Embed Size (px)

Citation preview

Pakistan

Clean Fuels

ESM246

~~~. ~

_ ~ ~ ~ ~ ~ ~ ~ ' ______J___

_~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~f ,.1- _us,= -._

' m -- , -,;-'' t ';.'

Energy

Sector

Management

Assistance

Programme

L~AAA AD6J,LY1 Ii Report 246/01

October 2001

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

JOINT UNDP / WORLD BANKENERGY SECTOR MANAGEMENT ASSISTANCE PROGRAMME (ESMAP)

PURPOSE

The Joint UNDP/World Bank Energy Sector Management Assistance Programme(ESMAP) is a special global technical assistance program run as part of the World Bank'sEnergy, Mining and Telecommunications Department. ESMAP provides advice togovernments on sustainable energy development. Established with the support of UNDPand bilateral official donors in 1983, it focuses on the role of energy in the developmentprocess with the objective of contributing to poverty alleviation, improving living conditionsand preserving the environment in developing countries and transition economies.ESMAP centers its interventions on three priority areas: sector reform and restructuring;access to modern energy for the poorest; and promotion of sustainable energy practices.

GOVERNANCE AND OPERATIONS

ESMAP is governed by a Consultative Group (ESMAP CG) composed of representativesof the UNDP and World Bank, other donors, and development experts from regionsbenefiting from ESMAP's assistance. The ESMAP CG is chaired by a World Bank VicePresident, and advised by a Technical Advisory Group (TAG) of four independent energyexperts that reviews the Programme's strategic agenda, its work plan, and itsachievements. ESMAP relies on a cadre of engineers, energy planners, and economistsfrom the World Bank to conduct its activities under the guidance of the Manager ofESMAP, responsible for administering the Programme.

FUNDING

ESMAP is a cooperative effort supported over the years by the World Bank, the UNDPand other United Nations agencies, the European Union, the Organization of AmericanStates (OAS), the Latin American Energy Organization (OLADE), and public and privatedonors from countries including Australia, Belgium, Canada, Denmark, Germany, Finland,France, Iceland, Ireland, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal,Sweden, Switzerland, the United Kingdom, and the United States of America.

FURTHER INFORMATION

An up-to-date listing of completed ESMAP projects is appended to this report. For furtherinformation, a copy of the ESMAP Annual Report, or copies of project reports, contact:

ESMAPc/o Energy and Water

The World Bank1818 H Street, NW

Washington, DC 20433U.S.A.

Pakistan Clean Fuels

October 2001

Joint UNDP/World Bank Energy Sector Management Assistance Programme(ESMAP)

Copyright © 2001The International Bank for Reconstructionand Development/THE WORLD BANK1818 H Street, N.W.Washington, D.C. 20433, U.S.A.

All rights reservedManufactured in the United States of AmericaFirst printing October 2001

ESMAP Reports are published to communicate the results of theESMAP's work to the development community with the least possibledelay. The typescript of the paper therefore has not been prepared inaccordance with the procedures appropriate to formal documents.Some sources cited in this paper may be informnal documents that arenot readily available.

The findings, interpretations, and conclusions expressed in thispaper are entirely those of the author(s) and should not be attributed inany manner to the World Bank, or its affiliated organizations, or tomembers of its Board of Executive Directors or the countries theyrepresent. The World Bank does not guarantee the accuracy of the dataincluded in this publication and accepts no responsibility whatsoeverfor any consequence of their use. The Boundaries, colors,denominations, other information shown on any map in this volume donot imply on the part of the World Bank Group any judgement on thelegal status of any territory or the endorsement or acceptance of suchboundaries.

The material in this publication is copyrighted. Requests forpermission to reproduce portions of it should be sent to the ESMAPManager at the address shown in the copyright notice above. ESMAPencourages dissemination of its work and will normally givepermission promptly and, when the reproduction is for noncomnmercialpurposes, without asking a fee.

"ESMAP Values your Feedback

If you have found this report useful, or would like toprovide comments on our reports and services, please

log on to our website at www.esmap.org and leaveyour feedback. In this way we can better understandour audience's needs and improve the quality of our

knowledge products. Thank you.

ESMAP Management"

Contents

Acknowledgments .......................................................... vii

Abbreviations and Acronyms .......................................................... viii

Units of Measure .......................................................... x

Glossary of Terms .......................................................... xi

Executive Summary .......................................................... 1

Clean-Fuels Workshops and Analysis ............................................................. ITransport Fuel Tax Policy ............................................................. 5

1. Background .......................................................... 9

The Link Between Fuel, Transport, and the Environment ...................................................... 10Lead ............................................................ 10Particulate Matter ............................................................ 13Other Pollutants ............................................................ 15Fuel Quality ............................................................. 16Fuel Quality Trend in Neighboring Countries and Implications for Pakistan .................. 19Downstream Petroleum Sector in Pakistan ............................................................ 20

Workshop ............................................................ 21Transport Fuel Tax Policy ............................................................ 22Structure of the Report ............................................................ 23

2. The Downstream Petroleum Sector .......................................................... 25

Role of the Government ............................................................ 25Product Pricing ............................................................ 26Economic Supply Zones ............................................................ 29

Other Agencies ............................................................. 29Refinery Configuration ............................................................ 30Selection of Crude -Oil ............................................................ 30Crude and Product Pipelines ............................................................ 31Overall Demand and Supply ..................................................................................... ............. 32

Gasoline ................................ 32Diesel ............................... 34Fuel Oil .35........ ................................... 35

Fuel Quality . 35

Hii

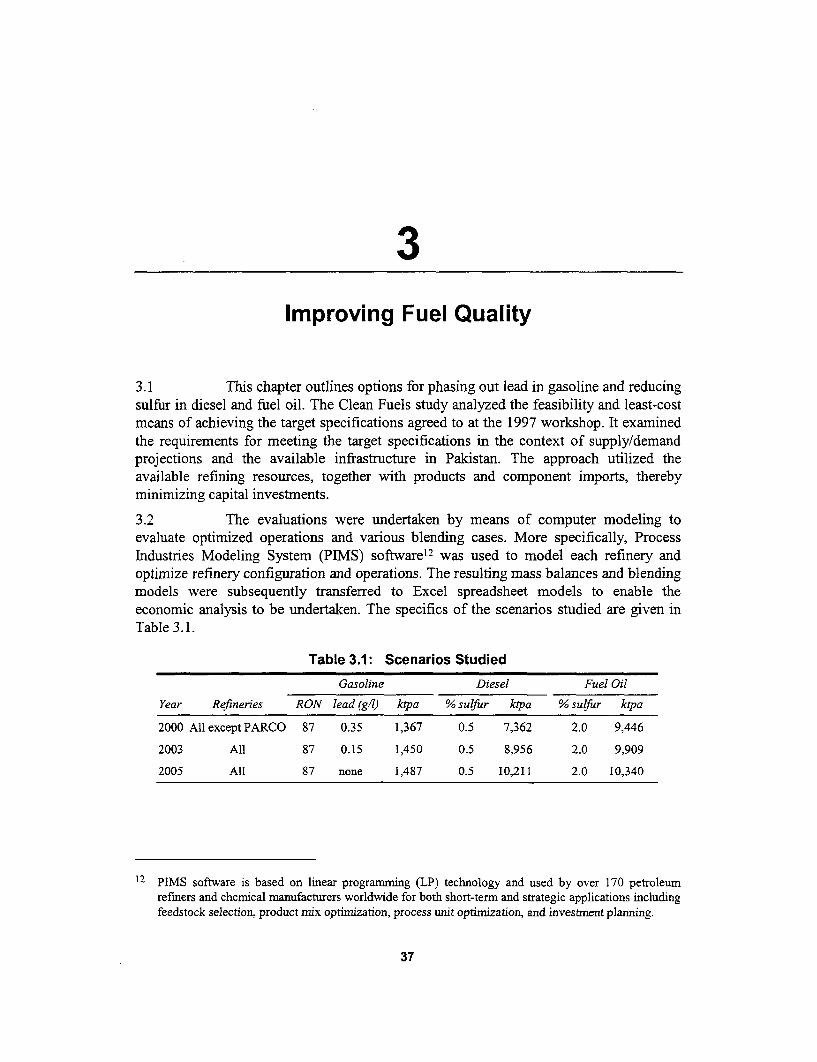

3. Improving Fuel Quality ................................................................. 37

Underlying Assumptions .................................................................... 38

Phaseout of Lead in Gasoline ................................................................... 38Proposals for 2000 ................................................................... 40Proposals for 2003 .................................................................... 42Proposals for 2005 ................................................................... 44

Diesel ................................................................... 47

Fuel Oil .51

Incremental Cost of Fuel Quality Improvement ................................................................... 54Refined Product Pricing Basis .................................................................... 54Economics for Gasoline ................................................................... 55

Incremental Cost of Diesel Sulfur Reduction ................................................................... 57Economics of Fuel-Oil Sulfur Reduction ................................................................... 59

4. Building a National Consensus . ................................................................. 61

5. Fuel Tax Policy ................................................................. 65

Fuel Consumption by Vehicle Category .................................................................... 65Incentives for Fuel Switching ..................................................................... 69Impact on Prices and Household Expenditures ................................................................... 71Balance of Payments and Tax Revenue ................................................................... 74Impact on the Macroeconomy ................................................................... 76Social Policies to Mitigate Adverse Impact .................................................................... 78Conclusions and Recommendations .................................................................... 82

Annex 1. Incremental Cost Calculations ................................................................. 85

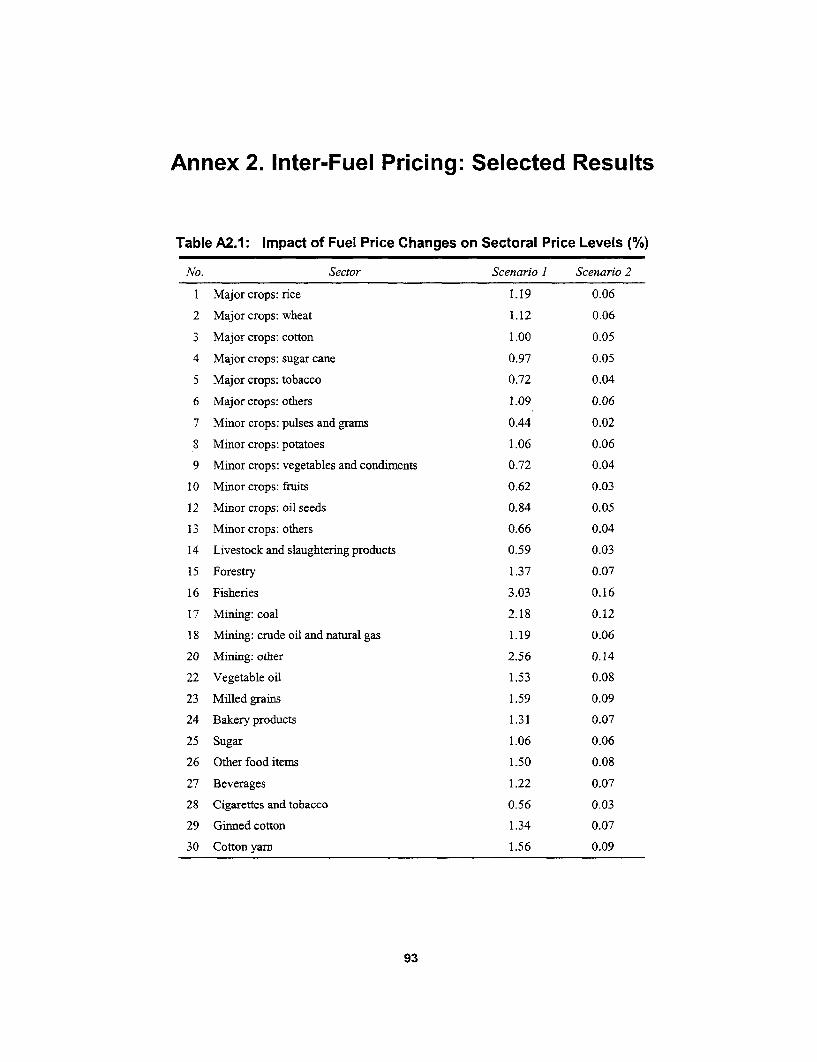

Annex 2. Inter-Fuel Pricing: Selected Results ........................................................ 93

Annex 3. Historical Overview of Social Safety Nets . ............................ 101

Bibliography ................................................................. 109

Tables

Table E.1 October 1997 Workshop: Recommended Timetable for Tightening FuelSpecifications, Including 1999 Revisions .................................................................... 2

Table E.2 Incremental Cost (1998 US$) ................................................................... 3

Table E.3 Gasoline Physical Properties in 2005 (percent by volume) .......................................... 3Table E.4 Changes in Macroeconomic Parameters for Fiscal 1999-2000 .................................... 7Table 1.1 Impact of a 10-p_g/m 3 Change in the Ambient Concentration of Particulate Matter

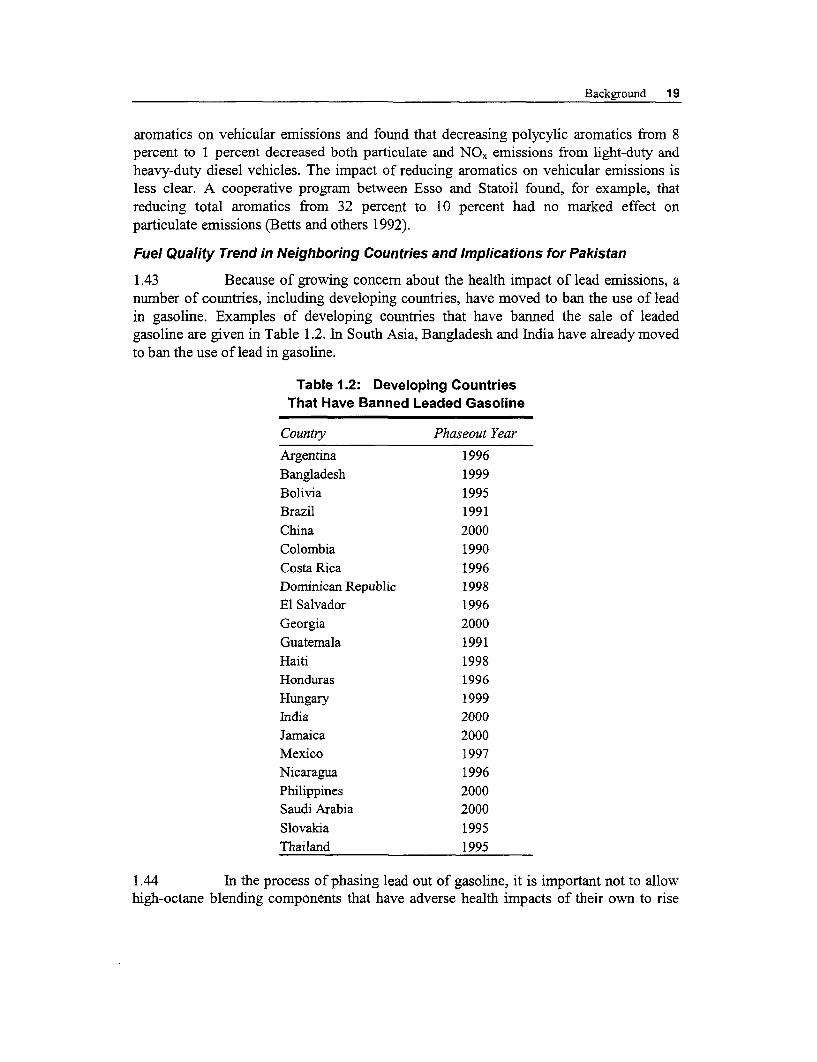

on Health .................................................................... 15Table 1.2 Developing Countries That Have Banned Leaded Gasoline ....................................... 19

iv

Table 1.3 October 1997 Workshop: Recommended Timetable for TighteningFuel Specifications, Including 1999 Revisions ............................................. 21

Table 2.1 Retail Prices (Rs per Liter) ............................................................. 27Table 2.2 Economic Supply Zones Post-PARCO startup ............................................................ 29Table 2.3 Configurations and Capacities of Refineries in Pakistan (thousand barrels per day) .30Table 2.4 Qualities of Low-Sulfur Crudes ............................................................. 31

Table 2.5 Pakistan Gasoline Demand Forecasts by Region (thousand tons per year) ................ 33Table 2.6 Pakistan Diesel Demand Forecasts by Region, 2000-2005 (thousand tons per year) 34Table 2.7 Pakistan Fuel Oil Demand Forecasts, by Region (thousand tons per year) ................ 35

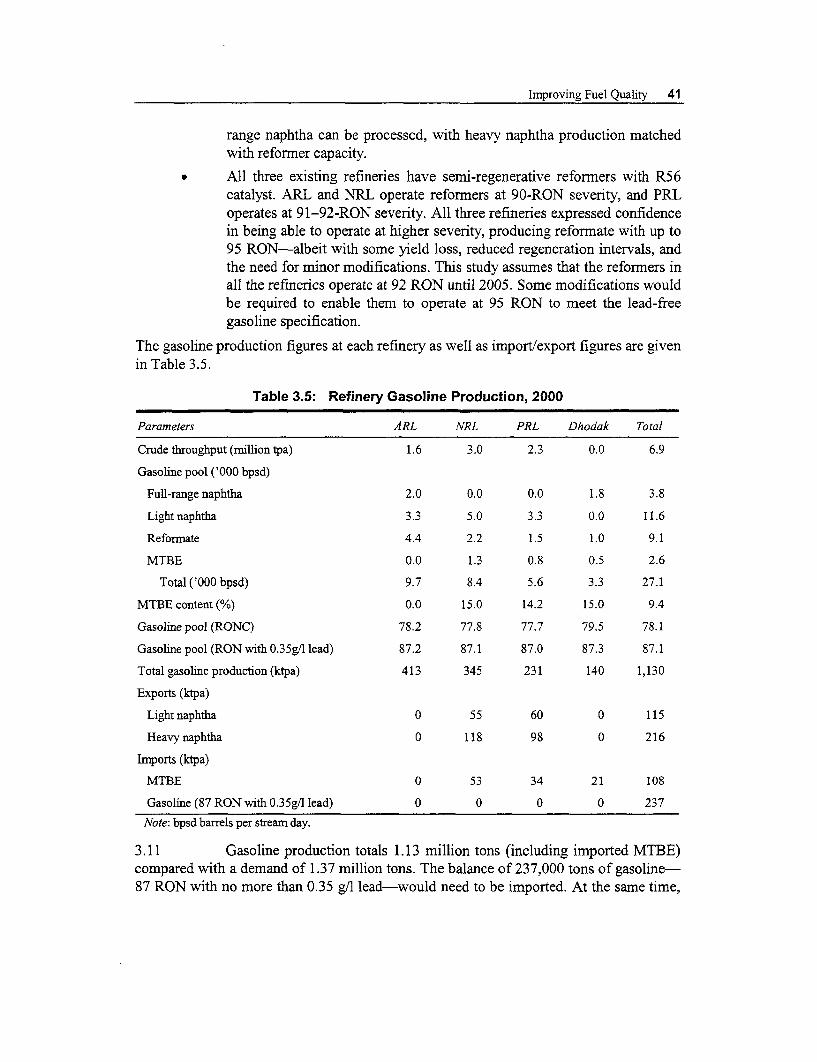

Table 2.8 Middle Distillate Production ............................................................. 36Table 2.9 Fuel Oil Production ............................................................. 36Table 3.1 Scenarios Studied ............................................................. 37Table 3.2 Quality Parameters Used for Gasoline Blending Options ........................................... 38Table 3.3 Leaded and Clear RON Requirements ............................................................. 39Table 3.4 Refinery Gasoline Production in Pakistan, 1999 (Base Case) .40

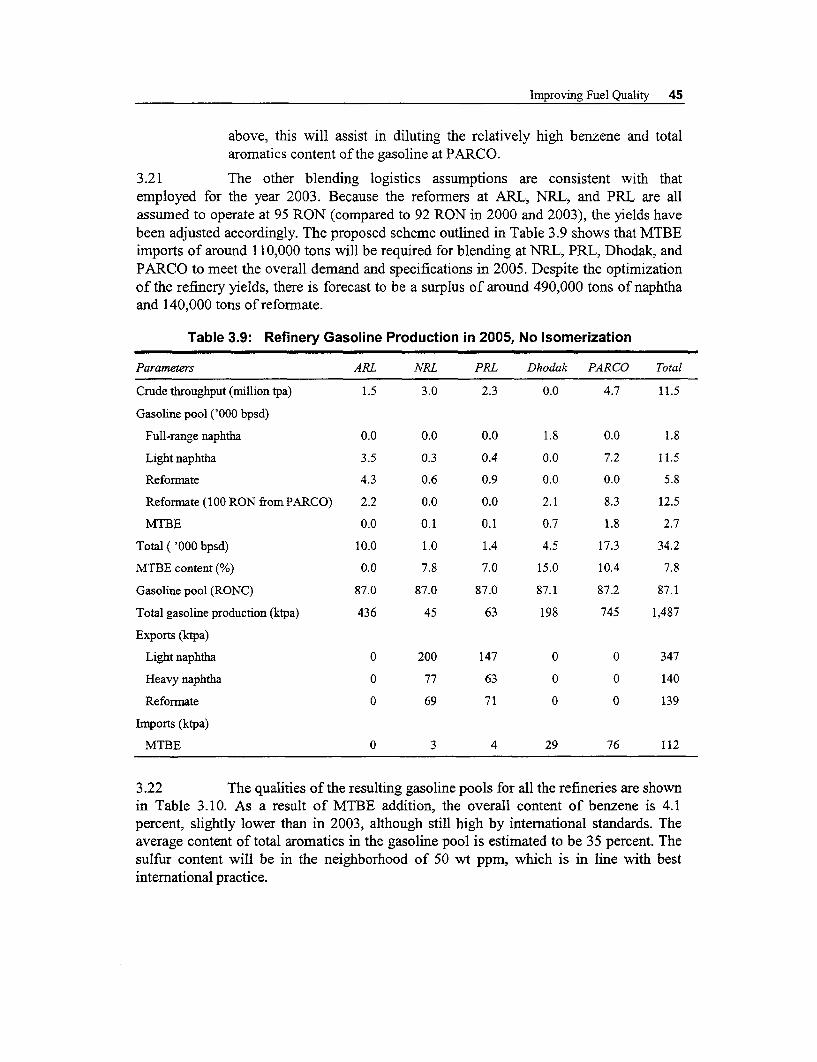

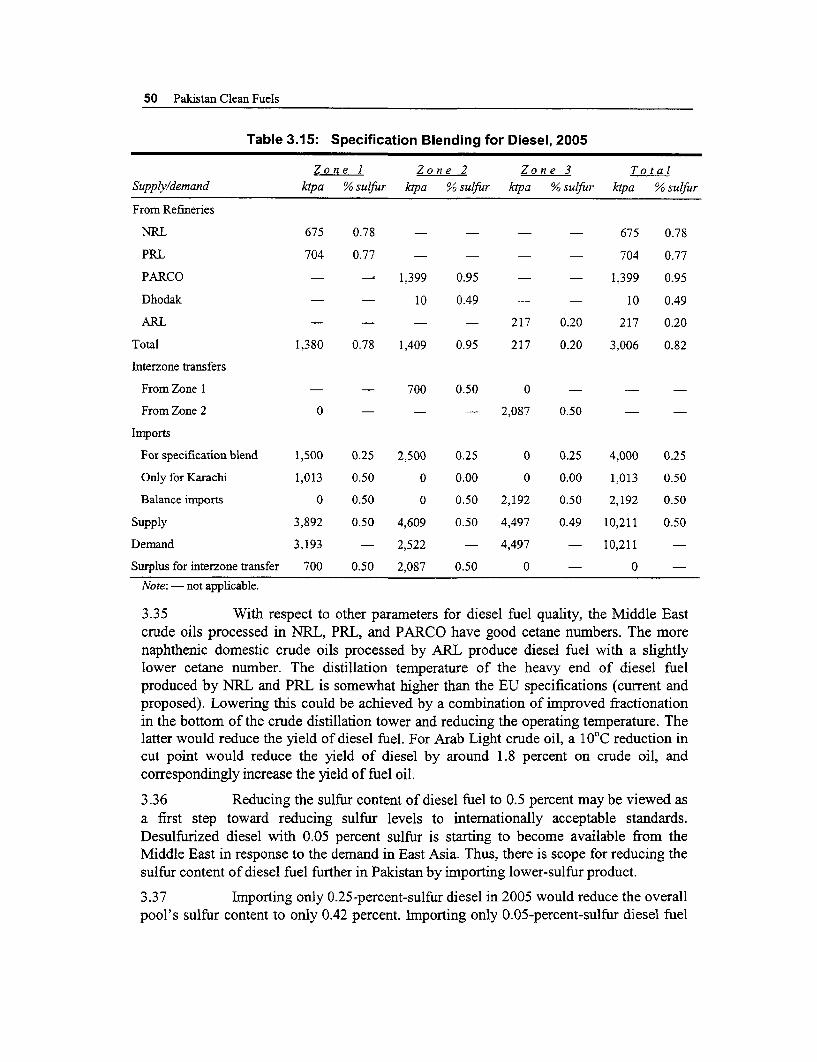

Table 3.5 Refinery Gasoline Production, 2000 .41Table 3.6 Physical Properties of Gasoline in 2000 .42Table 3.7 Refinery Gasoline Production in 2003 .43Table 3.8 Physical Properties of Gasoline in 2003 .44Table 3.9 Refinery Gasoline Production in 2005, No Isomerization .45Table 3.10 Physical Properties of Gasoline in 2005, No Isomerization . .46Table 3.11 Refinery Gasoline Production in 2005 with Isomerization . .46Table 3.12 Impact of Isomerization on Gasoline Physical Properties in 2005 . .47Table 3.13 Specification Blending for Diesel, 2000 .. 48Table 3.14 Specification Blending for Diesel, 2003 .. 49Table 3.15 Specification Blending for Diesel, 2005 .. 50

Table 3.16 Fuel Oil Pools, 2000 .. 52Table 3.17 Fuel Oil Pools, 2003 .. 53Table 3.18 Fuel Oil Pools, 2005 .. 53Table 3.19 Gasoline Quality Improvement: Free-Market Pricing . ............................................. 56Table 3.20 Gasoline Quality Improvement: Cost to Pakistan Refineries . . 56Table 3.21 Costs of Isomerization in 2005 ........................................................ 57Table 3.22 Cost of Reducing Sulfur in Diesel Fuel .......................................... 58Table 3.23 Cost of Reducing Sulfur in Fuel Oil ....................................................... 59Table 4.1 Workshop Programs ....................................................... 61Table 5.1 Motor Vehicle Population in Pakistan ('000) ....................................................... 66Table 5.2 Results of Survey of 20 Refueling Stations in Karachi and Lahore ............................ 66Table 5.3 Survey of 150 Vehicle Owners in Karachi, Lahore, and Peshawar ............................ 67Table 5.4 Intra- and Inter-City Fuel Consumption ('000 metric tons) ........................................ 68

v

Table 5.5 Price Adjustments undeT Different Scenarios ............................................................. 71Table 5.6 Annual Household Private Transport Expenditures, by Income Quartile (rupees) .... 73

Table 5.7 Changes in Annual Household Expenditure in Scenario 1 ......................................... 73

Table 5.8 Changes in Annual Household Expenditure in Scenario 2 ......................................... 74

Table 5.9 Demand Elasticities for Gasoline and Diesel ............................................................. 75Table 5.10 Consumption of Gasoline and Diesel in Two Scenarios and Impact on Balance

of Payments and Tax Revenue in Fiscal 1999-2000 ................................................................. 75

Table 5.11 Changes in Macroeconomic Parameters for Fiscal 1999-2000 ................................ 77Table 5.12 Evaluation of Social Safety Net Programs ................................................................ 80Table 5.13 Impact of Changes in GST ................................................................... 82

Table A1.1 Gasoline Prices in Pakistan (1998 US$ per ton) ....................................................... 86Table A1.2 Diesel Prices in Pakistan (1998 US$ per ton) ........................................................... 86

Table A1.3 Fuel Oil Prices in Pakistan (1998 US$ per ton) ........................................................ 86

Table A1.4 Gasoline Quality Improvement: Free-Market Pricing .............................................. 87Table A1.5 Gasoline Quality Improvement: Cost to Pakistan Refineries ................................... 88

Table A 1.6 Cost of Installing Isomerization Units ................................................................... 89

Table A1.7 Impact of Isomerization in 2005 ................................................................... 89Table A1.8 Infrastructure Investment Costs for Diesel Sulfur Reduction (1998 US$ million).90Table A1.9 Cost of Diesel Sulfur Reduction ................................................................... 90Table A 1.10 Capital Investment Required for Middle Distillate Hydrodesulfurization ... 91Table Al.1 1 Cost of Fuel-Oil Sulfur Reduction, 1998 US$ million . . 91

Table Al.12 Flue Gas Desulfurization Economics ................................................................... 92Table A2.1 Impact of Fuel Price Changes on Sectoral Price Levels (Percent) ............. ............. 93

Table A2.2 Annual Urban Household Expenditures, by Income Quartile and Sector (rupees). 95Table A2.3 Annual Rural Household Expenditures by Income Quartile and Sector (rupees)... 97

Figures

Figure 1.1 Evolution of U.S. Diesel Particulate Emissions ........................................................ 18Figure 2.1 Regular Gasoline Price Breakdown for NRL/PRL .................................................... 28Figure 2.2 High-Speed Diesel Price Breakdown for NRL/PRL .................................................. 28

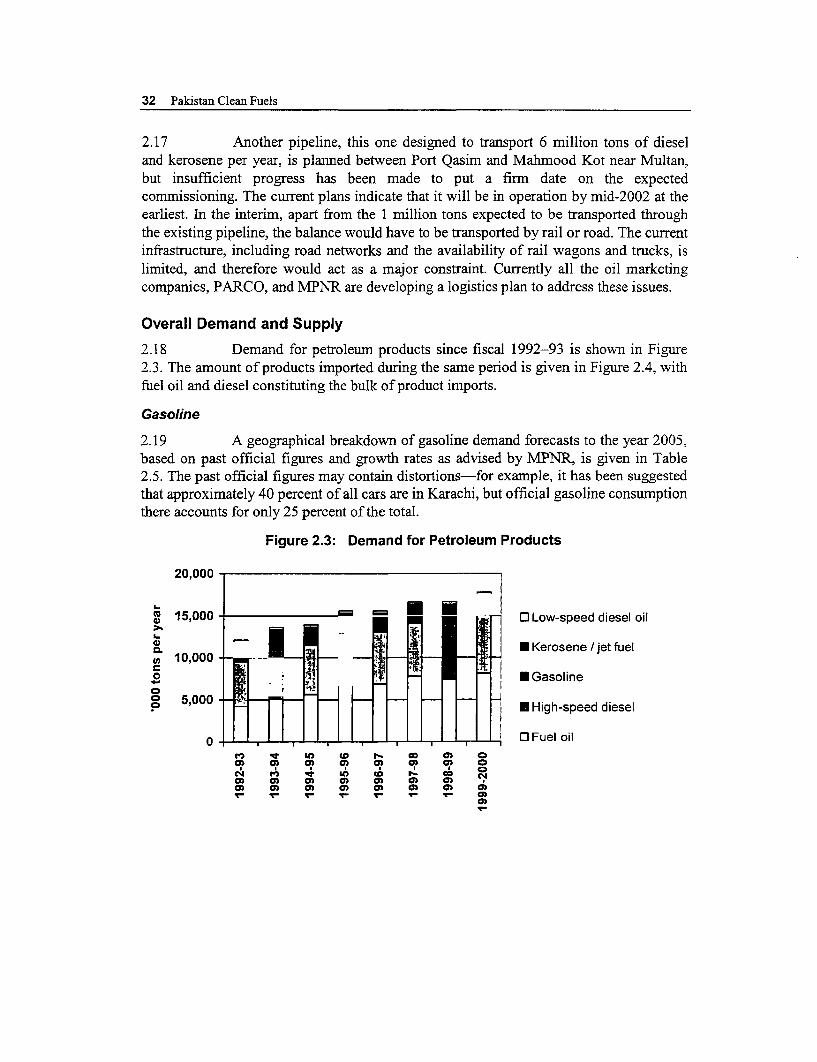

Figure 2.3 Demand for Petroleum Products ........................................................ 32Figure 2.4 Imports of Petroleum Products ........................................................ 33

Figure 3.5 Contribution to Sulfur Content of Overall Fuel Oil Pool, 2003 ................................ 52

vi

Acknowledgments

This report presents the results of a "Pakistan Clean Fuels" study undertaken by theEnergy Sector Management Assistance Programme (ESMAP), a joint program of theUnited Nations Development Programme (UNDP) and the World Bank. The financialassistance of the Government of the United Kingdom through ESMAP is gratefullyacknowledged.

The study was conducted under the guidance of Mr. G.A. Sabri, Director General (Oil) ofthe Pakistan Ministry of Petroleum and Natural Resources (MPNR), and Mr. Asif ShujaKhan, Director General of the Pakistan Environment Protection Agency (PEPA). Therefiners in Pakistan, fuel marketers, and the Hydrocarbon Development Institute ofPakistan (HDIP) contributed significantly to the analysis of clean fuels options carried outby Mike Webster, Phil Hunt, and Rizwan Sheikh of Chem Systems (U.K.) and presentedin Chapters 2 and 3. Professor Paul Stevens of the Centre for Energy, Petroleum, andMineral Law and Policy of the University of Dundee contributed to some of thediscussions found in Chapter 2. Hafiz Pasha, Zafar Ismail, Ejaz Rasheed, Alisha Ghaus-Pasha, and Sajjad Akhtar of the Social Policy Development Centre (SPDC) undertook thestudy described in Chapter 5. Historical product prices and production and consumptionfigures in this report were taken from Pakistan Energy Yearbook 2000, published jointlyby HDIP and MPNR.

This report was prepared by Masarni Kojima of the Policy Division, Oil, Gas andChemicals Departnent of the World Bank. The principal members of the ESMAP tearnwere Masami Kojima (task leader) and Robert Bacon of the Policy Division, Oil, Gas andChemicals Department. Other participants in this study from the World Bank includedRashid Aziz, Waqar Haider, Tjaarda Storm van Leeuwen, and Marc Heitner and of theSouth Asia Energy Unit; and Aziz Bouzaher of the South Asia Environment Unit. Thecomments of the reviewer, Kenneth Gwilliam of the Urban Development and TransportDepartment of the World Bank, and the editorial assistance provided by Chris Marquardtare gratefully acknowledged.

vii

Abbreviations and Acronyms

AJK Azak, Jammu, and KashmirAQIRP (U.S. Auto/Oil) Air Quality Improvement

Research ProgramARL Attock Refmery, LimitedASS Atta (wheat flour) Subsidy SchemeBOR Boards of RevenueCCR continuous catalyst regenerationCDC (U.S.) Centers for Disease Control and

PreventionCIF cost, insurance, and freight

CNG compressed natural gasCO carbon monoxide

CONCAWE Conservation of Clean Air and Water inEurope

DG Directorate GeneralEOBI Employees Old Age Benefits Institution

EPEFE European Programme on Emissions, Fuelsand Engine Technologies

ESMAP Energy Sector Management AssistanceProgramme

EU European UnionFBS Federal Bureau of StatisticsFCC fluidized catalytic crackingFGD flue gas desulfurizationFOB free on boardGDP gross domestic productGST general sales tax

HBFC House Building Finance CorporationHBL Habib Bank Limited

HDIP Hydrocarbon Development Institute ofPakistan

HIES Household Integrated Economic SurveyHOBC high-octane blending components

HSD high-speed dieselIFA Individual Financial AssistanceIMF International Monetary Fund

IQ intelligence quotientISPM integrated social policy and macroeconomic

(model)JICA Japan International Cooperation Agency

LP linear progranmmingLPG liquefied petroleum gas

viii

MPNR Ministry of Petroleum and NaturalResources

MTBE methyl tertiary-butyl etherNGO nongovemmental organizationNO2 nitrogen dioxideNO. oxides of nitrogenNRL National Refinery Limited

NRSP National Rural Support ProgramNWFP Northwest Frontier ProvinceOCAC Oil Company Advisory Committee

OEM original equipment manufacturerOMV Offenfuir Mehr Verantwortung

PARCO Pakistan Arab Refinery CompanyPBM Pakistan Bait-ul-Maal

PEPA Pakistan Environment Protection AgencyPIMS Process Industries Modeling System

PM particulate matterPMIo particles with an aerodynamic diameter less

than 10 micronsPM2.5 particles with an aerodynamic diameter less

than 2.5 micronsPRL Pakistan Refinery LimitedPSO Pakistan State OilRVP Reid vapor pressureSBP State Bank of PakistanS02 sulfur dioxideSO, oxides of sulfur

SPDC Social Policy and Development CentreTEL tetra-ethyl leadTSP total suspended particles

UNDP United Nations Development ProgrammeVKT vehicle kilometers traveledVOC volatile organic compoundWHO World Health OrganizationZOT Zulfiqarabad Oil Terminal

ix

Units of Measure

bpsd barrels per stream daydl deciliter

g/cc grams per cubic centimeterg/i grams per liter

GW gigawattkg kilogram

kg/m3 kilograms per cubic meterkm kilometer

kmlh kilometers per hourkPa thousand pascals

ktpa thousand (metric) tons per annumI liter

MON motor octane numberppm parts per millionpsia pounds per square inch absoluteRON research octane number

RONC research octane number clearRs Pakistani rupees

T90 temperature at which 90 percent of the fuel evaporatesktpsd thousand [metric] tons per stream day

tpa (metric) tons per annumvol% percent by volumewt% percent by weight

wt ppm parts per million by weightpig/m

3 mnicrograms per cubic meterpig/dl micrograms per deciliter

ptm micron (one-thousandth of a millimeter)

x

Glossary of Terms

API gravity An arbitrary gravity scale expressing the gravity or density of liquidpetroleum products, expressed in terms of degrees API. The formulais °API = (141.5/specific gravity at 60-60 °F) -131.5.

Aromatics Hydrocarbons that contain one or more benzene rings in theirmolecular structure. Aromatics have valuable anti-knock (high-octane) characteristics.

Benzene An aromatic hydrocarbon with a single six-carbon ring and no alkylbranches. Benzene is a carcinogen.

Blending octane The effective octane number of a gasoline component when it isnumber blended into gasoline. High blending octane materials behave as

though they had octane numbers higher than shown by laboratorytests on the pure material.

Blendstock A component combined with other materials to produce a finishedrefined product.

Catalytic converter A device built into the exhaust system of an engine containing acatalyst that converts carbon monoxide (CO) to carbon dioxide, andunburned hydrocarbons to carbon dioxide and water. If only CO andunburned hydrocarbons are converted, the catalyst is called a two-way catalyst. A three-way catalyst converts, in addition, oxides ofnitrogen (NO,) to nitrogen and water (or oxygen or carbon dioxide).

Cetane number An empirical measure of a diesel fuel's ignition quality thatindicates the readiness of the fuel to ignite spontaneously under thetemperature and pressure conditions in the engine's combustionchamber. Adding cetane improvement additives can increase thecetane number.

Clear octane The octane number of gasoline without octane-improving additivessuch as lead. Where RON rather than MON is being discussed (as inthis report), this is also referred to as clear RON, or RONC.

Cost, insurance, and A term used in foreign trade contracts where the exporter, infreight (CIF) addition to the free-on-board charges, pays the cost of the insurance

and the freight; in other words, the price includes all charges up tothe port of delivery.

Covariate An explanatory variable on the right-hand side of a regressionequation.

xi

Cut point A temperature limit of a cut, which in tum is the portion of crude oilboiling within certain temperature limits.

Diluent Something that dilutes. MTBE, for example, contains no benzene,no sulfur, no aromatics, and no olefins. Adding MTBE thus"dilutes" all other components having benzene, sulfur, aromatics,and olefins.

Elasticity Percent change in quantity caused by a I percent change in price.

Fluidized catalytic A refinery process for converting heavy oils into lighter products,cracking (FCC) including gasoline.

Flash point The lowest temperature (under certain conditions) at which acombustible liquid will give off sufficient vapor to form a flamrnablemixture with air. Denotes the volatility of the product.

Fractionation The separation of crude oil into a number of components accordingto their boiling points.

Free on board (FOB) The basis of an export contract in which the seller pays for sendingthe goods to the port of shipment and loading them on to the ship oraircraft. The seller also pays for the insurance up to this point.

Heavy end The higher boiling point and density fraction of a petroleumfraction, as in the heavy end of diesel.

Hydrocarbons Organic compounds composed of carbon and hydrogen.

Hydroskimming Simple refineries with a reformer to increase octane of the gasolinefraction, but not other conversion process units.

Hydrotreating A refinery process in which a stream is treated with hydrogen toreduce the amount of sulfur, nitrogen, and other heteroatoms, and tosaturate double bonds (for example, in aromatics and diolefins). Theterms hydrotreating, hydroprocessing, and hydrodesulfurization areused rather loosely in the industry.

Hydrodesulfurization Removal of sulfur in a fuel in the presence of hydrogen.

Input-Output Analysis A mathematical procedure that takes account of the interdependenceamong the economy's industries and determines the amount ofoutput each industry must provide as inputs to the other industries inthe economy.

Isomerization A process for increasing the octane of light hydrocarbons byconverting them from straight-chain hydrocarbons to branchedhydrocarbons. Once-through isomerization refers to a processconfiguration where the products are not recycled (product recyclingincreases the octane further).

xii

Motor octane number The octane number of a fuel, determined when vehicles are operated(MON) at high speed or under highway driving conditions.

Naphtha A petroleum fraction in the range of C5 (hydrocarbons with fivecarbon atoms) to 216f degrees Celsius. Naphthas are majorconstituents of gasoline and generally need processing to makesuitable quality gasoline.

Octane number A measure of resistance to self-ignition (knocking) of a gasolinewhen mixed with air in an engine cylinder. The higher the octanenumber, the higher the anti-knock quality of the gasoline. In theUnited States, the word octane, as used at filling stations, refers toan average of MON and RON; it is also called the anti-knock index.Because MON is usually lower than RON, averaging the two resultsin a lower number, typically by 4 or 5. For example, "87 octane" inthe United States corresponds to 91 or 92 RON.

Olefins A class of hydrocarbons that have one double-bond in their carbonstructure.

Oxygenates Any organic compounds containing oxygen. Specifically for thepetroleum industry, oxygenates typically refer to alcohols and ethersused to boost octane or to reduce CO in engine exhausts.

Ozone A colorless gas, it is an allotropic form of oxygen in which themolecule is 03.

Polycyclic aromatics Aromatic compounds with more than one six-membered ring.(polycyclics) Polycyclics are carcinogens. The diesel fraction of FCC product is a

source of polycyclics.

Reformate A high-aromatic, high-octane product made in a reformer and usedto blend motor gasoline or aviation gasoline.

Reid vapor pressure A standardized measure of a fuel's volatility at a specified set of(RVP) conditions, with a higher value indicating a more volatile fuel. RVP

is usually measured in psia (pounds per square inch absolute) or kPa(thousand pascals).

Research octane The octane number of a fuel, determined when vehicles are operatednumber (RON) at low speed or under city driving conditions.

Severity The intensity of the operating conditions of a process unit, indicatedby the product's clear research octane number (RONC) in the caseof reformers.

Sour crude oil A crude oil containing high levels of sulfur.

Slate A crude (or product) slate refers to the mix of crudes (or products)making up the total that a refinery processes (or produces).

xiii

Translog equation Equation in which the dependent variable is regressed against aproduct of logarithms of two or more independent variables.

Tgo TemperatuTe at which 90 percent of fuel evaporates.

xiv

Executive Summary

1. The Pakistan Clean Fuels program was undertaken at the request of theMinistry of Petroleum and Natural Resources (MPNR) and the Ministry of Environment,Local Government, and Rural Development to examine the feasibility of therecommendations made at the Clean Fuels Workshop held in Islamabad in October1997.1 More specifically, the workshop participants proposed a timetable for phasing leadout of gasoline, increasing the average gasoline octane, and reducing sulfur in diesel andfuel oil. Other recommendations included measures to reduce vehicular emissions andcollect air quality data more systematically.

2. Pakistan remains one of the two countries in South Asia still using leadedgasoline widely, the other country being Sri Lanka. Given extensively documentedepidemiological evidence concerning the adverse impact of lead on public health,particularly on the intellectual development of children, lead elimination is the highestpriority for fuel quality improvement facing the Government of Pakistan. Anotherpollutant of concem is high ambient concentrations of fine particles. Reducing sulfur infuels helps to lower particulate concentrations because sulfur contributes to the formationof secondary particulates. The workshop recommendations address these two concerns.

3. This program also examined another aspect of particulate emissions.Diesel vehicles generally contribute much more to particulate emissions than gasolinevehicles. Historically, consumption of diesel by vehicles has exceeded that of gasoline inPakistan several-fold, in part because of the governnent's inter-fuel pricing policy, whichhas set the price of diesel at about one-half that of gasoline. This has encouraged theconversion of light-duty vehicles, which might otherwise run on gasoline, to diesel.Narrowing the price difference between gasoline and diesel would discourage vehicleowners from converting light-duty vehicles to diesel in the future, and would evenpromote replacement of diesel vehicles with gasoline vehicles at the time of vehicleretirement.

Clean-Fuels Workshops and Analysis

4. A "Clean Fuels Workshop" was held in Islamabad on 20-21 October 1997to examine how to improve the quality of fuels in Pakistan. Sponsored by the Ministry ofEnvironment, Local Government, and Rural Development, the Ministry of Petroleum andNatural Resources, and the World Bank, the workshop was attended by representativesfrom the Government of Pakistan, the downstream petroleum sector, universities,research institutions, and nongovernmental organizations (NGOs), and by specialists from

This report was completed in May 2001 and reflects the situation in Pakistan up until that point.

2 Pakistan Clean Fuels

other countries. The workshop participants recommended (1) tightened specifications forgasoline, diesel, and fuel oil, as well as (2) a timetable for implementing the newspecifications, as shown in Table E. 1. The timetable was modified in 1999.

Table E.1: October 1997 Workshop: Recommended Timetable for Tightening FuelSpecifications, Including 1999 Revisions

Specifications TimetableParameter Old New Proposed in 10/9 7 Revised in 1999

Gasoline lead, g/l 0.42 0.35 end-1998 2000

0.35 0.15 2003 2003

0.15 0.013 2005 2005

Gasoline research 80 87 Withdraw 80 RON by end 1998 2000octane number (RON) and replace with 87 RON

- 92 unleaded Introduce by end 1998 Post-PARCOstartup

Diesel sulfur, wt% 1.0 0.5 2000 2001

Fuel oil sulfur, wt/o 3.5 2.0 2000 2001

Notes: gll grams per liter; wtPo percent by weight; PARCO Pakistan Arab Refinery Company. - notapplicable.

5. At the October 1997 workshop, it was decided that the Government ofPakistan and the World Bank would undertake a joint techno-economic analysis of clean-fuels options and the feasibility of the above timetable. The requirements of securingfunding, as well as intemal developments in Pakistan, delayed the commencement of thestudy until mid-1999.

6. Industry-standard linear programming software was used to analyze theimpact of the recommended specifications on the downstream petroleum sector.Additional steps to limit benzene and total aromatics in gasoline were also examined. Theresults are surnmarized in Table E.2. The gasoline quality improvement steps are thesame as those indicated in Table E. 1. For diesel and fuel oil, the incremental cost given ineach year is that required to reduce diesel sulfur to 0.5 percent by weight (on a per-literbasis) and the national average of fuel oil sulfur to 2 percent by weight. The last columnshows the cost of installing isomerization units at three refineries to lower benzene andtotal aromatics in gasoline. A comparison of gasoline fuel quality with and withoutisomerization is given in Table E.3.

Executive Sunmary 3

Table E.2: Incremental Cost (1998 US$)

Parameter 2000 2003 2005 2005, low aromatics

Annual cost for gasoline (US$ million) 1.8 -5.5 1.5 7.2

Cost per liter of gasoline (US cents) 0.1 -0.3 0.1 0.4

Annual cost for diesel (US$ million) 16.7 22.0 24.2

Cost per liter of diesel (US cents) 0.3 0.3 0.3

Annual cost for fuel oil (US$ million) 104 105 114

Note: - not applicable.

Table E.3: Gasoline Physical Properties in 2005 (percent by volume)

Parameter ARL NRL PRL Dhodak PARCO

Benzene, without isomerization 4.6 4.2 4.3 3.6 4.0

Benzene, with isomerization 3.5 1.1 0.9 1.3 1.5

Total aromatics, without isomerization 41 38 39 32 32

Total aromatics, with isomerization 41 33 31 33 35

Notes: ARL Attock Refinery Limited; NRL National Refinery Limited; PRL Pakistan RefineryLimiited; PARCO Paldstan Arab Refinery Company; Dhodak is a condensate distillation unitlocated in Dhodak in the Punjab Province.

7. Two workshops were held in Islamabad at the end of March 2001 todiscuss the findings of the study and reach a consensus on what concrete steps to take inthe coming months. The target audience for the first workshop-hosted by the Ministry ofEnvironment, Local Government, and Rural Development-was stakeholders in theenvironment sector. Attending were representatives from the Pakistan EnviromnentProtection Agency, other government agencies, NGOs, universities, research institutions,and one refinery. The second workshop was organized by MPNR, aiming specifically atreviewing the technical details of the study findings with the refiners and oil marketingcompanies.

8. At the first of these two recent workshops, the findings of the study weresummarized as follows:

* The cost of eliminating lead in gasoline is surprisingly low because thePakistan Arab Refinery Company (PARCO) refinery, a new facilitycapable of producing high-octane blending components, has recently comeon stream. The incremental cost to consumers would be on the order of 0.5to 1 percent of the retail price, requiring little capital expenditure.

* In the process of eliminating lead, it would be important to introducelimits on benzene and aromatics. Levels of 5 percent benzene and 40-45percent total aromatics would be considered minimally acceptable byinternational standards, and Pakistan is in a position to impose these limitswithout additional capital expenditures.

4 Pakistan Clean Fuels

The incremental cost of reducing sulfur in diesel from 1 percent to 0.5percent, now considered minimally acceptable by international standards,is similarly low: about 1 percent of the retail price and requiring capitalexpenditures of about US$10 million (for storage tanks and otherinfrastructure requirements for blending domestically produced diesel withimported lower-sulfur [0.25 percent] diesel).

* The cost to Pakistan of reducing sulfur in fuel oil, in contrast, would besubstantial: more than US$100 million per annum as a result of importinglower-sulfur fuel oil. This argues for accelerating the switch from fuel oilto natural gas.

9. At the second workshop organized by MPNR, refiners and oil marketingcompany representatives supported the following two points highlighted during thepresentation of the study findings.

The incremental cost of eliminating lead in gasoline and reducing sulfur indiesel to 0.5 percent is surprisingly low, for the former because PARCOhas already made much of the investment needed to eliminate lead, and forthe latter because Pakistan relies heavily on imports.

* It is important to introduce limits on benzene and total aromatics, andPakistan can currently initiate 5 percent and 40-45 percent limits,respectively, without incurring any capital expenditures in the future at thetime of complete lead elimination. This is important for preventingbenzene from exceeding 5 percent if and when octane grades higher thanthe current 87 RON are introduced on a wide scale.

10. MPNR, the Ministry of Environment, Local Government, and RuralDevelopment, and the industry expressed strong interest in accelerating the timetable foreliminating lead in gasoline. In particular, the relatively low incremental cost of doing sowas seen as a unique opportunity for the Government of Pakistan to upgrade the qualityof petroleum products.

11. The second workshop concluded by proposing the following action items:

* The timetable for lead phaseout is to be accelerated, with the final date forlead elimination brought forward from the original date of 2005 to 2002 or2003. One option is to supply unleaded gasoline to all areas except thoseserved by Attock Refinery as soon as possible.

* The government will issue revised gasoline specifications, limitingbenzene to 5 percent and aromatics to 40-45 percent (precise level to befinalized).

* Because of the contract with Kuwait Petroleum Corporation, whichinformed Pakistan that it cannot supply 0.5-percent-sulfur diesel until June2002 (because of a fire at one of their refineries), Pakistan will switch to0.5-percent-sulfur diesel in June 2002. The logistics of importing 0.25-

Executive Summary 5

percent-sulfur diesel and blending with domestically produced dieselwould need to be finalized.

* Because the incremental cost of lowering sulfur in fuel oil is considerable,the government should accelerate switching from fuel oil to natural gasand consider supplying imported lower-sulfur fuel oil to fuel oil userslocated in or near densely populated areas.

Transport Fuel Tax Policy12. Following the refinery study, the second component of the Pakistan CleanFuels program addressed how to stem the conversion of light-duty vehicles from gasolineto diesel, and in fact reverse the trend so that the majority of light-duty vehicles aregasoline-powered.

13. Once lead is phased out of gasoline, particulate emissions from dieselvehicles would be expected to be the most serious pollutant affecting public health in thetransport sector. Diesel vehicles of the technology used in Pakistan emit much more fineparticles than gasoline vehicles. Further, emerging evidence suggests that dieselparticulate emissions are more harmful than those of gasoline vehicles.

14. Because the price of diesel has historically been about one-half that ofgasoline, some owners of gasoline cars even convert their vehicles to run on diesel. Over90 percent of diesel was used in the transport sector in the second half of the 1990s.While heavy-duty vehicles would be expected to continue to run on diesel irrespective ofthe inter-fuel price difference, encouraging light-duty vehicles used in urban centers torun on gasoline rather than diesel would confer significant health benefits.

15. One effective option, if it can be implemented successfully, isdifferentiated vehicle taxation, by which light-duty diesel vehicles are taxed considerablymore than their gasoline equivalents so as to make the purchase of the formereconomically unattractive. However, discussions held with provincial tax officialsindicated that such a tax scheme would not be feasible given the limitations of Pakistan'stax collection mechanism. Therefore, this study's scope was limited to examining the useof fuel tax policy to achieve the same objective. More specifically, this componentinvestigated two scenarios for narrowing the price difference between gasoline and dieselto the level where the owners of light-duty vehicles would be indifferent to the choice offuel. The two scenarios are as follows:

* Scenario 1: A 10 percent decrease in the price of gasoline and a 67 percentincrease in the price of diesel

* Scenario 2: A 29 percent decrease in the price of gasoline and a 10 percentincrease in the price of diesel.

If light-duty diesel vehicles used in intra-city transport were hypothetically converted togasoline as a result of the above price adjustments, this would represent diesel savings ofapproximately 250,000 metric tons. Even more important is preventing the future

6 Pakistan Clean Fuels

conversion of gasoline vehicles currently driven in urban centers (all except gasoline usedby two- and three-wheelers)--amounting to 700,000 metric tons-to diesel.

16. It is important to acknowledge the serious limitation of using only fuel taxpolicy to influence the choice of fuel, given the large price difference between gasolineand diesel that exists today. Diesel is used in freight transport, so that a marked rise in theprice of diesel affects heavy-duty diesel vehicles for which the pricing scheme is notintended, resulting in economy-wide inflation. If the poor are to be affecteddisproportionately by the impact of the diesel price rise, such a measure will beregressive. General inflation would also affect the balance of payments by making export-oriented and import-substitution sectors less competitive.

17. At the same time, however, Pakistan is an importer of diesel-so if theconsumption of diesel falls in response to a price increase, the petroleum-product importbill will be reduced. Further, government revenue will rise because of greater tax takefrom the sale of diesel, and this additional income can be used to mitigate some of theadverse effects of the diesel price increase.

18. Modeling was carried out to address the above questions by means ofinput-output analysis, using household survey data and the Integrated Social Policy andMacroeconomic model developed by the Social Policy and Development Center inKarachi. Scenario 1 was found to have a significant impact on the cost of living ofhouseholds, amounting to an increase of 1.4 percent of income on average. The impact ishigher for urban households (1.5 percent) than rural (1.3 percent). The impact isregressive, with the increase in household expenditure falling from 1.9 percent for thebottom income quartile to I percent for the top income quartile in rural areas, and from1.9 percent to 1.2 percent for the corresponding income groups in urban areas. Therefore,if scenario 1 is adopted as a policy, it may be necessary to try to mitigate the impact onlower-income groups by means of safety net measures. In contrast, the impact on the costof living was found to be generally negligible in scenario 2, with the increase expressed inpercentage of income remaining below 0.1 percent. The top income quartile in rural areasand the top two income quartiles in urban areas actually benefit as a result of a large fallin the price of gasoline.

19. The government's tax revenue was found to increase by approximately Rs45 billion2 in scenario 1, and to suffer a slight loss (Rs 3 billion) in scenario 2. Theimpacts on other economic parameters are shown in Table E.4.

2 A billion is 1,000 million.

Executive Summary 7

Table E.4: Changes in Macroeconomic Parameters for Fiscal 1999-2000

Macroeconomic variable Unit Scenario I Scenario 2

Gross domestic product (GDP) growth rate %, absolute -0.26 -0.02

Unemployment rate %, absolute 0.27 -0.03

Rate of inflation %, absolute 1.43 -0.08

Current account deficit % of GDP -0.47 0.07

Budget deficit % of GDP -1.03 0.1

Rate of depreciation of nominal exchange rate %, absolute 1.43 -0.03

Ratio of tax to gross domestic product %, absolute 1.29 -0.08

Incidence of poverty % of population 1 -0.05

20. Scenario 1 has major economy-wide consequences. It generates substantialadditional revenues (thereby reducing the budget deficit) and reduces importssignificantly (thereby improving the balance of payments) but at the cost of somewhatlower growth (due primarily to contraction of the road transport sector), significantlyhigher short-run inflation, and slightly higher unemployment. The impact on the cost ofliving is regressive, with the poor being the most severely affected. The poor areconservatively estimated to increase by almost 1.5 million.

21. Scenario 2 benefits the richer car-users considerably, and encouragesrather than discourages the use of private cars in urban areas. As such, it is not a desirablepolicy option. It does have more limited macroeconomic implications than scenario 1,achieving the same desired inter-fuel price difference but causing much smallerdislocation to the economy. There are some minor revenue losses and a small worseningin the balance of payments, but it marginally affects the poorer sections of society whileconferring some benefits to car owners.

22. The sharp diesel price hike contemplated in scenario 1 is likely to meetstiff resistance, especially because heavy-duty vehicles (which account for bulk of dieselconsumption) will have no option but to bear the higher input costs and raise transporttariffs. This highlights the limitation of not incorporating differentiated vehicle tax in theanalysis. It is proposed that the government match such a move with a countervailingrelief in the form of a large reduction in the standard general sales tax (GST) rate. A one-third reduction in the GST rate is estimated to lower the average burden of the tax by 1.4percent of income in urban areas and 1 percent in rural areas. This intervention isestimated to compensate for the negative impact stemming from fuel price changes byover 92 percent in urban areas and by over 77 percent in rural areas.

23. Such a counter-measure may or may not succeed. Its success will dependessentially on the perceived burden of GST and the extent to which the fall in the rate ofGST is accompanied by a corresponding fall in the prices of the essential goods andservices. On balance, the political feasibility of raising the diesel price sharply isconsidered low. If a differentiated vehicle tax scheme must be ruled out, scenario 2 may

8 Pakistan Clean Fuels

be a less disruptive strategy than scenario 1, but it may also have serious adverse effectson the transport sector.

24. The above findings suggest that fuel tax policy alone is a poor instrumentfor inducing a shift from diesel- to gasoline-powered vehicles. Although scenario 2 mayhave negligible economy-wide consequences, the transport sector in Pakistan is plaguedby urban congestion and inadequate provision for road maintenance. A move that willcertainly encourage greater urban private car use will further exacerbate the transportsector's problems, even if there are environmental gains to be made. These observationshighlight the importance of coordinating policies across environment, transport, andenergy sectors, and of using a number of policy instruments rather than just one toaddress environmental and transport problems.

1

Background

1.1 Deteriorating urban air quality is one of the most serious environmentalproblems facing Pakistan today.3 Poor air quality threatens human health and causes otherforms of enviromnental damage. Among the greatest contributors to air pollution arevehicle emissions, including highly damaging emissions of lead and fine particulatematter. As incomes grow, so too do the numbers and use of motor vehicles, potentiallyworsening pollution.

1.2 Airbome fine particles and lead are the pollutants receiving the mostattention from policymakers in Pakistan because of their serious adverse effects on publichealth. A recent investigation into the quality of air in three cities-Lahore, Rawalpindi,and Islamabad-found high concentrations of PM, 0 (particles smaller than 10 microns, or10 gtm), lead and oxides of nitrogen (NOJ). Air quality was monitored continuously for16 to 18 hours at 10 locations, all located on major roads. Of these, an average of close to900 micrograms of PMIo per cubic meter (Qg/m3 ) was recorded at eight locations, and theremaining two locations recorded an average of about 500 4g/m3, both of which areexceptionally high levels by any standards. Airborne lead varied between 0.7 and 10jig/n 3, again very high (JICA 2000).

1.3 Sources of PMIo include large industrial sources such as power plants,small industrial sources and commercial establishments, houses, refuse burning, andvehicles. Among vehicles, diesel vehicles and two-stroke engine gasoline vehicles are thetwo largest sources. As for lead, the combustion of leaded gasoline in vehicles is asignificant source, but other sources such as smelters and battery manufacturing andrecycling facilities can also be important. While this report focuses on the combustion ofoil products, especially in vehicles, it is important to bear in mind that an effective urbanair quality management strategy needs to address all major sources of emissions,including such often neglected but important sources as biomass, refuse buming, andresuspension of road dust (road dust thrown into the air).

3 This report was comnpleted in May 2001 and reflects the situation in Pakistan up until that point.

9

10 Pakistan Clean Fuels

1.4 This chapter provides background information to place in context thestudies undertaken in the Pakistan Clean Fuels program. It begins by giving an overviewof major pollutants with serious health effects. This is followed by a discussion on therole of fuel quality and its effects on emissions, especially from vehicles. Specialemphasis is placed on lead in gasoline and sulfur in fuels, two of the focal points of thePakistan Clean Fuels program. The chapter then describes the downstream petroleumsector in Pakistan, the quality of domestically refined fuels, and the role of inter-fuelpricing. It closes by outlining the rest of the report.

The Link Between Fuel, Transport, and the Environment

1.5 Fuel quality and vehicle emissions are closely linked, and they in turnaffect the level of air pollution. In developing a strategy for urban air qualitymanagement, it is important first to understand which pollutants are affecting publichealth the most in a given city. This in turn depends on the toxicity and the ambientconcentrations of each pollutant. The next step is to identify sources that are makingsignificant contributions to the pollutants of concern, and formulate plans for controllingthese sources. Because transport is typically one of the major contributors to urban airpollution, reducing vehicle emissions is generally an important part of a strategy formanaging urban air quality. One of the available options for reducing emissions in thetransport sector is fuel quality improvement. Improving the quality of gasoline byeliminating lead is a particularly effective measure for reducing the exposure of thegeneral public to airborne lead.

1.6 The pollutants of special concern in Pakistan are lead and fine particulatematter. Transport contributes to high ambient levels of both pollutants. Vehicles emit leadas a result of the combustion of leaded gasoline. Fine particles are emitted directly fromvehicles, and in addition are formed as a result of secondary formation4 from NO, andoxides of sulfur (SO,). Both gasoline- and diesel-fueled vehicles emit NO,. In the case ofgasoline, NO, emissions can be reduced by means of three-way catalytic converters, butcatalysts cannot be used if gasoline is leaded because lead permanently deactivates thecatalyst. The amount of SO,, emitted is directly proportional to the amount of sulfur in thefuel and is reduced by treating the fuel itself.

Lead

1.7 Lead is one of the highest-risk pollutants still widely used in gasoline inPakistan as a historically inexpensive octane5 enhancer. The combustion of leadedgasoline contributes to the majority of airborne lead in many cities where leaded gasoline

4 See paragraph 1.25.

5 Octane is a measure of resistance to self-ignition (knocking) of a gasoline when rnixed with air in anengine cylinder. The higher the octane number, the higher the anti-knock quality of the gasoline. In theUTnited States, octane refers to an average of MON and RON; because MON is usually lower thanRON, averaging the two results in a lower number, typically by 4 or 5. For example, -87 octane" in theUnited States corresponds to 91 or 92 RON.

Background 1 1

is still used. Anthropogenic sources of lead include not only lead in gasoline, but also thefollowing:

* Lead in drinking water, because of the historical use of lead in pipes forwater distribution

* Lead-based paint

* Stationary sources such as smelters and lead-battery recycling andmanufacturing facilities

* Activities such as mining

* Tobacco

* Food

* Lead-soldered beverage and food cans

* Dust and soil* Traditional cosmetics and medicines

* Lead-glazed ceramics.

1.8 The toxicity of lead has been known for centuries. At levels exceeding 70micrograms (.g) per deciliter (dl) of blood for children and 100 pLg/dl for adults, lead cancause paralysis, seizures, coma, and death. What have come to light only in the last twodecades, however, are the adverse health effects of lead even at levels previouslyconsidered safe. As a result of new research findings, health organizations such as theU.S. Centers for Disease Control and Prevention (CDC) have steadily revised theirguidelines for lead. Today, environmental intervention is recommended for blood leadlevels above 10 F.g/dl (WHO 1995a).

1.9 It should be noted that airborne lead settles on dust, falls on vegetation, andmay contaminate drinking water. Therefore, airborne lead cannot be delinked from leadfound in food and water. For nonsmoking adults, major sources of lead are food, water, andairborne lead, if the level of the latter is high. For children, in addition to food, water, andair, dust and soil constitute a significant exposure pathway. Any program to combat theadverse health effects of lead should attempt to estimate all significant sources of leadexposure so that effective steps can be taken to reduce exposure. Whatever additionalsources of lead emissions may exist, eliminating lead in gasoline is important. Unlike otherpollutants, such as hydrocarbons, lead does not degrade and continues to accumulate in theenvironment unless the continuing emissions of lead, including those from gasoline, arestopped.

1.10 An excellent overview of the health effects of lead can be found in a 1995World Health Organization (WHO) publication Environmental Health Criteria 165:Inorganic Lead (WHO 1995b).6 Most of the lead absorbed by the body is found in the

6 Unless indicated otherwise, all the infornation presented in this section on the health effects of lead istaken from this WHO publication.

12 Pakistan Clean Fuels

bones, and some is found in blood. Moreover, bone is a major storage site of lead, andserves as an endogenous source of lead even after exposure to environmental lead hasceased. During pregnancy (Silbergeld 1991) and in old age, lead from the bones is releasedinto the blood.

1.11 The absorption of lead from environmental sources is not a linear functionof the amount of lead intake. It depends on the chemical and physical state of the lead, andon factors such as the age, nutritional condition, and physiological status of the individual.For example, there is evidence that more lead is absorbed when dietary calcium intake islow or if there is iron deficiency. The amount of lead absorbed by the body increasessignificantly when the stomach is empty. The rate of absorption is also higher for childrenthan for adults. That is to say, poor, malnourished children are even more susceptible to leadpoisoning than others.

1.12 The largest body of observational studies on the health effects of leadconcerns its impact on the intellectual development, typically measured in terms ofintelligence quotient (IQ), and behavioral problems of children. There has been much publichealth interest in this issue because of mounting evidence that continual exposure ofchildren to even low levels of lead could have a negative impact on their intelligence. Asystematic review of 26 epidemiological studies can be found in Pocock and others (1994).The published studies can be divided into two broad categories: prospective and cross-sectional. Prospective studies collect data from the same group of children over a number ofyears, so as to identify whether there is a specific period in a child's intellectualdevelopment when exposure to lead is particularly damaging. Cross-sectional studiesattempt to correlate the "body burden" of lead with children's intelligence, both beingmeasured at the same time. If environmental exposure to lead before commencement of thestudy significantly affected the child's IQ, cross-sectional studies would not be in a positionto identify the causal link unless the level of environmental exposure to lead has beenconstant.

1.13 Because a large number of factors affect IQ, a multiple-regression analysiswith a large number of independent variables, of which lead is one, needs to be conductedin order to isolate the effect of lead. Increasing the sample size will increase markedly thestatistical significance of the results. The small sample size of any given study, coupled withthe complexity of identifying all the relevant covariates (factors affecting IQ, or independentvariables on the right-hand side of the equation), make it impossible to draw definitiveconclusions from any single study; a synthesis of a number of studies is needed to overcomethese impediments.

1.14 These limitations not withstanding, the studies that have been conductedstrongly support an inverse association between the body burden of lead and children's IQs.A reasonable rule of thumb appears to be that increasing the level of blood lead from 10,ug/dl to 20 jtg/dl causes an average decrement of about 1-2 IQ points.

1.15 A follow-up study by Bellinger and others (1992) found that there was anage of critical exposure. IQ was strongly and statistically negatively associated with thelevel of lead in blood measured at two years of age. This was also supported by a study

Background 13

conducted in the lead-smelting community of Port Pirie in Australia (Baghurst and others1992). The evidence from other prospective studies, however, is conflicting.

1.16 Unless the level of blood lead is extremely high, the impact of lead on agiven individual's IQ may not be noticeable. It is, however, a serious public health concemfor the community as a whole, because exposure to lead shifts the IQ distribution curve ofthe entire population, reducing average intelligence. It is difficult to estimate the economiccosts of loss in IQ, but they are doubtless substantial. Costs incurred include additionalremedial education, health care, and loss in productivity.

1.17 While the effect of lead on children's IQ is probably the most significanthealth impact of using leaded gasoline, there are others:

* Qualitative evidence indicates that lead may adversely affect thereproductive process in men and women, including increased frequency ofmiscarriages, although the results are conflicting below blood lead levelsof 30 ,ug/dl.

* Renal (kidney) function impairment has been correlated with blood leadlevels above 35 1Lg/dl.

* The effect of lead on the cardiovascular system has been studiedextensively. There appears to be a weak but positive association betweenlead in blood and blood pressure.

1.18 Finally, it should be noted that many, if not most, of the studies examiningthe health impact of lead have been undertaken in the United States, Australia, and Britain,where living conditions differ from those in Pakistan. Any deleterious effects of leadexposure, even at low levels, may be exacerbated when additional factors such as calciumor iron deficiency are present. Studies examining and quantifying the covariate effects oflead in combination with these factors are likely to underscore the importance of furtherlead reduction, and would be helpful in guiding policymakers.

Particulate Matter

1.19 Small particles remain in suspension for hours or days, are liable to travelconsiderable distances from the source, and enter the respiratory tract and reach the deeperparts of the lungs. PM1o represents the size range of particles likely to pass the nose andmouth. PM2.5 (particles smaller than 2.5 p.m) represents more closely the size range ofparticles able to reach the deeper parts of the respiratory tract.

1.20 A series of extensive studies, conducted mainly in the United States, hasdemonstrated clearer associations between particulate concentrations and small changesin a wide range of health indicators-mortality, hospital admissions, emergency roomvisits, time off school or work, respiratory symptoms, exacerbations of asthma, andchanges in lung function-than with other pollutants. Of the various health indicators, themeasurement of mortality is the most certain, having been particularly well studied withmore consistent results than those regarding the other indicators. Although thecomposition of PM1 o can vary widely from area to area and with time, the size of the

14 Pakistan Clean Fuels

estimated effects does not vary greatly with location. The WHO estimates that highambient concentrations of particulate matter are responsible for about half-a-millionpremature deaths worldwide every year.

1.21 In terms of health impact, PMIo is much more serious than total suspendedparticles (TSP), which include particulate matter of all sizes. Coarse, wind-blown particles,for example, are believed not to have a significant effect upon health. In the United States,federal TSP standards were superseded by PMIO standards in 1987, and there are nowadditional standards for PM2.5. In the case of vehicles, the majority of the particles emittedfall in the sub-micron range and, furthermore, are emitted near ground level where peoplelive and work. Therefore, vehicular particulate emissions are especially harmful to publichealth. Particles found in vehicle exhaust consist of a carbonaceous core, adsorbedhydrocarbons from engine oil and fuel, adsorbed sulfates and nitrates, water, and inorganicmaterials such as those produced by internal engine abrasion.

1.22 Recent studies have indicated that the number of particles to which theindividual is exposed could be more important than their mass. Whereas air qualitystandards for particulate matter are currently based on mass throughout the world, agrowing number of countries will introduce standards based on number rather thanweight in the medium term. Measures that reduce the mass of particles emitted do notnecessarily reduce the number of fine particles. For example, a recent study showed that athighway speeds the numbers of particles emitted were similar among the three gasoline- andfour diesel-vehicle types tested and remained unaffected by the quality of the fuels(Automotive Environment Analyst 1998), although at lower speeds the number of particlesin diesel emissions was considerably greater.

1.23 Traffic is a large contributor to fine particulate emissions. On a mass basis,diesel vehicles emit much more fine particulate matter than gasoline vehicles in general.In terms of the number of particles, the difference between light-duty gasoline and light-duty diesel vehicle emissions in one study was found to vary from a factor of over 2,000at 50 kilometers per hour (km/h) to 3 at 120 km/h. Although the number of particles ingasoline exhaust is up to three orders of magnitude smaller than that in diesel exhaust, thehealth impact may not be correspondingly smaller: in terms of size, a higher proportion ofgasoline particulate emissions may be of smaller size (less than I .tm) than dieselemissions (CONCAWE 1998). At the same time, there is a growing view that dieselexhaust poses a serious cancer risk, suggesting that diesel particulate emissions may beespecially harmful to public health.

1.24 A significant vehicular source of fine particles in South Asia is two- andthree-wheelers run by two-stroke engines. Because they are less expensive than othervehicles, two- and three-wheelers account for nearly one-half of all vehicles in Pakistan.Until recently new two-stroke engines emitted as much as an order of magnitude moreparticulate matter than four-stroke engines of similar size. When vehicle age,maintenance, lubricant, and fuel quality are taken into account, two-stroke engines inPakistan probably emit particulate matter at an even higher factor. Two-stroke enginestypically have a lower fuel efficiency than four-stroke engines, with as much as 15-40

Background 15

percent of the fuel-air mixture escaping the engine's combustion chamber unburned.These "scavenging losses" contain a high level of unburned gasoline and lubricant, whichincreases emissions of hydrocarbons and organic lead (which is even more damaging tohealth than the inorganic lead produced when gasoline lead additives combust). Some ofthe incompletely burned lubricant and heavier portions of gasoline are emitted as smalloil droplets, which in turn increase visible smoke and particulate emissions.

1.25 All combustion and metallurgical processes and many other industrialoperations lead to the emission of particles into the atmosphere. The particles emitteddirectly from a source are termed primary. Particles formed within the atmosphere, mostlyfrom the chemical oxidation of atmospheric gases, are termed secondary. NO, and SO.contribute to secondary particulate formation. The largest individual contributor to primaryparticles is incomplete combustion of fossil fuels and biomass. As a rough generalization,particles generated from combustion and condensation of vapors are mostly in the PM2.5fraction (that is, 2.5 microns or smaller), while particles from mechanical breakup ofsolids and liquids are larger. Poor fuel quality, inefficient combustion processes, and poorvehicle and equipment maintenance all contribute to particulate emissions.

1.26 The WHO no longer has guidelines for PM,( or PM2.5 on the grounds that athreshold for the onset of health effects could not be detected. Instead, the WHOrecommends that the figures given in Table 1.1 be used to determine acceptable risk. Thefigures represent the percentage increase in health indicators as a result of a 10-jig'm 3

increase in the ambient concentration of PM1 o and PM2.5. For example, an increase in theambient PM2.5 concentration of 10 .g/rm3 increases the mortality of the exposed populationby 1.5 percent.

Table 1.1: Impact of a 1 O-pg/m3 Change in the Ambient

Concentration of Particulate Matter on Health

% Change

Health Endpoint PM10 PM2.5

Daily mortality 0.70 ± 0.12 1.5 ± 0.4

Hospital admissions 0.84 ± 0.33 5

Bronchodilator use 0.34 ± 0.13 No value given

Symptom exacerbation 0.35 + 0.16 No value given

Cough 0.45 ± 0.23 No value givenPeak expiratory flow 0.013 i 0.004 No value givenSource: WHO (2000)

Other Pollutants

1.27 Carbon monoxide (CO) is a colorless, odorless gas that inhibits thecapacity of blood to carry oxygen to organs and tissues. High levels of CO can cause

16 Pakistan Clean Fuels

people with chronic heart disease to experience chest pain. Very high levels of CO canimpair vision, manual dexterity, and learning ability, and can cause death.

1.28 CO is a product of the incomplete combustion of fossil fuels. In mostcities gasoline-fueled vehicles account for most CO emissions. The level of CO emissionscan be reduced by incorporating oxygenates in gasoline for old vehicles and by usingoxidation catalysts.

1.29 Sulfur dioxide (SO2), one of the oxides of sulfur, reduces lung function inasthmatics and exacerbates respiratory problems in sensitive individuals. Sulfur oxidesare formed when fossil fuels containing sulfur are burned. These oxides contribute to acidrain and to the formation of secondary particles. The amount of sulfur emitted is directlyproportional to the amount of sulfur in the fuel. It can be reduced by treating the fuel, forexample, through hydrotreating, or by installing sulfur removal devices at the point ofemission, such as flue gas desulfurization units at power plants. Nitrogen dioxide (NO2),one of the oxides of nitrogen, causes changes in lung function in asthmatics. Nitrogenoxides are formed during combustion as nitrogen in the air reacts with oxygen at hightemperature. Like sulfur oxides, these oxides contribute to both acid rain and secondaryparticulate formation. Nitrogen oxides are also precursors of ground-level ozone.

1.30 Power plants and diesel- and gasoline-fueled vehicles emit nitrogenoxides. The amount of NO, formed can be reduced by controlling the peak combustiontemperature (for example, by recirculating exhaust gas in vehicles); reducing the amountof oxygen available during combustion; or converting NO, to oxygen-containinginorganic compounds and nitrogen (for example, by installing three-way catalyticconverters).

1.31 Ozone causes photochemical smog and has been associated with transienteffects on the human respiratory system, particularly the decline in pulmonary functionduring light to heavy exercise. Gasoline-fueled vehicles are a significant source ofvolatile organic compounds, which along with NO, are precursors of ozone. Ozoneabatement is complicated by nonlinear interactions among ozone precursors-the amountof ozone formed is not directly proportional to the ambient concentrations of volatileorganic compounds and NO, but is a complex function of a number of factors thatinclude the ratio of these two precursors. It is therefore important to collect relevant dataand understand the chemistry of ozone formation before selecting mitigation measures.

1.32 Another concern is airborne toxics, of which only limited data on ambientconcentrations are available. Toxic emissions from vehicles include benzene, polycyclicaromatics (aromatics with more than one six-membered ring), 1,3-butadiene, andaldehydes. 1,3-butadiene is a potent carcinogen. Benzene, another carcinogen, isincreasingly targeted for reduction in gasoline.

Fuel Quality

1.33 There are complex interactions between fuels, vehicle technology, testdriving cycles, and reference fuels with regard to their relative influences on vehicleemissions. A given vehicle will show different emission levels depending on the test-

Background 17

driving cycle. Therefore, it is important to bear in mind that changing fuel specificationswill not necessarily affect all vehicles in the same way.

1.34 A number of fuel parameters affect vehicle emissions. For gasoline, theyinclude volatility, distillation temperature profile, and the amount of lead, sulfur, benzene,total aromatics,7 olefins, and oxygen-containing compounds commonly referred to asoxygenates. For diesel, they include the distillation temperature profile, density, cetane,and the amount of sulfur and aromatic-particularly polycyclic aromatic-compounds.

1.35 Lead is one pollutant whose removal from gasoline will have animmediate impact on emissions from all vehicles. As noted previously, in Pakistan, wherethere are a large number of two-stroke engine two- and three-wheelers, some of the leadis emitted uncombusted. Because the resulting emissions of organic lead are even moredamaging to public health than the inorganic lead that is formed when gasoline leadadditives combust, the need to phase out lead in gasoline becomes all the more urgent.Lead also acts as a permanent poison for catalytic converters, which are by far the mosteffective means of reducing emissions of CO, hydrocarbons, and NO,. As long asgasoline is leaded, there is no way of taking advantage of this exhaust control technology,which is now widely used in a large number of countries.

1.36 Experience elsewhere has demonstrated that gasoline lead eliminationshould be carried out within the broader context of an integrated approach to air pollutionmanagement. This is because gasoline components that are added to compensate for theoctane shortfall after lead removal can have harmful effects of their own. Concernsinclude increased emissions of carcinogens such as benzene (from higher-severityreformer operation).

1.37 Sulfur in gasoline acts as a (temporary) poison for catalytic converters.Vehicle manufacturers recommend that the level of sulfur in gasoline be kept below 500parts per million by weight (wt ppm), and preferably below 100 wt ppm. The impact ofreducing sulfur on the performance of catalytic converters is non-linear, with emissionsdecreasing more rapidly below 100-150 wt ppm.

1.38 Benzene is emitted from gasoline as a result of evaporation8 and asunconverted benzene from the exhaust pipe. Alkyl-aromatics (all aromatics other thanbenzene) also dealkylate during combustion and a fraction is emitted as benzene. Benzenein gasoline contributes much more to the overall benzene emissions than non-benzenearomatics: it takes roughly an order of magnitude more alkyl aromatics than benzeneitself in gasoline to result in the same amount of benzene emissions from the tailpipe, andonly benzene itself can contribute to evaporative emissions.

7 Total aromatics refers to all aromatics, as opposed to specific aromnatic compounds such as benzene orxylenes.

s There are three sources of evaporation: during refaeling, as the engine cools after being shut off, and inresponse to the rising temperature during the day.

18 Pakistan Clean Fuels

1.39 Aromatics with two or more alkyl groups are photochemically reactive andcontribute to ozone formation. Therefore, the photochemical reactivity of aromatics andtheir decomposition to benzene are the two primary environmental concems leading tolimits on the amount of aromatics in gasoline. Ozone does not appear to be a problem incities in Pakistan. In the United States, for vehicles equipped with catalytic converters,the U.S. Auto/Oil Air Quality Improvement Research Program (AQIRP) found thatdecreasing total aromatics from 45 percent to 20 percent had no significant impact onozone formation (Auto/Oil AQIRP 1997). For vehicles not equipped with catalyticconverters, increasing aromatics in gasoline increases NO, emissions-which, asdescribed earlier, are a precursor for both ozone and secondary fine particulate formation.Another component of gasoline with a related concern is olefins. Olefins arephotochemically reactive and are ozone precursors. In addition, at elevated levels olefinsincrease the emissions of NO,.

1.40 Oxygenates such as ethers and alcohols have high blending octanenumbers and facilitate combustion in vehicles not equipped with oxygen sensors. Theyalso dilute gasoline, thereby decreasing the amount of undesirable gasoline componentssuch as benzene and total aromatics. Oxygenates are more miscible with water thangasoline, however, and contamination with ground and drinking water with methyltertiary butyl ether (MTBE), the most extensively used oxygenate, is a growing concem inthe United States.

1.41 Sulfur in diesel was reduced to 500 wt ppm in 1993 in the United Statesand 1996 in the European Union (EU) to control particulate emissions. This limit wasmandated only after significant progress was made in vehicle technology to reducecarbonaceous contributions to exhaust particulate emissions, so that the sulfatecomponent of particulate emissions became important. This is illustrated in Figure 1.1. Ifthe sulfate contribution to total particulate emissions is small, reducing sulfur in dieselsignificantly would not be effective in lowering overall particulate emissions.

Figure 1.1: Evolution of U.S. Diesel Particulate Emissions

o 0.6

4! 0.5 _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _

30.4 I carbon soot &oL organics* 0.3-

IN sulfateo 0.2 -0.1 _ - _ __

1988- 1991- 1994- 1994-E 0.25% 0.25% 0.25% 0.05%o) sulfur sulfur sulfur sulfur

1.42 The European auto/oil program (the European Programme on Emissions,Fuels and Engine Technologies, or EPEFE) examined the impact of varying polycyclic

Background 19

aromatics on vehicular emissions and found that decreasing polycylic aromatics from 8percent to 1 percent decreased both particulate and NO, emissions from light-duty andheavy-duty diesel vehicles. The impact of reducing aromatics on vehicular emissions isless clear. A cooperative program between Esso and Statoil found, for example, thatreducing total aromatics from 32 percent to 10 percent had no marked effect onparticulate emissions (Betts and others 1992).