Embed Size (px)

Citation preview

Document of

The World Bank FIL COPYFOR OFFICIAL USE ONLY

Veport No.2830a-PH

PHILIPPINES

STAFF APPRAISAL REPORT

THIRD PORTS PROJECT

April 30, 1980

Projects DepartmentEast Asia and Pacific Regional Office

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENT EQUIVALENTS

-= Peso

P :- US$0.137

.k~.on = US$137,000

= P 7.30

WEIGHTS AND MEASURES

I mte() = 3.28 feet (ft)1 Ig -i2.r (km) 0.62 mile (mi)

(kg) = 2.2 pounds (lb)rL4i0t= 0.98 long ton (ton)

ABBREVIATIONS

ADB * Asian e . -- BankBOC - BureattBPW - Bureau w-Jt i ._

GR ross .. I 'IATCTP - lnter-Age - ;-S-: cal Committee on Transport PlanningILMLW - .iean Lowe-i erM. TC - linistri. -i:ort and CommunicationsNIH - Ministr', s -Lc HighwaysMPW - Ministry O. ic WorksMPWTC - Ministry of T>iU Works, Transportation and CommunicationsPAL - Philippine 3 L,nesPEA - ]?hilippine. :te AuthorityPMU - port mana&&. M titPNR - Philippine wisl RailwaysPPA - Philippine AuthorityPPDO - 1'lannin- e = ct Development OfficePTS - Phllpp.-- ort SurveyNEDA - National' -'c Development AuthorityNRT - net reg. onsNTSS - National ' t Systems Study

GOVERNMENT OFHIE REPUBLIC OF THE PHILIPPINES

FISCAL YEAR

January 1 to December 31

PHILIPPINES FOR OFFICIAL USE ONLY

APPRAISAL OF THE THIRD PORTS PROJECT

Table of Contents

Page No.

1. TRANSPORT SECTOR ....................... 1

General ............................................................ 1Transport Subsectors ...................., 2Transport Planning, Coordination and Strategies ...................... 5Previous Bank Assistance in the Transport Sector ..................... 7

2. PORT SUBSECTOR ....................................................... 8

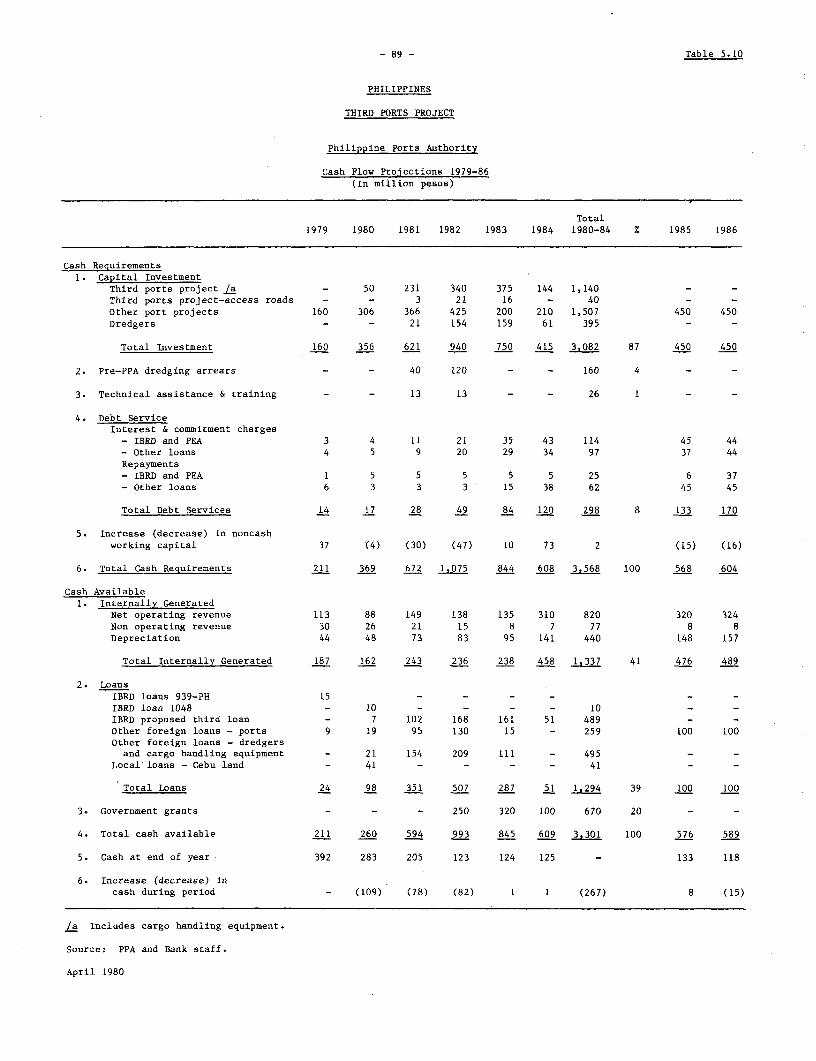

PPA Organization ................................ . . . 8Management, Staff and Training ........................................ Existing Port Facilities ........................................ 10Traffic .............................. 13Operations .............................. 15Tariffs and Costs .............................. 18Budget, Accounting and Audit ......................................... 19

3. INVESTMENT PLAN AND PROJECT .19

PPA's Investment Plan 1980-86 . -- 19The Project and the Proposed Loan .20Description of the Main Project Items . 21Cost Estimates ...................................................... 23Financing Plan .. ............................ 25Project Implementation .................................. 25Procurement and Disbursement ......... ....................... 26Ecology .................................. 26

4. ECONOMIC EVALUATION .................................. 27

Traffic ................................ 27Benefits .......,.. .............. 30Economic Evaluation and Sensitivity Analysis ....................... .. 35

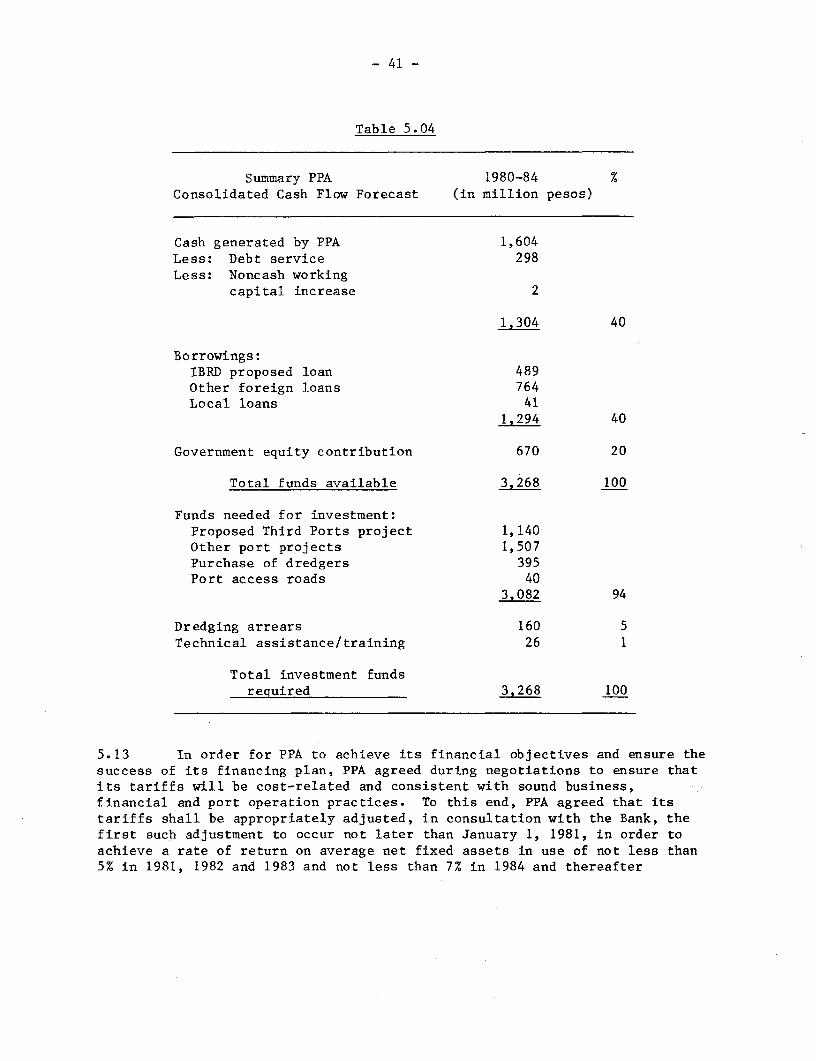

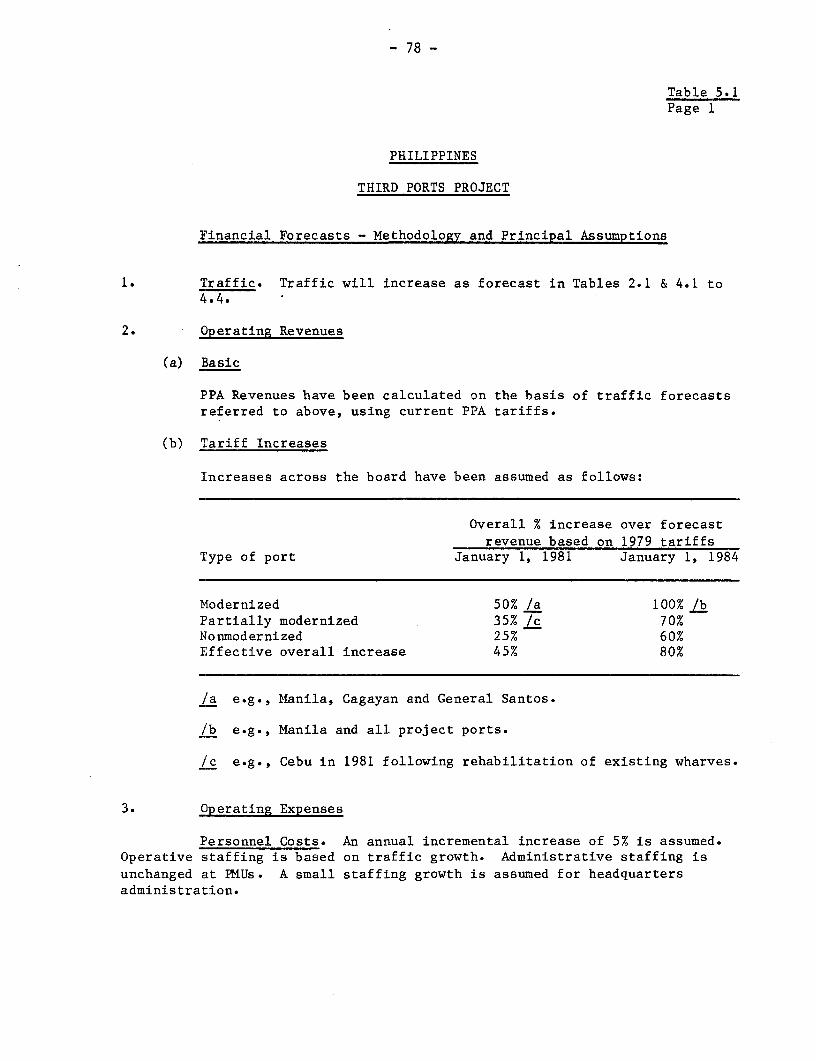

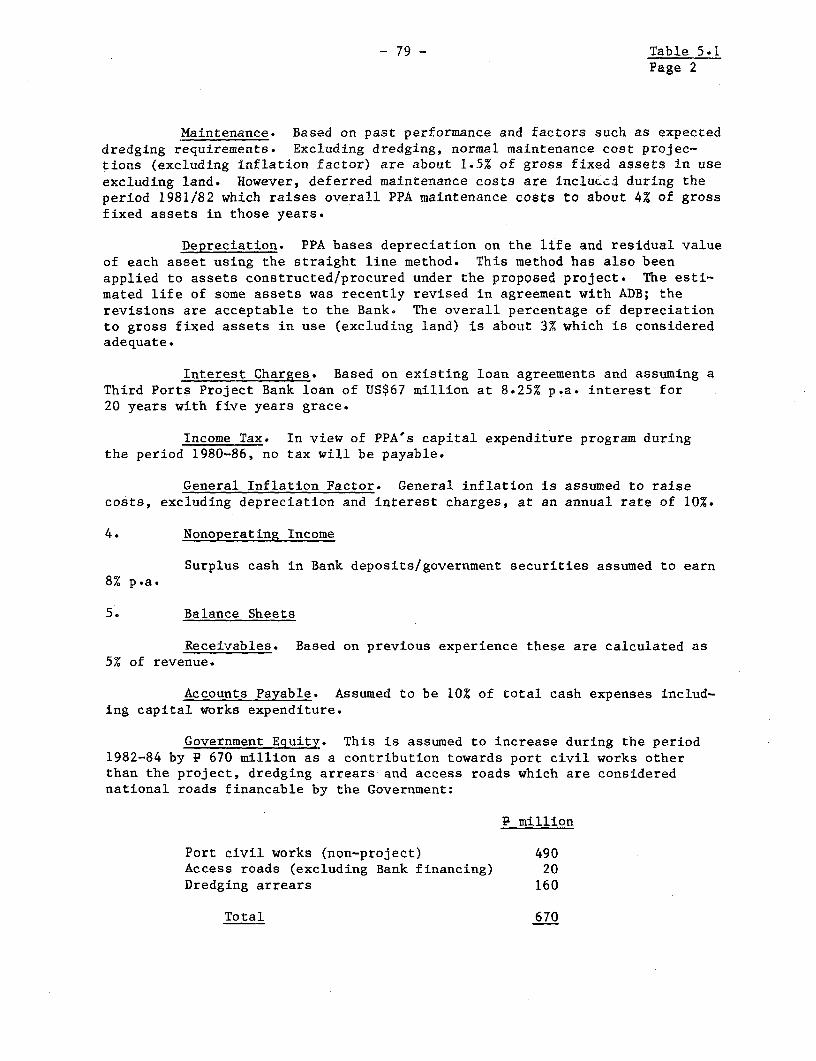

5. FINANCIAL EVALUATION ................................................ 37

General .. 37Present and Future Financial Performance - Project Ports ... 38PPA Consolidated Financial Performance .. . 39Sensitivity Analysis .-------------...----..... 42

6. AGREEMENTS REACHED AND RECOMMENDATIONS -------------------- - 43

This report is based on the findings of a Bank mission which visited the Philippinesin October 1979, comprising Messrs. K. C. Rodley (senior financial analyst) and F.Khin-Maung-Gyi (engineer) from the Bank; and Mr. J. Bigosinski (economist -consultant).

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

-2-

Page No.

TABLES IN TEXT

2.01 Philippine Ports Forecast Traffic Smmary ... ..................... 142.02 Project Ports Forecast Traffic Summary .......................... 153.01 PPA Investment Plan 1980-84 .l....... ... ... ...... .... ... . .. . .. . .. . 203.02 Project Cost Sumnary ....... 243.03 Project Financing Plan .. ............................... 254.01 Economic Rate of Return ............ .......... 364.02 Switch Value Analysis ***...................**g..... 364.03 Net Present Value .............................. 375.01 Summary Project Port Income & Expenditure Account 1979-86 ....... 385.02 Summary PPA Income & Expenditure Account 1980-86 ................ 395.03 Summary PPA Consolidated Balance Sheet 1980-86 .. 6................ 405.04 Summary PPA Consolidated Cash Flow Forecast 1980-84 ............. 415.05 Sensitivity Analysis ........... .0.0.0.0.o ............... ..... 43

ANNEXES

1. Outline Terms of Reference for Technical Assistance ............... 462. Supporting Tables, Charts and Maps ......................... $ .... 473. Selected Documents and Data Available in the Project File .... ..... 49

April 1980

PHILIPPINES

STAFF APPRAISAL REPORT

THIRD PORTS PROJECT

1. Transport Sector

A. General

1.01 In the last decade, t'he Philippines has made significant advances inthe transport field, far exceeding any previous ten-year period both in termsof funds expended and results achieved. Between 1968 and 1978, the totalpublic transport expenditures amounted to P 14 billion (US$1.9 billion)representing over 30% of total public investment outlays. Since 1975, annualpublic transport expenditures increased rapidly (although only representingabout 1.3% of GNP), with highways absorbing about 74% of the total; of theremainder, airports received 10%, ports 9% and railways 7%. These transportexpenditures for the development and improvement of thle hithierto neglectedtransport system were necessary to meet the increased demand for movement ofgoods and passengers in the seventies, which had resulted fromo higher income,population and industrial and agricultural production.

1.02 The 1978-81 projections for commodity flows and passenger trafficindicate a larger increase in inter-island movements of freight and passengersbetween the food deficit areas of Luzon and the agricultural surplus areasof Xindanao than for road transport within the major islands. Accordingly,the 1979-82 Investment Program allocates a greater share of total publictransport expenditures to the expansion of ports and airports; 19% for ports,14% for airports, 9% for railways, and 58% for highways. No significantpublic funds are allocated for shipping investment since it is largelyfinanced by the private sector.

1.03 The total transport investment tentatively allocated in the Govern-ment's indicative 1979-82 Investment Program is F 14,374 million(JS$1,942 million);/1 an increase of about one third over the previous four-year period. However, the transport share of total public investment willdecrease from the previous level of one third to about one fifth of the totalprogram; the power sector will receive an increased share of the allocation toimplement the Government's objective to reducing dependence on importedpetroleum by constructing hydro, nuclear, and geothermal power plants asalternative sources of electrical energy.

/1 A ten-year transport investment program is under preparation by theMinistry of Transport with the assistance of the National EconomicDevelopment Authority and foreign advisors.

-2-

1.04 Between 1970-76, transport developed somewhat faster than the economyas a whole: freight and passenger movements grew by about 8% and 7% p.a.respectively, while real GNP grew by 6%. Freight and passenger movements byinter-island shipping accounted for much of this increase, at 14% and 8%respectively, with road transport growing at a lesser pace: 4% for freightand 5% for passengers. The average annual target growth rate of GNP is 7.5%during 1978-85. In the light of the projected growth of the economy, bothroad freight and passenger transport is expected to grow at 8% during the sameperiod.

1.05 goad transport is the dominant mode within the two major islandsof Luzon and Mindanao, estimated to account for nearly 80% of passengertraffic; but it is estimated that the road's share of total freight traffichas decreased from 57% in 1970 to 44% in 1976. Although reliable data are notavailable, privately operated inter-island shipping, serving a populationscattered over hundreds of islands, appears to be the largest transport mode(about 54%) for freight traffic. The increased share of inter-island traffichas been due to the growing commerce between the food deficit areas of Luzonand the agricultural surplus areas of Mindanao. Relatively short inlanddistances have limited railways to a small fraction of total traffic.

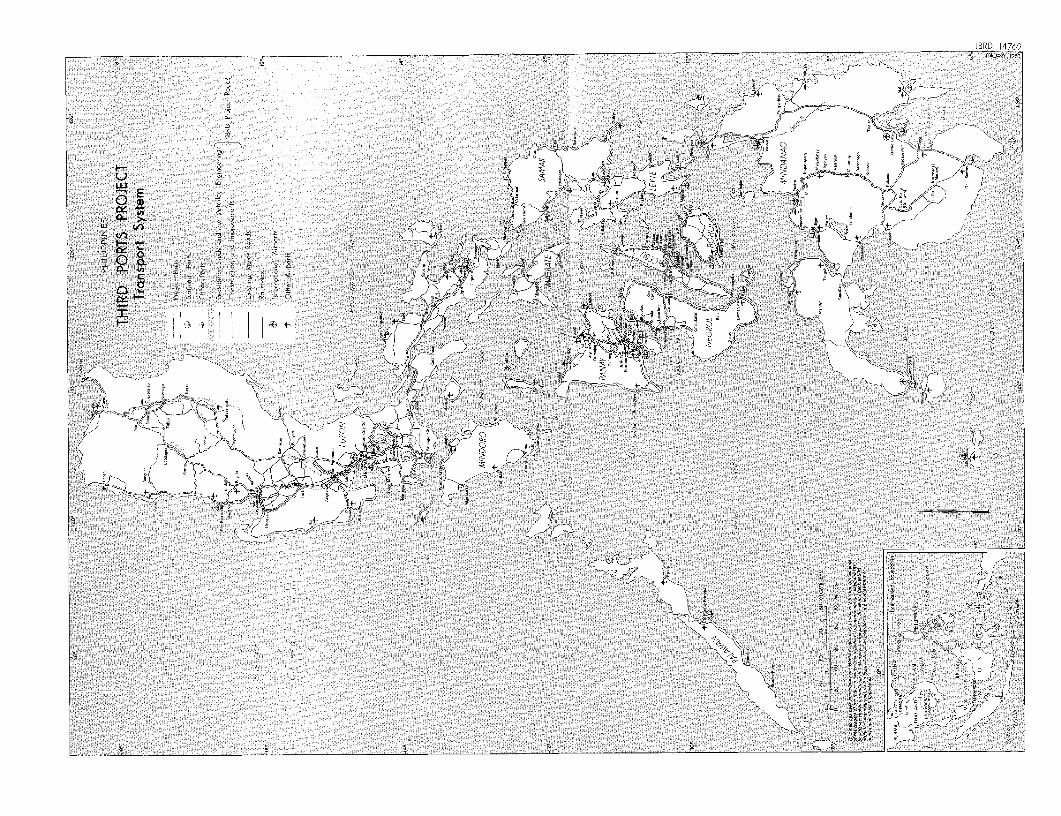

B. Transport Subsectors (Map 14769)

Highways

1.06 The public road transport system in the Philippines is made up ofthree major interlocking components: (a) national; (b) provincial, municipaland city; and (c) barangay (mainly farm-to-market) roads. The total networkconsists of about 152,800 km of roads, of which 22,900 km are classified asnational, 29,000 km provincial, 13,400 km city and municipal, and 87,500 kmbarangay roads. National roads include about 122 km of toll expressways withgrade separated intersections north and south of Manila. Except for the tollroads, road classification is often arbitrary as it is not always based onfunction. In remote areas such as northeastern Luzon and many parts ofMindanao, national roads serve as penetration roads providing the only accessto the villages. In many parts of the country, provincial and barangay roadsare indistinguishable, both being characterized by low volume traffic servingthe limited influence areas to move agricultural inputs and outputs and toconnect the rural communities with administrative and market centers.

-3-

1.07 Despite Government efforts /1 since 1969 to develop a modern highwaynetwork, the system is still inadequate for the current level of traffic.Although sufficient in location and extent, for the most part, condition ofthe roads is deplorable, and missing bridges effectively isolate many ruralcommunities. Most unimproved roads are in poor condition due to: (a) defi-cient designs resulting in inadequate drainage, embankment and pavements; (b)lack of proper maintenance; (c) damage from frequent overloading (many of thetrunk roads were built long ago and intended to carry only a small number ofvehicles); and (d) insufficient funds to repair flood damage caused during therainy and typhoon seasons. Moreover, vehicle operating and travel costs aregenerally high, as only 42% of the national highways and 13% of the provincialroads are paved, (compared with 85% and 35% in Thailand).

Railways

1.08 The Government-owned Philippine National Railways (PNR) has a networkon Luzon totalling 1,060 km, of which 740 km of main line and 80 km of branchlines and sidings are operating. Most of PNR's track was relaid during the1960s with Japanese aid; the rest is in very poor condition. Management,maintenance and operations of the railways have been inadequate. Except inthe Bicol region, the main line is paralleled by highways for most of itslength and, as haulage distances for most commodities are relatively short,and commodities are in small shipments, the railway is not presentlycompetitive with trucks and buses. It is unlikely that this situation willchange in the near future.

1.09 The Government's present objective is to improve PNR operations topermit the railroad to cover at least current operating costs. Programs underthe 1971-76 Rehabilitation Plan have improved services and passenger andfreight traffic have increased somewhat since 1973. In 1977, PNR obtained aloan from the Asian Development Bank (ADB) to rehabilitate its Southern Line(about 450 km), which serves the area between Manila and Legaspi. A secondrailway, the privately owned Panay Railway operates an antiquated 117 km oftrack on Panay Island: it is presently unsafe but is undergoing minimumrehabilitation to permit limited services on Panay Island which will includethe transport of sugar to Iloilo port for export.

/1 Major road improvement activities began in 1969 following completion ofthe Philippine Transport Survey (PTS), a two-year study conducted underUNDP financing with the Bank acting as Executing Agency. The PTSrecommended improvement of about 6,000 km of national roads,reorganization of the highway administration, and improvments in roadmaintenance procedures. Most of the priority roads identified in the PTShave been or are being improved with local resources, supplemented byassistance from Japan, USAID, ADB and the Bank. Between 1969 and 1979about 4,800 km of national and 5,200 km of provincial roads have beenconstructed or improved.

-4-

Ports

1.10 There are 18 major and 76 minor national ports, and about 390municipal ports throughout the Philippine archipelago, plus over 200 privatepiers and wharves. Manila, the largest port, accounts for about 46% of the23 million tons of cargo handled each year by public ports. Most long-established public ports are located where natural protection is available butsedimentation problems occur in many ports. More modern private piers andwharves, which handle mainly petroleum products and iron ore, are generallylocated to take advantage of naturally deep water. Many public ports sufferfrom inadequate work areas and transit sheds, and poor maintenance. Thecumulative effect of these deficiencies is congestion which unduly restrictsthe movement of cargo, slows stevedoring and lengthens ship turn-around time.

1.11 In the past few years the Government has received assistance fromthe ADB for improvement of port facilities at Manila, Davao and Cotabato,from the Federal Republic of Germany for port works at Davao and Iligan, andfrom the IBRD for the expansion of the ports of Cagayan de Oro and GeneralSantos under Loan 939-PH (Second Ports Project). As a part of the project,the Bank supported the establishment of the Philippine Ports Authority (PPA)which was mandated to consolidate and assume the port-related functionswhich had previously been fragmented between the Bureau of Customs (BOC) andBureau of Public Works (BPW) in the former Ministry of Public Works,Transportation, and Communications (MPWTC). Since it became operational in1976, PPA has taken over the management and operation of all national ports,expanded its technical staff and improved accounting procedures with theassistance of Bank-financed consultants.

1.12 The Bank's objective in the port sector is to assist the PPA indeveloping a national port policy, increasing port capacity to meet industrialdevelopment in secondary urban growth centers, and improving administration,operations, and planning for all major national ports. PPA's currentInvestment Plan (1979-83) not only aims at increasing capacity at major ports,but also at consolidating ports of various sizes and functions in outlyingareas where improved overland mobility makes economies of scale and efficiencypossible. The selection of ports for future improvement has been determinedin the context of the traffic-patterns of the total transport network, thedevelopment potential of the hinterlands, and the natural conditions of theharbors. Details on the subsector are given in Chapter 2.

Inter-Island and Coastal Shipping

1.13 Despite its status as the most important transport mode for freight,the potential of inter-island and coastal shipping has not yet been fullyrealized, mainly due to inadequate port facilities and the antiquated localshipping fleet. There are about 480 inter-island vessels of over 100 grosstons, and many more smaller ships. In 1976, more than 34% of the inter-islandfleet and 41% of the ocean-going fleet were 25 or more years old. Mostsmaller ships are converted naval or military vessels, and over-loading ischaracteristic. There are about 50 Philippine inter-island vessel operators,

but the majority of the fleet is owned by only ten major firms. In additionto the inter-island fleet, there are smaller craft providing low cost, short-haul transport of agricultural products for local as well as inter-islandmarkets, and barges are used extensively to move raw or refined sugar, rice,and other produce. Coastal transport is frequently a logical alternative in

areas where cross-island road construction is made difficult by mountainousterrain; thus numerous roadsteads and shallow water ports have been developedwhere land access to communities is severely limited.

1.14 The increasing regional specialization in production patterns andrural development has given inter-island shipping a new impetus to play amajor role in the Government's plans for increased food production andregional balance in economic and social development. The growing need forfood in deficit areas has to be met by increased production in surplus areassuch as Mindanao. This in turn, requires efficient marine transport of bothagricultural inputs and outputs. In recognition of this need to improveinter-island shipping services, the Bank provided a loan of US$20 million in1974 for a shipping project. Since 1977 ten interisland container vesselshave been put into service by major operators financed locally and more areexpected as port facilities are improved.

Civil Aviation

1.15 Manila, Cebu and Zamboanga, Philippines' international airports areserved by 20 international and regional airlines, including Philippine AirLines (PAL). The latter provides international services, and is the prin-cipal carrier for 78 domestic airports operated by the Government. Domesticpassenger traffic has increased by about 12% p.a. over the past six years,while air freight is still insignificant. With the assistance of a US$26

million loan from ADB, the Manila International Airport is being rehabilitatedand extended to meet the traffic demand expected by 1983.

C. Transport Planning, Coordination and Strategies

1.16 Until mid-1979, transport planning had been the joint responsibiltyof the National Economic and Development Authority (NEDA) and the Ministryof Public Works (MPW). As a central planning agency, NEDA had overall respon-sibility for public capital investments through its Infrastructure Program andProject Office, which reviewed and approved investments proposed by eachtransport operating agency. NEDA was assisted in this task by the Inter-Agency Technical Committee on Transport Planning (IATCTP), staffed by repre-sentatives from each transport agency, including the MPH and MPW. IATCTPprepared standards and guidelines for the formation of agency plans for devel-opment and coordination of transport programs and projects. It also servedas a forum for the resolution of operational problems of transport agencies.

1.17 MPW, the other major participant in the joint planning activity,used its Planning and Project Development Office (PPDO) to undertakeregional planning studies on infrastructure investments and formulate

- 6 -

priorities for major infrastructure projects. PPDO maintained liaison withNEDA and provided the bulk of technical input to transport planning. TheBoard of Transportation (BOT), as a semi-detached unit of the MPW, alsohandled the quasi-judicial function of granting routes to transportcompanies and enforcing rates and regulations for their operations on thebasis of IATCTP policy guidelines.

1.18 In July 1979 the Ministry of Transport and Communications (MOTC) wascreated to undertake transport planning, coordination and regulation. Itbecame operational with a small staff drawn mainly from PPDO of MPW and BOT.The Ministry is still evolving and is in the process of defining itsfunctions, expanding its staff and preparing to take necessary steps toabsorb the transport planning functions now discharged by NEDA. However, itwill be some time before MOTC can assume full responsibility for transportplanning, coordination and regulation. In the interim, MOTC will continue tobe assisted by NEDA, IATCTP and expatriate advisors.

1.19 One of the important transport planning activities is the Govern-ment's National Transport Systems Study (NTSS) undertaken in preparation ofa ten-year transport investment program. As a result of the Bank's Trans-port Planning Mission's recommendations, several resident planning advisorswere appointed in 1977 to assist the Government under the Manila UrbanDevelopment Project (Loan 1282-PH) in carrying out this study. The advisorswere expected to assist individual line agencies and MPW with mattersconcerning transport policy, coordination and modal planning. However,completion of the transport study has been delayed due to changes in theadvisory staff, a high turn-over among the counterpart team, and the lengthyperiod required for data collection. Accordingly, the Bank's Fourth HighwayProject (Loan 1661-PH) included additional advisory services to allowcompletion of the first phase of the transport study by mid-1980. Completionof the entire study is not expected until late 1981.

1.20 Transport improvement programs are designed to promote the Govern-ment's objectives of (a) increasing food production and rural incomes;(b) promoting regional balance in socio-economic development by establishinggrowth poles away from Metropolitan Manila; and (c) expanding industrialproduction for domestic and foreign markets. To increase transport capacityso that it can meet the growing demand, broad strategies are being pursuedconcerning two main aspects: investment and operational.

1.21 Investment strategies embody two major elements: (a) transportsector and program review; and (b) strengthening the planning capabilitiesof operating agencies. At the center, MOTC/NEDA are assisted by foreignadvisors to undertake review and evaluation of operating agency proposals fortheir consistency with i. sectoral and overall development objectives such asagricultural and industrial development; ii. financial resource availability;iii. inter-modal efficiency; and iv. agency implementation capabilities.Needless to say, the task of analyzing least cost solutions for theachievement of the desired development objectives is a complex one. It willtake long, deliberate and persistent efforts on the part of the Government

planners to effectively analyze feasible alternatives (e.g., a greaterutilization of existing facilities in lieu of new investments) and assesssocio-economic effects of major investment projects in arriving at optimalinvestment choices. However, a good beginning has been made by the Governmentin a systematic collection of data and analysis with which to undertakecoordinated investment programming.

1.22 To enable MOTC/NEDA to carry out inter-modal planning functions, theanalytical capacity of transport agencies both at the center and at theregional and provincial levels must be greatly strengthened. The Philippinearchipelago, with its chain of over 7,000 islands, provides a strong case fordelegating major planning responsibilities to regions and provinces. It is atthis level where relevant data must be assembled to identify specific trans-port problems, examine alternatives in terms of costs and benefits and rankpriorities on the basis of the intimate local knowledge of the transportfacilities under their control. Effective transfer and strengthening of localplanning responsibilities can be accomplished only in the long term. However,the Government has clearly established the direction in which it intends tomove.

1.23 In order to reduce the need for capital expenditures or, at least,make it possible to postpone investment needs, the Government is making anincreasingly greater effort to improve the operational efficiency of exist-ing facilities and administrative procedures. Plans are currently beingformulated to improve vehicle operations in Metropolitan Manila through acomprehensive scheme of traffic management. Greater attention is beingfocussed on the maintenance of roads and ports, and on a restructuring ofthe management staffing and procedures for port operations and transportregulation. These operational improvements would make existing and futureinvestments more productive and would yield much higher benefit cost ratiosthan similar sized investments in new projects.

D. Previous Bank Assistance in the Transport Sector

1.24 The Bank Group's assistance to support the Government's efforts tomodernize and expand the transport sector included the First Port Loan(290-PH) in 1961 amounting to US$8.5 million which financed procurement ofdredging equipment. However, US$1.1 million of the loan amount was cancelleddue to failure to operate and maintain the dredgers in an efficient manner.In 1973, a Second Port Loan (939-PH) of US$6.1 million was provided to assistthe expansion of two important ports on Mindanao: Cagayan de Oro in the northand General Santos in the south. Project completion was delayed by threeyears mainly because of retendering, dredger mobilization difficulties andinadequate project supervision control by BPW.

1.25 The Bank's First Shipping project was prepared to help modernize theold inter-island fleet, provide technical assistance to strengthen planningand administrative capabilities in the maritime industry sector and formulatea ten-year investment program for inter-island shipping. Until recently,

- 8 -

implementation of this project has been delayed by institutional problems.They related to the uncertainty about how various financial institutions wouldhandle interest rate issues and subloan administration and appraisal,subborrowers' reluctance to assume foreign exchange risks, and a disagreementabout how ship safety inspection is to be undertaken. Some of these issuesare now being resolved, and accordingly, the rate of commitment has increasedsubstantially.

1.26 The highway sector has received the bulk of the Bank's lending fortransport in the Philippines: four loans (Loans 731-PH, 950-PH, 1353-PH and1661-PH) totalling US$271 million have been made for the improvement ofimportant sections of national highways and connecting feeder roads, and for acountry-wide maintenance organization for national roads, includingimprovement of workshops and procurement of maintenance equipment, spare partsand workshop machinery. These projects have also helped to develop thePhilippine contracting industry through experience in fulfilling a steadilyincreasing stream of contracts. Philippine consulting firms have also gainedvaluable experience through their association with foreign consultants on thedesign of the project roads.

2. PORT SUBSECTOR

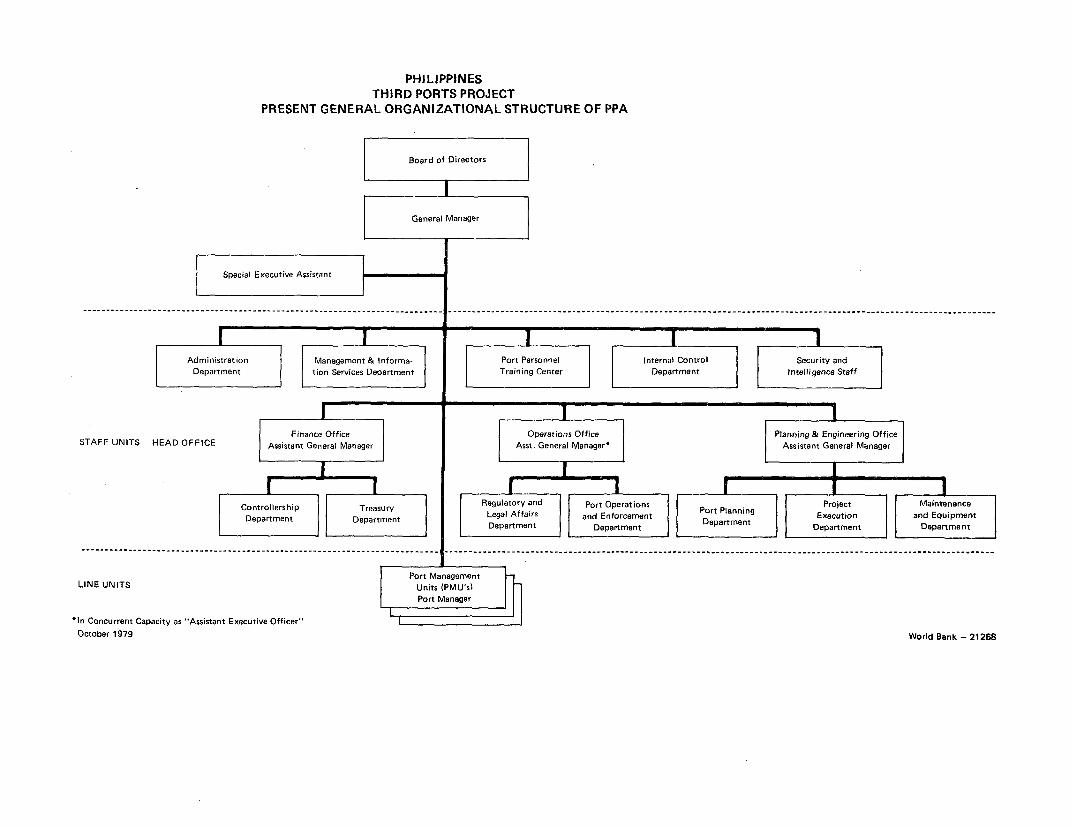

PPA Organization

2.01 PPA is a quasi-government corporate body created by PresidentialDecree in 1974. An amending decree in 1975 widened PPA's powers andfunctions which require the authority to develop, maintain, operate,supervise and regulate port services and facilities of national ports in thePhilippines. PPA's governing board, responsible directly to the Minister ofPublic Works, comprises seven directors, five of whom are cabinet ministers.The private sector is represented by one director, and PPA's general manageris a member ex-officio. PPA is empowered inter-alia to fix rates andcharges, determine terms and conditions of service for its employees broadlyconsistent with Civil Service rules and regulations, adopt recurrent incomeand expenditure budgets and capital expenditure budgets, invest surplusfunds in Government securities and borrow money after consultation with theCentral Bank and the Department of Finance and with the approval of thePresident. Dues, which are defined in the enabling decree as includingharbor fees, tonnage and wharfage dues, berthing charges, port dues, and anyother dues or fees imposed by virtue of existing law or the decree, areincreased or decreased by the President upon the recommendation of PPA, toprovide a satisfactory return on the Authority's assets and adjustments maybe similarly made to dues so as to reflect the costs of providing theservices.

2.02 During 1977 two Presidential Decrees (Nos. 1177 and 1234) resultedin fundamental changes to PPA's financial autonomy with effect fromJanuary 1,1978 by requiring PPA (and other agencies) to: (i) remit all

- 9 -

revenues to Treasury for crediting to a Special Account in the Government'sCeneral Fund; (ii) obtain quarterly, in advance, budget allotmentauthorization from the Government's Budget Commission to enable PPA funds tobe released by Treasury to meet recurrent and capital expenditures; and(iii) maintain financial records in accordance with governmental budgetaccounting rules. The application of these regulations has in the pastresulted in reduction by the Budget Commission of PPA's spending powersbelow the levels approved by PPA's own board. Some relief from budgetaryconstraints has been available to PPA for financing certain capital worksthrough the utilization of surplus funds (termed "corporate") which it hadaccrued up to December 31, 1977. However, these funds are gradually beingdepleted. In addition to maintaining commercial accounting records, PPA isnow required to provide supplementary financial data in compliance withgovernment budgetary procedures.

2.03 PPA's full-time General Manager (and ex-officio Vice-Chairman ofthe Board), who exercises day-to-day control, is an experienced and competentadministrator. Chart 21268 shows PPA's organization.

2.04 Port Management Units (PMUs) have been established at major nationalports with each PMU exercising control over neighboring minor national ports.There also exist over 200 private piers and wharves in the Philippines

from which traffic PPA derives revenues. Since its treation PPA's approvalis required before any private port can be constructed or expanded. There are

also some 390 municipal ports most of which offer only basic and simplelanding facilities for small craft.

Management, Staff and Training

2.05 M4anagement is generally very satisfactory, but there remains aneed to develop certain areas, in particular strengthen development projectplanning and execution, and improve financial and operational informationavailable to management to assist in both day-to-day control and corporateplanning.

2.06 The experience gained by PPA through the Third Ports ProjectFeasibility Study should be consolidated by allocating PPA's project planningand supervision activities to permanently staffed units suitably interlinked.A permanent planning division staffed with experienced engineers, economistsand statisticians is necessary to fulfill PPA's wide responsibilities indeveloping Philippine ports. The supervision of major projects also willrequire a nucleus of full-time engineers for years to come. Appropriateorganizational structure changes are now being considered by PPA to achievethese goals. PPA agreed during negotiations to discuss proposed majorchanges with the Bank prior to implementation [para. 6.02(a)] The establish-ment of a hydrographic division is required in view of PPA's extensivedredging responsibilities and the cost of related staff training and equipmentis included in the proposed project. The cost of a civil engineering adviserfor the duration of project construction, and training courses abroad forMPW and PPA port engineers is also provided under the proposed loan.

- 10 -

2.07 More accurate and succinct data are required for effective manage-ment control and to assist in corporate planning. The Bank's appraisalrevealed the inadequacy and inaccuracy of some of PPA's statistical datamuch of which is derived from shipping and arrastre companies. Consequentlymany productivity indices computed for PPA ports are unreliable. Moreemphasis is needed on quality rather than on quantity and greater presenta-tional uniformity is required to enable more useful comparisons to bemade especially of data supplied by PMUs. The scope, content and accuracyof financial reporting also needs improving substantially. The proposedproject includes the cost of a port experienced economist and a managementaccountant to assist PPA staff in these areas. These experts would alsoassist in the determifiation of reliable productivity indices which wouldenable PPA and the Bank to subsequently agree on suitable operationaltargets for the project ports. Agreement on these targets will be reachedby no later than December 31, 1981 [para 6.02(b)].

2.08 PPA operates a training school which was established in 1975 withILO/NORAD assistance. Initially the school trained stevedore and wharflabor; subsequently PPA introduced various work-oriented training coursesfor lower and middle management operational and administrative staff.

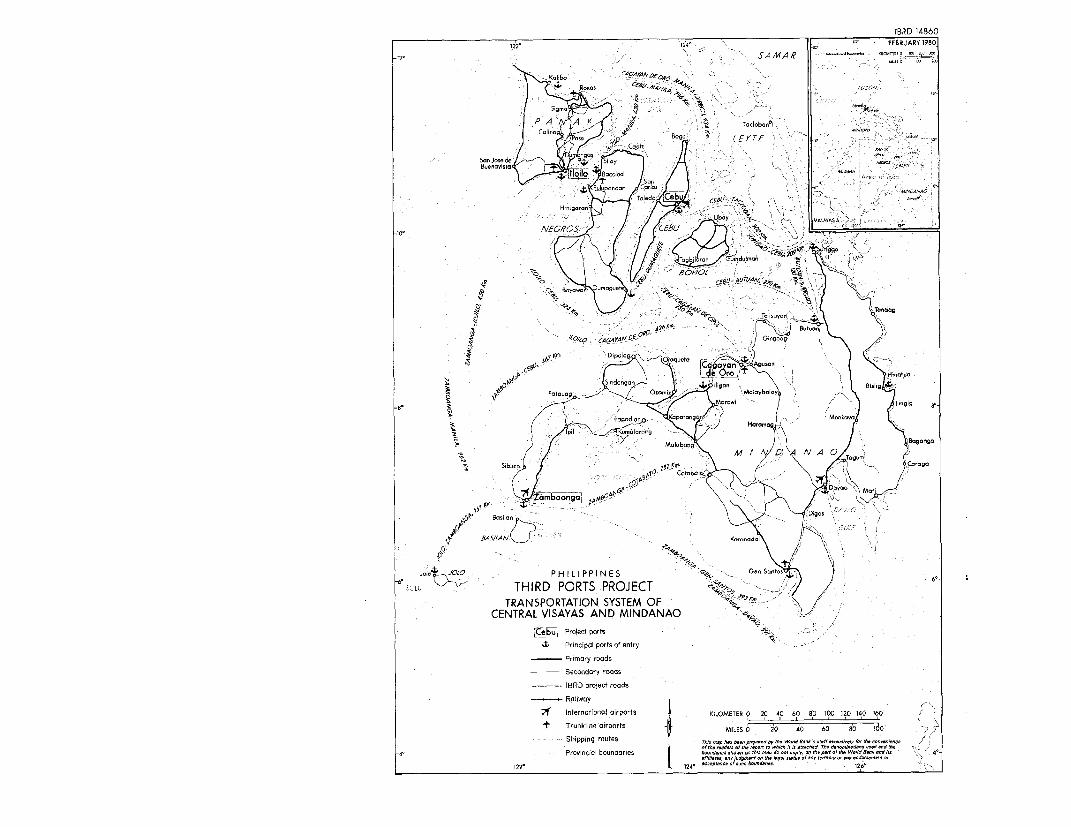

Existing Port Facilities (Map 14860)

2.09 Cagayan De Oro (Map 14771). Cagayan de Oro has a 451 m long,23 m wide marginal reinforced-concrete wharf on piled foundations, of which291 m consists of an earlier existing facility which was recently repairedand upgraded when a 160 m new extension was added, both sections having adredged alongside depth of 8.5 m below MLLW. The new extension wascompleted under the Second Ports Project which also provided paved storageand working areas behind the wharves, as well as transit sheds, administra-tive and other buildings, fencing and gates, drainage and other servicefacilities.

2.10 The tidal range is less than 1 m and siltation is virtuallynonexistent along the present wharves. However, to the south, where the nextextension is proposed, are shallow log-ponds divided by rock bulkheads.Currently, these log ponds are leased to private companies. Some 200 squatterhuts are also present outside the south boundary fence of the port. The earlytermination of the log-pond leases and their removal, and the relocationsatisfactory to the Bank of all huts encroaching within the proposed projectarea by no later than June 30, 1981 was agreed with the Government duringnegotiations [para. 6.01(a)]. The city government is already taking actionto move site occupants to an available temporary site pending finalresettlement in permanent quarters. The cost of relocation is estimatedat $40,000 to be borne by the relevant government agencies.

2.11 Just outside the proposed project area, an oil company has a tankfarm and supply depot. The incoming supply pipes cross the project area andare to be relocated. This was confirmed with PPA during negotiations.

2.12 The partly salvaged and partly submerged wreck of a small warshiplies to the south of the port, about 430 m from the existing wharf. As it

- 11 -

lies in the path of the proposed construction, its removal is included inthe project.

2.13 The 500 m long access road to the proposed project site will be anextension of a newly paved road leading from the Iligan-Cagayan de Oro-Butuanhighway to the recently completed Agora Market. Early right-of-wayacquisition will be necessary; both this and a construction schedule wasagreed by the Government during negotiations [para. 6.01(b)].

2.14 Cebu (Map 14770). Cebu has a narrow marginal waterfront for cargohandling, open storage and roadway. The width varies from 28 to 45 m overan overall length of 3.8 km with alongside depths of water varying between3 to 6.5 m below MLLW. Most of the berths are in poor condition. Exceptfor a 9 m alongside depth foreign berth and one 6.5 m alongside depthdomestic berth, maximum depth is 5 m due to existing structural foundationlimitations. In addition, there are three finger piers, each 33 m wide and155 m long, with alongside depths varying from 3 to 5 m below MLLIJ, whichare all in very poor condition. Existing structural foundation limitationsof the piers do not allow increasing the dredged depths beyond 5 m belowMLLW.

2.15 Tidal range is 1.6 m maximum; the tides are diurnal and currentsare insignificant. Some maintenance dredging is necessary, but informationis insufficient to determine necessary frequency and quantity. PPA proposesto conduct observations and review maintenance dredging requirements by nolater than December 31, 1982. This was agreed during negotiations[para 6.02(c)].

2.16 Some wrecks lie in the areas to be dredged for an access channelto the proposed quay. As removal powers do not rest solely with PPA, removalof these wrecks, which is not included in the project, was agreed by theGovernment during negotiations [para. 6.01(c)].

2.17 Iloilo (Map 14772). Iloilo has two sections of port facilities:(a) a narrow 10 m wide marginal waterfront extending about 2 km along thewest bank of the Iloilo river used by domestic traffic; and (b) a deep waterwharf for foreign and large domestic vessels located on the Iloilo straitside.

2.18 The river front wharves are generally of very old mass concreteand reinforced concrete construction, said to be built at the turn of thecentury, plans of which are no longer available. Part of the wharves aredeck platforms supported on open timber shallow depth piled foundations,which do not permit dredging alongside depths beyond 5 m below MLLW. Thewharf structures need extensive rehabilitation, but this is considereduneconomic as a main city street and a railway track frequently used forpassenger traffic prevent further widening of the narrow wharf aprons.

- 12 -

2.19 Heavy siltation occurs in the river and past dredging has providedonly temporary improvement to the channel. Siltation would rapidly fillthe dredged channels until stability was reached when depths returned tobetween 3 m and 4 m below MLLW. A detailed study of the siltation phenomenais necessary to determine whether more effective and less expensive measurescan and should be taken to maintain existing depths for craft using PPA andother upriver facilities, e.g. small ship repair yards. However, as alreadystated, depths alongside the river wharves cannot exceed 5 m due to structurallimitations. The cost of such a study is included in the project. The meantidal range in the river and in the Iloilo strait is 1.6 m.

2.20 Built in 1968, the deepwater wharf located just beyond and southof the mouth of the Iloilo river, faces the Iloilo strait. It is areinforced concrete wharf with a deck 12 m wide and 345 m long, on rein-forced concrete piled foundations, having a maximum alongside depth of 9 mbelow MLLW. A 140 m long, 18 m wide transit shed is located on the wharfstructure. An open shed for passengers, a private warehouse, and a smallcargo equipment maintenance workshop make up the port buildings in thisarea, all of which are in good condition. Road access to the city, securitylighting, water supply and fencing also are adequate. The berth nearest tothe mouth of the Iloilo river is subject to heavy siltation, whilst furtherexpansion at the other end is not possible because of exposure to heavy waveaction and erosion.

2.21 The site of the proposed quay for Iloilo lies north of themouth of the Iloilo river, and faces the Iloilo strait. It will be locatednortheast of the suburb known as Barrio Obrero. Since early construction ofa 1-km long temporary access road will be necessary to transportconstruction materials and equipment from the city to the project site, itscost is included in the project. Prompt acquisition of the right-of-way,and the construction of the road was agreed by the Government duringnegotiations [para. 6.01(b)]. Funds are also provided in the project for apermanent road access, its alignment to be decided when the proposed urbandevelopment of the new area behind the new port facility has been finalized.During negotiations the Government confirmed that suitable arrangements willbe made to construct a railway spur line for the conveyance of export sugarto the proposed quay.

2.22 Zamboanga (Map 14773R). Zamboanga has a tee-head jetty which wasconstructed prior to 1939. Constructed in reinforced concrete on open piledfoundations, the main wharf is 270 m long and 12 m wide, accessible to theshore by a skewed approach jetty of similar construction, 22 m wide, 165 mlong on its western side and 125 m long on its eastern side. A reinforcedconcrete finger pier addition, 54 m long and 9 m wide, joins the jettyapproach structure midway on its eastern side. Behind the approach jettyand contiguous to the port land, is a reinforced concrete sheet-piled

- 13 -

marginal wharf 268 m long with a paved apron 35 m wide, completed in 1964and extending eastward of the approach jetty0 Depths at the outer berths ofthe main wharf of the tee-head range from 5.6 m to 8.8 m below MLLW, at theinner berths from 5 to 7.1; at the finger pier from 5 to 5.8 m; and at themarginal whar£ from 3.7 to 5 m. Because of tidal currents averaging 1.5knots, only minor siltation occurs in the jetty head area. The mean tidalrange is I m.

2.23 The proposed extension is to be built west of the existingfacilities in a shallow basin used by fishing vessels. This basin isprotected by a small breakwater structure. The Kawa Kawa Boulevard, runsclose to the breakwater and will serve future port traffic once the proposedextension is completed. As the basin will be reclaimed for the newextension, arrangements for the relocation of the fishing vessels to anothersite will have to be made by no later than June 30, 1981, i.e., prior to newconstruction commencing at site. Timely port access road construction,linking Kawa Kawa Boulevard, included in the project, will also benecessary. These actions were agreed with the Government duringnegotiations [para. 6.01(b) and (d)].

Traffic

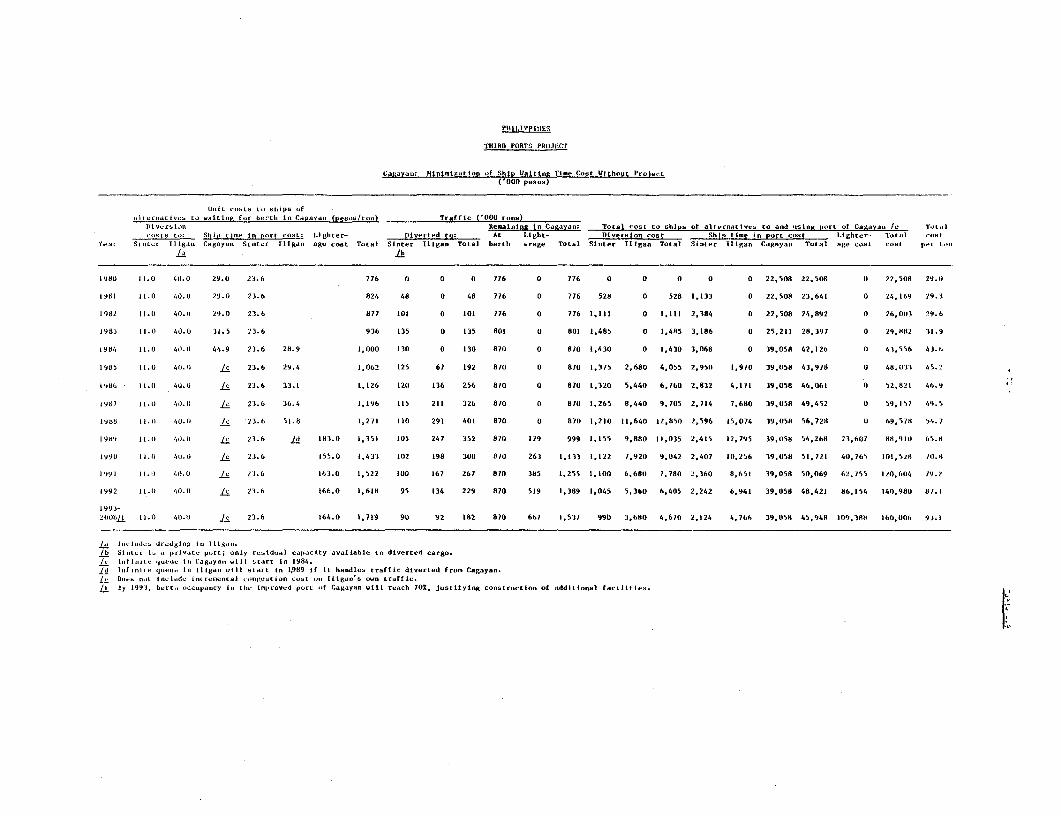

2.24 Reliable traffic data for most of PPA's ports are not availableprior to PPA completing the takeover of ports in December 1977. Subsequentto 1977 data on port cargo are reasonably reliable, however, passengertraffic statistics are still inaccurate (see para. 2.36).

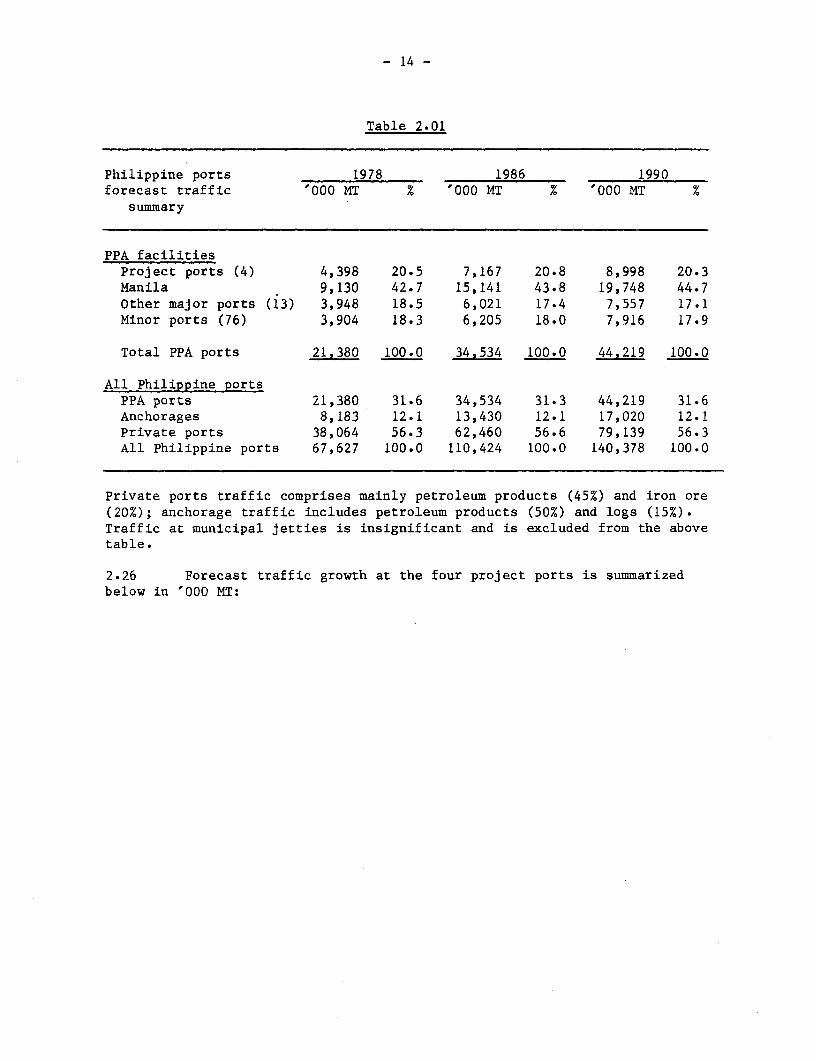

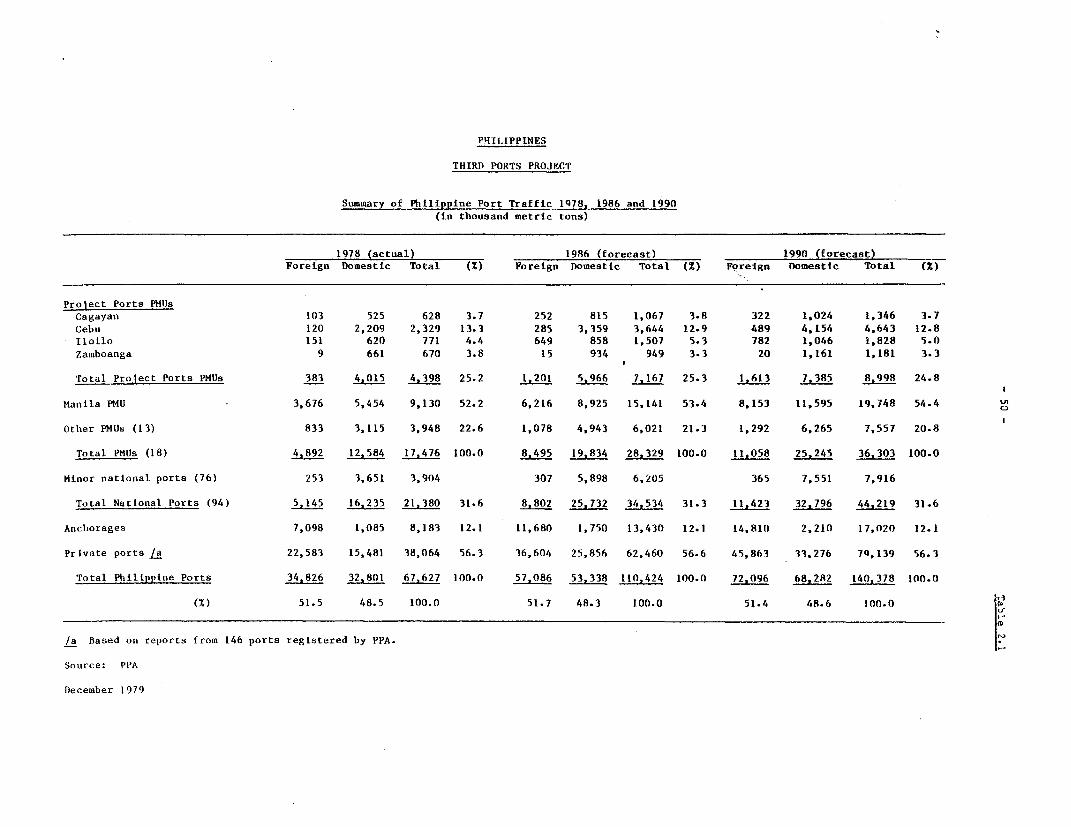

2.25 Cargo handled annually at all Philippine ports is expected to growfrom 67 million tons in 1978 to 110 million tons by 1986 and to 140 milliontons by 1990. PPA port facilities currently handle over 31% of totalPhilippine traffic and are expected to maintain this share. Details aregiven in Table 2.1 and summarized below:

- 14 -

Table 2.01

Philippine ports 1978 1986 1990forecast traffic '000 MT % '000 MT % '000 MT %

summary

PPA facilitiesProject ports (4) 4,398 20.5 7,167 20.8 8,998 20.3Manila 9,130 42.7 15,141 43.8 19,748 44.7Other major ports (13) 3,948 18.5 6,021 17.4 7,557 17.1Minor ports (76) 3,904 18.3 6,205 18.0 7,916 17.9

Total PPA ports 21,380 100.0 34,534 100.0 44,219 100.0

All Philippine portsPPA ports 21,380 31.6 34,534 31.3 44,219 31.6Anchorages 8,183 12.1 13,430 12.1 17,020 12.1private ports 38,064 56.3 62,460 56.6 79,139 56.3All Philippine ports 67,627 100.0 110,424 100.0 140,378 100.0

Private ports traffic comprises mainly petroleum products (45%) and iron ore(20%); anchorage traffic includes petroleum products (50%) and logs (15%).Traffic at municipal jetties is insignificant and is excluded from the abovetable.

2.26 Forecast traffic growth at the four project ports is summarizedbelow in '000 MT:

- 15 -

Table 2.02: PROJECT PORTS - FORECAST TRAFFIC SUMMARY('000 MT)

% increase1978 1986 1990 over 1978

Cagayan de OroForeign 103 252 322 213Domestic 525 815 1,024 95

Total 628 1,067 1,346 114

CebuForeign 120 285 489 307Domestic 2,209 3,359 4,154 88

Total 2,329 3,644 4,643 99

IloiloForeign 151 649 782 /a 418Domestic 620 858 1,066 72

Total 771 1,507 1,848 140

ZamboangaForeign 9 15 20 122Domestic 661 934 1,161 76

Total 670 949 1,181 76

/a Includes 213,000 tons of sugar currently handled atanchorage which will move across alongside berths from1984.

The above forecasts take into account major agricultural and forestry exports,including the extent to which they will be locally processed prior toshipment; import needs of these industries including fertilizers, machineryand construction materials; and consumer goods imports.

Operations

2.27 PPA is directly in charge of port administration, maintenance andsecurity at the project and other national ports, with the exception ofsecurity at Manila South Harbor which remains in the hands of the BOCpending a review of the situation by the Secretary of Defence. PPA does notemploy operational labor. Stevedoring and wharf cargo handling, and the

- 16 -

sorting, stacking and delivery to consignees of goods in PPA transit shedsare undertaken by private arrastre firms who supply all necessary mechanicalequipment. However, PPA staff monitor the activities of these companies toensure compliance with port regulations. Ship anchoring and berthingcontrol is exercised by PPA.

2.28 Most cargo is moved into and from the hold by ship's gear. Cargostored in sheds or open storage areas can remain free of charge in port forsix working days in the case of non-containerized foreign goods and twoworking days for domestic cargo. Foreign cargo in containers is allowedthree working days free storage. Penalty charges are then levied to induceconsignees to remove their goods promptly. PPA may also transfer non-delivered cargo to warehouse storage and charge consignees for removal coststhrough the arrastre operators. Ports operate 24 hours a day, though lessactivity occurs between 10 pm and 6 am as much of the cargo is currentlycarried by scheduled passenger-cargo vessels.

2.29 The Philippine Coast Guard is responsible for maritime andnavigational operations, communications with vessels at sea, lighthouses andother navigational aids. BOC carries out all customs activities within theport but has no control over the movement of goods within storage areas.PPA and arrastre working hours are adjusted to meet port needs. Goodworking relations prevail between PPA, BOC and the coast guard. Pilotage andtowage is by Pilots' Associations at the PMUs, subject to overall PPAsupervision.

2.30 Most of the cargo at the four project ports is handled by conven-tional break-bulk methods and operations are assisted by the use of pallets,forklifts, tractor/trailer units, mobile conveyors, etc. Between 1977 and1979 cellular container and side-loading RoRo ships have been introduced atCebu and Cagayan de Oro. Some of these and other ships also carry a rangeof non-standard boxes. On the more traditional interisland ships, efficientcargo handling is limited by the dominance of passenger needs in the shipdesign. Passenger decks cover much of the ship's length so that cargo canonly be handled from limited areas.

2.31 The designs of smaller ferries and local craft put further limitson cargo handling speeds. Passenger needs dominate the layout even moreand cargo is frequently carried in hatches below the passenger decks,reached by ladders. Movement to and from the shore is often by gangplankover the ship side or via small side-ports.

2.32 These constraints are compounded by narrow wharf aprons whichfurther hinder efficient and speedy cargo movements at all project portsexcept Cagayan de Oro. In Cebu, existing narrow marginal wharves can now bewidened by ten meters as the Philippine Estates Authority (PEA) recentlyagreed to allocate additional land to PPA for this purpose. However, atIloilo and Zamboanga, city development prevents any expansion of cargo

- 17 -

working areas at existing port sites. A further constraint, especially tothe improvement of existing wharves to cater for the expected growth incargo carried by larger vessels, is design limitations which preventdredging alongside most wharves below 5 m MLLW.

2.33 The proposed project focuses on providing additional cargo workingareas and deep water berths to handle expected growth in breakbulk cargoescarried in larger vessels and growth in container traffic which alsorequires deep water and larger land areas adjacent to the wharves for thehandling of containers. In addition, the proposed project will rehabilitateexisting marginal quay aprons at Cebu using the additional land recentlymade available. The nature and extent of productivity and other benefitsexpected from the proposed project are detailed in Chapter 4.

2.34 The large volume of passenger traffic on interisland vessels,which also mitigates against high cargo throughput, is expected to grow.Manifested passenger traffic in 1978 at the project ports was as follows:Cagayan de Oro 583,000; Cebu 3,527,000; Iloilo 1,828,000; and Zamboanga1,666,000.

2.35 The above figures are much lower than the actual numbers carried.Field surveys during 1979, showed underreporting of passengers in ships'manifests ranging between 60% and 200% in project ports. Several schemesdesigned to more effectively segregate passengers and cargo to facilitatefaster cargo working have been considered by PPA. However, most largeshipping companies are not convinced that the proposals are workable.Further studies both of the true volume and future trend of passengertraffic and suitable passenger facility improvement at PPA ports are clearlyneeded. Provision has been made for such studies in the proposed project.

2.36 The Loan Agreement under Loan 939-PH (Second Ports Project)provides that the number of cargo handling (arrastre) companies at eachproject port i.e. Cagayan de Oro and General Santos, be reduced to not morethan two. This measure was designed to avoid duplication of plant andequipment and diseconomies in operation and in the use of port labor. Priorto the creation of PPA, BOC reduced arrastre companies at Cagayan de Oro andGeneral Santos to one by encouraging the amalgamation of the numerous oper-ators. PPA eventually extended this policy to other ports.

2.37 The policy was recently challenged by the arrastre companies andthe dispute has been referred to a special committee set up by the Ministerof Public Works. An arrastre company in Cebu subsequently filed a courtsuit claiming that PPA has no power to determine the number of arrastrefirms operating in ports. Pending a decision by the court, the MinisterialCommittee has postponed consideration of the dispute.

2.38 There is clear evidence of operational improvements following thereduction of arrastre firms; however, shipowners have complained about themonopolistic attitude allegedly adopted by the sole arrastre organization

- 18 -

at Cagayan de Oro. The Bank considers that a port container complex, suchas proposed for Cebu, should be operated by only one arrastre firm in viewof the precise control over container movements and related cargo documenta-tion needed for efficient operation; and the need for the most economic useof expensive mechanical handling equipment. This conforms with the Govern-ment and PPA's policy embodied in a recent Presidential Decree governing theoperation of the Manila International Container Complex. At break-bulkberths, however, more than one arrastre firm could effectively be utilized,the exact number to be determined by the number and nature of berths at theport. During negotiations, the Government agreed that the number ofarrastre firms allowed to operate at the project ports be determined by PPAin consultation with the Bank (para. 6.01(e)].

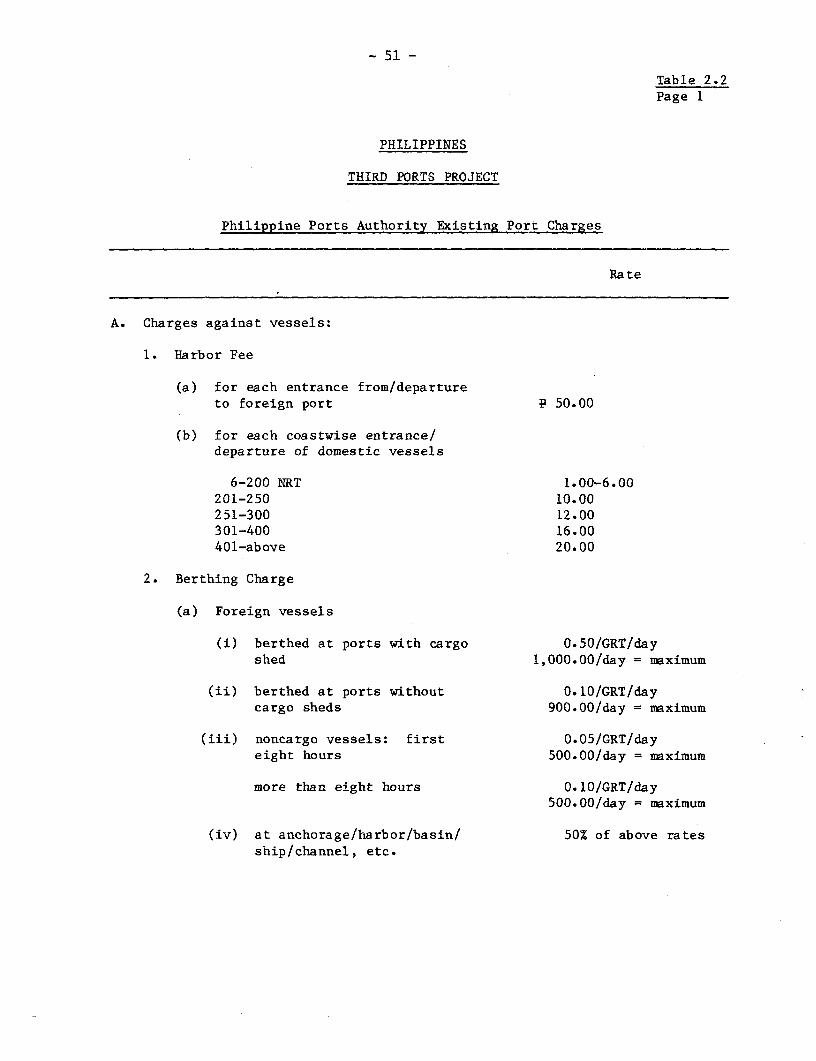

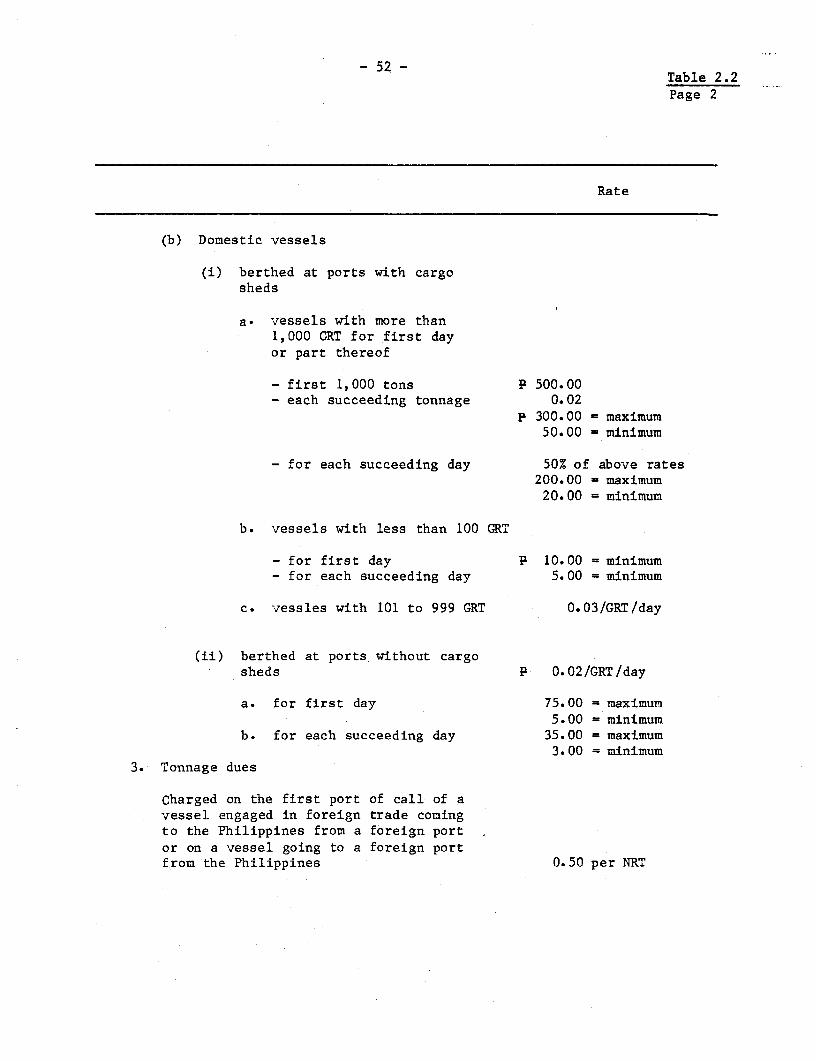

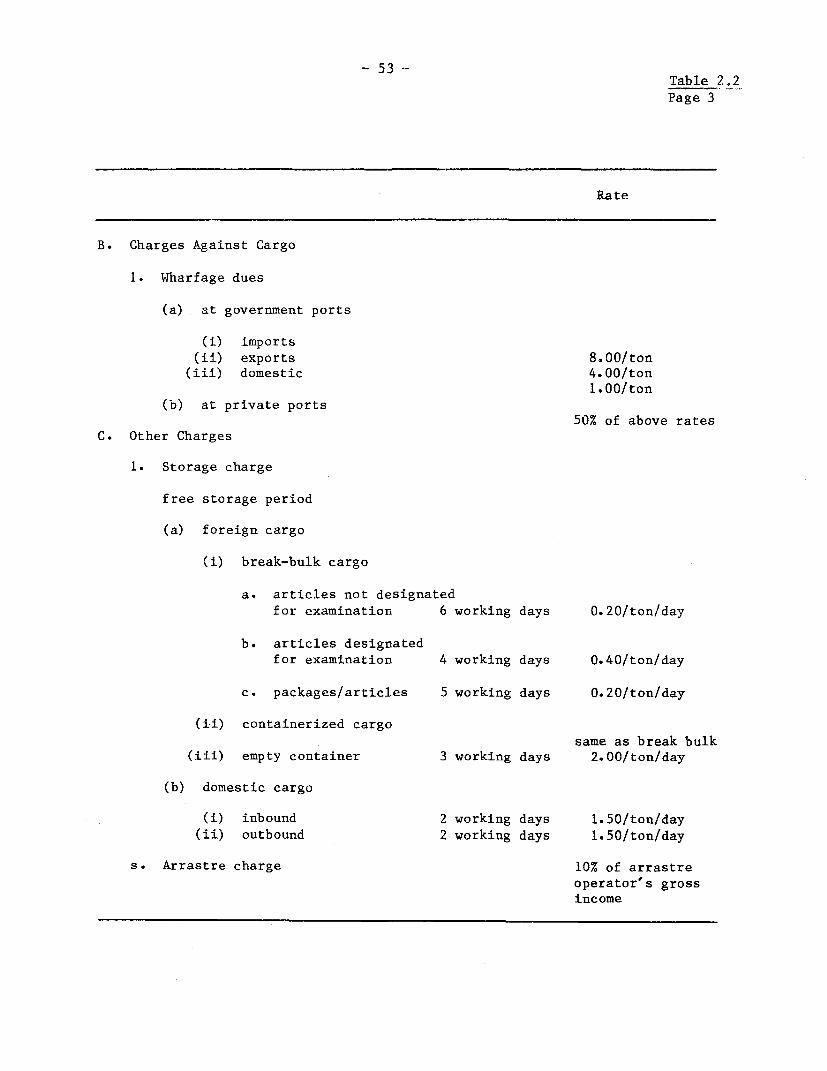

Tariffs and Costs

2.39 Tariffs for all PPA ports are regulated by PPA subject toPresidential concurrence. Most existing tariff levels were inherited by PPAin 1974 and have remained unchanged, with the exception of charges made byarrastre companies for cargo handling services, which were increased by 25%in June 1979 with PPA's approval. Tariffs are not cost based and are verylow compared to other ports in Southeast Asia. Principal PPA rates aregiven in Table 2.2. Substantial revisions upward are required to enable PPAto generate an adequate level of cash to meet a reasonable portion of futureport development expenditures. PPA staff were trained in tariff settingtechniques by consultants financed under Loan 939-PH (Second Ports Project)and are capable of recalculating new tariffs. They will be assisted byUNCTAD experts in establishing new tariffs for the international containercomplex in Manila.

2.40 PPA's level of operating costs is reasonable. Staffing is notexcessive; in fact government agencies are now required to hold costs at aslow a level as possible without unduly impairing efficiency. Currentstaffing levels are now being reviewed by a team comprising experts from thePresidential Reorganization Committee, the Ministry of Public Works and alocal firm of management consultants.

2.41 Recent government budgetary constraints required PPA to curtailexpenditure, particularly port maintenance on which only P 22 millionwas expended in 1979 i.e., only 1.2% of gross fixed assets in service(excluding land). Consequently, PPA's overall operating ratio in 1979 was alow 53%. Maintenance expenditure and operating ratios are expected to riseduring 1980-86. Nevertheless the operating ratio is expected to rangebetween 57% and 68% with the exception of 1983 when the ratio will probablyslightly exceed 70%. These ratios indicate a satisfactory relationshipbetween expenditure and revenue.

- 19 -

Budget, Accounting and Audit

2.42 PPA prepares detailed annual operating and investment budgets incommercial format which are approved by the board. In addition, sinceJanuary 1, 1978, PPA has prepared annual cash budgets in conformity withGovernment budgetary regulations and quarterly cash budgets required to obtainBudget Commission sanction for release of PPA funds from its Special Accountwith the Treasury.

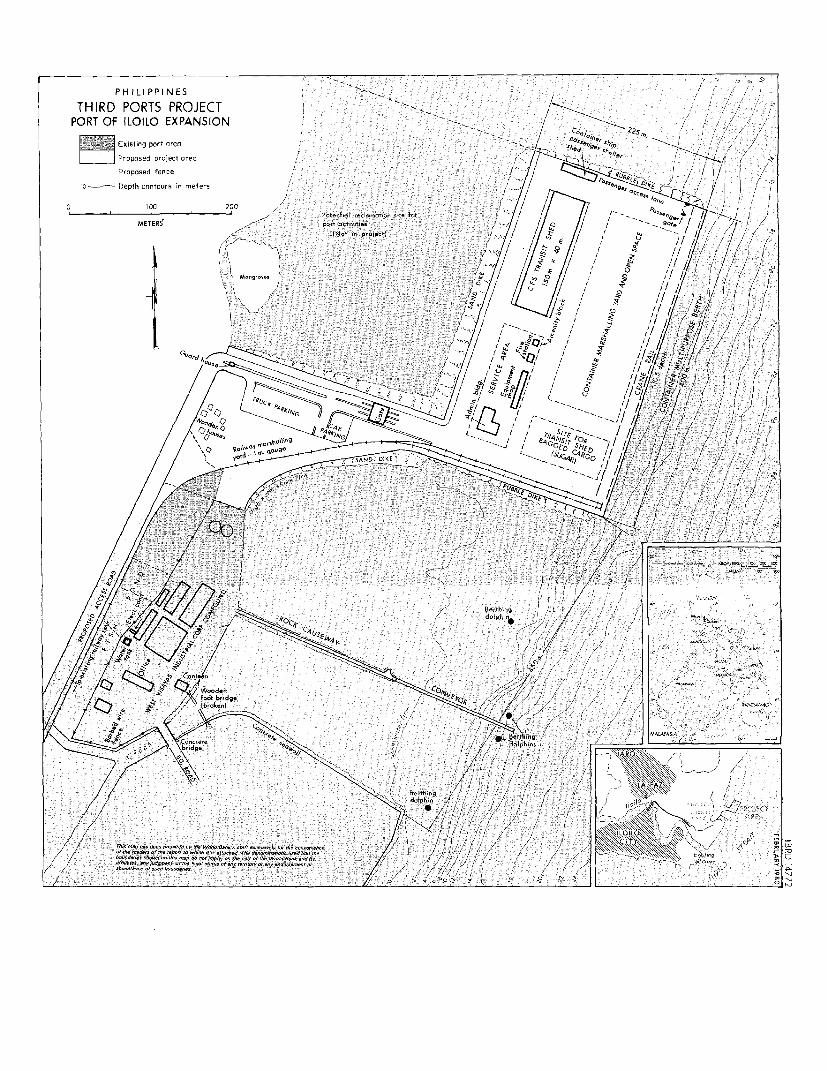

2.43 PPA's commercial accounting and costing systems were devised andintroduced with the assistance of consultants in 1977/78 financed under Loan939-PH (Second Ports Project). The system works well except that financialreporting to management needs to be improved (see para. 2.07).

2.44 PPA's governing decree provides for annual audit of the authority'saccounts by the Government's Commission on Audit. However, PPA may engage theservices of a private professional auditor or firm for the audit of itsaccounts in fulfillment of international contractual commitments of theauthority. Since PPA's creation, the Commission on Audit has promptly andsatisfactorily audited PPA's accounts. It was agreed during negotiations thataudited accounts for 1980 and thereafter be submitted to the Bank within sixmonths of each fiscal year end by auditors satisfactory to the Bank fpara.6.02(d)].

2.45 PPA operates an Internal Control Department the head of whichreports directly to the General Manager. The Department comprises two reviewand appraisal divisions, i.e., financial and operational management, employingten and seven staff respectively. The need for additional staff is beingreviewed (see para. 2.40).

3. INVESTMENT PLANI AND PROJECT

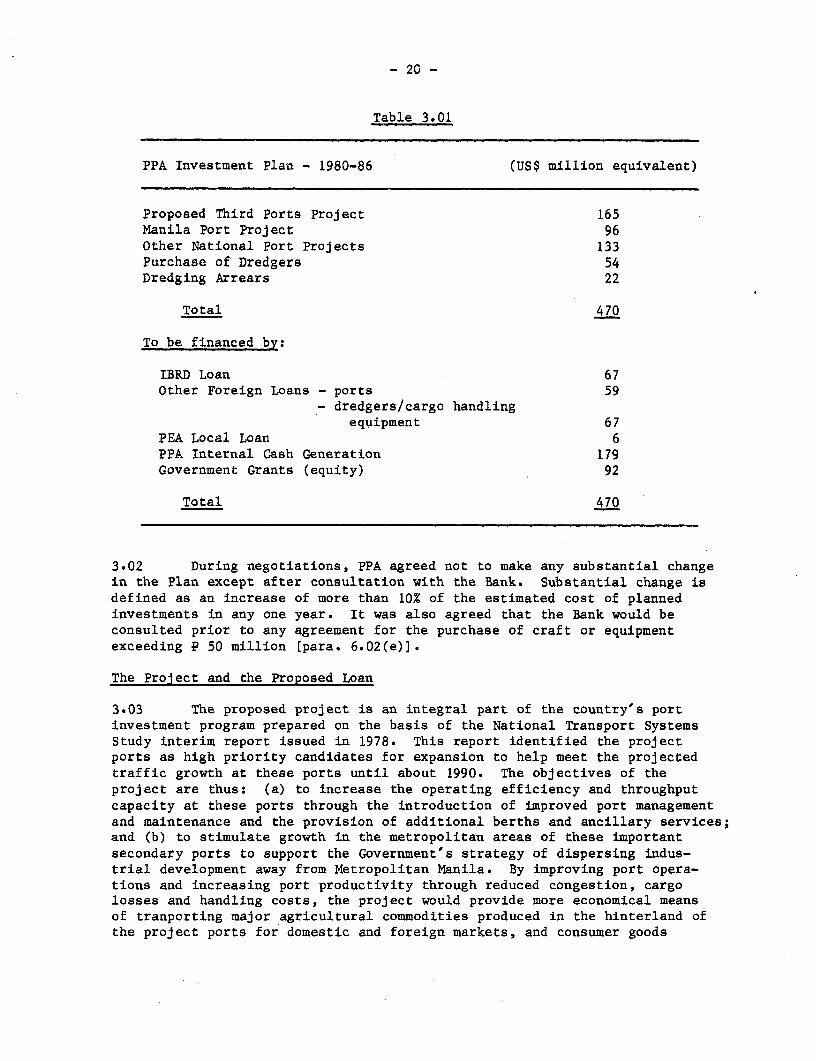

PPA's Investment Plan (1980-86)

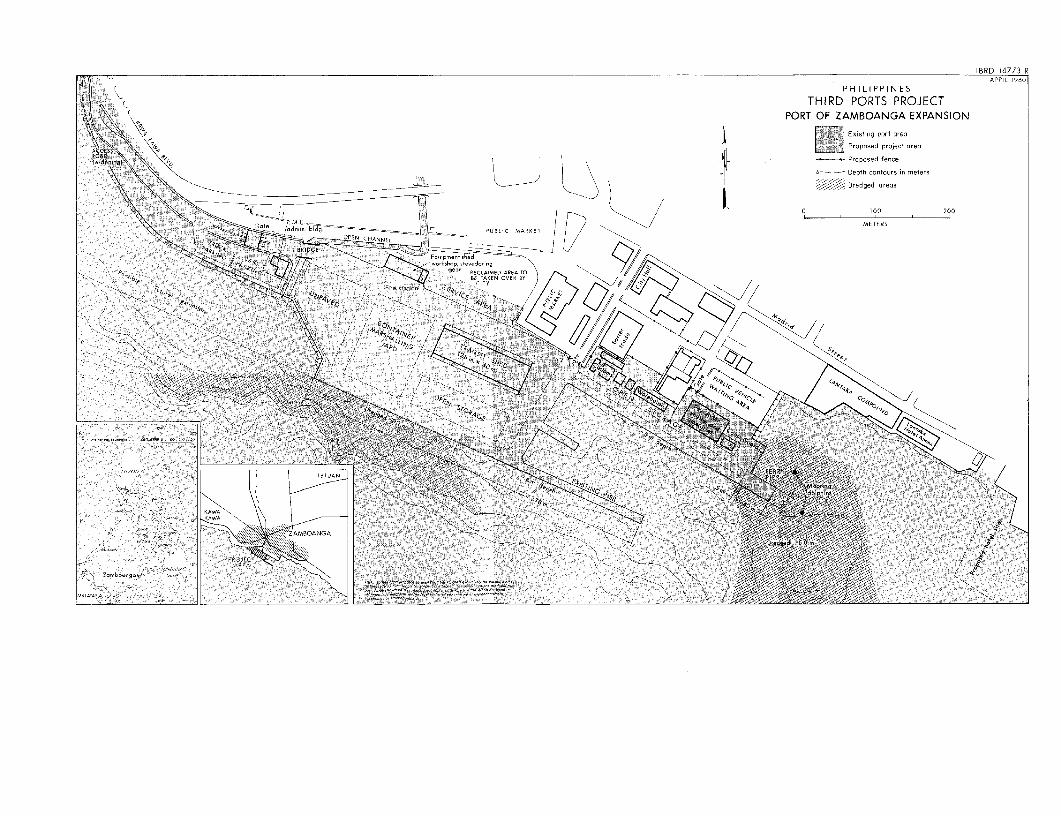

3.01 PPA's current Investment Plan covers the period 1980-86, andincludes major and minor projects at national ports identified as suitablefor investment. The Plan is indicative only insofar as about 50% ofprojected expenditure is concerned, relating to which neither feasibilitystudies nor preliminary engineering have yet commenced. A brief summary ofthe Plan and anticipated sources of finance are given below in Table 3.01.For purposes of this appraisal it is assumed that total Plan expenditureduring 1980-84 on other national port projects will amount to US$110 millioni.e. 17% less than the Plan provides, in view of possible national budgetaryand project technical supervisory staff constraints. The plan excludescapital works at municipal ports from which PPA does not derive anyrevenues. Such works will be constructed by MPW and be financed by theGovernment. Ownership of the municipal port assets after construction willnot be vested in PPA.

- 20 -

Table 3.01

PPA Investment Plan - 1980-86 (US$ million equivalent)

Proposed Third Ports Project 165Manila Port Project 96Other National Port Projects 133Purchase of Dredgers 54Dredging Arrears 22

Total 470

To be financed by:

IBRD Loan 67Other Foreign Loans - ports 59

- dredgers/cargo handlingequipment 67

PEA Local Loan 6PPA Internal Cash Generation 179Government Grants (equity) 92

Total 470

3.02 During negotiations, PPA agreed not to make any substantial changein the Plan except after consultation with the Bank. Substantial change isdefined as an increase of more than 10% of the estimated cost of plannedinvestments in any one year. It was also agreed that the Bank would beconsulted prior to any agreement for the purchase of craft or equipmentexceeding P 50 million [para. 6.02(e)].

The ProJect and the Proposed Loan

3.03 The proposed project is an integral part of the country's portinvestment program prepared on the basis of the National Transport SystemsStudy interim report issued in 1978. This report identified the projectports as high priority candidates for expansion to help meet the projectedtraffic growth at these ports until about 1990. The objectives of theproject are thus: (a) to increase the operating efficiency and throughputcapacity at these ports through the introduction of improved port managementand maintenance and the provision of additional berths and ancillary services;and (b) to stimulate growth in the metropolitan areas of these importantsecondary ports to support the Government's strategy of dispersing indus-trial development away from Metropolitan Manila. By improving port opera-tions and increasing port productivity through reduced congestion, cargolosses and handling costs, the project would provide more economical meansof tranporting major agricultural commodities produced in the hinterland ofthe project ports for domestic and foreign markets, and consumer goods

- 21 -

shipped from Manila for distribution in the influence areas of the projectports. The resulting increase in commerce between the major domesticmarkets near Metropolitan Manila and the project ports is expected tostimulate the economy of the project ports and their hinterland.

3.04 The project's major beneficiaries are interisland ship operatorswho have long suffered from inadequate port facilities with resultant slowturnaround time and high port costs which normally amount to 30% of shipoperating costs. Increased berth throughput of cargo per meter of quayreduces port costs per ton and permits more round voyages per ship peryear, and therefore fewer ships per route. The project will also encouragefurther investment in container vessels with resultant lower per tonshipping costs. Considering the high level of competition among shipoperators, a large portion of reduced operating costs is expected to bepassed on to shippers in the form of lower tariff or rebates, most of whichwould be passed on to the ultimate consumers. Resource cost savings to thecountry's economy are also considerable as the project would eliminate orreduce unnecessary costs associated with port operations.

3.05 The proposed project is based upon findings of port feasibilitystudies, financed under Loan 1048-PH (Shipping) and conducted by PPA and itsconsultants as modified by the Bank's appraisal conducted in October 1979.While it would have been desirable also to finance works at some minorports, it was generally felt by the government and the Bank that these havea somewhat lower priority and given resource constraints and inadequate dataon required improvements, should not be included in the project.

Description of the Main Project Items

3.06 The project consists of:

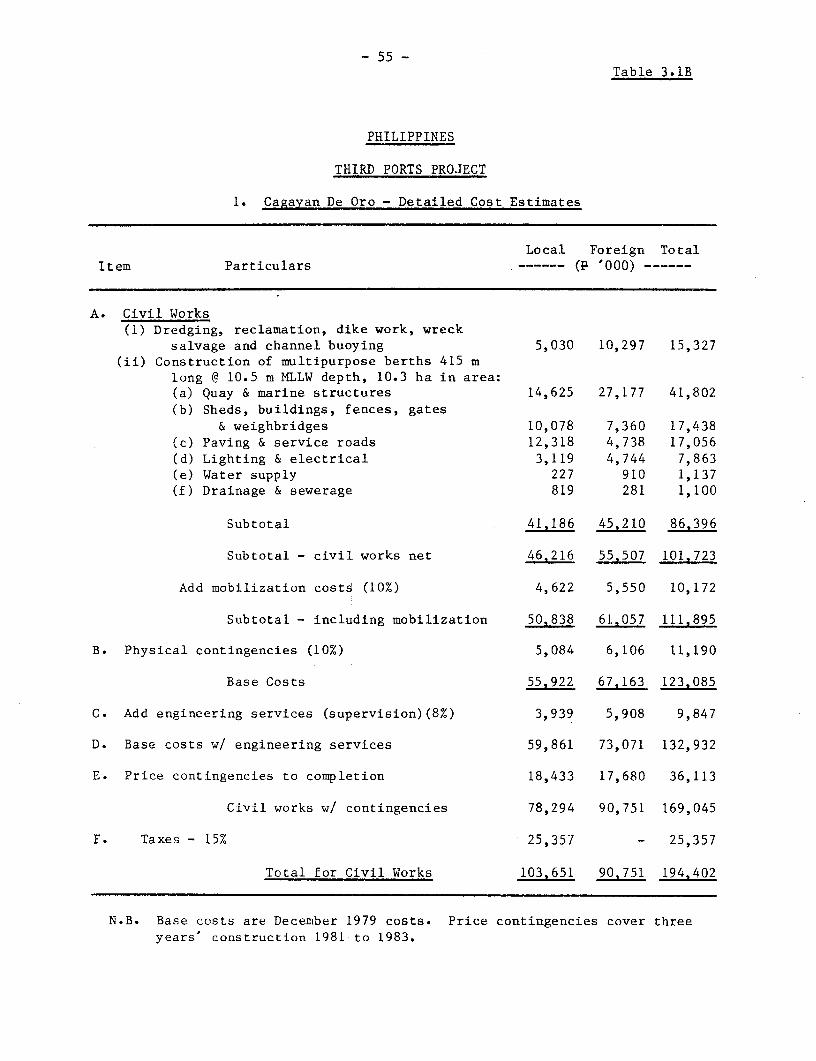

(a) at the port of Cagayan de Oro (Map 14771);

(i) 415 m of quay extension with an alongside depth of 10.5 mbelow MLLW, providing deep-water common user multipurposeberths;

(ii) one open transit shed 4,600 sq m for timber products storageand export, and one container freight station-cum-transitshed 5,500 sq m for the handling of container traffic;

(iii) ancillary works including surface roads and open areas total-ling about 46,000 sq m, services for water, electric supply,lighting, sewerage and drainage, weighbridges, separateaccess gate and security fencing;

(iv) engineering services for final engineering, bid evaluationand award and supervision of construction;

- 22 -

(b) At the port of Cebu (lIap 14770):

(i) dredging and disposal of about 460,000 cu m of spoil for theprovision of a deep water access navigation channel to adepth of 9.5 m below MLLW;

(ii) construction of 550 m of quay with an alongside depth of9.5 m below MLLW, providing deep-water common usermultipurpose berths;

(iii) one container freight station-cun-transit shed 7,800 sq m;

(iv) ancillary works including surface roads and open areas total-ling about 89,500 sq m, an administration building, equipmentand passenger sheds, and services for water, electricsupply, lighting, sewerage and drainage, weighbridges, accessgates and security fencing;

(v) rehabilitation and upgrading of existing marginal quayaprons and circulation roads, including provision of servicesfor water, electric supply, lighting, drainage and portperimeter security fencing;

(vi) engineering services for final engineering, bid evaluation andaward and supervision of construction;

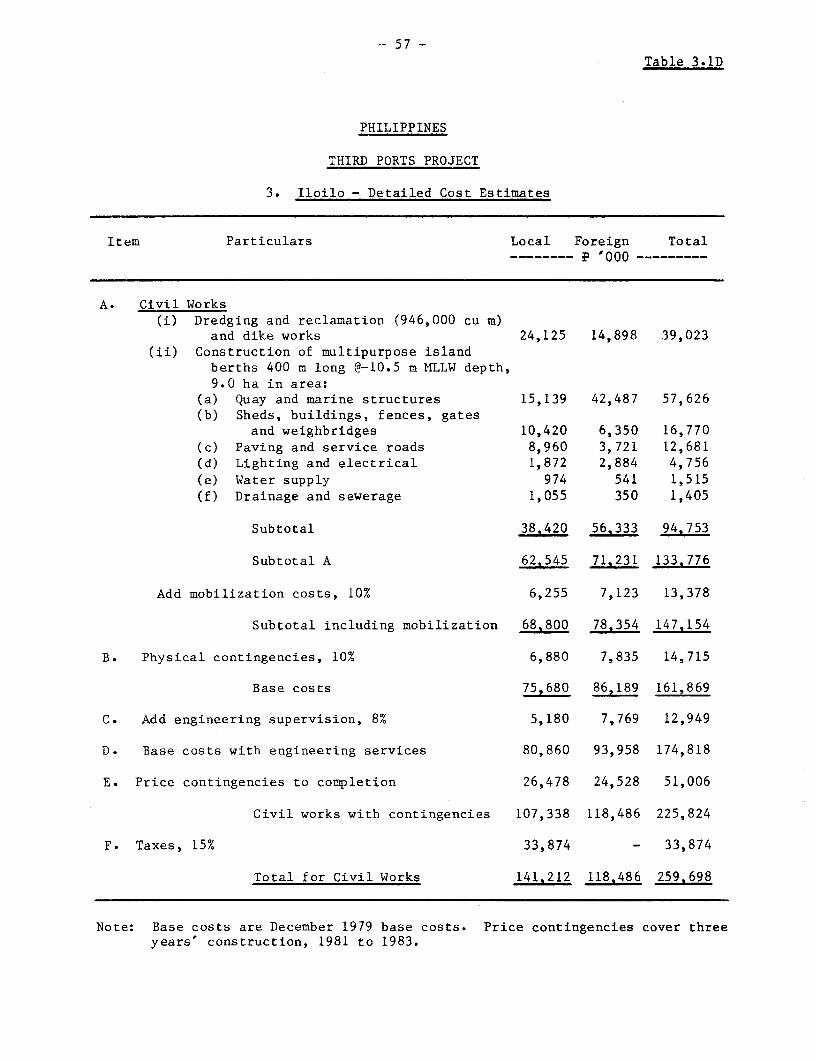

(c) at the Port of Iloilo (MIap 14772)

(i) dredging of about 460,000 cu m of spoil, reclamation and fillof about 946,000 cu m and dike works, for the provision of anisland wharf terminal;

(ii) construction of 400 m of quay with an alongside depth of10.5 m below MLLW, providing deepwater common usermultipurpose berths;

(iii) one container freight station-cun-transit shed 6,000 sq m;

(iv) ancillary works including surfaced roads and open areastotalling about 77,000 sq m, an administration building, firestation, and services for water, electric supply, lighting,sewerage and drainage, weighbridges, access gate and securityfencing;

(v) engineering services for final engineering, bid evaluation andaward and supervision of construction;

(d) at the Port of Zamboanga (M4ap 14773R)

(i) dredging and reclamation of about 505,000 cu m of generalfill, and attendant dike works, in the proposed extension;

- 23 -

(ii) 220 m of quay extension with an alongside depth of 10 m belowMLLW, providing deep-water common user multipurpose berths;

(iii) one container freight station-cum-transit shed 5,500 sq m;

(iv) ancillary works including surfaced roads and open areastotalling about 100,400 sq m, an administration building,fire station, amenities building for port labor, equipmentshed, an office block for Customs and relevant Governmentagencies, and services for water, electric supply, lighting,sewerage and drainage, weighbridges, access gate and securityfencing;

(v) rehabilitation and repair of damaged sections of the existingtee-head jetty;

(vi) addition of a new 50 m pier with mooring dolphins, a newpassenger waiting shed and an embarkation area at theexisting small craft ferry basin;

(vii) engineering services for final engineering, bid evaluationand award and supervision of construction;

(e) provision of external access roads for the ports of Cagayan deOro, Iloilo and Zamboanga;

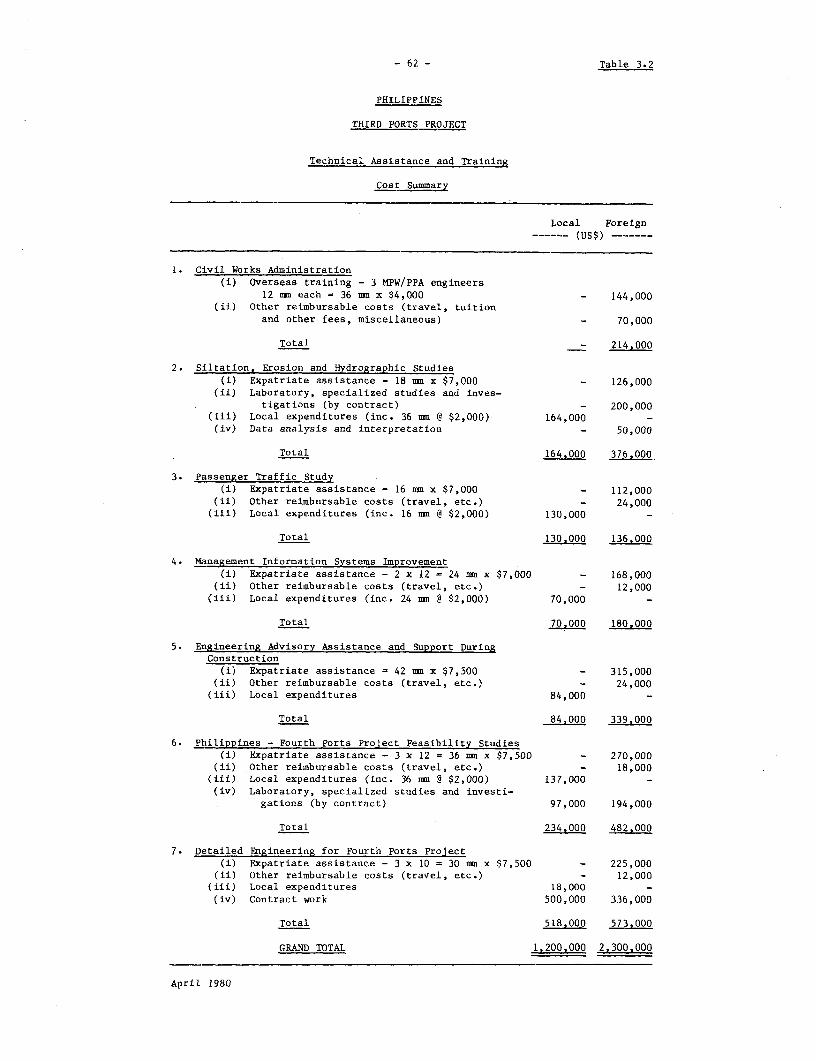

(f) technical assistance and training for:

(i) siltation and hydrographic studies at the project ports ofCebu and Iloilo and a study of seabed erosion at Cagayan deOro (Annex 1), a civil engineering adviser for the durationof project construction, and staff training for MPW and PPAengineers and for setting up a hydrographic survey unitwithin PPA;

(ii) the study of the effect which increased container serviceswill have on the number, type and scheduling of vessels forinterisland passenger sea transport, and consequent nationalport passenger facility development needs (Annex 1);

(iii) feasibility studies including detailed engineering, requiredfor a future ports project (Annex 1); and

(iv) improving PPA's management information system (Annex 1).

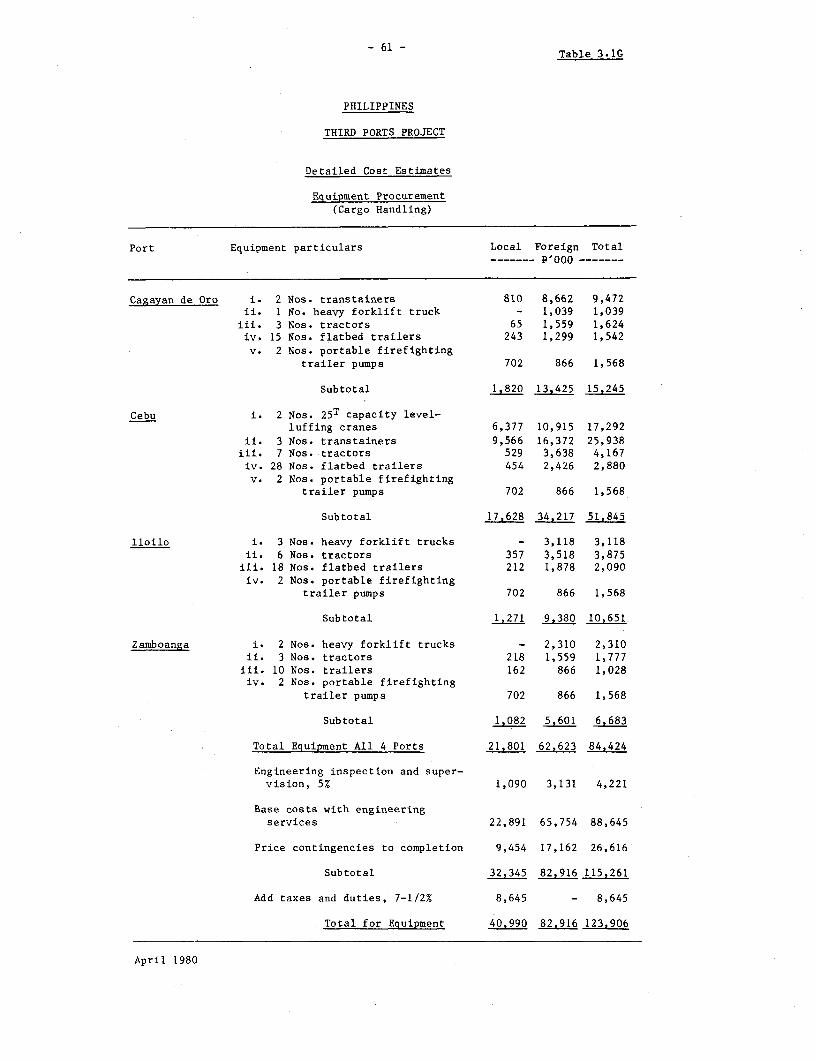

(g) provision of essential mechanical cargo handling equipment for theproject ports.

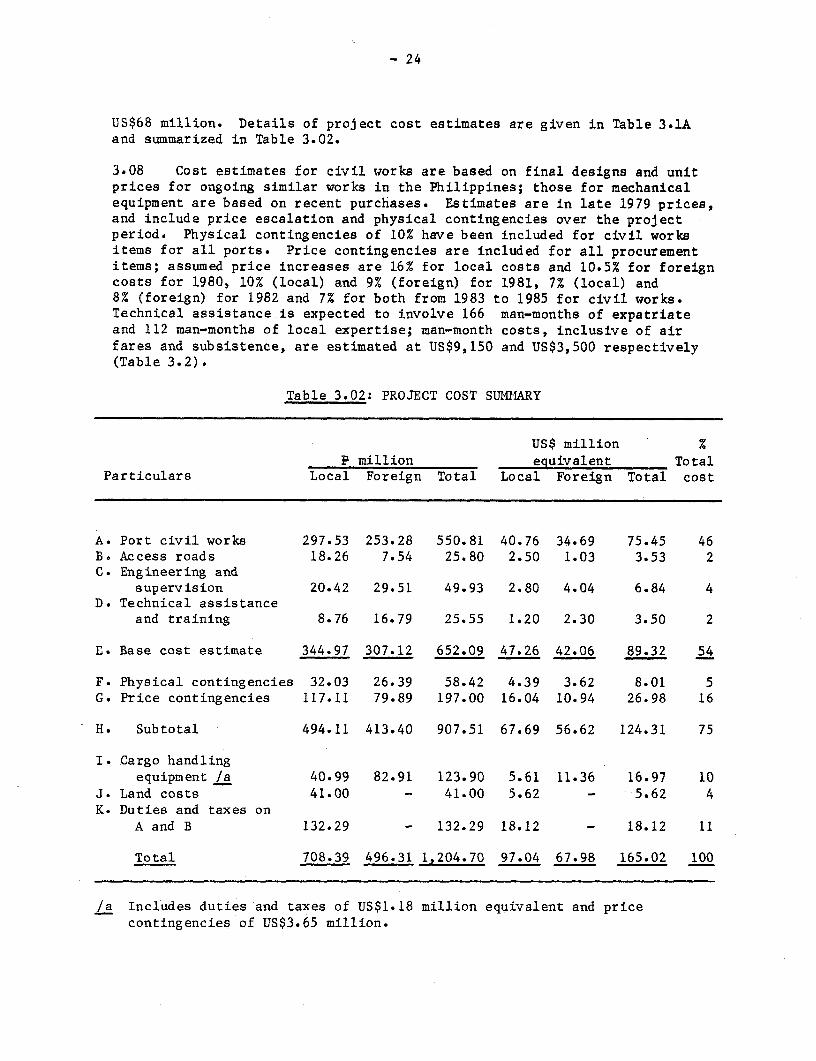

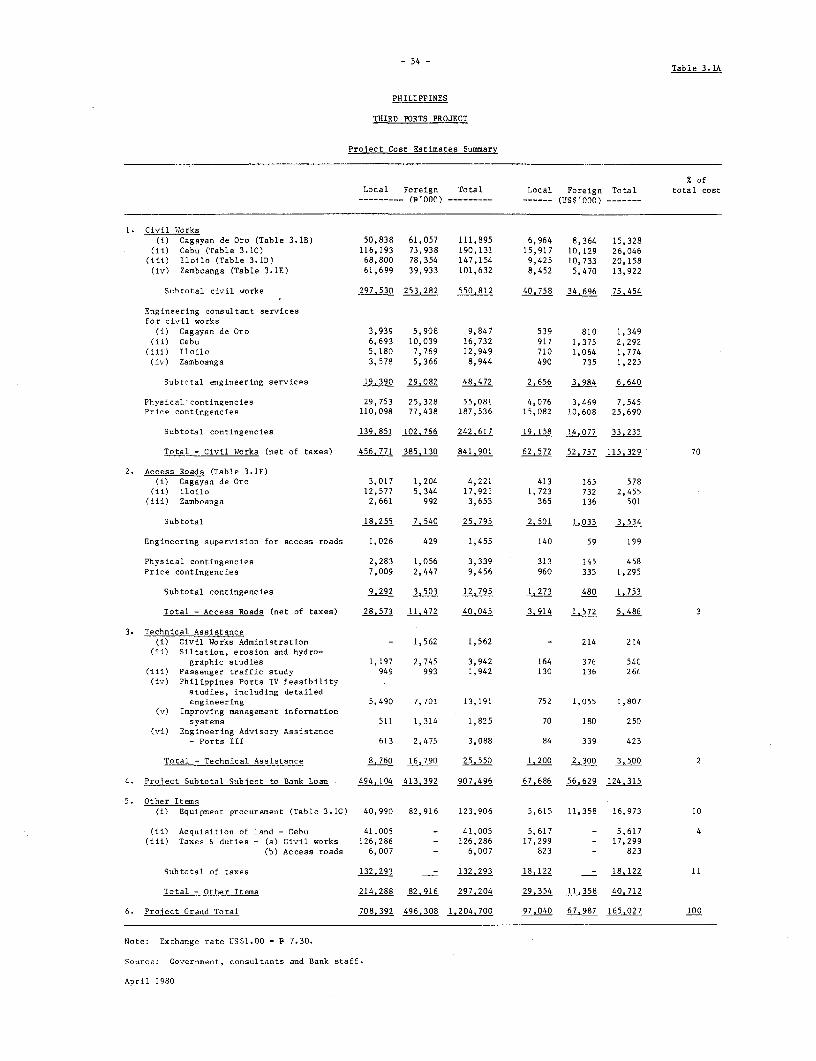

Cost Estimates

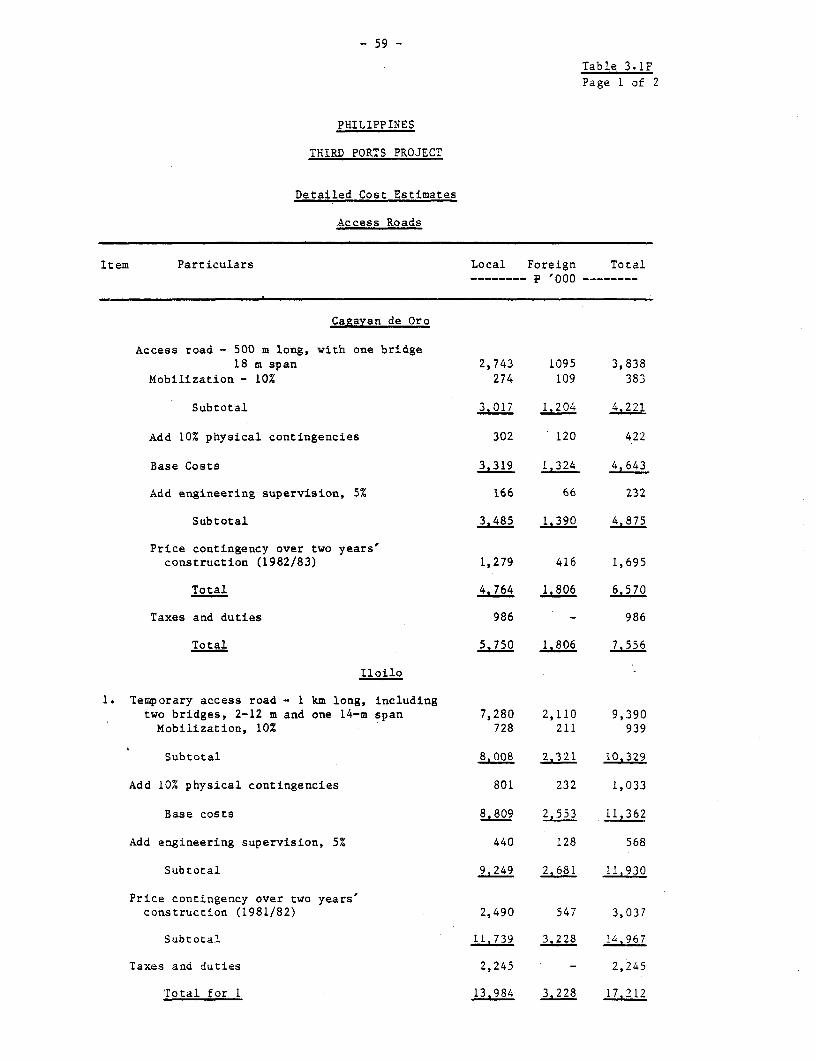

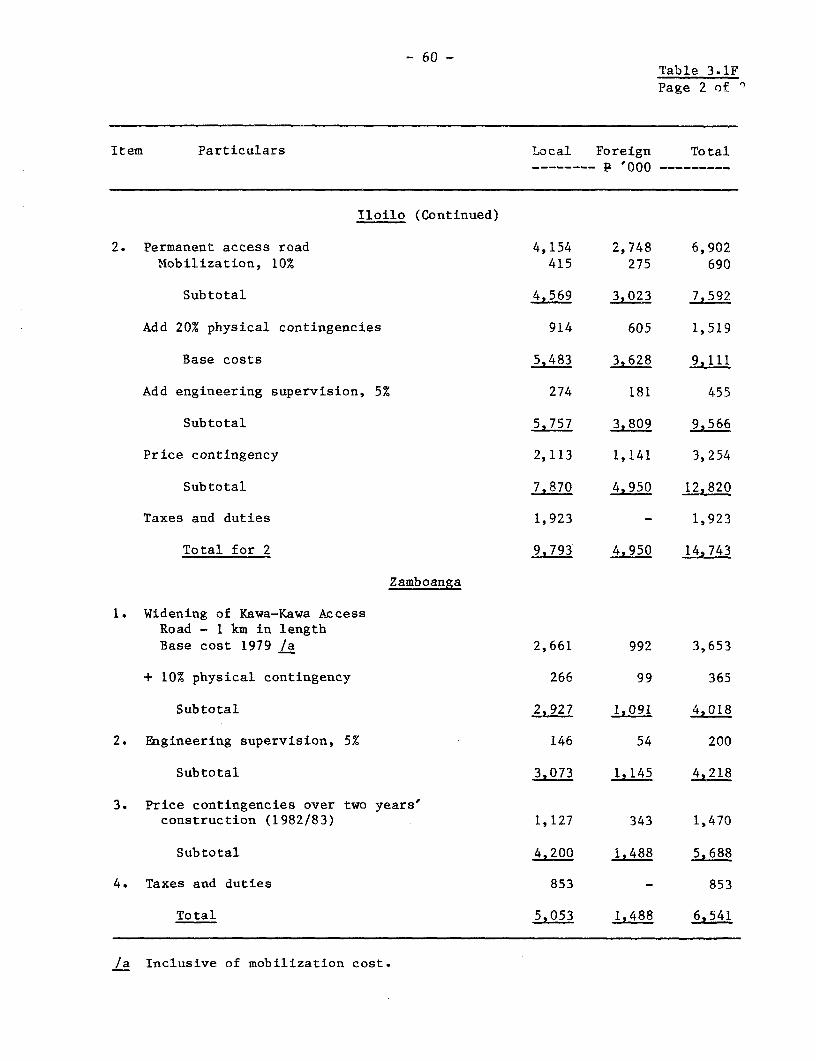

3.07 Total cost of the project is estimated at I 1,204.7 million(US$165 million equivalent) with a direct foreign exchange component of

- 24

US$68 million. Details of project cost estimates are given in Table 3.1Aand summarized in Table 3.02.

3.08 Cost estimates for civil works are based on final designs and unitprices for ongoing similar works in the Philippines; those for mechanicalequipment are based on recent purchases. Estimates are in late 1979 prices,and include price escalation and physical contingencies over the projectperiod. Physical contingencies of 10% have been included for civil worksitems for all ports. Price contingencies are included for all procurementitems; assumed price increases are 16% for local costs and 10.5% for foreigncosts for 1980, 10% (local) and 9% (foreign) for 1981, 7% (local) and8% (foreign) for 1982 and 7% for both from 1983 to 1985 for civil works.Technical assistance is expected to involve 166 man-months of expatriateand 112 man-months of local expertise; man-month costs, inclusive of airfares and subsistence, are estimated at US$9,150 and US$3,500 respectively(Table 3.2).

Table 3.02: PROJECT COST SUMM9ARY

US$ million %P million equivalent Total

Particulars Local Foreign Total Local Foreign Total cost

A. Port civil works 297.53 253.28 550.81 40.76 34.69 75.45 46B. Access roads 18.26 7.54 25.80 2.50 1.03 3.53 2C. Engineering and

supervision 20.42 29.51 49.93 2.80 4.04 6.84 4D. Technical assistance

and training 8.76 16.79 25.55 1.20 2.30 3.50 2

E. Base cost estimate 344.97 307.12 652.09 47.26 42.06 89.32 54

F. Physical contingencies 32.03 26.39 58.42 4.39 3.62 8.01 5G. Price contingencies 117.11 79.89 197.00 16.04 10.94 26.98 16

H. Subtotal 494.11 413.40 907.51 67.69 56.62 124.31 75

I. Cargo handlingequipment /a 40.99 82.91 123.90 5.61 11.36 16.97 10

J. Land costs 41.00 - 41.00 5.62 - 5.62 4K. Duties and taxes on

A and B 132.29 - 132.29 18.12 - 18.12 11

Total 708.39 496.31 1,204.70 97.04 67.98 165.02 100

/a Includes duties and taxes of US$1.18 million equivalent and pricecontingencies of US$3.65 million.

- 25 -

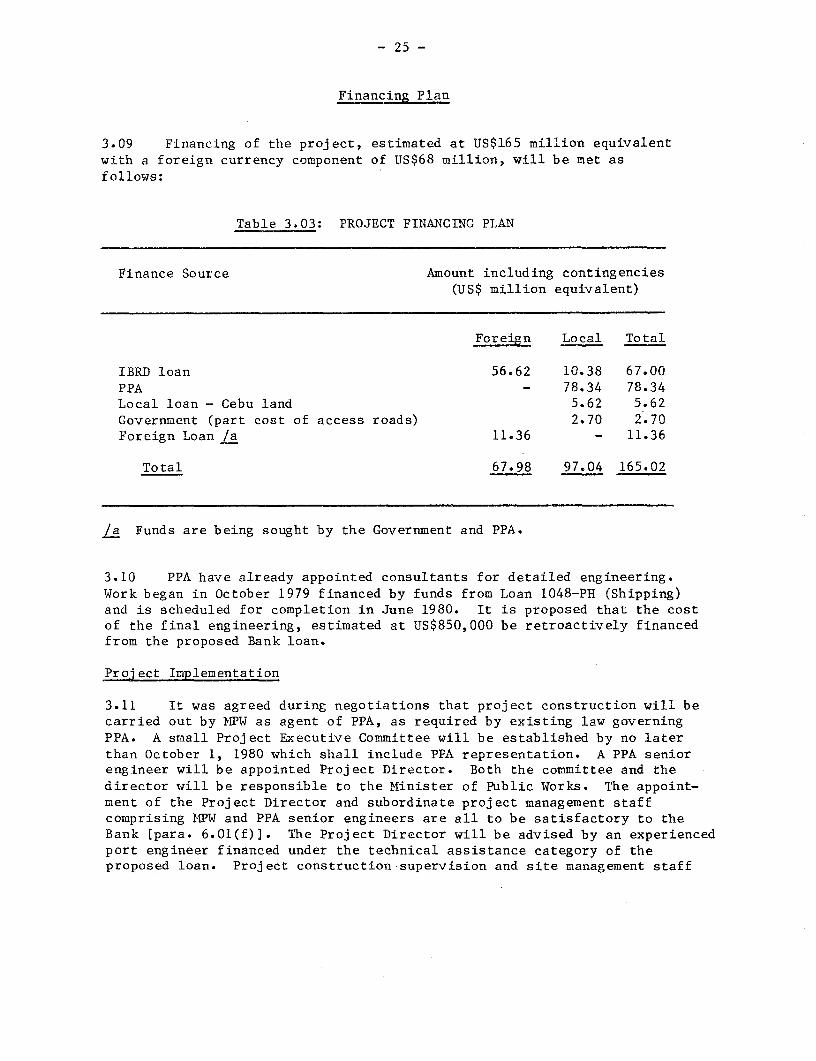

Financing Plan

3.09 Financing of the project, estimated at US$165 million equivalentwith a foreign currency component of US$68 million, will be met asfollows:

Table 3.03: PROJECT FINANCING PLAN

Finance Source Amount including contingencies(US$ million equivalent)

Foreign Local Total

IBRD loan 56.62 10.38 67.00PPA - 78.34 78.34Local loan - Cebu land 5.62 5.62Government (part cost of access roads) 2.70 2.70Foreign Loan /a 11.36 - 11.36

Total 67.98 97.04 165.02

/a Funds are being sought by the Government and PPA.

3.10 PPA have already appointed consultants for detailed engineering.Work began in October 1979 financed by funds from Loan 1048-PH (Shipping)and is scheduled for completion in June 1980. It is proposed that the costof the final engineering, estimated at US$850,000 be retroactively financedfrom the proposed Bank loan.

Project Implementation

3.11 It was agreed during negotiations that project construction will becarried out by I4PW as agent of PPA, as required by existing law governingPPA. A small Project Executive Committee will be established by no laterthan October 1, 1980 which shall include PPA representation. A PPA seniorengineer will be appointed Project Director. Both the committee and thedirector will be responsible to the Minister of Public Works. The appoint-ment of the Project Director and subordinate project management staffcomprising MPW and PPA senior engineers are all to be satisfactory to theBank [para. 6.01(f)]. The Project Director will be advised by an experiencedport engineer financed under the technical assistance category of theproposed loan. Project construction supervision and site management staff

- 26 -

will be assisted by consulting engineers acceptable to the Bank, upon termsand conditions, including provision for training engineering personnelsatisfactory to the Bank [para. 6.01(g)]. The appointment of foreign and/orlocal consultants/advisors for technical assistance and training shall alsobe upon terms and conditions satisfactory to the Bank [para. 6.02(f)].

Procurement and Disbursement

3.12 The project civil works would be executed under not more than four

civil engineering contracts, to be awarded on the basis of internationalcompetitive bidding, in accordance with Bank guidelines. The Government

intends to levy import duties on items procured for the project.

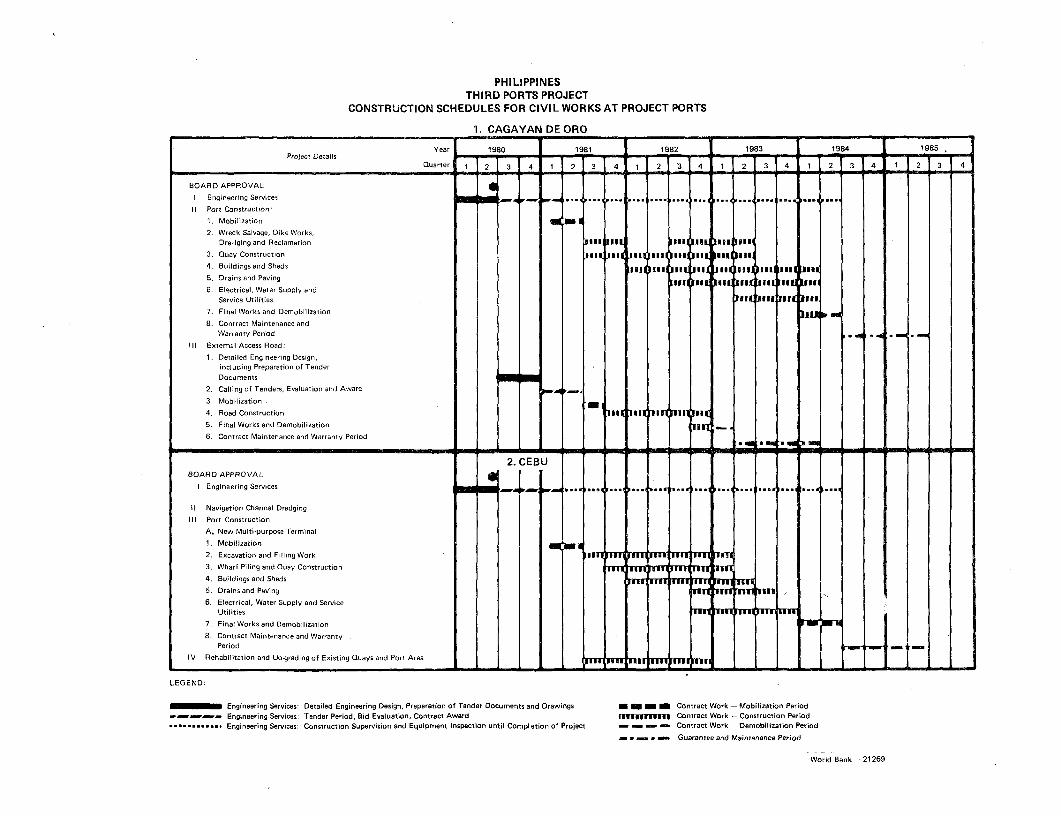

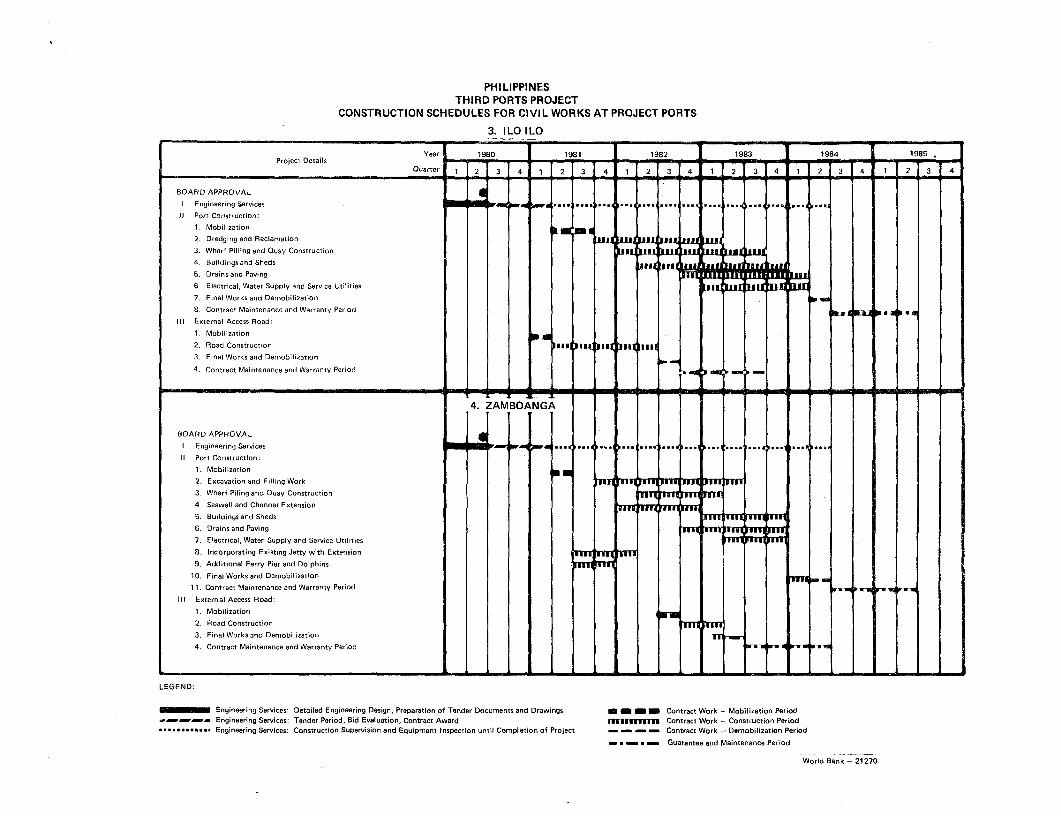

3.13 In order to accelerate the construction of civil works to be doneunder contract, and also to take advantage of favorable world prices ofcertain items of equipment (e.g. weighbridges) and materials (e.g. steelpiles and structural sections) which are part of the civil works, theGovernment intends to consider making early procurement of such directlyimported items common to the civil works of tle project ports. For thispurpose a notional sum of US$1.5 million will be provided as a separatecategory in the schedule of withdrawals of the proceeds of the loan in theLoan Agreement. The Government will seek the prior approval of the Bank onthe specific items prior to procurement. Disbursements will be 100% offoreign expenditures for such directly imported items.

3.14 The works are expected to be completed by the second quarter of1984, assuming effectiveness of the proposed loan by October 1, 1980. Theconstruction schedules shown in Charts 21269/70 have been agreed with PPA.

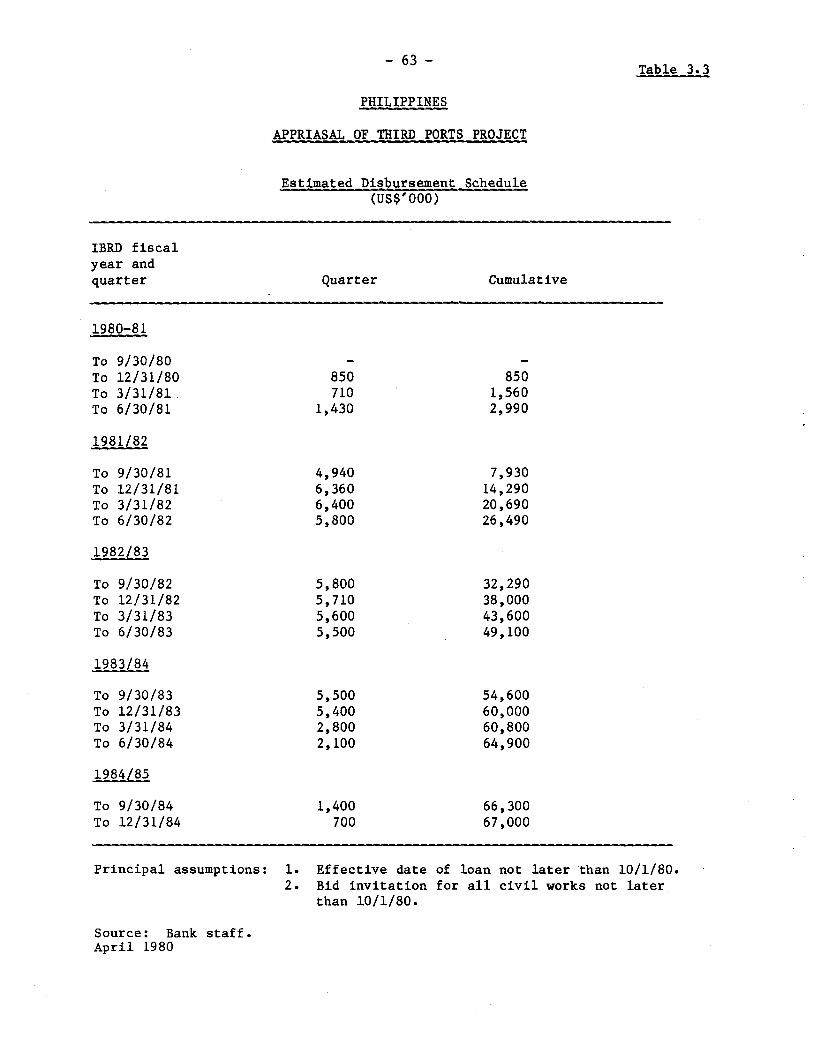

3.15 Disbursement for project civil works would be on the basis of 48%of total costs net of taxes. For consulting services, disbursement would beon the basis of actual cost; if local consultants are employed, disbursementwould be for 100% of local costs. Disbursements by the Bank are expected tobe completed by June 30, 1985. The estimated schedule of quarterlydisbursements, given in Table 3.3 is based on the assumption that theproposed loan would become effective by October 1, 1980.

3.16 Cargo handling equipment is to be procured by PPA with the aid ofa foreign loan now being sought by the Government and PPA. After purchase,PPA intends to lease the equipment to arrastre companies and has undertakento inform the Bank of the terms of the lease.

Ecology

3.17 None of the proposed works will affect the existing ecology of theports; reclamation dredging is envisaged for land-fill at the project sitesfor Cagayan de Oro, Iloilo and Zamboanga. In Cebu, most of the overlyinglayers on the sea bottom to be dredged out for the new approach channel are

- 27 -

not suitable as reclamation fill. Unsuitable dredged material will bedisposed of well outside the port area to designated areas of tidal flats onMactan Island, some 4 km away. Any suitable land-fill material found in thecourse of such dredging will be deposited in the future extension area northof the present project site.

3.18 The project ports do not handle or transfer crude oil or petroleumproducts, these being handled by oil companies at their specialized privateinstallations located well away from the public ports.

4. ECONOMIC EVALUATION

A. Traffic

General

4.01 Separate traffic forecasts were prepared for passengers, majorcommodities and commodity groups at each project port. Among commodityprojections, those for grain took into account production, consumption,grain surpluses and/or deficits in the hinterland of project ports, whileprojections of general cargo, including miscellaneous consumer goods,relied on income elasticity of demand indicators available for currenthousehold budget surveys. Impacts of economic programs and projects wereconsidered in projecting export and agricultural and industrial inputs. Baseyear data for passenger traffic was adjusted for underreporting and projectedbased on revised June 1979 population forecasts.

- 28 -

4.02 Both cargo and passenger forecasts relied on port area statisticsand route-specific origin/destination data. Efforts have been made toreconcile projections of major commodities known to move between the projectports, taking into account the interport and intermodal competition for portcargo. The projected passenger and commodity flows have been adapted to theneeds of port capacity analysis and project evaluation by classifying themaccording to direction, handling characteristics and port facilities.Detailed forecasts were prepared up to 1990; generalized projections wereused thereafter.

Cagavan de Oro

4.03 In 1978 the port of Cagayan de Oro handled 630,000 tons of cargo and583,000 passengers. Over 1.3 million tons of cargo and 1.1 millionpassengers are expected to move through the port in 1990 (Table 4.1). Notincluded in these totals for lack of concrete commitments by a fruitpacking company, is nearly 300,000 tons of potential container trafficnow handled over the company's own inadequate facilities across the bayfrom the port of Cagayan de Oro.

4.04 Domestic commerce, mostly consumer goods, accounts for 83% of thetotal port traffic. Corn shipped to the Cebu region is the single mostimportant product; the eventual need for bulk storage and handlingfacilities is being considered by PPA and the National Grain Authority.Foreign trade, 105,000 tons in 1978, will grow rapidly on the strength ofexport of wood products and new commodities such as cassava chips, sugar andchromite.

4.05 Container cargo, both domestic and foreign, as a percentage oftotal port traffic, will expand from 9% in 1979 to 36% in 1990. Even withoutthe potential container traffic referred to above, Cagayan de Oro alone amongthe project ports has a significant volume of outward container cargoes whichwill attract container vessels seeking return cargo.

Cebu

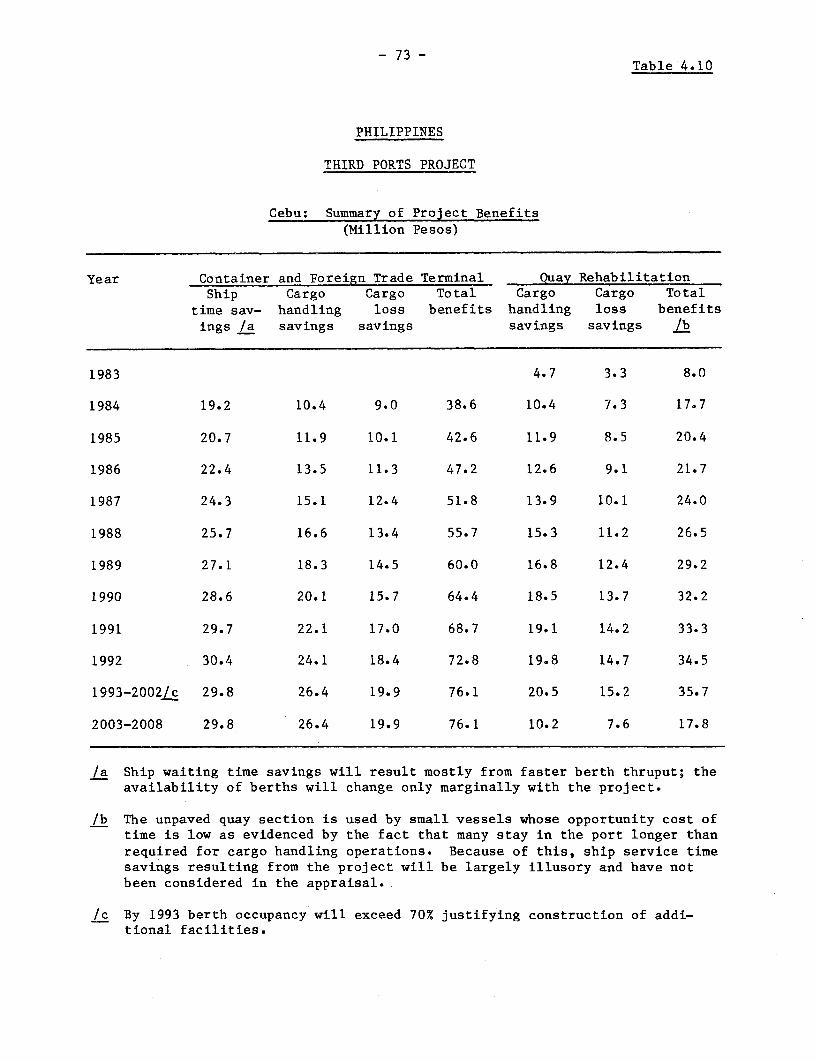

4.06 After Manila, Cebu is the most important public port and serves asthe distribution center of general cargo for the Visayas region. It alsoreceives large volumes of grain from Mindanao to supplement its ownproduction. Its foreign trade is now mostly transshipped via Manila butmuch of it will divert to Cebu when the new container terminal is constructed.

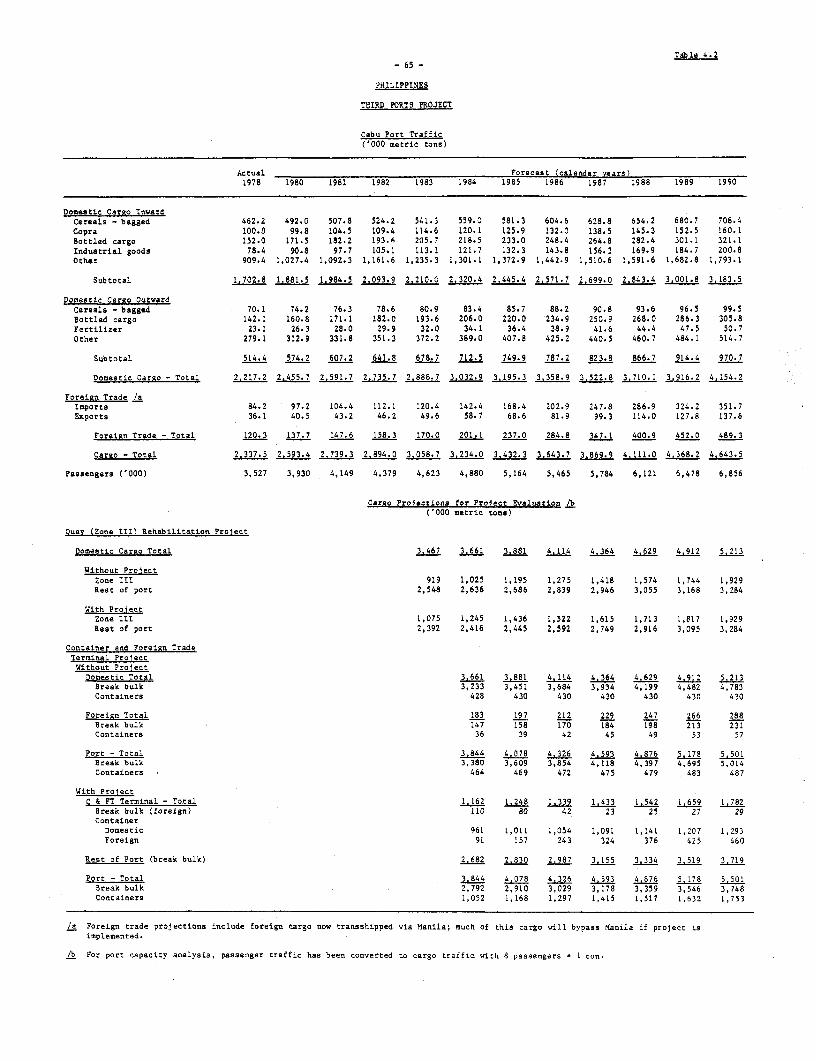

4.07 The port handled 2.3 million tons of cargo and 3.5 millionpassengers in 1978. These totals are expected to reach 4.6 million tons and6.9 million passengers by 1990 (Table 4.2).

4.08 Virtually all goods using the port are handled as general cargo.Container traffic, at 174,000 tons in 1978, is small but growing rapidlydespite the lack of specialized handling and storage facilities. It is

- 29 -

projected to reach 1.8 million tons by 1990. Without the project container-ization will level off at about 500,000 tons annually.

4.09 Separate traffic forecasts are provided in Table 4.2 for therehabilitation of the existing quay and for the proposed container andforeign trade terminal, the two main components of the Cebu port project.

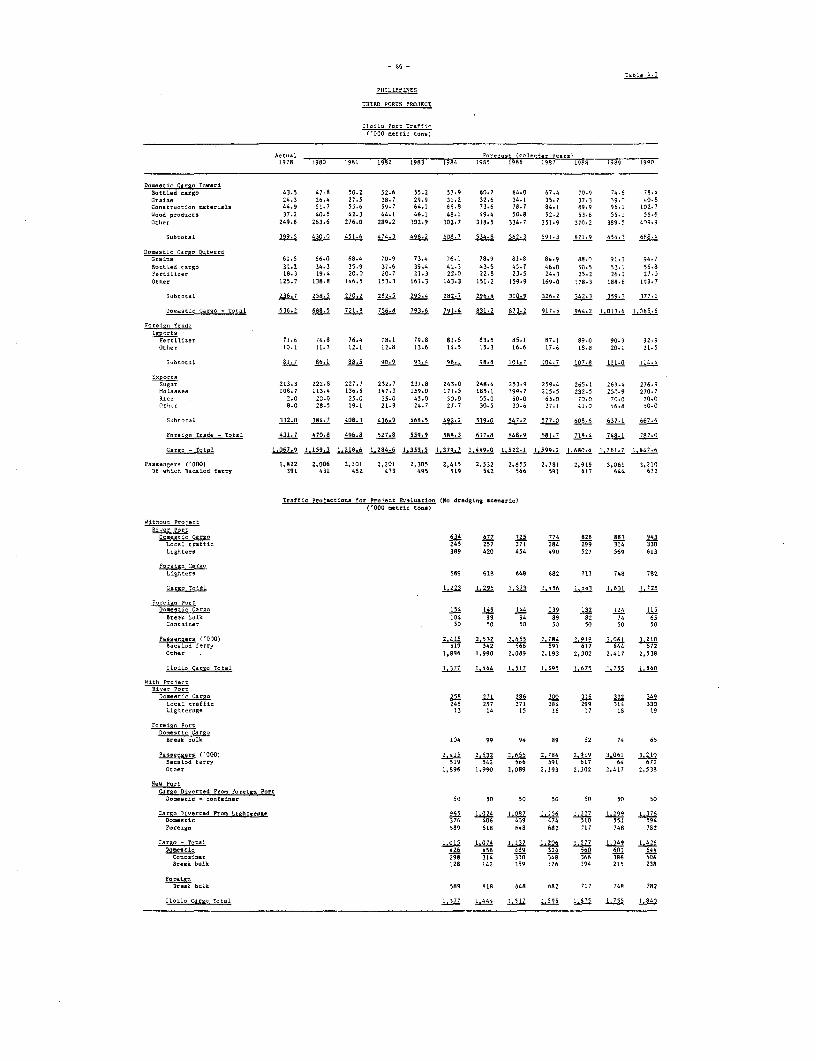

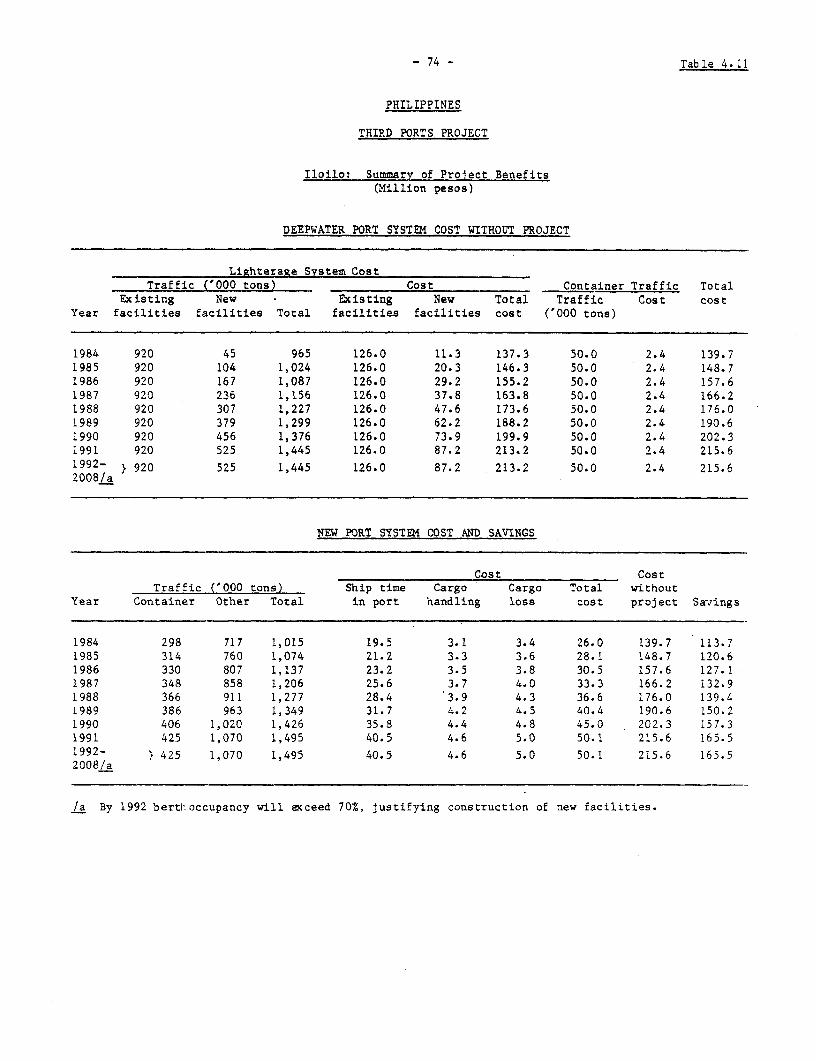

Iloilo

4.10 The port of Iloilo is a domestic river port, with a wharflocated in the straits serving both foreign and domestic traffic, andanchorage facilities. In 1978, the port handled nearly 1.1 million tons ofcargo and 1.8 million passengers; this is expected to increase to 1.8million tons of cargo and 3.2 million passengers by 1990 (Table 4.3).

4.11 Already an important foreign trade port, Iloilo will handle sub-stantially higher volumes of sugar and its byproducts from new refineries inits hinterland. Sharp increases are also expected in grain and mineralexports. Construction materials, grains and consumer goods will continue todominate domestic seaborne commerce. There is a twice-daily passenger ferryservice to nearby Bacolod, and Iloilo is also linked by regular passengerservices to all major ports in the Philippines.

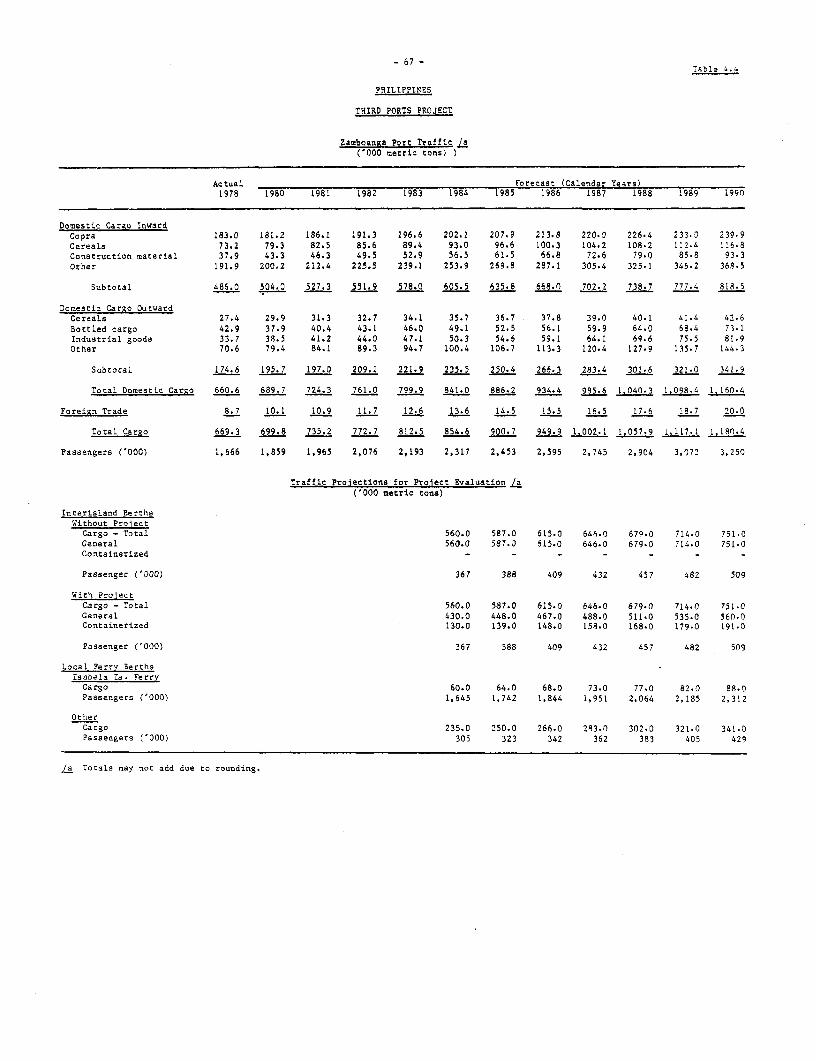

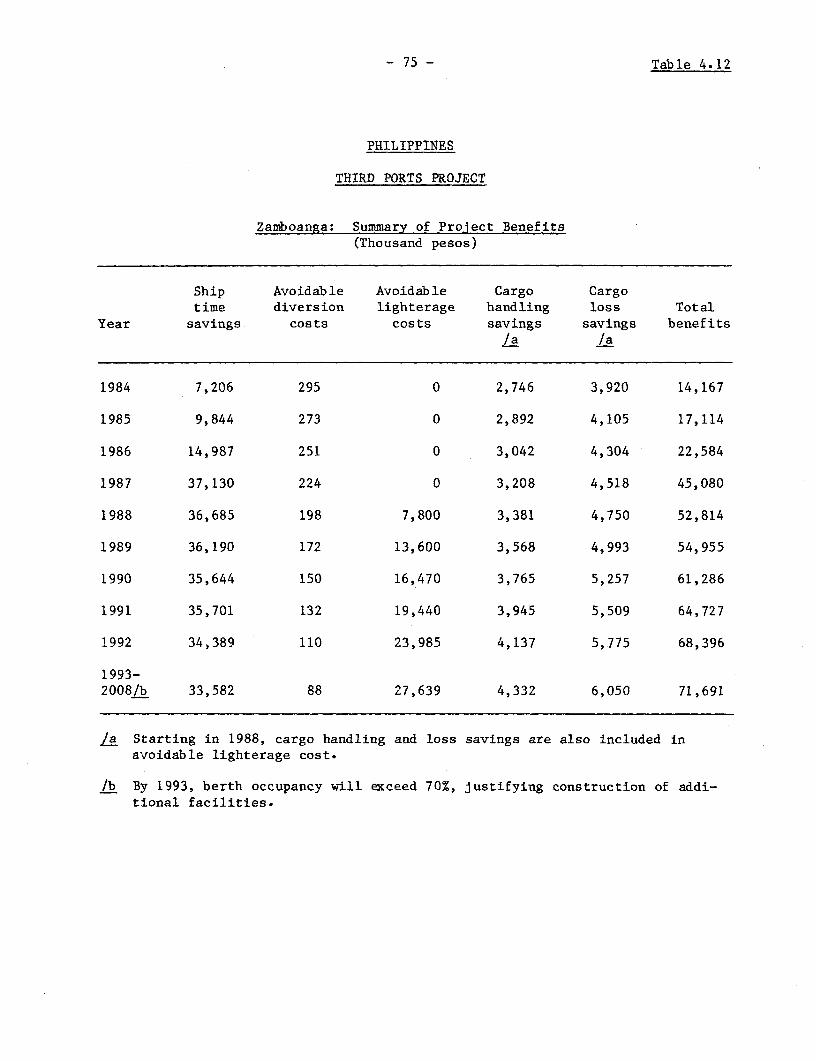

Zamboanga

4.12 This port serves several related functions including: (a) collec-tion and distribution of cargo to the neighboring islands; (b) connectionto other coastal urban centers of Mindanao; (c) stopover point forinterisland vessels plying between Manila and the ports of southeasternMindanao; and (d) terminal for local, coastal and interisland passengertravel.

4.13 The port handled 670,000 tons of cargo and 1,666,000 passengers in1978, which is projected to rise to 1.2 million tons of cargo and 3.2million passengers by 1990 (Table 4.4). Both cargo and passenger forecastsare based on Government expectations that conditions in the region which,until recently, has been troubled by civil disorders will remain stable.

4.14 Virtually all (99% in 1978) seaborne cargo is domestic; foreigncommerce is limited to barter trade with neighboring countries. Incomingcopra and cereals are the two most important products and accounted for 42%of the total in 1978. The rest consists of a wide range of consumerproducts and general cargo.

4.15 Approximately one half of passenger traffic is handled by anefficiently operated ferry service to nearby Isabela Island. Frequentpassenger services are also available to outlying islands of the SuluArchipelago, points along the coast of Mindanao and major ports elsewherein the Philippines.

- 30 -

B. Benefits

General

4.16 Quantifiable benefits attributed to proposed improvements inproject ports will consist of all or some of the following:

(a) ship time savings;

(b) avoidable cargo diversion costs;

(c) avoidable lighterage costs;

(d) lower cargo handling costs; and

(e) decrease in cargo losses including damages to containers.

Considering the high level of competition among ship operators, shipperswould benefit from reduced operating costs in the form of lower tariffs orrebates, most of which would be passed on to the ultimate consumers.

4.17 (a) Ship Time Savings

These include both the reduction in ship time while awaiting berthand lower "at berth" time due to improved cargo handling productivity.Estimates of ship time in port with and without the project were obtainedthrough the simulation of observed and expected values of operationalvariables for different levels and composition of port traffic.

4.18 Ship waiting and service time savings are estimated by weighingrepresentative values of major ship types using project ports. Thesevalues, range from P 4,700 per day for small passenger-cargo vessels toP 51,000 per day for foreign container feeder vessels. Higher thanrepresentative values were used for domestic container ships in Cebu andlower than representative values for foreign and domestic general cargoships at Zamboanga.