2015 Will Arkansas be operating as a State

Partnership Marketplace or will Arkansas become a State-Based Marketplace?

Implications for the Small Group Market and Small Employer Health Options Program (SHOP): Employer or employee choice model Active purchaser or market based

Key Aspects for Employers

New definition of Small Group moves to 100 employees in 2016 Rating rules apply to 50-100 groups Essential Health Benefits (EHB) package applies to 50-100 groups New way rates are built for 50-100 groups

HHS has reserved the right to define “Essential Health Benefits” Package for 2016 May result in a standardized EHB in all 50 States

State waiver for private option ends in 2016

Known Changes to the Market beyond 2015

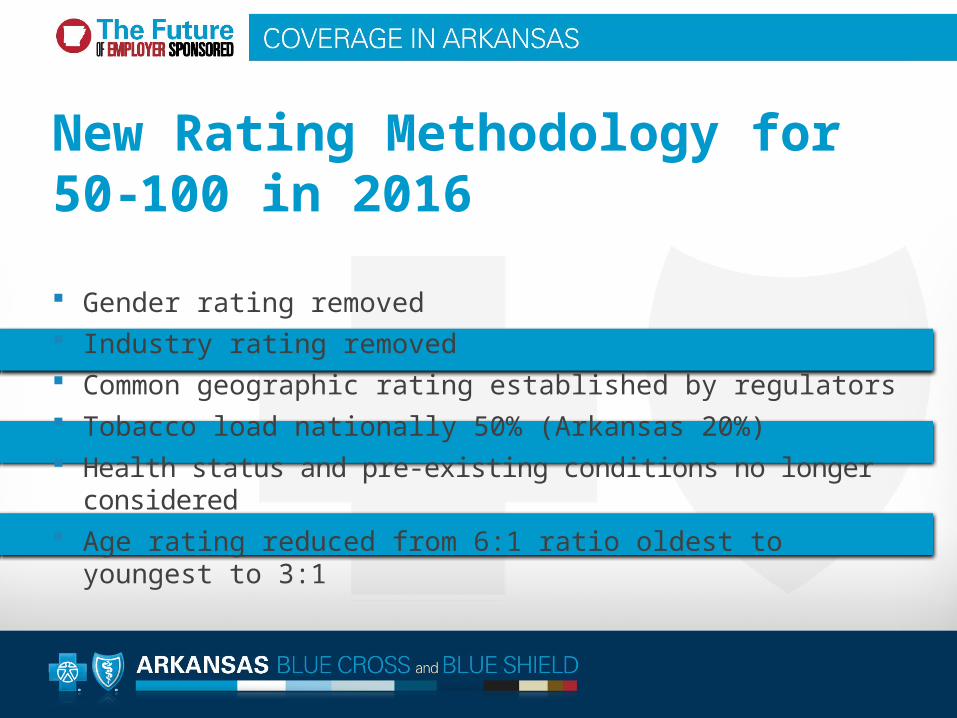

New Rating Methodology for 50-100 in 2016

Gender rating removed Industry rating removed Common geographic rating established by regulators Tobacco load nationally 50% (Arkansas 20%) Health status and pre-existing conditions no longer considered Age rating reduced from 6:1 ratio oldest to youngest to 3:1

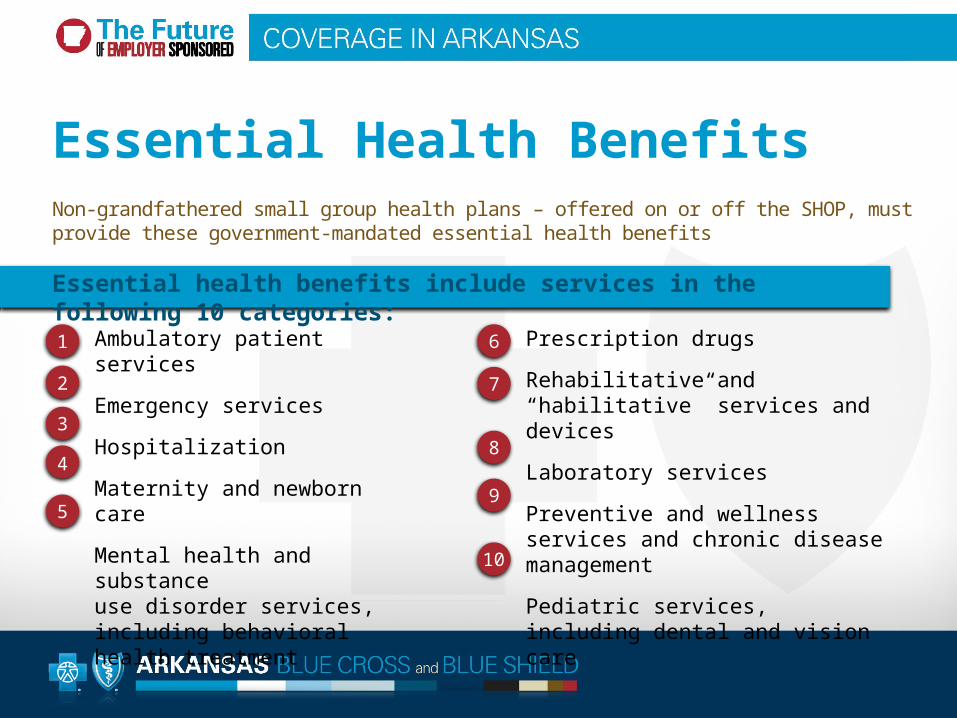

Essential Health Benefits

Prescription drugs

Rehabilitative and “habilitative” services and devices

Laboratory services

Preventive and wellness services and chronic disease management

Pediatric services, including dental and vision care

Non-grandfathered small group health plans – offered on or off the SHOP, must provide these government-mandated essential health benefits

Essential health benefits include services in the following 10 categories:

Ambulatory patient services

Emergency services

Hospitalization

Maternity and newborn care

Mental health and substanceuse disorder services, including behavioral health treatment

1

2

3

4

5

6

7

8

9

10

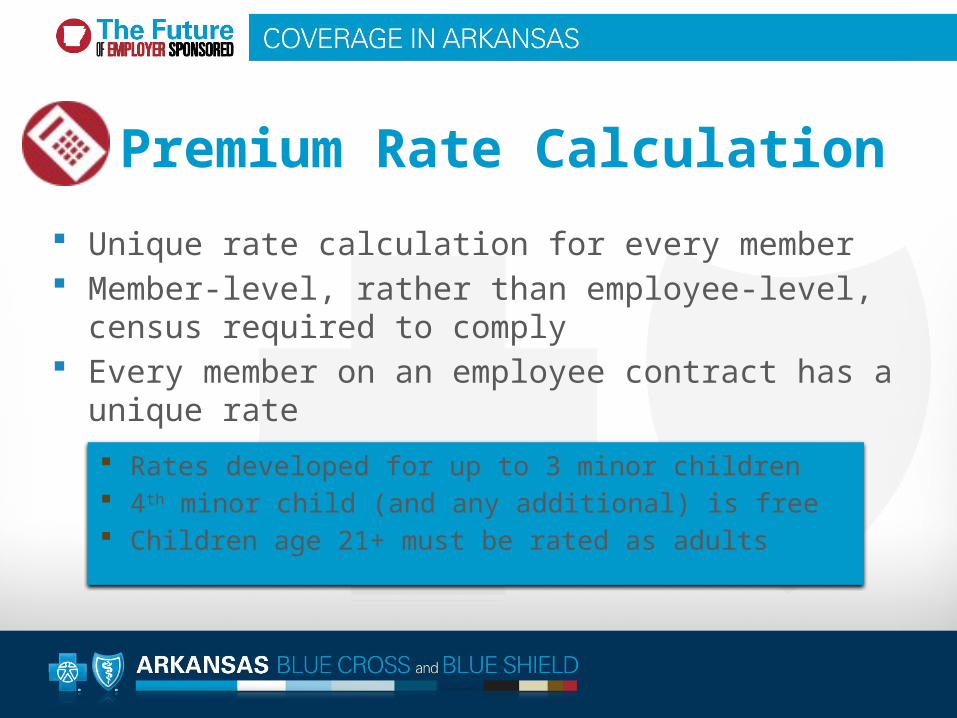

Premium Rate Calculation

Unique rate calculation for every member Member-level, rather than employee-level, census

required to comply Every member on an employee contract has a

unique rate

Rates developed for up to 3 minor children 4th minor child (and any additional) is free Children age 21+ must be rated as adults

2017 Marketplace

Marketplace can allow large groups (100+) to purchase through online marketplaces similar to SHOP for small employer groups. Implications

Essential Health Benefits Package

Employee Choice Model

Employer Open Enrollment Period

“Large Group” Purchasing on Marketplace

Self-Funding

Grandfathering

Defined contribution through private exchanges

Employer Strategies to Stay “Outside Marketplace”

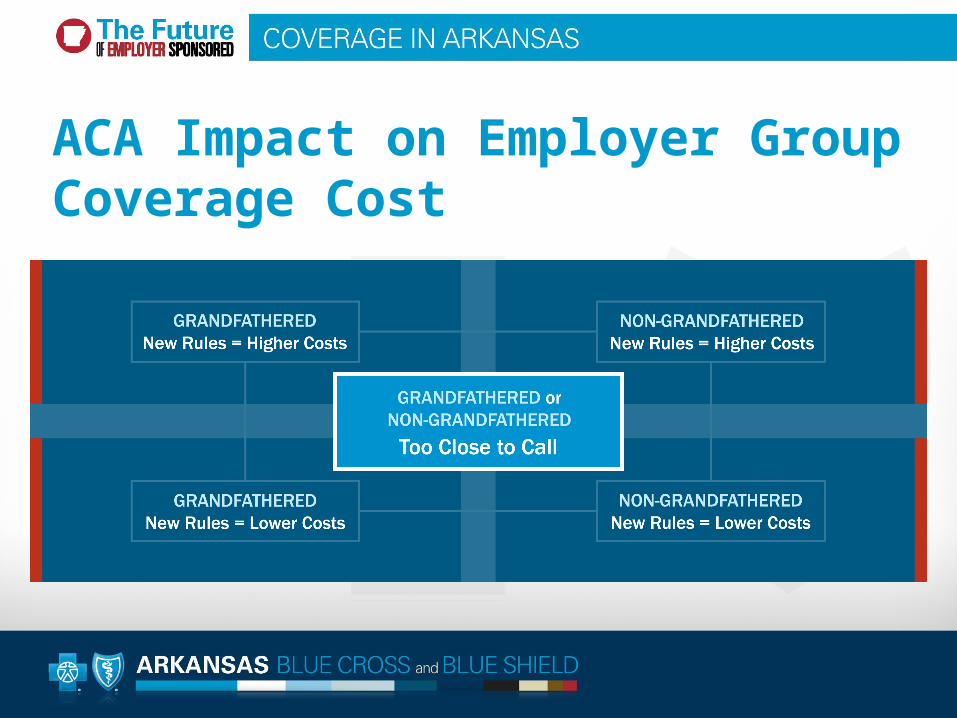

ACA Impact on Employer Group Coverage Cost

Employee/Incentives to drive engagement (Wellness and Health Management Incentives/Programs)

Medical Home Models

Health Improvement Tools

Employer Strategies to Control Costs

Management of “pre-crisis” chronic conditions – new models of Case Management

Focused Provider Panels Home Monitoring, Electronic Health Reference-based pricing Onsite health care New payment mechanism

Employer Strategies to Stay “Off Exchange” and Control Costs

13

Recommended