Embed Size (px)

Citation preview

MANAGERIAL A N D DFCISION ECONOMICS, VOL. 8. 333-338 (1987)

X-inefficiency and Market Power ~~ ~

R. K. ASHTON Lecturer, Industrial Economics, University of Nottingham, University Park, Nottingham, UK

This paper argues that dominant firms (those firms which, according to the theory, can tolerate inefficiency) face a number of external and internal constraints which force them to act more like the competitive firm assumed in neoclassical theory.

INTRODUCTION

Lei benstein ( 1 966,1975, I976,1983a, b) has argued that firms with market power are x-inefficient and do not operate on the boundary of their production function. The reason for this deparature is that ineffi- cient use is made of the various categories of labour in the production process. These inefficiencies enable the various layers of the managerial hierarchy to enjoy a quiet life’ and can only be tolerated because the firm earns above-normal profits. It follows that when the profit constraint becomes binding (as a result of competitive forces) any violation of the cost conditions imposed by neoclassical theory would jeopardize the firm’s long-run viability and possibly even its short-run viability. X-inefficiency is therefore a direct function of market power.

Since the concept was first formulated it has been considerably extended (see. for instance, Leibenstein, 1976, 1983). The extension has centred around two notions--an ‘effort index’ and an ‘inert’ area. The former determines the level of effort a person will supply and depends on a number of factors. These include what a person learns about the way a job has been done in the past or is being done, signs of approval or disapproval by peers and his perception of the observed effort norm. This norm will almost certainly be less than optimal and in terms of neoclass- ical theory (if the property rights issue is ignored) a labour market agent in such a group will receive a wage in excess of his marginal revenue product. The ‘inert’ area represents the cost (disutility) associated with dislodging a person from his accustomed routines. These include the costs of gathering and distributing information, persuading other workers (including others in the managerial hierarchy) of the desirability of the change and the possibility of sanctions by strong adherents. As a result the inert area is relatively stable and two points follow from this stability: (1) there will be little incentive to create a shift from a non-optimal position and (2) labour market agents will only reluc- tantly react to changes in environmental variables. I t is clear from this analysis that throughout the hierarchy of an organization there will be different effort levels and inert areas.

The empirical evidence put forward in support of the

01 43-6570/87/040333-06S05.00 0 1987 by John Wiley & Sons, Ltd.

concept has been based on engineering cost data taken from companies trading mainly in Third world coun- tries. The production function and consumer demand in these nations is likely to be changing rapidly, and the studies do not systematically test whether X- inefficiency is directly related to market power. A further limitation is that whilist the X-inefficiency concept is static the evidence has been taken from a dynamic environment. This has led to Stigler (1976) and others (such as De Alessi, 1983a, b) to criticize the testing (amongst other things) of the concept and to suggest that observed differences in cost functions of individual firms are concomitant with differences in entrepreneurial capacity, investment policies, site loc- ation, information costs and inadequately specified property rights. Whilst the difference in the two positions can only be resolved empirically, an early resolution of the debate seems unlikely, given the difficulties of unambiguously interpreting the available data. The practical importance of the debate is the extent to which resources are misallocated as a result of any departure from neoclassical theory. This in turn depends on the constraints facing such firms and their effect.

This paper will argue that whilst both positions are theoretically tenable there are various market forces at work in the real world which severely restrict the degree of inefficiency which can be tolerated by a firm with marker power. The tenor of the article will be therefore more sympathetic to Stigler and De Alessi than to Leibenstein. The first part of the paper will review the external constraints on a firm to minimize unit costs. These forces can be analysed under three headings: ( I ) the product markets; (2) the factor markets; and (3) the capital markets and, specifically, the stock market. The second part will analyse the effect of two important forces within firms which have the same effect-the management structure of most large companies and short-term capital constraints in the form of working capital.

EXTERNAL FORCES

Product Markets

Under this heading three market constraints will be identified and discussed: ( 1 ) potential entry by rivals; ( 2 )

334 R. K . ASHTON

the effect of competition in overseas markets; and (3) demand factors.

I t is self-evident that the possibility of entry places a limit on the amount of ineffciency which can be tolerated. In this context entry might take the form of developing new products which displace the existing one. The significance of this threat is a direct function of the rate at which technology (including information dissemination) and consumer demand is changing, profitability and barriers to entry.2 The importance of the last-mentioned will depend on the extent to which the market is contestable (Baumol, et al.. 1982), and for a critique of the concept see Shepherd (1984).

Under the second heading the impact of competition in overseas markets has most effect where a large proportion of the dominant firm’s output is sold overseas. Typically, margins in these markets are smaller (as a result of international competition), which puts pressure on management to reduce costs in order to compete more effectively. The degree of pressure will be a direct function of the proportion of output which is sold overseas, i.e. the higher the proportion, the greater the pressure on costs. As decisions relating to the utilization of inputs (and particularly labour) are almost certainly not affected by the destination of final output, overseas markets have a synergy effect on the cost of producing goods for the home market. In a UK context this pressure must not be underestimated, given the high proportion of manufacturing output which is exported.

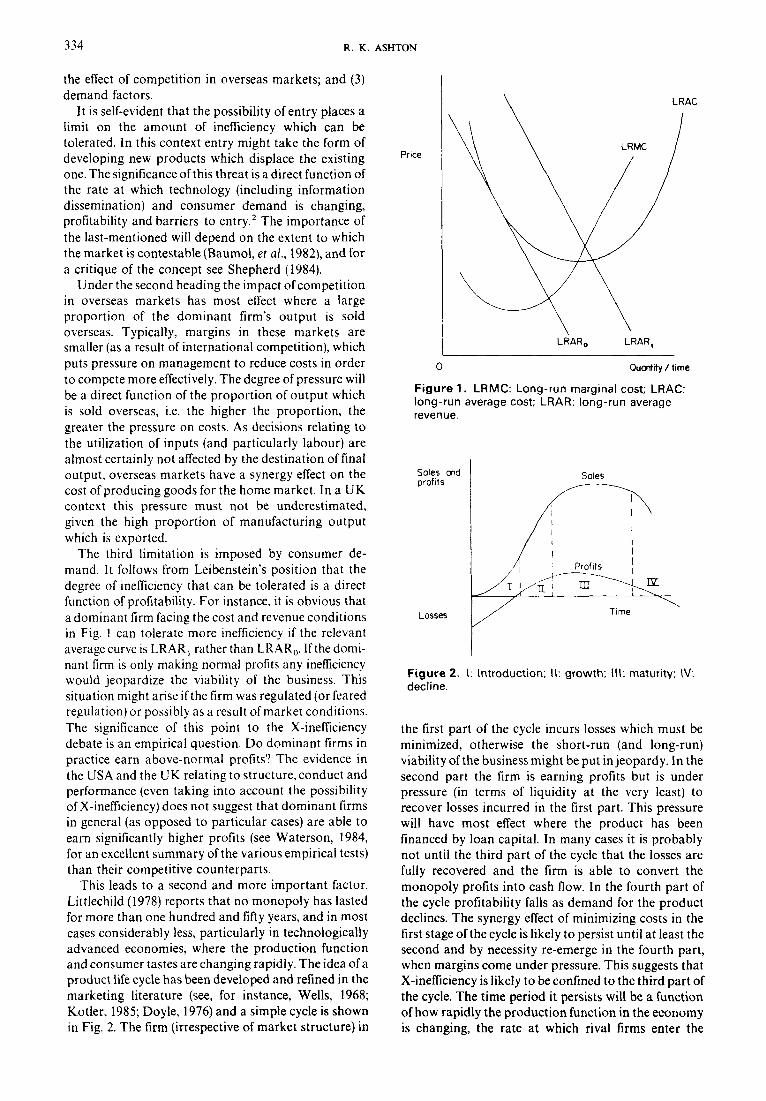

The third limitation is imposed by consumer de- mand. I t follows from Leibenstein’s position that the degree of inefficiency that can be tolerated is a direct function of profitability. For instance, it is obvious that a dominant firm facing the cost and revenue conditions in Fig. I can tolerate more inefficiency if the relevant averagecurve is LRAR, rather than LRAR,. Ifthe domi- nant firm is only making normal profits any inefficiency would jeopardize the viability of the business. This situation might arise if the firm was regulated (or feared regulation) or possibly as a result of market conditions. The significance of this point to the X-inefficiency debate is an empirical question. Do dominant firms in practice earn above-normal profits? The evidence in the USA and the UK relating to structure, conduct and performance (even taking into account the possibility of X-inefficiency) does not suggest that dominant firms in general (as opposed to particular cases) are able to earn significantly higher profits (see Waterson, 1984, for an excellent summary of the various empirical tests) than their competitive counterparts.

This leads to a second and more important factor. Littlechild (1978) reports that no monopoly has lasted for more than one hundred and fifty years, and in most cases considerably less, particularly in technologically advanced economies. where the production function and consumer tastes are changing rapidly. The idea of a product life cycle has been developed and refined in the marketing literature (see, for instance, Wells, 1968; Kotler, 1985; Doyle, 1976) and a simple cycle is shown in Fig. 2. The firm (irrespective of market structure) in

I LRAC

LRAR, LRAR,

0 Quantity / time

Figure 1. LRMC: Long-run marginal cost; LRAC: long-run average cost; LRAR: long-run average revenue .

Soles and Soles profits

I I

Time Losses Losses

Figure 2. I: Introduction; II: growth; III: maturity; IV: decline.

the first part of the cycle incurs losses which must be minimized, otherwise the short-run (and long-run) viability of the business might be put in jeopardy. In the second part the firm is earning profits but is under pressure (in terms of liquidity at the very least) to recover losses incurred in the first part. This pressure will have most effect where the product has been financed by loan capital. In many cases it is probably not until the third part of the cycle that the losses are fully recovered and the firm is able to convert the monopoly profits into cash flow. In the fourth part of the cycle profitability falls as demand for the product declines. The synergy effect of minimizing costs in the first stage of the cycle is likely to persist until at least the second and by necessity re-emerge in the fourth part, when margins come under pressure. This suggests that X-inefficiency is likely to be confined to the third part of the cycle. The time period it persists will be a function of how rapidly the production function in the economy is changing, the rate at which rival firms enter the

X-INEFFICIENCY AND MARKET POWER 33s

E mplcyment / time

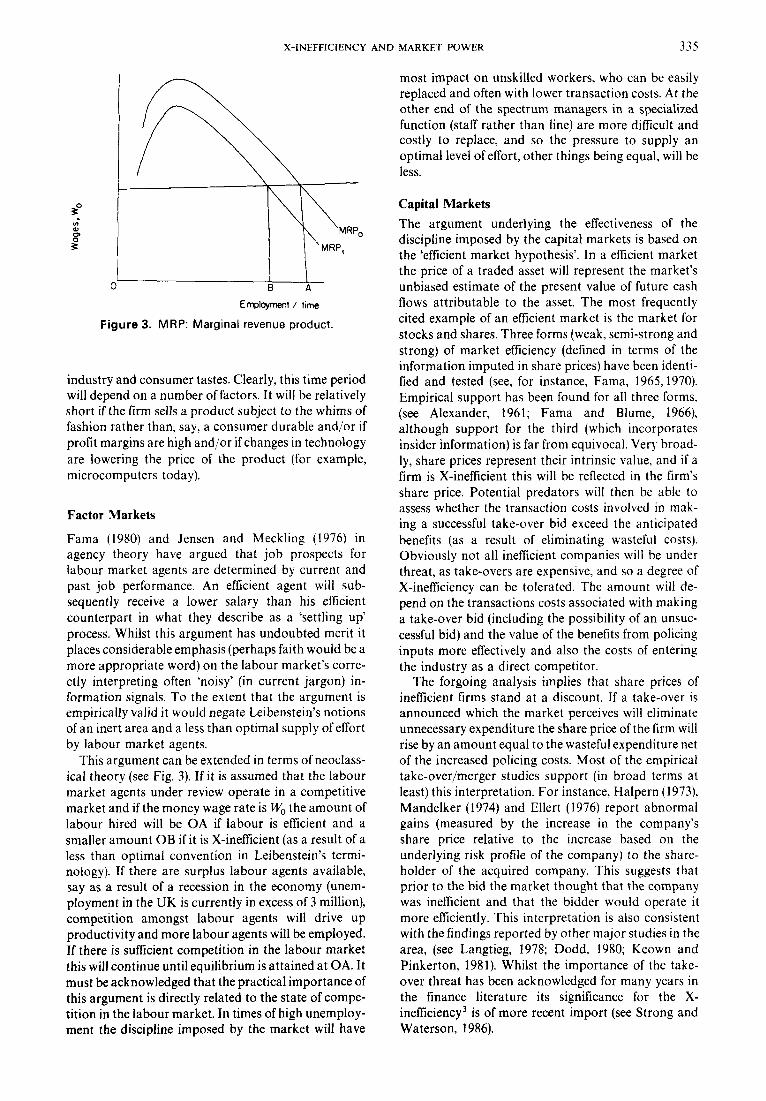

Figure 3. MRP: Marginal revenue product.

industry and consumer tastes. Clearly, this time period will depend on a number of factors. It will be relatively short if the firm sells a product subject to the whims of fashion rather than, say, a consumer durable and/or if profit margins are high and/or if changes in technology are lowering the price of the product (for example, microcomputers today).

Factor Markets

Fama (1980) and Jensen and Meckling (1976) in agency theory have argued that job prospects for labour market agents are determined by current and past job performance. An efficient agent will sub- sequently receive a lower salary than his efficient counterpart in what they describe as a ‘settling up’ process. Whilst this argument has undoubted merit it places considerable emphasis (perhaps faith would be a more appropriate word) on the labour market’s corre- ctly interpreting often ‘noisy’ (in current jargon) in- formation signals. To the extent that the argument is empirically valid it would negate Leibenstein’s notions of an inert area and a less than optimal supply of effort by labour market agents.

This argument can be extended in terms of neoclass- ical theory (see Fig. 3). If it is assumed that the labour market agents under review operate in a competitive market and if the money wage rate is W, the amount of labour hired will be OA if labour is efficient and a smaller amount OB if it is X-inefficient (as a result of a less than optimal convention in Leibenstein’s termi- nology). If there are surplus labour agents available, say as a result of a recession in the economy (unem- ployment in the UK is currently in excess of 3 million), competition amongst labour agents will drive up productivity and more labour agents will be employed. If there is sufficient competition in the labour market this will continue until equilibrium is attained at OA. It must be acknowledged that the practical importance of this argument is directly related to the state of compe- tition in the labour market. In times of high unemploy- ment the discipline imposed by the market will have

most impact on unskilled workers, who can be easily replaced and often with lower transaction costs. At the other end of the spectrum managers in a specialized function (staff rather than line) are more difficult and costly to replace, and so the pressure to supply an optimal level of effort, other things being equal, will be less.

Capital Markets The argument Underlying the effectiveness of the discipline imposed by the capital markets is based on the ‘efficient market hypothesis’. In a efficient market the price of a traded asset will represent the market’s unbiased estimate of the present value of future cash flows attributable to the asset. The most frequently cited example of an efficient market is the market for stocks and shares. Three forms (weak, semi-strong and strong) of market efficiency (defined in terms of the information imputed in share prices) have been identi- fied and tested (see, for instance, Fama, 1965,1970). Empirical support has been found for all three forms, (see Alexander, 1961; Fama and Blume, 1966). although support for the third (which incorporates insider information) is far from equivocal. Very broad- ly, share prices represent their intrinsic value, and if a firm is X-inefficient this will be reflected in the firm’s share price. Potential predators will then be able to assess whether the transaction costs involved in mak- ing a successful take-over bid exceed the anticipated benefits (as a result of eliminating wasteful costs). Obviously not all inefficient companies will be under threat, as take-overs are expensive, and so a degree of X-inefficiency can be tolerated. The amount will de- pend on the transactions costs associated with making a take-over bid (including the possibility of an unsuc- cessful bid) and the value of the benefits from policing inputs more effectively and also the costs of entering the industry as a direct competitor.

The forgoing analysis implies that share prices of inefficient firms stand at a discount. If a take-over is announced which the market perceives will eliminate unnecessary expenditure the share price of the firm will rise by an amount equal to the wasteful expenditure net of the increased policing costs. Most of the empirical take-over/merger studies support (in broad terms at least) this interpretation. For instance, Halpern (1 973). Mandelker (1974) and Ellert (1976) report abnormal gains (measured by the increase in the company’s share price relative to the increase based on the underlying risk profile of the company) to the share- holder of the acquired company. This suggests that prior to the bid the market thought that the company was inefficient and that the bidder would operate it more efficiently. This interpretation is also consistent with the findings reported by other major studies in the area, (see Langtieg, 1978; Dodd, 1980; Keown and Pinkerton, 1981). Whilst the importance of the take- over threat has been acknowledged for many years in the finance literature its significance for the X- inefficiency3 is of more recent import (see Strong and Waterson, 1986).

336 R. K . ASHTON

It has been suggested to this writer that since the concept of X-inefficiency is difficult to test empirically how can the market identify this factor? Obviously the capital market has the same problems as professional economists, and has to rely on imperfect information sources such as financial accounts and industry fore- casts. Whilst these sources and indicators contain a ‘noise’ factor, they have the affect of alerting the capital market. Analysts in stockbroking firms often have briefing meetings with top management, and as a result of their close working relationship with the institutional shareholders are able to remove, or exert, pressure on inefficient management. A much-publicized example in a UK context was the removal (some years ago) of top management at Burton’s (a large retailing group in the UK. This was a direct result of a report prepared by a prominent firm of stockbrokers4 which investigated the poor financial performance of the company. Although this evaluation by the financial community must. by definition, be imperfect, the market appears not to be at a disadvantage, otherwise there would be clamours for more detailed disclosure in company accounts. In recent years the demand for more inform- ation from the financial community has been directed towards greater refinement ofexisting principles rather than disclosure of more detailed information.

ment (and costs) in working capital and, in some cases, in fixed assets. With the exception of the retailing and service industries, there is often a considerable lead time between purchasing stock for conversion into final output and the receipt of cash from the sale of final output. This often necessitates a substantial investment (for varying intervals, depending on the nature of the product) in work in progress, which in most cases is financed on a short-term basis (for example, by bank overdraft). Firms in this position are extremely vulnerable to short-term liquidity crises and have an incentive to minimize costs in order to reduce their commitments to external suppliers of finance, who may either reduce or withdraw credit lines at short notice. It follows that the pressure on liquidity, or rather the absence of it, forces firms to be cost efficient. This pressure will be a direct function of the lead time involved in converting stock into final output and also the financial structure of the firm (i.e. the extent to which it is debt-rather than equity-financed). As most companies in the UK finance their working capital requirements and sometimes their fixed assets by short- term borrowing, this pressure, together with a shortage in recent years of trade credit generally, has meant that most firms, irrespective of market power, have had to act very cost-consciously.

INTERNAL FORCES ~ ~~~

CONCLUSIONS

Organizational Design

The previous paragraph has argued that quoted com- panies must be efficient, otherwise they are vulnerable to a take-over bid. This poses the question: how are companies with diverse activities managed efficiently’? Most companies delegate a certain amount of power (in terms of investment base) to divisionss and hold divisional managers accountable (in terms of financial targets) for their actions. This leads to competition between divisions, as both promotion and often salary are based (at least in part) on the financial results. Failure to maximize profits by not minimizing costs would jeopardize future prospects and salary. Whilst divisionalization can lead to decisions which are not in the interest ofthe group as a whole’ (possibly resulting in cost inefficiencies), the extent to which i t (div- isionalization) prevails and continues to grow in practice suggests that, on balance. it is found to be the most efficient way of managing a large organization. Divisionalization therefore encourages managers to minimize costs irrespective of the extent to which they dominate their particular market. Empirical support for this line of argument has been found by Steer and Cable (1978) in the UK and Armour and Teece (1978) in the USA.

Liquidity

Very few (if any) firms operate without any constraint on both short- and long-term liquidity. The effect of this constraint is to force management to minimize invest-

This paper has argued that Leibenstein’s concept of X- inefficiency is an oversimplification, as i t takes no account of various factors which limit the degree of inefficiency that can be tolerated in an organization. Whilst some of these factors are not new to the debate (i.e. the take-over threat) and some, it might be argued, are already implicit in the literature (i.e. the state of competition in the labour market), the aim ofthis paper has been to analyse all the relevant factors in order to assess the practical significance of the X-inefficiency problem.

It has been argued that firms with market power face a number of external and internal constraints which force them to operate like the competitive firm as- sumed in neoclassical theory. The misallocation of resources attributable to cost inefficiency is therefore likely to be small and attributable to transient (and disequilibrium) factors. The conclusions of this paper are therefore more sympathetic to Stigler than to Lei benstein.

I t has been suggested to the author that whilst these constraints are .likely to induce greater effort, their effect on the organizational hierarchy will not be uniform.’ Specifically, the amount of increased effort will be directly related to a person’s position in the organization. Changes in market forces are likely to have more effect on the effort supplied by management (and then in varying degrees) than shopfloor labour. In most companies, management, almost by definition, will be closer to developments in the marketplace and in a better position to assess these developments. In the

X-INEFFICIENCY AND MARKET POWER 337

limit those at the bottom of the organizational hierar- chy (shopfloor labour), are often unaware or do not fully appreciate the significance of changes in the marketplace, and are likely to treat requests for in- creased effort with cynicism and to dismiss these as part of a propaganda ploy by management. Even where such requests are met with less scepticism they are likely to be treated as containing a ‘noise’ factor. This does not affect the validity of the arguments set out in this paper, as management can impose the same discipline on the workforce by pursuing a competitive personnel policy, i.e. only promoting the most produc- tive workers and sacking those who supply less than an optimal amount of effort. Obviously, the effectiveness of this process is a function of the labour market, but even in times of relatively high unemployment there is an aversion to moving jobs (as a result of transactions and adjustment costs), and so

the effectiveness of a vigorous employment policy should not be underestimated.

The empirical question still remains to be answered, i.e. whether observed cost differences are attributable to inefficiency rather than, say, entrepreneurial capac- ity or different investment policies. One area where further research might be carried out is how the market and other companies resolve these important ques- tions. This paper has suggested that accounting in- formation and other industry data are basic inputs in making such assessments. Confirmation of this wodd provide a significant advance in terms of identifying X- inefficiency in practice.

Acknowledgement

Thanks are due to an anonymous referee. The usual disclaimers apply.

NOTES

1. A similar statement was made much earlier by Hicks (1935). 2. A convenient parallel can be drawn with oligopolistic pricing

behaviour (see Bain, 1949). 3. It has been referred to in the context of the profit-maximizing

debate (see Manne, 1961; Marris, 1963; Baumol, 1965). 4. The possibility of replacing inefficient management has in-

creased in recent years as a result of the increased importance of the institutional shareholders (see Briston and Dobbins,

1978) There are other less-publicized instances of inefficient management being replaced

5 Indeed Anthony and Dearden (1977) have argued that divisionalization is the only way a large multi-product organization can be managed efficiently In the economics literature this has been referred to as the M-form of organiz- ation (see Cowling, 1982)

6 See, for instance, Solomons (1 965) 7 I am grateful to the referee for making this point

REFERENCES

S. S. Alexander (1961). Price movements in speculative mar- kets: trends of random walks. Industrial Management Review May.

R. N. Anthony and J. Dearden (1977). Management Control Systems, Text and Cases, Homewood. Ill.: Irwin. Chapter 6.

H. 0. Armour and D. J. Teece (1 978). Organisational structure of economic performance: a test of multidivisional hypothesis. Bell Journal of Economics.

J. S. Bain (1949). A note on pricing in monopoly and Oligopoly. American Economic Review March, 448-64.

W. J. Baumol (1965). The Stock Market Economic Efficiency. New York: Fordham Universitv Press.

W. J. Baumol, J. C. Panzar and R . D. Willig (1982). Contes- table Markets and the Theory of Industry Structure, New York: Harcourt Brace Jovanovich.

R. J. Briston and R. Dobbins (1978). The Growth andlmpact of Institutional Investors, London: Institute of Chartered Accountants in England and Wales.

K. Cowling (1982). Monopoly Capitalism, New York: The Macmillan Press.

L. De Alessi (1983a). Property rights, transaction costs and X- inefficiency: an essay in economic theory. American Economic Review 73, March, 64-81.

L. De Alessi (1983b). Property rights and X-inefficiency: reply. American Economic Review 73. 843-5.

P. Dodd (1 980). Manager proposals, management discretion and stockholder wealth. Journal of Financial Economics June,

P. Doyle (1 976). The realities of the product life cycle. Quarterly

J. C. Ellert (1976). Merger, antitrust law enforcement and stock-

E. F. Farna (1 965). The behaviour of stock market prices. Journal

E. F. Fama (1 970). Efficient capital market: a review of theoryand

E. F. Farna (1980). Agency problems and the theory of the firm.

105-35.

Review of Marketing Summer, 1-6.

holder returns. Journal of finance May, 715-32.

of Business 38, 34-1 05.

empirical work. Journal of Finance May, 383-41 7.

Journal of Political Economy 88. 288-307. E. F. Fama and M. E. Blume (1 966). Filter rules and stock market

trading. Journal of Business 39, 226-41. P. J. Halpern (1973). Empirical estimates of the amount and

distribution of gains to companies in mergers. Journal of Business October, 554-75.

J. R. Hicks (1 935). Annual survey of economic theory: the theory of monopoly. Econometrica January, 8-35.

M. C. Jensen and W. H. Meckling (1 976). The theory of the firm; managerial behaviour, agency costs and ownership structure. Journal of Financial Economics 3. October, 305-60.

A. J. Keown and J. M. Pinkerton (1981). Merger announce- ments and insider trading activity: an empirical investigation. Journal of Finance September, 855-69.

P. Kotler (1 985). Marketing Management: Analysis. Planning and Control, Englewood Cliffs, NJ: Prentice-Hall, pp. 352-81,

T. C. Langetieg (1 978). An application of a Three-Factor Perfor- mance Index to Measure Stockholder Gains from Merger. Journalof FinancialEconomics December 1978. pp. 365-383.

H. Leibenstein (1 966). Allocative efficiency vs X-efficiency. American Economic Review June, 392-41 5.

H. Leibenstein (1975). Aspects of the X-efficiency theory of the firm. Bell Journal of Economics 6, August, 580-660.

H. Leibenstein (1 976). Beyond Economic Man; A New Found- ation for Micro-Economics, Boston, Mass.: Harvard University Press.

H. Leibenstein (1 983a). Property rights and X-efficiency: com- ment. American Economic Review 56, September, 831 -42.

H. Leibenstein (1 983b). Property rights and X-efficiency: com- ment. American Economic Review 73. 831-42.

S. C. Littlechild (1978). The fallacy of the mixed economy, an Austrian critique of economic thinking and policy. Institute of Economic Affairs. Hobart Paper , No. 80.

G. Mandelker (1 974). Risk and return: the case of merging firms. Journal of Financial Economics 303-35.

H. G. Manne (1961). Mergers and the market for corporate control. Journal of Political Economy 73, April, 753-61,

338 R. K. ASHTON

R. Marris (1963). A model of managerial enterprise. Quarterly Journal of Economics May, 185-209.

D. Solomons (1 965). Divisional Performance: Measurement and Control. New York: Financial Executives Research Foundation.

P. Steer and J. R. Cable (1979). Internal organisation and profit: an empirical analysis of large UK companies. Journal of Industrial Economics September.

W. C. Shepherd (1 984). Contestability vs competition. American Economic Review 74. 572-87.

G. J. Stigler (1966). Theory of Pnce, London: Macmillan. G . J. Stigler (1 976). The existence of X-efficiency. American

Economic Review 66, March, 21 3-1 6. N. Strong and M. Waterson (1986). Principals, Agents and

Information in Theory of the Firm. A. McGuinness and R. Clarke (eds), Oxford: Blackwell.

M . Waterson (1 984). Economic Theory ofthe Industry, Cambrid- ge: Cambridge University Press.

Wells, Jr (1 968). A product life cycle for international trade? Journal of Marketing July, 1-6.