Embed Size (px)

Citation preview

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No. P-4794-IND

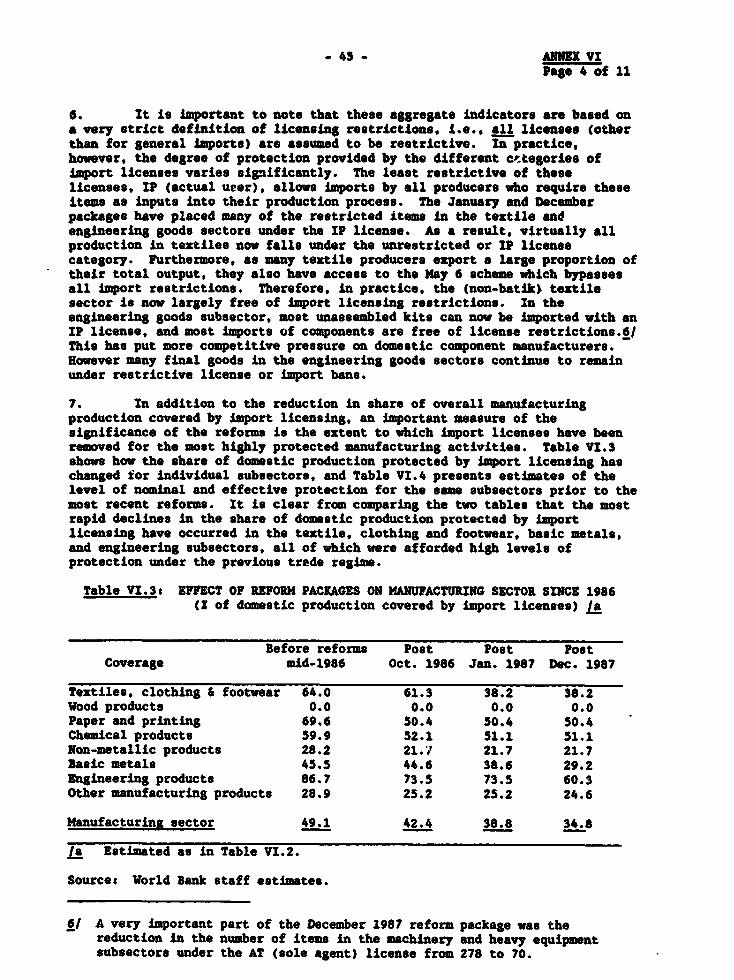

REPORT AND RECOMMENDATION

OF THE

PRESIDENT OF THE

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

TO THE

EXECUTIVE DIRECTORS

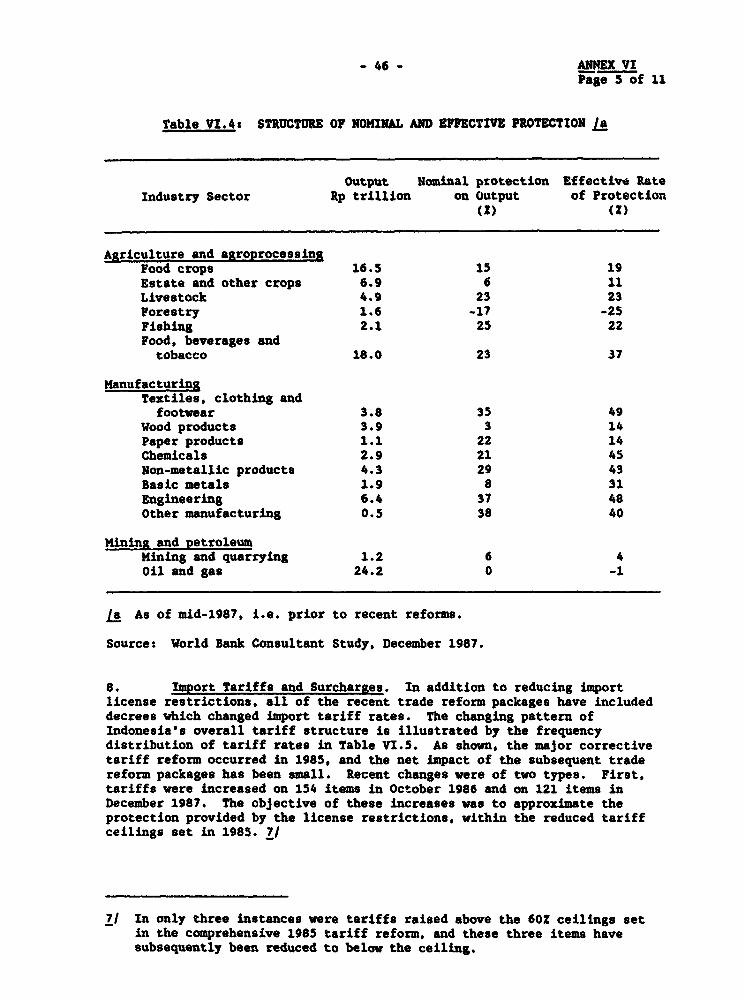

ON A

PROPOSED LOAN

IN AN AMOUNT EQUIVALENT TO US$300 MILLION

TO THE

REPUBLIC OF INDONESIA

FOR A

SECOND TRADE POLICY ADJUSTMENT LOAN

April 19, 1988

This document has a restricted distribution and may be used by recipients only in the performance oftheir ofricial duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

Currency Unit G RupiahUS$1.00 - Rupiah (Rp) 1,660Rp 1 million - US$602

GOVERNMENT OF INDONESIA FISCAL YEAR

April 1 - March 31

SYSTEM OF WEIGHTS AND MEASURES

Metric

ABBREVIATIONS AND ACRONYMS

BAPPENAS - National Development Planning AgencyBKPM - Investment Coordinating BoardBULOG - Badan Urusan Logistik (The National Logistics

Agency)CCCN - Customs Coordination Council NomenclatureCBU - Completely built-upCKD - Completely knocked-downEKUIN - Coordinating Ministry for Economic MattersGOI - Government of IndonesiaIGGI - Inter-Governmental Group on IndonesiaIPEDA - Iuran Pembangunan Daerah (the old land tax)NTB - Non-tariff barrierO&M - Operations and maintenanceP4BM - Implementing agency for May 6 schemeREPELITA - National Five-Year Development PlanSBI - Central Bank certificatesSBPU - Private Sector Promissory NotesSGS - Societe Generale de Surveillance S.A.SOE - Statement of ExpenditureTIPSC - Trade and Industrial Policy Steering CommitteeTPAL I - First Trade Policy Adjustment LoanVAT - Value-added tax

Import License Categories:

AT - Ager. Tunggal (licensed agent)IP - Importir Produser (actual user)IT - Importir Tardaftar (approved trader)IU - Importir Umum (general importer)KS - PT Krakatau SteelPI - Produsen Importir (producer importer)TT - PT Tambang Timah

FOR OMCLIL USE ONLY

INDONESIA

SECOND TRADE POLICY ADJUSTMENT LOAN

Table of Contents

Page No.

LOAN SUMMARY *..........i i..........i.......... .......

It BACKGROUND ....... ....... to...... ... to..................*.... .*.....1

II. THE FIRST ADJUSTMENT PERIOD, 1982-85 .................. .... 1

III. THE SECOND ADJUSTMENT PERIOD, 1986-89 ................... . 3

A. The Initial Policy Response . ....................... 3B. Continuing Macroeconomic Adjustment ......... . 3C. Continuing Structural Adjustment ..................... 5

Trade Policy Reform ..................................... 5Industrial Deregulation and Foreign TnvestmentPolicies ... ...................................... 7

Financial Sector Reforms .... ... ... .... ... ..... . 8D. Assessment of Performance and Costs of Adjustment-.... 9E. Management of External Capital Accounts .............. 10

IV. THE REMAINING POLICY AGENDA AND PROSPECTS FOR A RECOVERYIN GROWTH . ........... to......... **................................ 11

A. Continuing Measures for Economic Stabilization ....... 11B. Further Structural Adjustment Reforms ........ ........ 12C. Growth Prospects .......... . .. . ............to... ....... ... . ..... . 13D. External Capital Flows and Debt Management ........... 15

V. BANK'S OPERATIONAL STRATEGY .... ....... . .................. . 16

VI. THE PROPOSED LOAN ................ .......... .. . 18

A. Loan History ......................................... 18B. Loan Objectives .... .................................. 19C. Loan Administration ........... ............... ........ 19

Disbursement ............... ...... ........ . 19Procurement ..................................................... 19Accounts and Audits ....................... .. ........... 20

D. Monitoring and Follow-up ... .............. ................ . 20E. Program Benefits and Risks ........ * ........ 20

VII. RELATIONS WITH IMF ..................... ............. ...... 20

VIII. RECOMMENDATION ........ ............... .. ... ............ 21

This document ha a rtdcted disibution and may be used by rfipints only in the perfonnameaof their offAcil dutiest ts contents may not otherise be discloed without Wodd Bank authorhatioj.

TABLES:

Table l Recent Economic Developments ............................ 2Table 2: Central Government Budget ............ .... *...... * 4Table 3s Effect of Reform Packages on Import Licensing Coverage

Since 1986 .... ............. ..... . .. .. .. ..... *.. *.*. **.*****.............*** 7Table 4: Medium-Term Projections ............ ..................... 14Table 5s Balance of Payments Projections ............... 15

ANNEXESs

ANNEX I s Key Macroeconomic Indicators ........................ . 22ANNEX II s The Status of Bank Group Operations in Indonesia ....... 25ANNEX IIls Supplementary Data Sheet .............. ** . ....... 29ANNEX IV s Government's Statement on Economic and Trade Policy .... 30ANNEX V s Policy Framework .... . ................. .. ... . .. 39ANNEX VI s Trade Policy Reforms and Industrial Deregulation ....... 42

HAP: IBRD No. 11038R1.

INDONESIA

SECOND TRADE POLICY ADJUSTMENT LOAN

Loan Summary

Borrower: Republic of Indonesia

Executing Agencies: Bank Indonesia and Ministry of Finance

Amount: US$300 million equivalent

Terms: 20 years, including 5 years of grace, at thestandard variable interest rate

Project Descriptions The proposed loan would: (a) support the substantialreforms, especially in the area of trade policy,undertaken by the Government of Indonesia (GOI)during 1987, and ensure that they are implementedwell; (b) assist GOI to bring about an earlyrecovery in economic activity consistent withexternal and domestic financial stability; and (c)maintain the policy dialogue on further reform,including the preparation of a medium-term plan fortariff rationalization. The loan of US$300 millionequivalent would finance general imports of goods tomeet part of Indonesia's near-term foreign exchangerequirements, while supporting GOI's commitment topromote the efficiency and longer-term viability ofthe economy. It is envisaged that further suchactions could form the basis for a subsequent loanin about a year.

Benefits and Risks: The adjustment measures taken by GOI over the pasttwo years will provide balance of payments andfiscal stability, in the face of lower oil prices,and help develop the non-oil economy over the mediumterm. In particular, the recent trade policy anddomestic licensing reforms represent substantialprogress in GOI's efforts to reduce long-standingdistortions in Indonesia's highly protectedindustrial structure; improve internationalcompetitiveness of non-oil exports; and increasepotential for foreign investment, especially inexport-oriented industries. In addition, greatertransparency and administrative simplicity has beenintroduced into Indonesia's trade regime. Theprincipal risk is that the far-reaching nature ofthe reforms could encounter domestic opposition asthey are implemented and extended. This risk isoffset by the positive response, especially of non-oil exports, to earlier reforms and GOI'sdemonstrated commitment to carry out difficult andsensitive policy measures.

- l, -

Eetlmated Disbursements US$300 million will be disbursed In FY89.

Economlc Rate ofReturns Not applicable.

#nraisal Reports None.

NapDt IBID No. 11038R1.

REPORT AND RECOHQENDATION OF TEE PRESIDENTO THE INTERNATIONAL BANR FOR RECONSTRUCTION AND DEVELOPMENT

TO TEE EXECUTIVE DITECTORS ON A PROPOSED SECOND TRADEPOLICY ADJUSTMENT LOAN TO THE REPUBLIC OF INDONESIA

1. I submit the following report and recommendation on a proposed SecondTrade Policy Adjustment Loan to the Republic of Indonesia for the equivalentof US$300 million. The proposed loan would have a term of 20 years, including5 years of grace, at the standard variable interest rate.

2. An economic report, entitled *Indonesia: Strategy for EconomicRecovery" (No. 6694-IND, dated May 5, 1987) was distributed to the ExecutiveDirectors in May 1987. Annex I gives selected economic indicators for thecountry.

PART I - BACKGROUND

3. During the 19709, the Indonesian economy grew at almost 82 per annum.This growth was supported by a rapid expansion of net oillLNG export earnings,which rose from US$0.6 billion in 1973174 to a peak of US$10.6 billion in1980181. In that year, oil/LNG accounted for 751 of export earnings and 702of budget revenues. Compared to many oil exporters, Indonesia used theseresources well, bringing significant improvements in education, health andfamily planning, and a rapid growth in agriculture, especially rice.Indonesia also maintained sound macroeconomic management and, following thePertamina crisis of the mid-1970s, a conservative external borrowing strategy.By the end of the decade, the current account of the balance of payments wasIn surplus and debt-service payments were below 132 of exports.

4. The sharp drops in oil prices in the 1980s and associated changes inthe international economy have drastically altered the economic environmentfor Indonesia. In response, the Government has made two types of policyadjustments. First, since 1982, the Government has adopted more austeremacroeconomic policies. In comparison to the efforts of many countries duringthis period, the Government's macroeconomic stabilization programs are widelyregarded as very successful. Second, the vicissitudes of the oil market andthe sharp decline in the real price of oil have led to a major and on-goingprogram to restructure the economy over the medium to longer term, so as toreduce Indonesia's heavy dependence on oil as a source of foreign exchange andbudgetary revenues. The key elements of this structural adjustment programinclude a range of measures to strengthen domestic resource mobilization,expand non-oil exports, and promote a more competitive and dynamic non-oileconomy.

PART II - THE FIRST ADJUSTMENT PERIOD. 1982-85

5. The first period of stabilization followed the weakening of the oilmarket in 1982, the onset of a worldwide recession, and the decline in theprices of several important primary exports (e.g., rubber, palm oil and tin).By 1982183, Indonesia's current account deficit had widened to US$7.2 billion(7.81 of GNP). In response, the Government initiated a broad-based adjustmentprogram, designed to maintain balance of payments and fiscal stability, whilereducing the economy's dependence on oil revenues. The competitiveness ofIndonesia"s non-oil exports was improved by a 282 devaluation of the Rupiah in

- 2 -

March 1983 followed by more flexible exchange rate management; and publicexpenditure was sharply reduced through the rephasing of many large projectsand cutbacks in budgetary subsidies. At the same time, the foundations of aprogram of structural adjustment were established: resource mobilization wasimproved following comprehensive financial and tax reforms; and majorefficiency improvements were made in customs, ports and shipping.l/

6. By 1985186, these measures had succeeded in restoring macroeconomicstability (see Table 1). The current account deficit declined toUS$1.9 billion (2.42 of GNP) in 1985186; and significant progress was made incontrolling inflation, which was brought below 5Z. These adjustments led toshort-term costs in the form of slower growth of output and incomes, reducedprivate and public investment, low rates of capacity utilization, and theemergence of financial problems among industrial enterprises. Problems in theindustrial sector were compounded by high and variable levels of protectionprovided by a proliferation of import licensing restrictions. Nevertheless,prior to the unexpected collapse of oil prices in 1986, Indonesia seemed tohave largely overcome its balance of payments and macroeconomic adjustmentproblems, and was set on a path that potentially would have restored stablegrowth to the economy.

Table 1: RECENT ECONOMIC DEVELOPMENTS /a

Actuals Est. Proiected1978-82 1982-85 1986 1987 1988 1989

Real growth rates (S p.a.)GDP 5.3 3.8 3.6 3.7 3.6 4.5Non-oil GDP 6.9 4.0 3.8 4.3 4.4 4.6- Agriculture 5.0 3.7 2.5 2.3 2.5 3.0- Industry 10.1 1.8 4.8 6.0 6.1 6.3- Services 9.4 7.4 4.3 4.8 4.7 4.7National income .. 2.2 -2.5 4.1 3.5 4.2Non-oil exports 10.5 17.2 2.8 25.3 13.1 7.9Non-oil imports 13.8 -10.7 -12.4 1.6 4.4 4.0

Ratios (S) JbBudget balance/GDP -4.0 -2.8 -5.0 -2.4Current accountIGNP -7.8 -2.4 -6.1 -3.1 -2.7 -2.2Debt service/exports /c 16.4 25.4 36.9 34.6 39.6 38.2Fixed investment/GDP 25.9 20.7 20.4 18.6 18.6 18.7

PricesOil price (US$/bbl) /b 32.9 25.0 12.5 17.0 16.0 16.0Terms of trade(1983/84-100) /b 109.3 93.3 62.6 69.3 68.1 67.9

Domestic inflation(2 p.a.) 13.9 8.4 9.1 9.3 5.0 5.0

la Balance of payments data are for fiscal years (starting April 1). Otherindicators are for calendar years.

/b For last year of multi-year periods.Ic Debt service excludes prepayments.

Source: Central Bureau of Statistics and World Bank staff estimates.

1/ More details on those measures are provided in paras. 5-9 of thePresident's Report for TPAL I (No. P-4429-IND, December 30, 1986).

- 3 -

FART III - THE SECOND ADJUSTMENT PERIOD, 1986-89

A. The Initial Policy Response

7. In 1986, the economy again suffered a series of setbacks. Averagecrude oil prices fell by almost one-half from US$25/barrel in 1985186 to belowUS$13/barrel in 1986/87. The loss of oil revenues was equivalent to one-thirdof both domestic budget revenues and merchandise exports. Indonesia sufferedfurther external shocks from the weakening of non-oil commodity prices and thesharp depreciation of the US dollar. Indonesia was vulnerable to the declineof the US dollar because its exports were mostly dollar denominated andbecause about 602 of its external debt was in appreciating currencies. Thesetrends led to a 34S deterioration in the terms of trade and a jump in thedebt-service ritio from 261 in 1985 to 372 in 1986. Although the Governmenthad been adjusti*%% appropriately since the first signs of a deterioratingexternal environcent in the early 1980s, nothing could have prepared theeconomy for the magnitude of the new external shocks. Nor could theGovernment afford to make up this loss through additional commercialborrowing, as the decline in oil revenues was unlikely to be transitory andIndonesia already had a large overhang of external debt.

8. Once again, GOI took timely actions to restore macroeconomicstability. These included: (a) the introduction of an austere Budget forFY86/87 with investment spending cut by one quarter in real terms; and (b) a311 devaluation of the currency on September 12, 1986. In addition, theGovernment broadened its program to restructure the economy over the mediumterm. The main emphasis was on a package of trade policy reforms designed tobuild on the reforms introduced in 1985. These new measures signalled theGovernment's intention to shift from non-tariff barriers (NTBs) to tariffs asthe primary instrument of import policy, and were supported by the first TradePolicy Adjustment Loan, appro,ved by the Executive Directors on February 3,1987 (Loan 2780-IND). ¶%e policy measures taken contained the current accountdeficit to US$4.2 ;.iiiion in 1986/87. Inflation was also curbed, withconsumer prices rising by only 92 in 1986. Although real GDP growth in 1986was remarkably strong at 3.62, national income fell due to the deterioratingterms of trade.

B. Continuing Macroeconomic Adiustment

9. A successful program of stabilization in Indonesia is likely to takeabout three years to restore internal and external financial stability (ifsupported strongly by official external capital). With this in mind, theGovernment has maintained its prudent approach to macroeconomic management. Asecond austere budget was adopted for 1987188, with ni increase in civilservice salaries and additional cuts in the public investment program.Although higher oil/LNG revenues, resulting from the strengthening of oilprices in 1987, and special assistance from the Inter-Governmental Group onIndonesia (IGGI) eased the budgetary situation somewhat in 1987/88, investmentexpenditure will be substantially lower than the previous year in real terms.As a result, the budget deficit declined to 2.42 of GDP from 5.02 of GDP in1986/87 (see Table 2).

-4-

Tablo 2s CENTRAL GOVERNMENT BUDGET(ip trillion)

Actuals Estimate Budget1984/85 1985186 1986/87 1987188 1988/89

Revenue and grants 19.0 18.9 16.8 20.3 22.0Oil/LNG taxes 13.4 10.7 6.3 9.7 8.9son-oil taxes 4.8 6.6 8.2 9.3 11.7Other 0.8 1.6 2.3 1.3 1.4

Current expenditure la 10.8 12.7 13.5 1S.8 15.4Interest on external debt 1.6 1.8 2.8 3.8 4.4Subsidies 1.5 1.1 0.5 1.5 0.5Other 7.7 9.8 10.2 10.5 10.5

Government savings 8.2 6.2 3.3 4.5 6.6

Capital expenditure 7.6 8.9 8.4 7.3 7.4

Overall balance 0.6 -2.7 -5.1 -2.8 -0.8Financed bys

- External loans (net) 2.4 1.8 4.2 2.5 0.8- Asset drawdown -3.0 0.9 0.9 0.3 0.0

Ratios (Z of GDP)Revenues and grants 21.3 19.8 16.4 17.3 17.1

- Oil/LNG taxes 15.0 11.2 6.2 8.2 6.9- Ron-oil taxes 5.4 6.9 8.0 7.9 9.1

Total expenditure 20.6 22.7 21.4 19.6 17.7Government savings 9.1 6.6 3.2 3.8 5.2Overall balance 0.7 -2.9 -5.0 -2.4 -0.6

la Routine expenditure adjusted to exclude amortization payments and toInclude both the fertilizer subsidy and the recurrent component ofdevelopment expenditure.

Sources Ministry of Finance and World Bank staff estimates.

10. The GOI also employed monetary policy to complement fiscal policy inrestraining domestic demand and curbing inflationary pressures. In 1987,monetary management was complicated by speculative pressures on the Rupiah.Z/

21 These pressures emerged towards the end of 1986 and intensifiedduring May-June 1987. Subsequently, with the reversal of capitalflows, net foreign assets of the banking system rose from US$9.4billion at end-June to US$11.1 billion at end-1987.

These pressures were met by a firm policy response, as the authoritiescountered the loss of foreign exchange by curbing domestic credit, allowingdomestic interest rates to rise and providing more flexibility in monetarymanagement. These measures succeeded in reversing capital outflows, allowingforeign exchange reserves to rise to more adequate levels and permitting theauthorities gradually to ease monetary policy to relieve some of the pressureon domestic interest rates. Overall, the expansion of domestic liquidity wastightly controlled in 1987, representing a continuation of the policies ofdomestic demand restraint in support of the etabilization program.

C. Continuing Structural Adiustment

11. In the first period of adjustment (1982-85), the Governmentimplemented policies to mobilize domestic resources (the financial and fiscalreforms of 1983) and launched a program of trade reforms (the maritime andtariff reforms of 1985). The latter program was reinforced by the secondround of trade policy reforms in 1986, which were supported by the first TradePolicy Adjustment Loan. Since 1986, the Government has intensified itsprogram of structural adjustmwnt bys (a) extending the program of trade policyreform; (b) beginning to deregulate industry; (c) relaxing policies governingforeign investment; and (d) extending its 1983 financial sector reforms. Theprimary objective of these reforms, in conjunction with the aforementionedmacroeconomic adjustment measures, is to raise economic efficiency and toincrease earnings from non-oil exports. It is this new set of measures thatwould be supported by the Second Trade Policy Adjustment Loan.

12. Trade Policy Reform. In general, the trade regime of the 19709 andearly 1980. was inward looking, promoting industrial investment with highprotection from imports. At the start of this decade, Indonesia's importregime was characterized by high and disparate tariff rates. Pressures:esu'ting from the slowdown of the domestic economy led to an increase of non-tariff barriers (NTBs) in the early 19808, in the form of import licensing.Recognizing the adverse effects of the trade regime on the cost competitive-ness of the economy, GOI undertook two major trade-related reforms during1985s first, an across-the-board reduction in tariffs which reduced the leveland dispersion of tariffs and lowered the ceiling from 225Z to 60X; and,second, a complete overhaul of customs, ports and shipping operations.Reductions in these distortions increased the relative importance of NTBs. Bythe end of 1985, more than 1,700 items (CCCN categories) were subject toimport licensing.31 These items accounted for over 402 of both total importvalue and traded domestic production. Although import licenses variedconsiderably in their degree of restrictiveness, by 1986, the import licensingsystem was the most important distortionary influence in the trade regime,contributing not only to the high level and variability of protection but alsofostering unproductive 'rent-seeking' behaviour.

31 Of the 1700 items, only 296 had a formal quota imposed. Inaddition, there were 24 products under import ban (includingautomobiles, motorcycles, televisions and radios as completelybuilt up units).

13. During 1986, GOI moved to the next stage of trade policy reformthrough a two-pronged approacht first, to insulate exporters from the adverseeffects of the import regime; and second, to begin to dismantle the importlicensing system. In May 1986, the Goveranent announced a package of measuresthat gave major exporters access to unrestricted and duty-free imports. TheMay 6 scheme was seen as a useful mechanism by which to help exportersovercome the cost raising effects of NTBs and high tariffs, until more directmeasures could be taken. In October 1986, following the 312 devaluation ofthe previous month, GOI embarked upon a more fundamental program of reforms.The intention was to initiate a phased program to reduce import licenses andmove towards an import regime based solely on tariffs. Under the Octoberpackage, import restrictions were removed altogether on 197 items, accountingfor 112 of all items and 19X of total import value previously restricted. Asa result, the shere of manufacturing production under import licensingdeclined from 49% to 42Z.41 These reforms have been implementedsatisfactorily. Over US$1 billion of imports have been processed under theMay 6 scheme and, although there have been some bureaucratic delays, therelaxation of import restrictions and lowering of tariffs resulted in a sharpincrease in the imports of these items.

14. GOI maintained the momentum on trade policy reform in 1987 throughtwo major packages announced on January 15, 1987 and December 24, 1987, and aseries of smaller policy actions. These measures, havet (i) continued theshift from import restrictions to tarifi based protection; (ii) adheredstrictly to the lower tariff ceiling in setting tariff rates on the productsremoved from NTB protection; (iii) taken initial steps toward tariffrationalization; (iv) broadened the scope of the system giving exportersaccess to inputs at internationally competitive prices; and (v) reducedremaining export restrictions. A detailed analysis of these recent tradereforms is presented in Annex VI of this report.

15. The January and December packages of 1987 (which are being supportedby the Second Trade Poliy Adjustment Loan) marked substantial progress inGOI's primary objective of moving away from a trade regime dependent on NTBs.The combined impact of the January and December packages has been the removalof an additional 342 items from license control, accounting for 20? of allitems and 23Z of total import value previously restricted. More importantly,the share of manufacturing production protected by import licensing declinedsubstantially from 42? at the end of 1986 to 352 at the end of 1987 (seeTable 3). As shown in Annex VI, the reduction in NTBs has been concentratedin activities with the highest effective rates of protection. In addition tothe removal of import licensing restrictions, the January and Decemberpackages have relaxed some of the remaining restrictions, particularly in thetextile and engineering goods sectors, by placing them under the IP (actualuser) license category. This is the least restrictive license, and allows allproducers who require these items as inputs to import them freely. As aresult of the measures taken during 1987, virtually all production in textilesfalls under the unrestricted or IP license category. Given, in addition, therelatively easy access of exporters to the May 6 scheme, the textile sector isnow largely free of import licensing restrictions. Similar progress has beenmade in many branches of the engineering goods sector, although several finalgoods remain under restrictive license or import bans.

41 In addition, there was a significant relaxation of licensing foran additional 105 items.

- 7 -

Table 3: EFFECT OF REFORM PACKAGES ON TMPORT LICENSING COVERAGE SINCE 1986

Before After After AfterShare Covered Under Reforms Oct. 1986 Jan. 1987 Dec. 1987Import Licensing (X) (mid-1986) Reform la Refoms lb Reforms lb

Import Items 31.4 27.9 25.7 21.7Value of Imports 42.9 34.9 31.5 25.2Manufacturing Production 49.1 42.4 38.8 34.8

la Measures supported under TPAL I.b Measures supported under the proposed loan (TPAL II).

Sources Annex VI, Table VI.1

16. The second main element of the 1987 trade reforms related to tariffpolicy. Tariff adjustments during this stage of trade reform have aimed atconforming to the reduced level and dispersion of the new tariff structureIntroduced in 1985. Under the two trade reform packages of 1987, tariffs for121 items were adjusted upwards and tariffs for 178 items lowered. Temporarysurcharges were also imposed on 51 import items. The increases in tariffscompensated for the effects of the removal of import licensing restrictions,but remained within the lower tariff ceilings set in 1985. The reductions intariffs in the January 1987 package (as in the earlier October 1986 package)concentrated on products not locally produced, and were intended to offset thecost-raising effects of tha September 1986 devaluation. The Decemberreductions went beyond this limited objective by reducing tariffs on somedomestically produced items that were removed from import license restrictionin earlier decrees, thereby marking an important beginning towards the nexttrade reform objective of further tariff rationalization.

17. Lastly, the December package has made more substantial progress thanthe previous two packages in eliminating some of the direct impediments toexports. The need to obtain a special export license was abolished; severalexport bans and quotas have been removed; and access by exporters to the May 6scheme has been broadened. These reforms will reduce the impediments toexporters by eliminating redundant regulations. Furthermore, they willsubstantially reduce the anti-export bias of the trade regime for existingexporters, thereby increasing the relative profitability of exports andbolstering the export drive.

18. Industrial Deregulation and Foreign Investment Policies. Progress intrade policy reform has highlighted the need for complementary measures onindustrial deregulation. The performance of the industrial sector has beenhindered by a multitude of domestic regulations and licensing procedures,particularly investment and capacity licensing. Moreover, additionalregulations controlling the activities of foreign investment companies haverestricted the flexibility of these firms and reduced the attractiveness of

Indonesia to foreign investors. Recognizing these impediments to privatesector growth and investment, the Government has taken a series of steps tosimplify and relax the regulatory framework (a more detailed analysis of thesemeasures is presented in Annex VI. Section B).

19. A start was made in 1985 when the investment process was streamlined.In 1986, fields of investment open to both foreign and domestic companies werespecified more clearly and the number of areas open to private foreign anddomestic investment was expanded substantially. Moreover, foreign investmentcompanies were given greater access to domestic capital and financialinstitutions, and domestic ownership requirements were eased.

20. The Government's drive to revitalize the private sector and encourageforeign investment gained momentum during 1987. A number of major steps weretaken to relax the investment and capacity licensing system and ease foreigninvestment regulations. As a result of measures taken in June, firms are nowallowed to increase production by up to 30S of their licensed capacity withoutrequiring new investment approval. More significantly, firms have beenpermitted to diversify production within much broader product categories,thereby Improving the operational flexibility of firms and promoting greatercompetition. Furthermore, the requirements for investment licenses werestreamlined and additional fields of investment opened to private domestic andforeign investors. The December package included a series of measures torelax foreign investment regulations: domestic ownership requirements wereeased significantly; restrictions prohibiting foreign-owned companies frommarketing Indonesian export goods were removed; foreign firms are now allowedto purchase domestic inputs without restriction; and rules regarding thehiring of expatriate personnel were relaxed. These steps have addressed keyconcerns expressed by foreign investors in Indonesia and will reducedifferences in treatment between foreign and domestic firms. Together withthe broader regulatory measures, they have removed many of the disincentivesto foreign investors and have improved substantially the climate for foreigninvestment in Indonesia.

21. Financial Sector Reforms. In June 1983, GOI launched a comprehensivereform of the financial sector, which included a liberalization of mostinterest rate controls on state bank deposits, the elimination of creditceilings for all banks, and a reduction in the number of programs qualifyingfor new Bank Indonesia liquidity credits. These reforms have had a far-reaching impact on the financial system, successfully increasing domesticresource mobilization, promoting greater competition and market orientation,and improving the allocation of credit. Over the past three years, BankIndonesia has also introduced a range of new monetary instruments (e.g., SBIs,SBPUs)51 to improve monetary management and encourage development of an activeinterbank money market. In July 1987, an auction system was introduced todetermine SBI and SBPU volume and discount rates, which, in combination withother monetary measures, helped ease the speculative pressure against theRupiah.

22. Concerns about the longer-term effect of high interest rates onInvestment and the financial viability of enterprises, and the relative lackof term transformation in the banking system, led GO0 to undertake specific

5/ 8BI are Central Bank certificates and SBPUs are private sectorpromissory notes held by banks, and rediscounted by the CentralBank.

- 9 -

measures in December 1987 to strengthen the role of equity markets. First, toincrease the supply of securities, listing requirements on the Jakarta StockExchanges which now lists only 24 companies with a market capitalization ofabout US$60 million, were simplified through the elimination of all but threepieces of essential documentation. Second, supportive measures wereintroduced to improve the institutional framework (e.g., pricing mechanisms)and the operation of capital market institutions (e.g., underwriters,guarantors, stock traders). Third, G00 created an over-the-counter (OTC)market to enable smaller, less well-established companies to mobilizeinvestment requirements through the capital market. Finally, in an attempt tostrengthen the demand for securities, 001 will encourage the issue of bearershares and will allow foreign investors to purchase shares in the OTC market.

D. Assessment of Performance and Costs of Adiustment

23. The combination of austere fiscal and monetary measures has beenextremely successful in limiting the inflationary effects of the September1986 devaluation. Despite the magnitude of the devaluation (452 in domesticcurrency terms), inflation in 1987 was contained at less than 10. Moreover,exchange rate policy during 1987 has maintained stability in the Rupiah/US$rate. As a result, not only have the gains of the September 1986 devaluationbeen fully preserved, but the real exchange rate has depreciated subsequentlyby an additional 82, further strengthening competitiveness.

24. In response to the real exchange rate adjustment, as well as therecent deregulation measures, non-oil exports have increased substantially.Currently, non-oil exports are running at more than US$900 million per monthand are estimated to total US$9.5 billion in 1987188. This represents a 412increase in nominal terms and a 252 increase in real terms over 1986187.'hile increases have occurred in Indonesia's traditional exports (e.g., woodproducts, palm oil), about 65Z of this increment has been contributed by arapidly expanding and diversifying base of manufactured exports. This strongnon-oil export performance and the increase in oil earnings in 1987/88permitted a nominal increase in non-oil imports, while paring down the currentaccount deficit from US$4.2 billion in 1986/87 (6.1S of GNP) to US$2.0 billionin 1987/88 (3.1S of GNP).

25. Given the severity of the macroeconomic adjustment, GDP growth,though modest, has been surprisingly robust. Non-oil GDP growth averagedabout 41 in 1986 and 1987. The momentum for growth in 1987 has come from theindustrial sector, linked to export expansion, as the agricultural sector,particularly rice, has been adversely affected by drought. The continuationof economic growth under difficult circumstances reflects the promptness ofthe macroeconomic policy response, and the positive results from thestrengthening of competitiveness and improvement in the investment climate dueto deregulation. A noteworthy element has been the strong recovery in privateinvestment. Approvals of domestic investment by the Investment CoordinatingBoard (BKPM) jumped more than 1301 in rupiah terms in 1987, whereas foreigninvestment approvals rose by 761 in dollar terms, in both cases directedprimarily towards export activities. The surge in private investmentapprovals reflects renewed investor confidence and, in creating new exportcapacity, augurs well for the future of non-oil export earnings.

26. There has also been some recovery in incomes during 1987, based onthe expansion of domestic output and an improvement in the terms of trade.Zven so, in per capita terms, national income at the end of 1987 will still be

- 10 -

lower than in 1981. GOI has acted to contain the social costs of this incomeloss by: (a) giving priority to public spending on agriculture and localinfrastructure; (b) promoting non-oil exports, which are generally more labor-intensive; and (c) adopting a more supportive attitude toward activities inthe informal sector, particularly in urban areas. For example, the share ofagriculture and regional development programs in development expenditure wasincreased from 18.3X in 1985/86 to 26.21 in the 1988189 budget. Socialprograms were also protected, with the share of education, health and urbanservices remaining flat at about 20S, although the level of absolute cuts hasbeen substantial.

27. While slower growth in domestic demand and greater import competitionhave affected some activities, broad-based export growth and the recovery ofprivate investment have had a salutary effect on employment growth. Many ofthe fastest-growing export items--including agricultural products, textilesand garments--are labor-intensive and important employment-generatingactivities. Nevertheless, despite these positive factors which have moderatedthe social costs of adjustment, the Government remains concerned aboutemployment and income growth as Indonesia's labor force is expected to expandby about eight million over the next five years.

28. An additional area of concern in this adjustment period is theeffects of devaluation and high real interest rates on the financial positionof firms. Although there is little overt evidence of a rise in bankruptciesor widespread financial stress, the portfolios of some financial institutionsremain weak, and will require careful monitoring to ensure that the financialsystem can adequately support the adjustment process.

E. Management of External Capital Accounts

29. Despite the dramatic reduction in the current account deficit toabout US$2 billion, Indonesia has had to contend with a substantial increasein amortization payments in 1987/88 due both to the large share of its debt inappreciating currencies, and to the rising repayment obligations resultingfrom the increase in commercial borrowing in the early 1980s. Indonesia'sforeign exchange requirements for 1987/88 amounted to some US$7.3 billion, tofinance the current account deficit, amortize loans and support a rebuildingof foreign exchange reserves. These requirements were largely met bydisbursements of some US$5.9 billion of public MLT loans. An important partof the financing arrangements for 1987/88 was the extraordinary financingprovided by a number of the IGGI members--some US$1.3 billion of grossdisbursements--most notably the disbursements from the first Trade PolicyAdjustment Loan, the local cost financing of World Bank projects by Japan EXIMBank and extra program aid and local-cost financing from other donors. InApril 1987, Indonesia also obtained US$606 million from the IMF's CompensatoryFinance Facility (CFF). As a result of the impressive recovery of exports,the strong support from IGGI members, and restrained use of commercial credit,Indonesia's debt-service payments also stabilized at 352 of export earnings in1987, while net official reserves stood at about US$5.8 billion at end-December 1987, equivalent to 4.9 months of imports. This relatively highlevel of reserves is considered appropriate, given Indonesia's open capitalaccount and the need to ride out occasional episodes of speculation.

- 11 -

PART IV - THE REMAINING POLICY AGENDA AND PROSPECTS FOR A RECOVERY IN GROWTH

30. Adjustment in Indonesia is proceeding well. Substantial progress hasbeen made in reducing external and internal imbalances. Moreover, exchangerate depreciation, trade reforms and industrial deregulation have strengthenedcompetitiveness, reduced production costs and improved allocative efficiencyin the economy leading to a sharp increase in exports and a strong revival ofprivate investment. Nonetheless, the lower price of oil and the steepincrease in debt service suggest that stabilization efforts must continue toreduce fiscal and external deficits to sustainable levels during the next twoyears.

31. At the same time, investment must be maintained at its current rateand eventually increased to support the export drive and to provide the basisfor economic recovery. Over the medium term, the non-oil economy must grow atleast 52 per annum to absorb the growing labor force and permit a meaningfulreduction in the level of poverty. This will require policies that continueto restructure the economy while stimulating investment. Since much of themomentum for growth will come from export expansion and improvements ineconomywide efficiency, a strategy of growth with adjustment also will providethe best means to protect and improve the creditworthiness of the economy.Improved domestic resource mobilization and non-oil export growth willsteadily close internal and external resource gaps, providing the basis forgrowth without recourse to special external support.

A. Continuing Measures for Economic Stabilization

32. The two key constraints faced by Indonesia over the near to mediumterm are the low and uncertain price of oil and the large overhang of externaldebt. The price of crude oil is projected to remain at $16/barrel (in nominalterms) through 1990, so that net oil earnings could remain depressed for theremainder of this decade. Moreover, Indonesia faces high debt service becauseof a bunching in its debt obligations. These two factors will continue to putpressure both on Indonesia's external balance, through lower oil exportearnings and rising interest and amortization payments, and on internalbalance, through lower oil/LNG tax revenues and the need to devote a risingproportion of current expenditures to interest payments.

33. The restoration of internal and external financial stability thuswill require continued domestic austerity for another year or so, evenassuming no further serious deterioration in oil prices or the internationaleconomic environment. The key elements of the macroeconomic program ares(a) tight expenditure management to reduce the budget deficit; (b) carefulscrutiny of the public investment program to maximize returns from limitedresources; (c) supportive monetary policies to restrain aggregate demand andcurb inflationary pressures; and (d) timely steps to ensure that thecomi;etitive gains from the real exchange rate adjustment are preserved.

34. These objectives are clearly enunciated in the Government's PolicyStatement (Annex IV). GOI has indicated its strong commitment to maintain aprudent fiscal and monetary stance. The recently announced Budget for 1988/89calls for further restraint in both current and capital expenditures. For athird year in a row, the Government has decided to freeze civil service

- 12 -

salaries, and real capital spending Le projected to fall. Seun if some budgettargets are not realized, the budget deficit is projected to decline furtherduring the 1988189 fiscal year. GOI will also focus on the composition of thepublic investment program, giving priority tot (a) the completion of ongoingprojects; (b) counterpart funds for foreign-aided projects; (c) projectsserving equity and employment objectives; and (d) funding of operating andmaintenance (O&M) expenditures. As a result, there will be very little scopefor new projects, and many locally-funded projects have already beencurtailed. These expenditure priorities are appropriate to the current stageof macroeconomic adjustment.

35. Indonesia's competitive exchange rate has been one of the primaryfactors accounting for the strong performance of non-oil exports in the pastyear. The Government remains committed to the present foreign exchangesystem, including the open capital account. In its Policy Statement, theGovernment has emphasized that exchange rate and supporting macroeconomicpolicies will be geared to maintaining the competitiveness of Indonesia's non-oil exports, taking account of price and exchange rate movements in tradingpartners and competitor countries.

B. Further Structural Adjustment Reforms

36. A recovery in economic growth to around 52 per annum by the beginningof the 19908 is critical to Indonesia's employment and poverty alleviationneeds as well as for the long-term viability and creditworthiness of theeconomy. This suggests that the structural adjustment program must bevigorously pursued to set the stage for more rapid growth. The next steps insuch a program must center around further improvements in policies for:

o domestic resource mobilization;o the trade incentive regime;o the industrial regulatory framework; ando the financial sector.

37. Improved domestic resource mobilization over the next few years willprimarily depend on non-oil tax revenues and the performance of publicenterprises. Indonesia has made major strides in raising non-oil tax revenuessince the 1983 tax reform. GOI must now mount a concerted effort to maintainthis momentum, based primarily on better tax administration.6/ Steps havealso been taken to contain investment by public enterprises. Tight controlhas been kept on utilization of non-concessional import-related credits since1984185 and equity participation in public enterprises funded through theBudget has been held to a minimum. With IMP assistance, a preliminaryconsolidation of the financial accounts for 135 public enterprises wascompleted in January 1988. The financial position of a large number of publicenterprises remains weak, and constitutes a potential drain on domesticresources. The Government is undertaking a review of the financialperformance of all public enterprises, to identify potential candidates for

61 Specific measures to improve tax administration as well as otheractions to raise non-oil tax revenues are discussed in therecently completed World Bank study on "Issues in Public ResourceManagement", Report No. 7007-IND, March 11, 1988.

- 13 -

rehabilitation, merger or divestiture. As noted in the Policy Statement, theGovernment intends to take appropriate action in this area in the near future.The Government also plans to review the regulatory framework, with theobjective of improving the efficiency and operating performance of publicenterprises over the medium term.

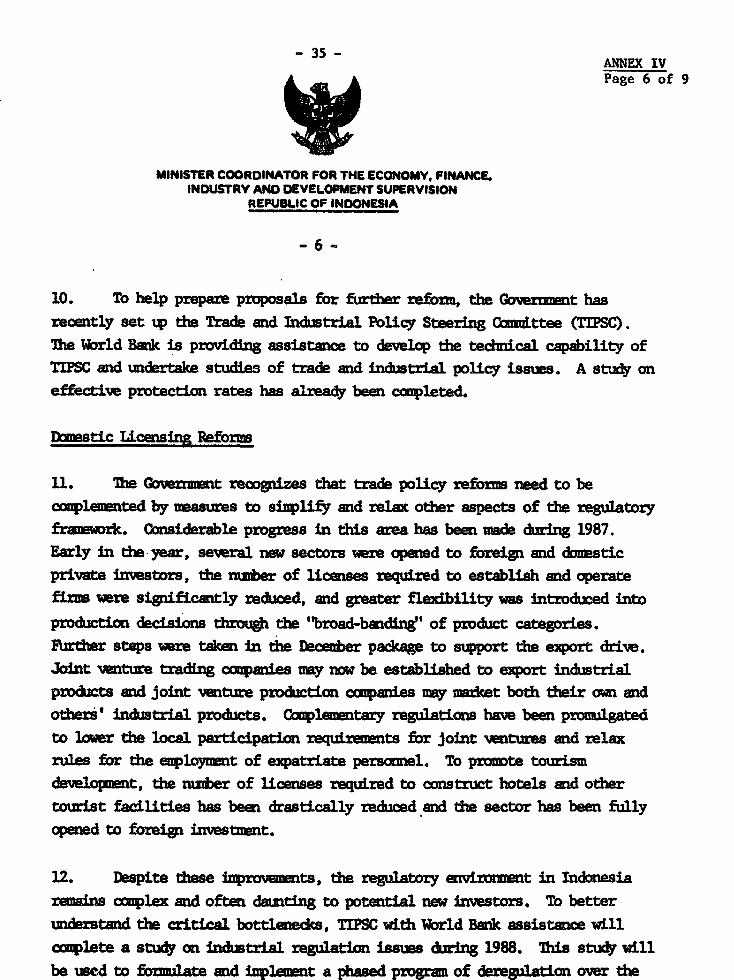

38. In the case of the trade incentives regime, the Government'sobjective is to eliminate gradually all NTBs, except on a small group ofproducts that are harmful to health, strategic to national defense or involvespecial economic or social considerations. As the earlier discussionindicates, steps to reduce the role of import licensing are now well underway.The next step of trade reform is to maintain this momentum through a furtherelimination of import licensing, especially in areas where such restrictionsare still important and provide high protection to domestic production. Overthe medium term, it will also be necessary to rationalize the tariff structurein erder to reduce excessive and disparate protection. A start has alreadybeen made through the tariff reductions announced in December 1987 on itemspreviously removed from import license restrictions. To help analyze tradepolicy issues and prepare proposals for further reforms, a Trade andIndustrial Policy Steering Committee (TIPSC) has been recently establishedwithin GOI. As an input to the work of TIPSC, the Bank has financed a studyon effective protection (which was completed in December 1987) and furtherlong-term technical assistance under ongoing Bank projects.

39. The industrial deregulation measures taken during 1987 are a welcomedevelopment and complementary to the trade policy reforms. Additionalmeasures will, however, be needed to simplify further the regulatory frameworkand to reduce the scope of industrial licensing. A first step is to ensurethat the 'broad-banding' measures introduced in 1987 are implemented well, andthat additional areas are opened to domestic and foreign private investment.Preparatory work to identify further steps in the deregulation process isbeing undertaken by TIPSC, and Bank staff are working with TIPSC on a study ofIndustrial regulations. Xey areas of focus would be investment and capacitylicensing, domestic content programs, regulations affecting domestic trade,and foreign investment policies.

40. An additional area of concern is the capacity of the financial systemto support the process of economic restructuring and recovery. The cost andavailability of credit, particularly for long-term investment funds, is apotential constraint, more so for newer export-oriented and small-scale firms.At the same time, segments of the corporate sector are facing financialdifficulties, as a result of the sluggish economy and the cost impact ofdevaluations in 1983 and 1986. Steps to address these problems are underway,but a more systematic review is needed of the current financial situation andof the market and institutional constraints that impede restructuring and newinvestment. In particular, careful attention must be paid tos (i) theportfolio problems of commercial banks and the effects of non-performing loanson intermediation costs to new borrowers; and (ii) the development of newinstruments that make term financing more widely available to investors.

C. Growth Prospects

41. With continued successful implementation of the stabilization programand further progress in structural reform, the outlook over the next two yearsis for a recovery in the GDP growth rate to 52 per annum by 1990. A recoveryFi agricultural production for domestic and export markets and further rapid

- 14 -

increases in industrial exports are expected to provide the impetus for thehigher GDP growth. Non-oil exports, which grew by 251 in volume terms in1987, are expected to expand on average by 101 per annum over the next twoyears. Much of this export growth has come from using existing capacity inresponse to the sharp Improvement in relative profitability of exportactivities. Sustained growth in exports over the medium term will requiresubstantial additional investment in new productive capacity. In the case oftree crops, there has already been a major expansion in plantings in the 1980sthat will lead to further increases in exports in coming years. In the caseof industrial exports, there is substantial evidence in the current pattern ofloan approvals by domestic banks (for example, under the Export DevelopmentProject, Loan 2702-IND, approved in 1986) and direct foreign investmentapprovals, that a build up in export capacity is already underway.

Table 4s MEDIUM-TERM PROJECTIONS la

Actual Estimate Projected1986 1987 1988 1989 1990 1990-95

Real growth rates (2 p.a.)GDP 3.6 3.7 3.6 4.5 4.9 4.5Non-oil GDP 3.8 4.3 4.4 4.6 5.0 5.7- Agriculture 2.5 2.3 2.5 3.0 3.5 3.5- Industry 4.8 6.0 6.1 6.3 6.8 8.3- Services 4.3 4.8 4.7 4.7 5.1 5.7National income -2.5 4.1 3.5 4.2 5.0 5.7Non-oil exports 2.8 25.3 13.1 7.9 6.1 5.8Non-oil imports -12.4 1.6 4.4 4.0 6.2 7.3

Ratios (2)Current account/GNP -6.1 -3.1 -2.7 -2.2 -1.6 -0.3/bDebt service/exports /c 36.9 34.6 39.6 38.2 35.3 22.4/bFixed investmenttGDP 20.4 18.6 18.6 18.7 19.2 23.2/b

PricesOil price (US$Ibbl) 12.5 17.0 16.0 16.0 16.0 28.1/bTerms of trade (1983/84-100) 62.6 69.3 68.1 67.8 67.9 84.7/bDomestic inflation (2 p.a.) 9.1 9.3 5.0 5.0 5.0 5.0

La Balance of payments data are for fiscal years (starting April 1). Otherindicators are for calendar years.

Jb For 1995./c Debt service excludes prepayments.Source: Central Bureau of Statistics and World Bank staff estimates.

42. Although private investment is already beginning to rise, theGovernment's program of fiscal restraint means that public investment cannotbe expected to recover before about 1990. Successful implementation of

- 15 -

measures to improve domestic resource mobilization in the public sector wouldlay the foundations for a recovery in public investment by that time, whenprudent expansion in public investment would contribute to faster growth.Priorities for increased levels of public investment would be in services foragricultural and rural development, basic infrastructure, and human resourcedevelopment programs in education and health.

D. External Capital Flows and Debt Management

43. The growth of non-oil exports and the improvement in domesticresource mobilization will provide the underpinnings for rapid sustainablegrowth in the 1990s. With a continuing conmitment to current policies, thecurrent account deficit is projected to decline to abou'; 1.62 of GNP by1990/91 and 0.3X by 1995196 (Table 4). These deficits would require a levelof caipital inflows that would be well within the limits of what Indonesiashould expect from official and private sources while maintaining prudent debtmanagement policies.

Table 5: BALANCE OF PAYMENTS PROJECTIONS(US$ billion)

Estimate Projections1987188 1988/89 1989/90 1990/91 1995/96

Oil/LNG earninas (net) 3.7 3.4 3.4 3.6 6.3Exports 8.4 8.1 8.6 9.0 14.2Payments -4.7 -4.7 -5.2 -5.4 -7.9

Non-oil earnings (net) -5.7 -5.3 -5.1 -4.9 -6.7Exports 9.5 11.2 12.5 14.0 24.3Imports -11.7 -12.6 -13.5 -14.8 -26.1Services (net) -3.5 -3.9 -4.1 -4.1 -4.9

Current account balance -2.0 -1.9 -1.7 -1.3 -0.4

Public MLT loans (net) 2.0 1.9 1.8 1.4 0.5Disbursements /a 5.9 6.4 6.4 6.0 5.5Amortization -3.9 -4.5 -4.7 -4.6 -5.0

Other capital (net) lb 1.4 0.7 0.8 0.7 1.3Use of net foreign assets -1.4 -0.7 -0.8 -0.9 -1.4

La Includes special assistance from IGGI members in the form of program aidand local-cost financing.

Lb Includes direct foreign investment and private borrowing.

Source: World Bank staff estimates.

- 16 -

44. Over the next two years, however, Indonesia will require additionalspecial assistance -- in the form of untied and conceesional fast-disbursingaid -- to support the adjustment in the balance of payments and the Budget tolower oil prices and adverse exchange rate changes. Program aid and local-cost financing provide free foreign exchange for the balance of paymentsduring the adjustment period. For the Budget, program aid has the addedadvantage that it can be used flexibly to finance all expenditures related toproject implementation (e.g., land acquisition) and project effectiveness(e.g., O&M, or tertiary canals for an irrigation system). Without thissupport, import and investment levels would be further constrained, therebyadversely affecting economic growth, the non-oil export effort and medium-termdevelopment prospects. This assistance will also provide an important signalto world financial markets that the IGGI members support the Government'sadjustment program and have confidence in Indonesia's economic prospects. Atthe same time, the provision of special assistance has to be seen as atemporary expedient, matched by the Government's efforts to improve non-oilexport performance and public resource mobilization. As the external anddomestic financing gaps are narrowed, special assistance can and should bephased out.

45. While Indonesia's debt burden has risen rapidly in dollar termslargely because of the effects of the dollar depreciation, its debt structureis relatively favorable with a high proportion of concessional and long-termdebt. Moreover, its debt burden is projected to grow much more slowly overthe medium term than in the past several years. A key indicator ofcreditworthiness is the ratio of debt to exports, which has risen sharplysince 1984, from 127X to 2512 at end 1986, because of the decline of oilprices and the depreciation of the US dollar. However, as a result of thestrong non-oil export performance, this ratio declined to 242? in 1987 despitethe adverse effects of the US dollar depreciation on the level of debt. Theratio is projected to decline steadily in the future, reaching 1362 in 1995.The debt service ratio which rose to 372 in 1986, is now projected to peak atclose to 401 in 1988, and then decline to 352 by 1990 and 222 by 1995.

PART V - BANK'S OPERATIONAL STRATEGY

46. Since 1983, the Bank's strategy in Indonesia has been to supportadjustment of the economy to lower oil revenues through maintenance ofmacroeconomic stability and a transition from oil-dependency to a morediversified and industrialized economy. The Bank has maintained a close andconstructive dialogue with the Government on emerging adjustment issues andthe design of suitable responses, including those supported by this loan. Inour policy discussions with the Government and our analytical work, there hasbeen increased emphasis on macroeconomic adjustment and key issues ofstructural reform such as rationalization of the trade regime, industrialderegulation and reform of pricing and other policies to enhance resourcemobilization and allocation. The strategy has been pursued in diverse ways,ranging from the preparation of major studies, including one on PublicResource Management, through major restructuring of existing operations, togreater emphasis in new projects on cost recovery, operation and maintenanceof existing facilities, and sector-specific policy and institutional changesto support increased efficiency and decentralization. The Bank has alsoprovided direct lending support for the Government's adjustment effortsthrough the first Trade Policy Adjustment loan, and has played an importantcatalytic role in mobilizing special assistance from other donors -- which isa critical requirement for the success of the adjustment program.

- 17 -

47. During the next three years, the Bank will continue to support theGovernment's adjustment program, with a view to reviving investment andpromoting the resumption of strong economic growth. In volume terms, theBank's lending program is expected to contribute one-fifth of Indonesia'sgross capital requirements and to serve as an important catalyst in attractingfunds from other agencies, including fast-disbursing assistance (such as theproposed loan) to relieve balance of payments pressures. To allow for exportgrowth to continue, Bank lending will be concentrated in two sectors: industryand agriculture.

48. In the industrial sector, the Bank hopes to achieve three objectives.Pirst, it will foster GOI's efforts to deregulate trade and industry, and toestablish appropriate incentives for investment in manufacturing industry,through a general policy dialogue and related loans, of which the proposedoperation would be the second. Subsequent loans may support furtherderegulation of trade and industry, as well as financial sector reforms.Second, the Bank will assist firms directly to respond to changed incentivesthrough a series of industrial restructuring operations, under whichparticular subsectors (textiles, pulp and paper, engineering, wood processingand, possibly, electronics, pharmaceuticals, agro-industry and packaging) willbe aided successively with technical assistance and finance, as appropriateincentive frameworks for each subsector are developed and implemented. Andthird, the Bank will support firms with substantial employment and exportpotential that are currently unable to secure financing on appropriate terms.Employment generation will be the focal point of a proposed Small and MediumIndustrial Enterprise Project, and export growth, of a second ExportDevelopment Project, under which term credit at market rates will be madeavailable to firms that might otherwise have little access to investmentfinance.

49. In agriculture, with its importance for incomes and employment, foodsecurity and exports, Bank assistance will focus on raising the efficiency ofproduction and farming systems, maintaining self-sufficiency in staple foods,and expanding exports. Our strategy will address issues of incentives, costrecovery and institutional development, particularly in sector planning andpolicy analysis, research management, extension services, and credit deliverymechanisms. It will involve specific programs and projects to achievebalanced regional development, reach specific target groups (mainly the ruralpoor and women), and promote sustainable development through efficient use ofresources and conservation and protection of the environment.

50. To support industrial and agricultural growth, the Bank's programwill continue to stress the improvement of infrastructure, education andhealth and family planning services. As mentioned above (para. 46), there hasalready been increased emphasis on the rehabilitation and maintenance ofexisting facilities in recent operations (such as the Urban Sector Loan,Irrigation Subsector Loan and Second Rural Roads Development Project). Thisemphasis will continue, while Indonesia's resource position remains tight,until it becomes possible to expand capacity. In transportation, the Bank isfocusing on efficiency improvements in the maritime sector and on improvingthe national network of highways and rural roads. In urban development andwater supply, efforts are being made to strengthen local government andregional enterprises, in order to minimize demands on the Central GovernmentBudget and decentralize the responsibility for addressing basic needs.

- 18 -

51. Progress in poverty alleviation has slowed considerably as a resultof the macroeconomic difficulties facing Indonesia since 1983. Compared withan average growth of 6.2Z per annum between 1971 and 1984, real per capitaconsumption is estimated to have declined by about 1? per annum between 1984and 1987. A resumption of investment and strong economic growth, along thelines described earlier In this report, should help to reverse this situationagain. In the meantime, Government programs of agricultural development,transmigration, educational services, urban development (water supply,sanitation, housing and transportation) and health and related social serviceswill remain important in cushioning the poor from the full costs of economicadjustment. During the last five years, just over half of the Bank's lendingprogram (522) has supported these key Government programs, and about 30X oftotal lending is estimated to have had a direct Impact on people below thepoverty line.

52. At the same time, there has been increased recognition of theenvironmental aspects of growth and adjustment in Java and the Outer Islands.increasingly, therefore, the Bank has been exploring ways and means ofassisting the Government to ensure more sustainable growth. To help theGovernment develop an appropriate strategy, the Bank is preparing a study ofselected environmental issues (including land and water use on Java, forestrymanagement on the Outer Islands, and industrial pollution on Java). Theresults of this initial review will be discussed at the IGGI Meeting In June1988. Future Bank projects will deal increasingly with issues of water supplyand quality on Java and better land use on the Outer Islands.

PART VI - THE PROPOSED LOAN

A. Loan History

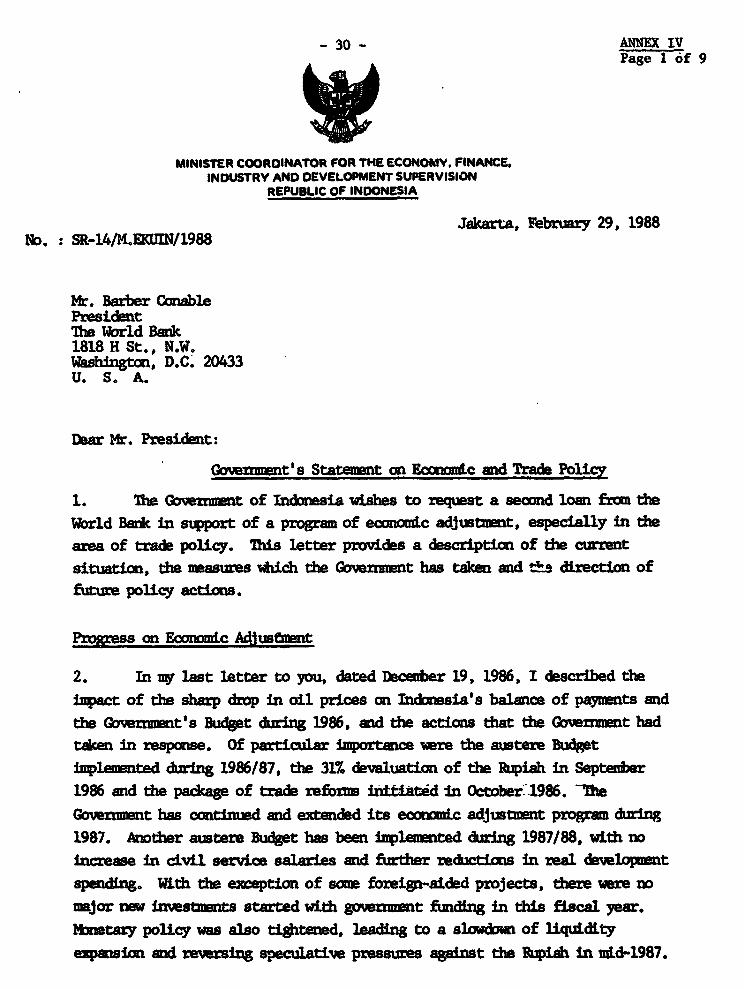

53. Direct Bank support to the Government's adjustment efforts, and inparticular, its trade policy reforms, was provided under the first TradePolicy Adjustment Loan. That loan was based on policy changes introduced In1986, and was intended to support both the implementation of those measuresand further progress in macroeconomic stabiliaation and structural reforms. Acomparison of actual steps taken since that loan was approved with the 'areasfor follow-up" noted in the Policy Frameworkl7 clearly indicates theGoverrment's commitment to the adjustment program. Implementation of theearlier trade policy measures has been generally quite effective and, asdiscussed above, significant steps have been taken to further improve thetrade regime through the reduction of import licensing and reforms of exportpolicies. In the area of industrial regulation, the Government's efforts wentbeyond what was stated in the Policy Framework by actually initiating measuresto relax investment licensing and taking steps to simplify and ease foreigninvestment regulations. Regarding public enterprises, the Government (withIMF assistance) completed a preliminary consolidation of the financialaccounts of public enterprises, but an actual program of reform has yet to beannounced. Finally, GOI has pursued, as suggested in the Policy Framework,appropriate macroeconomic policies through a prudent fiscal and monetarystance and sound exchange rate management.

7/ Annex V of the President's Report for TPAL I (No. P-4429-IND,December 30, 1986).

- 19 -

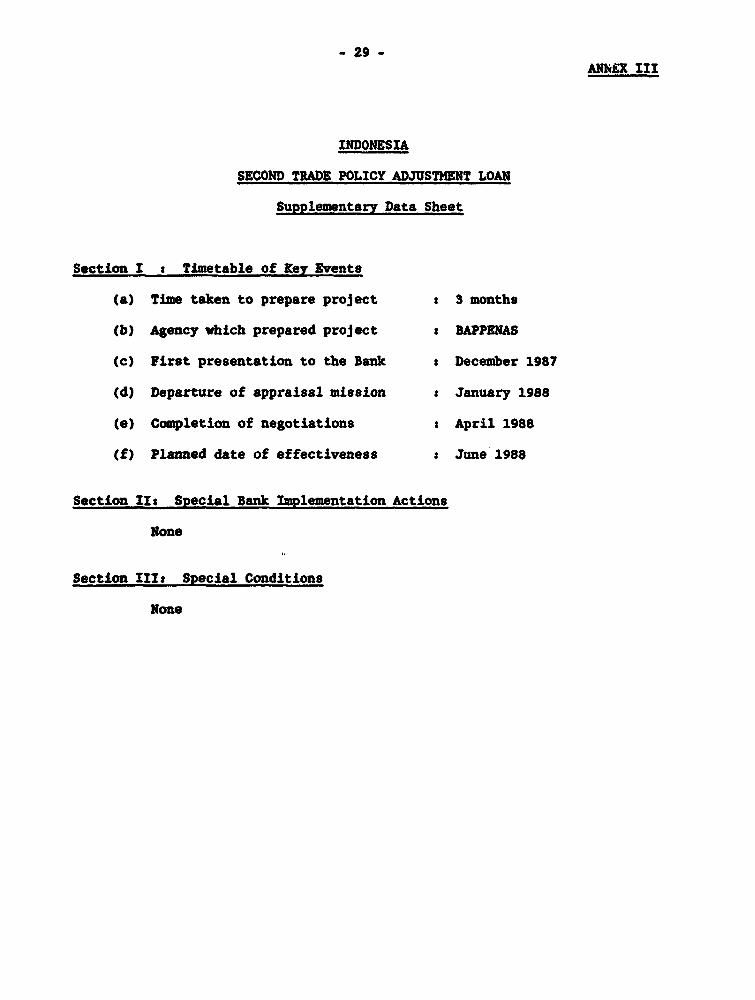

54. The proposed loan was prepared following GOils announcement of theDecember 24 reform measures and builds on ongoing active consultations betweenthe Bank and GOI on macroeconomic management, and trade and industrial policyissues. The loan was appraised in January 1988; negotiations were held inWashington from March 31 to April 1, 1988. The Indonesian delegation was ledby Mr. Boediono (BAPPENAS), and included representation from the Ministry ofFinance and the Indonesian Embassy. Supplementary loan data are provided inAnnex III.

B. Loan Objectives

55. The objectives of the proposed loan of US$300 million equivalent areto: (a) support the substantial reforms, especially in the area of tradepolicy, undertaken by the Government during 1987, and to ensure that they areimplemented well; (b) assist GOI to bring about an early recovery in economicactivity consistent with external and domestic financial stability; and(c) maintain the policy dialogue on further reforms for promoting theefficiency and longer-term viability of the economy, including the preparationof a medium-term plan for tariff rationalization. These objectives would beachieved in part through support to the balance of payments provided by theproposed loan and in part through ongoing dialogue on policy issues andimproved institutional arrangements for analysis of the trade and industrialpolicy regime. As part of this dialogue, the Bank will complete during 1988 astudy on industrial regulations and a study on financial sector efficiency anddevelopment.

C. Loan Administration

56. Disbursement. The proposed loan of US$300 million equivalent wouldbe available for disbursement upon loan effectiveness and would be used toreimburse 1002 of foreign expenditures for eligible imports for which paymentsare made after the date of loan signing. The list of ineligible imports forthe purposes of this loan would be standard i.e., goods intended for militaryor paramilitary purposes, or for luxury consumption; goods financed from otherofficial multilateral or bilateral sources; uranium; and goods procured undercontracts of less than US$100,000. Disbursement for reimbursement of eligibleimport expenditures would be based on documentation prepared by SocieteGenerale de Surveillance S.A. (SGS) in the course of their customs inspectionservices and which is routinely provided to Bank Indonesia. T'ae SGScertificate provides verification of shipment of goods and their value as wellas other information needed to ensure compliance with eligibility requirementsfor purposes of the Bank loan. Disbursement for eligible import expenditureswould be based on Statements of Expenditure (SOEs) for imports valued at lessthan US$5 million; for imports valued above this amount full documentationvwuld be provided. Applications for withdrawals based on SOEs would besubmitted in amounts not less than US$1 million and supporting documentationwould be retained by Bank Indonesia. All of the proceeds of the proposed loanare expected to be disbursed by March 31, 1989.

57. Procurement. Both private and public sector imports would be eligiblefor financing. Contracts under US$5 million each would be awarded on thebasis of normal procurement practices of the purchaser. Contracts for goodsand services estimated to cost US$5 million or more each, would be procuredthrough International Compet#tive Bidding in accordance with Bank Guidelines.

- 20 -

58. Accounts and Audits. Bank Indonesia would maintain loan accounts andsupporting documentation. Audits would be carried -ut by independent auditorsacceptable to the Bank within nine months of the closing of the GOI fiscalyear in which final disbursements under the loan are made.

D. Monitoring and Follow-up

59. The Bank would monitor closely, through frequent consultation withGOI, the progress on implementation of GOI's trade policy and industriallicensing reforms, as well as on macroeconomic management. Particularattention would be given tot (a) further measures to reduce NTBs andrationalize the tariff structure; (b) continued progress on simplifying theregulatory framework and reducing the scope of industrial licensing; (c) thestudy of complementary reforms in the financial sector, to support industrialrestructuring and recovery; (d) appropriate fiscal and monetary policies, toreduce the current account deficit, control inflation and preserve acompetitive exchange rate; and (e) prudent external debt management; includinglimits on Import-related credits and careful scrutiny of proposals for largecapital-intensive projects. Satisfactory progress in these areas could be thebasis for a third adjustment loan from the Bank in about a year.

E. Program Benefits and Risks

60. The adjustment measures taken by GOI over the past two years willprovide balance of payments and fiscal stability in the face of lower oilprices, and help develop the non-oil economy over the medium term. Inparticular, the recent trade policy and domestic licensing reforms representsubstantial progress in GOI's efforts to reduce long-standing distortions inIndonesia's highly protected industrial structure; improve internationalcompetitiveness of non-oil exports; and increase potential for foreigninvestment, especially in export-oriented industries. In addition, greatertransparency and administrative simplicity has been introduced intoIndonesia's trade regime. The principal risk is that the far-reaching natureof the policy reforms could encounter domestic opposition as they areimplemented and extended. This risk is offset by the positive responses,especially of non-oil exports, to earlier reforms and GOI's demonstratedcommitment to carry out difficult and sensitive policy measures.

PART VII - RELATIONS WITH IMF

61. The latest IMF Consultation Report, under Article IV, was released inMarch 1987. This year's consultation mission has cecently been completed andthe Board discussion of the staff report will be in May. GOI has not had anystandby or extended arrangements with the IMP since 1973. GOI1s last purchasefrom the IMP was for SDR 463 million in May 1987 under the CompensatoryFinancing Facility (CFF). This purchase increased Indonesia's totaloutstanding IMF obligations to SDR 505 million at the end of 1987. After thelast Consultation Report, the IMF Executive Board expressed its satisfactionthat 'Indonesia maintains an exchange system which is free of restrictions onpayments and transfers for current international transactions.'

- 21 -

PART VIII - RECOMMENDATION

62. T am satisfied that the proposed loan would comply with the Articlesof Agreement of the Bank and recommend that the Executive Directors approvethe proposed loan.

Barber B. ConablePresident

AttachmentsWashington, D.C.April 19, 1988

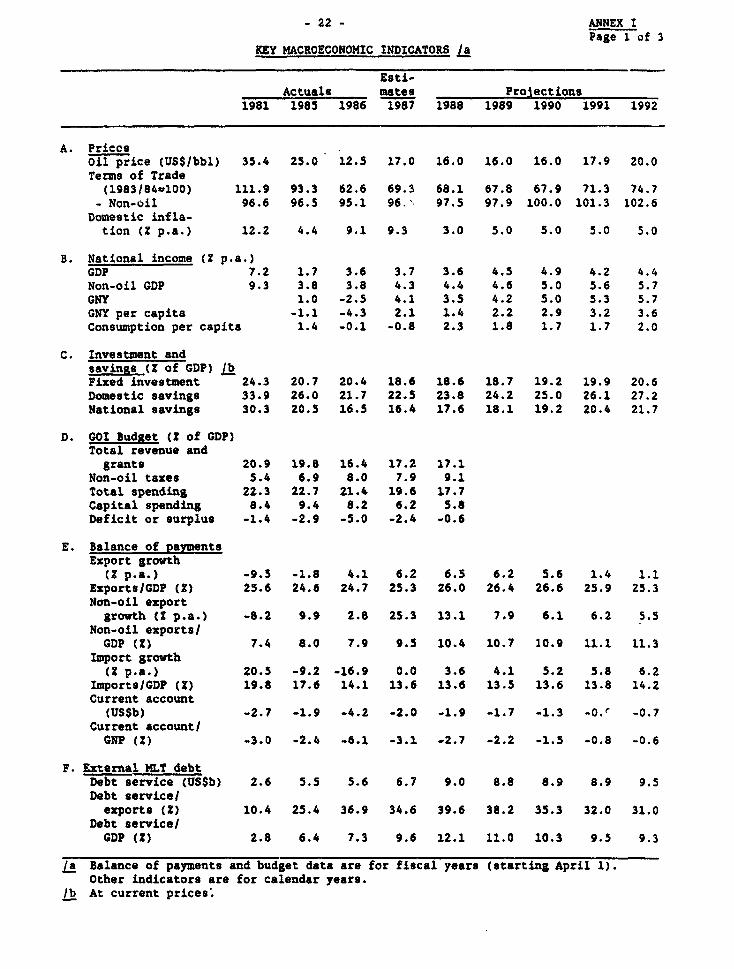

- 22 - ANNEX IPage 1 of 3

KEY HACROECONOHIC INDICATORS /a

Esti-Actuals mates Projections

1981 1985 1986 1987 1988 1989 1990 1991 1992

A. PricesOil price (US$/bbl) 35.4 25.0 12.5 17.0 16.0 16.0 16.0 17.9 20.0Terms of Trade

(1983I84m100) 111.9 93.3 62.6 69.3 68.1 67.8 67.9 71.3 74.7- Non-oil 96.6 96.5 95.1 96. 97.5 97.9 100.0 101.3 102.6

Domestic infla-tion (Z p.a.) 12.2 4.4 9.1 9.3 3.0 5.0 5.0 5.0 5.0

B. National income (t p.a.)GDP 7.2 1.7 3.6 3.7 3.6 4.5 4.9 4.2 4.4Non-oil GDP 9.3 3.8 3.8 4.3 4.4 4.6 5.0 5.6 5.7GNY 1.0 -2.5 4.1 3.5 4.2 5.0 5.3 5.7GNY per capita -1.1 -4.3 2.1 1.4 2.2 2.9 3.2 3.6Consumption per capita 1.4 -0.1 -0.8 2.3 1.8 1.7 1.7 2.0

C. Investment andsavints (2 of GDP) lbFixed investment 24.3 20.7 20.4 18.6 18.6 18.7 19.2 19.9 20.6Domestic savings 33.9 26.0 21.7 22.5 23.8 24.2 25.0 26.1 27.2National savings 30.3 20.5 16.5 16.4 17.6 18.1 19.2 20.4 21.7

D. GO1 Budget (2 of GDP)Total revenue and

grants 20.9 19.8 16.4 17.2 17.1Non-oil taxes 5.4 6.9 8.0 7.9 9.1Total spending 22.3 22.7 21.4 19.6 17.7Capital spending 8.4 9.4 8.2 6.2 5.8Deficit or surplus -1.4 -2.9 -5.0 -2.4 -0.6

E. Balance of paymentsExport growth

(Z p.a.) -9.5 -1.8 4.1 6.2 6.5 6.2 5.6 1.4 1.1Exports/GDP (2) 25.6 24.6 24.7 25.3 26.0 26.4 26.6 25.9 25.3Non-oil export

growth (2 p.a.) -8.2 9.9 2.8 25.3 13.1 7.9 6.1 6.2 5.5Non-oil exports/GDP (S) 7.4 8.0 7.9 9.5 10.4 10.7 10.9 11.1 11.3

Import growth(2 p.a.) 20.5 -9.2 -16.9 0.0 3.6 4.1 5.2 5.8 6.2

Imports/GDP (2) 19.8 17.6 14.1 13.6 13.6 13.5 13.6 13.8 14.2Current account

(US$b) -2.7 -1.9 -4.2 -2.0 -1.9 -1.7 -1.3 -0.r -0.7Current account/

GNP (2) -3.0 -2.4 -6.1 -3.1 -2.7 -2.2 -1.5 -0.8 -0.6

F. External MLT debtDebt service (US$b) 2.6 5.5 S.6 6.7 9.0 8.8 8.9 8.9 9.5Debt service/exports (2) 10.4 25.4 36.9 34.6 39.6 38.2 35.3 32.0 31.0

Debt service/GDP (2) 2.8 6.4 7.3 9.6 12.1 11.0 10.3 9.5 9.3

/a Balance of payments and budget data are for fiscal years (starting April 1).Other indicators are for calendar years.

lb At current prices;

- 28 -ANNEX"Pgeo 2 of 3

BALANCE OF PAYMENTS(USS billion at current prices)

Actuals sates Proloctlone1991/82 19S6/80 1986/8? 18?/88 lsae/99 1989/90 199O/91 1891/92 1992/98

A. Exports of goods and NFS 28.3 19.1 14.4 13.7 20.8 22.1 24.2 27.0 29.9Morchandise (fob) 23.0 18.5 13.7 17.9 19.3 21.1 23.0 26.7 28.4Non-factor cervices 0,3 0.6 0.7 0.8 0.9 1.1 1.2 1.8 1.6

S. Importo of goods and NFS -22.9 -10.5 -14.9 -16.6 -17.0 -18.9 -20.5 -22.5 -24.8Merchandloo (cif) -20.0 -14.2 -12.7 -14.1 -16.1 -16.7 -17.6 -19.4 -21.6Non-factor corvicoo -2.9 -2.3 -2.1 -2.4 -2.5 -2.7 -2.8 -3.0 -3.8

C. Reeourco balance 0.4 2.6 -0.6 2.8 2.7 3.3 3.8 4.6 6.1

0. Not factor Incoso -3.2 -4.8 -3.9 -4.6 -4.8 -5.2 -6.4 -S.7 -6.0Fector roceipto 1.7 0.8 0.8 0.7 0.9 0.9 0.9 0.9 0.9Factor peymonto -4.9 -5.4 -4.e -5.2 -5.7 -6.1 -4. -4.8 -7.0(Interest pets.) -1.8 -2.7 -2.9 -3.4 -3.8 -8.9 -3.0 -3.3 -3.8

E. Not Current transfers /a 0.1 0.1 0.2 0.2 0.2 0.2 0.8 0.3 0.8

F. Current account balance -2.7 -1.9 -4.2 -2.0 -1.9 -1.7 -1.3 -0.9 -0.7

0. MLT capital Infloe 2.6 1.7 3.1 2.6 2.6 2.5 2.2 1.7 1.4irec t In teedztnt 0.1 0.8 0.3 0.4 0.6 0.6 0.7 0.8 0.9Not pubilc MLT loans 2.2 1.4 2.b 2.0 1.9 1.8 1.4 0.8 0.7Dieburoreento 3.3 8.9 6.4 5.9 8.4 8.4 6.1 6.3 6.6Repsymonts -1.1 -2.6 -2.6 -3.9 -4.6 -4.7 -4.6 -4.5 -4.9

Otbor ULT inflows (net) 0.2 0.0 0.0 0.1 0.2 0.2 0.1 0.1 -0.1

M. Total other Itemo -0.4 0.7 -1.4 0.9 0.0 0.0 -0.1 -0.1 -0.1Not abort-torn capital -0.2 -0.1 1.0 0.0 0.0 0.0 0.0 0.0 0.0Capital f leo nol -0.2 0.8 -2.5 0.9 0.0 0.0 -0.1 -0.1 -0.1

I. Use of not foreign asset. 0.5 -0.6 2.6 -1.4 -0.7 -0.8 -0.9 -0.7 -0.7Not XIF credit 0.0 -0.3 0.0 0.6 0.0 0.0 -0.8 -0.3 0.0Other renorve change. 0.6 -0.2 2.5 -2.0 -0.7 -0.8 -0.6 -0.4 -0.7

Shareo of CDP (X)Resource balance 0.6 3.0 -0.6 8.2 8.6 4.0 4.3 4.7 4.9Total lnterst payeento -1. -8.2 -4.0 -4.8 -6.1 -4.8 -4.4 -3.0 -3.7Current account balanceo -2.9 -2.8 -5.8 -2.9 -2.5 -2.1 -1.5 -0.8 -0.6lLT capital Inflow 2.8 2.0 4.2 8.6 3.4 8.1 2.5 1.7 1.4Not IMF credit 0.0 -0.3 0.0 0.6 0.0 0.0 -0.8 -0.3 0.0

Foreign exchange reserves

International reeerves 6.2 4.9 4.0Gold 1.1 1.0 1.1Total offleial resorves 6.3 5.8 6.1(In aonths of isoprte) 8.8 4.9 4.8Total not foreign easotu 10.8 12.1 9.6

Exchange rates (Rp/USS)Neoinal official ER 688.5 1120.2 1411.6Real offectivo ER 111.7 85.8 62.8

La Ineludes offtetal grants.

- 24 -ANNEX IPage 3 of 3

EXTERNAL FINANCING AND MLT DEBT(Annual averages in US$ billion)

FY85-87 PY88-90 FY91-93

A. Gross disbursements 5.1 7.3 6.8Multilateral 1.0 2.0 2.1

of which: IBRD 0.8 1.5 1.5Bilateral 1.1 2.3 1.8Private la 3.1 2.8 2.9IlW purchases 0.0 0.2 0.0

B. Net disbursements 2.3 2.7 1.4Multilateral 0.8 1.6 1.4

of whichs IBRD 0.6 1.1 0.8Bilateral 0.6 1.4 0.7Private la 1.0 -0.5 -0.5IMP purchases -0.1 0.2 -0.2

C. Principal repayments lb 2.8 4.7 5.2Multilateral 0.2 0.5 0.8

of which: IBRD 0.2 0.4 0.6Bilateral 0.5 0.9 1.0Private /a 2.1 3.3 3.4

D. Interest payments 2.3 3.1 3.3Multilateral 0.4 0.9 1.2

of which: IBRD 0.3 0.7 0.9Bilateral 0.4 0.6 0.7Private /a 1.5 1.7 1.3

E. Rey ratios (Z) 1987188 1988189 1989190 1990191 1991192 1992193Interest/XGS 14.5 15.1 14.4 13.1 11.7 10.7DODIXGS 242.2 234.8 224.3 211.7 194.8 177.9Net disb./interest 76.4 64.3 58.9 47.1 27.2 16.3Net transfer/GDP -0.9 -1.5 -1.7 -2.0 -2.5 -2.7

/a Includes private guaranteed and nonguaranteed debt./b Includes repayments to the IMF.

- 25 -

ANNEX IIPage 1 of 4 pages

THE STATUS OF BANK GROUP OPERATIONS IN INDONESIA

A. STATEMENT OF BANK LOANS AND IDA CREDITS(as of March 31, 1988) /a

Loan/ Amount (US$ million)Credit Fiscal (less cancellations)number year Purpose Bank IDA Undisbursed

Fifty-three Loans and forty-seven Credits fully 3,175.00 890.45 -disbursed

946 1980 Yogyakarta Rural Development - 12.00 2.571751 1980 Nucleus Estate and Smallholders III 92.00 - 2.551835 1980 Nucleus Estate and Smallholders IV 30.00 - 12.101840 1980 National Agricultural Research 35.00 - 15.501872 1980 Ninth Power 218.18 - 3.891904 1981 University Development 45.00 - 10.021958 1981 Swamp Reclamation 22.00 - 0.731972 1981 Fourth Urban Development 43.00 - 0.812007 1981 Nucleus Estate and Suallholders V 127.16 - 54.052049 1981 Jakarta-Cikampek Highway 85.00 - 38.572056 1982 Eieventh Power 170.00 - 9.212066 1982 Second Seeds 15.00 - 2.612079 1982 Bukit Asam Coal Mining Development and

Transport 183.86 - 22.552083 1982 Rural Roads Development 85.00 - 10.052101 1982 Second Teacher Training 79.59 - 32.592102 1982 Second Textbook 25.00 - 7.092118 1982 Sixteenth Irrigation 37.00 - 6.392119 1982 Seventeenth Irrigation (East Java

Province) 70.00 - 21.352126 1982 Nucleus Estate and Smallholders VI 52.07 - 34.322153 1982 Coal Exploration Engineering 25.00 - 1.17

/a The status of the projects listed in Part A is described in a separate report onall Bank/IDA financed projects in execution, which is updated twice yearly andcirculated to the Executive Directors on April 30 and October 31.

- 26 -

ANNEX IIPage 2 of 4 pages

Loan/ Amount (US$ million)Credit Fiscal (less cancellations)number year Purpose Bank IDA Undisbursed

2214 1983 Twelfth Power 300.00 - 121.552232 1983 Nucleus Estate and Smallholders VII 135.23 - 104.302235 1983 Provincial Health 27.00 - 12.202236 1983 Jakarta Sewerage and Sanitation 22.40 - 12.742248 1983 Transmigration III 94.00 - 10.062258 1983 Public Works Manpower Development 30.00 - 7.542275 1983 East Java Water Supply 30.60 - 2.562277 1983 Fifth BAPINDO 208.90 - 77.382288 1983 Transmigration IV 53.50 - 35.642290 1983 Second Polytechnic 107.40 - 45.932300 1983 Thirteenth Power 279.00 - 59.892341 1984 Third Agricultural Training 63.30 - 20.322344 1984 Nucleus Estate and Smallholder Sugar 70.30 - 24.872355 1984 Second Nonformal Education 43.00 - 15.472375 1984 Second Provincial Irrigation Dev. 89.00 - 14.462404 1984 Highway Department 240.00 - 35.242408 1984 Fifth Urban Development 39.25 - 12.542430 1984 Third Small Enterprise Development 204.65 - 5.322431 1984 Second Swamp Reclamation 65.00 - 44.862443 1984 Fourteenth Power 210.00 - 79.302472 1985 Secondary Education and Management