Embed Size (px)

Citation preview

Azure InternationalTechnology & Development (Beijing) Limited

Sebastian Meyer Director, Research & Advisory

WTG Production and Installation volumes in China during 2008 -

2011

-

Chinese WTG industry to impact global market?

Presented at Global Wind Power 200830 October 2008

Sebastian Meyer Azure International Slide 2 of 26

Azure International -

About us

A specialized advisory and investment firm dedicated to the commercialization of clean, sustainable energy technologies that are commercially viable and have significant market potential in China

- “Tracker”

and advisory services covering market intelligence and commercial/financial due diligence in the China wind industry including project development and WTG and component manufacturing.

- Bespoke consulting services covering industry research, market intelligence, due diligence, industry monitoring.

Developer of sustainable energy projects in China, with focus on wind, biofuels, waste to energy and coal gasification

- Management capacity in engineering, energy development, project management, marketing & PR, strategic planning, knowledge transfer, domestic and international project and equity finance

- Broad experience within the energy industry, with a focus on new, cleaner energy technologies

- Hands-on knowledge and extensive professional experience in the Chinese, European and North American markets

Sebastian Meyer Azure International Slide 3 of 26

Presentation overview

Demand- Activity update- Economy / Power Sector & RPS- Operating track record - Supply

AnalysisConclusion

Will the domestic Chinese wind market to affect the global WTG market? –

Update Oct 2008

Sebastian Meyer Azure International Slide 4 of 26

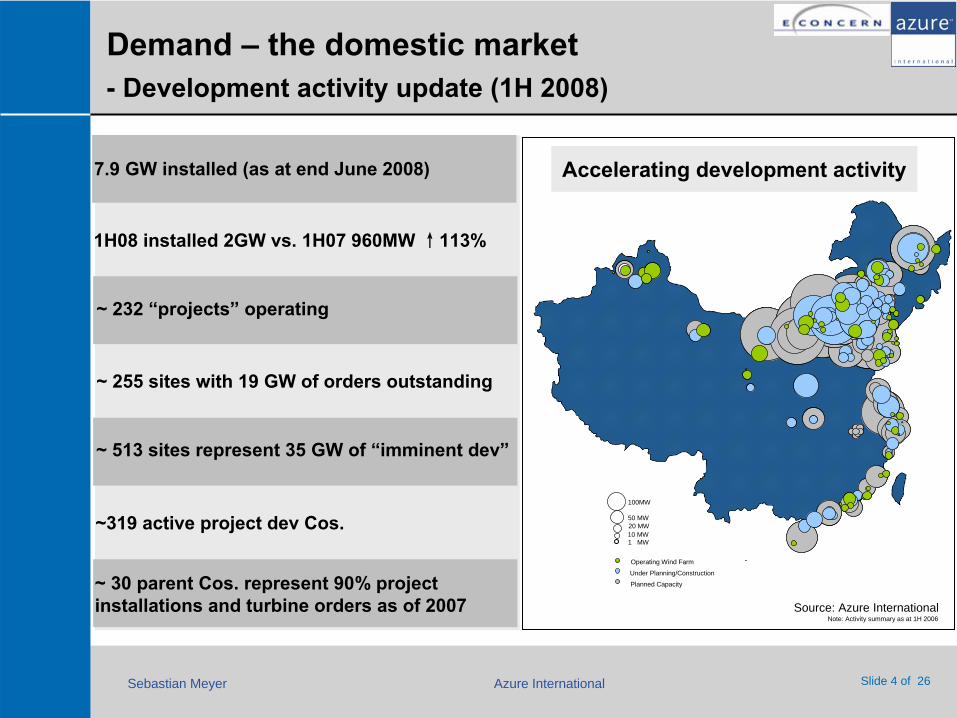

Demand –

the domestic market -

Development activity update (1H 2008)

Source: Azure International

163

100MW

50 MW20 MW10 MW1 MW

Operating Wind Farm

Under Planning/Construction

Planned Capacity

163163

1H08 installed 2GW vs. 1H07 960MW ↑113%

~ 30 parent Cos. represent 90% project installations and turbine orders as of 2007

Accelerating development activity

~319 active project dev Cos.

Note: Activity summary as at 1H 2006

~ 232 “projects”

operating

~ 255 sites with 19 GW of orders outstanding

~ 513 sites represent 35 GW of “imminent dev”

7.9 GW installed (as at end June 2008)

Sebastian Meyer Azure International Slide 5 of 26

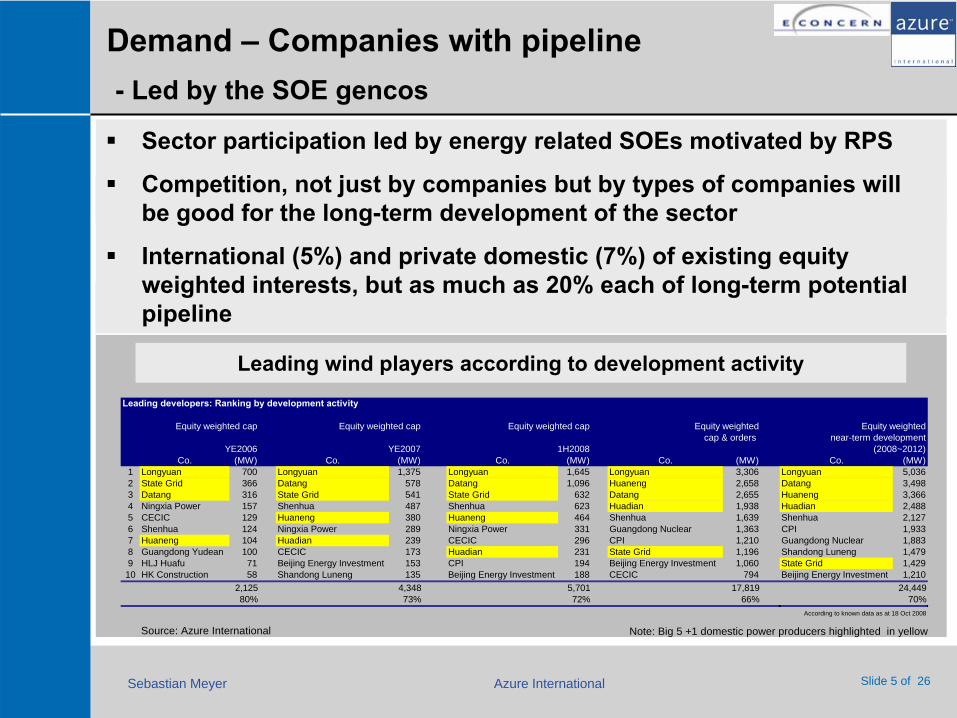

Demand –

Companies with pipeline -

Led by the SOE gencos

Source: Azure International

Leading wind players according to development activity

Sector participation led by energy related SOEs motivated by RPS

Competition, not just by companies but by types of companies will be good for the long-term development of the sector

International (5%) and private domestic (7%) of existing equity weighted interests, but as much as 20% each of long-term potential pipeline

Note: Big 5 +1 domestic power producers highlighted in yellow

Leading developers: Ranking by development activity

Equity weighted cap Equity weighted cap Equity weighted cap Equity weighted Equity weightedcap & orders near-term development

YE2006 YE2007 1H2008 (2008~2012)Co. (MW) Co. (MW) Co. (MW) Co. (MW) Co. (MW)

1 Longyuan 700 Longyuan 1,375 Longyuan 1,645 Longyuan 3,306 Longyuan 5,0362 State Grid 366 Datang 578 Datang 1,096 Huaneng 2,658 Datang 3,4983 Datang 316 State Grid 541 State Grid 632 Datang 2,655 Huaneng 3,3664 Ningxia Power 157 Shenhua 487 Shenhua 623 Huadian 1,938 Huadian 2,4885 CECIC 129 Huaneng 380 Huaneng 464 Shenhua 1,639 Shenhua 2,1276 Shenhua 124 Ningxia Power 289 Ningxia Power 331 Guangdong Nuclear 1,363 CPI 1,9337 Huaneng 104 Huadian 239 CECIC 296 CPI 1,210 Guangdong Nuclear 1,8838 Guangdong Yudean 100 CECIC 173 Huadian 231 State Grid 1,196 Shandong Luneng 1,4799 HLJ Huafu 71 Beijing Energy Investment 153 CPI 194 Beijing Energy Investment 1,060 State Grid 1,42910 HK Construction 58 Shandong Luneng 135 Beijing Energy Investment 188 CECIC 794 Beijing Energy Investment 1,210

2,125 4,348 5,701 17,819 24,44980% 73% 72% 66% 70%

According to known data as at 18 Oct 2008

Sebastian Meyer Azure International Slide 6 of 26

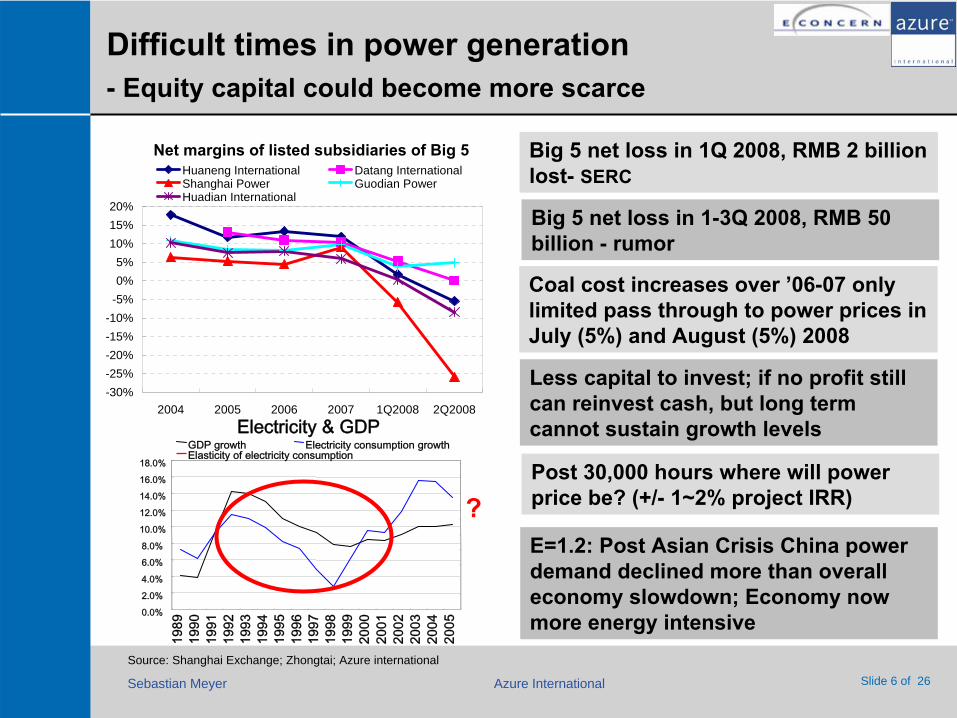

Difficult times in power generation -

Equity capital could become more scarce

Big 5 net loss in 1Q 2008, RMB 2 billion lost-

SERC

E=1.2:

Post Asian Crisis China power demand declined more than overall economy slowdown; Economy now more energy intensive

Coal cost increases over ’06-07 only limited pass through to power prices in July (5%) and August (5%) 2008

Less capital to invest; if no profit still can reinvest cash, but long term cannot sustain growth levels

Post 30,000 hours where will power price be? (+/-

1~2% project IRR)

Source: Shanghai Exchange; Zhongtai; Azure international

Electricity & GDP

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

GDP growth Electricity consumption growthElasticity of electricity consumption

?

Net margins of listed subsidiaries of Big 5

-30%-25%-20%-15%-10%

-5%0%5%

10%15%20%

2004 2005 2006 2007 1Q2008 2Q2008

Huaneng International Datang InternationalShanghai Power Guodian PowerHuadian International

Big 5 net loss in 1-3Q 2008, RMB 50 billion -

rumor

Sebastian Meyer Azure International Slide 7 of 26

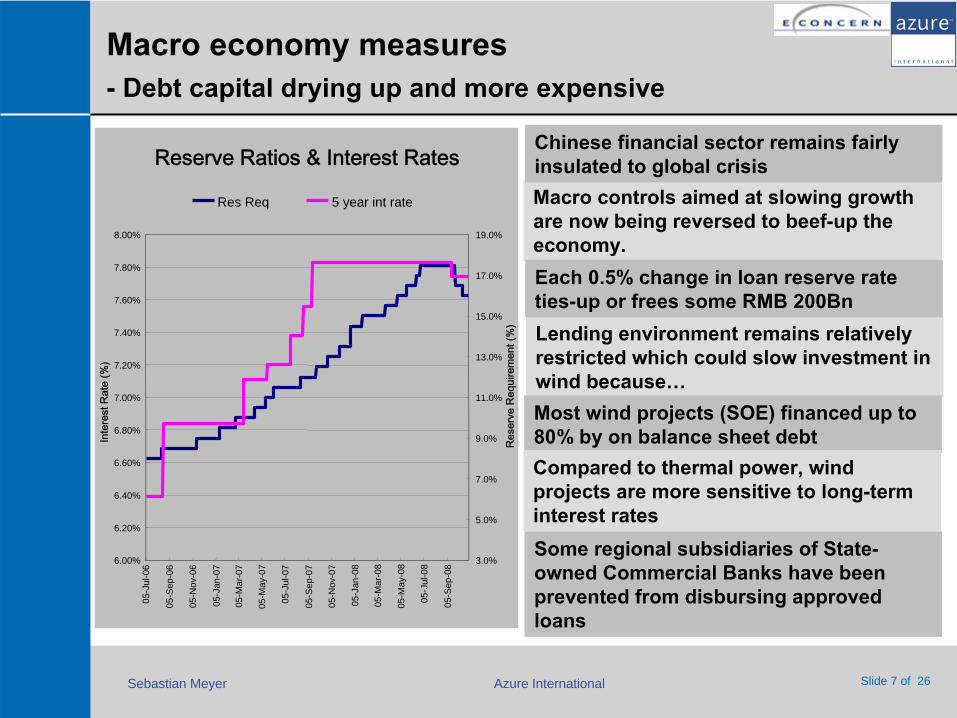

Macro economy measures -

Debt capital drying up and more expensive

Macro controls aimed at slowing growth are now being reversed to beef-up the economy.

Lending environment remains relatively restricted which could slow investment in wind because…Most wind projects (SOE) financed up to 80% by on balance sheet debt

Some regional subsidiaries of State-

owned Commercial Banks have been prevented from disbursing approved loans

Each 0.5% change in loan reserve rate ties-up or frees some RMB 200Bn

Compared to thermal power, wind projects are more sensitive to long-term interest rates

Reserve Ratios & Interest Rates

6.00%

6.20%

6.40%

6.60%

6.80%

7.00%

7.20%

7.40%

7.60%

7.80%

8.00%

05-J

ul-0

6

05-S

ep-0

6

05-N

ov-0

6

05-J

an-0

7

05-M

ar-0

7

05-M

ay-0

7

05-J

ul-0

7

05-S

ep-0

7

05-N

ov-0

7

05-J

an-0

8

05-M

ar-0

8

05-M

ay-0

8

05-J

ul-0

8

05-S

ep-0

8

Inte

rest

Rat

e (%

)

3.0%

5.0%

7.0%

9.0%

11.0%

13.0%

15.0%

17.0%

19.0%

Res

erve

Req

uire

men

t (%

)

Res Req 5 year int rate

Chinese financial sector remains fairly insulated to global crisis

Sebastian Meyer Azure International Slide 8 of 26

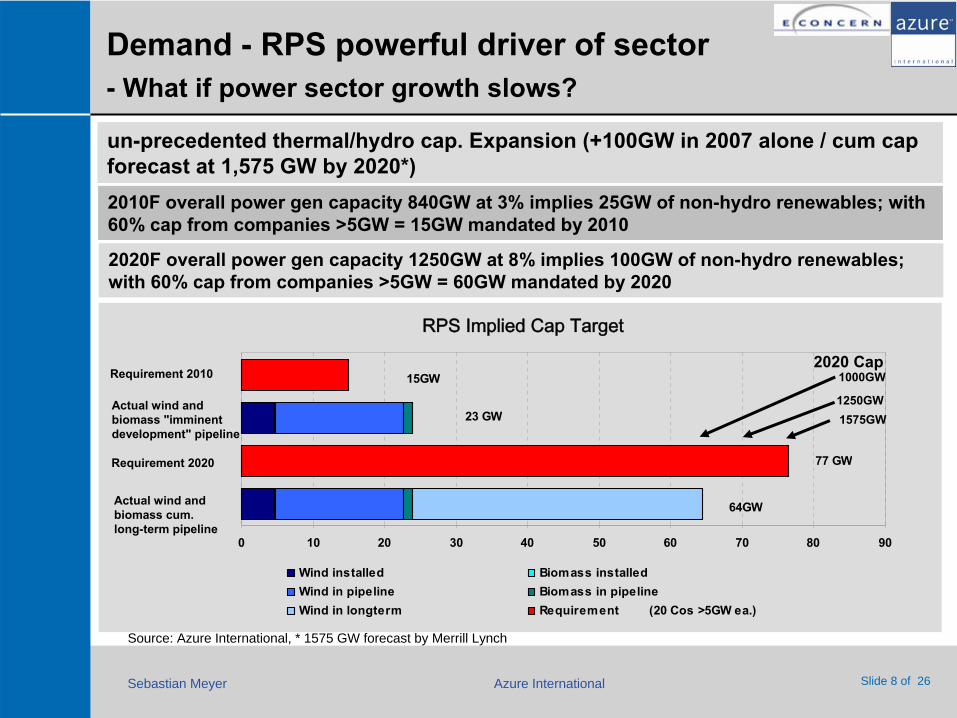

Demand -

RPS powerful driver of sector -

What if power sector growth slows?

2010F overall power gen capacity 840GW at 3% implies 25GW of non-hydro renewables; with 60% cap from companies >5GW = 15GW mandated by 2010

2020F overall power gen capacity

1250GW at 8% implies 100GW of non-hydro renewables;

with 60% cap from companies

>5GW = 60GW mandated by 2020

0 10 20 30 40 50 60 70 80 90

Wind installed Biomass installedWind in pipeline Biomass in pipelineWind in longterm Requirement (20 Cos >5GW ea.)

15GW

23 GW

77 GW

64GW

un-precedented

thermal/hydro cap. Expansion (+100GW in 2007 alone / cum cap forecast at 1,575 GW by 2020*)

RPS Implied Cap Target

Source: Azure International, * 1575 GW forecast by Merrill Lynch

2020 Cap

1575GW1250GW

1000GWRequirement 2010

Actual wind and biomass "imminent development" pipeline

Requirement 2020

Actual wind and biomass cum. long-term pipeline

Sebastian Meyer Azure International Slide 9 of 26

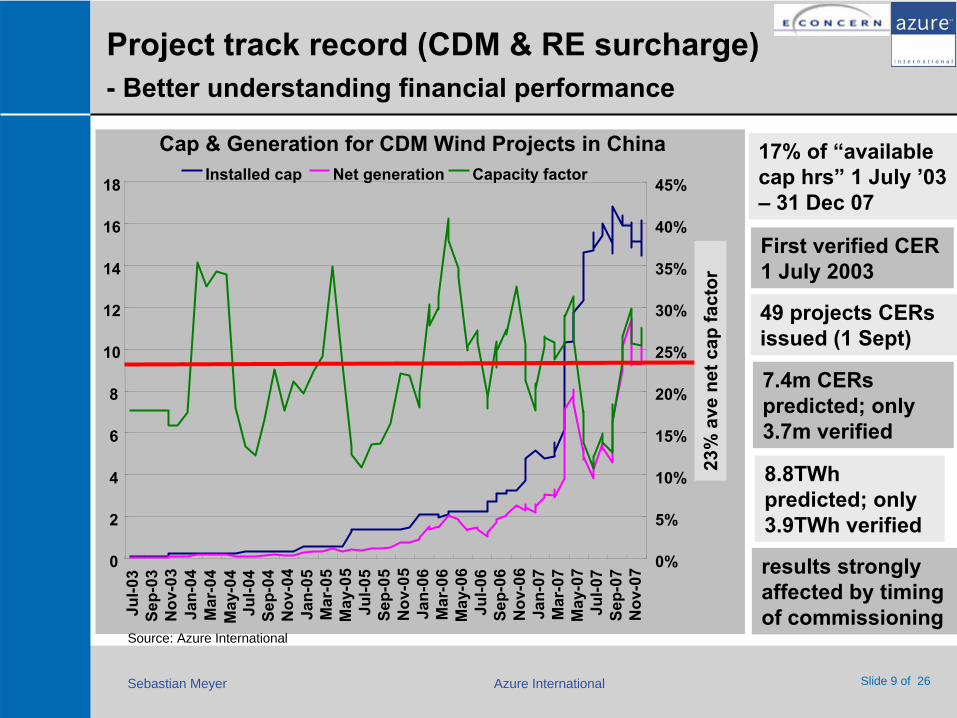

Project track record (CDM & RE surcharge) -

Better understanding financial performance

First verified CER 1 July 2003

7.4m CERs predicted; only

3.7m verified

49 projects CERs issued (1 Sept)

Source: Azure International

0

2

4

6

8

10

12

14

16

18

Jul-0

3Se

p-03

Nov

-03

Jan-

04M

ar-0

4M

ay-0

4Ju

l-04

Sep-

04N

ov-0

4Ja

n-05

Mar

-05

May

-05

Jul-0

5Se

p-05

Nov

-05

Jan-

06M

ar-0

6M

ay-0

6Ju

l-06

Sep-

06N

ov-0

6Ja

n-07

Mar

-07

May

-07

Jul-0

7Se

p-07

Nov

-07 0%

5%

10%

15%

20%

25%

30%

35%

40%

45%Installed cap Net generation Capacity factor

Cap & Generation for CDM Wind Projects in China

results strongly affected by timing of commissioning

8.8TWh predicted;

only 3.9TWh

verified

23%

ave

net c

ap fa

ctor

17% of “available cap hrs”

1 July ’03 –

31 Dec 07

Sebastian Meyer Azure International Slide 10 of 26

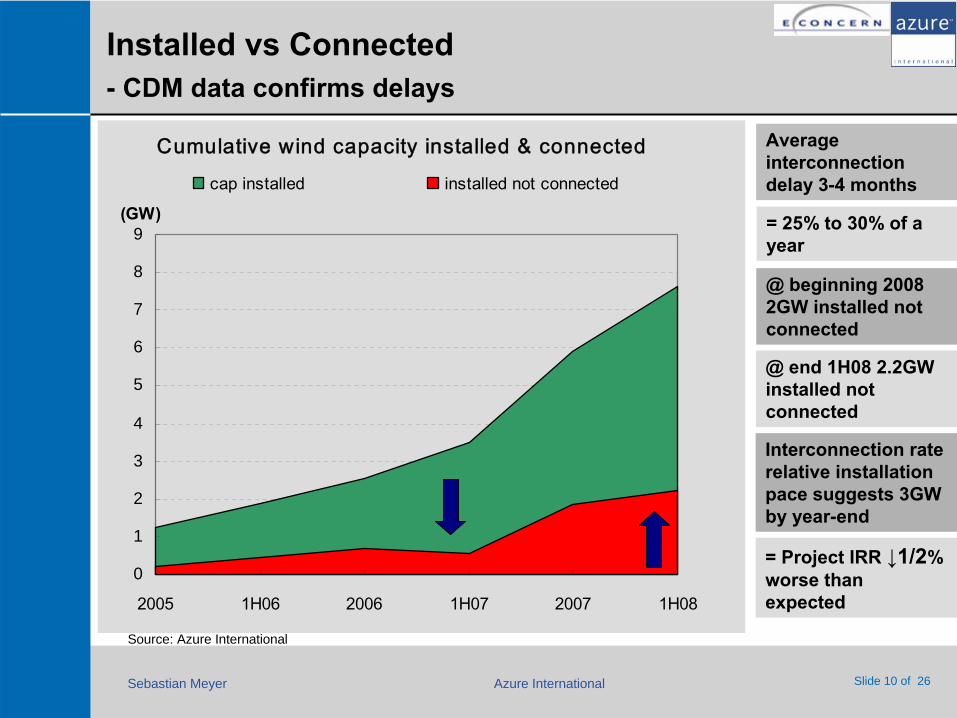

Installed vs Connected -

CDM data confirms delays

Average interconnection delay 3-4 months

= 25% to 30% of a year

@ beginning 2008 2GW installed not connected

@ end 1H08 2.2GW installed not connected

= Project IRR ↓1/2% worse than expected

Source: Azure International

Interconnection rate relative installation pace suggests 3GW by year-end

Cumulative wind capacity installed & connected

0

1

2

3

4

5

6

7

8

9

2005 1H06 2006 1H07 2007 1H08

(GW)

cap installed installed not connected

Sebastian Meyer Azure International Slide 11 of 26

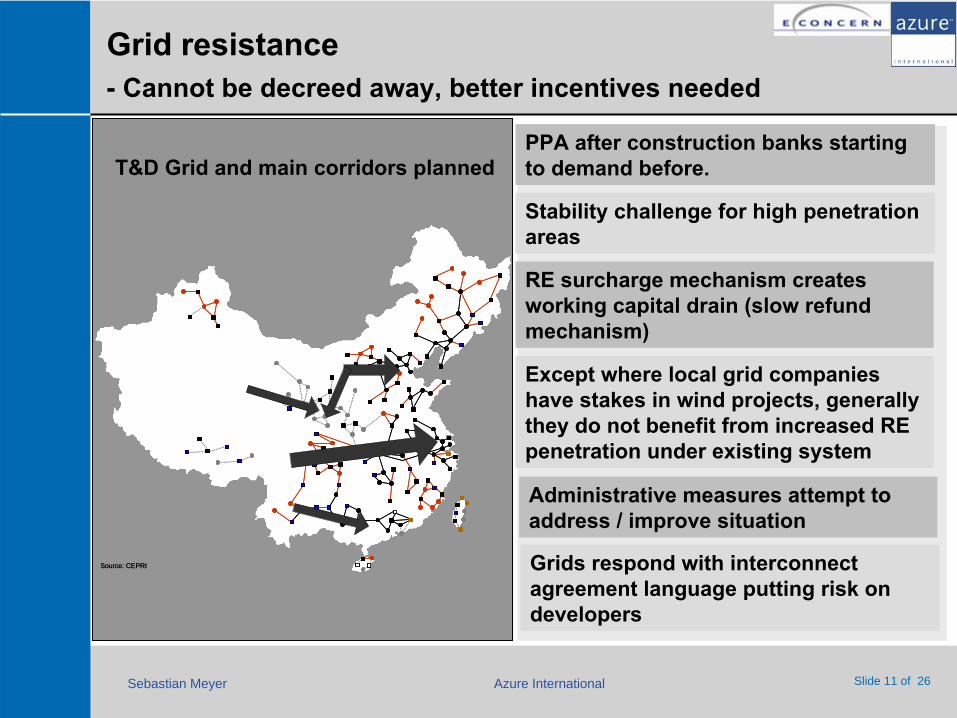

Grid resistance -

Cannot be decreed away, better incentives needed

PPA after construction banks starting to demand before.

RE surcharge mechanism creates working capital drain (slow refund mechanism)

Stability challenge for high penetration areas

Source: CEPRISource: CEPRI

T&D Grid and main corridors planned

Except where local grid companies have stakes in wind projects, generally they do not benefit from increased RE penetration under existing system

Administrative measures attempt to address / improve situation

Grids respond with interconnect agreement language putting risk on developers

Sebastian Meyer Azure International Slide 12 of 26

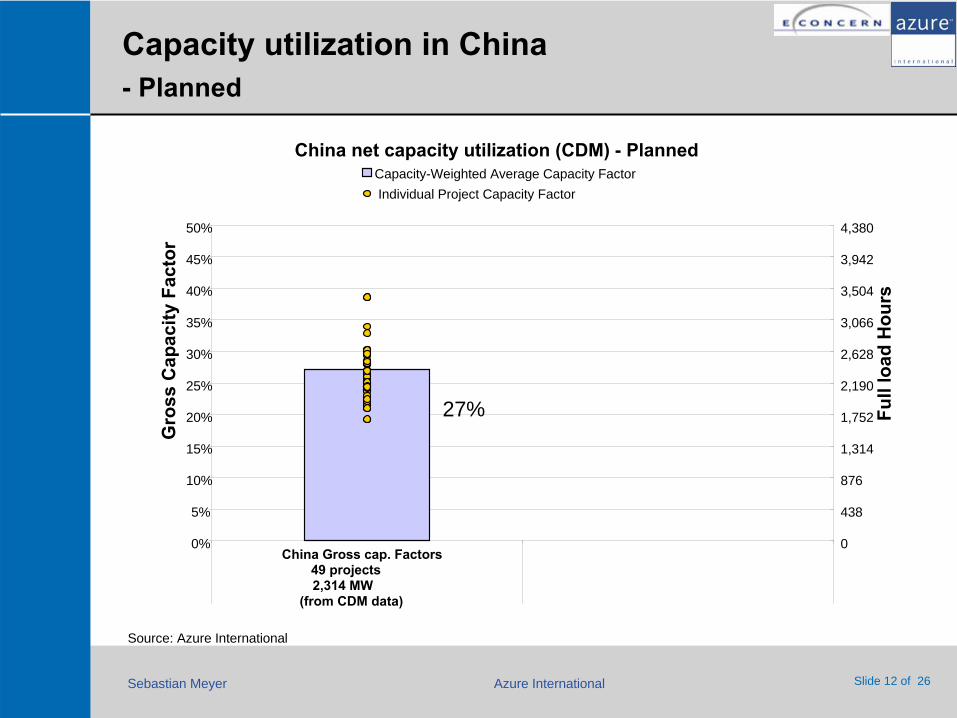

Capacity utilization in China - Planned

China net capacity utilization (CDM) -

Planned

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

China Gross cap. Factors49 projects2,314 MW

(from CDM data)

Gro

ss C

apac

ity F

acto

r

0

438

876

1,314

1,752

2,190

2,628

3,066

3,504

3,942

4,380

Full

load

Hou

rs

Capacity-Weighted Average Capacity FactorIndividual Project Capacity Factor

27%

Source: Azure International

Sebastian Meyer Azure International Slide 13 of 26

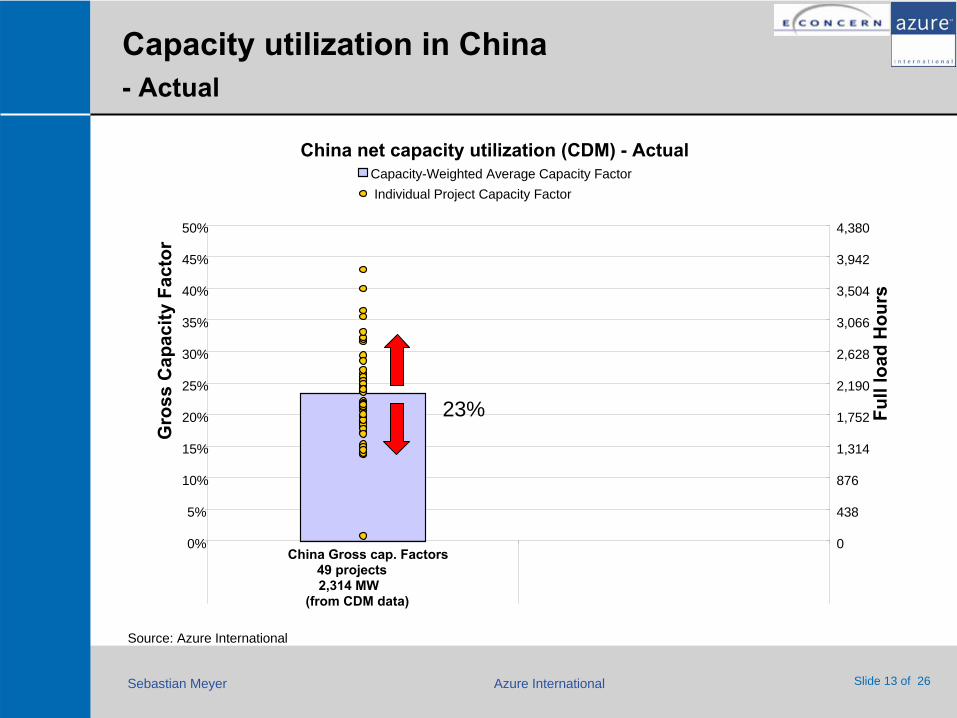

Capacity utilization in China - Actual

China net capacity utilization (CDM) -

Actual

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

China Gross cap. Factors49 projects2,314 MW

(from CDM data)

Gro

ss C

apac

ity F

acto

r

0

438

876

1,314

1,752

2,190

2,628

3,066

3,504

3,942

4,380

Full

load

Hou

rs

Capacity-Weighted Average Capacity FactorIndividual Project Capacity Factor

23%

Source: Azure International

Sebastian Meyer Azure International Slide 14 of 26

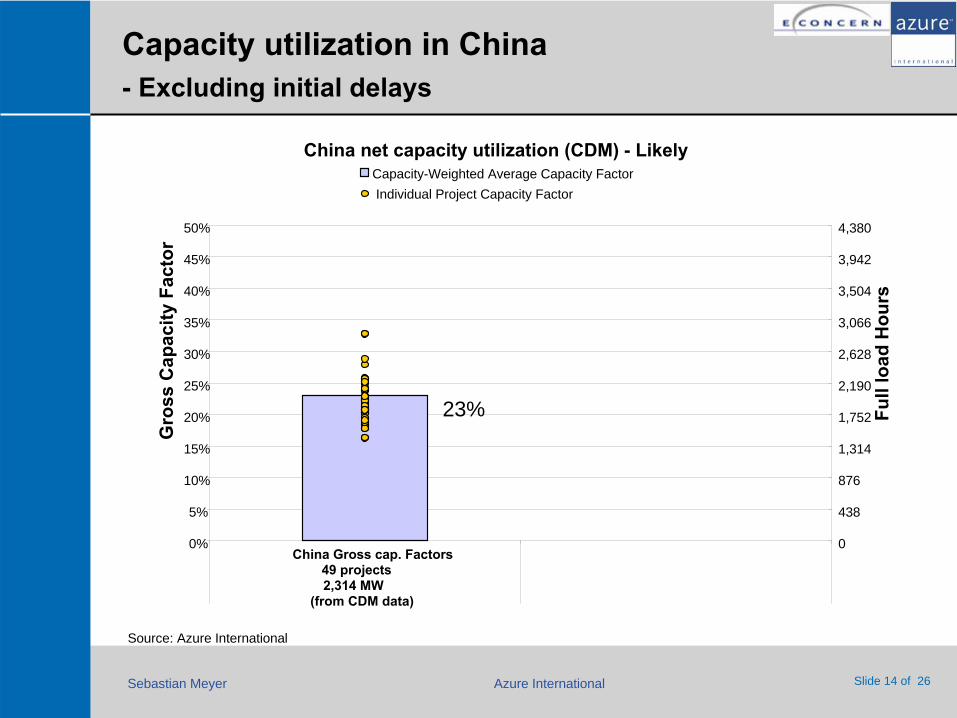

Capacity utilization in China -

Excluding initial delays

China net capacity utilization (CDM) -

Likely

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

China Gross cap. Factors49 projects2,314 MW

(from CDM data)

Gro

ss C

apac

ity F

acto

r

0

438

876

1,314

1,752

2,190

2,628

3,066

3,504

3,942

4,380

Full

load

Hou

rs

Capacity-Weighted Average Capacity FactorIndividual Project Capacity Factor

23%

Source: Azure International

Sebastian Meyer Azure International Slide 15 of 26

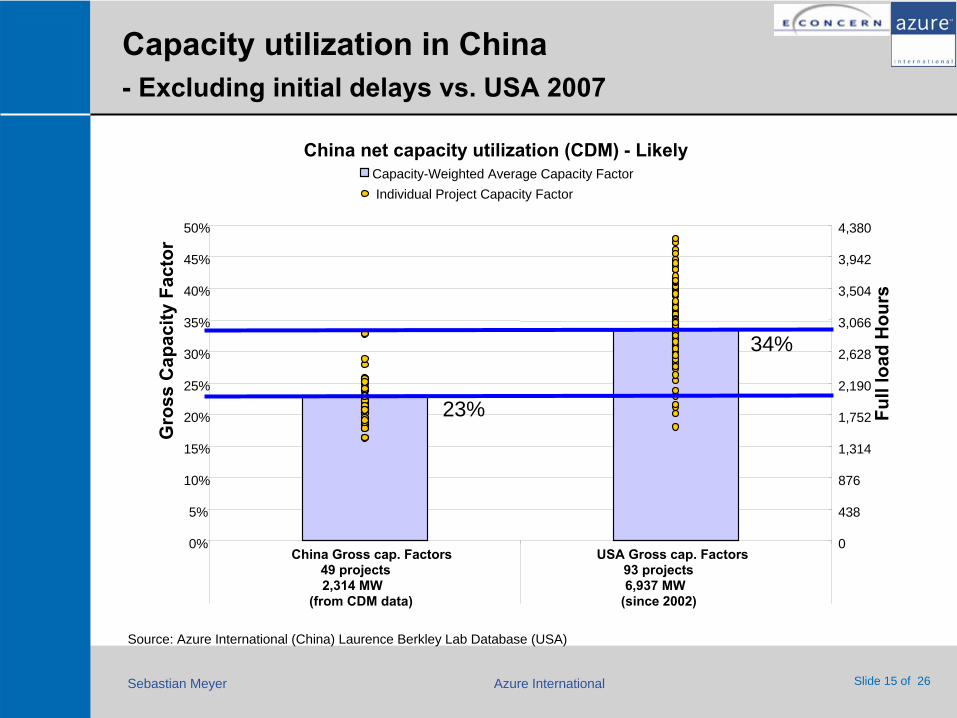

Capacity utilization in China -

Excluding initial delays vs. USA 2007

23%

34%

China net capacity utilization (CDM) -

Likely

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

China Gross cap. Factors USA Gross cap. Factors49 projects 93 projects2,314 MW 6,937 MW

(from CDM data) (since 2002)

Gro

ss C

apac

ity F

acto

r

0

438

876

1,314

1,752

2,190

2,628

3,066

3,504

3,942

4,380

Full

load

Hou

rs

Capacity-Weighted Average Capacity FactorIndividual Project Capacity Factor

Source: Azure International (China) Laurence Berkley Lab Database (USA)

Sebastian Meyer Azure International Slide 16 of 26

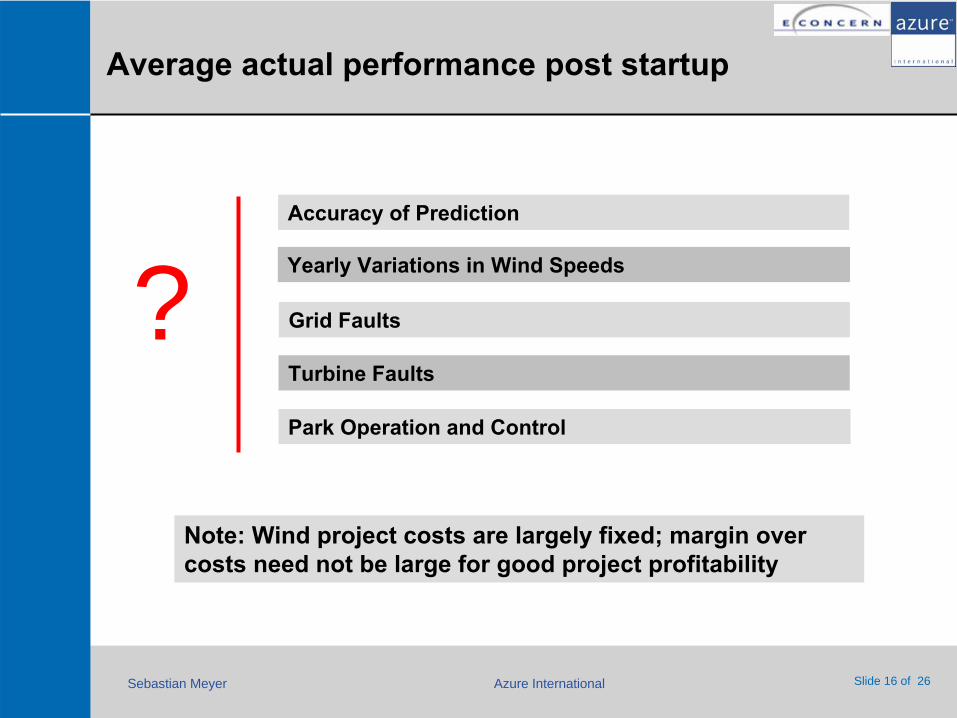

Average actual performance post startup

Accuracy of Prediction

Yearly Variations in Wind Speeds

Grid Faults

Turbine Faults

Park Operation and Control

?

Note: Wind project costs are largely fixed; margin over costs need not be large for good project profitability

Sebastian Meyer Azure International Slide 17 of 26

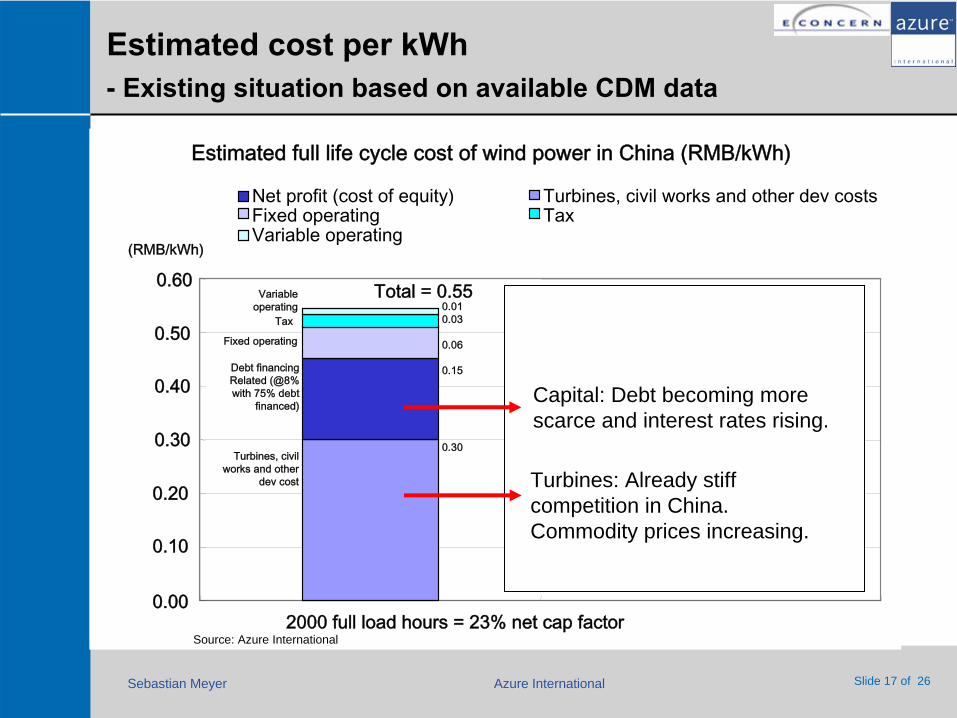

Estimated cost per kWh -

Existing situation based on available CDM data

Estimated full life cycle cost of wind power in China (RMB/kWh)

Turbines, civil works and other

dev cost

Variable operating

0.00

0.10

0.20

0.30

0.40

0.50

0.60

2000 full load hours = 23% net cap factor

(RMB/kWh)

Net profit (cost of equity) Turbines, civil works and other dev costsFixed operating TaxVariable operating

Tax

Fixed operating

Debt financing Related (@8% with 75% debt

financed)

Total = 0.550.010.03

0.06

0.15

0.30

Turbines: Already stiff competition in China. Commodity prices increasing.

Capital: Debt becoming more scarce and interest rates rising.

Source: Azure International

Sebastian Meyer Azure International Slide 18 of 26

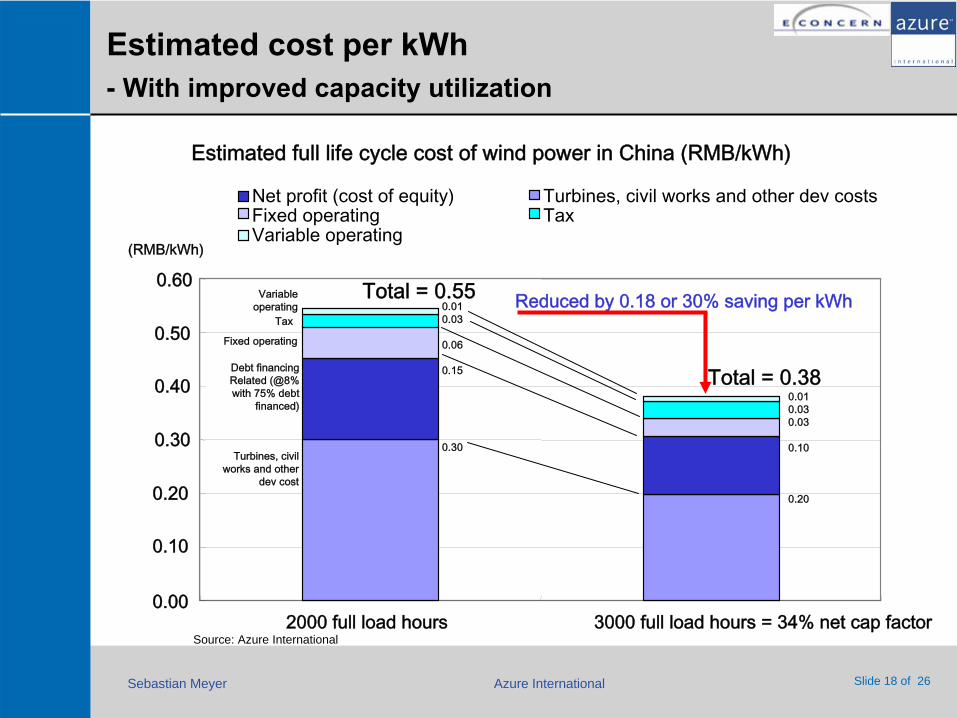

Estimated cost per kWh -

With improved capacity utilization

Estimated full life cycle cost of wind power in China (RMB/kWh)

Turbines, civil works and other

dev cost

Variable operating

0.00

0.10

0.20

0.30

0.40

0.50

0.60

2000 full load hours 3000 full load hours = 34% net cap factor

(RMB/kWh)

Net profit (cost of equity) Turbines, civil works and other dev costsFixed operating TaxVariable operating

Tax

Fixed operating

Debt financing Related (@8% with 75% debt

financed)

Total = 0.55

Total = 0.38

0.010.03

0.06

0.15

0.30

0.010.030.03

0.10

0.20

Reduced by 0.18 or 30% saving per kWh

Source: Azure International

Sebastian Meyer Azure International Slide 19 of 26

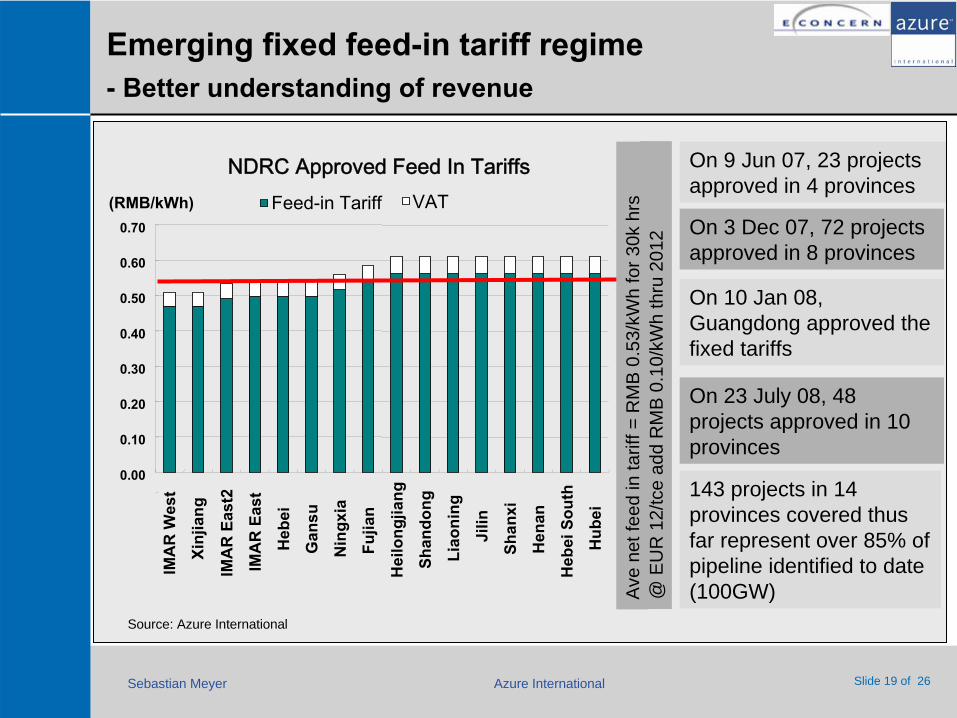

Emerging fixed feed-in tariff regime -

Better understanding of revenue

Source: Azure International

On 3 Dec 07, 72 projects approved in 8 provinces

On 9 Jun 07, 23 projects approved in 4 provinces

On 10 Jan 08, Guangdong approved the fixed tariffs

143 projects in 14 provinces covered thus far represent over 85% of pipeline identified to date (100GW)

On 23 July 08, 48 projects approved in 10 provinces

NDRC

Approved

Feed In Tariffs

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

IMA

R W

est

Xinj

iang

IMA

R E

ast2

IMA

R E

ast

Heb

ei

Gan

su

Nin

gxia

Fujia

n

Hei

long

jiang

Shan

dong

Liao

ning

Jilin

Shan

xi

Hen

an

Heb

ei S

outh

Hub

ei

(RMB/kWh) Feed-in Tariff VAT

Ave

net

feed

in ta

riff =

RM

B 0

.53/

kWh

for 3

0k h

rs@

EU

R 1

2/tc

e ad

d R

MB

0.1

0/kW

h th

ru 2

012

Sebastian Meyer Azure International Slide 20 of 26

`

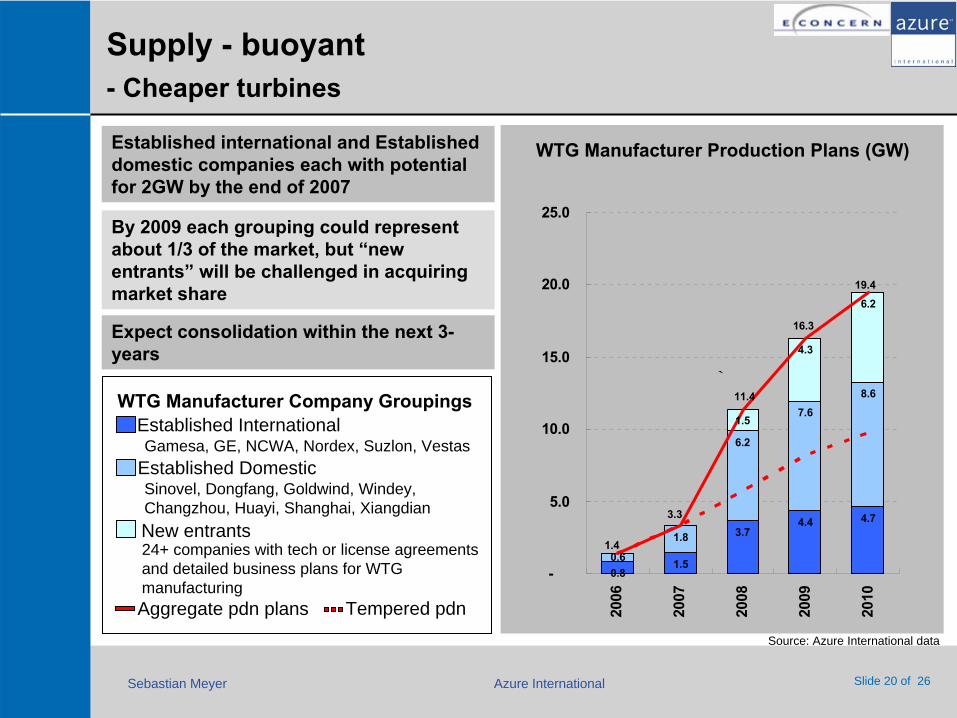

Supply -

buoyant -

Cheaper turbines

WTG Manufacturer Production Plans (GW)Established international and Established domestic companies each with potential for 2GW by the end of 2007

By 2009 each grouping could represent about 1/3 of the market, but “new entrants”

will be challenged in acquiring market share

Expect consolidation within the next 3-

years

24+ companies with tech or license agreements and detailed business plans for WTG manufacturing

Source: Azure International data

WTG Manufacturer Company Groupings

New entrants

Established Domestic

Established InternationalGamesa, GE, NCWA, Nordex, Suzlon, Vestas

Sinovel, Dongfang, Goldwind, Windey, Changzhou, Huayi, Shanghai, Xiangdian

Aggregate pdn plans Tempered pdn

0.81.5

3.74.4 4.7

1.8

6.2

7.68.6

1.5

4.3

6.2

0.6

19.4

16.3

11.4

3.3

1.4

-

5.0

10.0

15.0

20.0

25.0

2006

2007

2008

2009

2010

Sebastian Meyer Azure International Slide 21 of 26

`

Supply -

order backlog -

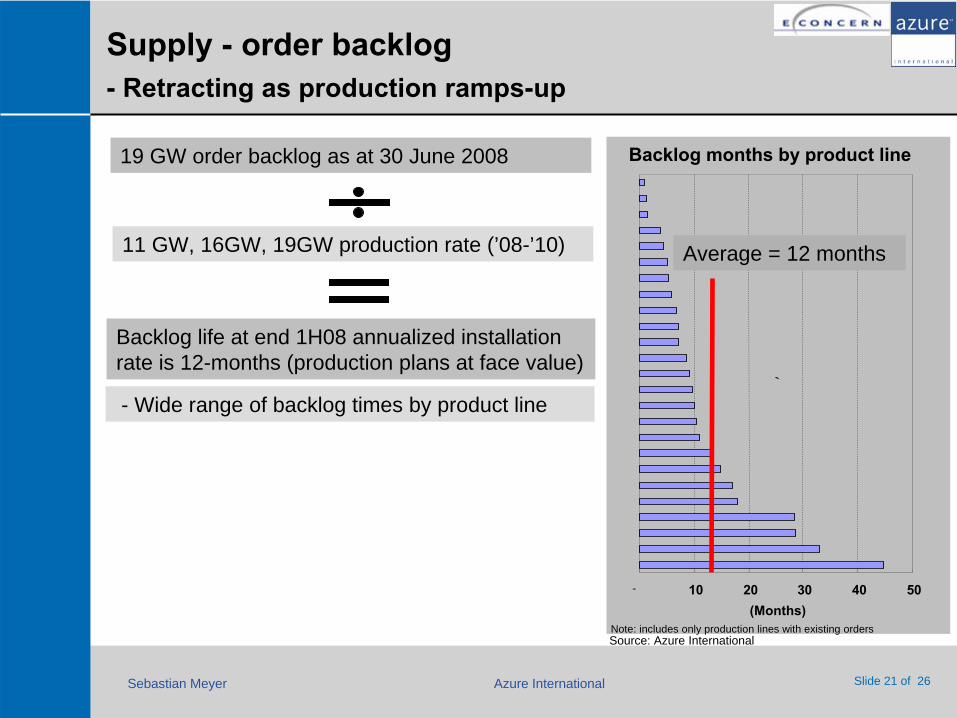

Retracting as production ramps-up

19 GW order backlog as at 30 June 2008

11 GW, 16GW, 19GW production rate (’08-’10)

Backlog life at end 1H08 annualized installation rate is 12-months (production plans at face value)

- Wide range of backlog times by product line

Note: includes only production lines with existing ordersSource: Azure International

Backlog months by product line

- 10 20 30 40 50(Months)

Average = 12 months

Sebastian Meyer Azure International Slide 22 of 26

Analysis -

near-term development foretold -

Pipelines of developers & ordered WTGs

`

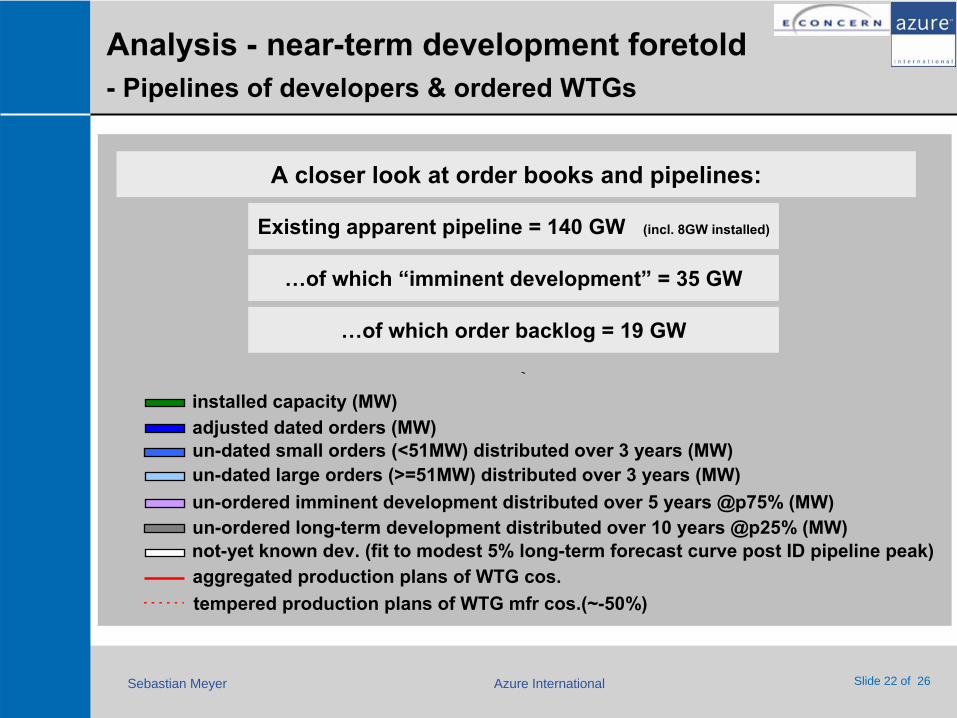

A closer look at order books and pipelines:

not-yet known dev. (fit to modest 5% long-term forecast curve post ID pipeline peak)

un-dated large orders (>=51MW) distributed over 3 years (MW)un-dated small orders (<51MW) distributed over 3 years (MW)

un-ordered imminent development distributed over 5 years @p75% (MW)un-ordered long-term development distributed over 10 years @p25% (MW)

adjusted dated orders (MW)installed capacity (MW)

aggregated production plans of WTG cos.tempered production plans of WTG mfr cos.(~-50%)

Existing apparent pipeline = 140 GW (incl. 8GW installed)

…of which order backlog = 19 GW

…of which “imminent development”

= 35 GW

Sebastian Meyer Azure International Slide 23 of 26

`

Analysis -

cumulative installations to 2020 -

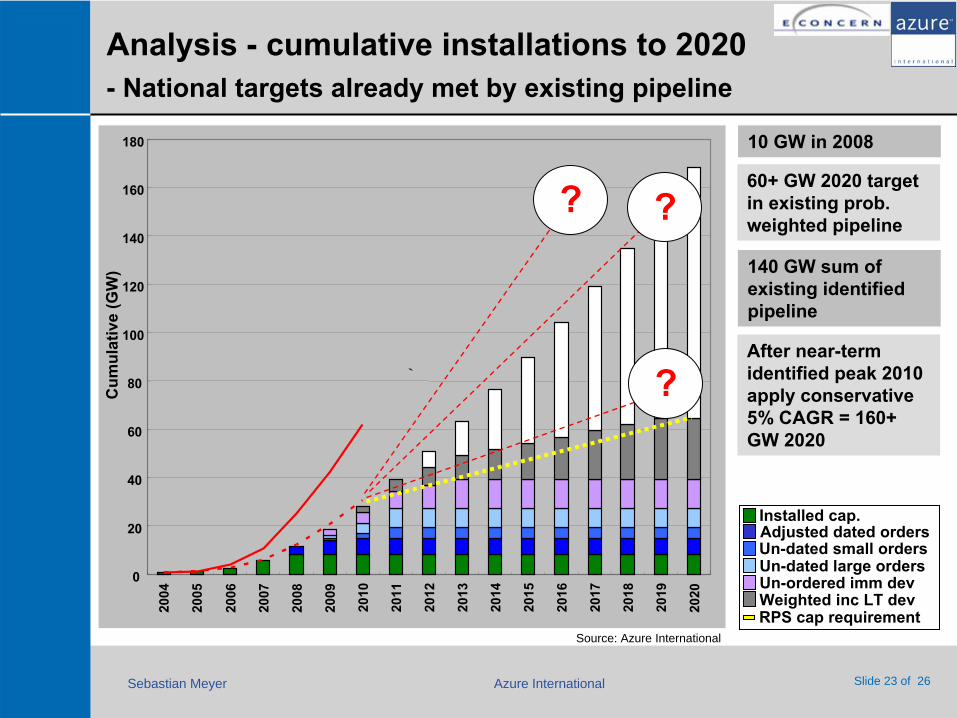

National targets already met by existing pipeline

10 GW in 2008

60+

GW 2020 target in existing prob. weighted pipeline

140

GW sum of existing identified pipeline

Installed cap.Adjusted dated ordersUn-dated small ordersUn-dated large ordersUn-ordered imm devWeighted inc LT dev

Source: Azure International

After near-term identified peak 2010 apply conservative 5% CAGR = 160+ GW 2020

RPS cap requirement

0

20

40

60

80

100

120

140

160

18020

04

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Cum

ulat

ive

(GW

)

? ?

?

Sebastian Meyer Azure International Slide 24 of 26

`

Analysis -

annual installations to 2020 -

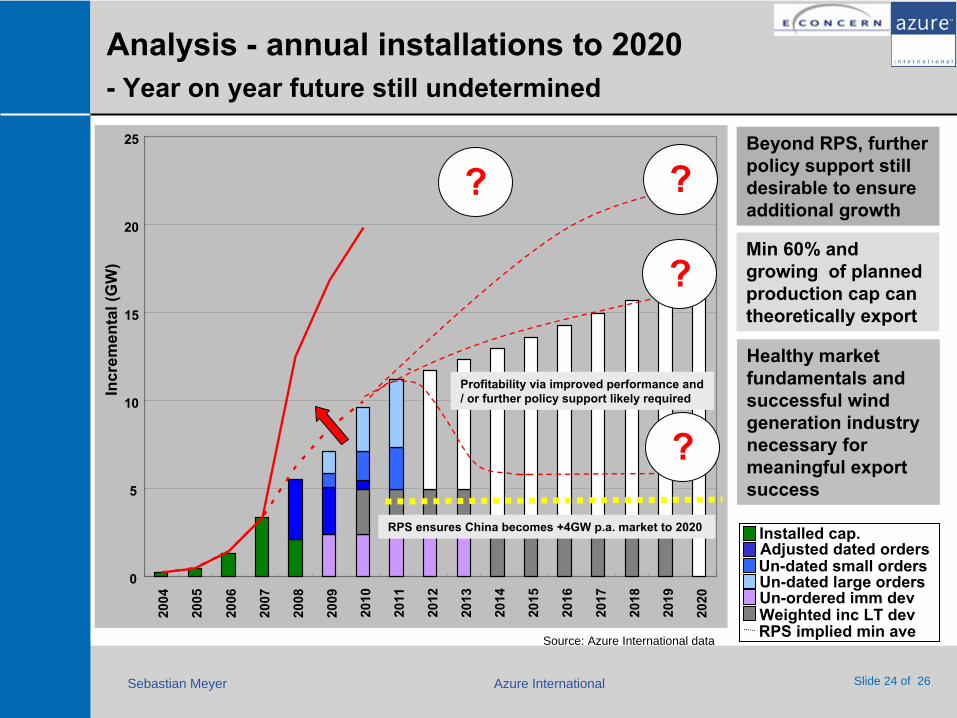

Year on year future still undetermined

Beyond RPS, further policy support still desirable to ensure additional growth

Min 60% and growing of planned production cap can theoretically export

Installed cap.Adjusted dated ordersUn-dated small ordersUn-dated large ordersUn-ordered imm devWeighted inc LT dev

Source: Azure International dataRPS implied min ave

Healthy market fundamentals and successful wind generation industry necessary for meaningful export success

0

5

10

15

20

25

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Incr

emen

tal (

GW

)

?

?

?

?

RPS ensures China becomes +4GW p.a. market to 2020

Profitability via improved performance and / or further policy support likely required

Sebastian Meyer Azure International Slide 25 of 26

Some conclusions -

China Domestic wind market to affect global market?

Near-term domestic demand is secured by aggressive RPS, but development beyond required levels remains uncertain; focus on kW (not kWh) may challenge industry health

Near-term capacity overhang suggests increasing focus to export markets & perceived limitation of licenses may not be the real limiting factor

It will be difficult for new WTG manufacturers make inroads in established markets like Europe & US with un-proven product and not-well understood financial status (among other things); Emerging markets new to wind will be a receptive market for cheaper turbines (SE Asia, Africa, Middle East & Latin America) (Canada, USA, Cuba, Chile, Poland, Korea, Pakistan, Turkey)

International established companies may be the first to export meaningful production

In the long run, a healthy, successful and profitable domestic wind industry experience remains key to international export success

Sebastian Meyer Azure International Slide 26 of 26

Azure International -

Contact information

Sebastian MeyerDirector, Research & [email protected]: +86 10 8447 7053Fax: +86 10 8447 7058

Oriental KenzoSuite H, Office Tower, 6th Floor48, Dongzhimen Wai Street100027 Dong Cheng District, BeijingPR Chinawww.azure-international.com

Welcome to visit us at our office: