Embed Size (px)

Citation preview

www.KPMGUniversityConnection.com

Fall 2013

Sales and Use Taxes and the Marketplace Fairness Act (MFA)

December 2013

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

2

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY KPMG TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY OTHER PERSON OR ENTITY FOR THE

PURPOSE OF (i) AVOIDING PENALTIES THAT MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR RECOMMENDING TO ANOTHER

PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons, without limitation, the tax treatment or tax structure, or both, of any transaction described in the associated materials we provide to you, including, but not limited to, any tax opinions, memoranda, or other tax

analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are subject to change. Applicability of the information to specific situations should be determined through

consultation with your tax adviser.

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

3

Dated Material

THE MATERIAL CONTAINED IN THESE COURSE MATERIALS IS CURRENT AS OF THE DATE PRODUCED.

THE MATERIALS HAVE NOT BEEN AND WILL NOT BE UPDATED TO INCORPORATE ANY TECHNICAL CHANGES TO THE CONTENT OR T0 REFLECT ANY MODIFICATIONS

TO A TAX SERVICE OFFERED SINCE THE PRODUCTION DATE. YOU ARE RESPONSIBLE FOR VERIFYING WHETHER OR NOT THERE HAVE BEEN ANY TECHNICAL CHANGES SINCE THE

PRODUCTION DATE AND WHETHER OR NOT THE FIRM STILL APPROVES ANY TAX SERVICES OFFERED FOR PRESENTATION TO CLIENTS. YOU SHOULD CONSULT

WITH WASHINGTON NATIONAL TAX AND RISK MANAGEMENT-TAX AS PART OF YOUR DUE DILIGENCE.

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

4

Introduction

The presentation provides an overview of state sales and use taxes and discusses the affect the Marketplace Fairness Act (MFA) will have on the states’ ability to require remote sellers to collect sales and use tax

Key topics include: general state sales and use tax overview, constitutional limitations on the states’ power of taxation, and how the MFA (if enacted) would expand the states’ ability to require sales and use tax collection on remote sales

www.KPMGUniversityConnection.com

Sales and Use Tax Overview

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

6

What is a Sales Tax?

There are four main types of sales taxes– Privilege tax– Consumer levy– Transaction tax– Gross receipts tax

Three characteristics distinguish these taxes– Shifting—tax burden transfers from collector to consumer– Absorption—collector can pay without passing burden

onto consumer– Separation—tax identified as line item on invoice

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

7

Which States Impose Broad- Based Sales and Use Taxes?

· 45 states and the District of Columbia impose some type of sales tax

· NOMAD– New Hampshire– Oregon– Montana– Alaska– Delaware

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

8

Definition of “Use Tax”

Tax imposed on the in-state use, storage, distribution, or consumption of tangible personal property (TPP) and enumerated services

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

9

Purpose of Use Tax

· Complementary to sales tax

· Equalize taxes on in-state and out-of-state purchases

· Ensures that sales tax doesn’t give incentive to

purchase from outside state

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

10

Use Tax on Items Subject to Sales Tax

· Usually not subject to use tax if sales tax already paid

· All 45 states and DC allow credit for sales taxes paid to

other states

· Credit for use taxes may be questionable

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

11

“First Functional Use” Rule

Tangible personal property is purchased out-of-state then brought into taxing state· Taxable if first functional use is in the state· Functional use means the use for which the property was

designed

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

12

Items Subject to Sales and Use Tax

Tangible personal property – "Tangible personal property" means personal property that

can be seen, weighed, measured, felt, or touched, or that is in any other manner perceptible to the senses

But, what about …– Digital Photographs– Downloaded software– Electricity

Note there is a trend for states to adopt legislation imposing sales and use tax on digital equivalents

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

13

Items Subject to Sales and Use Tax (Cont’d)

Certain enumerated services– i.e., repair services, telecommunications, maintenance– Some states have expanded or considered expanding

sales tax base to include more services– Very politically difficult to enact services tax legislation (i.e.,

Michigan experience)

True-object test– When a transaction involves tangible personal property

and services, the “true object” test is used to determine whether the taxpayer is purchasing a nontaxable service or taxable tangible personal property· Courts ask “what is the true object” of the purchase

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

14

Measure of Tax

Total sales price may include:– Property/service sold· NC sitting fees case/shipping charges

– Freight/handling charges– Value of trade-ins/barter– Hostess dollars– Value of manufacturer’s coupons or instant rebates– Other taxes included in price (i.e., taxes imposed on

manufacturers)– Sales tax (tax on tax)

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

15

Measure of Tax Deductions

Many states allow deductions for:– Discounts– Store coupons– Sales tax– Trade-in/barter value– Returns/allowances

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

16

Discounts, Coupons, and Rebates

· Purchase price discounts and retailers’ coupons generally reduce taxable base

· Manufacturers’ coupons and rebates are included in taxable base

· Shopper’s club card

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

17

Vouchers and Daily Deal Coupons

Tax Treatment of Group Discount Vouchers (e.g., Groupons, Living Social, etc.)

Kansas, Nebraska, Texas, Mississippi, Missouri · Tax due on the value exchanged for the voucher (non-discounted price)

California, Illinois, Iowa, Kentucky, Maine, Massachusetts, South Dakota, Wisconsin, Washington· Tax due on the voucher price

New York TSB-M-11(16)S (September 19, 2011)· Stated face value voucher - tax due on the value exchanged for the

voucher· Specific product/service voucher - tax due on voucher price

www.KPMGUniversityConnection.com

SAT Exemptions and Exclusions

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

19

Presumption of Taxability - Burden of Proof

· General presumption that all sales of TPP are subject to tax unless taxpayer can prove otherwise

· States have specific rules regarding documentation of exempt nature of sales

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

20

Reasons for Exemptions and Exclusions

Reasons for granting exemptions/exclusions:

Reason Federal Constitution Federal law preemption State policy Business incentives Social/economic policy

Example Purchases by federal

government Native American tribes Tax-exempt entities Manufacturing Food or medicine

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

21

Exemption Certificates

Generally, when the transaction is exempt due to the nature of the buyer (e.g., federal government), or the use of the purchased item (e.g., tractor used in agriculture)

– Resale– Industry (agricultural, etc.)– Property (manufacturing)– Generally must be taken in good faith– Obtained in a timely fashion– Retained for audit cycle

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

22

Exemption Certificate Basics

Exemption certificates have basic information provided to the seller

– Name of purchaser– Sales tax identification number provided by state– Date· Florida—yearly expiration—resale· Florida—five-year expiration—charitable organization

– Signature– Reason for exemption

Multi-jurisdictional certificates also available for participating states

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

23

What’s the Big Deal if Vendors Don’t Collect Exemption Certificates?

Sample Audit Assessment

Facts– $2 billion in annual sales– $100,000,000 in taxable sales– 1% error rate– 1% x $100,000,000 = $1,000,000 of non-exempt sales– Sales tax rate = 8.25%– $82,500 annual liability x 3 years

$285,000 liability in one state, not including penalty

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

24

Purchases for Resale

· In most states purchase for subsequent sale or lease are exempted/excluded as resale

· Seller has burden of establishing that purchase was for resale

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

25

Purchases for Resale (Cont’d)

Issues: Is property resold?– Meals purchased by airlines

– Free samples

– Prizes and awards

– Hamburger wrapper

– Hotel electricity

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

26

Manufacturing Exemptions

Manufacturing equipment/machinery– Most states exempt or reduce tax rate on purchases of

machinery/equipment used in production

– Application varies widely state to state

– Broad versus narrow application

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

27

Occasional/Isolated/Casual Sales

· Most states exempt “occasional” sales not made in ordinary course of business– Garage sale (frequency issue)– Sale of entire business

· May be construed narrowly/broadly

· May limit number of transactions or exclude sales of “big ticket” items (e.g., automobiles, aircraft, other registered assets)

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

28

Internet Services

Internet Tax Freedom Act– No state and local taxes on Internet access

– No discriminatory taxes on electronic commerce

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

29

Personal Necessities

· Promotes state public policy by reducing regressive nature of tax

· Examples

– Grocery food

– Utility services

– Medicine/drugs

– Clothing

www.KPMGUniversityConnection.com

Nexus

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

31

Nexus generally

Nexus = jurisdiction

– Nexus is a jurisdictional question: Does a state have the power to assert its taxing jurisdiction over a particular person or entity

Unless a retailer has nexus with a state, it cannot be required to collect and remit that state’s sales and use tax when it makes sales to in-state customers

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

32

Nexus: Constitutional Underpinnings

A state’s power of taxation is limited primarily by the Commerce and Due Process Clauses of the Constitution

– “Although the two claims are closely related, the Clauses pose distinct limits on the taxing powers of the [s]tates.” Quill Corp. v. North Dakota, 504 U.S. 298 (1992).

Due Process Clause (DPC)

– Requires some definite link, some minimum connection, between a state and the person, property or transaction it seeks to tax.

Commerce Clause

– Prohibits discrimination against interstate commerce and bars state regulations that unduly burden interstate commerce.

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

33

Nexus for Sales and Use Tax vs. Income Tax

· For income tax and sales and use tax, the DPC analysis is identical.

· However, the restrictions imposed by the Commerce Clause are more restrictive in the sales and use tax context. For sales and use tax nexus there is a physical presence requirement….

· BUT that physical presence does not need to be the taxpayer’s own physical presence

– Key question is whether the activities of the in-state entity are significantly associated with the taxpayer’s ability to establish and maintain a market in-state for sales

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

34

Attributional/Affiliate/Click-through Nexus

Affiliate nexus– In-state activities of related parties create nexus for

affiliated out-of-state retailers

Attributional nexus– In-state activities of unrelated parties create nexus for an

out-of-state retailer

Click-through nexus– Nexus results from the presence of a link on an in-state

person’s website to an out-of-state retailer and the in-state person receives a commission when sales are completed using the link

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

35

Sales and Use Tax Examples

Internet retailer located in Virginia makes sales of widgets to customers all over the U.S. All property and payroll in Virginia. Employees make several visits to Maryland to solicit. No third-parties perform activities on Retailer’s behalf.

Where is retailer required to collect and remit sales and use taxes?

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

36

Sales and Use Tax Examples (Cont’d)

Internet retailer located in Virginia makes sales of widgets to customers all over the U.S. All property and payroll in Virginia. Retailer owns a 60 percent interest in a distribution warehouse in South Dakota that delivers Retailer’s products. Retailer contracts with mechanics in New York that repair its products on occasion.

Where is Retailer required to collect and remit sales and use taxes?

www.KPMGUniversityConnection.com

Streamlined Sales Tax Project

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

38

Background

What is the Streamlined Sales Tax Project?· Multi-state effort to overhaul existing state sales and use tax

systems· Modernize sales and use tax laws

– Currently, there are over 9,600 state and local sales tax jurisdictions in the country

– Different tax rates and taxability rules for each jurisdiction

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

39

Background (Cont’d)

How will modernization be accomplished?– Simplification and uniformity– Use of advanced technology

Who is involved?– State governments· 39 states and the District of Columbia initially participated

– Local governments– Business community

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

40

Background (Cont’d)

Why is modernization important?– Reduce complexity of tax structure, especially for

multi-state taxpayers

– Increase voluntary compliance with sales and use tax laws

– Potentially lead to Congress overturning Quill

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

41

Background (Cont’d)

Why is this important to states?· Sales taxes are an important source of revenue for states

– Generally, less volatile than income tax revenues

· States increasingly concerned about loss of sales tax revenues as e-commerce grows

– Ongoing debates over actual amount of lost revenues

– Many internet vendors are already collecting sales and use taxes because they have in-state affiliates

– Example: Wal-Mart.com, Target.com, Gap.com

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

42

Background (Cont’d)

Why would this be important to businesses?· Ease of compliance

· Certainty as to taxability of items

· Uniform audit procedures

· Initial amnesty period for sellers voluntarily registering to collect taxes in streamlined states

· Use of certified service providers to perform sellers compliance functions

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

43

Streamlined Sales and Use Tax Agreement (SSUTA)

Drafted with input from states and businesses

· States incorporate the SSUTA agreed-upon provisions into their own laws

Agreement became effective on October 25, 2005, when states meeting 20% of the population were eligible for full or associate member status

www.KPMGUniversityConnection.com

Marketplace Fairness Act of 2013

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

45

Marketplace Fairness Act of 2013

Marketplace Fairness Act of 2013 (S. 743)· After being routed through an expedited voting process,

S.743 passed the Senate May 6, 2013 in a 69-27 vote

· If enacted, S. 743 would grant certain states the authority to require remote sellers to collect and remit sales and use taxes on sales into the state

· Bill now moves to the House, where it arguably faces greater opposition and will likely be amended

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

46

Marketplace Fairness Act of 2013

What Sellers would be required to collect and remit under Marketplace Fairness?

Generally, any seller making remote sales that is not currently required to collect sales and use taxes in certain states· Small seller exception

– Only sellers with gross annual receipts from total U.S. remote sales in the preceding calendar year exceeding $1 million can be required to collect and remit

– Aggregation rules apply for certain related sellers· No carve out for foreign (Non-U.S.) sellers or sellers located

in jurisdictions that do not impose a sales and use tax

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

47

Marketplace Fairness Act of 2013

What States would have this authority?· SSUTA full member states

· Other states implementing certain simplification requirements

– Authority could be exercised the first day of the calendar quarter that is at least 180 days after S.743 is enacted

– “State” is broadly defined and includes the District of Columbia, Puerto Rico, Guam, American Samoa, the United States Virgin Islands, the Northern Mariana Islands, tribal organizations, and any other territory or possession of the United States

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

48

Marketplace Fairness Act of 2013

What Minimum Simplification Requirements Must be Implemented in each non-SSUTA States?• Designating a single agency in the state responsible for all

state and local sales tax administration, return processing, and audits for remote sales sourced to the state;

• Designing a single return to be used by remote sellers for all state and local sales taxes within an individual state

• Having a single state and local audit for remote sellers

• Adopting a uniform tax base for state and local taxes within a state;

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

49

Marketplace Fairness Act of 2013

What Minimum Simplification Requirements Must be Implemented in each non-SSUTA States (cont’d)?

• Adopting a uniform tax base for state and local taxes;

• Adopting sourcing rules in accordance with the Act or the SSUTA;

• Providing information on taxable and exempt items;

• Providing software available free of charge to remote sellers

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

50

Marketplace Fairness Act of 2013

Other Key Provisions· Hold harmless provisions

– States must agree to hold remote sellers and certified service providers harmless under certain circumstances

· S. 743 does not subject a remote seller to any state taxes other than sales and use taxes– Likewise, the bill does not affect intrastate sourcing rules or

preempt the Mobile Telecommunications Sourcing Act

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

51

Knowledge Check

The following slides will test your knowledge of sales and use tax nexus under the assumption that the MFA has been signed into law.

Assumptions:

(1) All states mentioned have implemented the simplification requirements (either by joining the SSUTA or enacting their own uniformity provisions), and

(2) the provisions of the MFA have become effective on January 1 of Y1.

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

52

Knowledge Check

Slimmies, Inc., a Delaware corporation, specializes in making long shorts and Capri pants for the modern man. Slimmies, Inc. is headquartered in Georgia and owns manufacturing facilities in Texas and California. Additionally, the company has a distribution facility, customer service center, and retail shop located Kansas City, Kansas.

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

53

Knowledge Check – Question # 1

During Y1, Slimmies, Inc. has the following sales figures:– GA: $3 million– TX: $1.2 million– KS: $.5 million– CA: $.1 million

Starting in Y2, which states can require Slimmies, Inc. to collect and remit sales tax?

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

54

Knowledge Check – Question # 1 - Answer

Because Slimmies, Inc. has a physical presence in each state it is making sales, all the states (GA, TX, KS, and CA) may require Slimmies, Inc. to collect and remit sales tax.

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

55

Knowledge Check – Question # 2

During Y2, after localized marketing campaigns in Florida, Georgia, South Carolina, and Arizona, Slimmies, Inc. has the following sales figures:

– GA: $10 million

– TX: $5.2 million

– KS: $1.5 million

– CA: $10 million

– FL: $.3 million

– SC: $.4 million

– AZ: $.2 million

Starting in Y3, which states can require Slimmies, Inc. to collect and remit sales tax?

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

56

Knowledge Check – Question # 2 - Answer

· Because Slimmies, Inc. has a physical presence in GA, TX, KS, and CA, those states may require Slimmies, Inc. to collect and remit sales tax.

· Because Slimmies, Inc. makes less than $1 million of sales to states that, absent the MFA, could not require Slimmies, Inc. to collect and remit sales tax, the company does not have to collect and remit sales tax on sales made in FL, SC, or AZ.– In other words, Slimmies would meet the small seller

exception.

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

57

Knowledge Check – Question # 3

During Y3, after its product was worn by PSY, Korean musical genius responsible for “Gangnam Style,” to the Korean Grammys, Slimmies, Inc. has the following sales figures:

– GA: $13 million -- TX: $8 million

– KS: $4 million -- CA: $3 million

– FL: $.1 million -- SC: $.5 million

– AZ: $.3million -- DE: $1.1 million

– Korea: $300 million

Starting in Y4, which states can require Slimmies, Inc. to collect and remit sales tax?

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

58

Knowledge Check – Question # 3 - Answer

· GA, TX, KS, and CA may require Slimmies, Inc. to collect and remit sales tax. (See answer to Question # 2 for more details.)

· While Slimmies, Inc. makes $300.9 million of remote sales worldwide, the MFA’s $1 million threshold applies only to remote sales made in the United States, of which Slimmies, Inc. has made less than $1 million. As such, the company meets the small seller exception and cannot be required to collect and remit sales tax on sales made in FL, SC, or AZ.

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

59

Knowledge Check – Question # 4

During Y4, Slimmies, Inc. employs a sales force that conducts solicitation activities in MO and has the following sales figures:

– GA: $13 million -- TX: $8 million

– KS: $4 million -- CA: $3 million

– FL: $.7 million -- SC: $.6 million

– AZ: $.3million -- DE: $1.1 million

– Korea: $5 million -- SD: $.01

– MO: $3 million

Starting in Y5, which states can require Slimmies, Inc. to collect and remit sales tax?

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

60

Knowledge Check – Question # 4 - Answer

· Because of the company’s physical presence, GA, TX, KS, CA, and MO may require Slimmies, Inc. to collect and remit sales tax. (See answer to Question # 2 for more details.)

· Because Slimmies, Inc. made more than $1 million of remote sales during the preceding year, every state to which Slimmies, Inc. makes remote sales (FL, SC, AZ, and SD) may require Slimmies, Inc. to collect and remit sales tax.

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

61

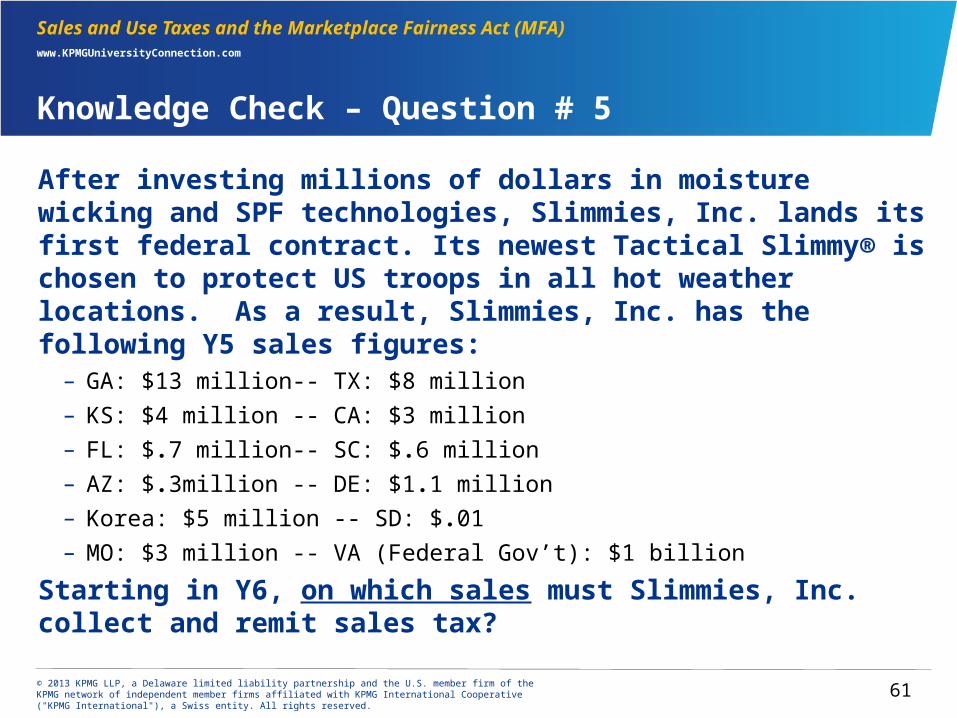

Knowledge Check – Question # 5

After investing millions of dollars in moisture wicking and SPF technologies, Slimmies, Inc. lands its first federal contract. Its newest Tactical Slimmy® is chosen to protect US troops in all hot weather locations. As a result, Slimmies, Inc. has the following Y5 sales figures:

– GA: $13 million -- TX: $8 million

– KS: $4 million -- CA: $3 million

– FL: $.7 million -- SC: $.6 million

– AZ: $.3million -- DE: $1.1 million

– Korea: $5 million -- SD: $.01

– MO: $3 million -- VA (Federal Gov’t): $1 billion

Starting in Y6, on which sales must Slimmies, Inc. collect and remit sales tax?

© 2013 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sales and Use Taxes and the Marketplace Fairness Act (MFA) www.KPMGUniversityConnection.com

62

Knowledge Check – Question # 5 - Answer

· Because of the company’s physical presence, Slimmies, Inc. must collect and remit sales tax on sales made to customers in GA, TX, KS, CA, and MO (assuming the relevant state imposes a sales tax). (See answer to Question # 2 for more details.)

· Because Slimmies, Inc. made more than $1 million of remote sales during the preceding year, every state to which Slimmies, Inc. makes remote sales (FL, SC, AZ, and SD) may require Slimmies, Inc. to collect and remit sales tax.

· Slimmies, Inc. is not required to collect and remit sales tax on sales made and shipped to the Federal Government in VA. As stated on slide 20, a state may not impose sales and use taxes on purchases by the federal government.

www.KPMGUniversityConnection.com

Questions?