Embed Size (px)

Citation preview

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 1/46

1

Introduction to Accounting and Business

1

Student Version

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 2/46

1-2

1-2

2

1

1

Describe the nature of a

business, the role ofaccounting, and ethics in

business.

1-2

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 3/46

1-3

1-3

3

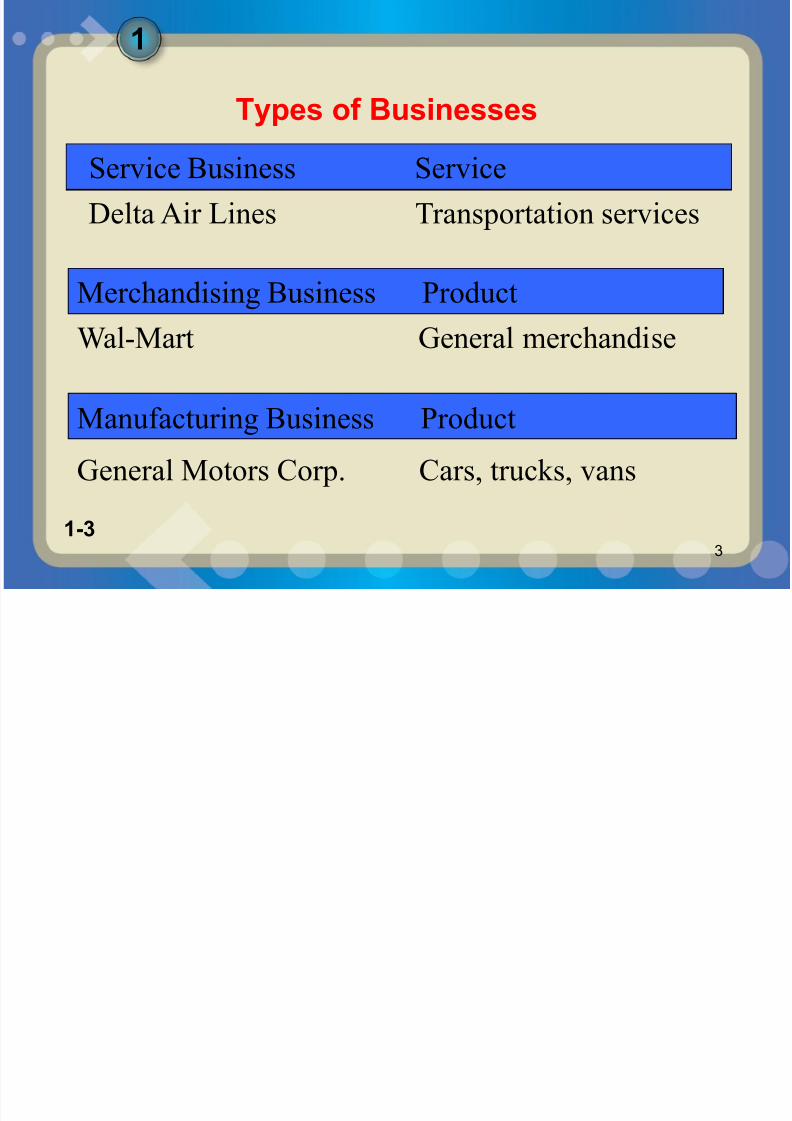

Types of Businesses

Delta Air Lines Transportation services

Service Business Service

1

Merchandising Business Product

Wal-Mart General merchandise

Manufacturing Business Product

General Motors Corp. Cars, trucks, vans

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 4/46

1-4

1-4

4

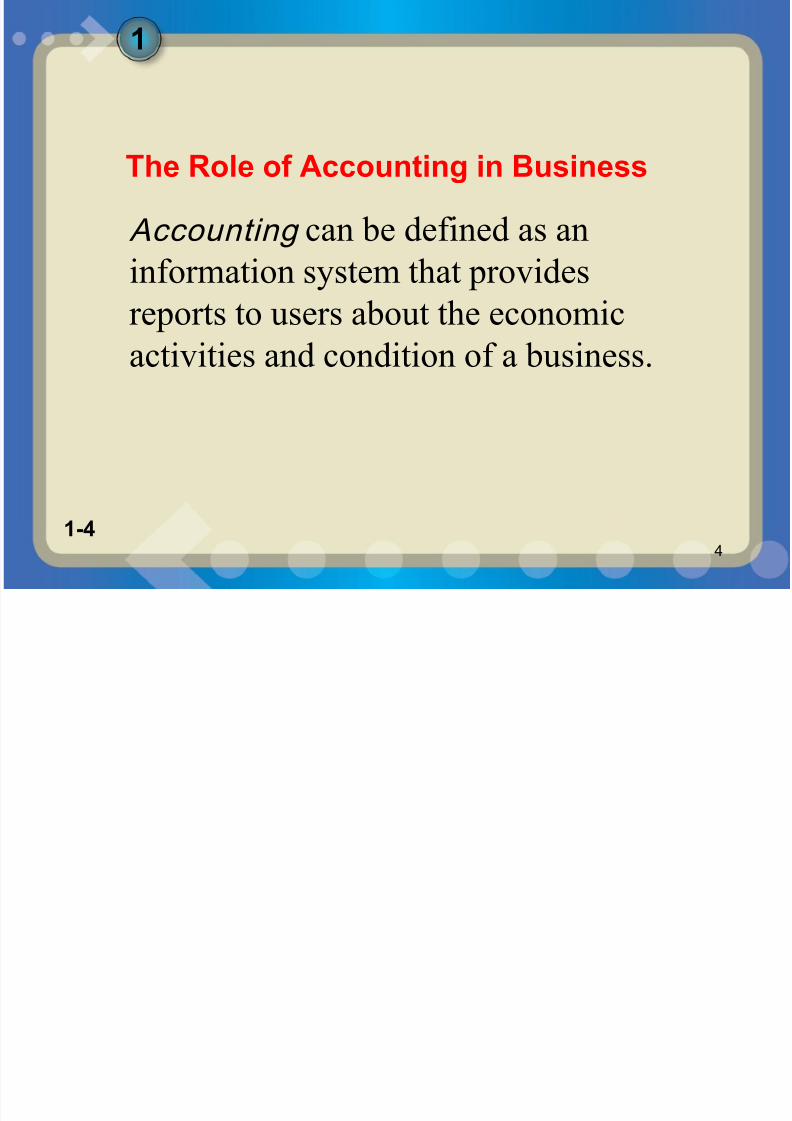

The Role of Accounting in Business Accounting can be defined as an

information system that providesreports to users about the economic

activities and condition of a business.

1

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 5/46

1-5

1-5

5

The area of accounting that provides

internal users with information is called

managerial accounting .

Managerial Accounting

The objective of managerial

accounting is to provide relevant and

timely information for managers’ andemployees’ decision-making needs.

1

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 6/46

1-6

1-6

6

The area of accounting that provides

external users with information is

called financial accounting .

Financial Accounting

The objective of financial accounting

is to provide relevant and timely

information for the decision-makingneeds of users outside of the

business.

1

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 7/46

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 8/46

1-81-8

8

Under the business enti ty

concept, the activities of a

business are recordedseparately from the activities

of its owners, creditors, or

other businesses.

Business Entity Concept

2

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 9/46

1-91-9

9

• A proprietorship is owned by one individual.

• A partnership is similar to proprietorship

except that it is owned by two or more

individuals.• A corporation is organized under state or

federal statutes as a separate legal taxable

entity.

• A l imited liabi l i ty company (LLC) combines

attributes of a partnership and a corporation.

2

Forms of Business Entity

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 10/46

1-101-10

10

Under the cost concept ,

amounts are initially recordedin the accounting records at

their cost or purchase price.

2

Cost Concept

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 11/46

1-111-11

11

The objectivity concept requires

that the amounts recorded in theaccounting records be based on

objective evidence.

2

Objectivity Concept

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 12/46

1-121-12

12

The unit of measure concept

requires that economic data be recorded in dollars.

2

Unit of Measure Concept

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 13/46

1-131-13

13

State the accounting

equation and define eachelement of the equation.

3

1-13

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 14/46

1-141-14

14

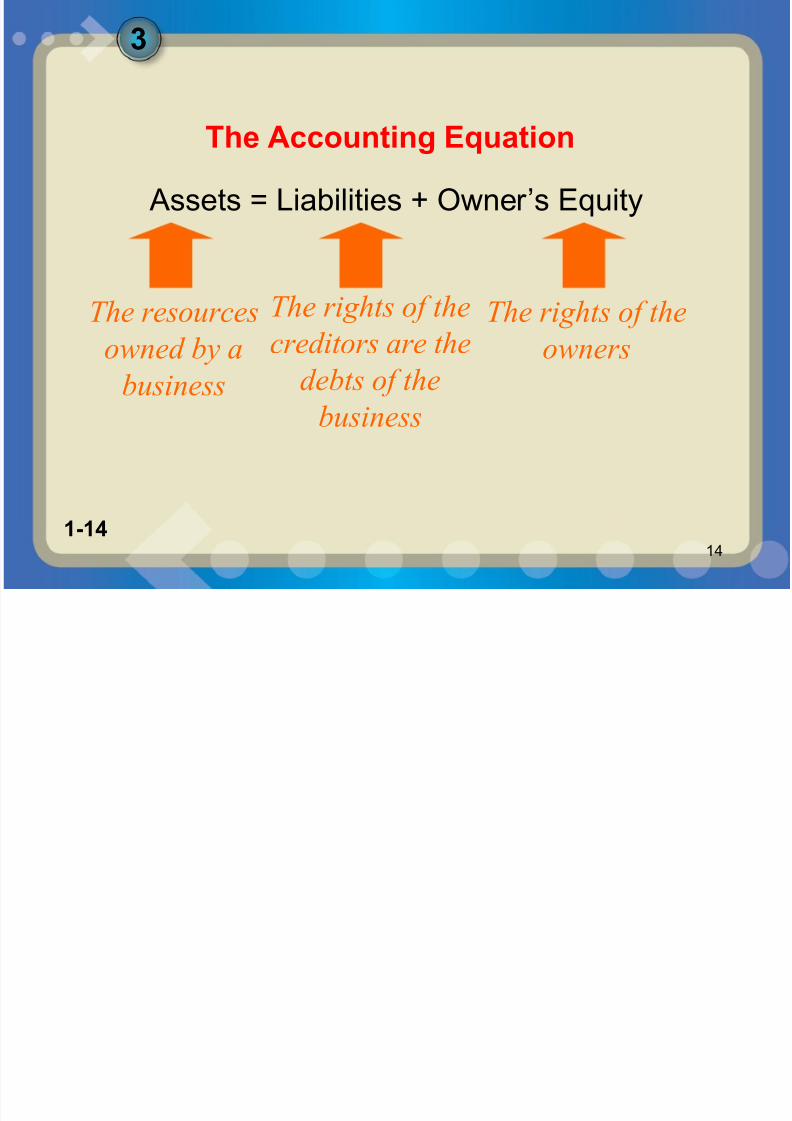

Assets = Liabilities + Owner’s Equity

The Accounting Equation

3

The resources

owned by a

business

The rights of the

creditors are the

debts of the

business

The rights of the

owners

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 15/46

1-151-15

15

4

Describe and illustrate how

business transactions can be

recorded in terms of the resultingchange in the elements of the

accounting equation.

1-15

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 16/46

1-161-16

16

A business transaction is an

economic event or condition thatdirectly changes an entity’s

financial condition or its results

of operations.

4

Business Transaction

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 17/46

1-171-17

17

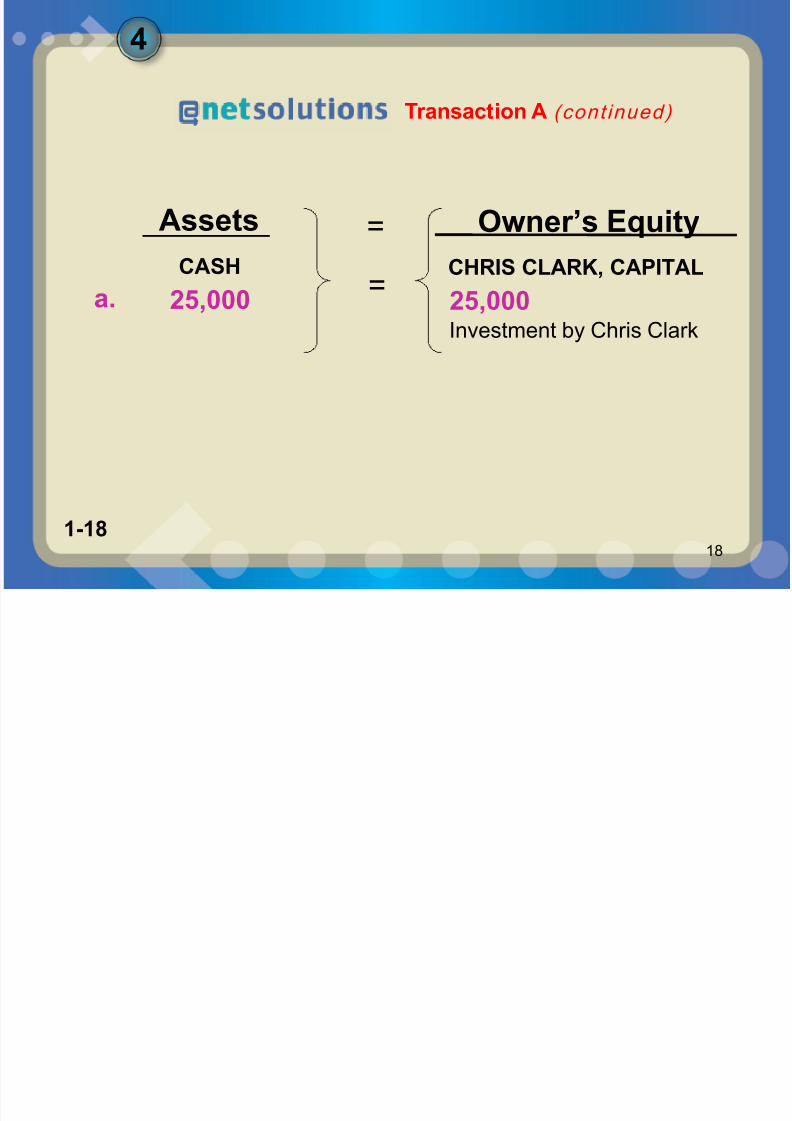

On November 1, 2009, Chris Clarkdeposits $25,000 in a bank account

in the name of NetSolutions.

Transaction A

4

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 18/46

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 19/46

1-191-19

19

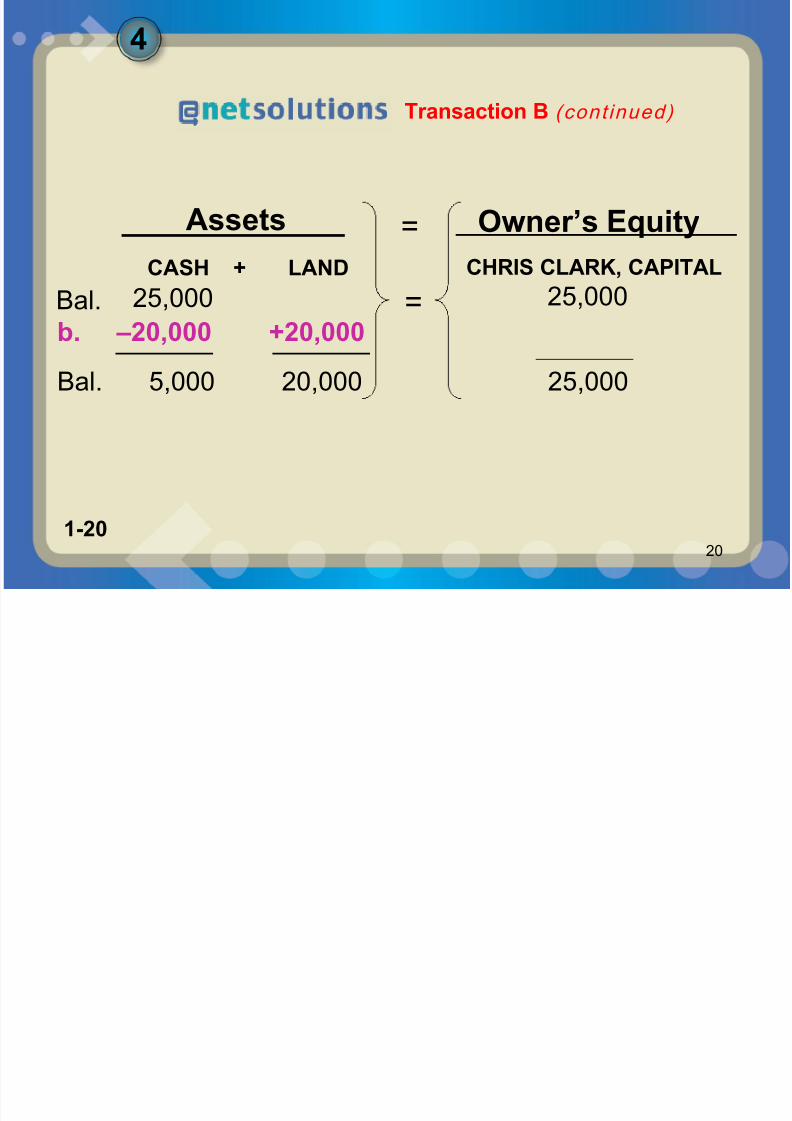

Transaction B

On November 5, 2009, NetSolutions paid $20,000 for the purchase of land

as a future building site.

4

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 20/46

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 21/46

1-211-21

21

On November 10, 2009, NetSolutions purchased supplies

for $1,350 and agreed to pay the

supplier in the near future.

4

Transaction C

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 22/46

1-221-22

22

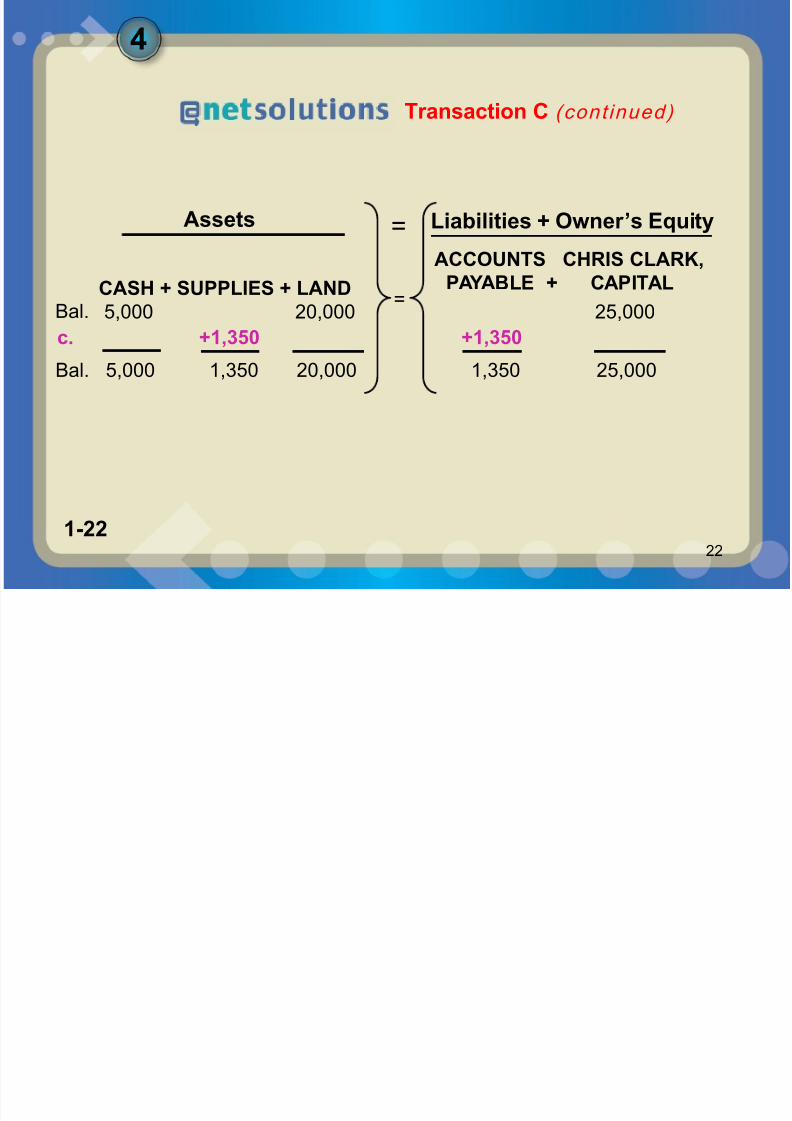

CASH + SUPPLIES + LAND

5,000 20,000 25,000Bal.

Assets =

=

ACCOUNTS CHRIS CLARK,

PAYABLE + CAPITAL

Liabilities + Owner’s Equity

Transaction C (cont inued)

c. +1,350 +1,350

Bal. 5,000 1,350 20,000 1,350 25,000

4

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 23/46

1-231-23

23

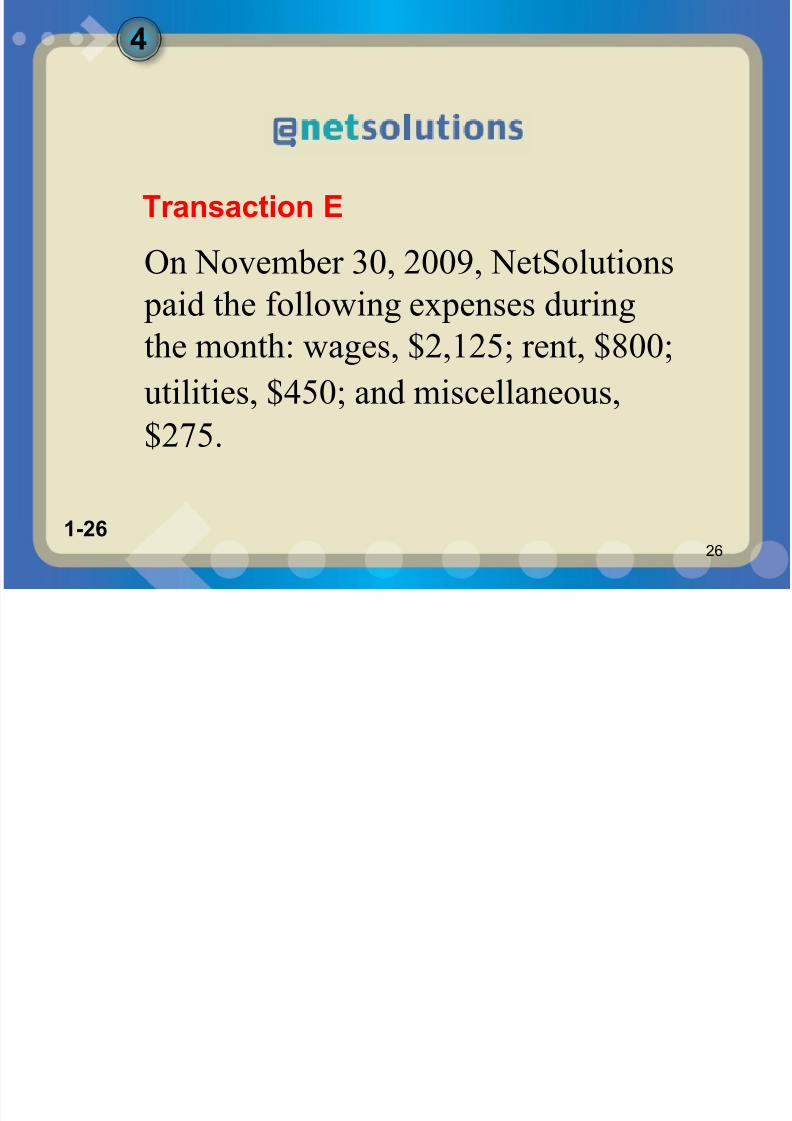

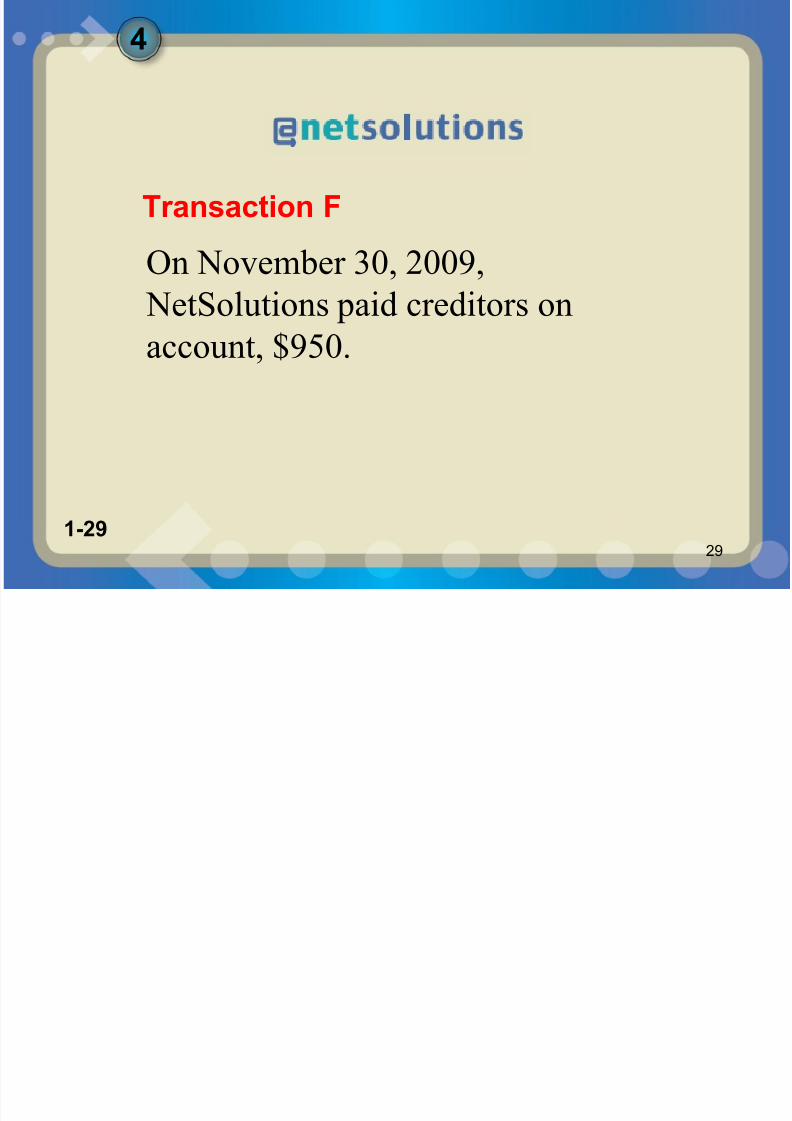

On November 18, 2009, NetSolutions

received cash of $7,500 for providingservices to customers. A business

earns money by selling goods or

services to its customers. This amount

is called Revenue.

Transaction D

4

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 24/46

1-241-24

24

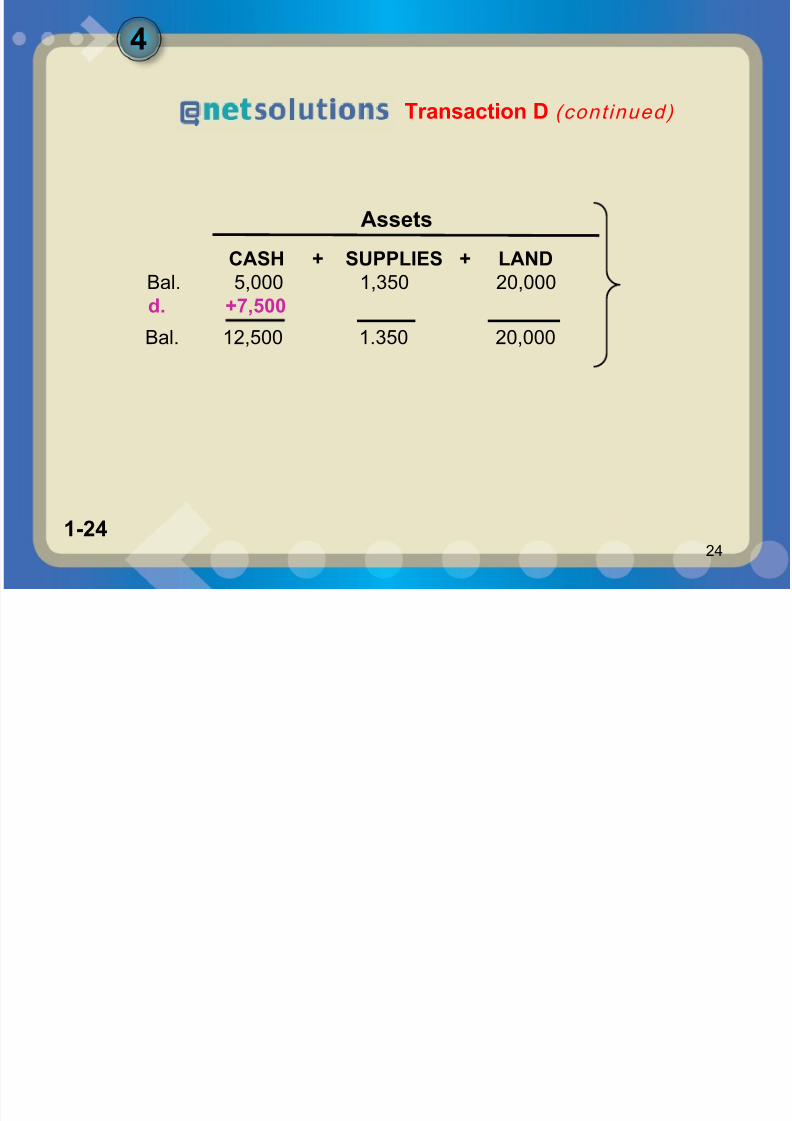

CASH + SUPPLIES + LAND

5,000 1,350 20,000Bal.

Assets

Transaction D (cont inued)

d. +7,500

Bal. 12,500 1.350 20,000

4

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 25/46

1-251-25

25

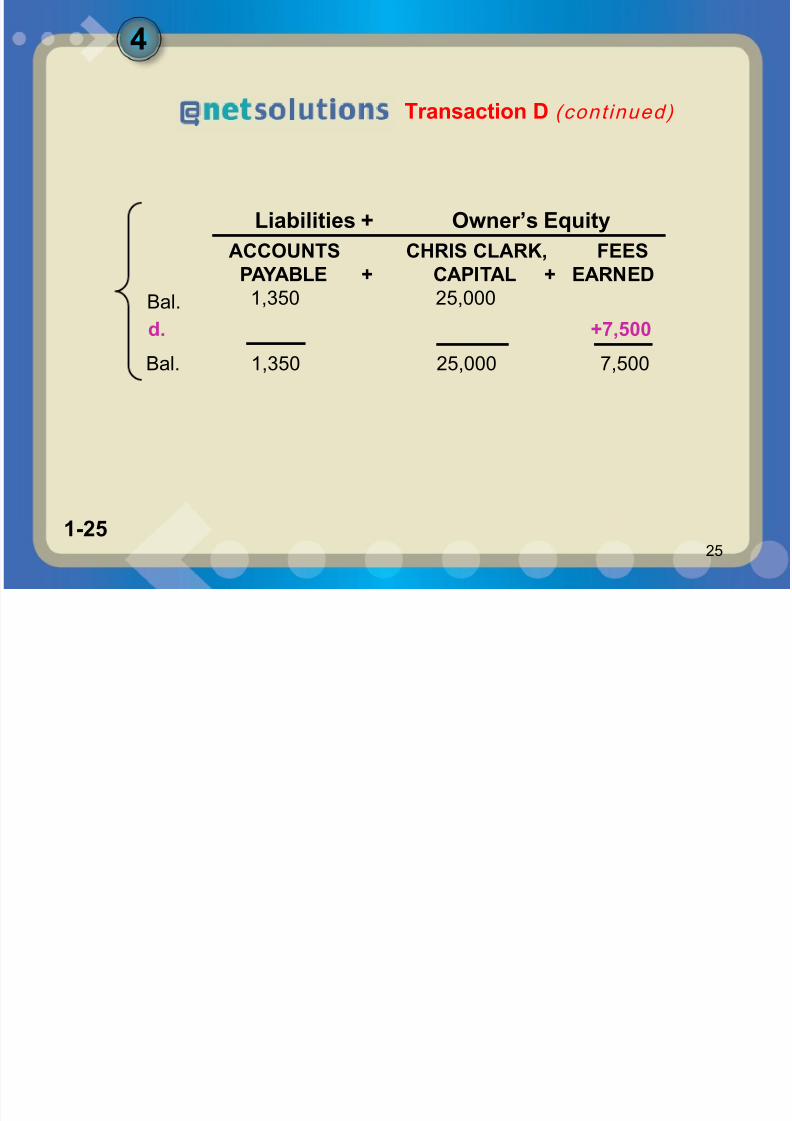

Transaction D (cont inued)

ACCOUNTS CHRIS CLARK, FEES

PAYABLE + CAPITAL + EARNED1,350 25,000Bal.

Liabilities + Owner’s Equity

d. +7,500

Bal. 1,350 25,000 7,500

4

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 26/46

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 27/46

1-271-27

27

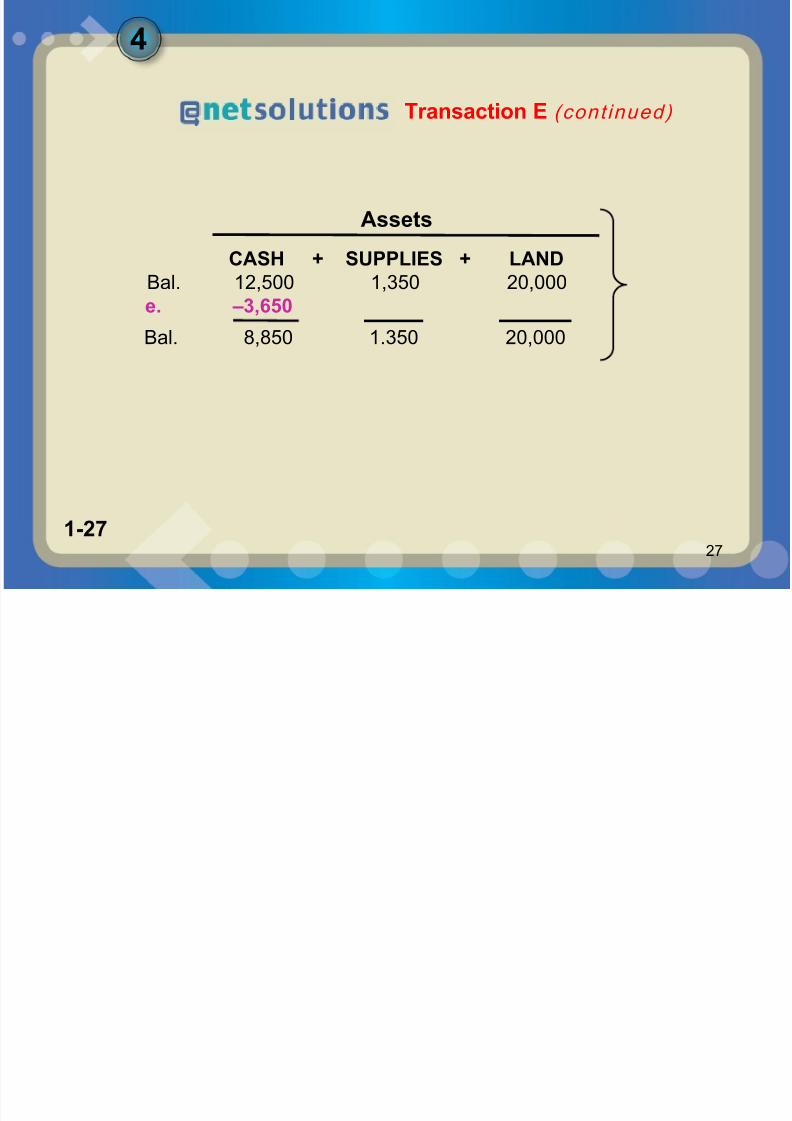

CASH + SUPPLIES + LAND

12,500 1,350 20,000Bal.

Assets

Transaction E (cont inued)

e. –3,650

Bal. 8,850 1.350 20,000

4

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 28/46

1-281-28

28

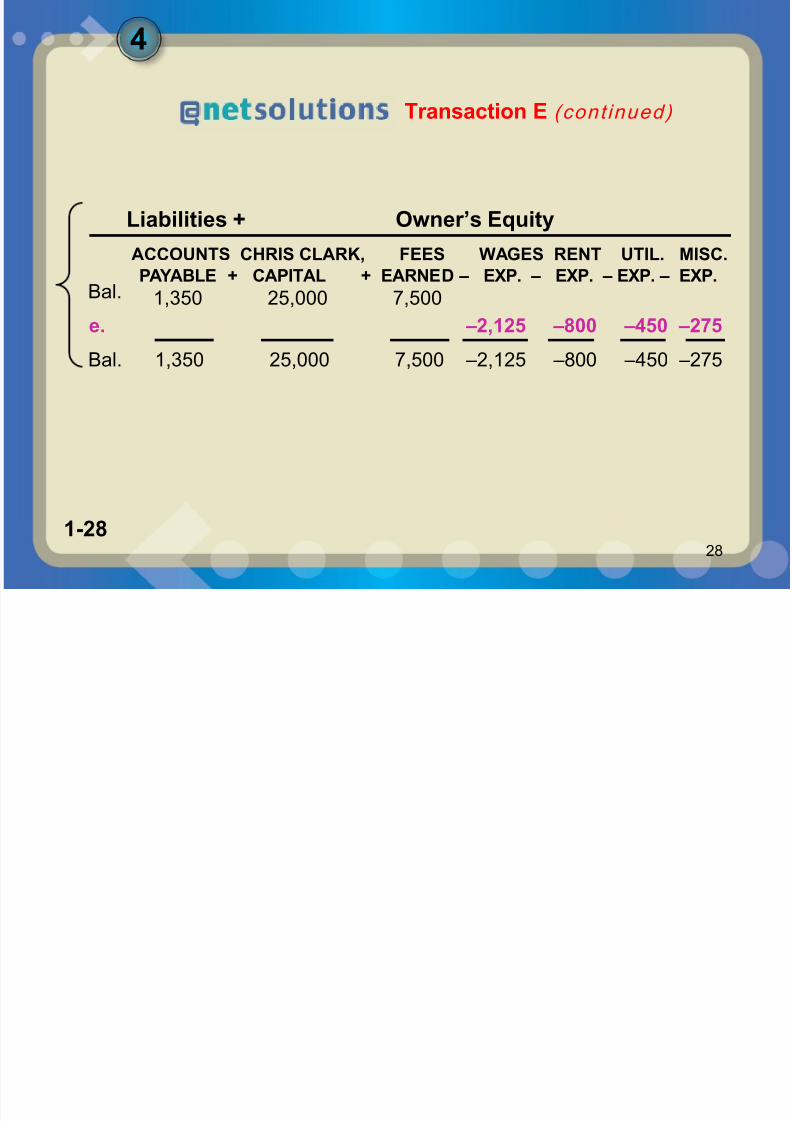

Transaction E (cont inued)

ACCOUNTS CHRIS CLARK, FEES WAGES RENT UTIL. MISC.

PAYABLE + CAPITAL + EARNED – EXP. – EXP. – EXP. – EXP.1,350 25,000 7,500Bal.

Liabilities + Owner’s Equity

e. –2,125 –800 –450 –275

Bal. 1,350 25,000 7,500 –2,125 –800 –450 –275

4

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 29/46

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 30/46

1-301-30

30

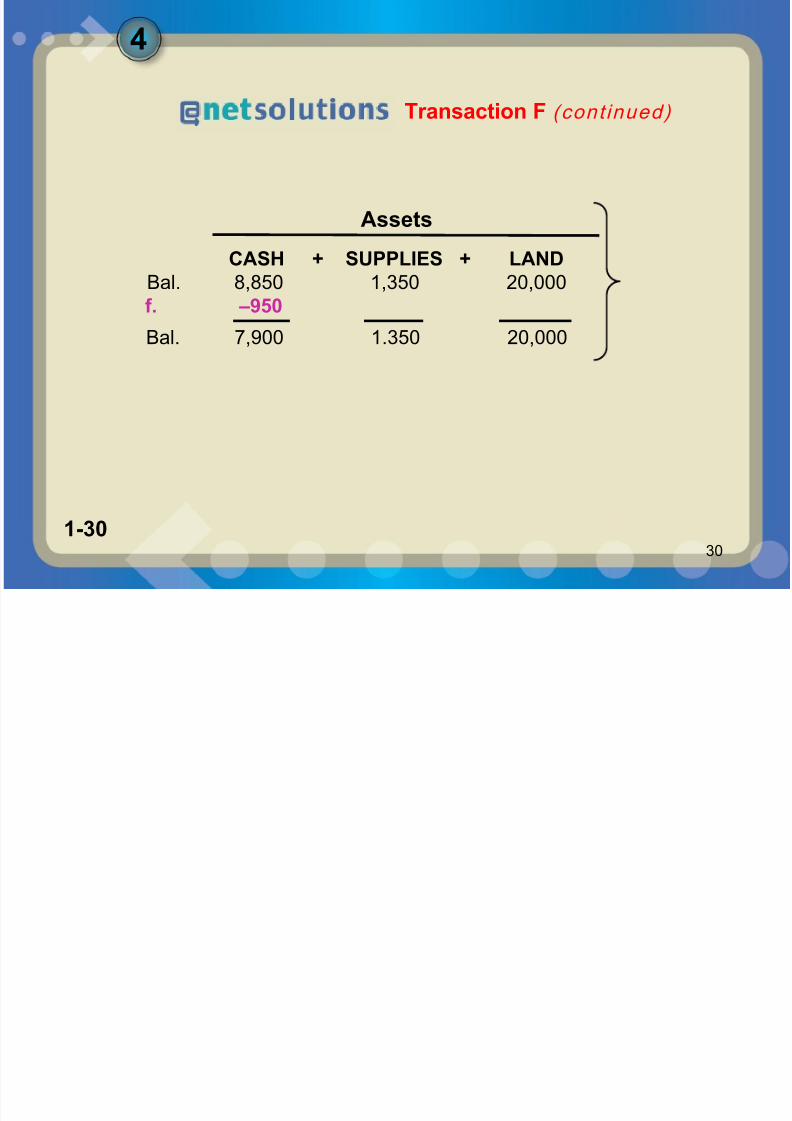

CASH + SUPPLIES + LAND

8,850 1,350 20,000Bal.

Assets

Transaction F (cont inued)

f. –950

Bal. 7,900 1.350 20,000

4

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 31/46

1-311-31

31

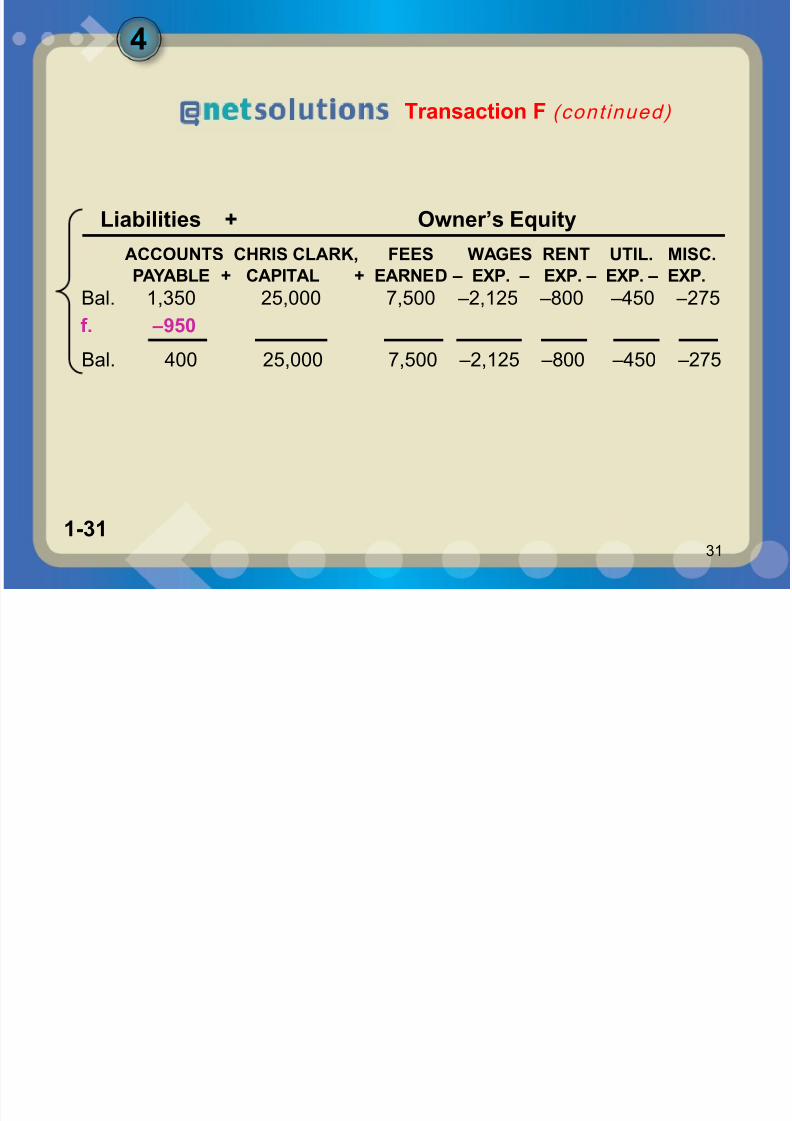

ACCOUNTS CHRIS CLARK, FEES WAGES RENT UTIL. MISC.

PAYABLE + CAPITAL + EARNED – EXP. – EXP. – EXP. – EXP.1,350 25,000 7,500 –2,125 –800 –450 –275Bal.

Liabilities + Owner’s Equity

f. –950

Bal. 400 25,000 7,500 –2,125 –800 –450 –275

Transaction F (cont inued)

4

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 32/46

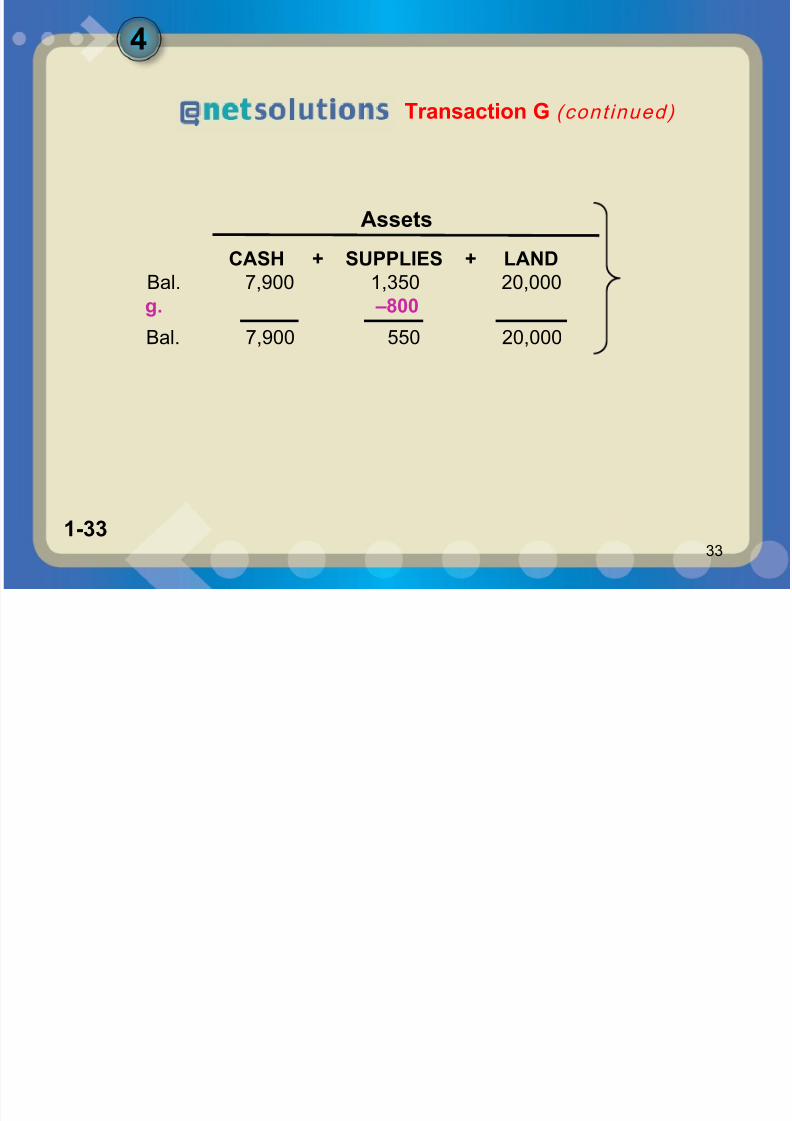

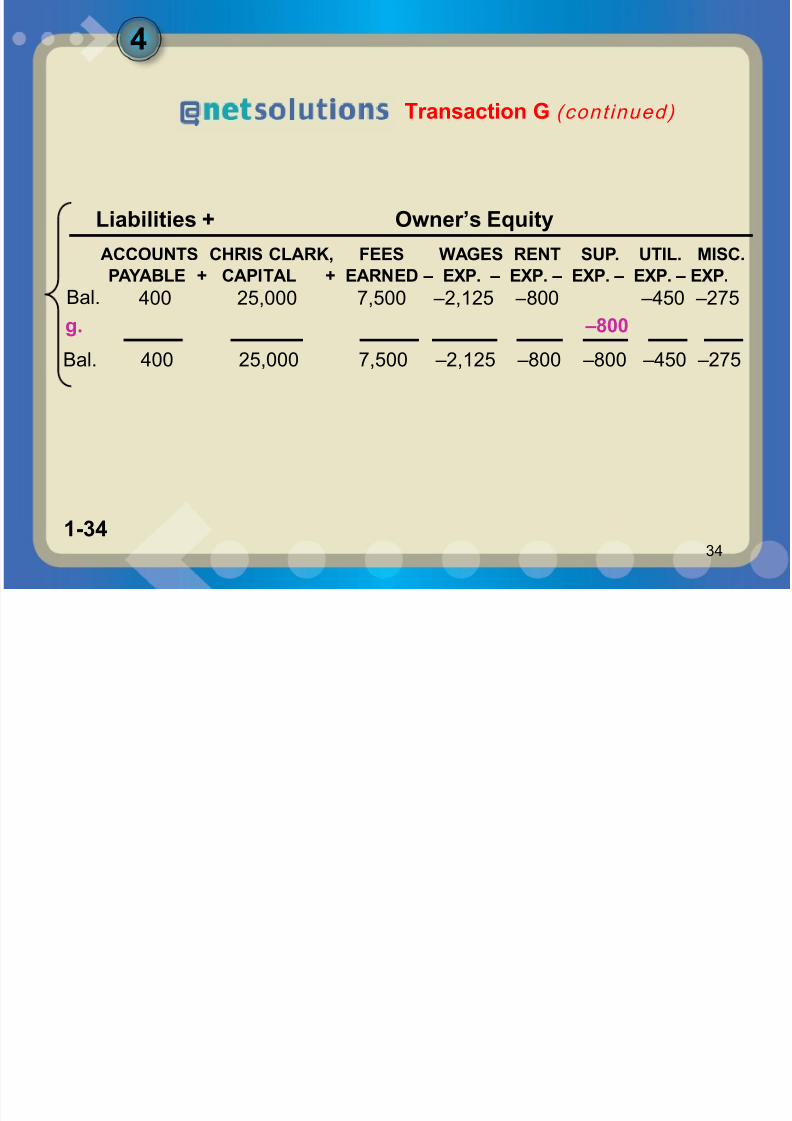

1-321-32

32

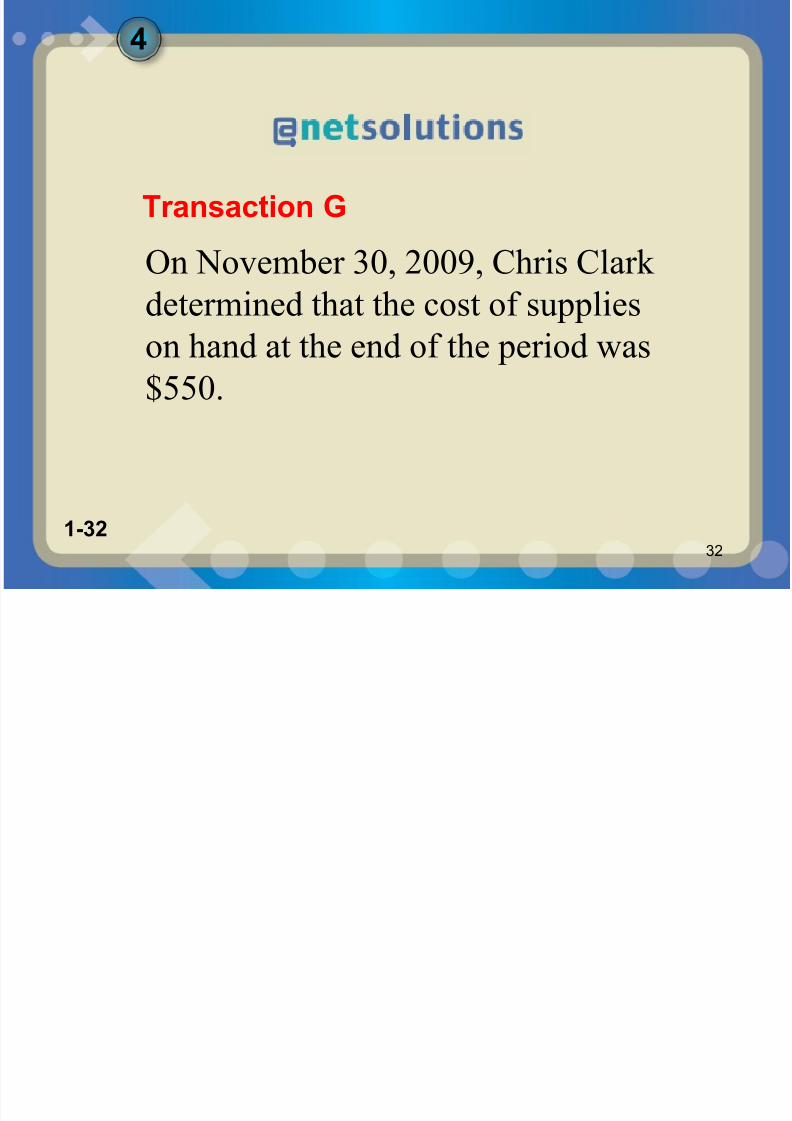

On November 30, 2009, Chris Clark

determined that the cost of supplies

on hand at the end of the period was

$550.

Transaction G

4

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 33/46

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 34/46

1-341-34

34

ACCOUNTS CHRIS CLARK, FEES WAGES RENT SUP. UTIL. MISC.

PAYABLE + CAPITAL + EARNED – EXP. – EXP. – EXP. – EXP. – EXP.400 25,000 7,500 –2,125 –800 –450 –275Bal.

Liabilities + Owner’s Equity

g. –800

Bal. 400 25,000 7,500 –2,125 –800 –800 –450 –275

Transaction G (cont inued)

4

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 35/46

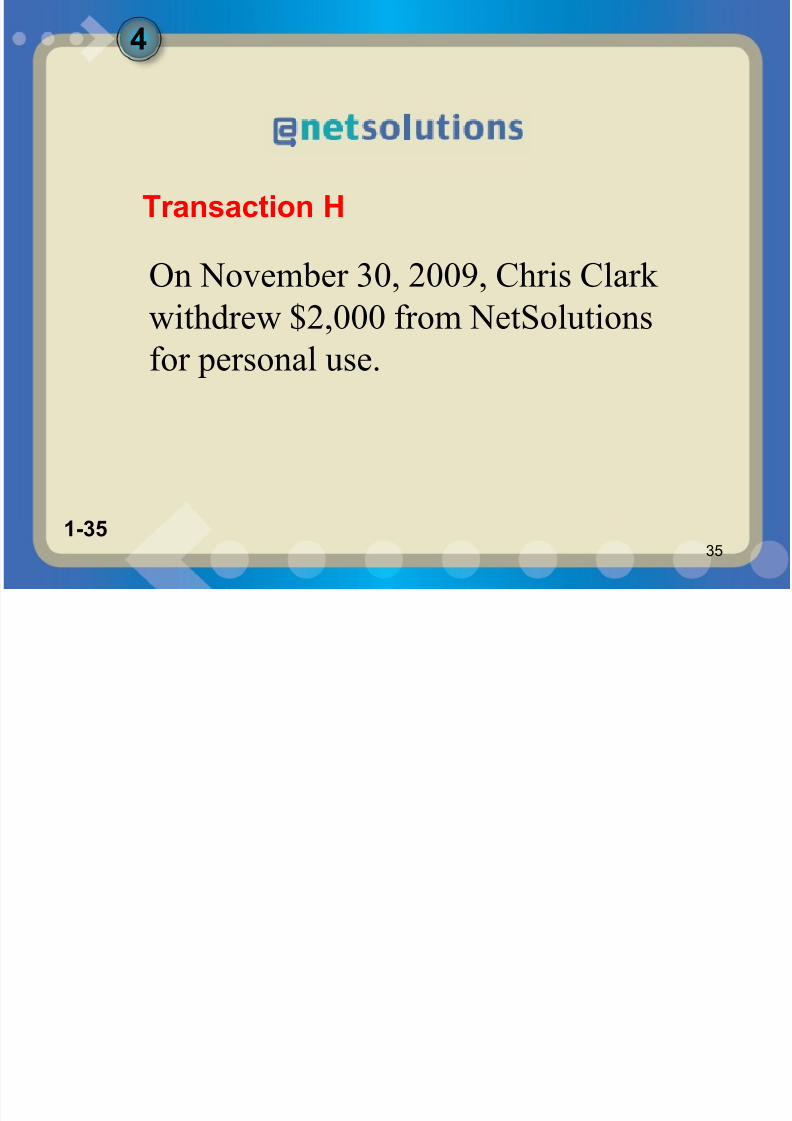

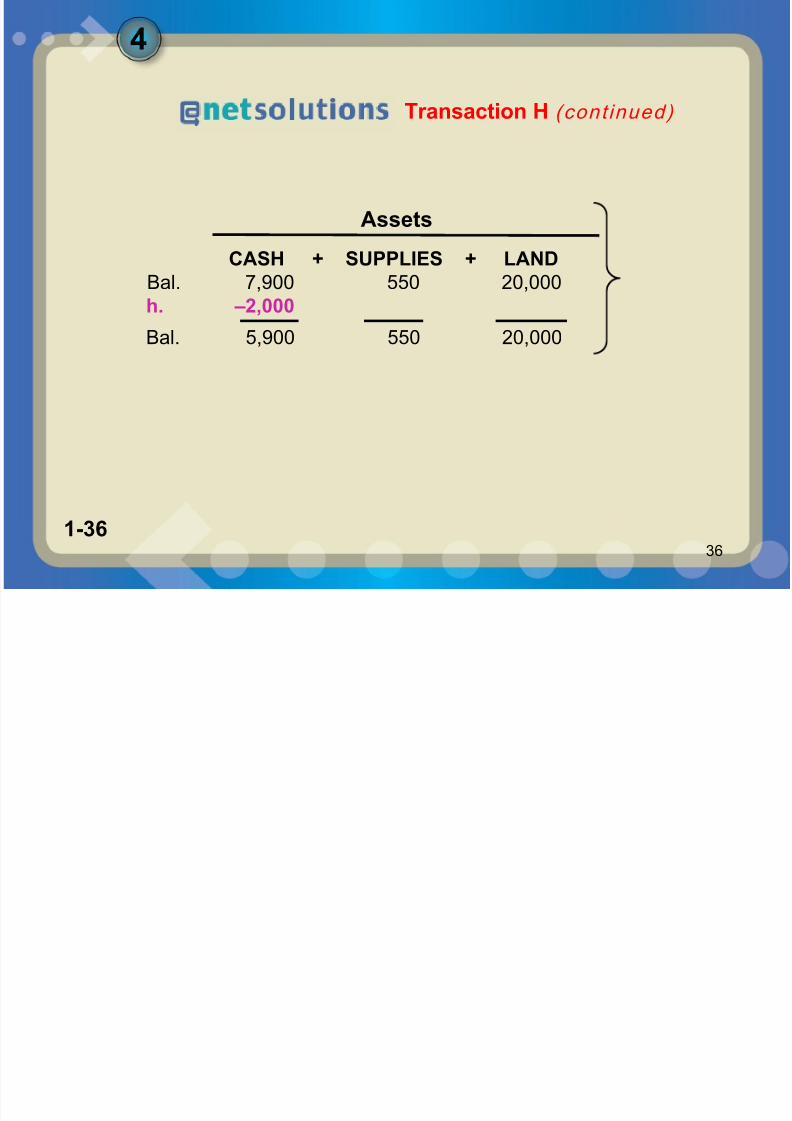

1-351-35

35

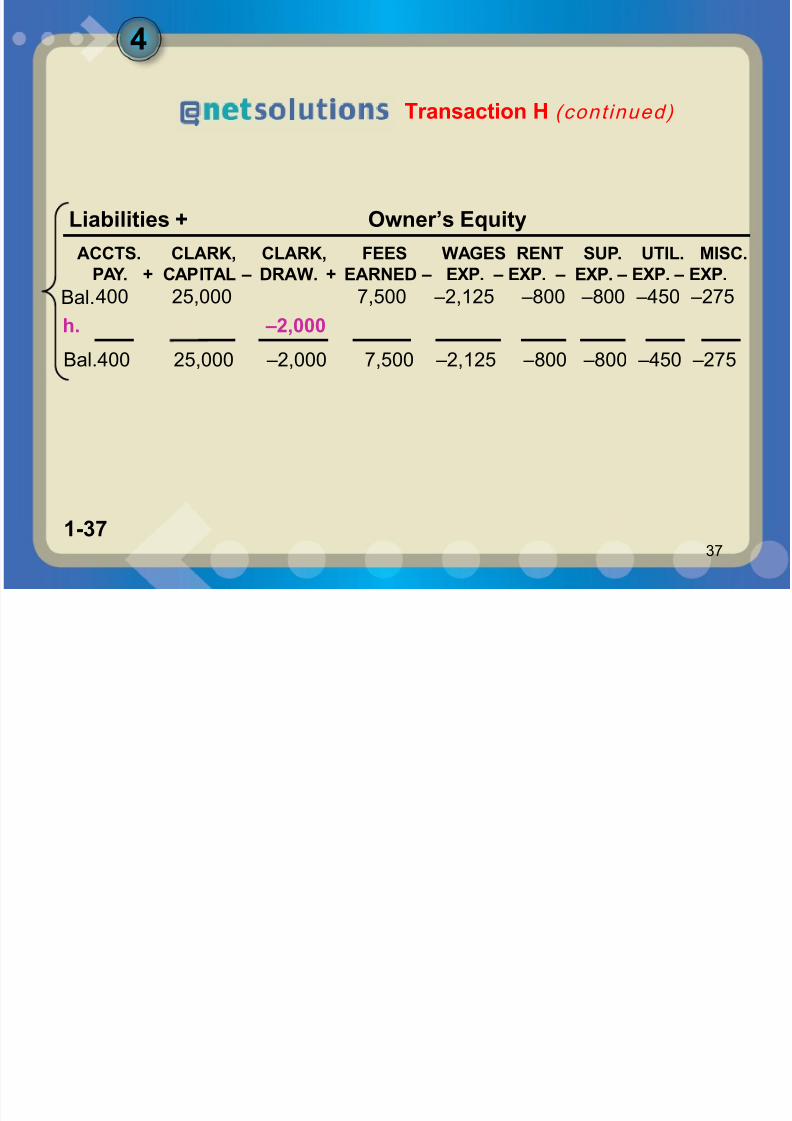

On November 30, 2009, Chris Clarkwithdrew $2,000 from NetSolutions

for personal use.

Transaction H

4

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 36/46

1-361-36

36

CASH + SUPPLIES + LAND

7,900 550 20,000Bal.

Assets

Transaction H (cont inued)

h. –2,000

Bal. 5,900 550 20,000

4

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 37/46

1-371-37

37

Transaction H (cont inued)

ACCTS. CLARK, CLARK, FEES WAGES RENT SUP. UTIL. MISC.

PAY. + CAPITAL – DRAW. + EARNED – EXP. – EXP. – EXP. – EXP. – EXP.400 25,000 7,500 –2,125 –800 –800 –450 –275Bal.

Liabilities + Owner’s Equity

h. –2,000

Bal.400 25,000 –2,000 7,500 –2,125 –800 –800 –450 –275

4

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 38/46

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 39/46

1-391-39

39

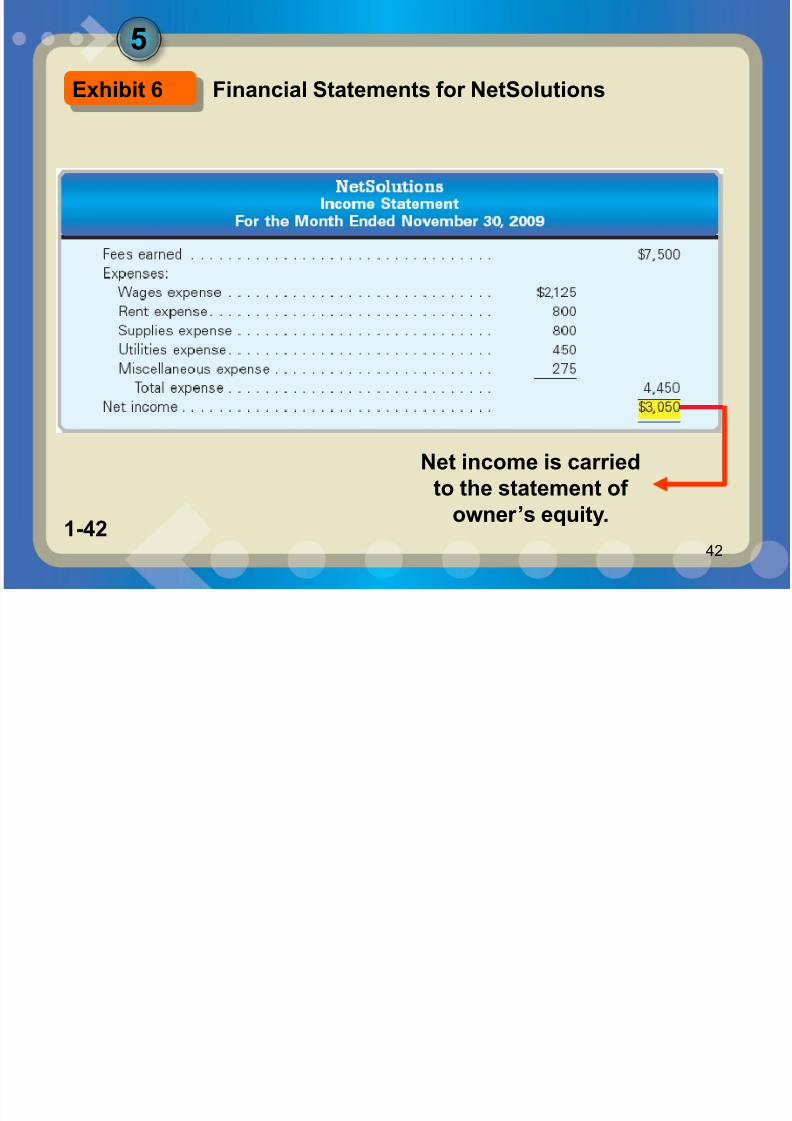

The income statement reports

the revenues and expenses fora period of time, based on thematching concept.

5

Income Statement

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 40/46

1-401-40

40

The matching concept is

applied by matching theexpenses with the revenuegenerated during a period by those expenses.

5

Matching Concept

5

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 41/46

1-411-41

41

The excess of revenue over the

expenses is called net income

or net prof it . If the expenses

exceed the revenue, the excess

is a net loss .

5

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 42/46

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 43/46

5

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 44/46

1-441-4444

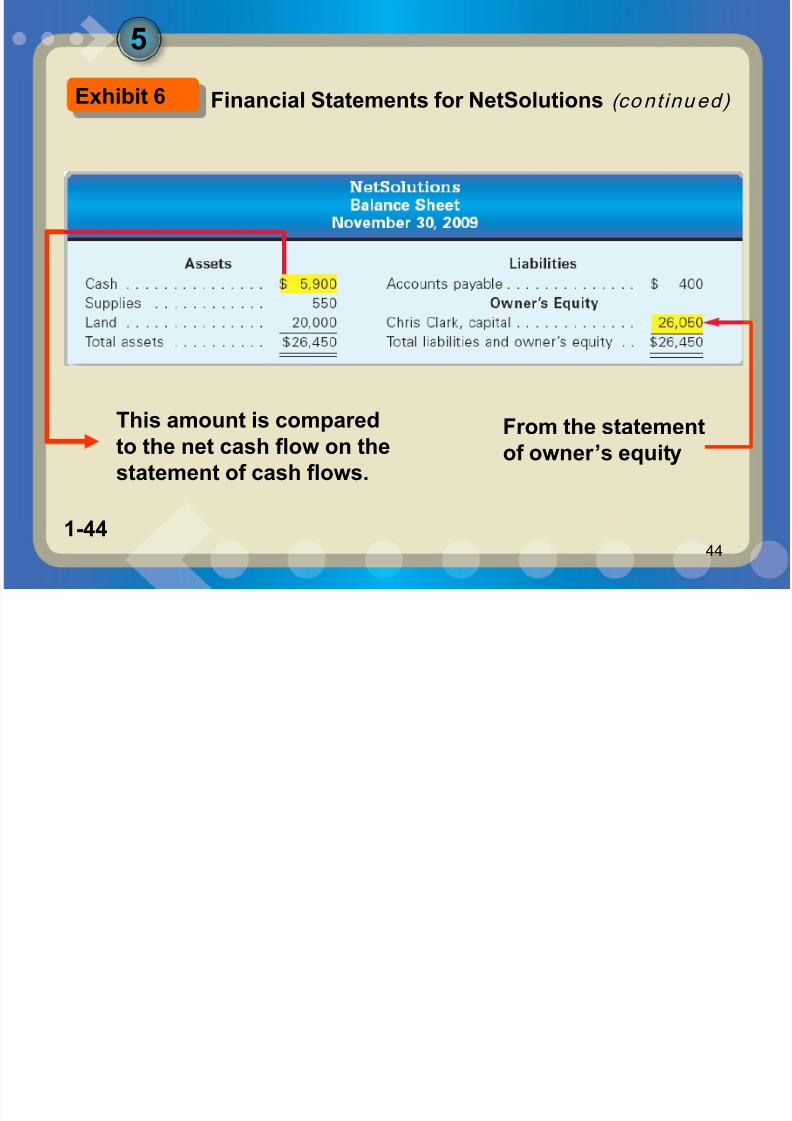

This amount is comparedto the net cash flow on the

statement of cash flows.

From the statementof owner’s equity

5

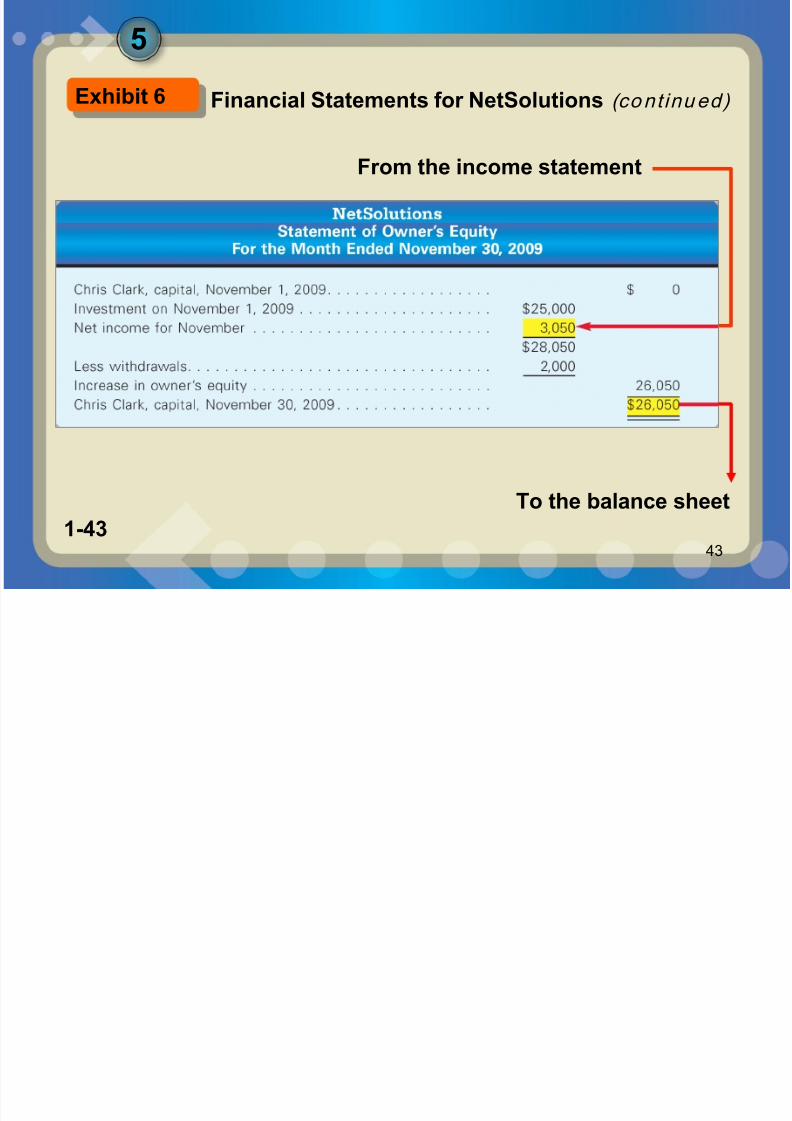

Exhibit 6 Financial Statements for NetSolutions (cont inued)

5

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 45/46

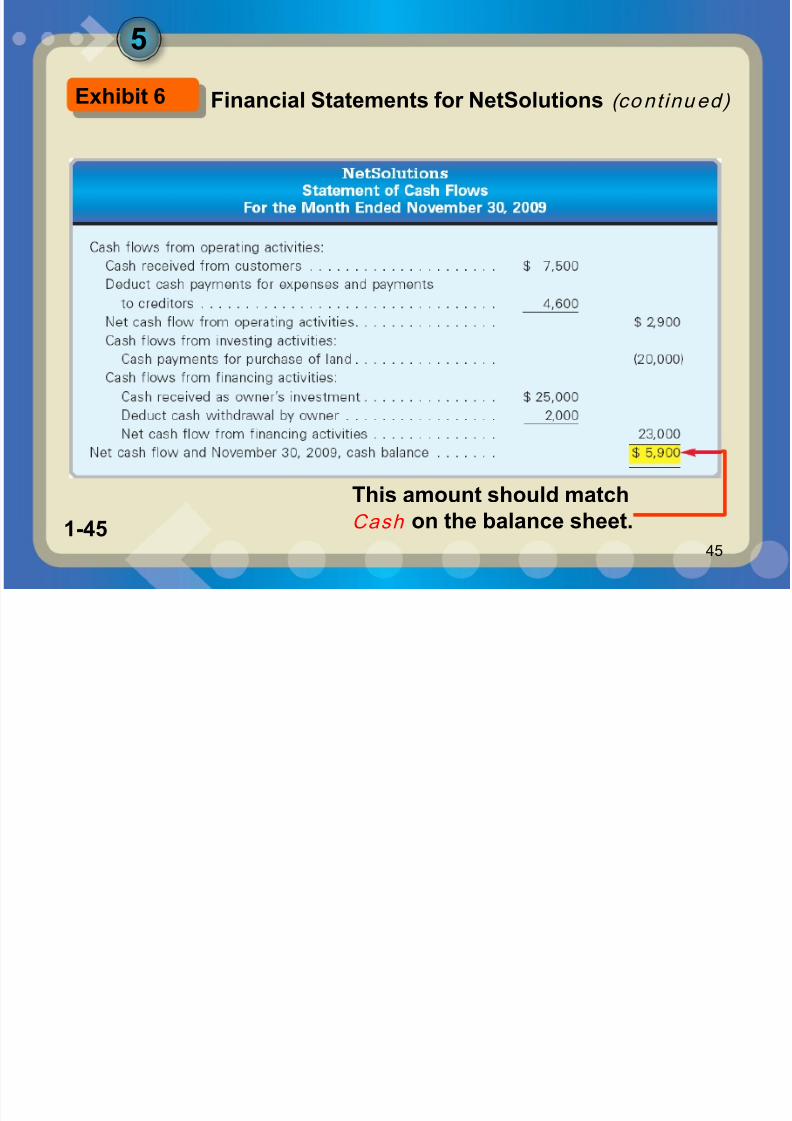

1-451-4545

This amount should match

Cash on the balance sheet.

5

Financial Statements for NetSolutions (cont inued) Exhibit 6

8/14/2019 WRD_ab.az.Ch01_SV Introduction to Acc

http://slidepdf.com/reader/full/wrdabazch01sv-introduction-to-acc 46/46

1-461-4646