Embed Size (px)

Citation preview

2011 Volume 47 Number 1

Please tick your box and pass this on:

■ CEO

■ Medical director

■ Nursing director

■ Head of radiology

■ Head of physiotherapy

■ Senior pharmacist

■ Head of IS/IT

■ Laboratory director

■ Head of purchasing

■ Facility manager

Editorial

Management

Hospital demand variations: suggested

instruments for hospital managers

Measuring availability, affordability and

management of essential medicines in public

hospitals of Burkina Faso

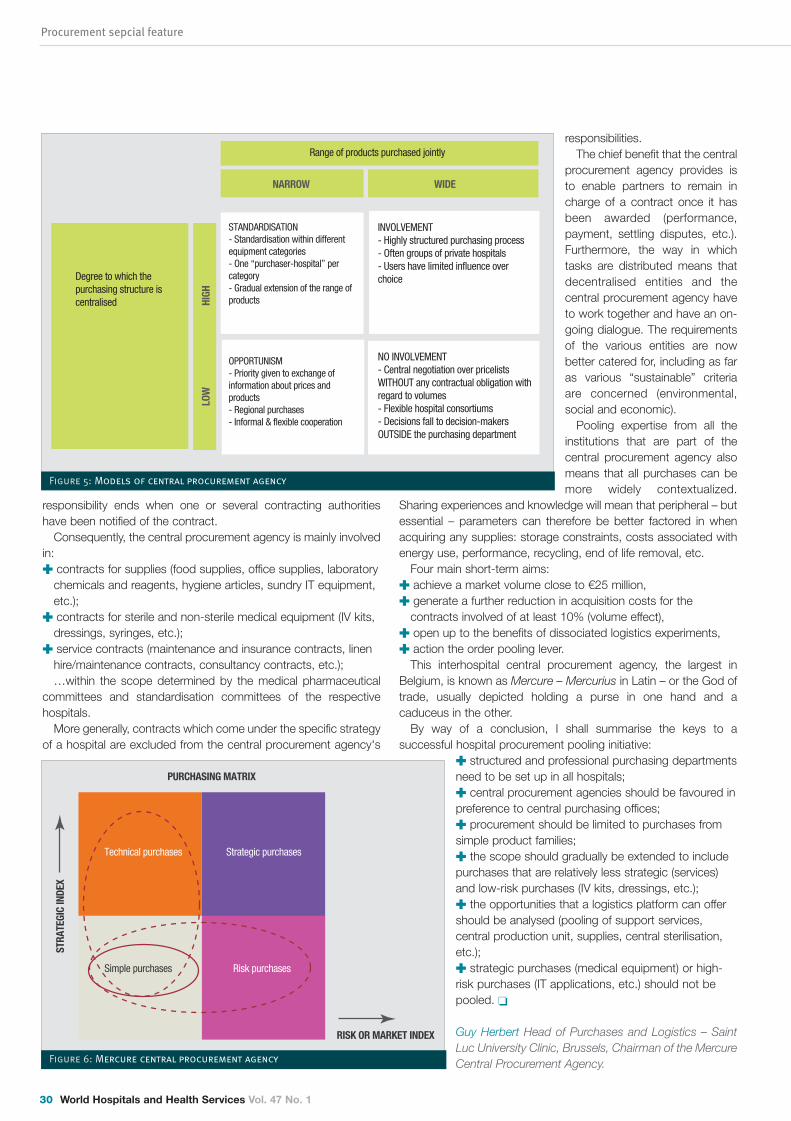

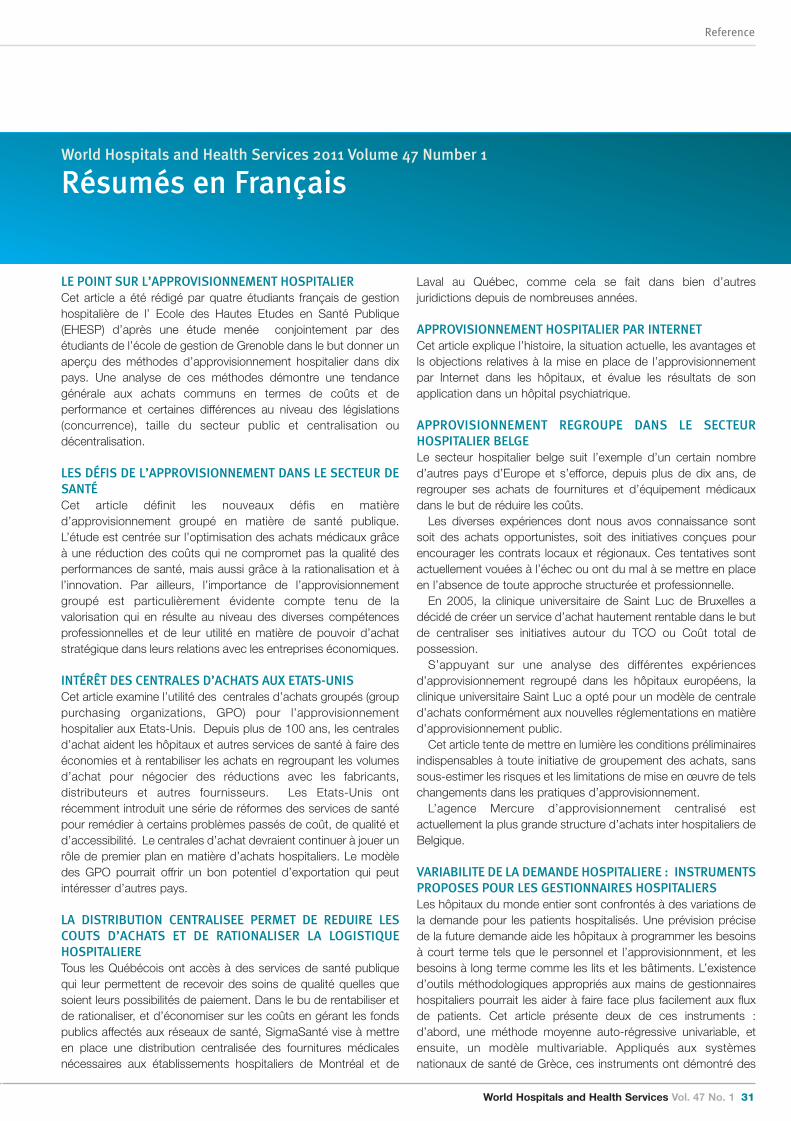

SSpecial feattuure: ProcurementInternational overview of hospital procurement

Centralized distribution: reducing ownership

costs by streamlining hospital logistics

The challenges of collaborative procuremement in

the healthcare sector

e-procurement in hospitals

The value of group purchassining organizations in

the United States

Pooling procuremenentt in the Belgian hospital

sector

World Hospitals and Health ServicesThe Official Journal of the International Hospital Federation

www.ihf-fih.org

C

M

Y

CM

MY

CY

CMY

K

00 cover vol47.1.ai 31/3/11 18:00:0400 cover vol47.1.ai 31/3/11 18:00:04

00-01 Contents 46_8:27 4/1/11 13:05 Page 1

World Hospitals and Health Services Vol. 47 No. 1 01

Contents

Contents volume 47 number 1

03 Editorial Eric de Roodenbeke

Management04 Hospital demand variations: suggested instruments for hospital managers

Zoe Boutsioli

08 Measuring availability, affordability and management of essential medicines in public hospitals of Burkina FasoHamado Saouadogo

Special feature: Procurement12 International overview of hospital procurement

Maud Ferrier, David Lariviere, Claire Laurent and Eric Roque

15 Centralized distribution: reducing ownership costs by streamlining hospital logistics Chantal S Laurin

18 The challenges of collaborative procurement in the healthcare sectorGabriella Margherita Racca

21 e-procurement in hospitalsJulio Villalobos Hidalgo, Joan Orrit and D Juan Pablo Villalobos

24 The value of group purchasing organizations in the United StatesCurtis Rooney

27 Pooling procurement in the Belgian hospital sectorGuy Herbert

Reference31 Language abstracts

34 IHF corporate partners

37 Governing Council list

39 Dates for your diary

Editorial StaffExecutive Editor: Eric de Roodenbeke, PhDDesk Editor: Ioana Rusu, MA.

Editorial BoardDr René PetersDutch Hospital Association Norberto LarrocaCamara Argentina de Empresas de SaludDr Harry McConnellGriffith University School of Medicine (Australia)Dr Persephone DoupiSTAKES

Editorial OfficeImmeuble JB SAY,13 Chemin du Levant, 01210 Ferney Voltaire, FranceEmail: [email protected] Internet: www.ihf-fih.org

Subscription OfficeInternational Hospital Federation c/o Fairfax House, 15 Fulwood Place, London WC1V 6AY, UKTelephone: +44 (0) 20 7969 5500;Facsimile: +44 (0) 20 7969 5600

ISSN: 0512-3135

Published by Pro-Brook Publishing Limited for the International Hospital Federation

6 Deben Mill Business CentreWoodbridgeSuffolk IP12 1BLUnited KingdomTel: +44 (0) 1394 446006 Fax: +44 (0) 1473 249034Internet: www.pro-brook.com

For advertising enquiries contact our CommunicationsManager at [email protected]

World Hospitals and Health Services is publishedquarterly. All subscribers automatically receive a copyof the IHF reference books. The annual subscription tonon-members for 2011 costs £175 or US$250.

World Hospitals and Health Services is listed inHospital Literature Index, the single mostcomprehensive index to English language articles onhealthcare policy, planning and administration. The index is produced by the American HospitalAssociation in co-operation with the National Library ofMedicine. Articles published in World Hospitals andHealth Services are selectively indexed in Health CareLiterature Information Network.

The International Hospital Federation (IHF) is anindependent non-political body whose aims are toimprove patient safety and promote health inunderserved communities. The opinions expressed inthis journal are not necessarily those of theInternational Hospital Federation or Pro-BrookPublishing Limited.

00-01 Contents 47_1:27 8/4/11 16:25 Page 1

Editorial

02 World Hospitals and Health Services Vol. 47 No. 1

Editorial

While this editorial is going to print, Japan is facing theworst natural disaster in its history. We want to expressour sympathy to all the people who have suffered and

still have to cope with the consequences of this terrible situation.Since the fifties, the Japan Hospital Association has been a pillarof our organization and in such circumstances, it is normal that theIHF Secretariat calls on other IHF members to offer support in oneform or another.

We would like to thank all those who have respondedimmediately at the request of our colleagues from Japan. Suchsupport expresses the solidarity that exists among us, as we knowthat we may all have to face harsh situations. It also highlights theimportance of international organizations such as IHF that createa venue for healthcare decision-makers to meet. Knowing eachother makes it easier to put in place a solidarity chain. We havehad the need for it in Japan, and we will certainly have similarneeds in the future. Mother Nature will continue to provide us withher beauty, but also reminds us that we are just guests whom shecan treat harshly when she decides to do so.

In a situation like the one in Japan, all those who require carehave to face an additional difficulty due to the conditions in whichthey have to live. Health workers have to face an additionalworkload resulting from the conditions and the casualties fromdisaster. First and foremost, the courage of the Japanese healthworkers has permitted coping with this massive destruction whichhas left so many people homeless. They have been on the frontline, however, it makes a difference for them to know that the restof world is behind them. IHF is not an emergency organization andis not equipped to provide rescue services. However, IHF hasmobilized and encouraged its members to make donations, andto provide in coordination with rescue organizations the criticalmedical consumables. The Japanese disaster has shown that ifresilient health facilities are critical to be able to respondimmediately to post disaster difficulties, there is urgent need formore than the goodwill of the people. Health workers needmedical consumables to deliver care.

In this edition of the World Hospitals and Health Services, we willbe presenting the importance of purchasing strategies for thehealthcare sector. One of the goals of group purchasing is toincrease standardization. Of course, by doing so, it is expected to

ERIC DE ROODENBEKE

CHIEF EXECUTIVE OFFICER, INTERNATIONAL HOSPITAL FEDERATION

have large volume allowing better commercial deals. But whatmay be more important is the standardization of healthcare,making it easier to cope with an unexpected upscaling of activitiesor a need to relocate part of the activities. This example illustrateswell that purchasing is not just about mastering the supply chainand getting best possible prices, but it is also a strategic issue forservice delivery.

IHF believes that purchasing is strategic. For this reason, it hasdecided to put in place a strong partnership with the newlycreated International Association of Group Purchasing (ASSIAPS)as well as to welcome large health care purchasers to become IHFassociate members and to have them create a dedicated chapter.IHF would also like to take this opportunity and thank Ile-de-France Hospital Buyers’ Network (Resah-idf) for its leadership androle in organizing the Purchasing Chapter. Resah-idf groups themajority of the public healthcare institutions in the Ile-de-Francearea. To learn more about the organization, please visithttp://www.resah-idf.com/. Resah-idf was also an active organizerand participant in the 2nd International Symposium on Hospital Procurement which took place last September in Paris (http://www.acheteurs-hospitaliers.com/index.asp). Thissymposium allowed the 400 participants present at the event todiscuss the challenges and prospects of change to procurementwithin the international healthcare sector. Within the PurchasingChapter, IHF will not get involved in the technical aspects relatedto purchasing (ASSIAPS is already doing this), but it will focus onthe policy implications of active purchasing strategies. As aplatform for cross fertilization, IHF is best placed to develop a newdynamic of dialogue between large purchasers from around theworld and large global providers. This may be accelerating theadoption of innovative approaches providing better value formoney.

An international overview of hospital procurement in over 10countries indicates that there is a trend in favour of grouppurchasing. There is, however, still a long way to go as the legalenvironment for procurement, and the differences in the setting ofhospitals does not yet allow full harmonization.

But before getting to harmonization, there is a strong need torely on effective collaboration. First, this collaboration must beinternal to allow all stakeholders within a facility to share the same

02-03 Editorial:29 7/4/11 14:19 Page 2

World Hospitals and Health Services Vol. 47 No. 1 03

Editorial

goals and realize them together with the appropriate inputs.Dialogue also needs to take place across borders to influence theproviders so that they shape their offer to respond to the evolvingdemand.

This effort to harmonize and to foster collaboration does notcome without a cost. The example of the US GPOs which aremore than a hundred year old demonstrates their role to containcost escalation, but also the permanent need to show that thetransaction costs are overridden by the purchasing benefits. Whilea major health reform has been launched in the US for improvingaccess to care, the GPOs will see their role strengthen to avoidthat an increase in demand for care will be fully translated in healthspending.

The Province of Quebec in Canada gives a good example of theimportance of strategic purchasing to curb cost trends in a publicsystem providing free care to all. Whether in public or privatesector and regardless of funding mechanisms, purchasing is nowfully considered an avenue for efficiency improvement.

In addition to implementing strategic purchasing, the e-procurement can allow the hospitals to move a step further. Therecent developments have shown how well designed e-procurement can reduce significantly transaction costs whileallowing better benchmarking of offering in a wider scale.

Group purchasing is often understood as seeking large volumesto get good prices. The example of Belgian hospitals gives anexcellent insight on the concept of the total cost of ownership. Thisconcept is the one guiding all effective purchasing and this is the

reason why dialogue is so important. These various articles on purchasing from both sides of the

Atlantic Ocean and from the largest health care market representa milestone to further invite IHF members to express their interestin this area. With the fast growing development of health caresector in the emerging world, the procurement is going to evolvewith healthcare providers becoming more and more international.The complexity of services offered to hospitals is also a challengethat purchasing organizations have to face.

Mirroring these articles on purchasing, I would you also like todraw your attention to two additional articles in this edition. Theyboth suggest that purchasing is to be related with the full masterof the supply chain in relation with the forecasting of activities.

In low income countries, mastering the supply chain remains thefirst priority. Although group purchasing has allowed reducedprices of essential drugs, it is not enough as the average availabilityof essential drugs remains under 80%. In Burkina Faso, forexample, when drugs are sold to the population, they represent animportant source of revenue, and this may be a challenge foraccessibility by the poor and trigger potential perversemechanisms. On the other hand, having a good forecast ofhospital care demand is not easy, as variation in demand eitherleads to excessive capital investment for avoiding out stocks or toperiodic stock failures as described in the case of Burkina Faso.The work developed in Greece to improve the forecasting ofactivities can allow better mobilization of all inputs and a bettermastering of the supply chain. �

02-03 Editorial:29 7/4/11 14:19 Page 3

Management

4 World Hospitals and Health Services Vol. 47 No. 1

Hospital demand variations: suggestedinstruments for hospital managersi

ABSTRACT: Hospitals worldwide face variations in demand for inpatient care. The accurate forecasting of future demandassists hospitals in programming short-term needs such as staff and supplies, and long-term needs such as beds andbuildings. The existence of the appropriate methodological instruments, applied by hospital managers, could help themsmooth down upcoming patient flows. This work presents two such instruments: first, a univariate autoregressive movingaverage method, and second, a multivariate model. By applying these to the Greek National Health System, we have foundsignificant demand variations. The univariate method provides more accurate forecasting of future unexpected demand.

Hospitals worldwide face considerable demand variations(Smet, 2007; Baker et al., 2004; Hughes & McGuire, 2003;Boutsioli, 2009). Some of these variations are unexpected.

The accurate forecasting of future demand assists hospitals inprogramming short-term needs, such as staff and supplies, andlong-term needs such as beds and buildings. The existence ofappropriate methodological instruments applied by hospitalmanagers could help them smooth down upcoming patient flows.In the literature, two approaches have been mostly used toforecast future hospital demand and particularly the unexpectedpart of demand. The first approach is a univariate autoregressivemoving average (ARMA) model. ARMA is a regression model,where the explanatory variables are lags of the dependentvariable. The model is made of two parts. The first part is theautoregressive part, i.e. hospital daily admissions depend onprevious daily admissions; the second part is the moving averagepart (MA), i.e. an average of all past errors made in predictinghospital admissions. Hospital emergency admissions are used asthe dependent variable to estimate unexpected demand.According to this model, the unexpected demand is based on aresidual estimate of forecasted daily emergency demand. Thus,the level of unexpected demand faced by a hospital is defined asthe difference between realized and forecasted emergencydemand, gained from the ARMA forecasting model (Hughes &McGuire, 2003; Boutsioli, 2010). The second method refers to amultivariate model that unexpected hospital demand is a functionof a number of explanatory variables. The most commonly usedvariables include the day of the week, i.e. the weekend, the “duty”status of the hospital, the summer and the official holiday effects(Hussain et al., 2005; Baker et al., 2004; Fullerton & Crawford,1999; Upshur et al., 2005).

Hospital demand variations in the Athenian hospital context The Greek public hospitals belong to a National Health System

DR ZOE BOUTSIOLI

RESEARCHER, HEALTH RESEARCH UNIT, ATHENS INSTITUTE FOR

EDUCATION AND RESEARCH (ATINER)

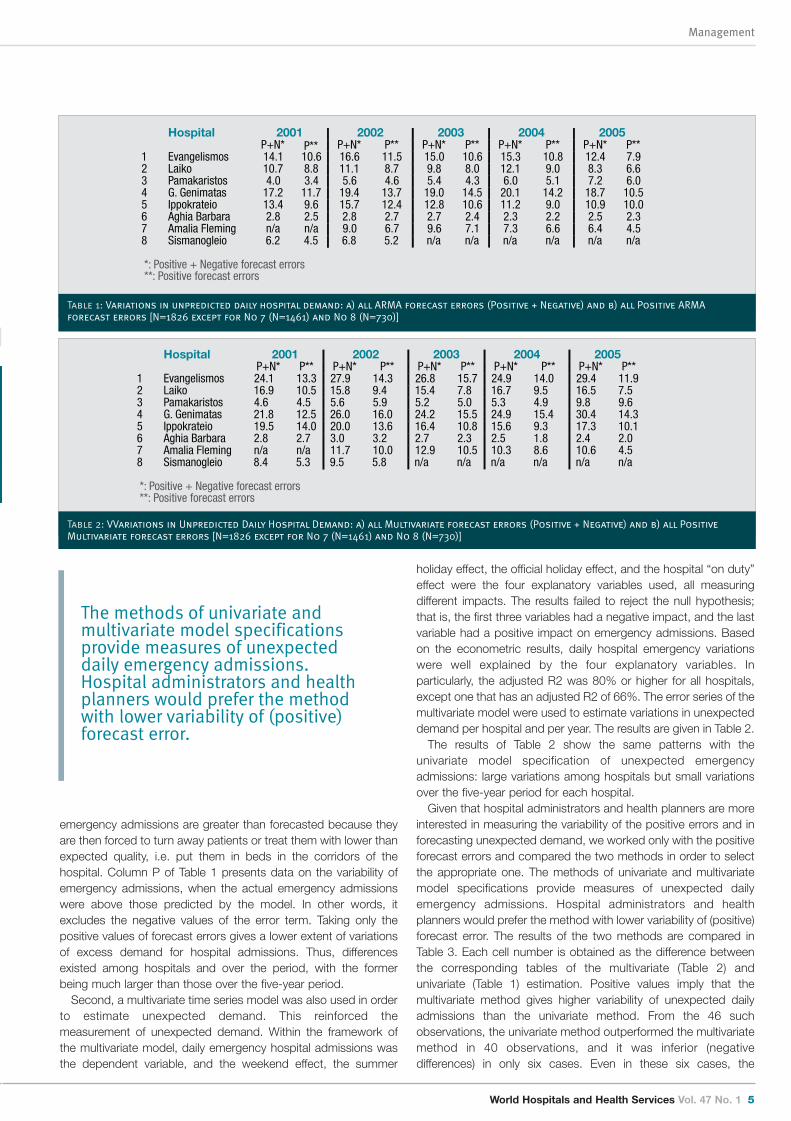

(NHS). We collected daily data of patient emergency admissionsfrom eight Athenian public hospitals from 2001 to 2005. First, weapplied the ARMA method to emergency hospital admissions datato estimate daily measures of unexpected demand. In the test forstationarity of daily emergency admissions, it was found that thenull hypothesis of unit root was rejected at the 1% level ofsignificance, implying that the series are stationary at that level.Based on the criteria proposed by Akaike and Schwarz, weselected the best ARMA model specification. The lower the valuesof the Akaike-Schwartz criterion, the most appropriate the ARMAmodel. Each hospital’s estimation process provides an estimate ofthe residual (_t), which is the unpredicted part of emergency dailyadmissions. These residuals had a zero mean, and their standarddeviation was constant. To estimate the average daily variations ofunexpected demand, we used two ways: a) all the residualsforecasts, both positive and negative, and b) only the positivevalues of forecast errors. These are positive when actual(emergency admissions) are more than the fitted, while they arenegative when the actual are less than the fitted. In case (a), if wesum up the residuals they should be equal to zero, according tothe theory. To overcome this, we have taken the absolute valuesof the negative forecast errors. In case (b), we call this “excessdemand” for unexpected admissions. Table 1 reports measures ofthe standard deviations of unpredicted emergency admissions perhospital per year. The unpredicted part of emergency admissionswas not the same for each hospital, and it also varied over theyears.

The results reported in P+N column of Table 1 treat variations ofdaily emergency admissions as equal around its mean. However,of importance for the hospital manager are the cases that

i This paper is part of my PhD thesis in the University of Kent, UK. I thank very muchfor their support and guidance Professor Ann Netten, University of Kent, UK andProfessor Alastair Gray, University of Oxford, UK.

04-07 Boutsioli:29 31/3/11 18:10 Page 4

World Hospitals and Health Services Vol. 47 No. 1 5

Management

emergency admissions are greater than forecasted because theyare then forced to turn away patients or treat them with lower thanexpected quality, i.e. put them in beds in the corridors of thehospital. Column P of Table 1 presents data on the variability ofemergency admissions, when the actual emergency admissionswere above those predicted by the model. In other words, itexcludes the negative values of the error term. Taking only thepositive values of forecast errors gives a lower extent of variationsof excess demand for hospital admissions. Thus, differencesexisted among hospitals and over the period, with the formerbeing much larger than those over the five-year period.

Second, a multivariate time series model was also used in orderto estimate unexpected demand. This reinforced themeasurement of unexpected demand. Within the framework ofthe multivariate model, daily emergency hospital admissions wasthe dependent variable, and the weekend effect, the summer

holiday effect, the official holiday effect, and the hospital “on duty”effect were the four explanatory variables used, all measuringdifferent impacts. The results failed to reject the null hypothesis;that is, the first three variables had a negative impact, and the lastvariable had a positive impact on emergency admissions. Basedon the econometric results, daily hospital emergency variationswere well explained by the four explanatory variables. Inparticularly, the adjusted R2 was 80% or higher for all hospitals,except one that has an adjusted R2 of 66%. The error series of themultivariate model were used to estimate variations in unexpecteddemand per hospital and per year. The results are given in Table 2.

The results of Table 2 show the same patterns with theunivariate model specification of unexpected emergencyadmissions: large variations among hospitals but small variationsover the five-year period for each hospital.

Given that hospital administrators and health planners are moreinterested in measuring the variability of the positive errors and inforecasting unexpected demand, we worked only with the positiveforecast errors and compared the two methods in order to selectthe appropriate one. The methods of univariate and multivariatemodel specifications provide measures of unexpected dailyemergency admissions. Hospital administrators and healthplanners would prefer the method with lower variability of (positive)forecast error. The results of the two methods are compared inTable 3. Each cell number is obtained as the difference betweenthe corresponding tables of the multivariate (Table 2) andunivariate (Table 1) estimation. Positive values imply that themultivariate method gives higher variability of unexpected dailyadmissions than the univariate method. From the 46 suchobservations, the univariate method outperformed the multivariatemethod in 40 observations, and it was inferior (negativedifferences) in only six cases. Even in these six cases, the

Hospital 2001 2002 2003 2004 2005P+N* P** P+N* P** P+N* P** P+N* P** P+N* P**

1 Evangelismos 14.1 10.6 16.6 11.5 15.0 10.6 15.3 10.8 12.4 7.92 Laiko 10.7 8.8 11.1 8.7 9.8 8.0 12.1 9.0 8.3 6.63 Pamakaristos 4.0 3.4 5.6 4.6 5.4 4.3 6.0 5.1 7.2 6.04 G. Genimatas 17.2 11.7 19.4 13.7 19.0 14.5 20.1 14.2 18.7 10.55 Ippokrateio 13.4 9.6 15.7 12.4 12.8 10.6 11.2 9.0 10.9 10.06 Aghia Barbara 2.8 2.5 2.8 2.7 2.7 2.4 2.3 2.2 2.5 2.37 Amalia Fleming n/a n/a 9.0 6.7 9.6 7.1 7.3 6.6 6.4 4.58 Sismanogleio 6.2 4.5 6.8 5.2 n/a n/a n/a n/a n/a n/a

*: Positive + Negative forecast errors **: Positive forecast errors

Table 1: Variations in unpredicted daily hospital demand: a) all ARMA forecast errors (Positive + Negative) and b) all Positive ARMA

forecast errors [N=1826 except for No 7 (N=1461) and No 8 (N=730)]

Hospital 2001 2002 2003 2004 2005P+N* P** P+N* P** P+N* P** P+N* P** P+N* P**

1 Evangelismos 24.1 13.3 27.9 14.3 26.8 15.7 24.9 14.0 29.4 11.92 Laiko 16.9 10.5 15.8 9.4 15.4 7.8 16.7 9.5 16.5 7.53 Pamakaristos 4.6 4.5 5.6 5.9 5.2 5.0 5.3 4.9 9.8 9.64 G. Genimatas 21.8 12.5 26.0 16.0 24.2 15.5 24.9 15.4 30.4 14.35 Ippokrateio 19.5 14.0 20.0 13.6 16.4 10.8 15.6 9.3 17.3 10.16 Aghia Barbara 2.8 2.7 3.0 3.2 2.7 2.3 2.5 1.8 2.4 2.07 Amalia Fleming n/a n/a 11.7 10.0 12.9 10.5 10.3 8.6 10.6 4.58 Sismanogleio 8.4 5.3 9.5 5.8 n/a n/a n/a n/a n/a n/a

*: Positive + Negative forecast errors **: Positive forecast errors

Table 2: VVariations in Unpredicted Daily Hospital Demand: a) all Multivariate forecast errors (Positive + Negative) and b) all Positive

Multivariate forecast errors [N=1826 except for No 7 (N=1461) and No 8 (N=730)]

The methods of univariate andmultivariate model specificationsprovide measures of unexpecteddaily emergency admissions.Hospital administrators and healthplanners would prefer the methodwith lower variability of (positive)forecast error.

04-07 Boutsioli:29 31/3/11 18:10 Page 5

admissions. Only in one hospital was the maximum value of theunivariate estimation higher, by two admissions.

Discussion and ConclusionsIn conclusion, this paper discusses two different ways to measureunexpected hospital demand: a univariate model and amultivariate model specification. The univariate model waspreferred because it required the least information, i.e. only thepast values of the variable to be estimated, and provided betterestimates. The univariate method made the lower forecasting errorin terms of the variability, the mean and maximum values of thepositive forecast errors. However, the multivariate model is veryimportant in the hands of policy-makers because if unexpecteddemand raises hospital costs, then the multivariate model can givesome guidance to hospital administrators on how to reduce thevariability of emergency admissions. However, two points shouldbe made here. First, the two models do not have the samepracticality of use by hospital managers and health planners. Themultivariate model is more straightforward and it can be easilyapplied because the four explanatory variables are easilyobservable. For example, it is easy to forecast that during thesummer holidays or the weekends, fewer admissions should beexpected. On the other hand, hospital managers do not use anARMA model to make forecasts, even though they should.

difference was very small and very close to zero. The mean of the total (positive and negative) unpredicted

demand was by definition equal to zero, but that of the positiveforecast errors was not. It was important to compare the twomethods in terms of the mean and maximum values of the positiveerrors. Table 4 reports the mean and the maximum values of thepositive errors in predicting daily unexpected emergency demandper hospital. The data refer to the entire period underconsideration (2001–2005) because as we have shown,differences per year for the same hospital are not very large. In allcases but one, the univariate method outperformed themultivariate method of estimating unexpected emergency

Management

6 World Hospitals and Health Services Vol. 47 No. 1

Hospital 2001 2002 2003 2004 20051 Evangelismos 2.70 2.74 5.04 3.15 4.002 Laiko 1.72 0.76 -0.19 0.53 0.873 Pamakaristos 1.16 1.33 0.63 -0.29 3.684 G. Genimatas 0.83 2.30 1.00 1.22 3.785 Ippokrateio 4.33 1.21 0.23 0.24 0.456 Aghia Barbara 0.17 0.49 -0.09 -0.40 -0.317 Amalia Fleming n/a 3.19 3.41 2.05 0.028 Sismanogleio 0.80 0.64 n/a n/a n/a

Table 3: Comparison of Multivariate and Methods of Estimating Variations in Unexpected Daily Emergency Admissions (Differences in

standard deviations)

[N=1826 except for No 7 (N=1461) and No 8 (N=730)]

Hospital Multivariate:Mean

Univariate:Mean

Mean Dif.

Multivariate:Maximum

Univariate:Maximum

Max. Dif.

1 Evangelismos 30.01 9.93 20.08 80.53 62.36 18.172 Laiko 17.94 6.86 11.08 55.76 55.16 0.63 Pamakaristos

6.57 3.59 2.98 36.79 38.43-

1.644 G. Genimatas 23.83 14.49 9.34 90.23 85.13 5.15 Ippokrateio 17.94 8.03 9.91 79.31 75.56 3.756 Aghia Barbara 1.77 1.43 0.34 18.85 18.30 0.557 Amalia Fleming 9.27 6.29 2.98 49.92 42.61 7.318 Sismanogleio 8.38 4.6 3.78 28.37 24.42 3.95

Table 4: Comparison of Multivariate and Methods of Estimating Variations in Unexpected Daily Emergency Admissions (mean and maximum

values)

[N=1826 except for No 7 (N=1461) and No 8 (N=730)]

ii This paper is part of my PhD thesis in the University of Kent, UK. I thank very muchfor their support and guidance Professor Ann Netten, University of Kent, UK andProfessor Alastair Gray, University of Oxford, UK.

The univariate model was preferredbecause it required the leastinformation, i.e. only the past valuesof the variable to be estimated, andprovided better estimates. Theunivariate method made the lowerforecasting error in terms of thevariability, the mean and maximumvalues of the positive forecast errors.

04-07 Boutsioli:29 31/3/11 18:10 Page 6

World Hospitals and Health Services Vol. 47 No. 1 7

Management

Second, the better performance of the univariate modelcompared to the multivariate modelii is to a large extent due tovariables omitted from the multivariate model. Unfortunately,important determinants of emergency admissions are not availableon a daily basis, resulting in inferior forecasts by the multivariatemodel. �

Dr Zoe Boutsioli holds a PhD in Social Policy and a MSc inInternational Health Policy. She has published a number of researchpapers on various peer-reviewed journals. Her research interestsfocuses on hospital economics, policy and management.

References1. 1. Baker, L.C., C.S. Phibbs, C. Guarino, D. Supina and J.L. Reynolds (2004). Within-year

Variation in Hospital Utilization and its Implications for Hospital Costs. Journal of HealthEconomics, 23, 191-211.

2. Boutsioli, Z. (2009). Measuring unexpected hospital demand: the application of a univariatemodel to public hopsitals in Greece. Hospital Topics 87(4, Fall): 14-21.

3. Fullerton, K.J. and V.L.S. Crawford (1999). The Winter Bed Crisis – Quantifying SeasonalEffects on Hospital Bed Usage. Quarterly Journal of Medicine: An International Journal ofMedicine, 92(4), 199-206.

4. Hughes, D. and A. McGuire (2003). Stochastic Demand, Production Responses and HospitalCosts. Journal of Health Economics, 22(6), 999-1010.

5. Hussain, S., R. Harrison, J. Ayres, S. Walter, J. Hawker, R. Wilson and G. Shukur (2005).Estimating and Forecasting Hospital Admissions due to Influenza: Planning for WinterPressure – The Case of the West Midlands, UK. Journal of Applied Statistics, 32(3), 191-205.

6. Smet, M. (2007). Measuring Performance in the Presence of Stochastic Demand for HospitalServices: An Analysis of Belgian General Care Hospitals. Journal of Production Annals, 27,13-29.

7. Upshur, R.E.G., R. Moineddin, E. Crighton, L. Kiefer and M. Mamdani (2005). Simplicity withinComplexity: Seasonality and Predictability of Hospital Admissions in the Province of Ontario1988-2001 – A Population-based Analysis. Health Services Research, 5(13)

04-07 Boutsioli:29 31/3/11 18:10 Page 7

Management

8 World Hospitals and Health Services Vol. 47 No. 1

Measuring availability, affordability andmanagement of essential medicines inpublic hospitals of Burkina Faso

ABSTRACT: In Burkina Faso, improving healthcare services and the availability of pharmaceutical productsconstitute a growing concern for the population. This study objective was to evaluate the availability, prices, andsales revenue for a grouping of 50 basic medications in public hospitals from 29 September – 29 December 2009.

The method used to study the prices, availability, affordability and price components from Health ActionInternational (HAI) and the World Health Organization (WHO) has been used to collect and analyze the data.

The results show that the average ratio between the pharmaceutical budget and that of the health centre is16.18. The average rate of availability was 77.69%.

The purchasing price from the hospitals providers is approximately the same as the international referenceprices (1.12). The public hospitals selling price to the public was double the buying price from their provider (2.20).

The total sales revenue from the first three trimesters of 2009 was 708,740,495 FCFA (€1,080,397). This revenueaccounted for roughly 23.02% of the total costs for available pharmaceuticals during the period (3,078,938,053FCFA/€4,693,503).

Faced with a growingdemand to improve themanner of supplying health

services and the place ofmedications and other medicalservices within hospitals, thedevelopment of a central hospitalpharmacy currently presents itselfas an inevitable strategy for theBurkinabé government.

The objective of hospital reformwas to increase the sector’sfunctionality and permit thesector to better place its rights,obligations, and responsibilitiesface-to-face with institutions andpatients. In order to reach thisobjective, each hospital mustassure equal and efficient accessto the health care available.

Pharmaceutical care bringstogether all pharmaceutical acts,from the acquisition to theobservance of treatment, thevigilance and ongoing patient care, and constitutes the centralpillar of healthcare. This care is the heart of each hospital unit andmust be performed with professionalism and dynamism.

Anxious to make public hospitals higher functioning, thegovernment has put in place a legislative framework and

DR HAMADO SAOUADOGO

MINISTRY OF HEALTH, BURKINA FASO

regulations to facilitate a better development of thepharmaceutical hospital sector.

Objective of the studyTo evaluate the availability, prices of a grouping of 50 essential

27

1411

1815

12 12

21

12

0

5

10

15

20

25

30

CHU

YO

CHU

P

CHU

SS

BANF

ORA

DEDO

UGOU

DORI

FADA

GAOU

A

KAYA

KOUD

OUGO

U

OUAH

IGOU

YA

TENK

ODOG

O

Ratio BPP/BT CH

Perc

enta

ge

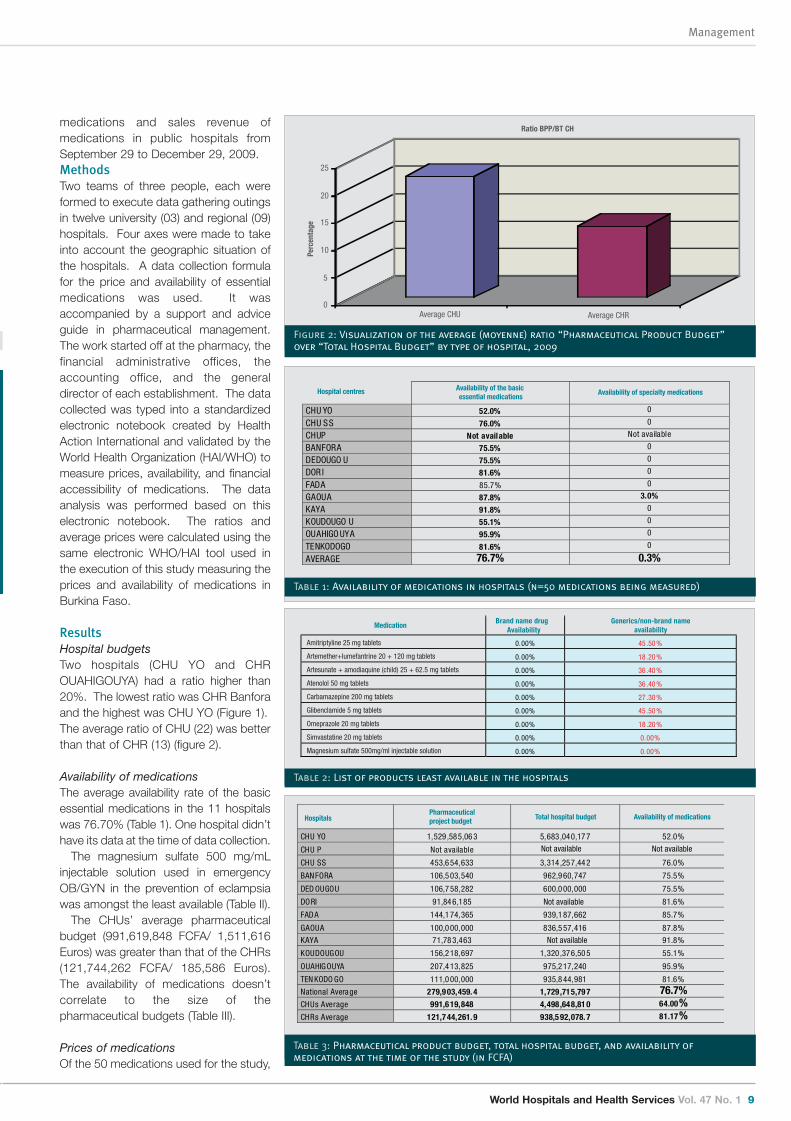

Figure 1: Visualization of the ratio “Pharmaceutical Product Budget” (BPP) over “Total

Hospital Budget,” (BT) 2009

08-11 burkina faso:29 31/3/11 18:13 Page 8

World Hospitals and Health Services Vol. 47 No. 1 9

Management

medications and sales revenue ofmedications in public hospitals fromSeptember 29 to December 29, 2009.MethodsTwo teams of three people, each wereformed to execute data gathering outingsin twelve university (03) and regional (09)hospitals. Four axes were made to takeinto account the geographic situation ofthe hospitals. A data collection formulafor the price and availability of essentialmedications was used. It wasaccompanied by a support and adviceguide in pharmaceutical management.The work started off at the pharmacy, thefinancial administrative offices, theaccounting office, and the generaldirector of each establishment. The datacollected was typed into a standardizedelectronic notebook created by HealthAction International and validated by theWorld Health Organization (HAI/WHO) tomeasure prices, availability, and financialaccessibility of medications. The dataanalysis was performed based on thiselectronic notebook. The ratios andaverage prices were calculated using thesame electronic WHO/HAI tool used inthe execution of this study measuring theprices and availability of medications inBurkina Faso.

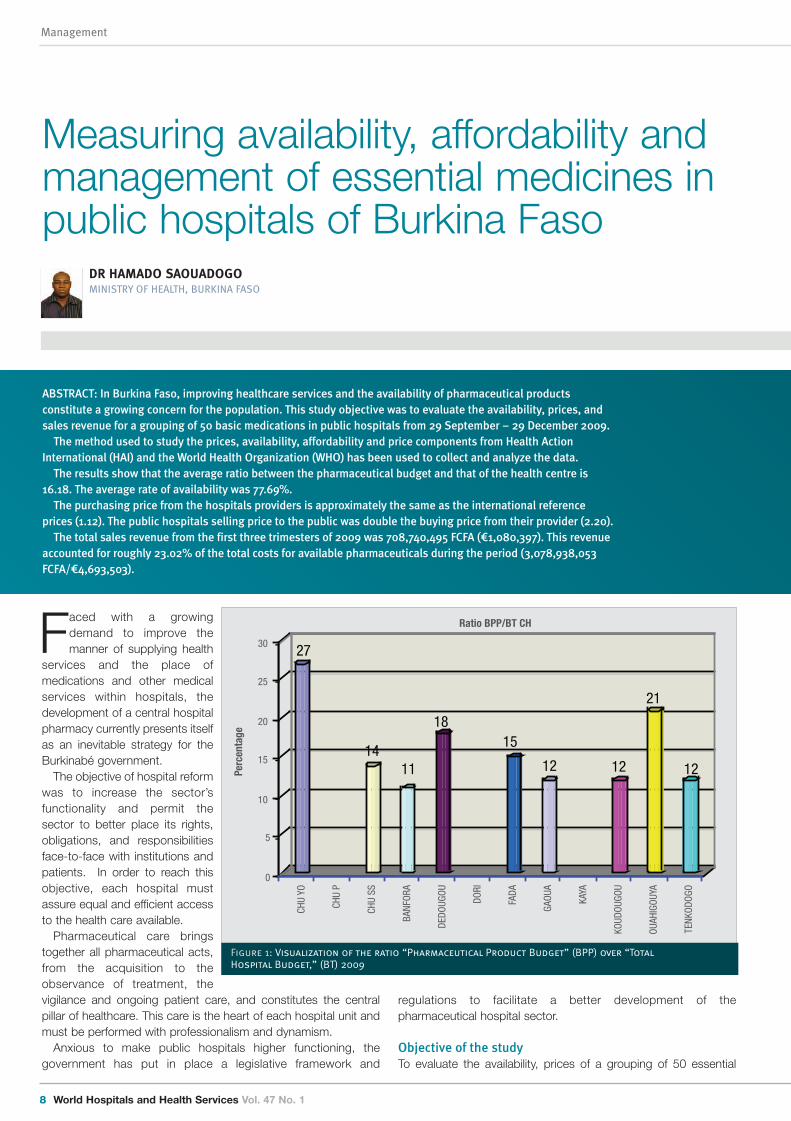

ResultsHospital budgetsTwo hospitals (CHU YO and CHROUAHIGOUYA) had a ratio higher than20%. The lowest ratio was CHR Banforaand the highest was CHU YO (Figure 1).The average ratio of CHU (22) was betterthan that of CHR (13) (figure 2).

Availability of medicationsThe average availability rate of the basicessential medications in the 11 hospitalswas 76.70% (Table 1). One hospital didn’thave its data at the time of data collection.

The magnesium sulfate 500 mg/mLinjectable solution used in emergencyOB/GYN in the prevention of eclampsiawas amongst the least available (Table II).

The CHUs’ average pharmaceuticalbudget (991,619,848 FCFA/ 1,511,616Euros) was greater than that of the CHRs(121,744,262 FCFA/ 185,586 Euros).The availability of medications doesn’tcorrelate to the size of thepharmaceutical budgets (Table III).

Prices of medicationsOf the 50 medications used for the study,

0

5

10

15

20

25

Average CHU Average CHR

Ratio BPP/BT CH

Perc

enta

ge

Figure 2: Visualization of the average (moyenne) ratio “Pharmaceutical Product Budget”

over “Total Hospital Budget” by type of hospital, 2009

CHU YO 52.0% 0

CHU SS 76.0% 0

CHUP Not available Not available

BANFORA 75.5% 0

DEDOUGO U 75.5% 0

DOR I 81.6% 0

FADA 85.7% 0

GAOUA 87.8% 3.0%

KAYA 91.8% 0

KOUDOUGO U 55.1% 0

OUAHIGO UYA 95.9% 0

TENKODOGO 81.6% 0

AVERAGE 76.7% 0.3%

Hospital centres Availability of the basic essential medications

Availability of specialty medications

Table 1: Availability of medications in hospitals (n=50 medications being measured)

MedicationBrand name drug

Availability

0.00% 45 .50%

0.00% 18 .20%

0.00% 36 .40%

0.00% 36 .40%

0.00% 27 .30%

0.00% 45 .50%

0.00% 18 .20%

0.00% 0.00%

0.00% 0.00%

Generics/non-brand nameavailability

Amitriptyline 25 mg tablets

Artemether+lumefantrine 20 + 120 mg tablets

Artesunate + amodiaquine (child) 25 + 62.5 mg tablets

Atenolol 50 mg tablets

Carbamazepine 200 mg tablets

Glibenclamide 5 mg tablets

Omeprazole 20 mg tablets

Simvastatine 20 mg tablets

Magnesium sulfate 500mg/ml injectable solution

Table 2: List of products least available in the hospitals

CHU YO 1,529,585,06 3 5,683,040,17 7 52.0%

CHU P Not available

CHU SS 453,6 54,633 3,314,257,44 2 76.0%

BANFORA 106,5 03,540 962,9 60,747 75.5%

DED OUGOU 106,7 58,282 600,0 00,000 75.5%

DORI 91,84 6,185 Not available 81.6%

FADA 144,1 74,365 939,1 87,662 85.7%

GAOUA 100,0 00,000 836,5 57,416 87.8%

KAYA 71,78 3,463 91.8%

KOUDOUGOU 156,2 18,697 1,320,376,50 5 55.1%

OUAHIGOUYA 207,4 13,825 975,2 17,240 95.9%

TEN KODO GO 111,0 00,000 935,8 44,981 81.6%

National Average 279,9 03,459. 4 1,729,715,79 7 76.7%CHUs Average 991,6 19,848 4,498,648,81 0 64.00%CHRs Average 121,7 44,261. 9 938,5 92,078. 7 81.17%

HospitalsPharmaceuticalproject budget Total hospital budget Availability of medications

Not available

Not available Not available

Table 3: Pharmaceutical product budget, total hospital budget, and availability of

medications at the time of the study (in FCFA)

08-11 burkina faso:29 31/3/11 18:13 Page 9

pharmaceuticals is important to thehospital, the more the medications areavailable.

A study performed in 2008 indicated thatthe absence of financial autonomy inpharmacies played into the quality ofmanagement and availability ofmedications. The absence of frank actionby the General Directors to put in place ahospital pharmacy policy also contributesto the lack of availability of medications.Also the absence of a central pharmacy forall hospitals is a handicap against greatermedication availability in hospitals. Finally,the absence of a health insurance systemdoes not favour the working of a basicpatient care system and plays into thequality of medication management.

The study for measuring medicine prices,availability, affordability and pricescomponents in Burkina Faso at 2009indicated that the existing low householdbuying power was also a negative factoragainst the creation of a good hospital

pharmacy policy. The recourse to social service and non-paymentof bills following un-prepaid urgent care can be seen as proof ofthis (Saouadogo, 2011).

ConclusionThis study allowed for the following of four principle indicators ofquality pharmaceutical management in the hospital setting. Theseindicators are measures of the ratio of the budget forpharmaceutical products over the total hospital budget, of theavailability rate of a grouping of 50 essential medications, of theprice ratio between the public selling price and the buying pricefrom the supplier, and of the financial value of the sales revenue ofthese medications. The results show that the pharmaceuticalmanagement in the hospital setting still needs additionalreinforcement. Also, the difference between the buying price CIFOuagadougou from the suppliers and the public selling price athospitals is 97%. As a result, the sales revenue has been weakerbut the patients are paying double the supply price. Finally, manyfactors affect the composition of the price of medications anddecrease household accessibility despite the introduction of thecommon exterior tariff (TEC) by the West-African Monetary andEconomic Union (UEMOA). This is why solid, rigorously followed,and evaluated hospital pharmacy policy is necessary in the region.

RecommendationsTo improve the following legislation frameworks :� Decree No. 2008-297/PRES/PM/MEF concerning the

accounting and financial Public State Establishments (PSE) ofBurkina Faso.

� Decree No. 2008-173/PRES/PM/MEF concerning generalrules of public functioning and the delegation of public servicesin Burkina Faso.

� Decree No. 2004-191/PRES/PM/MFB concerning the generalstatus of PSE; Decree No. 2006-355/PRES/PM/MS/MESSRS/MFB concerning the particularstatus of CHU; and Decree No. 2006 356/PRES/PM/MS/

41 were found at the bulk dealer and in the hospitals. The ratio ofthe average buying price from the bulk dealer is 1.12. However,the ratio of average selling price to the public is 2.20, producing adifference of 97%. The selling price to the public is double thetotal buying price from the distributor (Table IV).

Sales revenue for medicationsTotal sales of medications during the first three trimesters of 2009in Burkina Faso hospitals during the data collection period were708,740,495 FCFA (1,080,397 Euros). Sales revenue from CHUYO accounted for 31% of total sales, followed by CHU SS(21.94%). Amongst the CHR, Banfora’s sales revenue was thehighest and Dedougou’s was lowest (Table V).

DiscussionAccording to the WHO, a hospital’s pharmaceutical productsbudget must be between 20 and 40% of the hospital’s totalbudget. In Burkina Faso, the CHU YO has a ratio of 27, but theavailability of essential pharmaceutical products was only 52% andone of the lowest of all the hospitals. The average availability ratewas 64% in the CHUs and 81.2% in the CHRs, indicating that apatient has more ease of access to these essential medications ina CHR than in a CHU during the period we conducted our study.During the same period, amongst Burkina Faso’s hospitals, theCHR of Ouahigouya presented the greatest availability of studiedmedications. In most cases, the more budget put aside for

Management

10 World Hospitals and Health Services Vol. 47 No. 1

According to the WHO, ahospital’s pharmaceuticalproducts budget must bebetween 20 and 40% of thehospital’s total budget

Buying from bulkvendor

(n=1 sale )

Hospitals’ se llingprice to the public(n=11 hospitals)

Number ofmedications

found

% difference between hospitals’ PSP and the initial cost from

the bulk vendor

GenericMedications

1.12 2.20 41 96.8%

Table 4: Comparison of the average public selling prices (PSP) and the buying price from

the bulk vendor of generic medications found in hospitals (n=41 medications of the 50

being studied)

Hospitals Percent

CHU Y O 218,3 94,166 30.81

CHU SS 155,4 99,310 21.94

BANFORA 51,78 9,700 7.31

DEDOUGOU 38,81 5,440 5.48

DORI 44,94 5,431 6.34

FA DA 50,56 5,815 7.14

GAOUA 51,52 3,925 7.27

KAYA 49,30 4,423 6.96

KOUDOUGOU 47,90 2,285 6.76

Total 708,7 40,495 100

Sales revenue from medications sold in the first three trimesters of 2009

Table 5: Visualization of the sales revenue of medications during the first three

trimesters of 2009 in public hospitals

08-11 burkina faso:29 31/3/11 18:13 Page 10

World Hospitals and Health Services Vol. 47 No. 1 11

Management

MESSRS/MFB concerning the particular status of CHR.� Decree No. 2006- 463/PRES/PM/MFPRE/MS/MFB

concerning the organization of specific jobs from the Ministerof Health which define the attributes of a Pharmacist.

To use the following legislation for promoting hospital pharmacydevelopment:� Decree No. 2008-328/PRES/PM/MEF concerning the

organization and functioning of the rules for revenue and rulesof state and other public organization advancement.

� Decree No. 2003-372 PRES/PM/MFB concerning theconditions and modalities of the creation, management, andreduction of State run public establishments.

� Decree No. 2009-104/PRES/PM/MS concerning theorganization of the Ministry of Health.

� Decree No. 2009-108/PRES/PM/MATD/MS/MEF/MFPREconcerning the transfer of competencies and resources fromthe State to the communes in the field of health.

� Decree No. 2000-008/PRES/PM/MS from 26/01/00concerning the organization of the Hospital Pharmacy.

� To have specific essential medicine list in each hospital.� To collecte and analyze pharmaceutical data in each the

hospital every quater.� To improve pharmaceutical gouvernance, management and

policy in each hospital. �

Dr Hamado Saouadogo Pharm D, MPH and “Strategies againstemerging and infectious diseases”. He has many certificates. He isworking with the ministry of health in Burkina Faso. He is alsointernational consultant. He worked with the USA Peace Corps inBurkina Faso as Health Technical coordinator and trainer.

References

Decree No. 2008-297/PRES/PM/MEF concerning the financial and accountable program ofPublic State Establishments (PSE) in Burkina Faso

Decree No. 2008-173/PRES/PM/MEF concerning general regulation of public works anddelegations of public service in Burkina Faso

Decree No. 2004-191/PRES/PM/MFB concerning the general status of the PSEDecree No. 2006-355/PRES/PM/MS/MESSRS/MFB concerning particular status of CHUsDecree No. 2006-356/PRES/PM/MS/MESSRS/MFB concerning particular status of CHRsDecree No. 2006- 463/PRES/PM/MFPRE/MS/MFB concerning the organization of specific jobs

under the Ministry of Health and defining the attributes of PharmacistDecree No. 2008-328/PRES/PM/MEF concerning the organization and functioning of revenue

rules and rules governing State and other public organization advancementDecree No. 2003-372 PRES/PM/MFB concerning conditions and modalities of creation,

management, and reduction of State run public establishmentsDecree No. 2009-104/PRES/PM/MS concerning the organization of the Ministry of HealthDecree No. 2009-108/PRES/PM/MATD/MS/MEF/MFPRE concerning the transfer of State

competencies and resources to communes in the field of healthDecree No. 2000-008/PRES/PM/MS from 26/01/00 concerning the organization of the Hospital

PharmacySaouadogo H, Compaore M. Essential medicines access survey in public hospitals of Burkina

Faso. African Journal of Pharmacy and Pharmacology Vol.4 (6), pp.373-380, 2010Saouadogo H. Measuring medicine prices, availability, affordability and price components in

Burkina Faso. HAI/WHO. Ouagadougou, 2010WHO. Indicateurs pour le suivi de la mise en œuvre des politiquespharmaceutiques nationales. Guide pratique. WHO/DAP/94.12 : P19-30

08-11 burkina faso:29 31/3/11 18:13 Page 11

Procurement

12 World Hospitals and Health Services Vol. 47 No. 1

International overview of hospitalprocurement

ABSTRACT: This article was written by four French hospital director students at the Ecole des Hautes Etudes en SantéPublique (EHESP – School of Public Health) from a study conducted jointly with students at the Grenoble School ofManagement to present an international overview of hospital procurement methods in ten countries. An analysis of thesemethods showed that there was a general trend towards group purchasing, with some common aims in terms of costs andperformance and some differences in legislation (competition), size of the public sector and centralization ordecentralization.

In hospitals, procurement practices can reduce costs andimprove performance, releasing funds for investing in hospitalcare for the future.A study was carried out by French hospital director students at

the Ecole des Hautes Etudes en Santé Publique (EHESP – Schoolof Public Health) and students at the Grenoble School ofManagement to present an international overview of hospitalprocurement methods1 in ten countries (France, Italy, Belgium,Germany, United Kingdom, the Netherlands, Sweden, Quebec,the United States and Brazil)2.

An analysis of these methods showed that there was a generaltrend towards group purchasing, with some common aims interms of costs and performance and some differences inlegislation (competition), size of the public sector andcentralization or decentralization.

This article classifies the forms of group purchasing in thecountries studied and describes their advantages anddisadvantages for procurement practices and performance.

Classification of group purchasing The group purchasing forms were classified according to twocriteria. The first concerned the involvement of hospitals in thecreation and operation of the group purchasing organization(whether it was an independent organization supplying hospitalsor an organization set up by the hospitals it supplied). The secondcriterion was the function of the group purchasing organization(purchasing, supplier accreditation and consultancy). Theclassification shows the group purchasing forms used in thevarious countries.

Independent organizations providing services to hospitalsThis type of group purchasing organization is an independent legalentity, state-owned or not, which provides various common

MAUD FERRIER, DAVID LARIVIERE,

CLAIRE LAURENT AND ERIC ROQUE

STUDENT HOSPITAL DIRECTORS

EHESP SCHOOL OF PUBLIC HEALTH, FRANCE

services to hospitals and may involve hospitals in its management.

Independent legal entities purchasing on behalf of hospitalsThese mainly purchase goods and sell them on to the hospitals.They negotiate contracts with suppliers and make purchases onbehalf of the hospitals, taking advantage of volume pricing madepossible by grouping purchases.

In France, the Union des Groupements d’Achats Publics (UGAP– Union of Public Procurement Groups) acts for the whole of thepublic sector, enabling state-owned hospitals to purchasesupplies without requesting competitive quotations.

This form of group purchasing with state-owned nationwideorganizations also exists in Italy (CONSIP), Brazil (Federal stateprocurement services for medicaments) and England (NHS SupplyChain). In Sweden, the state procurement network,Landstingsnätverket för Upphandling (Lfu), covers the eightregions which send representatives to a national assembly. TheLfu has a complementary advisory mission, producing standardsand supplier codes of conduct. The regional procurement servicesare commissioned by the hospitals. The hospitals also have theirown procurement services.

The group purchasing corporations in Québec are owned by thehospitals which have representatives on the Board of Governorsand appoint a General Director responsible for the policy of thegroup purchasing organization. By grouping customers’purchases, they save about 30% on high value added products.The regional corporations combine to purchase medicalequipment and supplies in bulk.

There are also private purchasing organisations: in theNetherlands, the NIC (Nederlands Inkoop Centrum) is a large,highly skilled consultancy body. It acts mainly for the public sectorand has more than 150 consultants responsible for findingsolutions to procurement problems in a wide range of fields

12-14 International overview of hospital procurement - EHESP copy:29 31/3/11 19:19 Page 12

World Hospitals and Health Services Vol. 47 No. 1 13

Procurement

(equipment, information technology, energy).

Purchasing organizations providing supplier accreditationThese legally independent organisations group the purchasevolumes of their members and negotiate prices. However, thehospitals themselves make the purchases under the conditionsdefined in their contracts.

In the United States, Group Purchasing Organizations (GPO)cover most hospital requirements: pharmaceuticals, surgicalinstruments, capital equipment and office supplies. They provide arange of services: benchmarking, marketing, training programmesand insurance. The hospitals have great freedom – they can makepurchases outside the contracts, join other GPOs at any time –and are able to take part in the decisions made by the GPO(product selection). However, certain obligations may be imposedon members (minimum purchases). Most GPOs are financed bythe volume related administrative fees paid by the suppliers, whichare usually 2 to 3% of sales (the hospitals do not have to pay anymanagement fees).

Key figures on the GPOs� The number of GPOs has increased from 40 in 1974 to

900.� GPO contracts account for 70% of hospital purchases,

i.e. 150 billion dollars.� About 96% of hospitals belong to at least one GPO.� 6 GPOs are responsible for purchasing around 90% of all

contracts: Novation, Premier, HealthTrust, MedAssets,Broadlane Group and Amerinet.

In France, independent organisations – CAHPP, Helpévia andCACIC – provide supplier accreditations mainly for privatehospitals. These try to capture a share of state-owned hospitalpurchasing by grouping, drawing up requests for quotation andprocessing quotations, in accordance with the GovernmentContract Code, although currently little used.

Purchasing organizations providing consultancy and supportfunctionsThese are legally and strategically independent entities providingconsultancy for hospitals and encouraging the sharing ofexperience and methods. In the United Kingdom, Commercial

Support Units are responsible locally for the NHS procurementpolicy, pooling the members purchasing skills.

Organizations created by hospitals with a common policySome hospitals have created joint ventures to optimiseprocurement. The statutes of the organizations depend on thefounder members and may take the following forms.

Groups of hospitals making purchases on behalf of membersthrough an organization that may or may not have its own legalstatus The hospitals determine their own requirements, the grouppurchasing organisation manages the procurement procedure andproducts are delivered directly to the hospitals. There is no legalobligation for the hospitals to use the group purchasingorganisation.

This is used in Germany (purchasing cooperatives), in Belgium(IRIS-Achat) and in France (purchasing GIEs).

Supplier accreditation organisationsThe aim of this method is to source products in a way similar toGPOs, the difference being that the organization does not have aparticular legal status. The organization negotiates group pricesand the hospital members then undertake the procurementprocedures themselves.

In Brazil, the Pró-Saúde online marketplace tradesmedicaments, equipment and medical equipment by Internet onbehalf of 24 establishments. An agreement is signed between Pró-Saúde ABASH (the facilitator) and the supplier who then becomesaccredited for the marketplace. The hospital selects its suppliersand makes its purchases, which enables it to retain controlthroughout the order process.

Organisations with a common policy providing consultancy forpurchasersThese organisations have a pool of consultants and sharepractices, experience and procurement methods.

In the French public, not for profit health sector, organisationssuch as the RESHA-IDF Groupement d’Intérêt Public (GIE – PublicInterest Group) (121 members), the UNI-HA Groupement deCoopération Sanitaire (GCS – health cooperation Group) (54members) and the Consortium Achats Groupement d’IntérêtÉconomique (20 members) support collective procurementprocedures by providing technical advice and make it possible to

Function

Purchasing Supplier accreditation Consultancy and common purchasing policy

- France : UGAP - France: CACIC, CAHPP, Helpévia - United Kingdom: CSU- United Kingdom: NHS Supply Chain - USA : GPO- Italy: CONSIP - Netherlands: NIC- Brazil: Grupo des Compras Hospitalares- Sweden: Lfu

- Germany: purchasing cooperatives - USA: IHN - France: UNI-HA, RESAH IDF, Purchasing consortium- Belgium: IRIS-Achats - Brazil: Pró-Saúde - Cross-border cooperation agreement- Quebec: group purchasing corporations online marketplace

Independent organization

providing services to hospitals

Group purchasing for

several hospitals with a common

purchasing policy

Type

of o

rgan

izat

ion

Table 1: Types of organizations and their functions

12-14 International overview of hospital procurement - EHESP copy:29 31/3/11 19:19 Page 13

Conclusion Group purchasing organizations are becoming more common,even though there is no dominant type and several different formsmay exist within a country.

The new French plan focusing on hospital procurementperformance will certainly provide the opportunity for drawing onthe experience of other countries to improve national hospitalprocurement methods and continue to improve practices,perhaps by allowing the emergence of new players within thesupply chain process. �

exchange experience through secure online communities.

Group procurement methods improve performance and savemoney but they also have disadvantages Group purchasing improve performance of organizations andsave moneyGroup purchasing can save money, reducing costs by 10%–15%,depending on the country3.

In Québec, the group purchasing corporations have obtained areduction in equipment maintenance costs of 35% to 80%. InBrazil, using the BIONEXO online marketplace, five state hospitalsin São Paulo state that they save 20% on the group purchase of30 medicaments.

Group purchasing improves quality by standardising products,equipments and medical practices. The exchange of informationand experience via a working network stimulates innovation,harmonisation of practices and therapeutic treatment. In Brazil,group purchasing improves product security by preventing thepurchase of counterfeit medicaments.

Group purchasing is said to strengthen purchase managementwhile reducing the work load (simplifying procedures) and costs.Continuous contact with the suppliers promotes commitment andlong-term collaboration (confidence = quality + savings).

This is the justification in particular for group purchasing inGermany and Sweden where hospital procurement evaluationmodels (quality, price), standards and codes of conduct (humanrights, sustainable development) have been set up.

Group purchasing also improves the performance oforganisations by using skilled buyers. The hospitals share skills,practices and methods and increase “know-how”.

Group purchasing is confronted with barriers which hospitalsmust take into account when drawing up their procurementpoliciesGroup purchasing may skew the hospital market given the scopeand significant financial risks (high market concentration,monopolies or oligopolies).

In the United States, the GPOs are sometimes accused offavouring suppliers who pay high administrative fees. Certaincontractual practices of the GPOs (in particular single sourcecontracts, bundled discounts) favour major suppliers, excludingproducts from more innovative SMEs.

There seems to be a lack of competence and specialist trainingin hospital procurement, despite the increase in purchasingtraining. Purchasing is still often a secondary function, carried outmechanically. In Québec, there is a lack of skilled buyers (buyersare being recruited from abroad). In France, hospitals are startingto recruit purchasing directors and specialist buyers.

Doctors are usually opposed to the standardisation ofpurchasing, claiming that purchases must be made to suit specificlocal requirements.

The degree of group purchasing varies according to the politicalorganisation. In Italy, group purchasing is often at infra-regionallevel. In Sweden, group purchasing is at local level, depending onpolitical organisation. In these countries, group purchasing couldbe done at national level.

Group purchasing organisations can also collapse, for examplethe Dutch purchasing cooperative in Brabant, BKI – BrabantKoopt, which was created in 2008, went out of business in 2010.

Procurement

14 World Hospitals and Health Services Vol. 47 No. 1

References1. Health expenditure accounts for 16% of GDP in the United States, 11.2% in France, 10.5%

in Germany, 9.4% in Sweden and 8.7% in the United Kingdom (Source: OECD)2. Study presented at the Second International Symposium on Hospital Procurement in

September 20103. Conclusion of the Second International Public and Private Health Buyers Symposium, Issy-

les-Moulineaux, 20104. Fehosp- Federação das Santas Casas e Hospitais Beneficentes do Estado de São Paulo

12-14 International overview of hospital procurement - EHESP copy:29 31/3/11 19:19 Page 14

World Hospitals and Health Services Vol. 47 No. 1 15

Procurement

Centralized distribution: reducingownership costs by streamlininghospital logistics

ABSTRACT: All Quebecers have access to a public health system that enables them to receive high-qualityhealthcare, regardless of their individual ability to pay. With the aim of improving effectiveness and efficiencyand achieving cost savings in managing public funds allotted to the healthcare network, SigmaSanté intendsimplementing a central distribution of medical supplies needed by healthcare facilities in Montréal and Laval,Québec, as has been done in many other jurisdictions for numerous years.

It is fortunate that in the Province of Québec, all residents haveaccess to a public healthcare system that allows them to receivehigh-quality healthcare, regardless of financial status. We must,

however, bear in mind that taxpayers indirectly pay for theseservices, and that effective and efficient management of publicfunds financing the healthcare system is crucial.

In this context, SigmaSanté, a not-for-profit organization, offersa group purchase negotiation service for healthcare and socialservice centres in Montréal and Laval, which alone represent25,000 short- and long-term beds. In Québec, group purchasingin the healthcare field has existed for 50 years. Several companiessuch as SigmaSanté provide services of this nature to theprovince’s health centres.

In addition to negotiation of product prices and terms ofpurchase, a significant concern of SigmaSanté is total cost ofownership. SigmaSanté strives to reduce expenditures associatedwith purchasing logistics. It is with that aim that centralizeddistribution comes into focus.

Centralized drug distribution: a tried and proven modelCentralized distribution of drugs purchased by healthcare centresis a model in Québec that has, for several years, proven it’s worthand reliability. Indeed, since 1994, a group of pharmacists aimingto reduce the workload related to purchasing logistics introducedmeasures implementing centralized drug distribution.

Before this initiative, all drugs negotiated by SigmaSanté ordirectly by a healthcare centre were distributed by theirmanufacturers, resulting in numerous orders from severalmanufacturers and as many deliveries and invoices to process.Pharmacists thus decided to assess the impact of centralizeddistribution on their internal logistics; this study showed thatimplementation of this type of distribution could potentiallydecrease drug order processing time by 65%, generating

CHANTAL S LAURIN

CHIEF EXECUTIVE OFFICER, SIGMASANTÉ

significant annual savings in hospital logistics costs. This led to thecreation of the Québec centralized drug distribution model. Today,all healthcare centres enjoy the benefits of this approach.

Currently, SigmaSanté negotiates 88% of drugs purchased byits client institutions, representing more than 66 differentagreements with various manufacturers. The 73 memberinstitutions of SigmaSanté place their orders with a singledistributor who processes the order, ensures delivery to, andinvoices the healthcare centre. All drugs covered by theseagreements are sold at the pre-agreed price to which is added thepre-agreed distribution fee.

Manufacturers deliver their products to a single location, andhealthcare centres receive all the drugs they require by placing asingle order. Products are thus purchased at wholesale prices;logistics are simplified for all involved and environmental impactrelated to transportation, greatly reduced.

Rethinking medical supply distributionIn 2008, SigmaSanté launched a study aimed at improving itsservice package in the field of medical supplies. Collected dataanalysis indicated that expenditures of its members for purchaseof medical supplies had, over five years, increased by more than55%. This study also showed how current financial pressures hadmade institutional managers acutely aware of the importance ofefficiency in the supply chain, which requires multiple humaninterventions to ensure timely availability of supplies at the rightplace.

Beyond supply price management, several healthcare centreswished to reduce purchasing costs whilst improving quality ofservices offered to their in house customers. The centralizeddistribution model then appeared as a highly appealing solution,since it makes it possible to obtain products from multiplesuppliers whilst placing a single order to a single location, to group

15-17 Centralized distribution – lauren:29 31/3/11 19:18 Page 15

Procurement

16 World Hospitals and Health Services Vol. 47 No. 1

products in a single shipment and pay one invoice per order. Thisgain in efficiency is important to healthcare centres, who can thendevote resources to more strategic activities and better serve inhouse customers.

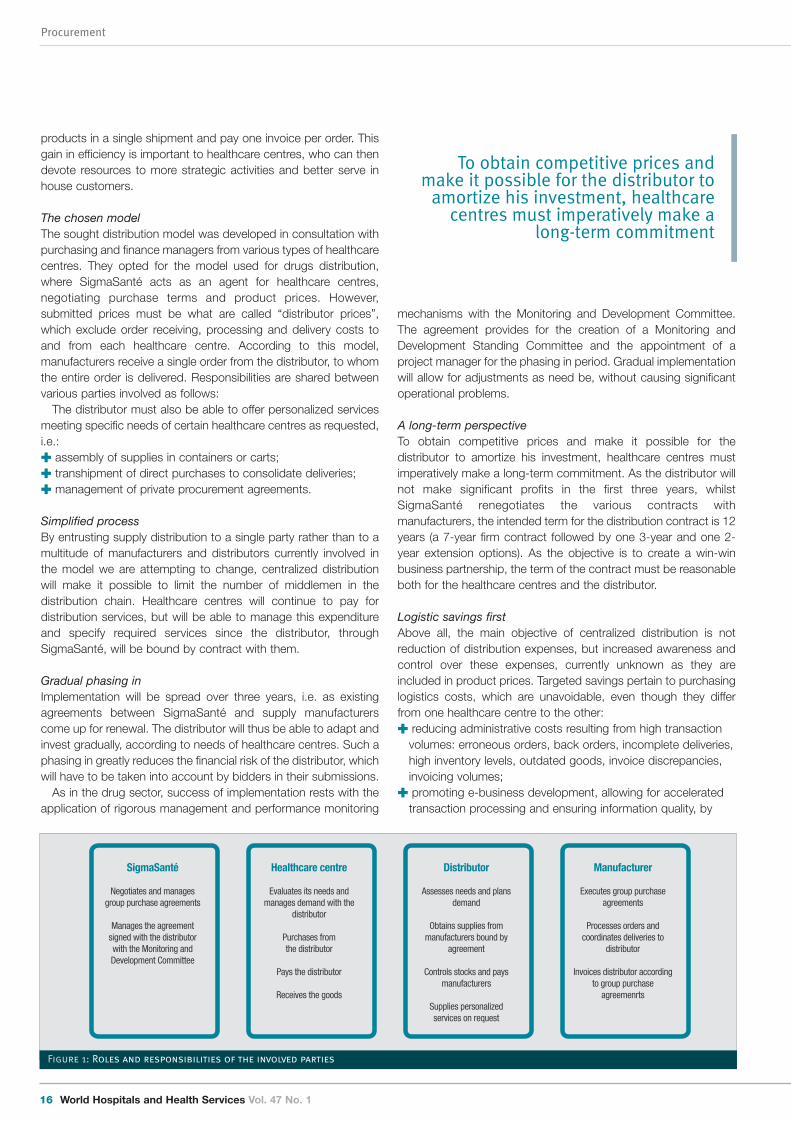

The chosen model The sought distribution model was developed in consultation withpurchasing and finance managers from various types of healthcarecentres. They opted for the model used for drugs distribution,where SigmaSanté acts as an agent for healthcare centres,negotiating purchase terms and product prices. However,submitted prices must be what are called “distributor prices”,which exclude order receiving, processing and delivery costs toand from each healthcare centre. According to this model,manufacturers receive a single order from the distributor, to whomthe entire order is delivered. Responsibilities are shared betweenvarious parties involved as follows:

The distributor must also be able to offer personalized servicesmeeting specific needs of certain healthcare centres as requested,i.e.:� assembly of supplies in containers or carts;� transhipment of direct purchases to consolidate deliveries;� management of private procurement agreements.

Simplified processBy entrusting supply distribution to a single party rather than to amultitude of manufacturers and distributors currently involved inthe model we are attempting to change, centralized distributionwill make it possible to limit the number of middlemen in thedistribution chain. Healthcare centres will continue to pay fordistribution services, but will be able to manage this expenditureand specify required services since the distributor, throughSigmaSanté, will be bound by contract with them.

Gradual phasing inImplementation will be spread over three years, i.e. as existingagreements between SigmaSanté and supply manufacturerscome up for renewal. The distributor will thus be able to adapt andinvest gradually, according to needs of healthcare centres. Such aphasing in greatly reduces the financial risk of the distributor, whichwill have to be taken into account by bidders in their submissions.

As in the drug sector, success of implementation rests with theapplication of rigorous management and performance monitoring

mechanisms with the Monitoring and Development Committee.The agreement provides for the creation of a Monitoring andDevelopment Standing Committee and the appointment of aproject manager for the phasing in period. Gradual implementationwill allow for adjustments as need be, without causing significantoperational problems.

A long-term perspectiveTo obtain competitive prices and make it possible for thedistributor to amortize his investment, healthcare centres mustimperatively make a long-term commitment. As the distributor willnot make significant profits in the first three years, whilstSigmaSanté renegotiates the various contracts withmanufacturers, the intended term for the distribution contract is 12years (a 7-year firm contract followed by one 3-year and one 2-year extension options). As the objective is to create a win-winbusiness partnership, the term of the contract must be reasonableboth for the healthcare centres and the distributor.

Logistic savings firstAbove all, the main objective of centralized distribution is notreduction of distribution expenses, but increased awareness andcontrol over these expenses, currently unknown as they areincluded in product prices. Targeted savings pertain to purchasinglogistics costs, which are unavoidable, even though they differfrom one healthcare centre to the other: � reducing administrative costs resulting from high transaction

volumes: erroneous orders, back orders, incomplete deliveries,high inventory levels, outdated goods, invoice discrepancies,invoicing volumes;

� promoting e-business development, allowing for acceleratedtransaction processing and ensuring information quality, by

Distributor

Assesses needs and plans demand

Obtains supplies from manufacturers bound by

agreement

Controls stocks and pays manufacturers

Supplies personalized services on request

Healthcare centre

Evaluates its needs and manages demand with the

distributor

Purchases from the distributor

Pays the distributor

Receives the goods

Manufacturer

Executes group purchase agreements

Processes orders and coordinates deliveries to

distributor

Invoices distributor according to group purchase

agreemenrts

SigmaSanté

Negotiates and manages group purchase agreements

Manages the agreement signed with the distributor with the Monitoring and Development Committee

Figure 1: Roles and responsibilities of the involved parties

To obtain competitive prices andmake it possible for the distributor to

amortize his investment, healthcarecentres must imperatively make a

long-term commitment

15-17 Centralized distribution – lauren:29 31/3/11 19:18 Page 16

World Hospitals and Health Services Vol. 47 No. 1 17

Procurement

months. We rely on the competitive factor, the term of the contractand the extraordinary opportunity afforded by implementation ofsuch a service for a party specialized in the distribution sector, toobtain fair and equitable prices for all parties involved.

Obviously, creation of such a distribution model will offendcurrent practices; this will cause fears to healthcare centres,industry manufacturers and distributors. At the time ofestablishment of centralized drug distribution, several key successfactors made it possible to counter these obstacles and ensuresuccess of the project: � a drug management committee made up of determined and

concerned pharmacists;� leadership of the committee’s chairman;� team spirit of institutional pharmacists vis-à-vis industry

pressures;� well-defined practice sector;� one spokesperson per healthcare centre.

In the case of medical supplies, the situation is somewhatdifferent. Because of the large variety of products, manystakeholders with different areas of specialization are affected bythe impact of the model, which makes team spirit and unanimitymore difficult to attain. Thus, industry pressures have a largerimpact, which has to be counterbalanced to allay fears anduncertainties.

In January 2011, SigmaSanté formally asked all institutionalleaders to grant it a clear mandate to allow it to proceed with thisproject with proper authority.

Positive responses will decide whether implementation of thismodel can be applied to the medical supply sector. �

Chantal S Laurin is Chief Executive Officer of SigmaSanté, a jointprocurement corporation that acts as broker for several Québechealthcare facilities, and whose annual transactions exceeds c$800million. Mrs Laurin has previously held the position of ChiefExecutive Officer of Montréal International Airport, as well asvarious key positions with Hydro-Québec and Transport Canada.

reducing human intervention;� savings resulting from the use of best practices: off-peak

deliveries, consolidation of volumes, use of e-business, promptpayment, etc.;

� subcontracting for occasional needs and low value-addedservices.

Centralized distribution also makes it possible for suppliers toachieve savings: � by filling a single order for all healthcare centres, they avoid

delivering at multiple addresses, reducing mileage, shorteningdelivery times and reducing environmental impact;

� decreasing the number of invoices to be processed savesvaluable time.

Better procurement practices and efficient logistics are the bestmeans of guaranteeing fair costs.

Competitiveness for a fair priceThe contract will be awarded to the lowest qualified bidder. Thequalification process has been well planned with representativesfrom various healthcare centres, and criteria are clearly defined.We rely on the competitive factor and the interest for the projectamong distributors (specialized in this sector or not) to obtain a fairand equitable contract price.

Countering resistance As no initial investment is necessary on the part of healthcarecentres, risk is kept to a minimum. The selected distributor willinvest funds gradually, over three years, as contracts come up forrenewal. Naturally, healthcare centres are anxious to know thecost of distribution expenses, which will be disclosed only at thetime of the bids. We will also know, as agreements are beingrenewed, the amount of price reductions which will allow us to freeup funds which will be used to pay our distributor.

The cost of the distributor’s services will become known as partof the tendering process which we plan to initiate in the upcoming

15-17 Centralized distribution – lauren:29 31/3/11 19:18 Page 17

Procurement

18 World Hospitals and Health Services Vol. 47 No. 1

The challenges of collaborativeprocurement in the healthcare sector

ABSTRACT: The article points out the new challenges of collaborative procurement in the healthcare sector.The research focuses on the optimization of healthcare purchasing through the reduction of costs withoutany prejudice to the quality of healthcare performances, but also assuring rationalization and innovation.Moreover, the importance of collaborative procurement is particularly evident considering the ensuingvalorization of the diverse professional skills and their use of strategic purchasing power in theirrelationships with economic operators.

Purchasing aggregation and the professionalization in thepublic procurement field have become two of the mostimportant challenges for public purchasers and for

procuring authorities in general and particularly in the healthcaresector1.

The importance of the public procurement is indeed evident to-date. It is worth mentioning that the procurement market canreach approximately 15% of EU’s GDP and account up to 20% ofdeveloping countries’ GDP2. Such considerable percentagedetermines a strong purchasing power that can be driven towardsinnovation and the creation of value.

Nonetheless, an overall vision of public organization strategicpower is still missing, probably as a widespread fragmentation ofprocuring entities is still present. This is often an obstacle to acomplete and comprehensive vision of the possible strategies ofpublic procuring policies. Thus, the promotion of every form ofcollaborative procurement so as to obtain instruments to steer theuses of such considerable resources is of the utmost importance3.

In general terms, every government, local authority and publicorganisation, utility and agency at any level is endowed withcontractual autonomy and can purchase according tointernational, European and national rules depending on the case,pursuing the goal of obtaining the best value for money4. However,the demand of reducing public expenditure, even as a result of theeconomic crisis, as well as the goal of the European Union toincrease competition in the public market can improve the value ofany form of collaborative procurement and of professionalization,thus achieving a wider and more comprehensive vision of thedifferent market conditions and characteristics.

Nevertheless, in order to create an internal market, theEuropean legislator set common rules for the Member Statesreferring to the principles and procedures of public contractsawarding5. An effective internal market in the supply and services

GABRIELLA MARGHERITA RACCA

FULL PROFESSOR OF ADMINISTRATIVE LAW, DEPARTMENT OF LAW FOR

ECONOMICS, UNIVERSITY OF TURIN (ITALY)

sectors has to be accomplished yet, in the healthcare sector too.Healthcare purchasing is surely a strategic sector in the area ofpublic procurement. The reduction of resources seems to requirethe development of public procurement policies in order tomaintain a high level of protection (as to the healthcareperformances), taking into account the new costs associated tothe evolution of medical science, too. In fact, collaborativeprocurement optimizes public purchasing, especially, but not only,thanks to the economy of scale it achieves.

Purchasing aggregation entails reduction of costs andconsequently may facilitate the achievement of such goalsbecoming creator of value. These costs concern on the one handthe prices of goods and services – for each unit – and, on theother hand, the awarding phase of public procurement (includinghuman resources savings, both in terms of time and money). Thelarge volumes purchased determine a higher purchasing power byassuring the effectiveness of the public action and by acquiringhealthcare products (drugs, equipments, medical devices) andservices at better market conditions and at the best value formoney. Furthermore, public bodies may enjoy the benefits arisingfrom the reduction of costs and time related to autonomous awardprocedures (according to a rough calculation the cost of anautonomous award procedure can reach €20,000). Moreover,purchases aggregation entails the reduction of human resourcesinvolved in the award procedures thus allowing – with a view toimproving the control of the performance phase – theirassignment to the task of monitoring contracts performance andpossible infringements6.

Purchases aggregation is not only an instrument to reducecosts, as it can drive innovation, by promoting competitionbetween economic operators. Indeed, collaborative procurementdoes not harm the development of competition, as it has beenclaimed, rather being an instrument that helps to improve its value

18-20 collaborative procurement - racca:29 31/3/11 18:56 Page 18

World Hospitals and Health Services Vol. 47 No. 1 19

Procurement

ensuring a competitive quality level. Regulatory rules at Europeanlevel have been introduced in 2004, so as to rationalize publicprocurement, providing a European definition of CentralPurchasing Bodies7. In fact, it has been considered that thosetechniques can help increase competition and streamline publicpurchasing in view of the large volumes purchased by theseorganizations. Obviously, collaborative procurement affects therole played by the contracting authorities, as long as anaggregated awarded procedure differs greatly from anautonomous one. In other words, the purchaser is not a personacting individually anymore, since, to the contrary, he is part of ateam of several people with different professional skills (technical,methodological, economic, legal, engineering etc.). Those skillsare often out of reach for most contracting authorities within thehealthcare sector and require the implementation of forms ofaggregation8.

In this context, an organization such as a central purchasingbody can enhance these skills and implement some newpurchasing techniques such as those defined by the 2004European Directives (framework agreements9, electronic auctions,dynamic purchasing systems), with the aim of managing better thecoordination of public demand, by referring to more complexaward procedures.