Embed Size (px)

Citation preview

Writing A New Story Writing A New Story for North Carolina’s for North Carolina’s 21 21 st st Century Economy Century Economy

Bill Prindle Deputy Director American Council for an EnergyEfficient Economy

February 8, 2008

Overview

How North Carolinians can use energy efficiency to write a new story for its 21 st Century economy

• The 19 th early 20 th century story is ending…. …. a new story awaits

• Efficiency can help write this new story because it is a state’s best energy investment

• Efficiency is available now, in large quantities, and is ready to report for duty!

• But efficiency requires state policy leadership • North Carolina can join the many states writing a new clean energy story, beginning with energy efficiency

The 19 th /Early 20 th Century EnergyEconomy Story

• Rapidly industrializing economy • Building out the modern power grid • Proliferation/saturation of end uses necessary for economic development

• Fossils fuels cheap and abundant • The environment was “free”—or at least the accounting was delayed

In the late 20 th Century…

• …the story changed: – Economic development shifted from industrial growth to service growth

– Energy systems reached economic maturity – The environmental cost of conventional fuels began to be reckoned

– The energy demand/services infrastructure matured

– Energy resource opportunities began shifting to the demand side

The 21 st Century Stage is Set

• The era of cheap energy has ended • Conventional energy is harder to deliver • Environmental cost of fossil fuels will further drive up

prices • Energy efficiency and other clean energy technologies

have become serious economic contributors • We are in a race for clean and affordable energy • Energy efficiency is the ‘first fuel’ in this race

…..Without efficiency, demand will grow too fast for ANY supply resource to keep up

Energy: Cheap No Longer

6

6.5

7

7.5

8

8.5

9

9.5

10

Jan00

Jul00

Jan01

Jul01

Jan02

Jul02

Jan03

Jul03

Jan04

Jul04

Jan05

Jul05

Jan06

Electricity

Pric

e (cen

ts/kWh)

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

Price ($/MMBtu)

Electricity Heating Oil Natural Gas NatGas Well Head

Residential Energy Prices

Energy: Cheap No Longer

20

30

40

50

60

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

World Oil Price (2004$ per barrel)

AEO 2005

AEO 2006

Crude Oil Price Forecast: 2006 vs. 2005

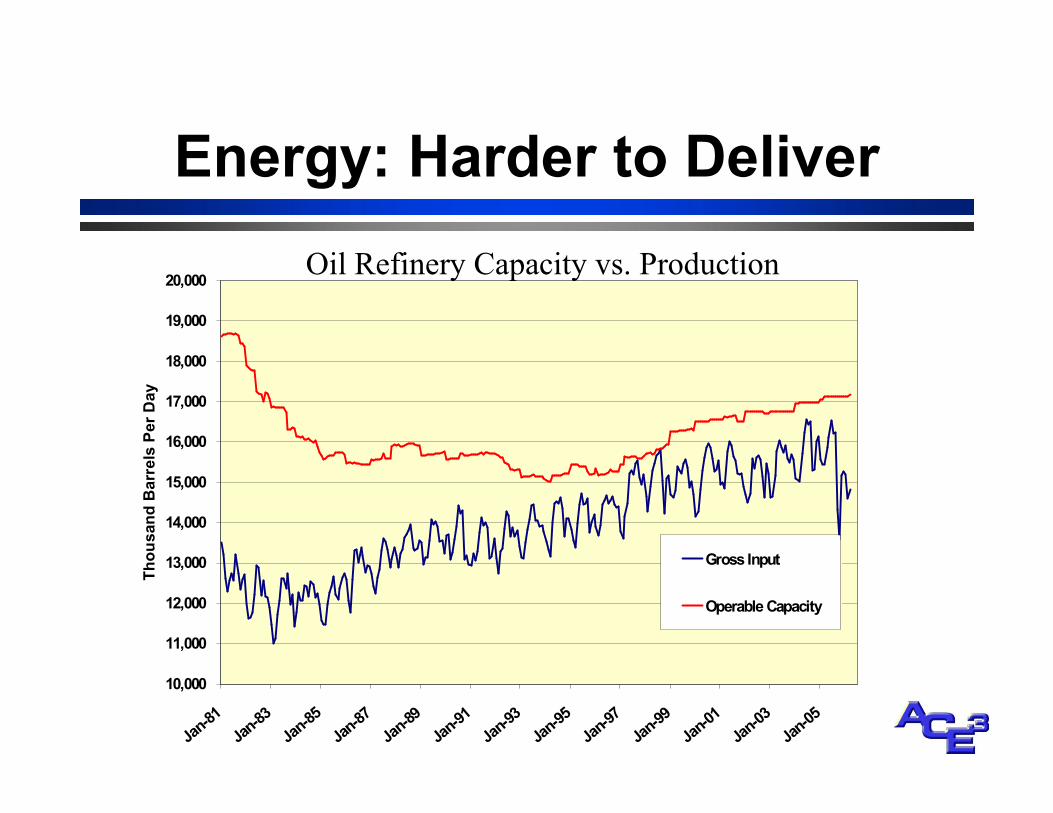

Energy: Harder to Deliver

10,000

11,000

12,000

13,000

14,000

15,000

16,000

17,000

18,000

19,000

20,000

Jan81

Jan83

Jan85

Jan87

Jan89

Jan91

Jan93

Jan95

Jan97

Jan99

Jan01

Jan03

Jan05

Thou

sand

Barrels Per Day

Gross Input

Operable Capacity

Oil Refinery Capacity vs. Production

Energy: Harder to Deliver

Natural Gas Capacity vs. Production

Energy: Harder to Deliver

0

10

20

30

40

50

60

Mar02

Jun02

Sep02

Dec02

Mar03

Jun03

Sep03

Dec03

Mar04

Jun04

Sep04

Dec04

Mar05

Jun05

Sep05

Dec05

Days Su

pply

0

50,000

100,000

150,000

200,000

250,000

300,000

Coa

l (short ton

s)

Consumption Stocks Days Supply

Coal Usage and Powerplant Stocks

Will We See Cheap and Abundant Energy Again?

• Prices not returning to 20 th century lows • Delivery problems mounting

– Resources ‘in ground’ mean less than deliverability capacity

• Bringing any new resources to energy markets is harder than ever

• U.S. energy markets are in a “straitjacket” situation

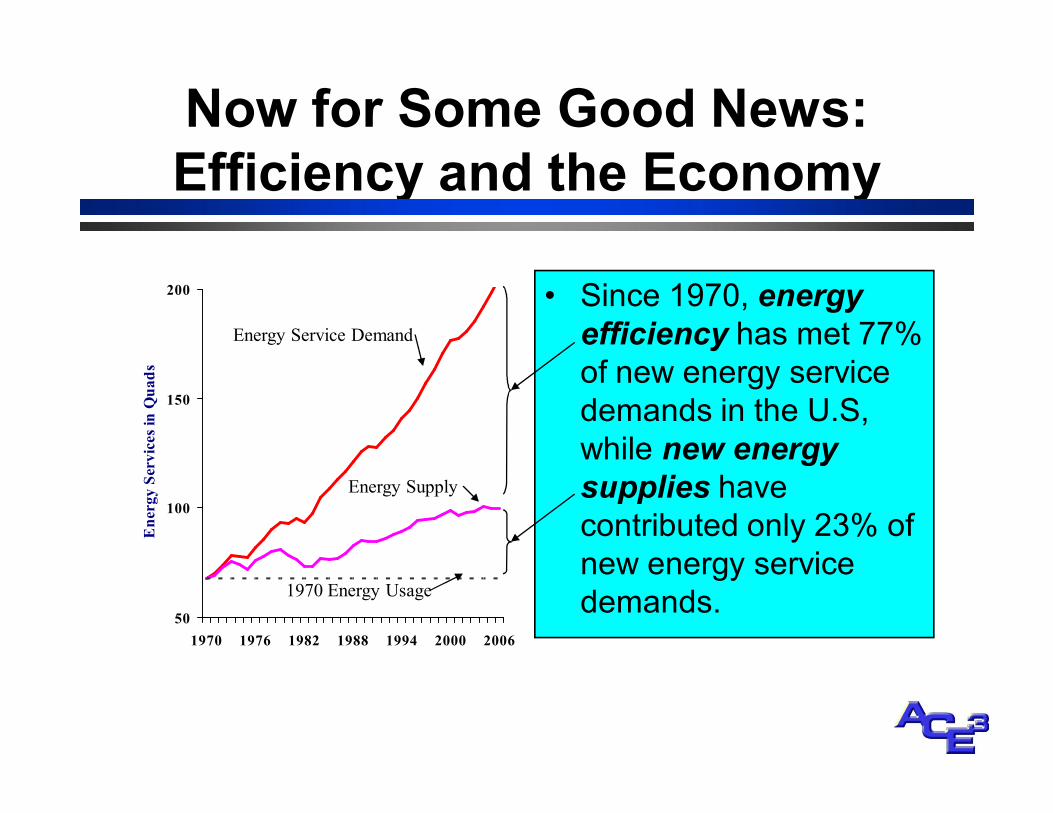

Now for Some Good News: Efficiency and the Economy

50

100

150

200

1970 1976 1982 1988 1994 2000 2006

Energy Services in Quads

• Since 1970, energy efficiency has met 77% of new energy service demands in the U.S, while new energy supplies have contributed only 23% of new energy service demands.

Energy Service Demand

Energy Supply

1970 Energy Usage

How Efficiency Meets New Service Demand

The humble refrigerator…

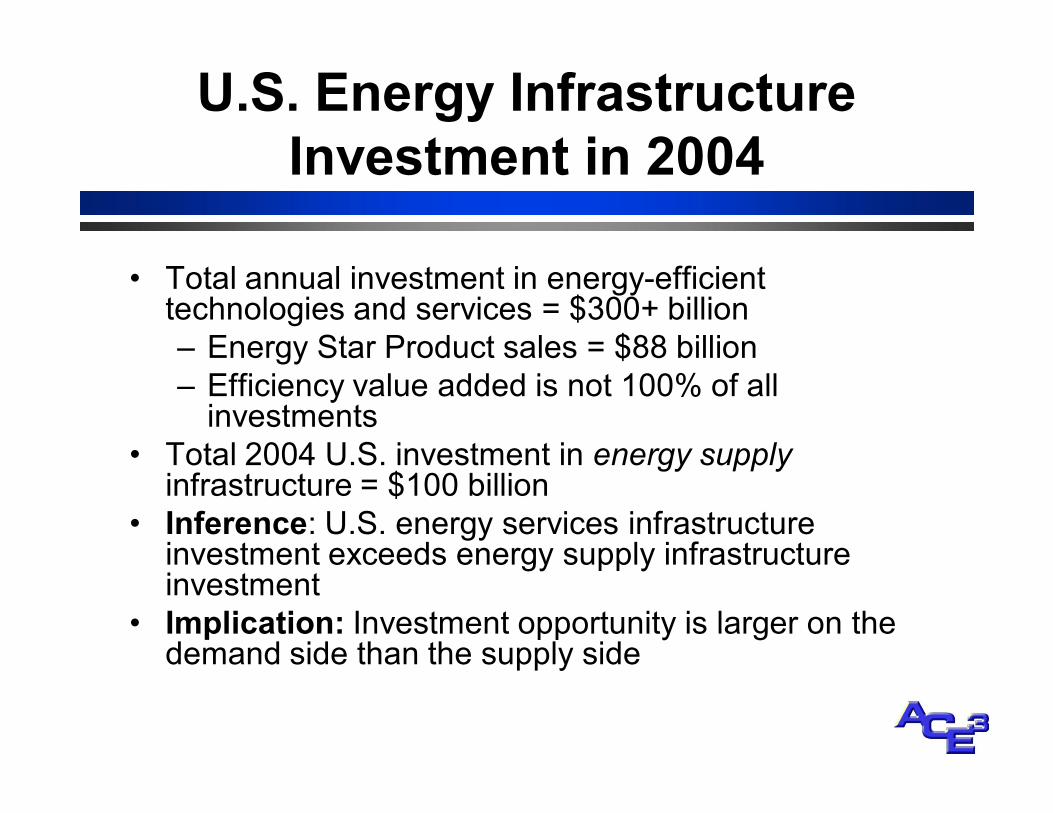

U.S. Energy Infrastructure Investment in 2004

• Total annual investment in energyefficient technologies and services = $300+ billion – Energy Star Product sales = $88 billion – Efficiency value added is not 100% of all investments

• Total 2004 U.S. investment in energy supply infrastructure = $100 billion

• Inference: U.S. energy services infrastructure investment exceeds energy supply infrastructure investment

• Implication: Investment opportunity is larger on the demand side than the supply side

Efficiency Investment and Job Creation

• 2004 energy efficiency investment supports 1.6 million U.S. jobs – 230,000 directly attributable to efficiency value added

– Distributed among manufacturing, services, construction

– Jobs created in more laborintensive sectors than those stimulated by energy supply investments

– Direct jobs multiplier: • > 6 jobs per $ million invested, vs. • ~ 2 jobs/$ million for typical supply investments

The ‘Eternal Caveat’ on Job Creation

“Your Majesty, my voyage will not only forge a new route to the spices of the East, but it will also create over 3,000 jobs.”

Efficiency and Future Energy Service Demands

• ACEEE efficiency potential studies show we can meet most energy service demand growth through efficiency

• Efficiency and renewables together can meet most future demand growth

• EE and RE provide price hedge and other value to resource portfolios

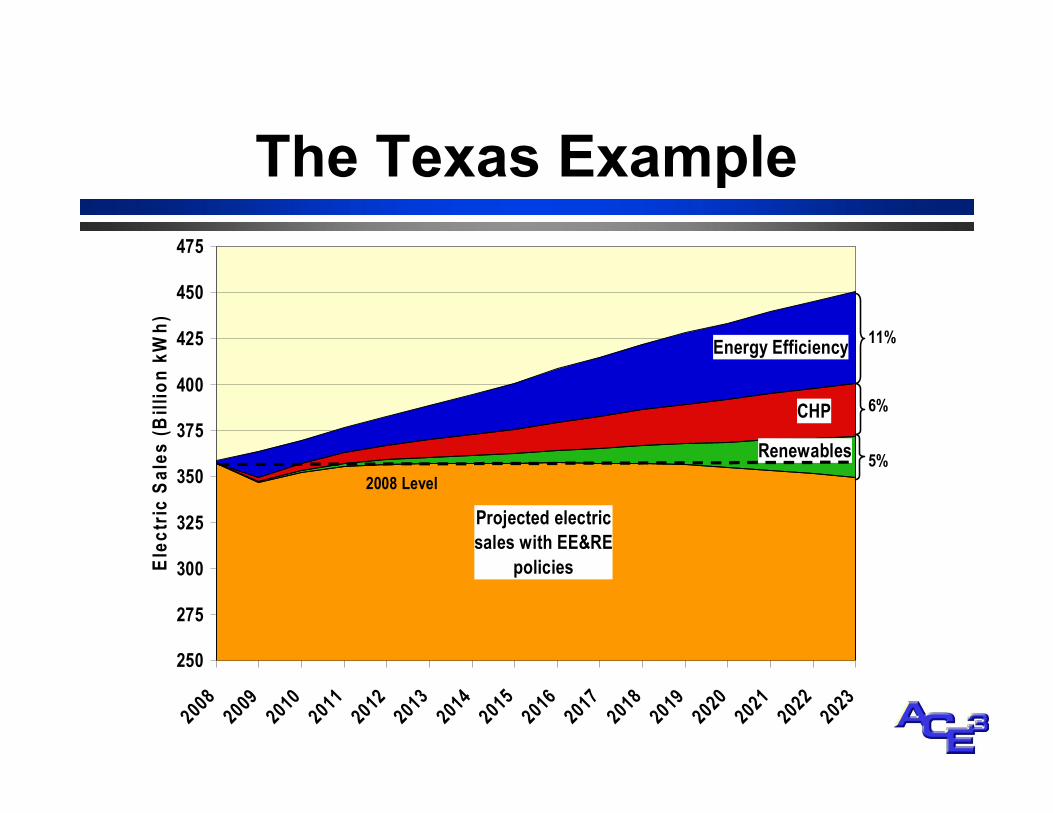

The Texas Example

Projected electric sales with EE&RE

policies

Renewables

CHP

Energy Efficiency

250

275

300

325

350

375

400

425

450

475

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

Elec

tric S

ales

(Billion kW

h)

2008 Level

11%

5%

6%

Efficiency: a Renewable Resource

• In the beginning, there was…not much • Today, we have efficient technologies in all enduse sectors

• Efficiency potential studies show we can cut demand growth by more than half

• Efficiency potentials stay high; new technologies and cost drops keep “refilling the well”

The Cheapest kWh

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.00

0 10 20 30 40 50

Levelized Cost of Electricity by Source

Wind @ 29% CF

IGCC w/o CCS

NGCC @ $6 gas Biomass

Nuclear Pulverized Coal w/o CCS Energy Efficiency

Cents per K

Wh

Carbon price: Dollars per ton

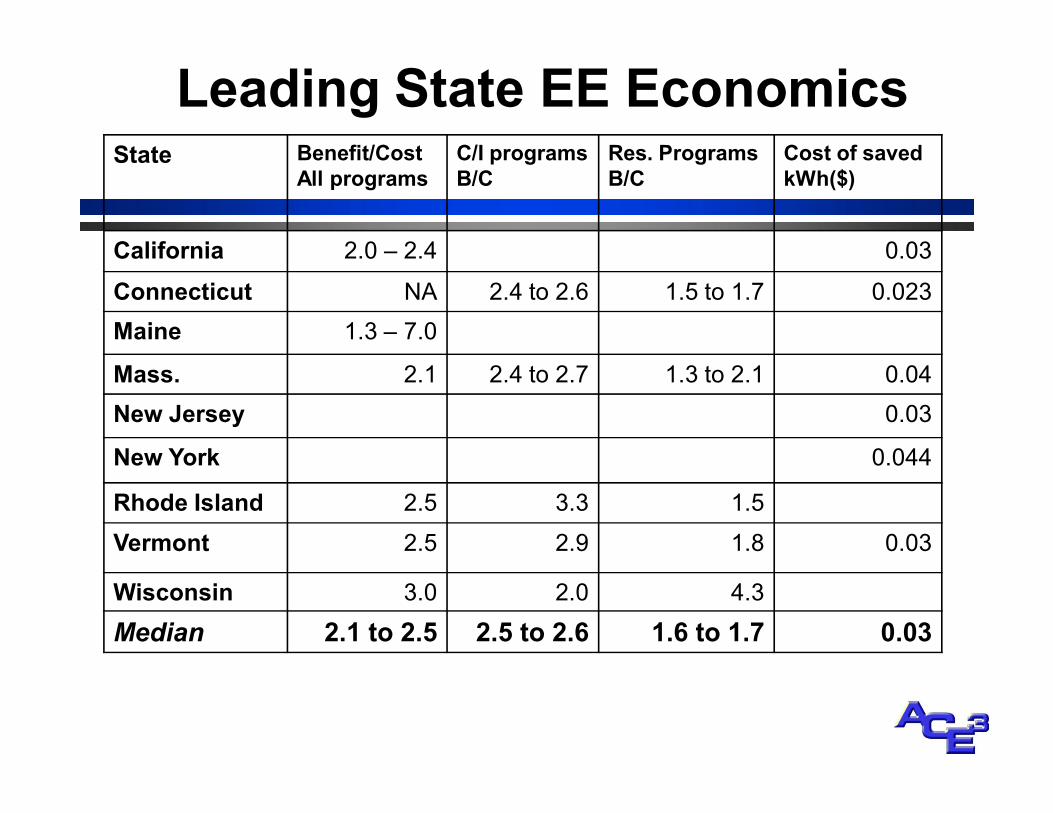

Leading State EE Economics State Benefit/Cost

All programs C/I programs B/C

Res. Programs B/C

Cost of saved kWh($)

California 2.0 – 2.4 0.03 Connecticut NA 2.4 to 2.6 1.5 to 1.7 0.023 Maine 1.3 – 7.0

Mass. 2.1 2.4 to 2.7 1.3 to 2.1 0.04 New Jersey 0.03

New York 0.044

Rhode Island 2.5 3.3 1.5 Vermont 2.5 2.9 1.8 0.03

Wisconsin 3.0 2.0 4.3 Median 2.1 to 2.5 2.5 to 2.6 1.6 to 1.7 0.03

Rising Powerplant Costs New pulverized coal capital costs

1,100

1,280 1,400

1,730 1,667

2,168

100 333

508

1,200 1,250

1,500 1,504 1,519 1,667 1,667

1,875 2,083

2,333 2,500

0 500 1,000 1,500 2,000 2,500 3,000

TXU 11 plants (TX) Prairie State Original (IL)

CliffsideDuke Original (NC) EIA (AEO 2006)

EPRI (2004) EPA (2003)

Weston 4 (WI) Council Bluffs (IA)

Prairie State Revised (IL) Westar Original (KS)

Black & Veatch (2006) Big Stone II Original (SD)

CliffsideDuke Revised (NC) Oak Creek (WI)

Westar Revised (KS) Springfield (IL)

Big Stone II Revised (SD)

$/kW

Generation Transmission Total

But: Policy Leadership is Needed To Spur EE Markets

• Markets work, but won’t reap enough EE fast enough – Income elasticity and crosselasticity block price elasticity

– Principalagent barriers—builderbuyer, landlordtenant – Informationcost barriers—consumers don’t have time/$ to study each purchase

• IEA study: over half of building heating/cooling/hot water is affected by the principalagent barrier

• Utility regulation must be reformed for the 21 st century

• Bottom line: policy action is need to make markets work for a clean energy future

States Have Become the Leaders on Energy Policy

• Congress struggling to move transformational energy policies

• States more and more the laboratories of innovation and effectiveness

• States now outspending the federal government by 3:1

• State leadership more important than ever

Why are So Many States Leading with Efficiency?

• It’s the only resource reliably available in EVERY STATE

• Most conventional energy dollars go out of state—more of the efficiency dollar STAYS HOME—so it’s an economic winner

• It’s something you can do NOW (IMTOO) • It’s a great hedge, against rising prices, supply problems, environmental problems

…that’s why we call it the ‘first fuel

Spending on Utility Sector Efficiency Programs

0.0

0.5

1.0

1.5

2.0

2.5

1993 1996 1997 1998 1999 2000 2003 2004 2005 2006

$ billion

s (nom

inal)

Three Utility Regulatory Issues

• Allowing timely cost recovery for direct costs of EE programs

• Removing the disincentives of “lost revenues” resulting from energy efficiency programs

• Creating earnings potential from energy efficiency program investments

Where’s the Electricity Business Heading?

• A shift in electricity industry strategy – Slowing load growth – Rising fuel prices and capital costs – Capacity shortages – Carbon risk – Growing understanding of demand side investment potential

– Consideration of new business models

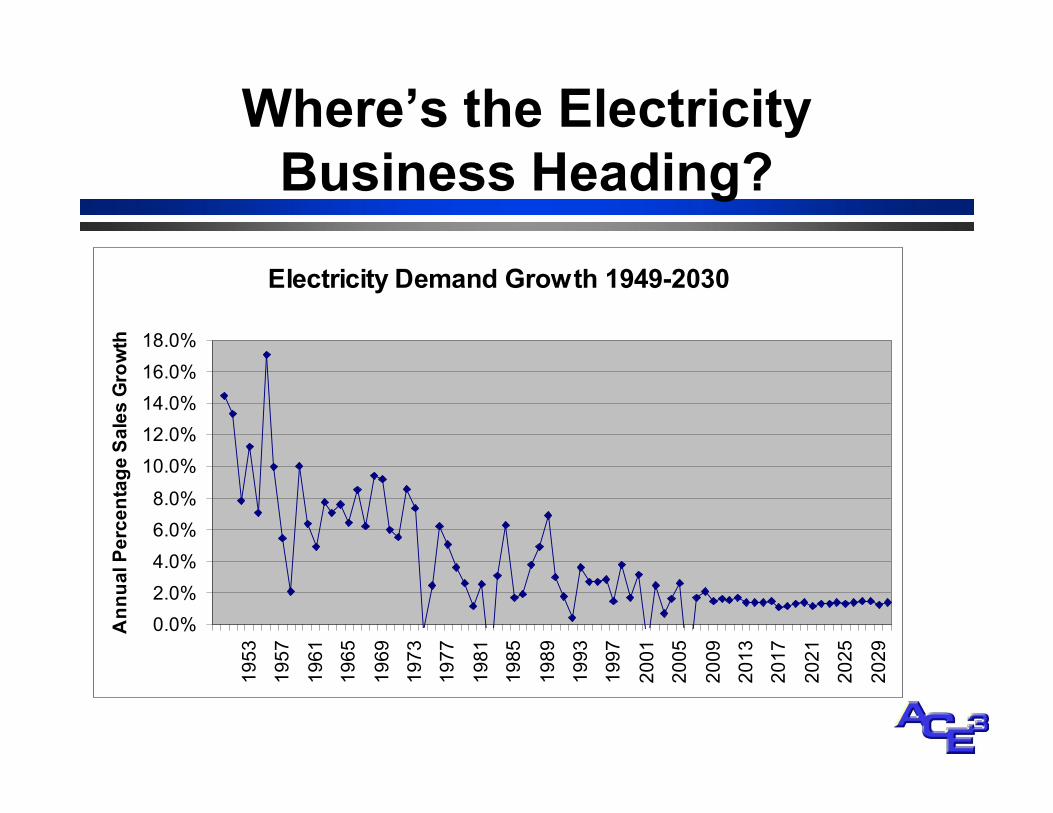

Where’s the Electricity Business Heading?

Electricity Demand Growth 19492030

0.0% 2.0% 4.0% 6.0% 8.0%

10.0% 12.0% 14.0% 16.0% 18.0%

1953

1957

1961

1965

1969

1973

1977

1981

1985

1989

1993

1997

2001

2005

2009

2013

2017

2021

2025

2029 Ann

ual P

ercentag

e Sales Growth

Where’s the Electricity Business Heading?

• Proliferating state EERS encouraging federal action

• Housepassed RPS bill in August requires 15% renewable electricity supply by 2020 – Allows EE to meet up to 27% of requirements – Could become part of federal climate bill

• Resembles the NC REPS • States may see a federal requirement driving EE and well as RE resource acquisition

Where Does North Carolina’s Energy Story Go From Here?

• There’s no turning back the clock – Energy prices aren’t falling – Fuels aren’t getting easier to deliver – The climate challenge is growing

• The rest of the story starts with energy efficiency – Policies that spur investment in EE for job creation and balanced economic growth

• The happy ending comes from building a 21 st century economy on clean technology

Contact Information

Bill Prindle Deputy Director ACEEE

1001 Conn. Ave, NW, Suite 801 Washington, DC 20036

2024298873 [email protected]

http://www.aceee.org/energy