Embed Size (px)

Citation preview

A Pension Plan Report to Members on behalf of the Avon Rubber Retirement and Death Benefits Plan

Your Pension. Your Future.

2 Message from the Chairman of the Trustees

3 Key Facts and Figures from 2018

4 Defined Contribution Section

5-6 What’s so good about a pension?

7 Default Fund

9 Latest News

10-11 Trustees and Plan Advisors

12 Further Information

8 Defined Benefit Section Focus

IN THIS ISSUE

Spring 2019

Avon Rubber Highlights 2018

Operating profit

£22.8m

2018 £22.8m

£20.1m

£16.6m

2017

2016

Net cash

£46.5m

2018 £46.5m

£24.7m

£2.0m

2017

2016

Revenue

£165.5m

2018 £165.5m

£159.2m

£138.1m

2017

2016

This year’s valuation will also include a full review with the Company of the longer term aims of the Plan and the investment strategy, to ensure the level of risk being taken is appropriate. Because the Plan has been closed for many years now and we have an ageing membership, it is important that we start to invest in less risky assets, whilst ensuring we continue to meet the investment return targets agreed with the Scheme Actuary.

Details of the Company’s contributions towards the funding deficit and administration costs and the current funding position can be found in the enclosed Summary Funding Statement. At the time of writing it is difficult to predict the impact Brexit will have on our investment strategy but this is something we are continuing to monitor and plan for, and we will take advice on what the eventual outcome means for the Plan.

The equalisation of benefits for men and woman has been in the news recently and this is covered in more detail below. Some members may be due to receive an increased pension but should note that the changes will take some time to calculate and are expected to be small. During the year we have also confirmed the impact of the new UK data protection regime on the Plan and its members. Last year you were sent a new privacy notice setting out how, as a Plan member, your personal data is being used and your rights in relation to your data. There is a reminder in this newsletter of the changes.

Since the last newsletter Mike Harral and Zoe Holland have settled into their roles as Company nominated appointments to the Trustee Board. As recently communicated in a separate letter, I am delighted that Eric Fielding and David Little have been re-appointed as Member Nominated Trustees. My thanks also to David and the Company’s marketing team for overseeing the revamping of our website which can be accessed at www.avon-rubber.com/pensions.

We have been keeping a close watch on administration service levels at Mercer following the increase in the volume of activity across all DB schemes in recent years. I apologise that some DB members have not received the best service this year. We are aware that it has taken Mercer longer than it should to clear certain cases due to staffing problems in the administration team, which we understand have finally been resolved. If you are concerned about the service

you have received from Mercer and have contacted their member helpline (details are set out on the last page of this newsletter) please contact us directly.

For members of our DC scheme, the last year has seen further changes with the introduction of revised death benefits for active members and continued monitoring of the performance of the funds that we make available to DC members to invest in through Standard Life. Please take a moment to log onto the Standard Life portal to see your investments, access your correspondence from Standard Life and check the illustration of your estimated pension at retirement.

If you have any comments about this newsletter or the Plan in general, please contact the administration teams or the Trustees directly.

Message from the Chairman of the Trustee Board

Welcome to the latest edition of the Avon Plan Trustee Newsletter.

Over the course of the year we have continued to monitor the financial strength of Avon Rubber and have no concerns over its ability to support the DB Scheme. Highlights of the latest set of financial results are in the box below. We have maintained an open dialogue on strategy and funding with the management team as we head towards the 2019 triennial valuation. This is the process where the Trustee Board works with the Scheme Actuary and the Company to value the assets and liabilities of the Plan, with the aim of making sure that the Company’s future contributions address any deficit over time.

2 AV O N R U B B E R R E T I R E M E N T A N D D E AT H B E N E F I T S P L A N

PensionNews | SPRING 2019

Miles Ingrey-Counter Chairman of the Trustee Board

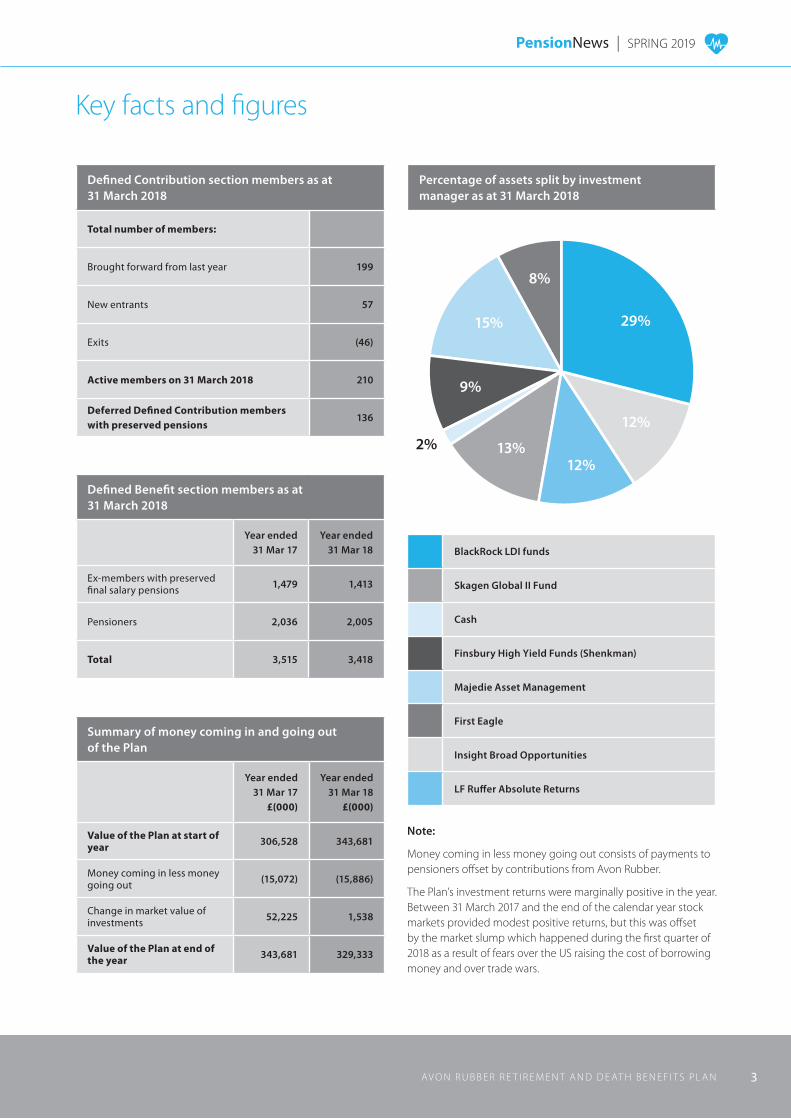

Percentage of assets split by investment manager as at 31 March 2018

BlackRock LDI funds

Skagen Global II Fund

Cash

Finsbury High Yield Funds (Shenkman)

Majedie Asset Management

First Eagle

Insight Broad Opportunities

LF Ruffer Absolute Returns

Key facts and figures

Defined Contribution section members as at 31 March 2018

Total number of members:

Brought forward from last year 199

New entrants 57

Exits (46)

Active members on 31 March 2018 210

Deferred Defined Contribution members with preserved pensions

136

Defined Benefit section members as at 31 March 2018

Year ended 31 Mar 17

Year ended 31 Mar 18

Ex-members with preserved final salary pensions 1,479 1,413

Pensioners 2,036 2,005

Total 3,515 3,418

Summary of money coming in and going out of the Plan

Year ended 31 Mar 17

£(000)

Year ended 31 Mar 18

£(000)

Value of the Plan at start of year 306,528 343,681

Money coming in less money going out (15,072) (15,886)

Change in market value of investments 52,225 1,538

Value of the Plan at end of the year 343,681 329,333

3AV O N R U B B E R R E T I R E M E N T A N D D E AT H B E N E F I T S P L A N

PensionNews | SPRING 2019

Note:

Money coming in less money going out consists of payments to pensioners offset by contributions from Avon Rubber.

The Plan’s investment returns were marginally positive in the year. Between 31 March 2017 and the end of the calendar year stock markets provided modest positive returns, but this was offset by the market slump which happened during the first quarter of 2018 as a result of fears over the US raising the cost of borrowing money and over trade wars.

13%2%

9%

12%

12%

15%

8%

29%

Defined Contribution sectionBenefits in the Defined Contribution (DC) section are determined by a combination of contributions paid by members and the Company and investment income earned. The Company pays an amount specified in the Rules that depends on each member’s chosen contribution rate.

This is a valuable benefit provided by the Company and we want members to be in a position to get the best possible outcomes from this. We have partnered with Standard Life to provide a wide range of funds you can choose to invest in and Standard Life offer a great online portal to access all the information you might need in relation to your personal benefits and the options available to you.

For further information about joining the pension plan, receiving tax benefits from the Government and also receiving additional contributions from the company you can visit the Standard Life Avon portal at: www.standardlifepensions.com/avonrubber

4 AV O N R U B B E R R E T I R E M E N T A N D D E AT H B E N E F I T S P L A N

PensionNews | SPRING 2019

Current members of the DC section of the plan can manage their pension online at: www.standardlife.co.uk/1/site/employeezone/login

GET STARTED

Joining the pension

The sooner you join, the sooner you’ll start receiving tax benefits from the Government - and you will also get extra contributions

from the company.

WHAT DOES THIS MEAN FOR

YOU?

Pension flexibilityEveryone has control over how they

take money from their pension. There’s a minimum age after which

you can withdraw money, but pensions are now one of the most tax-efficient

and flexible ways to save for the future.

YOUR PAYMENT CHOICES

How much should you pay?It’s up to you - as long as you meet the minimum set by the company. But remember, paying in a little bit

more now could make a big difference when you retire.

5AV O N R U B B E R R E T I R E M E N T A N D D E AT H B E N E F I T S P L A N

PensionNews | SPRING 2019

WHAT’S SO GOOD ABOUT A PENSION?

Maximise your workplace pension to claim all the money you’ve earned

A pension can be a great, tax-efficient way to save and if you are an Avon employee you can enrol in the DC Pension scheme which means the Company will be paying towards your future too.

Since people started being automatically enrolled into their workplace pension, more than 9.5 million people in the UK have joined one.

If you’re not currently in the Company pension scheme or taking full advantage of what you’re entitled to, you’re effectively missing out on money in the form of Company contributions. The Company will match the contributions you make to your pension pot, up to a maximum of 7.5% of salary.

Getting in the saving habit couldn’t be simpler

Once you’re in a workplace pension, it couldn’t be easier to stay in the habit because payments come straight from your salary.

That means money isn’t gathering in a bank account tempting you to spend it.

Increasing your pension contributions even just a little could make a big difference to your pension pot in the long run.

If you can take little steps now, your future self will thank you because it’s increasingly unlikely that you can rely on the State Pension alone to provide the lifestyle you’d like for your retirement. The basic State Pension is less than a minimum wage salary and the age when you can claim it is rising. You could be in your late 60s by the time you are eligible.

Give your money the chance to grow

The great thing about a pension is that any money you and your employer are putting aside for your future is invested and will have the chance to grow, although do bear in mind that a pension is an investment, it can go down as well as up and you could get back less than you paid in.

Where you choose to invest could make a big difference to your future lifestyle and when it comes to choosing and reviewing these investments you’ll want to think carefully about how involved you would like to be and how much risk you want to take, amongst other things.

Tax relief can be your pension’s secret weapon

Having a big impact on your future prosperity may not take as much out of your pocket today as you might expect because you get tax breaks on the payments you make to your pension.

These are normally at the highest rate of income tax that you pay. This means that saving £100 into your pension pot only normally costs you £80 – or just £60 if you are a higher rate taxpayer. Tax rules and legislation can change and your own circumstances will have an impact on tax.

WHAT’S SO GOOD ABOUT A PENSION?

6 AV O N R U B B E R R E T I R E M E N T A N D D E AT H B E N E F I T S P L A N

PensionNews | SPRING 2019

Pension freedoms give choicesWhen you eventually come to take your life savings - currently possible from the age of 55 - pension freedoms mean that you now have more choice and flexibility. It’s up to you when and how you take your money. But not all pension plans will offer these options - check you’re in the plan that’s right for you.

Pass on your savings to loved ones - sometimes tax freePension savings can pass to your children or other loved ones, sometimes tax free, and usually without paying inheritance tax (IHT) as pensions are not usually included in IHT.

You can find out more about passing pensions on from Pensionwise.

Just make sure you keep your provider up to date with which loved ones should benefit by keeping your beneficiary nomination form updated as your pension isn’t normally covered by your Will. It’s particularly important following major life events such as the birth of children or divorce. Employees will be issued ‘Expression of wish forms’ with the March payslips to help keep you updated. All members can update their beneficiaries using the Standard Life online portal or the App.

Where can you get more information on your Pension Scheme?For further information regards joining the pension plan, receiving tax benefits from the Government and also receiving additional contributions from the Company you can visit the Standard Life Avon portal at www.standardlifepensions.com/avonrubber.

Current members of the Plan can manage their pension online at www.standardlife.co.uk/1/site/employeezone/login

You can also access and manage your pension using the Standard Life App.

You can find out more about your pension freedom options by visiting Pensionwise.

Go to www.pensionwise.gov.uk or call 0800 138 3944

If IHT is a concern for you, it’s worth taking professional advice from your adviser. If you don’t have one you can get one at unbiased.co.uk

7AV O N R U B B E R R E T I R E M E N T A N D D E AT H B E N E F I T S P L A N

PensionNews | SPRING 2019

Default FundWhat’s the default fund?

The default fund is a ‘balanced’ investment profile chosen by the trustees following detailed analysis of the DC Scheme’s membership and investment advice from our advisers Aon Hewitt. New members are automatically joined into the ‘balanced’ investment profile unless they choose otherwise.

The ‘balanced’ investment profile is designed to provide:

• Medium risk

• Potential for long-term growth with some security

• Moves to lower risk investments approaching retirement

• Designed for members who prefer to take some risk but would also like some of their investments to be secure

Active Plus III Universal SLP

The fund selected by the trustee is the Standard Life Active Plus III Fund. The Active Plus Fund offers the potential for long-term growth with an appropriate level of risk for our members. It also provides “lifestyling” which means that as you approach retirement, investment risk is gradually reduced by moving your fund into deposit style investments. This profile is designed for members who want to take their full tax-free lump sum, and have the flexibility to take the rest of their pension savings the way they want. The fund is charge cap compliant and is actively managed. The trustees have negotiated a 0.71% scheme rebate which means effective total annual fund charge is just 0.42%. Note these charges and rebates are regularly reviewed and could be changed in the future.

To find more information on the individual funds that make up the lifestyle profile please access your fund account.

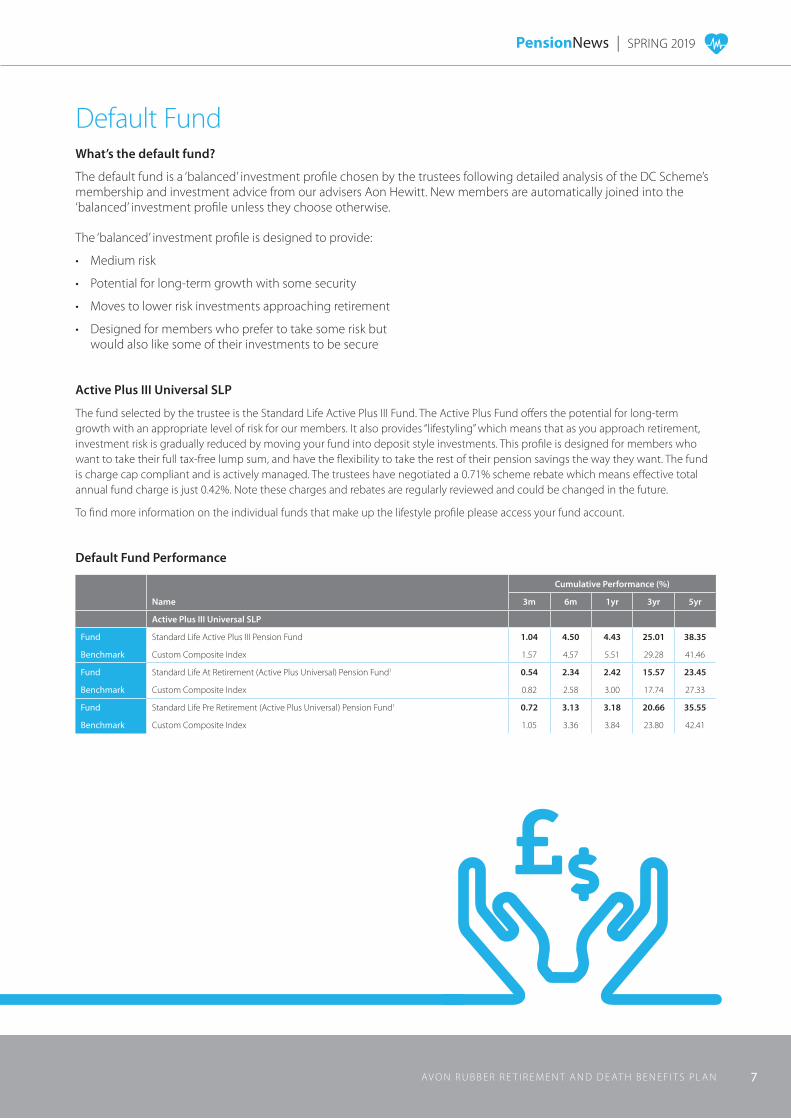

Default Fund Performance

Name

Cumulative Performance (%)

3m 6m 1yr 3yr 5yr

Active Plus III Universal SLP

Fund Standard Life Active Plus III Pension Fund 1.04 4.50 4.43 25.01 38.35

Benchmark Custom Composite Index 1.57 4.57 5.51 29.28 41.46

Fund Standard Life At Retirement (Active Plus Universal) Pension Fund1 0.54 2.34 2.42 15.57 23.45

Benchmark Custom Composite Index 0.82 2.58 3.00 17.74 27.33

Fund Standard Life Pre Retirement (Active Plus Universal) Pension Fund1 0.72 3.13 3.18 20.66 35.55

Benchmark Custom Composite Index 1.05 3.36 3.84 23.80 42.41

8 AV O N R U B B E R R E T I R E M E N T A N D D E AT H B E N E F I T S P L A N

PensionNews | SPRING 2019

Defined Benefit Section Focus

Actuarial valuation and funding positionThe Trustee Board is responsible for ensuring that sufficient contributions are paid into the Plan to cover benefits payable in accordance with the Rules and to build up funds to pay for future benefits.

Since the closure of the Defined Benefit section of the Plan in 2009, benefits in the Defined Benefit section are paid for by a combination of contributions paid by the Company and investment income earned.

The amount of contributions to be paid is agreed between the Company and the Trustee and recorded in a Schedule of Contributions. The Trustee Directors are advised by the Scheme Actuary who helps them agree appropriate assumptions with the Company for calculating contributions. Once the assumptions are agreed the Scheme Actuary assesses the amount of money in the Plan relative to the benefits that must be paid out, both now and in the future. This assessment is known as an actuarial valuation of the Plan and is normally carried out every three years.

We are due to carry out a valuation with an effective date of 31 March 2019 at which point the contributions to be paid by the Company will be reviewed. In the meantime, we have included with this publication an up to date ‘Summary Funding Statement’ which shows the estimated funding level at 31 March 2018.

GMP Equalisation in the High CourtYou may have seen in the news that there has been a High Court ruling regarding the equalisation of Guaranteed Minimum Pensions (‘GMPs’). Set out below is a brief summary of how this complex issue may affect you.

Does this ruling affect me?

The judgment only applies to benefits built up between 17 May 1990 and 6 April 1997. Only members or their dependents with pensions built up over this period will be affected. The ruling affects men and women, and both pensioners and members who have yet to draw their pension.

The Trustee and Company are working with their advisers to understand how this ruling affects the Plan. This judgment is complex, dealing with almost 30 years of uncertainty and we want to get this right. There is also the possibility of an appeal, and the Government has said it intends to publish further guidance. The process will therefore take time.

Once we know more, we will contact all affected members with details. In the meantime, we are conscious that there has been lots of coverage in the national press, not all of it accurate.

How much money am I going to get?

Contrary to much of the press coverage, we expect many individuals to see little or no increase in the value of benefits. There are a few reasons for this:

- GMP often only makes up a small part of an individual’s pension and so the amounts involved in addressing any inequality are likely to be small.

- Many members will receive no increase as in practice they have not been disadvantaged by the way their benefits have been treated.

- Many members won’t have benefits built up within the Plan between 17 May 1990 and 6 April 1997.

Will I need to pay any of my pension back?

No. You will not have to pay back any pension that you have already received following this ruling. Equalisation requires an improvement to the benefits of members who have been disadvantaged – not the other way around.

Why hasn’t this already been dealt with?

The way that GMP works is set out in legislation and is very complicated. Over a number of years, the Government has made suggestions as to how the differences between males and females could be addressed, but it wasn’t clear whether any action was required or whether the possible solutions would work from either a practical or legal perspective. This court case confirms action is required and gives clarity on what schemes can do to put things right going forwards.

Do I need to do anything to claim my benefits?

Not now. We are working with our advisers to identify if and how you are affected. Once we know more, we will get back to you and other members of the Plan with more information. It is the Trustee’s job to make sure you get the benefits you are entitled to and we are working to make sure that this happens. As noted above we expect this to be a long process so please don’t worry if you don’t hear from us for a while.

9AV O N R U B B E R R E T I R E M E N T A N D D E AT H B E N E F I T S P L A N

PensionNews | SPRING 2019

Latest NewsProtect yourself from pension fraudThe Pensions Regulator has recently joined forces with the Financial Conduct Authority in producing a TV advert to renew the awareness campaign. If you haven’t yet seen it, you can watch it online at www.youtube.com/watch?v=NeFvYtCaykI.

The Government is also trying to help tackle the problem by banning cold calling in relation to pensions. It intends regulations to be prepared to come into effect as soon as possible. If you think about it, no one should be making a decision in relation to something as valuable and important as their pension over the telephone with someone who has called them out of the blue.

Remember: only in cases of serious ill health (or if you have a protected pension age) are you able to access your savings before age 55.

If someone approaches you with an offer that sounds too good to be true, know what to look for and what your next steps should be.

If you have any doubts about the legitimacy of any offer you receive, speak to an expert before you sign up for anything.

For more information about pension scams and updated guidance on how you can keep your pension safe, visit the Pensions Regulator’s website. Go to www.thepensionsregulator.gov.uk/individuals/dangers-of-pension-scams

For free impartial guidance, phone the Pensions Advisory Service on 0800 011 3797 or visit their website at www.pensionsadvisoryservice.org.uk.

If you think you may be a victim of a pension scam, contact Action Fraud immediately. Phone 0300 123 2040 or go to their website and fill in an online fraud report.

www.actionfraud.police.uk/report_fraud

Please make use of these resources to help you keep your pension safe.

Financial adviceBefore taking a transfer value, you may wish to seek advice from an Independent Financial Adviser (IFA), who can help you to understand your options. They will require some personal details surrounding your finances and health in order to provide you with the right advice. Indeed, if the transfer value of your DB benefits is more than £30,000 you must take IFA advice from an appropriately qualified and FCA-approved adviser before your transfer value can be paid.To help you choose a suitable IFA, we have set out some things to think about.

1) You should always be sure that they are appropriately qualified to provide pensions transfer advice. Only individuals qualified as a Pension Transfer Specialist can give advice on pension transfers. You should check the adviser has this qualification.

2) Consider the level and experience the adviser has. Look at the service they offer and think about how they will interact with you. Ask them how many transfers from ‘defined benefit’ pension schemes they have advised on.

3) Are you clear on how the IFA will charge for their advice? It is important to make sure that the fees you pay are reasonable. Remember though, that for many people, their pension pot is the most valuable asset they have (even more than their home), so getting professional advice is important. You may want to ask the following questions before you take advice:

• “Can you confirm in pound terms, the fee you receive if I don’t go ahead with the transfer, and the fee you receive if I do go ahead with the transfer?”

• “Can you confirm if you will receive or request any ongoing supplementary fees after my transfer is made, and if so, what these are likely to be in pound terms?”

4) Before proceeding with a transfer, it is important that you understand all of your options. There are likely to be a variety of options available to you if you transfer. For example, you could buy an annuity, take all your pension savings as a one-off cash sum, or choose to take income over a period of time. Your adviser should provide you with a written recommendation as to whether you should transfer, and if they think that you should do so, which option they recommend for you (along with details as to how they have reached their recommendation).

10 AV O N R U B B E R R E T I R E M E N T A N D D E AT H B E N E F I T S P L A N

PensionNews | SPRING 2019

21st century TrusteesThe Pensions Regulator is carrying out a campaign to make clear what their expectations are on those responsible for managing a pension scheme effectively. It is designed to drive up governance standards by being clearer and more directive about the standards it expects of trustees and the action it will take if they do not meet these standards.

The Trustee takes the governance of the Plan very seriously and are reviewing our governance processes to ensure that they remain fit for the 21st century.

The Pensions OmbudsmanUntil recently, the first port of call for free and impartial guidance, including resolving complaints, was the Pensions Advisory Service (TPAS) before Pensions Ombudsman involvement.

Earlier in the year, TPAS transferred its role in the process to the Pensions Ombudsman. This means that all formal disputes that we are not able to deal with within a pension scheme are now dealt with in one place, making the process more efficient for everyone concerned.

To find out more about the Pensions Ombudsman, go to www.pensions-ombudsman.org.uk

New rules on protecting personal data As your Trustee, we hold personal details about you that are essential for running the Plan.

From 25 May 2018 new EU regulation, the General Data Protection Regulation (‘GDPR’), replaces the Data Protection Act. The aims of this new regulation are:

- to give people more say in how their personal information is used; and

- to improve security by standardising the way organisations throughout the EU and use personal information.

While the UK is currently negotiating to leave the EU, it will still be a member when the GDPR comes into effect, so UK organisations will have to comply.

We wrote to you recently to outline how we use your data and the procedures we have in place but please do let us know if you have any concerns on this or have not received this information from us.

11AV O N R U B B E R R E T I R E M E N T A N D D E AT H B E N E F I T S P L A N

PensionNews | SPRING 2019

The Plan’s advisorsAuditor

Banking

Final Salary Administrator & Investment Consultant

Scheme Actuary Susan Hoare FIA

Legal Advisor

Defined Contribution Provider

Investment Managers

Meet the Trustees

Miles Ingrey-Counter(Chairman)

Eric Fielding(Member Nominated)

David Little (Member Nominated)

Rob Wills(Company Nominated)

Zoe Holland(Company Nominated)

Mike Harral(Company Nominated)

INTERNAL DISPUTE RESOLUTION

If you do have any problems with the Plan it is hoped that these can be resolved by the Administrators. If necessary, however, the Trustee Directors have a formal process for dealing with member disputes. Further details of this are available from Mercer or via our website. You may also be able to obtain assistance from the following external bodies:

The Pensions Ombudsman The Pensions Ombudsman has the power to investigate and decide upon complaints and disputes involving occupational pension schemes. He will normally expect to act only when a matter has been through the Plan’s Internal Dispute Resolution Procedure and referred to TPAS and not satisfactorily concluded. The web address is:

www.pensions-ombudsman.org.uk

The Pension Tracing Service The Pension Tracing Service enables ex-members of schemes with pension entitlements, and members’ dependents, who have lost touch with earlier employers.

The web address is: www.gov.uk/find-lost-pension

If you need to contact the Registrar, the telephone number is 0345 6002 537or you can write to The Pension Service 9, Mail Handling Site A, Wolverhampton, WV98 1LU

TRUSTEE REPORT & ACCOUNTSThe Trustee Directors publish a formal Report and Accounts each year that covers some of the items outlined in this newsletter. Please ask Mercer if you would like a copy or a copy of the Funding Review by the Scheme Actuary. You should write to Mercer if you would like to see the Plan’s Trust Deed and Rules or if you want a further copy of the current Members’ Booklet. All of these documents are available on the Plan’s website at:

www.avon-rubber.com/pensions

DEFINED BENEFIT PLAN ADMINISTRATORS

Mercer Consulting Limited, PO Box 505, Chichester, PO19 9AF Member Helpline: 0800 046 6183

Further information If you would like advice about your retirement plans, we recommend you speak with an independent financial adviser (IFA). You can find an adviser in your area by searching the Money Advice Service directory at https://directory.moneyadviceservice.org.uk/en

Before you appoint anyone, you should check that the adviser is suitably qualified and authorised. You can do this online at https://register.fca.org.uk or by phoning the Financial Conduct Authority helpline, 0800 111 6768.

For more general information on pensions and saving for retirement, the following websites are useful resources: www.moneyadviceservice.org.uk

The Money Advice Service provides general advice on all money matters including pensions and finding an independent financial adviser.

www.gov.uk. The Government’s website features a section ‘Working, jobs and pensions’, which includes a State Pension Age calculator.

www.pensionwise.gov.uk. The Government’s guidance website explains the flexible DC retirement options.

If you have a concern about your benefits, contact the Early Resolution Team: Go to www.pensions-ombudsman.org.uk/our-service/make-a-complaint. Phone: 0800 917 4487 and select the option to discuss a potential complaint. Email: [email protected]

MONEY PURCHASE PLAN ADMINISTRATORS

Standard Life, Dundas House, 20 Brandon Street, Edinburgh, EH3 5PP Member Helpline: 0800 634 7479

12 AV O N R U B B E R R E T I R E M E N T A N D D E AT H B E N E F I T S P L A N

PensionNews | SPRING 2019