Embed Size (px)

Citation preview

1

PERFORMANCE MEASUREMENT

IN LOCAL GOVERNMENTS

“People and their managers are working so hard to be sure things are done right, that they hardly have time to decide if they are doing the right things.”

Stephen R. Covey

3

Outline

Why Performance measurement? Performance measurement in local

governments Best Practice Performance indicators Balanced Scorecard Logic Model Performance Budgeting Critical elements and some pitfalls

4

Why Performance Measurement?

In the spirit of good leadership and governance, there is the need to develop appropriate measures to assess performance

Government units of all sizes and types use performance measures as a tool for improving service delivery.

Performance measures offer many advantages to organisations

5

Why Performance Measurement?

Provide more effective management of your programmes Enhance decision making Identify and document areas that need

attention Strengthen managers’ focus on results Facilitate continuous improvement

Motivate staff and volunteersSupport annual and long-range

planning

6

Why Performance Measurement?

Explain your programme: get the story out to the public, to legislators, to elected officials

Document and publicize accomplishments

Build support for your programme Provide accountability: what the

public is (or will be) getting for the funds provided

7

Uses of Performance Measures in Local Government

1. To demonstrate accountability to citizens, elected officials and other interested parties by reporting the service efforts and accomplishments.

2. To improve the allocation of resources by using performance information to inform the development and enactment of a local government’s budget.

3. Assure the achievement of desired results by using performance information to monitor the delivery of services and make adjustments, if necessary, in the service delivery.

8

Things you Must be Aware of:

In any performance measurement system you will need to:

1. Know your output measures (that is, measures of the quantity of services provided) to monitor the delivery of services.

2. Know your outcome measures (that is, measures of the results associated with the provision of services) Please be aware of the difficulties of

measuring outcomes in the public sector

9

Things you Must be Aware of:

3. Use consistent measures from period to period in order to sustain attention to the process,

4. Ensure that there is periodic review and revision of the performance measures.

5. Ensure that comparisons are made with prior periods’ performance as well as with targets.

6. Comparison of performance data to the corresponding data from similar local governments.

10

Things you Must be Aware of:

7. Report performance results to the public and oversight bodies, as well as using the measures internally to initiate improvements.

8. Internally, ensure that the performance measures are used for the evaluation and recognition of departmental heads This can be an effective motivator, particularly if

incentives, such as staffing flexibilities, additional equipment and bonuses, can be partially based on meeting performance targets and goals.

9. Follow up on progress (or the lack thereof) of improvement plans.

11

Things you Must be Aware of:

10. To assure continuation of the use of performance measures for improving service delivery, the systems must be driven down into the organization such that the processes are in place, and the people want to continue using the processes.

11. Ensure that there is Chief Executive commitment and involvement in the overall process

12. Support staff involvement in the reviews of performance results.

12

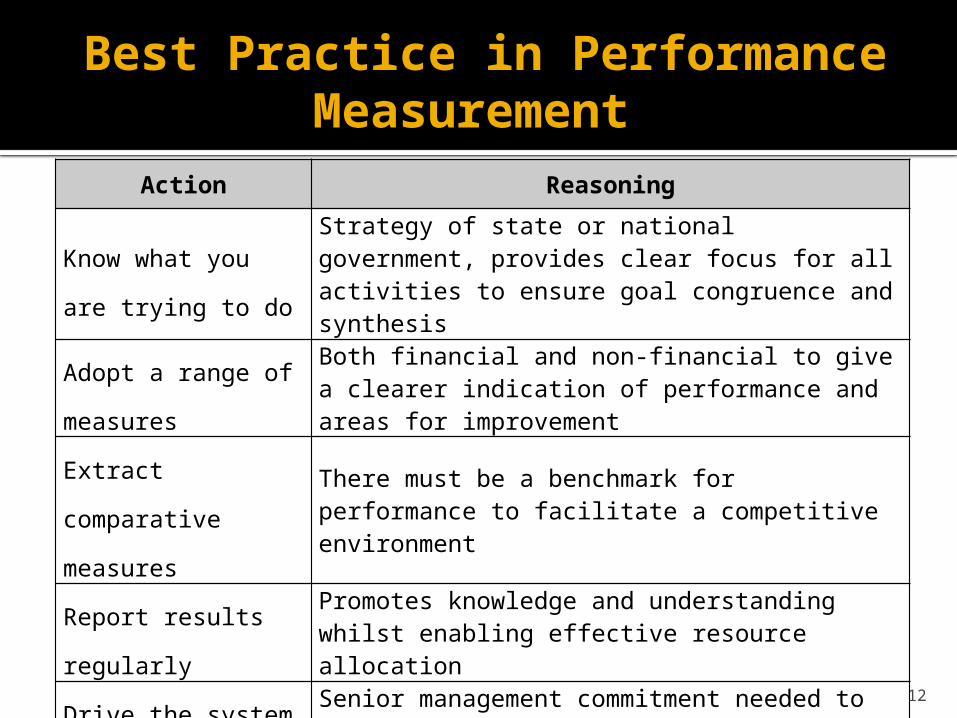

Best Practice in Performance Measurement

Action Reasoning

Know what you are

trying to do

Strategy of state or national government, provides clear focus for all activities to ensure goal congruence and synthesis

Adopt a range of

measures

Both financial and non-financial to give a clearer indication of performance and areas for improvement

Extract comparative

measures

There must be a benchmark for performance to facilitate a competitive environment

Report results

regularly

Promotes knowledge and understanding whilst enabling effective resource allocation

Drive the system from

the top

Senior management commitment needed to enable the ethos to permeate the entire organisation

A Good Performance Measurement Framework

Simple, meaningful, uncomplicated and easily understood

Crafted, owned, managed by the staff and management of the local government

Predicated on high data integrity Must be able to drive and sustain improved

performance of staff and of services rendered by the local authority

Linked to critical goals, targets and drivers of the local authority

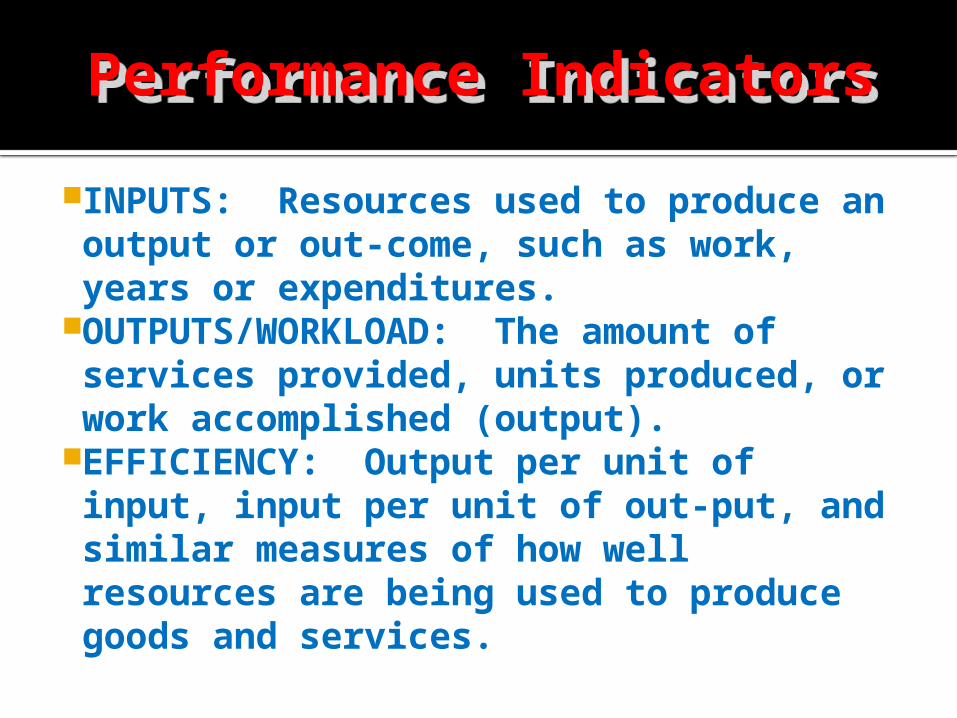

Performance IndicatorsPerformance Indicators

INPUTS: Resources used to produce an output or out-come, such as work, years or expenditures.

OUTPUTS/WORKLOAD: The amount of services provided, units produced, or work accomplished (output).

EFFICIENCY: Output per unit of input, input per unit of out-put, and similar measures of how well resources are being used to produce goods and services.

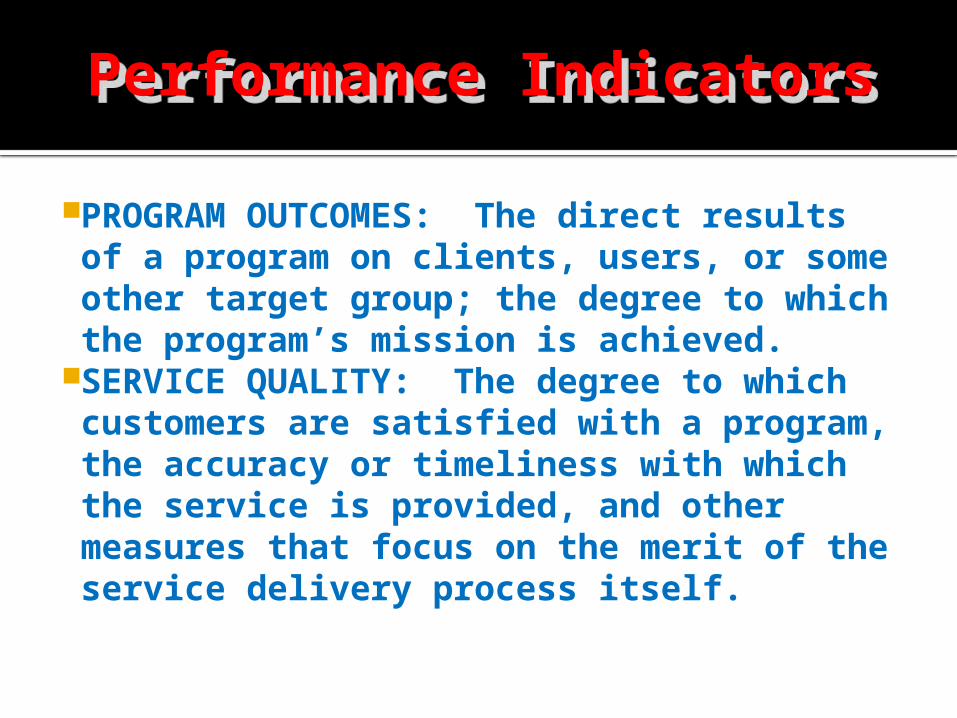

Performance IndicatorsPerformance Indicators

PROGRAM OUTCOMES: The direct results of a program on clients, users, or some other target group; the degree to which the program’s mission is achieved.

SERVICE QUALITY: The degree to which customers are satisfied with a program, the accuracy or timeliness with which the service is provided, and other measures that focus on the merit of the service delivery process itself.

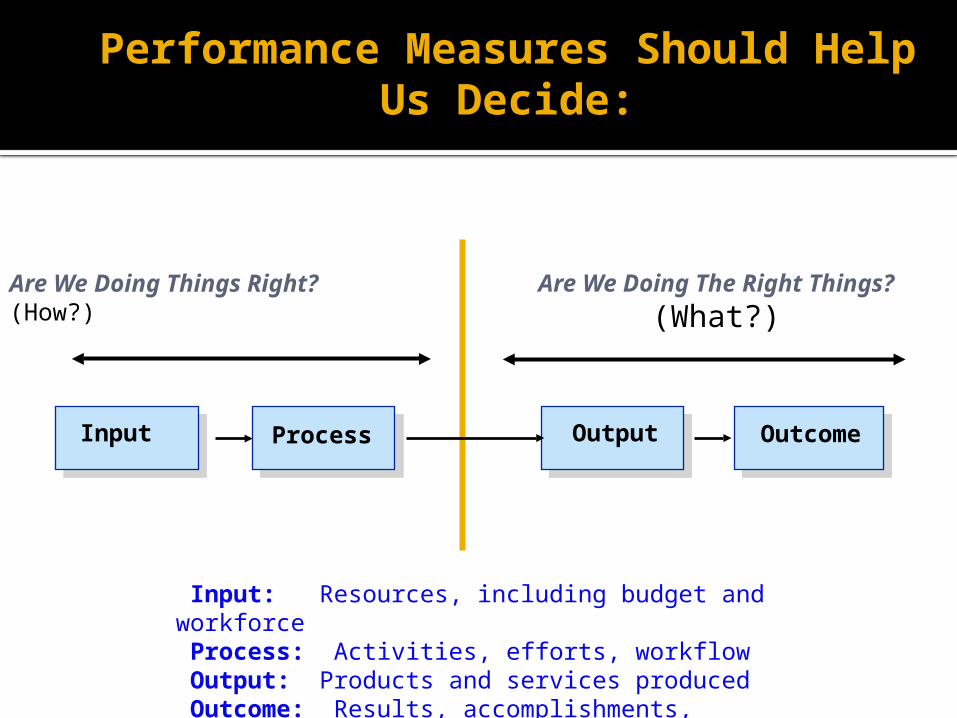

Performance Measures Should Help Us Decide:

Are We Doing Things Right?(How?)

Are We Doing The Right Things?

(What?)

Input Process Output Outcome

Input: Resources, including budget and workforce Process: Activities, efforts, workflow Output: Products and services produced Outcome: Results, accomplishments, impacts

MANAGEMENT STEPS

Build a performance team and communication networks

Only if the concept of performance measurement permeates through the whole organisation can it be successful. Involving employees, stakeholders and customers in planning the system is the first step to building their trust and commitment in the implementation phases.

Regular, open and accessible communication channels support the system throughout its lifecycle and ensure that deficiencies are communicated early.

Build Ownership and Commitment

Ownership and commitment relate closely to inclusion and communication. Because the key pressures of real measuring rest with the employees, it is vital that they believe in its benefits to themselves, to the organisation and to the customer.

Assign Accountability

Clear accountability represents a kind of system insurance, ensuring that measurement is properly conducted and results are properly reported.

It is unadvisable to leave all accountability to rest on top management; on the contrary, dividing it proportionally among management levels may help to prevent late revelation of possible system challenges.

Use performance data in service delivery decision-making

Integral use of performance information lies in making decisions about which services are underperforming and need more attention.

While a synthesis with other kinds of information is needed to establish ‘why’ a service is not performing, measurement data are the necessary foundation.

22

MODELS OF MEASUREMENT

BALANCED SCORECARD

LOGIC MODELBENCHMARKINGPERFORMANCE BUDGETING

What is a Balanced Scorecard?

BALANCED SCORECARD (BSC)

The Balanced Scorecard (BSC) is a strategic performance management framework that allows organisations to manage and measure the delivery of their strategy.

In a recent world-wide study on management tool usage, the Balanced Scorecard was found to be the sixth most widely used management tool across the globe which also had one of the highest overall satisfaction ratings

24

BALANCED SCORECARD (BSC)

It translates an organization’s mission and strategy into a comprehensive set of performance measures that provides the framework for strategic measurement and management systems.

It attempts to balance the use of financial and non-financial measures in driving both short-term and long-run performance.

The BSC system is used to communicate and manage strategy implementation.

25

26

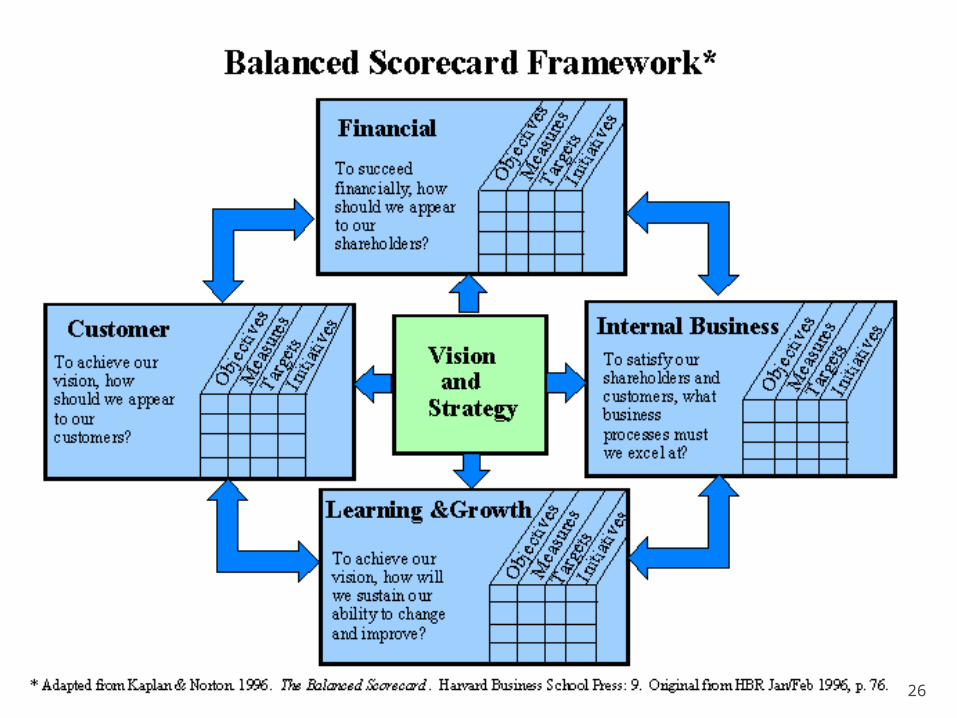

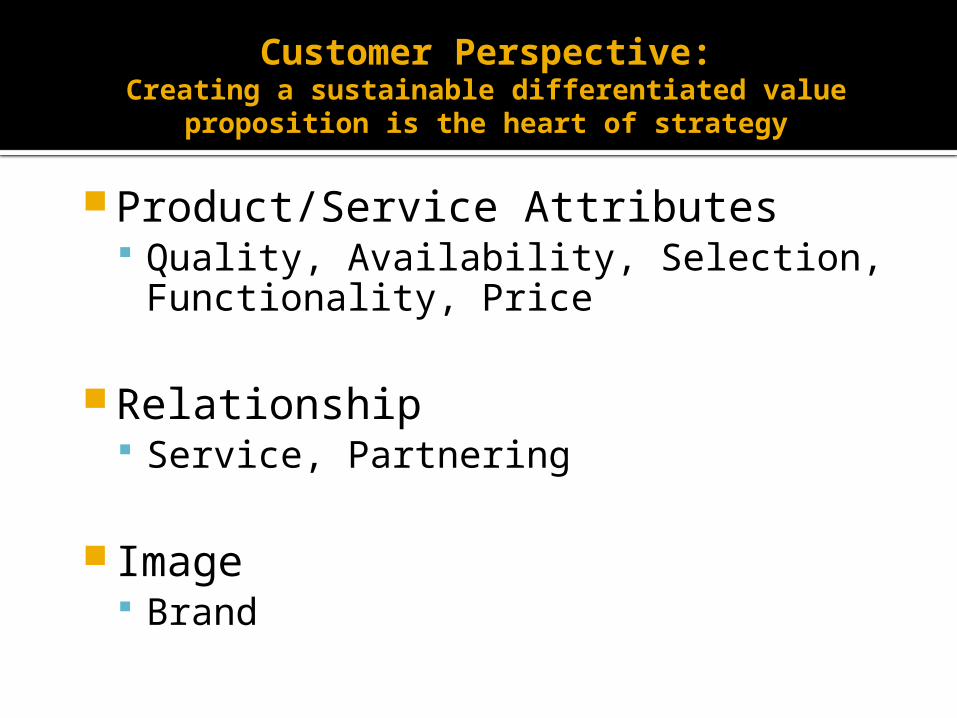

Customer Perspective:Creating a sustainable differentiated value

proposition is the heart of strategy

Product/Service Attributes Quality, Availability, Selection,

Functionality, Price

Relationship Service, Partnering

Image Brand

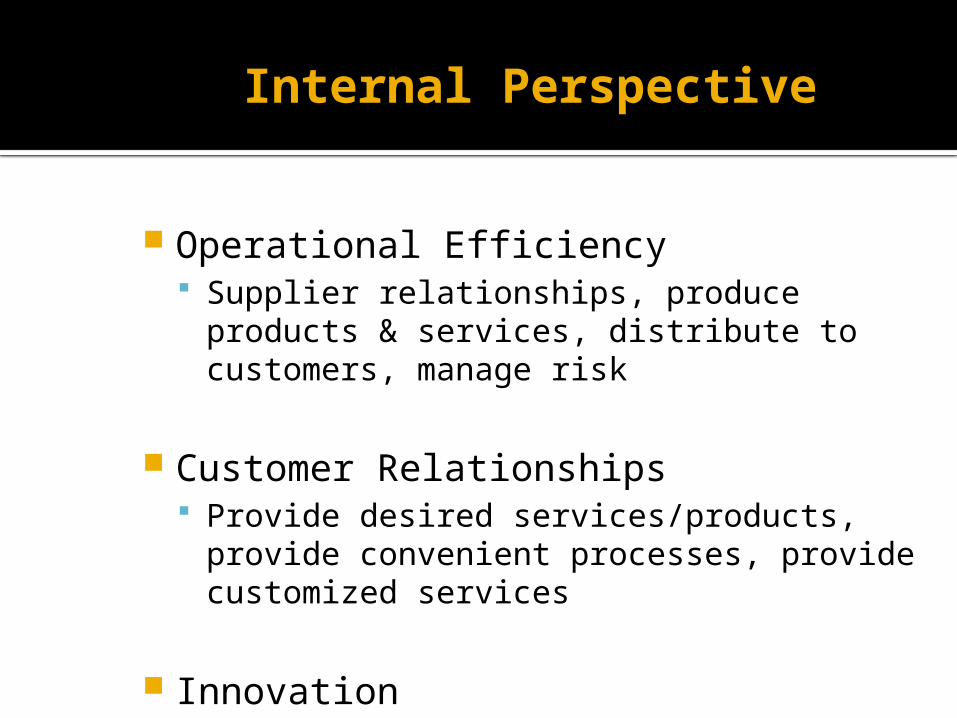

Internal Perspective

Operational Efficiency Supplier relationships, produce products &

services, distribute to customers, manage risk

Customer Relationships Provide desired services/products, provide

convenient processes, provide customized services

Innovation Process innovation, manage capital projects

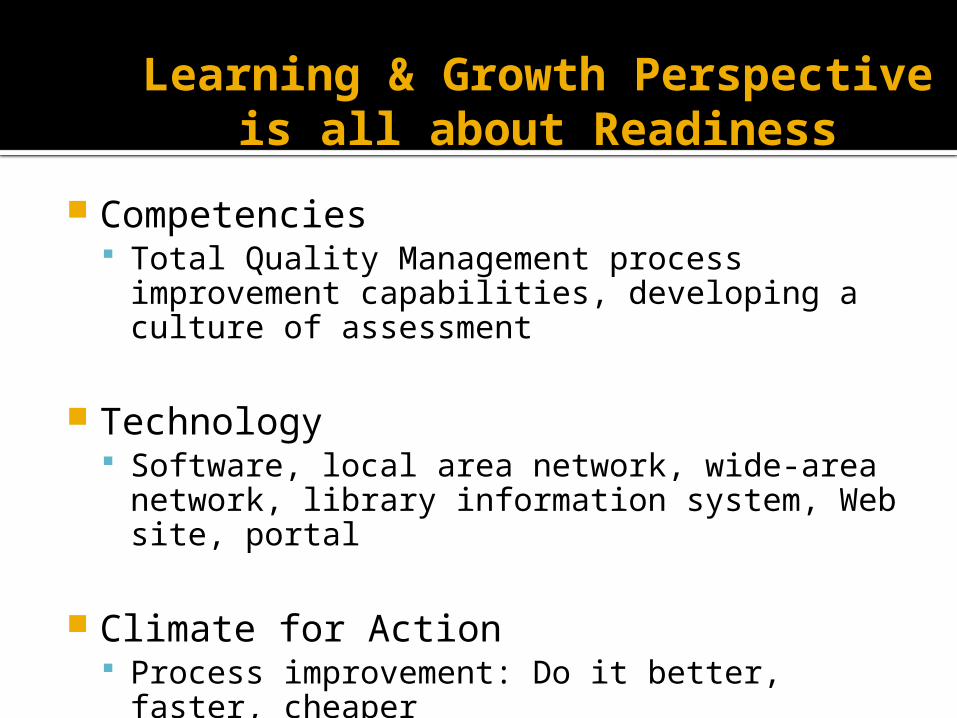

Learning & Growth Perspectiveis all about Readiness

Competencies Total Quality Management process

improvement capabilities, developing a culture of assessment

Technology Software, local area network, wide-area

network, library information system, Web site, portal

Climate for Action Process improvement: Do it better, faster,

cheaper

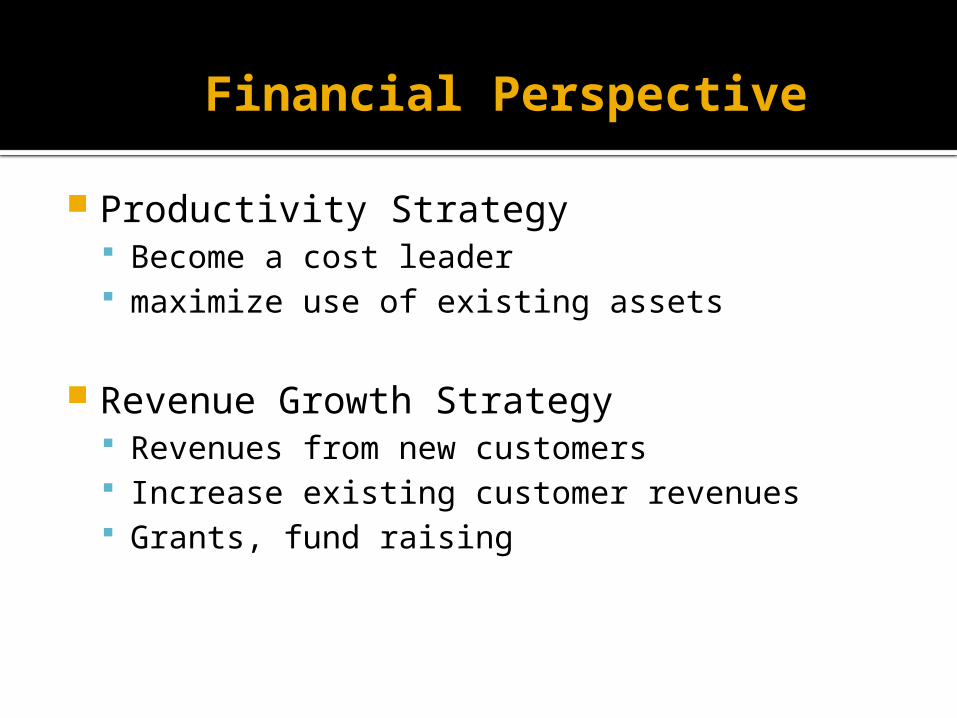

Financial Perspective

Productivity Strategy Become a cost leader maximize use of existing assets

Revenue Growth Strategy Revenues from new customers Increase existing customer revenues Grants, fund raising

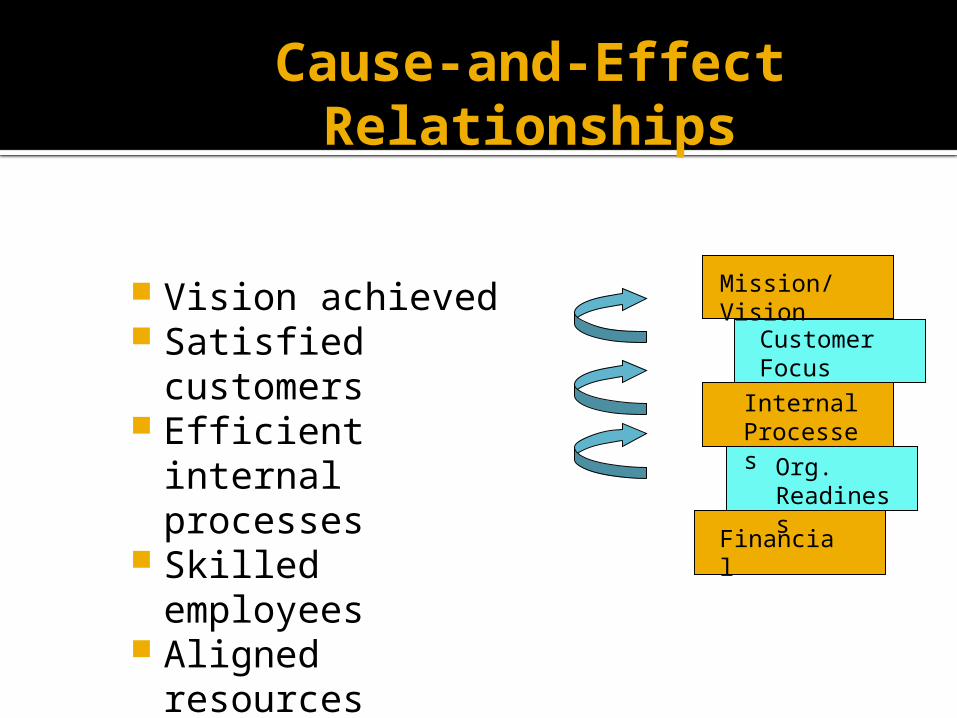

Cause-and-Effect Relationships

Vision achieved Satisfied

customers Efficient internal

processes Skilled employees Aligned resources

Mission/Vision

Customer Focus

Internal Processes

Org. Readiness

Financial

Who is Using the Scorecard?

CompaniesFederal governmentState and local government

Non-profit agenciesA few libraries

Starting Point Mission Statement (the present) Values Statement The Vision (the future) The gap between now and the

future leads to a plan of action to achieve the vision. How we get to the future involves strategies.

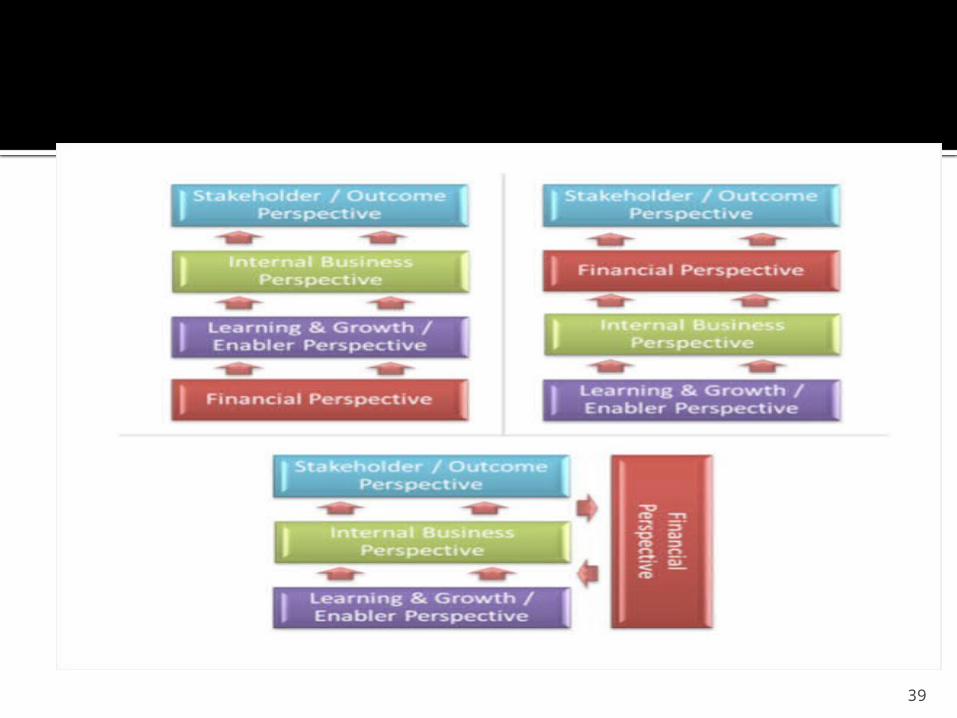

APPLICATION TO LGs

While the Balanced Scorecard was initially designed for commercial companies, the framework has found wide-spread use in the public and not-for-profit sector.

However, it is important to make a few changes to the strategy map template in order to make it suitable to government, public sector and not-for-profit organisations:

34

APPLICATION TO LGs

Strategy maps have to represent the strategy of the organisation.

Since the strategies of public and not-for-profit organisations differ widely, there are no right or wrong answers as to where the financial perspectives should go.

35

APPLICATION TO LGs

Move the Financial Perspective from top spot on the strategy map template. The overall objective of most public sector, government and not-for-profit organisations is not to make money, maximise profits or deliver shareholder return. While finance is important, it is usually not the overall reason why the organisation exists.

36

APPLICATION TO LGs

Instead, the main objective of public sector, government and not-for-profit organisations is to deliver services to their key stakeholders, which can be the public, central government bodies or certain communities.

This perspective usually sits at the top of the template to highlight the key stakeholder deliverables and outcomes.

37

APPLICATION TO LGs

The two remaining perspectives will largely stay as they are. Any public sector, government and not-for-profit organisations needs to build the necessary human, information and organisational capital to deliver its key processes to support its overall objectives of serving its stakeholders.

38

39

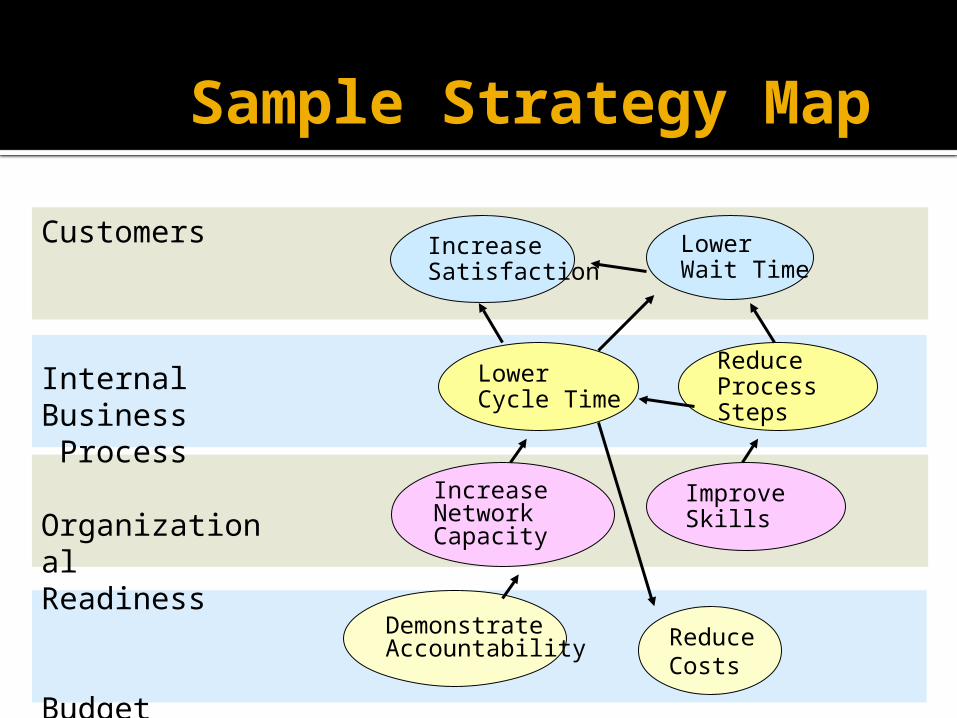

Sample Strategy Map

Customers

Internal Business Process

OrganizationalReadiness

Budget

DemonstrateAccountability Reduce

Costs

IncreaseNetworkCapacity

ImproveSkills

LowerCycle Time

ReduceProcessSteps

IncreaseSatisfaction

LowerWait Time

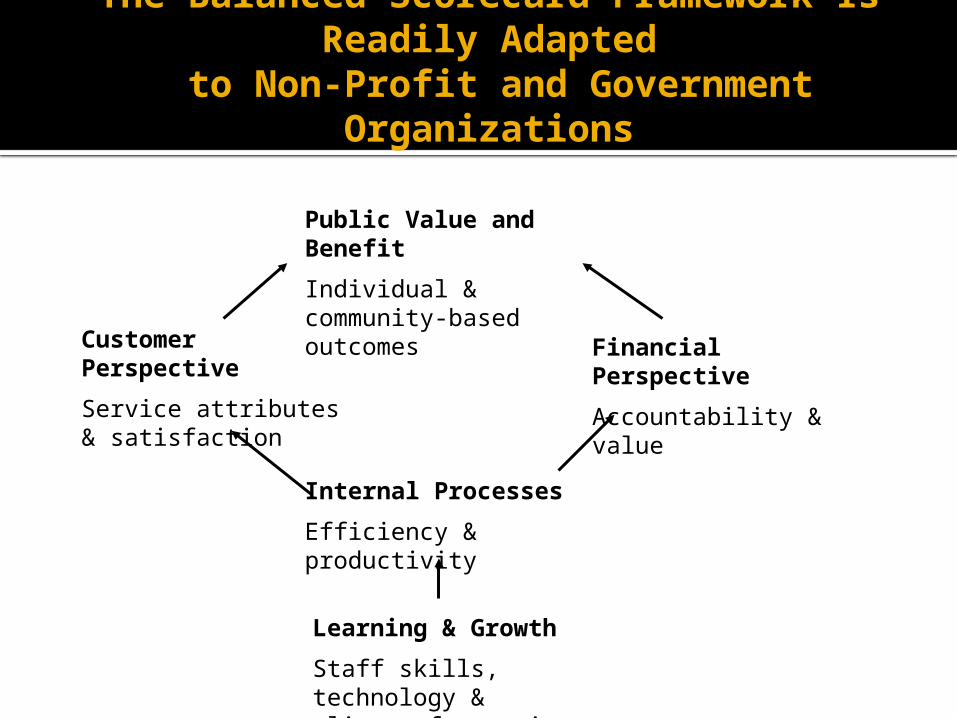

The Balanced Scorecard Framework Is Readily Adapted

to Non-Profit and Government Organizations

Public Value and Benefit

Individual & community-based outcomes

Customer Perspective

Service attributes & satisfaction

Financial Perspective

Accountability & value

Internal Processes

Efficiency & productivity

Learning & Growth

Staff skills, technology & climate for action

Critiques of the BSC

SC is labour intensive because it is a consensus-driven approach. The use of the BSC also requires

a change in the orientation of the employees (e.g. participation in decision making).

BSC may result in employees paying attention to the areas measured.

BSC may be too restrictive and also may not be able to cope with a fast changing environment.

42

The Logic ModelThe Logic Model

This is also known as Results Framework

“Begin with the end in mind”

Start by asking:▪ What results are we seeking?▪ What are we hoping to accomplish?▪ How will we accomplish it?

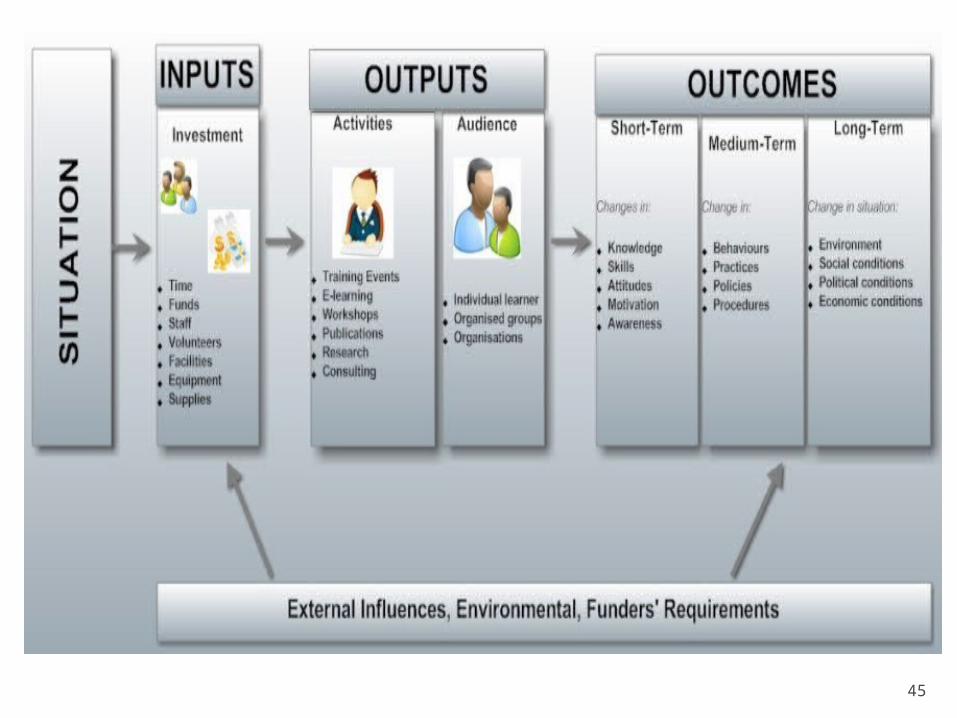

What is the Logic Model?What is the Logic Model?

A picture of a programA way to show the relationship

between what we put in (inputs), what we do (outputs) and what results occur (outcomes)

Sequence of if/then relationshipsCore of program planning and

evaluation

45

How the Logic Model can help the local government

Focuses on ultimate outcomes that the local government wants to achieve

It enables management to think backwards through the logic model to identify how best to achieve the desired results.

Thus, instead of focusing on what we are currently doing, we will shift focus to what we need to do to achieve our aim.

46

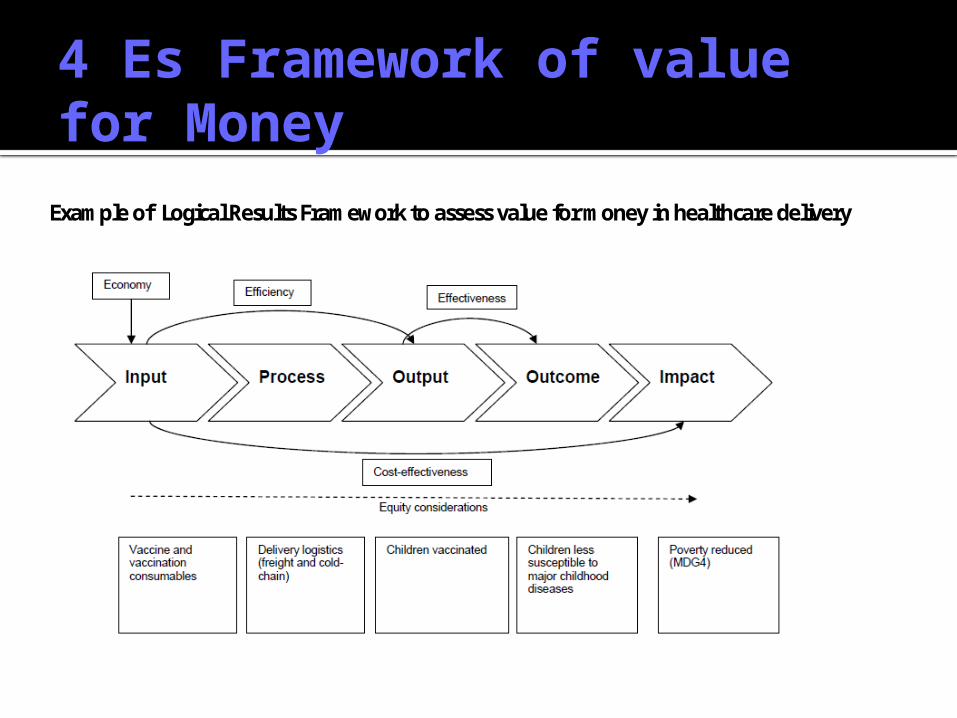

4 Es Framework of value for Money

Example of Logical Results Framework to assess value for money in healthcare delivery

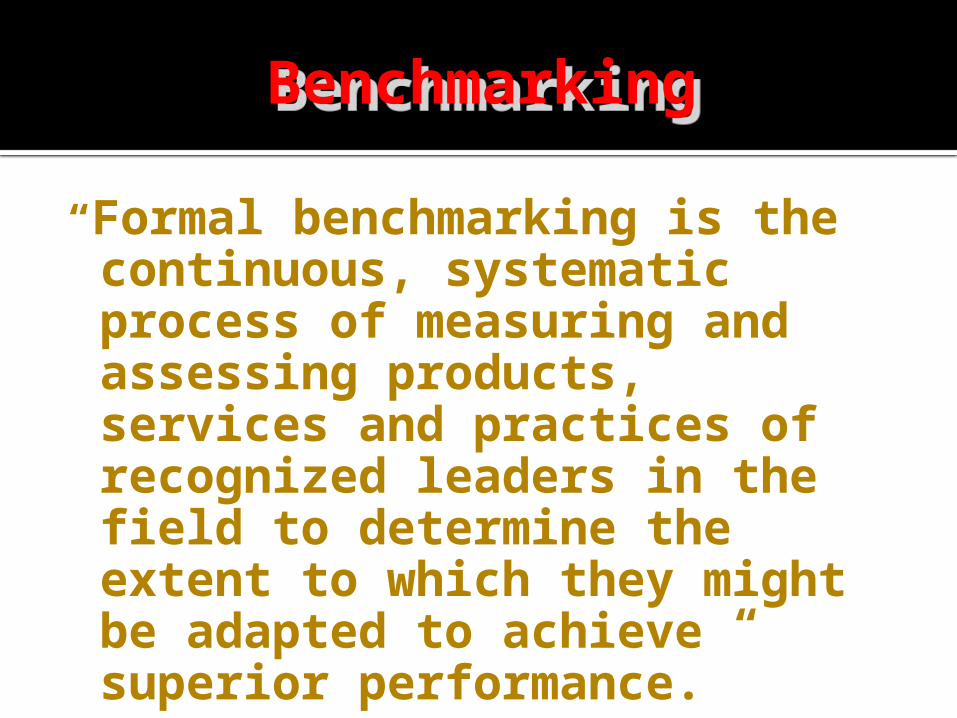

BenchmarkingBenchmarking

“Formal benchmarking is the continuous, systematic process of measuring and assessing products, services and practices of recognized leaders in the field to determine the extent to which they might be adapted to achieve superior performance.”

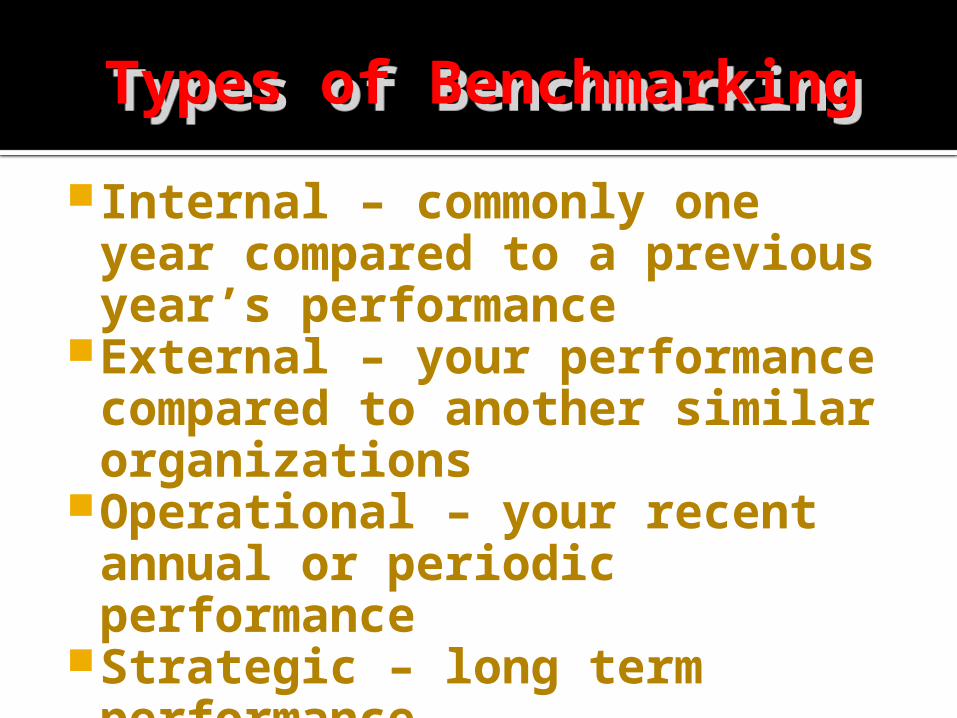

Types of BenchmarkingTypes of Benchmarking

Internal – commonly one year compared to a previous year’s performance

External – your performance compared to another similar organizations

Operational – your recent annual or periodic performance

Strategic – long term performance

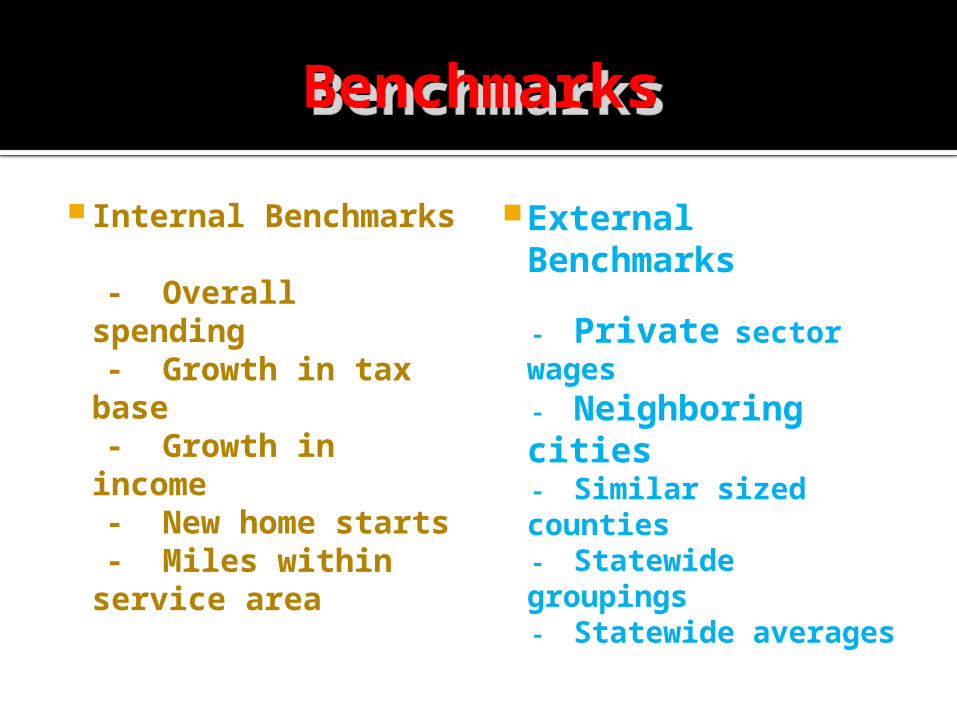

BenchmarksBenchmarks

Internal Benchmarks

- Overall spending - Growth in tax base - Growth in income - New home starts - Miles within service

area

External Benchmarks

- Private sector wages

- Neighboring cities - Similar sized counties - Statewide groupings - Statewide averages

Performance BudgetingPerformance Budgeting

Based on the assumption that presenting performance information alongside budget amounts will improve budget decision-making by focusing funding choices on program results

Performance BudgetingPerformance Budgeting

Performance based budgeting cannot begin until a system of performance measurement has been instituted

A functional performance based budgeting system cannot be expected to produce the long-term desired results in the first year of its inception

Must build a Performance Based Management System

Performance Budgeting

Performance budgeting relies on:

1. Strategic planning2. Operational planning3. Performance accountability4. A realistic performance

measurement system to build budgets.

Performance BudgetingPerformance budgets focus on “return on investment”—that is, what do we get for our investment of resources?

Basic service level (or continuation of basic services)?

Increased services (more services to same recipients or expansion of same services to more recipients)?

Better (higher quality) services?

More efficient services (cost savings in service delivery)?

Mitigation or resolution of a problem?

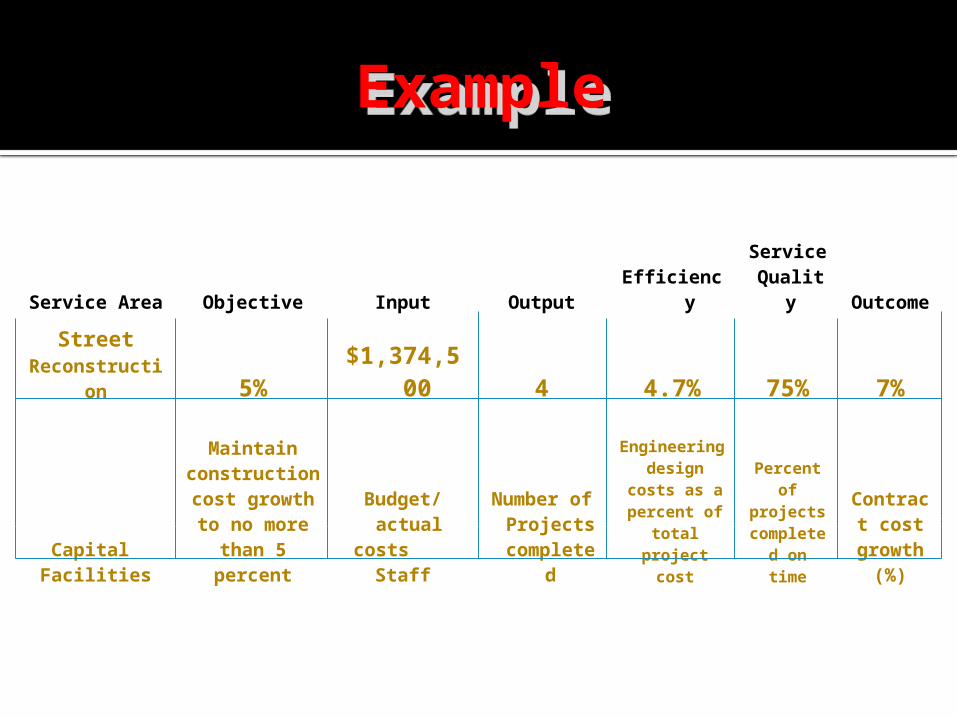

ExampleExample

Service Area Objective Input Output EfficiencyService Quality Outcome

Street Reconstruction 5% $1,374,500 4 4.7% 75% 7%

Capital Facilities

Maintain construction

cost growth to no more than 5

percent

Budget/actual costs

Staff

Number of Projects

completed

Engineering design costs as a percent

of total project cost

Percent of projects

completed on time

Contract cost

growth (%)

56

Integrating Performance into Budget Decision Making

Establish the link between resources and results early and maintain that link through budget development, appropriation, and budget control processes.

Set performance standards linked to appropriation levels Performance standards are the expected levels of performance

associated with a performance indicator for a particular period and funding level. They link dollars and results

Performance standards are one way to demonstrate RETURN ON INVESTMENT--what we can expect to receive for our money (easier to explain to stakeholders)

Use performance data to help make program decisions in budget development

The Failure of Strategy

"You can either take action or wait for a miracle to happen. Miracles are great but they are unpredictable."

Peter Drucker

58

Pitfalls

The performance measurement process should not be used for assigning blame or finding fault with others’ performance.

This is especially important since one person’s desire for accountability can be perceived by others, and particularly those on the front line of service delivery, as merely pointing fingers.

59

Pitfalls

Although the local government might conclude it obtained better service delivery or a process improvement from collecting and using performance data to trigger a change in the way the program operates, it needs to ascertain the explicit change in inputs, outputs, and/or outcomes to confirm that the improvement actually occurred.