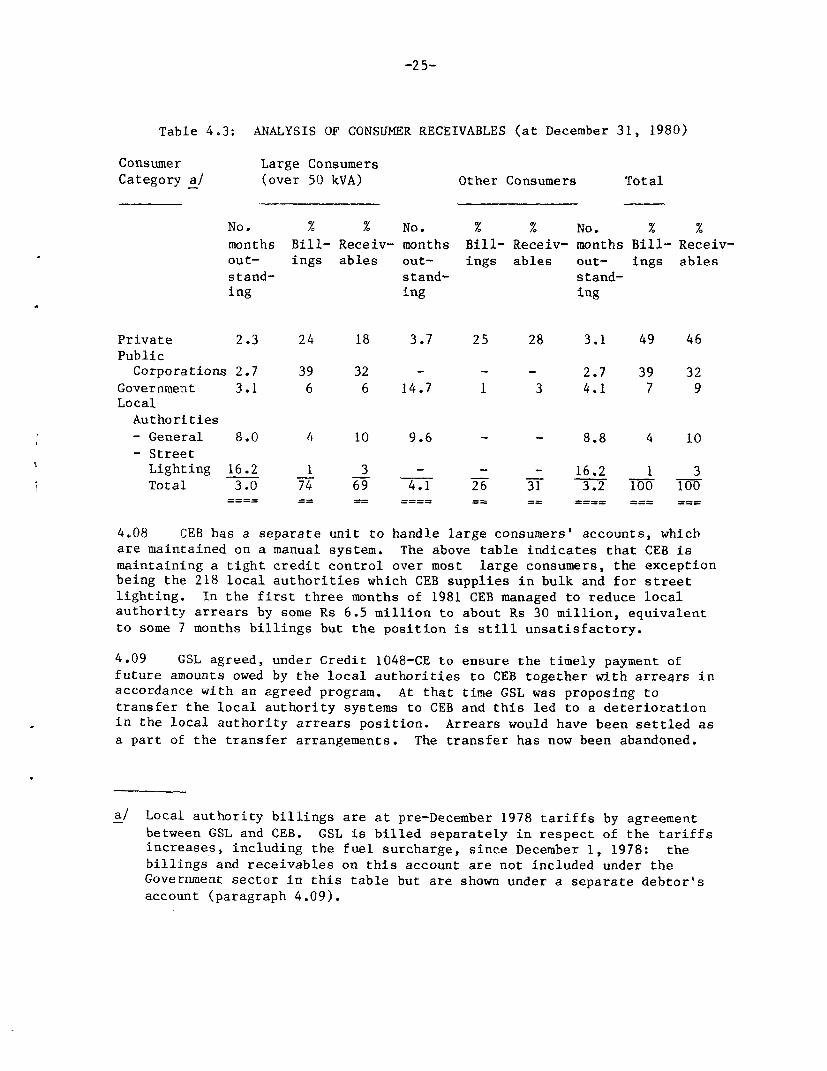

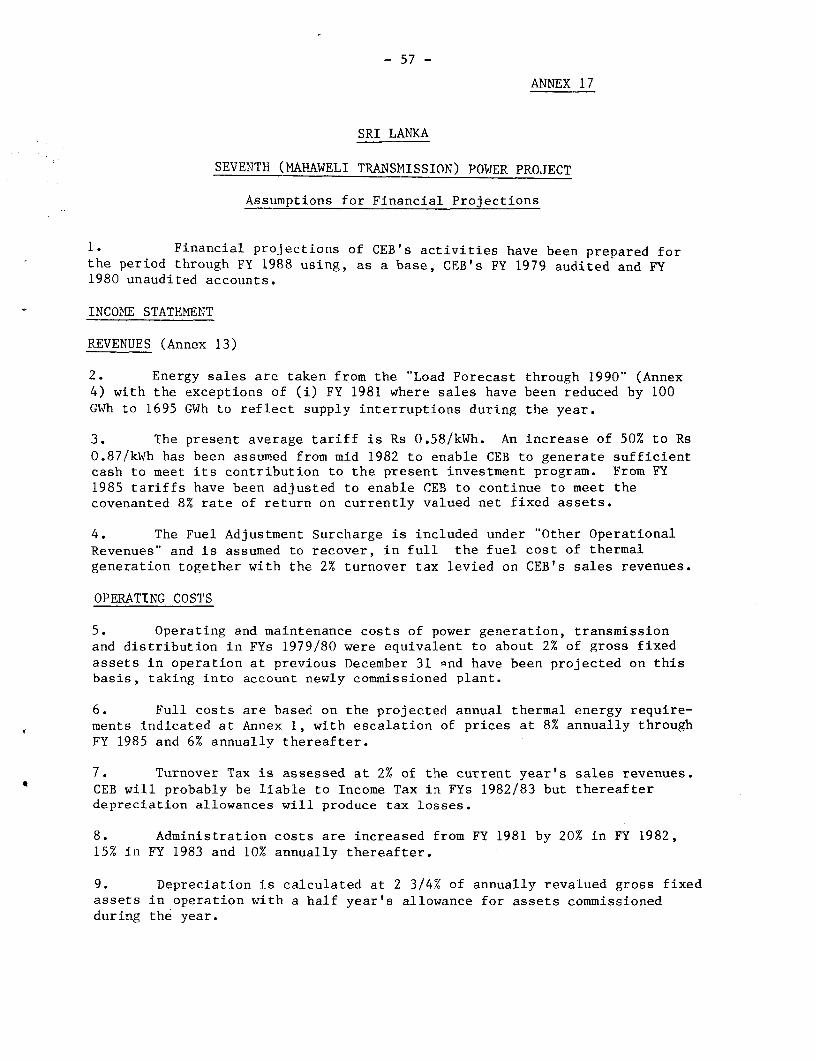

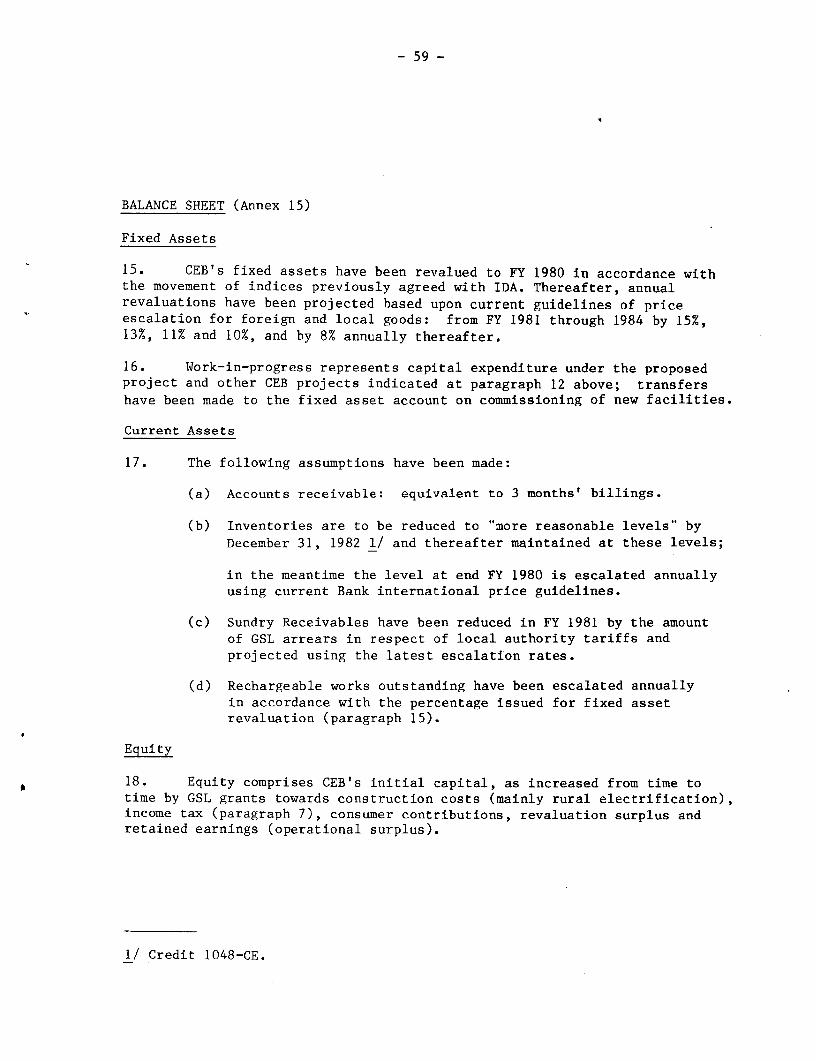

Embed Size (px)

Citation preview

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No. 3599b-CE

STAFF APPRAISAL REPORT

SRI LANKA

SEVENTH (MAHAWELI TRANSMISSION) POWER PROJECT

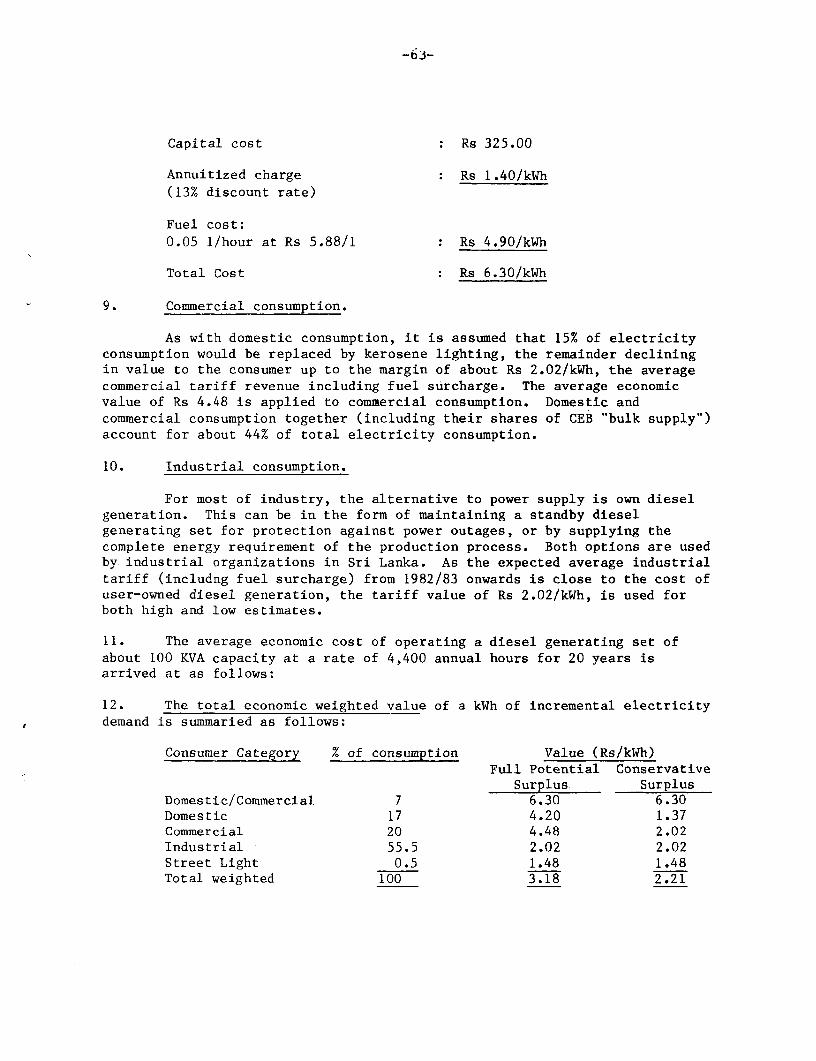

January 21, 1982

Regional Projects DepartmentSouth Asia Projects

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

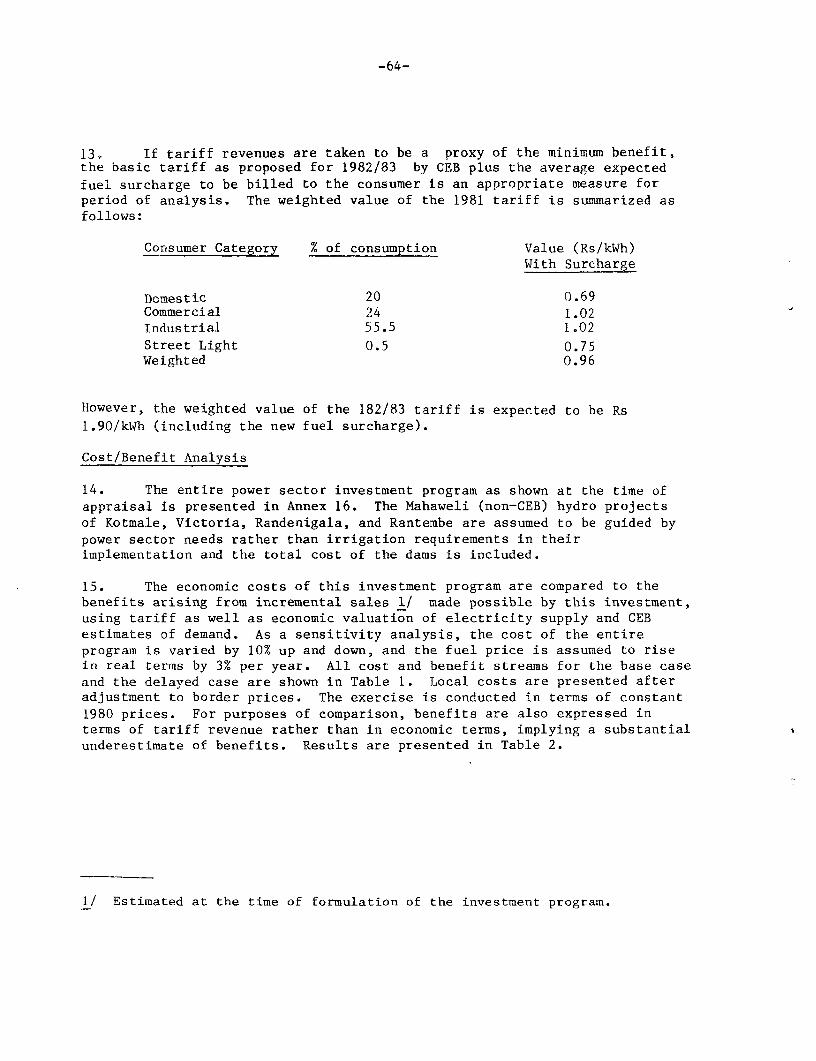

lic D

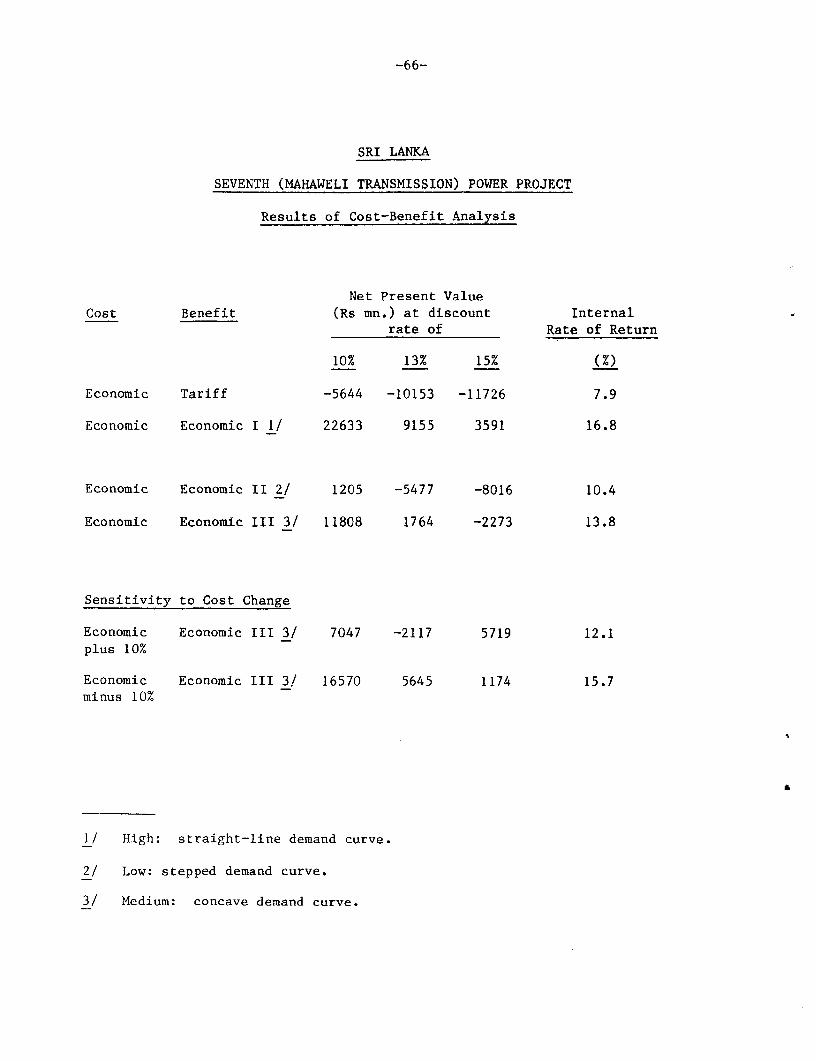

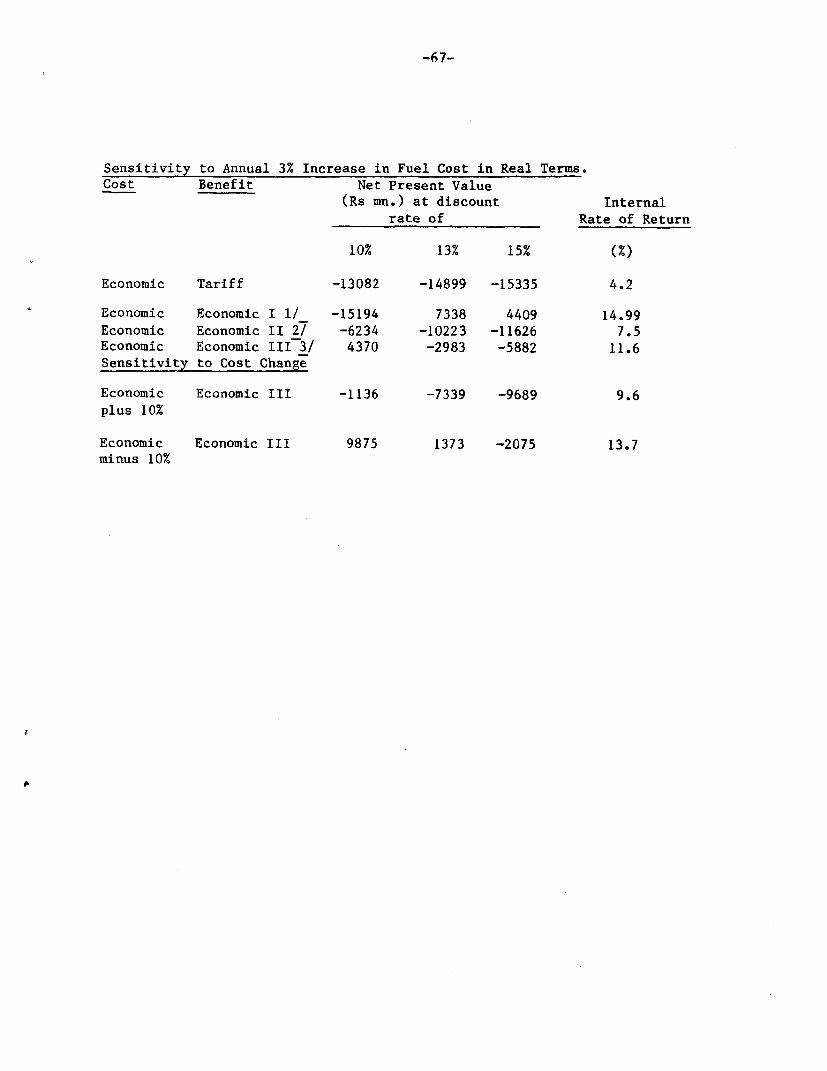

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

SRI LANKA

SEVENTH (MAHAWELI TRANSMISSION) POWER PROJECT

CURRENCY EQIJIVALENTS

US$1.00 = SL Rs 18.5SL Rs 1.00 = US$0.054

MEASURES AND EQUIVALENT

1 kilometer (km) = 0.6214 mile1 kilovolt (kV) = 1,000 volts1 megavolt ampere (MVA) = 1 million volt amperes

= 1,000 kilovolt amperes1 megawatt (MW) = 1 million watts

1,000 kilowatts1 kilowatt hour (kWh) = 1,000 watt hours1 gigawatt hour (GWh) = 1 million kilowatt hours

ABBREVIATIONS AND ACRONYMS

ADB - Asian Development BankCEB - Ceylon Electricity BoardCPC - Ceylon Petroleum CorporationDGEU - Department of Government Electrical UndertakingsGSL - Government of Sri LankaGTZ - German Agency for Technical CooperationLRMC - Long-Run Marginal CostMPE - Ministry of Power and EnergyMASL - Mahaweli Authority of Sri LankaPPAR - Project Performance Audit ReportUSAID - United States Agency for International Development.

FISCAL YEAR

January 1 - December 31

FOR OFFICIAL USE ONLY

SRI LANKA

SEVENTH (MAHAWELI TRANSMISSION) POWER PROJECT

STAFF APPRAISAL REPORT

Table of Contents

Page No.

1. THE ENERGY AND POWER SECTOR .................................

A. Energy Resources ........................................

Hydro Power .................... 0......................Traditional Fuels ....................................Petroleum ............................................

B. The Power Subsector ..................... ...............Sector Organization ............ .. ....................External Assistance . ................ ..... ...........Existing Facilities ..................................Development Program ..................................Access to Service and Status of Supply ...............Plant Maintenance ....................................Rural Electrification ........................ . .......System Losses ........................................Historical Consumption ...............................Load Forecast ........................................

fl. THE IMPLEMENTING AGENCY ........................... ..-...

Lending Arrangements ......................................Organization ...... ........ ..................Management and Staffing ..................................Management Systems .......................................Training ................... 0...............................Local Authority Distribution Systems .....................Audit .....................................................

Insurance ..............................................

This report is based on the findings of an IDA mission comprising B.C. Davis

and J.C. Ryan who visited Colombo in May/June 1981.

This document has a restricted distribution and may be used by recipients only in the performance oftheir offial duties. Its contents may not otherwise be disclosed without World Bank authorization.

-2-

Table of Contents (Cont'd)

Page No.

III. THE PROJECT .

Objectives .............................................Description ...............................................Project Cost ..............................................Project Financing Plan ....................................Engineering and Implementation ............................Procurement ...............................................Disbursements .............................................Land Acquisition ..........................................Risks .....................................................

IV. FINANCIAL ANALYSIS .........................................

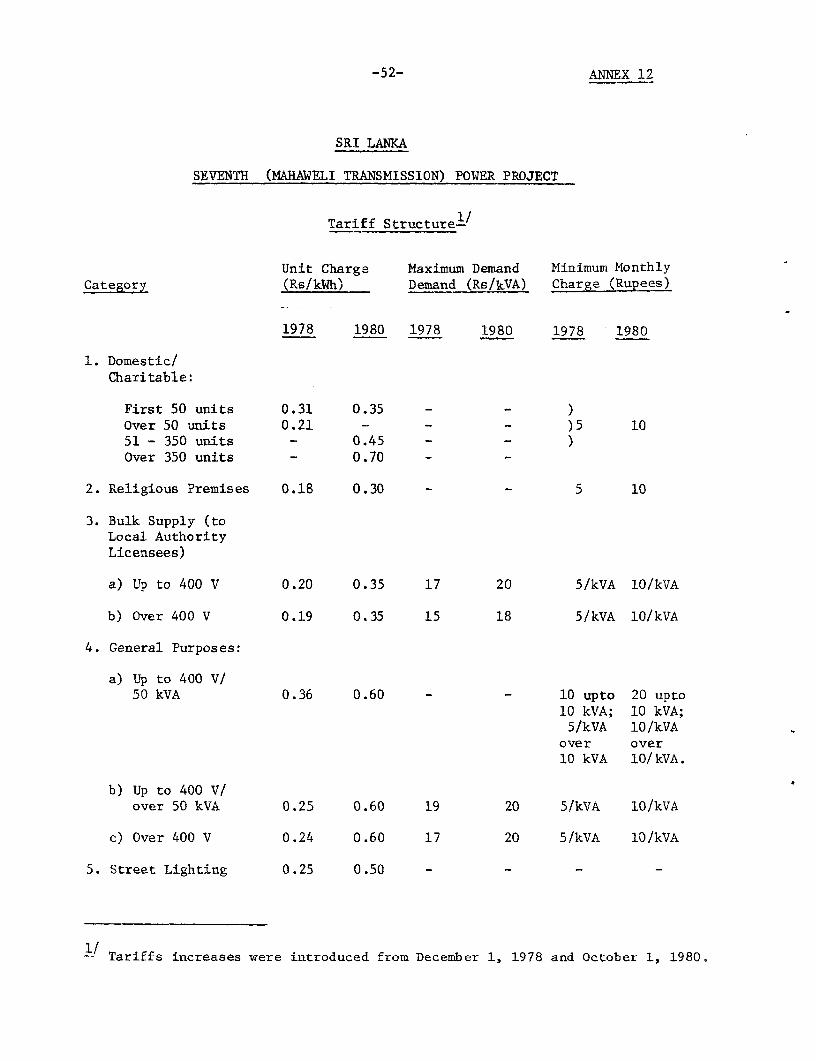

CEB's Statutory Position ...................................Past Financial Performance .................................Present Financial Position .................................Billing and Collection .....................................Revenues and Tariffs .......................................Transfer of Assets from the MASL ...........................Financing Plan (FYs 1981-85) ...............................Future Finances ............................................

V. JUSTIFICATION ..............................................

Approach ...................................................Economic Costs and Benefits ................................Results ....................................................

VI. AGREEMENTS REACHED AND RECOMMENDATION .....................

-3-

Tables of Contents (Cont-d)

Page No.

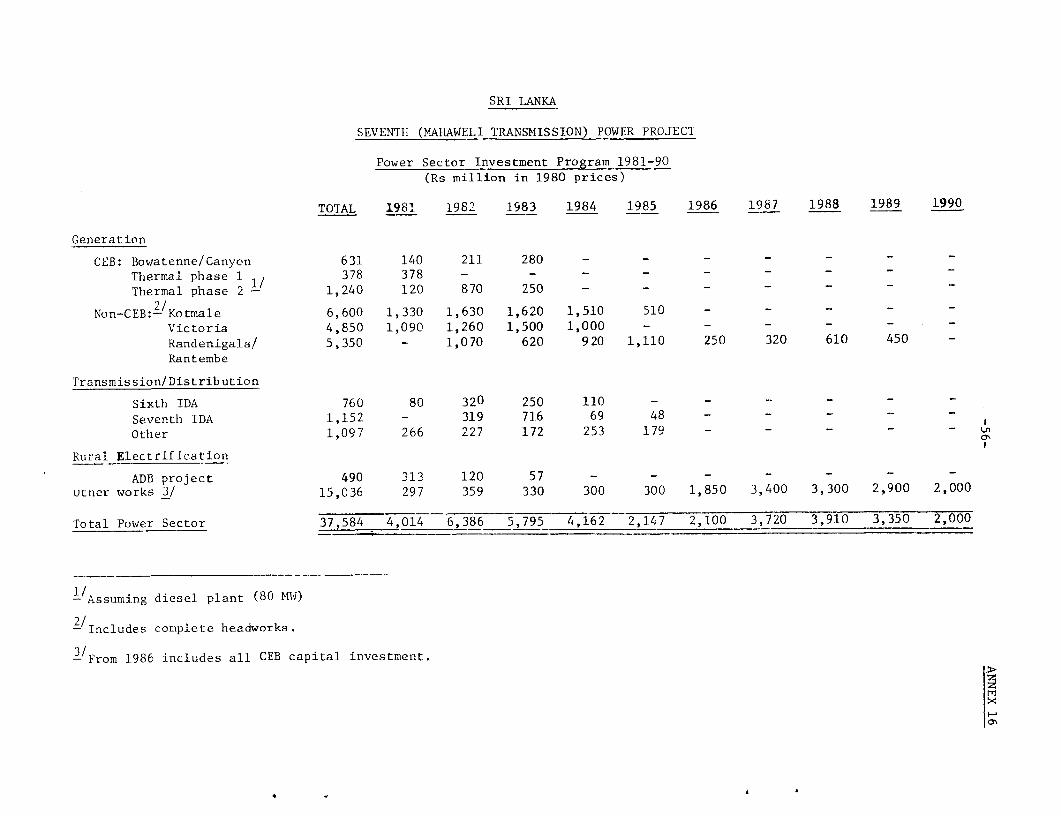

ANNEXES

1. Power and Energy Balances (through 1990).2. Generating Facilities.3. Existing Transmission and Distribution Systems.4. Load Forecast (through 1990) .5. Organization Chart.6. Reporting Requirements.7. Project Description.8. Project Cost Estimate .9. Construction Schedule ................................10. Schedule of Estimated Disbursements .....................11. Income Statement (FY1976 through FY1980) ................12. Tariff Structure ................................ .13. Income Statement (FY1979 through FY1988) ................14. Flow of Funds Statement (FY1979 through FY1988) .........15. Balance Sheets (FY1979 through FY1988) ..................16. Power Sector Investment Program (FY1981 through FY1990) .17. Assumptions for Financial Projections ...................18. Economic Analysis ................................

19. Related Documents and Information in the Project File ...

MAP

TBRD 16016R Seventh (Mahaweli Transmission) Power Project

A

I~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

I

SRI LANKA

STAFF APPRAISAL REPORT

SEVENTH (MAHAWELI TRANSMISSION) POWER PROJECT

I. THE ENERGY AND POWER SECTOR

A. Energy Resources

1.01 Sri Lanka in 1981 had a population of 14.9 million and a grossnational product of $250 per capita. Energy consumed in 1980 amounted toabout 3.7 million toel/, of which 60% was provided by fuelwood, 13% byhydropower and 27% by imported oil. The country has no known reserves ofcoal, oil or natural gas, and its small deposits of peat are not significant.An Energy Assessment mission from the Bank visited Sri Lanka in June 1981 andits report will be published shortly.

Hydro Power

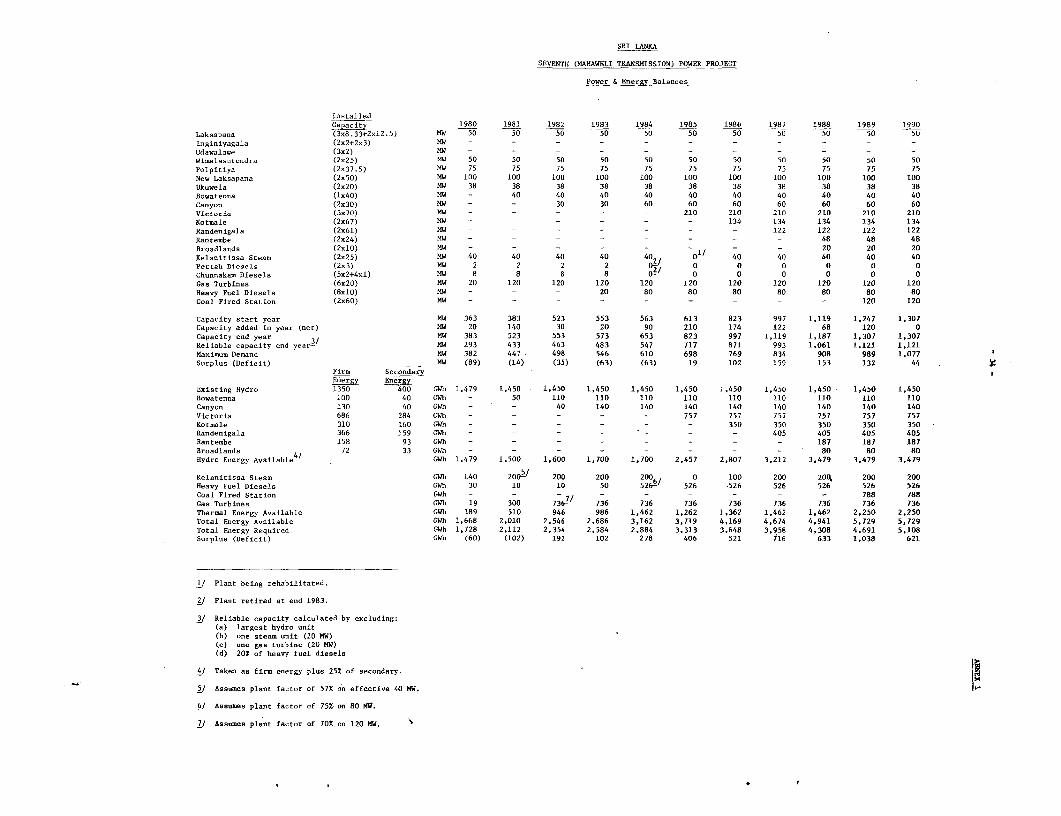

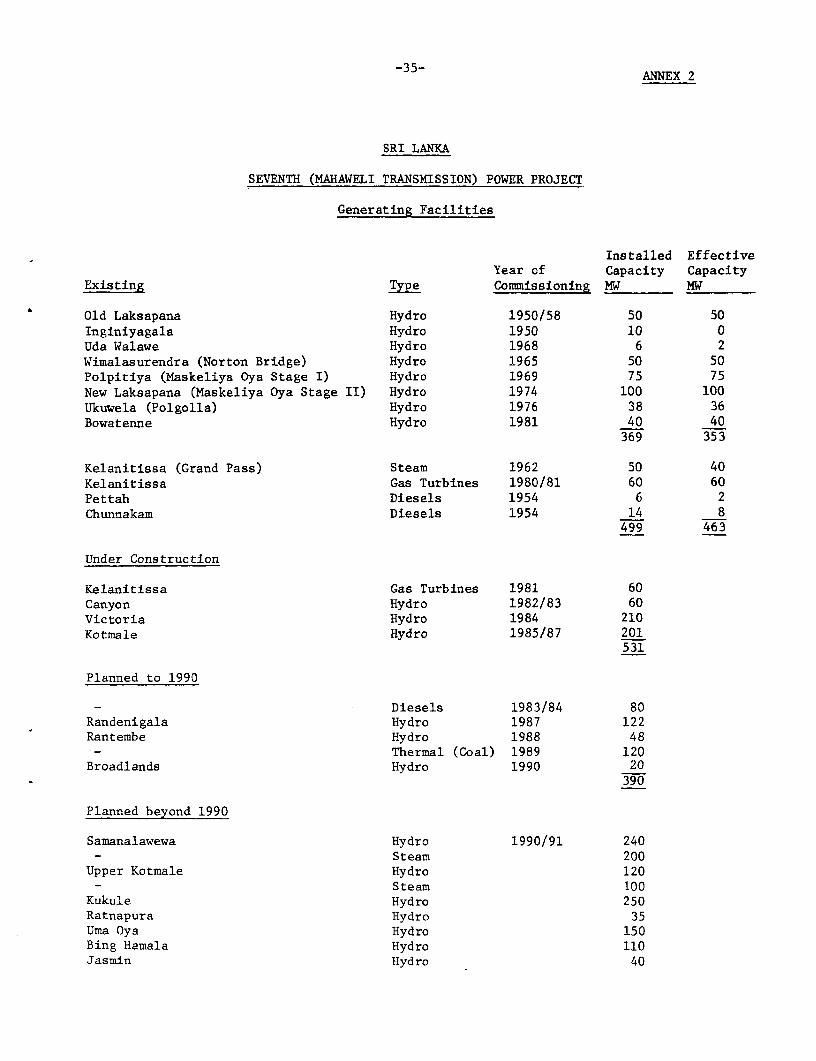

1.03 Sri Lanka has an area of 25,332 square miles. Most of itsprecipitation comes from the Southwest monsoon from about May to Septemberand from the Northeast monsoon from about December to March. Annual averagerainfall varies from less than 40 inches in some northern parts of the islandto more than 200 inches in places on the southwest slopes of the hills.Tlydro power potential totals about 6,600 GWh (1.7 million toe2/) per annum,or 2,500 MW at 30% load factor, mainly in three basins centered on thecentral highlands. They are the Mahaweli Basin in central Sri Lanka, theWalawe Basin to the south, and the Kehelgamu-Maskeliya Basin to thesouthwest. Some hydro power has already been developed in each of thesebasins.

1.04 Installed hydro generating capacity totals 369 MW out of a totalinstalled capacity of 499 MW. Six more hydro stations are planned to bringthe total hydro installed to about 1,100 MW by 1990. The present yield offirm energy is about 1,500 GWh per year; projected additions will increasethis to about 3,240 GWh by 1990 (Annexes 1 and 2).

Traditional Fuels

* 1.05 Wood is the most widely used fuel. From such statistics as areavailable it appears that annual consumption of wood from the forests isbetween 3.8 and 5.4 million tons per year (1.5 - 2.2 million toe). To this

1/ toe = tonne oil equivalent = 10.2 x 106 kcal

2/ Primary equivalent based on 0.25 kgoe/kWh = 10,500 BTU/kWh= 2,646 kcal/kWh

-2-

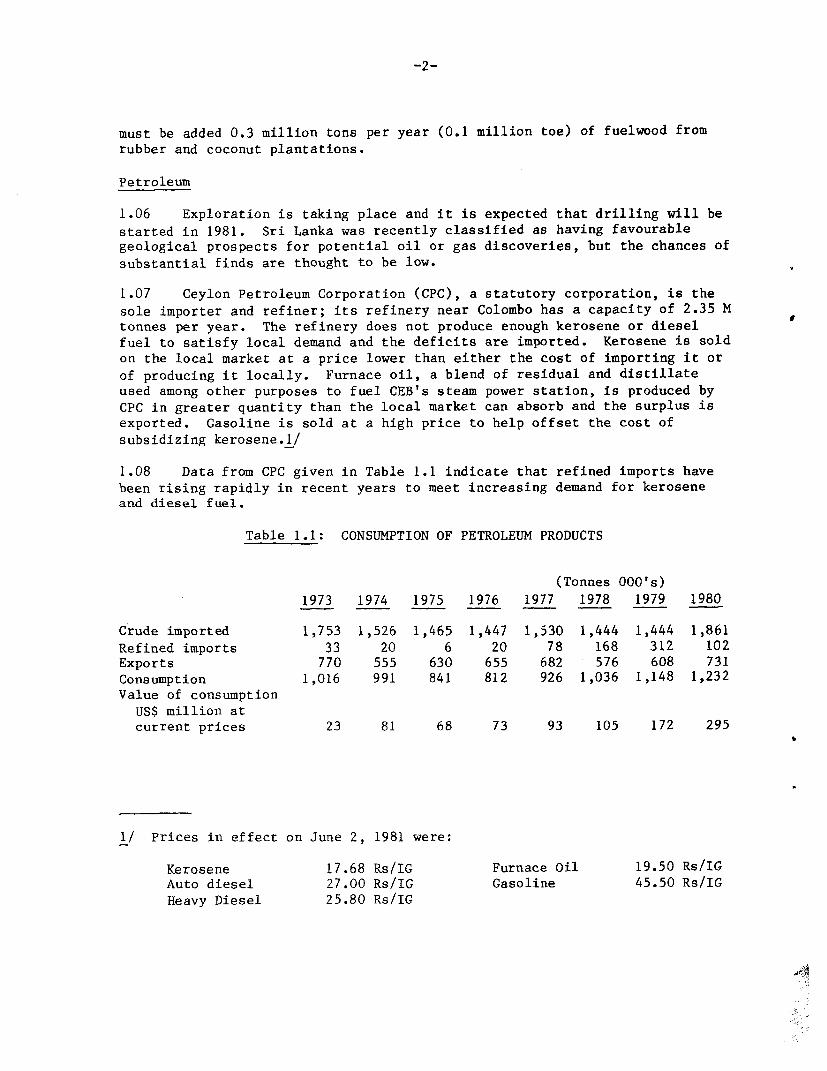

must be added 0.3 million tons per year (0.1 million toe) of fuelwood fromrubber and coconut plantations.

Petroleum

1.06 Exploration is taking place and it is expected that drilling will bestarted in 1981. Sri Lanka was recently classified as having favourablegeological prospects for potential oil or gas discoveries, but the chances ofsubstantial finds are thought to be low.

1.07 Ceylon Petroleum Corporation (CPC), a statutory corporation, is thesole importer and refiner; its refinery near Colombo has a capacity of 2.35 Mtonnes per year. The refinery does not produce enough kerosene or dieselfuel to satisfy local demand and the deficits are imported. Kerosene is soldon the local market at a price lower than either the cost of importing it orof producing it locally. Furnace oil, a blend of residual and distillateused among other purposes to fuel CEB's steam power station, is produced byCPC in greater quantity than the local market can absorb and the surplus isexported. Gasoline is sold at a high price to help offset the cost ofsubsidizing kerosene.l/

1.08 Data from CPC given in Table 1.1 indicate that refined imports havebeen rising rapidly in recent years to meet increasing demand for keroseneand diesel fuel.

Table 1.1: CONSUMPTION OF PETROLEUM PRODUCTS

(Tonnes 000's)1973 1974 1975 1976 1977 1978 1979 1980

Crude imported 1,753 1,526 1,465 1,447 1,530 1,444 1,444 1,861Refined imports 33 20 6 20 78 168 312 102Exports 770 555 630 655 682 576 608 731Consumption 1,016 991 841 812 926 1,036 1,148 1,232Value of consumption

US$ million atcurrent prices 23 81 68 73 93 105 172 295

1/ Prices in effect on June 2, 1981 were:

Kerosene 17.68 Rs/IG Furnace Oil 19.50 Rs/IGAuto diesel 27.00 Rs/IG Gasoline 45.50 Rs/IGHeavy Diesel 25.80 Rs/IG

-3-

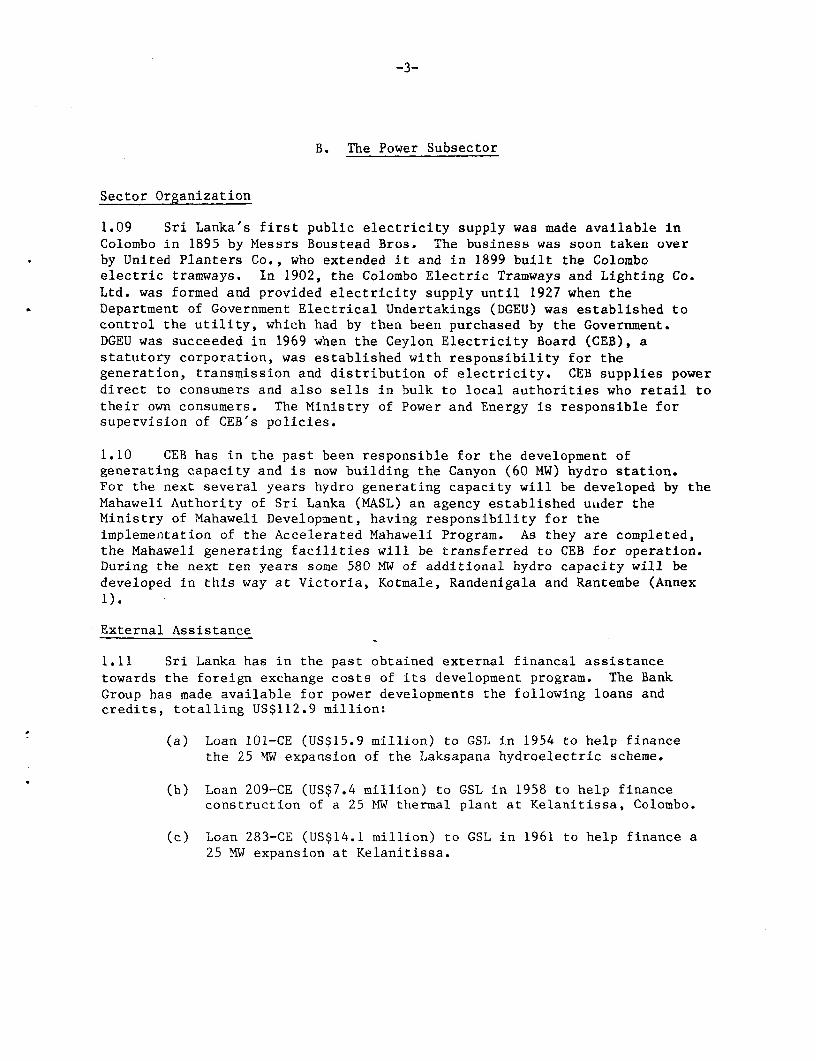

B. The Power Subsector

Sector Organization

1.09 Sri Lanka's first public electricity supply was made available inColombo in 1895 by Messrs Boustead Bros. The business was soon taken overby United Planters Co., who extended it and in 1899 built the Colomboelectric tramways. In 1902, the Colombo Electric Tramways and Lighting Co.Ltd. was formed and provided electricity supply until 1927 when theDepartment of Government Electrical Undertakings (DGEU) was established tocontrol the utility, which had by then been purchased by the Government.DGEU was succeeded in 1969 when the Ceylon Electricity Board (CEB), astatutory corporation, was established with responsibility for thegeneration, transmission and distribution of electricity. CEB supplies powerdirect to consumers and also sells in bulk to local authorities who retail totheir own consumers. The Ministry of Power and Energy is responsible forsupervision of CEB's policies.

1.10 CEB has in the past been responsible for the development ofgenerating capacity and is now building the Canyon (60 MW) hydro station.For the next several years hydro generating capacity will be developed by theMahaweli Authority of Sri Lanka (MASL) an agency established uiider theMinistry of Mahaweli Development, having responsibility for theimplementation of the Accelerated Mahaweli Program. As they are completed,the Mahaweli generating facilities will be transferred to CEB for operation.During the next ten years some 580 MW of additional hydro capacity will bedeveloped in this way at Victoria, Kotmale, Randenigala and Rantembe (Annex1).

External Assistance

1.11 Sri Lanka has in the past obtained external financal assistancetowards the foreign exchange costs of its development program. The BankGroup has made available for power developments the following loans andcredits, totalling US$112.9 million:

(a) Loan 101-CE (US$15.9 million) to GSL in 1954 to help financethe 25 MW expansion of the Laksapana hydroelectric scheme.

(b) Loan 209-CE (US$7.4 million) to GSL in 1958 to help financeconstruction of a 25 MW thermal plant at Kelanitissa, Colombo.

(c) Loan 283-CE (US$14.1 million) to GSL in 1961 to help finance a25 MW expansion at Kelanitissa.

-4-

(d) Loan 636-CE (US$21.0 million) to CEBI/ in 1969 to help finance

the 90 MW Maskeliya Oya Stage II project, a 25 MW gas turbine,and management consultancy and engineering services. US$4.5million of this loan was cancelled when the gas turbine was notpurchased.

(e) Credit 372-CE (US$ 6.0 million) to GSL in 1973 for reinforcementand extension of CEB's transmission and distribution systems.

(f) Credit 1048-CE (US$ 19.5 million) to GSL in 1980 for the SixthPower Project to provide further reinforcement and improvementof CEB's transmission and distribution systems.

(g) Further, the Bank Group made available Loan 653-CE/Credit 174-CE(US$29.0 million) to GSL in 1969 for the multi-purpose(irrigation and power) Mahaweli Ganga Development of which the38 MW Ukuwela power station formed a part.

1.12 Six projects have been completed satisfactorily while that underCredit 1048-CE is at an early stage. Project Performance Audit Reports(PPAR) have recently been prepared for three of the above projects. That forLoan 653-CE/Credit 174-CE, which was for both irrigation and electricity,concluded that although implementation was seriously delayed, theagricultural and power benefits turned out to be much greater than expectedat appraisal; the benefit of power generated was much increased by the risein petroleum prices in 1973 and afterwards. The PPAR report on Loan 636-CE,for the 90 MW New Laksapana hydro station, concluded that the project hadbeen well conceived and constructed; it was built at low cost, and its timingwas fortunate in that it was almost complete at the time of the 1973 oilcrisis. A significant institutional advance under Loan 636-CE was theestablishment of CEB as a public corporation, replacing the Department ofGovernment Electrical Undertakings. Despite a promising start, CEB has notdeveloped as well as expected and both the Sixth (Credit 1048) and theproposed projects are seeking to promote significant advances in CEB'smanagement. The PPAR report dealing with Credit 372-CE concluded that theproject met its major objectives; the extensions to the transmission anddistribution system built under it, though completed late, enabled full useto be made of the Ukuwela and New Laksapana hydro stations.

1.13 The Sixth Power Project is about a year behind schedule.Effectiveness of Credit 1048-CE was postponed about 6 months because of adelay in arranging cofinancing, and further delays arose owing to thecomplexities of making procurement decisions, and because of changes of

1/ CEB was established in June 1969.

-5-

senior staff in CEB. At negotiations IDA was assured that CEB would adoptquicker procurement procedures and such delays would be avoided in future.

1.14 CEB's management shortcomings were noted in the appraisal of theSixth Power Project and in the PPAR report on the Fifth Power Project. Areview of CEB's managerial performance and methods, financed under Credit1048-CE, has been carried out by consultants, and action is being taken torestore management systems, provide support to senior management, andimplement comprehensive training programs for all types of staff (paras2.09-2.11).

1.15 The Asian Development Bank (ADB) has provided finance forconstruction of the Bowatenne and Canyon hydro stations and for ruralelectrification. GSL has arranged bilateral financing of hydro generationcomponents of the Mahaweli program as follows: - Sweden (Kotmale), U.K.(Victoria) and the Federal Republic of Germany (Randenigala). Theconstruction of hydro generating facilities at Samanalawewa has beenpostponed until the early 1990's.

Existing Facilities

1.16 CEB's existing generating, transmission and distribution facilitiesare described in Annexes 2 and 3. CEB's present installed capacity is 499MW, all interconnected on one system. In addition there are privately ownedgenerating stations, most of them less than 500 kW but ranging as large as5.75 MW in CPC's refinery at Sapugaskande and 6 MW at the urea factory. Thetransmission and distribution system comprises 569 miles of 132 kV line with17 substations, 214 miles of 66 kV lines with 9 substations, about 3,250miles of 33 kV, and about 750 miles of 11 kV lines. The system control andload dispatching centre is at Kolonnawa, and all important plants andswitching centers can communicate by means of power line carrier.

Development Program

1.17 Of recent years detailed planning has not usually extended more thanfour or five years ahead, but in mid 1981 CEB prepared a detailed developmentplan to meet its generation requirements over the next 15 years. The planhas not yet been officially adopted by GSL. The proposed hydro program showsadditions to the end of this decade bringing the installed capacity to about950 MW with a firm energy capacity of 3,170 GWh. In the first four years ofthe next decade, additions to hydro capacity of 1,000 MW and 2,000 GWh areproposed. To complement the hydro, some hundreds of megawatts of thermalplant will be needed between 1985 and 1994.

1.18 At negotiations, it was agreed that the following steps would betaken to put CEB's planning on a workable footing. The new General Managershould make planning a matter of high priority for his personal attention.A corporate planning department should be formed to plan generation and

-6-

transmission and their associated capital expenditures. The same groupshould play a leading role in the preparation of one year and five yearoperational budgets and capital budgets. The group will be required toproduce, by the end of 1982, a comprehensive development plan for generation,transmission and distribution. The plan will extend 15 years ahead and willbe reviewed and updated annually. At negotiations an assurance was obtainedthat CEB will prepare such a plan by the end of 1982 to be endorsed by GSLand submitted to the Association.

1.19 CEB requires an effective planning unit to pursue a number ofpressing problems, including:

(a) the immediate addition of a diesel power station, which isnecessary if energy shortages in 1984 and 1985 are to beminimized (Annex 1).

(b) the timely commissioning of Victoria: in particular theimpounding of the 1984 monsoon rains is of primary importanceand CEB must make every effort to avoid delay.

(c) the energy shortages likely in 1982, 83 and 84: programs tominimize their impact, by means of economies and demandmanagement, have to be worked out in advance.

(d) the need for one or two coal fired generating stationstoward the end of the present decade: sites need to beselected and secured very soon.

1.20 In order to optimize the management and operation of the Mahaweliresource, as well as the planning of future construction, it is expected thatCEB and MASL will cooperate closely, perhaps forming a joint planning unit.An immediate planning requirement is an exhaustive hydro identification andranking study. CEB has requested GSL to have this performed and financed bythe German Agency for Technical Cooperation (GTZ), who have done similarservice to other countries. The planning unit will establish and maintainits mathematical models and computer programs in Colombo, so that forecastsand plans can be updated as needed, and suggested changes from any quartercan be readily and fully evaluated. Services required to assist CEB inestablishing its planning department will be funded from CrediL 1048-CE.

Access to Service and Status of Supply

1.21 The total energy generated by CEB's power stations in 1980 was 1,668GWh, about 89% of it hydro. CEB supplied about 208,000 consumers, including218 local authorities who distributed electricity to another 226,000consumers, making the total number of consumers about 434,000. Of these,about 333,000 were domestic. This suggests that at present only about onehousehold in eight has an electricity connection. Rural electrification has

-7--

been extended to over 2,000 of a total 25,000 villages (para 1.27), butelectricity consumption per head was less than 100 kWh in 1980. The majority

of households use firewood for cooking and kerosene for lighting.

1.22 The Bowatenne hydro station was commissioned in 1981 and Canyon is

scheduled to be commissioned in 1982. Victoria and Kotmale are to come online in 1984 and 1985. To prevent shortages of capacity and energy beforethe new hydro becomes available it was necessary to install additionalthermal plant. Three 20 MW gas turbines were installed in late 1980 andearly 1981. A second group of three 20 MW gas turbines was installed latein 1981.

1.23 Further generation will be needed in addition to the six gas turbinesto supply the forecast energy needed in 1984, 85 and 86, and it is expectedthat CEB will order 80 MW of diesel generators in 1982 for installation in

1983 (para 4.15).

1.24 In the months of May through August 1980 there was load shedding tothe extent of about 50 GWh (about 3.5% of annual sales), made necessary bylower than average rainfall, poor availability of steam units, and thebreakdown of one hydro unit at New Laksapana. Only one of the gas turbineswas in service before the end of 1980 because of ordering and constructiondelays. CEB entered 1981 with its hydro reservoirs only 2/3 full, and loadshedding was again inevitable. It was started in February and continued intoJune, with the loss of an estimated 69 GWh of sales. Toward the end of theperiod, supplies to the general public were off for 8 hours per day, and 16major public corporations were shut down to husband the little waterremaining in the reservoirs.

Plant Maintenance

1.25 The maintenance of CEB's transmission and distribution system has

been adequate although unsystematic. Less satisfactory are the distributionlines of some of the local authorities, where for many years only the barestmaintenance has been done and more consumers have continually been added toexisting lines so that voltages at peak times are well below acceptablelevels. The largest of the local authority undertakings, Mt. Lavinia, nearColombo, with about 14,000 consumers and serving a population of about250,000, was taken over by CEB in 1979.

1.26 Maintenance of CEB's generating stations was done reasonably wellin the past, but has deteriorated in recent years. Adequate systems existfor keeping plant history and maintenance records but in many stations theyare not kept up to date. There is no planned maintenance schedule for eachstation to permit management to check easily that all items of plant are

provided for and have duly been serviced. These deficiencies wereparticularly evident at the Kelanitissa steam plant, but efforts are nowbeing made to restore this station to a reasonable level of reliability.

-8-

Rural Electrification

1.27 The first rural electrification schemes were undertaken in the early1960s. Sri Lanka has about 25,000 villages and CEB had provided service toabout 2,000 of them by the end of 1979. Some of the local authorities whobuy in bulk from CEB have extended their lines into nearby villages, addingto the extent of rural electrification. By the end of 1984, an additional1,150 villages will be connected under a Rural Electrification projectfinanced by ADB and GSL at a total cost of US$ 31.8 million.

1.28 The ADB project is expected to introduce some significantimprovements in the handling of rural electrification:

(a) the rural electrification force in CEB will be expanded andempowered to scrutinize and monitor the formulation andimplementation of all new schemes and to implement theADB Project. CEB has agreed to appoint a Project Managerfor rural electrification and to establish a Load Promotionand Monitoring Unit;

(b) economic analysis and discounted cash flow calculations willbe employed in the feasibility analysis of rural schemes;

(c) CEB will arrange installment financing of house wiring andconnection charges.

System Losses

1.29 Before 1976, energy losses on CEB's system were less than 12%, butthey have since been rising and are currently reported in excess of 16%.Moreover, these figures do not include losses in the retail operations ofthe local authorities, who buy in bulk about 25% of the energy sold by CEBand distribute it at low efficiency. Analysis suggests that an acceptablelevel for overall losses would be about 13% of gross generation. In future,substantial blocks of energy will have to be generated thermally every yearmaking better control of losses even more important. It is CEB's intentionto establish a cell within the planning group to monitor and control losses.Funds for this will be provided under the project (Annex 7).

Historical Consumption

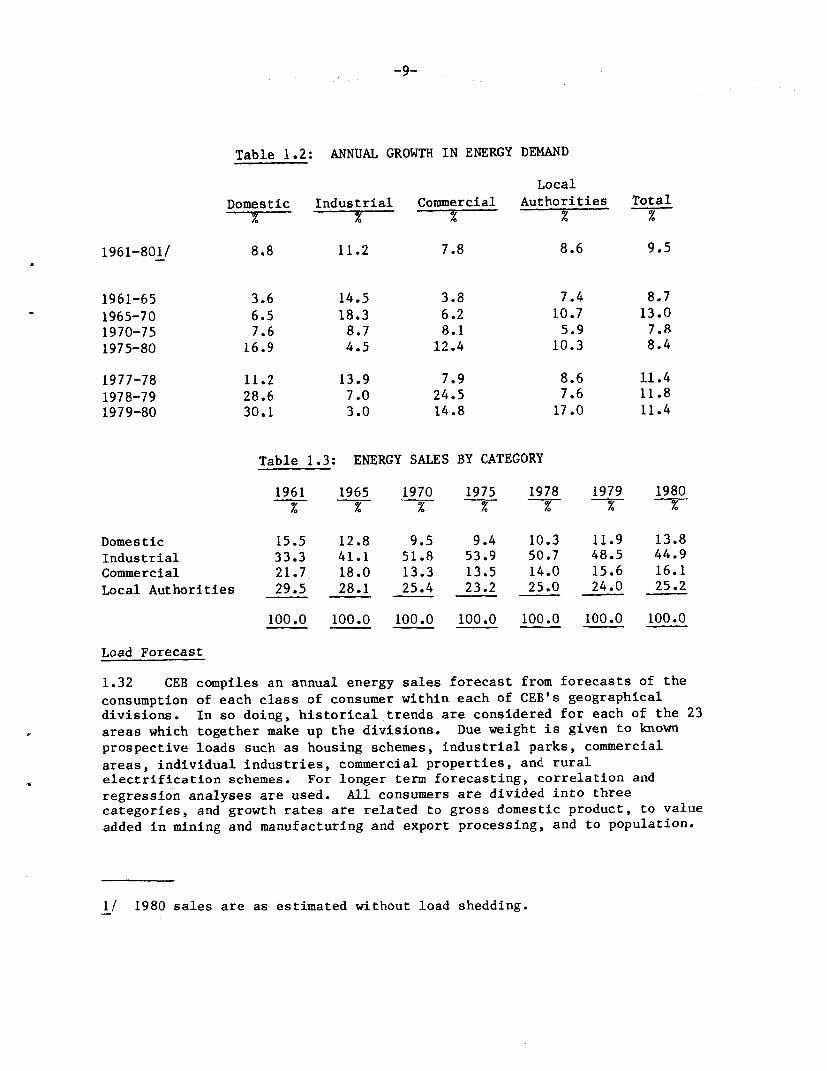

1.30 Growth in consumption of electrical energy over the period 1961 to1980 has averaged 9.5% p.a., ranging from 17.8% in 1966 to 3.3% in 1974.From 1972 to 1977 there was a period of weaker growth, but it appears that arate higher than the long term trend is now being established.

1.31 The short and long term annual growth rates for each class ofconsumer are summarized in Table 1.2. Energy sales since 1961 are analyzedin Table 1.3.

-9-

Table 1.2: ANNUAL GROWTH IN ENERGY DEMAND

LocalDomestic Industrial Commercial Authorities Total

1961-801/ 8.8 11.2 7.8 8.6 9.5

1961-65 3.6 14.5 3.8 7.4 8.71965-70 6.5 18.3 6.2 10.7 13.01970-75 7.6 8.7 8.1 5.9 7.81975-80 16.9 4.5 12.4 10.3 8.4

1977-78 11.2 13.9 7.9 8.6 11.41978-79 28.6 7.0 24.5 7.6 11.81979-80 30.1 3.0 14.8 17.0 11.4

Table 1.3: ENERGY SALES BY CATEGORY

1961 1965 1970 1975 1978 1979 1980

Domestic 15.5 12.8 9.5 9.4 10.3 11.9 13.8Industrial 33.3 41.1 51.8 53.9 50.7 48.5 44.9Commercial 21.7 18.0 13.3 13.5 14.0 15.6 16.1Local Authorities 29.5 28.1 25.4 23.2 25.0 24.0 25.2

100.0 100.0 100.0 100.0 100.0 100.0 100.0

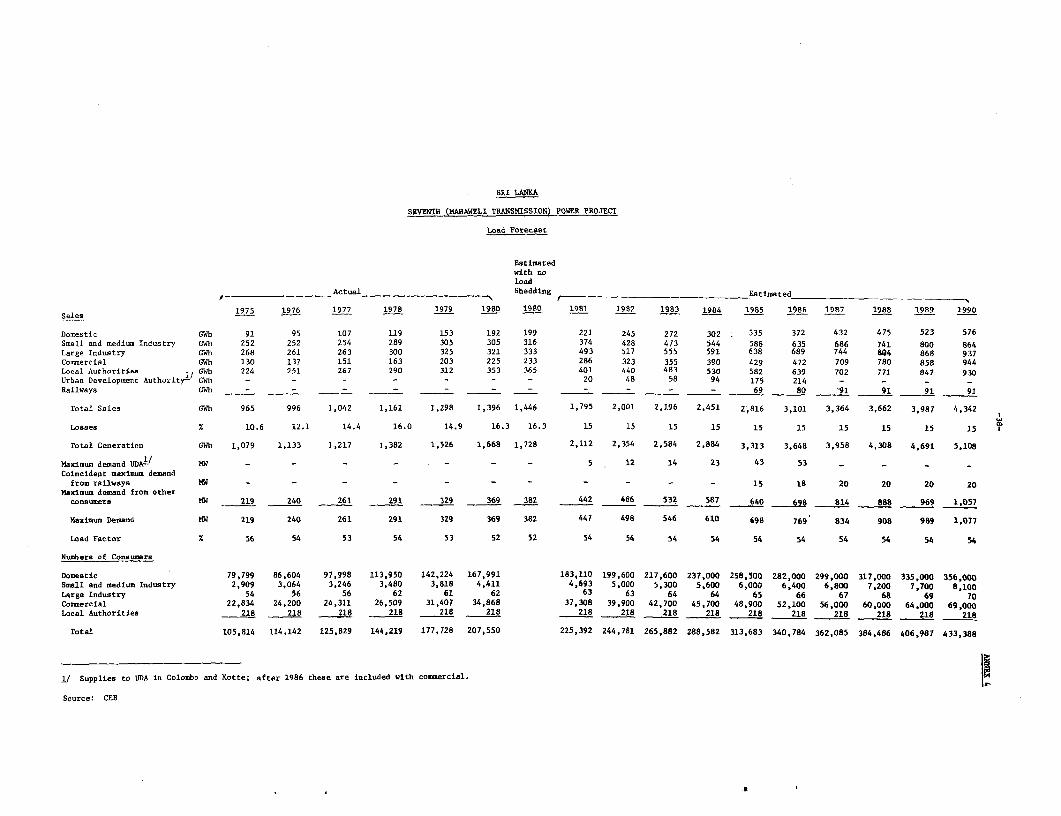

Load Forecast

1.32 CEB compiles an annual energy sales forecast from forecasts of theconsumption of each class of consumer within each of CEB's geographicaldivisions. In so doing, historical trends are considered for each of the 23areas which together make up the divisions. Due weight is given to knownprospective loads such as housing schemes, industrial parks, commercialareas, individual industries, commercial properties, and ruralelectrification schemes. For longer term forecasting, correlation andregression analyses are used. All consumers are divided into threecategories, and growth rates are related to gross domestic product, to valueadded in mining and manufacturing and export processing, and to population.

1/ 1980 sales are as estimated without load shedding.

-10-

To accommodate deviations from the trend, upper and lower limit estimates aremade.

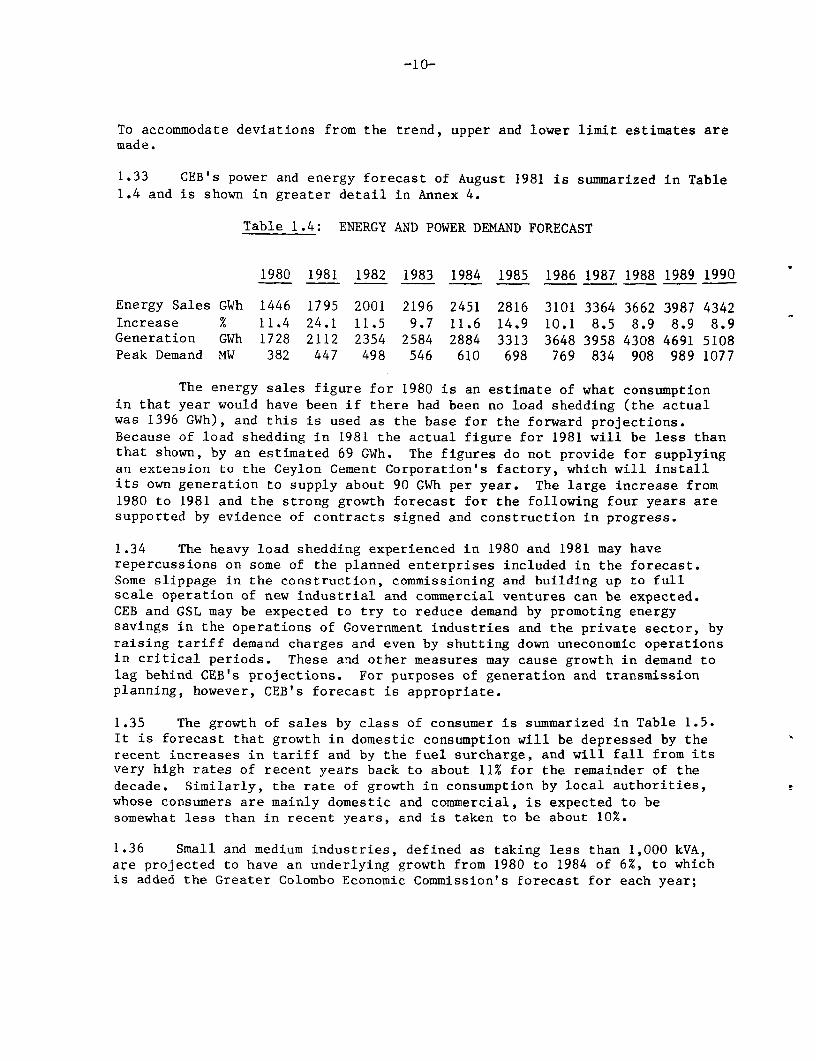

1.33 CEB's power and energy forecast of August 1981 is summarized in Table1.4 and is shown in greater detail in Annex 4.

Table 1.4: ENERGY AND POWER DEMAND FORECAST

1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990

Energy Sales GWh 1446 1795 2001 2196 2451 2816 3101 3364 3662 3987 4342Increase % 11.4 24.1 11.5 9.7 11.6 14.9 10.1 8.5 8.9 8.9 8.9Generation GWh 1728 2112 2354 2584 2884 3313 3648 3958 4308 4691 5108Peak Demand MW 382 447 498 546 610 698 769 834 908 989 1077

The energy sales figure for 1980 is an estimate of what consumptionin that year would have been if there had been no load shedding (the actualwas 1396 GWh), and this is used as the base for the forward projections.Because of load shedding in 1981 the actual figure for 1981 will be less thanthat shown, by an estimated 69 GWh. The figures do not provide for supplyingan extension to the Ceylon Cement Corporation's factory, which will installits own generation to supply about 90 GWh per year. The large increase from1980 to 1981 and the strong growth forecast for the following four years aresupported by evidence of contracts signed and construction in progress.

1.34 The heavy load shedding experienced in 1980 and 1981 may haverepercussions on some of the planned enterprises included in the forecast.Some slippage in the construction, commissioning and building up to fullscale operation of new industrial and commercial ventures can be expected.CEB and GSL may be expected to try to reduce demand by promoting energysavings in the operations of Government industries and the private sector, byraising tariff demand charges and even by shutting down uneconomic operationsin critical periods. These and other measures may cause growth in demand tolag behind CEB's projections. For purposes of generation and transmissionplanning, however, CEB's forecast is appropriate.

1.35 The growth of sales by class of consumer is summarized in Table 1.5.It is forecast that growth in domestic consumption will be depressed by therecent increases in tariff and by the fuel surcharge, and will fall from itsvery high rates of recent years back to about 11% for the remainder of thedecade. Similarly, the rate of growth in consumption by local authorities,whose consumers are mainly domestic and commercial, is expected to besomewhat less than in recent years, and is taken to be about 10%.

1.36 Small and medium industries, defined as taking less than 1,000 kVA,ave projected to have an underlying growth from 1980 to 1984 of 6%, to whichis added the Greater Colombo Economic Commission's forecast for each year;

-1 1-

for 1985 and thereafter 8% growth is used. Consumption by large industriesis forecast to increase by 13.9% per year on average up to 1985. This isexplained mainly by the considerable number of projects expected to come tofruition in 1981-83. The underlying growth for the period 1980-83 was takenas 4% p.a., and after 1983, 8% was applied.

1.37 Commercial consumption is forecast to continue to grow rapidly in theyears up to 1986, as it has in the recent past. Up to 1986 an underlyinggrowth rate of 11% is expected, and to this is added the individualconsumptions of the expanded airport at Katunayake, the substantial loadsto be fed at the Urban Development Authority's developments in Colombo, andthe new Parliamentary complex at Kotte. After 1987 a rate of 10% isestimated for all commercial consumers taken together.

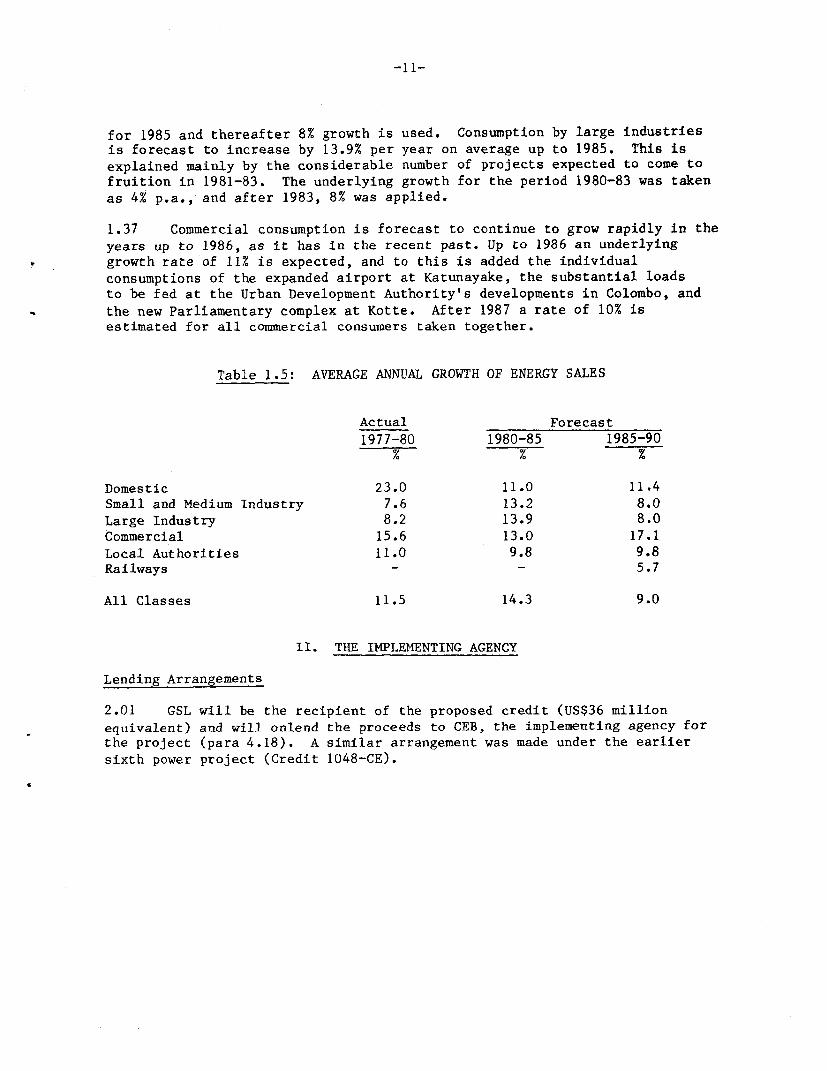

Table 1.5: AVERAGE ANNUAL GROWTH OF ENERGY SALES

Actual Forecast1977-80 1980-85 1985-90

Domestic 23.0 11.0 11.4Small and Medium Industry 7.6 13.2 8.0Large Industry 8.2 13.9 8.0Commercial 15.6 13.0 17.1Local Authorities 11.0 9.8 9.8Railways - - 5.7

All Classes 11.5 14.3 9.0

II. THE IMPLEMENTING AGENCY

Lending Arrangements

2.01 GSL will be the recipient of the proposed credit (US$36 millionequivalent) and will onlend the proceeds to CEB, the implementing agency forthe project (para 4.18). A similar arrangement was made under the earliersixth power project (Credit 1048-CE).

-12-

Organization

2.02 CEB was established by the CEB Act, No. 17 of 1969 (1969 CEB Act)as the successor to the Department of Government Electrical Undertakings(DGEU) and is responsible for the development and coordination of thegeneration, supply and distribution of electrical energy in Sri Lanka. WhileCEB is a public corporation the 1969 CEB Act does not endow it with fullyautonomous powers and the government has reserved to itself a substantialrole in important policy matters and in particular tariffs, capitalinvestment, borrowing and the appointment of the Chairman and the GeneralManager. The conditions of service of all CEB staff are subject to GSLregulation. CEB is also subject to the provisions of the Finance Act, No.38 of 1971 (1971 Finance Act) which regulates the finances of all publiccorporations in Sri Lanka.

2.03 CEB is a corporate body governed by a seven-member Board; membersserve a five-year term and may be reappointed. Board members are appointedby GSL - four with experience in either engineering, commerce, administrationor accountancy, and the others representing local authorities, industry andthe Ministry of Finance - and may be removed at any time. The Chairman isappointed from amongst the Board members. The present Chairman is also theSecretary, Ministry of Power and Energy.

2.04 CEB's organization structure was designed by consultants, UrwickInternational Ltd., in the early 1970's under Loan 636-CE. While somemodifications have been made in recent years including the addition of twoposts of Additional General Manager, the original pattern is basicallyunchanged. Changes are now contemplated as part of the general managementimprovements now taking place in CEB (para 2.08). They would strengthen thedecentralization of CEB's operations while retaining key controls in Colombo.The assurance obtained under Credit 1048-CE that CEB will submit to IDA, inadvance, any proposal for major change to CEB's organizational structure isrepeated under the proposed project.

Management and Staffing

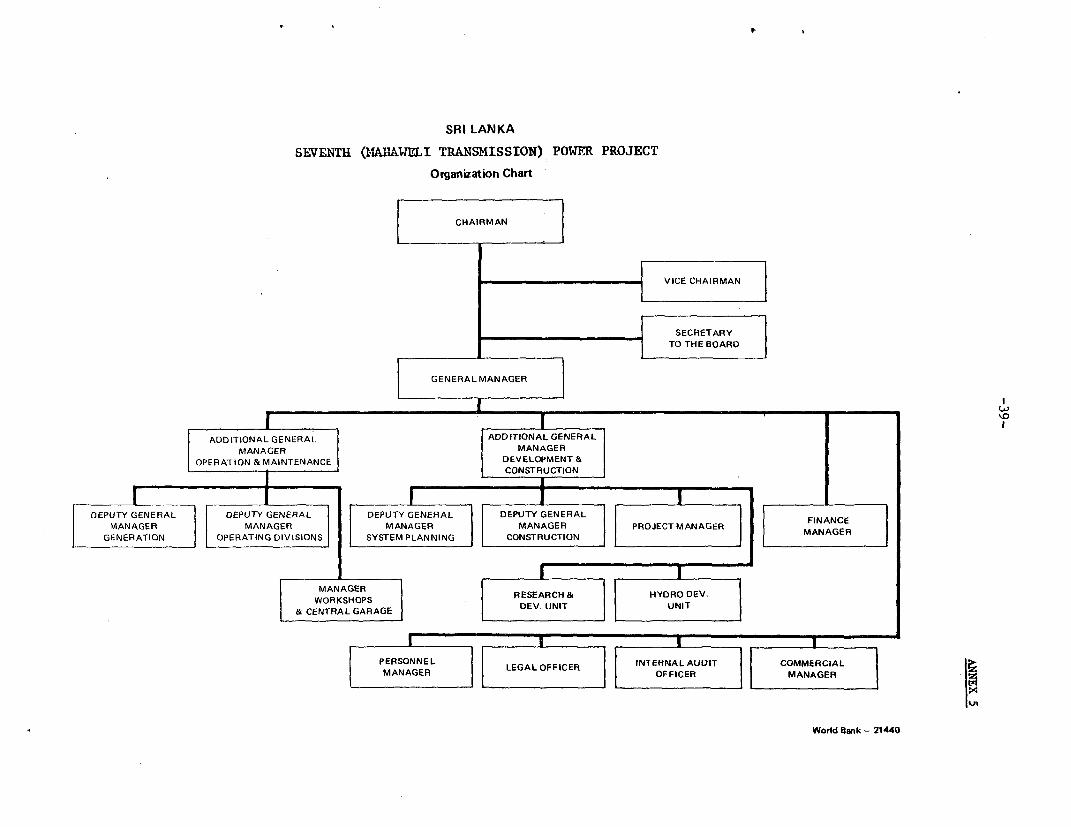

2.05 While the Chairman is responsible through the Board for policymatters and close liaison with government, the General Manager is CEB's ChiefExecutive Officer. He is responsible for the overall direction and controlof CEB's day-to-day business. The present General Manager was recentlypromoted to the post and is an experienced and long-serving engineer. He ispresently assisted by an Additional General Manager, four Deputy GeneralManagers and a Finance Manager. With the exception of the Finance Manager,who is not fully qualified in matters of finance but is a competent andlong-serving administration officer, all top management posts are filled byengineers. The Commercial and Personnel Managers, Chief Internal Auditor(vacant), and the Legal Officer all report directly to the General Manager.CEB's present senior management structure is set out in Annex 5. Below this

-13-

level, CEB operations are decentralized and are controlled at plant (forgeneration) and divisional level. Each of the seven operating divisions into

which Sri Lanka is organized is headed by a Divisional Manager, who is aqualified engineer; the divisions are further divided into areas which arethe primary units for systems maintenance, meter reading and consumerservices.

2.06 CEB has had considerable difficulty in retaining experienced staff inrecent years as many engineers and accountants have left for overseas orprivate sector posts offering substantially higher monetary rewards. Salary

differentials for senior CEB staff do not adequately reflect the heavyadditional responsibilities of such posts. The lack of experiencedengineering staff in the 30-45 year range is particularly noticeable at CEBwhile qualified or part-qualified accountants are now extremely difficult torecruit. These problems appear to be common to many public sectorenterprises in Sri Lanka. A number of key finance posts which were vacant atthe time of appraisal have since been filled.

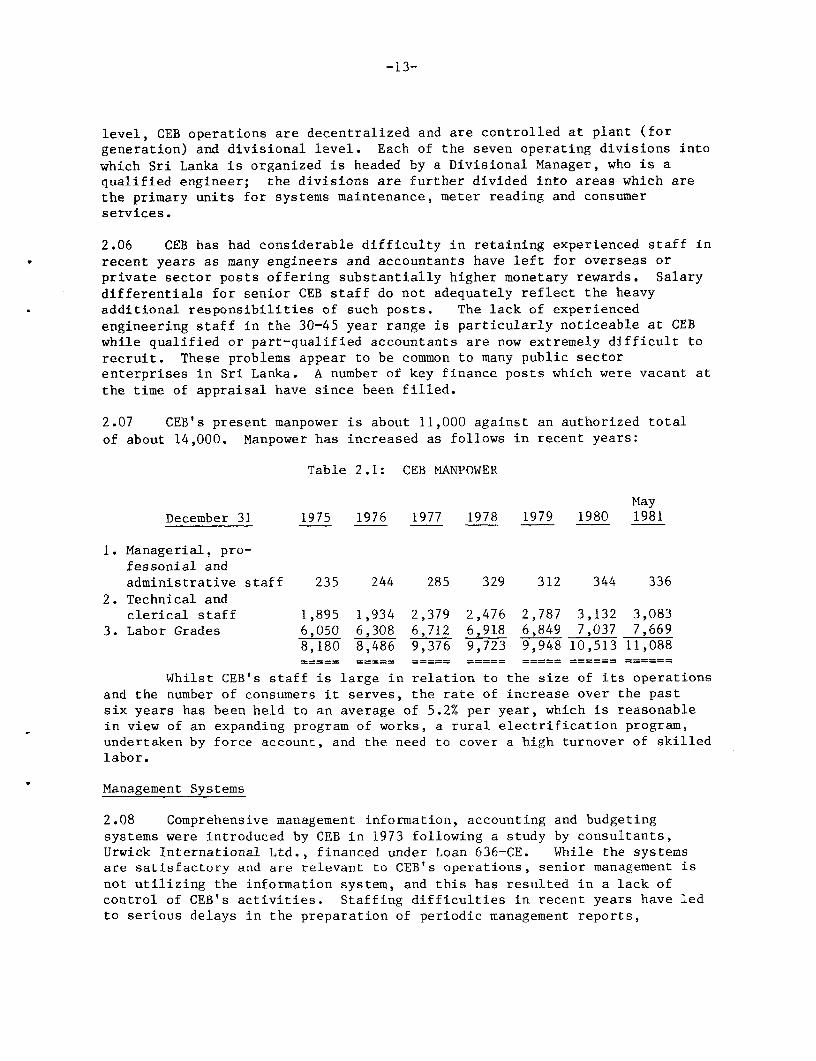

2.07 CEB's present manpower is about 11,000 against an authorized total

of about 14,000. Manpower has increased as follows in recent years:

Table 2.1: CEB MANPOWER

MayDecember 31 1975 1976 1977 1978 1979 1980 1981

1. Managerial, pro-fessonial andadministrative staff 235 244 285 329 312 344 336

2. Technical andclerical staff 1,895 1,934 2,379 2,476 2,787 3,132 3,083

3. Labor Grades 6,050 6,308 6,712 6,918 6,849 7,037 7,6698,180 8,486 9,376 9,723 9,948 10,513 11,088

Whilst CEB's staff is large in relation to the size of its operations

and the number of consumers it serves, the rate of increase over the pastsix years has been held to an average of 5.2% per year, which is reasonablein view of an expanding program of works, a rural electrification program,undertaken by force account, and the need to cover a high turnover of skilledlabor.

Management Systems

2.08 Comprehensive management information, accounting and budgetingsystems were introduced by CEB in 1973 following a study by consultants,Urwick International Ltd., financed under Loan 636-CE. While the systemsare satisfactory and are relevant to CEB's operations, senior management is

not utilizing the information system, and this has resulted in a lack ofcontrol of CEB's activities. Staffing difficulties in recent years have ledto serious delays in the preparation of periodic management reports,

-14-

particularly financial reports. Present IDA reporting requirements areoutlined in Annex 6, but are not being achieved. Internal audit arrangementshave never been satisfactorily established in CEB largely due to theinability to recruit a Chief Internal Auditor.

2.09 In view of the acknowledged weaknesses in CEB's present managementarrangements, CEB agreed under the sixth power project (Credit 1048-CE) toimplement a program of management improvements. To this end, UrwickInternational Ltd., were recalled to review the situation and, in particular,the status of implementation of their earlier recommendations and theeffectiveness of management practices in certain specified areas and torecommend a program of measures to restore CEB's managerial effectiveness.

2.10 This short assignment is now complete: recommendations for the"restoration phase cover (a) general management advice, (b) restoration andfurther development (e.g. computerization) of CEB's systems, and (c) theintroduction of management development and training programs. Therestoration of management systems and the development of training (para 2.11)are most urgent tasks and CEB has recently appointed Urwick InternationalLtd., with their extensive background knowledge for this purpose. Theappointment of a general management advisor requires a person experienced inpower utility management and CEB will be discussing a number of options withIDA in the coming months. Funding is available under Credit 1048-CE for therestoration" program.

Training

2.11 CEB operates a residential training center at Castlereagh for

technicians which offers courses related to CEB's operations. Accommodationis limited and CEB is planning to develop non-residential technical trainingfacilities in Colombo as a result of an earlier investigation by the NationalRural Electric Cooperative Association, Washington, D.C., financed under theUSAID program. Regular training programs are required to fit engineers formanagerial positions; prior to assuming responsibility for operatingfacilities newly qualified engineers should receive six-months on-the-jobtraining: at present this requirement is not consistently achieved. Thereis no program for progressive management development. Training programs arealso required to familiarize accounting staff with CEB's financial operationsand reporting requirements for financial control. CEB agreed under Credit1048-CE to submit to IDA a satisfactory training program for all cadres ofCEB staff by June 30, 1981, and thereafter to implement an agreed program.CEB has submitted an outline training program after discussions with IDA andfollowing Urwick's recent report. This proposal will be developed to suitCEB's needs and provision is made under the proposed project to financetraining expenditure.

-15-

Local Authority Distribution Systems

2.12 While CEB supplies power directly to some 208,000 domestic,commercial and industrial consumers throughout Sri Lanka, another 226,000consumers are supplied by local authorities which purchase power in bulk fromCEB.The quality of local authority service to consumers is unsatisfactory(para 1.25). GSL planned that CEB should assume responsibility for thedistribution facilities of the local authorities. CEB would take over allstaff, assets and liabilities relating to electricity supply. In view ofCEB's present managerial problems and the heavy additional burden such atransfer would place on CEB, including its financial position, the transferis presently deferred and may not now proceed. GSL has confirmed thisposition (para 4.09).

Audit

2.13 The present arrangements under Credit 1048-CE require CEB to submit(a) unaudited accounts to IDA within four months of the year-end (the timepermitted by law for their submission to the Auditor General) and (b) theAuditor Generals report on the accounts within ten months of the year-end.CEB-s FY 1980 unaudited accounts were submitted for audit in May 1981, aconsiderable improvement on earlier years, but the final audit report isstill awaited. The above arrangements are satisfactory and will be continuedunder the proposed project.

Insurance

2.14 CEB has for a number of years borne its own insurable risks and hasestablished an Insurance Reserve to which an annual contribution of 1/10% ofgross fixed assets values is transferred from retained earnings. Thisarrangement is satisfactory.

-1.6-

III. THE PROJECT

Objectives

3.01 The main objective of the project is to supply efficieLitly, reliablyand at minimum cost the output from the hydro electric power stations in theMahaweli basin to the principal load centres in and around Colombo. In doingthis CEB will establish the first elements of a 220 kV grid that willeventually cover much of the country. It was therefore essential to performscreening studies looking well into the future to ensure that a system willevolve that is flexible enough to accommodate any reasonable generationprogram. This meant considering how to handle the outputs from all majorgeneration developments probable in the next twenty years, including suchhydro electric potentials as Upper Kotmale, Uma Oya, Samanalawewa and Kukule,and possible coal fired stations at Colombo and Trincomalee. A secondaryobjective of the project is to inject power into the existing 66 kV system soas to enable it to function at acceptable levels of reliability, voltagecontrol and energy losses.

Description

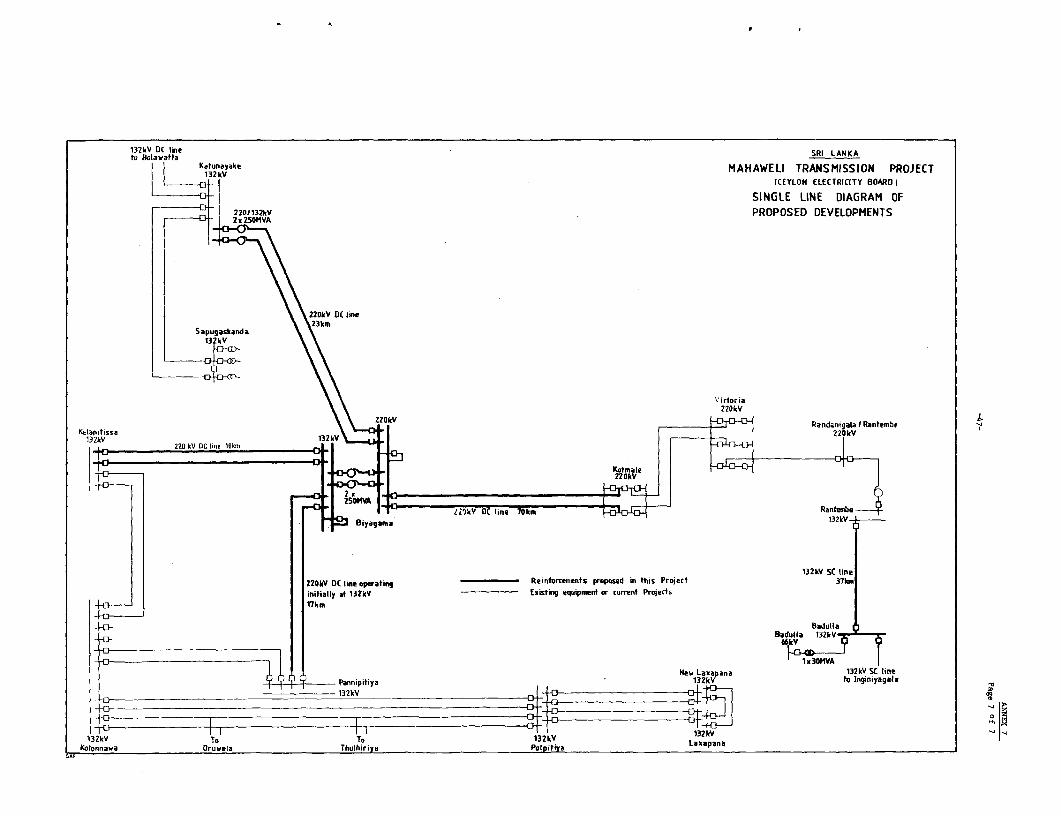

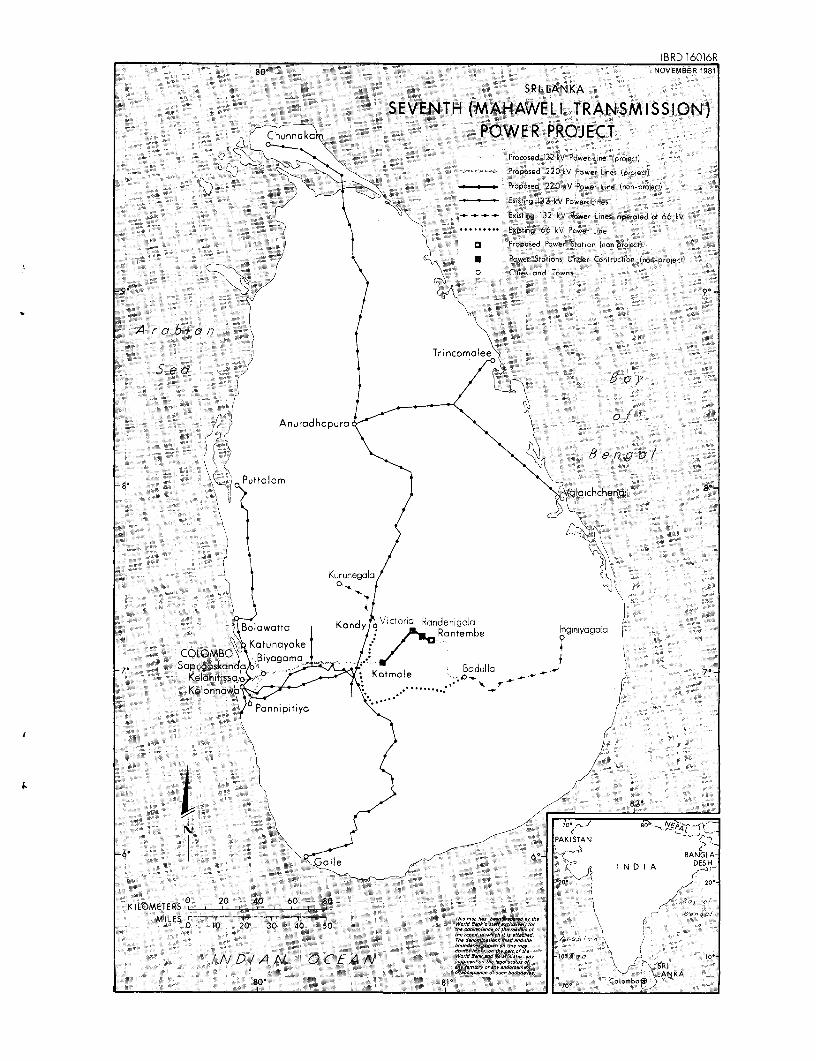

3.02 The project consists of the following components (for details seeAnnex 7 and the map IBRD 16016R.

(a) 126 km of 220 kV doable circuit transmission line and 38 km of132 kV single circuit transmission line.

(b) One new 220/132 kV substation, additions to three existing 132 kVsubstations, one new 132 kV switching station and additions to anexisting 66 kV substation.

(c) Replacement of circuit breakers with new ones of higherrupturing capacity.

(d) Power factor correction equipment.

(e) Power line carrier equipment.

(f) Equipment for a loss reduction cell.

(g) Vehicles, tools and buildings.

(h) Engineering consulting services, technical assistance andtraining.

-17-

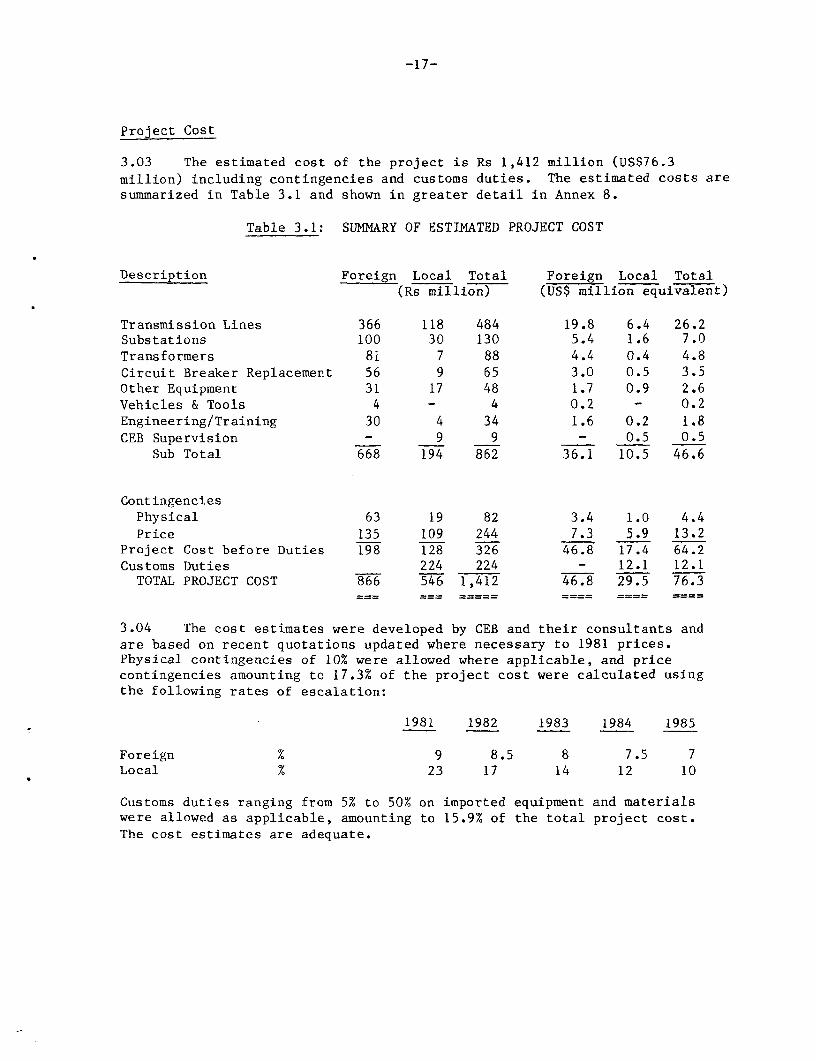

Project Cost

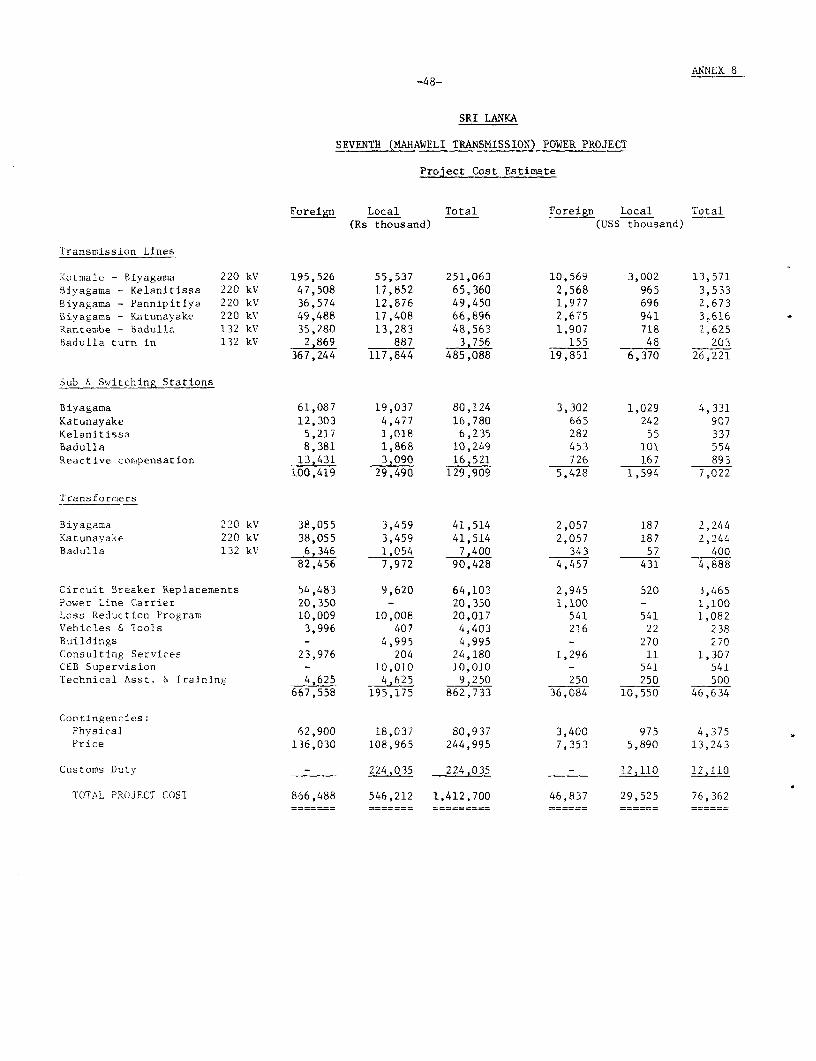

3.03 The estimated cost of the project is Rs 1,412 million (US$76.3million) including contingencies and customs duties. The estimated costs aresummarized in Table 3.1 and shown in greater detail in Annex 8.

Table 3.1: SUMMARY OF ESTIMATED PROJECT COST

Description Foreign Local Total Foreign Local Total(Rs million) (US$ million equivalent)

Transmission Lines 366 118 484 19.8 6.4 26.2Substations 100 30 130 5.4 1.6 7.0Transformers 81 7 88 4.4 0.4 4.8Circuit Breaker Replacement 56 9 65 3.0 0.5 3.5Other Equipment 31 17 48 1.7 0.9 2.6Vehicles & Tools 4 - 4 0.2 - 0.2Engineering/Training 30 4 34 1.6 0.2 1.8CEB Supervision - 9 9 - 0.5 0.5

Sub Total 668 194 862 36.1 10.5 46.6

ContingenciesPhysical 63 19 82 3.4 1.0 4.4Price 135 109 244 7.3 5.9 13.2

Project Cost before Duties 198 128 326 46.8 17.4 64.2Customs Duties 224 224 - 12.1 12.1TOTAL PROJECT COST 866 546 1,412 46.8 29.5 76.3

3.04 The cost estimates were developed by CEB and their consultants andare based on recent quotations updated where necessary to 1981 prices.Physical contingencies of 10% were allowed where applicable, and pricecontingencies amounting to 17.3% of the project cost were calculated usingthe following rates of escalation:

1981 1982 1983 1984 1985

Foreign % 9 8.5 8 7.5 7Local % 23 17 14 12 10

Customs duties ranging from 5% to 50% on imported equipment and materialswere allowed as applicable, amounting to 15.9% of the total project cost.The cost estimates are adequate.

-18-

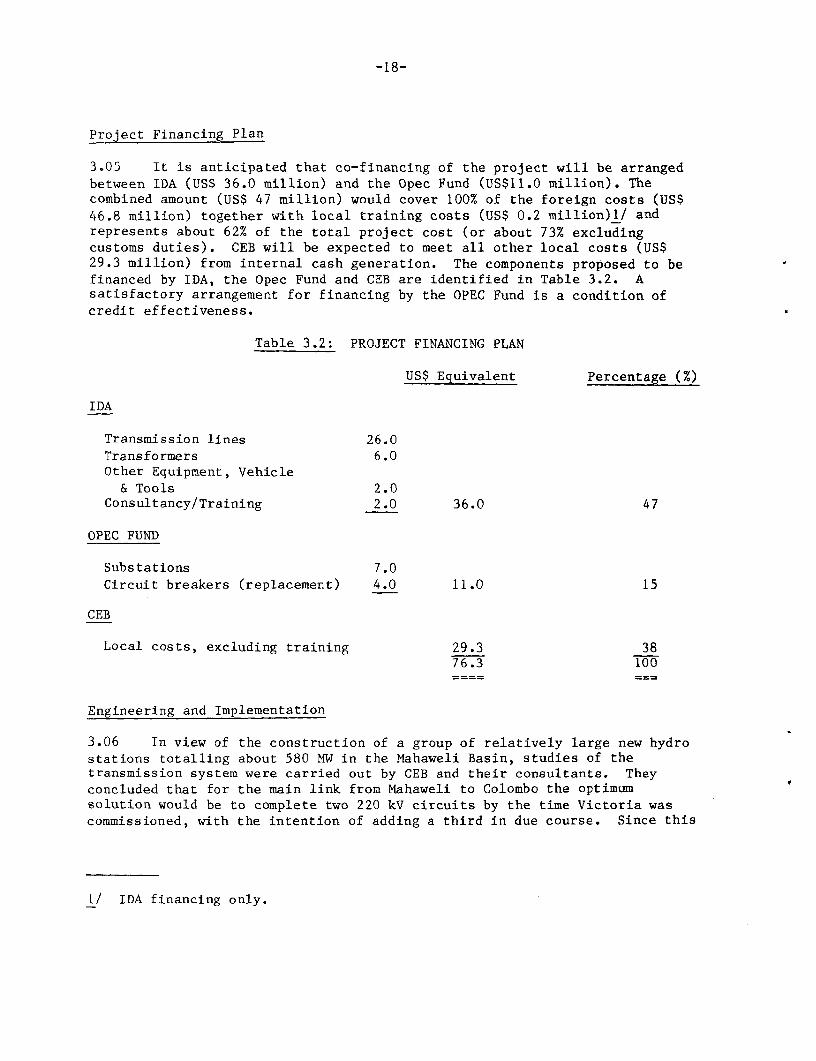

Project Financing Plan

3.05 It is anticipated that co-financing of the project will be arrangedbetween IDA (US$ 36.0 million) and the Opec Fund (US$11.0 million). Thecombined amount (US$ 47 million) would cover 100% of the foreign costs (US$46.8 million) together with local training costs (US$ 0.2 million)1/ andrepresents about 62% of the total project cost (or about 73% excludingcustoms duties). CEB will be expected to meet all other local costs (US$29.3 million) from internal cash generation. The components proposed to befinanced by IDA, the Opec Fund and CEB are identified in Table 3.2. Asatisfactory arrangement for financing by the OPEC Fund is a condition ofcredit effectiveness.

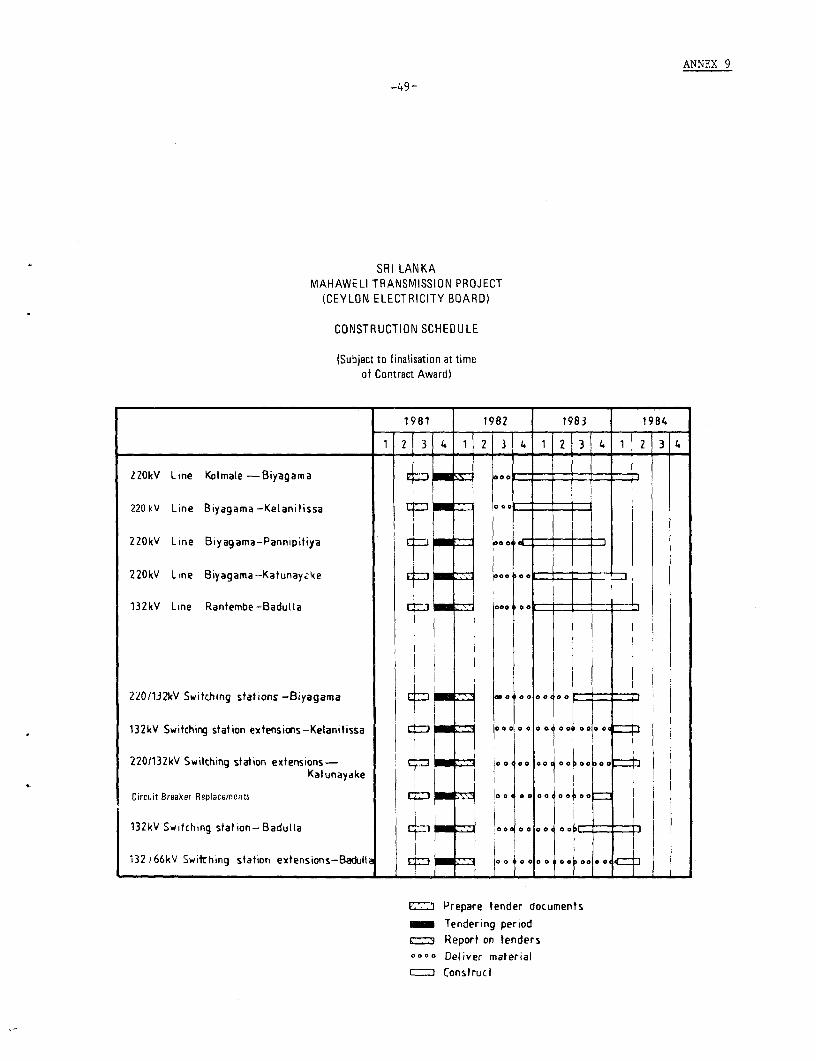

Table 3.2: PROJECT FINANCING PLAN

US$ Equivalent Percentage (%)

IDA

Transmission lines 26.0Transformers 6.0Other Equipment, Vehicle& Tools 2.0

Consultancy/Training 2.0 36.0 47

OPEC FUND

Substations 7.0Circuit breakers (replacement) 4.0 11.0 15

CEB

Local costs, excluding training 29.3 3876.3 100

Engineering and Implementation

3.06 In view of the construction of a group of relatively large new hydrostations totalling about 580 MW in the Mahaweli Basin, studies of thetransmission system were carried out by CEB and their consultants. Theyconcluded that for the main link from Mahaweli to Colombo the optimumsolution would be to complete two 220 kV circuits by the time Victoria wascommissioned, with the intention of adding a third in due course. Since this

1/ IDA financing only.

-19-

voltage had not previously been used in the country, they decided to employconsultants for this project, and engaged the firm which had already starteddesigning the 220 kV substation at Victoria and the line from there toKotmale. The cost of engineering for the lines and substations as far asevaluation of tenders is being financed from Credit 1048-CE. The balance ofthe consulting work comprising detailed design, contract supervision,inspection and testing, and supervision of construction will be financed fromthe proposed Credit. The contract provides for about 140 man months offoreign engineers' services at an average man-month cost (including fees,international travel, subsistence, allowances, and reimbursable foreign

costs) of US$ 9,300.

3.07 The specification of the 220 kV lines will be essentially thatdeveloped for the line from Victoria to Kotmale, while the 132 kV lines willfollow CEB's established practice. The areas through which the lines willpass have been surveyed by helicopter and then visited on land, andprovisonal routes chosen. As soon as the contract is awarded the contractorwill perform check surveys. It is expected that tenders will have beenreceived and evaluated by end-March 1982.

3.08 The project will be constructed between September 1982 and slay 1984(Annex 9). Completion by this date is necessary to permit the firstgenerator in Victoria to come on line as scheduled in mid-1984.

Procurement

3.09 The main part of the project will be constructed under the followingcontracts:

(a) A single responsibility contract for the 220 kV and 132 kVlines.

(b) A single responsibility contract for the new 220 kV substation,the new 132 kV switching station, and the modifications tothe existing 132 kV and 66 kV substations; this contractwill include the supply and installation of the reactivecompensation equipment, and the installation (but not thesupply) of the power transformers and the power line carrierequipment.

(c) A supply contract for the power transformers.

(d) A supply contract for the circuit breaker replacements.

(e) A supply contract for the power line carrier equipment.

3.10 International competitive bidding in accordance with IDA's guidelineswill be employed for the major contracts. Vehicles, equipment and materials

-20-

3.10 International competitive bidding in accordance with IDA's guidelineswill be employed for the major contracts. Vehicles, equipment and materialsnot exceeding US$15,000 per item and US$150,000 in aggregate may be procuredin accordance with local procedures, which are satisfactory. For materialsand equipment tendered internationally, the standard domestic preference of15% on the c.i.f. price, or the prevailing duty, whichever is less, will beapplied in bid evaluation.

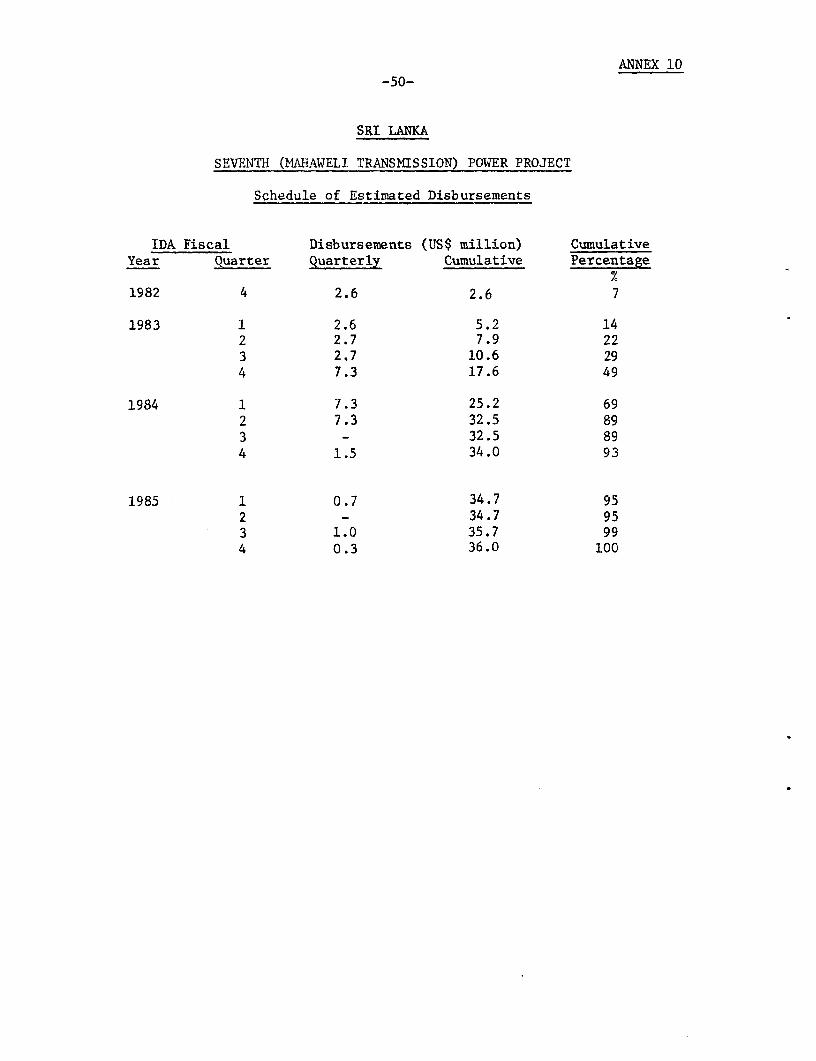

Disbursements

3.11 The Credit will be disbursed against the following items:

(a) 100% of the foreign expenditures for 220 kV and 132 kVtransmission lines.

(b) 100% of foreign expenditures for directly imported items, or100% of the local expenditure (ex-factory) for locallymanufactured items, or 65% for locally procured items(equipment and materials for power transformers, power linecarrier, loss reduction program, and vehicles and tools).

(c) 100% of foreign expenditures on engineering consultants.

(d) 100% of expenditures on technical assistance and 100% oftraining.

A schedule of estimated disbursements is provided in Annex 10. It isconsistent with the proposed implementation period for the project (para3.08) and provides for about 90% disbursements by project completion. Theproposed credit would be fully disbursed by June 1985, some 3 1/2 years fromproject approval. Similar recent Bank Group projects have been disbursedover about 4 1/2 years, but CEB is confident that it can complete the projectin a shorter period.

Land Acquisition

3.12 No problems are foreseen. The site for the Biyagama substation hasto be acquired but no difficulty is expected as the land is owned by GSL.Wayleaves for transmission lines are routinely acquired without difficulty.

Risks

3.13 The project consists of normal electric utility work entailing nounusual risks and no particular difficulty is foreseen in its execution.Price contingencies in the estimate have been allocated to minimise the riskof cost overruns.

-21-

IV. FINANCIAL ANALYSIS

CEB's Statutory Position

4.01 CEB's finances are regulated by the provisions of the 1969 CEB Actand the 1971 Finance Act, which affects all public corporations in Sri Lanka.CEB is required, by Section 38 of the 1969 CEB Act, to operate in acommercial manner so as to ensure that revenues are sufficient to meet alloutgoings, including depreciation and interest, and a reasonable proportionof development costs. CEB's statutory obligations were amended in twoimportant respects following IDA approval of Credits 372-CE and 1048-CE. 1/in 1973:

(a) CEB is permitted to charge depreciation in its accounts basedon a current valuation of fixed assets rather than the historiccost of such assets.

(b) CEB's obligation to pay an 8% annual dividend on GSL's equitycapital is waived each year until CEB has generated cashequivalent to a 30% contribution to the combined annualcapital expenditure on electricity supply, including interestduring construction, of CEB and any other body responsiblefor undertaking a joint scheme with CEB.

Past Financial Performance

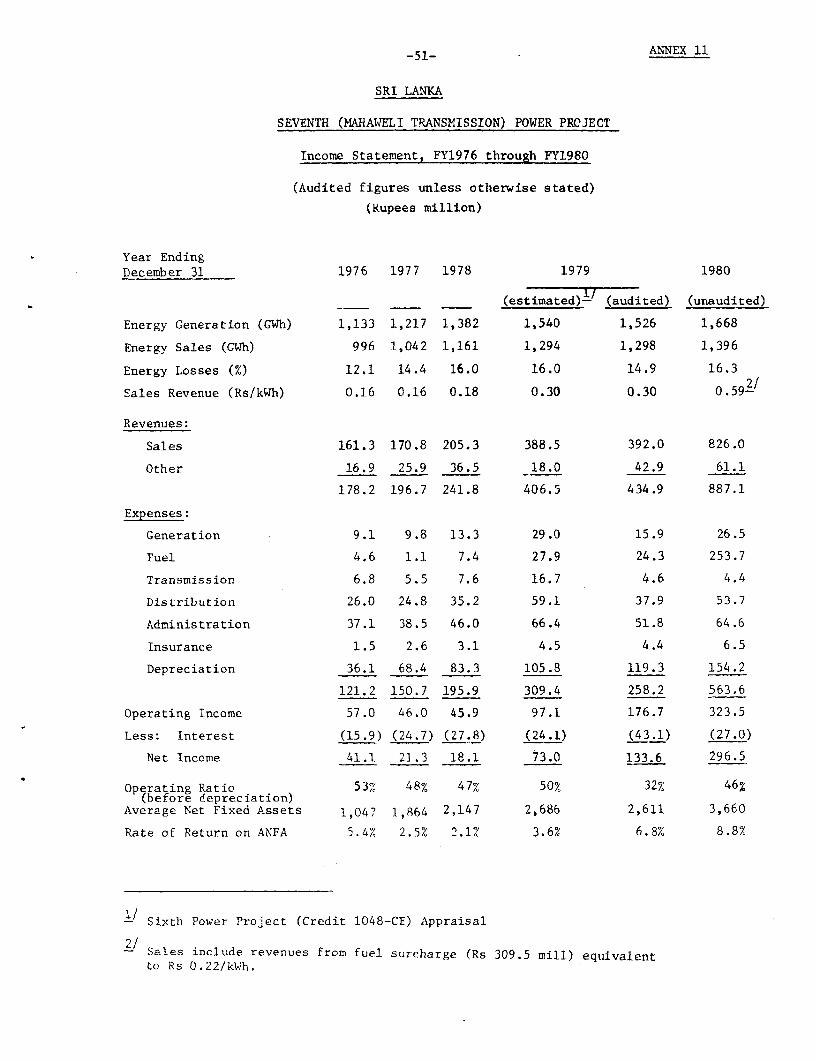

4.02 CEB's actual financial operations for the five years to FY 1980 aresummarized in Table 4.1 below and are shown in greater detail in Annex 11.

1/ These conditions are repeated under the proposed Credit.

-22-

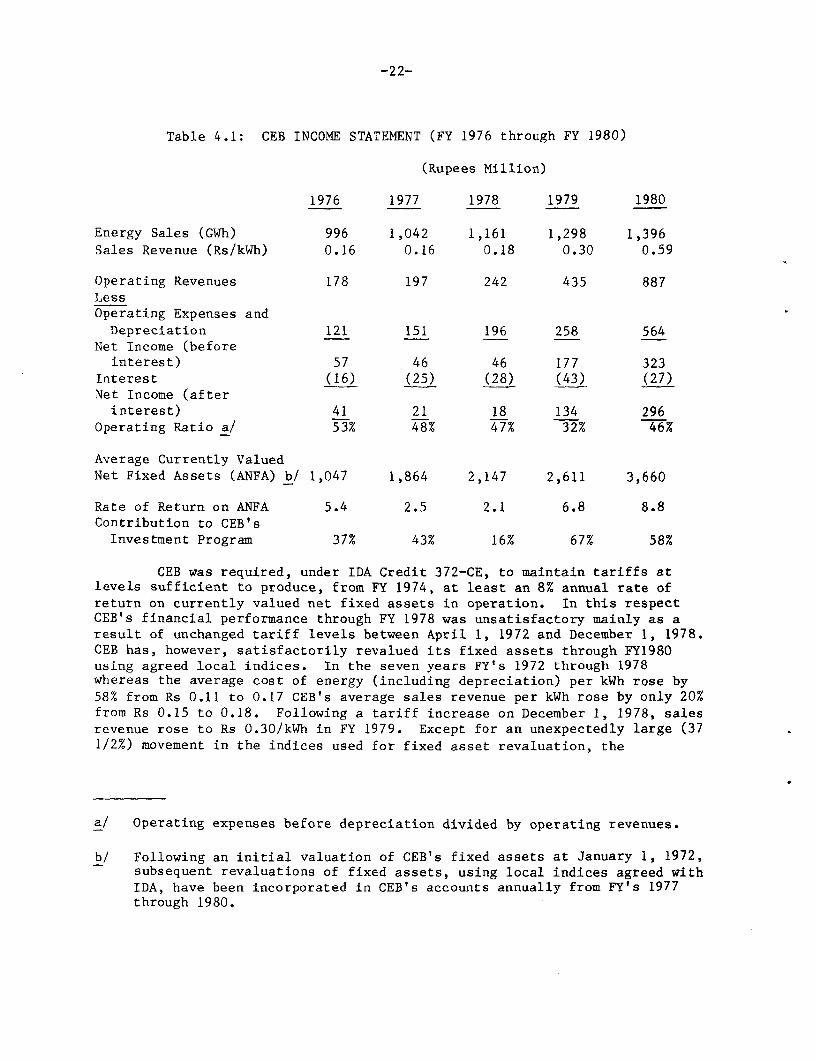

Table 4.1: CEB INCOME STATEMENT (FY 1976 through FY 1980)

(Rupees Million)

1976 1977 1978 1979 1980

Energy Sales (GWh) 996 1,042 1,161 1,298 1,396Sales Revenue (Rs/kWh) 0.16 0.16 0.18 0.30 0.59

Operating Revenues 178 197 242 435 887LessOperating Expenses andDepreciation 121 151 196 258 564

Net Income (beforeinterest) 57 46 46 177 323

Interest (16) (25) (28) (43) (27)Net Income (afterinterest) 41 21 18 134 296

Operating Ratio a/ 53% 48% 47% 32% 46%

Average Currently ValuedNet Fixed Assets (ANFA) b/ 1,047 1,864 2,147 2,611 3,660

Rate of Return on ANFA 5.4 2.5 2.1 6.8 8.8Contribution to CEB'sInvestment Program 37% 43% 16% 67% 58%

CEB was required, under IDA Credit 372-CE, to maintain tariffs atlevels sufficient to produce, from FY 1974, at least an 8% annual rate ofreturn on currently valued net fixed assets in operation. In this respectCEB's financial performance through FY 1978 was unsatisfactory mainly as aresult of unchanged tariff levels between April 1, 1972 and December 1, 1978.CEB has, however, satisfactorily revalued its fixed assets through FY1980using agreed local indices. In the seven years FY's 1972 through 1978whereas the average cost of energy (including depreciation) per kWh rose by58% from Rs 0.11 to 0.17 CEB's average sales revenue per kWh rose by only 20%from Rs 0.15 to 0.18. Following a tariff increase on December 1, 1978, salesrevenue rose to Rs 0.30/kWh in FY 1979. Except for an unexpectedly large (371/2%) movement in the indices used for fixed asset revaluation, the

a/ Operating expenses before depreciation divided by operating revenues.

b/ Following an initial valuation of CEB's fixed assets at January 1, 1972,subsequent revaluations of fixed assets, using local indices agreed withIDA, have been incorporated in CEB's accounts annually from FY's 1977through 1980.

-23-

covenanted 8% rate of return would have been achieved, the actual being about7%. Operating expenses increased in FY 1979 by about 32%, much less thanbudgetted, bringing the average energy cost to Rs 0.20/kWh.

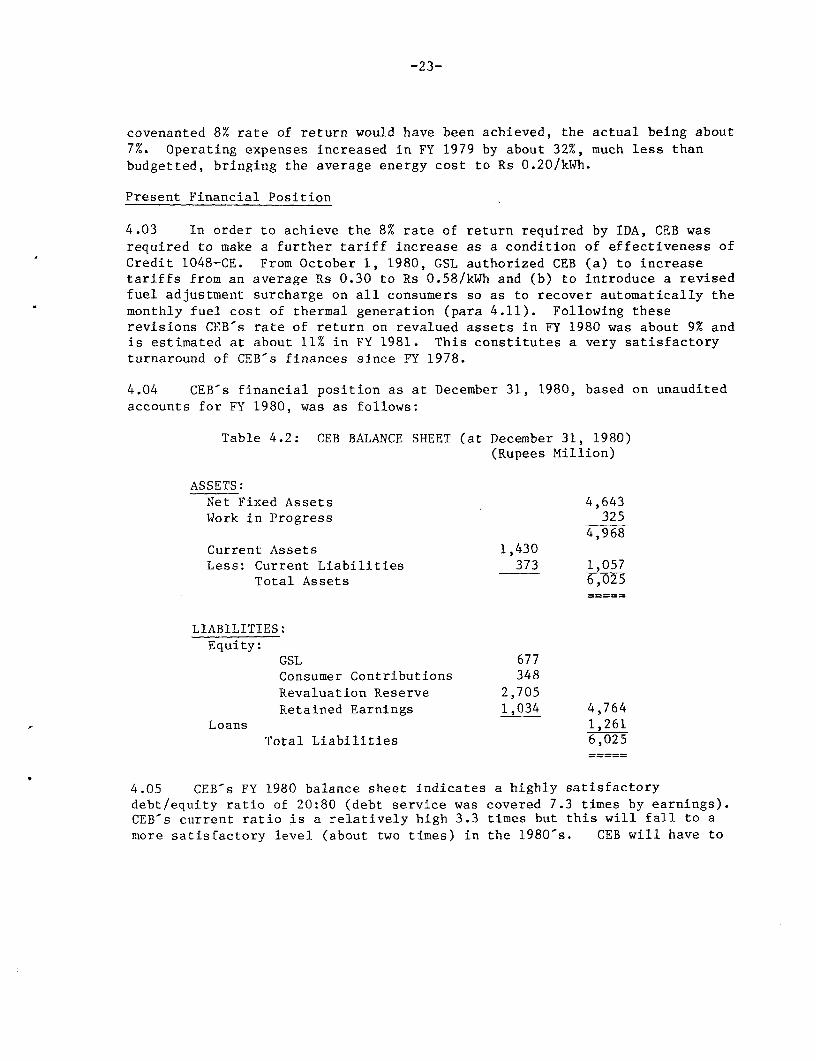

Present Financial Position

4.03 In order to achieve the 8% rate of return required by IDA, CEB was

required to make a further tariff increase as a condition of effectiveness ofCredit 1048-CE. From October 1, 1980, GSL authorized CEB (a) to increasetariffs from an average Rs 0.30 to Rs 0.58/kWh and (b) to introduce a revisedfuel adjustment surcharge on all consumers so as to recover automatically themonthly fuel cost of thermal generation (para 4.11). Following theserevisions CEB's rate of return on revalued assets in FY 1980 was about 9% andis estimated at about 11% in FY 1981. This constitutes a very satisfactoryturnaround of CEB's finances since FY 1978.

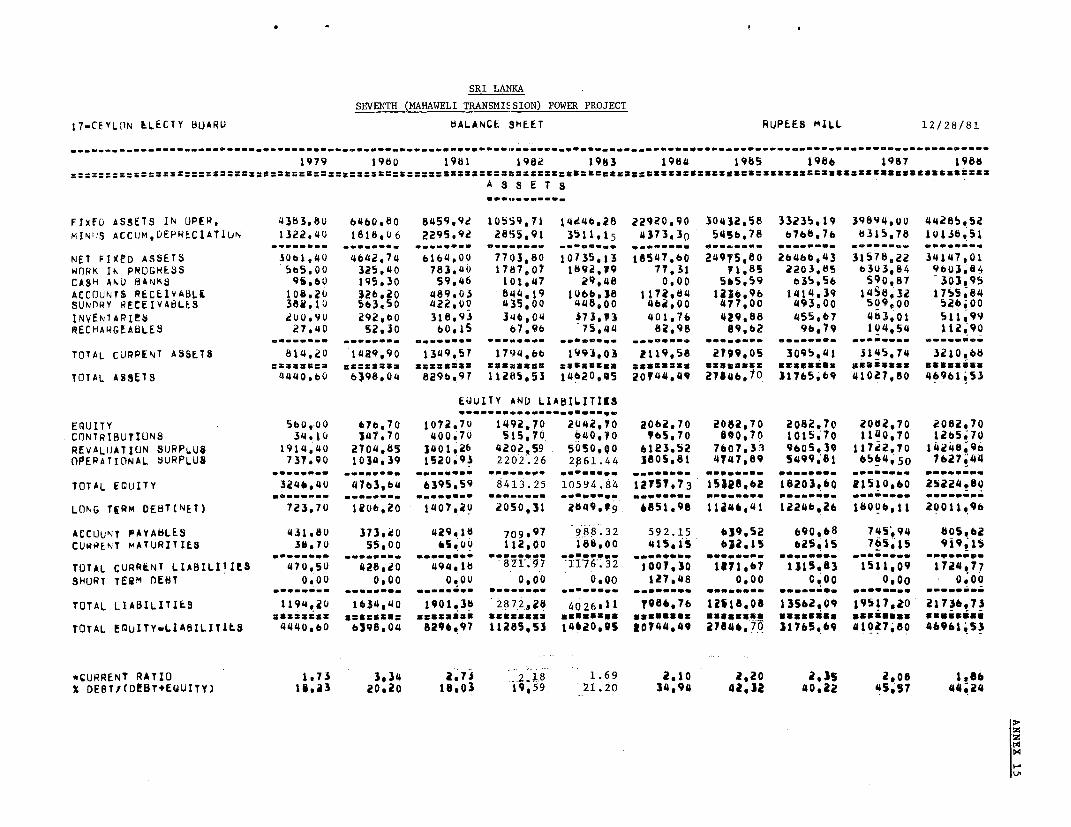

4.04 CEB's financial position as at December 31, 1980, based on unauditedaccounts for FY 1980, was as follows:

Table 4.2: CEB BALANCE SHEET (at December 31, 1980)(Rupees Million)

ASSETS:Net Fixed Assets 4,643Work in Progress 325

4,968Current Assets 1,430Less: Current Liabilities 373 1,057

Total Assets 6,025

LIABILITIES:Equity:

GSL 677Consumer Contributions 348Revaluation Reserve 2,705Retained Earnings 1,034 4,764

Loans 1,261Total Liabilities 6,025

4.05 CEB's FY 1980 balance sheet indicates a highly satisfactorydebt/equity ratio of 20:80 (debt service was covered 7.3 times by earnings).CEB's current ratio is a relatively high 3.3 times but this will fall to amore satisfactory level (about two times) in the 1980's. CEB will have to

-24-

maintain a tight control over the level of consumer receivables (paras 4.06 -

4.10) and inventories.l/

Billing and Collection

4.06 CEB's billing and collection performance has been reasonablysatisfactory in recent years. Under Credit 1048-CE, CEB's customerreceivables on the last day of each month should not exceed the aggregatebillings for the three months ending on the same day and this requirementis repeated under the proposed project. CEB has made considerable effortsto meet this target: the position at December 31, 1980 indicates receivablesequivalent to 3.2 months billings compared to 3.6 months billings at end FY1978. As CEB's revenues have quadrupled in this short period the presentreceivables position represents a commendable performance by CEB staff.

4.07 An analysis of consumer receivables at end FY 1980 is as follows:

1/ Under the Sixth Power Project CEB agreed to reduce inventories to a

satisfactory level by December 31, 1982 and GSL agreed to ensure thetimely availability of foreign exchange for inventories: materialsmanagement problems have already been reviewed by CEB's management con-sultants and action is being taken to improve controls. These conditionsare repeated under the proposed project.

-25-

Table 4.3: ANALYSIS OF CONSUMER RECEIVABLES (at December 31, 1980)

Consumer Large ConsumersCategory a/ (over 50 kVA) Other Consumers Total

No. % % No. % % No. % %months Bill- Receiv- months Bill- Receiv- months Bill- Receiv-out- ings ables out- ings ables out- ings ablesstand- stand- stand-ing ing ing

Private 2.3 24 18 3.7 25 28 3.1 49 46

PublicCorporations 2.7 39 32 - - - 2.7 39 32

Government 3.1 6 6 14.7 1 3 4.1 7 9LocalAuthorities- General 8.0 4 10 9.6 - - 8.8 4 10

- StreetLighting 16.2 1 3 - - - 16.2 1 3

Total 3.0 74 69 4.1 26 31 3.2 100 100

4.08 CEB has a separate unit to handle large consumers' accounts, whichare maintained on a manual system. The above table indicates that CEB ismaintaining a tight credit control over most large consumers, the exceptionbeing the 218 local authorities which CEB supplies in bulk and for streetlighting. In the first three months of 1981 CEB managed to reduce localauthority arrears by some Rs 6.5 million to about Rs 30 million, equivalentto some 7 months billings but the position is still unsatisfactory.

4.09 GSL agreed, under Credit 1048-CE to ensure the timely payment offuture amounts owed by the local authorities to CEB together with arrears inaccordance with an agreed program. At that time GSL was proposing totransfer the local authority systems to CEB and this led to a deteriorationin the local authority arrears position. Arrears would have been settled as

a part of the transfer arrangements. The transfer has now been abandoned.

a/ Local authority billings are at pre-December 1978 tariffs by agreement

between GSL and CEB. GSL is billed separately in respect of the tariffsincreases, including the fuel surcharge, since December 1, 1978: the

billings and receivables on this account are not included under theGovernment sector in this table but are shown under a separate debtor's

account (paragraph 4.09).

-26-

An assurance was obtained, therefore, at negotiations that, from October 1,1981, the local authorities will pay the current CEB tariffs for bulksupplies and introduce retail tariffs which are sufficient to cover CEB'sbulk supply charges and the local authorities distribution costs. PresentlyGSL is responsible for payment of increases in the local authority bulksupply tariffs since December 1, 1978, but to date has made payments to CEBonly up to March 31, 1981. Arrangements are in progress to settle theremaining amount and the payment to CEB of the amount outstanding atSeptember 30, 1981 is a condition of credit effectiveness.

4.10 The bulk of CEB's billings are of relatively small amounts and aremaintained on computer. They constitute some 25% of CEB's billings byamount. Over 50% of such monthly accounts are for less than Rs 15. Thedifficulty of recruiting satisfactory meter readers poses a continuingserious problem for CEB and leads to some delays in billing and problems incollection. CEB is striving for improved performance in this sector.

Revenues and Tariffs

4.11 The details of CEB's recent tariff structure are set out in Annex12. CEB's tariffs were unchanged between April 1972 and December 1978 butsince then two tariff increases have been made which have increased CEB'saverage tariff by about 260% from Rs 0.16 to 0.58/kWh (about 3 US cents).l/In addition to raising tariff levels in recent years, which has enabled it tomeet financial rate of return criteria, CEB has also made some structuralimprovements to its tariffs. Domestic consumers now pay higher block tariffsand non-domestic tariffs have been rationalized. Further, from October 1,1980, CEB is recovering automatically the cost of fuel needed for CEB'sincreasing thermal generation by way of a surcharge on consumers' monthlybills. The first 200 units of domestic consumption (equivalent to a maximumcharge of US$ 5) are exempt from the surcharge and this exempts over 90% ofdomestic consumers.

4.12 CEB agreed under Credit 1048-CE to carry out a study of long runmarginal cost (LRMC) pricing with technical assistance from the Bank. Thisstudy should have been completed by December 31 1980 but staffingconstraints in particular have led to delay and it was agreed to extend thedeadline by one year to December 31, 1981. Preliminary results of the studywere submitted at negotiations but further refinements are needed for theresults to be useful for tariff restructuring. The study is now beingrevised and CEB gave an assurance during negotiations to implement anyrecommendations agreed after consultation with GSL and IDA.

1/ with the addition of the fuel surcharge this was equivalent to about -6 US cents/kwh. in 1981.

-27-

4.13 An assurance was obtained at negotiations that CEB will continue,as previously, to review tariffs annually, before the start of each financialyear to ensure that revenues are sufficient to meet operating expenses,including fuel and depreciation, and to produce at least an 8% rate of returnon currently valued net fixed assets. While the presently agreed rate ofreturn is 8%, in FY 1982 CEB will have to increase tariffs by about 50%,(equivalent to a 12% rate of return) in order to generate sufficient internalresources to meet the local costs of its approved investment program through1985. This increase in tariffs is a condition of credit effectiveness. InFYs 1982 and 1983 such tariffs would produce a before-tax rate of return of16% (para 4.16). From FY 1985 onwards further tariff increases will berequired to enable CEB at least to maintain the covenanted 8% rate of return:the amount of such increases will depend to a great extent upon the size ofCEB's future investment program.

Transfer of Assets from MASL

4.14 The 1969 Act authorizes CEB to enter into "joint schemes" with otheragencies for the generation of electricity. The Act does not detail thearrangements for the transfer and operation of assets created under suchschemes. Subsequently, under Credit 372-CE, GSL agreed to ensure that CEB issufficiently involved on the formulation of all future joint schemes, andthat the power assets are transferred on completion to CEB on termssatisfactory to IDA. This was done in the case of the 38 MW Ukuwela hydrostation constructed under the Mahaweli Ganga Stage I (para 1.11(g)). Most ofthe hydro-power development in the 1980's in Sri Lanka will be carried outunder the Accelerated Mahaweli Program. CEB is not required to contribute tothe costs of these schemes during the construction phase but ownership willbe transferred to CEB on their completion. The need for adequateco-ordination between CEB and in the design and construction of thesefacilities was discussed in the context of the Sixth Power Project and againduring negotiations for the proposed project. CEB is not represented on theMASL Board and such representation would require legislation. However,technical co-ordination between the two agencies is now satisfactory. GSLagreed during negotiations to ensure proper future co-ordination between CEBand any other agency involved in a joint scheme. Futhermore, in view of themajor impact that the Victoria and Kotmale assets will have on CEB-sfinances, GSL and CEB have agreed a satisfactory provisional basis for thetransfer of these assets.

Financing Plan (FYs 1981-85)

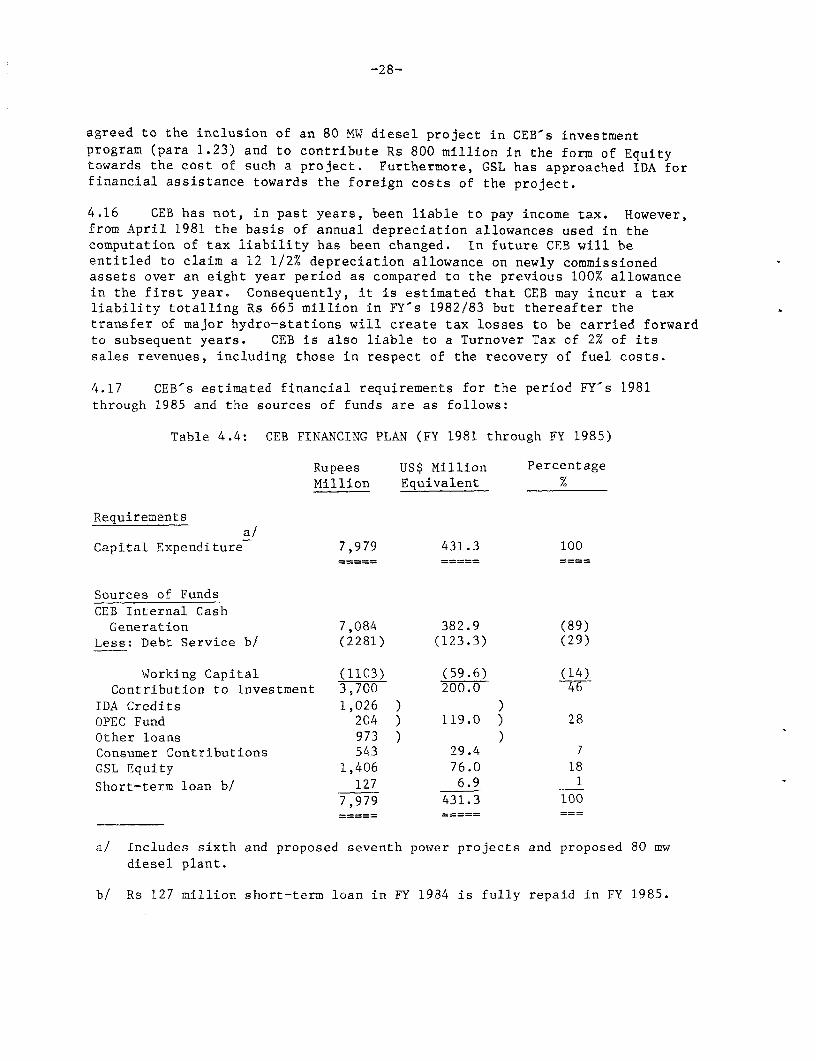

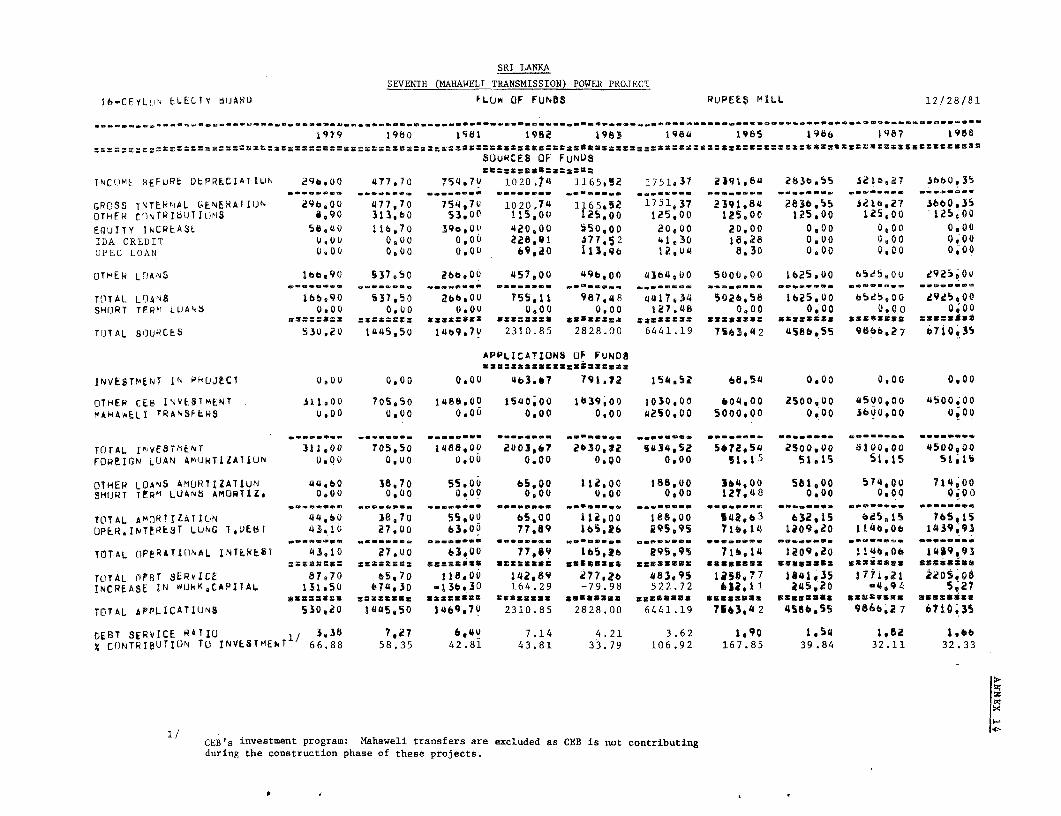

4.15 CEB's presently approved investment program through FY 1985,comprises the ongoing ADB-assisted Bowatenne, Canyon and RuralElectrification projects, the IDA-assisted sixth (transmission anddistribution) and proposed seventh (Mahaweli transmission) projects, varioussmall system augmentation works and the installation of a second 60 MW of gasturbines in FY 1982. GSL confirmed at negotiations that it has recently

-28-

agreed to the inclusion of an 80 MW diesel project in CEB's investmentprogram (para 1.23) and to contribute Rs 800 million in the form of Equitytowards the cost of such a project. Furthermore, GSL has approached IDA forfinancial assistance towards the foreign costs of the project.

4.16 CEB has not, in past years, been liable to pay income tax. However,from April 1981 the basis of annual depreciation allowances used in thecomputation of tax liability has been changed. In future CEB will beentitled to claim a 12 1/2% depreciation allowance on newly commissionedassets over an eight year period as compared to the previous 100% allowancein the first year. Consequently, it is estimated that CEB may incur a taxliability totalling Rs 665 million in FY-s 1982/83 but thereafter thetransfer of major hydro-stations will create tax losses to be carried forwardto subsequent years. CEB is also liable to a Turnover Tax of 2% of itssales revenues, including those in respect of the recovery of fuel costs.

4.17 CEB's estimated financial requirements for the period FY's 1981through 1985 and the sources of funds are as follows:

Table 4.4: CEB FINANCING PLAN (FY 1981 through FY 1985)

Rupees US$ Million PercentageMillion Equivalent %

Requirementsa/

Capital Expenditure 7,979 431.3 100

Sources of FundsCEB Internal CashGeneration 7,084 382.9 (89)

Less: Debt Service b/ (2281) (123.3) (29)

Working Capital (1103) (59.6) (14)Contribution to Investment 3,700 200.0 46

IDA Credits 1,026 ) )OPEC Fund 204 ) 119.0 ) 28Other loans 973 ) )Consumer Contributions 543 29.4 7GSL Equity 1,406 76.0 18

Short-term loan bJ 127 6.9 17,979 431.3 100

a/ Includes sixth and proposed seventh power projects and proposed 80 mwdiesel plant.

b/ Rs 127 million short-term loan in FY 1984 is fully repaid in FY 1985.

- 29 -

4.18 The proceeds of the IDA credit of US$36 million will be madeavailable to CEB by GSL at 12% interest for a 20 year period with 3 yearsgrace. 1/ GSL will bear any foreign exchange risk in accordance with the1969 CEB Act. The execution of an onlending agreement satisfactory to IDA isa condition of credit effectiveness.

4.19 To protect its future financial viability, CEB has agreed previouslynot to incur any long-term debt without IDA's prior agreement unless itsmaximum future debt service is covered at least 1.25 times by its most recent12 months operating surplus before depreciation. This condition is repeatedunder the proposed Credit.

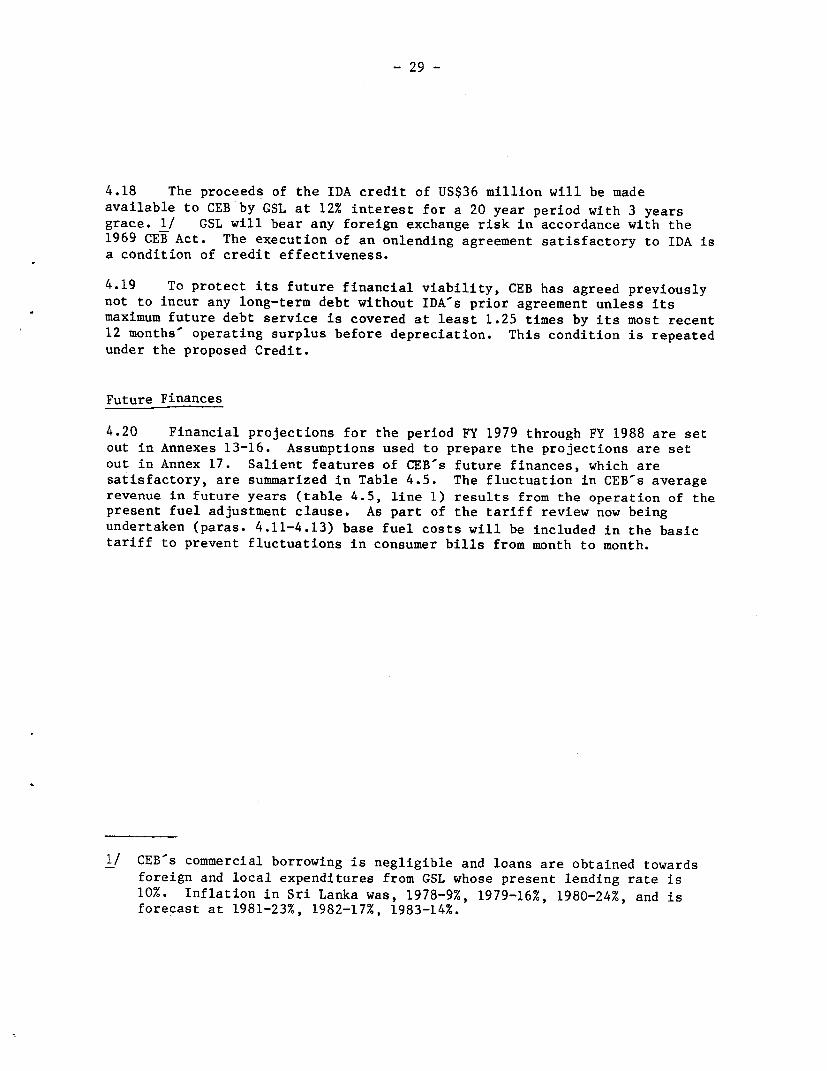

Future Finances

4.20 Financial projections for the period FY 1979 through FY 1988 are setout in Annexes 13-16. Assumptions used to prepare the projections are setout in Annex 17. Salient features of CEB's future finances, which aresatisfactory, are summarized in Table 4.5. The fluctuation in CEB's averagerevenue in future years (table 4.5, line 1) results from the operation of thepresent fuel adjustment clause. As part of the tariff review now beingundertaken (paras. 4.11-4.13) base fuel costs will be included in the basictariff to prevent fluctuations in consumer bills from month to month.

1/ CEB's commercial borrowing is negligible and loans are obtained towardsforeign and local expenditures from GSL whose present lending rate is10%. Inflation in Sri Lanka was, 1978-9%, 1979-16%, 1980-24%, and isforecast at 1981-23%, 1982-17%, 1983-14%.

-30-

Table 4.5: SUMMARY OF CEB'S FUTURE FINANCES

1981 1982 1983 1984 1985 1986 1987 19881. Average Revenue a/ b/

(Rs/kWh) 1.15 1.69 1.94 1.91 1.76 1.82 1.73 1.92(US cents/kWh) 6 9 10 10 10 10 10 10

2. Average Tariff b/(Rs/kWh) 0.58 0.74 0.87 0.87 1.05 1.15 1.20 1.27

3. Average Cost ofEnergy Sold c/

(Rs/kWh) 0.71 1.18 1.41 1.20 0.91 0.91 0.78 0.92(US cents/kWh) 4 6 8 6 5 5 4 5

4. Operating Ratio c/ 61 70 73 63 52 50 45 485. Rate of return on

annually revalued (%)Net Fixed Assets d/ 11 12 10 9 8 8 8 8

6. Debt service coverage 6.4 7.1 4.2 3.6 1.9 1.5 1.8 1.77. Contribution to CEB-s

Investment Program (%)e/ ---- 46 -- ----- 32…

8. Current Ratio 2.7 2.2 1.7 2.1 2.2 2.4 2.1 1.9

9. Debt/Equity Ratio 18/82 20/80 21/79 35/65 42/58 40/60 46/54 44/56

a/ Including fuel adjustment surcharge.

b/ Assuming a tariff increase of 50% from mid-1982 and further increases fromFY 1985 to meet a minimum of 8% financial rate of return on currentlyvalued net fixed assets.

c/ Before depreciation.

d/ Rate of return before tax is 16% in FYs 1982/83.

e/ Excluding works undertaken by MASL for subsequent transfer to CEB.

-31-

V. JUSTIFICATION

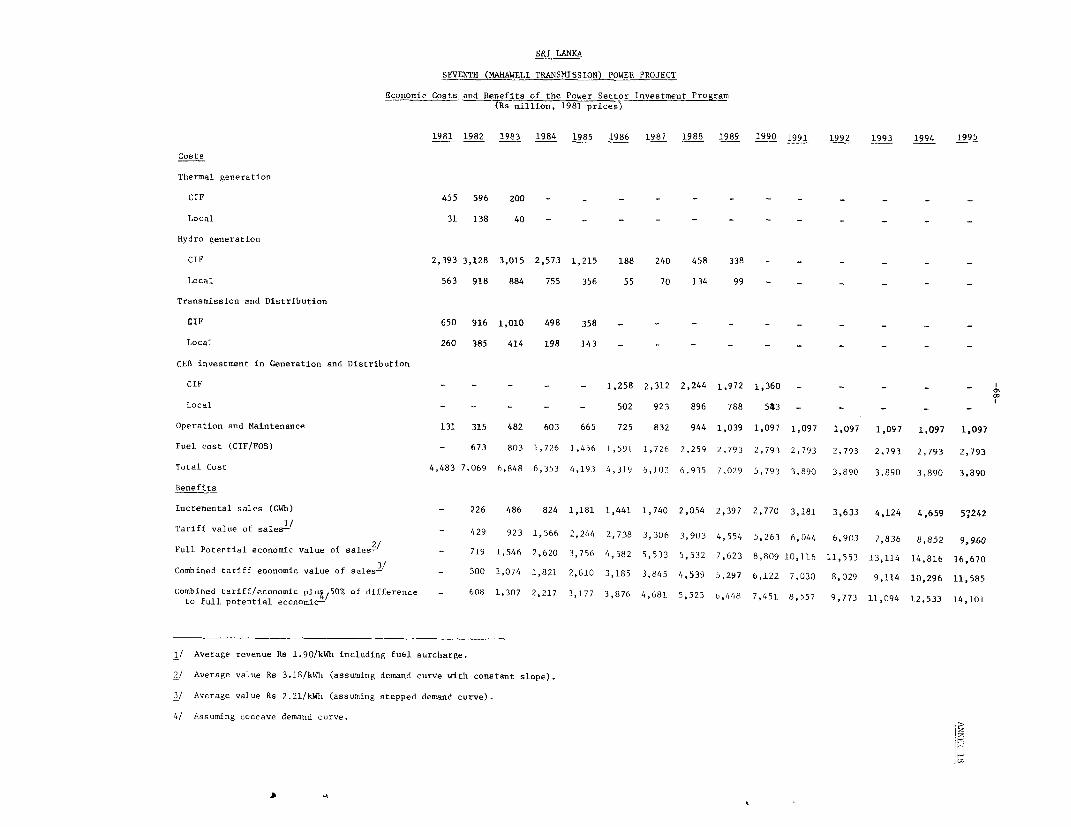

Approach

5.01 The proposed project is an integral part of a total power

sector investment program in Sri Lanka, incorporating CEB's expenditureson generation, transmission and distribution, extra thermal capacity,the Mahaweli program of hydroelectric stations, and the Samanalawewahydro station. It is the critical link conveying the additional power to begenerated at Victoria and Kotmale to the load centers. The rate of returnon the small incremental investment would be exceedingly high.However, the method employed in this report is one of justifying the entireinvestment program and recognizes all inherent costs, thereby covering theproposed project implicitly.

5.02 As two agencies are involved in the planning of parts of theinvestment program, conscious efforts to identify an overall least-cost

solution have only recently begun (para 1.17), and a least-cost programhas been developed with the help of an improved computer model. However,the only aggregate investment program at the time of appraisal may nothave been the least-cost solution, and is, therefore, analyzed with respct toits feasibility in economic terms, rather than compared to other potentialprograms.

Economic Costs and Benefits

5.03 The investment program in its present form is presented in Annex 16.It is based on CEB demand forecasts and represents all known plannedexpenditure relevant to the power sector for the period 1981-1990. Whereavailable, costs, and benefits are expressed in CIF or equivalent borderterms. Local values are converted to border prices using a shadow/marketwage ratio and a standard conversion factor (Annex 18, paras. 3 to 5).Economic benefits arising from incremental supply to electricity consumers

are calculated as the total willingness to pay including the consumers'surplus, assumed to be approximated by the cost and extent of usingalternative energy sources for economic activities and lighting (Annex 18,paras 6 to 12).

Results

5.04 The economic justification involves quantifying benefits in theform of user surplus, assuming various possible shapes of the demandcurve for power. In economic terms, the best estimate of the rate ofreturn is about 14%, and about 8% if tariffs are used as benefit proxy.A 10% increase in costs would reduce the rate of return to about 12%,

-32-

while a 10% decrease in costs would boost it to about 16%. If a real fuelprice increase of 3% p.a. is assumed, the rate of return with consumer surplusis reduced to about 12%, with tariff revenue as benefit proxy to about4% (Annex 18). The investment program in its aggregate form isjustified in economic terms if a conservative estimate of consumer surplusis used as part of the benefit. Given the large build-up of generatingcapacity in the next years, tariff revenue appears to be somewhat inadequateto recover the full cost (including headworks) of the program.

Tariffs and Marginal Cost

5.05 The average revenue for CEB (including fuel surcharge) is expectedto approach Rs 2.00/kWh in 1983 (table 4.5). Present preliminary estimatesof long-run marginal cost for the system range between Rs 1.80/kWh andRs 2.50/ kWh, depending on voltage level and consumer characteristics. Amore detailed study of the structure of long-run maginal cost is underpreparation and is expected to be completed by January 1982: a first draftis being finalized by CEB with Bank Group assistance. At present, itappears likely that average revenue will be approaching marginal cost by1983.

VI. AGREEMENTS TO BE REACHED AND RECOMMENDATION

Agreements during Negotiations

6.01 Satisfactory agreements were reached with GSL/CEB during negotiationswith regard to:

(a) the preparation and submission by December 31, 1982, andthereafter annually, of a long-term power development plan(para 1.18)

(b) modifications to CEB's organizational structure (para 2.04)

(c) implementation of CEB's training program (para 2.11)

(d) audit of CEB-s accounts (para 2.13)

(e) restriction of dividend payments by CEB and charge ofdepreciation on revalued assets (para 4.01)

(f) control of CEB's inventory levels and the provision of foreignexchange by GSL for inventories (para 4.05)

-33-

(g) CEB's consumer receivables not to exceed three months' billings(para 4.06)

(h) timely payment by GSL's local authorities of CEB's bulk supplycharges and adequate local authority retail tariffs (para 4.09)

(i) improvements to CEB's tariff structure (para 4.12)

(j) rate of return on CEB's currently valued net fixed assets(para 4.13)

(k) arrangements for GSL co-ordination of Joint Schemes (para 4.14)

(1) CEB's debt service coverage (para 4.19)

Conditions of Effectiveness

6.02 The following will be required prior to Credit effectiveness

(a) satisfactory arrangements for OPEC co-financing. (para 3.05);

(b) GSL's payment to CEB of outstanding arrears in respect ofits local authorities (para 4.09); and

(c) a tariff increase averaging about 50% (para 4.13);

(d) conclusion of a satisfactory onlending agreement for theproposed Credit (para 4.18).

Recommendation

6.03 Subject to agreement on the above matters the proposed project issuitable for an IDA credit of US$36 million equivalent.

SRI LANKA

SEVENTH (MAHAWELI TRANSMISSION) POWER PROJECT

Power & Energy Balances

InstalledCapacity 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990

Laksapana (3x8.33+2x12.5) MW 50 50 50 50 50 50 50 50 50 50 50Inginiyagala (2x2+2x3) MW - - - - - - - - -Udawalawe (3x2) MW - - - - - - - - - -Wimalaaurendra (2x25) MW 50 50 50 50 50 50 50 50 50 50 50Polpitlya (2x37.5) MW 75 75 75 75 75 75 75 75 75 75 75New Laksapana (2x50) MW 100 100 100 100 100 100 100 100 100 100 100Ukuwela (2x20) MW 38 38 38 38 38 38 38 38 38 38 38Bowatenna (1s40) MW - 40 40 40 40 40 40 40 40 40 40Canyon (2x30) MW - - 30 30 60 60 60 60 60 60 60Victeria (3x70) MW - - - - - 210 210 210 210 210 210

Cotmale (2x67) MW - - - - - 134 134 134 134 134

Randenigala (2

x61) MW - - - - - - - 122 122 122 122Rantembe (

2x24) MW - - - - - - - - 48 48 48

Broadlands (2x10) MW - - - - - - - - 20 20 20Kelanitissa Steam (2x25) MW 40 40 40 40 40 0°/ 40 40 40 40 40Pettabh Diesal (2x3) MW 2 2 2 2 0 0 0 0 0 0Chunnakam Diesels (5x2+4xl) MW 8 8 8 8 0 / 0 0 0 0 0 0

Gas Turbines (6x20) MW 20 120 120 120 120 120 120 120 120 120 120Heavy Fuel Diesels (810) MW - - - 20 80 80 80 80 80 80 80Coal Fired Station (2x60) MW - - - - - - - - - 120 120

Capacity start year MW 363 383 523 553 563 613 823 997 1.119 1.247 1,307Capacity added in year (net) MW 20 140 30 20 90 210 174 122 68 120 0

Capacity end year 3/ MW 383 523 553 573 653 823 997 1,119 1.187 1,307 1,307Reliable capacity end y- MW 293 433 463 483 547 717 871 993 1.061 1.121 1,121Maxims Demand MW 382 447 498 546 610 698 769 834 908 989 1.077Surplus (Deficit) MW (89) (14) (35) (63) (63) 19 102 159 153 132 44

Firm SecondaryEnergy Energy

Existing Hydro 1350 400 GWh 1,479 1,450 1,450 1,450 1,450 1,450 1,450 1,450 1,450 1,450 1,450Bowatenna 100 40 GWh - 50 110 110 110 110 110 110 110 110 110Canyon 130 40 GWh - - 40 140 140 140 140 140 140 140 140Victoria 686 284 GWh - - - - - 757 757 757 757 757 757

Kotmal 310 160 GWh - - - - - 350 350 350 350 350Randenigala 366 159 GWh - - - - - - - 405 405 405 405Rantembe 158 93 GWh - - - - - - - - 187 187 187Broadlands 4/ 72 33 GWh - - - - - - - - 80 80 80

Hydro Energy Available GWh 1,479 1.500 1,600 1.700 1,700 2,457 2.807 3,212 3,479 3,479 3,479

Kelanitissa Steam GWh 140 200 / 200 200 200 0 100 200 209, 200 200Heavy FPel Diesels GWh 30 10 10 50 526 526 526 526 526 526 526

Coal Fired Station 1Wh - 7/ - 7 - - - - 788 788Gas Turbines GWb 19 300 736 736 736 736 736 736 736 736 736Thermal Energy Available GWh 189 510 946 986 1,462 1,262 1,362 1,462 1.462 2,250 2.250Total Energy Available GWh 1,668 2,010 2,546 2,686 3.162 3.719 4,169 4,674 4.941 5,729 5,729Total Energy Required GWh 1,728 2,112 2,354 2,584 2,884 3,313 3,648 3.958 4,308 4.691 5,108Surplas (Deficit) GWh (60) (102) 192 102 278 406 521 716 633 1,038 621

1/ Plant being rehabilitated.

2/ Plant retired at end 1983.

3/ Reliable capacity calculated by excluding:(a) largest hydro unit(b) one steam unit (20 MW)(c) one gas turbine (20 MW)(d) 20% of heavy foel diesels

4/ Taken as firm energy plus 25% of secondary.

5/ Assumes plant factor of 57% on effective 40 MW,

6/ Assumes plant factor of 75% on 80 MY.

7/ Assumes plant factor of 70% on 120 MW. s

-35- ANNEX 2

SRI LANKA

SEVENTH (MAHAWELI TRANSMISSION) POWER PROJECT

Generating Facilities

Installed EffectiveYear of Capacity Capacity

Existing Type Commissioning MW MW

Old Laksapana Hydro 1950/58 50 50Inginiyagala Hydro 1950 10 0Uda Walawe Hydro 1968 6 2Wimalasurendra (Norton Bridge) Hydro 1965 50 50Polpitiya (Maskeliya Oya Stage I) Hydro 1969 75 75New Laksapana (Maskeliya Oya Stage II) Hydro 1974 100 100Ukuwela (Polgolla) Hydro 1976 38 36Bowatenne Hydro 1981 40 40

369 353

Kelanitissa (Grand Pass) Steam 1962 50 40Kelanitissa Gas Turbines 1980/81 60 60Pettah Diesels 1954 6 2Chunnakam Diesels 1954 14 8

499 463

Under Construction

Kelanitissa Gas Turbines 1981 60Canyon Hydro 1982/83 60Victoria Hydro 1984 210Kotmale Hydro 1985/87 201

531

Planned to 1990

Diesels 1983/84 80Randenigala Hydro 1987 122Rantembe Hydro 1988 48

Thermal (Coal) 1989 120Broadlands Hydro 1990 20

390

Planned beyond 1990

Samanalawewa Hydro 1990/91 240Steam 200

Upper Kotmale Hydro 120Steam 100

Kukule Hydro 250Ratnapura Hydro 35Uma Oya Hydro 150Bing Hamala Hydro 110Jasmin Hydro 40

- 36 -

ANNEX 3Page I of 2

SRI LANKA

SEVENTH (MAHAWELI TRANSMISSION) POWER PROJECT

Existing Transmission and Distribution Systems

132 kV System

1. The 132 kV system comprises 569 miles of line, of which 361 milesare double circuit and 208 miles single circuit.