Embed Size (px)

Citation preview

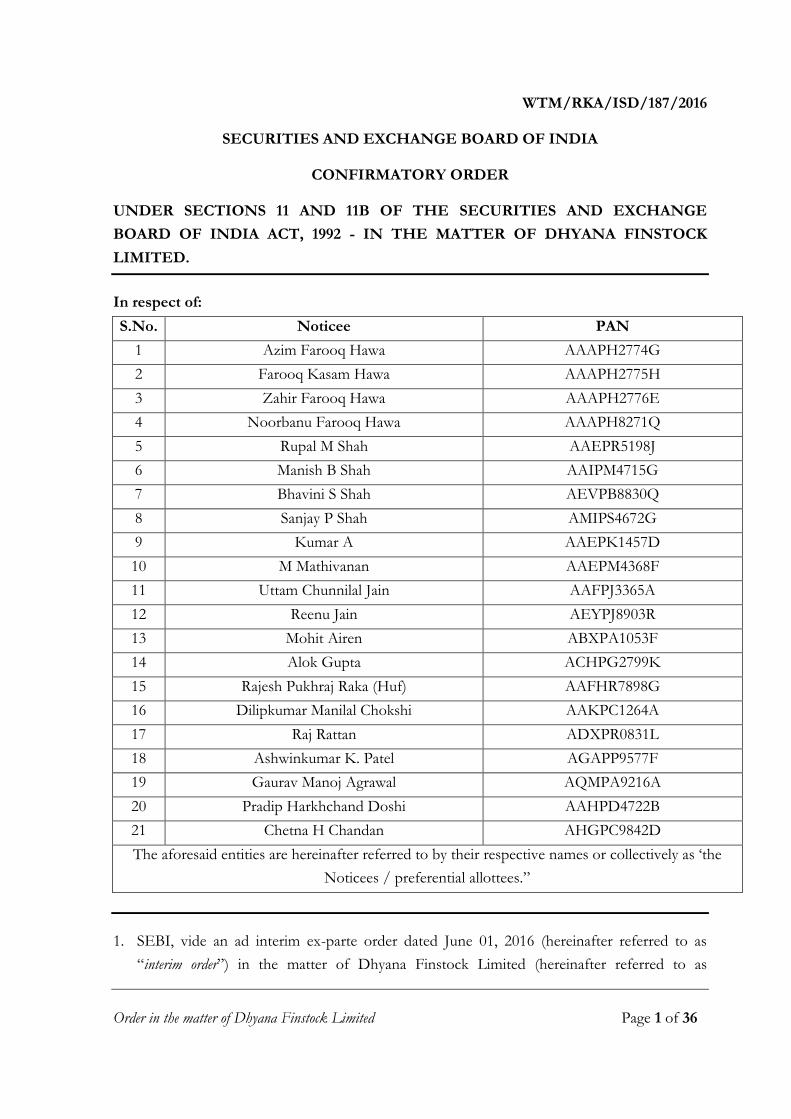

Order in the matter of Dhyana Finstock Limited Page 1 of 36

WTM/RKA/ISD/187/2016

SECURITIES AND EXCHANGE BOARD OF INDIA

CONFIRMATORY ORDER

UNDER SECTIONS 11 AND 11B OF THE SECURITIES AND EXCHANGE

BOARD OF INDIA ACT, 1992 - IN THE MATTER OF DHYANA FINSTOCK

LIMITED.

In respect of:

S.No. Noticee PAN

1 Azim Farooq Hawa AAAPH2774G

2 Farooq Kasam Hawa AAAPH2775H

3 Zahir Farooq Hawa AAAPH2776E

4 Noorbanu Farooq Hawa AAAPH8271Q

5 Rupal M Shah AAEPR5198J

6 Manish B Shah AAIPM4715G

7 Bhavini S Shah AEVPB8830Q

8 Sanjay P Shah AMIPS4672G

9 Kumar A AAEPK1457D

10 M Mathivanan AAEPM4368F

11 Uttam Chunnilal Jain AAFPJ3365A

12 Reenu Jain AEYPJ8903R

13 Mohit Airen ABXPA1053F

14 Alok Gupta ACHPG2799K

15 Rajesh Pukhraj Raka (Huf) AAFHR7898G

16 Dilipkumar Manilal Chokshi AAKPC1264A

17 Raj Rattan ADXPR0831L

18 Ashwinkumar K. Patel AGAPP9577F

19 Gaurav Manoj Agrawal AQMPA9216A

20 Pradip Harkhchand Doshi AAHPD4722B

21 Chetna H Chandan AHGPC9842D

The aforesaid entities are hereinafter referred to by their respective names or collectively as ‘the

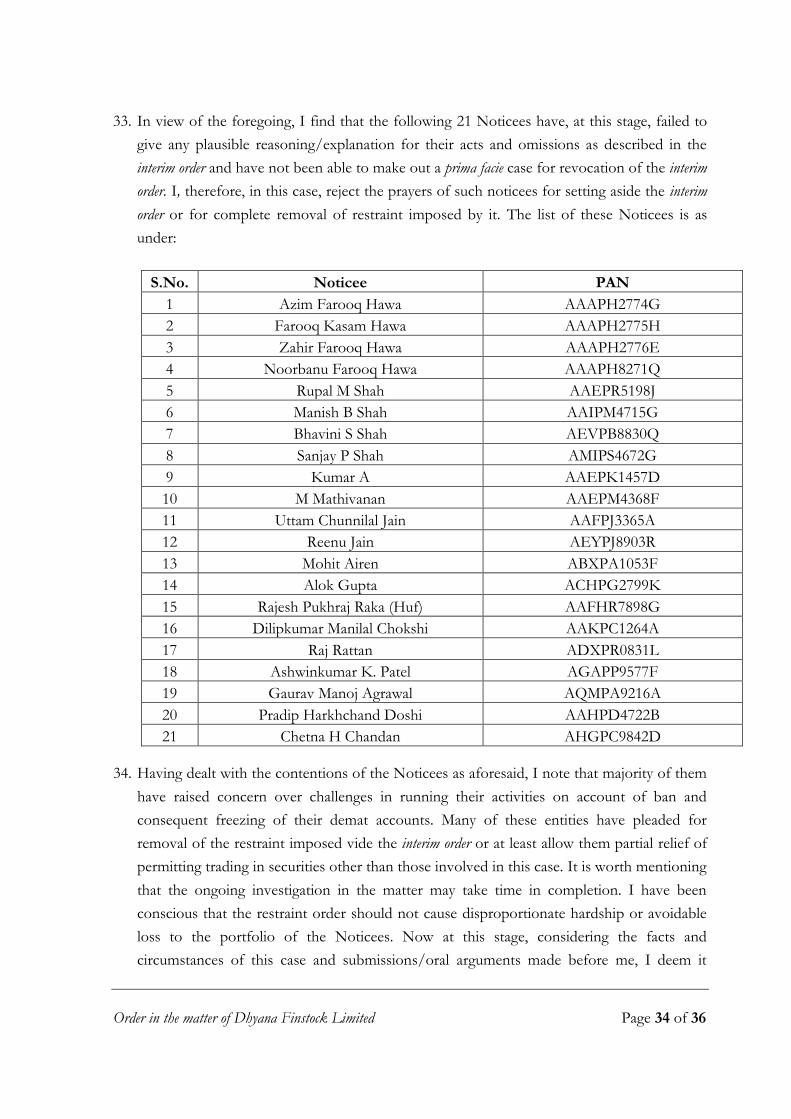

Noticees / preferential allottees.”

1. SEBI, vide an ad interim ex-parte order dated June 01, 2016 (hereinafter referred to as

“interim order”) in the matter of Dhyana Finstock Limited (hereinafter referred to as

Order in the matter of Dhyana Finstock Limited Page 2 of 36

"Dhyana" or "the company"), restrained 76 entities, including the aforesaid 21 entities

(hereinafter referred to as "Noticees"), from accessing the securities market and further

prohibited them from buying, selling or dealing in securities in any manner whatsoever, till

further directions. Further, it was also directed that BSE shall withhold the pay-out of funds

for the trades in Dhyana executed on July 27, 2015 and keep the same in interest bearing

escrow account and shall release the securities to the buyers for the trades executed on July

27, 2015. The persons/entities against whom the interim order was passed were advised to file

their objections, if any, within twenty one days from the date of the order and, if they so

desire, to avail themselves of an opportunity of personal hearing before SEBI.

2. The interim order was passed taking into account facts and circumstances more particularly

described therein and summarised, inter-alia, as under:

a) The equity shares of the company were listed on Ahmedabad Stock Exchange (ASE) in

1996. There was no trading history of the company at ASE.

b) On November 30, 2013, Dhyana made a preferential allotment of 64,25,000 equity

shares at the price of ₹ 10 per share to 49 entities.

c) The equity shares allotted on preferential basis to aforesaid allottees were locked-in for a

period of one year i.e. up to November 30, 2014 in terms of Securities and Exchange

Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2009. Thus,

the shares held by 49 entities who were allotted shares in the preferential allotment were

not tradable till November 30, 2014.

d) On June 13, 2014 this company with poor fundamentals (no income, no fixed assets)

and no trading history was listed on BSE from ASE. Company connected entity was

instrumental in establishing equilibrium price at BSE on June 13, 2014 in the Special Pre

Open Session (SPOS).

e) Between June 13, 2014 and November 28, 2014, ("Patch 1") the price of the scrip

opened at ₹ 251 and closed at ₹ 355. During this period, the scrip was traded with an

average volume of 5277 shares per day and total volume of 5,75,235 shares in 109

trading days.

f) Thereafter, between December 01, 2014 and July 27, 2015 ("Patch 2"), the price of the

scrip opened at ₹ 351 and closed at ₹ 405.7. During this period, the scrip was traded

with an average volume of 24,376 shares per day and total volume of 39,97,754 shares

in 164 trading days and the entities connected / related, directly or indirectly, to Dhyana

(forming part of a group named 'Dhyana Group' and also called named as 'exit providers'), started

providing hugely profitable exit to the preferential allottees..

g) During Patch 2, out of the 49 preferential allottees, 39 allottees exited and sold

31,67,410 shares and have in aggregate made profit of ₹.107.43crores. Of the shares

Order in the matter of Dhyana Finstock Limited Page 3 of 36

sold by preferential allottees, 18,22,678 shares representing 57.54% shares were bought

by Dhyana Group. Of the total purchase (23,03,449 shares) of Dhyana group, 18,37,121

shares (80%) were bought by them from the preferential allottees.

h) Certain private corporate bodies connected to each other and to Dhyana were observed

to have given funds to exit providers. Some of these exit providers were immediately

transferring the funds to trading members for purchase of shares of Dhyana.

i) During the patch 2, since July 2015 several SMS were circulated among investing public

to the effect of inducing them to buy the shares of Dhyana specially highlighting to make

"Jackpot "profit on July 27, 2015.

j) In the influence of SMS tips investors placed buy orders on July 27, 2015 at price

ranging from ₹ 396-₹ 406 resulting in purchase of 3,18,971 shares from the net sellers.

k) The 29 Net sellers who were part of Dhyana group sold 2,62,682 shares on July 27, 2014

representing 82.35% of total shares bought by the investors in the influence of SMSs.

There were 6 Preferential Allottees who sold 53,289 shares on July 27, 2015 and made

profit of ₹21.65 crores.

3. The allegations against Noticees as mentioned in the interim order are that, the acts and

omissions of Noticees are ‘fraudulent’ as defined under regulation 2(1)(c) of the SEBI

(Prohibition of Fraudulent and Unfair Trade Practices relating to Securities Market)

Regulations, 2003 (‘PFUTP Regulations’) and are in contravention of the provisions of

Regulations 3(a), (b), (c) and (d) and 4(1), 4(2)(a), (b), (e) (g) and (r) thereof and section

12A(a), (b) and (c) of the Securities and Exchange Board of India Act, 1992. These

allegations have been made, inter alia, on the basis of following:

a) Preferential allotment was used as a tool for implementation of the dubious plan,

device and artifice of Dhyana group and preferential allottees. Prior to the trading in its

scrip during the Examination Period, Dhyana did not have any business or financial

standing in the securities market. The traded volume and price of the scrip

increased substantially only after Dhyana group and preferential allottees started trading

in the scrip. Dhyana group entities were trading in the scrip above the LTP and their

trades resulted into artificial increase in price.

b) Dhyana group entities and preferential allottees traded amongst themselves as

substantiated by their trading details given in Table 7 and Annexure A of the interim

order. There was no change in the beneficial ownership of the substantial number of

traded shares as the buyers and sellers both were part of the common group and

were acting in league/concert to provide LTCG benefits to the allottees. In the

process, Dhyana group and allottees used securities market system to artificially

increase volume and price of the scrip for making illegal gains to and to convert ill-

Order in the matter of Dhyana Finstock Limited Page 4 of 36

gotten gains into genuine one.

c) The net sellers on July 27, 2015, who were either preferential allottees themselves or

had purchased shares of preferential allottees at a high price during the examination

period, may have availed the services of some unscrupulous elements to send the

SMS and thereafter dumped the shares of Dhyana so acquired on unsuspecting

investors by employing a scheme of sending fake SMS inducing them to buy in the

scrip. The facts and circumstances discussed in the interim order further indicate a

scheme, device and artifice to dump shares on July 27, 2015 in a pre-planned

manner i.e. by employing a scheme of sending fake SMS inducing investors to buy

in the scrip.

4. Pursuant to the interim order, some of the entities filed their replies in the matter.

Information/documents which were relied upon by SEBI for passing the interim order were

also provided to entities who had requested for the same. In the interim, some of the

entities filed their replies in the matter and sought opportunity of personal hearing. They

were granted opportunity of personal hearing on September 29, 2016. Few of the Noticees

also filed additional written submissions after availing the personal hearings.

5. Out of total 76 entities debarred vide interim order dated June 01 2016 in the matter; the

confirmatory orders have been passed in respect of 34 entities. The proceedings against 21

Noticees are being dealt with in this order. The proceedings in respect of remaining entities

would be dealt with separately in compliance with the principles of natural justice.

6. The replies/submission of 21 Noticees are summarised below. It is noted that certain

Noticees have submitted replies that are similar /identical in nature. Such replies have been

grouped together for the sake of brevity. In addition, various case laws referred by the

Noticees are also summarized below:

Gaurav Manoj Agrawal and Rajesh Pukhraj Raka (HUF) (both represented by Mr.

Ashish Satpute, Advocate):

a. They had denied all allegations made against them in the order.

b. Their role has not been explained in the entire order. Their names have been simply

inserted without evidence only because they are preferential allottee and they have

partially sold their shares.

c. They have purchased the shares after discussion with the financial advisor and

broker.

d. Out of the 1,00,000 shares so acquired by each of them they have sold only few

shares of the company. It can be safely concluded that such a miniscule amount of

Order in the matter of Dhyana Finstock Limited Page 5 of 36

trade cannot be alleged for manipulation in the price and volume of the scrip in any

manner.

e. They have sold the part of the stocks under question in the month of March 2015

and they did not entered in to any transaction in Dhyana in the month of July 2015,

i.e. the period of controversy.

f. The investment made by them in the company was as per the SEBI (ICDR)

Guidelines and Companies Act. Also the shares allotted to them were locked in for

1 year as per the said guidelines. The act of investment and sale of shares is lawful

act done by them.

g. The direction of debarring them is an arbitrary decision of SEBI. The order had a

great impact on his reputation in their personal and professional life. This order had

caused great hardship to them without any wrong doing on their part.

h. Power to issue directions under section 11, 11(4) and 11(B) is a drastic power and

and needed to be used only in extraordinary and exceptional SEBI needs to justify

the use of said action against them. Mere debarring them without justification is

irresponsible act done by SEBI.

i. The entities deny that they are in any way connected with the Company, its

Promoter/directors, Dhyana Group Entities/ Preferential Allottees, Exit Providers,

Trade Manipulators/SMS tips providers.

j. They had no role in price rigging and have no relation with alleged entities that were

responsible for price rigging.

k. They submit that long-term capital gains arising on account of sale of equity shares

listed in a recognised stock exchange, i.e., LTCG exempt under section 10(38) of

Income Tax Act, 1961. Hence, they cannot be charged for the allegations and

manipulation of tax evasion and money laundering.

l. Accordingly, the entities requested to set aside the arbitrary ad interim order of SEBI

against them.

Alok Gupta (represented by Mr. Vinay Chauhan, Advocate & Mr. K. C. Jacob,

Advocate):

a. He denied all allegations made against him in the order.

b. His role has not been explained in the entire order. His name has been simply

inserted without evidence only because he is a preferential allottee and he has

partially sold their shares.

c. The said Order is vitiated by gross violation of principles of natural justice, in as

much as no opportunity was provided to him to explain his version and the

circumstances as stated in the said Order do not justify dispensation of pre-

Order in the matter of Dhyana Finstock Limited Page 6 of 36

decisional hearing. Also, granting a post decisional hearing would not cure the

defect of not granting a hearing to him before passing a drastic order.

d. In October 2013 he was informed of a proposal to invest in preferential allotment

of equity shares made by DFL. He subscribed to 1,00,000 shares and paid

consideration amount of ₹. 10,00,000.

e. The shares allotted to him were locked in for 1 year. However, in February, 2015 he

required some funds for his internal purpose and hence decided to gradually start

selling the shares in the market as and when he required these funds. During the

period from February 2015 to April 2015 he sold 37,865 shares at the market price

at which it was trading in the exchange. As on date he continues to hold 62135

shares of the Company. His last sale transaction was on 15/04/2015. Further, sales

made by him had no connection/ nexus with the alleged SMS circulated by other

entities.

f. He has sold the part of the stocks under question in the month of March 2015 and

did not enter in to any transaction in Dhyana in the month of July 2015, i.e. the

period of controversy.

g. The investment made by him in the company was as per the SEBI (ICDR)

Guidelines and Companies Act. Also the shares allotted to him were locked in for 1

year as per the said guidelines. The act of investment and sale of shares is lawful act

done by him.

h. The direction of debarring him is an arbitrary decision of SEBI. The order had a

great impact on his reputation in his personal and professional life. This order had

caused great hardship to him without any wrong doing on their part.

i. Power to issue directions under section 11, 11(4) and 11(B) is a drastic power and

and needed to be used only in extraordinary and exceptional SEBI needs to justify

the use of said action against him. Mere debarring him without justification is

irresponsible act done by SEBI. SEBI has not made out any fact as to what is the

eminent danger caused by him or what is the urgency which require SEBI to

exercise power under Section 11 and 11 B it is clear that there was no imminent

danger or urgency so as to exercise powers under section 11 and 11(B) dispensing

with the pre decisional hearing in gross violation of principles of natural justice.

j. The entity deny that he is in any way connected with the Company, its

Promoter/directors, Dhyana Group Entities/ Preferential Allottees, Exit Providers,

Trade Manipulators/SMS tips providers.

k. He had no role in price rigging and has no relation with alleged entities that were

responsible for price rigging.

l. He submit that long-term capital gains arising on account of sale of equity shares

listed in a recognised stock exchange, i.e., LTCG exempt under section 10(38) of

Order in the matter of Dhyana Finstock Limited Page 7 of 36

Income Tax Act, 1961. Hence, he cannot be charged for the allegations and

manipulation of tax evasion and money laundering.

m. Accordingly, the entity requested to set aside the arbitrary ad interim order of SEBI

against him. He also requested that his demat account be unfreezed or alternatively,

he be allowed to sell his shareholding in the scrips other than the impugned scrip,

since the investigation is qua the impugned scrip only and to utilise the sale

proceeds, for his requirements.

Chetna H. Chandan (represented by Kirti S. Chandan, authorized representative) &

Pradip Harkhchand Doshi (appeared in person):

a. They have denied all allegations made against them in the order.

b. The entities have submitted that their names have been inserted in the list of

debarred entities under the heading preferential allottees; however, their roles are

not explained in the entire order.

c. They are not involved in any of the manipulations mentioned in the order. None of

their trades can be termed as the scheme of money laundering.

d. They have traded in their shares as normal course of business in the securities

market and as per the lawful provisions.

e. They are High Net worth individual (HNI) and have invested/traded in many

scrips. The order has adversely affected their investments and reputation. All their

business has come to standstill. This order had a great negative impact on reputation

and livelihood. It had caused them great hardship.

f. The investment made by them in the company was as per the SEBI (ICDR)

Guidelines and Companies Act. Also the shares allotted to them were locked in for

1 year as per the said guidelines.

g. They have sold their maximum holding before 27/07/2015 i.e. the day on which the

SMS scam took place. Hence, it is obvious that they cannot be alleged for the root

cause of the order i.e. fraudulent SMS tips to deceit the investors.

h. The investment made in the Dhyana was made from their owned funds. They have

invested in many scrips and this order has hampered their business, liquidity,

livelihood, growth, etc.

i. SEBI took this step arbitrary and thus defaming them in the society. SEBI order has

adversely impacted reputation in their personal and professional life. This order had

caused great hardship to them without any wrong doing on his part.

j. All their trades are genuine and with bonafide intention.

k. Power to issue directions under section 11, 11(4) and 11(B) is a drastic power and

and needed to be used only in extraordinary and exceptional SEBI needs to justify

the use of said action against them. Mere debarring them without justification is

Order in the matter of Dhyana Finstock Limited Page 8 of 36

irresponsible act done by SEBI. This act of SEBI has caused severe loss to them as

they are not able to earn her livelihood due to the mental pressure caused by the

said order.

l. The entities deny that they are in any way connected with the Company, its

Promoter/directors, Dhyana Group Entities/ Preferential Allottees, Exit Providers,

Trade Manipulators/SMS tips providers.

m. They submit that long-term capital gains arising on account of sale of equity shares

listed in a recognised stock exchange, i.e., LTCG exempt under section 10(38) of

Income Tax Act, 1961. Hence, they cannot be charged for the allegations and

manipulation of tax evasion and money laundering.

n. Their trades were independent and done by their own decision. Further, when SEBI

found the initial listing of the company suspicion then why didn't they took remedial

action at the time when the company got listed at BSE.

o. Interim order is passed when there is urgency in the matter; this order is passed after

more than 2 years from the listing of Company at BSE, after 12 months is of their

trades and also after withholding of payout since 11 months. What took so long for

SEBI to pass interim order, if they presume or if they had prior knowledge of any

misuse of system?

p. Hence, they have requested to reverse the order restraining them from accessing

securities market and buying, selling, or dealing in securities market directly or

indirectly in any manner.

q. Further, the entities have also requested that Pending investigation in the matter

following interim/alternative reliefs may be allowed:

(a)Permission to liquidate stocks/securities held in their portfolio and use the same

for their needs;

(b) Permission to avail rights/bonus, etc. accruing on the shares held by them.

Mohit Airen (represented by Mr. Vinay Chauhan, Advocate & Mr. K. C. Jacob,

Advocate):

a. He has denied all allegations made against him in the order.

b. The said Order is vitiated by gross violation of principles of natural justice, in as

much as no opportunity was provided to him to explain his version and the

circumstances as stated in the said Order do not justify dispensation of pre-

decisional hearing. Also, granting a post decisional hearing would not cure the

defect of not granting a hearing to him before passing a drastic order.

Order in the matter of Dhyana Finstock Limited Page 9 of 36

c. In October 2013 he was informed of a proposal to invest in preferential allotment

of equity shares made by DFL. He subscribed to 1,00,000 shares and paid

consideration amount of ₹. 10,00,000.

d. He bought from his own funds on preferential basis which were locked in for one

year. However, in February, 2015 he required some funds for his internal purpose

and hence decided to gradually start selling the shares in the market as and when he

required these funds. During the period from February 2015 to April 2015 he sold

36945 shares and sale proceeds of Rs.1.25 crore was utilised for business and

internal purpose. The balance 63055 shares are still lying with him. Also shares have

been sold on BSE BOLT system, which provides an anonymous platform where

buying and selling party are not known to each other.

e. The entity has denied any connection with the Company, its Promoter/directors,

Dhyana Group Entities/ Preferential Allottees, Exit Provider, fraudulent

SMS/email providers as alleged in the order.

f. He did not use the securities market system to artificially increase volume and price

of the scrip for making illegal gains.

g. The entity submitted that he has sold the part of the stocks under question in the

month of March 2015 and did not enter in to any transaction in Dhyana in the

month of July 2015 when the SMS tips were circulating in the market. He has

neither played any role in the SMS scam and nor allegation regarding the same has

been set out in the Order against him. Further, no connection of his has been

established with the manipulators in the Order.

h. As per the order, he has been alleged for violation of SEBI - Prohibition of

Fraudulent and Unfair Trade Practices Regulations, it is fact to be noted that, none

of his trades are alleged to be structured, synchronized, manipulative, reversal, off

market, with meeting of mind or pre-decided trades, etc.

i. The direction of debarring him is an arbitrary decision of SEBI. The order had a

great impact on his reputation in his personal and professional life. This order had

caused great hardship to him without any wrong doing on their part.

j. Power to issue directions under section 11, 11(4) and 11(B) is a drastic power and

and needed to be used only in extraordinary and exceptional SEBI needs to justify

the use of said action against him. Mere debarring him without justification is

irresponsible act done by SEBI. SEBI has not made out any fact as to what is the

eminent danger caused by him or what is the urgency which require SEBI to

exercise power under Section 11 and 11 B it is clear that there was no imminent

danger or urgency so as to exercise powers under section 11 and 11(B) dispensing

with the pre decisional hearing in gross violation of principles of natural justice.

Order in the matter of Dhyana Finstock Limited Page 10 of 36

k. He denied that his act and/or omission amounts to fraud, as he had no intentions

of creating any kind of artificial price rise, nor did he conceal any fact of make false

representation. He cannot be held liable for any violation of the SEBI Act of the

PFUTP Regulations and strongly state that the shareholders cannot be held liable

for the alleged misdeeds of the promoters of the company or their related entities.

l. He denied that there are acts and omissions pertaining to him which are fraudulent.

He has not contravened any of the provisions of Regulations 3(a), (b), (c) and (d)

and 4(1), 4(2)(a), (b), (e) and (g) thereof and section 12A(a), (b) and (c) of the SEBI

Act.

m. Accordingly, the order passed against him debarring him from accessing the

securities market in any manner be lifted and permitted to deal in securities market.

Further, he also requested that his demat account be un freezed or alternatively,

allowed to sell his shareholding in scrips other than the impugned scrip and to

utilize the sale proceeds.

Ashwin Kumar K Patel (represented by Mr. Mayukh Pandya, consultant):

a. He has denied all the allegations made against him in the order. Requesting SEBI to

provide specific evidence against him. None of his trades can be termed as the scheme

of money laundering and traded in normal course of business in the securities market as

per the lawful provisions.

b. There is no material on record to show that false and misleading appearance in trading

was given to the investors by him in connivance with the other alleged entities, by

executing the impugned transactions.

c. He submitted that his name had been wrongly lumped, bunched and clubbed with the

alleged group entities without any cogent evidence.

d. He is a High Net worth Individual (HNI) and has traded/invested in many scrips. This

order had a great negative impact on reputation and livelihood. It had caused great

hardship.

e. He had acquired 50,000 share of Dhyana Finstock Ltd. on 5th February, 2014 on

preferential basis which were locked in for one year and was in Compliance with SEBI

(ICDR) guidelines and relevant provisions of Companies Act.7.

f. Out of 50,000 preferential shares allotted sold only 9,500 shares from 24 February, 2015

to 16 March, 2015 due to requirement of fund. The shares were sold before

27/07/2015 i.e. the day on which the SMS scam took place. Hence it is obvious that he

cannot be alleged to be part of any scam i.e. fraudulent SMS tips to deceit the investors.

The Order also does not allege him for the same.

Order in the matter of Dhyana Finstock Limited Page 11 of 36

g. He does the business of Farming/Agriculture and investor in stock market. He is not

directly or indirectly involved with Dhyana Group Entities and /or Exit Providers,

promoters/directors mentioned in the above referred Order.

h. He made the investment in the company from his own funds and invested in many

scrips and this order has hampered his business, liquidity, livelihood, growth, etc.

i. He has been alleged for violation of SEBI (PFUTP), it is fact to be noted that, none of

his trades are alleged to be structured, synchronized, manipulative, reversal, off market,

with meeting of mind or pre-decided trades, etc.

j. The entity deny that he is in any way connected with the Company, its

Promoter/directors, Dhyana Group Entities/ Preferential Allottees, Exit Providers,

Trade Manipulators/SMS tips providers

k. It is alleged by him that SEBI has used its powers under section 11 (B) of SEBI Act,

which is drastic power and needed to be used only in extraordinary and exceptional

cases. SEBI needs to justify the use of said action against him.

l. He submit that Long Term capital gains arising on account of sale of equity shares

listed in a recognized stock exchange, i.e., LTCG exempt under section 10(38) of

Income Tax Act. Hence, he cannot be charged for the allegations and manipulation of

tax evasion and money laundering.

m. The interim order is vitiated by gross violation of principles of natural justice, equity and

fair play as the same has been issued arbitrarily by SEBI without any evidence. SEBI

needs to provide justification and documentary evidence with regards to his

involvement in the alleged illegal activities, which is nowhere mentioned in the Said

Order.

n. His name is wrongly inserted in the Order and requesting to reverse the order

restraining him from accessing securities market and buying, selling, or dealing in

securities market directly or indirectly in any manner.

o. When SEBI found the initial listing rates of the Company Suspicious then why didn't

they took remedial action at the time when the company got listed at BSE.

p. Interim order is passed when there is urgency in the matter; this order is passed after more

than 2 years from the listing of Company at BSE, after 15 months of my trades. What

took so long for SEBI to pass interim order, if they presume or if they had prior

knowledge of any misuse of system?

q. The ex parte interim order debarring him from accessing the Securities market in any

manner is passed against principles of natural justice as it was passed without giving an

opportunity of hearing and hence is ab initio illegal and deserved to be set aside.

r. Further, the entity has also requested that Pending investigation in the matter following

interim/alternative reliefs may be allowed:

to liquidate stocks/securities held in his portfolio and use the same for his needs;

Order in the matter of Dhyana Finstock Limited Page 12 of 36

to avail rights/bonus, etc. accruing on the shares held.

to access securities market and to buy, sell or in other manner deal in Securities.

Manish B Shah and Rupal M Shah (represented by Mr. Nithish Bangera, Practicing

Company Secretary):

a. The entities have denied all the allegations made against them in the order.

b. Allotted 150000 shares on preferential basis whilst the company was listed at ASE. The

shares allotted were locked in for 1 year as per ICDR guidelines & Companies act. They

sold shares after holding the same for almost 15-18 months.

c. Their investment in DFL is one of their trade decisions. They have invested in Dhyana

Finstock Limited in the normal course from their owned funds. They have invested in

the preferential allotment in DFL at the instance of Mr. Vishaal Tamker.

d. The act of allotment and sale of investment was done lawfully and also have not

misused the stock exchange system. All trades are genuine and lawful. As a result of this

order, they are not able to do any business and live a normal life. This is a violation of

Right to live and do business inherited to them by the Indian Constitution.

e. The order is based on the assumptions, presumptions and guesses of SEBI. The order

speaks about the fraudulent SMS tips by certain entities which induced gullible investors

to buy shares. However, the order itself does not allege them for any of the above

allegations.

f. They have sold all their shares before 27/07/2015, hence, they cannot be alleged for

SMS scam.

g. The entities submit that they are in no way connected with the Company, its

Promoter/directors, Dhyana Group Entities/ Preferential Allottees, Exit Providers,

Trade Manipulators/SMS tips providers and counterparties.

h. They have invested in the company as Long term capital, and also hold the shares for

almost 18 months. LTCG is government scheme and is exempt under Income Tax Act.

Their trades cannot be termed as manipulative and dishonest.

i. They submit that, SEBI feels that preferential allotment is genuine as SEBI has not

debarred all preferential allottees. 10 preferential allottees who have not sold their

holdings are not debarred. It means SEBI feels that acquisition/purchase of shares is

genuine and selling of acquired shares is wrongful act.

j. The interim order is vitiated by gross violation of principles of natural justice, equity and

fair play as the same has been issued arbitrarily by SEBI without any evidence. SEBI

needs to provide justification and documentary evidence to them with regards to the

said order.

Order in the matter of Dhyana Finstock Limited Page 13 of 36

k. They requested to set aside the directions issued against them under Section 11(4) and

Section 11B of the SEBI Act, 1992 in the interest of justice and equity.

l. The entities have also submitted that they do not want such interim and generalised

reliefs as provided by SEBI in other cases.

Sanjay P Shah and Bhavini S Shah (represented by Mr. Nithish Bangera, Practicing

Company Secretary):

a. The entities have denied all the allegations made against them in the order.

b. The order had a great impact on their reputation in personal and professional life.

c. They have sold all their shares before 27/07/2015, hence, they cannot be alleged for

SMS scam.

d. Their investment in DFL is one of their trade decisions. They have invested in Dhyana

Finstock Limited in the normal course from their owned funds. They have invested in

the preferential allotment in DFL at the instance of Mr. Vishaal Tamker.

e. The investment in the Company was made as per the SEBI (ICDR) guidelines and

Companies Act and by investing their owned funds. Also the shares allotted to them

were locked in for 1 year as per the said guidelines. The act of investment and sale of

shares is lawful act.

f. The act of allotment and sale of investment was done lawfully and also have not

misused the stock exchange system. All trades are genuine and lawful. As a result of this

order, they are not able to do any business and live a normal life. This is a violation of

Right to live and do business inherited to them by the Indian Constitution.

g. The entities submit that they are in no way connected with the Company, its

Promoter/directors, Dhyana Group Entities/ Preferential Allottees, Exit Providers,

Trade Manipulators/SMS tips providers and counterparties.

h. The Long Term capital gains Long-term capital gains arising on account of Sale of

equity shares listed in a recognised stock exchange, i.e., LTCG exempt under section

10(38) of Income Tax Act. Hence, they cannot be charged for the allegations and

manipulation of LTCG.

i. They submit that, SEBI feels that preferential allotment is genuine as SEBI has not

debarred all preferential allottees. 10 preferential allottees who have not sold their

holdings are not debarred. It means SEBI feels that acquisition/purchase of shares is

genuine and selling of acquired shares is wrongful act.

j. The interim order is vitiated by gross violation of principles of natural justice, equity and

fair play as the same has been issued arbitrarily by SEBI without any evidence. SEBI

needs to provide justification and documentary evidence to them with regards to the

said order.

Order in the matter of Dhyana Finstock Limited Page 14 of 36

k. In capital market investors invest in shares mainly to earn profit. Even their act of

making investment and selling the same was the part of trading process of Securities

market. No one is expected to hold the shares till eternity. They made investment with a

view to en cash the same at a future date and has done the same.

l. They requested to set aside the directions issued against them under Section 11(4) and

Section 11B of the SEBI Act, 1992 in the interest of justice and equity.

m. The entities have also submitted that they do not want such interim and generalised

reliefs as provided by SEBI in other cases.

Dilipkumar Manilal Chokshi (appeared in-person along with Mr. Viral Shah, Chartered

accountant):

a. During course of business, he came to know one Mr. Pritesh Y. Shah of Ahmedabad

who is also associated with him as business colleague since long and his dues also.

b. Mr Pritesh Y Shah offered him that he has got an avenue by which he will help realise

his dues in which he will be allotted certain shares in a listed company named Dhyana

Finstock Ltd which is expanding its horizons in a big way in micro finance Sector and

also intending to apply for payment bank/Small bank licence to Reserve bank of India.

It is also proposing to be listed at Bombay Stock exchange Ltd later on soon then.

c. Mr Pritesh Shah has shown him various documents evidencing new projects and also

explained future beneficial positions by the said company in the micro finance sector

which is in thing in the then times and promised his dues will be recovered over a

period of time.

d. The shares proposed to be allotted will have lock in period of one year and thereafter,

he can dispose it off subject to liquidity in trading of said Stock.

e. Mr Pritesh shah gave him confidence that through such transaction, he will get his dues

back after lapse of lock in period rather than to wait for indefinite period for his dues.

f. After a lot of debate and interaction, he agreed to involve in such share allotment

transaction but put a disclaimer that he will not be spending a penny for that and it is

for Mr Pritesh shah to settle share purchase transaction in his name.

g. Thereafter, he was not made known the way to subscribe shares in his name. Mr

Pritesh Shah somehow managed to fund his account to enable application in

preferential issue of the said company. Mr Pritesh Shah got managed Rs.30,00,000/- in

his account for the specific purpose of application only.

h. He got an allotment letter from the company for allotment of 3,00,000 (Three lacs

only) equity shares of Rs 10/- each on 30th November, 2013 which will remain under

lock in for one year.

Order in the matter of Dhyana Finstock Limited Page 15 of 36

i. In December, 2014, when he came to know that securities of the company got listed on

BSE, he asked his M/s Dani Stock Brokers to dispose off certain shares to recover his

dues but could not be sold as volume was quite thin.

j. At last on 31st December, 2014, he was able to dispose off 3000 shares at Rs.321/- and

shocked as got more return than expected.

k. In July, 2015 as volume began to shrink along with the price of shares for no reason

known to him. Thereafter, he could not dispose off any shares.

l. Meanwhile, he came to know that BSE has held back settlement of pay-out for trades

executed on 27th July, 2015 acting upon complaints received from some investors

about illicit trades in the said Scrip. BSE also immediately suspended trading in the

securities of the company by then.

m. As he had recovered his dues and also earned handsome money, was least concerned

with the developments.

n. However, in June 2016, he received SEBI interim order restraining him along with others

from dealing in securities market till further directions as a consequence of being a part

of Dhyana preferential issue.

o. He does not know any of the entities named in the order nor associated with any of

them including Dhyana Finstock Ltd in any manner whatsoever.

p. He still holds more than 2 lacs shares of the said Company in his demat account.

q. Further, please note that the entire financial transaction as far as his shares are

concerned was carried out by Mr Pritesh Shah described above and have no clue

neither about how he managed the fund nor how he routed the fund. At that time, he

was only concerned with his money rather than anything else.

r. His name nowhere appears in interim order as regards illicit funding of application and

subscription money for the application for preferential issue.

s. The entity requested to lift the ban for investing in securities market as it affects his

credibility in the market.

Kumar A (represented by Mr. Nithish Bangera, Practicing Company Secretary):

a. He had acquired 50000 shares in the company by way of preferential allotment from his

owned funds and sold 18500 shares in the month of June 2015 over 5 days at the rate of

Rs. 355 before 27.07.2015. i.e. the day when the SMS scam took place. Also he is still

holding shares of the company. It is evident from above that he cannot be blamed for

price volume manipulation.

b. His trades are genuine, independent and should be viewed individually.

c. His investment in DFL is one of his trade decisions. He has invested in Dhyana

Finstock Limited in the normal course from his owned funds. He has invested in the

preferential allotment in DFL at the instance of Mr. Vishaal Tamker

Order in the matter of Dhyana Finstock Limited Page 16 of 36

d. The interim order is vitiated by gross violation of principles of natural justice, equity and

fair play as the same has been issued arbitrarily by SEBI without any evidence. SEBI

needs to provide justification and documentary evidence to him with regards to the said

order.

e. It is submitted that the power to issue directions under section 11(B) is a drastic power

available with SEBI. The directions under this section had a great consequence on his

reputation and livelihood. It is exceptional, extraordinary and discretionary power and

SEBI has to justify the need for invocation of the said power clearly.

f. The act of allotment and sale of investment was done lawfully and also has not misused

the stock exchange system. All trades are genuine and lawful. As a result of this order,

he is not able to do any business and live a normal life. This is a violation of Right to

live and do business inherited to him by the Indian Constitution.

g. He is not connected to any Dhyana group entity, Company, Directors, promoters,

Dhyana Group, Exit Providers, Other Preferential Allottees, etc. has been set out, his

name does not appear anywhere and connection with the said entities is not established.

h. He has not played any role in the SMS scam and no allegation regarding the same has

been established in the order against him.

i. He submits that, SEBI feels that preferential allotment is genuine as SEBI has not

debarred all preferential allottees. 10 preferential allottees who have not sold their

holdings are not debarred. It means SEBI feels that acquisition/purchase of shares is

genuine and selling of acquired shares is wrongful act.

j. He has not acted in concert with any group entities to misuse the stock exchange system

and transactions are genuine and were not done with an intention to inflate or cause

fluctuation in the market price of the securities.

k. He requested to set aside the directions against him under Section 11(4) and Section

11B of the SEBI Act, 1992 in the interest of justice and equity. Further, he also submits

that he does not want such interim and generalised reliefs as provided by SEBI in other

cases.

M. Mathivanan (represented by Mr. Nithish Bangera, Practicing Company Secretary):

a. He refutes all the allegations against him in the order.

b. He has bought 150000 shares through preferential allotment and sold 66791 shares.

Balance 83209 shares are still lying in his name.

c. His investment in DFL is one of their trade decisions. He has invested in Dhyana

Finstock Limited in the normal course from his owned funds. He has invested in the

preferential allotment in DFL at the instance of Mr. Vishaal Tamker.

d. His investment in this company was long term in nature. Long term Capital gain is

exempted from Income Tax.

Order in the matter of Dhyana Finstock Limited Page 17 of 36

e. The act of allotment and sale of investment was done lawfully and also has not misused

the stock exchange system. All trades are genuine and lawful. As a result of this order,

he is not able to do any business and live a normal life. This is a violation of Right to

live and do business inherited to him by the Indian Constitution.

f. He is being alleged for violation of SEBI (PFUTP), in spite of that none of his trades

are alleged to be manipulative with meeting of mind with anyone. Long Term Capital

Gain etc. is subject matter Income Tax Authorities. And till day he has not received any

communication from Income tax Authorities.

g. His investment was in compliance with the SEBI (ICDR) guidelines and Companies

Act. His investment and disinvestment was genuine and legitimate.

h. He has sold all his shares before the 27.07.2015. Hence, he cannot be blamed for any so

called manipulation done on 27.07.2015.

i. He submits that, SEBI feels that preferential allotment is genuine as SEBI has not

debarred all preferential allottees. 10 preferential allottees who have not sold their

holdings are not debarred. It means SEBI feels that acquisition/purchase of shares is

genuine and selling of acquired shares is wrongful act.

j. He is not connected to any Dhyana group entity, Company, Directors, promoters,

Dhyana Group, Exit Providers, Other Preferential Allottees, etc. has been set out, his

name does not appear anywhere and connection with the said entities is not established.

k. SEBI has wrongly considered his trades as a part of some scheme, potential case of

money laundering and tax evasion. There is no evidence to prove that his trades are

meant for money laundering. All his trades were in normal course of business.

l. He requested to reverse the order restraining him from accessing securities market and

buying, selling, or dealing in securities market directly or indirectly in any manner.

Further, he also submits that he does not want such interim and generalised reliefs as

provided by SEBI in other cases.

Uttam Chunnilal Jain and Reenu Uttam Jain (represented by Mr. Nithish Bangera,

Practicing Company Secretary):

a. They have been debarred from accessing the securities market, due to which

investments of about ₹. 91.13 Lac and ₹ 22 respectively is blocked. It is against the

principle of natural justice, right to life and to do business.

b. The act of allotment and sale of investment was done lawfully and also has not misused

the stock exchange system. All trades are genuine and lawful. As a result of this order,

they are not able to do any business and live a normal life. This is a violation of Right to

live and do business inherited to them by the Indian Constitution.

Order in the matter of Dhyana Finstock Limited Page 18 of 36

c. The power to issue directions under section 11(4) and 11(B) is a drastic power having

serious civil consequences and ramifications on the repute and livelihood of those

against whom it is directed. Said power is not available for routine and retrospective

application and cannot be used for penal action. It is exceptional, extraordinary and

discretionary power and SEBI has to justify the need for invocation of the said power

clearly.

d. Total 50000 shares each were allotted to them in preferential allotment and they sold

entire holding of 50000 shares before 27/07/2015. Their transactions were made out of

their own funds. They have traded in a narrow price range from ₹. 317.50 to ₹. 345 and

not played any role in the SMS scam. They cannot be blamed for price volume

manipulation.

e. Their investment in DFL is one of their trade decisions. They have invested in Dhyana

Finstock Limited in the normal course from their owned funds. They have invested in

the preferential allotment in DFL at the instance of Mr. Vishaal Tamker.

f. They submit that, SEBI feels that preferential allotment is genuine as SEBI has not

debarred all preferential allottees. 10 preferential allottees who have not sold their

holdings are not debarred. It means SEBI feels that acquisition/purchase of shares is

genuine and selling of acquired shares is wrongful act.

g. They are not connected to any of the alleged group entities i.e. promoter group entities,

company and its directors and no fund transfers with the alleged group entities.

h. Not violated the provisions of Regulation 4(b), 4(c) and 4(d) of SEBI (Prohibition of

Fraudulent and Unfair Trade Practices Relating to Securities Market) Regulation read

with Regulation 13(2) of the SEBI (Prohibition of Fraudulent and Unfair Trade

Practices Relating to Securities Market) Regulations, 2003.

i. There is no lapse or wrongdoing on their part as alleged or otherwise. Their trades

could not be said to have contributed to any false or misleading appearance of trading in

the said scrips. Further, volume of trading was delivery based and hence genuine and

not artificial as sought to be suggested.

j. They requested to set aside the directions against him under Section 11(4) and Section

11B of the SEBI Act, 1992 in the interest of justice and equity.

k. Their portfolio is worth ₹. 92 lac and ₹. 22 lacs respectively. Their holding is in 32 blue

chip scrips and 22 blue chip scrips respectively. They are going through financial crunch

and wants to urgently en cash his investments and also the rates of certain securities are

high currently which can fetch him good amount and will resolve the issue of liquidity.

l. Accordingly, they requested that interim order should be suspended till completion of

investigation. Further, they should be permitted to sell his existing portfolio and

proceeds of the same be credited to his bank account.

Order in the matter of Dhyana Finstock Limited Page 19 of 36

m. Further, they also submit that they do not want such interim and generalised reliefs as

provided by SEBI in other cases.

Raj Rattan (represented by Mr. Prakash Shah, Advocate):

a. He is a pure investor and shareholder in DFL and had no role in internal affairs of the

company.

b. He submit that he invested in DFL at the instance of Mr. Ramesh Kumar Tiberewala, a

stock broker, who regularly gives him financial advice with respect to investing his

money.

c. He had not traded in scrip of Dhyana on 27.07.2015. Merely because he was allotted

preferential shares of company he cannot be blamed or alleged to have been involved in

any fraudulent' activity by company or any of its allegedly connected entities.

d. He had purchased 1,00,000 shares of Dhyana on 30.11.2013 with his legitimate income

and except for being a bonafide shareholder he has no connection and relationship of

whatsoever nature with the company, its promoters, directors, employee or any of its

alleged connected entities.

e. He had sold his shares on floor of market in bonafide manner and had no idea who

bought the same. He has no connection of whatsoever nature with counterparties of his

sale transactions, Dhyana Group or exit providers and other preferential allottees

mentioned in Interim order. He also does not have any connection with said Mr. Ravi

Makwana, M/s Shubh Investment and any other telecom operators, telemarketers and

aggregators i.e. DD-BSE Bull, VM-BSE Bull, DM-BSE Bull, AM-BSE Bull, VM-StAxis,

BH-StAxis, BH-StAxis, MD-TRFID, VM-HBJCAP who had sent bulk SMS on and

around 27.07.2015 to investors allegedly luring them to trade in scrip of Dhyana.

f. BSE would have obtained requisite disclosures and carried out adequate due-diligence

before granting permission of listing new securities of Dhyana.

g. Except for price paid for application of preference share of Dhyana, he has no other

financial relationship with Dhyana Company or any other entity named therein.

h. The Interim order against him be vacated at the earliest. The order has been issued ex

parte without any prior communication, notice, letter or any correspondence seeking his

explanation or clarification on the subject matter. Thus, Order is in gross violation of

the basic principles natural justice viz. 'audi alteram partem'.

i. In this regard, he would like to draw attention to following judicial pronouncements:

I. In the case of Painter v. Liverpool Oil Gas Light Co.

It was held that "A party is not to suffer in person or in purse without an opportunity of being heard.

Order in the matter of Dhyana Finstock Limited Page 20 of 36

II. In State of AP vs. Nagam Chandrashekhara Lingam and Asst. Collector of Customs

& Ors vs. Bibhuti Bhushan Bagh & Anr

'Hon'ble Supreme Court of India held that a right of hearing would become an

empty formality without a notice and issuance of a notice can be treated as

being a part of fair procedure as envisaged under the Article 14, 19 and 21 of

Constitution of India.

j. A unilateral open ended coercive action is taken against him whereby he has been

debarred for an uncertain period. Further, without any specific direction contained

therein, the depositories have immediately frozen his demat account even though SEBI

itself has given him 21 days time to file his objections in the aforesaid matter. Such an

open ended restraint order against him is in breach of fundamental right of carrying on

business bestowed upon every citizen under Article 19 (g) of the 'Constitution of India'.

k. As a consequence of Interim order his demat account has been frozen and SEBI has acted

beyond its scope and purview and power assigned to it and transgressed the power

delegated to it by Parliament of India.

l. SEBI has attached his demat accounts without the approval of Judicial Magistrate as

required under the provisions of section 11 (4) (e) of the SEBI Act which mandates

such approval for all accounts including a bank accounts as well as demat accounts.

m. He denies alleged violation of provisions of Section 12 A (a),(b) & (c) of SEBI Act,

1992 and Regulation 3 (a),(b),(c),(d) r/w Regulations 4(1), 4 (2) (a),(b),(e),(g) and (r) of

SEBI (PFUTP) Regulations, 2003.

n. He requested that until passing of Final Order by SEBI, SEBI ought to grant him

certain interim reliefs so as to avoid erosion of value of securities, maintain some

investment avenue in Capital Market and address need for meetings funds for

business/other exigencies. In view of the same, he may be permitted:

To sell shares & securities held in his demat account and utilize sale proceeds.

To liquidate and redeem units of mutual funds and utilize the proceeds.

To buy, sell and deal in shares and securities, except in the shares of Dhyana.

To subscribe to units of mutual funds, including SIP, and redeem the units of

mutual funds so subscribed.

To avail benefits of corporate actions like rights issue, bonus issue, stock split,

dividend and so on.

o. Further, he also requested that:

Order in the matter of Dhyana Finstock Limited Page 21 of 36

The Interim order against him be vacated, directions qua him be revoked and he

may be discharged at the earliest.

The investigation in the matter be concluded within a reasonable period of time

of about 3-6 months and consequently final order be passed within 3 months

thereof after providing him an opportunity of being heard.

Alternatively:

(a) He may be provided with complete set of relevant documents referred

to and relied upon by SEBI while passing the Interim order;

(b) He may be granted Interim Relief(s), as prayed hereinabove, pending

investigation and passing of Final Order by SEBI.

Azim Farooq Hawa, Farooq Kasam Hawa, Zahir Farooq Hawa and Noorbanu Farooq

Hawa (Mr. Azim Farooq Hawa appeared along with Mr. Joby Mathew, Advocate and

Ms. Harshada Nagore, Advocate):

a. The entities deny all the allegations and findings made against them in the said order.

b. SEBI did not seek their explanations to the serious and unfounded allegations made

against them and therefore, have failed to consider all relevant facts and records and on

this ground alone, the said order and the directions therein ought to be withdrawn

against them immediately.

c. They are a family engaged in the business of trading and manufacturing engineering

goods.

d. In and around October 2013, Rashmee B. Shah who is a proprietor of Rashmee

Associates (Chartered Accountants) and Rashmikant B. Acharya, proprietor of R. B.

Acharya & co. (Tax Consultants), who was the Statutory Auditor/Tax Consultant to

Fluidline Valves Co. Pvt. Ltd suggested that investments by the aforesaid members of

our family, which were mostly in Mutual Funds were yielding inadequate returns and

recommended that they make some investments in equity markets. They both suggested

that they invest a relatively small amount (around Rs.20-25 Lakhs) in an. upcoming

preferential issue by DFL. They also told them that the shares of the Company were

listed on the Ahmedabad Stock Exchange and were expected to get listed on the BSE;

thereafter, the shares were expected to fetch a good price. They valued the advice given

by Rashmi Shah and Rashmikant Acharya; decided to spare Rs.20 Lakhs for investment

in the preferential allotment and followed the procedure for making an application for

the said preferential issue. They were allotted 50,000 shares each for a total amount of

Rs.20 Lakhs.

Order in the matter of Dhyana Finstock Limited Page 22 of 36

e. They made application for preferential allotment of shares to DFL on the

recommendation of Rashmi Shah and Rashmikant Acharya. Further, they do not have

any connection with the Company or its promoters.

f. They subscribed to the preferential issue of shares by the Company using funds that

were accounted for in the income tax returns filed by them from time to time; the profit

that they made from the sale of the shares allotted to them has also been duly accounted

for and tax paid on the same as required under the existing tax laws.

g. The shares allotted to them by the Company in the preferential allotment were under

lock-in for a period of 1 year. By the time the lock in on the shares was released, they

found that the price had increased substantially and therefore, as a commercially

prudent measure, they sold most of the shares on the BSE during the period December

2014 and January 2015.

h. However, instead of seeking any explanation from them, SEBI has passed drastic

directions effectively prohibiting them from accessing or using any of their investments

besides harming their reputation. This is most unfair and arbitrary and on this ground

also, they request that the directions against them in the said order may be withdrawn.

i. They are neither privy to the complaints filed by various investors regarding the trades

in the shares of DFL on the BSE on July 27, 2015 nor aware of the SMSs received by

such complainants.

j. They are not concerned with the pay-out relating to the trades on July 27, 2015 since

they did not buy or sell the shares of the Company on that day.

k. They submit that from the perspective of an investor, reasons for the increase in price

may not be as important as the rise in price itself. Even assuming that the price rise was

not justified by the fundamentals of the company or in the absence of any favorable

news, they cannot be faulted for selling their shares to take advantage of the same.

Moreover, it is erroneous to assume that they knew about the reasons for the abnormal

rise in price merely because they sold the shares allotted to them when the price was

rising. In fact, it would have been suspicious if they had not sold any shares under such

favorable market conditions.

l. Neither they trade in the shares of the Company on July 27, 2015 nor they neither

received the SMSs nor sent out the same. It is pertinent to note that they are not and

they should not be held to be part of the said alleged "Dhyana Group".

Order in the matter of Dhyana Finstock Limited Page 23 of 36

m. Out of the 2,00,000 shares allotted to the four of them, they sold 1,79,000 shares; all

except Mr. Zahir Farooq Hawa sold 50,000 share each. Mr. Zahir Farooq Hawa sold

29,000 shares, retaining 21,000 shares.

n. The trading on the BSE is both automatic and anonymous and that therefore, the

identity of the counterpart to their trades would not be known to even the stock broker.

Therefore, the finding of SEBI that the Dhyana Group entities acted as buyers to their

sales is erroneous.

o. SEBI has not shown that the sell orders placed on their behalf by their broker-Pilot

Capital Private limited matched with the buy orders of the Dhyana Group. In the

absence of the same, the allegation that their trades were illegal or that the profit that

they made from the sale of shares legally allotted to them was illegitimate, is erroneous

and false. Furthermore, it is erroneous to hold that their profit was not legitimate merely

because the fundamentals of the Company did not justify the prevailing price in the

market when they sold the shares.

p. They are not concerned with the members of the Dhyana Group or the inter se transfer

for funds between them; however, they deny that any of the entities mentioned in

paragraph 45 of the said order provided an exit to them as falsely alleged or otherwise.

q. While denying that they misused the stock exchange system to generate fictitious

LTCG, they submit that SEBI has not provided any particulars of the same. No details

of their purported unaccounted income or the manner and method of its conversion to

accounted income through the subscription and subsequent sale of shares of the

Company are set out. In the absence of such details, it is not established that the profit

or LTCG made by them is fictitious or illegal. In fact, their profits are from trades done

on the stock market and legitimate.

r. They merely subscribed to the preferential allotment of shares of the Company and

were in no way connected to the promoters or management. Therefore, they were not

involved in the listing of the shares of the Company on the BSE and cannot comment

on whether the listing price of Rs.251/- per share was justified or not. However, to the

best of their understanding, the price of the share on listing is determined by a

combination of factors including the demand and supply in the market.

s. The increased price and volume are some of the important commercial considerations

that encouraged them to sell the shares allotted to us by the Company. At that time, the

Order in the matter of Dhyana Finstock Limited Page 24 of 36

cause of the price and volume increase was not known to them and in any case, the

same would not have been a reason to refrain from sale of our shares.

t. They are not concerned with the transfer of funds between entities connected to the

Dhyana Group or between them and the said alleged "exit providers".

u. They are not concerned with the SMSs which were circulated among investors since

they did not receive or send the same and they were not aware of the same until they

read the said order. Moreover, they did not trade in the shares of the Company on July

27, 2015.

v. They also submit that SEBI has erred in imposing restraints on them from accessing the

securities market and from buying, selling or otherwise dealing in securities without

seeking an explanation from them regarding their dealings in the shares of the Company

and without completing their investigation.

w. At the time of the preferential allotment, the scrip was not traded on the BSE and there

was very little liquidity on the ASE; therefore, the finding that they could have bought in

the secondary market and waited for a year before selling the shares to avail of the

benefits of LTCG is erroneous and misplaced.

x. In the light of the above, they deny that they acted fraudulently and/or that they

violated the provisions of Regulations 3 and 4 of the Securities and Exchange Board of

India (Prohibition of Fraudulent and Unfair Trade Practices Relating to the Securities

Market) Regulations, 2003 and/or the provisions of Section 12A of the Securities and

Exchange Board of India Act, 1992, as falsely alleged or otherwise.

y. Substantial damage has been done to their reputations and financial condition, which

cannot be reversed or compensated when SEBI finds that they were not part of the

fraudulent scheme allegedly carried out by the Dhyana Group and others acting

together with them.

z. In the light of the above submissions, they request that they may be discharged from the

present proceedings that the directions restraining them from accessing the securities

market and buying, selling or otherwise dealing in securities, directly or indirectly, may

be withdrawn qua them and an order may be passed accordingly.

7. I have considered the allegations levelled against the Noticees in the interim order, their

replies/written submissions and other material on record. I note that in the instant case, the

directions issued against the Noticees are interim in nature and have been issued on the basis

Order in the matter of Dhyana Finstock Limited Page 25 of 36

of prima facie findings. SEBI had issued directions vide the interim order in the matter in order

to protect the interests of investors in the securities market. Detailed investigation in the

matter is still in progress. Thus, the issue for consideration at this stage is whether the interim

directions, issued against the Noticees vide the interim order, need to be confirmed, vacated

or modified in any manner, during pendency of investigation in the matter. It is noted that

the Noticees have not disputed the facts relating to preferential allotments and the trading

in the scrip, as alleged in the interim order.

8. Before dealing with replies/submissions of the Noticees on merit I deem it necessary to deal

with preliminary and common contentions raised by some of the Noticees. The first such

contention is that the interim order has been passed in complete disregard of the principles of

natural justice in as much as no opportunity of hearing was provided to the Noticees In this

regard, I note that the interim order has been passed on the basis of prima facie findings

observed during the preliminary examination/inquiry undertaken by SEBI. The facts,

circumstances and the reasons necessitating issuance of directions by the interim order have

been examined and dealt with in the said interim order. The interim order has also been issued in

the nature of a show cause notice affording the Noticees a post decisional opportunity of

hearing. I also note that the power of SEBI to pass interim orders flows from sections 11 and

11B of the SEBI Act which empower SEBI to pass appropriate directions in the interests of

investors or securities market, pending investigation or inquiry or on completion of such

investigation or inquiry. While passing such directions, it is not always necessary for SEBI to

provide the entity with an opportunity of pre-decisional hearing. The law with regard to

doing away with the requirement of pre-decisional hearing in certain situations is also well

settled. The following findings of the Hon'ble Supreme Court of India in the matter of

Liberty Oil Mills & Others Vs Union Of India & Other (1984) 3 SCC 465 are noteworthy:-

"It may not even be necessary in some situations to issue such notices but it would be sufficient but

obligatory to consider any representation that may be made by the aggrieved person and that would

satisfy the requirements of procedural fairness and natural justice. There can be no tape-measure of the

extent of natural justice. It may and indeed it must vary from statute to statute, situation to situation

and case to case. Again, it is necessary to say that pre-decisional natural justice is not usually

contemplated when the decisions taken are of an interim nature pending investigation or enquiry. Ad-

interim orders may always be made ex-parte and such orders may themselves provide for an opportunity

to the aggrieved party to be heard at a later stage. Even if the interim orders do not make provision for

such an opportunity, an aggrieved party have, nevertheless, always the right to make appropriate

representation seeking a review of the order and asking the authority to rescind or modify the order. The

principles of natural justice would be satisfied if the aggrieved party is given an opportunity at the

request. "

Order in the matter of Dhyana Finstock Limited Page 26 of 36

9. Thus, considering the facts and circumstances of a particular case, an ad-interim ex-parte order

may be passed by SEBI in the interests of investors or the securities market. It is pertinent to

note that the interim order in the present case was passed under the provisions of sections

11(1), 11(4) and 11B of the SEBI Act. The second proviso to section 11(4) clearly provides

that "Provided further that the Board shall, either before or after passing such orders, give an opportunity of

hearing to such intermediaries or persons concerned". Further, various Courts, while considering the

aforesaid sections of the SEBI Act have also held that principles of natural justice will not be

violated if an interim order is passed and a post-decisional hearing is provided to the affected

entity. In this regard, the Hon'ble Bombay High Court in the matter of Anand Rathi & Others

Vs. SEBI (2002) 2 Bom CR 403, has held as under:

"It is thus clearly seen that pre decisional natural justice is not always necessary when ad-interim orders

are made pending investigation or enquiry, unless so provided by the statute and rules of natural justice

would be satisfied if the affected party is given post decisional hearing. It is not that natural justice is not

attracted when the orders of suspension or like orders of interim nature are made. The distinction is that

it is not always necessary to grant prior opportunity of hearing when ad-interim orders are made and

principles of natural justice will be satisfied if post decisional hearing is given if demanded. Thus, it is a

settled position that while ex parte interim orders may always be made without a pre decisional

opportunity or without the order itself providing for a post decisional opportunity, the principles of natural

justice which are never excluded will be satisfied if a post decisional opportunity is given, if demanded."

10. Further, the Hon'ble High Court of Judicature of Rajasthan at Jaipur in the matter of M/s.

Avon Realcon Pvt. Ltd. & Ors Vs. Union of India & Ors (D.B. Civil WP No. 5135/2010 Raj

HC) has held that:

“…Perusal of the provisions of Sections 11(4) & 11(B) shows that the Board is given powers to take

few measures either pending investigation or enquiry or on its completion. The Second Proviso to Section

11, however, makes it clear that either before or after passing of the orders, intermediaries or persons

concerned would be given opportunity of hearing. In the light of aforesaid, it cannot be said that there is

absolute elimination of the principles of natural justice. Even if, the facts of this case are looked into, after

passing the impugned order, petitioners were called upon to submit their objections within a period of 21

days. This is to provide opportunity of hearing to the petitioners before final decision is taken. Hence, in

this case itself absolute elimination of principles of natural justice does not exist. The fact, however,

remains as to whether post-decisional hearing can be a substitute for pre-decisional hearing. It is a settled

law that unless a statutory provision either specifically or by necessary implication excludes the application

of principles of natural justice, the requirement of giving reasonable opportunity exists before an order is

made. The case herein is that by statutory provision, principles of natural justice are adhered to after

orders are passed. This is to achieve the object of SEBI Act. Interim orders are passed by the Court,

Tribunal and Quasi Judicial Authority in given facts and circumstances of the case showing urgency or

Order in the matter of Dhyana Finstock Limited Page 27 of 36

emergent situation. This cannot be said to be elimination of the principles of natural justice or if ex-parte

orders are passed, then to say that objections thereupon would amount to post-decisional hearing. Second

Proviso to Section 11 of the SEBI Act provides adequate safeguards for adhering to the principles of

natural justice, which otherwise is a case herein also…"

11. I, therefore, note that interim order has not been passed in violation of principles of natural

justice as has been contended by the Noticees.

12. The Noticees have raised another contention that the power to issue directions under

section 11(4) and 11(B) is a drastic power having serious civil consequences and

ramifications on the repute and livelihood of those against whom it is directed. Said power

is not available for routine and retrospective application and cannot be used for penal action.

In this regard, I note that in this case the purpose of the interim order is to achieve the

objectives of investor protection and safeguarding the market integrity by enforcing the

provisions of the SEBI Act. In my view, section 11(1) of the SEBI Act casts the duty on

SEBI to protect the interests of the investors, promote development of and regulate the

securities market, “by such measures as it thinks fit”. Apart from this plenary power, section

11(2) of the SEBI Act enumerates illustrative list of measures that may be provided for by

SEBI in order to achieve its objective. One of the measures enumerated in section 11(2)(e) is

"prohibiting fraudulent and unfair trade practices relating to securities markets". The word 'measure' has

not been defined or explained under the SEBI Act. It is well settled position that this word

has to be understood in the sense in which it is generally understood in the context of the

powers conferred upon the concerned authority. From the provisions of section 11, it is

clear that the purpose of section 11(2)(e) of the SEBI Act is to prohibit all fraudulent and

unfair trade practices relating to the securities market and the Board may take any 'measures'

in order to achieve this purpose.

13. The 'measures' and the directions under sections 11 and 11B of the SEBI Act can be

taken/issued for prohibiting the fraudulent and unfair trade practices relating to securities

market and achieving the objective of investor protection, and promotion of and regulation

of the securities market. It is also pertinent to mention that the interim order has been passed

in the course of preliminary inquiry and the investigation in the matter is ongoing. Based on

the prima facie findings in the matter and in order to protect the interest of investors in the

securities market, SEBI had issued directions vide the interim order.

14. Another contention of the Noticees is that the open restraint order is in breach of their fundamental

right to carry on business under Article 19(1)(g) of the Constitution of India. In this regard, it is

noted that Article 19 (1) (g) guarantees to all citizens the right to practice any profession or to carry

on any occupation, trade or business. However, at the same time it is pertinent to mention that this

Order in the matter of Dhyana Finstock Limited Page 28 of 36

freedom is not uncontrolled as clause (6) of Article 19 authorises legislation which imposes

reasonable restrictions on this right in the interest of general public. It is a matter of common

knowledge that Securities and Exchange Board of India, 1992 is a special Act enacted by the

Parliament conferring on SEBI the duty to protect the interests of investors in securities and to

promote the development of, and to regulate the securities market, by such measures as it thinks fit.

In the present case, the restraint order has been passed by SEBI in exercise of the powers conferred

upon it by law and towards fulfilment of the duties cast under the SEBI Act. As noted in the interim

order, the conduct of the Noticees has been found to be prima facie fraudulent and the Noticees have

therefore been restrained from accessing the securities market and dealing in securities till further

directions. In view of the above, I find that the restraint order against the Noticee is not in violation