Embed Size (px)

Citation preview

Your Guide to Getting Started in the UNE Defined Contribution Plan

Invest some of what you earn today for what you plan toaccomplish tomorrow.

Dear Employee:

UNE offers a generous matching contribution, outstanding convenience, and a variety of investmentoptions. Take a look and see what a difference enrolling in the plan could make in achievingyour goals.

Benefit from:

Matching contributions. UNE helps your contributions grow through a generous Employer matchof up to 8% annually — it’s like getting “free” money. That’s why it makes good financial sense tocontribute at least this amount of your salary to the plan. Take advantage of this greatbenefit today!

Retirement planning tools. You have access to online tools designed to help you manage yourassets as you plan for retirement.

Convenience. Your contributions are automatically deducted regularly from your paycheck.

Tax savings now. Your pretax contributions are deducted from your pay before income taxes aretaken out. This means that you can actually lower the amount of current income taxes you pay eachperiod. It could mean more money in your take-home pay versus saving money in ataxable account.

Tax-deferred savings opportunities. You pay no taxes on any earnings until you withdraw themfrom your account, enabling you to keep more of your money working for you now.

Investment options. You have the flexibility to select from investment options that range frommore conservative to more aggressive, making it easy for you to develop a well-diversifiedinvestment portfolio.

Automatic annual increases. Save a little more each year, the easy way — the Annual IncreaseProgram automatically increases your contribution each year on the date that you choose.

Online beneficiary. With Fidelity’s Online Beneficiaries Service, you can designate yourbeneficiaries, receive instant online confirmation, and check your beneficiary information virtuallyany time.

Catch-up contributions. If you make the maximum contribution to your plan account, and you are50 years of age or older during the calendar year, you can make an additional “catch-up”contribution of $6,000 in 2019.

To learn more about what your plan offers, see “Frequently asked questions about your plan” laterin this guide.

Enroll in your plan and invest in yourself today.

FAQ

sFo

r mo

re inform

ation visit w

ww

.netbenefits.co

m/une o

r call 1-800-343-0860

Frequently asked questions about your plan.Here are answers to questions you may have about the key features, benefits, and rules of your plan.

When can I enroll in the Plan?

There is no waiting period. You can enroll inthe Plan at any time.

How do I enroll in the Plan?

Enroll online at any time, click on the "Enroll-Sign up Now" box in the center of the homepage and the system will guide you throughthe enrollment process. You can also enroll bycontacting the Fidelity Retirement BenefitsLine at 1-800-343-0860.

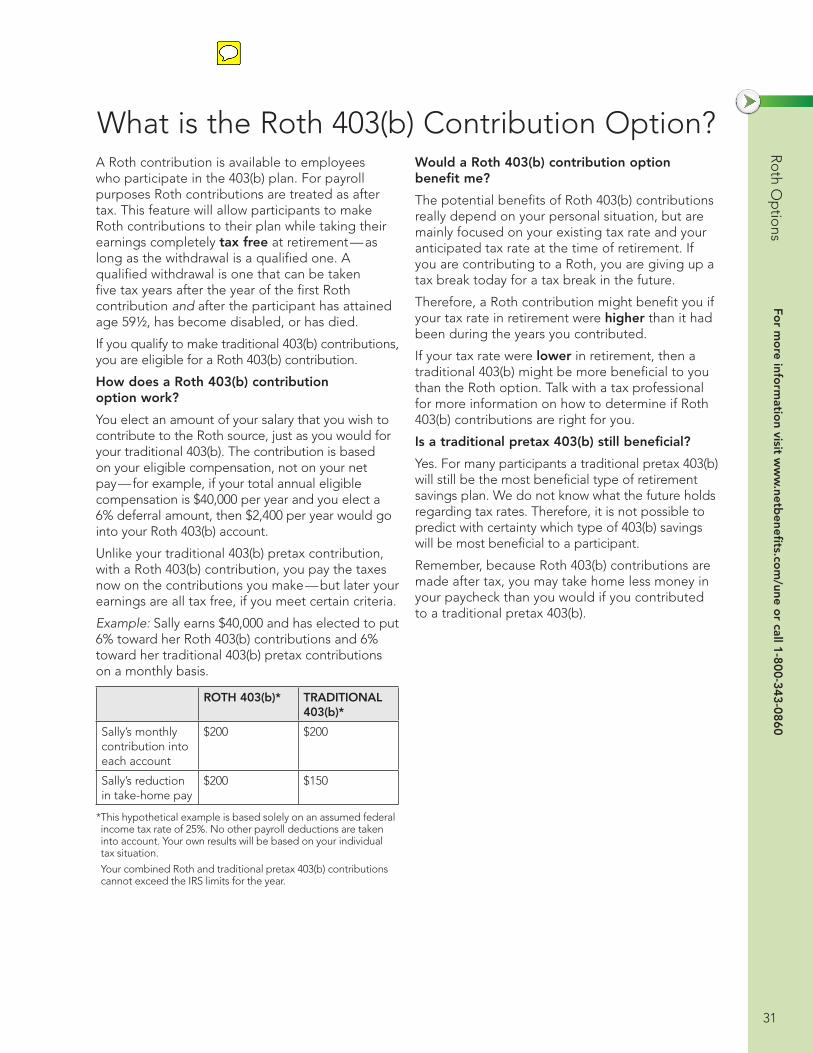

What is the Roth contribution option?

A Roth contribution to your retirement savingsplan allows you to make after-tax contributionsand take any associated earnings completelytax free at retirement - as long as thedistribution is a qualified one. A qualifieddistribution, in this case, is one that is taken atleast five tax years after your first Roth 403(b)contribution and after you have attained age59½, or become disabled or die. Throughautomatic payroll deduction, you cancontribute between 1% and 100% of youreligible pay as designated Roth contributions,up to the annual IRS dollar limits.

Find more information online within the“Library” section of NetBenefits®.

How much can I contribute?

Through automatic payroll deduction, you maycontribute up to 100% of your eligible pay on apretax or after-tax Roth basis. In addition, youcan automatically increase your retirementsavings plan contributions each year throughthe Annual Increase Program. Employeesdetermined to be highly compensated mayhave additional limitations. Sign up online byaccessing the “Contribution Amount” section

on NetBenefits®, or by calling the FidelityRetirement Benefits Line at 1-800-343-0860.

What is the IRS contribution limit?

The IRS contribution limit for 2019 is $19,000.

When is my enrollment effective?

Your enrollment becomes effective once youelect a deferral percentage, which initiatesdeduction of your contributions from your pay.These salary deductions will generally beginwith the first payroll of the month followingyour eligibility or enrollment in the Plan.However, the payroll deduction effective datemay be determined depending upon whenyou elect your deferral amount with Fidelity.

Does the Employer contribute to myaccount?

UNE helps your retirement savings grow by matching up to 8% of your pretax contributions to the plan. PLEASE NOTE: The UNE match ONLY applies to the pretax contributions and not your Roth contributions.

You are eligible for the matching contributionafter completing 12 consecutive months ofservice in higher education.

How do I designate my beneficiary?

If you have not already selected yourbeneficiaries, or if you have experienced a life-changing event such as a marriage, divorce,birth of a child, or a death in the family, it’s timeto consider your beneficiary designations.Fidelity’s Online Beneficiaries Service, offers astraightforward, convenient process that takesjust minutes. To make your elections, click onthe “Profile” link, then select “Beneficiaries”and follow the online instructions.

1

FAQ

s

What are my investment options?

To help you meet your investment goals, thePlan offers you a range of options. You canselect a mix of investment options that bestsuits your goals, time horizon, and risktolerance. The many investment optionsavailable through the Plan includeconservative, moderately conservative, andaggressive funds. A complete description ofthe Plan’s investment options and theirperformance, as well as planning tools to helpyou choose an appropriate mix, are availableonline.

What if I don’t make an investmentelection?

We encourage you to take an active role in theUNE Retirement Plan and choose investmentoptions that best suit your goals, time horizon,and risk tolerance. If you do not select specificinvestment options in the Plan, yourcontributions will be invested in the FidelityFreedom® Fund with the target retirement dateclosest to the year you might retire, based onyour current age and assuming a retirementage of 65, at the direction of UNE.

If no date of birth or an invalid date of birth ison file at Fidelity your contributions may beinvested in the Fidelity Freedom® IncomeFund. More information about the FidelityFreedom® Fund options can be found online.

Target Date Funds are an asset mix of stocks,bonds and other investments thatautomatically becomes more conservative asthe fund approaches its target retirement dateand beyond. Principal invested is notguaranteed.

How much should I save for retirement?

Fidelity’s online planning tools are designed tohelp you manage your assets as you plan forretirement.

What "catch-up" contribution can I make?

If you have reached age 50 or will reach 50during the calendar year January 1 –December 31 and are making the maximumplan or IRS pretax contribution, you may make

an additional “catch-up” contribution each payperiod. The maximum annual catch-upcontribution is $6,000. Going forward, catch-upcontribution limits will be subject to cost ofliving adjustments (COLAs) in $500 increments.

When am I vested?

You are immediately 100% vested in your owncontributions to the UNE Retirement Plan, aswell as in any of the organization’s matchingcontributions and any earnings on them.

Can I take a loan from my account?

Although your plan account is intended for thefuture, you may borrow from your account forany reason.

Learn more about and/or request a loanonline, or by calling the Fidelity RetirementBenefits Line at 1-800-343-0860.

Can I make withdrawals?

Withdrawals from the Plan are generallypermitted when you terminate youremployment, retire, reach age 59½, becomepermanently disabled, have severe financialhardship, as defined by your plan.

Learn more about and/or request a withdrawalonline, or by calling the Fidelity RetirementBenefits Line at 1-800-343-0860.

Can I move money from another retirementplan into my account in the UNE RetirementPlan?

You are permitted to roll over eligible pretaxcontributions from another 401(k) plan, 401(a)plan, 403(b) plan or a governmental 457(b)retirement plan account or eligible pretaxcontributions from contributions from conduitindividual retirement accounts (IRAs). A conduitIRA is one that contains only money rolled overfrom an employer-sponsored retirement planthat has not been mixed with regular IRAcontributions.

Additional information can be obtained online,or by calling the Fidelity Retirement BenefitsLine at 1-800-343-0860.

2

FAQ

sFo

r mo

re inform

ation visit w

ww

.netbenefits.co

m/une o

r call 1-800-343-0860

Be sure to consider all your availableoptions and the applicable fees and featuresof each before moving your retirementassets.

3

FAQ

s

4

Investment O

ptio

nsFo

r mo

re inform

ation visit w

ww

.netbenefits.co

m/une o

r call 1-800-343-0860

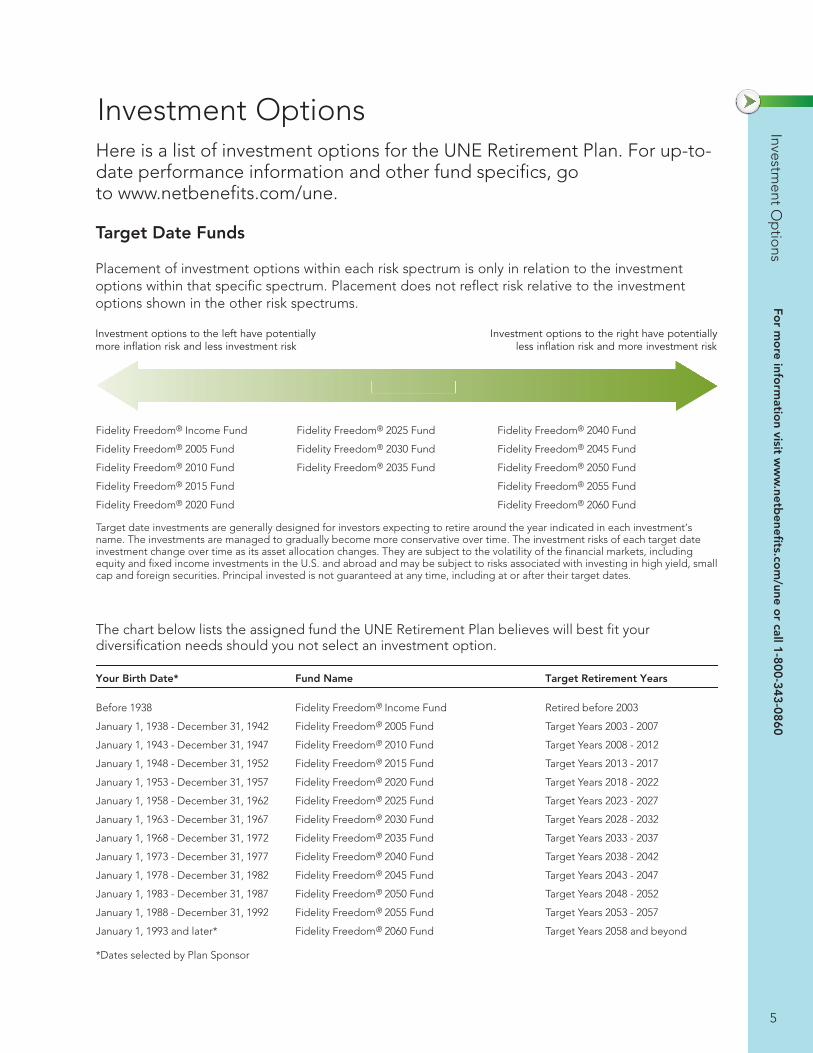

Investment OptionsHere is a list of investment options for the UNE Retirement Plan. For up-to-date performance information and other fund specifics, goto www.netbenefits.com/une.

Target Date Funds

Placement of investment options within each risk spectrum is only in relation to the investment options within that specific spectrum. Placement does not reflect risk relative to the investmentoptions shown in the other risk spectrums.

ptions to the left have potentiallymore inflation risk and less investment risk

ptions to the right have potentially less inflation risk and more investment risk

Investment o Investment o

Fidelity Freedom® Income Fund

Fidelity Freedom® 2005 Fund

Fidelity Freedom® 2010 Fund

Fidelity Freedom® 2015 Fund

Fidelity Freedom® 2020 Fund

Fidelity Freedom® 2025 Fund

Fidelity Freedom® 2030 Fund

Fidelity Freedom® 2035 Fund

Fidelity Freedom® 2040 Fund

Fidelity Freedom® 2045 Fund

Fidelity Freedom® 2050 Fund

Fidelity Freedom® 2055 Fund

Fidelity Freedom® 2060 Fund

Target date investments are generally designed for investors expecting to retire around the year indicated in each investment‘sname. The investments are managed to gradually become more conservative over time. The investment risks of each target dateinvestment change over time as its asset allocation changes. They are subject to the volatility of the financial markets, includingequity and fixed income investments in the U.S. and abroad and may be subject to risks associated with investing in high yield, smallcap and foreign securities. Principal invested is not guaranteed at any time, including at or after their target dates.

The chart below lists the assigned fund the UNE Retirement Plan believes will best fit yourdiversification needs should you not select an investment option.

Your Birth Date* Fund Name Target Retirement Years

Before 1938 Fidelity Freedom® Income Fund Retired before 2003

January 1, 1938 - December 31, 1942 Fidelity Freedom® 2005 Fund Target Years 2003 - 2007

January 1, 1943 - December 31, 1947 Fidelity Freedom® 2010 Fund Target Years 2008 - 2012

January 1, 1948 - December 31, 1952 Fidelity Freedom® 2015 Fund Target Years 2013 - 2017

January 1, 1953 - December 31, 1957 Fidelity Freedom® 2020 Fund Target Years 2018 - 2022

January 1, 1958 - December 31, 1962 Fidelity Freedom® 2025 Fund Target Years 2023 - 2027

January 1, 1963 - December 31, 1967 Fidelity Freedom® 2030 Fund Target Years 2028 - 2032

January 1, 1968 - December 31, 1972 Fidelity Freedom® 2035 Fund Target Years 2033 - 2037

January 1, 1973 - December 31, 1977 Fidelity Freedom® 2040 Fund Target Years 2038 - 2042

January 1, 1978 - December 31, 1982 Fidelity Freedom® 2045 Fund Target Years 2043 - 2047

January 1, 1983 - December 31, 1987 Fidelity Freedom® 2050 Fund Target Years 2048 - 2052

January 1, 1988 - December 31, 1992 Fidelity Freedom® 2055 Fund Target Years 2053 - 2057

January 1, 1993 and later* Fidelity Freedom® 2060 Fund Target Years 2058 and beyond

*Dates selected by Plan Sponsor

5

Inve

stm

ent

Op

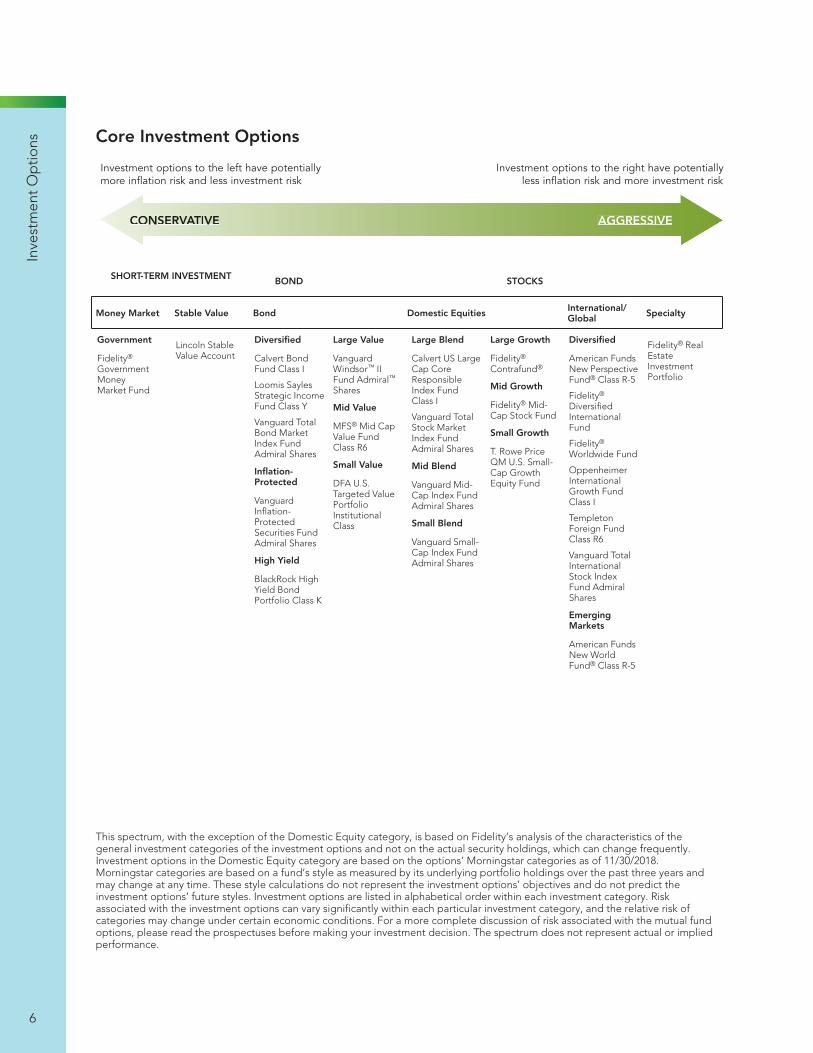

tions Core Investment Options

ft have potentially more inflation risk and less investment risk less inflation risk and more investment risk

CCONSEERVVATIIVE AGGRESSIVE

Investment options to the le Investment options to the right have potentially

SHORT-TERM INVESTMENT BOND STOCKS

Money Market Stable Value Bond Domestic Equities International/Global Specialty

Government

Fidelity® GovernmentMoneyMarket Fund

Lincoln StableValue Account

Diversified

Calvert BondFund Class I

Loomis SaylesStrategic IncomeFund Class Y

Vanguard TotalBond MarketIndex FundAdmiral Shares

Inflation-Protected

VanguardInflation-ProtectedSecurities FundAdmiral Shares

High Yield

BlackRock HighYield BondPortfolio Class K

Large Value

VanguardWindsor™ IIFund Admiral™ Shares

Mid Value

MFS® Mid CapValue FundClass R6

Small Value

DFA U.S.Targeted ValuePortfolioInstitutionalClass

Large Blend

Calvert US LargeCap CoreResponsibleIndex FundClass I

Vanguard TotalStock MarketIndex FundAdmiral Shares

Mid Blend

Vanguard Mid-Cap Index FundAdmiral Shares

Small Blend

Vanguard Small-Cap Index FundAdmiral Shares

Large Growth

Fidelity® Contrafund®

Mid Growth

Fidelity® Mid-Cap Stock Fund

Small Growth

T. Rowe PriceQM U.S. Small-Cap GrowthEquity Fund

Diversified

American FundsNew PerspectiveFund® Class R-5

Fidelity® DiversifiedInternationalFund

Fidelity® Worldwide Fund

OppenheimerInternationalGrowth FundClass I

TempletonForeign FundClass R6

Vanguard TotalInternationalStock IndexFund AdmiralShares

EmergingMarkets

American FundsNew WorldFund® Class R-5

Fidelity® RealEstateInvestmentPortfolio

This spectrum, with the exception of the Domestic Equity category, is based on Fidelity’s analysis of the characteristics of thegeneral investment categories of the investment options and not on the actual security holdings, which can change frequently.Investment options in the Domestic Equity category are based on the options’ Morningstar categories as of 11/30/2018.Morningstar categories are based on a fund’s style as measured by its underlying portfolio holdings over the past three years andmay change at any time. These style calculations do not represent the investment options’ objectives and do not predict theinvestment options’ future styles. Investment options are listed in alphabetical order within each investment category. Riskassociated with the investment options can vary significantly within each particular investment category, and the relative risk ofcategories may change under certain economic conditions. For a more complete discussion of risk associated with the mutual fundoptions, please read the prospectuses before making your investment decision. The spectrum does not represent actual or impliedperformance.

6

Investment O

ptio

nsFo

r mo

re inform

ation visit w

ww

.netbenefits.co

m/une o

r call 1-800-343-0860

Investment OptionsBefore investing in any mutual fund, consider the investment objectives,risks, charges, and expenses. Contact Fidelity for a mutual fundprospectus or, if available, a summary prospectus containing thisinformation. Read it carefully.

American Funds New Perspective Fund® Class R-5

VRS Code: 046994

Fund Objective: The investment seeks long-term growth of capital; future income is a secondary objective.

Fund Strategy: The fund seeks to take advantage of investment opportunities generated by changes in international tradepatterns and economic and political relationships by investing in common stocks of companies located around the world. Inpursuing its primary investment objective, it invests primarily in common stocks that the investment adviser believes have thepotential for growth. In pursuing its secondary objective, the fund invests in common stocks of companies with the potential topay dividends in the future.

Fund Risk: Foreign securities are subject to interest-rate, currency-exchange-rate, economic, and political risks, all of whichmay be magnified in emerging markets. Stock markets are volatile and can decline significantly in response to adverse issuer,political, regulatory, market, economic or other developments. Additional risk information for this product may be found in theprospectus or other product materials, if available.

Fund short term trading fees: None

Who may want to invest:● Someone who is seeking an investment that invests in both domestic and international markets.

● Someone who is willing to accept the volatility of the markets and the generally higher degree of risk associated withinternational investments.

Footnotes:● This description is only intended to provide a brief overview of the mutual fund. Read the fund’s prospectus for more detailed

information about the fund.

● The analysis on these pages may be based, in part, on adjusted historical returns for periods prior to the class’s actualinception of 05/15/2002. These calculated returns reflect the historical performance of the oldest share class of the fund, withan inception date of 03/13/1973, adjusted to reflect the fees and expenses of this share class (when this share class’s fees andexpenses are higher.) Please refer to a fund’s prospectus for information regarding fees and expenses. These adjustedhistorical returns are not actual returns. Calculation methodologies utilized by Morningstar may differ from those applied byother entities, including the fund itself.

American Funds New World Fund® Class R-5

VRS Code: 046494

Fund Objective: The investment seeks long-term capital appreciation.

Fund Strategy: The fund invests primarily in common stocks of companies with significant exposure to countries withdeveloping economies and/or markets. Under normal market conditions, the fund will invest at least 35% of its assets in equityand debt securities of issuers primarily based in qualified countries that have developing economies and/or markets.

Fund Risk: Foreign securities are subject to interest-rate, currency-exchange-rate, economic, and political risks, all of whichmay be magnified in emerging markets. Stock markets are volatile and can decline significantly in response to adverse issuer,political, regulatory, market, economic or other developments. Additional risk information for this product may be found in theprospectus or other product materials, if available.

Fund short term trading fees: None

Who may want to invest:● Someone who is willing to accept the higher degree of risk associated with investing in emerging markets.

● Someone who is seeking to complement a portfolio of domestic investments and/or international investments in developedcountries with investments in developing countries, which can behave differently.

7

Inve

stm

ent

Op

tions

Footnotes:● This description is only intended to provide a brief overview of the mutual fund. Read the fund’s prospectus for more detailed

information about the fund.

● The analysis on these pages may be based, in part, on adjusted historical returns for periods prior to the class’s actualinception of 05/15/2002. These calculated returns reflect the historical performance of the oldest share class of the fund, withan inception date of 06/17/1999, adjusted to reflect the fees and expenses of this share class (when this share class’s fees andexpenses are higher.) Please refer to a fund’s prospectus for information regarding fees and expenses. These adjustedhistorical returns are not actual returns. Calculation methodologies utilized by Morningstar may differ from those applied byother entities, including the fund itself.

BlackRock High Yield Bond Portfolio Class K

VRS Code: 043673

Fund Objective: The investment seeks to maximize total return, consistent with income generation and prudent investmentmanagement.

Fund Strategy: The fund invests primarily in non-investment grade bonds with maturities of ten years or less. It normallyinvests at least 80% of its assets in high yield bonds. The fund may invest up to 30% of its assets in non-dollar denominatedbonds of issuers located outside of the United States. Its investment in non-dollar denominated bonds may be on a currencyhedged or unhedged basis. The fund may also invest in convertible and preferred securities.

Fund Risk: The fund may invest in lower-quality debt securities that involve greater risk of default or price changes due topotential changes in the credit quality of the issuer. In general the bond market is volatile, and fixed income securities carryinterest rate risk. (As interest rates rise, bond prices usually fall, and vice versa. This effect is usually more pronounced forlonger-term securities.) Fixed income securities also carry inflation risk and credit and default risks for both issuers andcounterparties. Unlike individual bonds, most bond funds do not have a maturity date, so avoiding losses caused by pricevolatility by holding them until maturity is not possible. Additional risk information for this product may be found in theprospectus or other product materials, if available.

Fund short term trading fees: None

Who may want to invest:● Someone interested in a bond fund that provides the potential for both current income and share-price appreciation.

● Someone who is seeking to complement his or her core bond holdings with a bond investment that seeks higher returns fromriskier bonds, and who can tolerate higher risk.

Footnotes:● This description is only intended to provide a brief overview of the mutual fund. Read the fund’s prospectus for more detailed

information about the fund.

Calvert Bond Fund Class I

VRS Code: 047214

Fund Objective: The investment seeks to provide as high a level of current income as is consistent with preservation of capitalthrough investment in bonds and other debt securities.

Fund Strategy: Under normal circumstances, the fund invests at least 80% of its net assets (including borrowings forinvestment purposes) in bonds. Bonds include debt securities of any maturity. At least 80% of the fund’s net assets are investedin investment grade debt securities. The fund may also invest up to 25% of its net assets in foreign debt securities.

Fund Risk: In general the bond market is volatile, and fixed income securities carry interest rate risk. (As interest rates rise,bond prices usually fall, and vice versa. This effect is usually more pronounced for longer-term securities.) Fixed incomesecurities also carry inflation risk and credit and default risks for both issuers and counterparties. Unlike individual bonds, mostbond funds do not have a maturity date, so avoiding losses caused by price volatility by holding them until maturity is notpossible. Additional risk information for this product may be found in the prospectus or other product materials, if available.

Fund short term trading fees: None

Who may want to invest:● Someone who is seeking potential returns primarily in the form of interest dividends rather than through an increase in share

price.

● Someone who is seeking to diversify an equity portfolio with a more conservative investment option.

8

Investment O

ptio

nsFo

r mo

re inform

ation visit w

ww

.netbenefits.co

m/une o

r call 1-800-343-0860

Footnotes:● This description is only intended to provide a brief overview of the mutual fund. Read the fund’s prospectus for more detailed

information about the fund.

● The analysis on these pages may be based, in part, on adjusted historical returns for periods prior to the class’s actualinception of 03/31/2000. These calculated returns reflect the historical performance of the oldest share class of the fund, withan inception date of 08/24/1987, adjusted to reflect the fees and expenses of this share class (when this share class’s fees andexpenses are higher.) Please refer to a fund’s prospectus for information regarding fees and expenses. These adjustedhistorical returns are not actual returns. Calculation methodologies utilized by Morningstar may differ from those applied byother entities, including the fund itself.

Calvert US Large Cap Core Responsible Index Fund Class I

VRS Code: 041086

Fund Objective: The investment seeks to track the performance of the Calvert U.S. Large-Cap Core Responsible Index, whichmeasures the investment return of large-capitalization stocks.

Fund Strategy: The fund normally invests at least 95% of its net assets, including borrowings for investment purposes, insecurities contained in the index. The index is composed of the common stocks of large companies that operate theirbusinesses in a manner consistent with the Calvert Principles for Responsible Investment.

Fund Risk: Value and growth stocks can perform differently from other types of stocks. Growth stocks can be more volatile.Value stocks can continue to be undervalued by the market for long periods of time. Stock markets are volatile and can declinesignificantly in response to adverse issuer, political, regulatory, market, economic or other developments. These risks may bemagnified in foreign markets. Additional risk information for this product may be found in the prospectus or other productmaterials, if available.

Fund short term trading fees: None

Who may want to invest:● Someone who is seeking the potential for long-term share-price appreciation and, secondarily, dividend income.

● Someone who is seeking both growth- and value-style investments and who is willing to accept the volatility associated withinvesting in the stock market.

Footnotes:● This description is only intended to provide a brief overview of the mutual fund. Read the fund’s prospectus for more detailed

information about the fund.

● The Calvert U.S. Large Cap Core Responsible Index is composed of companies that operate their businesses in a manner thatis consistent with Calvert’s responsible investment principles.

DFA U.S. Targeted Value Portfolio Institutional Class

VRS Code: 042267

Fund Objective: The investment seeks long-term capital appreciation.

Fund Strategy: The fund purchases a broad and diverse group of the readily marketable securities of U.S. small and mid capcompanies that the Advisor determines to be value stocks. It may purchase or sell futures contracts and options on futurescontracts for U.S. equity securities and indices, to adjust market exposure based on actual or expected cash inflows to oroutflows from the fund. The advisor does not intend to sell futures contracts to establish short positions in individual securitiesor to use derivatives for purposes of speculation or leveraging investment returns.

Fund Risk: The securities of smaller, less well-known companies can be more volatile than those of larger companies. Valuestocks can perform differently than other types of stocks and can continue to be undervalued by the market for long periods oftime. Stock markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market,economic or other developments. These risks may be magnified in foreign markets. Additional risk information for this productmay be found in the prospectus or other product materials, if available.

Fund short term trading fees: None

Who may want to invest:● Someone who is seeking the potential for long-term share-price appreciation and, secondarily, dividend income.

● Someone who is comfortable with value-style investments and the potentially greater volatility of investments in smallercompanies.

Footnotes:● This description is only intended to provide a brief overview of the mutual fund. Read the fund’s prospectus for more detailed

information about the fund.

● Additional Risk Information: Short positions pose a risk because they lose value as a security’s price increases; therefore, theloss on a short sale is theoretically unlimited.

9

Inve

stm

ent

Op

tions

Fidelity Freedom® 2005 Fund

VRS Code: 001312

Fund Objective: Seeks high total return until its target retirement date. Thereafter, the fund’s objective will be to seek highcurrent income and, as a secondary objective, capital appreciation.

Fund Strategy: Designed for investors who anticipate retiring in or within a few years of the fund’s target retirement year at oraround age 65. Investing in a combination of Fidelity domestic equity funds, international equity funds, bond funds, and short-term funds (underlying Fidelity funds). Allocating assets among underlying Fidelity funds according to a "neutral" assetallocation strategy that adjusts over time until it reaches an allocation similar to that of the Freedom Income Fundapproximately 10 to 19 years after the target year. Ultimately, the fund will merge with the Freedom Income Fund. FMR Co.,Inc. (the Adviser) may modify the fund’s neutral asset allocations from time to time when in the interests of investors. Buyingand selling futures contracts (both long and short positions) in an effort to manage cash flows efficiently, remain fully invested,or facilitate asset allocation. Through an active asset allocation strategy, the Adviser may increase or decrease neutral assetclass exposures by up to 10 percentage points for equity, bond and short-term funds to reflect the Adviser’s market outlook,which is primarily focused on the intermediate term.

Fund Risk: Investment performance of the Fidelity Freedom Fund products depends on the performance of the underlyinginvestment options and on the proportion of the assets invested in each underlying investment option. The investment risk ofeach Fidelity Freedom Fund changes over time as its asset allocation changes. These risks are subject to the asset allocationdecisions of the Investment Adviser. Pursuant to the Adviser’s ability to use an active asset allocation strategy, investors may besubject to a different risk profile compared to the fund’s neutral asset allocation strategy shown in its glide path. The funds aresubject to the volatility of the financial markets, including that of equity and fixed income investments in the U.S. and abroad,and may be subject to risks associated with investing in high-yield, small-cap, commodity-linked and foreign securities.Leverage can increase market exposure, magnify investment risks, and cause losses to be realized more quickly. No target datefund is considered a complete retirement program and there is no guarantee any single fund will provide sufficient retirementincome at or through retirement. Principal invested is not guaranteed at any time, including at or after the funds’ target dates.

Fund short term trading fees: None

Who may want to invest:● Someone who is seeking an investment option intended for people in or very near retirement and who is willing to accept the

volatility of diversified investments in the market.

● Someone who is seeking a diversified mix of stocks, bonds, and short-term investments in one investment option or whodoes not feel comfortable making asset allocation choices over time.

Footnotes:● This description is only intended to provide a brief overview of the mutual fund. Read the fund’s prospectus for more detailed

information about the fund.

Fidelity Freedom® 2010 Fund

VRS Code: 000371

Fund Objective: Seeks high total return until its target retirement date. Thereafter, the fund’s objective will be to seek highcurrent income and, as a secondary objective, capital appreciation.

Fund Strategy: Designed for investors who anticipate retiring in or within a few years of the fund’s target retirement year at oraround age 65. Investing in a combination of Fidelity domestic equity funds, international equity funds, bond funds, and short-term funds (underlying Fidelity funds). Allocating assets among underlying Fidelity funds according to a "neutral" assetallocation strategy that adjusts over time until it reaches an allocation similar to that of the Freedom Income Fundapproximately 10 to 19 years after the target year. Ultimately, the fund will merge with the Freedom Income Fund. FMR Co.,Inc. (the Adviser) may modify the fund’s neutral asset allocations from time to time when in the interests of investors. Buyingand selling futures contracts (both long and short positions) in an effort to manage cash flows efficiently, remain fully invested,or facilitate asset allocation. Through an active asset allocation strategy, the Adviser may increase or decrease neutral assetclass exposures by up to 10 percentage points for equity, bond and short-term funds to reflect the Adviser’s market outlook,which is primarily focused on the intermediate term.

10

Investment O

ptio

nsFo

r mo

re inform

ation visit w

ww

.netbenefits.co

m/une o

r call 1-800-343-0860

Fund Risk: Investment performance of the Fidelity Freedom Fund products depends on the performance of the underlyinginvestment options and on the proportion of the assets invested in each underlying investment option. The investment risk ofeach Fidelity Freedom Fund changes over time as its asset allocation changes. These risks are subject to the asset allocationdecisions of the Investment Adviser. Pursuant to the Adviser’s ability to use an active asset allocation strategy, investors may besubject to a different risk profile compared to the fund’s neutral asset allocation strategy shown in its glide path. The funds aresubject to the volatility of the financial markets, including that of equity and fixed income investments in the U.S. and abroad,and may be subject to risks associated with investing in high-yield, small-cap, commodity-linked and foreign securities.Leverage can increase market exposure, magnify investment risks, and cause losses to be realized more quickly. No target datefund is considered a complete retirement program and there is no guarantee any single fund will provide sufficient retirementincome at or through retirement. Principal invested is not guaranteed at any time, including at or after the funds’ target dates.

Fund short term trading fees: None

Who may want to invest:● Someone who is seeking an investment option intended for people in or very near retirement and who is willing to accept the

volatility of diversified investments in the market.

● Someone who is seeking a diversified mix of stocks, bonds, and short-term investments in one investment option or whodoes not feel comfortable making asset allocation choices over time.

Footnotes:● This description is only intended to provide a brief overview of the mutual fund. Read the fund’s prospectus for more detailed

information about the fund.

Fidelity Freedom® 2015 Fund

VRS Code: 001313

Fund Objective: Seeks high total return until its target retirement date. Thereafter, the fund’s objective will be to seek highcurrent income and, as a secondary objective, capital appreciation.

Fund Strategy: Designed for investors who anticipate retiring in or within a few years of the fund’s target retirement year at oraround age 65. Investing in a combination of Fidelity domestic equity funds, international equity funds, bond funds, and short-term funds (underlying Fidelity funds). Allocating assets among underlying Fidelity funds according to a "neutral" assetallocation strategy that adjusts over time until it reaches an allocation similar to that of the Freedom Income Fundapproximately 10 to 19 years after the target year. Ultimately, the fund will merge with the Freedom Income Fund. FMR Co.,Inc. (the Adviser) may modify the fund’s neutral asset allocations from time to time when in the interests of investors. Buyingand selling futures contracts (both long and short positions) in an effort to manage cash flows efficiently, remain fully invested,or facilitate asset allocation. Through an active asset allocation strategy, the Adviser may increase or decrease neutral assetclass exposures by up to 10 percentage points for equity, bond and short-term funds to reflect the Adviser’s market outlook,which is primarily focused on the intermediate term.

Fund Risk: Investment performance of the Fidelity Freedom Fund products depends on the performance of the underlyinginvestment options and on the proportion of the assets invested in each underlying investment option. The investment risk ofeach Fidelity Freedom Fund changes over time as its asset allocation changes. These risks are subject to the asset allocationdecisions of the Investment Adviser. Pursuant to the Adviser’s ability to use an active asset allocation strategy, investors may besubject to a different risk profile compared to the fund’s neutral asset allocation strategy shown in its glide path. The funds aresubject to the volatility of the financial markets, including that of equity and fixed income investments in the U.S. and abroad,and may be subject to risks associated with investing in high-yield, small-cap, commodity-linked and foreign securities.Leverage can increase market exposure, magnify investment risks, and cause losses to be realized more quickly. No target datefund is considered a complete retirement program and there is no guarantee any single fund will provide sufficient retirementincome at or through retirement. Principal invested is not guaranteed at any time, including at or after the funds’ target dates.

Fund short term trading fees: None

Who may want to invest:● Someone who is seeking an investment option intended for people in or very near retirement and who is willing to accept the

volatility of diversified investments in the market.

● Someone who is seeking a diversified mix of stocks, bonds, and short-term investments in one investment option or whodoes not feel comfortable making asset allocation choices over time.

Footnotes:● This description is only intended to provide a brief overview of the mutual fund. Read the fund’s prospectus for more detailed

information about the fund.

11

Inve

stm

ent

Op

tions

Fidelity Freedom® 2020 Fund

VRS Code: 000372

Fund Objective: Seeks high total return until its target retirement date. Thereafter, the fund’s objective will be to seek highcurrent income and, as a secondary objective, capital appreciation.

Fund Strategy: Designed for investors who anticipate retiring in or within a few years of the fund’s target retirement year at oraround age 65. Investing in a combination of Fidelity domestic equity funds, international equity funds, bond funds, and short-term funds (underlying Fidelity funds). Allocating assets among underlying Fidelity funds according to a "neutral" assetallocation strategy that adjusts over time until it reaches an allocation similar to that of the Freedom Income Fundapproximately 10 to 19 years after the target year. Ultimately, the fund will merge with the Freedom Income Fund. FMR Co.,Inc. (the Adviser) may modify the fund’s neutral asset allocations from time to time when in the interests of investors. Buyingand selling futures contracts (both long and short positions) in an effort to manage cash flows efficiently, remain fully invested,or facilitate asset allocation. Through an active asset allocation strategy, the Adviser may increase or decrease neutral assetclass exposures by up to 10 percentage points for equity, bond and short-term funds to reflect the Adviser’s market outlook,which is primarily focused on the intermediate term.

Fund Risk: Investment performance of the Fidelity Freedom Fund products depends on the performance of the underlyinginvestment options and on the proportion of the assets invested in each underlying investment option. The investment risk ofeach Fidelity Freedom Fund changes over time as its asset allocation changes. These risks are subject to the asset allocationdecisions of the Investment Adviser. Pursuant to the Adviser’s ability to use an active asset allocation strategy, investors may besubject to a different risk profile compared to the fund’s neutral asset allocation strategy shown in its glide path. The funds aresubject to the volatility of the financial markets, including that of equity and fixed income investments in the U.S. and abroad,and may be subject to risks associated with investing in high-yield, small-cap, commodity-linked and foreign securities.Leverage can increase market exposure, magnify investment risks, and cause losses to be realized more quickly. No target datefund is considered a complete retirement program and there is no guarantee any single fund will provide sufficient retirementincome at or through retirement. Principal invested is not guaranteed at any time, including at or after the funds’ target dates.

Fund short term trading fees: None

Who may want to invest:● Someone who is seeking an investment option that gradually becomes more conservative over time and who is willing to

accept the volatility of the markets.

● Someone who is seeking a diversified mix of stocks, bonds, and short-term investments in one investment option or whodoes not feel comfortable making asset allocation choices over time.

Footnotes:● This description is only intended to provide a brief overview of the mutual fund. Read the fund’s prospectus for more detailed

information about the fund.

Fidelity Freedom® 2025 Fund

VRS Code: 001314

Fund Objective: Seeks high total return until its target retirement date. Thereafter, the fund’s objective will be to seek highcurrent income and, as a secondary objective, capital appreciation.

Fund Strategy: Designed for investors who anticipate retiring in or within a few years of the fund’s target retirement year at oraround age 65. Investing in a combination of Fidelity domestic equity funds, international equity funds, bond funds, and short-term funds (underlying Fidelity funds). Allocating assets among underlying Fidelity funds according to a "neutral" assetallocation strategy that adjusts over time until it reaches an allocation similar to that of the Freedom Income Fundapproximately 10 to 19 years after the target year. Ultimately, the fund will merge with the Freedom Income Fund. FMR Co.,Inc. (the Adviser) may modify the fund’s neutral asset allocations from time to time when in the interests of investors. Buyingand selling futures contracts (both long and short positions) in an effort to manage cash flows efficiently, remain fully invested,or facilitate asset allocation. Through an active asset allocation strategy, the Adviser may increase or decrease neutral assetclass exposures by up to 10 percentage points for equity, bond and short-term funds to reflect the Adviser’s market outlook,which is primarily focused on the intermediate term.

12

Investment O

ptio

nsFo

r mo

re inform

ation visit w

ww

.netbenefits.co

m/une o

r call 1-800-343-0860

Fund Risk: Investment performance of the Fidelity Freedom Fund products depends on the performance of the underlyinginvestment options and on the proportion of the assets invested in each underlying investment option. The investment risk ofeach Fidelity Freedom Fund changes over time as its asset allocation changes. These risks are subject to the asset allocationdecisions of the Investment Adviser. Pursuant to the Adviser’s ability to use an active asset allocation strategy, investors may besubject to a different risk profile compared to the fund’s neutral asset allocation strategy shown in its glide path. The funds aresubject to the volatility of the financial markets, including that of equity and fixed income investments in the U.S. and abroad,and may be subject to risks associated with investing in high-yield, small-cap, commodity-linked and foreign securities.Leverage can increase market exposure, magnify investment risks, and cause losses to be realized more quickly. No target datefund is considered a complete retirement program and there is no guarantee any single fund will provide sufficient retirementincome at or through retirement. Principal invested is not guaranteed at any time, including at or after the funds’ target dates.

Fund short term trading fees: None

Who may want to invest:● Someone who is seeking an investment option that gradually becomes more conservative over time and who is willing to

accept the volatility of the markets.

● Someone who is seeking a diversified mix of stocks, bonds, and short-term investments in one investment option or whodoes not feel comfortable making asset allocation choices over time.

Footnotes:● This description is only intended to provide a brief overview of the mutual fund. Read the fund’s prospectus for more detailed

information about the fund.

Fidelity Freedom® 2030 Fund

VRS Code: 000373

Fund Objective: Seeks high total return until its target retirement date. Thereafter, the fund’s objective will be to seek highcurrent income and, as a secondary objective, capital appreciation.

Fund Strategy: Designed for investors who anticipate retiring in or within a few years of the fund’s target retirement year at oraround age 65. Investing in a combination of Fidelity domestic equity funds, international equity funds, bond funds, and short-term funds (underlying Fidelity funds). Allocating assets among underlying Fidelity funds according to a "neutral" assetallocation strategy that adjusts over time until it reaches an allocation similar to that of the Freedom Income Fundapproximately 10 to 19 years after the target year. Ultimately, the fund will merge with the Freedom Income Fund. FMR Co.,Inc. (the Adviser) may modify the fund’s neutral asset allocations from time to time when in the interests of investors. Buyingand selling futures contracts (both long and short positions) in an effort to manage cash flows efficiently, remain fully invested,or facilitate asset allocation. Through an active asset allocation strategy, the Adviser may increase or decrease neutral assetclass exposures by up to 10 percentage points for equity, bond and short-term funds to reflect the Adviser’s market outlook,which is primarily focused on the intermediate term.

Fund Risk: Investment performance of the Fidelity Freedom Fund products depends on the performance of the underlyinginvestment options and on the proportion of the assets invested in each underlying investment option. The investment risk ofeach Fidelity Freedom Fund changes over time as its asset allocation changes. These risks are subject to the asset allocationdecisions of the Investment Adviser. Pursuant to the Adviser’s ability to use an active asset allocation strategy, investors may besubject to a different risk profile compared to the fund’s neutral asset allocation strategy shown in its glide path. The funds aresubject to the volatility of the financial markets, including that of equity and fixed income investments in the U.S. and abroad,and may be subject to risks associated with investing in high-yield, small-cap, commodity-linked and foreign securities.Leverage can increase market exposure, magnify investment risks, and cause losses to be realized more quickly. No target datefund is considered a complete retirement program and there is no guarantee any single fund will provide sufficient retirementincome at or through retirement. Principal invested is not guaranteed at any time, including at or after the funds’ target dates.

Fund short term trading fees: None

Who may want to invest:● Someone who is seeking an investment option that gradually becomes more conservative over time and who is willing to

accept the volatility of the markets.

● Someone who is seeking a diversified mix of stocks, bonds, and short-term investments in one investment option or whodoes not feel comfortable making asset allocation choices over time.

Footnotes:● This description is only intended to provide a brief overview of the mutual fund. Read the fund’s prospectus for more detailed

information about the fund.

13

Inve

stm

ent

Op

tions

Fidelity Freedom® 2035 Fund

VRS Code: 001315

Fund Objective: Seeks high total return until its target retirement date. Thereafter, the fund’s objective will be to seek highcurrent income and, as a secondary objective, capital appreciation.

Fund Strategy: Designed for investors who anticipate retiring in or within a few years of the fund’s target retirement year at oraround age 65. Investing in a combination of Fidelity domestic equity funds, international equity funds, bond funds, and short-term funds (underlying Fidelity funds). Allocating assets among underlying Fidelity funds according to a "neutral" assetallocation strategy that adjusts over time until it reaches an allocation similar to that of the Freedom Income Fundapproximately 10 to 19 years after the target year. Ultimately, the fund will merge with the Freedom Income Fund. FMR Co.,Inc. (the Adviser) may modify the fund’s neutral asset allocations from time to time when in the interests of investors. Buyingand selling futures contracts (both long and short positions) in an effort to manage cash flows efficiently, remain fully invested,or facilitate asset allocation. Through an active asset allocation strategy, the Adviser may increase or decrease neutral assetclass exposures by up to 10 percentage points for equity, bond and short-term funds to reflect the Adviser’s market outlook,which is primarily focused on the intermediate term.

Fund Risk: Investment performance of the Fidelity Freedom Fund products depends on the performance of the underlyinginvestment options and on the proportion of the assets invested in each underlying investment option. The investment risk ofeach Fidelity Freedom Fund changes over time as its asset allocation changes. These risks are subject to the asset allocationdecisions of the Investment Adviser. Pursuant to the Adviser’s ability to use an active asset allocation strategy, investors may besubject to a different risk profile compared to the fund’s neutral asset allocation strategy shown in its glide path. The funds aresubject to the volatility of the financial markets, including that of equity and fixed income investments in the U.S. and abroad,and may be subject to risks associated with investing in high-yield, small-cap, commodity-linked and foreign securities.Leverage can increase market exposure, magnify investment risks, and cause losses to be realized more quickly. No target datefund is considered a complete retirement program and there is no guarantee any single fund will provide sufficient retirementincome at or through retirement. Principal invested is not guaranteed at any time, including at or after the funds’ target dates.

Fund short term trading fees: None

Who may want to invest:● Someone who is seeking an investment option that gradually becomes more conservative over time and who is willing to

accept the volatility of the markets.

● Someone who is seeking a diversified mix of stocks, bonds, and short-term investments in one investment option or whodoes not feel comfortable making asset allocation choices over time.

Footnotes:● This description is only intended to provide a brief overview of the mutual fund. Read the fund’s prospectus for more detailed

information about the fund.

Fidelity Freedom® 2040 Fund

VRS Code: 000718

Fund Objective: Seeks high total return until its target retirement date. Thereafter, the fund’s objective will be to seek highcurrent income and, as a secondary objective, capital appreciation.

Fund Strategy: Designed for investors who anticipate retiring in or within a few years of the fund’s target retirement year at oraround age 65. Investing in a combination of Fidelity domestic equity funds, international equity funds, bond funds, and short-term funds (underlying Fidelity funds). Allocating assets among underlying Fidelity funds according to a "neutral" assetallocation strategy that adjusts over time until it reaches an allocation similar to that of the Freedom Income Fundapproximately 10 to 19 years after the target year. Ultimately, the fund will merge with the Freedom Income Fund. FMR Co.,Inc. (the Adviser) may modify the fund’s neutral asset allocations from time to time when in the interests of investors. Buyingand selling futures contracts (both long and short positions) in an effort to manage cash flows efficiently, remain fully invested,or facilitate asset allocation. Through an active asset allocation strategy, the Adviser may increase or decrease neutral assetclass exposures by up to 10 percentage points for equity, bond and short-term funds to reflect the Adviser’s market outlook,which is primarily focused on the intermediate term.

14

Investment O

ptio

nsFo

r mo

re inform

ation visit w

ww

.netbenefits.co

m/une o

r call 1-800-343-0860

Fund Risk: Investment performance of the Fidelity Freedom Fund products depends on the performance of the underlyinginvestment options and on the proportion of the assets invested in each underlying investment option. The investment risk ofeach Fidelity Freedom Fund changes over time as its asset allocation changes. These risks are subject to the asset allocationdecisions of the Investment Adviser. Pursuant to the Adviser’s ability to use an active asset allocation strategy, investors may besubject to a different risk profile compared to the fund’s neutral asset allocation strategy shown in its glide path. The funds aresubject to the volatility of the financial markets, including that of equity and fixed income investments in the U.S. and abroad,and may be subject to risks associated with investing in high-yield, small-cap, commodity-linked and foreign securities.Leverage can increase market exposure, magnify investment risks, and cause losses to be realized more quickly. No target datefund is considered a complete retirement program and there is no guarantee any single fund will provide sufficient retirementincome at or through retirement. Principal invested is not guaranteed at any time, including at or after the funds’ target dates.

Fund short term trading fees: None

Who may want to invest:● Someone who is seeking an investment option that gradually becomes more conservative over time and who is willing to

accept the volatility of the markets.

● Someone who is seeking a diversified mix of stocks, bonds, and short-term investments in one investment option or whodoes not feel comfortable making asset allocation choices over time.

Footnotes:● This description is only intended to provide a brief overview of the mutual fund. Read the fund’s prospectus for more detailed

information about the fund.

Fidelity Freedom® 2045 Fund

VRS Code: 001617

Fund Objective: Seeks high total return until its target retirement date. Thereafter, the fund’s objective will be to seek highcurrent income and, as a secondary objective, capital appreciation.

Fund Strategy: Designed for investors who anticipate retiring in or within a few years of the fund’s target retirement year at oraround age 65. Investing in a combination of Fidelity domestic equity funds, international equity funds, bond funds, and short-term funds (underlying Fidelity funds). Allocating assets among underlying Fidelity funds according to a "neutral" assetallocation strategy that adjusts over time until it reaches an allocation similar to that of the Freedom Income Fundapproximately 10 to 19 years after the target year. Ultimately, the fund will merge with the Freedom Income Fund. FMR Co.,Inc. (the Adviser) may modify the fund’s neutral asset allocations from time to time when in the interests of investors. Buyingand selling futures contracts (both long and short positions) in an effort to manage cash flows efficiently, remain fully invested,or facilitate asset allocation. Through an active asset allocation strategy, the Adviser may increase or decrease neutral assetclass exposures by up to 10 percentage points for equity, bond and short-term funds to reflect the Adviser’s market outlook,which is primarily focused on the intermediate term.

Fund Risk: Investment performance of the Fidelity Freedom Fund products depends on the performance of the underlyinginvestment options and on the proportion of the assets invested in each underlying investment option. The investment risk ofeach Fidelity Freedom Fund changes over time as its asset allocation changes. These risks are subject to the asset allocationdecisions of the Investment Adviser. Pursuant to the Adviser’s ability to use an active asset allocation strategy, investors may besubject to a different risk profile compared to the fund’s neutral asset allocation strategy shown in its glide path. The funds aresubject to the volatility of the financial markets, including that of equity and fixed income investments in the U.S. and abroad,and may be subject to risks associated with investing in high-yield, small-cap, commodity-linked and foreign securities.Leverage can increase market exposure, magnify investment risks, and cause losses to be realized more quickly. No target datefund is considered a complete retirement program and there is no guarantee any single fund will provide sufficient retirementincome at or through retirement. Principal invested is not guaranteed at any time, including at or after the funds’ target dates.

Fund short term trading fees: None

Who may want to invest:● Someone who is seeking an investment option that gradually becomes more conservative over time and who is willing to

accept the volatility of the markets.

● Someone who is seeking a diversified mix of stocks, bonds, and short-term investments in one investment option or whodoes not feel comfortable making asset allocation choices over time.

Footnotes:● This description is only intended to provide a brief overview of the mutual fund. Read the fund’s prospectus for more detailed

information about the fund.

15

Inve

stm

ent

Op

tions

Fidelity Freedom® 2050 Fund

VRS Code: 001618

Fund Objective: Seeks high total return until its target retirement date. Thereafter, the fund’s objective will be to seek highcurrent income and, as a secondary objective, capital appreciation.

Fund Strategy: Designed for investors who anticipate retiring in or within a few years of the fund’s target retirement year at oraround age 65. Investing in a combination of Fidelity domestic equity funds, international equity funds, bond funds, and short-term funds (underlying Fidelity funds). Allocating assets among underlying Fidelity funds according to a "neutral" assetallocation strategy that adjusts over time until it reaches an allocation similar to that of the Freedom Income Fundapproximately 10 to 19 years after the target year. Ultimately, the fund will merge with the Freedom Income Fund. FMR Co.,Inc. (the Adviser) may modify the fund’s neutral asset allocations from time to time when in the interests of investors. Buyingand selling futures contracts (both long and short positions) in an effort to manage cash flows efficiently, remain fully invested,or facilitate asset allocation. Through an active asset allocation strategy, the Adviser may increase or decrease neutral assetclass exposures by up to 10 percentage points for equity, bond and short-term funds to reflect the Adviser’s market outlook,which is primarily focused on the intermediate term.

Fund Risk: Investment performance of the Fidelity Freedom Fund products depends on the performance of the underlyinginvestment options and on the proportion of the assets invested in each underlying investment option. The investment risk ofeach Fidelity Freedom Fund changes over time as its asset allocation changes. These risks are subject to the asset allocationdecisions of the Investment Adviser. Pursuant to the Adviser’s ability to use an active asset allocation strategy, investors may besubject to a different risk profile compared to the fund’s neutral asset allocation strategy shown in its glide path. The funds aresubject to the volatility of the financial markets, including that of equity and fixed income investments in the U.S. and abroad,and may be subject to risks associated with investing in high-yield, small-cap, commodity-linked and foreign securities.Leverage can increase market exposure, magnify investment risks, and cause losses to be realized more quickly. No target datefund is considered a complete retirement program and there is no guarantee any single fund will provide sufficient retirementincome at or through retirement. Principal invested is not guaranteed at any time, including at or after the funds’ target dates.

Fund short term trading fees: None

Who may want to invest:● Someone who is seeking an investment option that gradually becomes more conservative over time and who is willing to

accept the volatility of the markets.

● Someone who is seeking a diversified mix of stocks, bonds, and short-term investments in one investment option or whodoes not feel comfortable making asset allocation choices over time.

Footnotes:● This description is only intended to provide a brief overview of the mutual fund. Read the fund’s prospectus for more detailed

information about the fund.

Fidelity Freedom® 2055 Fund

VRS Code: 002331

Fund Objective: Seeks high total return until its target retirement date. Thereafter, the fund’s objective will be to seek highcurrent income and, as a secondary objective, capital appreciation.

Fund Strategy: Designed for investors who anticipate retiring in or within a few years of the fund’s target retirement year at oraround age 65. Investing in a combination of Fidelity domestic equity funds, international equity funds, bond funds, and short-term funds (underlying Fidelity funds). Allocating assets among underlying Fidelity funds according to a "neutral" assetallocation strategy that adjusts over time until it reaches an allocation similar to that of the Freedom Income Fundapproximately 10 to 19 years after the target year. Ultimately, the fund will merge with the Freedom Income Fund. FMR Co.,Inc. (the Adviser) may modify the fund’s neutral asset allocations from time to time when in the interests of investors. Buyingand selling futures contracts (both long and short positions) in an effort to manage cash flows efficiently, remain fully invested,or facilitate asset allocation. Through an active asset allocation strategy, the Adviser may increase or decrease neutral assetclass exposures by up to 10 percentage points for equity, bond and short-term funds to reflect the Adviser’s market outlook,which is primarily focused on the intermediate term.

16

Investment O

ptio

nsFo

r mo

re inform

ation visit w

ww

.netbenefits.co

m/une o

r call 1-800-343-0860

Fund Risk: Investment performance of the Fidelity Freedom Fund products depends on the performance of the underlyinginvestment options and on the proportion of the assets invested in each underlying investment option. The investment risk ofeach Fidelity Freedom Fund changes over time as its asset allocation changes. These risks are subject to the asset allocationdecisions of the Investment Adviser. Pursuant to the Adviser’s ability to use an active asset allocation strategy, investors may besubject to a different risk profile compared to the fund’s neutral asset allocation strategy shown in its glide path. The funds aresubject to the volatility of the financial markets, including that of equity and fixed income investments in the U.S. and abroad,and may be subject to risks associated with investing in high-yield, small-cap, commodity-linked and foreign securities.Leverage can increase market exposure, magnify investment risks, and cause losses to be realized more quickly. No target datefund is considered a complete retirement program and there is no guarantee any single fund will provide sufficient retirementincome at or through retirement. Principal invested is not guaranteed at any time, including at or after the funds’ target dates.

Fund short term trading fees: None

Who may want to invest:● Someone who is seeking an investment option that gradually becomes more conservative over time and who is willing to

accept the volatility of the markets.

● Someone who is seeking a diversified mix of stocks, bonds, and short-term investments in one investment option or whodoes not feel comfortable making asset allocation choices over time.

Footnotes:● This description is only intended to provide a brief overview of the mutual fund. Read the fund’s prospectus for more detailed

information about the fund.

Fidelity Freedom® 2060 Fund

VRS Code: 002708

Fund Objective: Seeks high total return until its target retirement date. Thereafter, the fund’s objective will be to seek highcurrent income and, as a secondary objective, capital appreciation.

Fund Strategy: Designed for investors who anticipate retiring in or within a few years of the fund’s target retirement year at oraround age 65. Investing in a combination of Fidelity domestic equity funds, international equity funds, bond funds, and short-term funds (underlying Fidelity funds). Allocating assets among underlying Fidelity funds according to a "neutral" assetallocation strategy that adjusts over time until it reaches an allocation similar to that of the Freedom Income Fundapproximately 10 to 19 years after the target year. Ultimately, the fund will merge with the Freedom Income Fund. FMR Co.,Inc. (the Adviser) may modify the fund’s neutral asset allocations from time to time when in the interests of investors. Buyingand selling futures contracts (both long and short positions) in an effort to manage cash flows efficiently, remain fully invested,or facilitate asset allocation. Through an active asset allocation strategy, the Adviser may increase or decrease neutral assetclass exposures by up to 10 percentage points for equity, bond and short-term funds to reflect the Adviser’s market outlook,which is primarily focused on the intermediate term.

Fund Risk: Investment performance of the Fidelity Freedom Fund products depends on the performance of the underlyinginvestment options and on the proportion of the assets invested in each underlying investment option. The investment risk ofeach Fidelity Freedom Fund changes over time as its asset allocation changes. These risks are subject to the asset allocationdecisions of the Investment Adviser. Pursuant to the Adviser’s ability to use an active asset allocation strategy, investors may besubject to a different risk profile compared to the fund’s neutral asset allocation strategy shown in its glide path. The funds aresubject to the volatility of the financial markets, including that of equity and fixed income investments in the U.S. and abroad,and may be subject to risks associated with investing in high-yield, small-cap, commodity-linked and foreign securities.Leverage can increase market exposure, magnify investment risks, and cause losses to be realized more quickly. No target datefund is considered a complete retirement program and there is no guarantee any single fund will provide sufficient retirementincome at or through retirement. Principal invested is not guaranteed at any time, including at or after the funds’ target dates.

Fund short term trading fees: None

Who may want to invest:● Someone who is seeking an investment option that gradually becomes more conservative over time and who is willing to

accept the volatility of the markets.

● Someone who is seeking a diversified mix of stocks, bonds, and short-term investments in one investment option or whodoes not feel comfortable making asset allocation choices over time.

Footnotes:● This description is only intended to provide a brief overview of the mutual fund. Read the fund’s prospectus for more detailed

information about the fund.

17

Inve

stm

ent

Op

tions

Fidelity Freedom® Income Fund

VRS Code: 000369

Fund Objective: Seeks high total current income and, as a secondary objective, capital appreciation.

Fund Strategy: Investing in a combination of Fidelity domestic equity funds, international equity funds, bond funds, and short-term funds (underlying Fidelity funds). Allocating assets among underlying Fidelity funds according to a stable "neutral" assetallocation strategy. FMR Co., Inc. (the Adviser) may modify the fund’s neutral asset allocations from time to time when in theinterests of shareholders. Buying and selling futures contracts (both long and short positions) in an effort to manage cash flowsefficiently, remain fully invested, or facilitate asset allocation. Through an active asset allocation strategy, the Adviser mayincrease or decrease neutral asset class exposures by up to 10 percentage points for equity, bond and short-term funds toreflect the Adviser’s market outlook, which is primarily focused on the intermediate term.

Fund Risk: The fund is subject to risks resulting from the asset allocation decisions of the Investment Adviser. Pursuant to theAdviser’s ability to use an active asset allocation strategy, investors may be subject to a different risk profile compared to thefund’s neutral asset allocation strategy shown in its glide path. The fund is subject to the volatility of the financial markets,including that of equity and fixed income investments. Fixed income investments entail issuer default and credit risk, inflationrisk, and interest rate risk (as interest rates rise, bond prices usually fall and vice versa). This effect is usually more pronouncedfor longer-term securities. Leverage can increase market exposure, magnify investment risks, and cause losses to be realizedmore quickly. No target date fund is considered a complete retirement program and there is no guarantee any single fund willprovide sufficient retirement income at or through retirement. Principal invested is not guaranteed at any time, including at orafter the funds’ target dates.

Fund short term trading fees: None

Who may want to invest:● Someone who is seeking an investment option intended for people in retirement and who is willing to accept the volatility of

diversified investments in the market.

● Someone who is seeking a diversified mix of stocks, bonds, and short-term investments in one investment option and lookingprimarily for the potential for income and, secondarily, for share-price appreciation.

Footnotes:● This description is only intended to provide a brief overview of the mutual fund. Read the fund’s prospectus for more detailed

information about the fund.

Fidelity® Contrafund®

VRS Code: 000022

Fund Objective: Seeks capital appreciation.

Fund Strategy: Investing in securities of companies whose value FMR believes is not fully recognized by the public. Investingin either ’growth’ stocks or ’value’ stocks or both. Normally investing primarily in common stocks.

Fund Risk: The value of the fund’s domestic and foreign investments will vary from day to day in response to many factors.Stock values fluctuate in response to the activities of individual companies, and general market and economic conditions.Investments in foreign securities involve greater risk than U.S. investments. You may have a gain or loss when you sell yourshares.

Fund short term trading fees: None

Who may want to invest:● Someone who is seeking the potential for long-term share-price appreciation.

● Someone who is willing to accept the generally greater price volatility associated with growth-oriented stocks.

Footnotes:● This description is only intended to provide a brief overview of the mutual fund. Read the fund’s prospectus for more detailed

information about the fund.

Fidelity® Diversified International Fund

VRS Code: 000325

Fund Objective: Seeks capital growth.

Fund Strategy: Normally investing primarily in non-U.S. securities. Normally investing primarily in common stocks.

18

Investment O

ptio

nsFo

r mo

re inform

ation visit w

ww

.netbenefits.co

m/une o

r call 1-800-343-0860

Fund Risk: Stock markets, especially foreign markets, are volatile and can decline significantly in response to adverse issuer,political, regulatory, market, or economic developments. Foreign securities are subject to interest rate, currency exchange rate,economic, and political risks, all of which are magnified in emerging markets.

Fund short term trading fees: None

Who may want to invest:● Someone who is seeking to complement a portfolio of domestic investments with international investments, which can

behave differently.

● Someone who is willing to accept the higher degree of risk associated with investing overseas.

Footnotes:● This description is only intended to provide a brief overview of the mutual fund. Read the fund’s prospectus for more detailed

information about the fund.

Fidelity® Government Money Market Fund

VRS Code: 000458

Fund Objective: Seeks as high a level of current income as is consistent with preservation of capital and liquidity.

Fund Strategy: The Adviser normally invests at least 99.5% of the fund’s total assets in cash, U.S. Government securities and/orrepurchase agreements that are collateralized fully (i.e., collateralized by cash or government securities). Certain issuers of U.S.Government securities are sponsored or chartered by Congress but their securities are neither issued nor guaranteed by theU.S. Treasury. Investing in compliance with industry-standard regulatory requirements for money market funds for the quality,maturity, liquidity and diversification of investments. The Adviser stresses maintaining a stable $1.00 share price, liquidity, andincome. In addition the Adviser normally invests at least 80% of the fund’s assets in U.S. Government securities and repurchaseagreements for those securities.

Fund Risk: You could lose money by investing in the fund. Although the fund seeks to preserve the value of your investment at$1.00 per share, it cannot guarantee it will do so. An investment in the fund is not insured or guaranteed by the FederalDeposit Insurance Corporation or any other government agency. Fidelity Investments and its affiliates, the fund’s sponsor, haveno legal obligation to provide financial support to the fund, and you should not expect that the sponsor will provide financialsupport to the fund at any time. The fund will not impose a fee upon the sale of your shares, nor temporarily suspend yourability to sell shares if the fund’s weekly liquid assets fall below 30% of its total assets because of market conditions or otherfactors. Interest rate increases can cause the price of a money market security to decrease. A decline in the credit quality of anissuer or a provider of credit support or a maturity-shortening structure for a security can cause the price of a money marketsecurity to decrease.

Fund short term trading fees: None

Who may want to invest:● Someone who has a low tolerance for investment risk and who wishes to keep the value of his or her investment relatively

stable.

● Someone who is seeking to complement his or her bond and stock fund holdings in order to reach a particular assetallocation.

Footnotes:● This description is only intended to provide a brief overview of the mutual fund. Read the fund’s prospectus for more detailed

information about the fund.

● Fidelity is voluntarily reimbursing a portion of the fund’s expenses. If Fidelity had not, the returns would have been lower.

Fidelity® Mid-Cap Stock Fund

VRS Code: 000337

Fund Objective: Seeks long-term growth of capital.

Fund Strategy: Normally investing at least 80% of assets in common stocks of companies with medium market capitalizations(companies with market capitalization similar to companies in the Russell Midcap Index or the S&P MidCap 400). Investing ineither "growth" stocks or "value" stocks or both. Potentially investing in companies with smaller or larger market capitalization.

19

Inve

stm

ent

Op

tions

Fund Risk: Stock markets, especially foreign markets, are volatile and can decline significantly in response to adverse issuer,political, regulatory, market, or economic developments. The securities of smaller, less well-known companies can be morevolatile than those of larger companies. Foreign securities are subject to interest rate, currency exchange rate, economic, andpolitical risks

Fund short term trading fees: None

Who may want to invest:● Someone who is seeking the potential for long-term share-price appreciation.

● Someone who is willing to accept the generally greater price volatility associated both with growth-oriented stocks and withsmaller companies.

Footnotes:● This description is only intended to provide a brief overview of the mutual fund. Read the fund’s prospectus for more detailed

information about the fund.

● The Russell Midcap® Index is an unmanaged market capitalization-weighted index of 800 medium-capitalization stocks. Thestocks are also members of the Russell 1000® index.

● The S&P® MidCap 400 Index is an unmanaged market capitalization-weighted index of 400 medium-capitalization stocks.

Fidelity® Real Estate Investment Portfolio

VRS Code: 000303

Fund Objective: Seeks above-average income and long-term capital growth, consistent with reasonable investment risk. Thefund seeks to provide a yield that exceeds the composite yield of the S&P 500 Index.