Embed Size (px)

Citation preview

The Financial Advisor Guide to Money Laundering

Self Study Course # 25

COURSE DESCRIPTIONThis course introduces the Financial Advisor to money laundering. It will help you

understand what money laundering is and provide you with information on how to

identify probable money laundering activities. You will also learn how to protect you,

your clients and your associates.

In addition, you will learn about current Money laundering regulations and your

obligations to comply under existing and future legislation.

INTRODUCTIONThere is little doubt that narcotics trafficking and other organized criminal conspiracies

generate billions of dollars annually. Cash is the universally accepted mode of payment

in the underground economy and, as a result, criminal entrepreneurs – in particular drug

traffickers – accumulate cumbersome amounts of currency, often in small

denominations. A daunting task that confronts profitable criminal entrepreneurs is how

to spend, invest, or transfer large amounts of cash, without attracting suspicion.

Money laundering is a necessity if cash-intensive criminal entrepreneurs are to

maximize their ability to use and enjoy the fruits of their illegal activity without attracting

suspicion and/or government action. Within the criminal milieu, money laundering has

taken on a life of its own and has become an integral component in the operations of

criminal organizations, in part because of the dogged pursuit of illicit funds by law

enforcement agencies.

In recent years, money laundering has been highlighted as an emerging problem both in

Canada and internationally. In Canada, it is estimated that the amount of money

laundered on an annual basis is somewhere between $5 and $15 billion. Worldwide, it

has been estimated that this figure may be as high as $1 trillion in U.S. currency.

In 2009, Canadian police services substantiated 525 incidents of money laundering,

accounting for about 1% of all police-reported Criminal Code incidents.

−2−Financial Advisors Guide to Money laundering SSC #25

Pro-Seminars International © 12/11

Expressed as a rate, there were approximately two police-reported incidents of money

laundering for every 100,000 Canadians.

Over the past 10 years, the rate of money laundering incidents reported by police has

changed considerably. Following a period of relative stability in the early part of the

decade, the rate of money laundering grew five-fold from 2004 to 2006.

DEFINITION OF MONEY LAUNDERINGMoney laundering can be broadly defined as a process by which cash and other assets

derived from illegal activity are disbursed for the purpose of concealing or disguising

their criminal origin.

A comprehensive money laundering operation satisfies three objectives: (1) it converts

the cash proceeds of crime to another, less suspicious form, (2) it conceals the criminal

origins and ownership of the funds and/or assets, and (3) it creates a legitimate

explanation or source for the funds and/or assets.

According to the Criminal Code, money laundering, also referred to as laundering the

proceeds of crime, occurs when an individual or group uses, transfers, sends, delivers,

transports, transmits, alters, disposes of or otherwise deals with, any property or

proceeds that was obtained as a result of criminal activity. This is done with the intent

to conceal or convert illegal assets into legitimate funds.

THE PROCESSTo realize the greatest benefit from money laundering, criminally-derived cash should

not simply be converted to other, less suspicious assets; the illicit financing of the

assets must also be hidden. The third objective (creating a legitimate explanation),

while less frequently satisfied in most money laundering operations, is no less important

than the former two: the effectiveness of a laundering scheme will ultimately be judged

by how convincingly it creates a legitimate front for illegally-acquired cash and assets.

−3−Financial Advisors Guide to Money laundering SSC #25

Pro-Seminars International © 12/11

In short, “money is not truly laundered unless it is made to appear sufficiently legitimate

so that it can be used openly, precisely what the final stage of the cycle is designed to

achieve.” Moreover, one of the keys to satisfying the objectives of the laundering

process is to conduct commercial and financial transactions that appear as legitimate as

possible. The more successful a money laundering operation is in emulating the

patterns of legitimate financial or commercial transactions, the less suspicion it will

attract.

In order to satisfy the above objectives, the money laundering process generally entails

four stages: placement, layering, integration, and repatriation.

The initial placement stage is where the cash proceeds of crime physically enter the

legitimate economy, which satisfies the first objective of the laundering process. Once

the funds have been placed in the legitimate economy, a process of layering takes

place.

It is during this stage that much of the laundering activity takes place, as funds are

circulated through various economic sectors, companies, and commercial or financial

transactions in order to conceal the criminal source and ownership of the funds and

obscure any audit trail. The penultimate step of the money laundering process is

termed integration because “having been placed initially as cash and layered through a

number of financial operations, the criminal proceeds are fully integrated into the

financial system and can be used for any purpose.”

The final stage of the process involves repatriating the laundered funds into the hands

of the criminal entrepreneur, ideally with a legitimate explanation as to their source, so

that they can be used without attracting suspicion.

The placement stage is the most perilous for the launderer as it involves the physical

movement of bulk cash, usually in small denominations. It is at this stage that the

offender is most vulnerable to suspicion and detection and where the funds can most

easily be tied to criminal sources. −4−

Financial Advisors Guide to Money laundering SSC #25Pro-Seminars International © 12/11

Once the funds are placed with the legitimate economy and converted from their original

cash form, the opportunities for money laundering increase exponentially: the funds can

transferred among, and hidden within dozens of financial intermediaries and commercial

investments, domestically and internationally.

SOURCES OF FUNDSAccording to RCMP data (which examined approximately 150 recent cases of money

laundering), drug trafficking accounts for seventy two percent of all offenses relating to

laundered money – making it the single largest source of “laundered” proceeds.

Customs and excise offences (e.g., the smuggling and distribution of contraband

cigarettes and liquor) are next in line (15.4% of cases). Theft and fraud accounted for

7.4% of offences.

SECTORS OF THE ECONOMY USED TO LAUNDER FUNDSMultiple sectors of the economy are often used to launder money. The most significant

sectors of the economy used for laundering purposes – in terms of both frequency and

volume - are deposit institutions and real estate. Deposit institutions are used in 76.5%

of cases while real estate transactions are involved 55.7% of cases.

The service used most frequently at a deposit institution for money laundering purposes

was a savings or chequing account.

Other commonly used products and services were bank drafts, mortgages, safety

deposit boxes, and wire transfers.

The proceeds of crime found their way into the real estate sector in the form of

mortgages, cash, and monetary instruments. According to RCMP data, a mortgage is

used in slightly less than three quarters of cases involving real estate, and cash

generated directly from illegal activities is used to finance the purchase of real property

slightly more than three quarters of the time. Cash was generally used for the deposit,

down payment, or mortgage payments, although in some cases real property was

wholly purchased with cash. −5−

Financial Advisors Guide to Money laundering SSC #25Pro-Seminars International © 12/11

The insurance sector was also implicated in about two thirds of money laundering

cases, but in most of these, insurance was not used explicitly as a laundering vehicle –

instead insurance was purchased to cover big ticket assets (financed with the proceeds

of crime). Motor vehicles were purchased or leased with the proceeds of crime with

some regularity and in roughly a third of cases, companies are established or

purchased by offenders to facilitate the laundering process.

While, the insurance sector was somewhat tangential to the actual money laundering

objectives and processes, in most cases, police cases also show that traditional

services offered by the insurance industry – such life insurance policies – have also

been used expressly to launder the proceeds of crime. According to a 1998 report,

entitled Money Laundering Typologies, the Financial Action Task Force (FATF), single

premium insurance contracts are often purchased from insurance companies and then

redeemed prior to their full term at a discount. The balance is paid to the launderer in

the form of a “sanitized” cheque from the insurance company, thereby creating a

seemingly legitimate source for the funds.

In a small number of cases, the insurance sector is used much like a bank: cash is

deposited into accounts or term deposits; investments – such as RRSPs and mutual

funds – are purchased; and mortgage financing is received. As the barriers that

separate the different financial sectors continue to crumble in Canada, insurance

companies are increasingly providing the type of banking services favoured by money

launderers.

As noted above, in the course of a single money laundering operation, a number of

different sectors will often be used. Moreover, when used for money laundering

purposes, these sectors are not mutually exclusive, but critically interconnected: one

sector of the economy, such as deposit institutions, will frequently be used to access

other sectors, such as real estate.

−6−Financial Advisors Guide to Money laundering SSC #25

Pro-Seminars International © 12/11

Both operating and shell companies are often established to facilitate the laundering

process. No one type of business, however, is predominant. Collectively, money

laundering companies operate (or purported to operate) in various lines of commerce,

including currency exchange, retail fish sales, masonry, paving, painting, auto

wholesaling, auto leasing, lumber supplies, fitness clubs, courier services, gas stations,

hotels, restaurants, and bars, etc.

MONEY LAUNDERING TECHNIQUESThe techniques used to facilitate the laundering process generally involve attempts to

hide the true ownership and source of criminal proceeds (through the use of nominees),

avoid suspicion associated with large amounts of cash (by using “smurfs”), circumvent

reporting requirements (by structuring transactions), or create the perception that the

criminal funds were derived from legitimate sources (e.g., establishing companies and

then claiming the proceeds of crime as legitimate revenue). Each of these techniques is

discussed in more detail below.

NomineesThe most common technique used in conjunction with money laundering was the use of

nominees. Close to one half of money laundering cases involved some attempt by the

accused to obscure a direct connection between himself and assets he owned, primarily

by registering legal title to the asset in the name of another individual, usually a relative,

a friend, business associate, or a lawyer. In most cases, the nominee is unconnected to

the criminal activities and has no criminal record. The assets most often placed in the

name of nominees were real estate, cars, companies, and banks accounts.

SmurfsAbout 20% of the time a money laundering technique known as smurfing is used. A

“smurf” is an individual used by a criminal enterprise to attend numerous banks or other

financial service providers and perform, at each, transactions with a relatively small

amount of cash.

−7−Financial Advisors Guide to Money laundering SSC #25

Pro-Seminars International © 12/11

Used primarily during the placement stage of the laundering process to circumvent

mandatory reporting requirements and avoid the suspicion associated with large

amounts of cash, each smurf is instructed to deposit less than $10,000 at a time.

Larger criminal organizations may utilize a number of smurfs as part of an elaborate

money laundering effort. The objective of this laundering technique is to avoid

transactions involving large amounts of cash by spreading the funds among a sizeable

number of individuals, financial institutions, and accounts. In the context of money

laundering, the term “smurf” was derived from the blue cartoon characters, all of whom

are innocuous in appearance (a characteristic of nominees that is highly valued by

money launderers).

StructuringStructuring is used to facilitate the laundering process in one out of every seven cases.

Structuring refers to a process whereby large cash deposits and other transactions are

broken down into smaller amounts to avoid the suspicion associated with large amounts

of cash. Structuring is most commonly practiced at banks and similar financial service

providers and is an integral part of smurfing. Then need for structuring as part of the

money laundering process is heightened in Canada since legislation requires the

financial services sector to record and report most cash transactions over $10,000.

LayeringLayering involves efforts to distance the illicit proceeds from their source, while

obstructing any audit trail by creating several “layers” of financial and commercial

transactions and/or assets.

Specifically, layering is accomplished by either conducting multiple transactions with the

illicit funds or by setting up complex hierarchies of assets in order to put as much

distance between the laundered assets and their original source of funding. The

layering stage is often the backbone of the money laundering process.

−8−Financial Advisors Guide to Money laundering SSC #25

Pro-Seminars International © 12/11

Claiming the Proceeds of Crime as Legitimate RevenueOne of the techniques used frequently to satisfy the third objective of the laundering

process –creating the perception that the criminal proceeds were derived from a

legitimate source – is to claim the proceeds of crime as revenue from a legal business.

Once this seemingly lawful source of revenue is established, criminal proceeds can be

deposited into bank accounts under the guise of this business. In some cases, the

proceeds of crime will be co-mingled with revenues generated from legal businesses

and deposited into bank accounts.

THE ROLE OF PROFESSIONALSIn the vast majority of money laundering schemes, the money launderer or an

accomplice conducts a transaction with a company in the legitimate economy and as

such, they make contact with a professional. The professionals that most frequently

came into contact with the proceeds of crime were deposit institution staff, lawyers,

insurance agents or brokers, and real estate professionals. In the majority of these

cases, the professionals were unwittingly used to facilitate the money laundering

process, although, in some cases, the circumstances surrounding the transaction

should have raised some suspicions. While lawyers were implicated in almost half of

the proceeds of crime cases, the nature of the transactions they conducted suggest that

they were not expressly sought out by offenders to facilitate money laundering. Instead,

most lawyers came into contact with illegally-generated funds because the transaction

conducted by the offender – most notably, the purchase or sale of real estate –

commonly requires the services of a lawyer.

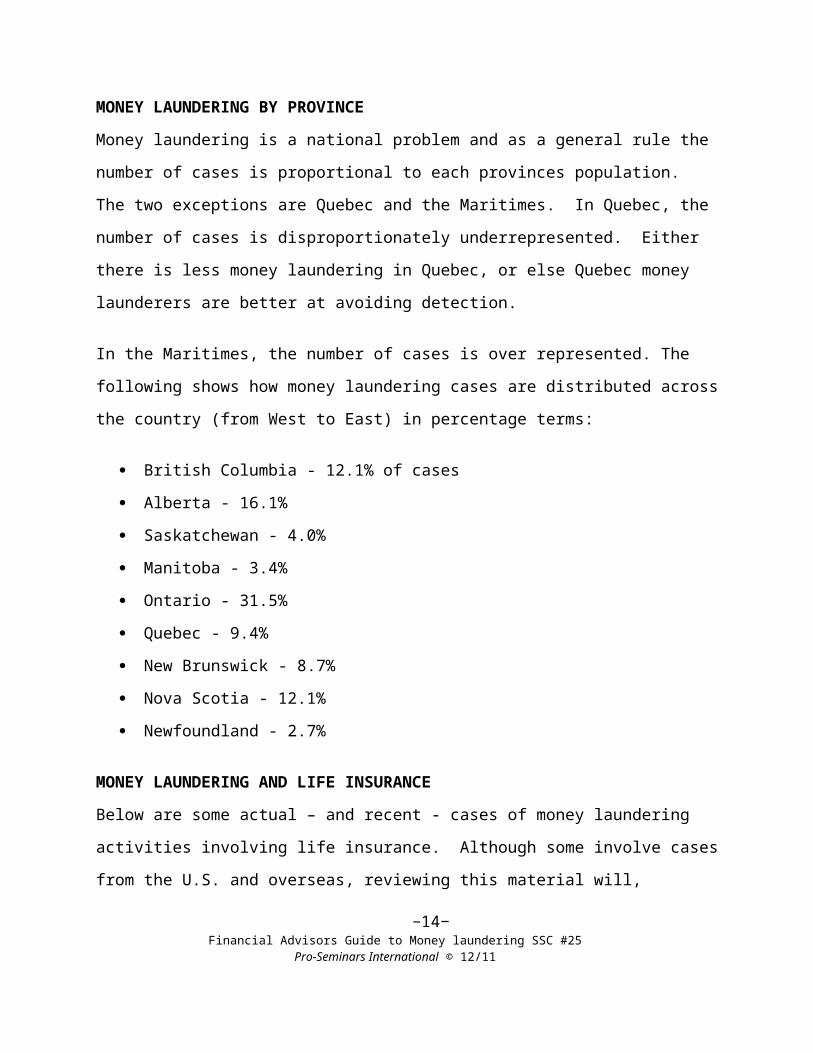

MONEY LAUNDERING BY PROVINCEMoney laundering is a national problem and as a general rule the number of cases is

proportional to each provinces population. The two exceptions are Quebec and the

Maritimes. In Quebec, the number of cases is disproportionately underrepresented.

Either there is less money laundering in Quebec, or else Quebec money launderers are

better at avoiding detection.

−9−Financial Advisors Guide to Money laundering SSC #25

Pro-Seminars International © 12/11

In the Maritimes, the number of cases is over represented. The following shows how

money laundering cases are distributed across the country (from West to East) in

percentage terms:

British Columbia - 12.1% of cases

Alberta - 16.1%

Saskatchewan - 4.0%

Manitoba - 3.4%

Ontario - 31.5%

Quebec - 9.4%

New Brunswick - 8.7%

Nova Scotia - 12.1%

Newfoundland - 2.7%

MONEY LAUNDERING AND LIFE INSURANCEBelow are some actual – and recent - cases of money laundering activities involving life

insurance. Although some involve cases from the U.S. and overseas, reviewing this

material will, nonetheless, help you to identify some of the situations that suggest

money laundering activities.

An individual attempted to purchase life policies for a number of foreign nationals. He requested life coverage with a high surrender value relative to the

premium paid. There were also indications that in the event that the policies

were cancelled, any money returned was to be paid into a bank account in a

different jurisdiction.

A drug trafficker deposited funds into several bank accounts and then transferred the funds to an account in a foreign jurisdiction. The drug

trafficker then purchased a large life insurance policy and payment for the policy

was made by two separate wire transfers from the foreign account.

−10−Financial Advisors Guide to Money laundering SSC #25

Pro-Seminars International © 12/11

It was purported that the funds used for payment were the legitimate proceeds of

overseas investments.

Over a million dollars of questionable funds was deposited in a bank account. The “layering process” involved the purchase of large high cash value

insurance policies. In this process, the insurance agent became a top producer

at his insurance company and later won a company award for his sales efforts.

The insurance agent’s supervisor was also involved in the scheme. Both were

charged and convicted. This case has shown how money laundering, coupled

with corrupt employees, can expose an insurance company to both negative

publicity and criminal liability.

Customs officials initiated an investigation which identified narcotics trafficking organisation buying insurance products with the rate of return tied

to the major world stock market indices so the insurance policies were able to

perform as investments. The account holders would over-fund the policy, moving

monies into and out of the fund for the cost of the penalty for early withdrawal.

The funds would then emerge as a wire transfer or cheque from an insurance

company and the funds therefore appeared to be clean. Over 29 million dollars

was laundered through this scheme.

A person (later arrested for drug trafficking) made a financial investmentby means of an insurance broker. He delivered a total amount of $250,000 in

three cash instalments. The insurance broker did not report the delivery and

deposited the three instalments in the bank. These actions raise no suspicion at

the bank, since the insurance broker was known to them and was connected to a

reputable insurance operation. The insurance broker then delivered three

cheques – payable to the insurance company - from the bank account under his

name - thus avoiding raising any suspicions from the insurance company

−11−Financial Advisors Guide to Money laundering SSC #25

Pro-Seminars International © 12/11

Clients in several countries used the services of an intermediary to purchase insurance policies. Identification was taken from the clients, but

these details could not be clarified by the insurance company which was reliant

on the intermediary doing due diligence checks. The policies were put in place

and the relevant payments were made by the intermediary. Then, after a couple

of months had passed, the institution would receive notification from the clients

stating that there was now a change in circumstances, and they would have to

cancel their policies and suffer the penalties. Despite the penalties, the criminals

involved received “clean” and substantial cheques from the institution.

Another simple method by which funds can be laundered is taking out a large insurance contract and then “accidentally,” but on a recurring basis,

significantly over pay the premiums due and then request a refund for the

excess. Often, the person does so in the belief that his relationship with the

company is such that no one will dare confront a longstanding and profitable

customer.

COMPLIANCE GUIDELINESThe following material will provide you with an overview of the Proceeds of Crime

(money laundering) and Terrorist Financing Act. This material will assist you in

developing a “knowledge base” from which you can exercise your judgement in carrying

out your obligation to report suspicious activity related to a money laundering or terrorist

activity financing offence.

The Act was passed on June 29, 2000 and amended in December 2001 to include

provisions dealing with the financing of terrorism. It was amended further in December

2006 and again on June 23, 2008.

The legislation’s intent is to strengthen Canada’s efforts in the fight against transnational

crime – specifically money laundering and the financing of terrorist activities.

−12−Financial Advisors Guide to Money laundering SSC #25

Pro-Seminars International © 12/11

The Act is divided into six parts. They are as follows:

Part 1 - Identifies the groups and individuals to which the Act applies and sets out the

reporting requirements.

Part 2 - Sets out the requirements to report certain currency and monetary instruments

for the amounts indicated in the regulations.

Part 3 - Establishes the Financial Transactions and Reports Analysis Centre of Canada

(FINTRAC) to which reports are made.

Part 4 - Provides for the creation of regulations.

Part 5 - Details the offences and punishments for failure to comply with the reporting

and record keeping provisions.

Part 6 - Provides for the transition from the previous legislation to the current Act.

The Act makes it mandatory for various individuals and entities, including life insurance

agents and brokers, to report a variety of transactions to the Financial Transaction and

Reports Analysis Centre of Canada (FINTRAC). The mandatory reporting is designed

to assist in the detection and deterrence of money laundering and terrorist financing

activities as well as to facilitate the investigation and prosecution of money laundering

and terrorist activity financing offences.

−13−Financial Advisors Guide to Money laundering SSC #25

Pro-Seminars International © 12/11

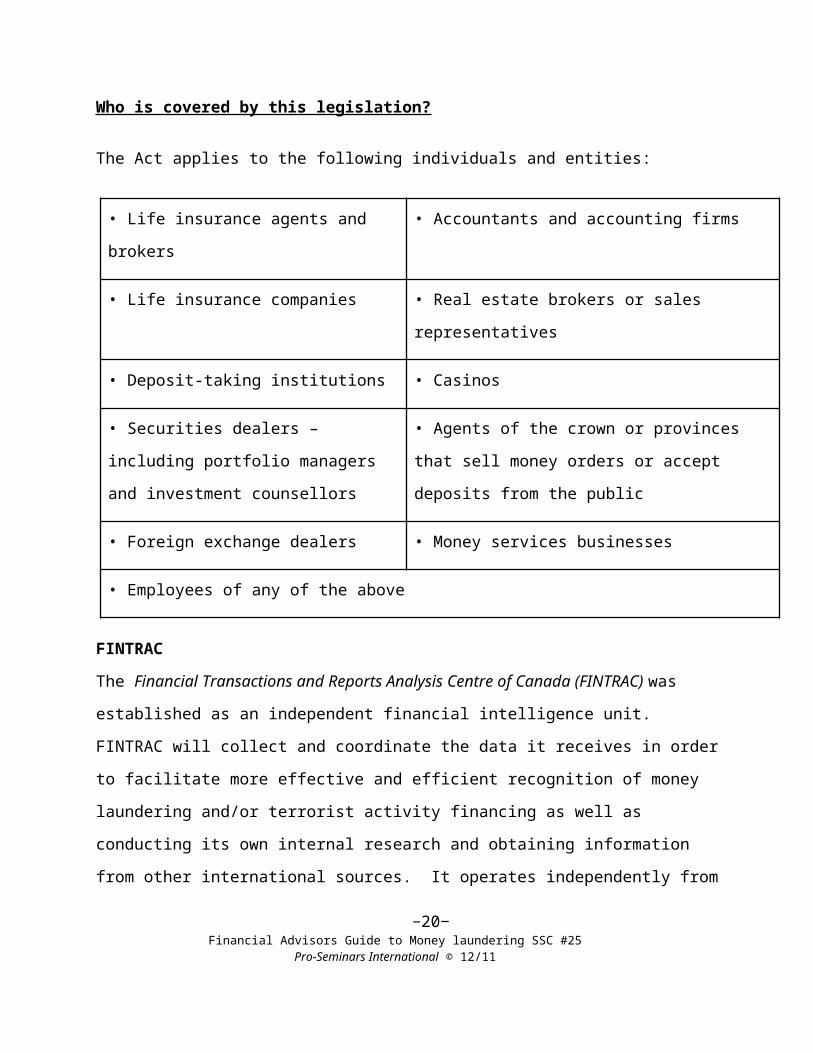

Who is covered by this legislation?

The Act applies to the following individuals and entities:

• Life insurance agents and brokers • Accountants and accounting firms

• Life insurance companies • Real estate brokers or sales representatives

• Deposit-taking institutions • Casinos

• Securities dealers – including portfolio

managers and investment counsellors

• Agents of the crown or provinces that sell money

orders or accept deposits from the public

• Foreign exchange dealers • Money services businesses

• Employees of any of the above

FINTRACThe Financial Transactions and Reports Analysis Centre of Canada (FINTRAC) was

established as an independent financial intelligence unit. FINTRAC will collect and

coordinate the data it receives in order to facilitate more effective and efficient

recognition of money laundering and/or terrorist activity financing as well as conducting

its own internal research and obtaining information from other international sources. It

operates independently from law enforcement agencies even though part of its mandate

is to assist in the detection and deterrence of money laundering and the financing of

terrorist activity in Canada and around the world.

FINTRAC also has the primary responsibility to ensure entities, such as life insurance

agents and brokers comply with the Act and its requirements. FINTRAC has the

authority to inquire into any life agents or brokers business and examine their records to

ensure compliance with the Act.

−14−Financial Advisors Guide to Money laundering SSC #25

Pro-Seminars International © 12/11

FINTRAC’s mandate also includes increasing the public’s awareness and

understanding of money laundering and it will issue periodic reports on the usefulness

of information it has received.

What does FINTRAC do with the Information reported? If FINTRAC determines, based on its analysis and assessment, that there are

reasonable grounds to suspect that the information reported would be relevant to the

investigation or prosecution of a money laundering or terrorist activity financing offence,

it will disclose this information to the appropriate police force.

If the police force wants more information than what FINTRAC has provided, it must

obtain a court order.

FINTRAC may also disclose this same information to other government agencies if

certain key conditions have been met. Some of the other government agencies and

some examples of the additional criteria that must be met are:

Canada Revenue Agency (CRA) – if FINTRAC determines that information is

also relevant to an offence of evading or attempting to evade paying taxes or

duties imposed under an Act of Parliament administered by the Minister of

National Revenue.

Canadian Security Intelligence Service (CSIS) – If FINTRAC determines that

the information is also relevant to threats to the security of Canada within the

meaning of the Canadian Security Intelligence Service Act.

Canada Border Services Agency, if FINTRAC determines that the information

is also relevant to determining whether a person is a person described in section

34 to 42 of the Immigration and Refugee Protection Act (the IMRPA) or is

relevant to an offence under any sections the IMPRA.

FINTRAC may also disclose the designated information to other Financial Intelligence

Units where an information-sharing agreement is in place called “Memorandum of

Understanding.” −15−

Financial Advisors Guide to Money laundering SSC #25Pro-Seminars International © 12/11

Protection of PrivacyThe Act requires FINTRAC to respect individual privacy and to protect confidential

information. Some of the safeguards intended to protect the privacy of individuals are:

Independence of FINTRAC from law enforcement and other government

agencies,

Significant criminal penalties for unauthorized use or disclosure of personal

information

That only limited designated information may be disclosed to law Enforcement

and only once FINTRAC has determined that there are reasonable grounds to

suspect that the information would be relevant to the investigation or prosecution

of a money laundering offence or a terrorist activity financing offence

The requirement that certain designated law enforcement and government

agencies have to get a Production Order to obtain more than the designated information

The fact that FINTRAC is subject to the federal Privacy Act.

FINTRAC’S AUTHORITY The Act authorizes FINTRAC to enter, at any reasonable time, any individual’s or

entity’s business premises without a warrant. The only time a warrant may be required

is when the individual’s or entity’s business premises are in a dwelling house.

The owner or person in charge of the business premises and every person found there

are required to give the authorized person all reasonable assistance to enable them to

carry out their responsibilities. They are also required to furnish them with any

information with respect to the Act.

A failure to assist a compliance officer (authorized person) in their effort could, upon

conviction, can lead to up to five years imprisonment and/or a fine of $500,000.

FINTRAC’s Approach to Compliance Monitoring

−16−Financial Advisors Guide to Money laundering SSC #25

Pro-Seminars International © 12/11

FINTRAC favours a co-operative approach to monitoring. The emphasis will be on

working with life insurance agents and brokers to achieve compliance with the Act and

regulations. As a general rule, when compliance issues are identified, FINTRAC will

work with the life insurance agents and brokers in a constructive manner to find

reasonable solutions. If these efforts are not successful or the breach is particularly

egregious, FINTRAC may refer non-compliance cases to the appropriate law

enforcement agencies.

YOUR OBLIGATIONS The following is a summary of the legislative requirements under the Act applicable to

life insurance companies, brokers or independent agents. If you are a life insurance

agent and an employee of a life insurance company or broker, these requirements are

the responsibility of the life insurance company except with respect to reporting

suspicious transactions and terrorist property, which is applicable to both.

All of the following areas will be discussed below: mandatory compliance, mandatory

reporting, suspicious transactions, large cash transactions, terrorist property, record

keeping, ascertaining identity, and penalties.

MANDATORY COMPLIANCE All individuals and entities covered under the Act are required to have a compliance

regime. The compliance regime is intended to ensure compliance with all obligations

under the Act. Although you may never have to file a report, you will still have to put a

compliance regime in place. The compliance regime is statutory required – it is not an

option.

The following five requirements must be met:

1. The appointment of an individual (the compliance officer) who is to be

responsible for the implementation of the regime. A sole practitioner may serve

−17−Financial Advisors Guide to Money laundering SSC #25

Pro-Seminars International © 12/11

as the compliance officer.

2. The development and application of compliance policies and procedures. These

policies and procedures have to be written and kept up to date. If you are an

entity, they also have to be approved by a senior officer.

3. An assessment and documentation of risks related to money laundering and

terrorist activity financing. Where there is a high risk, special measures must be

taken for identifying clients, keeping records and monitoring financial transactions

in respect of the activities that pose the high risk.

4. A review, as often as is necessary, but at least every two years, of those policies

and procedures to test their effectiveness, to be conducted by an internal or

external auditor, where the person or entity has one, or by the person or entity

itself, where it does not have an internal or external auditor.

5. If you have employees or agents or any other individuals authorized to act on

your behalf, the implementation of an on-going compliance training program is

required for them and it has to be in writing and maintained.

Implementation of a compliance regime is a requirement as well as a good business

practice for anyone subject to the Act and regulations. A well-designed, applied and

monitored regime will provide a solid foundation for compliance with the legislation.

FINTRAC recognizes that not all individuals or entities operate under the same

circumstances, hence compliance regimes should be tailored to fit individual and entity

needs and should consider the nature, size, and complexity of operations.

Although there is some “flexibility”, your program has to contain all five elements

describe above.

Appointment of a Compliance OfficerThe appointed compliance officer should have the authority and the resources

−18−Financial Advisors Guide to Money laundering SSC #25

Pro-Seminars International © 12/11

necessary to discharge his/her responsibility effectively. Depending on the type of

business, the compliance officer should report to the Board of Directors or senior

management or to the owner or chief operator. You can also appoint yourself if your

business is small.

To ensure consistent and ongoing attention to the compliance regime, the compliance

officer may choose to delegate certain duties to other employees. Even though the

compliance officer may wish to delegate some of these duties, the compliance office

remains responsible for overall compliance.

Individuals who are subject to the Act may appoint themselves as “compliance officer”

or may choose to appoint another individual to help them implement the compliance

regime.

The Act covers life insurance agents and brokers as a profession – as individuals, as

firms or members of firms and as partners in a partnership.

This means individual practitioners in a firm or partnership will be responsible to make

sure that their reporting obligations are met when it relates to any life insurance

transaction they may be involved with.

Establishing Compliance Policies and ProceduresAn effective compliance regime is a commitment by each life insurance agent and

broker to institute policies and procedures to prevent, detect, and address non-

compliance with the Act and the regulations.

The formality of the policies and procedures will depend on the degree of detail,

specificity and formality of the regime, the complexity of the issues and transactions that

you are involved in or will be involved in as well as the risk of exposure to money

laundering and terrorist activity financing.

−19−Financial Advisors Guide to Money laundering SSC #25

Pro-Seminars International © 12/11

The policies and procedures should provide you and/your personnel with enough

information to properly process and complete a transaction.

They should also provide a clear definition of roles and responsibilities for identifying

reportable transactions, record keeping, record retention, and completing and filing of

reports. You should consider what is necessary to ensure compliance with the

requirements when assessing what specific policies and procedures should be

implemented. The scope of policies and procedures will vary depending on the type

and size of business you have.

Assessment and Documentation of RisksYou must take a risk-based approach to assessing and documenting the risks related to

money laundering and terrorist activity financing. You have to assess and document

the risks by considering the following factors:

1. Your products and services and the delivery channels through which you offer

them,

2. The geographic locations where you conduct your activities and the geographic

locations of your clients,

3. Other relevant factors related to your business,

4. Your clients and the business relationships you have with them.

If you consider the risk of a money laundering offence or a terrorist activity financing

offence to be high, the risk has to be mitigated by adopting prescribed special measures

for identifying clients, keeping records and monitoring such life insurance transactions.

The special measures that are required to be taken when the risk is high include the

development and application of written policies and procedures for:

taking reasonable measures to keep client identification information up to date,

taking reasonable measures to conduct ongoing monitoring for the purpose of

detecting transactions that are required to be reported to FINTRAC, &

−20−Financial Advisors Guide to Money laundering SSC #25

Pro-Seminars International © 12/11

mitigating the risks identified.

Review of Compliance Policies and ProceduresThe Act calls for a mandatory review of the policies and procedures program. The

review allows you to monitor the effectiveness of your compliance regime and evaluate

the need to modify existing policies and procedures if necessary or implement new

ones. The compliance review should be conducted as often as necessary but must be

carried out every two years. Some factors to consider that would prompt a need for a

review are changes in the legislation, non-compliance issues, or new services and

products being offered beyond life insurance. The review must be conducted by either

an internal or external auditor. If you do not have an internal or external auditor, you

can do a “self-review” or have another outside party conduct the review. Whenever

possible, the review should be conducted by an individual who is independent of the

reporting, record keeping, and compliance monitoring so as to maintain objectivity.

Within thirty days after the assessment, the following is required to be reported in writing

to a senior officer:

the findings of the review,

any updates made to the policies and procedures within the reporting period,

the status of the implementation of the updates to policies and procedures.

While not specifically required under the Act, it would be good business practice to

document the scope and results of the review. Deficiencies and weaknesses that

appear should be identified and reported to the senior management.

The report should also include a request for a response indicating corrective measures

and follow-up actions as well as a time-line for implementing such actions.

Ongoing Compliance TrainingThe success of a compliance regime is highly dependent on adherence. Only when you

and/your staff are made aware of the requirements and responsibilities will you and/or

−21−Financial Advisors Guide to Money laundering SSC #25

Pro-Seminars International © 12/11

they be able to contribute to the program. On-going training is essential to maintaining

a sound compliance regime.

All individuals should be generally familiar with the legislation and regulations and

should receive training in areas directly affecting their responsibilities. They must also

be trained in policies and procedures the entity or individual adopts to ensure

compliance with legal obligations.

Periodic training will help ensure adherence to policies and procedures. The method of

training may vary greatly depending on your business’ size, time requirements, and the

complexity of the subject matter.

When assessing training needs, individuals and entities subject to the Act should

consider the following elements:

Legislative and regulatory requirements and related liabilities – the training

should provide an understanding of the legislative and regulatory requirements

as well as the liabilities under the Act and applicable regulations,

Policies and procedures – the training should provide awareness of the internal

policies and procedures for deterring and detecting money laundering that are

associated with the job. It should also provide a concrete understanding of

responsibilities,

Background information on money laundering and terrorist activity financing – any training program should include some background information

on money laundering and terrorist activity financing to ensure that money

laundering and terrorist activity financing are understood. Staff also need to

understand why criminals choose to launder money, and how the process usually

works.

−22−Financial Advisors Guide to Money laundering SSC #25

Pro-Seminars International © 12/11

MANDATORY REPORTING REQUIREMENTSThe requirement to report is set in motion when a transaction occurs. In other words,

the moment a deposit is received, you must consider whether it is large enough or

suspicious enough to report.

If a sales representative receives an amount in cash of $10,000 or more it must be

reported within 15 days.

You must also be aware of cross border transactions. All cross border transactions of

$10,000 or more must be reported when they occur (note: cheques, drafts and money

orders are not included in this requirement).

There is no minimum dollar threshold for reporting suspicious transactions or attempted

transactions. Suspicious transactions must be reported within 30 days.

The Act has three sections that deal with mandatory reporting requirements that are

applicable to the life insurance industry:

1. Suspicious transaction or attempted transaction reporting,

2. Large cash transaction reporting,

3. Terrorist group and listed person property reporting.

Life insurance agents and brokers are covered as a “reporting entity” under the

legislation.

SUSPICIOUS TRANSACTIONS OR ATTEMPTED TRANSACTIONSOfficially, a suspicious transaction is a financial transaction where there are reasonable

grounds to suspect a link to money laundering.

It is important to understand that no minimum amount is set in identifying a suspicious

transaction. You have to trust your own judgement! If a transaction or a series of

transactions raises questions or gives rise to discomfort, apprehension or mistrust, then

seriously consider whether it might be a suspicious transaction.−23−

Financial Advisors Guide to Money laundering SSC #25Pro-Seminars International © 12/11

As was mentioned already, no minimum monetary value helps identify a suspicious

transaction. Cash amounts of $10,000 or more must be reported, but all suspicious

amounts under $10,000 must also be reported. In other words, the amount of the

transaction is not the only indicator. Essentially, the Act is meant to address all types of

transactions and amounts.

The Suspicious Transaction or Attempted Transaction Report (STATR) The Act requires you to submit a Suspicious Transaction or Attempted Transaction

Report (STATR) if you have reasonable grounds to suspect that the transaction or

attempted transaction is related to a money laundering or terrorist activity financing

offence. The reporting of suspicious activity will require you, or your staff, to exercise

judgement.

The key questions to be asked are: “What constitutes a suspicious transaction or

attempted transaction?” and “What are reasonable grounds?” There are no easy

answers. It is expected that through training (this course being an example), you will

develop the judgement necessary to answer these key questions for yourself and

thereby fulfil your legal obligations under the Act.

Two important factors to understand concerning your obligation to report a suspicious

transaction or attempted transaction under the Act are:

1. You are required to take reasonable measures to ascertain the identity of the

person with whom the suspicious transaction or attempted transaction is being or

has been conducted, unless you believe it would inform the person that the

transaction or attempted transaction and related information is being or would be

reported.

−24−Financial Advisors Guide to Money laundering SSC #25

Pro-Seminars International © 12/11

2. The transaction or attempted transaction has to occur in the course of your

activities as a life insurance broker or agent.

Recognizing Suspicious TransactionsWhen looking at a transaction or attempted transaction with a view towards deciding

whether it is suspicious, remember that behaviour is suspicious, people aren’t.

It is the consideration of many factors which will lead you to conclude that there are

reasonable grounds to suspect that the transaction or attempted transaction is related to

the commission of a money laundering or terrorist activity financing offence.

What constitutes “reasonable grounds” must be decided in the context of what is

reasonable under the circumstances, such as normal business practices and

procedures within the client’s industry, profession or environment.

You must look at the overall picture and consider some of the following factors:

Your knowledge of the client.

Your knowledge of the client’s industry.

The context of the transaction - is it normal?

Your understanding of money laundering and terrorist activity financing.

When looking at the context of the transaction and what is normal, think of the following

example. Would you consider it normal for a client to buy a whole life policy based on a

needs analysis? The answer is probably yes. Would you consider it normal for a whole

life policy buyer to be more interested in early redemption features than financial

security needs? Probably not. As you can see the same insurance transaction can be

normal in one circumstance, but not in another.

General Indicators of Suspicious Transactions or Attempted Transactions

−25−Financial Advisors Guide to Money laundering SSC #25

Pro-Seminars International © 12/11

The following is a sample of some general indicators that might lead a life insurance

agent or broker to suspect that a transaction or attempted transaction is related to

money laundering or terrorist activity financing. It will not be just one of these factors

alone – that will trigger suspicion - but a combination of several factors in conjunction

with what is normal and reasonable in the circumstances of the transaction or attempted

transaction.

Client admits to or makes statements about involvement in criminal activities.

Client does not want correspondence sent to home address.

Client appears to have accounts with several financial institutions in one area for

no apparent reason.

Client repeatedly uses an address but frequently changes the name involved.

Client is accompanied and watched.

Client shows uncommon curiosity about internal controls and systems.

Client presents confusing details about the transaction.

Client makes inquiries that would indicate a desire to avoid reporting.

Client is involved in unusual activity for that individual or business.

Client insists that a transaction be done quickly.

Client seems very conversant with money laundering or terrorist activity financing

issues.

Client refuses to produce personal identification documents.

“Life Industry” Specific Indicators of Suspicious Transactions or Attempted Transactions The following is a sample of some of the life insurance industry specific indicators that

might lead you to suspect that a transaction is related to a money laundering or terrorist

activity financing offence. It will not be just one of these factors alone, but a

combination of several factors in conjunction with what is normal and reasonable in the

circumstances of the transaction or attempted transaction.

−26−Financial Advisors Guide to Money laundering SSC #25

Pro-Seminars International © 12/11

Client proposes to purchase a life insurance product using a cheque drawn on

an account other than his/her personal account.

Client conducts a transaction that results in a conspicuous increase in investment

contributions.

Client cancels investment or insurance soon after purchase.

Client shows more interest in the cancellation or surrender provisions, than in the

long-term results of the investment.

Client makes payments in cash, uncommonly wrapped notes, with postal money

orders or with similar means of payment.

The duration of the life insurance contracts is less than three years.

The first (or single) premium is paid form a bank account outside the country.

Client accepts very unfavourable conditions unrelated to his/her health or age.

Additional situations that should raise suspicion include:

Application for a policy from a potential client in a distant place where a

comparable policy could be provided “closer to home”.

Application for business outside the policyholder’s normal pattern of business.

Introduction by an agent/intermediary in an unregulated or loosely regulated

jurisdiction or where organised criminal activities (e.g. drug trafficking or terrorist

activity) or corruption are prevalent.

Any shortage of information or delay in providing information related to

verification.

An atypical incidence of pre-payment of insurance premiums.

Large fund flows through non-resident accounts with brokerage firms.

Insurance policies with premiums that exceed the client’s apparent means.

The client requests an insurance product that has no discernible purpose and is

reluctant to divulge the reason for the investment.

Insurance policies with values that appear to be inconsistent with the client’s

insurance needs.

−27−Financial Advisors Guide to Money laundering SSC #25

Pro-Seminars International © 12/11

The client conducts a transaction that results in a conspicuous increase of

investment contributions.

Any transaction involving an undisclosed party.

Early termination of a product, especially at a loss, or where cash was tendered

and/or the refund cheque is to a third party.

A transfer of the benefit of a product to an apparently unrelated third party.

A change of the designated beneficiaries (especially if this can be achieved

without knowledge or consent of the insurer and/or the right to payment could be

transferred simply by signing an endorsement on the policy).

Substitution, during the life of an insurance contract, of the ultimate beneficiary

with a person without any apparent connection with the policyholder.

Requests for a large purchase of a lump sum contract where the policyholder has

usually made small, regular payments.

Attempts to use a third party cheque to make a proposed purchase of a policy.

The applicant for insurance business shows no concern for the performance of

the policy but much interest in the early cancellation of the contract.

The applicant for insurance business attempts to use cash to complete a

proposed transaction when this type of business transaction would normally be

handled by cheques or other payment instruments.

The applicant for insurance business requests to make a lump sum payment by a

wire transfer or with foreign currency.

The applicant for insurance business is reluctant to provide normal information

when applying for a policy, providing minimal or fictitious information or, provides

information that is difficult or expensive for the institution to verify.

The applicant for insurance business appears to have policies with several

institutions.

The applicant for insurance business establishes a large insurance policy and

within a short time period cancels the policy, requests the return of the cash value

payable to a third party.

−28−Financial Advisors Guide to Money laundering SSC #25

Pro-Seminars International © 12/11

The applicant for insurance business wants to borrow the maximum cash value of

a single premium policy, soon after paying for the policy.

The applicant for insurance business use a mailing address outside the insurance

supervisor’s jurisdiction and where during the verification process it is discovered

that the home telephone has been disconnected.

Note that the above indicators are far from exhaustive.

Reporting Timelines for STATRYou have thirty (30) days, from the date on which you have reasonable grounds to

suspect that the transaction or attempted transaction is related to a money laundering or

terrorist activity financing offence to file your report. If suspicion occurs at the time of

the transaction or attempted transaction, the 30-day reporting timeline begins at that

time.

If the suspicion occurs after the transaction or attempted transaction or after multiple

transactions or attempted transactions, the 30-day reporting timeline begins at the later

time. You are not permitted to tell the client that you have made a report.

FINTRAC will send you an acknowledgement message when your report has been

received electronically. This will include the date and time your report was received and

a FINTRAC-generated identification number. If your report contains incomplete

information, FINTRAC may contact you by phone, and you can file an updated report

using the identification number assigned to the original report.

This process must be completed within the 30-day time period, your obligation to report

is not considered fulfilled unless the report is complete.

Liability in Relation to Reporting STATR to FINTRACThe Act states that no criminal or civil proceedings lie against a person or an entity for

−29−Financial Advisors Guide to Money laundering SSC #25

Pro-Seminars International © 12/11

making a report in good faith. In other words, you cannot be sued for disclosing

information to FINTRAC as long as the report has been made in good faith. Failure to

file STATRs carries a maximum $2 million fine and five years’ imprisonment.

Prohibited Disclosure to ClientsNo person or entity shall disclose that they have made a report or disclose the contents

of such a report, with the intent to prejudice a criminal investigation, whether or not a

criminal investigation has begun. Basically, you are prohibited by law to tell the client

that you have filed a report under the Act. The clause “with the intent to prejudice a

criminal investigation” may be a defence in case of accidental disclosure.

Every person or entity who submits a STATR to FINTRAC, must keep a copy of the

report.

LARGE CASH TRANSACTIONSGiven the no cash policy of most, if not all, life insurance companies, the large cash

transaction reporting obligation should be minimal.

You have to send a Large Cash Transaction Report (LCTR) to FINTRAC in either of the

following situations:

1. You receive an amount of $10,000 or more in cash in the course of a single

transaction

2. You receive two or more cash amounts of less than $10,000 that total $10,000 or

more from the same individual or on behalf of the same individual or entity. In

this case, you have to make a LCTR if you know the transactions were made

within 24 consecutive hours of each other by or on behalf of the same individual

or entity.

−30−Financial Advisors Guide to Money laundering SSC #25

Pro-Seminars International © 12/11

The "24-Hour Rule"The material that follows is designed to further clarify for reporting entities the measures

they must undertake with respect to reporting two or more cash transactions or

electronic funds transfers in a 24-hour period. Any references to dollar amounts (such

as $10,000) refer to the amount in Canadian dollars or its equivalent in foreign currency.

You have to submit an LCTR if you conduct two or more cash transactions of less than

$10,000 each within 24 consecutive hours of one another, that were made by or on

behalf of the same individual or entity, and that add up to $10,000 or more, unless the

cash is received from a financial entity or a public body.

The 24-hour rule applies if you as the reporting entity know, or your employee or your

senior officer knows, that the transactions were made within 24 consecutive hours of

each other, by or on behalf of the same individual or entity. It applies only to

transactions that are under $10,000. If a transaction is for $10,000 or more, it is

reportable as a single transaction.

Reporting Timelines for LCTRAs noted earlier, you have to send LCTRs to FINTRAC within 15 days after the

transaction. FINTRAC will send you an acknowledgement message when your report

has been received electronically. This will include the date and time your report was

received and a FINTRAC – generated identification number. If your report contains

incomplete information, FINTRAC may notify you, and you can send an additional report

using the identification number assigned on the original report.

Any subsequent reports must be completed within the time period because your

obligation to report is not considered fulfilled unless the report is complete.

−31−Financial Advisors Guide to Money laundering SSC #25

Pro-Seminars International © 12/11

TERRORIST GROUP OR LISTED PERSON PROPERTY According to FINTRAC, a terrorist or a terrorist group can include an individual, a group,

a trust, a partnership or a fund, and unincorporated association or an organization that

facilitates or carries out any terrorist activity as one of their purposes or activities and

will also include anyone on the list published in Regulations issued under the Criminal

Code. Under the Criminal Code, “terrorist group” has a similar meaning to FINTRAC

and includes a listed entity.

The Criminal Code defines “listed entity” as including a person, group, trust, partnership

or fund or an unincorporated association or organization that has been placed on list by

the Governor in Council. This is done on the recommendation of the Minister, where

the Governor in Council is satisfied that there are reasonable grounds to believe that the

entity has knowingly carried out, attempted to carry out, participated in or facilitated a

terrorist activity; or the entity is knowingly acting on behalf of, at the direction of or in

association with a listed entity. The term “listed person” is defined under the

Regulations Implementing the United Nations Resolution on the Suppression of

Terrorism to be a person whose name appears on the list that the Committee of the

Security Council of the United Nations established and has a similar meaning to the

definition in the Criminal Code.

FINTRAC defines “property” as any type of real or personal property. This includes, but

is not limited to, any deed or instrument giving title or right to property, or any deed or

instrument giving a right to money or goods. For example, cash, bank accounts,

insurance policies, money orders, real estate, securities (including mutual funds), and

traveller’s cheques. This can also include business assets such as a plant, property,

and equipment.

Reporting Under the Act Every life insurance agent and broker are subject to the Act and the reporting of terrorist

property.

−32−Financial Advisors Guide to Money laundering SSC #25

Pro-Seminars International © 12/11

As a “reporting entity”, you have a legal obligation to send a terrorist property report to

FINTRAC if you have property in your possession or control that you know is owned or

controlled by or on behalf of a terrorist group or listed person. This includes information

about any transaction or attempted transaction relating to the property. All Terrorist

Group and Listed Person Property Reports must be sent by paper as they cannot be

sent electronically.

Reporting Under The Criminal Code of CanadaIn addition to making a Terrorist Group or Listed Person Property Report to FINTRAC

under the Act, the Criminal Code also have reporting requirements for terrorist property.

These Criminal Code requirements apply to every person in Canada and any Canadian

outside of Canada. It does not matter whether you are a reporting entity under the Act

or not and you do not have to be involved in any life insurance transactions before you

are subject to the Criminal Code requirements.

The Criminal Code requires you to disclose to the RCMP and CSIS the existence of

property in your possession or control that you know is owned or controlled by or on

behalf of a terrorist group or listed person.

This includes information about any transaction or attempted transaction relating to that

property information is to be provided to the RCMP and CSIS immediately, at:

RCMP – Financial Intelligence Task Force unclassified fax: (613) 993-9474

CSIS Financing Unit, unclassified fax: (613) 231-0266

If you have property in your possession or control that you know is owned or controlled

by or on behalf of a terrorist group or listed person, including information about any

transaction or attempted transaction relating to that property, you may not complete or

be involved in the transaction or attempted transaction. It is an offence under the

Criminal Code to deal with any property if you know that is owned or controlled by or on

−33−Financial Advisors Guide to Money laundering SSC #25

Pro-Seminars International © 12/11

behalf of a terrorist group or listed person. It is also an offence to be involved in any

transaction in respect of such property. In such circumstances, you are to remove

yourself from any involvement.

The Criminal Code has a 10-year maximum jail term for failure to report terrorist

property to the RCMP and CSIS.

Reporting Scenarios There are four scenarios that can arise and your course of action depends on which set

of circumstances is present. In all cases, if you have been involved in a life insurance

transaction you may have a reporting obligation to FINTRAC and under the Criminal

Code. If you have not been involved in a life insurance transaction, then your only

potential reporting obligation will be under the Criminal Code.

Scenario 1 – If you do not know that the property in your possession or control

is terrorist property and you do not suspect that it is, there is no obligation to

report to FINTRAC under the Act or under the Criminal Code.

Scenario 2 – If you do not know that the property in your possession or control

is terrorist property but you suspect that it is, there is no obligation to file a

Terrorist Group or Listed Person Property Report to FINTRAC under the Act or

disclose it to the RCMP and CSIS under the Criminal Code.

In this circumstance you will have to file a Suspicious Transaction or Attempted Transaction Report regarding such property.

Scenario 3 – If you have property in your possession or control that you know is

owned or controlled by or on behalf of a terrorist group or listed person, including

information about any transaction or proposed transaction relating to that

property, AND you have been involved in a life insurance transaction, you must

−34−Financial Advisors Guide to Money laundering SSC #25

Pro-Seminars International © 12/11

file a Terrorist Group or Listed Personal Property Report to FINTRAC and

disclose it to the RCMP and CSIS under the Criminal Code.

Scenario 4 – If you have property in your possession or control that you know is

owned or controlled by or on behalf of a terrorist group or listed person, including

information about any transaction or proposed transaction relating to that

property, BUT you have not been involved in a life insurance transaction, you

must disclose it to the RCMP and CSIS under the Criminal Code.

REPORTING TO FINTRACYou must submit all reports electronically, if you have the technical capabilities to do so,

except for the Terrorist Group or Listed Person Property Reports which can only be

paper filed.

Electronic reporting must be done by logging on to FINTRAC’s secure web site (F2R).

All reporting entities must register for and utilize F2R if they have the technical

capabilities. Generally “technical capability” means a computer and Internet access.

This can be done via FINTRAC’s website at www.fintrac.gc.ca.

Report Acknowledgement and Correction requestsFINTRAC will send you an acknowledgement message when you report has been

received electronically. This will include that date and time your report was received and

a FINTRAC- generated identification number. Keep this information for your records.

If your report contains incomplete information, FINTRAC may notify you. The notification

will indicate the date and time your report was received, a FINTRAC-generated

identification number, along with information on what must be completed.

Any additional or incomplete information must be sent to FINTRAC within 30 days of the

time the suspicion was first detected. Your obligation to report will not be fulfilled until

you send the completed report to FINTRAC. In light of this 30-day requirement, you

should ensure that your policies and procedures call for the reports to be made quickly

as possible to leave you enough time to respond to any correction requests. −35−

Financial Advisors Guide to Money laundering SSC #25Pro-Seminars International © 12/11

Paper ReportingIf you do not have the technical capability to report electronically or you have to file a

Terrorist Group and Listed Person Property, you must submit paper reports to

FINTRAC. The following forms can be accessed from FINTRAC’s website and printed

at your office or local library, or other public place with Internet access or call 1-866-

346-8722 for a copy to be faxed or mailed to you.

Suspicious Transaction or Attempted Transaction Report (FINTRAC may refer to

this report as a Suspicious Transaction Report)

Large Cash Transaction Report

Terrorist Group or Listed Person Property Report (FINTRAC may refer to this

report as a Terrorist Property Report)

There are two ways to send a paper report to FINTRAC:

Fax: 1-866-266-2346; or Registered, mail to the following address:

Financial Transaction and Report Analysis Centre of CanadaSection A, 234 Laurier Avenue West, 24th FloorOttawa, ON K1P 1 H7

FINTRAC will not send you any acknowledgement when a paper report has been

received.

Information to be Contained in ReportsThe information to be contained in reports depends on the type of report being filed.

There are several parts that must be completed on both the Suspicious Transaction or

Attempted Transaction Report form and the Large Cash Transaction Report form but

some parts are only to be completed if applicable. Any fields marked with an asterisk

−36−Financial Advisors Guide to Money laundering SSC #25

Pro-Seminars International © 12/11

(*) must be completed. All other fields require you to make a reasonable effort to get

the information. The information that is required to be provided includes:

Information about the reporting entity (you)

Information about the transaction or attempted transaction and its disposition

Information about the individual conducting a transaction or attempting to conduct

a transaction and/or the individual on whose behalf the transaction is being

conducted or attempted to be conducted

Information explaining your reasons for suspicion and if you have taken action

One of the requirements for reporting large cash transactions is that multiple

transactions under $10,000 each within a 24-hour period that exceed $10,000 in

aggregate must be reported if you are aware that the transactions were conducted by,

or on behalf of, the same person or entity.

Certain information for some mandatory fields on the LCTR may not be available

because the individual transactions were under $10,000. In this case, “reasonable

efforts” can now apply to those mandatory fields on the LCTR. This means that if

information was not obtained at the time of the transaction because it was under

$10,000 and it is not available from your records you can leave the applicable LCTR

field blank.

With Suspicious Transaction or Attempted Transaction Reports, you should use field

“G” to record the details of the transaction or attempted transaction and why you felt it

was suspicious.

RECORD KEEPINGPursuant to the regulations under the Act, as a “reporting entity”, i.e., a life insurance

agent or broker, you are required to keep certain records, namely large cash transaction

and client information records. Other records that you may be required to keep,

−37−Financial Advisors Guide to Money laundering SSC #25

Pro-Seminars International © 12/11

depending on the situation, may include records related to beneficial ownership, not-for-

profit organizations, third party determinations, and politically exposed foreign persons.

Large Cash Transaction Record The requirements are:

Prepare a large cash transaction record in respect of every amount in cash of

$10,000 or more that is received in the course of a single transaction, unless the

cash is received from a financial entity (such as a bank, credit union, caisse

populaire or trust company) or public body.

Ascertain the identity of the individuals involved in the transaction at the time of

the transaction.

Take reasonable measures to determine whether the individual who in fact gives

the cash in respect of which the record is being made is acting on behalf of a

third party.

Prepare and retain a third party disclosure statement signed by the client if they

are acting on behalf of a third party.

Where you are not able to determine if the client is acting on behalf of a third

party but there are reasonable grounds to suspect that the client is acting on

behalf of a third party, prepare and retain a third party disclosure statement

signed by the client stating that they are not acting on behalf of a third party.

There is no standard format or template for the large cash transaction record. The

information required is specified in detail in the regulations.

The information required in the large cash transaction record includes the following:

The name of the individual who in fact gives the amount (cash)

The address and date of birth of the individual and the nature of their principal

business or occupation

The date and nature of the transaction

−38−Financial Advisors Guide to Money laundering SSC #25

Pro-Seminars International © 12/11

The number of any account that is affected by the transaction as well as the type

of account, the name of any person or entity that holds/owns the account, and the

currency in which the account transactions are conducted

The purpose and details of the transaction, including other persons or entities

involved and the type of transaction (such as cash, electronic funds transfer,

deposit, currency exchange, or the purchase or cashing of a cheque, money

order, travellers’ cheque or banker’s draft)

Whether the cash is received in person, by mail, or in any other way

The amount and currency received

It is important to remember that the large cash transaction record is different from the

large cash transaction report (LCTR). Although there is some overlap of information

required in each of these reports/records, there are differences.

As such, the filing of a LCTR is not a substitute for having to also maintain the large cash transaction record. Keeping a copy of the LCTR that was submitted to

FINTRAC can be used as large cash transaction record if all of the information for the

record is included.

ASCERTAINING IDENITYIf your client pays you $10,000 or more for an annuity or a life insurance policy, over the

duration of the annuity or policy, you have to keep a client information record. This has

to be kept no matter how the client paid for the annuity or policy, whether or not it was in

cash.

For an individual – You must ascertain and record your client’s name, address, date of

birth and the nature of the client’s principal business or occupation. In the case of a

group life insurance policy or a group annuity, the client information record is about the

applicant for the policy or annuity.

Client identity must be verified. While client identity for a large cash transaction record

must be at the time of the transaction, client identity for a client information record, must −39−

Financial Advisors Guide to Money laundering SSC #25Pro-Seminars International © 12/11

be done within thirty (30) days of creating the record. This is true whether the

transaction is conducted on the client’s own behalf, or on behalf of a third party.

However, if you have reasonable grounds to believe that another life insurance

company, broker or agent has confirmed the individual’s identity, you do not have to

confirm his/her identity again unless you have doubts about the information collected.

Unless otherwise specified, only original documents that are valid and have not expired

may be referred to for the purpose of ascertaining identity. The identity is to be

ascertained by reference to the individual’s:

Birth certificate

Drivers license

Provincial health insurance card

Passport

Any similar record other than the individual’s social insurance number

If you are required to ascertain the identity of an individual purchasing an annuity or life

insurance policy, the client information record has to contain the individual’s date of birth

along with the following information:

If you used a document to confirm the individual’s identity, the type of

identification document used, its reference number and its place of issue.

If you used a cleared cheque to confirm the individual’s identity, the name of the

financial entity and the account number of the account on which the cheque was

drawn.

If you confirmed the individual identity by confirming that the individual holds an

account with a financial entity, the name of the financial entity, the account

number and the date of confirmation.

If you relied on previous confirmation of their identity by an entity that is affiliated

with the entity ascertaining the identity of the individual or an entity that is a

member of the same association – being a central cooperative credit society

−40−Financial Advisors Guide to Money laundering SSC #25

Pro-Seminars International © 12/11

within the meaning of section 2 of the Cooperative Credit Association Act – the

name of that entity and the type and reference number of the record that entity

previously relied on to ascertain the individual’s identity.

If you used an identification product to confirm the individual’s identity, the name

of the identification product, the name of the entity offering the product, the

search reference number, and the date the product was used to ascertain the

individual’s identity.

If you are consulting a credit file kept by an entity in respect of the individual to

ascertain the individual’s identity, the name of the entity and the date of the

consultation.

If you use an attestation signed by a commissioner of oaths in Canada or a

guarantor in Canada to ascertain the individual’s identity, the attestation.

If you ascertain the individual’s identity by consulting an independent data

source, the name of the data source, the date of the consultation and the

information provided by the data source.

If you rely on a utility invoice issued in the individual’s name, the invoice or a

legible photocopy or electronic image of the invoice.

If you rely on a photocopy or electronic image of a document provided by the

individual to ascertain the individual’s identity, the photocopy or electronic image.

If you rely on a deposit account statement issued in the individual’s name by a

financial entity to ascertain the individual’s identity, a legible photocopy or

electronic image of the statement.

For a corporation – You must ascertain the existence, name and address of the

corporation, and the names of its directors. This can be done by reference to:

Certificate of corporate status

A record that it is required to file annually under the applicable provincial

securities legislation