Embed Size (px)

Citation preview

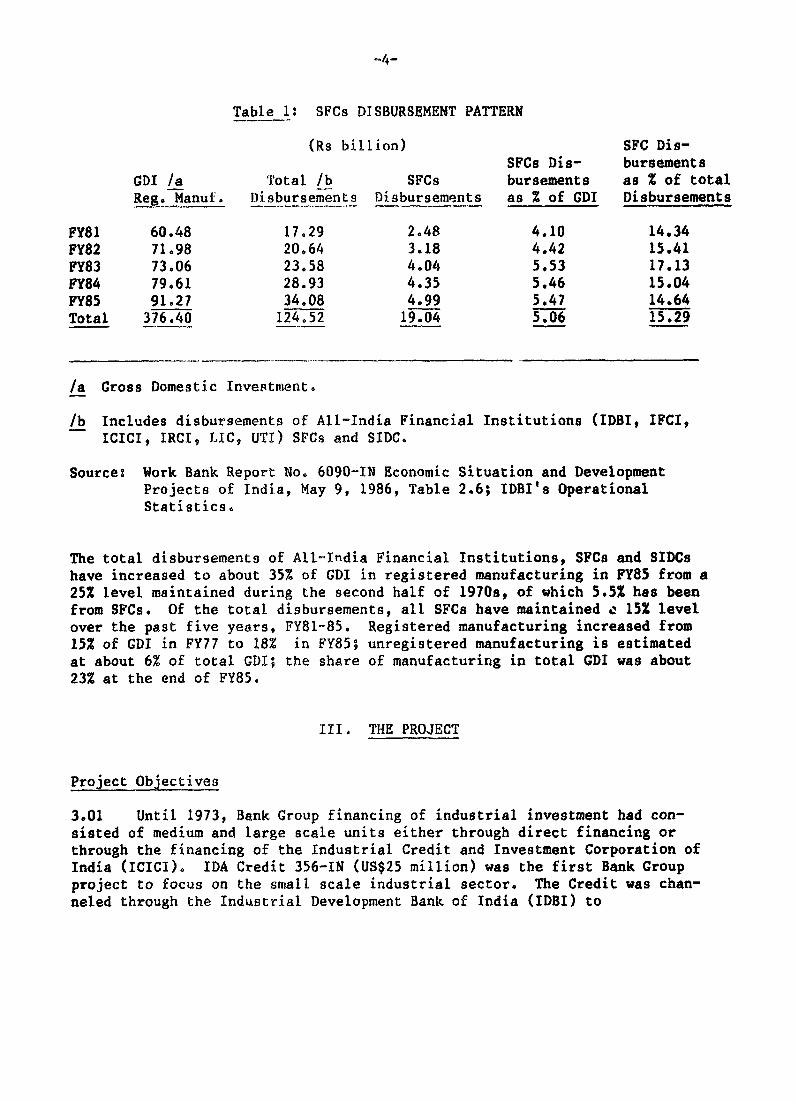

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No. 6876

PROJECT COMPLETION REPORT

INDIA

SECOND IDBI/SFC'S PROJECT(LOAN 1260-IN)

June 29, 1987

Industrial Development and Finance DivisionSouth Asia Projects Department

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

ABBREVIATIONS AND ACRONYMS

APSFC - Andhra Pradesh State Financial CorporationAFC - Assam Financial CorporationBSFC - Bihar State 4Financial CorporationDFC - Delhi Financial CorporationDGTD - Directorate General of Technical DevelopmentGNP - Gross National ProductGOI - Government of IndiaGSFC - Gujarat State Financial CorporationHFC - Haryana Financial CorporationHPFC - Himachal Pradesh Financial CorporationICICI - Industrial Credit and Investment Corporation of IndiaIDB- - Industrial Development Bank of IndiaIFCI - Industrial Finance Corporation of IndiaIFD - Industrial Finance Department (of RBI)JKSFC - Jammu and Kashmir State Financial CorporationKFC - Kerala Financial CorporationKSFC - Karnataka State Financial CorporationMPFC - Madhya Pradesh Financial CorporationMSFC - Maharashtra State Financial CorporationOSFC - Orissa State Financial CorporationPFC - Punjab Financial CorporationRBI - Reserve Bank of IndiaRFC - Rajasthan Financial CorporationSBI - State Bank of IndiaSFC - State Financial CorporationSIDF - Small Industries Development FundSISI - Small Industries Service InstituteSSI - Small Scale IndustriesSSIC - Small Scale Industries CorporationSSIDC - Small Scale Industries Development CorporationSSIDO - Small Scale Industries Development OrganizationSTC - State Trading CorporationTCO - Technical Consultancy OrganizationTIIC - Tamil Nadu Industrial Investment CorporationUPFC - Uttar Pradesh Financial CorporationWBFC - West Bengal Financial Corporation

CURRENCY EQUIVALENTS(annual averages)

Rs per US$1.00 US$ per Rs 1.00

Rs 8.0 US$0.125

Since September 1975, the Rupee has been fixed against a "basket" ofcurrencies. As these currencies are floating, the U.S. Dollar/Rupee exchangerate is subject to change. Conversions in this report have been made at US$1to Rs 8.00, which was the short-term average rate prevailing at the time ofthe project appraisal.

FISCAL YEAR (FY)

Government of India : April 1 - March 31

SFCs : April 1 March 31

RBI, IDBI : July 1 - June 30

THE WORLD BANK OFFICIAL USE OfLYWashington, DC 20433

USA

01Qfge of 0si.cuwCaiOpw ft Ev^aitegn

June 29, 1987

M,EMORANDUM TO THE EXECUTIVE DIRECTORS AND THE PRESIDENT

SUBJECT: Project Completion Report on India - Second IDBI/SFCs Project(Loan 1260-IN)

Attached, for information, is a copy of a report entitled "ProjectCompletion Report on India - Second IDBI/SFCs Project (Loan 1260-IN)" preparedby the South Asia Projects Department. Under the modified system for projectperformance auditing further evaluation of this project by the OperationsEvaluation Department has not been made.

Attachment

This document has a retricted distribution and may be used by recipients only in the performanceOf their offcial duties. Its contents may not otherwise be discled without Wofid Barlk authorization.

FOR OmCIL USE ONLY

PROJECT COMPLETION REPORT

INDIA - SECOND IDBI/SFCs PROJECT

(LOAN 1260-IN)

Table of Contents

Page

PREFACE *...00-00aos.aaa..osoa*aoa- a.oaooo.aaaaaas*aaaaaa iBASIC DATA SHEET .... a a@o*0a@aaa@00, a a .............. o...e....0 iiHIGHLIGHTS ,*-a-.a0aaa0aaa*a00a0000**a@0aaa,a00ae**aaa*a4 iv

I. INTRODUCTION I......aaaaaaaoaaoaoaaaaaaaoea.aaoaaoaaaa 1

II. ECONOMIC ENVIRONMENT .................................. 1

Economic Performance *a.a.ao...a.a.a,aao.aaaaaaaaaao 1Recent Policy Changes.................. . . 2Small and Medium Industries............................ 3Investment Tren3s ........... ......... a 3

III. PROJECT. ...... 4

Project Objectives ............ .. 4Project Design. a.a.a.a.a.a.a.a.a.a.a.a.a.a...a.a...a..a.a.... .aaa 5Institutional Arrangements. .a a aa a.................ee a .*eo a 6

IV. PERFORMANCE OF IMPLEMENTING AGENCIES ................... 6

SFCs Operations.... .... .... a 6SPCs Institutional Achievement ........................ .9IDBI's Performance ..... . a a 00a a a a a a. 11

V. SUBPROJECT PERFORMANCE ...................000 aa 0 s 0asoaose,esse 14

Outcome of Loan 1260-IN Subproject....................... 14Sumary ..... a o. a.o.... ao. aa.... ao..a 16

VI. CONCLUSIONS AND LESSONS LEARNED. 0 *0 0 *........... 0 *.. 0 *.. 16

This document has a restricted distribution and may be used by recipients only in the perfotmanceof their offcil duties. Its contents may not otherwie be disctosed without World Bank authorization.

TABLE OF CONTENTS (cont'd)

ANNEXES

1: SFC's Sanctions and Disbursementst FY81-86 ...................... 19

2: Summary of SFC's Operations ................... ........... ....... 20

3: SFC's Net Sanctions and Disbursements, Distribution by Subsector 21

4: Assistance (Disbursements) to Small Industries, FY81-86 .......... 22

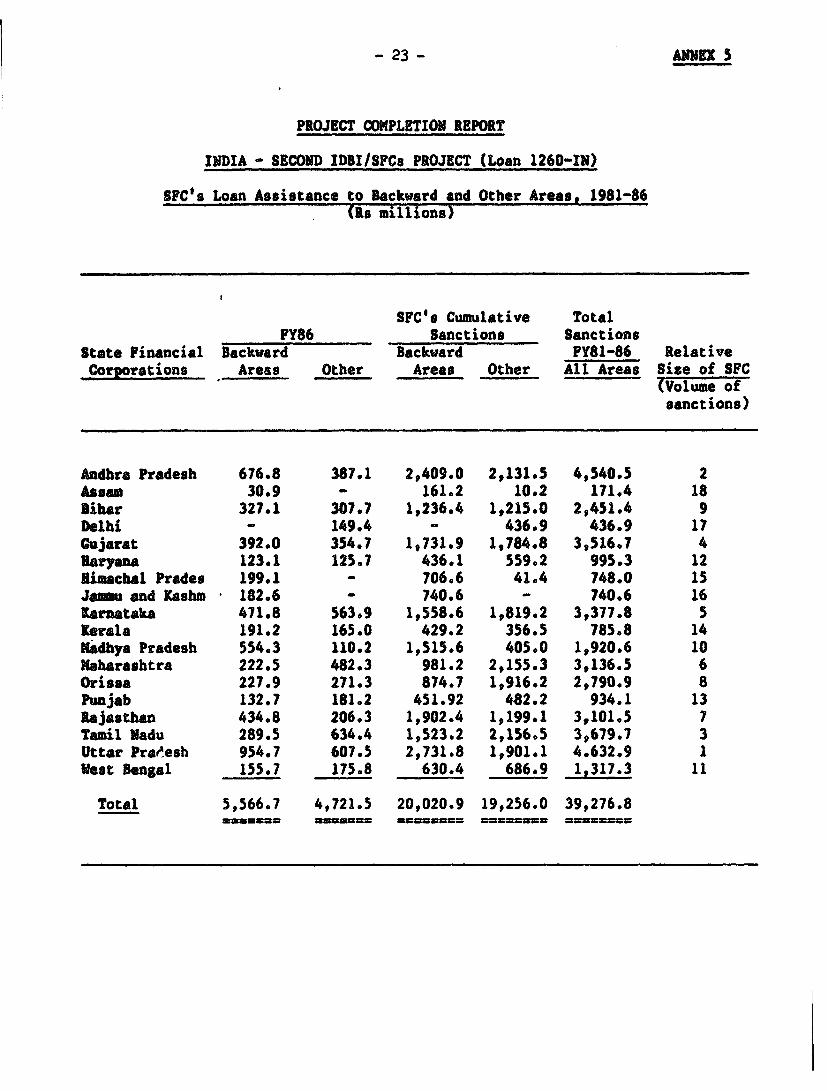

5: SFC's Loan Assistance to Backward and Other Areas, 1981-86 ...... 23

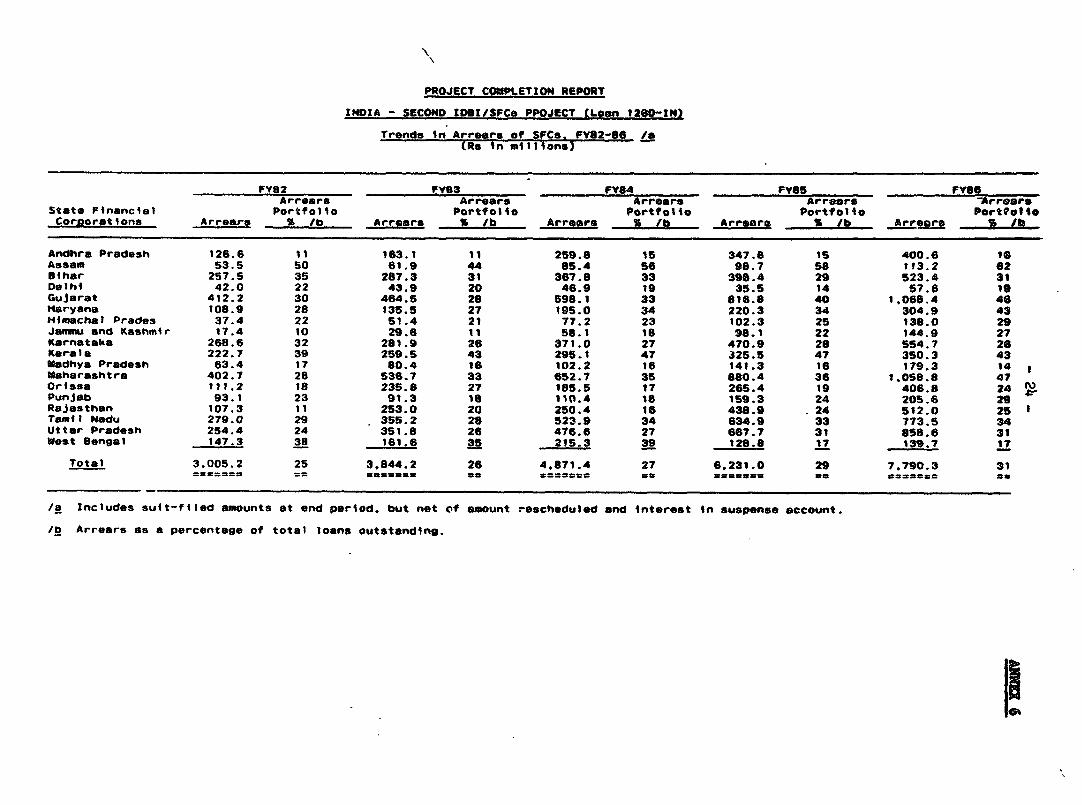

6: Trends in Arrears of SFCs, FY82-86 ...... * ....... 0*.... . ... s.. 24

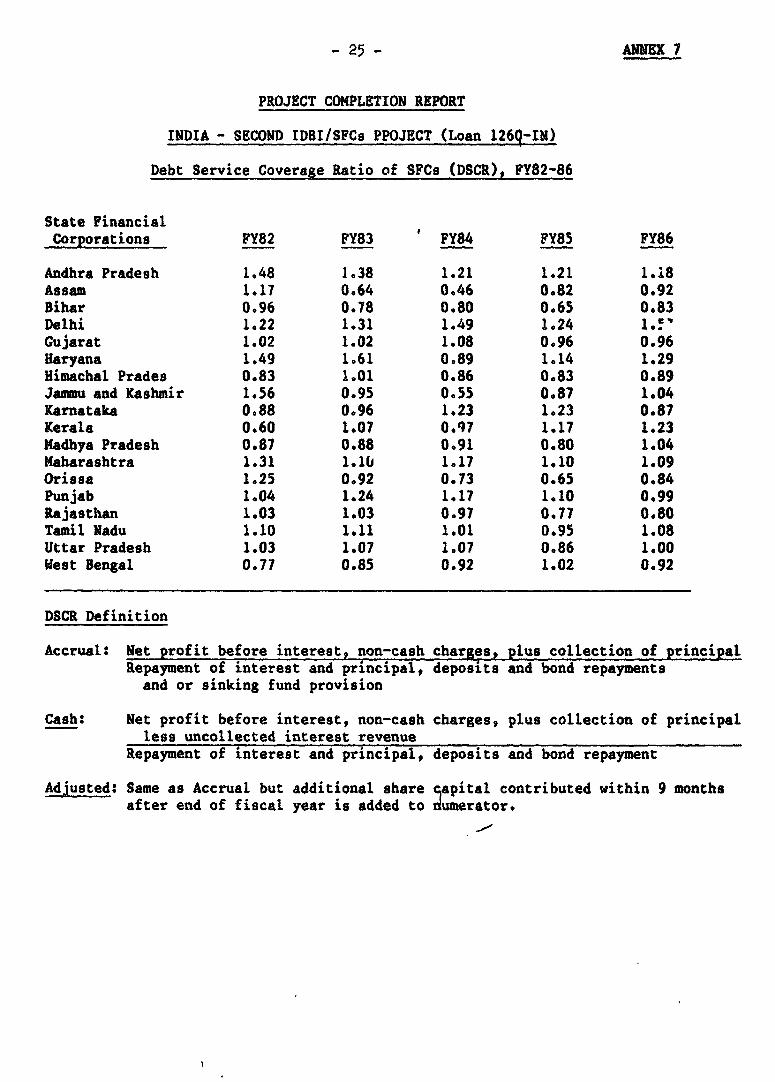

7: Debt Service Coverage Ratio of SFCs (DSCR), FY82-86 ............. 25

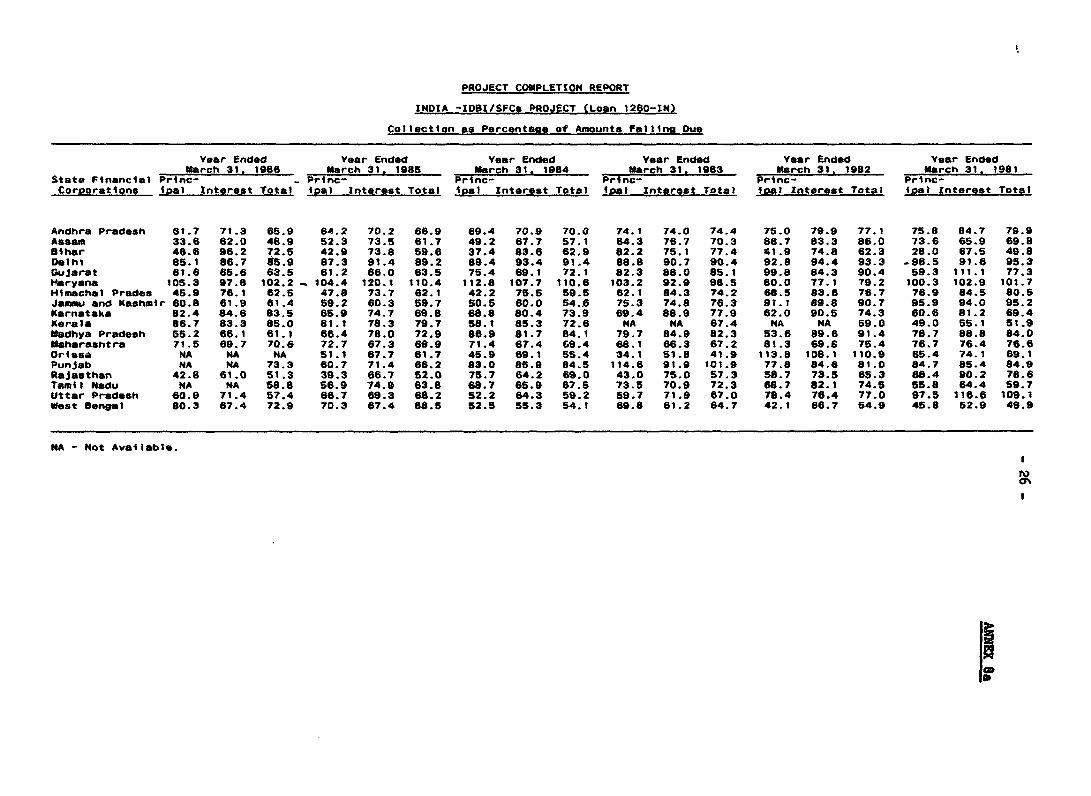

8a: Collection as Percentage of Amounts Falling Due.............-.. 26

8b: Collection Performance of SFCs9 ..................,.............. 27

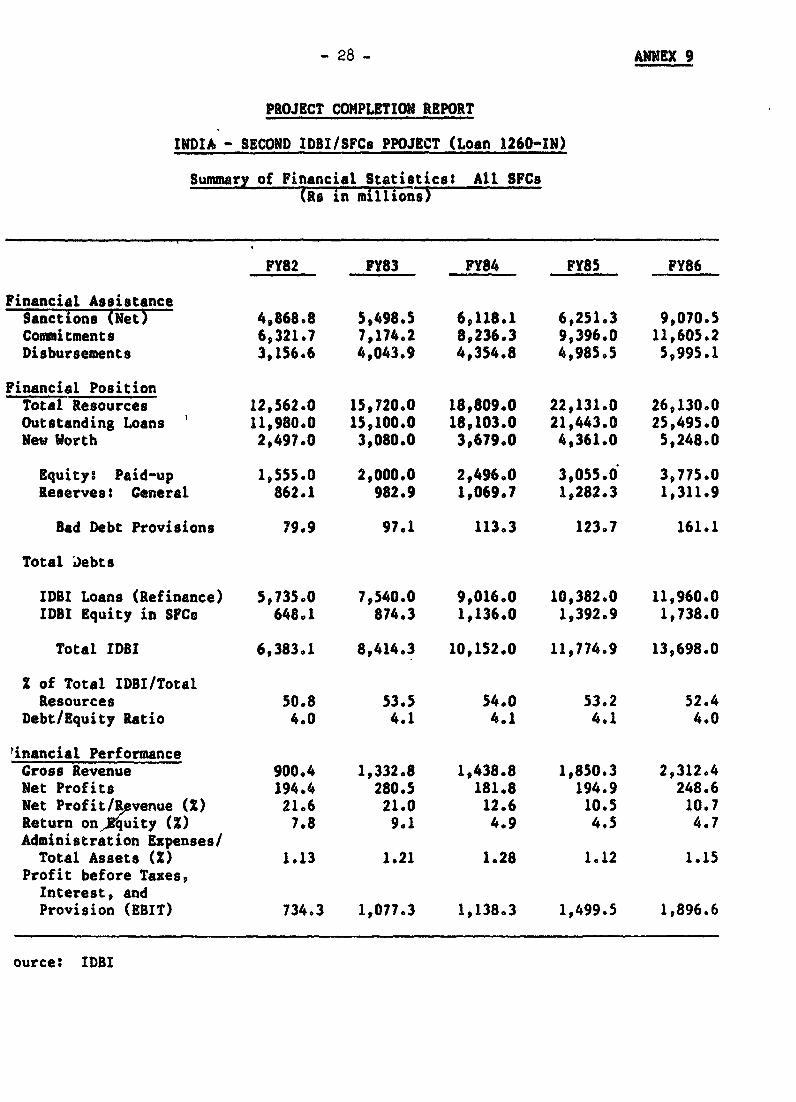

9: Summary of Financial Statistics$ All SFCs ....................... 28

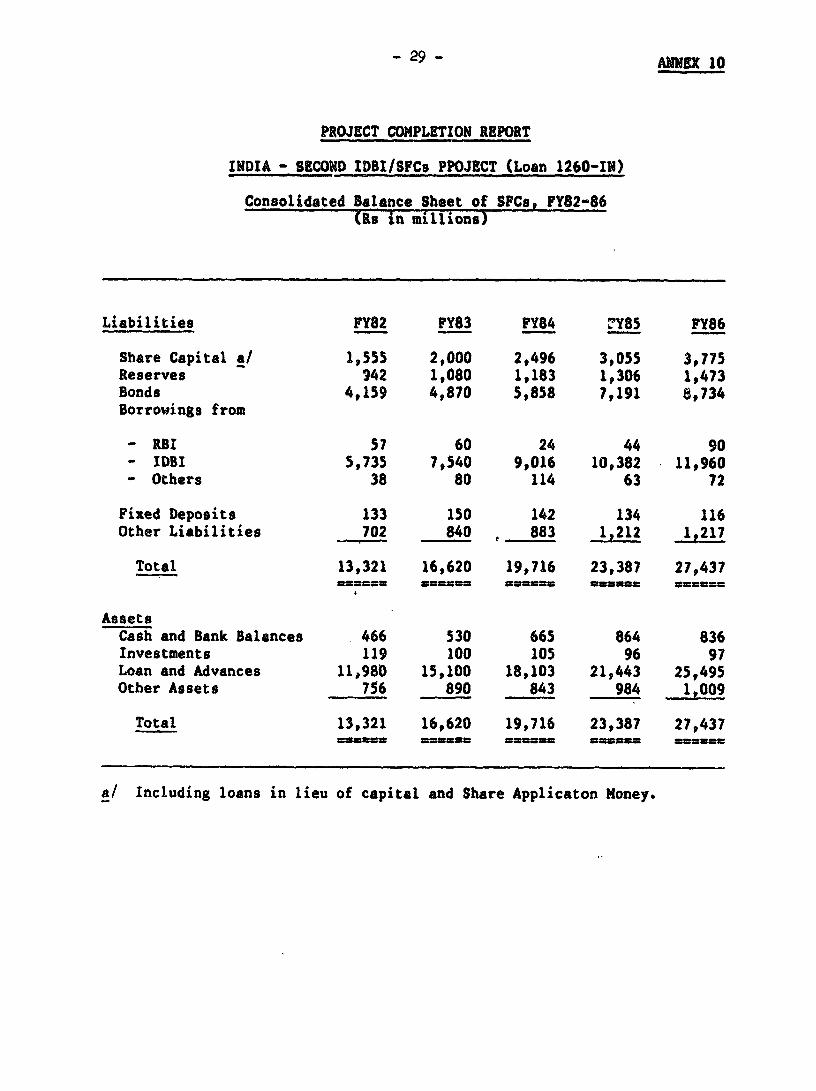

10: Consolidated Balance Sheet of SFCs. FY82-86.......,......,,.. 29

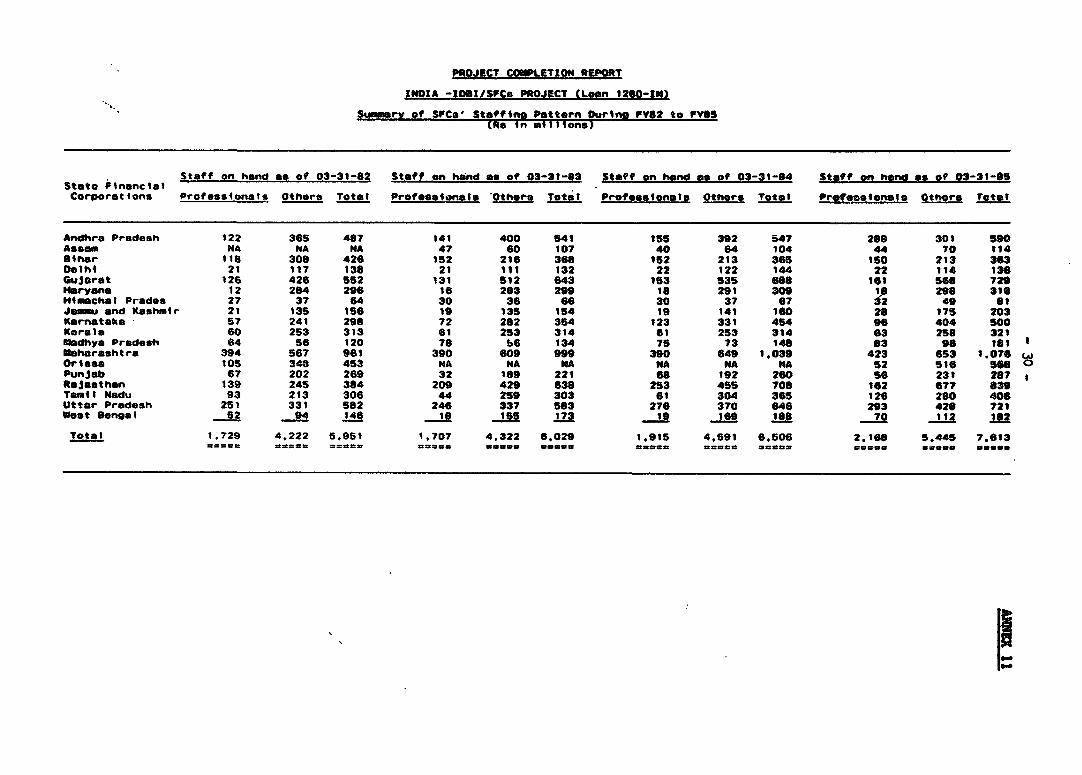

11: Summary of SFCs' Staffing Pattern, 1981/82 - 1984/85 .......4... 30

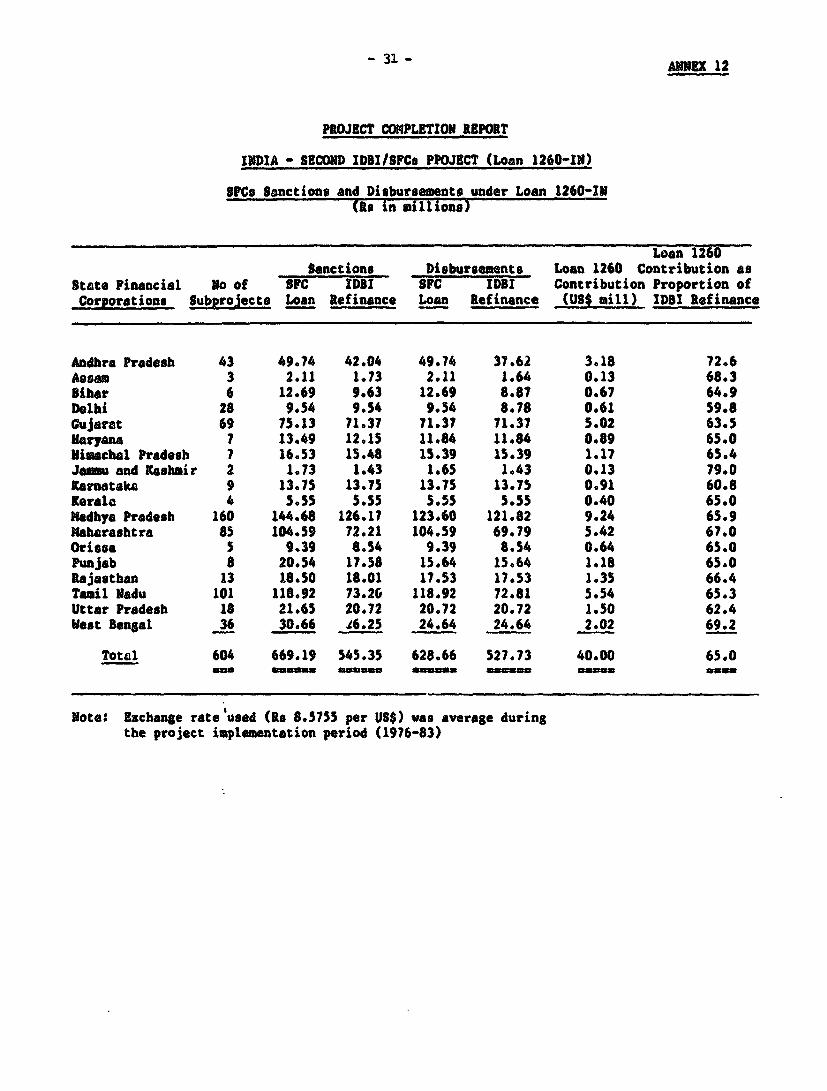

12: SFCs Sanctions and Disbursements under Loan 1260-IN ............. 31

13: Size Distribution of Subprojects and Subloans ................... 32

14: Financing of Subprojects under Loan 1260-IN ..................... 33

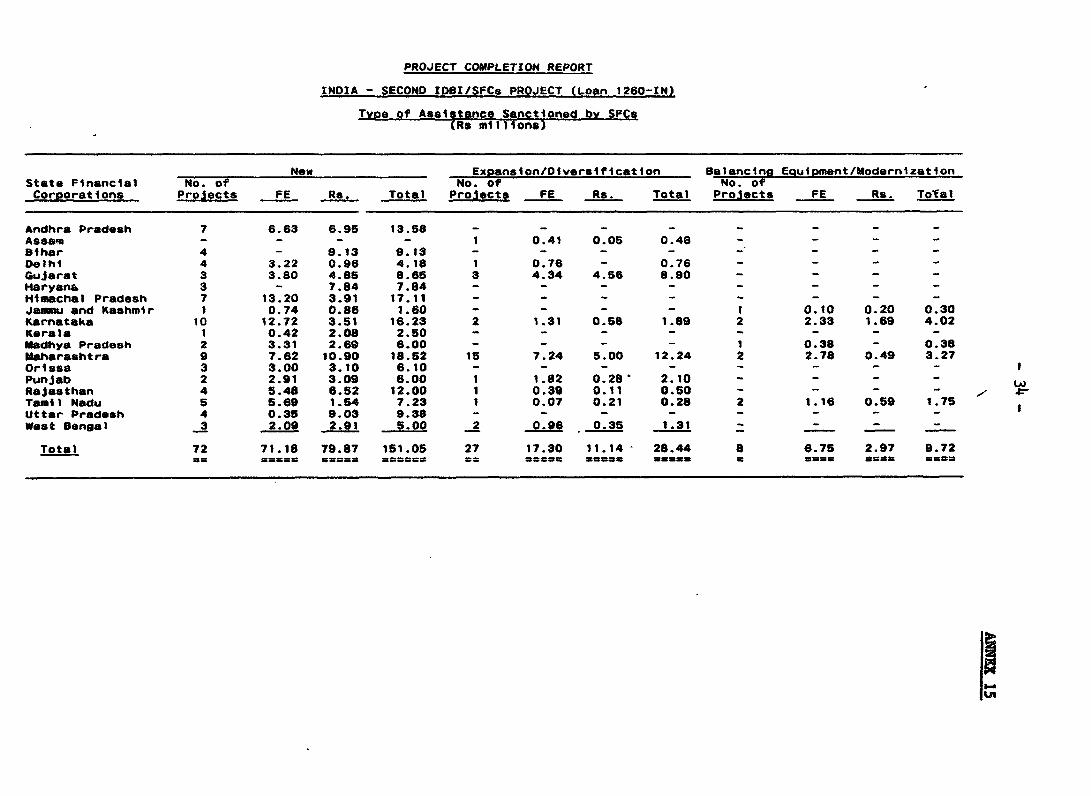

15: Type of Assistance Sanctioned by SFCs ........................... 34

16: Subproject Implementation Performance ....................... .... 35

17: Economic Indicators of Subprojects Financed .................... 36

18: Financial Performance of Projects ............................... 37

19: Actual Investment Costs per Job by Subsector,.........,.,,,,,.. 38

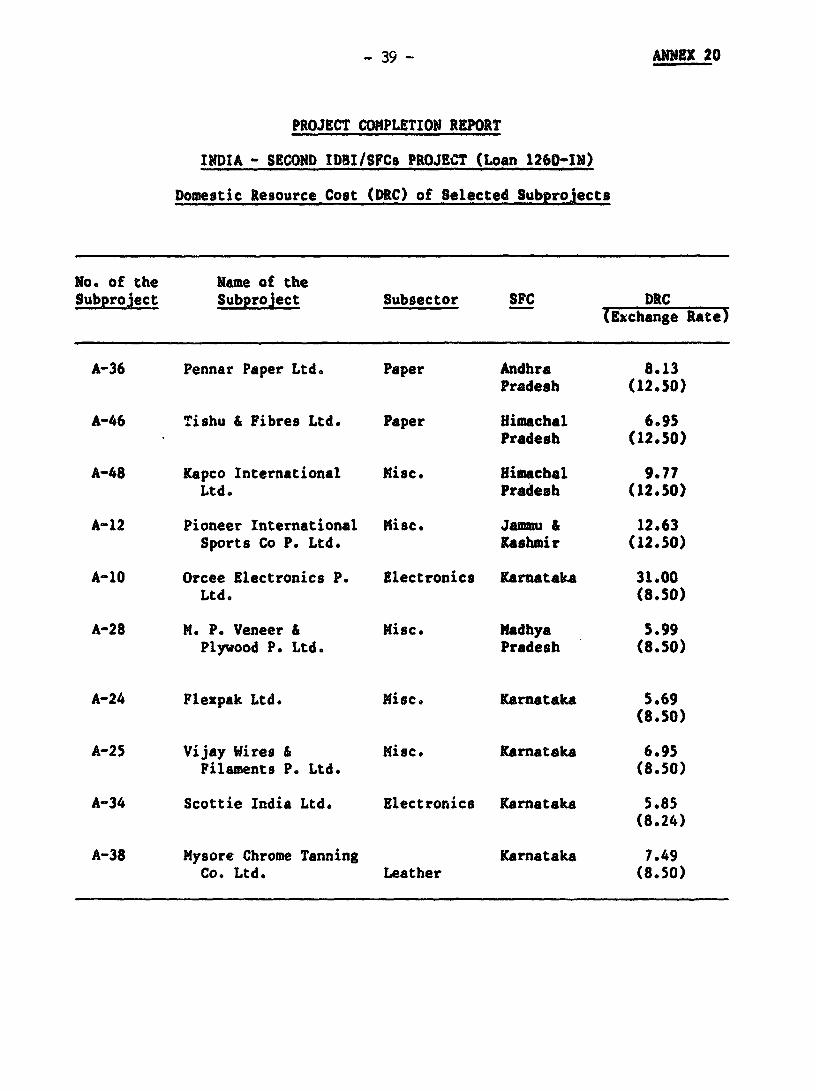

20: Domestic Resource Cost (DRC) of Selected Subprojects ........... 39

21: Estimated and Actual Disbursements under Loan 1260-IN .......... 40

ATTACHMENT

I - Comments Received from the Borrower .......................... ,. 41

PROJECT COMPLETION REPORT

INDIA - SECOND IDBI/SFCs PROJECT

(LOAN 1260-IN)

PREFACE

This report reviews the *.mplementation of the second IDBI/SFCsProject (Loan 1260-IN) in India. It assesses the performance of the mainproject implementing agencies, namely, the eighteen State FinancialCorporations (SFCs) which provide medium and long term finance to small andmedium scale industries (SMI). It also reviews the impact of the project onIndia's credit delivery system for SMI and the economic impact of the SMIsubprojects financed. The US$40 million loan was approved on May 16, 1976and was declared effective on August 10, 1976. By March 1983, the entireamount of the Loan was disbursed. This Project Completion Report wasprepared by the Industrial Development and Finance Division of the ProjectsDepartment, South Asia Regional Office, based on the findings of a projectcompletion mission to India in October 1986 and data prepared by IndustrialDevelopment Bank of India (IDBI), the apex agency for the Project.

Comments received from the Borrower have been taken into account asappropriate in finalizing the report and are reproduced as an Attachment.

This projoect has not been audited by the Operations EvaluationDepartment.

^ it -

PROJECT COMPLETION REPORT

INDIA - SECOND IDBI/SFCs PROJECT

(WAN 1260-IN)

BASIC DATA SHEET(Amounts it US$14)

Loan Status As of April 30L 1987

Original Disbursed Cancelled Repaid Outstanding

Loan 1260-IN 40.0 40,0 21.4 18.6

Cumulative Loan Disbursement

FY76 FY77 FY78 FY79 PY80 PY81 FY82 FY83

(i) Planned 1.6 12.6 28.30 37.30 40.00 40.00 40.00 40.00(ii) Actual - 2.0 7.10 14.64 22.92 31.22 35.78 40.00(iii) (ii) as % - 15.90 25.00 39.30 57.30 78.05 89.45 100.00

of (i)

Other Project Data Actual

Board Approval May 18, 1976Loan Agreement June 10, 1976Effectiveness August 10, 1976Loan ClosingOrg.ginal December 31, 1978Actual March 31, 1983

Borrower Government of IndiaExecutive Agency IDBI

- iii -

PROJECT COMPLETION REPORT

INDIA - SECOND IDBI/SFCs PROJECT

(LOAN 1260-IN)

MISSION DATA

Month/ Number of Number of Staff Date ofYear Weeks Persons Weeks Report

Appraisal 05/75 6 4 24 10/75

Supervision 12/77 5 4 20 03/77

Supervision 01/78 3 2 6 03/78

Supervision 02/79 4 3 12 04/79

Supervision 03/80 2 2 4 04/80

Supervision 02/81 2 3 6 04/81

Supervision 05/82 3 3 9 07/82

Completion 10/86 2 1 4 03/87

- iv -

PROJECT COMPLETION REPORT

INDIA - SECOND IDBI/SFCs PROJECT

(LOAN 1260-IN)

HIGHLIGHTS

1. Loan 1260-IN, which financed the second IDBI/SFCs Project in India,was designed to support the objectives of the first Project. The two majorobjectives were: (i) to provide financial assistance to high-priorityindustrial enterprises in the SMI sector; and (ii) to upgrade 18 StateFinancial Corporations (SFC) through specific institution-building programs,in order to help improve India's credit delivery system to SKI. In the faceof the large number of SFCs iavolved, their deep-seated problems and theextensive assistance requirements, the scope of the first Project was veryambitious; and the Project was only partially successful in realizing itsinstitution-building objectives. The majority of SFCs still needed assis-tance to improve their organizational structures, the quality of appraisalsand supervision and collection procedures. Under the second Project,therefore, the institutional upgrading program focussed on improving thequality of management and staff, stieamlining procedures and strengtheningappraisal capacity (para. 4.08).

2. The project partly achieved its objectives. There was rapid growthin the SFCs' lending operations during the first half of the 1980s. Moreresources were allocated for industrial enterprises in less developed areas.The eighteen SFCs tully disbursed the Loan of US$40 million to 604 sub-projects by March 1983. SFCs and Industrial Development Bank of India (IDBI)disbursed a total of Rs 628.66 million (equivalent of US$78.6 million) andrefinancing of Rs 529.73 million (equivalent of US$66.2 million),respectively, for these subprojects. The Loan contributed 65% of IDBI'stotal refinances, as agreed with the Bank under the Loan. The sectoral andsize distribution of the subprojects supported by the Loan was satisfactory.Subloans were concentrated in light engineering, chemicals, and electronics.Seventy percent of subloans were "B" projects (under Rs 2 million crUS$250,000), indicating that adequate attention was given to smaller units(pdra. 5.01).

3. On the whole, the subprojects financed under the Loan indicate someimprovement in the overall performance relative to those under the firstProject. Based on the IDBI's ex-post review of the results of 69subprojects, about 5,044 jobs, wbich representad 91% of the projected level,were generated; average investment cost per job was US$9,795; and annualexport earnings estimated at Rs 59.2 million (US$7.5 million). Under thisLoan, there was a considerable improvement in economic and financial perfor-mance of subprojects, compared to those under the first Project. Apart fromdirect benefits, such as incremental investment and employment generation,the Project also contributed significantly to the diffusion of modern tech-nology to small and medium industries. However, the delays in implementationand resultant cost overruns experienced in the first Project continued in

_ lr -

this Project. Although some factors that caused time and cost overruns werebeyond the control of the lending institutions, nevertheless SFCs could havedealt with these problems to a significant extent, if they had properlystrengthened their appraisal capability to review more carefully technicaldesigns, to assess project costs more realistically, to allow for adequateprice escalations and physical contingencies and to develop more realisticfinancing plans and implementation schedules (paras. 5.04-5.08).

4. On the objective of institution-building, the project had a positiveimpact. Lessons learned and experience gained through the first Projectenabled IDBI and SFCs to achieve some tangible results. IDBI,,as the apexdevelopment bank in India, substantially enhanced its interactions with SFCsand actively assisted tOem to implement the institutional upgrading programsduring the project period. While IDBI devised effective communication chan-nels with SPCs, IDBI itself underwent changes in organizational structure inorder to achieve higher efficiency. Most SFCs have extended the term ofManaging Directors to two years or more, in order to retain the continuityessential for institutional upgrading. The management quality of SFCs hasalso improved to a significant extent. Clearly, there is room for furtherdevelopment in the area, and hence many SPCs are strengthening management andstaff capability by various training programs offered by the ManagementDevelopment Institute, Bankers Training College, RBI and IDBI. Several SFCsrecently created separate appraisal and recovery departments which are tohelp refine the quality and effectiveness of loan processing and supervision;and others have adopted Management Information Systems which helpedstrengthen the personnel functions and streamline the procedures (paras. 4.09and 4.18).

5. While an indigenous instLtutional capacity for term financing of SMIis developing, the serious problem of collections and arrears has persisted.The drive to accelerate project approvals without comparable results fromimproved collections led to an increased level of arrears. The high levelof arrears tied up a large amount of resources, and led SFCs to increaseddependence on external sources for financing their new loans, as well astheir debt service obligations (paras. 4.02 and 4.04). In the past fiscalyear, 1985/86, several SFCs initiated various sbhemes to increase collectionincluding: (i) an incentive to subborrowers for timely repayment (funds formodernization and T.A.); (ii) exercise of 8FCs' right (empowered by the SFCAct, Section 32G of 1985) to recover the certified amount in the same marxeras arrears of land revenue; (iii) an incentive bonus scheme applied to thestaff for successful collectinn; and (iv) strengthening project supervisionand loan recovery activities. Ic is premature to assess the full impact ofthese measures on the arrears problem. Nevertheless, SFCs will have to makemuch greater efforts to resolve this long-standing problem in order toachieve the objective of becoming a sound credit delivery system serving theSKI sector (para. 4.03).

6. The implementation of Credit 356-IN and Loan 1260-IN provides animportant lesson. The experience of lending through an apex agency subjectto a system requiring interaction with central and state governments by meansof institutional processes outside of its direct control may require somedilution of good banking practice. For example, the record of low collec-tions and mounting arrears suggests that there needs to be a common under-standing among all parties concerned of the objectives of financial institu-tions concerned. The SFCs were clearly unable to sustain internal account-

- vi -

ability for loan quality and IDBI was unable to effectively discipline theseinstitutions, given the political priority accorded to rapid expansion inlending. It would help if IDBI were given some legal instruments to enforcefinancial disc'pline on the SFCs. Firm commitments by financial inter-mediaries and consistent support by state governments to institutionaldevelopment is extremely important, if financial and institutional objectivesare to be achieved. In particulars stability and quality of top managementneeds to be retained for the effectiveness of leadership and organizations.Moreover, commitment to the longer term financial viability must rank inimportance with lending targets, and all concerned agencies must encouragethe SFCs to make the firm decisions which will be necessary to improve col-lection performance. IDBI's continued support to SFCs should be. linked tocollection performance as measured by specific targets (Attachment, page 4).

PROJECT COMPLETION REPORT

INDIA - SECOND IDBI/SFCs PROJECT

(LOAN 1260-IN)

I. INTRODUCTION

1.01 IDA Credit 356-IN of US$25.0 million, to the Government of India(GOI) in January 1973, was the first World Bank project for small scaleindustry in India, and the Bank's first involvement with the IndustrialDevelopment Bank of India (IDBI) and India's State Financial Corporations(SFCs). The second IDBI/SFCs Project (Loan 1260-IN) of US$40 million wasapproved in 1976 for the same purpose. In each project, IDBI was selected asthe executing agency and the apex institution, because it was already provid-ing local refinancing for the lending operations of the SFCs. Also, IDBI wasconsidered to be in a good position, on the basis of its equity shares in theSFCs to exert financial discipline on these state-level financial institu-tions and to provide technical assistance to them through an institutionalupgrading program which the Bank Group supported.

1.02 The PCR and PPAR for the first IDBI/SFCs project were issued in 1982and 1984 respectively. These reports assessed the institutional developmentof IDBI and SPCs as of the respective dates, and reviewed subproject perfor-mance of small and medium industries based on statistical data available upto 1980/81. Therefore, this PCR for Loan 1260-IN covers the remainingproject implementation period, 1981-83 and thereafter up to 1985/86 withrespect to SFCs' institutional development and subproject performance.

II. ECONOMIC ENVIRONMENT

Economic Performance

2.01 India's economy has grown more rapidly in the past ten years than inany previous decade since the early 1950s, and came through the difficultperiod after the first oil shock in 1973 without major economic disruptions.India adjusted to the first oil price increase mainly through additionalexport earnings supported by appropriate exchange rate and domestic policies,and hence industry and overall economic performance improved. In 1979, whileIndia responded to the second major oil price increase with successful importsubstitution in foodgrains and petroleum, the real exchange rate appreciatedand export, industrial and overall growth declined. Industry's contributionto GDP stagnated as annual growth of output barely kept up with GDP growth.The initially high growth of the inadustrial sector gradually declined from 8%in the late fifties to middle sixties to less than 6% during the decade ofthe seventies, and to 2% in the first years of the current decade.Underlying these trends were declining factor productivity, implying a steadydeterioration in efficiency of resource use. Positive factor productivity inrelatively few industries was offset by negative or zero growth in others.The long-term objectives of industrialization -- accelerated growth andproductivity improvement -- therefore remain as priority objectives.

-2-

2.02 The pattern of industrial activity during the implementation periodof the second IDBI/SFCs Project (1976-83) is generally characterized by themajor setback to India's industry. Manufacturing stagnated and capacityutilization slipped to the low level of the early seventies. The second oilshock of 1979 was severely compounded by wide-spread failure of the monsoon,resulting in a sharp decline in agricultural production. Consequent declinein inputs for important agro-industries depressed demand in rural areas formajor consumer goods. The drought also influenced production through crip-pling infrastructural bottlenecks in power and transportation. Fortunatelypexternal reserves were initially ample because of large inflows of workers'remittances and continuation of foreign aid disbursements. In addition, GOInegotiated a three-year program with the IMF using the Extended Fund Facilityto stem the decline in reserves. Domestic constraints thus coincided WiLthample foreign currency resource availability at the beginning of the period.As import liberalization began to spread wider in subsequent years, competi-tive pressures on Indian industry began to develop, which increasinglyrevealed the need for modernization through technology-upgrading,rationalization and foreign collaboration arrangements to improve capacityutilization, efficiency and product quality.

Recent Policy Changes

2.03 Since 1983, concern with India's industrial performance has led GOIto reassess its industrial strategy and related system of controls. Duringthe past few years, a more pragmatic approach to industrial development hasbeen manifested. Important modifications were introduced in the industrial,fiscal and capital market policy framework. The principal objective of theindustrial policy initiatives have been those of deregulating the economywith a view to accelerate the growth and to achieve more efficient use ofresources, especially of capital, thereby improving the competitiveness ofIndian industry. In March 1985, a significant beginning towards deregulationwas made, exempting companies other than MRTP and FERA companies from thepurviews of licensing requirement. Initially, 25 broad groups of industrieswere delicensed, followed by 82 bulk drugs and related formulations inJune 1985. To alleviate the problems arising out of capacity fragmentation,the Government announced, in May 1986, that letters of intent will be issuedregarding the minimum capacity sizes for 65 major industries. Another changemade in the licensing policy, i.e., "broad-banding" of licenses, aims optimumutilization of industrial capacity in keeping with the evolving market condi-tions of supply and demand.

2.04 The Long-Term Fiscal Policy (LTFP) was presented to Parliament inDecember 1985. Its objectives is to impart a greater degree of predict-ability and stability to the Government fiscal policy over the Seventh Planperiod. The thrust of the FY86/87 Budget is directed towards rationalizationand simplification of both direct and indirect taz arrangements as con-templated in LTFP. In direct taxation, the Government announced severalmeasures to affect corporate taxation, and in indirect taxation introducedthe Modified Value Added Tax (MODVAT) for rationalizing the excise dutystructure and doing away with the cascading effects of indirect taxes. Inorder to encourage healthy growth of the capital market, Government hiasliberalized restrictions on capital markets; and both the equity and deben-ture markets have grown rapidly.

-3-

Small and Medium Industries

2.05 In the 1970s, India was making special efforts to develop small- andmedium-scale industries (SMI) at both the federal and the state levels. Thissector was considered important for actual and potential contribution tooutput, employment and income distribution. The development of small, labor-intensive industries was expected to function as an especially convenientvehicle for economic growth and export expansion in less developed areas. In1972, small industries contributed about 502 of value added and 80X ofemployment in the entire manufacturing sector. At that time, GOI defined asmall-scale manufacturing unit as one with investment of less than Rs 750,000in plant and equipment (currently the official definition specifies theinvestment size of SSI unit less than Rs 3.5 million). Important policyinstruments affecting the SKI sector in the 1970s were (i) industrial andimport licensing and (ii) targets set by the Reserve Bank of India (RBI) forcommercial bank lending to priority sectors, such as SSI. The Governmentinitiated an array of fiscal and financial incentives 1/ to stimulate thedevelopment of SSIs and reserved many product groups for exclusive productionby the small-scale sector. In 1979, GOI extended the reservation to 807items and in October 1986 to 863 items.

2.06 National and State institutions were established to provide technicalassistance and infrastructural facilities to small industries. Commercialbanks and State Financial Corporations (SFCs), the latter being specializedinstitutions providing term finance to small and medium size enterprises,have been the principal sources of SKI finance. IDBI, an apex term-lendinginstitution, has played a major indirect role in financing SMI projects byrefinancing SFC loans. Commercial banks have provided the bulk of financing,mainly working capital, to SMI enterprises. In the latter part of the 1970s,term lending also became an important activity for these banks. In the areasof promotion, technical assistance and extension services, IDBI sponsored thecreation of eight Technical Consultancy Organizations (TCOs) which operate asnon-profit, state-level agencies. In May 1986, GOI announced the estab-lishment of a separate fund called Small Industries Development Fund (SIDF)in IDBI. This Fund is exclusively for the development, expansion,modernization, diversification and rehabilitation of the small sector, cover-ing a wide spectrum of small-scale, tiny, village and cottage sectors.Besides ensuring increased flow of financial and non-financial assistance tothe SSI sector, the SIDP is intended to serve as a focal point for effectivecoordination of the promotional activities by various organizations,

Investment Trends

2.07 The contribution of SFC loans to total investments (gross domesticinvestment) in the manufacturing sector during FY81-85 is shown below:

1/ Incentives included credit at concessionary terms, hire-purchaseschemes, special deductions on income taxes for priority industries,simplified licensing procedures, and a Credit Guarantee Scheme (CCS)administered by RBI. In addition, each state provided wide-range taxconcessions for location in"backward districts" where many small-scaleunits are concentrated.

-4-

Table 1: SFCs DISBURSEMENT PATTERN

(Rs billion) SFC Dis-SFCs Dis- bursements

GDI /a Total /b SFCs bursements as % of totalRet. Manuf. Disbursements Disbursements as % of GDI Disbursements

FY81 60.48 17.29 2.48 4.10 14.34FY82 71.98 20,64 3.18 4.42 15.41FY83 73.06 23.58 4.04 5.53 17.13FY84 79.61 28.93 4.35 5.46 15.04FY85 91.27 34.08 4.99 5.47 14.64Total 376.40 124.52 19.04 5.06 15.29

/a Gross Domestic Investment.

/b Includes disbursements of All-India Financial Institutions (IDBI, IFCI,ICICI, IRCI9 LIC, UTI) SFCs and SIDC.

Source: Work Bank Report No. 6090-IN Economic Situation and DevelopmentProjects of India, May 9, 1986, Table 2.6; IDBI's OperationalStatistics.

The total disbursements of All-India Financial Institutions, SFCs and SIDCshave increased to about 35% of GDI in registered manufacturing in FY85 from a25% level maintained during the second half of 1970s, of which 5.5% has beenfrom SFCs. Of the total disbursements, all SFCs have maintained 0 15Z levelover the past five years, FY81-85. Registered manufacturing increased from15% of CDI in FY77 to 18% in FY85; unregistered manufacturing is estimatedat about 6% of total GDI; the share of manufacturing in total GDI was about23% at the end of FY85.

III. THE PROJECT

Project Objectives

3.01 Until 1973, Bank Group financing of industrial investment had con-sisted of medium and large scale units either through direct financing orthrough the financing of the Industrial Credit and Investment Corporation ofIndia (ICICI). IDA Credit 356-IN (US$25 million) was the first Bank Groupproject to focus on the small scale industrial sector. The Credit was chan-neled through the Industrial Development Bank of India (IDBI) to

-5-

18 SFCs 1/ for relending to small- and medium-scale industry with two basicobjectives: (i) to finance the import component of high-priority i.tdustrialenterprises in the SMI sector, and (ii) to assist in upgrading the operationsand procedures of the SFCs through the review and refinance operations ofIDBI.

3.02 In 1976 the Bank undertook the Second IDBI/SFCs Project (Loan1260-IN; US$40 million). The objectives of this Loan were (i) to expandfinancial assistance to the small and medium scale industrial sector; and(ii) to contribute to the on-going institutional upgrading of the SFCs. Atthe time of the first Credit, the SFCs suffered from a number of weaknesses,including shortcomings in the quality of management and staff, inadequateprocedures and appraisal standards, high arrears and insufficient provisionsfor possible losses. To assist SFCs in alleviating these shortcomings, IDBIand Industrial Finance Department (IFD of RBI) developed specific institu-tional upgrading programs, which IDA agreed to include in the first Project.In the initial two years, considerable progress was made, particularly inmanagement, general operational procedures, and appraisal standards.However, in subsequent years, the upgrading programs themselves were found tobe insufficiently detailed and not broad enough in scope. Accordingly,IDBI/IFD prepared revised upgrading programs 2/ based on IDA's recommenda-tions in March/April 1975. Implementation of these revised programs formedone of the major objectives of the second Project.

Project Design

3.03 As in the previous Credit (356-IN), the Project involved a loan toIDBI, an apex institution, for on-lending to SMI through 18 SFCs, whichcovered the entire country. The Project did not include promotional ortechnical assistance components for SMI, because these were deemed to bealready available and because the Bank expected to have greater impact bystrengthening the credit delivery system. In view of the objectives toupgrade SFC standards and to support SMI enterprises, the lehding schemerequired special arrangements to ensure effectiveness and efficientadministration of the Loan.

3.04 Subloan Criteria. The eligibility criteria for subloans clearlyplaced the project in the small and medium scale sector. IDBI establishedbasic financial and economic selection criteria for subloans, and these wereapproved by the Bank. Under the SFC Act, SFC subloans were limited to amaximum size of Rs 3 million. 3/ Eligible enterprises had to have a totalequity (paid-up share capital and free reserves) of no more than Rs 10

1/ SFCs are responsible for providing medium and long term finance, under-writing facilities and guaranties to small and medium scale industrialunits, and had total outstanding of Rs 2.8 billion as of March 31, 1975.(Appraisal Report No. 1158-IN)

2/ The programs included detailed recommendations on management, organiza-tion and staffing, policies and procedures, appraisal standards.

3/ It has been raised to Rs 6 million; and the SSr definition has beenaltered to enhance the limit of investment in plant and machinery fromRs 2 million to Rs 3.5 million (Attachment, page 5).

-6-

million. The Bank Loan financed imports, mainly of capital equipment butalso raw materials that constituted permanent working capital in a project.The Bank fixed its disbursement proportion at 65Z of TDBI's refinance toSFCs.

3.05 Terms and Conditions. The proceeds of the Loan were on-lent by IDBIto SFCs at an interest rate of 82 per annum in the case of SFCs re-lending tosmall-scale units covered under the Credit Guarantee Schemep technician-entrepreneurs and units in specified backward districts. SFC re-lent tothese subborrowers at 11.5. In case of all other lending, the correspondingon-lending and re-lending rates were 8.752 and not less than 12,OZ. GOIon-lent the Bank loan to IDBI at an interest rate of 7.752 (excluding 0.25Xrebate for prompt payment). These rates provided the SFCs with a spread of3.52, which was larger than the 2.52 spread under the Credit 356-IN. Thiswas mainly due to an increase in the re-lending rate to subborrowers. Theforeign exchange risk was borne by GOI. Only those SFCs that adopted andcontinued to meet the requirement of the upgrading program were eligible toparticipate under the Loan. The free limit was raised from Rs 1 millionunder the first loan to Rs 2.5 million under this loan.

Institutional Arrangements

3.06 IDBI was selected as the apex agency for the Project because italready had a refinance role in India's financial system, and through its SFCshareholdings (50% of capital) and its monitoring and reviewresponsibilities, IDBI was considered a capable institution to exert finan-cial discipline over the SFCs and to upgrade their operations. In an effortto improve SFC*s operations, IDBI and RBI jointly,developed individualupgrading programs which IDA agreed to form a part of the first Credit. Inthe context of the first Project, deficiencies in these programs wereidentified, such as insufficient detail and limited scope (para. 4.08). Theprograms were therefore revised to tailor them to the specific needs of eachSFC with detailed recommendations on mgnagement, organization and staffing,policies and procedures, appraisal standards, portfolio quality and financialmanagement and planning. Along with the debt service coverage limitations,an agreement between IDBI and each SFC on these revised upgrading programsbecame the basis of each SFC's eligibility for participation under the Loan(1260-IN).

IV. PERFORKANCE OF IMPLEMENTING AGENCIES

SFCs Operations

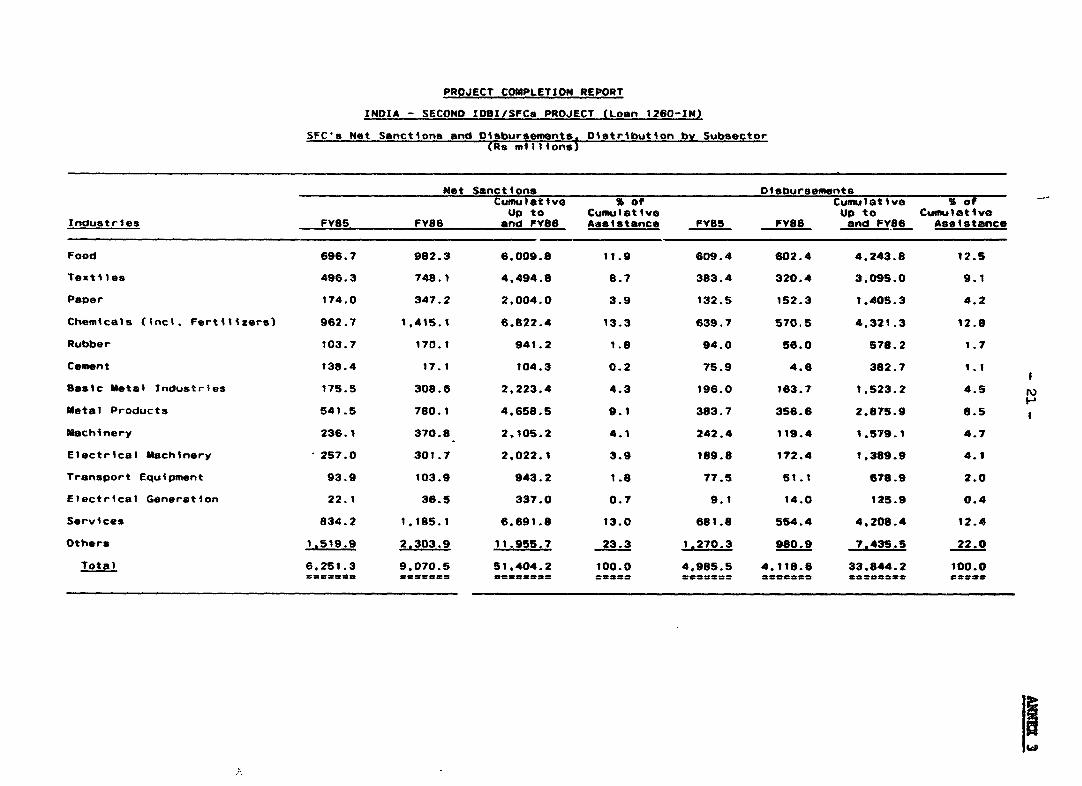

4.01 Investments. Net sanctions for all SFC9 increased by about two andhalf times between FY81 and FY86, rising from Rs 3.7 billion to Rs 9.1billion, a rate of nearly 202 per annum. Of these sanctions, 902 in valueterms were new projects, 76% for 8SI and 512 for units located in backwardareas. Public sector units were assisted only through joint financing withthe State Industrial Development Corporation (SIDC); and the private sectorcontinued to receive the bulk of SFC assistance. Five subsectors accountedfor almost 502 of total sanctions, i.e. chemical and chemical products(142), food processing (112), metal products (92), textiles (82) andmachinery (52). Additional data on subsector distribution of loans are shownin Annex 3. The average size of SPC loans decreased from Rs 210,000 in FY77

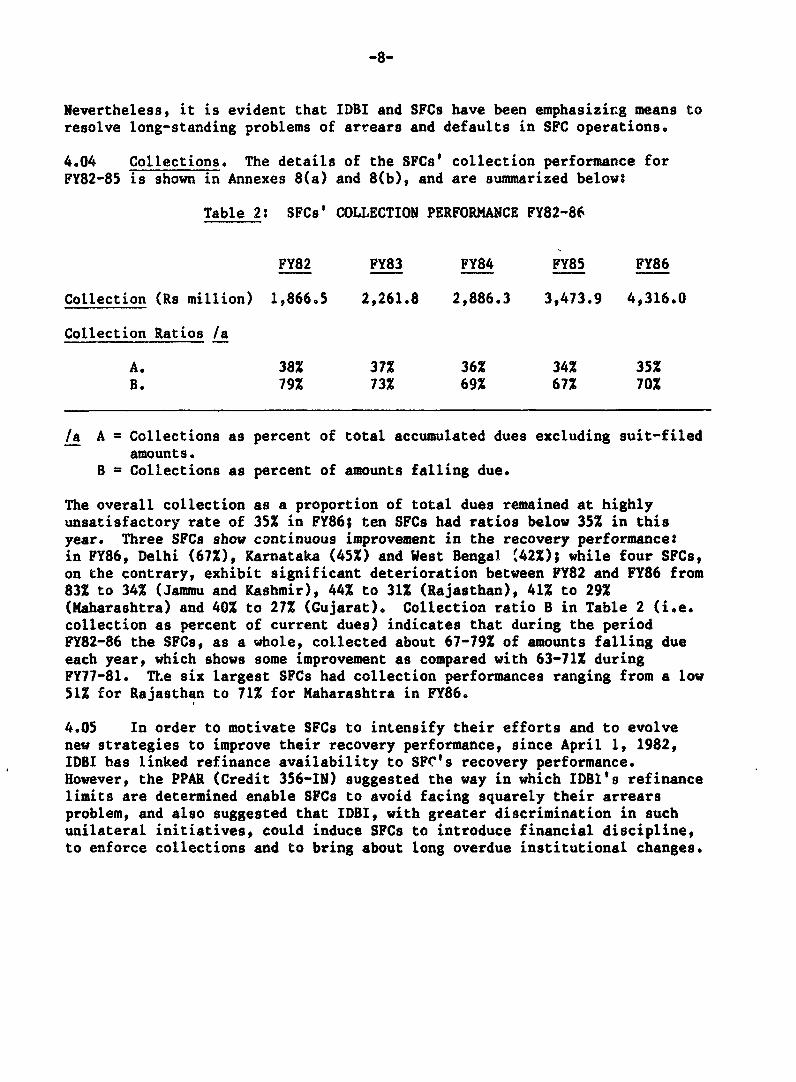

-7-

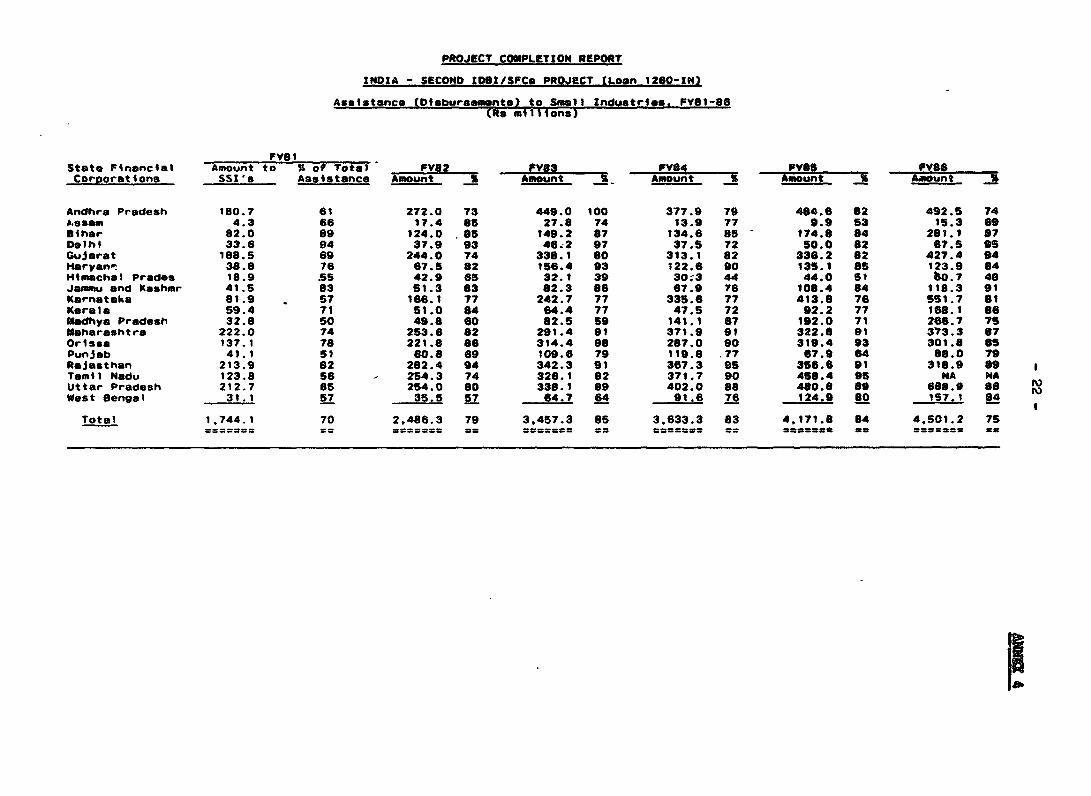

to Re 166,000 in PY84, but has risen since that time to Rs 310,000 in FY86.Annex 4 shows the increase in lending to SSI and Annex 5 the lending tobackward areas. The high growth figures recorded in these annexes, takentogether with the arrears problem discussed below, illustrate the problemendemic to all the SFCs: a heavy emphasis on loan approvals which outweightsthe attention to supervision, collection and arrears. The main factor caus-ing the rapid growth in approvals was that the SFCs' managements were judgedby the state governments on their ability to approve an increasing number ofprojects. In addition, both central and state governments have emphasizedthe development of SSI and backward regione; and SFCs have accorded highpriority to these twin tasks.

4.02 Arrears. The problem of collections and arrears remains. While SFCshave been seriously pursuing the upgrading programs (para. 4.09), theirrecovery position, as judged by the proportion of recoveries to outstandings,has not improved. A breakdown of arrears by SFC for FY82-86 is shown inAnnex 6. In FY81, the SFCs' total arrears were Re 2.6 billion, which repre-sented about 271 of the SFCs' combined portfolios at that time, ranging from10% (Andhra Pradesh and Jammu and Kashmir) to 561 (Assam). In the two fol-lowing years (FY82 and FY83), the proportion decreased to around 251, butincreased thereafter reaching 31% of their combined portfolios by FY86.During the past 5 years, in only four States have the arrears positionimproved-Karnataka (261), M4adhya Pradesh (141), West Bengal (171) and Delhi(19Z); in all other states there was further deterioration. The causes arewell identified in PPAR (Credit 356-IN). Although the growth of arrears aredue in part to the rapid growth of the portfolio, a disquieting feature istheir chronic nature, with a good part overdue for two years or more.Perhaps more disturbing is the existence of wilful defaulters, arising ini-tially from the soft attitude taken by the SFCs in handling their cases andthe resulting impunity of borrowers to penalties for delinquency; and theweak recovery machinery of the SFCs, including insufficient iniormation onindividual subborrowers (Attachment, page 4).

4.03 Recently, many SFCs have taken steps to reduce arrears, including:strengthening project supervision and loan recovery activities, reducing thedifferential between short- and long-term rates through a rebate scheme forprompt repayment and penal isates for delayed payments, and using recourse toSection 29 of SFCs Act for take-over of management, outright sale, andrevenue recovery proceedings (Attachment, page 4). Also, Default ReviewCommittees in SFCs monitor the arrears and review the defaulting accounitscase-by-case. Each SFC has now assigned senior level officials to be incharge of collection activity. In addition, during FY86 three specificmeasures have been implemented. First, as an incentive to subborrowers torepay on time, 8FC provides additional funds to them for modernization andother technical assistance. The fund comprises contributions from SFCs(401), IDBI (40%) and the subborrower (201). The scheme has already coveredtwenty-five units. Second, newly added Section 32G to the SFC Act (1985Amendment) empowers SFCs to make an application to a state government forrecovery of the amount due to the SFC, and enables the Collector to processrecovery of the certified amount (by the State Government) in the same manneras arrears of land revenue. Third, to stimulate collection activity, someSFCs have devised an incentive bonus scheme, which provides a bonus up to 251of annual salary for successful collection, compared to a normal maximumbonus rate of 8 1/31 for all staff members of SFCs. It is too soon to assessthe impact of these measures on the overall collection performance.

-8-

Nevertheless, it is evident that IDBI and SFCs have been emphasizir.g means toresolve long-standing problems of arrears and defaults in SFC operations.

4.04 Collections. The details of the SFCs' collection performance forFY82-85 is shown in Annexes 8(a) and 8(b), and are summarized below:

Table 2: SFCs' COLLECTION PERFORMANCE FY82-86

FY82 FY83 FY84 FY85 FY86

Collection (Rs million) 1,866.5 2,261.8 2,886.3 3,473.9 4,316.0

Collection Ratios /a

A. 38% 37% 36Z 34% 35%B. 79% 73% 69% 67% 70%

/a A = Collections as percent of total accumulated dues excluding suit-filedamounts.

B = Collections as percent of amounts falling due.

The overall collection as a proportion of total dues remained at highlyunsatisfactory rate of 35% in FY86; ten SFCs had ratios below 352 in thisyear. Three SFCs show continuous improvement in the recovery performance:in FY86, Delhi (67%), Karnataka (45%) and West Bengal '42%); while four SFCs,on the contrary, exhibit significant deterioration between FY82 and FY86 from83% to 34% (Jammu and Kashmir), 44% to 31% (Rajasthan), 41% to 29%(Maharashtra) and 40% to 27% (Gujarat). Collection ratio B in Table 2 (i.e.collection as percent of current dues) indicates that during the periodFY82-86 the SFCs. as a whole, collected about 67-79% of amounts falling dueeach year, which shows some improvement as compared with 63-71% duringFY77-81. The six largest SFCs had collection performances ranging from a low51% for Rajasthan to 71% for Maharashtra in FY86.

4.05 In order to motivate SFCs to intensify their efforts and to evolvenew strategies to improve their recovery performance, since April 1, 1982,IDBI has linked refinance availability to SFr's recovery performance.However, the PPAR (Credit 356-IN) suggested the way in which IDB1's refinancelimits are determined enable SFCs to avoid facing squarely their arrearsproblem, and also suggested that IDBI, with greater discrimination in suchunilateral initiatives, could induce SFCs to introduce financial discipline,to enforce collections and to bring about long overdue institutional changes.

-9-

4.06 Debt Service Coverage Ratio (DSCR). 1/ Annex 7 shows the DSCR (ona cash basis) for each SFC' from FY82 to FY86. The Bank recommended in April1980 the measure of the DSCR on a cash basis which was more realistic test ofcredit-worthiness than the accrual basis. Except for FY82, when 12 SFCs hadDSCRs above 1.0, the DSCR position of a majority of SFCs deteriorated in thefollowing two years. But, in FY86 the position slightly recovered with 9SFCs having DSCRs above 1.0. The higher ratios were 1.59 (Delhi), 1.29(Haryana) and 1.23 (Kerala). In the same year, 9 SFCs had DSCRs below 1.0,as compared to 15 SFCs in FY80 with a DSCR below 1.0.

4.07 Operations. Annex 9 provides a summary of financial statistics ofSFCs for FY82-86 and Annex 10 shows the consolidated balance sheet for allSFCs during FY82-86. Cumulative disbursements were nearly 71% ofcommitments, as compared with only 62% during the period of FY72-81 (PCR forCredit 356-IN, para. 3.07). Under the Business Plan and Resources Forecast(BPRF) exercised by IDBI, targets of loan approvals are set, taking intoaccount the organizational and resource mobilization effort of each SFC. Asa result, gaps between loan sanctions and disbursements by SFCs has graduallynarrowed over the past several years. During the period FY82-86, SFC's totalassets/liabilities grew from Rs 13.3 billion to Rs 27.4 billion and theircombined share capital grew from Rs 1.6 billion to Rs 3.8 billion. Thecombined debt!equity ratio of all SFCs was 4.1 in recent years. Profitmargins decreased largely due to increased administrative costs; for example,on a combined basis the SFCs' return on equity declined from 7.8% in FY82,4.7% in FY86.

SFCs Institutional Achievement

4.08 Upgrading Programs. Under this Project, the upgrading programsinitiated under the first IDBI/SFCs Project, were revised incorporatingproposals to:

(a) increase the role of the Boards of Directors and the sanctioningauthority of the Executive Committee;

(b) provide the continuity and smooth turnover of top management and thestrengthening of the second layer of management; and

(c) restructure IDBI/SFCs interest rate structures (para. 3.04).

These revised upgrading programs, along with the debt service coveragelimitation, formed the basis for an agreement between IDBI and each SFC toenable the latter to be eligible for withdrawal under the Loan. The programfor each SFC envisaged improvements in management, organization, staffing,policies and procedures, appraisal standards, improvements in portfolio

1/ Upon IDBI's request, Bank made informally a few modifications to thecovenant (Credit 356): - (i) In November 1976 the Bank aliowed a temporaryrelaxation of the DSCR from 1.25 to 1.0, provided that satisfactoryrecovery and follow-up action programs were adopted by the SFCs; (ii) InMarch 1977 the Bank agreed to modify the DSCR definition to include addi-tional share capital, if paid-in within nine months after the end of thefiscal year.

-10-

quality and financial management and planning. (Appraisal Report No.1158-IN).

4.09 Over the last five years, many SFCs notably, those in Karnataka,Madhya Pradesh, Orissa, Kerala, Andhra Pradesh, Bihar, Tamil Nadu, Punjab,H.P. and J&K, have restructured their organization and streamlinedpolicies/procedures concerning loan sanctions. SFCs' achievements have beengreatly facilitated by IDBI's influence and development measures taken underthe institutional upgrading programs. IDBI monitors the overall operationsof SFCs through its annual evaluation and through Business Plan and ResourcesForecast (BPRF). The latter serves also as an instrument to evaluate theadministrative structure, management and staffing of each SFC, to assess theoperational policies and procedures, and to establish standards of appraisaland supervision.

4.10 Management. SFC Managing Directors are appointed by the stategovernment in consultation with IDBI. Rapid turnover of Managing Directorshas undermined the management continuity needed for institutional upgrading.In 1980, IDBI issued to all state governments a comprehensive set ofguidelines in respect to appointment, tenure, change of Managing Directors ofSFCs. Since then, state governments have increasingly been aware of the needfor providing a reasonably long tenure to the top management. Currently, asmany as 15 SFCs extend the term of Managing Directors for two to five years,while several States have set a minimum tenure of three years (Attachment,page 6). Overall, SPC management quality has improved to a significantexteat, while several SFCs have already adopted a proposed minimum three-yearterm. Also, the second layer of management has been considerablystrengthened through the recruitment of qualified professionals from avariety of disciplines.

4.11 Staff. As a part of the upgrading program in the second IDBI/SFCsProject, the Bank emphasized the need to recruit additional professionalstaff, particularly to strengthen follow-up work, and to provide more techni-cal and legal expertise. Annex 11 shows the growth pattern of professionaland other staff from PY82 to PY85 for each SFC. Total recruitment of profes-sionals in SFCs increased from 1,729 in end-FY82 to 2,168 in end-FY85, at thegrowth rate of 7.8% p.a., even though total employment of Bihar and DelhiSFCs slightly decreased over the period. The pay scales, which are linked toState Government levels, had seriously constrained the recruitment of vir-tually all SFCs. IDBI reported that a recent revision of the pay scales hasmade them more competitive and may allow SFCs to attract more competentstaff.

4.12 Training. For the past three years, considerable effort has beendevoted to the training of professional staff. More than 900 professionalsunderwent training in project appraisal and supervision courses offered bythe Management Development Institute, Bankers Training College, Reserve Bankof India and IDBI. This training has improved the quality of staff in SFCs.Prior to 1982, the SFCs generally suffered from deficiencies in appraisalstandards, assessment of working capital requirements, evaluation ofmanagerial competence of the entrepreneurs, cost estimates, implementationschedules and financial projections. SFCs' project appraisal performance hasbeen gradually improving since then. Further, SFCs have been continuouslyimproving their competence in financial appraisal including ratio analysis,evaluation of technical, organizational and managerial aspects. IDBI reportsthat all SFCs have expressed willingness to improve further their staff

-11-

skill3 in project appraisal through the training opportunities provided byIDBI.

4.13 Project Appraisal. Sanctioning authority has been decentralized todelegate the authority to SFC regional/branch offices in charge. It hasgreatly accelerated the appraisal process, especially in the case of smallscale enterprises whose financial requirements are relatively small. SomeSFCs have opened 'Guidance Cells" to assist and guide entrepreneurs in com-pleting applications and furnishing the required information. The loanapplication formats are standardized; and SFCs now maintain better liaisonwith other state-level financial inititutions azd banks. Also, SFCs haveintroduced the concept of economic cost/benefit analysis to projectappraisal.

4.14 Institutional Coordination. The success of SFCs' effort to developindustries depends considerably on the extent to which SFCs are able to bringabout coordination among other state-level institutions and banks.Especially, such coordination is of particular help in providingentrepreneurs with assured flow of term loans and working capital financeduring project implementation. Over the review period (PY82-86), theinstitutional coordination between SFCs, commercial banks and state-levelagencies noticeably improved. Continuous periuasion was effective in gettingcommercial bank approvals of working capital finance to the projects whichSFCs assisted. In the case of coniortium financing, several SFCs (Karnataka,Kerala and West Bengal) adopted the system of exchanging appraisal memorandawith SIDCs and commercial banks. IDBI is also promoting close coordinationamong various state-level institutions to enable SFCs to act on the improve-ment of the credit delivery system.

4.15 Summary. Overall, SFCs devoted considerable attention to theimprovement of organizational structure during the secod IDBI/SFCs Project.Some SFCs created separate appraisal and recovery departments in order torefine the quality and effectiveness of loan processinO and supervision, andadopted Management Information Systems (MIS), which helps strengthen thepersonnel functions and streamline procedures. However, while the secondProject had some positive effect on the SFCs' management and other institu-tional upgrading aspects, it did not result in the improvement of collectionsand arrears position. The major increases in SFC activity were in loansanctions. The drive to accelerate project approvals successively increasedarrears without comparable results from improved collections. The recoveryrecord has in fact deteriorated since FY82. Persistent high levels ofarrears has tied up a large amount of resources, and has led to SFCs'increasing dependence on external sources to finance their new loans and tomeet their debt service obligations. It is expected that the new incentivesfor the collection drive would bring positive results.

IDBI's Performance

4.16 Under the Project, IDBI was assigned the pivotal role for monitoring,guiding and improving the performance of the SFCs. IDBI owns 502 of each SFCand the IDBI-SFCs telationship comprises board membership, guidance inpolicies, financial, managerial and technical advice and more importantlyprovision of capital and financial resources to s8Cs.

4.17 IDBI for SFCs' Institutional Development Program. Under the Loan(1260-IN), the eligibility for IDBI's refinancing facility waS tied to SPCs

-12-

effort to implement the revised upgrading programs. RBI and IDBI had jointlyformulated the original institutional upgrading programs for the SFCs, whichthe Bank agreed in 1972 as part of the first Credit (356-IN). Subsequentlyin 1975, IDBI and RBI developed detailed institutional upgrading programs foreach SFC covering the eight areas listed in para. 4.08. Under the secondProject IDBI/RBI presented to the SFCs specific programs to:

(a) Expedite review of loan applications;

(b) Improve appraisal standards, including preparation of industryprofiles;

(c) Expedite disbursement and introduce systematic reviews of slow dis-bursing projects;

(d) Improve pre- and post-implementation procedures and strengthenfollow-up and project supervision, including coverage and frequencyof supervision reports to be prepared to SFC managers;

(e) Pursue legal and other remedies to resolve overdue accounts; and

(f) Expand recruitment and training of professional staff (PCR, Credit356-IN para. 3.15).

However, as identified by the PCR (for Cr. 356-IN), the absence of specific-'time-bound" implementation of those programs was serious deficiency. Forthis reason, IDBI, through the annual evaluation report on the SFCsoperation, recently introduced sections summarizing the progress and atimetable for implementing the institutional upgrading programs. Initially,IDBI's evaluation reports tended to be, merely descriptive with insufficientanalysis of specific problems facing the SFCs. Over the past few years,however, the quality of reports and discussions between IDBI and the SFCs hasimproved, while the reports have also served as a vehicle to convey manage-ment iLnformation.

4.18 IDBI/SFCs Interaction. In the 1980s, IDBI actively assisted SFCs ininstitutional upgrading, especially with arrears/defaults, collections,continuity in management, 'nd identification of industrial problems specificto certain subsectors. To exchange views on problems of mutual interest,IDBI convened periodic conferences attended by the Chief Executives of SFCs,RBI, IDBI and Government representatives. The most recent conference washeld in April 1986. These conferences have served as useful forum forSFCs/IDBI interaction, and also provided insight into various operationalproblems that SFCs were facing. For IDBI, such conferences have provided anopportunity to assess the progress in SFCs' implementation of upgradingprograms as well as achievement in the key areas viz. recovery of dues,follow-up and monitoring projects, appraisal standards, manpower developmentand management capacity. Upon Bank's recommendation in 1980, IDBI has alsoassisted the SFCs in developing annual business plans and resource forecasts(BPRF). The annual exercise clearly provides a framework to establish objec-tives and to assess progress each year.

4.19 Some of the measures agreed upon at such conferences have had greatimpact on the SFCs performance when implemented. For example, in pursuanceof the decision taken at 22nd Conference in December 1983, IDBI appointed theDave Committee, comprising representatives of SFCs, RBI, IDBI under the

-13-

chairmanship of IDBI's Executive Director# to examine the financial structureand operation of SFCs in all aspects and make appropriate recommendations.The Committee submitted its report in June 1984 with a pet of specific recom-mentdations for containing the volume of arrears and developing balancedportfolios by diversifying into short/medium financing. Similarly, the 23rdConference in April 1985 formed a Committee to examine computerization ofAccounts and Systems Development of SFCs and establishment of a standardpackage for computer hardware as well as sqftware. IDBI accepted theCommittee Report in January 1986 and forwarded it to the SPCs for theiradoption. In fact, the PCR mission in October 1986 was informed that threeSFCs (AP, Karnataka and Kerala) have already installed computers, whileothers are actively pursuing the recommendations of the Committee.

4.20 Organizational Changes. llnder the first Project (Credit 356-IN),IDBI agreed to create three divisions within its Refinance Department --Appraisal, Operations, and Follow-up; and in 1976 IDBI decentralized most ofthe SFC evaluation and insp.ction functions to its regional offices in Delhi,Madrast Calcutta and Ahmedabad. This change has resulted in more effectivemonitoring and supervision of SFCs in recent years. In addition, IDBI set uptwo new departments during FY86, i.e. the Market Research Department and theTechnology Department, each headed by a General Manager. The former conductsresearch on demand potential, undertakes studies of marketing arrangements invarious industries and monitors market developments. The latter assists increating a technology data base, disseminating information on changingindustrial technology, and providing advice on technology transferarrangements. The two departments have been assisting project appraisals offinancial institutions with particular respect to technology, market researchand international competitiveness. To cater exclusively to the needs ofNon-Resident Indian (NRI) entrepreneurs, IDBI created a special "NRI Cell" inthe Head Office (Bombay). The primary objective is to work for greaterinteraction between NRIs and financial institutions.

4.21 Arrears and Recovery Measures. IDBI has continuously stressed co allSFCs the need to improve their recovery rates. As a result, the SFCs haveadopted a two-pronged program of (i) sharpening appraisal tools to preventtime and cost overruns and to ensure a sound financing pattern for assistedprojects and (ii) intensifying monitoring and recovery efforts by streamlin-ing procedures. In respect to default accounts, all institutions have heldmeetings of the Regional Executives (REMs) every two months in each region,reviewing and initiating remedial actions in close coordination with commer-cial banks. Also, most of SFCs have constitgted Default ReviewCommittees/Recovery Cells (Attachment, page 3). Throuth the Special RecoveryCell, IDBI monitors the recovery performance and stressts the credit recordsat the time of new project appraisal.

4.22 Summery. IDBI, as the apex development bank in India, has substan-tially enhanced its interaction with SFCs. Particularly, IDBI has activelyassisted SFCs to implement the revised institutional upgrading programs underthe Project (Loan 1260-IN). Some of the tangible outcomes were: (i) annualplanning exercises by .the SFCs which enable them to assess progress each yearagainst expected achievement; (ii) ovetall upgrading of the skills of SFCspersonnel; and (iii) enchanced interaction (e.g. conferences) between IDBIand SFCs to review SFC's financial/operational constraints. IDBI has nowembarked on assisting SFCs in building up computer-based management informa-tion systems. However, despite substantial and systematic effort on the partof IDBI.'s management and staff in institutional upgrading, the impact on the

-14-

improvements in SFC's operational/financial performance has been generallylimited. The state governments' power over the SFCs, has severely underminedIDBr's ability to fulfill its functions. State governmepts have constantlybeen involved in SPC matters -- for example, appointment of managing direc-tors and their premature transfer, emphasis on new loan approvals rather thanstrengthening existing firms, restrictions on staff recruitment to fillvacancies -- reflecting different perceptions, priorities and expedienciesregarding the role of the SPCs. Nevertheles,s, some improvements were notedin recent years. IDBI has been continuously working on the establishment ofa closer relationship with State governments on the SFC matters and, at thesame time, on creating effeqtive vehicles to communicate with SFCs and adviseon their performance.

V. SUBPROJECT PERFORMANCE

Outcome of Loan 1260-IX Subprojects

5.01 Sanctions and Disbursements. The Bank authorized 763 subprojectsunder Loan 1260-IN; 159 were cancelled subsequently, leaving 604 net ofcancellations. The original closing date was December 31, 1978, which wassubsequently extended twice to June 30, 1981 and to March 31, 1983.Extensions were requested by IDBI, largely because of slow proceeding ofcommitments and disbursements and partly because of a 21 interest premium ofBank funds over other funds available for designated backward areas. As ofMarch 31, 1983, the actual closing date of this Loan, the entire amount ofthe Loan of US$40 million (equivalent of Rs 360 million) was sanctioned.8FCs authorized a total of Rs 669.19 million, and IDBI authorized refinancingof Rs 545.35 million (Annex 12). As against the above authorizations, SFCsand IDBI disbursed Rs 628.66 million and Rs 527.73 million, respectively.The Loan contribution represented 651 of total IDBI refinannes (disbursed) inaccordance with the agreement reached with the Bank under the Loan.

5.02 The Sample. To evaluate the impact of subprojects financed, IDBIreviewed a random sample of 123 subprojects, i.e. a 201 sample, consistingof 47 "A" subprojects and 76 "B" subprojects. 1/ The detailed evaluation ofthese subproject's performance is sumarized below in respect to geographicaldistribution, size, profiles of projects, subsector distribution, cost andfinancial and economic performanee.

5.03 Geographical Distribution. As shown 1i Annex 12, five states -- Mad-hya Pradesh, Tamil Nadut Maharashtra, Gujarat -- accounted for 691 of sub-projects by number (415 out of 604) and 631 by amount (US$25.22 million outof US$40 million disbursements) (Annex 12). This distribution is due partlyto these States being more industrialized and having aggressive $FCs. TheSFC in Madhya Pradesh in particular has made a great progress in increasingthe number of subprojects and disbursements during the project period(Loan 1260). The "first-come-first serve" policy enabled the more aggressiveSFCs to take a large share of the loan uwder the second Project.

1/ "A" subprojects were those above the free limit"B" below the free limit (para. 3.04).

-15-

5.04 Size of Subloans and Subprojects. Most "A" subprojects were in therange between Rs 5 million and Rs 10 million. As regards "B" subprojects,the majority fell in the range of Rs 2 million and under. The average costsof "A" and "B" subprojects were Rs 11.71 million and Rs 2.13 million (equiv-alent of US$1.46 million and US$266,000), respectively. The average costs ofsubloans was Rs 1.64 million (equivalent of US$200,000). "A" and "B" sub-loans financed 14X and 23% of respective subproject costs. Although onlythree subprojects in the "A" sample belongtd to the smaxll scale sector, i.e.fixed investment of less than Rs 2.5 million, about 702 of the "B" sub-projects fell within the SSI defirition. The site distribution suggests thatsufficient attention was paid for the development of small industries, inaccordance with the project objectives.

5.05 Profile of Sub-Projects. Annex 14 shows the financing pattern of 88subprojects. The foreign exchange content was Rs 72.43 million, equivalentto 482 of the total amount of IDBI's refinance of the SFCs' loans. IDBI'srefinance (foreign exchange and rupee loans) constituted about 45Z of theSFCs' loans overall. The bulk of financing came from local funds, includingsponsors' equity. Of 107 subprojects, 72 were new, 27 involved expansion and8 modernization (Annex 15). The general pattern of SFCs financial assistanceclearly indicates a strong bias towards new project approvals, rather thanstrengthening and modernizing the existing industrial enterprises. This isconsistent with the first Project.

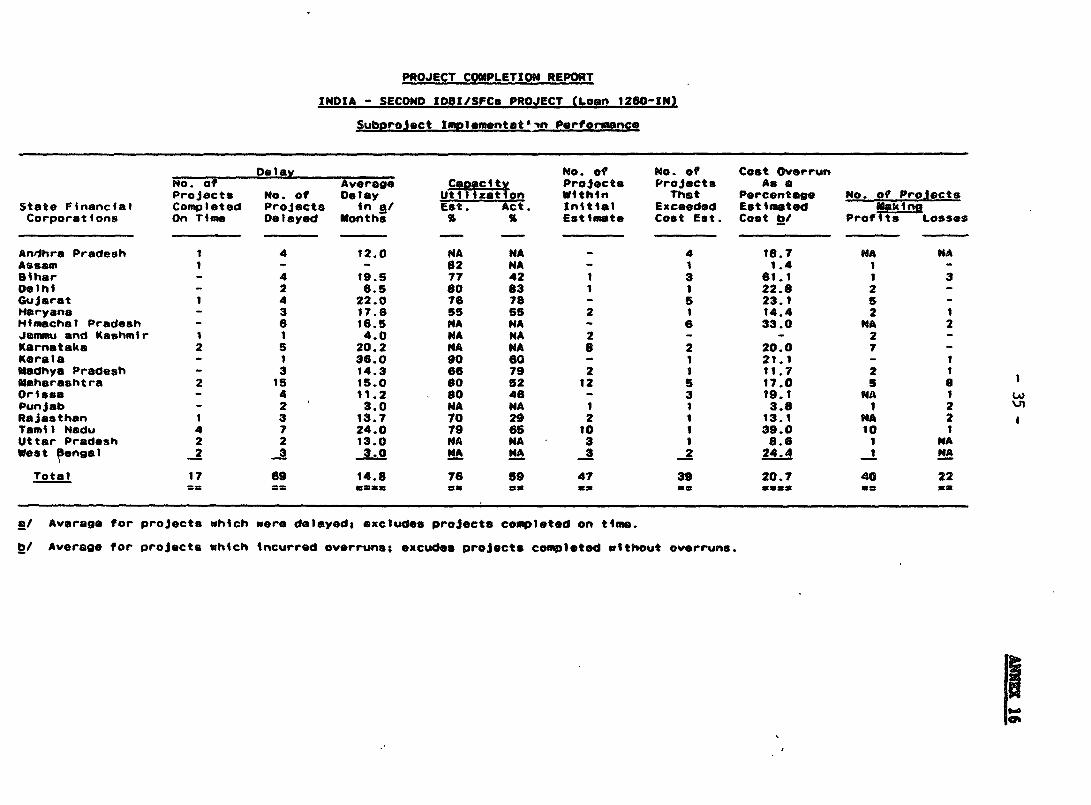

5.06 Project Cost Estimates and Completion. Of the 86 subprojects in thesample (net of cancellations), 47 subprojects, or 55S, were completed withinthe cost estimated in the subproject appraisals. The remaining 39 overranestimates by an average of 212 (Annex 16). Only 17 subprojects in the samplewere completed on time; and the remaining 69 were delayed by 14.8 months onaverage. Causes for delay varied. Most delays were due to late arrival ofimported machinery, delay in acquiring technical know-how, and changes inproject designs. In some cases, arranging adequate bank support for workingcapital caused delays. In other cases, various government clearances throughrelatively cumbersome procedures resulted in a significant delay.

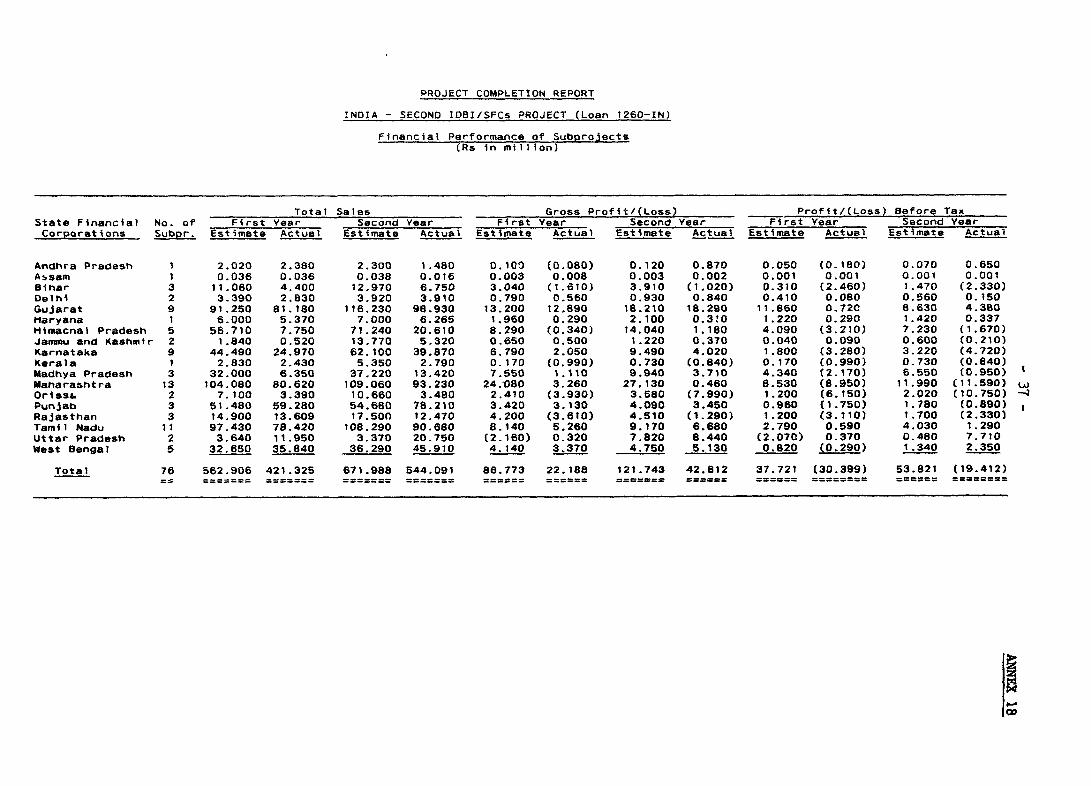

5.07 Financial Performance. The financial parameters indicate that actualperformance of subprojects fell short of the SFCs' appraisal estimates(Annex 18). In the first two years, actual sales, in respect of 76subprojects, were 751 and 81X respectively of expected sales; as against theestimated profits of Rs 37.7 million (year 1) and Rs 53.8 million (year 2),subprojects as a whole recorded large losses Tf Rs 30.4 million and Rs 19.4million, respectively; average capacity utilization was less than 59% andfell short of the estimated target of about 75Z. Among 62 subprojects whichreported their implementation performance, 40 projects (or 65%) made profitswhile 22 firms (or 35%) recorded losses during the second year (Annex 16).The reasons cited by IDBI for this unsatisfactory financial performance were,most of all, the increased costs due to time and cost overruns, infrastruc-tural problems, changes in market conditions, and implementation delays onaverage 15 months which resulted in large cost overruns. These factorsdemonstrate that loan approval was premature in many instances which reflectsSFCs' drive to increase project approvals without simultaneous effort tomaintain or improve appraisal standards. In India, many of the smallindustries are family-operations with a long tradition in the subsector.While they may know production aspects of the business, their managementskills are outdated and decision-making tends to be ad-hoc. Under thecircumstances, SFCs' appraisal capability could have not only contributed to

-16-

their profitability, but also supported small industries generally by provid-ing the required training for management and technology advancements.

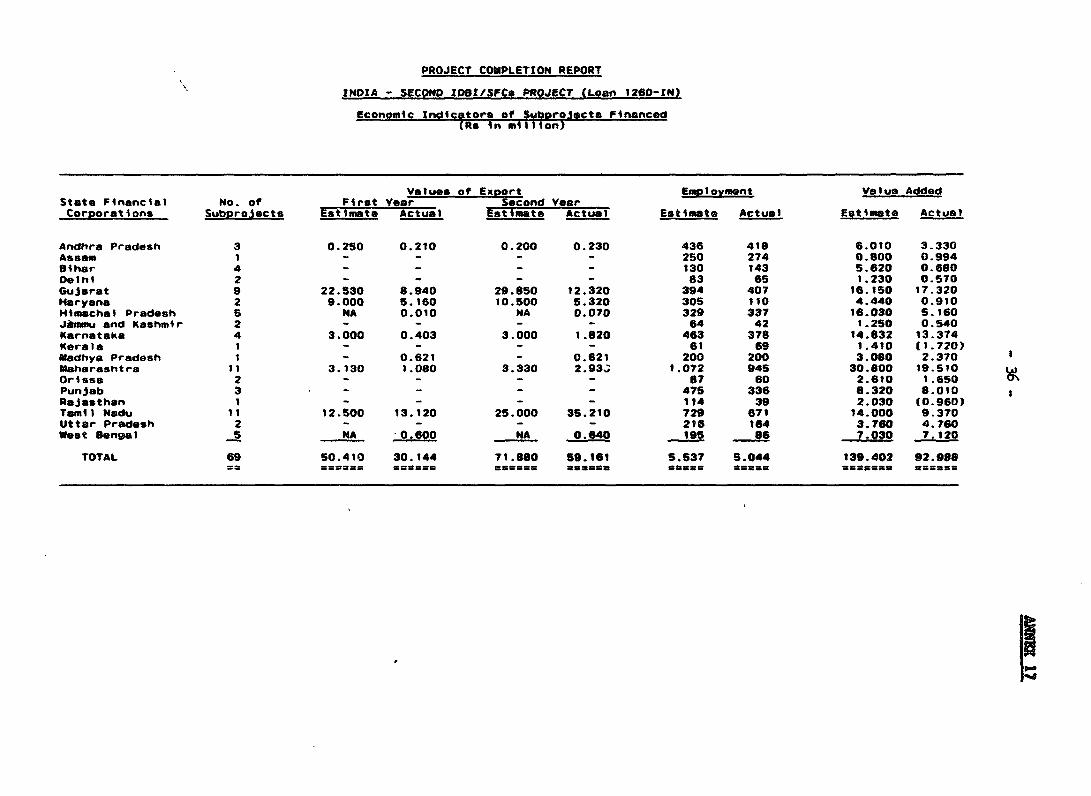

5.08 Economic Performance. Data on economic indicators for 69 subprojects(Annex 17) shows that export earnings increased from Rs 30 million in thefirst year to Rs 59.2 million in the second year, or more than 96% increaseover the previous year. This impressive growth was largely attributable toTamil Nadu SFC projects -- i.e. the actual export earnings exceeded theprojected export value of Rs 25.0 million. These subprojects generated 5,044jobs, and the average investment cost per job 1/ was US$9,795 (Annex 19).The most capital intensive subsectors were chemicals (US$22,156/job), elec-tronics (US$13,294/job), and paper (US$11,428/job). Printing (US$2,099/job)and services (US$2,565) were the most labor intensive. The largestsubsector, light engineering, had an investment cost of US$8,279 per job.Actual value added was about 67% of the estimated figures. Domestic resourcecost (DRC) calculations for 10 selected subprojects (Annex 20) show that 8 ofthese had DRCs less than the prevailing exchange rate, indicating economicefficiency and justification for these subprojects.

5.09 Summary. The overall implementation performance of the subprojectsunder the Bank Loan 1260-IN indicates that many of those incurred financiallosses during the initial two years, largely due to delays in implementationand the resultant cost overruns. The number of subprojects implementedwitbii. initial estiLhates were about 55% of the projects reviewed, an increasefrom 35% under the first Project (Cr. 356-IN); cost overruns as percentage ofestimated costs decreased from 26.2% to 20.7Z; and the number of projectsmaking profits rose to 65% from about 45% while the projects incurring lossesdeclined to around 35% from 55% (Annex 16). IDBI views that a major factorcausing time and cost overruns was the entrepreneurs' unwarranted optimism,as well as failure to perceive factors over which they had little control.Though the data base is limited on the economic performance of thesubprojects, it can be observed that this Project (Loan 1260-IN) provideddirect benefits such as additional investments and employment generation; andin addition, contributed significantly to the diffusion of modern technologyinto a number of small and medium enterprises. Consequently, many of themtoday produce quality goods for domestic and export markets.

VI. CONCLUSIONS AND LESSONS LEARNED

6.01 Loan 1260-IN was the second IDBI/SFCs ?roject for India. Continuingthe objectives of the first Project, Credit 356-IN, the Loan provided foreignexchange resources to the SFCs for their financing of SMI projects; assistedIDBI and 18 SFCs in institutional development and in augmenting operationalefficiency; supported GOI in monitoring the performance of key financialagencies; and allowed the Bank to participate in the development of smallindustries and also to broaden the knowledge regarding state level financialinstitutions.

6.02 During the decade when the two projects were implemented, IDBI andSFCs continuously pursued the project objectives of financing high priority

1/ Investment cost per job excludes land from fixed assets, and includesbuildings, machinery, equipment and permanent working capital.

-17-

SMIs and institutional development of the eighteen SFCs. The PCR (1982) andthe PPAR (1984) for the first Project both concluded that the institutionalupgrading program had not been implement d satisfactorily; collections andfinancial performance of the SFCs had deteriorated, and a serious levrel ofarrears had developed. The PCR further pointed out that many subprojectsincurred delays and cost overruns, which reduced their financial and economicreturns. During the second Project, the implementation of the institutionalupgrading program improved, although much remans to be done. Many SFCs haverestructured their organization and streamlined procedures, while IDBI hasincreasingly assisted the SFCs with various measures to enhance their opera-tional and financial capability. However, considering the long time periodand sizable financial resources involved, what SFCs as a whole hadaccomplished by the completion of this project was far less than the expectedoutcome, i.e. a sound credit delivery system to SMI.

6.03 There remain several outstanding issues. First, the problem ofcollections and arrears has persisted, threatening the financial viabilityand creditworthiness of many SFCs. Only in the most recent year (PY86) haveSFCs implemented incentive measures to reduce arrears and to increasecollections. Their impact has yet to be assessed. Second, close coordina-tion between the SFCs and the commercial banks needs to be encouraged. Theviability of small undertakings depends critically on access to workingcapital. The 1984 PPAR stressed that the timely provision of working capitalto SMI was a pressing issue deserved RBI's full attention, study andintervention. IDBI reported that since FY82, the individual SFCs have workedout some coordination arrangements with other state-level agencies and com-mercial banks: some were successful in getting the commercial banks'favorable response to the demand for timely sanctions of working capital forthe SFCs' subprojects; and in the case of consortium financing, other SFCs(Karnataka, Kerala, West Bengal) have adopted a system of exchangingappraisal memoranda with SIDCs and commercial banks. All SFCs need furtherencouragement to establish a firm link and effective coordination betweenterm lending by SF.Cs and working capital availability from the commercialbanks. However, until the SFCs can achieve collections that indicate soundbanking practice, the commercial banks will be justified in their skepticismtoward SFCs operations. Consideration should be given to linking continua-tion of commercial bank lending to repayment of SFC loans. Third, theimplementation of subprojects was marred by time and cost overruns. Mostdelays and cost escalation were due to late arrivals of imported machinery,delay in acquiring technical know-how, and lack of bank support for workingcapital. These major problems should be overcome mostly by streamliningimport procedures, providing access to new technology, and an effectivecoordination between SFCs, state-level agencies, and commercial banks.

6.04 During the second Project period, IDBI's efforts to help SFCsinstitutional development were much more effective than during the firstProject period, With experience gained and its refinancing capabilitystrengthened, IDBI, as the apex lending institution, has been making progressin monitoring, supervising and advising on the SFCs operations. IDBI hasalso been successful in refining monitoring devices, including annual evalua-tion reports, Business Plans and Resource Forecasts (BPRFs), operationalguidelines and procedures to provide adequate support to the SFCs inimplementing the upgrading programs. But the problem remains with the SFCs'deficient collection performance and mounting arrears. IDBI will have totake a much more assertive stance in resolving this long-standing problem asa shareholder, creditor and overseer of the SFCs.

-18-

6.05 The Bank's involvement, though it attained less than expectedresults, helped identify deficiencies in the SFCs' organizational andinstitutional set-up and operations, led to the development of the realisticupgrading programs, and supported IDBI's efforts to help SFCs introduceinstitutional reforms. The 1984 PPAR recognized that as a result of theproject, an indigenous institutional capacity for term financing wasdeveloping, albeit very slowly, catering to the needs of the SMI.

6.06 The implementation of Credit 356-IN and Loan 1260-IN provides animportant lesson. The experience of lending through an apex agency subjectto a system requiring interaetion with central and state governments by meansof institutional processes outside of its direct control may require somedilution of good banking practice. For example, the record of low collec-tions and mounting arrears suggests that there needs to be a common under-standing among all parties concerned of the objectives of financial institu-tions concerned. The SFCs were clearly unable to sustain internal account-ability for loan quality and IDBI was unable to effectively discipline theseinstitutions, given the political priority accorded to rapid expansion inlending. It wou4d help if IDBI were given some legal instruments to enforcefinancial discipline on the SFCs. Firm commitments by financial inter-mediaries and consistent support by state governments to institutionaldevelopment is extremely important, if financial and institutional objectivesare to be achieved. In particular, stability and quality of top managementneeds to be retained for the effectiveness of leadership and organizations.Moreover, commitment to the longer term financial viability must rank inimportance with lending targets, and all concerned agencies must encouragethe SFCs to make the firm decisions which will be necessary to improve col-lection performance. IDBI's continued support to SPCs should be linked tocollection performance as measured by specific targets (Attachment, page 4).

April 1987Revised: June 1987

PROJECT COMPLETION REPORT

INDIA - SECOND IDBI/SFCa FROJECT (Loan 1260-1N)

SFC's Sanctin- and DisburemEnts. FYSI-s6

State Financial 1980-St _' 1961-82 _t1962-3 1963-84 1_ _984-8r 1965-1Corporations Sanc. D1ub. SoWC. Dlib. Sanc. D1ib. Sonc. Diab. sinc. ab. Sanc. C1sb.

Andhra Pradesh 466.8 296.1 615.9 371.6 699.9 449.6 738.9 478.6 907.4 593.7 1.063.9 665.1A8ssa 9.1 6.5 40.7 20.4 36.1 37.4 26.0 18.0 28.6 18.6 30.9 22.2Dihar 184.0 92.2 369.1 145.1 426.4 17t.4 336.7 157.5 496.4 209.2 634.6 321.3Delhi 50.1 3S.6 S8.6 40.9 77.7 47.6 63.0 51.8 79.8 60.9 149.4 70.?Gujarat 365.9 275.1 471.5 330.S 645.3 421.0 581.9 383.2 655.4 412.5 746.7 454.9Haryana 105.S 51.2 166.6 92.7 312.3 168.0 170.9 135.9 127.7 158.3 240.8 147.7Himachal Prades 103.5 34.6 107.6 65.7 73.1 61.7 93.6 60.9 165.3 85.6 199.1 12S.5Jaemu and Kashmir 73.3 50.2 93.4 62.1 119.4 96.0 122.3 88.8 160.0 128.7 182.6 130.5Karnataka 210.S 144.1 321.? 216.4 437.6 314.4 582.7 434.6 763.2 846.3 1.035.7 662.9Kerala 99.5 84.2 40.2 61.0 122.1 83.1 82.1 6S.7 103.8 120.0 356.2 195t.Madhya Pradesh 111.6 66.1 162.9 _ a3.5 239.4 140.6 332.9 210.8 419.3 271.6 664.5 3S3.3Maharashtra 347.7 301.7 345.1 308.7 497.1 321.5 566.6 410.2 578.2 355.6 704.6 431.0Orissa 293.7 176.3 425.0 286.8 547.1 320.7 532.4 317.3 531.0 341.9 499.1 3SS.3Punjab 93.3 80.1 109.1 87.S 280.0 136.4 224.3 1S5.7 29.6 106.6 313.9 112.1RaJasthan 373.9 261.0 4S1.4 299.6 "55.2 375.2 S31.7 388.0 526.3 393.0 641.1 359.7 7Test) Hadu 362.3 222.S 519.9 345.2 S55.3 395.6 S95.5 411.1 675.5 493.1 923.0 600.0 "0Uttaer Pradesh 413.0 249.9 557.8 310.2 544.0 360.5 624.5 458.9 924.8 542.8 1.562.2 780.3West Bengal 114.2 54.4 153. 62.7 _ 192.0 tOO. 249.1 119.8 27f.9 157.1 331.S 187.

TotalGrosg 3.777.9 2.481.8 5,010.5 3,16S.6 6,363.3 4,043.9 6,449.1 4.354.8 7,387.8 4.905.5 10.280.2 S.995.1Sanctions and ====- inuuau i-Du--- uumu. u2um mgmumu Cuin uaminua unmSmu Pm uuinuUDisbursements

Net Sanctions 3,651.9 4,868.8 5,498.5 6,118.1 6.25143 9.070.S

Source: tOOt

-20 - ANNEX 2

PIOJECT COMPLETION REPORT

INDIA - SECOND IDBI/SFCs PROJECT (Loan 1260-IN)

Sumary of SFC's Operations(FY82-86)

FY82 PY83 FY84 FY85 FY86 FY82-86

Total Sanctions 4,868.8 5,498.5 6t118.1 6,251.3 9,070.5 31,807.2(Net Disbusements) (3,156.6) (4,043.9) (4,354.8) (4,985.5) (5,995.1) (22,535.9)

Percentage ofTotal Sanctions:

Backward Areas 46 47 50 55 54 51SSI (Net of S8TO) /a 74 77 75 77 76 76Nev Projects 91 90 91 92 90 91Private Sector 98 97 98 97 97 98IndustriesFood 11 11 13 11 11 11Textiles 7 7 8 8 9 8Chemicals 11 13 13 15 15 14Metal Products 10 11 9 9 8 9Kachinery 7 5 4 4 4 5Services 12 14 15 13 13 13Other /b 42 39 38 40 40 40

Number of Units(000) Average perUnit (Net Sanctions) 32 33 31 31 29 156

Rs. '000 152.15 166.62 197.36 201.66 312.78 204USDollars '000 17.74 19.42 23.01 23.52 36.47 23.79(Rs.8.5755) /c

/a SSI - Small-Scale Industries.SRTO - Small Road Transport Operators

/b Include Paper, Rubber, Cement, Basic Metals, Electrical Machinery,Transport Equipment and Others.

/c Average rate during the project implementation period.

Note: Some percentages are approximate figures due to non-availabilityof detailed breakdown for some SFCs.

Source: IDBI

PROJECT COMPLETION REPORT

INDIA - SECOND I08I/SFCs PROJECT (Loan 1260-IN)

SFC's Net Sanctions and Disbursements Distribution by Subsector(Rs millions)

Net Sanctions DisbursementsCumulative % of Cumulative % of

Up to Cumulative Up to CumulativeIndustries FYSS FY86 and Fr86 Assistance FY85 FY86 and FY66 Assistance

Food 696.7 982.3 8.099.8 11.9 609.4 602.4 4.243.8 12.5

Textiles 496.3 748.1 4.494.8 8.7 383.4 320.4 3.095.0 9.1

Paper 174.0 347.2 2,004.0 3.9 132.5 1S2.3 1,405.3 4.2

Chemicals (mdcl. Fertilizers) 962.7 1,415.1 6,822.4 13.3 639.7 570.5 4,321.3 12.0

Rubber 103.7 170.1 941.2 1.8 94.0 S.0 578.2 1.7

Cement 138.4 17.1 104.3 0.2 75.9 4.6 382.7 1.1

Basic Metal Industries 175.5 308.6 2,223.4 4.3 196.0 163.7 1.523.2 4.5

Metal Products 541.5 780.1 4,658.5 9.1 383.7 356.6 2,875.9 8.5 £

Machinery 236.1 370.8 2,105.2 4.1 242.4 119.4 1.579.1 4.7

Electrical Machinery 257.0 301.7 2,022.1 3.9 189.8 172.4 1,389.9 4.1

Transport Equipment 93.9 103.9 943.2 1.8 77.5 51.1 678.9 2.0

Electrical Generation 22.1 36.5 337.0 0.7 9.1 14.0 125.9 0.4

Services 834.2 1.185.1 6.691.8 13.0 681.8 554.4 4,208.4 12.4

Others 1,519.9 2,303.9 11.955.7 23.3 1.270.3 980.9 7.435.5 22.0

Total 6,251.3 9,070.5 51,404.2 100.0 4,985.5 4,118.6 33,844.2 100.0

Ii

PROJECT COMPLETION REPORT

INDIA - SECOND 1081/SFCO PROJECT (Loan 1260-tH)

Assistance toisburamonts) to Small Induistries. FYSI-8B(Res millions)

FY81State Financial Amount to % of Total FY82 FY6 F84 F8Corporations SSI*s Assistance Amoun~t I Amon3t Amount __ A=nt %AvVount U