Embed Size (px)

Citation preview

Your Health Idaho UpdateHealth Care Task Force

Pat Kelly

Executive Director, Your Health Idaho

3

Our Mission

Maintain maximum control of Idaho’s

health insurance marketplace

at minimal cost to its citizens.

Your Health Idaho

4

Our Goals

We are meeting the goals placed in front of us

less than three years ago.

1. Idaho is in control of our marketplace.

2. We are providing Idaho-based resources to thousands of

Idahoans who choose to use the exchange to find health

insurance.

Your Health Idaho

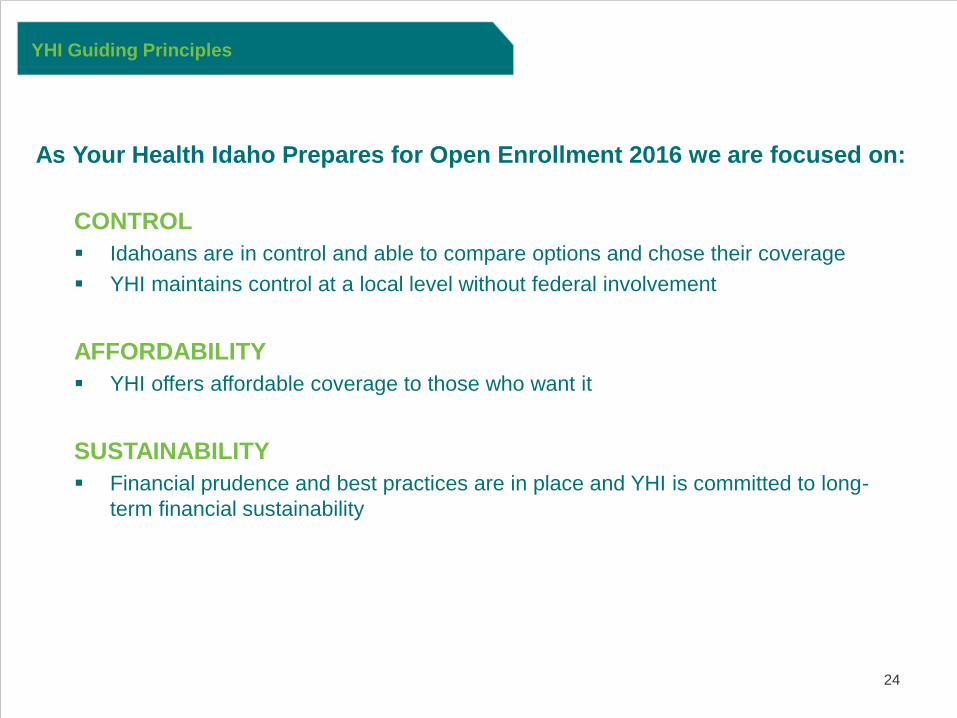

YHI Guiding Principles

6

CONTROL

Idahoans are in control and able to compare options and chose their coverage

YHI maintains control at a local level without federal involvement

AFFORDABILITY

YHI offers affordable coverage to those who want it

SUSTAINABILITY

Financial prudence and best practices are in place and YHI is committed to long-

term financial sustainability

As Your Health Idaho Prepares for Open Enrollment 2016 we are focused on:

YHI Guiding Principles

Sustainability of Your

Health Idaho

8

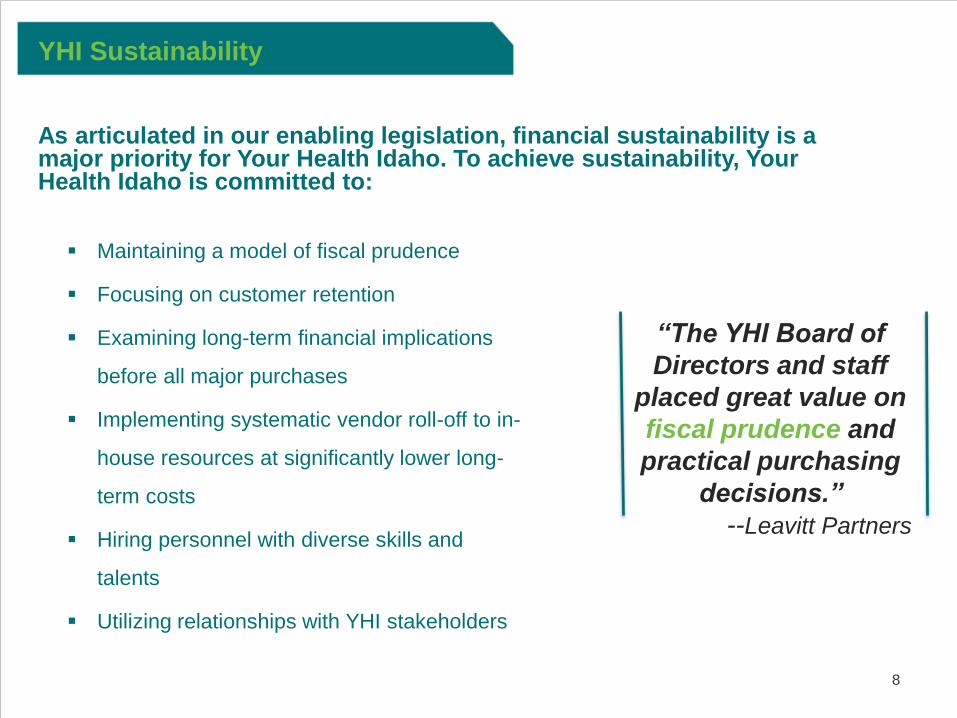

As articulated in our enabling legislation, financial sustainability is a major priority for Your Health Idaho. To achieve sustainability, Your Health Idaho is committed to:

YHI Sustainability

Maintaining a model of fiscal prudence

Focusing on customer retention

Examining long-term financial implications

before all major purchases

Implementing systematic vendor roll-off to in-

house resources at significantly lower long-

term costs

Hiring personnel with diverse skills and

talents

Utilizing relationships with YHI stakeholders

“The YHI Board of

Directors and staff

placed great value on

fiscal prudence and

practical purchasing

decisions.”

--Leavitt Partners

9

Commitment to Sustainability

YHI Sustainability

YHI has been the least expensive, fully functional, state based exchange to

implement

Total Federal Grant Monies: $104M

Total Monies Spent to date: $76M

Beginning with Plan Year 2016, Your Health Idaho assessment fees will increase from 1.5% to

1.99% which is substantially lower than the FFM fee of 3.5%

Enrollment

11

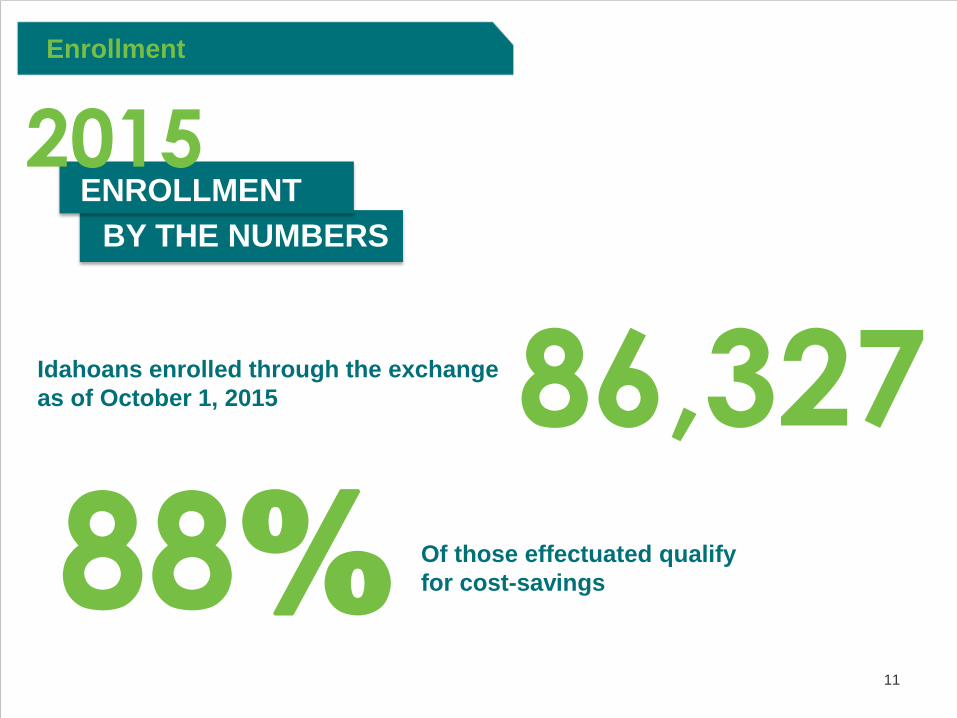

Enrollment

86,327Idahoans enrolled through the exchange

as of October 1, 2015

ENROLLMENT

BY THE NUMBERS

2015

88% Of those effectuated qualify

for cost-savings

12

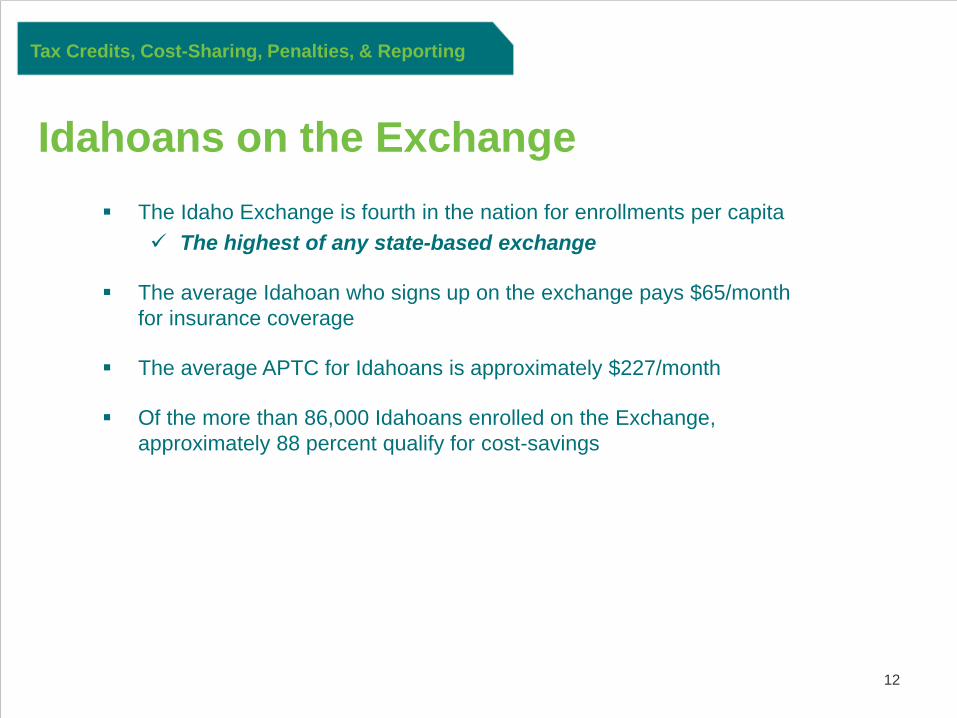

Idahoans on the Exchange

The Idaho Exchange is fourth in the nation for enrollments per capita

The highest of any state-based exchange

The average Idahoan who signs up on the exchange pays $65/month

for insurance coverage

The average APTC for Idahoans is approximately $227/month

Of the more than 86,000 Idahoans enrolled on the Exchange,

approximately 88 percent qualify for cost-savings

Tax Credits, Cost-Sharing, Penalties, & Reporting

Improving the Consumer

Experience

14

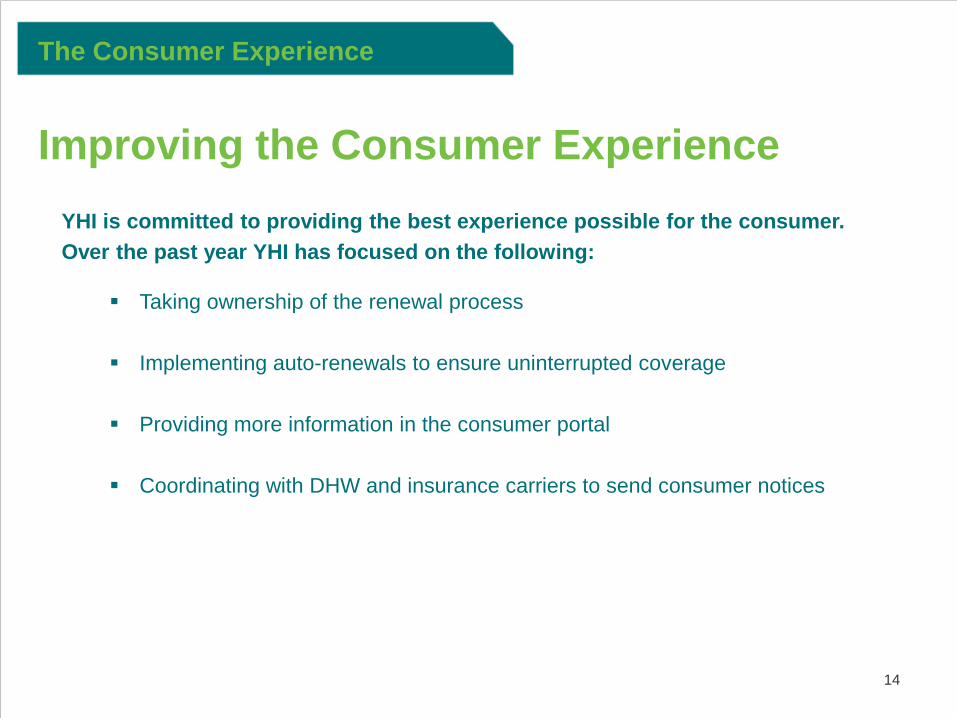

Improving the Consumer Experience

The Consumer Experience

YHI is committed to providing the best experience possible for the consumer.

Over the past year YHI has focused on the following:

Taking ownership of the renewal process

Implementing auto-renewals to ensure uninterrupted coverage

Providing more information in the consumer portal

Coordinating with DHW and insurance carriers to send consumer notices

15

The Consumer Experience

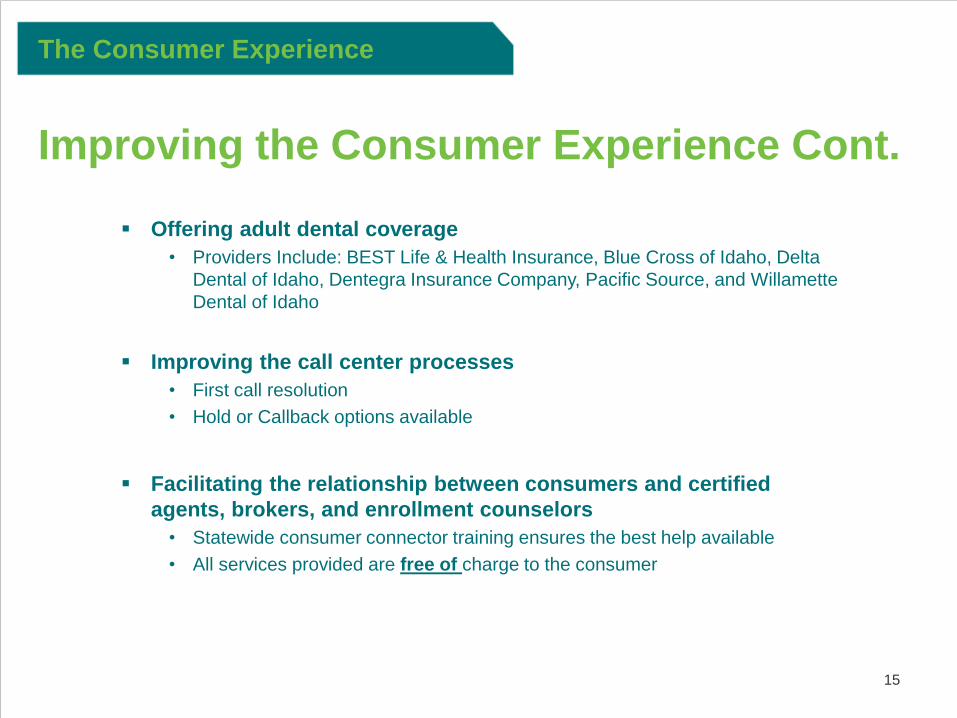

Improving the Consumer Experience Cont.

Offering adult dental coverage

• Providers Include: BEST Life & Health Insurance, Blue Cross of Idaho, Delta

Dental of Idaho, Dentegra Insurance Company, Pacific Source, and Willamette

Dental of Idaho

Improving the call center processes

• First call resolution

• Hold or Callback options available

Facilitating the relationship between consumers and certified

agents, brokers, and enrollment counselors

• Statewide consumer connector training ensures the best help available

• All services provided are free of charge to the consumer

16

The Consumer Experience

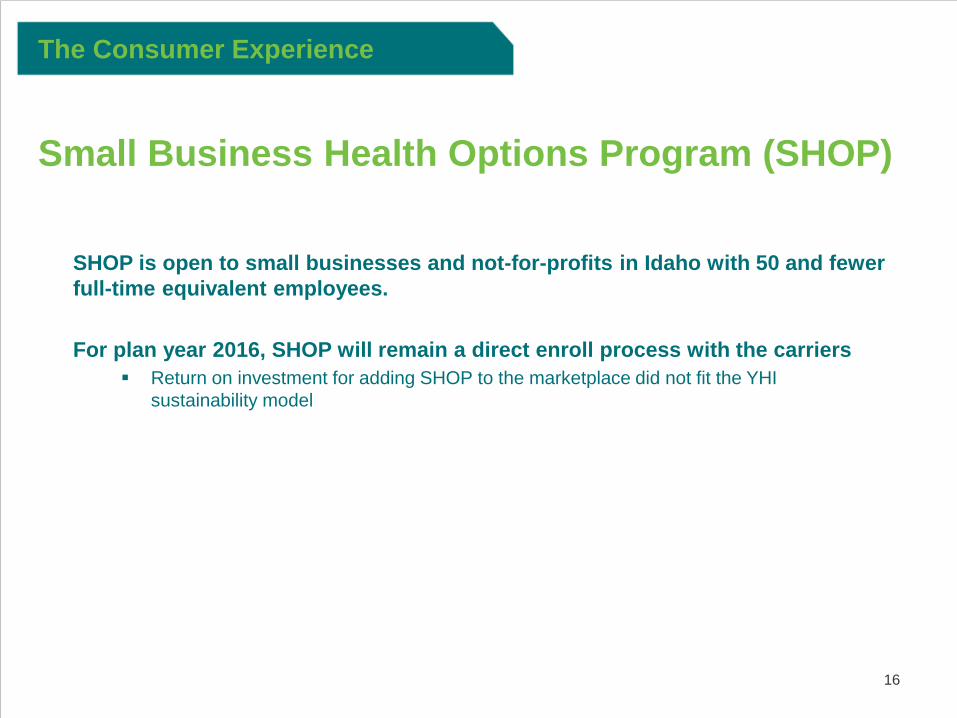

Small Business Health Options Program (SHOP)

SHOP is open to small businesses and not-for-profits in Idaho with 50 and fewer

full-time equivalent employees.

For plan year 2016, SHOP will remain a direct enroll process with the carriers

Return on investment for adding SHOP to the marketplace did not fit the YHI

sustainability model

Improving the Consumer

Connector Experience

18

Improving the Consumer Connector Experience

Improving the Consumer Connector Experience

Consumer Connectors are essential to helping Idahoans apply for coverage through

the exchange. YHI recognizes that relationship and is committed to improving the

necessary technology. Updates include:

Ability to sort and export all active individuals to spreadsheet

Option to submit a support ticket directly to YHI from the portal

Improving the individual toolbar to include shortcuts to household, eligibility,

APTC/CSR, and support ticket template

Improvements to the consumer connector inbox

Call center process improvement

• First call resolution

• Hold or Callback options available

In conjunction with these updates, YHI has enhanced agent training to include state-

wide in-person & live experience opportunities.

Renewals & Open

Enrollment

20

2016 Renewals

Renewals & Open Enrollment

In 2015, more than 86,000 Idahoans enrolled in coverage through Your Health Idaho.

Your Health Idaho is pursuing a path to ensure Idahoans that enrolled in coverage in

2015:

• Receive an accurate re-determination of their eligibility for the Advanced Premium

Tax Credit (APTC) and Cost Sharing Reductions.

• Maintain coverage without interruption into plan year 2016 if they take no action.

• Have an opportunity to shop for a new plan for 2016 if they choose.

21

Operational Readiness

Renewals & Open Enrollment

Renewal Campaign

“What to Expect” mailers sent to Idahoans

DHW to send APTC updates

Web site updates staged

Consumer Connector Certification

Over 450 agents and brokers have been certified

for 2016

Statewide Training

Renewals & Tec Updates – Sept.

Live Application Training – Oct.

Open Enrollment Procedures – Nov.

Technology Updates

Release 3.0 implemented Sept. 30

“The achievements and

lessons learned from the

YHI marketplace represent

an attractive opportunity

for FFM states that my be

interested in taking on

more responsibility for

marketplace operations.”

--Leavitt Partners

22

Important Dates

Renewals & Open Enrollment

October 1, 2015 – Anonymous shopping available

November 1, 2015 – Open Enrollment 2016 begins

December 15, 2015 – Last day to submit an application for coverage beginning

Jan. 1, 2016

January 31, 2016 – Open Enrollment ends

YHI Guiding Principles

24

CONTROL

Idahoans are in control and able to compare options and chose their coverage

YHI maintains control at a local level without federal involvement

AFFORDABILITY

YHI offers affordable coverage to those who want it

SUSTAINABILITY

Financial prudence and best practices are in place and YHI is committed to long-

term financial sustainability

As Your Health Idaho Prepares for Open Enrollment 2016 we are focused on:

YHI Guiding Principles

25

THANK YOU

Appendix

27

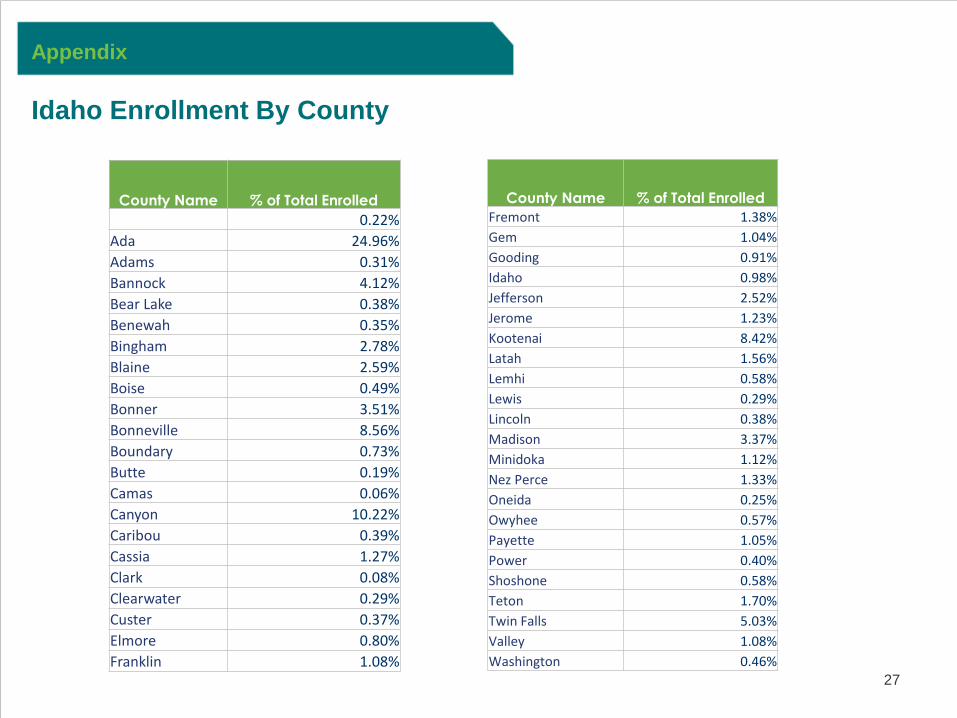

Appendix

Idaho Enrollment By County

County Name % of Total Enrolled

0.22%

Ada 24.96%

Adams 0.31%

Bannock 4.12%

Bear Lake 0.38%

Benewah 0.35%

Bingham 2.78%

Blaine 2.59%

Boise 0.49%

Bonner 3.51%

Bonneville 8.56%

Boundary 0.73%

Butte 0.19%

Camas 0.06%

Canyon 10.22%

Caribou 0.39%

Cassia 1.27%

Clark 0.08%

Clearwater 0.29%

Custer 0.37%

Elmore 0.80%

Franklin 1.08%

County Name % of Total Enrolled

Fremont 1.38%

Gem 1.04%

Gooding 0.91%

Idaho 0.98%

Jefferson 2.52%

Jerome 1.23%

Kootenai 8.42%

Latah 1.56%

Lemhi 0.58%

Lewis 0.29%

Lincoln 0.38%

Madison 3.37%

Minidoka 1.12%

Nez Perce 1.33%

Oneida 0.25%

Owyhee 0.57%

Payette 1.05%

Power 0.40%

Shoshone 0.58%

Teton 1.70%

Twin Falls 5.03%

Valley 1.08%

Washington 0.46%

28

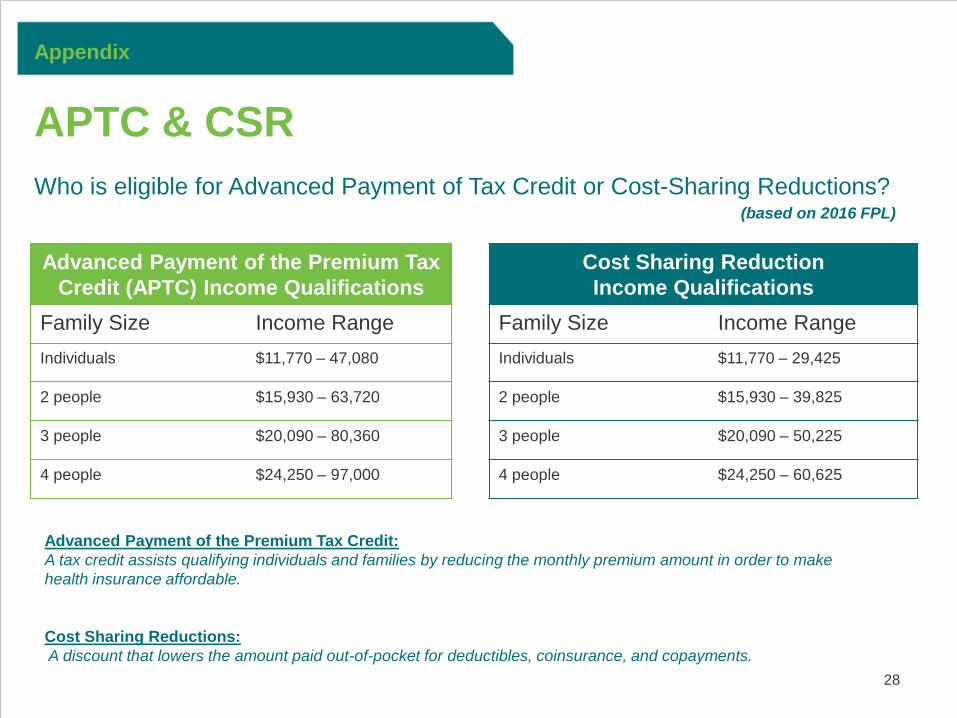

APTC & CSR

Appendix

Advanced Payment of the Premium Tax

Credit (APTC) Income Qualifications

Family Size Income Range

Individuals $11,770 – 47,080

2 people $15,930 – 63,720

3 people $20,090 – 80,360

4 people $24,250 – 97,000

Cost Sharing Reduction

Income Qualifications

Family Size Income Range

Individuals $11,770 – 29,425

2 people $15,930 – 39,825

3 people $20,090 – 50,225

4 people $24,250 – 60,625

Who is eligible for Advanced Payment of Tax Credit or Cost-Sharing Reductions?(based on 2016 FPL)

Advanced Payment of the Premium Tax Credit:

A tax credit assists qualifying individuals and families by reducing the monthly premium amount in order to make

health insurance affordable.

Cost Sharing Reductions:

A discount that lowers the amount paid out-of-pocket for deductibles, coinsurance, and copayments.

29

Reporting | 1095 Forms

Form 1095-A: Health Insurance Marketplace Statement

Sent from YHI to the consumer. Shows monthly premium & APTC amounts.

Form 1095-B: Health Coverage

Sent from insurance carriers to the consumer. Shows months that consumer had

Qualifying Health Plan. - If an individual receives Medicaid, this form will come from DHW

Form 1095-C: Employer-Provided Health Insurance Offer & Coverage

Sent from employer to the consumer and the IRS. Includes employer coverage

information (type, periods, affordability, etc.)

Tax Credits, Cost-Sharing, Penalties, & Reporting

THE YOUR HEALTH IDAHO MARKETPLACE: A MODEL FOR STATE BASED ADOPTION

MARKETPLACE SUSTAINABILITY A MAJOR CONCERNThe Patient Protection and Affordable Care Act (ACA) originally required all states to adopt some type of health insurance marketplace so that eligible consumers could enroll in qualified health plans (QHPs) and potentially receive a premium subsidy to help defray the cost of purchasing insurance. Alternatively, the federal government built a federally facilitated marketplace (FFM) for states that chose not to establish SBMs.

Beginning in 2011, the federal government provided grants to states to pay for the research, planning, and building of their respective marketplaces. However, the opportunity for states to apply for new or additional grant funding ended in 2014 and it is highly unlikely that Congress will appropriate any additional funding.

One of the growing concerns that current and future SBMs are facing is the difficult task of determining how to pay for ongoing operational costs now that the grant

funding has ended. Many of the SBMs have developed revenue models in hopes of achieving sustainability, and these models largely seek to expand funding sources to support the scope of the marketplace operations. Among the states that initially established a marketplace, there is currently not an established—and proven—sustainability model that can be replicated and guarantee viability for future SBMs. The high costs to sustain state based marketplaces may not be desirable among other states given that these costs are ultimately absorbed within the overall health system. As such, financial sustainability continues to be one of the primary impediments holding back many FFM and partnership states from transitioning to an SBM.

THE YOUR HEALTH IDAHO APPROACHIdaho’s health insurance marketplace was established by Governor Butch Otter in March 2013 with the goal of retaining maximum control of the state’s insurance market.

Recognizing the importance of not contributing to the cost of insurance coverage, the YHI Board of Directors and staff placed great value on fiscal prudence and practical purchasing decisions during implementation. Over time, this became the “low-cost promise” that marketplace staff keep in mind in all walks of operation. Long-term sustainability is a major priority for YHI and influences every key decision and process.

While the implementation of other ACA-compliant state-based marketplaces (SBMs) have been marred by technical issues and runaway budgets, the Your Health Idaho marketplace opened with few technical complications and touts an annual budget of less than $9 million. It also has plans to be self-sustaining within the first few years of operation. Leavitt Partners’ analyses of publicly available budget data from other SBMs suggest a range of annual budgets from $32.5 million to $340 million, with a median of $63.2 million.1

The goal of this case study is to identify the successful traits of the Your Health Idaho marketplace that have led to a successful rollout and put it on a fast-track to financial sustainability. Other states which may be interested in pursuing an SBM, but are justifiably concerned about costs, may consider these lessons to be best practices.

THE YOUR HEALTH IDAHO MARKETPLACE: A MODEL FOR STATE BASED ADOPTION 1

1 Leavitt Partners conducted a robust analysis of six other state-based marketplace budgets. State selection was premised on the amount of budgeting data available—not all SBMs have publicly released annual budgeting data.

Your Health Idaho Mission:

“Maintain maximum control of the insurance marketplace at minimum cost to consumers.”

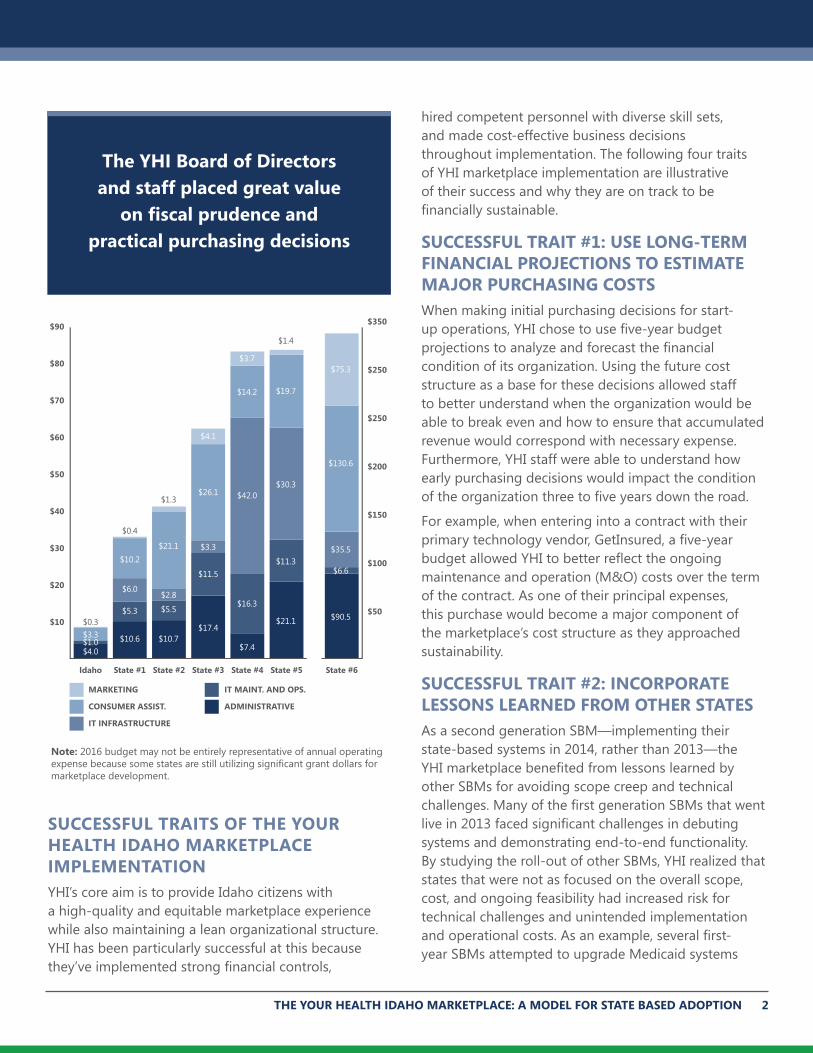

SUCCESSFUL TRAITS OF THE YOUR HEALTH IDAHO MARKETPLACE IMPLEMENTATIONYHI’s core aim is to provide Idaho citizens with a high-quality and equitable marketplace experience while also maintaining a lean organizational structure. YHI has been particularly successful at this because they’ve implemented strong financial controls,

hired competent personnel with diverse skill sets, and made cost-effective business decisions throughout implementation. The following four traits of YHI marketplace implementation are illustrative of their success and why they are on track to be financially sustainable.

SUCCESSFUL TRAIT #1: USE LONG-TERM FINANCIAL PROJECTIONS TO ESTIMATE MAJOR PURCHASING COSTS

When making initial purchasing decisions for start-up operations, YHI chose to use five-year budget projections to analyze and forecast the financial condition of its organization. Using the future cost structure as a base for these decisions allowed staff to better understand when the organization would be able to break even and how to ensure that accumulated revenue would correspond with necessary expense. Furthermore, YHI staff were able to understand how early purchasing decisions would impact the condition of the organization three to five years down the road.

For example, when entering into a contract with their primary technology vendor, GetInsured, a five-year budget allowed YHI to better reflect the ongoing maintenance and operation (M&O) costs over the term of the contract. As one of their principal expenses, this purchase would become a major component of the marketplace’s cost structure as they approached sustainability.

SUCCESSFUL TRAIT #2: INCORPORATE LESSONS LEARNED FROM OTHER STATESAs a second generation SBM—implementing their state-based systems in 2014, rather than 2013—the YHI marketplace benefited from lessons learned by other SBMs for avoiding scope creep and technical challenges. Many of the first generation SBMs that went live in 2013 faced significant challenges in debuting systems and demonstrating end-to-end functionality. By studying the roll-out of other SBMs, YHI realized that states that were not as focused on the overall scope, cost, and ongoing feasibility had increased risk for technical challenges and unintended implementation and operational costs. As an example, several first-year SBMs attempted to upgrade Medicaid systems

THE YOUR HEALTH IDAHO MARKETPLACE: A MODEL FOR STATE BASED ADOPTION 2

Idaho

$10

$20

$30

$40

$50

$60

$70

$80

$90

State #1 State #3State #2 State #4 State #5 State #6

$50

$100

$150

$200

$250

$250

$350

MARKETING

CONSUMER ASSIST.

IT MAINT. AND OPS.

ADMINISTRATIVE

IT INFRASTRUCTURE

$4.0$1.0$3.3$0.3

$10.6

$5.3

$6.0

$10.2

$0.4

$10.7

$5.5

$2.8

$21.1

$1.3

$17.4

$11.5

$3.3

$26.1

$4.1

$7.4

$16.3

$42.0

$14.2

$3.7

$21.1

$11.3

$30.3

$19.7

$1.4

$90.5

$6.6

$35.5

$130.6

$75.3

Note: 2016 budget may not be entirely representative of annual operating expense because some states are still utilizing significant grant dollars for marketplace development.

The YHI Board of Directors and staff placed great value

on fiscal prudence and practical purchasing decisions

and integrate eligibility engines while simultaneously developing marketplace technologies and policies. Ambitious objectives frequently led to systemic challenges and high costs and, since then, several of these marketplaces have opted to abandon their technologies and move to the FFM.

When developing their implementation plan, YHI staff understood that achieving a basic level of marketplace functionality would require strict scope management to deal with major challenges. YHI staff also understood that the go-live date at the start of open enrollment could not be extended if technical difficulties were encountered. As such, YHI staff prioritized projects that could enable marketplace operation and minimum essential functionality by the required launch date. For instance, during the first year of operation, YHI enrollees were required to establish two separate accounts for obtaining marketplace coverage—one for the Department of Health and Welfare (DHW), who oversees the eligibility engine, and one for the marketplace, where consumers log-in and shop for coverage. The hand-off between websites was not automated, so consumers were required to follow a link sent via email which connected the DHW eligibility determination to the YHI marketplace where they could shop for coverage. While this resulted in a somewhat cumbersome experience for consumers, staff recognized that integrating systems would increase the technology-build risk significantly and require time that the team didn’t have. Since its launch, the YHI marketplace has been working to improve integration of the two systems and is now providing a more seamless experience to consumers.

SUCCESSFUL TRAIT #3: SELECT VENDORS THAT ARE CAPABLE AND LOW COSTWith a state population of approximately 1.6 million individuals and the marketplace-eligible population being a fraction of that, YHI staff understood that the customer base would not be sufficient for sustaining a major technology expense. For this reason, YHI staff chose to heavily weight the proposed ongoing M&O technology costs when bidding for marketplace solutions. While technical competency accounted for 70% of the requisite scoring criteria, cost accounted for the remaining 30% (and two-thirds of this category

was weighted for ongoing M&O). YHI also chose to adopt a commercial off-the-shelf (COTS) solution rather than a design, develop, and implement (DDI) approach (i.e., build from scratch), which would have required a longer implementation timeline, more complex technology build, and would have been significantly more expensive.

By implementing its SBM after most other states, Idaho was able to procure refined, second-generation technology at a lower cost from the technology vendors that were successful in first-generation implementations. YHI also benefited by being able to compare M&O bids against other states and, as a result, secure M&O at a lower price point. YHI used those savings as part of its long-term sustainability plan.

It is also important to note that YHI is not vendor supported with the exception of a few specialized services. YHI operates an “in-house supported” model, which means that YHI staff oversee the bulk of day-to-day marketplace operations and contract-out for only a few specialized vendor services—like system M&O and marketing activities such as advertising and media production. This is a significant contrast from many of the other SBMs and also a major source of cost savings for the YHI marketplace.

SUCCESSFUL TRAIT #4: LEVERAGE EXISTING SOLUTIONSYHI staff defined the roles and responsibilities of the state’s marketplace early on and opted to administer only essential marketplace functions. For example, the YHI marketplace relies on DHW to provide eligibility determination services and serve as the entry point for all call center operations. Through cost allocation, the YHI marketplace reimburses DHW for eligibility determination services used by consumers deemed QHP eligible as well as related call center functions (the marketplace handles only call center escalations). The marketplace incorporated these existing state infrastructures and processes in an effort to spare unnecessary expense. Similarly, plan management and rate review is handled entirely by the Idaho Department of Insurance (DOI). The YHI marketplace saves money by not being involved in this process and by not purchasing resources that would be duplicative for plan review and regulation.

THE YOUR HEALTH IDAHO MARKETPLACE: A MODEL FOR STATE BASED ADOPTION 3

For other YHI responsibilities, such as outreach and education, the marketplace has primarily relied on existing solutions. Agents and brokers were incorporated as a vital part of the YHI business model and are a major contributor to the marketplace’s enrollment. Additionally, YHI has chosen to adopt only the optional ACA provisions that could be sustainable and worth the cost of investment. For example, YHI declined to build a Small Business Health Options Program (SHOP) marketplace when it was realized that anticipated SHOP enrollment would not justify the costs

of building a functional SHOP marketplace. Thus, YHI has opted to rely on carriers for direct enrollment into SHOP products rather than build costly and low-use systems they would have to support and administer.

YOUR HEALTH IDAHO PRIORITIES: LOOKING FORWARDThe YHI marketplace has almost completed its first year and is quickly transitioning from a start-up to a sustainable marketplace. With this comes a general recognition that customer retention will be a critical component for achieving long-term viability. During the first few years, YHI’s focus is on marketing, increasing awareness, and acquisition of new consumers. But, as the marketplace matures and looks to shift some of its budget priorities, YHI staff are aware that it is far less costly to retain customers than it is to replace them. This requires that YHI consistently provide quality customer service and a positive marketplace experience, which is where YHI is focusing its technology improvements today.

The YHI marketplace also recently revised its assessment fee from 1.5% to 1.99% of premium cost to ensure that YHI can maintain its current cash reserves. YHI’s strict focus on economic stability is allowing the marketplace to meet short-term expenses while also setting aside funds that can add to the longevity of the organization.

CONCLUSIONThe YHI marketplace was established with the primary goal of preventing the federal government from inserting its involvement into the state’s insurance market. Yet, over time, the YHI marketplace has plotted its own path and is now identified as one of the efficient methods for establishing an SBM. The achievements and lessons learned from the YHI marketplace represent an attractive opportunity for FFM states that may be interested in taking on more responsibility for marketplace operations. YHI’s lean marketplace approach has accomplished two goals that could be very attractive to other states: (1) it is able to maintain decision-making at a local level; and (2) it is able to operate the state-based platform at a substantially lower cost to consumers than the federal alternative (i.e., 1.99% of premium cost rather than 3.5%).

THE YOUR HEALTH IDAHO MARKETPLACE: A MODEL FOR STATE BASED ADOPTION 4

INTER-AGENCY COORDINATION OF MARKETPLACE OPERATIONS

Your Health Idaho• Determines

exchange eligibility (non-financial criteria)

• Administers shop & compare platform

• Shares enrollment transmittals with carriers

• Handles Call center escalations

Department of Health and Welfare• Conducts eligibility

determinations for APTC and Cost-sharing Reductions

• Functions as the call center point of entry

Department of Insurance• Conducts QHP

rate review• Certifies

participating QHPs

Insurance Carriers• Facilitate direct

enrollment into the Small Business Health Options Program (SHOP)

• Collect premium payment