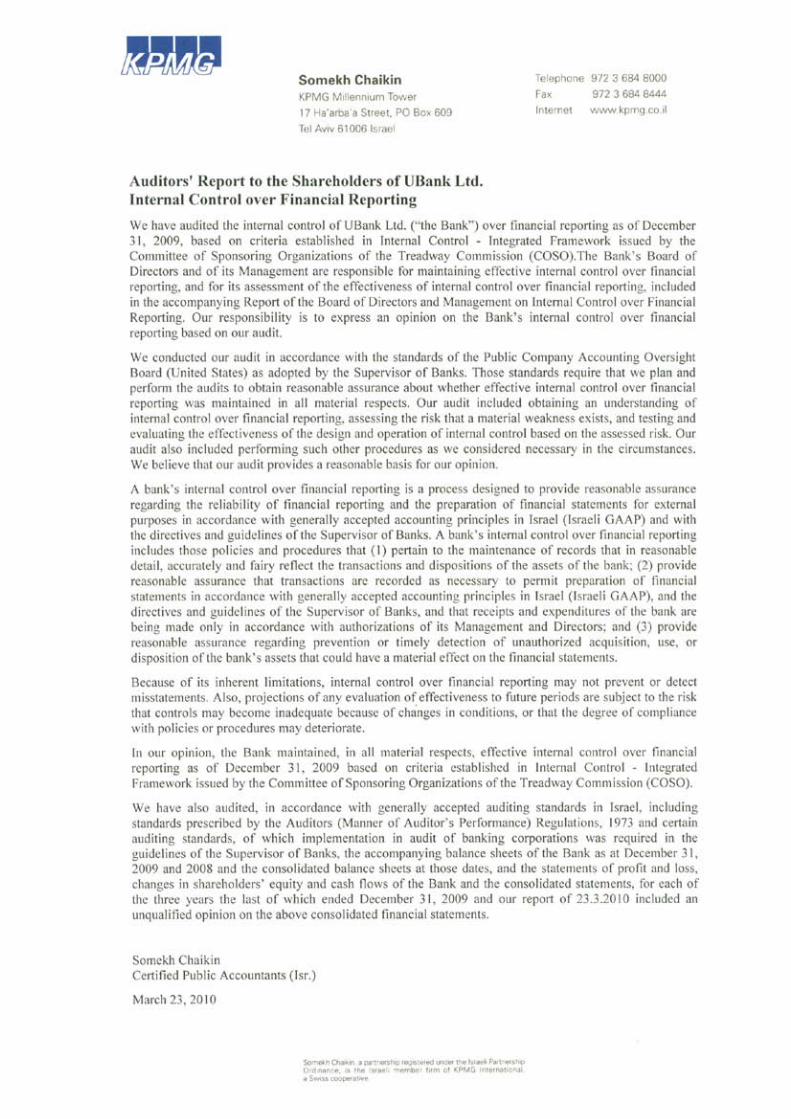

138 Report of the Board of Directors and Management Regardinginternalcontroloverfinancialreporting, and auditor’s report to the shareholders of UBank Ltd. Regardinginternalcontroloverfinancialreporting.

142 FinancialStatementsasatDecember31,2009

This is a translation from the Hebrew and has been preparedforconvenienceonly.Incaseofanydiscrepancy,theHebrewwill prevail.

Annual Report 2009

Contents

4 / Annual Report 2009

UBank Ltd.

Description of the General Development of Bank’s Business6 History of the Bank6 ProfitandProfitability8 Developments in Balance Sheet items11 Holdings Structure Chart12 SignificantInvesteecompanies12 Information about the Parent Company12 Description of the Bank’s Operational Segments13 Distribution of Dividends13 The Bank’s Rating by a rating company13 Human Resources15 Restrictions and Supervision of the Bank’s Activities16 SignificantAgreements16 Information Systems18 Legal Proceedings

General Environment and Influence of External Factors on the Bank’s Activity19 Economic Developments in 200921 Updates in legislation in respect of the Banking system in 2009

47 Description of the Bank’s Business according to Operational Segments59 Fixed assets and Facilities59 Taxation

Additional Information59 Risk Management Policy95 Accounting Policy on Critical Matters and Critical accounting estimates99 Contribution to the Community and Donations99 Disclosure with Regard to the Bank’s Internal Auditor101 The Approval Process for Financial Report102 Report on Directors with Accounting and Financial Expertise103 Operation of the Board of Directors and Changes in Board Membership103 Members of the Bank’s Board of Directors106 Members of the Bank’s Management107 Assessment of Controls and Procedures with Regard to the Disclosure in the Financial Report108 DetailsoftheAmountsandBenefitspaidtotheRecipientsoftheHighestSalariesintheBank112 Auditing Accountants’ Remuneration

The Board of Directors’ Report to theShareholders’ General Meeting

Annual Report 2009

6 / Annual Report 2009

UBank Ltd.

Attheboardofdirectors’meetingwhichwasheldonMarch23,2010itwasresolvedtoapproveandpublishtheconsolidatedfinancialstatementsofUBankLtd(hereinafterreferredtoas“theBank”)anditsconsolidatedsubsidiariesfortheyearendedonDecember31,2009.

ThefinancialstatementshavebeenpreparedinaccordancewiththeSupervisionofBanks’directivesandguidelines.

Description of the General Development of the Bank’s Business

History of the Bank

TheBankwasincorporatedinIsraelin1934underthename“BankEretzIsraelle’ToeletHa’ashraiLtd”.In1965theBankwasacquiredbyBaronRothschildwhonamedit“IsraelGeneralBankLtd”.In1978,theBank’sshareswereissuedtothepublicontheTelAvivStockExchange.In1996,theBankwasacquiredbytheInvestecWorldBankingGroupandin1999theBank’snamewaschangedto“InvestecBank(Israel)Ltd”.OnDecember22,2004ownershipoftheBankwastransferredto“TheFirstInternationalBankofIsraelLtd”(hereinafterreferredtoas“FIBI”).

UpontheacquisitionoftheBankbyFIBI,andfollowingtheacceptanceinfullofapurchaseoffermadetothepublic,theBankbecameaprivatecompanyfullyheldbyFIBI.

Followingthechangeofownership,theBank’snamewaschangedinMarch2005to“UBankLtd”,whichactsasaseparateandindependentbank,specialisinginthepersonalbankingandcapitalmarketsegments.

ProfitAndProfitability

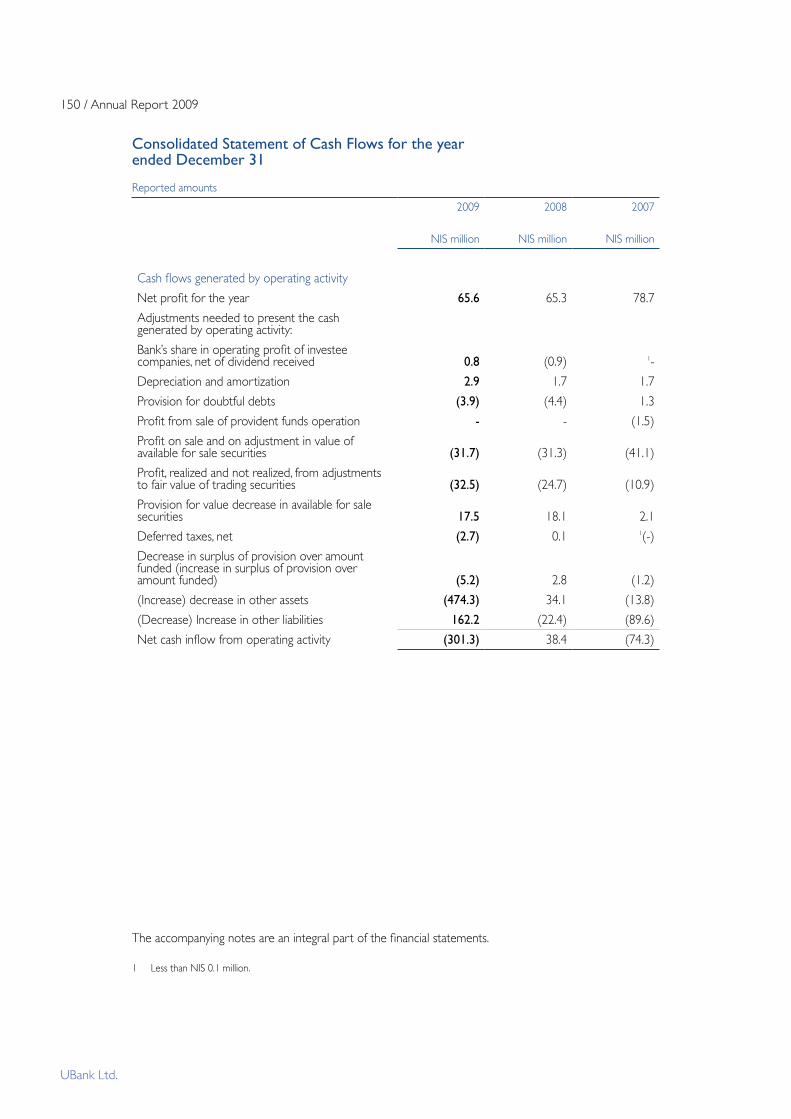

Net profitin2009amountedtoNIS65.6million,comparedwithNIS65.3millionin2008,anincreaseof0.5%.

Net profitinthefourthquarterof2009amountedtoNIS9.8million,comparedwithNIS19.7millioninthecorrespondingquarterlastyear,adecreaseof50.2%.Thedecreasederivesmainlyfromadecreaseintheprofitfromfinancingoperations.

Profit from ordinary operations before taxestotalledNIS109.8millionin2009,comparedwithNIS103.8millionin2008,anincreaseof5.8%.Theincreasederivesmainlyfromanincreaseof10.5%inprofitfromfinancingoperations(NIS15.3million),whichwasoffsetPartiallybyanincrease4.9%inoperatingandotherexpenses(NIS8.4million).See itemisation in the income and expenses analysis below.

Provision for taxes on profit from ordinary operations totalled NIS 43.4 million in 2009 and represented 39.5%oftheprofitbeforetax,comparedwithaprovisionofNIS39.4millionin2008thatrepresented38.0%oftheprofitbeforetax.

Theincreaseintheeffectiverateofprovisionfortaxesderivesfromadecreaseinreceiptofdividends,whichistaxesatlowertaxrate,anincreaseinprofitfaxratefor2009,from15.5%to16%andtheexpectedgradualinfluenceofthedecreaseinthestatutorytaxrateonthedeferredtaxesbalances(accordingtotheEconomicEfficiencyLaw),whichwerepartiallyoffsetbydecreaseinthecompaniestaxrate.

The return on equity of the net profit totalled 13.1% compared with 15.0% in 2008.

The return on equity of the profit from ordinary operations before taxes reached approx. 21.9% compared with approx. 23.9% in 2008.

The Board of Directors’ Report 2009 / 7

UBank Ltd.

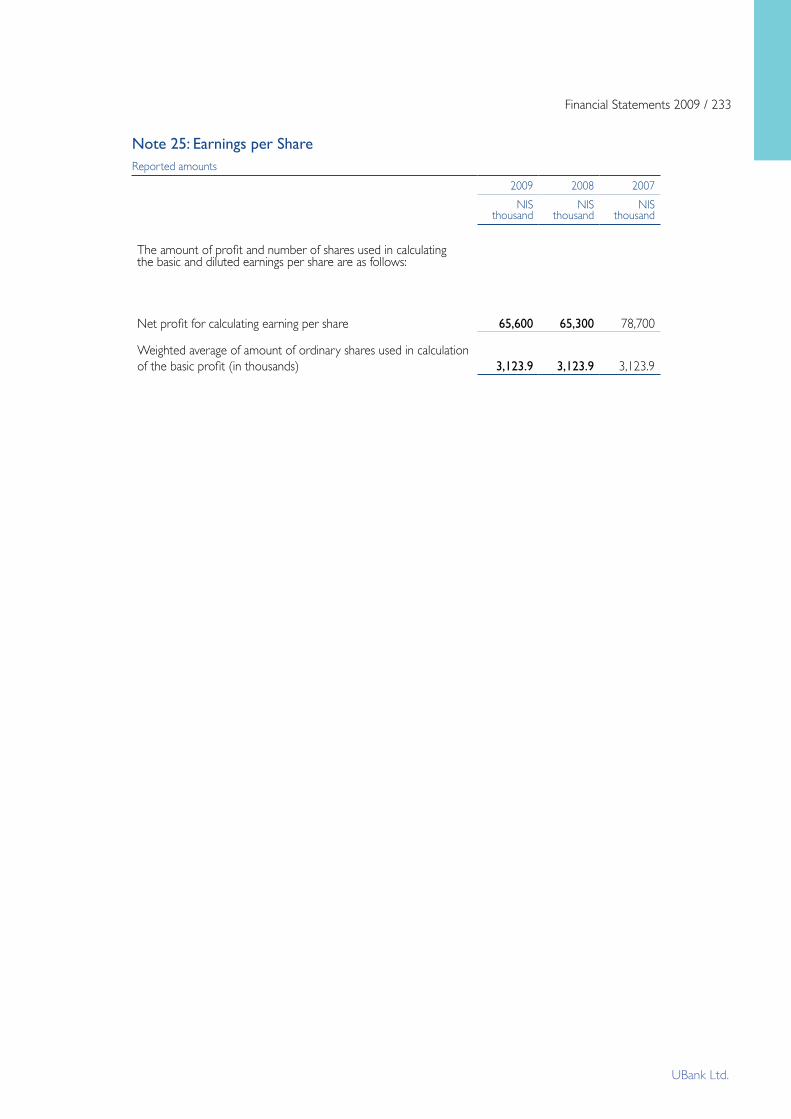

Net profit per NIS 1 par value of share capitalamountedtoNIS21.0in2009,comparedwithNIS20.9in 2008.

Income and Expenses

(NISmillion):

2009 2008 Change %

Profitfromfinancingoperations 160.4 145.1 10.5

Operating and other income 124.0 124.4 (0.3)

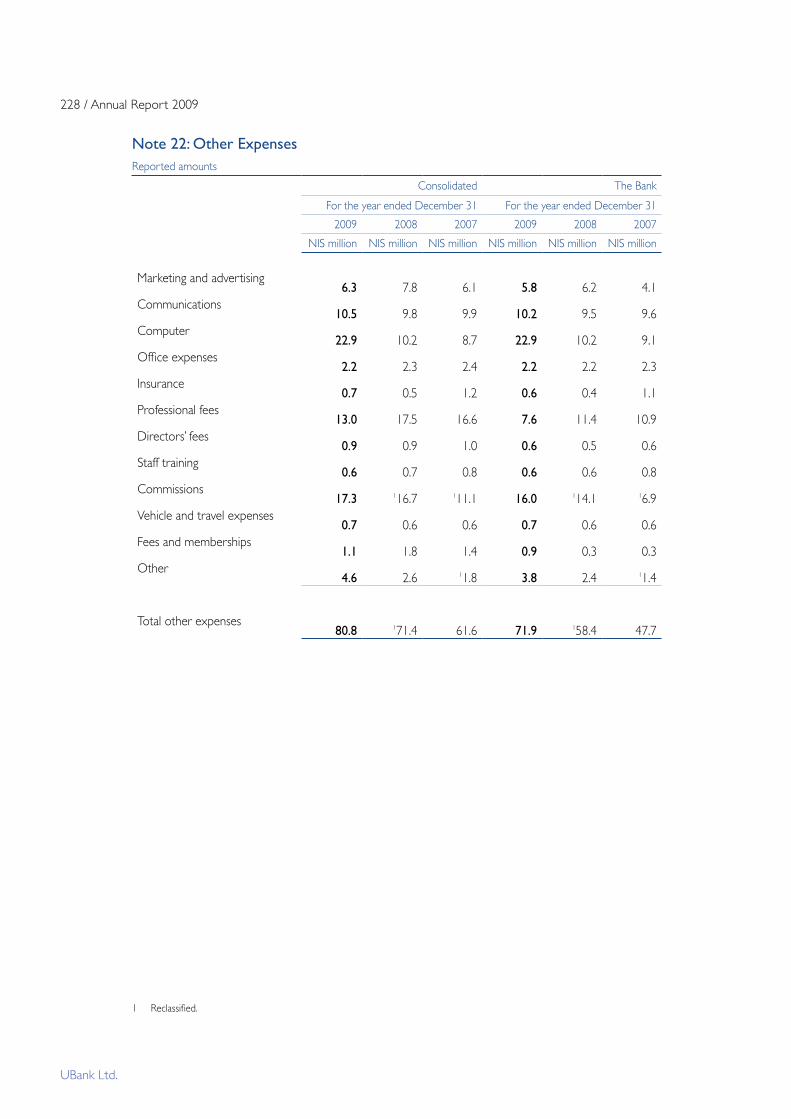

Operating and other expenses 178.5 170.1 4.9

Ofwhich:otherexpenses 80.8 71.4 13.2

Ofwhich:salariesexpenses 75.8 79.3 (4.4)

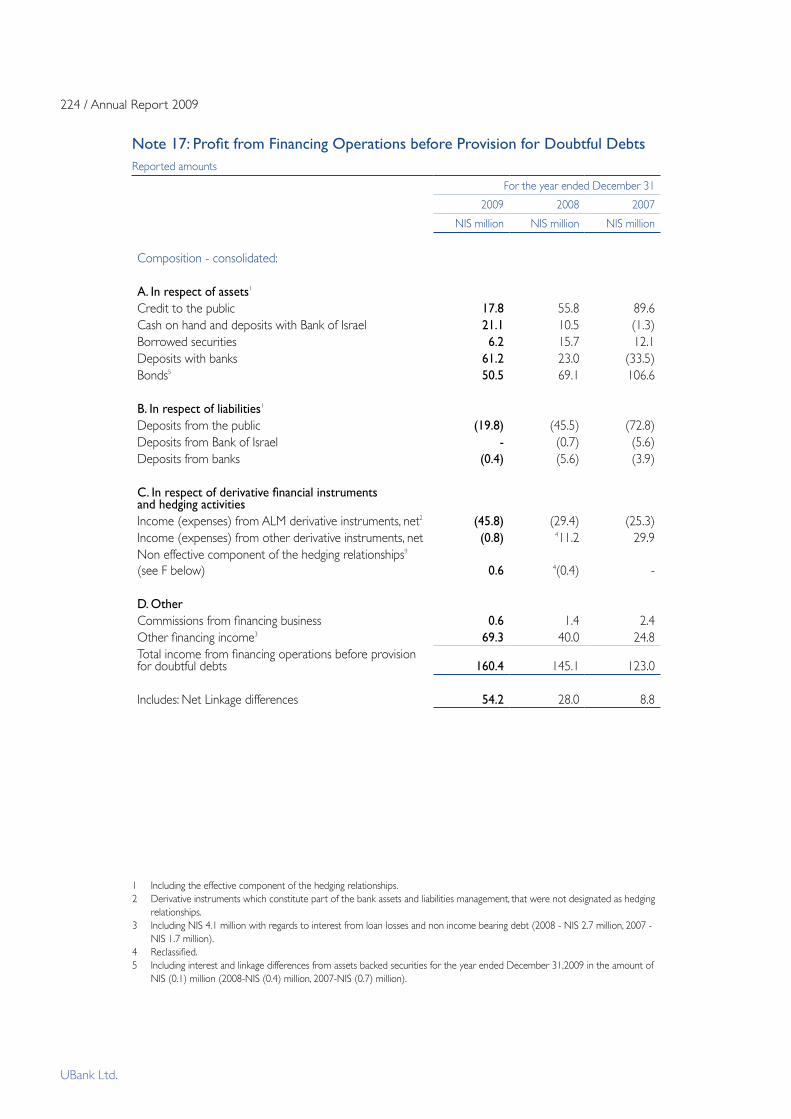

Profit from financing operations before provision for doubtful debtstotalledNIS160.4millionin2009,comparedwithNIS145.1millionin2008,anincreaseof10.5%.The increase derives mainly from an increase in the operating return on the available-for-sale securities portfolio,locallyandabroad,andanincreaseinprofitrealizationintheavailable-for-salesecuritiesportfolioin the amount of NIS 20.8 million.Profitsintheavailable-for-salesecuritiesportfolioin2009areoffsetbyotherthattemporaryimpairmentofNIS13.7million.(Anotherthantemporaryimpairmentwasrecordedin2008intheamountofNIS15.4millionofwhichwereNIS5.4millioninmortgage-backedbonds).Inadditionincreasederivesfromarangeofactivitiesintheareaofthefinancedivision,includingbeingamarket-makerforgovernmentbondsandothertradingactivities,whicharepartoftheroutineactivityofthe Bank.

Provision for doubtful debtsamountedtoanincomeintheamountofNIS3.9millionin2009,comparedwith an income in the amount of NIS 4.4 million in 2008.Theincomeinbothyearsderivesmainlyfromadecreaseinthespecificprovisionduetorepaymentofdebts.

Operating and other incomeamountedtoNIS124.0millionin2009,comparedwithNIS124.4millionin2008,adecreaseof0.3%.Thedecreasederivesmainlyfromadecreaseinincomefromforeigndealingroomcommissions,adecrease in income from management fees of the mutual funds of the Bank a decrease in income from dividend. The decrease was partially offset by an increase in income from the activity in the Various spheres of the capital market and an increase in the Bank’s Severance Pay Fund.DuetothenewBankCommission’sLaw,Managementfeesfrommutualfundsanddistributionfeeswerereclassifiedfromotherincometooperatingcommissions.

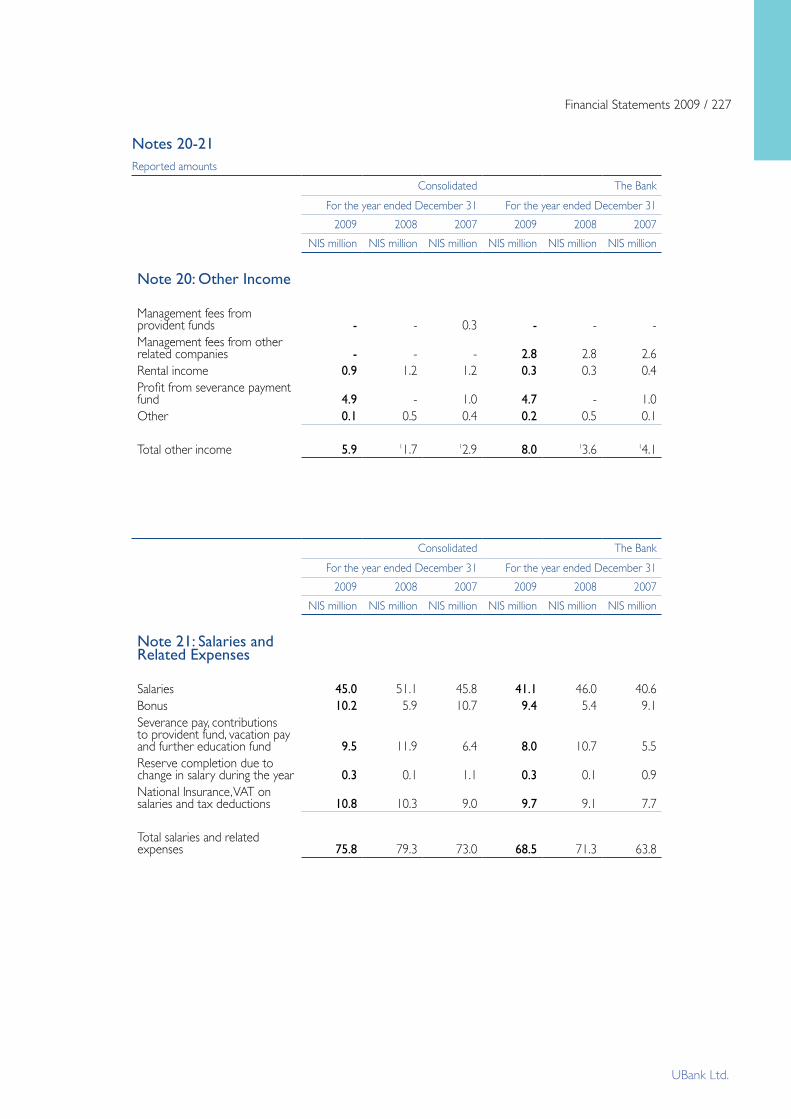

Operating and other expensesamountedtoNIS178.5millionin2009,comparedwithNIS170.1millionin2008,anincreaseof4.9%.Salaries and related expenses in 2009 amounted to NIS 75.8 million compared with NIS 79.3 million duringthecorrespondingperiodtheyearbefore,adecreaseof4.4%.ThedecreaseisduemainlytothereallocationofsalariesoftheBank’scomputerunitemployeestransferredtoMataf(”ComputerizationandFinancialOperations”-asubsidiarycompanyoftheFirstInternationalBankofIsrael),inlightoftheconversion of the computer systems completed in January 2009.Inaddition,lossesintheSeverancePayFundin2008wererecordedinthisitem.Thisdecreaseispartiallyoffset by the increase in the provision for bonuses related to performance in 2009 and an increase in the numberofemployeesemployedintheBank(anincreaseof2.6%),duemainlytotheopeningofbranchesforaffluentcustomers.

Maintenance expenses and depreciation of buildings and equipment in 2009 amounted to NIS 21.9 million,comparedwithNIS19.4millionduringthecorrespondingperiodlastyear,anincreaseof12.9%.The increase derives too mainly from an increase in expenses due to the opening of the new branches.

8 / Annual Report 2009

UBank Ltd.

Other expenses amounted to NIS 80.8 millionin2009,comparedwithNIS71.4 million in the corresponding period thelastyear,anincreaseof13.2%.Theincrease is due mainly to an increase in computerizationexpensesaftertheabove-mentionedconversionofthesystems,asa consequence of reallocation of salaries of the Bank’s computer unit employees transferredtoMataf,andariseintheoverall payment for computer services toMataf.(Forfurtherinformationonthesubject of the computer services agreement with Mataf see the chapter dealing with InformationSystemsonpage16).This increase was partially offset by a decrease in expenses for professional services,marketingandpublicity.

The rate of cover of operating expenses by operating incomewas69.5%in2009,compared with 73.1% in 2008.

The Bank’s share in profits (Losses) from equity basis companies amounted to a loss of NIS 0.8 million in2009,comparedwithaprofitthan0.9millionin2008.

Developments in Balance Sheet items

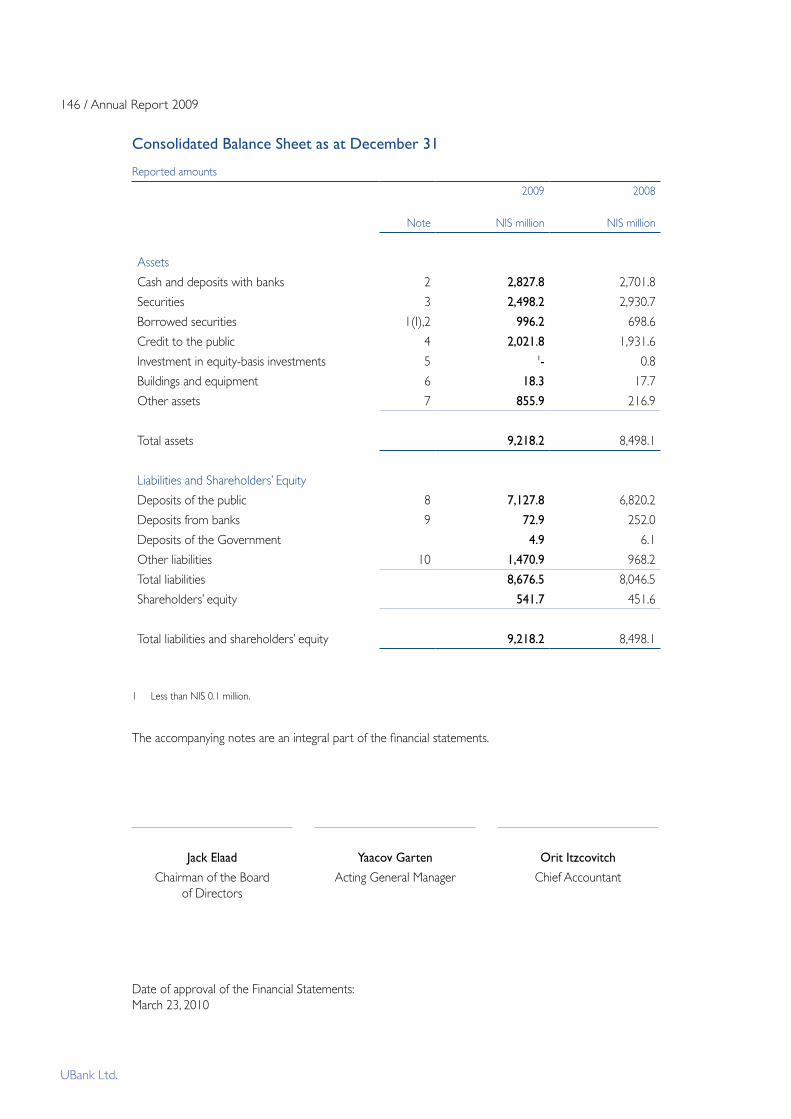

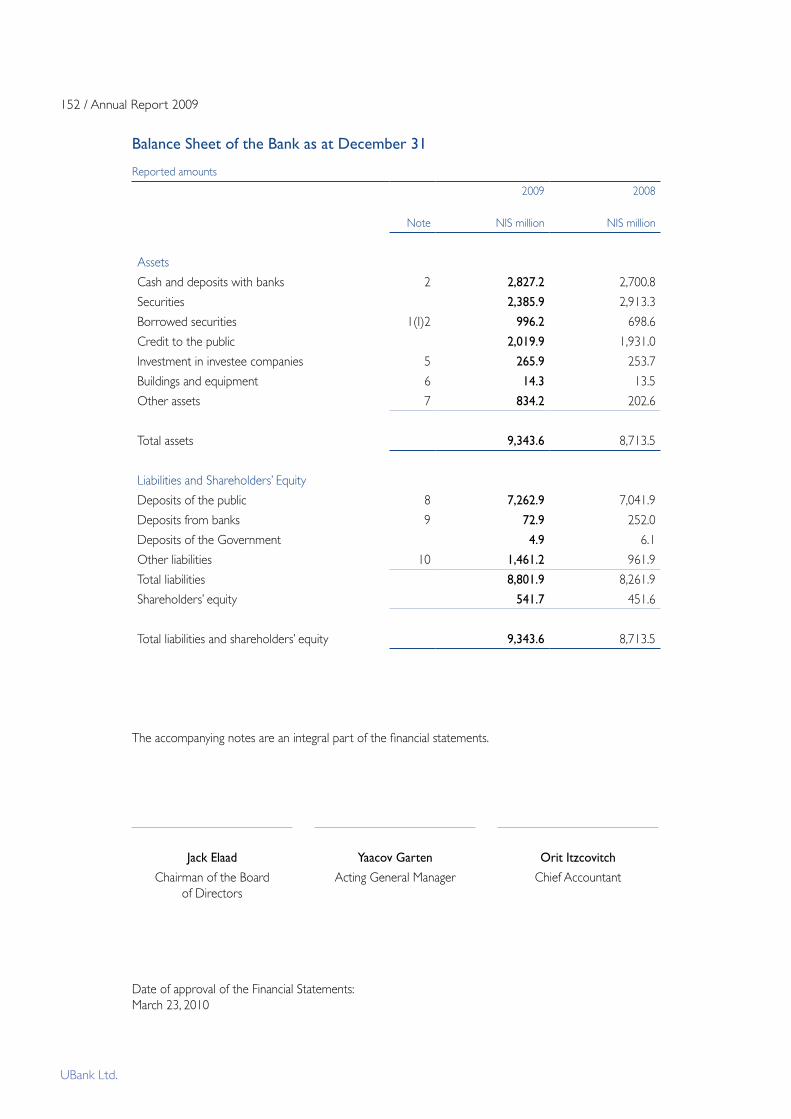

The total balance sheetasatDecember31,2009amountedtoNIS9,218.2million,comparedwithNIS8,498.1millionasatDecember31,2008,anincreaseof8.5%.

Cash and deposits with banksamountedtoNIS2,827.8millionattheendof2009,comparedwithNIS2,701.8millionattheendof2008,anincreaseof4.7%.

Investment in securitiesamountedtoNIS2,498.2millionattheendof2009,comparedwithNIS2,930.7millionattheendof2008,adecreaseof14.8%.Theinvestmentconsistsof:- GovernmentbondsandMakamintheamountofNIS2,060.9million.- Foreignbanksbonds(“Eurobonds“)intheamountofNIS209.3million,of20differentissuers.- Banks in Israel bonds in the amount of NIS 108.0 million.- Government owned companies bonds in the amount of NIS 12.3 million.- Corporate companies bonds in the amount of NIS 100.9 million’ of approx. 28 different issuers*.

* of which a non material investment in mortgage-backed bonds in the amount of approx. NIS 1.2 million,rated‘AAA’,issuedbytheFederalHomeLoanMortgageCorporation(FHLMC-“FreddieMac”)for a duration of 4.0 years.

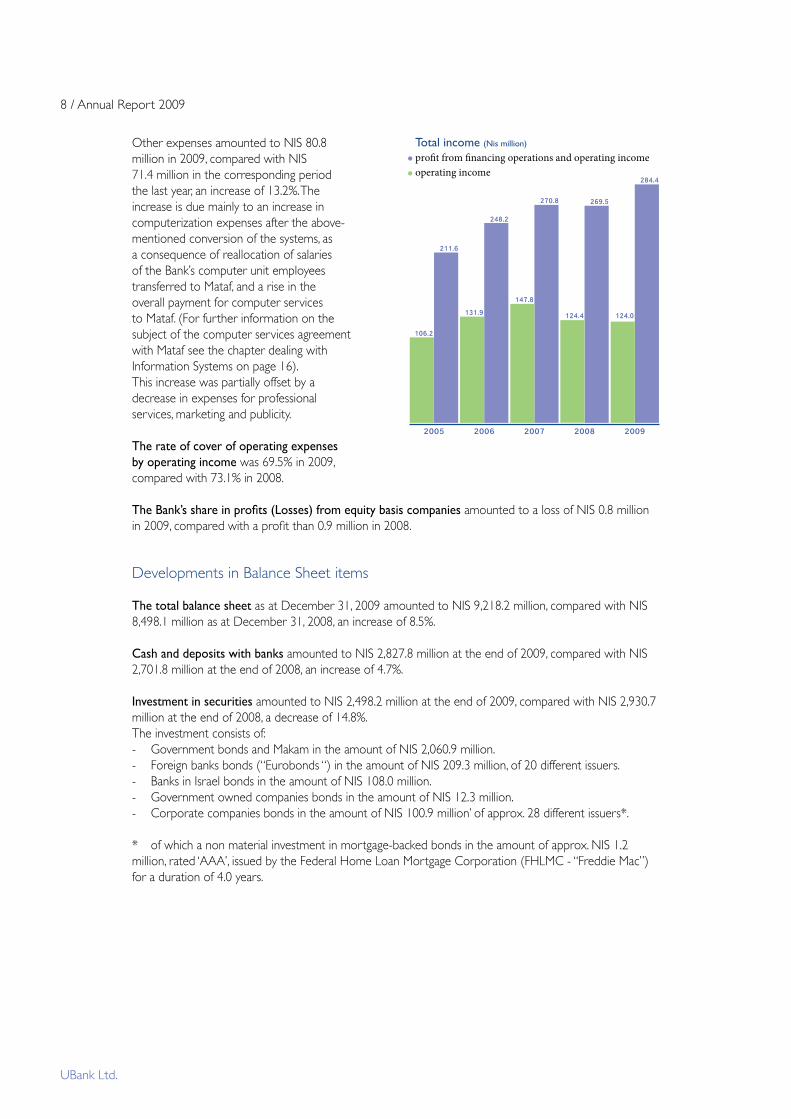

2008200720062005 2009

124.0

106.2

131.9

147.8

124.4

284.4

211.6

248.2

270.8 269.5

Total income (Nis million)

profit from financing operations and operating incomeoperating income

The Board of Directors’ Report 2009 / 9

UBank Ltd.

Following information regarding the duration and rate of the decrease of fair value of available for sale bonds,directlyrealizedinthecapitalreserveandnotrecordedinprofitandloss,asat31.12.09(inNISmillion):

Rate of decrease Durationofdecrease(inmonths)

Up to 6 6-9 9-12 Over 12 Total

Up to 16.8% (4.8) (0.8) - (6.6) (12.2)

Following information regarding the duration and rate of the decrease of fair value of available for sale bonds,directlyrealizedinthecapitalreserveandnotrecordedinprofitandloss,asat31.12.08(inNISmillion):

Rate of decrease Durationofdecrease(inmonths)

Up to 6 6-9 9-12 Over 12 Total

Up to 20% (24.9) (2.8) (2.9) (0.5) (31.1)

20% - 40% (3.2) (15.4) (0.3) (4.1) (23.0)

Over 40% (1.4) (1.4) (7.8) (4.7) (15.3)

Total (29.5) (19.6) (11.0) (9.3) (69.4)

ThedecreaseoffairvalueofbondsforDecember31,2009consistsof:Governmentbonds,governmentbondstradedabroadorbondsofgovernmentownedcompaniesintheamount of NIS 4.3 million. The entire rate of decrease of government bonds is up to 20% and up to 6 months.AdecreaseofNIS3.1millioninthefairvalueofforeignbank’sbonds,rated‘A-’andup(exceptforonebondthatisrated‘BBB’+)asatthebalancedate.(Seealsothereportofexistingcreditexposurestoforeignfinancialinstitutions).ThedecreaseconsistsNIS0.5millionupto6monthsandtherestisover12months. The entire rate of fair value decrease is up to 20%.CorporatebondsintheamountofNIS4.8million,consistsofNIS0.8millionbetween6-9months,andthe rest is over 12 months. The entire rate of the decrease is up to 20%. The negative capital reserve oftheBanksignificantlydecreasesin2009fromNIS69.4millionasat31December2008toNIS12.2million as at 31 December 2009. The date excludes the effect of a positive capital reserve and tax. The capitalreserveoftheBankasat31December,2009isnegativeintheamountofNIS4.3million,includingtheeffectsmentionedabove(seenote3Securities).

Whenexaminingtheneedtomakeaprovisionforimpairment,inaccordancewiththeaccountingpolicyforcriticalmattersandcriticalaccountingestimates,andinviewofthefactthattherewerenomaterialchangesconcerningthebondissuersmentioned,BankManagementisoftheopinionthatthereisnoneedtomakeaprovisionforimpairmentofanotherthantemporarynatureregardingthesedecreasesinvalue,inthefinancialstatementsasat31December2009.Theexaminingofimpairmentwasmadeaccordingtothe circular of the Banking Supervision department that was published on 1.3.09. See the section dealing with impairment of assets in the Accounting Policy on Critical Matters.

Credit to the publicamountedtoNIS2,021.8millionattheendof2009,comparedwithNIS1,931.6millionattheendof2008,anincreaseof4.7%.Theaveragebalancein2009wasNIS1,804.7millioncomparedwithanaveragebalanceofNIS1,950.6millionin2008,adecreaseof7.5%.Thedecreasederivesmainlyfromshorttermcreditforactivityinthecapital market.

10 / Annual Report 2009

UBank Ltd.

Other assetsamountedattheendof2009toNIS855.9million,comparedwithNIS216.9millionattheendof2008,anincreaseof294.6%.Theincreasederivesmainlyfromanincreaseinthenetclearingbalance in connection with securities activity with the Stock Exchange.

Deposits of the publicamountedtoNIS7,127.8millionattheendof2009,comparedwithNIS6,820.2millionattheendof2008,anincreaseof4.5%.Theaveragebalancein2009wasNIS6,736.6millioncomparedwithanaveragebalanceofNIS6,265.9millionin2008,anincreaseof7.5%.Theincreasederivesmainlyfromshorttermdepositsfromactivityinthe capital market.

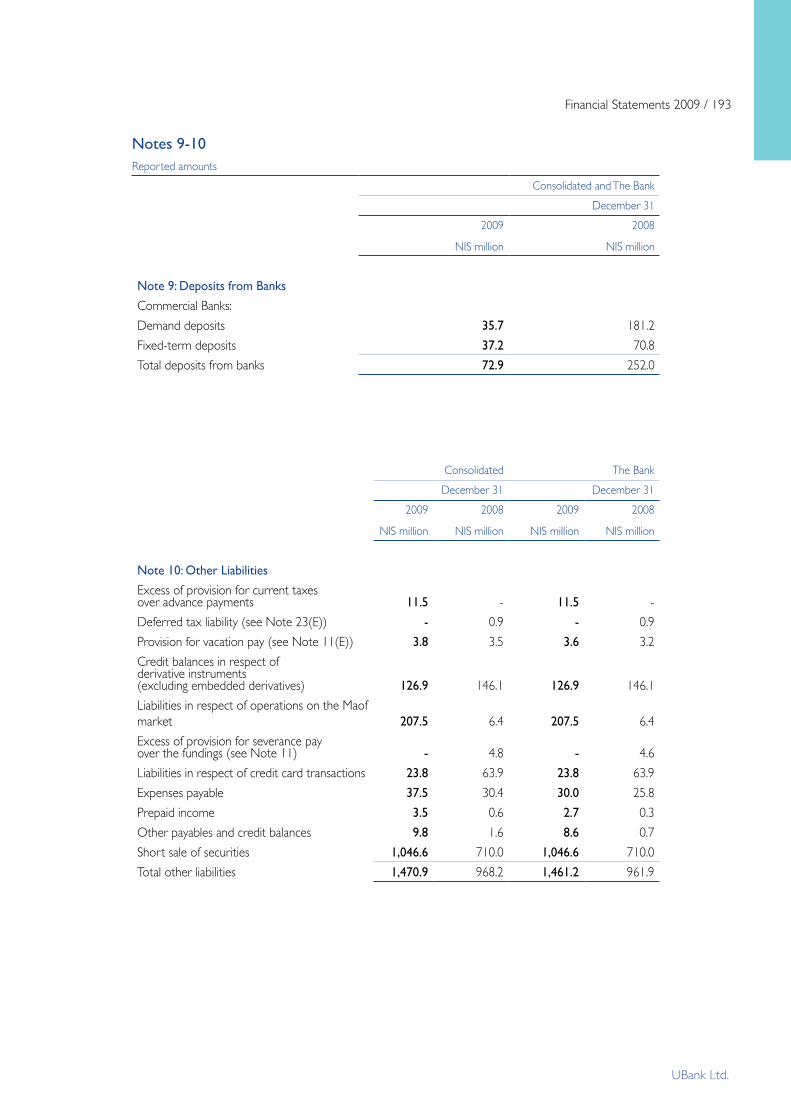

Deposits from banksamountedtoNIS72.9millionattheendof2009,comparedwithNIS252.0millionattheendof2008,adecreaseof71.1%.Movement in this item derives mainly from daily interbank activity.

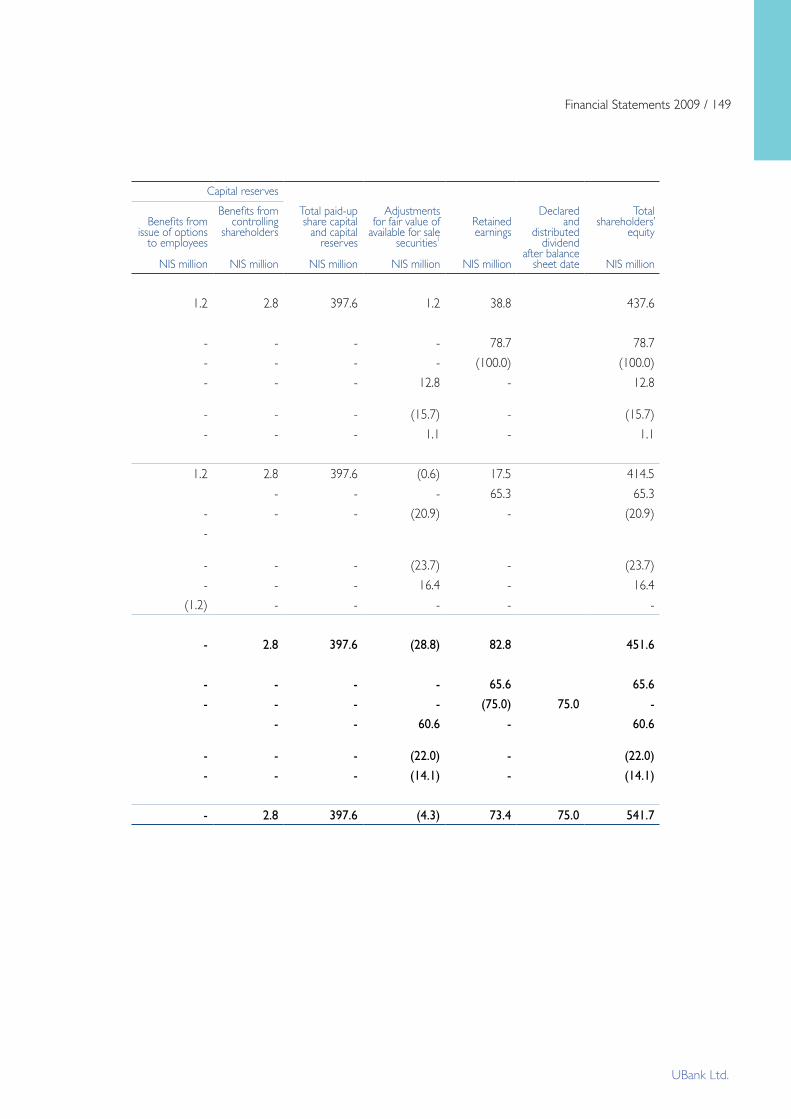

The Bank’s equityamountedtoNIS541.7milliononDecember31,2009,comparedwithNIS451.6milliononDecember31,2008.

The ratio of equity to total assetsstoodat5.9%attheendof2009,comparedwith5.3%attheendof2008.

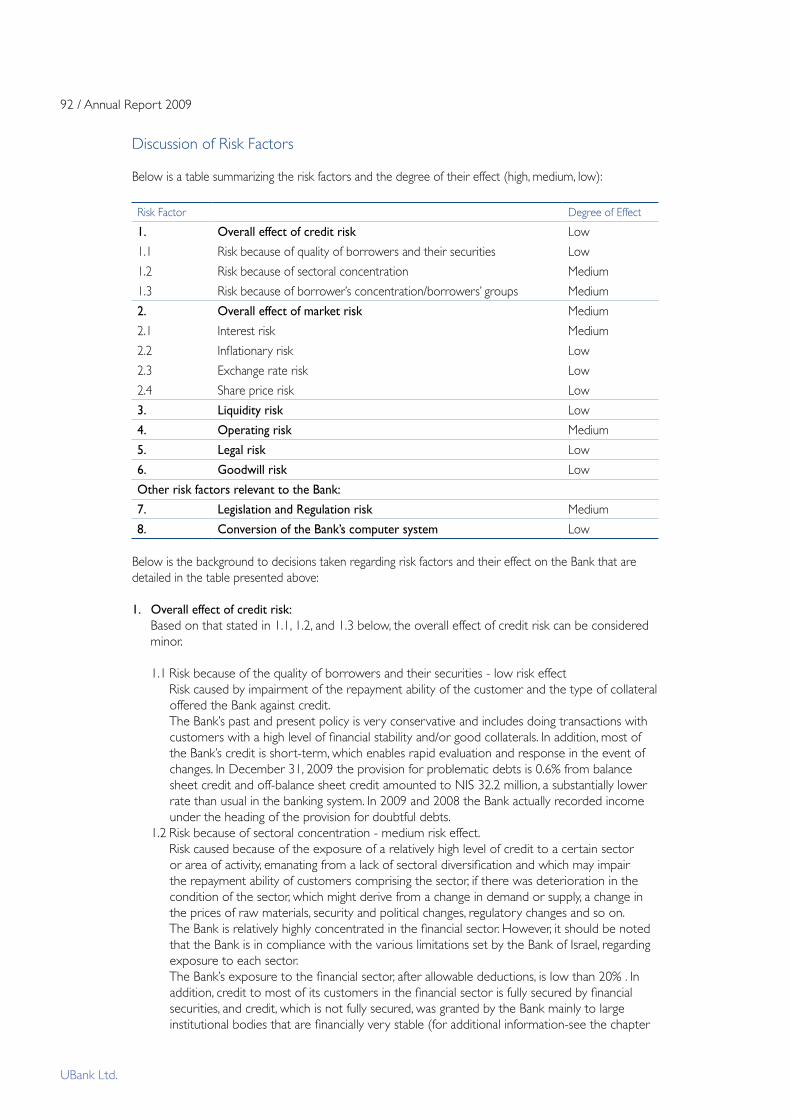

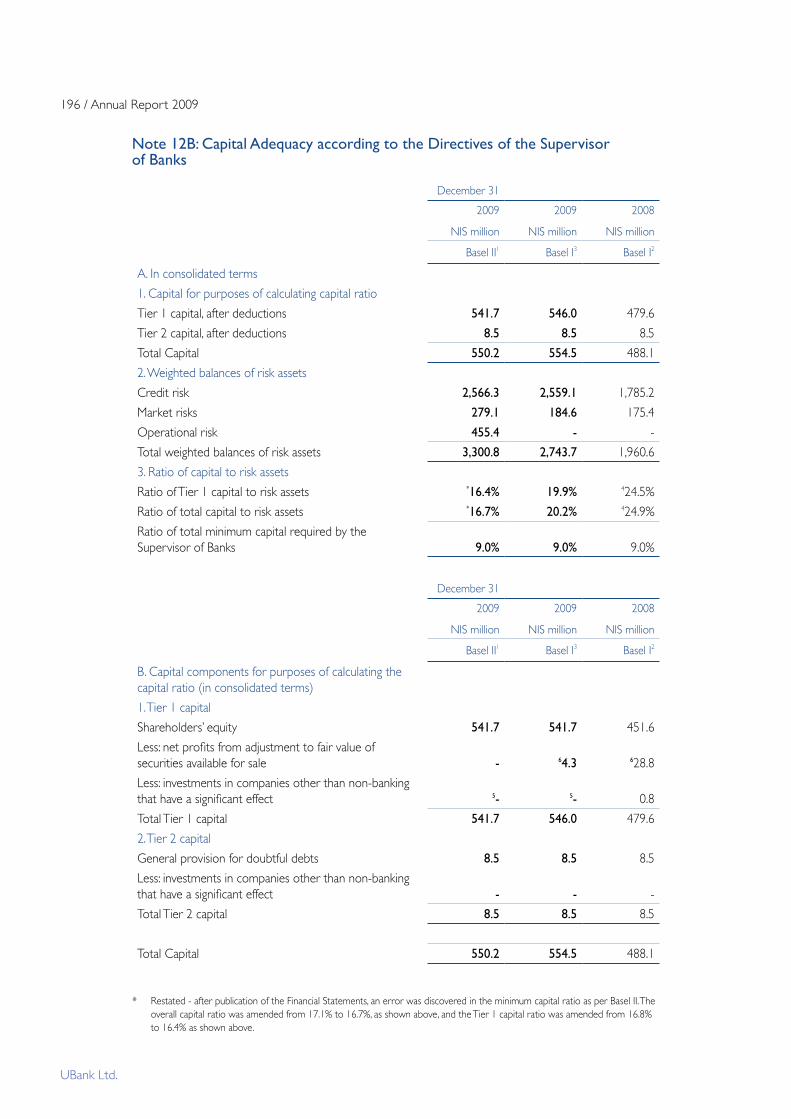

The capital to risk assets ratio according to proper Conduct of Banking Business Directive 311amountedto20.2%onDecember31,2009,comparedwith24.9%onDecember31,2008.The capital to risk assets ratio that is required by the Bank of Israel is 9%.

The capital to risk assets ratio, as of 31 December, 2009 calculated in accordance with the provisional directive “working Framework for Capital Measurement and Adequacy” (BaselII),is16.7%.

The Board of Directors’ Report 2009 / 11

UBank Ltd.

* Significantcompanies.

Holdings structure chart*

UBank Ltd

UBank Financial Asset Management LtdCapital 100%

UBank Trust Company LtdCapital 100%

UBank Mutual Funds LtdCapital 100%

UBank Underwriting & Consulting LtdCapital 100%

Manif Financial Services LtdCapital 19.6%

UBank Investments and Holdings LtdCapital 100%

12 / Annual Report 2009

UBank Ltd.

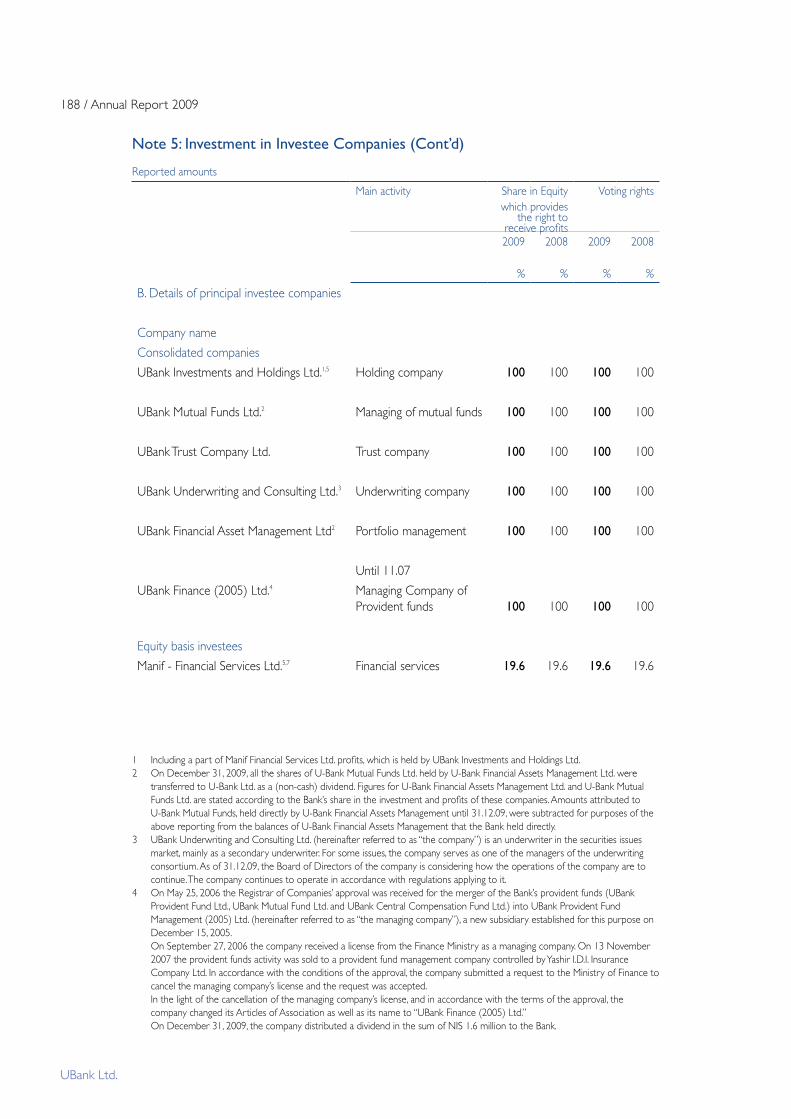

SignificantInvesteeCompanies

A. “UBankAssetManagementLtd.”(hereinafterreferredtoas“theCompany”)engagesinprovidinginvestment portfolio management services for private and institutional customers. Until 31 December,2009Thecompanywhollyowned“UBankMutualFundsLtd.”,whichengagesinmanagingvariousmutualfunds.On31December,2009theentireholdingwastransferredtoUBankLtd.(forfurtherinformation,seenote5).Thetotalassetsundermanagementattheresponsibilityofbothcompaniesin2009isapprox.NIS1.4billion,ofwhichapprox.NIS0.7billionrepresents investment portfolio management and approx. NIS 0.7 billion represents mutual fund management.

TheCompanyended2009withalossofNIS0.2million,comparedwithalossofNIS1.0millionin2008(excludingtheresultsof“UBankMutualFundsLtd”.).

B. “UBankMutualFunds”Ltd.ended2009withanetProfitofNIS0.2millioncomparedtoNIS1.2million in 2008.

C. "UbankTrustCompanyLtd."(henceforth:"theCompany")isengagedmainlyinprovidingtrustservicesformutualfunds,andinaddition,asatrusteeforbondsseriesofspcandadvancedfincialinstrumentsandholdingassetsofindividualsetc.ThenetprofitoftheCompanyfor2009totaledaboutNIS13.0million,comparedwithNIS13.5millionin2008.

D. “UBankUnderwriting&ConsultingLtd.”engagesinunderwritingissuesandfinancialcounselling.Thecompany’snetprofitamountedtolessthan0.1millionin2009,comparedwithalossoflessthan0.1millionin2008.Asof31December,2009theBoardofdirectorsofthecompanyisconsidering how the operations of the company are to continue.

E. “UBankInvestmentsandHoldingsLtd.”(henceforth:“thecompany”)isengagedmainlyinrentingpremises,equipmentandfurniturefortheBankandconnectedcompanies.

ThenetprofitoftheCompanyfor2009amountedtoNIS0.8million,comparedtoNIS4.4million in 2008.

Information about the Parent Company

TheFIBIGroupisoneofthefivelargestbankinggroupsinIsrael.TheGroupoperatesinanumberoffinancialactivitysectors:commercialbanking,privatebanking,mortgages,activityinthevariouslayersofthecapitalmarket,internationalfinancialactivity,leasingfinancing,factoring,creditcardsandvariousfinancialservices.InadditiontoUbank,theFIBIGroupownsthreecommercialbanksinIsrael-OtsarHahayalBank,PoaleyAgudatIsraelBankandMassadBankLtd.-and2subsidiariesinabroad,FIBIBank(UK)plcheadquarteredinLondonandFIBIBank(Switzerland)headquarteredinZurich.TheGroupoperatesthrough175branchesandextensionsinIsrael,outofwhich85branchesandextensionsattributedtotheParent Company.

Description of the Bank’s Operational Segments

ThefollowingisashortdescriptionofthesegmentsoftheBank’sbusinessactivities:

The Private Banking segment - includes all the Bank’s private customers and their businesses.These are both private customers belonging to the personal banking division and also private customers inthecapitalmarketdivision,whoseprincipaloperationsareinsecurities.Inaddition,thesegmentincludestheactivityoftheAssetManagementcompanyoftheBank,theFundManagementcompanyandtheBank’s Trust company customers except from trust services for mutual funds area.

The Corporate banking segment - includes all the institutional customers whose principal engagement is inthefinancialsphere,suchas:groupsengagedininsurance,pensionsandprovidentspheres,mutualfunds,

The Board of Directors’ Report 2009 / 13

UBank Ltd.

portfolio managers and the like. These customers are attributed to the capital market division.Inaddition,thesectorincludesthecustomersoftheTrustcompanyoftheBankintheareaoftrustservices to mutual funds.

The Financial segment-thissegmentincludestheactivitiesofthedealingrooms,liquidityunitandtheassets and liabilities management department of the Bank.

TheBankhasnosignificantactivityinthehouseholds,smallbusinesssegmentsandcommercialBankingSegment.

Fordetailedinformation,includingafinancialanalysis,seethesectionthatdiscussesthedescriptionofthebusiness of the Bank according to operational segments.

Distribution of Dividends

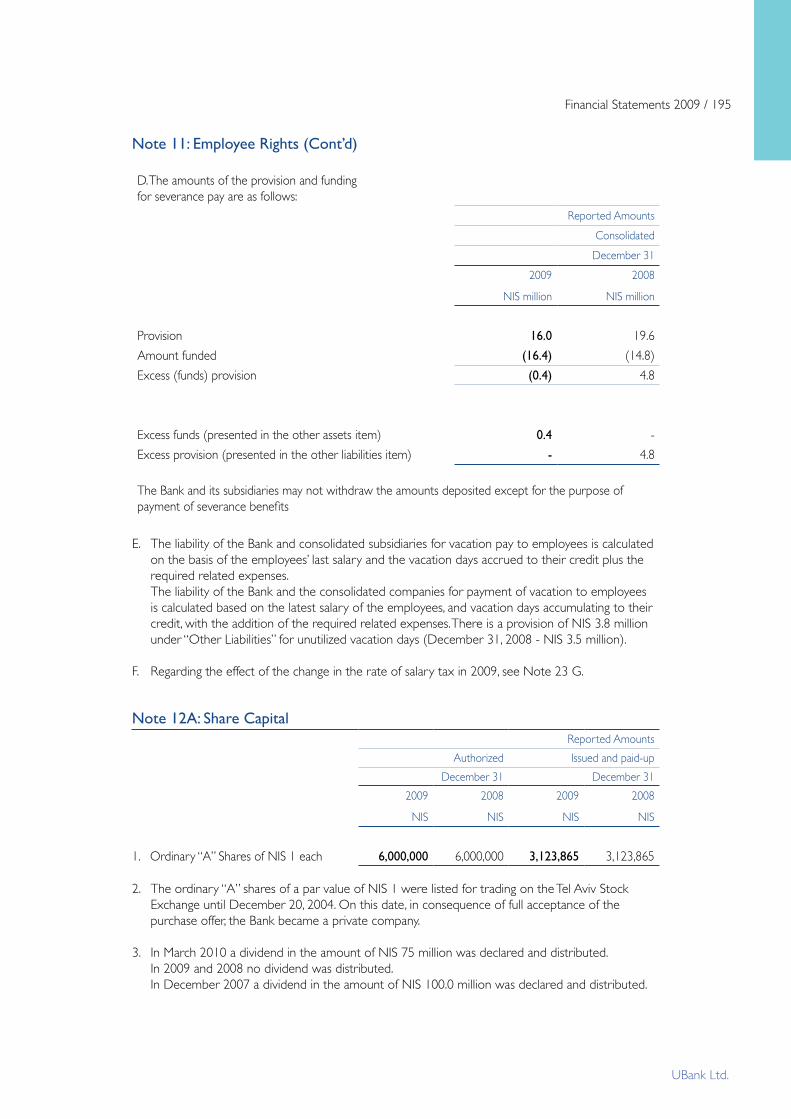

In December 2007 a dividend in the amount of NIS 100 million was declared and distributed.During 2008 and 2009 there was no distribution of dividends.In March 2010 a dividend in the amount of NIS 75 million was declared and distributed.

The Bank’s rating by a rating company

The“Midroog”companyratedtheBank’sdepositsasAa3andtheshort-termdepositswitharatingofP-1.

Human Resources

DescriptionoftheOrganizationalStructureandtheNumberofStaffemployed

FivemanagersaredirectlysubordinatetotheBank’sGeneralmanager,asfollows:

ThemanageressofthePersonalBankingdivision,towhomtheBank’sbranchesaresubordinated(includingthebusinessandcurrentaccount).Theaveragenumberofemployeesinthepersonalbankingdivisionin2009amountedto96(in2008-98).

The manager of the Capital Market division to whom the Israeli securities and foreign securities trading departments,theIsraelisecuritiesandforeignsecuritiesback-roomsystems,themutualfundsoperationsdepartmentandthebankingteamthatprovidesservicesforthecustomersofthedivision,areallsubordinate. The average number of employees in the Capital Market division in 2009 amounted to 83(in2008-80).

ThemanageroftheFinancialdivisiontowhomtheassetsandliabilitiesdepartment,theliquidityunitandthedealingroom,aresubordinate.TheaveragenumberofemployeesintheFinancialdivisionin2009amountedto13(in2008-14).

ThemanageroftheCentralServicesdivision,towhomthefollowingdepartmentsaresubordinate:Humanresourcesandadministration,creditandriskmanagement,Regulationandprocesses,thelegaldepartment,planningandmarketingandcomputerizationliaisonofficer.The number of workers employed at the Headquarters Division amounted in 2009 to 55 employees onaverage(in2008-68employees).Themaindecreaseinthenumberofworkersemployedderivesfrom the reallocation of the Bank’s computer unit employees to Mataf following the conversion of the computersystemscompletedinJanuary2009(forfurtherinformationseethechapterdealingwithInformationSystemsonpage16).

ThemanageressoftheChiefAccountantdivision,towhomthefollowingdepartmentsaresubordinate:accounting,internationalandreconciliationsandbookkeepingandpayments.Theaveragenumberof

14 / Annual Report 2009

UBank Ltd.

employeesintheChiefAccountantdivisionin2009amountedto18(in2008-17).

Inaddition,internalauditservicesrelyforthemostpartontheinternalauditingsystemofFIBI.Foradditional information see the section that deals with disclosure with regard to the Bank’s internal auditor.

Inrespectofinformationsystemsservices,seedetailsinthesectionthatdealswithinformationSystems.

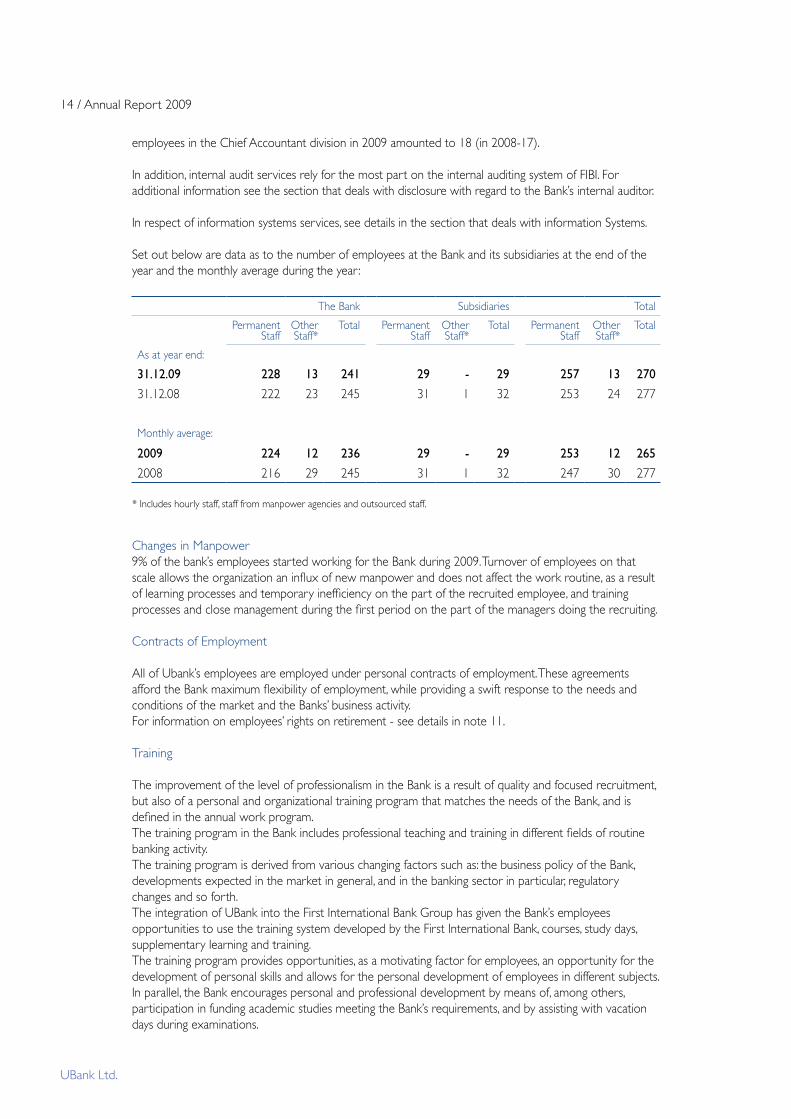

Set out below are data as to the number of employees at the Bank and its subsidiaries at the end of the yearandthemonthlyaverageduringtheyear :

The Bank Subsidiaries Total

PermanentStaff

OtherStaff*

Total PermanentStaff

OtherStaff*

Total PermanentStaff

OtherStaff*

Total

Asatyearend:

31.12.09 228 13 241 29 - 29 257 13 270

31.12.08 222 23 245 31 1 32 253 24 277

Monthlyaverage:

2009 224 12 236 29 - 29 253 12 265

2008 216 29 245 31 1 32 247 30 277

*Includeshourlystaff,stafffrommanpoweragenciesandoutsourcedstaff.

Changes in Manpower9% of the bank’s employees started working for the Bank during 2009. Turnover of employees on that scaleallowstheorganizationaninfluxofnewmanpoweranddoesnotaffecttheworkroutine,asaresultoflearningprocessesandtemporaryinefficiencyonthepartoftherecruitedemployee,andtrainingprocessesandclosemanagementduringthefirstperiodonthepartofthemanagersdoingtherecruiting.

Contracts of Employment

All of Ubank’s employees are employed under personal contracts of employment. These agreements affordtheBankmaximumflexibilityofemployment,whileprovidingaswiftresponsetotheneedsandconditions of the market and the Banks’ business activity.For information on employees’ rights on retirement - see details in note 11.

Training

TheimprovementofthelevelofprofessionalismintheBankisaresultofqualityandfocusedrecruitment,butalsoofapersonalandorganizationaltrainingprogramthatmatchestheneedsoftheBank,andisdefinedintheannualworkprogram.ThetrainingprogramintheBankincludesprofessionalteachingandtrainingindifferentfieldsofroutinebanking activity.Thetrainingprogramisderivedfromvariouschangingfactorssuchas:thebusinesspolicyoftheBank,developmentsexpectedinthemarketingeneral,andinthebankingsectorinparticular,regulatorychanges and so forth.The integration of UBank into the First International Bank Group has given the Bank’s employees opportunitiestousethetrainingsystemdevelopedbytheFirstInternationalBank,courses,studydays,supplementary learning and training.Thetrainingprogramprovidesopportunities,asamotivatingfactorforemployees,anopportunityforthedevelopment of personal skills and allows for the personal development of employees in different subjects. Inparallel,theBankencouragespersonalandprofessionaldevelopmentbymeansof,amongothers,participationinfundingacademicstudiesmeetingtheBank’srequirements,andbyassistingwithvacationdays during examinations.

The Board of Directors’ Report 2009 / 15

UBank Ltd.

Remuneration programs for employees

InaccordancewiththedirectivesoftheSupervisorofBanksfromApril2009,theBoardofDirectorsoftheBankdiscussedremunerationpolicyandthemethodologyforitsimplementation,withtheaimoffindingabalancebetweenthedesiretoencouragemotivation,creatingidentificationoflong-terminterestsamongthemanagerswiththeBank,retainingandrewardingmanagersandthedesireforachievement,togetherwiththeneedtopreventexaggeratedrisk-taking.The policy relates to all Bank employees and is a part of Group policy that was put together with the participationoftheparentcompany,inaccordancewiththedirectiveoftheSupervisorofBanks.ThepolicyisstillinthefinalstagesofformulationandawaitstheapprovaloftheBankofIsrael.

Code of Ethics

During2009thewritingoftheBank’sCodeofEthicswascompleted,withtheaimofpromotingethicsand social responsibility and incorporating appropriate norms of behavior among the Bank’s employees and its managers.The writing of the Code of Ethics was done with the participation of the Banks’ employees. Ethics institutionswerecreatedandactivitieswerecarriedouttoincorporatetheCodeofEthics,including:lectures directed to all employees and the distribution of the Code of Ethics brochure to each and every employee individually.

Restrictions and Supervision of the Bank’s Activities

InProperConductofBankingBusinessRegulation313-“LimitationsontheIndebtednessofaBorrowerandaGroupofBorrowers”,therearerestrictions,accordingtowhichtheBankisnotallowedtoextendcredittoa“singleborrower”,toa“groupofborrowers”andtothe“sixlargestborrowersincludinggroupsofborrowers”(asdefinedintheRegulation)inamountsthatexceed15%,30%and135%ofitsshareholders’equity,respectively.The Bank reached an agreement with certain borrowers and certain groups of borrowers in respect of thesaidRegulation,thattheircreditfacilitieswillonlybeexercisedifthatdoesnotresultintheexceedingof the restrictions that are described above.

InProperConductofBankingBusinessRegulation337-“ActivityontheFutureContractsandOptions(MAOF)Market”therearerestrictions,accordingtowhichthetotalamountoftheliabilitiesofabankinginstitutionvis-à-vistheMAOFclearingsystem(afteralloweddeductions)shallnotexceed30%oftheBank’s equity. In light of the high volume of activities of the customers of the capital market segment on theMAOFmarket,theBankexaminesthesaidrestrictiononacurrentbasis.

InProperConductofBankingBusinessRegulation315-“SupplementaryProvisionforDoubtfulDebts”,itis stipulated that an additional provision for doubtful debts is to be made in respect of the concentration ofdebtinsectors.TheBankisexposedtosuchconcentrationinthefinancialservicessector.Thisconcentration follows the business policy of the Bank according to which the capital market customers segment is among the main segments of activity.The Bank is meticulous in implementing the restriction. In 2008 and 2009 no exception occurred to the sector concentration limit.

Inaddition,seedetailsonthesubjectofthereforminthecapitalmarket,inthechapterthatdealswithoperational segments with reference to the activity of UBank Mutual Funds.

Otherthanwhatisdescribedabove,therearenootherrestrictionsandsupervisionthatarespecificorrelatingtotheBankintheperiodunderrevieworwhichareexpectedtohaveasignificanteffectontheactivities of the Bank in the future.

16 / Annual Report 2009

UBank Ltd.

SignificantAgreements

a.Agreementforthetransferoffactoringoperations:

OnJanuary25,2007anagreementwassignedbetweentheBankandOtsarHahayalBankLtd.(hereinafterreferredtoas“OtsarHahayal”)(fullyownedbyacontrollingshareholderoftheBank)forthetransferoftheBank’soperationsintheareaoffactoringservicestoOtsarHahayal,includingtransferringthe expertise acquired by Ubank in the sphere.Pursuanttotheagreement,fromFebruary1,2007UbankwillceasegivingitscustomersfactoringservicesinnewtransactionsandwillrefersuchcustomerstoOtsarHahayal(hereinafterreferredtoas“theexistingcustomers”)toobtainservices.Furthermore,theBankshallbeentitledtoreferOtsarHahayalnewcustomerswhowishtoreceivefactoringservicesfromitinthefuture(hereinafterreferredtoas“thenewcustomers”).Inreturnforthetransferoftheaboveactivity,TheBankisentitledtoannualpaymentsderivingfromtheprofitsofOtzarHachayalfromfactoringactivityofexistingcustomersandnewcustomers,afteroffsettingprovisionsfordoubtfuldebtsinrespectofexistingclientsuptothetotaloftheprofits,allinaccordancewithdefinitionsandformulasforcalculationdeterminedintheagreement.Theperiodoftheagreementisfixedforeightyears.Sinceitcameintoeffect,itsinfluenceontheresultsoftheBank’sactivityhasnotbeenmaterial.

b. Computer services agreement

For detailed information see a chapter regarding the information system.

c.Seeadditionalrelevantinformationinthefollowingnotestothefinancialstatements:

-WithregardtoagreementsrelatingtothechangeofcontrolintheBank-seenote16(E).-WithregardtotheBank’sliabilitiestotheMAOFclearinghouse-seenotes15(C)(2)and15(C)(3).-WithregardtotheBank’sliabilitiestotheStockExchangeclearinghouse-seenote15(C)(4).-WithregardtothecollateralagreementwithEuroclear-seenote15(C)(5).-Withregardtotheindemnificationofofficeholders-seenote15(C)(8).-WithregardtothecommitmentsbetweentheBankandFIBI-seenote15(C)(10).-Withregardtopledges-seenote15(D).-Withregardtotheextensionoftherentalofbuildings-seenote15(c)(11).

Information Systems

a.Computerization:

AspartoftheFIBIGroup,stepsaretakingplacetotakeadvantage,invariousareas,oftheGroup’ssize.OneoftheareasisintegratingUbank’scomputersystemwiththeGroup’ssystems,whilepreservingtherelative advantage of the Bank.

Withinthisframework,thetwobanks’computerinfrastructureswereamalgamatedandthecomputersystems supporting the various applications were converted. The responsibility for data security was transferredtoMataf(“Operational&FinancialComputerization”-asubsidiaryofFIBI).Most of the process of amalgamating applications in the framework of which the computer applications of UBankandFirstInternationalBankLtd.wereunified,wascompletedby31.12.08andasat1.1.09thebankworks with FIBI’s computer infrastructures.

Thenewcomputersystemsintegratespecial-purposesystemstogetherwiththebranchsystem,suchas:themutualfundoperatingsystem,thetrusteeshipmanagementsystem,systemssupportingdealingroomactivities,thefinancialriskmanagementsystemandsoon.

The Board of Directors’ Report 2009 / 17

UBank Ltd.

Duringthemigrationofsystemstothenewcomputerapplications,problemsaroseinanumberofareas,which necessitated concentration of inputs and investment of resources. These matters were dealt with by the Bank in cooperation with Mataf and with the help of other external suppliers.The Bank has made preparations to deal with completing adaptations required to the needs of users and customers,Specialemphasishasbeenplacedontheimplementationofcontrolsforpurposesoffinancialreportingandforthemanagementofexposuresandrisks.However,theBankisawarethatmanagementandfinancialreportsareproducedonthebasisofnewcomputersystemsinwhichworkprocessaretakingplaceforthefirsttimeinUBankin2009.Boththesystems,andthewayinwhichtheyareoperated,arebasedonthatexistingintheFIBIGroup,whichisfollowinguptheprocessfromthebeginninguntilthecompletion of its integration.For purposes of the Board of Directors’ and Management’s signature on the Report on Internal Control overFinancialReportingforthe2009financialstatements,theBankperformedafullmappingoutofthecontrolenvironmentoverfinancialreporting,whiletestingforoperationaleffectivenesstowardstheendoftheyear.Duringthepreparationofthefinancialstatements,theBankverifiedthatkeycontrolsinfinancialreporting processes are carried out also at present.

TheBankexamineseveryimprovementrequiredinthevarioussystems,bothforoperatingandcontrolling business activity and in the areas of online banking in order to make it easier for customers. In this framework substantial improvements and changes have been integrated in 2009 in a number of applications,andtheBankhasdefinedandcharacterizedadditionalrequirementswhichareinadvancedstages of treatment.

InaccordancewiththeprinciplesoftheundertakingbetweentheBankandMataf,Matafborethecostsofthe process of unifying applications between the banks.TheBankpaysMatafforongoingcomputingservicesthesameamountofcomputercosts(includingdepreciation)thattheBankhadin2005and,inaddition,itbearsitsshareindevelopmentofregulatoryandGroupapplicationsaswillbeagreedupon,withtheadditionofanagreedincrease.Recently,anewmodeloftheundertakingthatwillbeginin2010wasapproved,whichisbasedontherelative share of the Bank in all computer activities carried out in the FIBI Group.

Mr.AmnonBeck,Mataf ’sCEO,servesasmanagerofinformationtechnologiesoftheBankasof18.5.08.

b.ProvidingofComputerServices:

As a separate matter from the question of the systems themselves and as part of the strategy of the FIBI Group,computerservices,includingoperationsandprogramming,areprovidedbymeansofthesubsidiarycompany - Mataf.The services are provided directly by the staff of Mataf.Aspartofthisstrategy,theemployeesoftheBank’scomputerdepartmentbecameemployeesofMatafin2005.Asaresult,alloftheBank’scomputerservices,includingoperationalservicesandprogrammingservices,are provided to the Bank by the Mataf company.

18 / Annual Report 2009

UBank Ltd.

Legal Proceedings

Setoutbelowaredetailsoffiveactionsformaterialamounts,exceeding1%oftheBank’sequity,againstthe Bank and its consolidated companies.IntheviewofManagement,basedonlegalopinions,appropriateprovisionshavebeenmadeinthefinancialstatements,ifrequired,tocoveranydamageresultingfromthesaidactions.IntheBank’sview,basedontheopinionofitslegaladvisers(andintheviewofconsolidatedcompaniesbasedontheirlegaladvisers’opinion),theprobabilityofariskexposureoccurringtotheBankislow,inallfiveactionsspecifiedbelow:

1.OnJuly25,2002anactionwasbroughtintheTelAvivDistrictCourtagainstacompanywhichsharesweretradedinthestockexchange(”thecompany”),UBankTrustCo.Ltd.-awhollyownedsubsidiaryoftheBank(“TrustCompany”),PoalimCapitalMarkets&InvestmentsLtd.,directorsofthecompany,itscontrollingshareholders,theparentofthecompany,andtheaccountantswhoauditedthecompanyaccounts.ThetotaldamageallegedbythePlaintiffisapprox.NIS32,000(ThequotedamountofthesuitisNIS36.7million).TogetherwiththeactionanapplicationwasfiledinCourttorecogniseitasaclassactiononbehalfofalltheholdersofthedebenturesthatthecompanyissued,inanestimatedamountofapprox.NIS 34.2 million.

After several delays in proceedings in the class action caused by the need to complete the process of liquidatingthecompany,theTrustCompanysubmittedaresponsetothepetitionforapprovaloftheclaimas a class action.Theevidenceinthecasewasheard,andwearewaitingforahearingonthecaseandthesummingup.IntheopinionoftheTrustCompanyanditslegaladvisors,theTrustCompanyhasvalidclaims,bothagainstthesuitbeingadmissibletobejudgedasaclassaction,andalsoonthematterofthelaw-suitagainsttheTrust Company.

2.OnJuly27,2003twocustomersbroughtaclaimintheTelAvivDistrictCourtfortheawardofdeclaratory judgment to the effect that one of the customers does not owe the Bank money and that the pledgeofsharesofaStockExchangelistedcompanythatservesascollateralforbothcustomers’debts,whichtheBankisseekingtorealize,isinvalid.Thevalueofthedisputeaccordingtothestatementofclaimamounts to approx NIS 25.6 million. The claim is at the pre-trial stage.

3.OnDecember22,2005aclaimwasbroughtintheTelAvivDistrictCourtagainstUBankTrustCo.Ltd.(“theCompany”)whichwascorrectedtoapprox.NIS30.6milliononSeptember15,2009bythreePlaintiffs,whicharerelatedcompanies.ThePlaintiffshelddebenturesforwhichtheCompanyservedastrustee.Becauseoffinancialdifficultiestheissuerofthedebenturesdidnotdischargeitsdebtstothedebenture holders. The company has submitted an amended defense plea.IntheopinionoftheTrustCompanyanditslegaladvisors,theCompanyhasagooddefenseagainstthelawsuit.

4.InOctober2006,judgmentwasgivenbytheJerusalemDistrictCourt,accordingtowhichthecounterclaimsubmittedbyacustomeroftheBank,foradeclaratoryjudgmentthathislossesintheamountofNIS10.1millionresultedfromtheBank’serrorsandnegligence,wasdismissed.ThecustomerfiledanappealagainsttheverdictwiththeSupremeCourt.

5.On18.03.09,alawsuitwassubmittedtotheTel-AvivDistrictCourtinTel-AvivagainsttheBankbyacustomer in the sum of NIS 7.6 million. It was claimed that the Bank was negligent in honoring checks amounting to NIS 5.0 million. The checks were forged by an employee of the customer; the Bank has submitted a defense plea and a third party declaration against the employee.

The Board of Directors’ Report 2009 / 19

UBank Ltd.

General Environment and Influence of External Factors on the Bank’s Activity

Economic Developments in 2009

2009 ended in a positive trend of development in the Israeli economy and the worldwide economy. The globaleconomiccrisis,thatbegandevelopinginthesecondhalfof2007uptothethirdquarterof2008,ledtoadeeprecessionthathasbeenmuchshorterthanearlierexpectations:inthelastquarterof2008andthefirsthalfof2009.Beginninginthethirdquarteroftheyearthereweresignsofrecoveryfromtheglobalrecession.IntheIsraelieconomy,greenshootsoftherecoverywereseenearlier-fromthesecondquarterof2009.Ifinthefirstmonthsof2009theestimatewasfornegativegrowthinIsraelofabout1.5%,theestimateattheendoftheyearforgrowthinGDPfor2009isapositiverateof0.5%.Allinall,the Israeli economy has suffered less than other countries from the global crisis - the global rate of growth in2009is(0.8%)andindevelopedcountries(3.2%).In2010,accordingtotheforecastoftheInternationalMonetaryFund,worldwidegrowthshouldreach3.9%,indevelopedcountries-2.1%,andintheU.S.A-2.7%.TheInternationalMonetaryFundestimateforIsraelisforgrowthof2.5%,buttheBankofIsraelexpectsamorerapidgrowthof3.5%.

Economicanalysesindicatetheunorthodoxmacro-economicinterventioninthemonetary,physicalandfinancialfieldsasthereasonfortherelativelyrapidglobaleconomicimprovementinthestateoftheeconomy.Againstthisbackground,thereisuncertaintyregardingcontinuationinthetrendofendingtheeconomiccrisis,duetothefactthatpolicymakersaredeclaringtheirintentionofendingtheirpolicyofmacro-economicsupport.Moreover,interventionbygovernmentshascreatedadifficultfiscalsituationwitharealpotentialforfinancialcrisisinseveralcountries.InGreece,PortugalandSpain,theratingandratingforecasthavebeendecreased,outofconcernoverdebtrepaymentability.Fiscalincentivesandtheever-growingburdenofdeficitfunding,haveincreasedgovernmentdebtstremendouslyandreachedall-timerecords.Alloftheabove,anduncertaintyregardingthedegreeofstabilityofmanyfinancialinstitutionsworldwide,castacloudoverthetrendofrecoverythatasstatedhasclearlybeenobservedand is still continuing since the second half of 2009.

TheendingoftherecessionintheIsraelieconomy,thatasmentionedstartedearlier,seemsmuchmoreestablishedandlessfragilecomparedtoworldwidetrends,eventhoughglobaltrendshaveasignificanteffectonIsrael.ThefiscalsituationinIsraelisalsomuchbetterthanintherestoftheworld.Thebudgetdeficithasgrownmuchmoremoderately,andthedebt-to-GDPratiomaintaineditsstability.TrendsinIsraeli capital market have been much more positive compared to those in global capital markets. Trends in the labor market are much more positive - the increase in the unemployment rate has been much more moderateandeversincethethirdquarterof2009isindecline,comparedtoaworldwideincrease.

The estimate of growth in GDP in Israel for 2009 was as mentioned 0.5%. In the second half of the year,itreached2.9%inannualtermsand,inthelastquarteroftheyear,morethan4.0%.Productionofthebusinesssectordecreasedin2009by0.4%.Mostprominentisthedecreaseinexports,excludingdiamonds,of10.8%.Imports,excludingdefenseimportsanddiamondsalsorecordedasignificantdecreaseof13.4%.Privateconsumptionincreasedby1.1%,whichmeansadecreaseinconsumptionpercapita(thestandardofliving)of0.6%.Excludingtheeffectofprivatevehicles,theincreaseinprivateconsumptionis2.1%,andwithoutadecreaseinconsumptionpercapita.Investmentinfixedassetsexcludingshipsandaircraft dropped by 6.6% and public consumption excluding defense imports grew by 2.5%. The trend of recoverystartinginthesecondquarteroftheyearbeganwithprivateconsumption,butfromthethirdquarteroftheyear,therealsowasanincreaseinexportsandinvestments,andtherateofgrowthofimports also accelerated.

Therateofunemployment,followingtheeconomiccrisis,increasedin2009andreached7.7%oftheworkforce,afterreachingarelativelylowratein2008of6.1%.Duringthesecondhalfof2009,adecreasein the unemployment rate began and the assessment is that in 2010 it will reach 7.0% of the work force. Thedeficitinthegovernmentbudgethasalsorisenfollowingthecrisis,anditseffectonrevenuesfromtaxes,andreached5.15%ofGDP.Thatisalowerratethanthebudgetestimatefor2009thatforecastadeficitof6.0%ofGDP.In2010,afurtherdecreaseinthedeficitisexpected,ofupto4.0%ofGDP.Thedebt-to-GDPratiohasremainedmoreorlessstable,andhasnotexceededthelevelof80%,despitethe

20 / Annual Report 2009

UBank Ltd.

increaseinthedeficitandtheneedtofinanceitbyraisingfundsfromthepublic.Thisisduetotheeffectof the increase in prices of production and the strengthening of the shekel last year. The current account surplusinthebalanceofpaymentsincreasedsignificantlyin2009andreached$7.2billioncomparedwith$2.1billionin2008.Themainfactorintheincreaseinthesurplusisthesharpdecreaseincommodityprices,especiallyfuelprices,incomparisonwiththeaveragesof2009and2008.Inaddition,asmentioned,the decline in imports has been stronger in comparison with the decrease in exports of commodities and services.Theexpectationisthatrecoveryineconomicactivity,togetherwitharapidincreaseinimportsincomparisonwiththeincreaseinexports,willreducethecurrentaccountsurplusto$3.0-3.5billionin2010,andthathassignificantconsequencesonthestrengtheningorweakeningoftheshekelintheyeartocome.

InflationinIsraelduring2009reached3.9%,similartotheinflationratein2008of3.8%.Incomparisonwithdevelopedcountries,whereinflationduringthelastyearwasclosetozero,thatisconsideredahighrateofinflation,butincomparisonwithemerginganddevelopingcountries,whereitreached5.2%,itisarelativelylowinflationrate.Itexceedsthetargetrangeforinflationandhasbeenaffectedthisyearbypriceincreasesthatresultedfrominvolvementbygovernment-V.A.T,watertariffs,cigarettes,andtaxonfuel.Afterdeductingthesepriceincreases,inflationreached2.8%,slightlylowerthanthetopendoftheinflationtarget.Housingandenergyitemshadthemosteffectontheincreaseinpriceslastyear.Itshouldbementionedthattheincreaseinpricesofhousingofhome-owners,whichisnotpartofhousingpricesmeasuredintheConsumerPriceIndex,amountedtoabout18%fromthebeginningoftheyear.Themostprominentincreaseinhousingpriceswasaffectedbythesharpdecreaseintheinterestrate,resultinginadecreaseinthecostofmortgages.Thepublictendedtoshifttowardsinvestmentinrealestate,againstabackdropofalackofattractiveinvestmentalternatives.Atthesametime,thedecreaseintheinterestratehadnoaffectonthegrowthofthehousingsupply,wherestartsandcompletionsofresidentialconstructionreflectedadeclineaswellasthenumberofhousesforsale.In2010,adecreaseisexpectedininflationtoreachtheinflationtargetrangeof1%-3%,withthefactorsthataccelerateditin2009notexpectedtocontinuehavinganeffectin2010.Duringthefirstthirdoftheyear,theBankofIsraelinterestratewasinanunprecedenteddownwardtrend,reaching0.5%,withthepurposeofmoderatingtheeffectofthedeepglobalcrisisonthefinancialandnon-bankingmarketsinIsrael,againstthebackdropof weakness in overseas markets and the enhanced risks of heavy recession. Similar action was taken by central banks around the world. With the accumulation of indicators pointing to a continuous and significantrecovery,theinterestratebegantoclimbagainstartingfromSeptember2009.Thepaceoftheincreaseintheinterestrateisslowandprecedesincreasesininterestratesaroundtheworld,whichareexpectedtobeginonlyinthemiddleof2010,withtheestablishingofthetrendforendingtherecession,whichisatthisstage,asmentioned,notyetcertain.UntilFebruary2010theinterestrateincreasedbyonly1.25%,reflectingastillconsiderablerealnegativeinterestrateofabout2.5%.Towards2010,apositiveinterest-rate gap began to develop again between Israel and the rest of the world when comparing central bankinterestrates.However,thepositivegaponlong-termbondsisonadecreasingtrend.Theendingofthe crisis for the economy should bring about the continuation of adjustment of the interest rate to the ongoingestablishmentofthenewdomesticeconomicenvironment.Despitethat,thepaceofadjustmentdepends on developments in the global economic environment that do not match developments in the Israelieconomy.Undercurrenttrends,itisverylikelythatthisprocesswillnotbecompletedduring2010.

The management of monetary policy of close to two years by the Bank of Israel is not only executed throughinterestratedecisions,butalsothroughinterventionbytheBankofIsraelintheforeignexchangemarket. The increasing current account surplus in the balance of payments and positive capital movements intotheeconomy,reflectamongothersthegapinthedepthoftheeconomiccrisisbetweenIsraelandtherestoftheworld(intheworldthecrisisisrelativelydeeper).ThissituationledtheBankofIsraeltointerveneintheforeignexchangemarketandpurchasedollarsinconsiderableamounts,inordertoprevent excessive strengthening of the shekel that could seriously harm the export sector and deepen therecession.During2009,theshekelstrengthenedagainstthedollaratanaggregaterateof2.1%.Thesetrends,perhapswithalowerintensity,areexpectedtocontinueduring2010,againstthebackgroundofthe expectation of a current account surplus and positive capital movements in the coming year also. To that should be added the positive interest rate gap that has increased during recent months and should continue to rise also in 2010. The strengthening trend of the shekel is one of the factors that are supposed tostabilizeinflationin2010withintheinflationtargetrange,eventhoughthelevelofinterestrateswillcontinuetoberelativelylow,andmaypushinflationupwards.

The Board of Directors’ Report 2009 / 21

UBank Ltd.

2009 marked the ending of the crisis affecting capital markets in Israel and around the world. After the sharpdecreaseinthemarketsinthelastquarterof2008,thefearofcollapseoftheworldeconomydeclined and negative trends became more moderate. Price increases in 2009 were a natural reaction to the sharp decreases at the peak of the crisis.TheTel-Aviv25indexincreasedbyapprox.75%in2009,andattheendoftheyearreachedalevelhigherthan on the eve of the crisis in September 2008. The index increased by close to 95% from the low point of November 2008. Increases focused on stocks included in sectors that had been eroded due to negative developmentsinthesesectorsoverseas-banking,insuranceandrealestate.Aprominentincreaseofapprox.150%wasregisteredintheTel-Aviv75index,causedbyajumpintheprices of several stocks connected to drilling for gas along the coast of Israel.Sharpincreaseshavecharacterizedmoststockindices,amongthemtheYeter50andRealEstate15,thathavemorethandoubled,andtheTel-Tek15indexthatincreasedbyapprox.85%.Theseindicesstoodoutin 2008 with sharp decreases of approx. 65%-80%.

Instockmarketsabroad,despitetheproblematicstarttotheyear,stocksoftheS&P500ended2009withthebestreturnsince2003,23.5%,ofwhich,sincethelowpointinMarch,theindexaddedabout67%to its value. The Dow-Jones increased this year by 18.9% and the NASDAQ index increased by 43.9%. Europealsoregisteredincreases:theFrenchCAC-40indexincreasedby22.3%andtheGermanDAXindexby23.9%.InJapan,theNikkeiindexincreasedby19%andinHonk-KongtheHang-Sengindexjumped by 52%.

Thebondmarketin2009wascharacterizedbypriceincreasesinallbondtypes.Incorporatebondslinkedtotheindex,anaverageincreaseofcloseto40%wasrecordedthisyear.Theincreaseinpricesofcorporate bonds this year follows their erosion by approx. 20% in September-December 2008. The Tel-Bond20indexincreasedbycloseto22%andtheTel-Bond40index,ofwhichmanyofthebondsincludedinitareconnectedtotherealestatesector,increasedbytwicethatrate,closeto44%,sincethebeginningoftheyear,followingadecreaseofabout33%duringthelastfourmonthsof2008.Governmentbondprices,whichwerenotaffectedbythecrisis,recordedanincreasethisyearofuptoapprox.10%,whereasnon-linkedbonds,Shahar,increasedbyonlyapprox.afteranincreaseofcloseto12.5% in the previous year.

Updates in Legislation and Rulings affecting the Banking System in 2009

Overthelastyear,therewerechangesandinitiativesforchangesinlegislation,togetherwithchangesinregulations,whichhaveimplicationsonthebankingsystemandontheBank,assetoutbelow:

JointInvestmentTrustLaw(AmendmentNo.14),2009The draft law was published on 16.2.10.The main amendment is a change to section 69 in the Joint Investment Trust Law.Themainchangesareasfollows:anobligationwasimposedonthefundmanagertoholdatenderforbrokeragecommissionswitha“tradingcompany”(amemberoftheStockExchange);theBoardofDirectorsofthefundmanagermustfixaprocedureforholdingatenderwhichwillbeapprovedbythetrustee; entering an undertaking with a stock exchange member overseas can be made without a tender (withinthetermsofthelaw);anundertakingbyafundmanagerunderabrokerageagreementwithastock exchange member controlling the fund manager or the trustee of the fund can be made without a tendersubjecttothefollowingconditions:1. The stock exchange member must meet the minimum conditions that were set out in the tender.2. The commission for any kind of a deal will not exceed the commission that the winner of the

tender will be paid for a similar deal.3. The undertaking was approved by the Audit Committee and the Board of Directors of the fund

manager.The fund manager will not make payments from the fund’s assets to stock exchange members related to thefundmanagerortrustee,foraperiodof12monthscommencingonthedatedecidedbythefundmanagerintheprospectus,fortheexecutionoftransactionsinthetrust’sassets,inanamountexceeding20%ofallcommissions(ofalltypes)thatwerepaidfromthefund’sassetsinthatyear.

22 / Annual Report 2009

UBank Ltd.

The amendment will come into effect 12 months after publication of the amendment to the law.It should be mentioned that the amendment to the law replaces the same sections in the proposed Joint InvestmentTrustLaw(AmendmentNo.13),2008,whichdealwiththerequirementforatenderandrestrictions on payments of brokerage commissions to a company related to a fund manager or a trustee.

TheamendmentshouldhaveasignificanteffectonthebusinessoftheBankandtheresultsofitsactivities,becausetheBankhassignificantactivitybothasabankerandasatrusteeformutualfundsthroughitssubsidiarycompanyUBankTrustCompanyLtd.,whichmaybringabouttheneedforsignificantreductionin one of these activities.AsofthedateofapprovaloftheseFinancialStatements,nodecisionhasyetbeenmadebytheBank,regarding the manner of preparation for the implications of the above-mentioned legislation.

RegulationofEngagementinInvestmentAdvice,InvestmentMarketingandInvestmentPortfolioManagementLaw(AmendmentNo.13),2008TheamendmentwaspublishedintheOfficialGazette(Reshumot)on16.2.10,andwillcomeintoeffectsixty days after its publication.Theproposedamendmentdealswiththefollowingsubjects,amongothers:Settingupanarrangementwherebyforeignersthathavebeenauthorizedintheirowncountriestoengageininvestmentadvice,investmentmarketingandportfoliomanagement,willbeallowedtooffertheirservicesinIsraelwithouttheneedofanappropriateIsraelilicense,onconditionthattheserviceswillbegivenwithintheframeworkofanauthorizedIsraelicorporation.Theauthorizedcorporationwill be made responsible and be given the duty of supervision with regard to the activity of the foreign traderinitsframework.Amongthethresholdconditionsforanundertakingbetweentheauthorizedcorporationandtheforeigntrader:anundertakingagreement,theforeigntradermustholdalicensefromhiscountryoforigintoengageinthesameserviceandtheauthorizedcorporationmustbeauthorizedon its own merit to provide the same services to which the undertaking agreement applies - regulations areproposed(detailedasfollowsfortheregulationoftherequestforregistration);thegrantingofanexemptionfromthelicensetomanageportfoliosforsophisticatedcustomers(henceforth:“qualifiedcustomers”)andtheaddingofcustomerswithlargeassetportfoliosandcustomerswithsignificantexperience in the capital market activity or relevant expertise for activity in this market to the list of customersforwhichthereisanexemptionfromowningalicenseforadvising,investmentmarketingand,asproposed,alsoinvestmentportfoliomanagement,duetotheirbeingqualifiedtopurchaseprofessionalassistance with their own money in order to make investment decisions by themselves or because of theirskillinthecapitalmarket,andasaresult,donotrequiretheprotectionofthelawinherentintherequirement for a license; the granting of authority to the Israel Securities Authority to make use of outsourcing for purposes of supervision of license-holders; increasing activities permitted for a portfolio managementcompany,includingpensioncounseling/marketingandothersubjects.

Israel Securities Authority Circular - Principles of measurement of the Bank’s earnings from investment advisory activities and the remuneration of investment advisorsOn15.2.09,theISApublishedacirculartobankingcorporationsconcerningthemethodofmeasuringtheBank’s earnings from investment advisory activities and the remuneration of investment advisors.TheaimofthecircularwastoprovideabalancebetweenaconflictofinterestthatmightbecreatedbetweenthebenefitoftheBankandthepersonalbenefitoftheinvestmentadvisor,andthebenefitofthecustomers,andtheconcernofabreachoffiduciarydutyandtheexerciseofcautionsetoutinthelaw:1. When use is made of measuring or compensatory mechanisms based on the contribution

toprofitabilityoftheunitorthebranch,actionshouldbetakentoreducethepotentialforconflictofinterestsbydilutingtheeffectoftheparameterofprofitabilityonmeasurementandcompensation,anddilutingtheeffectoftheindividualadvisorontheprofitsoftheunit.

2. An investment advisor should not be compensated directly or indirectly for the Bank’s income from his investment advisory activity.

3. Personal measurement of investment advisors is permitted only on the basis of qualitative parameters,asmuchaspossible,whicharesegregatedfromtheBank’sprofitsfrominvestmentadvisory activity which they performed.

The Board of Directors’ Report 2009 / 23

UBank Ltd.

Circular of the Supervisor of Banks concerning environmental risks to banking corporationsOnJune11,2009,theSupervisorofBanksissuedadirectiveconcerningenvironmentalriskstobankingcorporation(henceforth:“thedirective”).Bankingcorporationswillberequiredtoincorporateintherangeofcreditconsiderationstheidentificationandassessmentofenvironmentalrisk,andtotakestepsto assimilate the management of exposure to environmental risk in the range of risks of the banking corporation. Implementation of the circular will be in accordance with criteria and timetables to be approvedbytheboardofdirectorsofthebankingcorporation,by30.6.2010,whileforpurposesofimplementation it will be possible to draw on accepted principles and international standards on the subjectofenvironmentalriskmanagement,withthoseadjustmentsnecessarytotheenvironmentinIsrael.

Reform in the area of banking commissionsAnumberofprivatemembers’billsaretabledintheKnessetconcerningrestrictionsonthelevelofcommissions,basketsofcommissions,theprohibitiononchargingtypesofpopulationswithcertaincommissions,theprohibitionofchargingcertaintypesofcommissionsandsoon.Inaddition,thereareprivatemember’sbillstabledintheKnessetseekingtomakebankingcorporationspayinterestoncurrentaccount balances of their customers. The Bank is monitoring developments in the legislative process of thoseproposals,whicharestillinthepreliminarystagesoflegislation.

PowersoftheSecuritiesAuthorityLaw(AmendmentstoLegislation),2008The Law was passed in the plenum of the Authority on 14.12.08.Themainchangesproposedare:unifyingtherulesbywhichtheTASEoperates,whicharenowinthreebodiesoflaws-theConstitution,InstructionsandTemporaryInstructions,intoasingleinclusivevolumetobecalled“Instructions”,andthatdecidingonInstructionsandmakingamendmentstoitwillbeperformedbywayofapprovinganadministrativedirective,afterthereceiptoftheapprovaloftheTASEBoardofDirectorsfortherulingorfortheamendment,whicheveristhecase;empoweringtheAuthoritytoregularize,byadministrativedirectives,mostofthemattersgovernedatpresentbyregulations,inthoseareas over which it has jurisdiction; and deciding that the plenum of the Authority will be the body to give approval to administrative directives proposed by the staff of the Authority. The plenum will be responsible forimposingsanctionsonthoseunderthesupervisionoftheAuthority,includingdecisionsregardingtheimpositionofmonetarysanctionsandcivilfines,anditisproposedtogiveauthoritytothepowersoftheAuthority by pre-ruling.

AmendmenttoIncomeTaxOrdinance(AmendmentNo.169andTemporaryOrder),2008The Amendment was passed on 29.12.08. The Amendment grants tax incentives to foreign residents to investinIsrael:anexemptionfromtaxoninterest,discountfeesandlinkagedifferentialsonbondstradedontheStockExchangeinIsrael,andataxexemptiononcapitalgainsforaforeignresidentofacountrythathassignedadoubletaxationavoidanceagreement.Furthermore,acorporationreceivingadividendin the 2009 tax year from a foreign resident corporation will be liable to Companies’ Tax at a rate of 5% insteadof25%,iftheproceedsofthedividendareusedinIsrael.Inaddition,taxbenefitswereextendedfor residents of Sderot and Western Negev settlements.

ExecutionLaw(AmendmentNo.29)On16.5.09,AmendmentNo.29totheExecutionLawcameintoeffect,underwhichthesubjectofalternativehousingisregulated.AccordingtotheAmendment,itwillnotbepossibletomakeconditionsontherightofadebtortoalternativehousing,althoughitispossibletodeterminethatthealternativehousingofferedtothedebtorwillbeunderanarrangementdetailedbelow,providedthatthesignificanceof the matter is explained to the debtor in clear language that he understands. Under the above-mentionedproposal,thevalueofthealternativehousingwillbeofanamountwhichwillenablethedebtor to rent an apartment in the area where he lives which is appropriate to his needs and the needs of hisfamilymemberslivingwithhimforaperiodnotexceeding18months(exceptinspecialcircumstanceswheretheEnforcementOfficeRegistrarcanextendthatperiod).Thevalueofthealternativehousingwill be deemed to be part of the receivership expenses. Regarding pledge or mortgage agreements that wereenteredintobeforetheAmendmentcomesintoforce,theproposedAmendmentdeterminesthatitispossibletomakeconditionalthedebtor’srighttoalternativehousing,exceptifisproventotheEnforcementOfficeRegistrarthatthedebtor’srighttoalternativehousing,andthesignificanceofwaivingit,werenotexplainedtothedebtor.

24 / Annual Report 2009

UBank Ltd.

AmendmenttotheCompaniesLaw,1999-RecordingacompanyasacompanyinviolationTheAmendmentwaspublishedon23.7.09.Asof1.1.2010,ifacompanybreacheditsdutyofpayingafeeand/orotherpaymentsthatitisobligedtopaytotheRegistrarofCompanies,orifacompanybreacheditsdutyofsubmittinganannualreport,theRegistrarofCompaniesinauthorizedtorefusetoregisteralien on the assets of the company in violation.

MemorandumSupplementaryEnforcementbytheIsraelSecuritiesAuthorityLaw(AmendmentstoLegislation),2009The draft law was approved by the Ministerial Committee for Legislative Matters on 6.12.09.TheAmendmentbringsabouttheexistenceofthreeparallelchannelsofenforcement:a. ProceedingsfortheimpositionofamonetarysanctionbytheAuthority,intendedtodealwith

minor violations.b. Administrative enforcement proceedings - allowing the Administrative Enforcement Committee

toimposeaseriesofmeasuresofenforcement,intendedtodealwithviolationstheproofofwhich requires the existence of disciplinary investigation proceedings.

c. Criminal proceedings - which are intended to deal with serious crimes and which only at its conclusion will it be possible to impose punishment by imprisonment; an Administrative Committee will be set up to review the above violation of the laws. The Committee will be authorized,amongotherthings,toimpose:monetarysanctionsofasignificantamount;arequirementtopaycompensationtothosehurtbytheviolation,prohibitionfromservingincertain bodies and suspension of the license.

Drafts and Proposed Legislation

ProposedLawamendingtheIncomeTaxOrdinance(ExemptionfromTaxonInterestandProfitsfromLong-TermSavings),2009Aprivatemember’sbill,tabledintheKnesseton30.11.09.It is proposed to exempt long-term savings plans from tax.

ProposedExecutionLaw(Amendment-DischargeofaBorrowerofLimitedMeans),2009Aprivatemember’sbill,tabledintheKnesseton23.11.09.ItisproposedtoallowthegrantingofadischargetoaborroweroflimitedmeansbytheExecutionOfficeand thus to equate his status with a borrower of limited means who has been declared bankrupt.

ProposedJointInvestmentTrustLaw,1994,(AmendmentNo.13),2008The proposed Law was approved by the Ministerial Committee for Legislative Matters on 28.6.09.Themainamendmentsproposedare:offertothepublicofforeignmutualfunds;increasingthedutiesofsupervision imposed on the trustee and tightening supervision over fund managers; granting authority to the Securities Authority to deny as well as not to grant a company approval to serve as trustee or fund manager for reasons connected with its reliability; prohibiting a company from serving as a trustee in a fundifoneofthefollowingalternativesexist:1. Intheeventthatthecompanyiscontrolledbythefundmanager,apersoncontrollingit,ora

company under the control of any of them with more than 10% of the issued share capital of the company.

2. Thereisabusinessconnectionbetweenthecompany,orapersoncontrollingit,andthefundmanager,oramaterialbusinessconnectionwithapersoncontrollingafundmanageroracorporation under his control.

3. The revenues of the company together with the revenues of a person controlling it and a corporationunderthecontrolofsuchanabove-mentionedperson,whichderivefromabusinessconnectionwiththefundmanagergroup,includingrevenuesfromtrusteeshipforfundsmanagedbythefundmanagergroup,fromtrusteeshipforbondsissuedbyacorporationincludedinthefundmanagergroup,andfromtheprovisionofusualbankingservices,exceed15%ofitsrevenues together with the revenues of a person controlling it and a corporation under the controlofsuchanabove-mentionedperson.Forthismatter,abusinessconnectionisdefinedas-includingsupplier-customerrelationships,serviceproviders/recipients,loanproviders/recipients

The Board of Directors’ Report 2009 / 25

UBank Ltd.

andothers,excludingaconnectionderivingfromtheprovisionofservicestoatrusteeshipforfundsorbonds,andusualbankingservicesduringthecourseoftheusualbusinessofthebank,andonmarkettermsonly,wheretherevenuefromthemdoesnotexceed5%oftherevenuesofthebank;amaterialbusinessconnectionisdefinedas-abusinessconnectionincludingtheprovisionofusualbankingservices,wheretotalrevenuesincludingrevenuesfromallthebusiness connections with the fund manager group exceed 5% of the revenues of the company together with the revenues of a person controlling it and a corporation under the control of such an above-mentioned person.

4. Therearecircumstancesinwhichconflictmaybecreatedbetweenthebenefitofthecompanyor the person controlling it or a corporation under the control of such an above-mentioned person,andthebenefitoftheunitholders:prohibitionofreceiptofbrokerageservicesfromaparty connected with the fund manager or the trustee; a duty to hold a tender for purposes of a commitmentwithabank/memberoftheStockExchangeforthereceiptofbrokerageservices,as well as prohibiting the payment of brokerage commissions or any other payment from fund assetstoacompanyconnectedwiththefundmanagerorthetrustee(whenbodiesconnectedwiththefundmanagerorthetrusteecannotparticipateinsuchatender);aprohibitionofpreferenceofthebenefitofunitholdersinaspecificfundoveranotherfundwhentheyaremanaged by the same fund manager; determining provisions concerning the participation of the fund manager in meetings of public companies whose securities are held by mutual funds; allowing the charging of differential management fees in a fund from different populations of unit holders; changing the format of liquidating a fund and granting authority to the Israel Securities Authoritytoorderthedissolutionofafund.Inaddition,obligingafundmanagertodissolveamutualfundwithalowasset-value;similarly,variousmattersareregulatedintheproposedlawconnectedwiththemannerofmanagementofmutualfunds,chargingofmanagementfees,transferringvitalinformationtounit-holders,liquidatingafund,civilenforcementauthoritiesoftheIsrael Securities Authorities and so on.

IftheAmendmentinitspresentversionwillbecomebindinglegislation,thereisexpectedtobeamaterialeffectonthebusinessofthebankanditsoperatingresults,becausetheBankhassignificantactivitybothasabankerandasatrusteeformutualfundsthroughitssubsidiarycompanyUBankTrustCompanyLtd.,whichmay,ifthelegislativeprocessiscompleted,bringabouttheneedforsignificantreductioninoneofthese activities.AsofthedateofapprovaloftheseFinancialStatements,nodecisionhasyetbeenmadebytheBank,regardingthemannerofpreparationfortheimplicationsoftheabove-mentionedlegislation,ifitisapprovedinitscurrentversion,andregardingwhichactivitieswillbereduced,asmentionedabove.

ProposedJointInvestmentTrustLaw,1994,2009The draft Proposed law was approved in the plenum of the Israel Securities Authority on 15.11.2009 and published for comments by the public by 31.12.2009.Themainamendmentsproposedare:RegulationofExchange-TradedNotes(TeudotSal):1. Activity by exchange-traded notes and issuers of exchange-traded notes will be regulated by

means of the Joint Investment Trust Law and will be subject to supervision by the Authority.2. Exchange-tradednoteswillbedefinedinamannersimilarandcorrespondingtothatofmutual

fundsandissuersofexchange-tradednoteswillbedefinedasexchangetradednotesmanagers(correspondingtofundmanagers).Thesenoteswillchangefromthelegalstructureofa“bond”issuedasasecurityunderprospectus,toalegalstructuresimilarinsubstancetoamutualfundinwhichtherightofacquisitionoftheassetswillbelongtotheinvestors.Inaddition,andunlikeamutualfund,anexchange-tradednotewillincludeanobligationoftheexchange-tradednotesmanagertomakeupthedifference,ifsuchiscreated,betweentheamounttowhichtheholderoftheexchange-tradednoteisentitledonredemption,andtheactualassetvalueoftheexchange-tradednote,Asdistinctfrommutualfunds,theexchange-tradednotesmanagercan“withdraw”moniesfromthearrangementifthevalueoftheassetsishigherthanthevalueoftheliabilities,inaccordancewithamechanismtobedetermined.

3. Theapplicationofnormsapplyingtodaytofundmanagersandfundtrustees,includingthedutyoflicensing,toexchange-tradednotesmanagersandtheirtrustees.Amongthenormsthereare

26 / Annual Report 2009

UBank Ltd.

requirementsonthesubjectofconditionsforqualificationtoserveasafundmanagerandasatrustee,limitsonmarketshare,themannerofmanagementofthefunds,limitsoftheassetswhichit is permitted to hold in a fund and their maximum amounts etc.

RegulationofExchange-TradedFunds(KranotSal):1. A fund whose investment policy is intended to track through replication a market index or other

underlyingasset,canregisteritsunitsfortradingontheTel-AvivStockExchange,andtransactionsinitsunitswillbeallowedduringtradingonly,inasimilarmannertoexchange-tradednotes.

2. Afundmanagerwillbea“marketmaker”forunitsinthefundandwillquotepricesaccordingtorules stipulated in the legislation.

3. Tradingofunitsinthesecondarymarket-Concurrentwiththeactivityofthefundmanager,therewillbeanormal“secondarymarket”forunitsofthefund.

4. Existing tracker funds will be entitled to register for trading and convert themselves into exchange-traded funds.

Additionalchanges:1. Arrangementmanager-Itisproposedthatanarrangementmanager(i.e.afundmanageror

exchange-tradednotesmanager)can,subjecttotherequirementsofstabilitytobedeterminedforeachtypeofarrangement,managealltypesofarrangements.

2. Itisproposedtodeterminethatthetermofserviceofatrusteewillnotbelessthanfiveyears(atpresentthelimitisthreeyears),andanyextensionwillbeforafurtherfiveyears.Inanyinstanceofnon-extensionoftheagreement,thefundmanagerandthetrusteehavetoreportthe reasons for the non-extension of the period of service to the Authority.

3. Change in investment policy - This is possible once every twelve months. It will not be possible tomakeanymaterialchange(achangeininvestmentpolicyofafundwhichaffectsthevolatilityofthepricesofthefundorrequiresachangeinitsclassification),inthefund’sinvestmentpolicy.Exceptional cases will be determined in the regulations when it will nevertheless be permitted to make a material change in an arrangement. It is also proposed to determine that a merger will be allowedonlyregardingfundsinthesameclassification.

ProposedJointInvestmentTrustLaw(TenderforUndertakingwithStockExchangeMember),2009TheproposedlawpasseditssecondreadingintheKnesseton14.3.07.Accordingtotheproposedlaw,theselectionofastockexchangememberbyafundmanagerandenteringintoanundertakingwithhimforpurposesofexecutingtransactionsinsecurities,optionsandfuturescontractsforthefund,willbecarriedoutbymeansofatenderunderrulestobedeterminedbytheMinisterofFinance.Inaddition,itisproposedtoallowafundmanagertoreceiveafullorpartial refund of commission paid by the fund to a stock exchange member for purposes of executing transactionsinsecurities,optionsandfuturescontractsonbehalfofthefund.IntheframeworkofthedebateheldintheKnesseton1.7.09,itwasdecidedthattheproposedlawwouldbejoinedandcombined with Amendment No. 13 to the Joint Investment Trust Law and integrated into it.

ProposedLawamendingtheCompaniesLaw(RecoveryofCompanies),2010The proposed law was published on 6.1.10.The aim of the proposal is to regulate the area of recovery of companies regulated at present under section350oftheCompaniesLaw,1999.Themainpartsoftheproposal:toprovidealegalbasisformeetingsofholdersofdifferenttypesofbonds; to consider the cancellation of a requirement for obtaining a numerical majority in meetings of creditors and shareholders; creating a speedy process for obtaining approval of a compromise or arrangement formulated outside of the Court; granting authority to the Court to extend the period of freezingofproceedingsforspecialreasons;anownerofapropertycannotobtainpossessionintheeventthat the property is needed for the ongoing operation of the company; the debt of the company to the owner of a property is the amount that would be paid to a seller as a condition for transferring ownership not exceeding the value of its sale. The provisions concerning a compromise or an arrangement will apply toacompanyagainstwhomanordertofreezeproceedingshasbeengranted.Providingalegalbasisfortheauthoritytoappointanofficeholderanddetermininghisauthoritiesineveryevent,thepossibilityofusing pledged properties during the normal course of business of the company unless the Court ordered

The Board of Directors’ Report 2009 / 27

UBank Ltd.

otherwise.TheCourtcanobligeaproviderofavitalservicetocontinuesupplyingit,subjecttothereceiptofconsideration.Theauthorityofanofficeholdertoadoptorrejectanexistingcontract,toreceivealoan.TheCourtwillbeauthorizedtoenforceanarrangementoracompromiseonmeetingsoftypesofbondholders who objected to them on condition that the proposal is fair and just in relation to all types of bonds not agreeing to it. The granting of authority to the Court to cancel proceedings if it is convinced that there is no possibility of saving the company.

ProposedSecuritiesLaw,2009The proposed law was updated on 26.11.09.Itisproposedtochangethedefinitions“ownership”,“purchase”,and“interestedparty”sothatadditionalsituationswillbedealtwithforpurposesofexaminingreportingrequirements,inrelationtotransactionsexecuted with an interested party in relation to his holdings in the securities of the corporation. In this manner a mutual fund manager will be considered a holder of securities included in the assets of the fund andunderhismanagement,andatrusteewillbeconsideredaholderofsecuritiesforwhichheservesastrustee,ineverymatterandnotonlyconcerningtheirclassificationasinterestedparties.Apersonwill be considered a holder of securities also in the event that the holding is performed by means of his investment portfolio manager. It is proposed that a creditor be deemed a holder of securities pledged in hisfavorasofthefirsttimehetookstepstorealizethepledgeorthefirsttimehemadeuseofvotingrightsrelatingtothepledgedsecurities,whichevertheearlier.Itisproposedtoamendthedefinitionofa“familymember”toincludealsofamilymemberswhoserelationshiptotheholderderivesfromtheirbeingparentsorsiblingsofthespouseoftheholder(additionofsiblingorparentofthespouse).Itisproposedtonarrowthedefinitionofjointownershiporpurchasesothatthisapparentownershipwillapplyonlyaslong as there in no controlling shareholder in the corporation. It is proposed to add additional apparent ownershiptothedefinition“ownershiporpurchaseofsecuritiestogetherwithothers”inaccordancewithwhichanindividualandmembersofhisfamilywillbedeemedasholdingtogether(evenifthefamilymembersdonotlivetogetherorthelivelihoodofoneisnotdependentontheother).Itisproposedtoincludeinthedefinition“interestedparty”alsocasesofownershipofsecuritiesthatareconvertibleintoshares,andofrightstoreceivesharesordebt.Itisproposedthattheresponsibilityofapersonmakingaproposalinapurchaseofferorsaleofferwillbemadeequaltothatofanissuer.Furthermore,apersonmakingaproposalinapurchaseofferwillberesponsibletotheholderofsecurities(includingoptions,bondsandconvertibles)ofthetargetcompanyasdefinedinthePurchaseOfferRegulations,fordamagecaused to him as a result of his violating the provisions of the law.

MemorandumSecuritiesLaw,2009,SecuritiesRegulations(Certificatesofindebtedness),2009ThedraftproposedLawwasapprovedbytheplenumoftheSecuritiesAuthorityon30.3.09,andpublished on the website of the Authority on 1.6.09 for comments by the public. The major changes proposedare:theestablishmentofaregisteroftrusteesandthecheckingofcompliancebytrusteecompanywiththeconditionsofqualificationsetoutinthelawinthisconnection;determininganamountofthedepositinsteadofarequirementforownequity,minimumamountsofinsuranceforatrusteecompanyderivingfromthevolumeofbondsforwhichitservesasatrustee,determiningconditionsofqualificationfordirectorsandthoseemployedbythetrustee;fixingthedutyofreportingtothetrusteeand determining the contents of the annual report on trust matters; the duty to summon an annual meetingtoapprovethecontinuationinofficeofthetrusteeandtosummonameetingatthedemandofa bondholder or at the demand of the trustee; determining the duty of the trustee to act in the interest ofthepublicholdingbondsofthesameseries,includingexaminingcompliancebytheissuerwithhisobligationstowardsthebondholders,andthedutiesderivedfromthisgeneralobligation;safeguardingtrusteeassetsforthebenefitofthepublicholdingthebonds,examiningpossibleactionsavailabletothebondholdersiftherearegroundstomakethebondsrepayableimmediately(includingarealconcernofamaterialbreachofobligationsbytheissuer).

ProposedLawamendingtheBillsofExchangeOrdinance(ChecksCrossedNon-negotiable),2009Thisisaprivatemember’sbilltabledintheKnesseton21.12.09.Itisproposedtoprotecttheconsumer(mainlyhouseholdsandprivateindividuals)andobligethebanksto issue them with books of non-negotiable checks only as the default alternative. A customer requesting checkbooks with no limitation of negotiability can do so by special request at the branch of his bank and on his responsibility.

28 / Annual Report 2009

UBank Ltd.

ProposedSecuritiesLaw(AmendmentNo.38)(SecureElectronicMailSystem),2008The proposal was published on 27.7.09 and will come into effect after regulations will be made and rules determined by the Authority.ThemainchangesproposedaretoallowtheIsraelSecuritiesAuthoritytoprovideadvices,demands,instructionsoranyotherdocumentthattheAuthorityisauthorizedtoprovidetobodiesunderitssupervision,bymeansofasecureelectronicmailsystem.Itisproposedtoimposeonaddresseestheobligation to use the said electronic mail system and to receive documents from the Authority through itatafrequencytobedeterminedinregulations,anditisproposedtodetermineapresumptionthatadocument provided through the system reached its destination after two business days.

ProposedSecuritiesLaw(OffExchangeDealerSystem),2009The proposal was approved in the Ministerial Committee for Legislative Matters on 10.1.2010.Themainchangesproposedare:adefinitionwillbeaddedof“dealer”;thedefinitionof“securities”willbeexpandedtoincludeallfinancialinstruments;a“dealer”willbeobligedtoobtainalicensefromtheAuthorityforpurposesofitsactivity;dutieswillbeimposeduponadealerwhoseaimisminimizingtheeffectofconflictsofinterestsbetweenthedealerandcustomers,includingincreaseddisclosuredutiestowardsitscustomers.Adealerwillberequiredtoshowfinancialstabilitybymeansofhavingminimumownequity,adepositandliquidassets.Itwillalsohavetoholdappropriateinsuranceandwillberequiredto comply with the rules determined in the regulations concerning the manner of handling customer funds.Inaddition,itwillberequiredtoprovecompliancewithtechnicalconditionsofcomputerizationforpurposesofcompliancewithhisobligations.Furthermore,thedutiesofcautionandskilltowardscustomerswillapplytoitanditscontrollingshareholder,directorsandCEO;reportingrequirementstothe public and to the ISA will be imposed on dealers.

ProposedBankofIsraelLaw,2009TheproposedlawwasapprovedinfirstreadingintheplenumoftheKnesseton8.2.2010.ItisproposedthattheGovernorbeauthorizedtoissuedirectivesconcerningliquidassetstobeheldbyabankingcorporation,andthatincaseswhenitdidnotactaccordingly,theGovernorisauthorizedtodetermine the rate of interest that the corporation is to pay. There is a possibility for granting credit to bankingcorporationsandreceivingdepositsfrombankingcorporationsagainstthepledgeofsecurities,whileitisproposedthatthepledgewillbeineffectagainstthirdparties,evenifithasnotbeenrecordedinfavortheBankofIsrael(henceforth:“theBank”)ornotdeposited,providedthatthepledgedsecuritiesarerecordedinfavoroftheBankofIsraelwiththefinancialintermediary,suchas:aStockExchangememberoftheStockExchangeClearingSystem.TheBankwillbeauthorizedtorequirereportingandtosupervisefinancialbodiesthataresubjecttoit,itisproposedtodetermineasageneralrulethattheBankofIsraelisauthorizedtomanageaccounts,andnotjustdeposits,forbankingcorporations.Non-compliancewithoneofthedirectiveswillenabletheGovernortoimposeamonetarysanction,includingimposingdirectresponsibilityontheorganizationthatactedonbehalfofthecorporation.ItisproposedtoauthorizetheGovernortoissueanorderrequiringthegivingofinformationinrelationtotransactionsin the foreign currency market in Israel.

ProposedCourtsLaw(CombinedVersion)(Amendment),2009The proposed law was promulgated by the Advisory and Legislation Committee of the Ministry of Justice for comments by the public by 11.1.09.ItisproposedtosetupanEconomicDepartmentintheTel-AvivDistrictCourt,whichwillhearalleconomicmatterstoallowfortheefficientmanagementofproceedings.Economicmattersasper:theCompaniesLaw,theSecuritiesLaw,theJointInvestmentTrustLaw,andtheRegulationofEngagementinInvestmentAdvice,InvestmentMarketingandInvestmentPortfolioManagementLaw.