Embed Size (px)

Citation preview

Yearbook 2012 Activity Data on Fundraising, Investments and Divestments by

Private Equity and Venture Capital Firms in Europe

9 May, 2012

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012

Acknowledgements and Disclaimer

| 2

Acknowledgements

We are very grateful for the generous support by General Partners representing Private Equity and Venture Capital firms across Europe who are

directly submitting their activity data to our survey. Without their commitment providing comprehensive and verified pan-European statistics

would not be possible.

We also thank all regional and national private equity associations that collect their activity data via PEREP_Analytics, the pan-European statistics

platform, making it the most comprehensive European private equity database: APCRI (Portugal), AVCO (Austria), BVA (Belgium), BVK (Germany),

CVCA (Croatia), CVCA (the Czech Republic), DVCA (Denmark), EstVCA (Estonia), EVCA (Europe), FVCA (Finland), HVCA (Hungary), IVCA (Ireland),

LTVCA (Lithuania), NVCA (Norway), NVP (the Netherlands), PPEA (Poland), SECA (Switzerland), SEEPEA (South Eastern Europe), SLOVCA

(Slovakia), SVCA (Sweden). PEREP has collected data directly from associations’ members and participants in the other countries in Europe.

Version

Presentation as of 9/5/2012

Disclaimer

The information contained in this report has been produced by EVCA, based on PEREP_Analytics data and third parties information. While the

EVCA has made every effort to ensure the reliability of the data included in this report, EVCA can not guarantee the accuracy of the information

collected and presented. Therefore, EVCA cannot accept responsibility for any decision made or action taken based upon this report or the

information provided herein.

Copyright information

No part of this publication may be reproduced by any process except in accordance with the provisions of the Copyright Act 1968. Copyright

enquiries should be directed to EVCA, Tel: + 32 2 715 00 20.

© Copyright EVCA May 2012

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012

Executive Summary

| 3

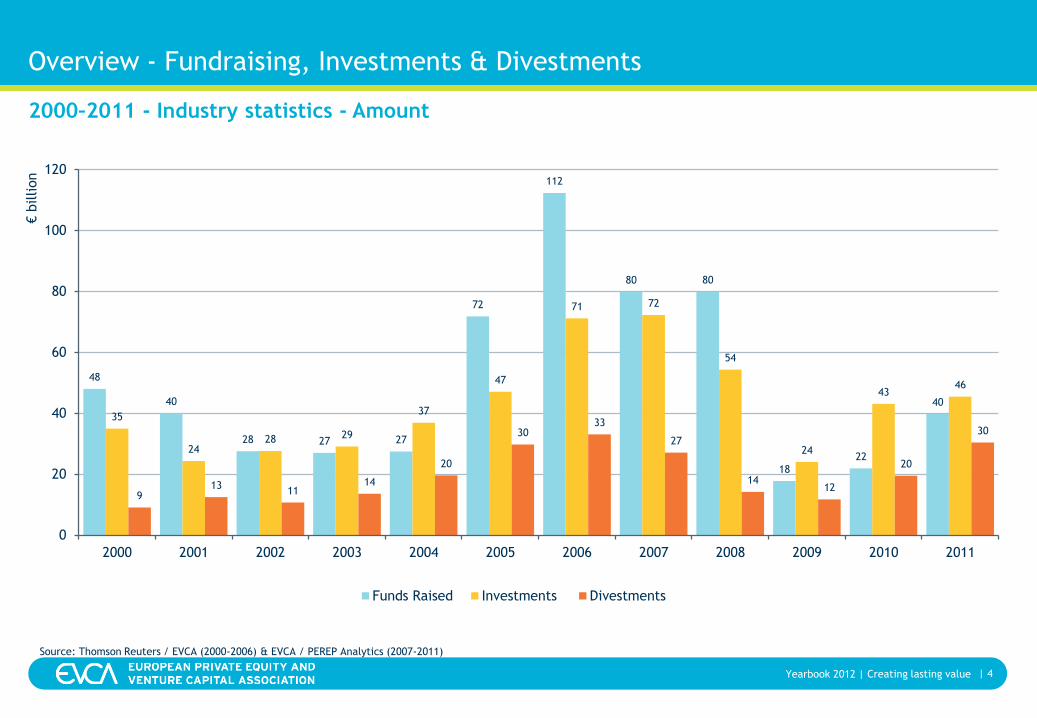

• In 2011 30 bn EUR were divested showing a 50% increase compared to the previous year and almost reaching the 2006 peak. This

increase was triggered by the Buyout & Growth segment which accounted for 92% of the total amount. More than 2000 companies

were divested of which Venture Capital and Buyout & Growth had about an equal share.

• The most preferred exit routs were Trade sale and Secondary sale, together representing more than 60% of the market in terms of

amount divested.

Fundraising

Investments

Divestments

• Investments remained stable at 46 bn EUR showing a 6% increase from 2010. This figure resembles the investment level of 2005.

Buyout & Growth accounted for 91% of the total amount invested.

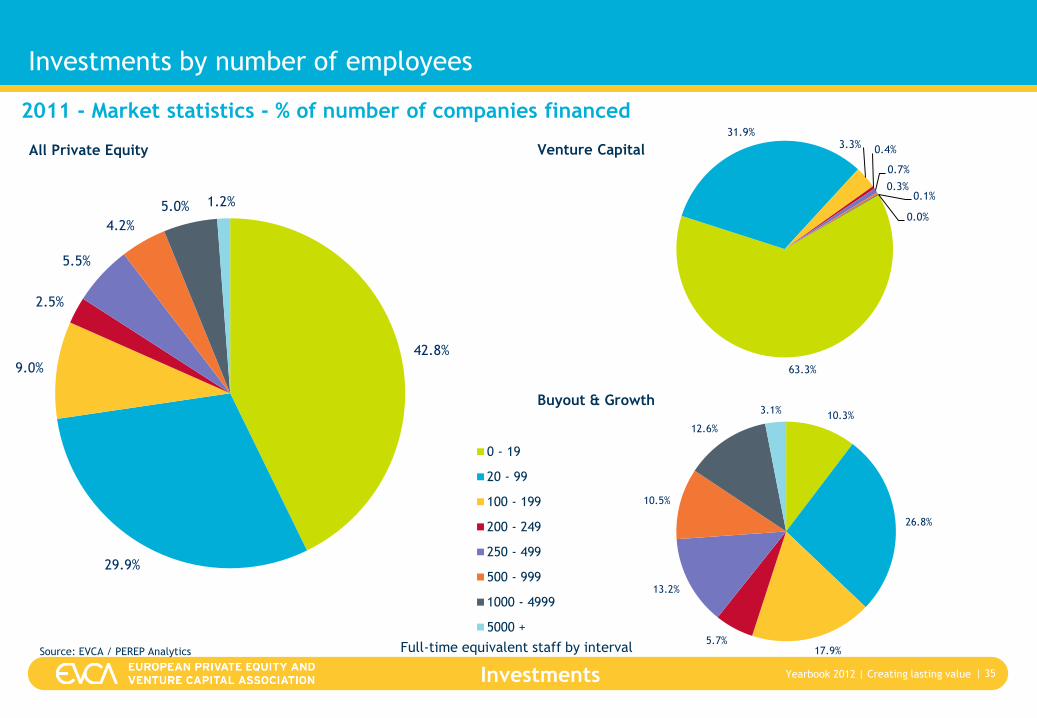

• In 2011 more than 4,800 companies received investments in Europe out of which SMEs accounted for 85% with an average

investment per company of 3m EUR. More than 60% of these investments were attribute to Venture Capital.

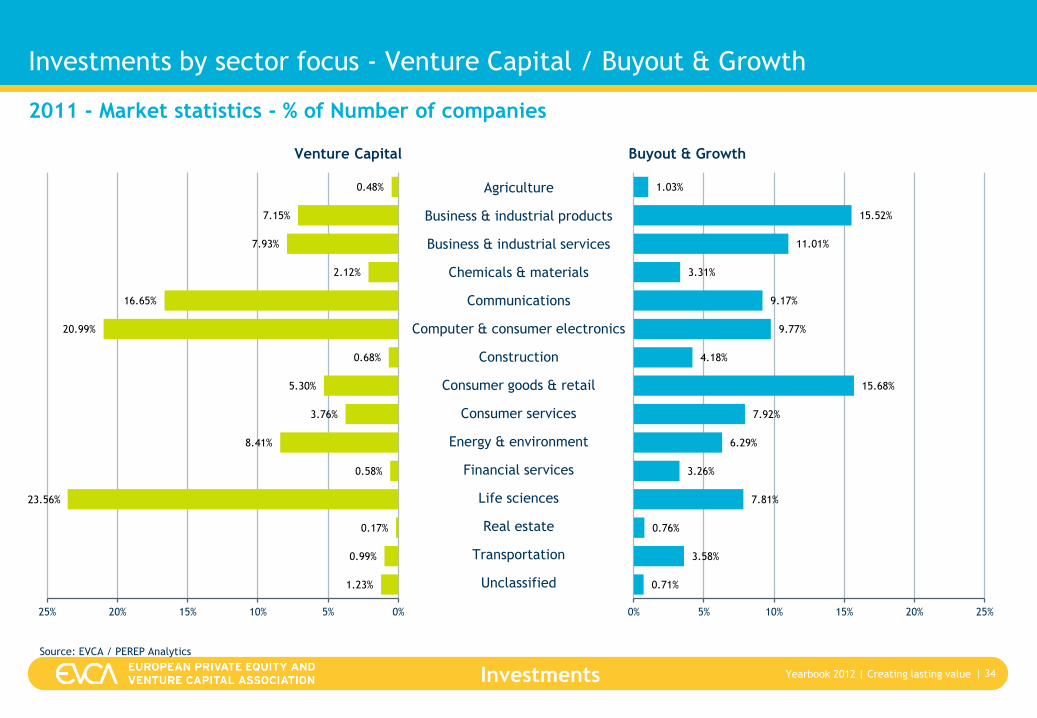

• The three most targeted sectors by number of companies in 2011 were Life sciences, Computer & consumer electronics and

Communications together accounting for 50% of the total. The stage focus split reveals a sector specificity in case of Venture

Capital (Life sciences, Computer & consumer electronics and Communications) and a more homogeneous distribution for Buyout &

Growth.

• In 2011 overall fundraising increased by 80% to 40 bn EUR compared to the previous year, matching 2001 level. VC contributed to

this trend with its 50% increase compared to 2010. The buyout & growth segment almost grew by 100% compared to 2010 and

attributed for 30 bn EUR. More than half of the buyout amount raised came from pension funds, banks and fund of funds.

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012

Overview - Fundraising, Investments & Divestments

| 4

2000–2011 - Industry statistics - Amount

48

40

28 27 27

72

112

80 80

18

22

40

35

2428 29

37

47

71 72

54

24

4346

913

1114

20

3033

27

1412

20

30

0

20

40

60

80

100

120

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

€billion

Funds Raised Investments Divestments

Source: Thomson Reuters / EVCA (2000-2006) & EVCA / PEREP Analytics (2007-2011)

Fundraising

Fundraising Statistics explained:

• Current direct funds under management monitored are primarily focused on investments in Europe.

• Funds raised are recorded in the country of the advisory team that is raising/managing the fund (“industry

statistics”).

• The funds included in the statistics are: private equity funds making direct private equity investments,

mezzanine private equity funds, co-investment funds, rescue/turnaround funds.

• The following funds are excluded from the statistics: infrastructure funds, real estate funds, distress debt

funds, primary funds-of-funds, secondary funds-of-funds.

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Fundraising

Glossary – Fundraising

| 6

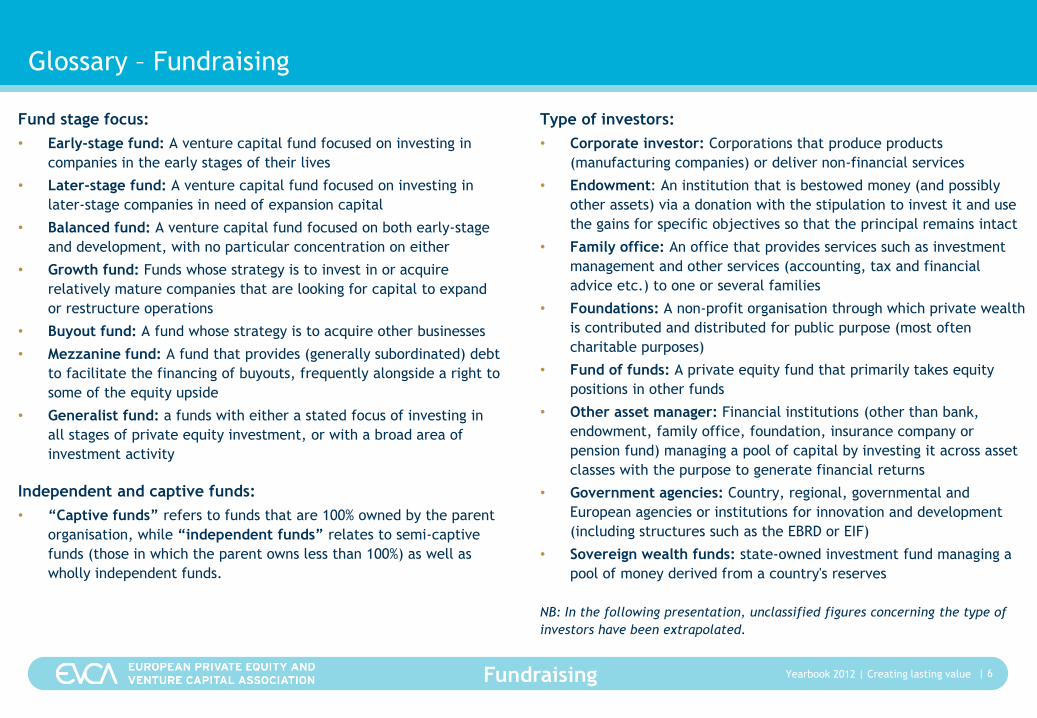

Fund stage focus:

• Early-stage fund: A venture capital fund focused on investing in

companies in the early stages of their lives

• Later-stage fund: A venture capital fund focused on investing in

later-stage companies in need of expansion capital

• Balanced fund: A venture capital fund focused on both early-stage

and development, with no particular concentration on either

• Growth fund: Funds whose strategy is to invest in or acquire

relatively mature companies that are looking for capital to expand

or restructure operations

• Buyout fund: A fund whose strategy is to acquire other businesses

• Mezzanine fund: A fund that provides (generally subordinated) debt

to facilitate the financing of buyouts, frequently alongside a right to

some of the equity upside

• Generalist fund: a funds with either a stated focus of investing in

all stages of private equity investment, or with a broad area of

investment activity

Type of investors:

• Corporate investor: Corporations that produce products

(manufacturing companies) or deliver non-financial services

• Endowment: An institution that is bestowed money (and possibly

other assets) via a donation with the stipulation to invest it and use

the gains for specific objectives so that the principal remains intact

• Family office: An office that provides services such as investment

management and other services (accounting, tax and financial

advice etc.) to one or several families

• Foundations: A non-profit organisation through which private wealth

is contributed and distributed for public purpose (most often

charitable purposes)

• Fund of funds: A private equity fund that primarily takes equity

positions in other funds

• Other asset manager: Financial institutions (other than bank,

endowment, family office, foundation, insurance company or

pension fund) managing a pool of capital by investing it across asset

classes with the purpose to generate financial returns

• Government agencies: Country, regional, governmental and

European agencies or institutions for innovation and development

(including structures such as the EBRD or EIF)

• Sovereign wealth funds: state-owned investment fund managing a

pool of money derived from a country's reserves

NB: In the following presentation, unclassified figures concerning the type of

investors have been extrapolated.

Independent and captive funds:

• “Captive funds” refers to funds that are 100% owned by the parent

organisation, while “independent funds” relates to semi-captive

funds (those in which the parent owns less than 100%) as well as

wholly independent funds.

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Fundraising

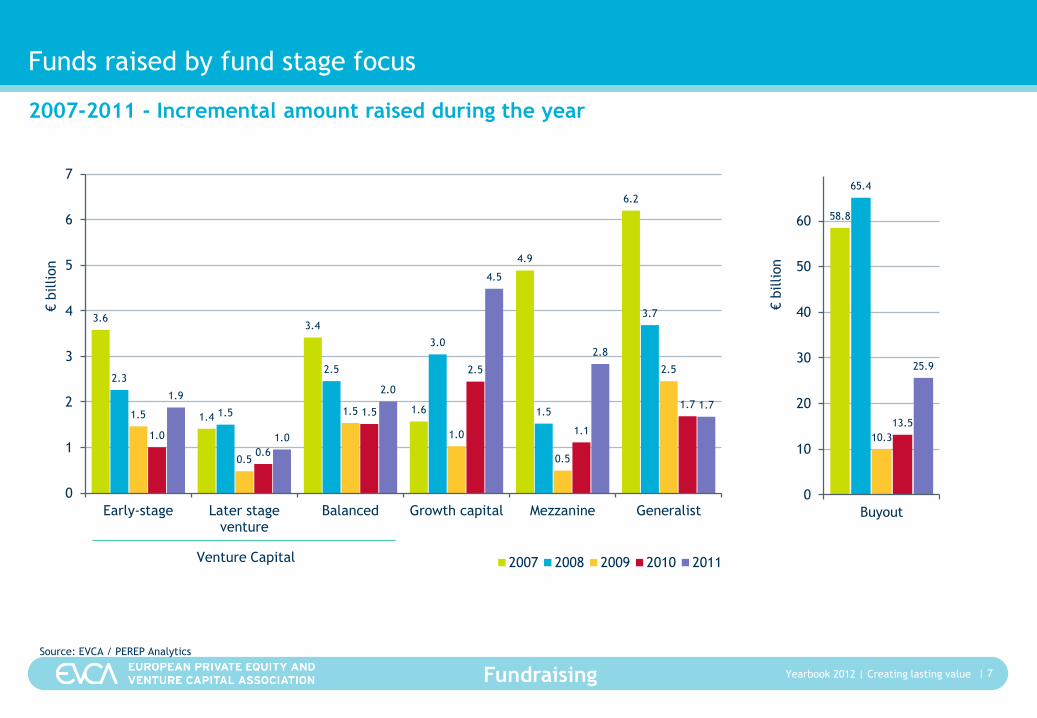

3.6

1.4

3.4

1.6

4.9

6.2

2.3

1.5

2.5

3.0

1.5

3.7

1.5

0.5

1.5

1.0

0.5

2.5

1.0

0.6

1.5

2.5

1.1

1.71.9

1.0

2.0

4.5

2.8

1.7

0

1

2

3

4

5

6

7

Early-stage Later stageventure

Balanced Growth capital Mezzanine Generalist

€billion

2007 2008 2009 2010 2011

Funds raised by fund stage focus

| 7

2007-2011 - Incremental amount raised during the year

Source: EVCA / PEREP Analytics

Venture Capital

58.8

65.4

10.3

13.5

25.9

0

10

20

30

40

50

60

Buyout

€billion

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Fundraising

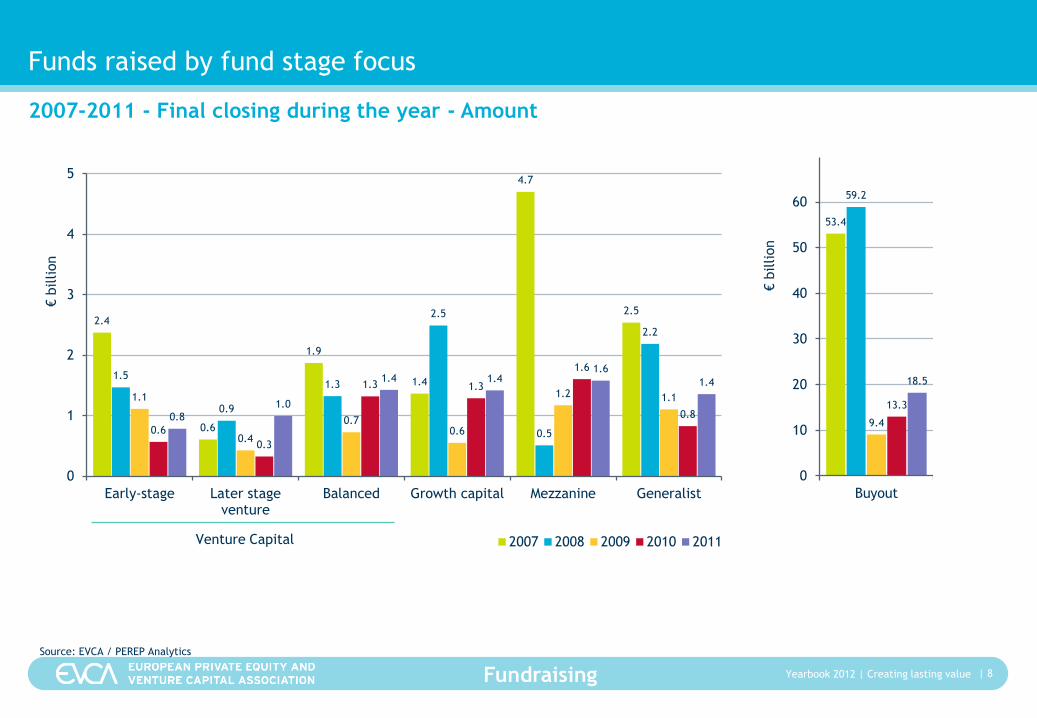

2.4

0.6

1.9

1.4

4.7

2.5

1.5

0.9

1.3

2.5

0.5

2.2

1.1

0.4

0.70.6

1.2 1.1

0.6

0.3

1.3 1.3

1.6

0.80.8

1.0

1.4 1.41.6

1.4

0

1

2

3

4

5

Early-stage Later stageventure

Balanced Growth capital Mezzanine Generalist

€billion

2007 2008 2009 2010 2011

Funds raised by fund stage focus

| 8

Source: EVCA / PEREP Analytics

Venture Capital

2007-2011 - Final closing during the year - Amount

53.4

59.2

9.4

13.3

18.5

0

10

20

30

40

50

60

Buyout

€billion

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Fundraising

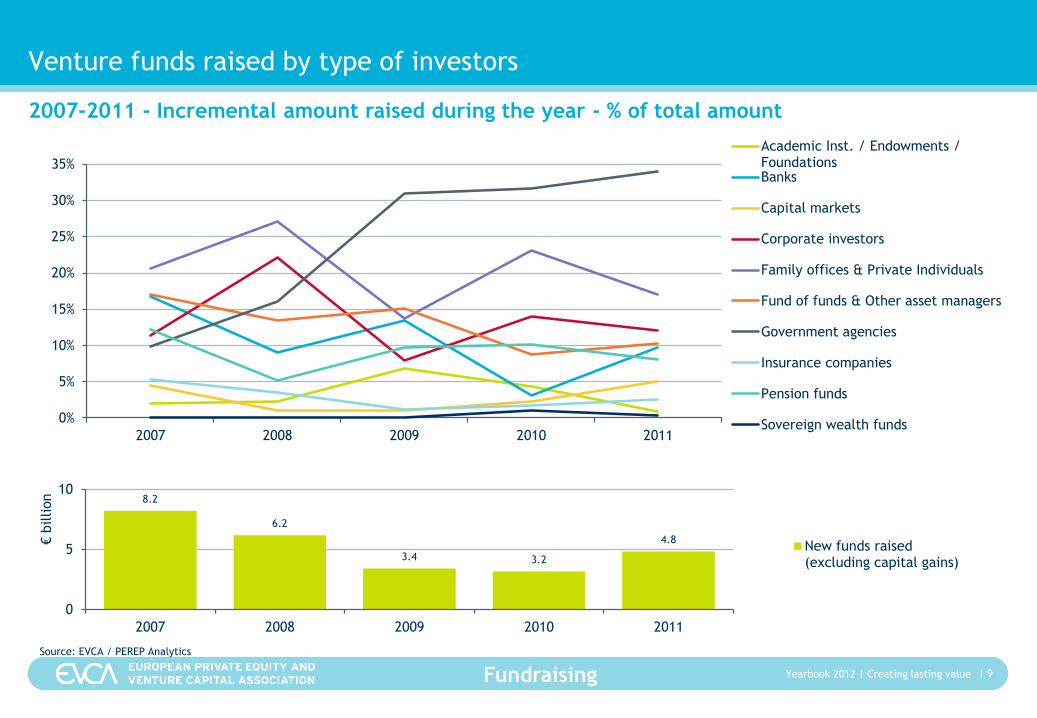

Venture funds raised by type of investors

| 9

2007-2011 - Incremental amount raised during the year - % of total amount

Source: EVCA / PEREP Analytics

8.2

6.2

3.4 3.2

4.8

0

5

10

2007 2008 2009 2010 2011

€billion

New funds raised(excluding capital gains)

0%

5%

10%

15%

20%

25%

30%

35%

2007 2008 2009 2010 2011

Academic Inst. / Endowments /FoundationsBanks

Capital markets

Corporate investors

Family offices & Private Individuals

Fund of funds & Other asset managers

Government agencies

Insurance companies

Pension funds

Sovereign wealth funds

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Fundraising

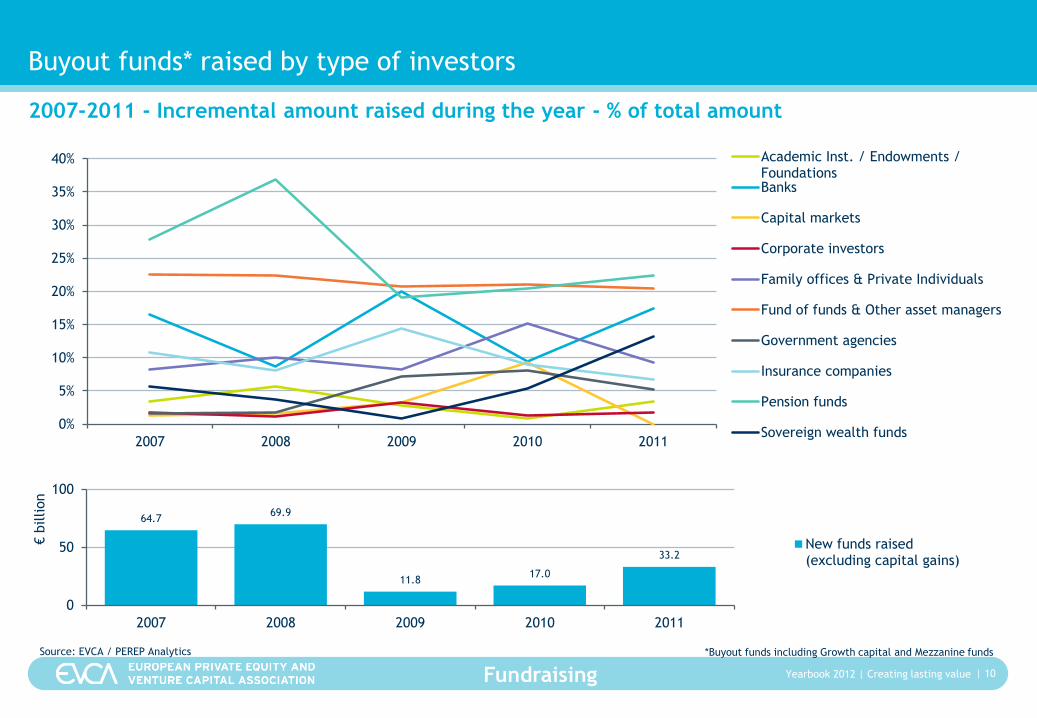

Buyout funds* raised by type of investors

| 10

2007-2011 - Incremental amount raised during the year - % of total amount

Source: EVCA / PEREP Analytics

64.769.9

11.817.0

33.2

0

50

100

2007 2008 2009 2010 2011

€billion

New funds raised(excluding capital gains)

*Buyout funds including Growth capital and Mezzanine funds

0%

5%

10%

15%

20%

25%

30%

35%

40%

2007 2008 2009 2010 2011

Academic Inst. / Endowments /FoundationsBanks

Capital markets

Corporate investors

Family offices & Private Individuals

Fund of funds & Other asset managers

Government agencies

Insurance companies

Pension funds

Sovereign wealth funds

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Fundraising

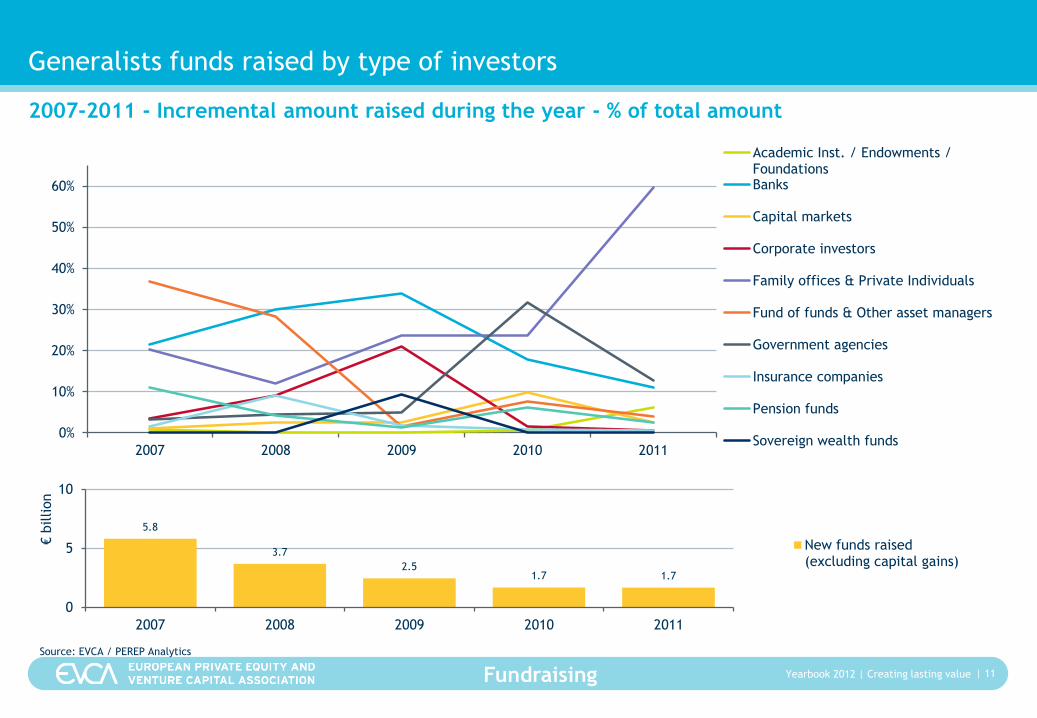

Generalists funds raised by type of investors

| 11

2007-2011 - Incremental amount raised during the year - % of total amount

Source: EVCA / PEREP Analytics

5.8

3.7

2.51.7 1.7

0

5

10

2007 2008 2009 2010 2011

€billion

New funds raised(excluding capital gains)

0%

10%

20%

30%

40%

50%

60%

2007 2008 2009 2010 2011

Academic Inst. / Endowments /FoundationsBanks

Capital markets

Corporate investors

Family offices & Private Individuals

Fund of funds & Other asset managers

Government agencies

Insurance companies

Pension funds

Sovereign wealth funds

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Fundraising

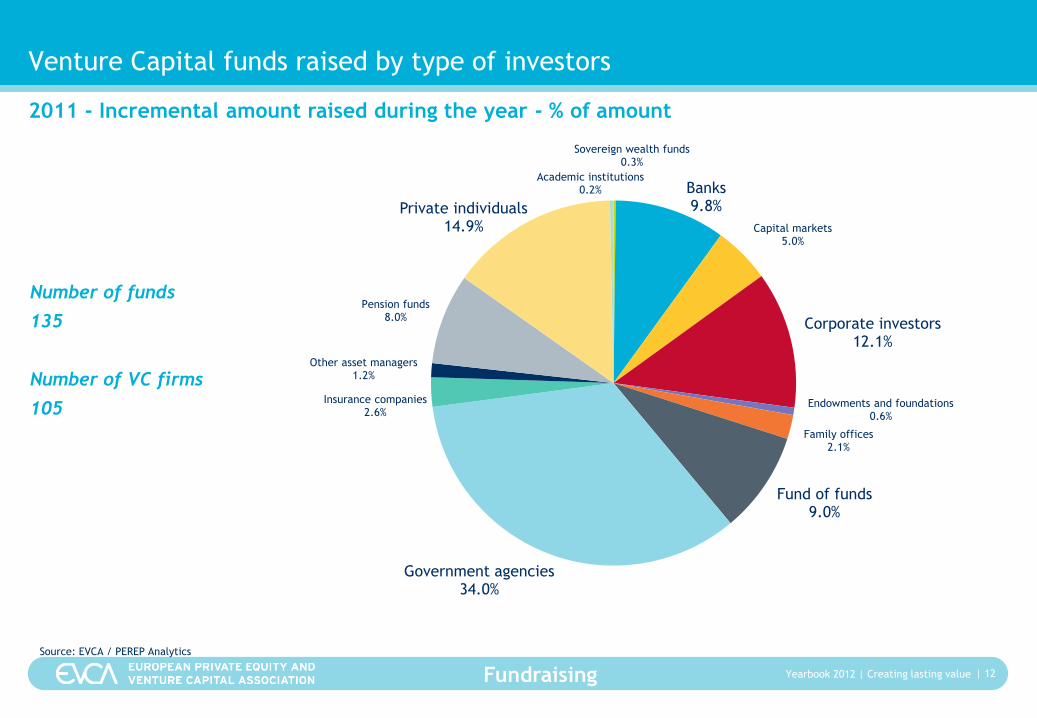

Academic institutions0.2% Banks

9.8%

Capital markets5.0%

Corporate investors12.1%

Endowments and foundations0.6%

Family offices2.1%

Fund of funds9.0%

Government agencies34.0%

Insurance companies2.6%

Other asset managers1.2%

Pension funds8.0%

Private individuals14.9%

Sovereign wealth funds0.3%

Venture Capital funds raised by type of investors

| 12

Number of funds

135

Number of VC firms

105

2011 - Incremental amount raised during the year - % of amount

Source: EVCA / PEREP Analytics

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Fundraising

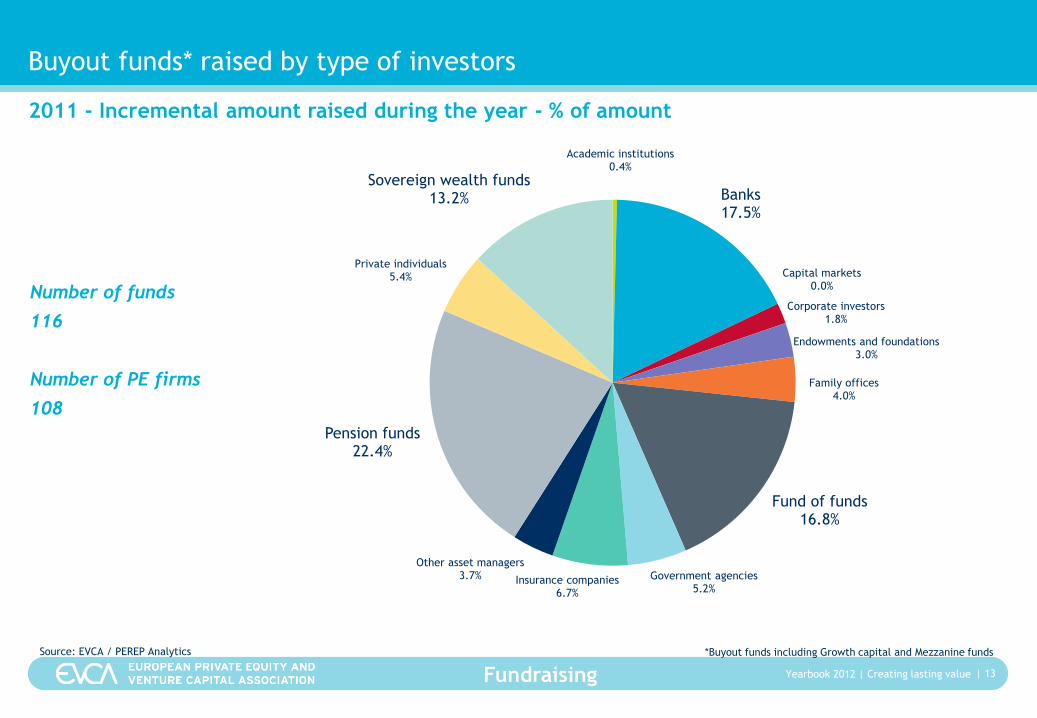

Academic institutions0.4%

Banks17.5%

Capital markets0.0%

Corporate investors1.8%

Endowments and foundations3.0%

Family offices4.0%

Fund of funds16.8%

Government agencies5.2%

Insurance companies6.7%

Other asset managers3.7%

Pension funds22.4%

Private individuals5.4%

Sovereign wealth funds13.2%

Buyout funds* raised by type of investors

| 13

Number of funds

116

Number of PE firms

108

2011 - Incremental amount raised during the year - % of amount

Source: EVCA / PEREP Analytics *Buyout funds including Growth capital and Mezzanine funds

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Fundraising

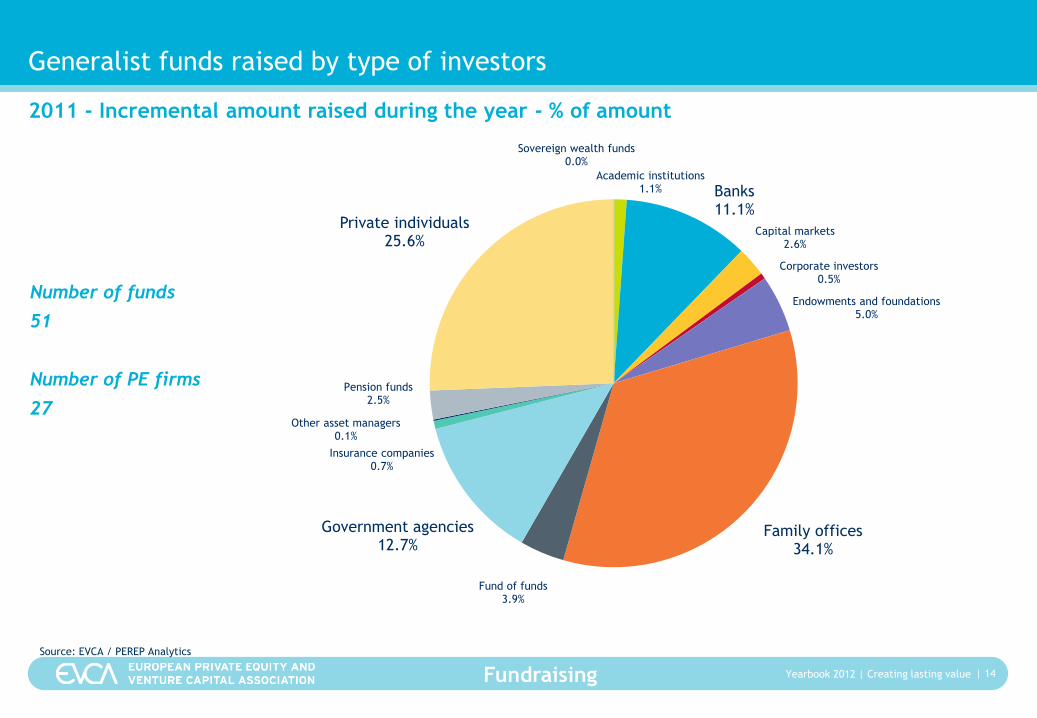

Academic institutions1.1% Banks

11.1%

Capital markets2.6%

Corporate investors0.5%

Endowments and foundations5.0%

Family offices34.1%

Fund of funds3.9%

Government agencies12.7%

Insurance companies0.7%

Other asset managers0.1%

Pension funds2.5%

Private individuals25.6%

Sovereign wealth funds0.0%

Generalist funds raised by type of investors

| 14

Number of funds

51

Number of PE firms

27

2011 - Incremental amount raised during the year - % of amount

Source: EVCA / PEREP Analytics

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Fundraising

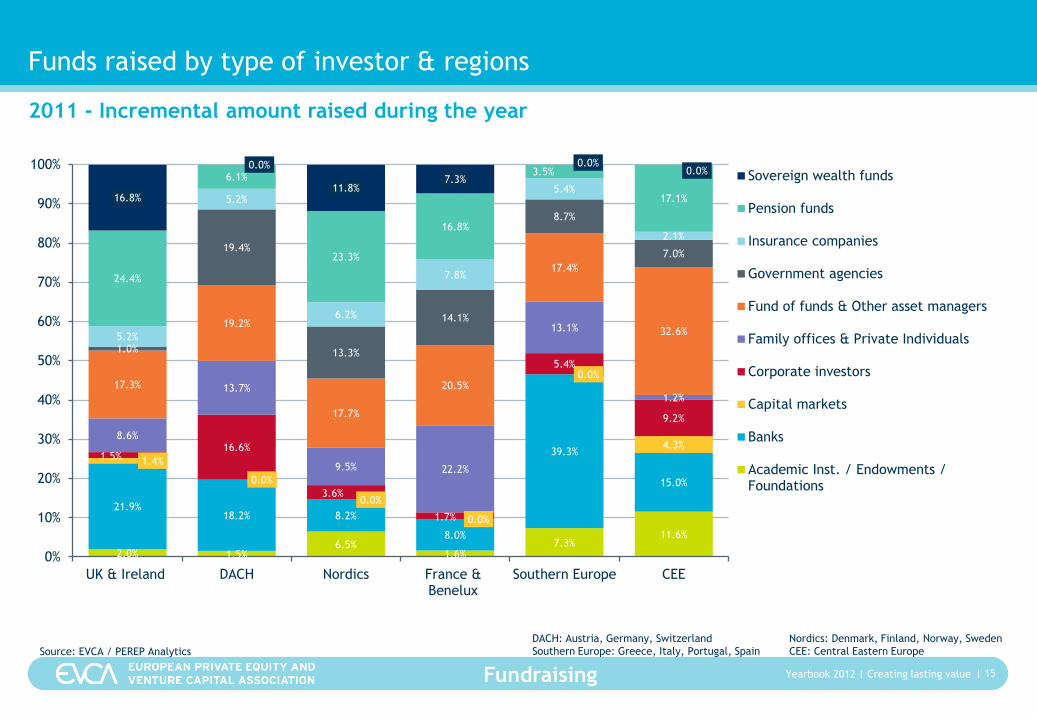

Funds raised by type of investor & regions

| 15

2011 - Incremental amount raised during the year

Source: EVCA / PEREP Analytics

2.0% 1.5%6.5%

1.6%7.3%

11.6%

21.9%18.2% 8.2%

8.0%

39.3%

15.0%

1.4%

0.0%

0.0%

0.0%

0.0%

4.3%1.5%

16.6%

3.6%

1.7%

5.4%

9.2%

8.6%

13.7%

9.5% 22.2%

13.1%

1.2%

17.3%

19.2%

17.7%

20.5%

17.4%

32.6%

1.0%

19.4%

13.3%

14.1%

8.7%

7.0%

5.2%

5.2%

6.2%

7.8%

5.4%

2.1%

24.4%

6.1%

23.3%

16.8%

3.5%

17.1%16.8%

0.0%

11.8%7.3%

0.0%0.0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

UK & Ireland DACH Nordics France &Benelux

Southern Europe CEE

Sovereign wealth funds

Pension funds

Insurance companies

Government agencies

Fund of funds & Other asset managers

Family offices & Private Individuals

Corporate investors

Capital markets

Banks

Academic Inst. / Endowments /Foundations

DACH: Austria, Germany, Switzerland

Southern Europe: Greece, Italy, Portugal, Spain

Nordics: Denmark, Finland, Norway, Sweden

CEE: Central Eastern Europe

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Fundraising

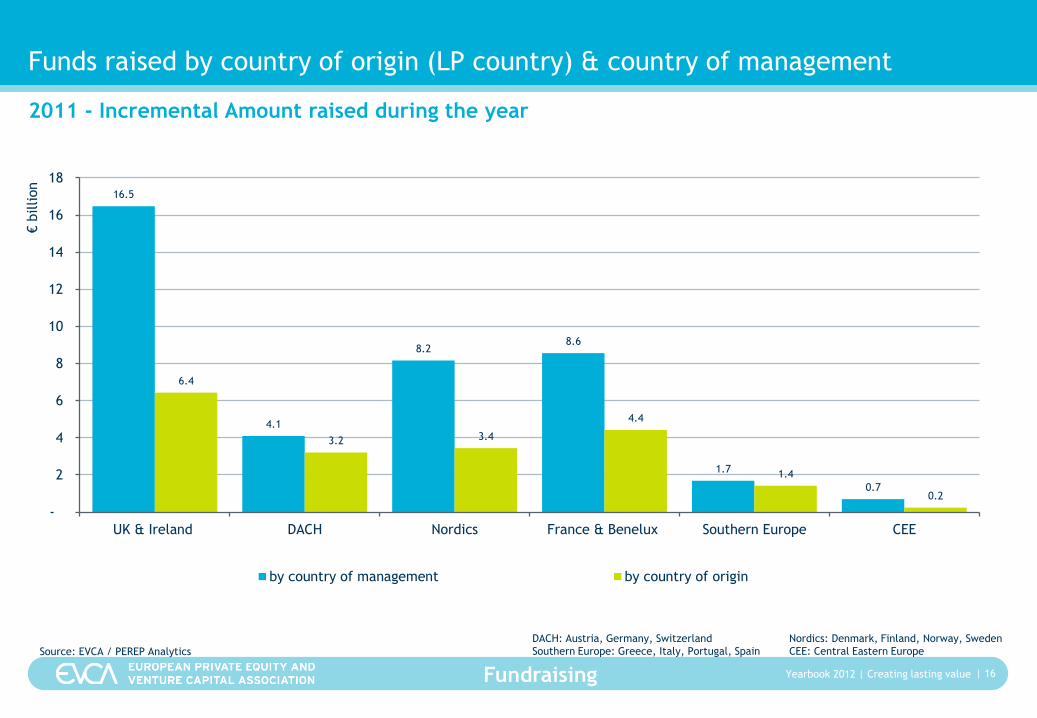

Funds raised by country of origin (LP country) & country of management

| 16

2011 - Incremental Amount raised during the year

Source: EVCA / PEREP Analytics

16.5

4.1

8.28.6

1.7

0.7

6.4

3.2 3.4

4.4

1.4

0.2

-

2

4

6

8

10

12

14

16

18

UK & Ireland DACH Nordics France & Benelux Southern Europe CEE

€billion

by country of management by country of origin

DACH: Austria, Germany, Switzerland

Southern Europe: Greece, Italy, Portugal, Spain

Nordics: Denmark, Finland, Norway, Sweden

CEE: Central Eastern Europe

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Fundraising

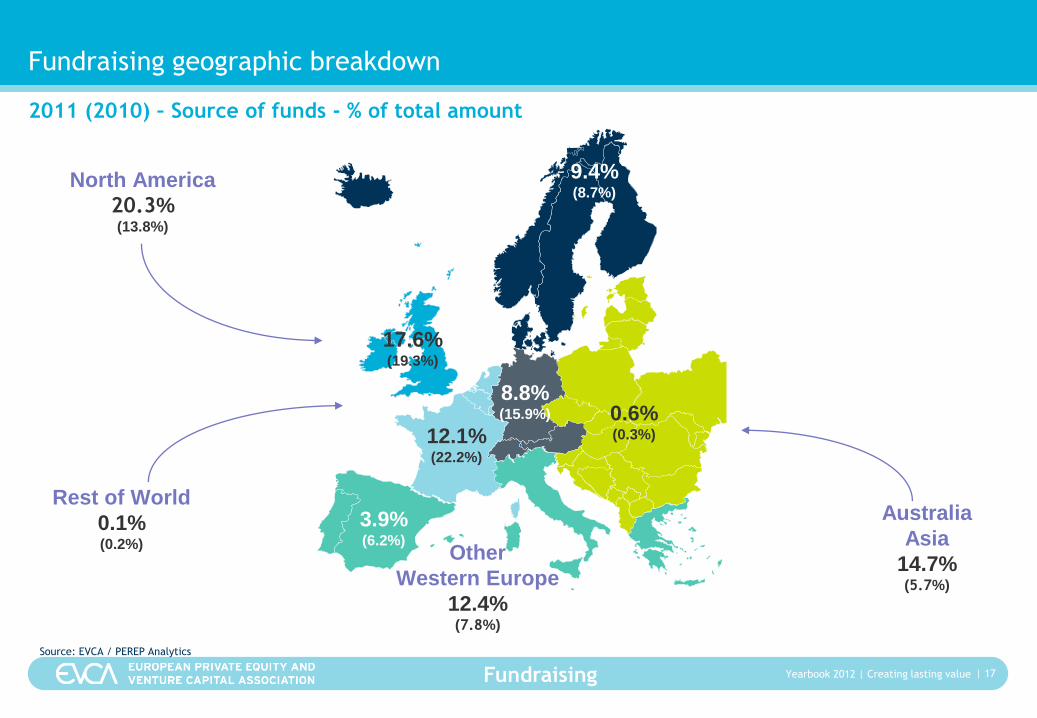

Fundraising geographic breakdown

| 17

17.6% (19.3%)

12.1% (22.2%)

0.6% (0.3%)

Rest of World

0.1% (0.2%)

Australia

Asia

14.7% (5.7%)

North America

20.3% (13.8%)

Other

Western Europe

12.4% (7.8%)

8.8% (15.9%)

3.9% (6.2%)

9.4% (8.7%)

2011 (2010) – Source of funds - % of total amount

Source: EVCA / PEREP Analytics

Investments

Investments Statistics explained:

• Industry statistics are an aggregation of the figures according to the country of location of the private

equity firm’s office in charge of the deal. At the European level, this relates to investments made by

European private equity firms regardless of the location of the target company.

• Market statistics are an aggregation of the figures according to the location of the portfolio company. At

the European level, this relates to investments in European companies regardless of the location of the

private equity firm.

• Equity value: Stricto sensu, the amount of capital invested to acquire shares in an enterprise. The equity

value includes equity, quasi-equity, mezzanine, unsecured debt and secured debt provided by the firm.

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Investments

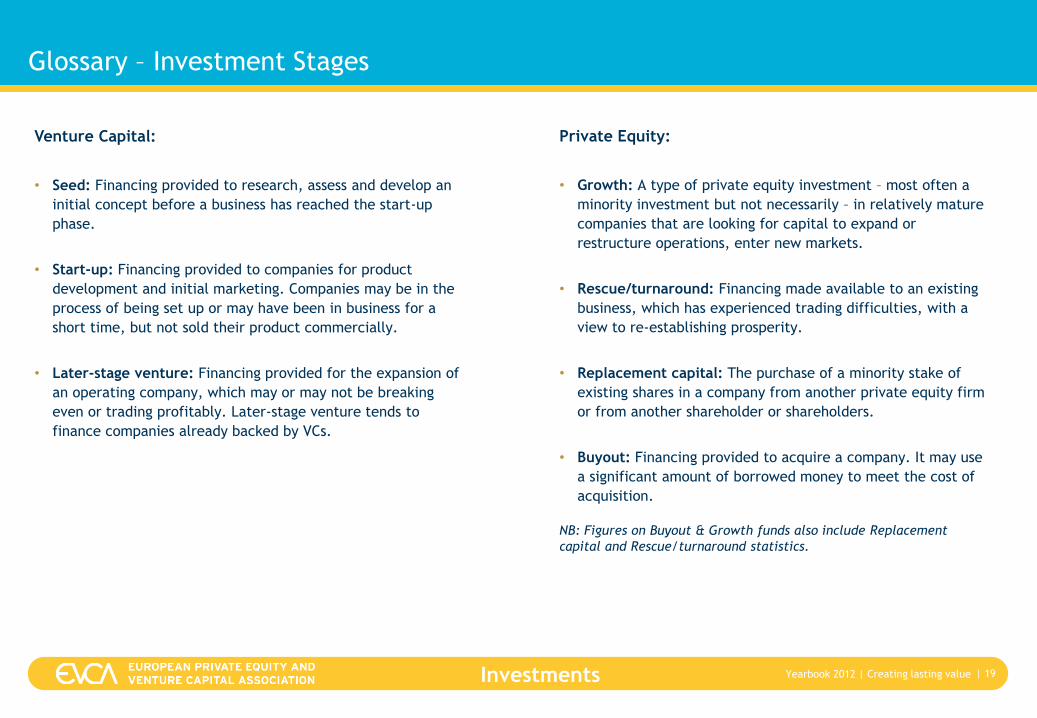

Glossary – Investment Stages

| 19

Venture Capital:

• Seed: Financing provided to research, assess and develop an

initial concept before a business has reached the start-up

phase.

• Start-up: Financing provided to companies for product

development and initial marketing. Companies may be in the

process of being set up or may have been in business for a

short time, but not sold their product commercially.

• Later-stage venture: Financing provided for the expansion of

an operating company, which may or may not be breaking

even or trading profitably. Later-stage venture tends to

finance companies already backed by VCs.

Private Equity:

• Growth: A type of private equity investment – most often a

minority investment but not necessarily – in relatively mature

companies that are looking for capital to expand or

restructure operations, enter new markets.

• Rescue/turnaround: Financing made available to an existing

business, which has experienced trading difficulties, with a

view to re-establishing prosperity.

• Replacement capital: The purchase of a minority stake of

existing shares in a company from another private equity firm

or from another shareholder or shareholders.

• Buyout: Financing provided to acquire a company. It may use

a significant amount of borrowed money to meet the cost of

acquisition.

NB: Figures on Buyout & Growth funds also include Replacement

capital and Rescue/turnaround statistics.

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Investments

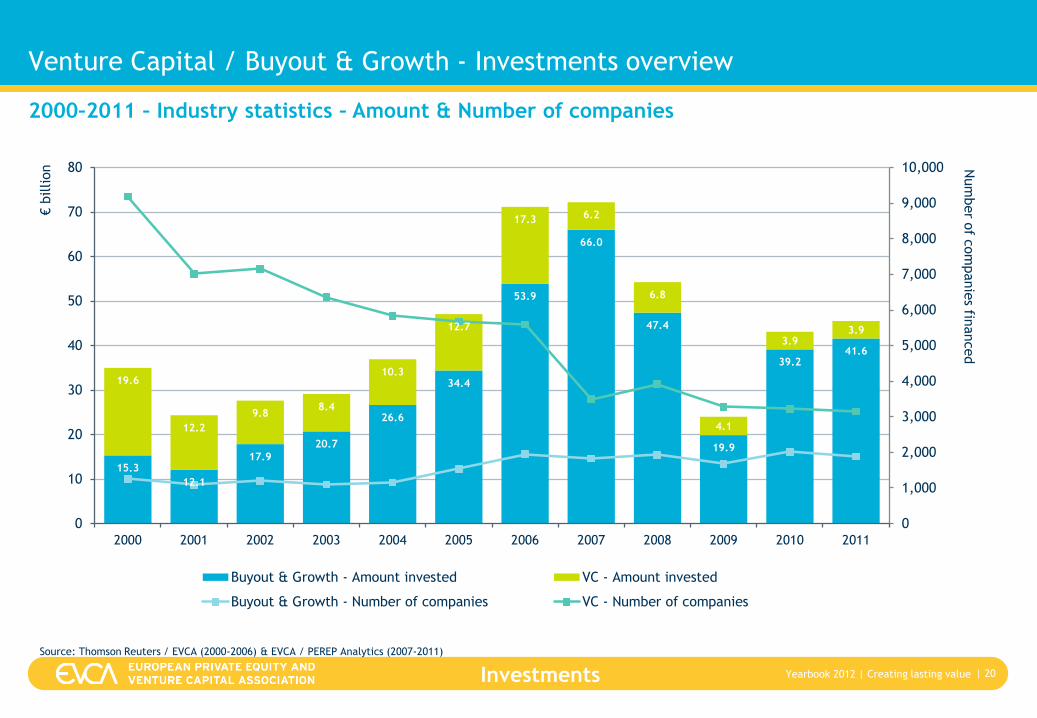

Venture Capital / Buyout & Growth - Investments overview

| 20

2000–2011 – Industry statistics – Amount & Number of companies

Source: Thomson Reuters / EVCA (2000-2006) & EVCA / PEREP Analytics (2007-2011)

15.3

12.1

17.9

20.7

26.6

34.4

53.9

66.0

47.4

19.9

39.241.6

19.6

12.2

9.88.4

10.3

12.7

17.3 6.2

6.8

4.1

3.93.9

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

0

10

20

30

40

50

60

70

80

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Num

ber o

f com

panie

s financed

€billion

Buyout & Growth - Amount invested VC - Amount invested

Buyout & Growth - Number of companies VC - Number of companies

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Investments

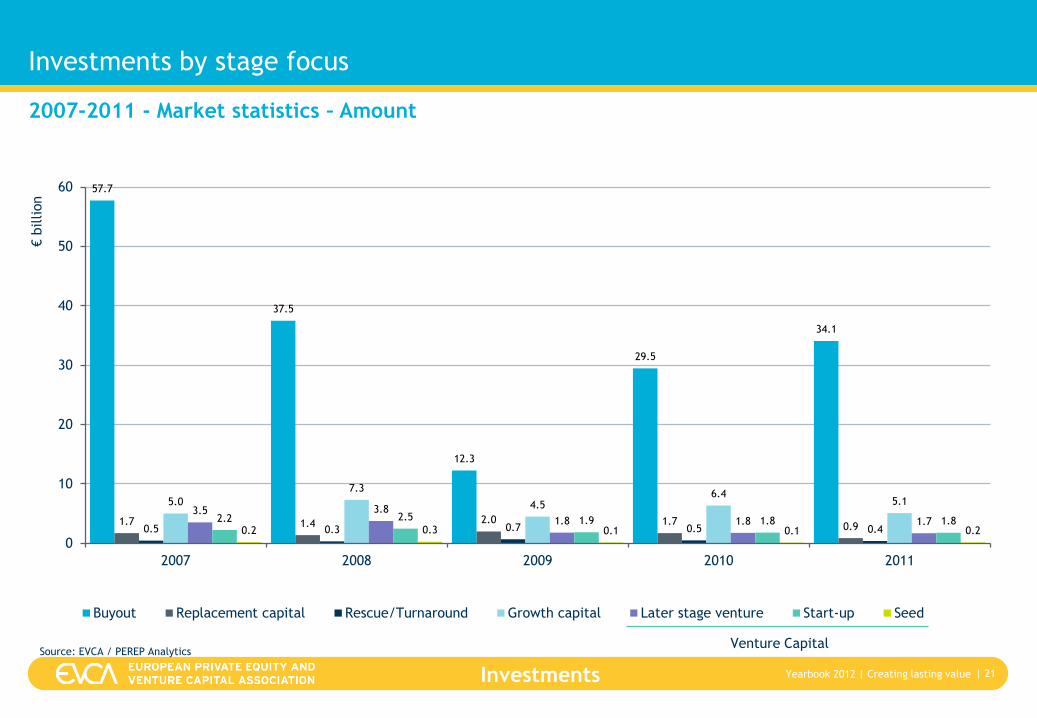

Investments by stage focus

| 21

2007-2011 - Market statistics – Amount

Source: EVCA / PEREP Analytics

57.7

37.5

12.3

29.5

34.1

1.7 1.4 2.0 1.70.90.5 0.3 0.7 0.5 0.4

5.0

7.3

4.56.4

5.13.5 3.8

1.8 1.8 1.72.2 2.5 1.9 1.8 1.80.2 0.3 0.1 0.1 0.2

0

10

20

30

40

50

60

2007 2008 2009 2010 2011

€billion

Buyout Replacement capital Rescue/Turnaround Growth capital Later stage venture Start-up Seed

Venture Capital

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Investments

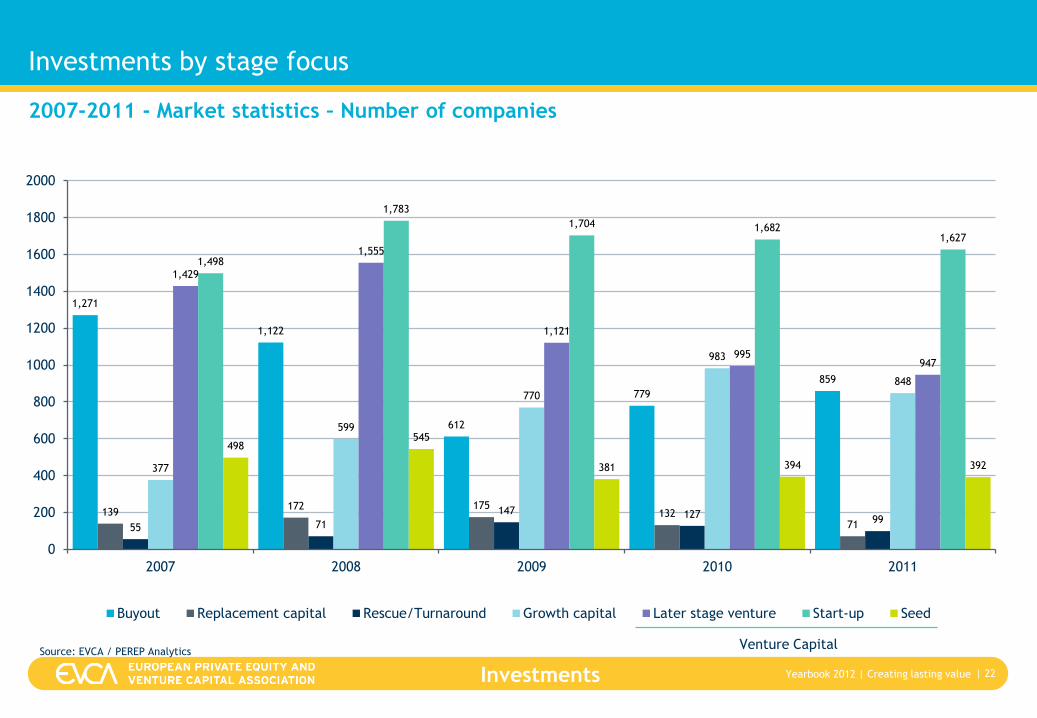

Investments by stage focus

| 22

2007-2011 - Market statistics – Number of companies

Source: EVCA / PEREP Analytics

1,271

1,122

612

779

859

139172 175

1327155 71

147 12799

377

599

770

983

848

1,429

1,555

1,121

995947

1,498

1,783

1,704 1,6821,627

498545

381 394 392

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2007 2008 2009 2010 2011

Buyout Replacement capital Rescue/Turnaround Growth capital Later stage venture Start-up Seed

Venture Capital

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Investments

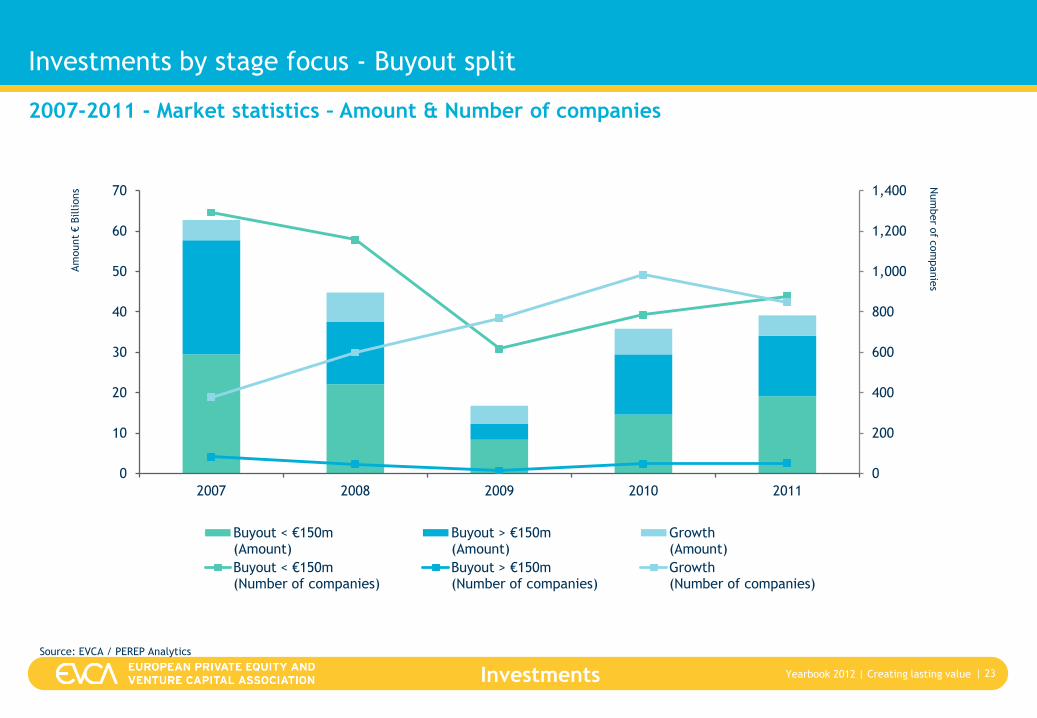

Investments by stage focus - Buyout split

| 23

Source: EVCA / PEREP Analytics

2007-2011 - Market statistics – Amount & Number of companies

0

200

400

600

800

1,000

1,200

1,400

0

10

20

30

40

50

60

70

2007 2008 2009 2010 2011

Num

ber o

f com

panie

s

Am

ount

€Billions

Buyout < €150m (Amount)

Buyout > €150m(Amount)

Growth(Amount)

Buyout < €150m (Number of companies)

Buyout > €150m (Number of companies)

Growth(Number of companies)

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Investments

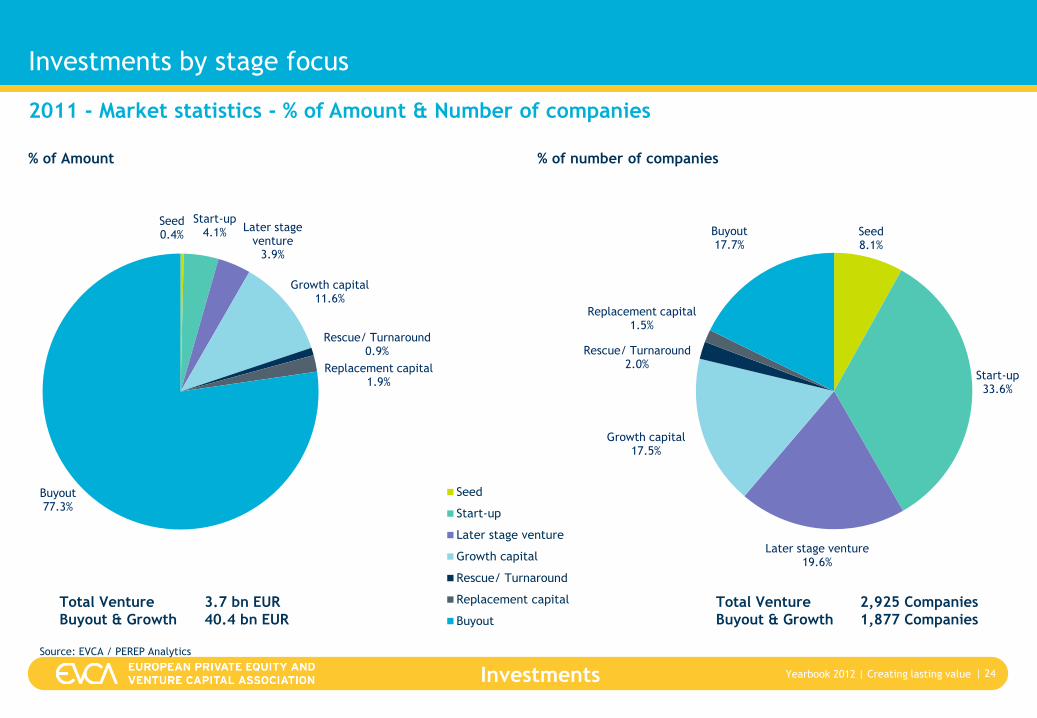

Investments by stage focus

| 24

% of Amount % of number of companies

2011 - Market statistics - % of Amount & Number of companies

Source: EVCA / PEREP Analytics

Seed0.4%

Start-up4.1% Later stage

venture3.9%

Growth capital11.6%

Rescue/ Turnaround0.9%

Replacement capital1.9%

Buyout77.3%

Seed

Start-up

Later stage venture

Growth capital

Rescue/Turnaround

Replacementcapital

Buyout

Seed8.1%

Start-up33.6%

Later stage venture19.6%

Growth capital17.5%

Rescue/ Turnaround2.0%

Replacement capital1.5%

Buyout17.7% Seed

Start-up

Later stage venture

Growth capital

Rescue/Turnaround

Replacementcapital

Buyout

Seed0.4%

Start-up4.1%

Later stage venture

3.9%Growth capital11.6%Rescue/ Turnaround

0.9%Replacement capital1.9%

Buyout77.3%

Seed

Start-up

Later stage venture

Growth capital

Rescue/ Turnaround

Replacement capital

Buyout

Total Venture 3.7 bn EUR

Buyout & Growth 40.4 bn EUR

Total Venture 2,925 Companies

Buyout & Growth 1,877 Companies

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Investments

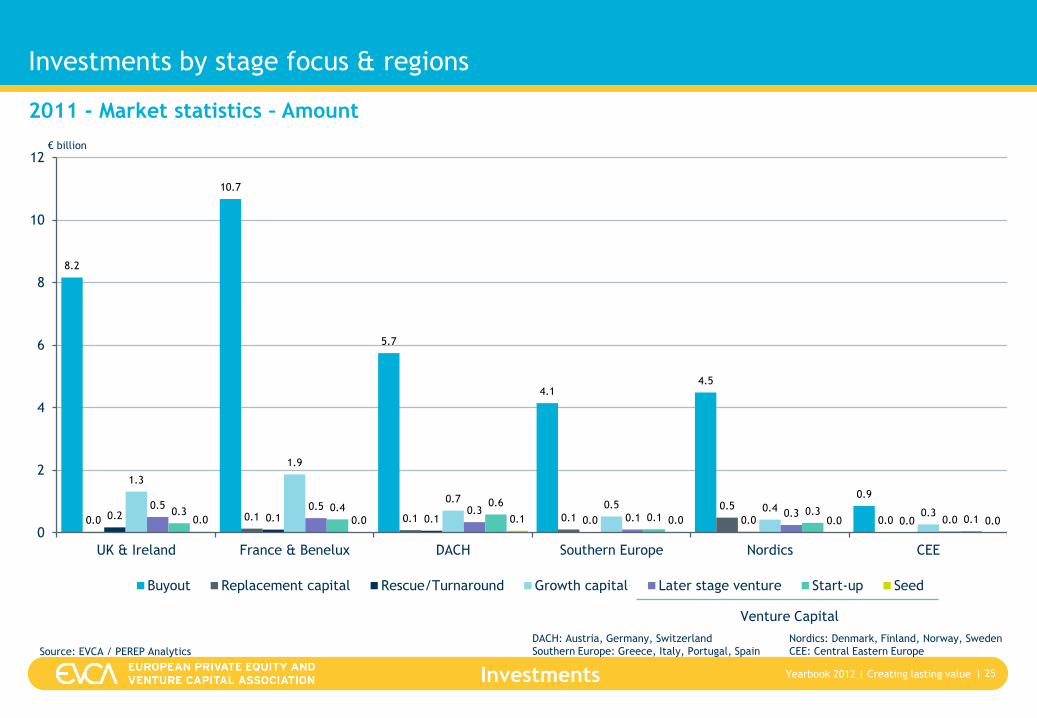

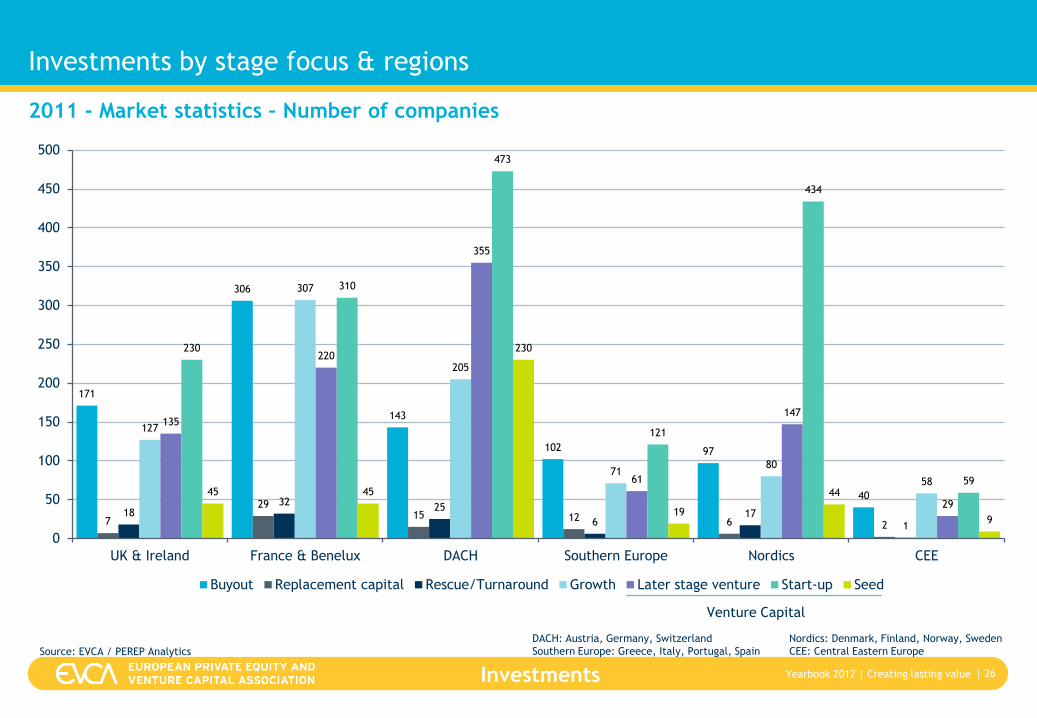

Investments by stage focus & regions

| 25

2011 - Market statistics – Amount

Source: EVCA / PEREP Analytics

8.2

10.7

5.7

4.14.5

0.9

0.0 0.1 0.1 0.10.5

0.00.2 0.1 0.1 0.0 0.0 0.0

1.3

1.9

0.70.5 0.4 0.3

0.5 0.5 0.30.1 0.3

0.00.3 0.4 0.6

0.10.3

0.10.0 0.0 0.1 0.0 0.0 0.0

0

2

4

6

8

10

12

UK & Ireland France & Benelux DACH Southern Europe Nordics CEE

€ billion

Buyout Replacement capital Rescue/Turnaround Growth capital Later stage venture Start-up Seed

DACH: Austria, Germany, Switzerland

Southern Europe: Greece, Italy, Portugal, Spain

Nordics: Denmark, Finland, Norway, Sweden

CEE: Central Eastern Europe

Venture Capital

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Investments

Investments by stage focus & regions

| 26

2011 - Market statistics – Number of companies

Source: EVCA / PEREP Analytics

171

306

143

102 97

40

7

2915 12 6 2

1832

25

617

1

127

307

205

7180

58

135

220

355

61

147

29

230

310

473

121

434

5945 45

230

19

44

9

0

50

100

150

200

250

300

350

400

450

500

UK & Ireland France & Benelux DACH Southern Europe Nordics CEE

Buyout Replacement capital Rescue/Turnaround Growth Later stage venture Start-up Seed

Venture Capital

DACH: Austria, Germany, Switzerland

Southern Europe: Greece, Italy, Portugal, Spain

Nordics: Denmark, Finland, Norway, Sweden

CEE: Central Eastern Europe

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Investments

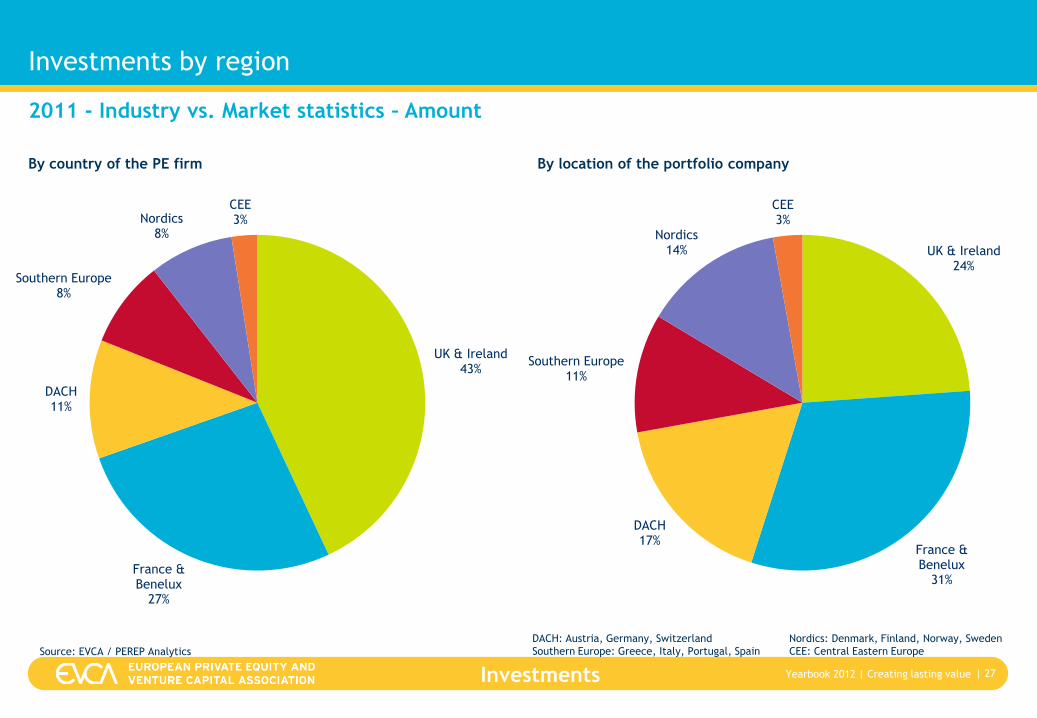

Investments by region

| 27

By country of the PE firm By location of the portfolio company

2011 - Industry vs. Market statistics – Amount

Source: EVCA / PEREP Analytics

UK & Ireland43%

France & Benelux

27%

DACH11%

Southern Europe8%

Nordics8%

CEE3%

UK & Ireland24%

France & Benelux

31%

DACH17%

Southern Europe11%

Nordics14%

CEE3%

DACH: Austria, Germany, Switzerland

Southern Europe: Greece, Italy, Portugal, Spain

Nordics: Denmark, Finland, Norway, Sweden

CEE: Central Eastern Europe

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Investments

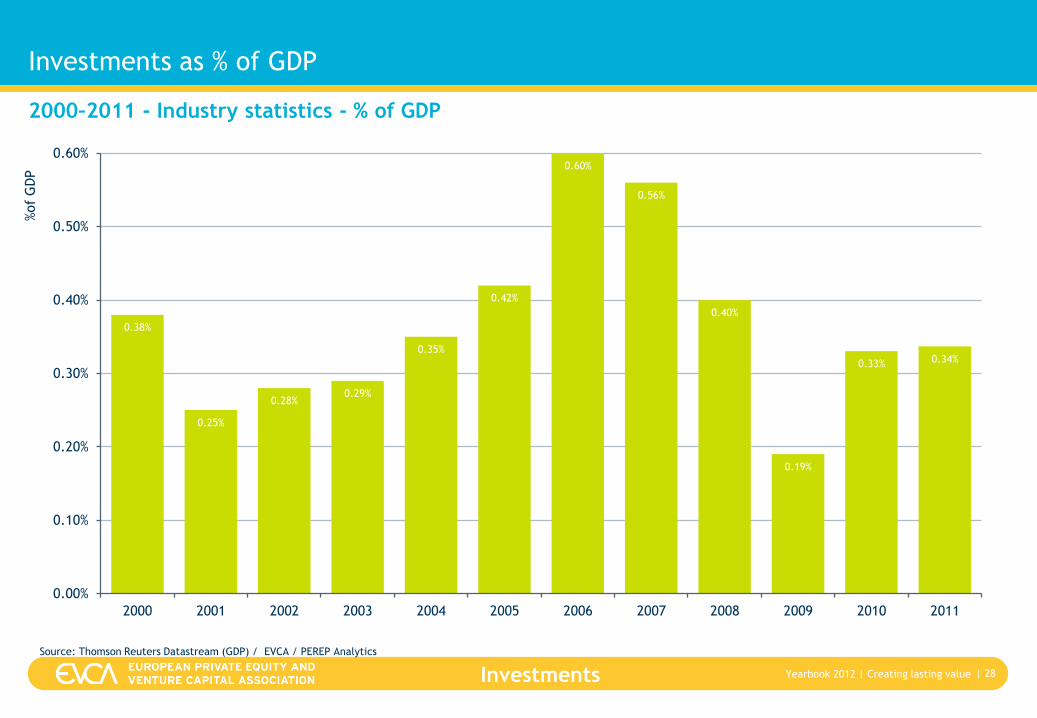

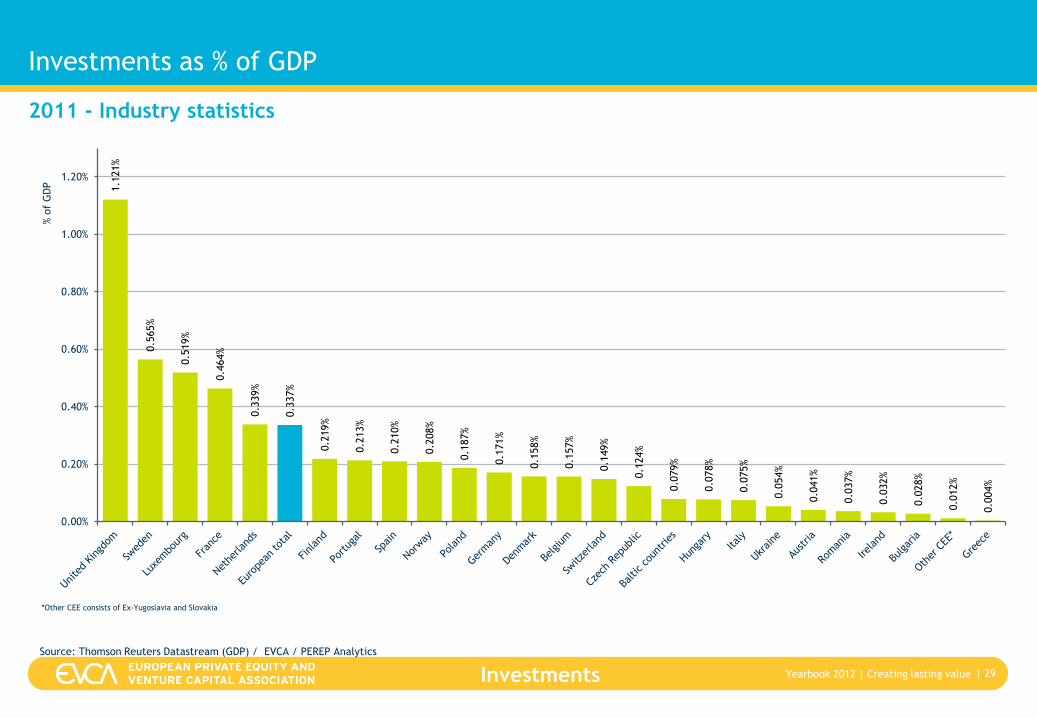

Investments as % of GDP

| 28

2000–2011 - Industry statistics - % of GDP

Source: Thomson Reuters Datastream (GDP) / EVCA / PEREP Analytics

0.38%

0.25%

0.28%0.29%

0.35%

0.42%

0.60%

0.56%

0.40%

0.19%

0.33% 0.34%

0.00%

0.10%

0.20%

0.30%

0.40%

0.50%

0.60%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

%of

GD

P

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Investments

Investments as % of GDP

| 29

*Other CEE consists of Ex-Yugoslavia and Slovakia

2011 - Industry statistics 1.1

21%

0.5

65%

0.5

19%

0.4

64%

0.3

39%

0.3

37%

0.2

19%

0.2

13%

0.2

10%

0.2

08%

0.1

87%

0.1

71%

0.1

58%

0.1

57%

0.1

49%

0.1

24%

0.0

79%

0.0

78%

0.0

75%

0.0

54%

0.0

41%

0.0

37%

0.0

32%

0.0

28%

0.0

12%

0.0

04%

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

% o

f G

DP

Source: Thomson Reuters Datastream (GDP) / EVCA / PEREP Analytics

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Investments

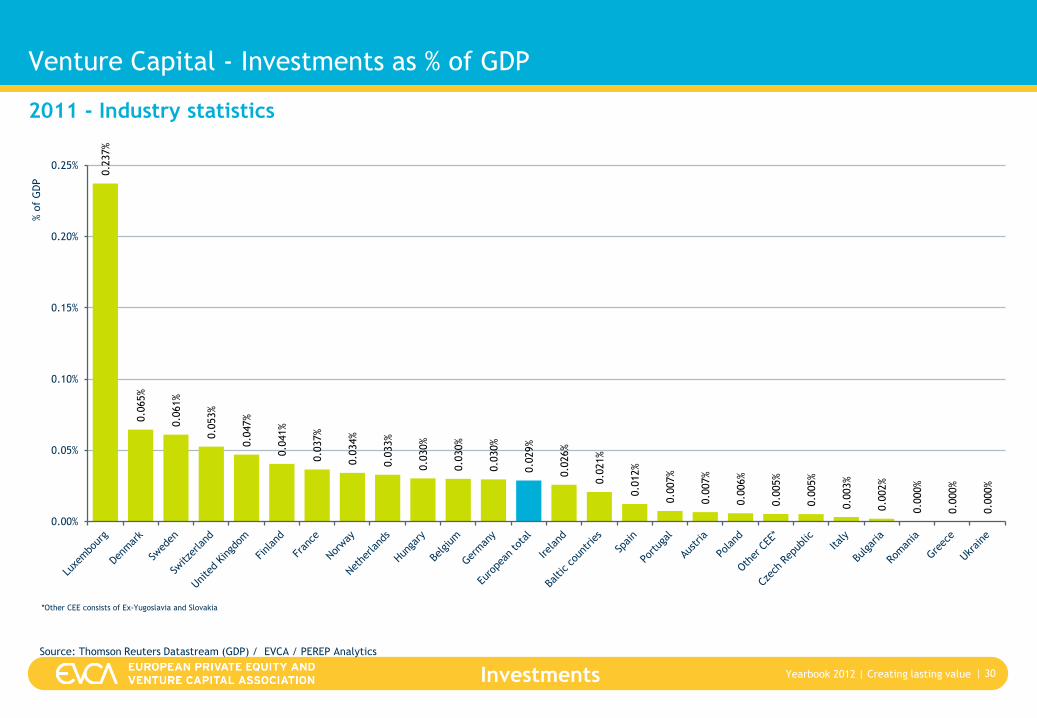

Venture Capital - Investments as % of GDP

| 30

2011 - Industry statistics

*Other CEE consists of Ex-Yugoslavia and Slovakia

0.2

37%

0.0

65%

0.0

61%

0.0

53%

0.0

47%

0.0

41%

0.0

37%

0.0

34%

0.0

33%

0.0

30%

0.0

30%

0.0

30%

0.0

29%

0.0

26%

0.0

21%

0.0

12%

0.0

07%

0.0

07%

0.0

06%

0.0

05%

0.0

05%

0.0

03%

0.0

02%

0.0

00%

0.0

00%

0.0

00%

0.00%

0.05%

0.10%

0.15%

0.20%

0.25%

% o

f G

DP

Source: Thomson Reuters Datastream (GDP) / EVCA / PEREP Analytics

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Investments

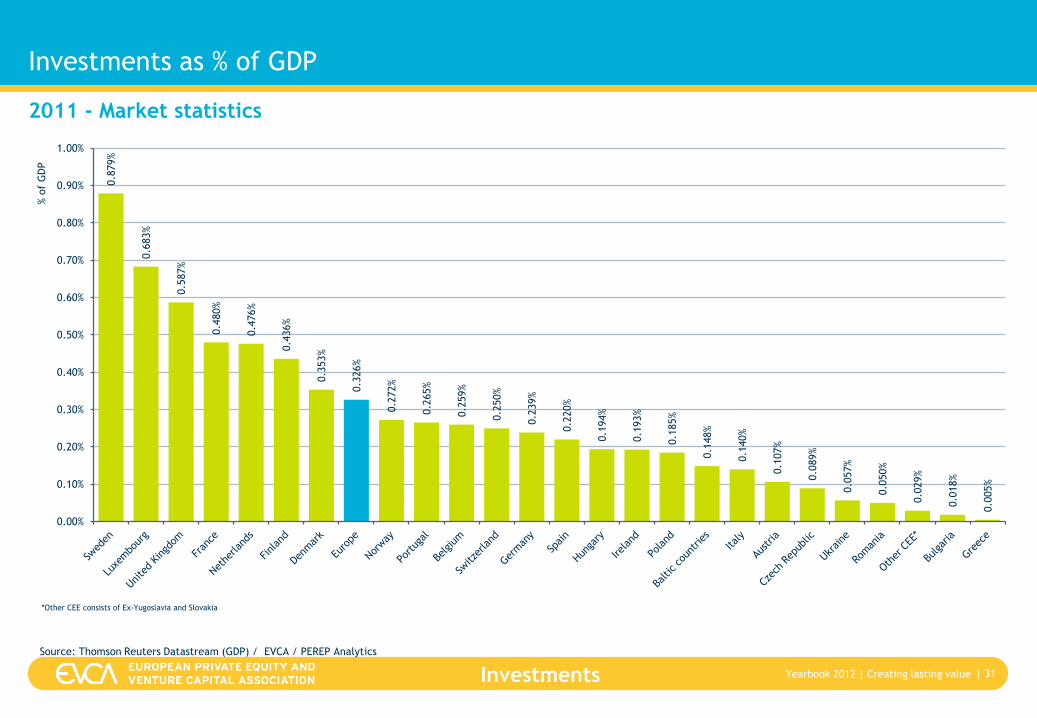

Investments as % of GDP

| 31

2011 - Market statistics

*Other CEE consists of Ex-Yugoslavia and Slovakia

0.8

79%

0.6

83%

0.5

87%

0.4

80%

0.4

76%

0.4

36%

0.3

53%

0.3

26%

0.2

72%

0.2

65%

0.2

59%

0.2

50%

0.2

39%

0.2

20%

0.1

94%

0.1

93%

0.1

85%

0.1

48%

0.1

40%

0.1

07%

0.0

89%

0.0

57%

0.0

50%

0.0

29%

0.0

18%

0.0

05%

0.00%

0.10%

0.20%

0.30%

0.40%

0.50%

0.60%

0.70%

0.80%

0.90%

1.00%

% o

f G

DP

Source: Thomson Reuters Datastream (GDP) / EVCA / PEREP Analytics

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Investments

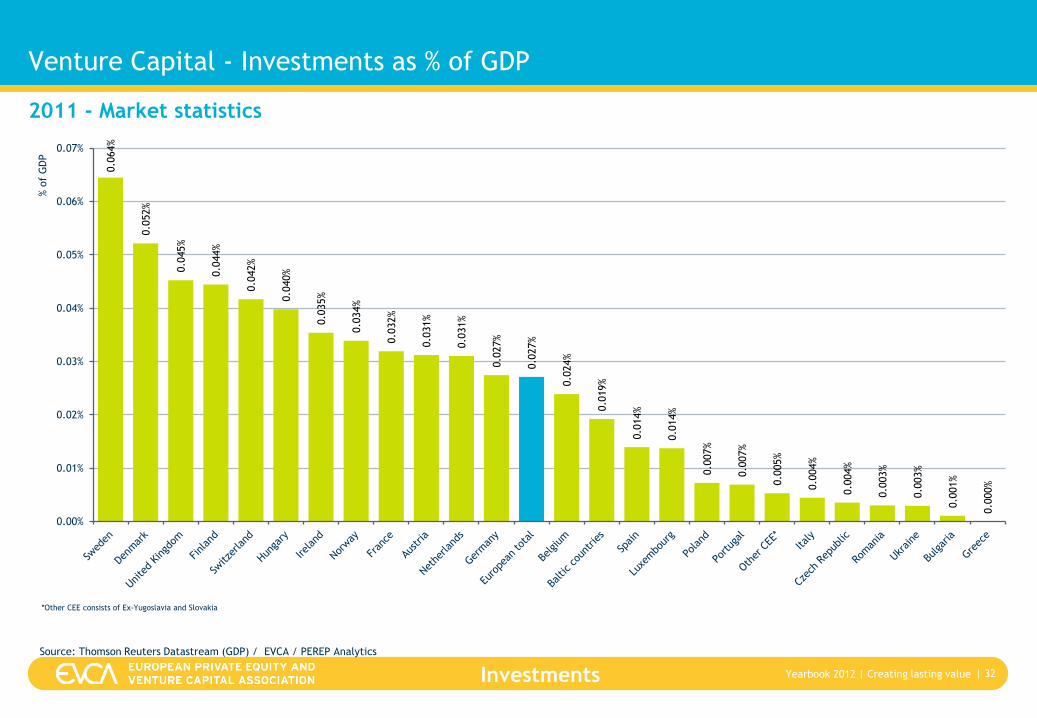

Venture Capital - Investments as % of GDP

| 32

2011 - Market statistics

*Other CEE consists of Ex-Yugoslavia and Slovakia

0.0

64%

0.0

52%

0.0

45%

0.0

44%

0.0

42%

0.0

40%

0.0

35%

0.0

34%

0.0

32%

0.0

31%

0.0

31%

0.0

27%

0.0

27%

0.0

24%

0.0

19%

0.0

14%

0.0

14%

0.0

07%

0.0

07%

0.0

05%

0.0

04%

0.0

04%

0.0

03%

0.0

03%

0.0

01%

0.0

00%

0.00%

0.01%

0.02%

0.03%

0.04%

0.05%

0.06%

0.07%

% o

f G

DP

Source: Thomson Reuters Datastream (GDP) / EVCA / PEREP Analytics

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Investments

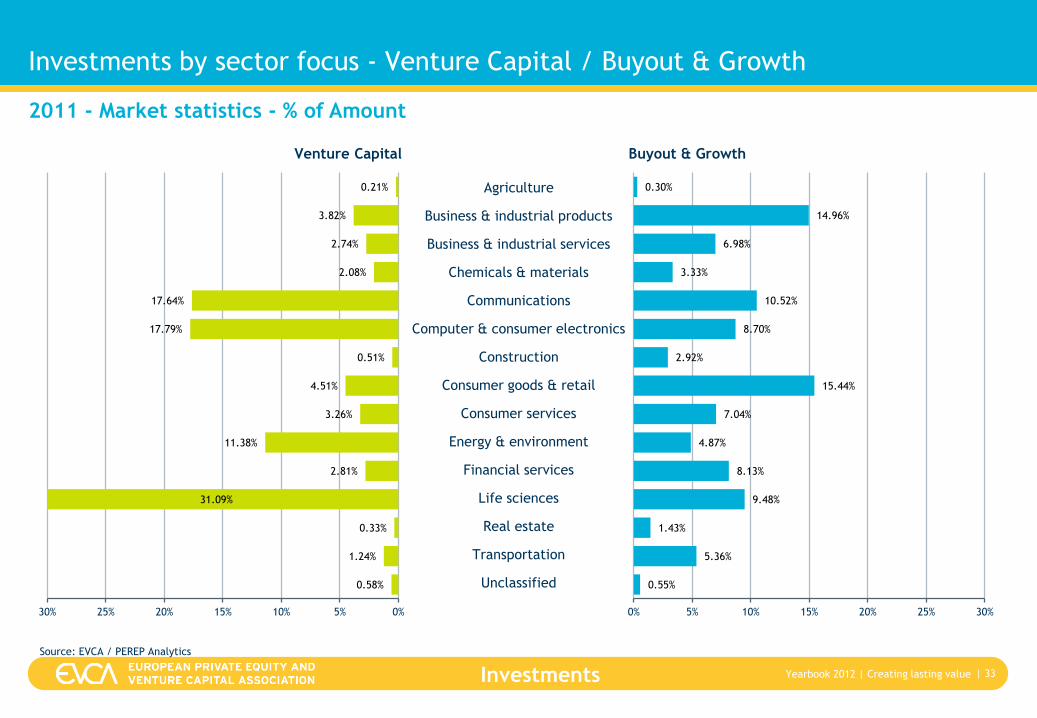

Investments by sector focus - Venture Capital / Buyout & Growth

| 33

Venture Capital Buyout & Growth

2011 - Market statistics - % of Amount

Source: EVCA / PEREP Analytics

Agriculture

Business & industrial products

Business & industrial services

Chemicals & materials

Communications

Computer & consumer electronics

Construction

Consumer goods & retail

Consumer services

Energy & environment

Financial services

Life sciences

Real estate

Transportation

Unclassified 0.58%

1.24%

0.33%

31.09%

2.81%

11.38%

3.26%

4.51%

0.51%

17.79%

17.64%

2.08%

2.74%

3.82%

0.21%

0%5%10%15%20%25%30%

0.55%

5.36%

1.43%

9.48%

8.13%

4.87%

7.04%

15.44%

2.92%

8.70%

10.52%

3.33%

6.98%

14.96%

0.30%

0% 5% 10% 15% 20% 25% 30%

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Investments

Investments by sector focus - Venture Capital / Buyout & Growth

| 34

Venture Capital Buyout & Growth

2011 - Market statistics - % of Number of companies

Source: EVCA / PEREP Analytics

Agriculture

Business & industrial products

Business & industrial services

Chemicals & materials

Communications

Computer & consumer electronics

Construction

Consumer goods & retail

Consumer services

Energy & environment

Financial services

Life sciences

Real estate

Transportation

Unclassified 1.23%

0.99%

0.17%

23.56%

0.58%

8.41%

3.76%

5.30%

0.68%

20.99%

16.65%

2.12%

7.93%

7.15%

0.48%

0%5%10%15%20%25%

0.71%

3.58%

0.76%

7.81%

3.26%

6.29%

7.92%

15.68%

4.18%

9.77%

9.17%

3.31%

11.01%

15.52%

1.03%

0% 5% 10% 15% 20% 25%

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Investments

Investments by number of employees

| 35

Full-time equivalent staff by interval

2011 - Market statistics - % of number of companies financed

Source: EVCA / PEREP Analytics

Venture Capital

Buyout & Growth

All Private Equity

63.3%

31.9%3.3%

0.4%

0.7%

0.3%0.1%

0.0%

10.3%

26.8%

17.9%5.7%

13.2%

10.5%

12.6%

3.1%

42.8%

29.9%

9.0%

2.5%

5.5%

4.2%

5.0% 1.2%

0 - 19

20 - 99

100 - 199

200 - 249

250 - 499

500 - 999

1000 - 4999

5000 +

42.8%

29.9%

9.0%

2.5%

5.5%

4.2%

5.0% 1.2%

0 - 19

20 - 99

100 - 199

200 - 249

250 - 499

500 - 999

1000 - 4999

5000 +

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Investments

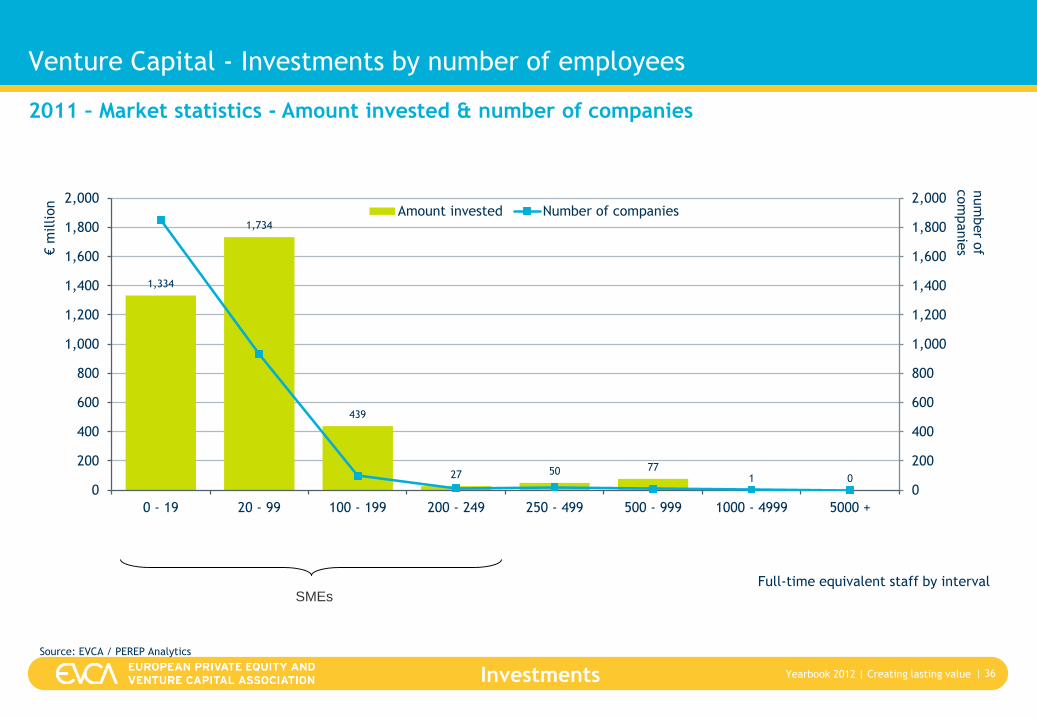

Venture Capital - Investments by number of employees

| 36

Full-time equivalent staff by interval

2011 – Market statistics - Amount invested & number of companies

Source: EVCA / PEREP Analytics

1,334

1,734

439

27 50 771 0

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

0 - 19 20 - 99 100 - 199 200 - 249 250 - 499 500 - 999 1000 - 4999 5000 +

num

ber o

f com

panie

s€m

illion

Amount invested Number of companies

SMEs

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Investments

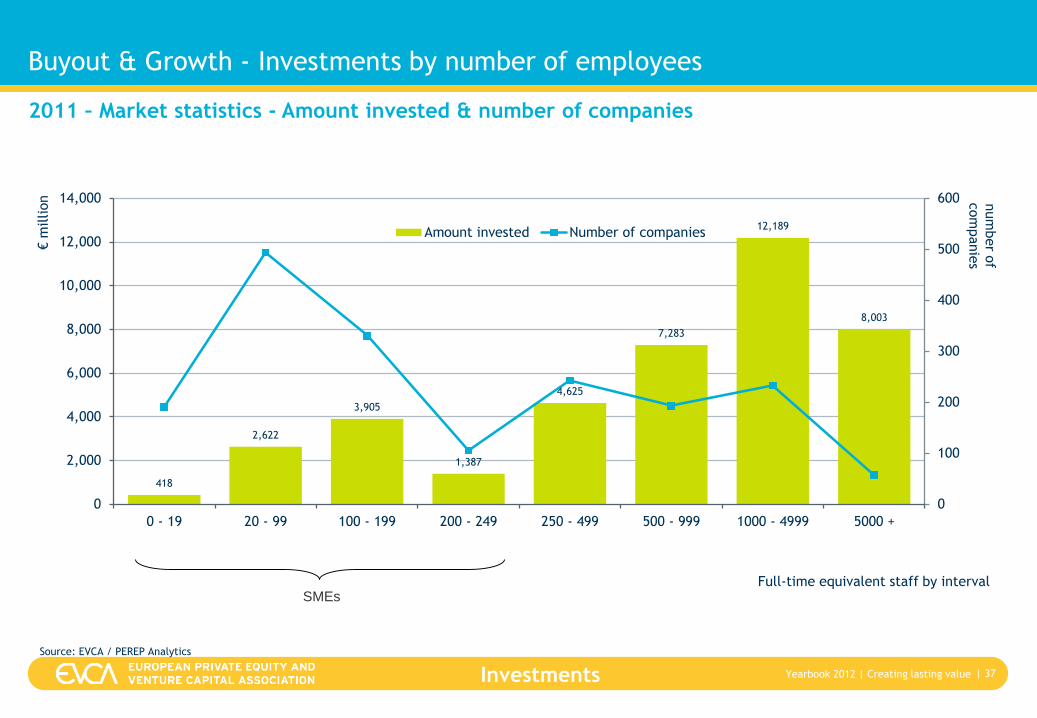

Buyout & Growth - Investments by number of employees

| 37

2011 – Market statistics - Amount invested & number of companies

Source: EVCA / PEREP Analytics

418

2,622

3,905

1,387

4,625

7,283

12,189

8,003

0

100

200

300

400

500

600

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

0 - 19 20 - 99 100 - 199 200 - 249 250 - 499 500 - 999 1000 - 4999 5000 +

num

ber o

f com

panie

s

€m

illion

Amount invested Number of companies

SMEsFull-time equivalent staff by interval

Divestments

Divestments Statistics explained:

• Industry statistics are an aggregation of the figures according to the country of location of the private

equity firm’s office in charge of the deal. At the European level, this relates to divestments made by

European private equity firms regardless of the location of the target company

• Market statistics are an aggregation of the figures according to the location of the portfolio company. At

the European level, this relates to divestments of European companies regardless of the location of the

private equity firm

• Divestment amounts are recorded at cost (i.e. the total amount divested is equal to the total amount

invested before)

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Divestments

Glossary – Divestment Stages

| 39

• Divestment by public offering: the sale or distribution of a company’s shares to the public for the first time by listing the

company on the stock exchange, also includes sale of quoted shares after a lock-up period

• Repayment of principal loans: If a private equity firm provided loans or bought preference shares in the company at the time of

investment, then their repayment according to the amortisation schedule represents a decrease of the financial claim of the

firm into the company, and hence a divestment.

• Repayment of silent partnership: A silent partnership belongs to the so-called mezzanine financing instruments. It is similar to

a long-term bank loan but, in contrast to a loan, a silent partnership is subject to a subordination clause, so that in the event of

insolvency all other creditors are paid before the silent partner. The company has to repay the partnership and has to pay

interest and possibly a profit-related compensation. The subordination clause gives the capital the status of equity despite its

loan character. This financing instrument is frequently used in Germany.

• Sale to another private equity house: See sale to financial institution.

• Sale to financial institution: The sale of company shares to banks, insurance companies, pension funds, endowments,

foundations and other asset managers other than private equity firms.

• Trade sale: The sale of company shares to industrial investors.

• Divestment by write-off: The total or partial write-down of a portfolio company’s value to zero or a symbolic amount (sales for

a nominal amount) with the consequent exit from the company or reduction of the share owned. The value of the investment is

eliminated and the return to investors is equal or close to -100%.

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Divestments

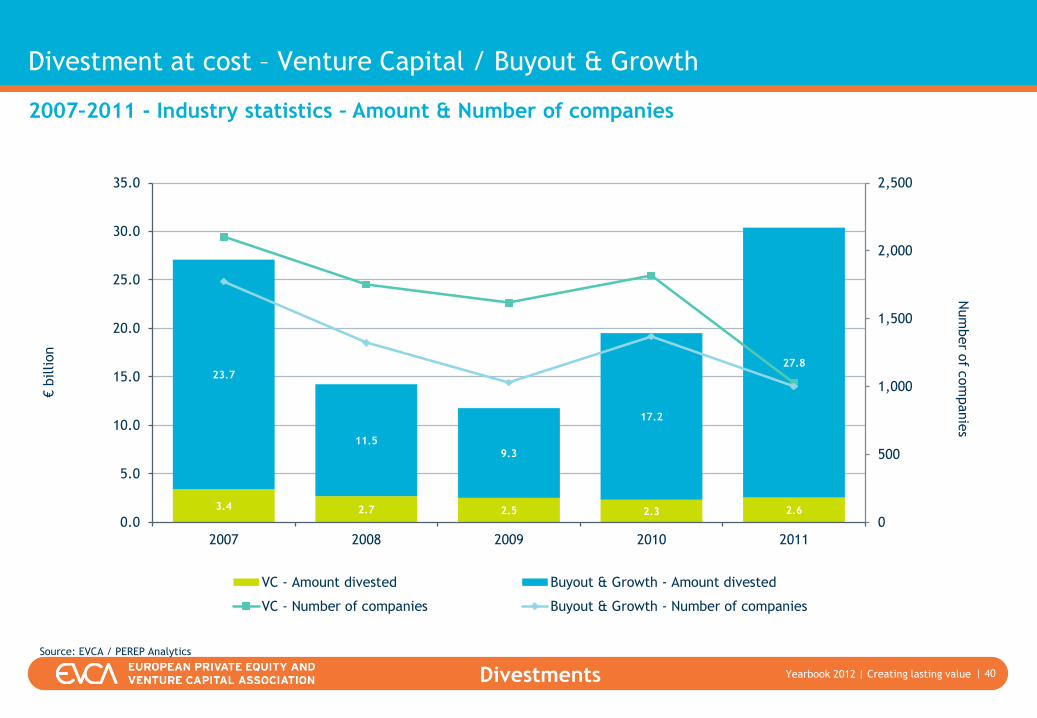

Divestment at cost – Venture Capital / Buyout & Growth

| 40

2007–2011 - Industry statistics – Amount & Number of companies

Source: EVCA / PEREP Analytics

3.4 2.7 2.5 2.3 2.6

23.7

11.5

9.3

17.2

27.8

0

500

1,000

1,500

2,000

2,500

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

2007 2008 2009 2010 2011

Num

ber o

f com

panie

s

€billion

VC - Amount divested Buyout & Growth - Amount divested

VC - Number of companies Buyout & Growth - Number of companies

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Divestments

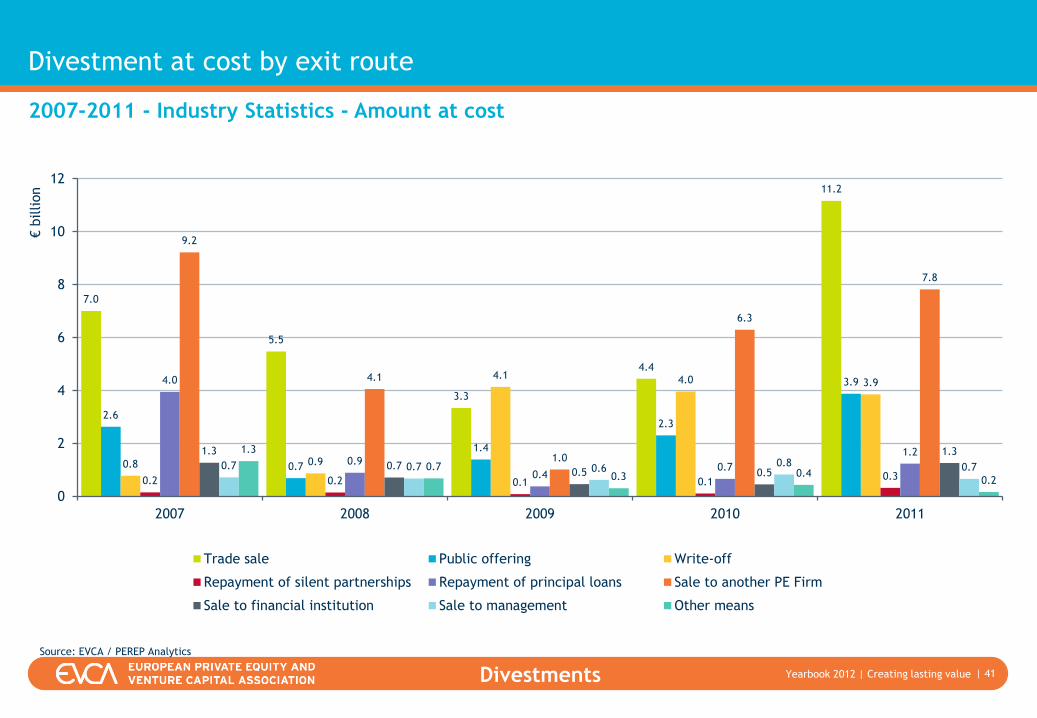

Divestment at cost by exit route

| 41

2007-2011 - Industry Statistics - Amount at cost

Source: EVCA / PEREP Analytics

7.0

5.5

3.3

4.4

11.2

2.6

0.7

1.4

2.3

3.9

0.8 0.9

4.1 4.0 3.9

0.2 0.2 0.1 0.10.3

4.0

0.9

0.40.7

1.2

9.2

4.1

1.0

6.3

7.8

1.3

0.70.5 0.5

1.3

0.7 0.7 0.60.8 0.7

1.3

0.70.3 0.4

0.2

0

2

4

6

8

10

12

2007 2008 2009 2010 2011

€billion

Trade sale Public offering Write-off

Repayment of silent partnerships Repayment of principal loans Sale to another PE Firm

Sale to financial institution Sale to management Other means

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Divestments

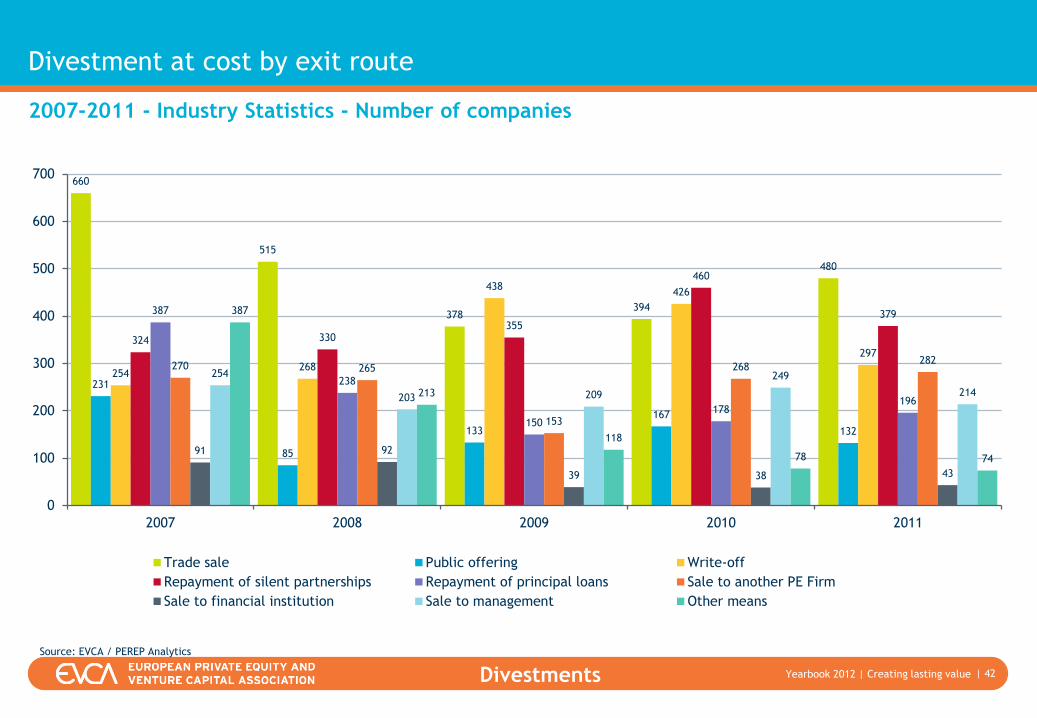

Divestment at cost by exit route

| 42

2007-2011 - Industry Statistics - Number of companies

Source: EVCA / PEREP Analytics

660

515

378394

480

231

85

133

167

132

254268

438426

297

324 330355

460

379387

238

150

178196

270 265

153

268282

91 92

39 38 43

254

203 209

249

214

387

213

118

78 74

0

100

200

300

400

500

600

700

2007 2008 2009 2010 2011

Trade sale Public offering Write-off

Repayment of silent partnerships Repayment of principal loans Sale to another PE Firm

Sale to financial institution Sale to management Other means

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Divestments

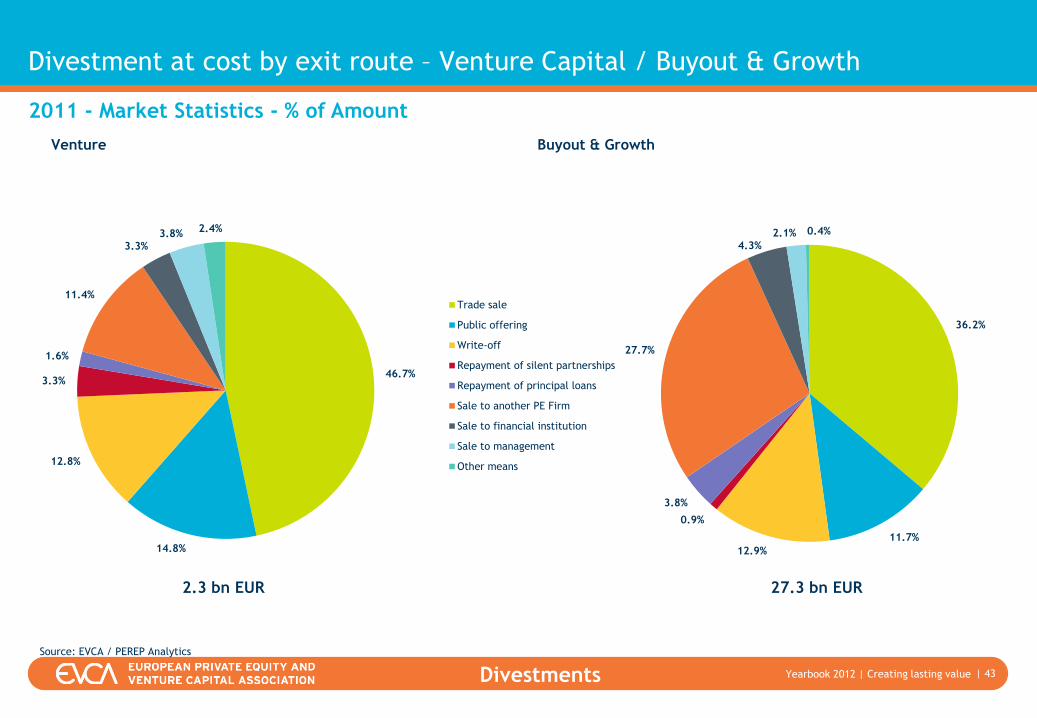

Divestment at cost by exit route – Venture Capital / Buyout & Growth

| 43

Buyout & Growth Venture

2011 - Market Statistics - % of Amount

Source: EVCA / PEREP Analytics

46.7%

14.8%

12.8%

3.3%

1.6%

11.4%

3.3%3.8% 2.4%

Trade sale

Public offering

Write-off

Repayment of silent partnerships

Repayment of principal loans

Sale to another PE Firm

Sale to financial institution

Sale to management

Other means

46.7%

14.8%

12.8%

3.3%

1.6%

11.4%

3.3%3.8%

2.4%

Trade sale

Public offering

Write-off

Repayment of silent partnerships

Repayment of principal loans

Sale to another PE Firm

Sale to financial institution

Sale to management

Other means

36.2%

11.7%

12.9%

0.9%

3.8%

27.7%

4.3%2.1% 0.4%

27.3 bn EUR 2.3 bn EUR

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Divestments

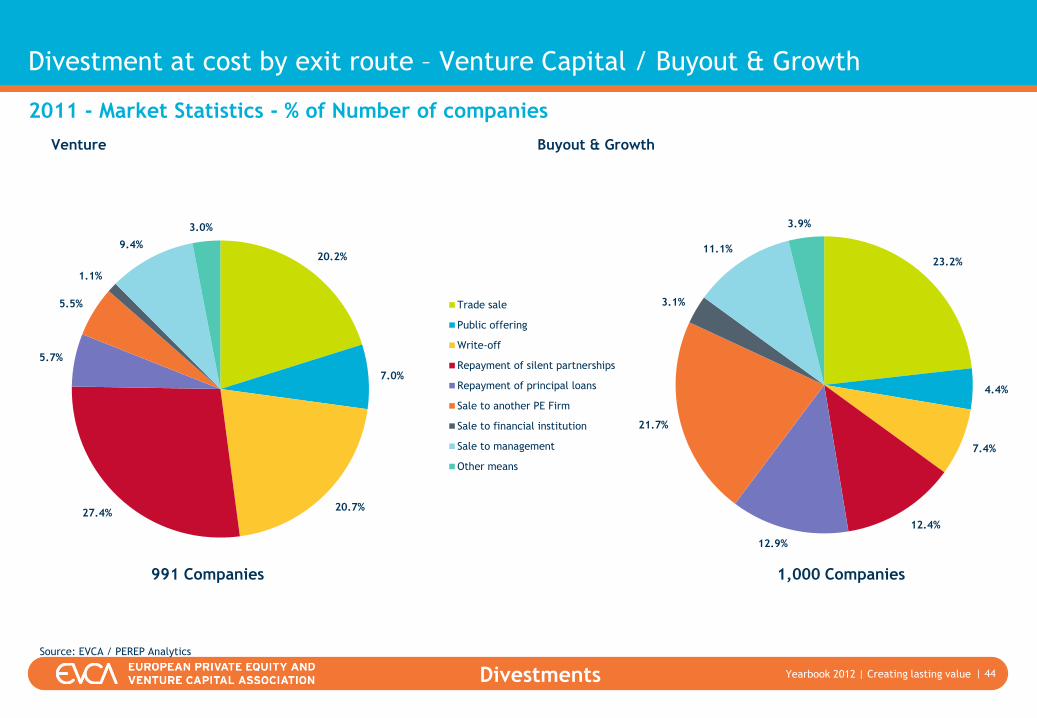

Divestment at cost by exit route – Venture Capital / Buyout & Growth

| 44

Venture Buyout & Growth

2011 - Market Statistics - % of Number of companies

Source: EVCA / PEREP Analytics

46.7%

14.8%

12.8%

3.3%

1.6%

11.4%

3.3%3.8% 2.4%

Trade sale

Public offering

Write-off

Repayment of silent partnerships

Repayment of principal loans

Sale to another PE Firm

Sale to financial institution

Sale to management

Other means

20.2%

7.0%

20.7%27.4%

5.7%

5.5%

1.1%

9.4%

3.0%

Trade sale

Public offering

Write-off

Repayment of silent partnerships

Repayment of principal loans

Sale to another PE Firm

Sale to financial institution

Sale to management

Other means

23.2%

4.4%

7.4%

12.4%

12.9%

21.7%

3.1%

11.1%

3.9%

991 Companies 1,000 Companies

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Divestments

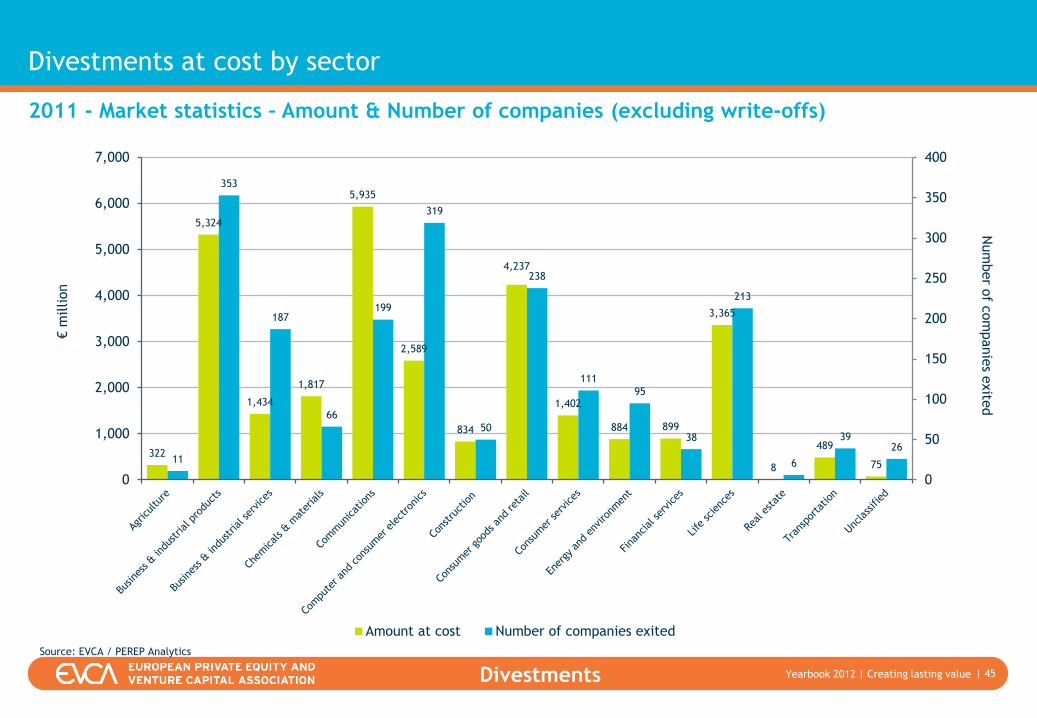

Divestments at cost by sector

| 45

2011 - Market statistics – Amount & Number of companies (excluding write-offs)

Source: EVCA / PEREP Analytics

322

5,324

1,434

1,817

5,935

2,589

834

4,237

1,402

884 899

3,365

8

489

7511

353

187

66

199

319

50

238

111

95

38

213

6

3926

0

50

100

150

200

250

300

350

400

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Num

ber o

f com

panie

s exite

d€

million

Amount at cost Number of companies exited

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012 Divestments

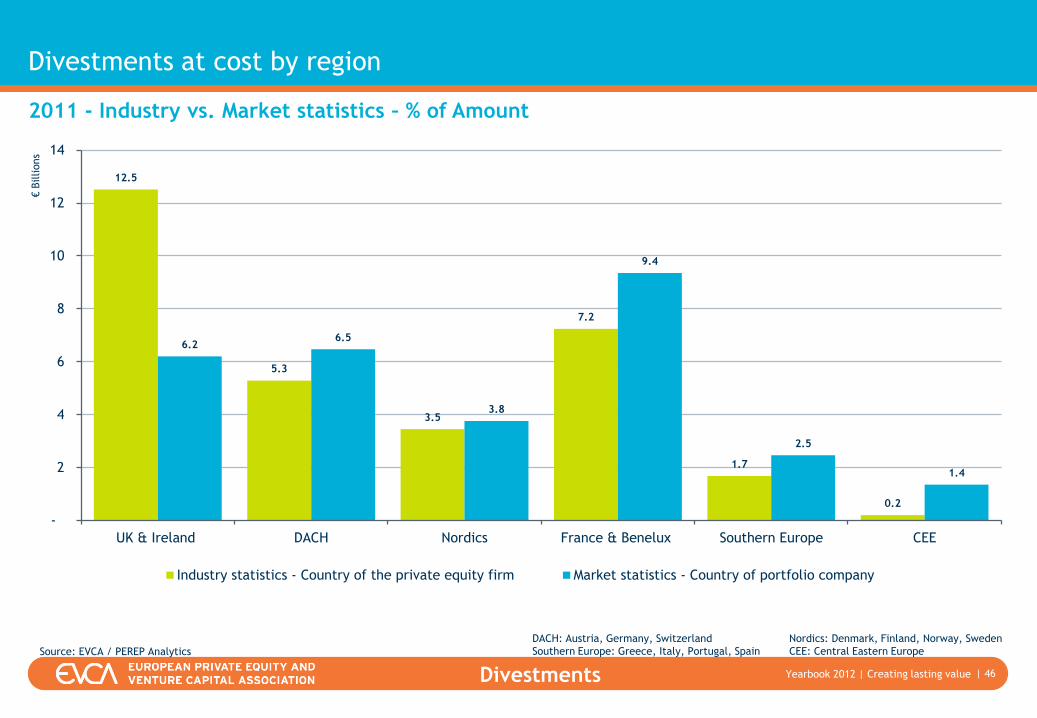

Divestments at cost by region

| 46

2011 - Industry vs. Market statistics – % of Amount

12.5

5.3

3.5

7.2

1.7

0.2

6.26.5

3.8

9.4

2.5

1.4

-

2

4

6

8

10

12

14

UK & Ireland DACH Nordics France & Benelux Southern Europe CEE

€Billions

Industry statistics - Country of the private equity firm Market statistics - Country of portfolio company

Source: EVCA / PEREP Analytics

DACH: Austria, Germany, Switzerland

Southern Europe: Greece, Italy, Portugal, Spain

Nordics: Denmark, Finland, Norway, Sweden

CEE: Central Eastern Europe

| Creating lasting value YearBook 2011 | Creating lasting value Yearbook 2012

About PEREP_Analytics and EVCA Research

| 47

• The overall coverage rate of all European private equity firms was 64% based

on 1,967 eligible private equity firms. In terms of capital under

management, the 2011 annual survey covered 88% of the total European

market (base € 539 billion)

• PEREP is a joint Pan-European statistics platform of the following private

equity associations: APCRI (Portugal), AVCO (Austria), BVA (Belgium), BVK

(Germany), CVCA (Croatia), CVCA (the Czech Republic), DVCA (Denmark),

EstVCA (Estonia), EVCA (Europe), FVCA (Finland), HVCA (Hungary), IVCA

(Ireland), LTVCA (Lithuania), NVCA (Norway), NVP (the Netherlands), PPEA

(Poland), SECA (Switzerland), SEEPEA (South Eastern Europe), SLOVCA

(Slovakia), SVCA (Sweden). PEREP has collected data directly from

associations’ members and participants in the other countries in Europe.

PEREP_Analytics Staff EVCA Research Staff

Statistics Manager

• Dan Magirescu

Head of Research

• Dr Cornelius Mueller

Research Specialist

• Julien Krantz

Central Analyst Team:

• Adriana Andronic

• Andreea Banica

• Monica Biolan

• Alina Ciucardel

• Laura Dumitrascu

• Iulia Furica

• Alina Marinescu

• Raluca Rosca

• Adelina Stefan

Email: [email protected]

Web: www.perepanalytics.eu

Email: [email protected]

Web: www.evca.eu

EVCA European Private Equity and Venture Capital Association

Bastion Tower

Place du Champs de Mars 5

B – 1050 Brussels – Belgium

www.evca.eu

Tel: +32 2 715 00 20