Embed Size (px)

Citation preview

A Report by Daman Investments PSC, September 2014

Year of the Primaries

Disclaimer: This report is presented solely for educational and informational purposes. Daman Investments is not offering it as legal, accounting, or other professional services advice. Any forward-looking information and statements are based on current expectations, estimates and projections about global economic conditions, the economic conditions of the regions and industries that are major markets for Daman Investments and its subsidiaries and affiliates (the “Daman group”) lines of business. These expectations, estimates and projections are generally identifiable by statements containing works such as “expects,” “believes,” “estimates,” or similar expressions. Important factors that could cause actual results to differ materially from those expectations include, among others, economic and market conditions in the geographic areas and industries that are or will be major markets for the Daman group’s businesses, oil prices, changes in government regulations, interest rates, fluctuations in currency exchange rates and such other factors as may be discussed from time to time. Although Daman Investments believes that its expectations and the information in this report were based upon reasonable assumptions at the time when they were made, it can give no assurances that those expectations will be achieved or that the actual results will be as set out in this report. While best efforts have been used in preparing this report, neither Daman Investments nor any other company within the Daman group is making any representation or warranty, expressed or implied, as to the accuracy, reliability or completeness of the information in this report, and neither Daman Investments, any other company within the Daman group nor any of their directors, officers or employees will have any liability to you or any other persons resulting from your use of the information in the report.

Daman Investments undertakes no obligation to publicly update or revise any forward-looking information or statements in the report.

P.O.BOX 9436Suite 600, 6th FloorDubai World Trade CenterSheikh Zayed RoadDubai, United Arab Emirates

TelephoneFax Asset Management Email

For more information please visit:www.daman.ae

: +971 4 332 4140: +971 4 332 4240: +971 4 408 0333: [email protected]

© Copyright 2014 3 DAMAN INVESTMENTS PSC - Year of the Primaries, September 2014

Source:Bloomberg*Figures up to Aug 31 2014

Since 2004 we have had two consecutive years of greater than a hundred percent growth in the DFM (2004 +152% & 2005 +190%) and greater than 60% growth for the ADX (2004 +75% & 2005 +67%). These were exceptional circumstances, where the economy was firing on all cylinders with bank credit growing by 25% in 2004 followed by 43% in 2005. From a valuation perspective the combined UAE markets P/E was at the giddy levels of 47x. Hence, we feel that in order to gain a better relative perspective one should compare where our markets were trading on the onset of the 2008 financial crisis and how far we have come since then.

Source: Bloomberg *Figures Up to Aug 31 2014

The DFM is still -9.85% of from its peak level in 2008 and the ADX has turned positive by 11.23% since its 2008 peak. On

DFM & ADX Price Index 2003 - 2014 *2015 Investment Outlook

As we had correctly forecast in our report “The best is yet to come” (July 2013), the full year returns for the UAE markets were amongst the best in the world in 2013, with the DFM up 108% and ADX up 63%. As attentive readers of our reports will know we first turned overweight on the UAE equity markets in the first quarter of 2012 in our report entitled “Is the quarter 1 rally a mirage?” (June, 2012)

In this piece we shall discuss how the mindset of investors has shifted during 2014 and the prospect for 2015. As such we will answer the question as to whether or not the UAE markets will be able to maintain their top flight status. Opinion on the street is as divided as it has ever been, with two main prevailing arguments. These arguments are often mixed but let’s pry them apart and address them separately. The bearish side point to high valuations and argue that all the good news on the UAE equity markets has already been priced in, whilst the bullish side argue that the UAE markets are set to usher in a new era of growth and that markets are set to go higher still as the growth translates into higher earnings.

In this paper we will look to address these arguments with the use of empirical and fundamental data as well as adding our own insights to the debate and conclude by weighing up all the relevant factors thereby giving our view on the remainder of 2014 market outlook and what is in store for 2015.

Firstly let’s digress into a little history...

Outlook for rest of 2014 & 2015

DFM still off 2008 peak levels

Performance of UAE Indices Vs MSCI EM and S&P 500

© Copyright 20144 DAMAN INVESTMENTS PSC - Year of the Primaries, September 2014

Source: REIDIN

According to the REIDIN Sale Index Dubai apartment prices have increased by 34% YoY, as of August 2014 surpassing their 2008 peaks by 16%. Villas under performing the apartment sector have gone up by 20% YoY as of August 2014 and are 3% higher from their peak levels. The general residential index has shown 31% growth YoY as of August 2014. This has grown by 13% from its 2008 peak level.

Source: REIDIN

Growth in Abu Dhabi has been mixed with the villa sector greatly outperforming the residential sector in terms of peak price levels. On the other hand, we see that apartments have risen by 15% YoY as of August 2014 slightly outperforming the villas that only rose by 14% YoY in the same time frame. The REIDIN residential Sales Price index rose by 17% YoY as of August 2014.

the other hand the MSCI emerging markets index is off -0.08% whereas the S&P 500 is up 45.32 % as at August 31 2014. From this perspective the DFM still has the most to recover.

Real Estate Bubble Redux?

With the real estate sector recovery in full swing in Dubai, some pundits are now pointing towards another real estate bubble in the making. In an effort to assuage these concerns, a number of measures have been undertaken at both the company level and the governmental level in order to have a more robust supply-demand driven real estate market. For example Emaar, the biggest real estate developer in Dubai banned the reselling of off-plan properties. The Dubai Land Department also increased registration fees from 2% to 4% in October 2013.

The UAE Central Bank has also done its bit by capping the mortgage expatriates can seek to a maximum loan to value ratio of up to 75% of the respective property’s value providing the entire investment value is less than AED 5 million. For Emiratis the first time borrowing limit is kept at 80% of the property value if the entire investment is less than AED 5 million. For properties which are more than AED 5 million the amount of mortgage which can be extended to expatriates and Emiratis are 65% and 70% respectively.

The key to price appreciation in the future is the supply/demand dynamics and according to Jones Lang LaSalle, if all residential projects which have been announced are delivered on time, there should be an additional 28,000 units which will have been completed in 2014. This would represent an increase of ca. 8% over the current stock which should portend an amelioration in the rate of price appreciation thereby leading to a more stable market.

Measures undertaken for healthy real estate growth

Future supply points to easing price pressures

Dubai Sales Price Index

Dubai Property Sale Prices Since the 2008 Peak Levels

© Copyright 2014 5 DAMAN INVESTMENTS PSC - Year of the Primaries, September 2014

REIDIN sales price index in general is off by 15% since its peak. The pace of price appreciation is set to increase further now that Abu Dhabi has introduced freehold status coupled with the limited supply of new units in 2014, with only 8500 units being delivered excluding units meant only for Emiratis.

Source: REIDIN

Source: REIDIN

Given the time lag between that of Dubai and Abu Dhabi, apartment prices in the capital are still off by 32% since their 2009 peak levels. Villas on the other hand are now 6% above their 2009 peak levels. The

We have repeatedly mentioned in our previous reports that banks in the UAE had significantly controlled lending in between the years 2009 and 2012 as the prevailing mantra for them was to clean up their balance sheets and improve their funding profiles. Last year, finally, we had the first visible signs of a revival in the UAE banks’ loan portfolios. As per the UAE central bank data, gross system loans increased by 5.11% in July 2014. However, this increase in lending has been coupled with deposits increasing across the system, with deposits increasing at a faster clip of 9.51% last year and already 9.84% this year.

Source: UAE Central Bank

Apartment prices still off peak in Abu Dhabi

Bank loan growth revival to continue

Return of loan growth

Evolution of Banking Aggregates

US$ million 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Total Assets 173,845 234,057 327,375 396,515 413,642 437,195 455,521 487,510 571,510 609,306

% yearly growth in Assets 41.87% 34.64% 39.87% 21.12% 4.32% 5.69% 4.19% 7.02% 17.23% 6.61%

Total Deposits 111,550 141,268 194,968 251,191 267,550 285,800 291,075 317,768 348,000 382,259

% yearly growth in deposits 41.02% 26.64% 38.01% 28.84% 6.51% 6.82% 1.85% 9.17% 9.51% 9.84%

Total bank loans and advances 101,384 137,857 185,138 270,579 277,114 291,429 310,912 322,312 347,074 364,816

% yearly growth in bank loans and advances 44.88% 35.98% 34.30% 46.15% 2.42% 5.17% 6.69% 3.67% 7.68% 5.11%

Source: UAE Central Bank* Figures up to July 2014 | in Millions of USD

Abu Dhabi Sales Price Index

Abu Dhabi Property Sale Prices Since 2009 Peak Levels

Deposit and Loan Growth in UAE as of July 2014

© Copyright 20146 DAMAN INVESTMENTS PSC - Year of the Primaries, September 2014

Banking Profitability

The banking industry has had a solid first half in 2014. Dubai listed banks grew their bottom line by an impressive 58% in the first six months of 2014 as compared to the same time period last year, generating a net income of AED 6 bn while Abu Dhabi listed banks grew ca. 13% with net income of AED 11.5 bn for the first half of this year.

Strong asset growth coupled with improved asset quality has enhanced the net interest margins for most banks; in fact banks such as RAKBank, ENBD, DIB and ADCB lowered their cost of funds by substituting their higher cost deposits with lower cost term deposits as well as dynamically managing their liabilities. Higher growth in consumer lending and the positive impact of declining EIBOR rate on loan spreads all added up to strong NIMs for the sector.

Source:Bloomberg

The UAE banks continued to remain well capitalized in 2014 with overall capital adequacy ratio in excess of the central bank requirements.

Source:Bloomberg

As of now most corporations in the UAE have recovered completely from the financial crisis and this in turn can be reflected in the declining trends of UAE Banks Non Performing Loans (NPL). We forecast this trend to continue and furthermore we expect a decline in provisioning expenses. Due to the high base of provisioning burdens most banks in the UAE are coming from, we expect this to reduce sharply in the upcoming quarters.

Source: Bloomberg

Source: Bloomberg

We continue to remain positive on the banking sector in 2014 with several favorable trends for the near term economic outlook including strong growth prospects for the domestic economy led by the non-oil private sector peaking in the provisioning cycle for most banks, improved asset quality metrics supported by record low interest rates and stimulus by major central banks all pointing to a strong outlook for the UAE banks.

Solid bank earnings

Outlook for banks remain positive

Non Performing Loans/ Total Assets

Provisions for Loan Losses

Net Interest Margin

Capital Adequacy Ratio

© Copyright 2014 7 DAMAN INVESTMENTS PSC - Year of the Primaries, September 2014

Source: BloombergFigures as of Q2 2014

Banks continue to be the highest dividend paying sector in the UAE paying out in aggregate AED 3.6bn for Dubai banks in 2013 versus AED 9.6bn for Abu Dhabi banks, (Please see section, “Dividend Factor”).

In our previous report we identified the lack of bank financing for stock market portfolios as a development, to keep an eye out for, as it would provide further liquidity and support to our markets. Banks by their nature do not disclose financing provided against stock market portfolios; however at present clients are able to avail financing from banks

EARNING MOMENTUMADX

Sector Q2 2014 Q1 2014 Q4, 2013 Q3, 2013 Q2, 2013 Q1, 2013 2012 QoQ YoY

Banks 5,844.89 5,668.17 4,911.24 4,992.03 5,057.85 5,092.27 17,572.35 3% 16%

Diversified Finan. Serv. 1,161.56 184.02 78.45 128.56 66.99 109.21 184.44 531% 1634%

Real Estate 515.25 495.58 512.47 427.08 1,262.92 194.40 299.92 4% -59%

Telecommunications 3,324.70 2,910.78 510.00 2,162.47 2,898.74 2,633.06 1,645.17 14% 15%

Others 914.12 959.26 358.39 286.38 367.91 540.15 282.11 -5% 148%

Insurance 101.35 132.79 98.57 151.85 112.77 217.33 76.55 -24% -10%

Grand Total 11,861.86 10,350.60 6,469.12 8,148.38 9,767.19 8,786.43 31,007.84 15% 21%

DFMSector Q2 2014 Q1 2014 Q4, 2013 Q3, 2013 Q2, 2013 Q1, 2013 2012 QoQ YoY

Banks 3,536.50 2,525.84 1,908.81 1,939.08 2,043.89 1,801.87 1,385.21 40% 73%

Diversified Finan. Serv. 280.82 246.60 135.14 110.31 95.55 47.54 23.56 14% 194%

Real Estate 1,457.83 1,094.42 2,096.17 793.51 815.46 597.19 537.40 33% 79%

Telecommunications 547.75 490.26 570.28 474.31 473.90 467.91 994.00 12% 16%

Others 1,055.53 701.32 318.48 -76.61 438.12 456.49 181.72 51% 141%

Insurance 71.54 119.17 166.19 75.30 98.57 109.18 56.36 -40% -27%

Grand Total 6,949.97 5,177.61 5,195.06 3,315.90 3,965.49 3,480.16 11,516.15 34% 75%

Source: Bloomberg

by way of term loans collateralized against stock market portfolios or overdrafts taken against shares as collateral.

Stock market brokers have also started similar initiatives and as a statistic the percentage of ESCA approved margin brokerages have increased significantly over the past twelve months. Currently blue chip names such as Emaar command a 1:1 leverage to equity ratio while investors have also been able to avail lesser ratios on small and midcap names.

UAE Corporates Post Stellar Earnings

UAE corporations posted stellar earnings in the first half of 2014 with Abu Dhabi Firms’ net income growing by 19% YoY as compared to the first half of the year in 2013. Dubai firms lead the way with a spectacular 63% growth in the same time period. The earnings momentum remains strong this year. A boom in the real estate industry followed by a revival in bank lending has helped ignite the growth cycle in the economy which can easily be seen by the momentum in the markets.

Strong earnings for UAE companies

Real estate and banks leading the charge

Return on Risk Weighted Assets

© Copyright 20148 DAMAN INVESTMENTS PSC - Year of the Primaries, September 2014

Rotation out of midcaps and into bluechips

High dividend growth expectations

The performance in Dubai has been led by the strong surge in the real estate sector. The banking and real estate sector contributed upwards of AED 4.9bn out of a total AED 6.9bn total net income in Q2 2014 which indicates the dependency of the market on these two sectors. Banking profitability was due to two main factors; the growth in lending and the reduction in provisions (see previous section on banking profitability).

Dividend Factor

Dividends play a vital role in the UAE stock markets and on the back of such stellar earnings; most investors in the UAE expect strong dividends from their holdings. As such, UAE corporations are under strong pressure from investors to pay attractive dividends with the dividend yield at the DFM coming in at 2% and the ADX dividend yield coming in at 3.65% for the FY’13.

ADXSector 2012 2013

Banks 7,872.97 9,603.59

Diversified Financial Services 155.35 265.33

Real Estate 503.53 650.38

Telecommunications 7,149.92 5,534.30

Insurance 364.50 432.00

Others 1,695.63 1,660.83

Grand Total 17,741.90 18,146.43

YoY Growth 36% 2%

Payout Ratio 54% 72%

Source:Bloomberg

DFMSector 2012 2013

Banks 3,211.56 3,665.70

Diversified Financial Services 50.00 450.00

Real Estate 859.05 976.33

Telecommunications 1,371.43 1,874.29

Insurance 117.09 131.28

Others 577.78 1,615.11

Grand Total 6,186.91 8,712.71

YoY Growth 41% 41%

Payout Ratio 55% 77%

Source:Bloomberg

Given the strong growth in earnings momentum in 2014, we expect the dividend season this fiscal year to be in effect stronger than the year before.

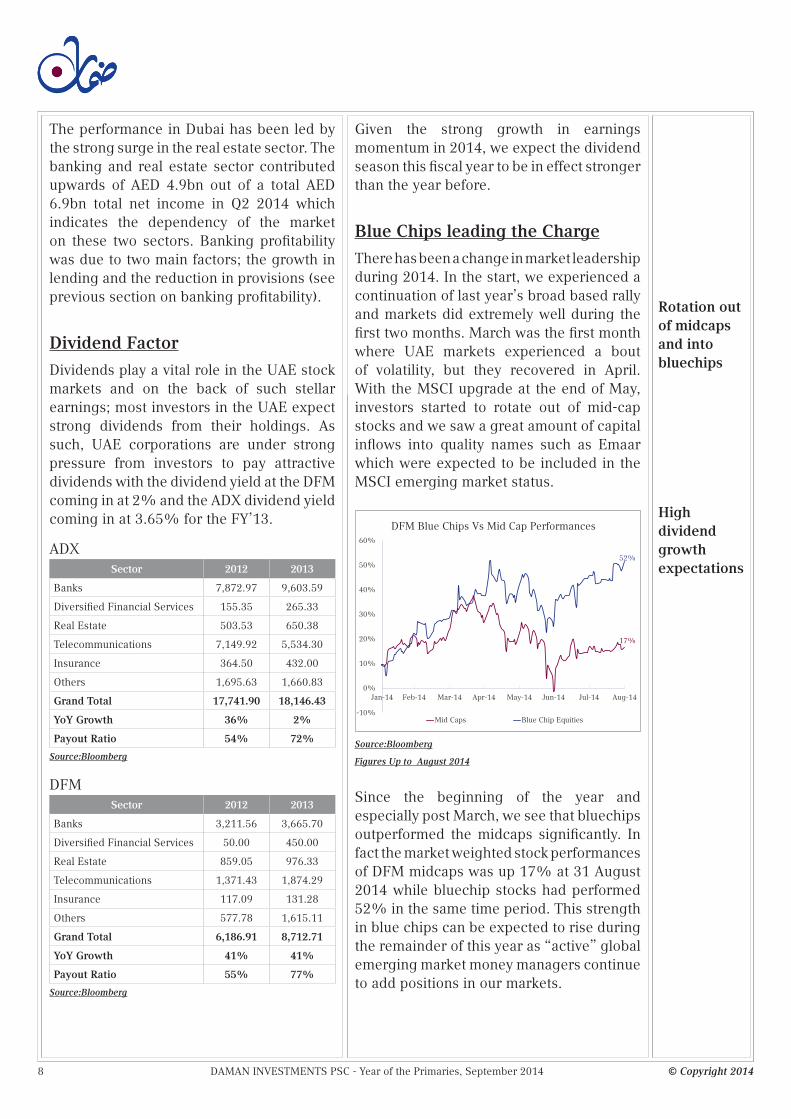

Blue Chips leading the Charge

There has been a change in market leadership during 2014. In the start, we experienced a continuation of last year’s broad based rally and markets did extremely well during the first two months. March was the first month where UAE markets experienced a bout of volatility, but they recovered in April. With the MSCI upgrade at the end of May, investors started to rotate out of mid-cap stocks and we saw a great amount of capital inflows into quality names such as Emaar which were expected to be included in the MSCI emerging market status.

Source:Bloomberg

Figures Up to August 2014

Since the beginning of the year and especially post March, we see that bluechips outperformed the midcaps significantly. In fact the market weighted stock performances of DFM midcaps was up 17% at 31 August 2014 while bluechip stocks had performed 52% in the same time period. This strength in blue chips can be expected to rise during the remainder of this year as “active” global emerging market money managers continue to add positions in our markets.

DFM Blue Chips Vs Mid Cap Performances

© Copyright 2014 9 DAMAN INVESTMENTS PSC - Year of the Primaries, September 2014

7. Emaar Properties8. First Gulf Bank9. National Bank of Abu Dhabi

Although the upgrade is a positive development for our markets we have noticed that traditionally markets which are upgraded go through a short term decline in performance, in the months following a MSCI upgrade. For comparison we have taken both the Indian and Pakistani stock markets which were upgraded at the end of 1992.

Source:Bloomberg

We can see that in the month running up to the MSCI upgrade both markets have an uptick in prices and we also see both markets decline, approximately 60 days post the upgrade. This behavior was repeated in our markets albeit at a faster pace and with greater volatility.

Source:Bloomberg

Markets sell off post upgrade

9 stocks upgraded to MSCI

Source:BloombergFigures Up to August 2014

In Abu Dhabi we see that midcaps were performing quite strongly up until mid February when Blue Chips start to strengthen. This corresponds with a large inflow of institutional money which entered the Abu Dhabi markets. The major rally in bluechips occurred after mid February. Once again we expect blue chip names to lead the way as active emerging market money managers start taking positions in Abu Dhabi Bluechips.

The MSCI / S&P Upgrade

Dubai Financial Market and Abu Dhabi Securities exchange both received upgrades on the 31st of May 2014 progressing from Frontier Markets into the Emerging Markets arena. The Qatar stock market also received the same upgrade. UAE markets accounted for 0.40% of the MSCI EM index while Qatar’s contribution was 0.45%. The upgrade took place on May 31st, 2014 and an estimated AED 5.5bn of new funds have entered into the UAE and Qatar bourses since the start of the year.

MSCI confirmed a total of 9 stocks in the UAE that were part of this upgrade and they are listed as follows:

1. Abu Dhabi Commercial Bank2. Aldar Properties3. Arabtec Holding4. DP World5. Dubai Financial Market6. Dubai Islamic Bank

ADX Blue Chips Vs Mid Cap Performances

Indian and Pakistani Markets Post MSCI EM Upgrade

UAE Markets Post MSCI Upgrade

© Copyright 201410 DAMAN INVESTMENTS PSC - Year of the Primaries, September 2014

Sell in May is back

Resilient markets in the face of corporate governance issues

UAE markets experienced new highs of liquidity in the first half of 2014, (Please refer to “Value Traded Over The Years Section”). The availability of margin from brokerages and the increase in bank financing for stock collateral has played a great part in this increase. Given the aforementioned margin financing, this has led to increasing volatility in our markets.

The breadth of stocks in our markets is limited yet the levels of liquidity are growing higher translating into the new liquidity entering the same names driving their valuations further north. In the month of June this exuberance and excessiveness led to the first bear market in the DFM in over five years with the index falling by a sharp -22.5%. The Abu Dhabi Stock Exchange also followed suit ending the month down -13.37%.

The initial catalyst for the sell off was the UAE Central Bank Report describing the UAE Real Estate Market as “overheating”. Adding further impetus to the prevailing bearish sentiment was the sudden sell-off in Arabtec, which had been one of the best performing stocks YTD on the DFM. The speed and ferocity of the sell off led to multiple margin calls being triggered in namely Arabtec and by extension the broader market.

Our markets have traditionally been resilient when faced with issues of corporate governance and the rights of minority interests such as when former market bellwethers Amlak and Tamweel were suspended in November 2008 in the wake of the global financial crisis. Investors were effectively kept in the dark whilst Tamweel restructured and were officially notified only after a period of three years before Tamweel resumed trading on May 10, 2011 and was later bought out by DIB in 2013. Amlak is still suspended and is in its final phase of restructuring.

A Tale of Two Halves

Sell In May and Go Away is back.

With the exception of the last two years and 2009, “Sell In May and Go Away” has been the ‘modus operandi’ of the retail investor base in the UAE markets. Given the strong recovery, coupled with a lack of external catalysts post the MSCI upgrade in May; we anticipated a sell off in May this year. The consolidation did in fact take place but it occurred in June (Please refer to earlier section on the MSCI Upgrade). Post the traditional summer slowdown we expect activity to regain its momentum in the fourth quarter of 2014 with the investors positioning themselves for full year results, the upcoming Emaar Mall Group IPO, as well as the upcoming dividend season.

Sell in May & Go Away?DFM

YearBefore May After May

3 Months 6 Months 3 Months 6 Months

2005 94.92% 187.09% 43.63% 59.10%

2006 -24.99% -35.03% 0.22% -13.54%

2007 -6.81% -15.58% -4.93% 19.63%

2008 3.55% 8.77% -16.12% -65.40%

2009 7.95% -45.43% 1.93% 3.32%

2010 7.09% -16.21% -6.07% 5.65%

2011 5.48% -8.61% -4.33% -11.60%

2012 11.69% 17.42% 5.19% 9.27%

2013 13.20% 31.63% 6.61% 24.47%

2014* 21% 42% -0.48% ?Source: Bloomberg

* Figures up to August 31st, 2014

ADX

YearBefore May After May

3 Months 6 Months 3 Months 6 Months

2005 91.75% 167.29% -7.45% -4.22%

2006 -19.14% -32.71% -0.09% -17.37%

2007 3.26% -9.25% -3.93% 16.37%

2008 9.96% 15.74% -12.40% -44.90%

2009 13.48% -24.05% 8.13% -0.42%

2010 4.21% -4.90% -4.06% 4.83%

2011 3.52% -4.01% -0.88% -7.36%

2012 1.57% 0.34% 4.94% 9.57%

2013 13.59% 22.45% 4.82% 24.47%

2014* 5.94% 36% -3.25% ?Source: Bloomberg

* Figures up to August 31st, 2014

© Copyright 2014 11 DAMAN INVESTMENTS PSC - Year of the Primaries, September 2014

Source: DFM Website

Source: ADX Website

Our markets remain retail dominated; the Dubai market has the most retail activity in the UAE - 3.48x more than institutional investors, while the Abu Dhabi market has 1.98x more retail investors than institutional.

Furthermore in lieu of the MSCI and S&P upgrade as of 31st of May, foreigners have indeed become more active. However the biggest increase has come from the GCC based investors rather than other nationalities. This is significant as it not only denotes the fact that we are yet to receive a significant amount of foreign money and as such this could provide a second leg to our rally. The EM upgrade took effect on the 1st of June and we saw a significant increase in foreign institutional cash flows in our markets. This coupled with the SCA’s new rules which are set to come into force allowing shorting of stocks our markets should reach new levels of efficiency.

Markets remain retail dominated

Thriving liquidity

Growth is sustainable

Liquidity Factor Value Traded Over The Years (in AED billions)

Date ADX YoY DFM YoY

2006 70.60 -32.57% 347.98 -14.10%

2007 175.34 148.36% 379.41 9.03%

2008 232.16 32.40% 305.20 -19.56%

2009 70.17 -69.78% 173.51 -43.15%

2010 34.58 -50.72% 69.66 -59.85%

2011 24.73 -28.48% 29.41 -57.78%

2012 22.05 -10.84% 43.75 48.76%

2013 84.00 280.95% 140.67 221.54%

2014* 253.06 201.26% 554.03 302.48%

Source: Bloomberg & Daman Investments *Values are annualized as of 31st August 2014

Liquidity in the market has had a significant improvement with annualized figures in 2014 for DFM far surpassing the figures last year. Figures in ADX in 2014 have also surpassed last year which reflect just how much liquidity has increased in our markets.

Source: BloombergValues are annualized as of 31st August 2014

A general increase in the volume and value traded is a sign of a strong recovery in UAE equity markets. The growth in volumes is at sustainable levels and driven by local catalysts which have a real translation into the economy unlike the inflated levels of growth we saw in 2005/2008.

Value Traded Over The Years

Institutional vs Individual Buying - DFM

Institutional vs Individual Buying - ADX

© Copyright 201412 DAMAN INVESTMENTS PSC - Year of the Primaries, September 2014

GCC based investors most active

Start of the IPO cycle

LSE premium eroded

Source: DFM, ADX website & Daman Investments

Source: DFM, ADX website & Daman Investments

While a lot of companies have recently started to increase their foreign ownership limits to take advantage of the expected foreign institutional money from both active and passive EM funds, only 9 have been confirmed by the MSCI. A large number of companies have yet to make the jump to being eligible for receiving foreign direct investments. There still remains ample room for foreign investors to participate in local companies’ ownership.

DFMForeign Ownership

Stock Dec-13 Sep-14Foreign

Ownership Permitted

EMAAR 28.96% 33.58% 49.00%

DIB 5.24% 17.59% 25.00%

ENBD 4.99% 5.00% 5.00%

DIC 13.94% 14.06% 35.00%

DFM 6.29% 8.07% 49.00%

AIRARABIA 26.38% 24.38% 49.00%

ARMX 48.95% 48.96% 49.00%

ARTC 41.33% 43.81% 49.00%

Source: Daman Investments & Bloomberg

ADXForeign Ownership

Stock Dec-13 Sep-14Foreign

Ownership Permitted

FGB 15.53% 15.16% 25.00%

NBAD 3.02% 3.74% 25.00%

ADCB 8.59% 9.33% 49.00%

UNB 8.93% 10.34% 40.00%

ALDAR 13.75% 18.20% 40.00%

RAKBANK 18.78% 20.31% 40.00%

DANA 30.17% 35.30% 49.00%

Source: Daman Investments & Bloomberg

The Local IPO Environment

As avid readers of our last report, “The Best Is Yet to come”, (July 2013), will know we identified rights issues and IPOs to be two of the key factors to give further impetus to our markets.

Marka, a mixed retail and F&B holding company was the first company to IPO on the Dubai Financial Market after a period of five years. The IPO was hugely successful and was massively oversubscribed at 36x, managing to receive a mammoth AED 10bn in subscriptions whilst the book size was only AED 275mn. The stock price jumped +59% on the first day of trading, signifying the pent up demand for new issuances. Emaar Malls and Hospitality will be the next big IPO which investors will be focused on, with Emaar Properties planning to raise AED 5.8 billion for spinning off 15% of its hospitality division.

Last year we saw two local firms IPO, starting with Al Noor Hospital in June followed by Damac Properties, the first Dubai based real estate developer to list since the economic downturn. What was significant of the listings was that they both chose to list on the LSE as opposed to local markets. Part of the justification for the overseas listing was the valuation premium of the LSE vis- à -vis our local markets which is now no longer the case.

Growth in Value Traded, GCC Vs Non-GCC for DFM

Growth in Value Traded, GCC Vs Non-GCC for ADX

© Copyright 2014 13 DAMAN INVESTMENTS PSC - Year of the Primaries, September 2014

confidence in our markets the time is now prime for IPOs and from all indications the pipeline seems strong.

Capital Market Activity

While there has been an increase in debt capital market activities, little activity is the norm in equity capital markets. One of the major expectations in the second half of 2014 is the increased level of IPO activity we expect to see in the UAE. As mentioned in “The Local IPO Environment” section of our report, this is mainly due to the constrictive nature of the current regulations vis-à-vis the company’s law.

Corporate Actions 2006 - 2014*

ADX

YearDebt

Offering-New Issue

Debt Offering / Increase

Equity Offering -

IPO

Rights Offerings

2006 6 1 0 6

2007 3 1 1 1

2008 3 0 0 3

2009 0 0 0 0

2010 1 1 0 0

2011 3 0 2 0

2012 4 1 0 1

2013 8 0 0 0

2014* 12 0 0 0

DFM

YearDebt

Offering-New Issue

Debt Offering/Increase

Equity Offering -

IPO

Rights Offerings

2006 2 1 2 4

2007 2 1 2 0

2008 0 0 1 2

2009 0 0 1 0

2010 1 0 0 1

2011 0 0 0 0

2012 2 1 0 0

2013 23 1 0 1

2014* 24 0 2 0

Source: Bloomberg* Figures up to August, 2014

The rights issue that took place in 2013 is that of Arabtec which was oversubscribed by 30% and share price reaction to the stock post the issue was positive.

P/E’s at long term averages

Source: Bloomberg

The DFM General Index is now trading at 20.5x P/E ratio v/s the London Stock Exchange which is at 16.3x, which removes the premium from the London market and sets the background for companies to start listing locally. A major factor which influenced many of the companies to list abroad is the restrictive IPO requirement in the UAE where at least 55% of the company must be listed. This is no longer the case as the Emirates Securities and Commodities authority has now allowed Emaar to list just 15% of its hospitality unit. Prior to this a lot of the companies that were looking to IPO were not willing to give up more than half of the share capital, as seen by Al Noor Hospitals which only floated 33% of its share capital. Another constricting regulatory requirement which has subsequently been removed was that all share sales on the UAE bourses must be priced at a par value of 1 dirham per share, limiting owners’ options in structuring their offers. Emaar Malls and Hospitality is the first IPO in the UAE which has been allowed to go through a book building process by which the price of the share sale was set at 2.90.

After rising +108% in Dubai and +63% in Abu Dhabi in 2013 and rallying much further in 2014, the market climate is now drastically different and P/E’s are now trending towards long term averages, although still significantly lower than historical highs (see section on valuations). With this improving macro-economic backdrop, driving up stock market valuations and rising investor

P/E of UAE Markets Vs LSE

© Copyright 201414 DAMAN INVESTMENTS PSC - Year of the Primaries, September 2014

Abu Dhabi still cheapest in the region

Strong macro tailwinds

Valuations

Source: Bloomberg

Currently both Dubai and Abu Dhabi are trading at premiums to their book value which is a stark comparison to yesteryears. This is a display of the enormous growth which has taken place until now. Having said this, Abu Dhabi still remains amongst the cheapest markets in the region. On a P/E basis we are still below our long term average on the DFM.

Source: Bloomberg*Figures up to Aug 2014

Source: BloombergFigures as of Aug 31 2014

On an individual sector basis, financial services, which due to the likes of DFM, seem clearly on “inflated” multiples; the rest and more importantly the banks still trade below the market P/E while the important real estate sector is at a slight premium. Hence given that banks and Telco’s are 33.5% of the market we continue to see further upside in these respective sectors.

The ADX market is trading on a slight premium to its long term P/E average.

Source: Bloomberg*Figures Up to Aug 31 2014

On a sectorial basis, only construction and industries are significantly above their market average. Similar to Dubai the important banks (61% of the ADX) and telecommunications sectors (15% of the ADX) are still below the market average.

Source: BloombergFigures as of Aug 31 2014

P/E Ratio Flow from 2007 - 2014*

ADX Price / Earnings by Sector

DFM Price / Earnings by Sector

P/E Ratio Flow from 2007 - 2014*

Price-to-Book vs ROE

© Copyright 2014 15 DAMAN INVESTMENTS PSC - Year of the Primaries, September 2014

ADXRisk Free Rate

(Yield)

DateAbu Dhabi Govt.

30/04/2009 - 08/04/2019

ADX Equities Earning Yield

Equity Risk

Premium

2011 3.23% 10.23% 7.00%

2012 1.89% 11.75% 9.86%

2013 2.31% 8.35% 6.04%

2014 1.80% 6.93% 5.13%

The yields on UAE sovereign debt continue to be relatively low in comparison to the UAE stock markets’ earnings yield and given the high equity risk premium in the Dubai and Abu Dhabi stock markets we remain overweight on UAE equities. The Abu Dhabi markets in particular provide almost 5.13% over the risk free rate premium. Within the UAE we continue to have a bias for Abu Dhabi over Dubai, given the higher equity risk premiums in Abu Dhabi.

As the risk premium spread in the Dubai markets starts to tighten investors should rotate into the Abu Dhabi markets, hence our overweight of Abu Dhabi markets over Dubai.

On an absolute inflated adjusted basis, equities still prove to be the better performing asset class:

Investment YieldInflation Adj Yield

Average 12 months bank deposit 1.50% 0.10%

Equities Earning Yield - DFMGI 3.95% 2.55%

Equities Earning Yield - ADSMI 6.93% 5.53%

Dividend Yield - ADSMI 3.31% 1.91%

Dividend Yield - DFMGI 2.06% 0.66%

Bond Yield - Dubai 2015 0.81% -0.59%

Bond Yield - Abu Dhabi 2019 2.02% 0.62%

Given the strong earnings and dividend yields we continue to be strategically and tactically overweight in equities and we have been since Q1 2012 (See our report “UAE Equities: Is the Q1 Rally a Mirage?” June 2012) when we had correctly forecasted that equities were about to bounce back.

Equities risk premium still positive

Inflation adjusted equities still the best asset class

The UAE is currently in a strong macro and micro environment with the Expo 2020 spurring the economy northwards. Corporations in the UAE, especially public companies have already seen a positive growth in both the top and bottom lines thereby strengthening their balance sheets which in turn translates to positive increases in their capital expenditure.

Equities still the best performing investment vehicle

The U.S. Federal Reserve has now started tapering in full force and is scheduled to conclude its exercise by the end of October. Given that the UAE’s monetary policy is aligned with the US, we expect the fixed income markets to be under further pressure, thus reiterating our overweight position in equities.

Equity Risk Premium:

The equity risk premium is the “extra return” that investors collectively demand for investing their money in stocks. Classically the equity risk premium is the reward to be found in stocks rather than “risk-free” bonds. Economic theory suggests that investors in equities demand an extra risk premium above prevailing risk-free rates in their earnings yield to compensate them for the higher risk of owning stocks over bonds and other asset classes.

DFMRisk Free Rate

(Yield)

DateDubai Govt. 22/04/2009 - 22/04/2019

DFM Equities Earning Yield

Equity Risk

Premium

2011 1.27% 6.78% 5.51%

2012 1.20% 8.62% 7.43%*

2013 1.00% 6.29% 5.29%

2014 2.00% 4.76% 2.76%

* Daman turns overweight in equities; see our report, “UAE Equities: Is the Q1 Rally a Mirage?” June 2012

© Copyright 201416 DAMAN INVESTMENTS PSC - Year of the Primaries, September 2014

Liquidity scarcity to be prevailing mantra beyond Q1 2015

Outlook positive until Q1 2015

Inflection point to come beyond Q1 2015

Long term market breadth set to increase

ConclusionFactors in play Positive Negative Ambiguous

General Macro Environment J

Real Estate Revival J

Bank Earnings J

Bank Lending J

Corporate Earnings J

Dividend Factor J

MSCI Upgrade J

Liquidity J

Capital Market Activity K

Lack of Breadth L

Valuations K

Asset Allocation J

Corporate Governance L

Given that 9 out of 13 factors in the table above are positive, we conclude that investors should still enter the market as we expect a strong finish to the year as well as a robust Q1 2015. We expect investors to start positioning for fourth quarter earnings and the upcoming dividend season.

In summary up until the end of the Q1 2015, we think that valuation metrics in the UAE bourses still look attractive given the expected growth potential in the companies’ bottom lines. External catalysts such as winning the Expo 2020 have had a ‘halo effect’ leaving the market and the economy with a palpable sense of optimism besides adding to the momentum of the recovery in the real estate sector by boosting the construction near and around the Expo.

The equity markets continue to experience multiple expansion encouraged by strong bottom line earnings, share buybacks, talk of M&A and limited equity issuance. We also continue to see the process of balance sheet repair coming to an end with the end of the bank provisioning cycle thereby positioning them to fully capitalize on their future growth potential. Bank financing for stock market purchases is yet another indicator of not only the increased liquidity in the markets but can also be taken as a token of confidence in the strength of our markets.

Developments such as the announcement of the Saudi market opening up have also garnered huge attention to our region and as such, the GCC has so far in 2014 enjoyed an enviable growth rate. Despite this, valuations in Abu Dhabi still remain to be very attractive on a P/E basis and the market has been trading at 14x earnings compared to an average GCC P/E of 17x.

Beyond Q1 2015 the outlook becomes ambiguous at best, given the increase in capital market activities in the form of IPO’s. Our retail dominated markets will go through cycles of liquidity scarcity depending on the size and the timing of the IPO’s. The United Arab Emirates stock exchanges’ plan to offer a trading platform for shares in private joint-stock companies so that they can raise capital with less disclosure of corporate information than publicly listed firms. The thought process behind this is that it will serve as a stepping stone for companies to eventually go public. However the new exchange will also compete for liquidity from the public bourses.

The stock market performance beginning Q2 2015 will hinge primarily on two factors namely the foreign ownership limits of the companies which plan to list and the fund inflow of foreign investors. If the companies’ list with high foreign ownership limits and qualify to participate in indices such as the MSCI EM index we can expect large foreign flows into the qualified names and this new money in the market will provide room for growth. On the other hand if the companies list with low foreign ownership limits, the cycles of liquidity entering and leaving the market will create a dampening effect and we then expect markets to remain volatile for the remainder of the year.

However in the long term new companies entering the market will add to the depth and breadth of the market and with ESCA liberalizing the current stringent listing requirements coupled with the imminent change in the company’s law the outlook remains positive post the IPO cycle.