Embed Size (px)

Citation preview

YEAR END SPECIAL - 2014!

1

Newsmakers of 2014 in Tax – By Taxsutra Editorial

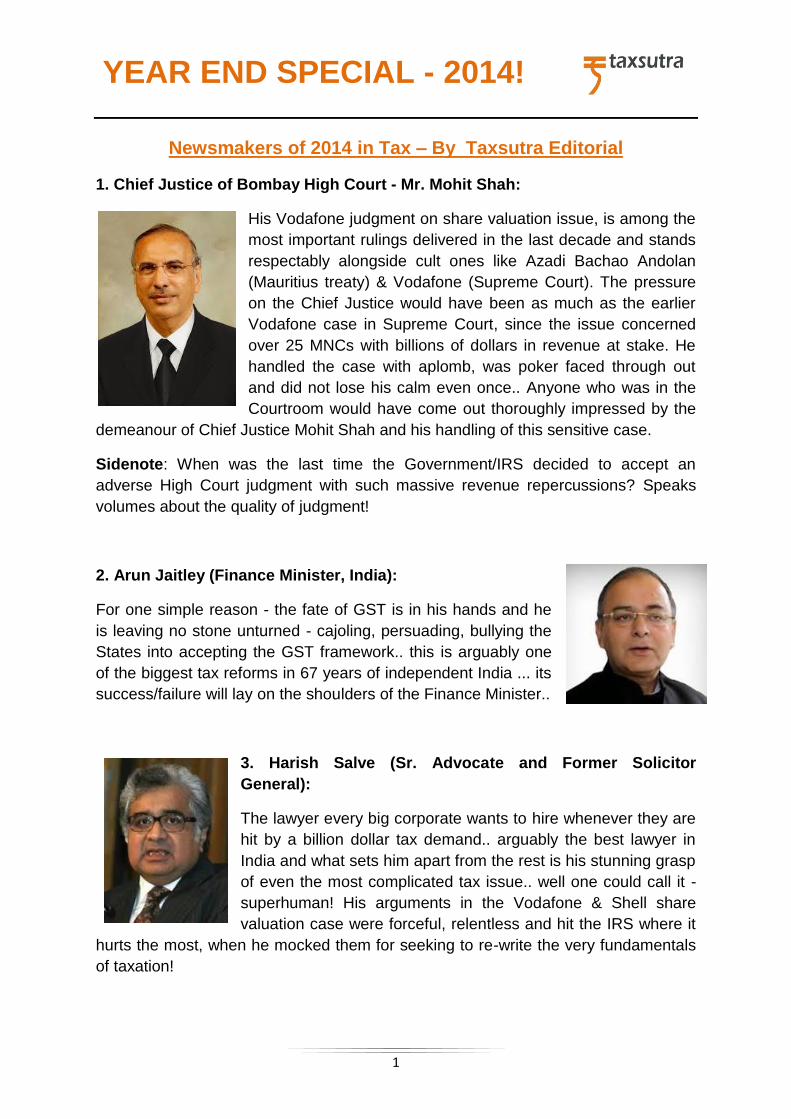

1. Chief Justice of Bombay High Court - Mr. Mohit Shah:

His Vodafone judgment on share valuation issue, is among the

most important rulings delivered in the last decade and stands

respectably alongside cult ones like Azadi Bachao Andolan

(Mauritius treaty) & Vodafone (Supreme Court). The pressure

on the Chief Justice would have been as much as the earlier

Vodafone case in Supreme Court, since the issue concerned

over 25 MNCs with billions of dollars in revenue at stake. He

handled the case with aplomb, was poker faced through out

and did not lose his calm even once.. Anyone who was in the

Courtroom would have come out thoroughly impressed by the

demeanour of Chief Justice Mohit Shah and his handling of this sensitive case.

Sidenote: When was the last time the Government/IRS decided to accept an

adverse High Court judgment with such massive revenue repercussions? Speaks

volumes about the quality of judgment!

2. Arun Jaitley (Finance Minister, India):

For one simple reason - the fate of GST is in his hands and he

is leaving no stone unturned - cajoling, persuading, bullying the

States into accepting the GST framework.. this is arguably one

of the biggest tax reforms in 67 years of independent India ... its

success/failure will lay on the shoulders of the Finance Minister..

3. Harish Salve (Sr. Advocate and Former Solicitor

General):

The lawyer every big corporate wants to hire whenever they are

hit by a billion dollar tax demand.. arguably the best lawyer in

India and what sets him apart from the rest is his stunning grasp

of even the most complicated tax issue.. well one could call it -

superhuman! His arguments in the Vodafone & Shell share

valuation case were forceful, relentless and hit the IRS where it

hurts the most, when he mocked them for seeking to re-write the very fundamentals

of taxation!

YEAR END SPECIAL - 2014!

2

4. Arvind Datar (Sr. Advocate):

He was a part of arguably one of the most important cases of

2014, wherein the Constitution Bench of Supreme Court

struck down the National Tax Tribunal. The reason - they

accepted the brilliant, nuanced arguments of Arvind Datar

that the National Tax Tribunal which sought to usurp the

powers of High Court, was violative of the 'basic structure'

doctrine laid down in the historic case of Kesavananda

Bharati. The judgment will not only have huge repercussions

on Govt's plans to reduce disputes through creation of an alternative tax tribunal but

has also stopped in its track, 'Tribunalization of Justice', as Datar termed it in the

Courtroom.

5. Justice S.C. Dharmadhikari (Judge, Bombay High

Court):

His spate of rulings, lambasting the Revenue for frivolous

appeals on settled issues and imposing costs for wasting

Court's 'precious' time, have surely been heard with long ears

by the tax department. Justice Dharmadhikari has been

unsparing in his criticism, invoking public interest and

observing rightly that this Court also deals with issues

concerning the 'life and liberty' of citizens. Heading the tax bench based in the

financial capital of the country, that contributes over 40% of direct tax revenues of

the exchequer, is a challenge in itself. Justice Dharmadhikari's 'no nonsense'

approach is refreshing and welcome.

6. Justice S. Ravindra Bhat (Judge, Delhi High Court):

Justice Bhat delivered several significant tax judgments

during the course of 2014, three of which have made it to

Taxsutra's Top 20 Judgments of the year - Copal Research

(Indirect transfers & 50% threshold for the term

'substantially'), Centrica Offshore (Employee secondment)

and Radials International (PMS income classification). In all these cases, there is a

common thread.. Justice Bhat hasn't shied away from laying down the law wherever

YEAR END SPECIAL - 2014!

3

there was an ambiguity/grey zone and has infact done with so with well reasoned

judgments, citing OECD commentaries and UN Reports, thereby giving us a different

flavour.

7. Dr. Parthasarathi Shome (Chairman, Tax Administration Reforms

Commission):

His current designation is not why he makes it to this list,

but it his immense contribution to development of tax policy

in India, that deserves a special mention. As Advisor to

former Finance Minister Mr. P. Chidambaram in the UPA

regime, he championed the cause of progressive tax policy,

non-adversarial regime and a tax administration that

fundamentally changes its mindset and treats the taxpayers

as a 'customer.' Some of these words are now slowly

finding their way into the CBDT lexicon.. He has delivered

some important reports over the last several months on Tax Administration Reforms.

Some of the recommendations are revolutionary but the jury is still out on whether

Govt. will bite the bullet!

8. CBDT:

But for them, we probably wouldn't have too much work. Over the last 12 months,

the tax department has faced scorched earth criticism for what the then Opposition

party and now ruling party, BJP termed 'tax

terrorism.' The CBDT has had to therefore make big

adjustments in their attitude towards the taxpayer

and to their credit, they have, by bringing out

circulars and clarifications to reduce litigations and

imploring the tax officers to shed their

'confrontationist' approach. The CBDT plays a

crucial role in tax policy development as well as

administration and taxpayers would be hoping that the new Chairman Ms. Anita

Kapur would take a break from precedent and showcase a new, more taxpayer

friendly side of the Board.

YEAR END SPECIAL - 2014!

4

9. Foreign Tax Division:

The troika of Competent Authority Akhilesh Ranjan, Joint

Secretary Rajat Bansal and APA Commissioner Kamlesh

Varshney have worked beautifully as a team, knitting together a

cohesive approach towards taxation of MNCs. While Akhilesh

Ranjan has smoothened the rough edges in the relationship with

USA's IRS and stamped India's imprint on OECD's BEPS project,

Rajat Bansal's round the clock efforts led to India recently signing

its first Bilateral APA with Japan. APA Commissioner Kamlesh

Varshney, in the last 2 years of APA regime, has succeeded in

creating an atmosphere of trust, thus resulting in a record number

of APA applications. These three gentlemen and their respective

teams surely deserve a special recognition for being the faces of India's international

tax policy.

10. IFA India:

If there was any proof needed of the important role India

now plays with regards to development of international tax

jurisprudence, one ought to have been only present at the

IFA Mumbai Congress to witness the spectacle! The

Mecca of all tax conferences, IFA India played hosts to

over 1500 international delegates, dished out the famous

Indian hospitality and confidently put its foot forward as one of the

thought leaders when it comes to tax policy. The India Chapter is now

one of the biggest, most vibrant branches of IFA worldwide and hence

this special mention. This mention would however be incomplete

without recognizing the person who has led this charge - IFA

President Porus Kaka (Sr. Advocate), who is the first Asian to occupy

this prestigious office.

YEAR END SPECIAL - 2014!

5

Top 20 Tax rulings of 2014

These are the rulings picked by Taxsutra’s Editorial Team for the third edition of the

book - ‘Top 100 Income-tax rulings of 2014’, being published by CCH.

1. Supreme Court : Lays down law on retrospective taxation, principle of

"fairness" the balancing factor

Vatika Township Private Limited [TS-573-

SC-2014]

2. Supreme Court : Strikes down National Tax

Tribunal as violative of ‘basic structure’

doctrine

Madras Bar Association [TS-600-SC-2014]

3. Supreme Court : Explains religious/charitable purpose duality; Gives

guidelines on "substantial question of law"

Dawoodi Bohara Jamat [TS-148-SC-2014]

4. Delhi HC : Word "substantially" for indirect transfers given 'restrictive'

meaning; Sets 50% assets threshold

Copal Research Limited [TS-509-HC-2014(DEL)]

5. Delhi HC : Upholds AAR ruling on employee secondment creating PE; FTS

also applicable

Centrica India Offshore Pvt. Ltd. [TS-237-HC-2014(DEL)]

6. Gujarat HC : Directs CBDT to extend returns filing due date

All Gujarat Federation Of Tax Consultants [TS-601-HC-2014(GUJ)]

YEAR END SPECIAL - 2014!

6

7. Bombay HC : Share issue transactions outside TP

net; Chapter-X invocation only where income arises

Vodafone India Services Pvt. Ltd. [TS-308-HC-

2014(BOM)-TP]

8. Karnataka HC : Questions DTAA coverage to domestic law amendment;

"Sovereign power" to break treaties

Vodafone South Limited [TS-173-HC-2014(KAR)]

9. Delhi HC : Lays down tests / principles to determine

characterization of share transactions under

discretionary PMS

Radials International [TS-238-HC-2014(DEL)]

10. Karnataka HC : Deduction claim unaffected by 'window dressing' of balance

sheet to satisfy shareholders

Karnataka Soaps and Detergents Ltd [TS-765-HC-2014(KAR)]

11. Bombay HC : Reads Rajdharma to Revenue for wasting 'precious' court time;

Public interest paramount

Larsen and Toubro Ltd [TS-441-HC-2014(BOM)]

12. Karnataka HC : Sim card distribution = sale of 'right to service', Sec 194H

Commission TDS inapplicable

Bharti Airtel Limited & Ors [TS-722-HC-2014(KAR)]

13. Delhi ITAT : Admits employees' LinkedIn profiles as

additional "evidence" for PE determination

GE Energy Parts Inc. [TS-400-ITAT-2014(DEL)]

YEAR END SPECIAL - 2014!

7

14. Delhi ITAT : Corporate guarantee not 'international transaction' absent

bearing on profits; Interprets Sec 92B

Bharti Airtel Limited [TS-76-ITAT-2014(DEL)-TP]

15. Mumbai ITAT : SB lays down law on BPO-KPO & abnormal high profit margin

comparable

Maersk Global Centres (India) P. Ltd. [TS-74-ITAT-2014(Mum)-TP]

16. Delhi ITAT : Nortel US mere "shadow" company; Indian arm constitutes PE,

attributes 50% profit

Nortel Networks India International Inc. [TS-355-ITAT-2014(DEL)]

17. Mumbai ITAT : Disproportionate / non-uniform allotment under rights issue

can attract rigours of Sec. 56(2)(vii)(c)

Sudhir Menon HUF [TS-146-ITAT-2014(Mum)]

18. Mumbai ITAT : Raises alarm over CA's reckless advice, calls

ICAI to stem "deteriorating standards"

Vijay V Meghani [TS-548-ITAT-2014(Mum)]

19. Mumbai ITAT : Emphatic Revenue victory in Vodafone TP call options case;

Tribunal pierces 'Corporate Veil

Vodafone India Services Private Ltd. [TS-422-ITAT-2014(Mum)-TP]

20. Sessions Court : Favorable ITAT order no saviour for

Jayalalitha in corruption case

State vs. J. Jayalalitha & Others

YEAR END SPECIAL - 2014!

8

Top judgments of 2014 picked by Experts

Each of the experts has picked their Top 5 rulings of the year for the 3rd edition of

Taxsutra’s book – Top 100 Income-tax Rulings of 2014, being published by CCH.

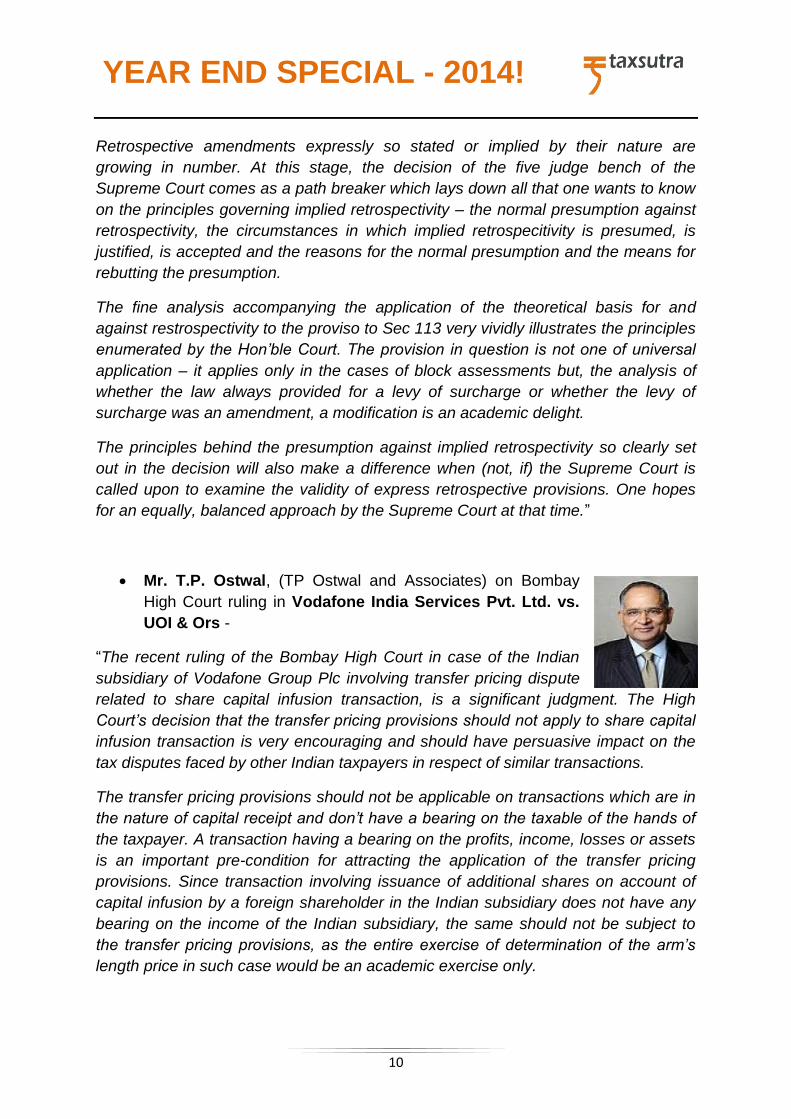

Mr. Dinesh Kanabar (CEO , Dhruva Tax Advisors) on

Supreme Court ruling in Madras Bar Association v. Union of

India –

“The striking down of the proposed National Tax Tribunal by a

Constitution bench of the Supreme Court is without doubt one of the

most far reaching decisions in recent times. In arriving at this conclusion, the Court

referred to the basic structure doctrine expounded in the landmark Kesavananda

Bharati case and held that when judicial powers are sought to be transferred to

newly created tribunals, Parliament must ensure that such tribunals must confirm to

the salient characteristics and standards of the Courts.

Not only does this judgment have immediate ramifications in terms of the setting up

of the National Tax Tribunal, the various observations and findings of the Court will

have a significant bearing on the formation and operations of tribunals generally. If

implemented, they will also help ensure that such dispute resolution mechanisms

remain independent and highly effective.”

Mr.Ketan Dalal (Managing Partner (West) and Sr. Partner,

Tax & Regulatory Services, PwC India) on Delhi Tribunal ruling in

GE Energy Parts Inc. v. ADIT –

“In this case, the LinkedIn profile of employees filed by the revenue

was admitted as additional evidence, and the assessee’s argument

that LinkedIn profiles being self appraisal of employees should not be considered

was overruled. The issue before the Tribunal was whether there is a permanent

establishment existence based on factual finding, and that is the context in which the

LinkedIn profile of the employees was considered as relevant for the purpose of

determining the existence of the PE.

While these decisions will certainly be agitated further, it drives home the importance

of social media and that communication through social media is nowadays taken

cognizance of by judicial authorities and considered as evidence.”

YEAR END SPECIAL - 2014!

9

Mr. Mukesh Butani (Managing Partner , BMR Legal) on

Delhi High Court ruling in Radials International vs

Assistant Commissioner of Income-tax -

“Whether income from PMS scheme has to be characterized as

business income or capital gains has been a bone of contention for

several investors and PMS service providers from the point of view of withholding tax

obligation. The HC has laid down broad principles that ease the task of such an

exercise. Whilst doing so, it has highlighted important principles on Assessee’s intent

being inferred holistically, the fact that that such intent cannot be judged at the time

of deposit. It also highlighted that the number of transactions and period of holding

cannot be a determinative test for characterization, a principle laid down in the CBDT

circular and followed by several tribunals. Taking note of the PMS agreement, it held

that the intent to make profit from such investment cannot be the sole guiding factor.

It relied on SC ruling in the case of Motors & General stores that highlighted that the

agreement is not conclusive and Courts are expected to assess its true impact. The

Delhi HC affords another opportunity to put the controversy at rest by clarifying the

law and lend clarity to the vexed issue.”

Mr . Gautam Doshi (Reliance Anil Dhirubhai Ambani

Group ) on Supreme Court ruling in CIT vs. Vatika Township

Pvt. Ltd. -

“Legislative drafting is a fine art. A good piece of legislation

normally, survives the passage of time. The same words do take

different colours in changing times and thereby achieve the intention of the

legislature. But, sometimes it may be found that the language has failed to capture

certain nuances - either because the situation giving rise to those nuances did not

exist or was not envisaged or merely because the language fails to carry the

intended meaning. In such cases, it is an accepted position that the Legislature can

clarify, explain or declare what the law always intended. Such amendments can be

and often are expressly, stated to be retrospective. But, even if it is not so stated,

such amendments can have retrospective effect.

YEAR END SPECIAL - 2014!

10

Retrospective amendments expressly so stated or implied by their nature are

growing in number. At this stage, the decision of the five judge bench of the

Supreme Court comes as a path breaker which lays down all that one wants to know

on the principles governing implied retrospectivity – the normal presumption against

retrospectivity, the circumstances in which implied retrospecitivity is presumed, is

justified, is accepted and the reasons for the normal presumption and the means for

rebutting the presumption.

The fine analysis accompanying the application of the theoretical basis for and

against restrospectivity to the proviso to Sec 113 very vividly illustrates the principles

enumerated by the Hon’ble Court. The provision in question is not one of universal

application – it applies only in the cases of block assessments but, the analysis of

whether the law always provided for a levy of surcharge or whether the levy of

surcharge was an amendment, a modification is an academic delight.

The principles behind the presumption against implied retrospectivity so clearly set

out in the decision will also make a difference when (not, if) the Supreme Court is

called upon to examine the validity of express retrospective provisions. One hopes

for an equally, balanced approach by the Supreme Court at that time.”

Mr. T.P. Ostwal, (TP Ostwal and Associates) on Bombay

High Court ruling in Vodafone India Services Pvt. Ltd. vs.

UOI & Ors -

“The recent ruling of the Bombay High Court in case of the Indian

subsidiary of Vodafone Group Plc involving transfer pricing dispute

related to share capital infusion transaction, is a significant judgment. The High

Court’s decision that the transfer pricing provisions should not apply to share capital

infusion transaction is very encouraging and should have persuasive impact on the

tax disputes faced by other Indian taxpayers in respect of similar transactions.

The transfer pricing provisions should not be applicable on transactions which are in

the nature of capital receipt and don’t have a bearing on the taxable of the hands of

the taxpayer. A transaction having a bearing on the profits, income, losses or assets

is an important pre-condition for attracting the application of the transfer pricing

provisions. Since transaction involving issuance of additional shares on account of

capital infusion by a foreign shareholder in the Indian subsidiary does not have any

bearing on the income of the Indian subsidiary, the same should not be subject to

the transfer pricing provisions, as the entire exercise of determination of the arm’s

length price in such case would be an academic exercise only.

YEAR END SPECIAL - 2014!

11

The on-going transfer pricing litigation on share issue transaction has been a drain

on India's reputation and has been a dampener on the foreign direct investment into

the country in last few years. With this decision of the Bombay high court, it is likely

expectation that the on-going controversy around the share issue transaction will get

settled and hopefully, the Revenue will not take the dispute further to the Supreme

Court and let the High Court decision prevail. This would have a positive impact on

the overall tax environment in India and should encourage Multinationals to infuse

additional equity in the Indian subsidiaries for on-going business expansion plans

without any hassle.”

Mr. Ajay Vohra, Senior Advocate on Delhi High Court ruling in DIT vs. Copal

Research Ltd. and Ors.-

“The Delhi High Court in the aforesaid case, dismissed the writ

petitions filed by the tax authorities against the ruling of the Authority

for Advance Rulings (AAR), wherein it was held that the capital gains

arising on sale of shares of an Indian company by a Mauritius

company (Direct Transfer), and on the sale of shares of a US

company (which in turn held shares of an Indian company) by another Mauritian

company (Indirect Transfer), shall not be chargeable to tax in India in accordance

with the provisions of Article 13(4) of the India -Mauritius Tax Treaty.

The decision has been welcomed by foreign investors and is likely to bring much

needed clarity as regards the Treaty entitlement in respect of capital gains to a

Mauritian investor.

This decision reaffirms the principles articulated by the Supreme Court in the case of

Vodafone BV on legitimacy of corporate holding company structures. The High Court

has unequivocally held that a company cannot be disregarded as a mere sham

merely on the ground of being an intermediate or holding entity.”

Mr. Sunil Kapadia , (Senior Partner, E&Y) on Delhi High Court ruling in

Centrica India Offshore Pvt Ltd vs Commissioner of

Income-tax - I & ORS -

“Secondment of employees by foreign companies to Indian affiliates

is a common practice amongst multinational groups. Such

arrangements have been under the constant scrutiny of the tax

authority in India and have been the subject matter of controversy/litigation in the

absence of specific provisions in the Indian Tax Laws (‘ITL’). Various judicial

YEAR END SPECIAL - 2014!

12

precedents have looked at diverse factors to determine who is the “real” employer or

“economic” employer of the seconded employees. The concept of “economic

employer”, other than the “legal employer”, is also acknowledged in various

international commentaries/rulings. It also assumes significance for determining tax

liability of such employees in the host jurisdiction. In certain cases, where the Indian

entity (which receives the seconded employees) is seen as the economic employer,

presence of such employees has been held to be not triggering Permanent

Establishment (‘PE’) exposure or service arrangement for the overseas legal entity

seconding employees. Under such circumstances, a payment by the Indian entity to

the overseas entity through whom salary is disbursed is accepted to be a non-

chargeable payment in the nature of reimbursement of salary costs. As against that,

a contract of service through employees triggers tax liability, including transfer

pricing and tax withholding obligation for the parties.This unfavourable ruling of the

Delhi High Court (‘HC’) follows a different approach by considering the legal

employment relationship, right to termination contract and right of employees to

enforce payment of salary as crucial factors to determine the ‘employer’ of the

assignees. Multinationals may need to critically consider and evaluate impact of this

ruling on their existing/proposed secondments.”

K.R. Sekar (Partner & Co-Lead Global Business Tax- Deloitte

Haskins&Sells ) on Mumbai Tribunal ruling in Sudhir Menon HUF vs

Assistant Commissioner of Income-tax -

“The conclusion by Mumbai Tribunal on the application of Section

56(2)(vii) (c ) on the issuance of rights issue has a far reaching

implications. The Mumbai Tribunal observed that Tribunal is not competent to read

down the provision of Section 56(2) (vii) to conclude that this provision applies only

for transfer and not for allotment creates an interesting debate on the powers and

approach of Tribunal. Ignoring the rationale behind the introduction of section

56(2)(vii) which is self- contained Anti-Avoidance Regulations by itself, the moot

point arises is whether the approach of Tribunal is correct. In my humble view it is in-

correct. Though Tribunal made a passing remark that Bonus issue stands on a

different footing from right issue, yet the conclusion by Tribunal may lead to

significant tax debate on the power/approach to be adopted by Tribunal in

interpreting law. The conclusion of Mumbai Tribunal on the definition of Income in

the context of Anti-Avoidance Regulation is contrary to views expressed by Bombay

High Court in Vodafone, though the HC ruling came later. This ruling indicates how

the judicial thinking can be divergent on important principles thus leading to

“avoidable legal disputes”.”

YEAR END SPECIAL - 2014!

13

Cases to watch out for in 2015

(Excerpts from the book Top 100 Income-Tax Rulings of 2014, being published by

CCH)

1. Kalanithi Maran & Ors (Supreme Court)

A bench headed by then Chief Justice of India – R.M. Lodha, was quick to stay the

Madras HC judgment, that had literally shut the door on writ petitions against re-

assessment orders. Madras HC had ruled that where hierarchy of

remedy of appeals are provided in a fiscal statute, party has to

exhaust them instead of seeking relief by invoking writ jurisdiction

of Court, which according to the Court, was 'discretionary' and

'extraordinary'. The Court further observed that in writ petition,

Court is concerned with decision making process adopted by an

authority, rather than decision itself. Differentiating between

'jurisdictional' fact and 'adjudicating' fact, HC had held that where

an adjudicatory process was involved on merits, then only remedy open to an

assessee was to go through procedure provided under the enactment. HC further

had rejected assessees' strong reliance on SC ruling in Calcutta Discount and

observed that factual position prevailing then, no longer existed. The fact that Sr.

Advocate Harish Salve appeared for the assessees in Supreme Court, is a good

indicator of how important this case is.

2. IBM (Supreme Court)

Not many cases get an early hearing. This is one of those

few and for good reason – the issue of taxability of packaged

software payments has a significant impact on the software

industry. The Karnataka HC ruled that consideration paid by

the assessee to a foreign supplier for transfer of right to use

the software or computer program, was taxable as royalty u/s

9(1)(vi) of the Income tax Act. Harish Salve once again,

leading the charge on behalf of the assessees!

3. Cannon India (Delhi HC)

Let there be no doubt whatsoever that whichever

way the Delhi HC rules in the marketing intangibles

case, it will make it to our Top 20 rulings next year!

The marathon hearings in High Court were

YEAR END SPECIAL - 2014!

14

concluded in November 2014, with an array of top lawyers appearing for taxpayers,

arguing that the ITAT Special Bench decision in LG must be set aside. The issue of

marketing intangibles, i.e. Advertising, Marketing & Promotion (AMP) has fast

become one of the most litigated Transfer Pricing issues in India, but be rest assured

that other jurisdictions too will be closely following the HC verdict, which is expected

early in the new year!

4. Expro Gulf Ltd. (Uttarakhand HC)

This could turn out to be one of those sleeper of a case, and Uttarakhand HC has

seen quite a few of them in the last couple

of years (remember the case challenging

the constitutional validity of DRP?). The

CBDT’s notification (Nov. 2013) declaring

Cyprus as a non-cooperative jurisdiction,

has been challenged vide a writ petition,

with the petitioner arguing that the said notification supersedes the India-Cyprus

DTAA and hence ought to be struck down, since the DTAA ought to prevail over

domestic law. The notification has serious consequences on availing deduction with

regard to transactions with Cyprus parties, transfer pricing implications and a higher

TDS rate on payments to Cyprus entities.

5. Poompuhar Shipping Corporation (Supreme Court)

The judgment delivered by Madras HC in this case, made it to our Top 20 Rulings of

2013. Hence but natural that the Apex Court admitting the assessee’s SLP should

find a prominent mention in this space. HC had ruled that income from time

chartering or use of ships constitutes equipment royalty u/s 9(1)(vi)(b). It also held

that ship constitutes ‘equipment’ and that meaning of equipment under royalty

definition should be construed widely.

YEAR END SPECIAL - 2014!

15

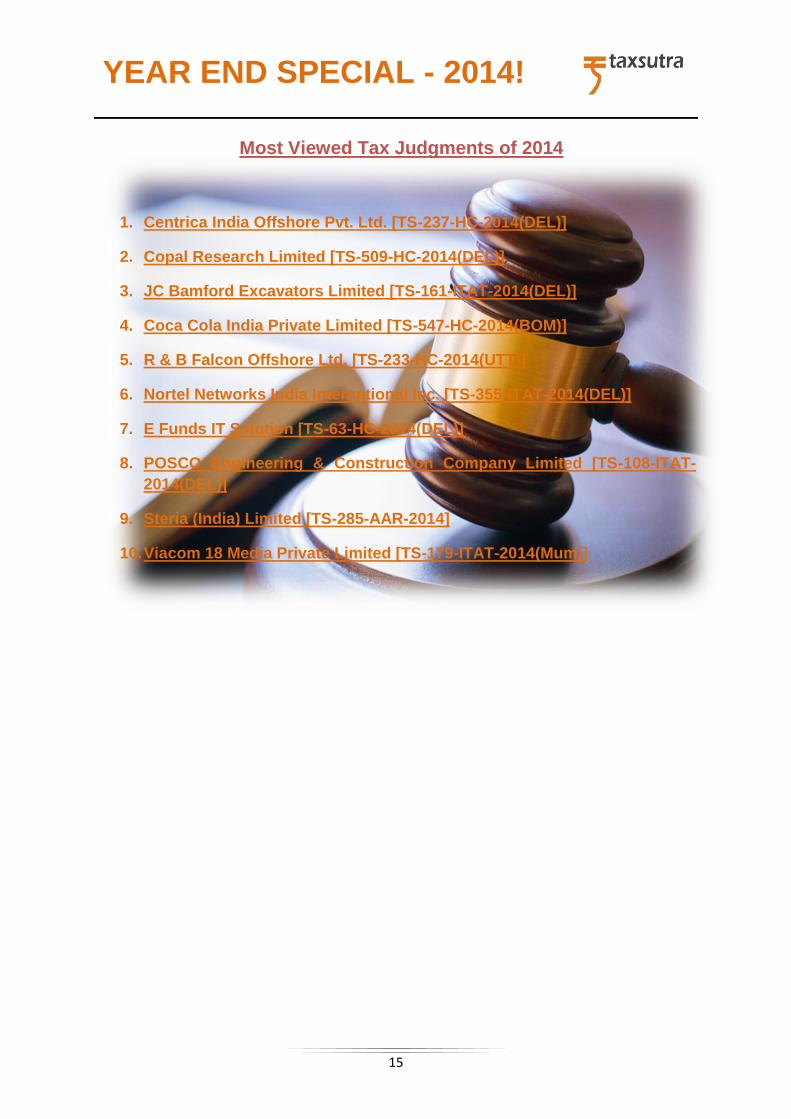

Most Viewed Tax Judgments of 2014

1. Centrica India Offshore Pvt. Ltd. [TS-237-HC-2014(DEL)]

2. Copal Research Limited [TS-509-HC-2014(DEL)]

3. JC Bamford Excavators Limited [TS-161-ITAT-2014(DEL)]

4. Coca Cola India Private Limited [TS-547-HC-2014(BOM)]

5. R & B Falcon Offshore Ltd. [TS-233-HC-2014(UTT)]

6. Nortel Networks India International Inc. [TS-355-ITAT-2014(DEL)]

7. E Funds IT Solution [TS-63-HC-2014(DEL)]

8. POSCO Engineering & Construction Company Limited [TS-108-ITAT-

2014(DEL)]

9. Steria (India) Limited [TS-285-AAR-2014]

10. Viacom 18 Media Private Limited [TS-179-ITAT-2014(Mum)]

YEAR END SPECIAL - 2014!

16

Most Viewed Expert Columns of 2014

1. Analysis of section 35AD changes

Decoding Finance Bill, 2014, Milind Kothari (Managing Partner,

BDO INDIA LLP) analysed the changes relating to Section 35AD,

which provides for deduction in computing taxable income in

respect of capital expenditure (other than expenditure on

acquisition of land or goodwill or financial instrument) incurred for

the purposes of specified business prior to commencement of

operations of such business. The author wrote how the

amendment would have positive and negative affects. He

concluded by writing, “While the deduction is well-intended to grant deduction in

respect of investment in specified businesses, it remains to be seen that needless

controversies are not created while administering the benefit under this section

which has been the bugbear of many such provisions under the Act.”

2. Sec 14A disallowance when there is no exempt income – An unsettled

controversy

Rohit Garg (Senior Associate, Vaish Associate, Advocates) in

his article discussed the issue that whether Section 14A

disallowance can be made in the year when no exempt income has

been earned or received by assessee. Noting that various High

Courts had given relief to the taxpayer on this issue despite the

adverse Special Bench decision in Cheminvest, the author wrote, “It

would now be interesting to see what view would other High Court

(s) take, especially Delhi High Court where the assessee’s appeal is

pending in the case of Cheminvest Ltd (surpa).”

3. CBDT's benevolent circular on TDS on service tax - Putting controversy at

rest?

K R Girish, Partner and Dinesh Daga, Senior Manager of BSR

& Co LLP, in their article, traced the background and judicial

developments necessitating issuance of Circular 1/2014 that

relaxed withholding on service tax component on payments to

residents. On the question of when the Circular comes into

effect, they believe “In the absence of any effective date

mentioned in Circular, the said Circular ought to be effective with

YEAR END SPECIAL - 2014!

17

immediate effect.”

4. The long and short of it – Period of holding for capital gains

While decoding Finance Bill, 2014 which proposed an increase in the

period of holding for capital gains on transfer of certain securities to

be ‘long-term’ from 12 months to 36 months, Tejas Desai (Partner,

EY) and Shonna Mascarenhas (Manager, EY) talked about the amendment and its

effects. They wrote, “The proposed change in the holding period of unlisted debt

units coupled with removal of the concessional rate of 10%, is likely to put a strain on

the asset management industry.”

5. Corporate Social Responsibility (CSR) Deduction - a

critique

The Finance (No 2) Bill, 2014 brought about a far-reaching

amendment as far as Corporate Social Responsibility (‘CSR’)

expenditures by corporates are concerned. While the newly

enacted Companies Act, 2013 mandates corporates to incur

the said expenditure, the Bill proposes that CSR expenditure

shall not be deductible u/s 37 of Income Tax Act. Giving a

critique on CSR expenditure deduction non-allowability u/s 37, Nihar Jambusaria

(Sr. Vice President-Taxation, Reliance Industries Ltd) wrote, “The proposed

amendment in the Bill does not provide a level playing field for all kinds of CSR

expenditure. If CSR is not treated as an allowable expenditure, Companies would be

inclined to give funds only to those organisations where they get maximum tax

benefit.”

YEAR END SPECIAL - 2014!

18

Most Viewed Tax Ring of 2014

5 ideas for new FM to end "tax terrorism"

Ruling party BJP's election manifesto promised a slew of radical changes to both tax

policy and approach to tax disputes. BJP accused the UPA govt. of unleashing 'tax

terrorism' and 'uncertainty', thereby creating anxiety amongst the business class and

negatively impacting the investment climate. It also called for a 'non-adversarial',

'conducive' tax environment and a tax policy roadmap, that would include a simplified

tax regime and an 'overhaul' of the dispute resolution

mechanism.

So what are the immediate steps that the new Finance Minister

Arun Jaitley needs to take, so as to put an end to 'tax terrorism'

and bring back foreign investors?

Tax experts Mr. Mohan Parasaran (Senior Advocate & Former Solicitor General of

India), Mr. Girish Dave (Former Chief Commissioner of Income Tax), Mr. Rupak

Saha, (GE India), Mr. Nihar Jambusaria (Reliance Industries Ltd.) Ms. S.

Gayathri (Essar Energy Business), Mr.Krishan Malhotra (Amarchand & Mangaldas

& Suresh a. Shroff & Co.), Mr. Uday Ved(Chartered

Accountant) Mr. K.R. Sekar (Deloitte Haskins & Sells), Mr. Mukesh Butani (BMR

Legal) and Mr. Sunil Kapadia (EY LLP) shared their views.

Click here to read what the above experts stated.

YEAR END SPECIAL - 2014!

19

3 Significant Transfer Pricing Moments of 2014

2014 will be remembered as a year dotted with some significant developments from

a transfer pricing standpoint. Whether it was signing of the first bilateral APA with

Japan or landmark Bombay HC verdict on Vodafone / Shell's share issue transaction

or OECD's BEPS initiatives, this year has seen some major evolution in the Indian as

well as global transfer pricing landscape.

As we say goodbye to 2014, top tax professionals talk about the significant moments

in their opinion, on developments relating to transfer pricing during 2014. Excerpts

from Taxsutra’s Tax Ring :

Rahul Mitra (Chartered Accountant)

“The year of 2014 was a milestone in transfer pricing (TP),

both in the global and Indian landscapes. From the global

standpoint, OECD issued a number of position papers and

discussion drafts on TP under the BEPS initiative, which aim

at creating a more transparent regime of reporting by MNCs of

their global supply chain; and also re-enforcing the concept of

substance in the context of TP. The emphasis on intangibles, risks associated with

functions, etc would define the way Revenue Administrators across the world would

view TP in the coming years.”

Sudhir Nayak (Partner, International Tax, Sudit K. Parekh &

Co.)

“The year 2014 saw the Tax courts deciding on a number of

vexing transfer pricing issues like issue of equity shares,

corporate guarantee. The courts have given well reasoned

orders on these controversial issues in the case of Vodafone,

Shell and Bharati Airtel. These pronouncements would serve as guiding principles

for taxpayers while determining the applicability of transfer pricing provisions to such

transactions and also help put to rest similar controversies involving high value

transactions in the coming years.”

YEAR END SPECIAL - 2014!

20

Subhankar Sinha (VP, Head of Taxation, Siemens South

Asia)

“When we look back to the developments in the transfer pricing

arena during 2014, clearly the most pleasant surprise came from

the Finance Minister when he introduced the NDA government’s

first Budget in July this year. Introduction of range concept as

against arithmetic mean for determining arm’s length prices; use

of multiple year data up to two prior years instead of restricting the comparables’

financial data only to the year under evaluation; rollback provisions for Advance

Pricing Agreements will go a long way in simplifying our transfer pricing laws and

reducing long drawn disputes. With these measures, India has moved a step closer

to best practices that are followed by other mature jurisdictions of the world.”

Amod Khare (Partner, Transfer Pricing, BMR Advisors)

“Another big reason for cheer in 2014 was the Bombay High Court

decision on the applicability of transfer pricing provisions to issue

of shares. With the Honorable High Court ruling that transfer

pricing provisions should not be applicable to transactions that

have no element of income in them, the potential tidal wave of adjustments on non-

existent income have been kept at bay. (At least till Budget 2015!)”

Ajay Rotti (Partner, Dhruva Tax Advisors LLP)

“In the year gone by, the Government, after seeing a good

response to the Advance Pricing Agreements, introduced the

rollback mechanism. The amendment enables the taxpayer to

apply a concluded APA to international transactions in four

previous years covered in the APA. Interestingly, restricted use of

multiple year data and use of arithmetic mean have contributed the most to the

current TP litigations on benchmarking. The Indian TP provisions were aligned to

global best practices by permitting use of range and multiple year data.

APA rollback and rationalisation of TP regulations would go a long way in reducing

the transfer pricing litigations and is encouraging given that it signals the intent to

address the problem of growing tax litigation.”

YEAR END SPECIAL - 2014!

21

Rohan K Phatarphekar (Partner and National Leader -

Transfer Pricing, KPMG India)

“Another important development in the Indian TP landscape was

the decision in case of SogaShosha companies, which are

Japanese entities, engaged in general trading of diverse range

of products. The Delhi Tribunal in case of Mitsubishi Corporation

not only clearly distinguished the SogaShosha entities from other normal trading

companies but also reiterated certain important points relating to attribution of profits

in case of location savings and other routine intangibles. The Tribunal stated that in

computation of arms length profits it was not necessary to consider the entire

turnover or cost of goods as a component but comparison could be based on Berry

Ratio ( Gross Profit to Operating expenses ratio) where taxpayer did not assume

significant inventory risk or perform any value added functions. The upholding of the

use of the berry ratio augurs well not only for Soga Shosha companies but also for

commissionaire and limited risk distributor arrangements. Also, based on the OECDs

view the Tribunal ruling clarified that there was no need for allocation of additional

returns where location savings were passed on to the customers and where no non-

routine intangibles existed in the Indian company.”

Sanjay Tolia (Country Leader, Transfer Pricing Practice, Price

Waterhouse & Co LLP)

“The appointment of the Modi Government, India's successful

mission to Mars and the awarding of Nobel Peace Prize jointly to

Kailash Satyarthi and Malala Yousafzai for their struggle against

the suppression of children and young people and for the right of

all children to education would be considered as landmark moments in the history of

India. Equally so, it is going to be a memorable year for the world of Transfer Pricing!

2014 saw some significant developments within India ranging from signing of 5

unilateral APA's and 1 Bilateral APA with Japan, introduction of the range and roll-

back concepts, enabling use of multiple year data, expansion of APA team to

introduction of stringent regulations for related party disclosures under the

Companies Act and SEBI Rules.”

Click here to read the full article.

YEAR END SPECIAL - 2014!

22

'Crystal Ball Gazing 2015 - Tax trends to watch out for

(Excerpts from the book Top 100 Income-Tax Rulings of 2014, being published by

CCH)

Girish Vanvari, Co-Head of Tax, KPMG in India

Promote the Ease of Doing Business in India by

providing clarity on tax laws

Considering the need to promote the ease of doing business in

India and to attract FDI into the country, one may see the government providing

clarity on the certain ambiguous provisions in the present tax laws.

One may expect clarity on the manner of taxability of offshore transactions involving

indirect transfer of assets in India by the introduction of rules in this regard. In

formulating the same one could also see many of the recommendations of the

Shome Committee finding its place in the final regulations.

Provisions such as prescribing a 50% threshold for global assets to be located in

India to determine ‘substantiality of value derived from India’, prescribing safe

harbours for portfolio investments, foreign listed companies and group restructuring

from the applicability of these provisions could be a reality.

Also the government may choose to defer the implementation of the General Anti

Avoidance Rules which are slated to come into effect from 1st April 2015 considering

the uncertainty created by its introduction in the international investor community

coupled with the perceived lack of readiness for its implementation.

Formulating a ‘Future ready’ Tax Legislation

The Modi government may choose to rethink the tax policies and

administration practices with a fresh mind and align the same

with the present economic reality rather than improvise upon an

earlier piece of draft legislation i.e. the Direct Tax Code.

Also considering the fact that many of the provisions proposed in

the DTC such as introduction of capital gains tax on indirect

transfer and general tax avoidance rules have already been incorporated in the

prevailing law, the government would do well to wait for a consensus to emerge from

the various debates / committee proposals on various issues such as Base Erosion

and Profit Shifting (‘BEPS’), Tax Administration Reform Commission (TARC)

recommendations etc before introducing a robust tax legislation that adopts the

global best practices in India. One could expect the government to announce various

measures towards formulating a ‘future ready’ tax framework.

YEAR END SPECIAL - 2014!

23

Coming Soon…