Embed Size (px)

Citation preview

II

•

..

Document of , "

The World Bank

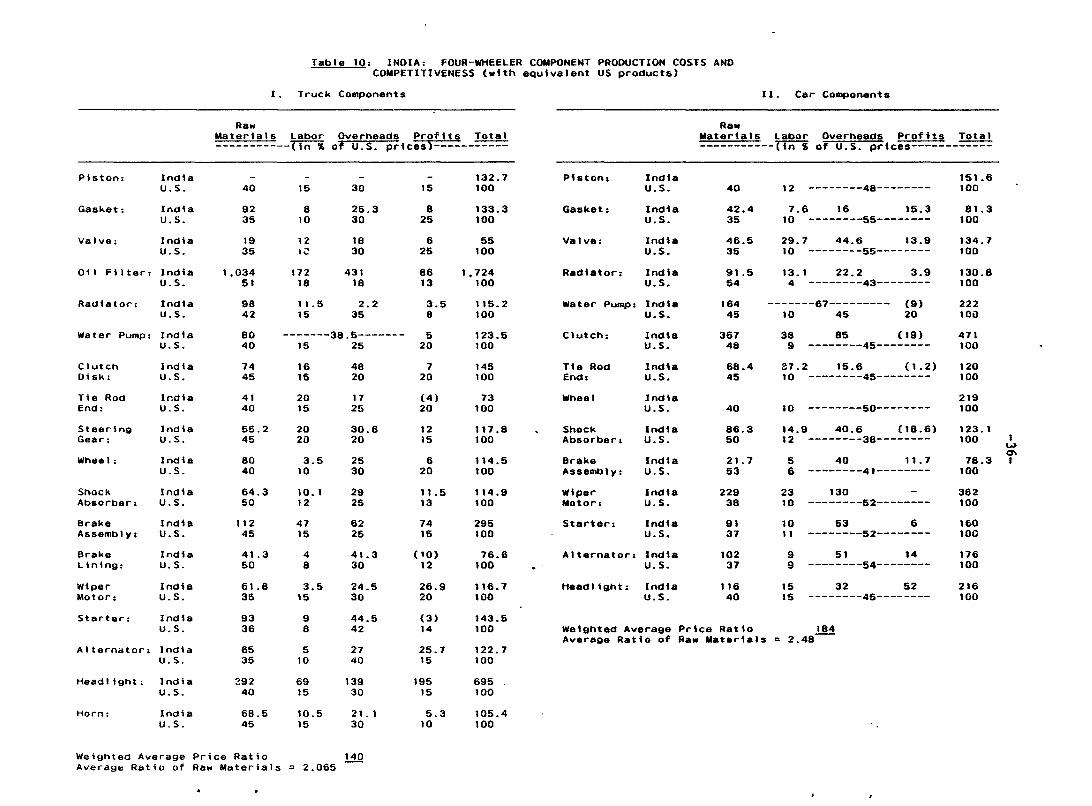

FOR OFFICIAL USE ONLY

INDIA

REVIEW OF THE

AUTOMOTIVE PRODUCTS INDUSTRY

March 9, 1987

Industrial Development and Finance Division South Asia Projects Department

CONFIDENTIAL

Report No. 6667-IN

This document has a restricted distribution and may be used by recipients only in tbe performance c,{ their offic:ial duties. Its ('ontents may not otberwise be disclosed witbout World Bank autborization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

FOR OFFICIAL USE ONLY

ACHA I:

AI AM I:

AIEl = ARAI = Ashok. Leyland = Bajaj , = cc: = CKD = CV = DGTD = CM I:

CW = HM = lSI I:

Kinetic = LCV = HI CO = Maruti = MES = M/HCV = OCL = PMPs = Premier = RD = SSIs . ::

Telco =

CONFIDENTIAL

LIST OF ABBREVIATIONS

Automobile Components Manufacturers Association' Association of Indian Automobile Manufacturers Associatiou of Indian Enginedring Industry Automotive Research Association of India Ashok. Leyland Limited Bajaj Auto Limited Cubic Centimeters Completely Knocked, Down Commercial Vehicle Directorate Ceneral of Technical Development Ceneral Motot's Cross Vehicle Weight Hindustan Motors Limited Indian Standards Institute Kinetic Engineering Limited Light Commercial Vehicles Motor Industries Company Limited Maruti Udyog Limited Minimum Economic Scale Medium and Heavy Commercial Vehicle Open.Ceneral License Phased Manufacturing Programs Premier Automobiles Limited

Research and' Development Small Scale Industries ' Tata Engineering and Locomotive Company Limited

LIST OF CURRENCY CONVERSION RATES (Source: IMF)

1971/72 : 1972/73: 1973/74: 1974/75: 1975/76: 1976/77 : 1977/78: 1978179: 1979/80: 1980/81: 1981/82: 1982/83: 1983/84: 1984/85:

7.444 7.706 7.791 7.976 8.653 8.939 8.563 8.206 8.076 7~893 8.929 9.628

10.312 11.887

This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be dis(;iosed withou! World Bank authorization.

INDIA

AUTOMOTIVE PRODUCTS INDUSTRY

Table of Contents

• Page No.

Text. FOREWORD

EXECUTIVE SUMMARY

I. OVERVIEW OF THE AUTOMOTIVE PRODUCTS SUBSECTOR AND STRUCTURAL CHARACTERISTICS OF THE VEHICLE INDUSTRY

A. B. C. D. E. F.

G.

Automotive Products Overview • •••••••••••••••••••••••••••••• Motor Vehicle InJustry Profile •••••••••••••••••••••••••••••• Scales by Major Vehicle Segments •••••••••••••••••••••••••••• Vehicle Prices ••••••••••••••••••••••••••••••••••••••••••••• Technology •••••••••••••••••••••••••••••••••••••••••••••••••• Plan Projections and Strategy for Growth in the

Vehicle Industry •••••••••••••••••••••••••••••••••• -: ••••• The Automotive Components Industry: A Priority

for Development Now •••••• 0 ••••••••••••••••••••••••••••••••

II • THE AUTOMOTIVE COMPONENTS INDUSTRY

i

1

2 8

10 16 23

25

29

31

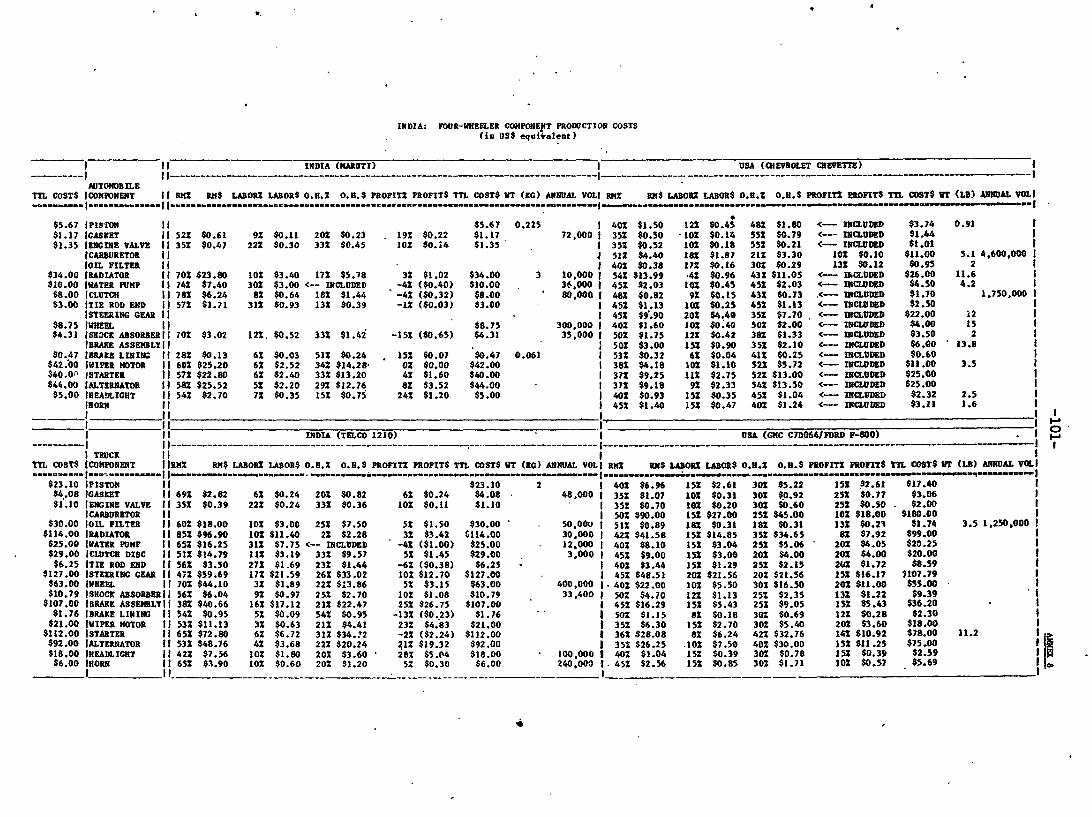

A. Industry Profile •••••••••••••••••••••••••••••••••••••••••••• 31 B. Production Cost Performance ••••••••••••••••••••••••••••••••• 35 C. Manufacturing Efficiency and Technical Shortfalls ••••••••••• 42 D. Modernization Investm~nt Needs •••••••••••••••••••••••••••••• 46 E. Labor, Infrastructural and Fiscal Constraints ••••••••••••••• 47 F. Potential for Cost Reductions in the Component Industry..... 51

III. PROSPECTS AND RECOMMENDED STRATEGIES FOR THE AUTOMOTIVE INDUSTRY 53

A. Strategies by Segment ••••••••••••••••••••••••••••••••••••••• 53 B. Indicative Guidelines for Project Design •••••••••••••••••••• 63 C. Strategy and Policy Paper ••••••••••••••••••••••••••••••••••• 64

IV. POLICY FRAME~ORK AND ISSUES 66

A. Introduction •••••••••••••••••••••••••••••••••••••••••• ~..... 66 B. Policy Instruments ••••••••••••• oo.w......................... 67 C. Strategy for Policy Reform •••••••••••••••••••••••••••••••••• 74

The report findings are based on the work of a te~~ led by Ms. Danielle Berthelot (Project Officer), and comprising Mr. Harry Mathews (specialist of the automotive industry from Arthur D. Little), Mr. Donald Keesing (Senior Economist) and Ms. Michele de Nevers (Economist). Mr. Francois Ettori (Senior Industrial ficonomist) contributed to the final analysis and report preparation.

V. POSSIBLE BANK ASSISTANCE IN THE DEVELOPMENT OF THE INDIAN AUTOMOTIVE INDUSTRY

A. Project Objectives and Description •••••••••••••••••••••••••• B. Issues ••••••••••••• 0 •••••••••••••••••••••••••••••••• ••••• •••

c. Benefits •••••••••••••••••••••••••••••••••••••••••••••••••••• D. Risks •••••••••••••••••••••••••••••••••••••••••••••••••••••••

ANNEXES

1. 02. 3.

4.

5., 6. 7.

8. 9.

10.

11. 12. 13. 14.

~5. 16. 17.

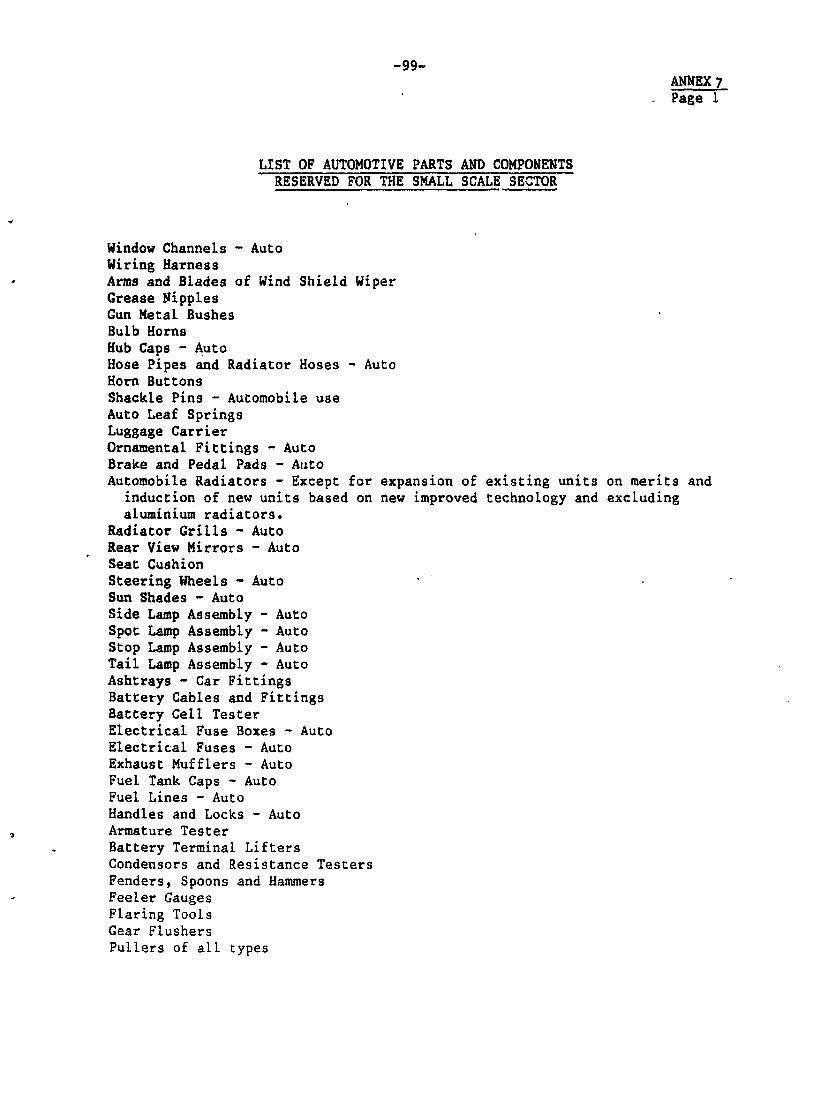

World Motor Vehicle Production/Assembly, 1984 ••••••••••••••••••• Customs Tariffs on Automotive Products •••••••••••••••••••••••••• 1985 Vehicle Prices and Unit Sales of India's Main Motor Vehicle Models •••••••••••••••••••••••••••••••••••••••••••• Four-Wheeler Ex-factory Price Indices and Comparison with Selected Price Indices (1970-1985) ••••••••••••••••••••••••• Production Cost Structure of Telco Truck •••••••••••••••••••••••• Demand Models for Two-Wheelers and Policy Implications •••••••••• List of Automotive Parts and Components Reserved for tae Small Scale Sector ••• e .••••••••••••••••••••••••••••••••••••••••••

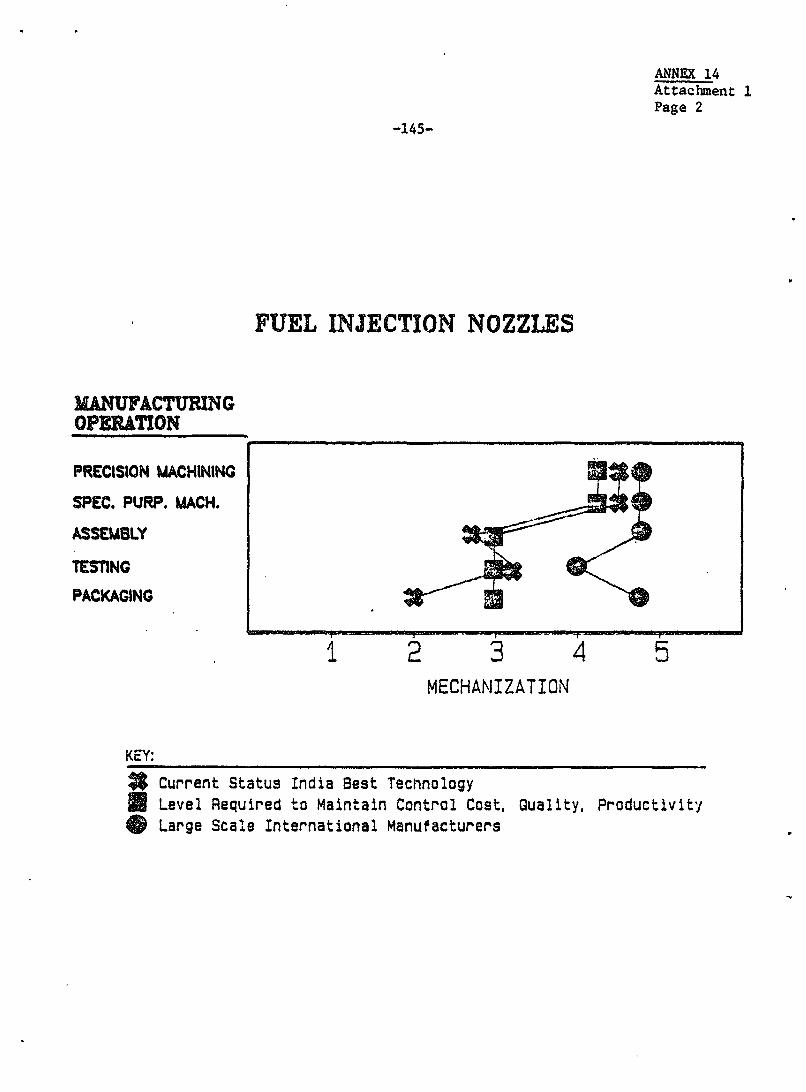

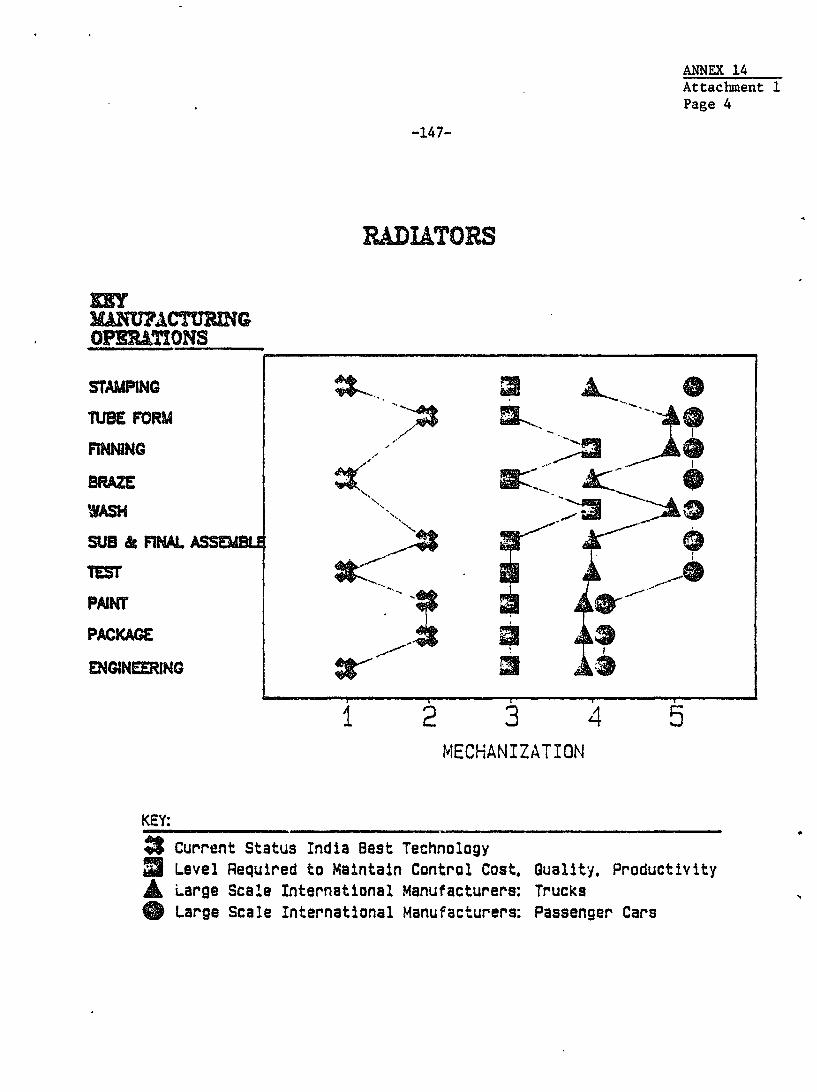

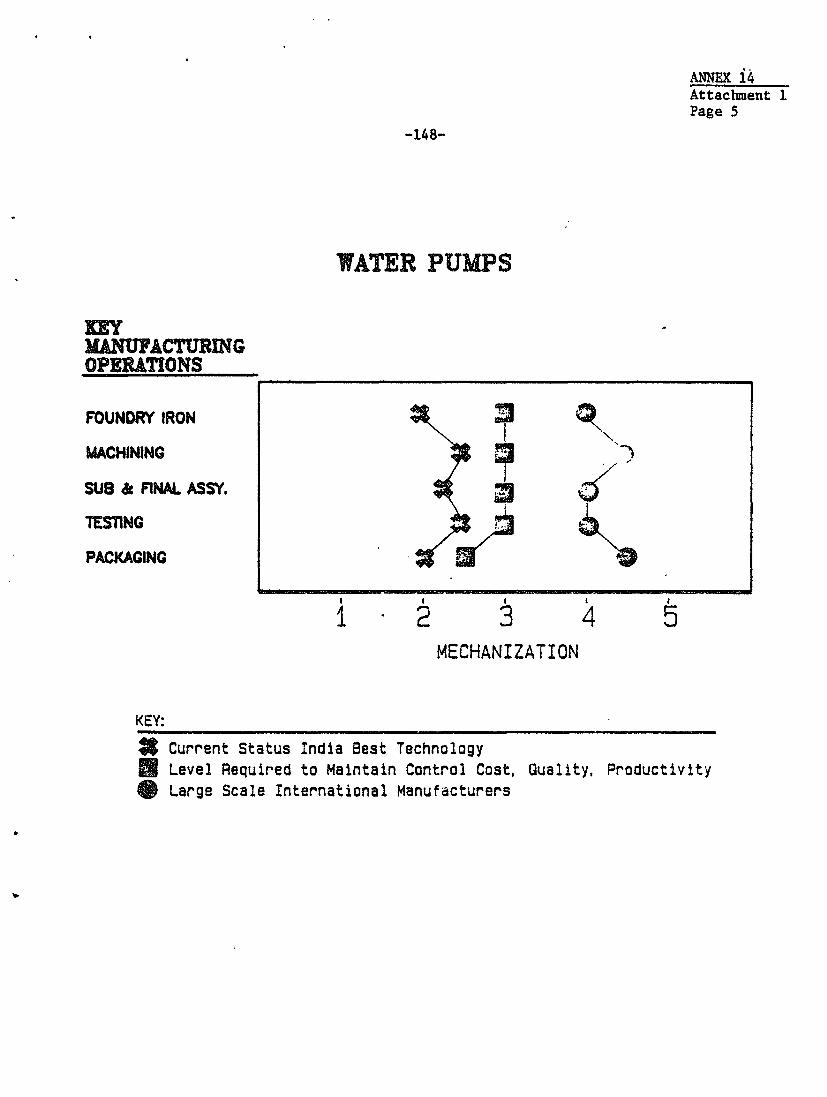

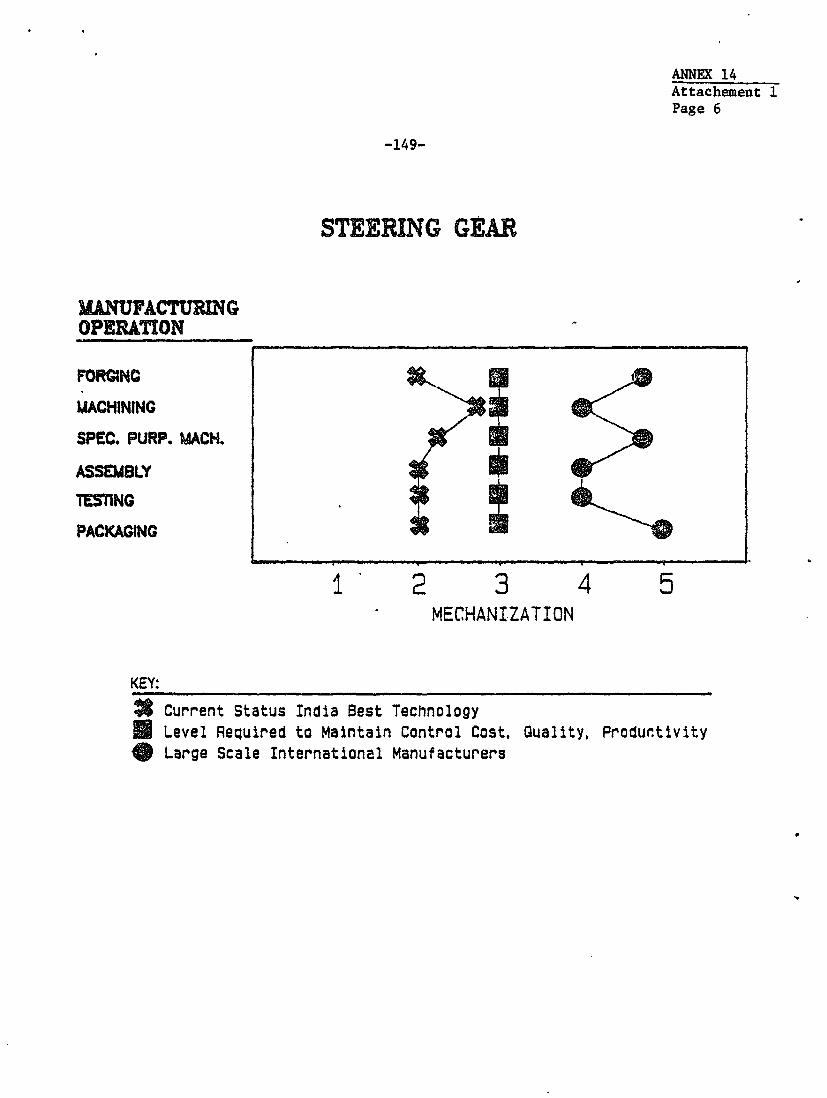

Four-Wheeler Component Production Costs ••••••••••••••••••••••••• EPRs and DRCs for Four-Wheeler Components ••••••••••••••••••••••• Rates of Import Duties on Raw Materials Used in Auto Components Industry •••••••••••••••••••••••••••••••••••••••• Comparative Capabilities (India-World) per Automotive Component •• ' Korea's Strategy in Developing its Automotive Component Industry. Automotive Components Field Study ••••••••••••••••••••••••••••••• Four-Wheeler Component Production: Major Process Steps va. Level of Mechanization •••••••••••••••••••••••••••••••••••••••••• Details of Tax on Bought-out Items (Telco 1210 Truck) ••••••••.••• India-Japan Collaboration in Auto-Ancillary Industry •••••••••••• Experiences of Developing Countries in A~tomotive Industries ••••

85 89 90 90

91 92

93

94 95 96

99 101 102

103 104 108 110

142 160 161 163

•

FOREWORD

The automotive products subsector in India has been targeted by the 1985-1989 Plan to grow more rapidly than the overall industrial sector, and the Covernment of India expects the subsector to constitute a spearhead for technological renovation and modernization in the engineering industries and accelerate the growth of industrial output, employment and exports. Moreover, the Government of India has expressed its interest in a possible support of the World Bank to the development of the automotive subsector in the coming years. For these reasons, the World Bank has undertaken, with the concurrence and support of the Indian Government, a review of the situation~ performance, potential and prospects of the automotive subsector. The follo~ing report presents ~ the major findings and conclusions of this review.

The review is based on the factory visits and interviews of about 10 vehicle manufacturers, 35 automotive component suppliers and 5 machine-tool producers undertaken during three missions between June 1985 and March 1936. In-field work was actively supported by the Association of Indian Automobile Manufacturers (AIAM) and the Automotive Component Manufacturers Association of India (ACHA). Highly valuable discussions were held in the Covernment with the Joint Secretary in charge of the' automotive industry and the Additional Secretary in the Ministry of Industry, the Secretary of the Directorate General of Technical Development (DGTD), and the Sec~etary and Joint Secretary of the Department of Economic Affairs of the Ministry of Finance. The World Bank team also consulted with a former executive of Tata Engineering and Locomotive Company (TELCO) and a former Director of FIAT-IVECO. Finally, the review's findings were discussed with the International Finance Corporation (IFC), and particularly its Engineering Department. This report may not fully reflect changes in Government policies for the automotive industry that have occurred since the last field mission in March 1986.

INDIA: AUTOMOTIVE PRODUCTS INDUSTRY •

EXECUTIVE SUMMARY

Role, Structure and Performance

1. India's automotive products industry has been targeted by the 7th Plan (1985-1989) to be a leading sector in the growth of the industrial sector and to constitute a spearhead for technological re.novation and modernization in the engineering industries. Within the industry, the critical subsector, that producing automotive components, which det~rmines the cost, quality and technological parameters of the finished vehicles, has remained relatively underdeveloped in terms of output and technology, and is challenged to meet the needs of a rapidly renovating and growing vehicle sector. Despite its relatively small size, the automotive products industry was assigned high priority in the 7th Plan, and significant policy measures introduced in recent years confirm the Government's intention to re-establish the industry's competitiveness and to foster its quantitative and qualitative development. For these reasons, a specific review of the potential and prospects of the automotive industry has been undertaken, with the focus on the component sector.

2. The automotive industry consists of producers of medium/heavy and light commercial vehicles, passenger cars, two and three wheeled vehicles and components. With an output from registered firms of is 27.3 billio~£ (US$3 billion) in 1981/82, it.represents a small fraction of the industrial sector and the economy. Its share in total manufacturing output, value-added., employment and investment has ranged between 2% and 4%. Nevertheless, it has been growing faster than the industrial sector (8% p.a. versus 4.5% p.a.) in recent years (1980-85). Its value-added per worker, despite a relatively l~w level by international standards, has been almost twice the Indian manufacturing average, with a capital-labor ratio higher by 30% only. Automotive exports had been growing quickly compared to other Indian manufactured exports until the early 1980s, but ~xport performance of the industry has deteriorated in the last five years. Total automotive exports peaked at US$153 million in 1981/82, but declined to US$87 million and US$98 million in 1983/84 and 1984/85 respectively. This decline is due to the contraction of India's traditional markets in Africa and Middle East and the partial loss of its competitiveness, mostly with respect to product quality.

3. India's automotive industry tradition~lly has been highly indigenized. Its domestic content averaged about 95% until 1983, but has declined marginally since with the recent emergence of modern vehicles based largely o~ imported components. The industry is essentially inward-oriented. Automotive exports (almost equally shared between commercial vehicles and parts ~r components) have represented only some 5% of the industry's output. However, the share of component output exported has been consistently higher than that of the industry as a whole (14% Ln 1979/80 and 7% in 1984/85).

-ii-

4. The industry comprises about 1,900 registered enterprises, of which about 25 vehicle manufacturers and 185 component producers are of significant size. In addition, a few thousand small-scale firms produce parts and components. The industry is essentially privately owned; two govern~ntowned firms (one producing cars, and the other one scooters) contribute only about 1% of the industry's output value. In terms of value of output, commercial vehicles dominate, accounting for 60% of the value of vehicle output, while cars/jeeps and two/four wheelers account for about 20% each. The total value of vehicle output in 1984 was about Rs 18.9 bill:.on (US$2.3 billion). In t~rms of units, the 14 firms licensed to produce four wheel vehicles turned out 62,000 medium/heavy commercial vehicles (MaeVs), 33,000 light commercial vehicles (LCVs) and 86,000 cars and jeeps in 1984. The 27 licensed producers of two-three wheelers produced 850,000 units in 1984 (and 1,100,000 in 1985). About 80% of two-three wheelers were scooters or mopeds, the remainder were motorcycles. Passenger cars have thus rep~esented a small share of the vehicle sector both in volume and value, and the subsector's output has been dominated by MaCVs in value terms and by two-wheelers in number of vehicles.

5. The automotive component sector, which comprises about 300 licensed firms (of which about 90 involve foreign collaboration), had an output of Rs 8.4 billion) (US$700 million) in 1984. Firms ~arely specialize and parts and components for four- and two-wheelers are generally produced in common facilities. The sector's output value is distributed over five main product groups: 37%, . engine parts; 25%, transmission and steering; 18%, suspension and brakes; 1!%, electrical components; and 9%, for other parts. Each product group generally comprises six to eight licensed firms, of which two or three supply most of the bought-out needs of vehicle producers. Small firms producing components generally serve th~ after-sale and replacement needs of the vehicle fleet (1.2 million cars, 0.8 million CVs, and 3.2 millivn two-wheelers in 1984). The component sector is underdeveloped relative to the vehicle sector, ~epresenting only one-third of the vehicle output value, compared to about two-thirds in well-structured and balanced automotive industries world-wide (e.g., Japan, Europe). This indicates excessive vertical integration of vehicle manufacturers (which produce in-house an overly large share of their parts), due to the absence of institutional and operational linkages between vehicle and component producers, and the technological backwardness of the component sector. In a survey conducted for this report, vehicle manufacturers identified about 52 groups of domestic components that could not meet their needs in term of quality, design or performance, particularly for braking, suspension, fuel-efficient engines, front-wheel drive systems and electrical/electronic components.

Assessment of Competitiveness and Potential

6. Production of automobiles developed in a protected environment largely without domestic and international competition. As a result, they are uncompetitive when compared with vehicles produced in the rest of the world in terms of design and quality. Two sturdy but expensive, fuel-inefficient and technically outmoded models of the 19505 have dominated the market for 30

-iii-

years, discouraging potential customers to buy or car 'owners to replace them. However, in 1984 a small, fuel-efficient car was introduced by Maruti. This vehicle, which is suitable for urban conditions, is assembled from largely imported components. It is much closer to international standardd of price/quality than the traditional vehicles. Moreover, five two-wheeler producers and two MaCVs manufacturers are now producing at levels of output that enable them to take advantage of economies of scale consistent with international practice (e.g., between 5,000 and 15,000 units p.a. per model of truck) and are producing at competitive prices. Production cost and sales price datA indicate that production of medium and heavy cummercial vehicles and two wheelers may be approaching levels of international competitiveness. Prices and costs are uniformly aelow those in developed country markets (at the present exchange rate, which is, because of heavy protection, overvalued). Available data suggest tna't Domestic Resource Costs (ORCs) are below 1 for MaCVs (about 0.9) and two-wheelers (about 0.6). However, a substantial part, if not most, of the apparen~ price/cost advantage of Indian producers is attributable to differences in engine specifications and vehicle designs and to inferior "fit and finish" and safety. Such quality differences have had a substantial effect on India's vehicle exportd which, despite their lower prices, have steadily declined since 1982.

7. Component producers also developed in a protected environment, insu-lated from technical progress abro~d and operating in a high-cost environment. A survey undertaken for this study indicates that ex-factory p~ices of modern car components average about l8~% of international prices (range 80-220%) whi1~ truck components, which generally have lower minimum economic scales, average 140% (55%-300% range). The limited available data, on two-wheeler components suggest that price comparisons are more favorable, due to their lower complexity in terms of both the number and technology of parts. Ex-factory prices of 19 components of a modern Indian motorcjcle average 127% of international prices. However, there are a number of examples of success in achieving international standards of cost and quality (e.g., brake linings, shock absorbers, fuel pumps and injectors). These point to large potential for efficiency, competitiveness and exports in selected component groups.

8. Analysis of production cost stcuctures of 15 truck and car comronents indicates that production of truck components and selected car components could be internationally competitive if not handicapped by high cost of raw materials. However, the passenger car components subsector in general ha~ far to go.

(a) production volumes are generally adequate (by international standards) for truck components, but too low (by a factor of 5 to 10) for car components due to the number of car models with short prOduction runs and distinct part requirements;

-iv-

(b) India's labor costs often provide ~ clear comparative advantage, particularly for truck components and a selected range of car components, which could make Indian automotive components competitive if raw materials were available at world prices. DRCs for such components based on world prices for inputs are generally below 1, with an averag~ of about 0.7; and

(c) the share of materials in total costs is on average more than double their share in other countries, due to the lack of scale economies, the use of bulky or obsolete designs, and primarily the high domestic costs of raw materials leading in most cases to negative effective protection rates (-17% on average).

Development Constraints andOPolicy Issues

9. The industrial protection and transport policies followed by the Government favored the development of KRCVs and two-wheelers considered more adapted to India's markets and transport needs. Such preference permitted producers of MHevs and two-wheelers easier access to foreign technology and collabora,ion and led to comparatiNely better performance in these vehicle subsectors. Nevertheless the policy regime led to development of a highly fragmented industry structure:

(a) the industrial licensing system has severely constrained competition (entry, exit) and growth of the most efficient producers;

(b) the 'structure and level of protection have shielded the 40mestic vehicle industry from all import competition and discouraged technical modernization and updating and cost competitiveness; and

(c) the modalities of indirect taxation have inflated production costs, encouraged excessive vertical integration and hampered the growth of demand and production.

10. Industrial Licensing. Capacity licensing and the associated restrictions on imports of foreign technology and investment (e.g., FER! firms), and the tight constraints on the expansion of large enterprises (KaTP) have been a major influence on the structure of the automotive industry. In most subsectors, small inefficient firms with low capacity utilization, high cost and poor quality products have coexisted with large and relatively efficient firms. The latter enjoy large market shares and higher capacity utilization due to the better quality of their products and after-sale services, but have been restricted by regulations from meeting higher demand through capacity expansion or merging with similar firms. This has led to a large surplus of licensed capacity in some firms along with shortages of, and long waiting lists for, the quality products of other firms. Restrictions on entry and expansion have also made entry of credible competitors difficult or impossible. Moreover, regulations have hampered the establishment of close institutional and operational linkages (e.g. equity participations) between vehicle manufacturers (generally KaTP) and their component suppliers (frequently smaller firms or 881s), as traditionally practiced in well integrated automotive industries abroad.

-v-

11. In the component sector, a large number of product groure <currently 60) have been reserved for SSIs, including some functional parte (e.g. radiators, leaf spring's, oil filters) and other parts which in other countries are mass-produced by large firms and exported. In the "reserved" product groups, investments are often scaled down by firms to remain eligible for SSI-specific incentives and advantages and have thus been insufficient to bring about adequate modernization. This, combined with the lack of competition from large firms, has contributed to the technical stagnation and inadequate quality of the reserved products.

12. Protection. The vehicle sector has been protected by a nearly' total ban on the import of finished vehicles. While imports of modern components are allowed at relatively moaarate tariff rates, absolute protection is being introduced for the component sector through the "Phased Manufacturing Programs" (PMPs) which impose a 95% local content requirement on vehicle producers after the first 5 years of production. Import duties (which have been largely redundant in view of the quantitative restrictions on imports and the price competitiveness of many types of vehicles) are 150%-200% on cars and two-wheelers, 65%-110% on CVs, and 150% on parts and components. Moreover, import duties on the 45 raw materials and products most frequently used in component production range between 100% and 150%, and duties on 25 other frequently used products range between 150 and 300%. In contrast, the Government is allowing, on an exceptional basis, import of components for fuel efficient vehicles at a 50% tariff. This applies to pract,ically all modern and up-to-date components which require modern materials either not produced in India or not available in sufficient quantities or quality. The resulting negative effective protection on modern components constitutes an almost insurmountable disincentive to component manufacturers to undertake the substantial investments that would be necessary to modernize their products and processes. This places the objective of producing modern, fuel-efficient vehicles with substantial domestic content and with quality and price close to international standards in serious jeopardy.

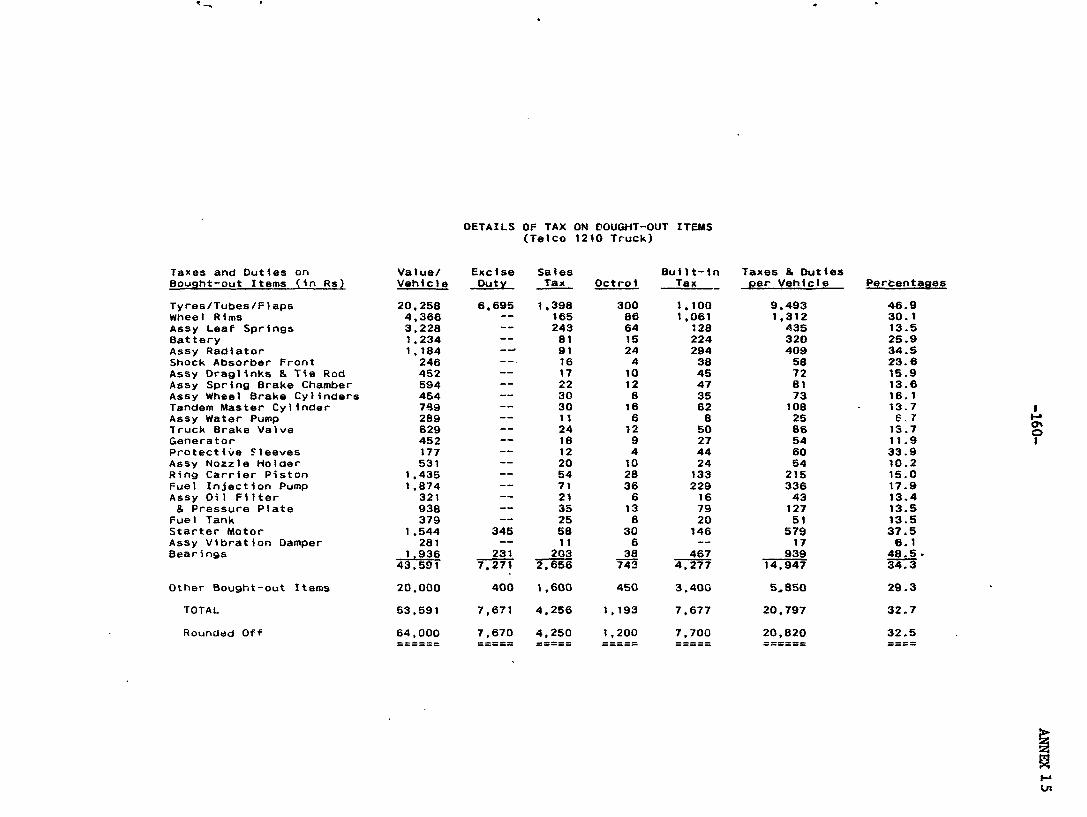

13.' Indirect Taxes. The impact of indirect taxation on the prices of vehicles has been high. The cumulative indirect taxes levied at the various stages of manufacture, together with post-manufacture tax~s such as excise duty and sales taxes and octroi, are estimated to add some 50% to the exfactory cost (net of such indirect ta~es) of cars and two-wheelers and about 60% to the ex-factory cost of CVs. About two-thirds of these taxes are post-manufacture taxes, levied on the sale of the finished vehicle to the customer; one-third constitutes the "tax in manufacture", comprising all indirect taxes from raw materials to final assembly. Moreover, as illustrated by the case of MHCVs, two-thirds of the "tax in manufacture" of finished vehicles are levied on bought-out components supplied by the component producers. In turn, these taxes account for the equivalent of 11% of the ex-factory prices of such comp0:1ents (Le., the "tax in manufacture" of the components themselves) and the equivalent of 18% of the ex-factory prices of components levied on their purchase by the vehicle assemblers. Indirect taxes paid on account of components have thus increased their cost to the final assemblers by about 30% and added 14% to the ex-factory price of the vehicles.

-vi-

14. The cumulative and cascading effects of indirect taxes have encouraged excessive vertical integration by the vehicle producers and component produce~s as well, and contributed to their insufficient specialization. As important, the burden of all indirect taxes on the customer prices of vehicles has probably reduced the sales of vehicles, in particular for two-wheelers the demand for which shows a relatively high price elasticity (about 1.6). This has made it more difficult for enterprises to reach economic scales of prOduction. Finally, the higher ex-factory prices resulting from taxation have reduced the price competitiveness of Indian automotive products on export markets, since the indirect tax element is often not fully offset by the rates of the Cash Compensatory Support (CCS) scheme for exports.

15. Recent Policy Reforms. The Government has taken major steps in recent years to develop the automotive industry. In view of the increasing ne~ds for fuel-efficient transport, the Government encouraged new entry and capacity and permitted collaboration with foreign investors. A public enterprise (Maruti Udyog Ltd.) was established with foreign collaboration with 3 licensed capacity of 100,000 units p.a. to revive the dormant car industry and produce fuel-efficient, low cost cars. Maruti was granted some important concessions and incentives, the most significant being the reduced 50% tariff duty on imports of components and CKDs for fuel-efficient vehicles. In 1982 the Government constituted a Subcommittee "to prepare a Perspective Plan for the growth of the Automobile In4ustry."

16. The Subcommittee report issued in mid-1984 recommended a new initia-tive to increase the subsector's efficiency and meet the pent-up demand for cheaper and more efficient vehicles. This included (a) upgrading products and process technologies with appropriate foreign collaboration; (b) licensing new production with minimum economic scales (MESs) and reducing constraints on growth and competition by "broad-banding" the product-mix·(e.g., allowing scooter assemblers to produce mopeds); (c) intrOducing uniform indirect taxes and deductibility of central taxes; (d) dereserving critical components from SSIs; and (e) extending lower import duties to all components and equipment for modern vehicles. Underlying these recommendations was the recognition by Government officials that maintaining control on the market (through licensing) and total protection of domestic producers would continue to prevent the most efficient producers from tapping the potential market and the advantage of low cost versatile labor.

17. Following the Subcommitteets recommendations and in support of the 1985-1989 Plan's objectives, measures were taken by the Government in late 1985-early 1986 to foster efficier.~y in the subsector. The most significant measures have been the delicensing of the component sector (except for MRTP and FERA firms) and partial delicensing of HRTP and FERA two-wheeler producers, broad-banding all vehicle manufacturers, and easing of import and technology licensing procedures for joint ventures, in particular in twowheelers. These measures should provide the component and two-wheeler producers with much more freedom and flexibility for growth, higher capacity

•

..

-vii-

utilization and foreign support. Moreover, new legislation (enacted in December 19&5) for "sick" industrial companies has brought about some progress toward the exit of inefficient firms and the necessary rationalization of the automotive industry. A new indirect tax system of the Value-Added type (MODVAT), designed to permit the deductibility of taxes in manufacture up to the purchase of the final good, was introduced in 1986 in a number of industries, including the automotive industry. Since 1983, a large number of forei~n collaboration agreements for manufacture of vehicles and components have been approved, supporting the process of renovation and modernization of the industry. Licenses for a do~en join~ ventures aimed at producing cars and LCVs were requested in 1986.

18. Remaining Issues. Despite substantial progress that has been made in recent years in establishing a policy framework conducive to the efficient growth and mOdernization of the automotive industry, there remain significant constraints on the development of a modern, competitive automotive industry. Further progress toward rationalization of the automotive industry and adjustment of import protection and indirect taxation is most important. The most immediate need is to eliminate the negative effective protection on production of modern components; tariffs paid by component suppliers on imported inputs should be harmonized with the tariff duty levieu on components imported by the manufacturers of fuel-efficient vehicles. Otherwise, component producers will, for the most part, be unable to substitute effi- . ciently for imports of modern components, because they will not have sufficient incentives to undertake the sizeable incremental investments required to achieve quantum jumps in productiop volumes, quality ~nd reliability needed. . .

19. The phased manufacturing program, which requires progressive increases in domestic content, up to 95% in five years, also creates a problem. The effective protection of the vehicle components indus'try, which is now negative, will gradually become virtually absolute as domestic content requirements bite. This could lead to rapid escalation in the cost of both components and vehicles. Moreover, the Government has created considerable uncertainty by frequently not enforcing domestic content requirements. This creates the worst of all possible worlds; by making producers unsure of the rules of the game, it discourages forward planning and investment.

20. The high p~otection on finished vehicles continues to be a problem. It has resulted in some joint ventures, particularly in LCV manufacture, with project design at low, uneconomic scale.

21. With respect to indirect taxation, the MODVAT scheme is not yet fully effective, due to its partial coverage of products (only 37 product chapters, ex~tuding in particular machinery and energy), taxes (it covers only central excise taxes) and entities (traders, wholesalers and input dealers, as well as SSIs which choose so, are not subject to it). While the introduction of the MODVAT system was intended to be gradual, it would be urgent to expand the scope of its application. A comprehensive application of MODVAT, n·_·twithstanding its practical difficulties, would resolve the indirect taxation

-viii-

issue in a multi-stage industry such as automotives, which relies on a large number of suppli~rs for its components. Finally, furth~r reforms in delicensing fully the automotive industry, particularly dereserving critica~ and scale-sensitive components from SSIs which often cannot produce them efficiently, and eliminating most remaining coftstraints on expansion of HaTP or FERA enterprises, would be desirable.

Potential and Prospects for Development

22. Motor Vehicles. Notwithstanding the rapid increase in passenger vehicle sales with the start up of Maruti's production (sales jump~d from 64,000 in 1984 to 103,000 in 1985), the cutting edge of development of the motor vehicle sector is likely to be heavy commercial vehicles and two and three wheelers. Moreover, passenger cars, which are largely for private transport of high income consumers, are not fuel efficient relative to two wheelers and mass transit and place a heavy burden on already clogged urban roads. The domestic market for cars is not expected to exceed the total licensed capacity of 185,000 units nor to reach the MES for a car plant. (about 250,000 units per model with flexible engineering) in the medium-term. The small scale of Indian production and the rapidly evolving international markets preclude export of passenger cars from India. Similar conclusions apply to LeVs, where MESs are similar to those for cars, and which have had a small stagnant market (about 30,000 units p.a.). In this context, major additional investments in the subsector of cars and LeVs deserve a lower. priority than MHCVs and two-wheelers at this time. The Government's recent refusal to grant licenses for all the uneconomically scaled joint yent.~res will help avoid furt~er ca~acity splintering ind high cost production in the highly protected and regulated Indian market.

23. This does not necessarily mean that a mass market approach for cars and LCVs is inconceivable for India, but new approache~ would have to be considered. On one hand, a replication or large expansion of Maruti would entail substantial foreign exchange costs for comparatively small benefits in value-added and employment creation, and could be rapidly constrained by the demand from urban areas. On the other hand, there may exist a large pent-up demand from the higher income subsectors of rural areas for a small, sturdy and rustic multi-purpose light vehicle (car and/or pick-up) as developed in Europe. The market for such a vehicle should be further inv£stigated and, if found to be sufficiently large for MES production, might be licensed to a credible applicant.

24. MHeVs and two-wheelers offer at pr~sent the most promising prospects for vehicle production. In these two areas, leading firms (two in MHeVs, five in two-wheelers) have emerged with economic scales of international magnitude and have produced at competitive costs. In the two-wheeler subsector, domestic competition, combined with the strength of firm leaders, has led to limited but continuous technology upgrading through foreign collaborations and technology imports and to maintaining emphasis on quality control and product adaptation. This, along with the market entry of joint ventures in two-wheelers and the 1985 measures, should continue to stimulate

-ix-

competition, efficiency, technical upgrading and updating, and growth. Prospects for export of two wheelers are favorable provided that there are adequate incentives to stimulate furth~r quality improvements and marketing efforts.

25. There are still substantial needs for technical updating and quality improvement in MHCVs, as evidenced by their declining exports due in large part to product obsolescence. For example, a modern fuel-efficient diesel engine for trucks still needs to be introduced and produced in India. Technical progress could be accelerated by encouraging one of the present heavy vehicle manufactur~rs to enter into technical collaboration with a foreign producer or by allowing entry of a new strong competitor into the truck market. It would also be stimulated by reducing protection of the heavy vehicles market and allowing foreign firms to challenge for market shares.

26. The apparent price advantage India presently enjoys in most vehicle subsectors could be eroded by the additional costs to be incurred by technical updating of prOducts and processes, as suggested by the preliminary experience of two-wheeler plant modernizations recently undertaken with foreign collaboration. Nevertheless, such technical updating and modernization should increase the exportability of MHCVs and two-wheelers, provided that modern components can be supplied at competitive cost and quality levels. Exportability would be further enhanced by ex-factory price reductions through an improved system of indirect taxation. A comprehensive application of MODVAT to the automotive industry with the standard exemption on exports would enhance the price advantage of Indian products in these vehicle subsectors and thus promote their exports. The current CCS scheme is a second best solution because of administrative problems and because its benefits are not strictly linked to indirect taxation.

27. Automotive Components. So far, the new production of modern fuel-efficient vehicles has had only a limited impact on the component sector. ~e modern vehicles being introduced in India rely largely on imported CKDs, as opposed to the older generation of vehicles which have virtually 100% domestic content. Given the pressure on India's balance of payments, the modernization and expansion of the vehicle sector may not be sustainable without a quantum jump in the capability of the component sector to substitute efficiently for a major portion of imported CKDs and to support exports. The success of the development of India's automotive industry will thus be determined to a substantial extent by the structural changes in the production of components.

28. Many components are or could be produced efficiently in India. The comparative analysis of prices (corrected for differences in unit costs of raw materials between India and abroad) and of labor cost shares in total production costs indicates that components requiring large amounts of labor for sub- and final assembly have the greatest comparative advantage in India. Components for the four wheeled vehicles can be classified as those:

-x-

(a) requlrlng much sub- and final assembly work, including shock absorbers and brake assemblies for all four-wheelers, and radiators, starters, alternators and wiper motors for MHCVs. These components reap most of India's labor cost advantage, and would be highly competitive with adequate costs for raw materials. Brake assemblies and steering gears, which usually fall in the c~Legory, appear to be inefficiently produced in India.

(b) requiring more machining and less assembly operations could still be competitive if machinery and labor are combined effectively (semiautomated processes and machine-pace work) and material prices are adequate. These include brake lining and gaskets for all fourwheelers; and wheels, valves and pistons for MHCVs; and

(c) requiring a moderate amount of assembly and manufacture on large scale to cut machining costs are unlikely to be competitive in the near term. These include head lights, and oil filters for all fourwheelers. However, water pumps and tie-rod ends, which usually fall in this category, appear to be efficiently produced in India.

29. As far as four wheel vehicles are concerned, products in categories (a) and (b) above appear to have the best potential as components. However, the component sector is already in a position to produce most of the domestic needs for two-wheeler components efficiently, as they are technically simpler and the market is already large enough to permit production of these components at MES levels. Those components assessed to have the best potential include: carburetors, fuel pumps, fly-wheel magnetos, brakes, clutch assemblies, wheels, shock absorbers, lighting equipment and pistons and parts.

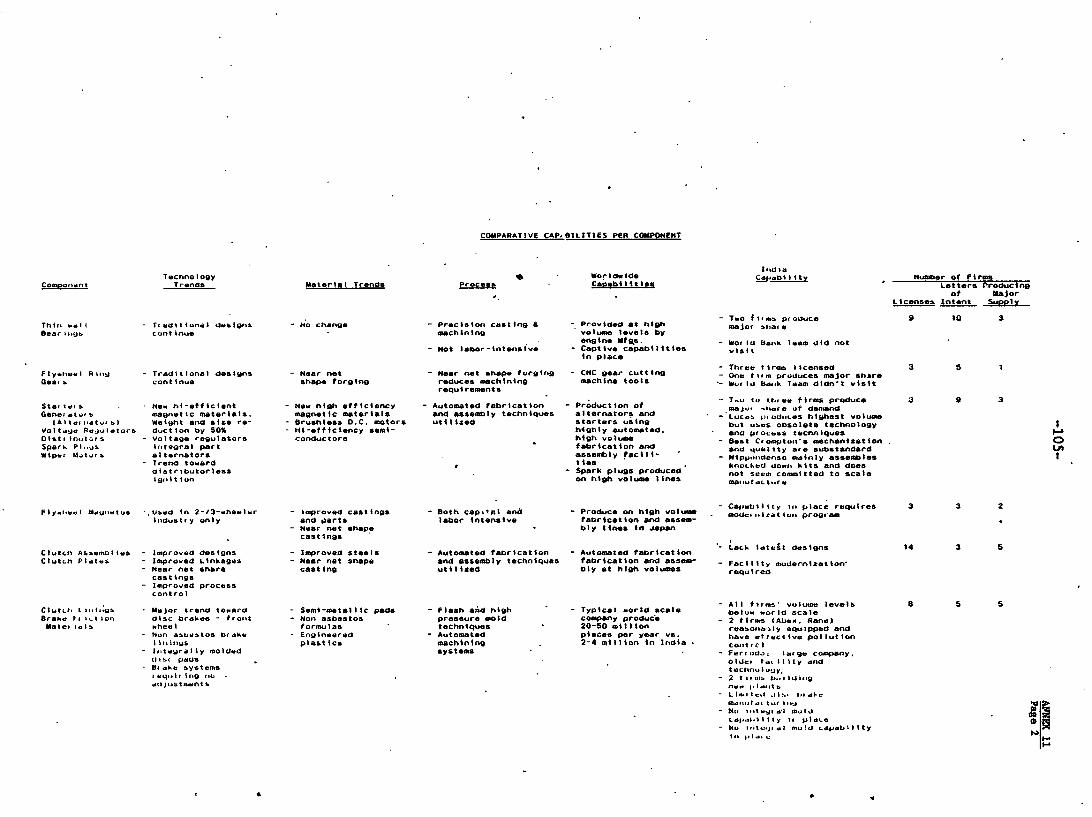

30. Reviews of manufacturing capabilities in the major components groups, comparing India's position with prevailing or shortly £xpected international technologies and practices, indicate that despite the basic advantages outlined above, the industry suffers from some crucial deficiencies:

(a) current levels of mechanization are insufficient to achieve international standards of quality and reliability;

(b) there are process deficiencies in the areas of tooling, stamping, metal treatment, sub- and final assembly, painting, testing, quality control and packaging of finished products; and

(c) master planning and lay-out of plants, including recent ones, has been generally inadequate in terms of process efficiency.

31. These reviews also indicated the investment mix the Government should encourage, through an improved policy framework, the private sector to undertake. The marginal, low-risk investments and solutions presently being considered or planned in the component sector will not achieve the required quantum improvements in efficiency and quality. Instead, achieving the

-xi-

required improvementg will necessitate the establishment of a new generation of highly productive facilities with adequate MESs. The reviews, combined with estimates of the demand prospects for each component indicate, in broad terms, that two new or updated plants of MES with at least semi-automated levels of mechanization would be required in each product group. These plants would be able to supply the domestic needs for modern components at competitive cost and quality, and some to export substantial volumes of some of these products. In addition, the next two best existing plants in each product group should be significantly modernized to supply the country's needs for after-market and service parts. This would require total involvement of US$250-300 million between now and 1990. Major investment would be required for production of pistons and parts, shock absorbers, and electrical components (starters, alternators, regulators, ignition coils). Their investment would permit expansion of exports in nine product groups (pistons and parts, fuel pumps and carburetors, fuel injection systems1 fly-wheel magnetos, clutch plates, clutch facings, shock absorbers, brake linings, brake assemblies); and provision of the domestic market with vehicles at lower prices and higher quality, through the supply of these components and six other products group (valves, spark plugs, tie-rod ends, steering gears, wheels, electrical components). In each case, the components with the best potential for efficient low cost production are generally those for MaCVs because of their lower MESs~ and those for two-wheelers because of lower technical requirements and prospects for higher production scales.

32. Improving the price and quality competitiveness of the components sector requires actions on three fronts; first encouraging investment in modern produc\ion facilities as outlined above; second reducing costs due to high priced domestic raw materials and cascading indirect taxes; and third, changing the trade regime and regulatory policy to provide a more competitive environment. The investment programs delineated above, if designed and implemented to adequately achieve product updating and manufacturing efficiency, could yield reductions in production costs and ex-factory prices of components by up to 15%. The share of material costs in total production costs could be reduced on average by half, essentially by aligning the domestic prices of materials to world levels, thus reducing ex-factory prices by up to 25% on average. The comprehensive application of MODVAT to the automotive industry would permit component producers and vehicle assemblers to reduce their ex-factory prices by about 10% and 20%, re3pectively. Combined actions and measures in these areas (investments, material prices, indirect taxation) could bring increased quality and reliability and reduce the exfactory prices of components by up to 50% of their present levels, thus making Indian automotive components competitive in price and quality on the export markets. This, in turn, would allow a reduction in tee ex-factory prices of finished vehicles, MaCVs and two-wheelers in particular, and further iffiprove their exportability.

33. Private individual firms are likely to undertake the investments and introduce the operating efficiencies essential to the success of this strategy only if there exists a more competitive market environment providing sufficient pressure for improvements in cost and quality.

-xii-

Conclusions and Recommendations

34. Over the past 30 years India has developed an automotive industry which provided positive benefits to the economy by meeting the essential needs for road transport and made a contribution to exports. However, the policies aimed at protecting and encouraging this industry have outlived their usefulness. They have not kept up with the needs of an industry in an era of rapidly evolving technological change and shifting demand. They have allowed the sector to become technologically out of date and produce vehicles not of international standards of quality or design and performance. The component sector is now hampered by high production costs, except in some enclaves of performance. However, most product groups (except passenger cars and some components) can be competitive. The industry is now in a transition pha'e. The basic challenge is to extend the existing momentum for modernization on a large scale to the component subsector, to unleash the subsector's potential and to create an environment in which there are both the incentives and the flexibility needed to maintain a competitive and technologically modern automotive indu6try.

35. The interventionist approach, which has traditionally been used in India, is no longer advisable for an indu~try that has been evolving relatively quickly worldwide. The basic thrust of the following recommendations is to move towards a more market-oriented approach, and, in particular, to introduce the degree of competition necessary to ensure continuous technological upgrading, c~st reduction and exports. It would be d~sirable for a~omotive exports to expand markedly, in view of the import costs involved in modernization (equipment, CKD kits, raw materials). The industry should receive comprehensive, clear and stable signals from the Government on the new framework for competition, as well as incentives for undertaking desirable actions and investments. In the latter respect, the Government should therefore prepare and publish, in close collaboration with industry's leaders, an integrated long-term strategy and policy paper for the automotive industry outlining its goals and the policy framework for the industry.

36. The basic objectives of such a strategy should be to:

(a) promote efficiency and continuous technological updating through active competition with easy access to foreign technologies; and

(b) remove the constraints on the growth of the market and of efficient manufacturers, in order to initiate a "virtuous causality circle" whereby higher demand permits larger scales which in turn lead to lower costs and prices which again generate higher demand.

Domestic Competition and Regulations

37. Deregulation of capacity licensing for the automotive industry should continue an~ be extended further to the removal of all remaining capacity licensing aad MRTP/FERA regulations. However, for the time being technology

-xiii-

licensing may need to be maintained to provide for MES requirements (particularly for ~ars and LCVs) until the market becomes more competitive. This delicensing process could be undertaken gradually in several steps: capacity and import licensing and other regulations could be removed for MHCVs and two-wheelers in the near-term, and for cers and Levs (including MRTP/FERA firms) in the medium and longer terms. All automotive products and components with significant economies of scale and all functional and critical parts should be removed from the SSI reservation list soon and minority participations by large automotive firms should ~e allowed in SSIs producing components. Restrictions on industrial location should also be eliminated or greatly reduced for the automotive industry, since it is one where there are considerable economies of agglomeration, particularly with the relatively modern systems of "just in time" inventory management. A more competitive environment will also require more flexible exit policies which allow firms to discontinue operations, allow for systematic bankruptcy proceedings and attempt to cushion the dislocation effects for the labor force. Finally, the development by the industry of common standards and designs for components would be desirable to improve quality and enlarge production scale.

Import Competition and Protection

38. The first priority is to eliminate the negative protection of the component sector. As underscored above, it is essential that raw materials be provided to component producers at competitive, or a least more reasonable, prices to induce them to undertake the necessary modernization investments. With respect to steel products, the World Bank has recommended that an across-the-board reduction in the tariffs for all steel products to 25% over a five- to seven-year period shoutd be carried out. Most of the specialty and high grade steel required by the automotive industry are not produced in India or are produced in inadequate quantity C~ quality. Freeing the imports of such steels could take place more rapidly without serious effects on the domestic steel industry. It is therefore recommended that these higher grades of steel be placed on OCL and their tariffs be reduced immediately to no more than 50%, thus helping to eliminate the negative effective protection of the component sector. Although there might be some temporary distortions resulting from the fact that tariffs on specialty and high grade steels would come down more rapidly than general tariffs on steel, they are not likely to be significant if the proposed tariff reform program for steel is implemented on schedule. Similar adjustments should also be explored for the import protection on other important inputs of the component sector (e.g., aluminum, engineered plastics and special rubber compounds). Finally, the measures recommended in another World Bank report for the promotion of manufactured exports (e.g, ces and 00 schemes, duty-free access to imported inputs and equipment) should be implemented with priority attention to component exporters.

39. While rationalizing the tariff structure to eliminate negative effec-tive protection for the component sector is an essential. step for the future of the automotive industry, it is not sufficient. Promotion of the industry would require not only sufficient competition among domestic firms, but also

-xlv-

price signal& aligned to the performunce of the most, not the least, efficient firms. The threat of import competiti~n should be instrumental in pressing domestic firms to bring their pLuducts to internat~onal standards of price and quality. It is recommended in this respect that quantitative restrictions and bans on all finished vehicles (exc~pt luxury cars) be progressively removed, possibly through increasing import quotat with a sim~ltaneous gradual reduction of total customs tariffs to a maximum of 50-75%. Such an adjustment would be particularly desirable for trucks, given the long overdue need for a fuel-efficient truck engine and the duopolistic production structure of this subsector in India. Practically the whole vehicle sector (except for 'traditional passenger cars) is actually or potentially competitive and could meet the increased competition from imports, but such potential competition would bring about the desired pressure to develop and maintain competitiveness and modernization.

40. With respect to PMPs, the preferred option would be to phase out these programs, allowing the domestic vehicle producers to choose among foreign and domestic components subject only to the existing tariff of 50%. Another but less desirable option would be to apply PMPs with greater flexibility. Minimum local content requirements could 3ignificantly be lowered. Components would be indigenized only after they meet acceptable cost and quality standards, and exports of components by vehicle assemblers (e.g.~uy-back arrangements) could be taken into account in meeting the local content targets.

Indirect Taxation

41. In a multi-stage industry such as automotives, it is highly desirable that indirect taxation be deductible at all stages of manufacturing and that its cumulative impact be transferred to the final purchas~r. Application of MODVAT to cover most, if not all, stages at which indirect taxation occur (including agents and entitieb which are presently exempt) would be most beneficial for the automotive industry. Most importantly, exports should be exempted from MODVAT as usually done in other countries.

420 This, however, does not necessarily entail a reduction in total indirect taxes levied on automotive products. Public revenue and social considerations, inter alia, should dictate the rates of taxation applicable to the various autOmOtive products. However, in view of the high price elasticity of demand for two-wheelers, economic efficiency and general welfare consideration strongly suggest that a reduction of indirect tax rates on these vehicles would, without lowering total tax returns, stimulate a faster growth of demand. It would permit a larger number of vehicle and component producers to achieve higher economies of scale and become internationally competitive.

•

-xv-

Benefits and Costs

43. The measures suggested above are not all of equal urgency or importance. and their impact will vary in time and scope. Some are meant to have an effect on producer costs, ~nd it is thus possible to approximate their impact on the subsector's development. After discussion of these measures th~ relative importance and effects of less quantifiable measures are assessed qualitatively.

44. Maintaining a rapid growth of the automotive industry over the long term once the present backlog of pent-up demand is met will require lower costs, higher quality vahicles. As indicated above, a sine qua ~ condition, for this purpose is the modernization and updating along with cost reduction actions, in the component sector. The combined actions and measures proposed could make most Indian automotive components fully competitive in price and quality. The proposed strategy would allow imports to continue in the shortterm, but the subsector would become increasingly able to substitute efficiently for imports, export a broader range of products, regain its former export volumes and possibly position itself favorably with major automotive assemblers abroad, and thus generate in the longer term large net foreign exchange earnings on both components and vehicles. It would also best serve the needs of the domestic market and thus maintain a high growth rate over the long term.

45. The proposed measures would not affect public revenues significantly. Lower rates of final excise ta~ation on two-wheelers should be compensated by higher production volumes, because of their high price elasticity of demand. The removal of Qas on imports would have positive revenue effects. The revenues foregone by tariff reductions would be small becaqse the alternative pOlicy of self-sufficiency based on import bans and PMPs would generate little revenue. The full fiscal implications of these measures should be further studied.

46. The potential socio-economic benefits of lower cost and higher quality products will be achieved only if the necessary quantum of competition, both domestic and external, is introduced and/or maintained in the subsector as suggested in the previous section. This may require some reshaping of the subsector's production structure and the temporary displacement of some enterprises and workers. However, the overall benefits in terms of consumer welfare, larger exports and higher labor productivity and employment dwarf such temporary costs. The Government can, and should, assist in creati~g this competitive environment by promoting increasing domestic, import and export competition, and fostering lower costs through the full implementation of MODVAT and the reduction of excise duties and customs tariffs on automotive products ~nd strategic inputs.

47. In sum, the opportunity exists to expand rapidly an automotive industry which responds to a broader range of consumer needs, increases exports and serves as a spearhead for technology upgrading at large in the industrial sector. The balance of payment and fiscal costs associated with the proposed strategy, though not fully assessed, seem to be quite manageable.

I. OVERVIEW OF THE AUTOMOTIVE PRO~UCTS SUBSECTOR AND STRUCTURAL CHARACTERISTICS OF THE VEHICLE INDUSTRY

Focus and Outline of the Report

1.01 The automotive industries worldwide generally comprise two main segments, one producing components and parts and the other one assembling them into finished vehicles. The segment producing components holds the key to th~ qualitative development of the entire industry, essentially because it determines the cost, quality and technological parameters of finished vehicles. Conversely, in integrated automotive industries like India's where vehicles are assembled mainly from locally available components and parts, the growth of the vehicle segment determines the quantitative development and prospects of the component segment. Moreover, as the report will show, India's component segment of the automotive subsector has remained relatively underdeveloped compared to the vehicle segment in terms of volumes and technology. and is presently under challenge to meet the needs of a rapidly growiug and renovating vehicle segment. For these reasons, the report has given particular attention and focus to the crit:.ca1 segment of automotive components within the overall development pro~pects of the automotive subsector.

1~02 Chapter I provides an overview of the whole automotive products subsector, .its structure, characteristics, performance (output, growth, exports) and general prospects, with attention more particularly to the vehicle segment. The performance of the component segment and its capability to meet efficiently the future needs of India's domestic and export markets are the sole subject of Chapter II. Development options and strategies for the component segment, as well as the vehicle segment on which the component segment highly depends for its growth, are presented in Chapter III. Chapter IV analyzes the present policy framework and constraints under which the automotive subsector and its segments have been operating, and underlineR the major policy adjustments and reforms considered necessary for an efficient and self-sustained development of the subsector in the long term. Finally, as requested by the Government, the outline of a possible financial support of the World Bank to India's automotive subsector is provided in Chapter V.

-2-

A. Automotive Products Overview 1/

Structure of Production

1.03 Indian vehicle production, which involves about 40 manufacturers, has traditionally focused on commercial vehicles which account for 60% ot vehicle output value. The other 40% are almost equally shared between passenger cars/jeeps and two/three-wheelers. In 1984, India manufactured some 62,000 medium/heavy commercial vehicles (trucks, buses) and about 33,000 light commercial vehicles (LCVs, vans •• pick-ups). India was the thirteenth largest producer of commercial vehicles worldwide, after Korea and before Sweden, with 0.8% of world commercial vehicle production (see Annex 1). India's production of passenger cars is much less significant by world standards with 64,000 cars in 1984, or 0.2% of world passenger cars production. India ranked twenty-fourth among car manufacturers, after Venezuela and before Turkey. The ratio of population per car in India was the world's fifth largest after China, Bangladesh, Burma and Ethiopia. 2/ However, the beginning of production of a low-cost, fuel-efficient passenger car in the early 1980s raised domestic sales above 100,000 units in 1985.

1.04 In terms of number of vehicles produced and growth, the two-wheeler segment has become dominant in the Indian vehicle industry. This reflects the high cost of passenger cars relative to disposable incomes. In 1984, 84% of all vehicles produced were two/three-wheelers. Of the balance, half was accounted ,for by commercial vehicles and the other half by· passenger cars/jeeps. Two/three-wheelers, mopeds in particular, are the fastest growing products of the vehicle market. Their growth was 11% p.a. (30% p.a. for mopeds) over the period 1975-1984 compared to 12% p.a. for passenger cars and 9% p.a. for commercial vehicles. The total output of 1,100,000 two-wheelers in 1985 was greater than that of Italy and France which manufactured about 800,000 and 450,000 units respectively in 1985. However, India's two-wheeler industry remains a distant second to Japan's, which produced 4 million units in 1984.

1/ The definition of automotive products follows the Standard International Trade Classification (SITC 1975, Revision II), item 78. Less generic equipment, such as batteries and some electrical equipment for automotive and other applications may recorded under SITC codes other than item 78. Therefore, the SITC 78 category, which is considered in the present report, includes the main but not necessarily all automotive products. The SITC 78 main sub-categories are: (1) Passenger Motor Vehicles Excluding Buses (SITC 7810); (2) Buses (SITC 7831; (3) Lorries and Trucks (SITC 7821); (4) Lorry, Truck and Bus Chassis (SITC 7841); (5) Motor Vehicle Parts, n.e.s (SITe 7849) (other than motorcycles); and (7) Motorcycle and motorized cycles (two-wheelers), etc. and Parts (SITC 785).

2/ ACMA's Statistics.

-3-

1.05 Production of automotive components involves about 190 large and medium scale firms and an estimated 8,000 small scale units. Only 300 firms in all hold a government license to manufacture components. About 90 of these firms had foreign technical support in 1984. Output in 1984/85 was Rs 8.4 billion (US$704 million). The most important "products were engine parts (40%) and transmission and steering parts (25%). Since 1974, the value of component manufacturing has grown at the rate of 13.5% p.a. in current terms, with a fairly even distribution of growth in the various categories. A large number of peripheral parts (e.g. mirrors, seat cushions, ash trays, etc.) are reserved for SSIs. Some components, such as radiators, oil seals, filters, leaf springs and rubber-to-metal components, which are functionally important to the manufacture of a vehicle, are also reserved for SSIs.

1.06 Components production is closely linked to the development of vehicle markets. Its structure is fragmented, reflecting the fragmentation of production capacities among vehicle manufacturers compounded by the unwillingness of Indian vehicle manufacturers to rely on only one source of supply, as is done in Japan, because supply might be interrupted by unforeseen problems of suppliers (e.g., strike, fire, etc.). For example, in 1984, India had fourteen licensed suppliers of clutch plates compared to only four in Japan, and eight carburetor manufacturers compared to only three in Japan. The difference in the number of suppliers is even more critical when considering the wide size difference in the respective domestic markets. Because a large number of suppliers produce each type of component, component manufacturers operate at rather small and uneconomic scales, leading to high production costs. Also, ~ow individual output does not permit subs~antial investments in Research and Development' to update both products and processes. Therefore, Indian vehicle manufacturers tend to produce, in-house components which have the most bear~ng on the final cost and quality of an engine or vehicle. As a result, the vehicle industry in India is strongly vertically integrated: vehicle manufacturers produce a significantly larger number of parts in-house than do their counterparts in industrialized countries. On average, bought-out components are estimated to amount to about 35-40% of the cost of a vehicle in India, whereas in Japan and most Western countries they represen~ 60-70% of the cost of a vehicle.

1.07 About a dozen component manufacturers have succeeded in focusing their manufacturing efforts on only one product group, very often with the technical and financial assistance of a foreign firm. In most cases, these companies have enjoyed a dominant position in their field, and sometimes a virtual monopoly in their market. However, even in these cases, production has not been of optimum economic scale because (i) prOduction volumes which, until recently, prevailed. in India were too low, and (ii) multiple specifications for vehicles and parts, including British, German, Italian and most recently French and Japanese, coexist in the Indian automotive industry. In sum, with a few exceptions, the large number of suppliers for the relatively low volume output of vehicles, the high level of vertical integration of vehicle manufacturers and the lack of

-4-

standardization have contributed to the development of an Indian component industry which is fragmgnted and generally inefficient. !/

Exports

1.08 Exports of automotive products, which are almost equally shared between complete vehicles and a~tomotive components, never exceeded 5% of the automotive industry's total output value. Production has traditionally been oriented to the more profitable domestic market. However, the percentage of components exports was as much as 14% of the components output in 1919/80. This percentage came down to 1% in 1984/85. As indicated in Table 1 below, automotive expurts accounted for 10% to 15% of engineering goods exports over the 1974-82 period. At their peak, in 1981-82, exports of automotive products were in excess of US$150 million and amounted to 2.6% of Indian manufactured exports and 1.8% of total exports. Also, with a yearly growth rate of 17% up to 1981/82, they had developed significantly faster than engineering goods, manufactured and total exports, whose annual growth rates had been respectively 12%, 12% and 9%. India's exports of automotive products did not exceed 0.1% of world trade of such products. This indicates the general inefficiency and technological backwardness of the industry.

1.09 Starting in 1982, automotive exports sharply decltned to less than US$100 million in 1984/85. This set back has been largely due to the competition from Japanese and Korean quality and fuel-efficient automotive prod~cts in India's traditional markets of Africa, SQuth Asia,and the Middle East. Due to the recent decline in performance, the overall growth in value of India's automotive exports over the 1974-85 period was only 7.2% p.a. as compared to 8.7%.p.a. for manufactured exports. Growth of automotive exports remained~ howev~r, above the growth of total exports (5.9% p.a.) over the decade.

1.10 More than half of the US$98 million automotive exports in 1984/85 were accounted for by vehicle components, 43% by commercial vehicles and jeeps, and less than 3% by two-/three-wheelers. Two-wheeler exports declined markedly from a peak of US$14 million in 1980/81. The 1984/85 automotive exports are detailed by category and destination in Table 2 and can be summarized as follows: 48% of automotive products were exported to Africa (Algeria, Egypt, Tanzania an~ Kenya); 23% to the Middle East (Iran, Saudi Arabia); 12% to South East Asia (Sri Lanka and Singapore); 8% to Western Europe (Germany and England); 6% to USA and Canada; and only 3% to the Eastern Bloc countries such as Russia and Yugoslavia.

1/ Vehicle manufacturers have always opposed the existence of virtual monopolies in each major group of components because of the risks of depending on only one source of supply: vulnerability to quality variations and delays due to labor unrest, price levels and obsolescence afforded by quasi domestic monopolies and protection from imports.

Table 1 : MAIN ENGINEERING GOODS EXPORTS: RELATIVE SHARE AND COMPARATIVE GROWTH (Current Prices)

Annual Up to 1974/75 1971/78 1980/81 1981/82 1982/83 1983/84 1984/85 Growth 1981-82

(in Rs Millions) ---_ .. ------ - (Over (7 yra.) the

Decade)

Automobile: Vehicle Components 387 937 1,162 1,366 1,190 900 1,160 11 .1 18.4 Diesel Engine Parts Pumps 191 261 655 760 100 630 165 14.1 20.2 Industrial Machinery, Others 46 203 285 400 610 32.1 Bicycles and Parts 218 303 549 550 400 450 500 8.4 13.4 Electric Wires Cables 173 298 247 450 520 300 360 7.4 13.9 Hand Tools, Small Cutting Tools 142 331 509 420 470 450 370 9.7 15.8 Iron Steel Castings (a 11 sorts) 98 340 306 460 460 22.7 Electronics 850 1,050 1,170

TOTAL ENGINEERING GOODS 3,565 6,174 8,153 9,384 12,497 11,116 13,753 13.7 14.1 ===== ===== ===:;:= ====== =:;:==== ------ ====== ==== ==== ------

(in US$ Million)

Automotive Exports 48 109 147 153 124 87 98 7.2 16.9 Engineering Goods Exports 447 721 1,033 1,051 1,298 1,078 1,157 9.6 12.4 Manufactured Exports 2,602 4,187 5,620 5,820 5,503 5,899 6,167 8.7 11.7 I

In

Total Exports (Customs) 4,672 6,315 8,502 8,523 8,037 8,380 8,406 5.9 8.7 I

----- ===== :==:= ===== :::==== ===== ===== === ====

% Share of Automotive Exports in Engineering Exports 10.7 15.1 14.2 14.6 9.6 8.1 8.5 in Manufactured Goods 1.8 2.6 2.6 2.6 2.3 1.5 1.6 in Total Exports 1.0 1.7 1.7 1.8 1.5 1.0 1.2

SOURCES, AIEl, Handbook of Statistics, 1985; World Bank Statistics.

-6-

Table 2: EXPORTS OF AUTOMOTIVE PRODUCTS 1984/85

(Million Rs)

Main Directions of Exports

Commercial Vehicles Two- and Automotive and Jeeps Three-Wheelers Components Total %

Africa 298 ~ 169 473 48.5 Middle East 107 1<+ 103 224 23.0 Southea::.t Asia 27 4 83 114 11.7 West Europe 2 75 77 7.9 North America 55 55 5.6 Eastern Europe 32 32 3.3

TOTAL 434 24 517 975 100 === == === === ===

Source: ACMA, Facts and Figures, 1985.

The ~erspect~ve Plan ,for Growth of the Automobile Industry, 1985-90

1.11 In an effort to reverse the declining trend of exports, the Government looked for determinant factors and key policies which could rejuvenate the automotive industry and provide for better export prospects. In fact, Government was concerned not only by the decline in automotive exports, but also about the catalytic role which the automotive industry should play in the development of India's economic activity. The Government objectives (as indicated in the introduction to the Perspective Plan for Growth of the Automotive Industry, 1985-90) were to develop an industry which could: (i) contribute to the development not only of automotive exports, but also of exports from directly related industries such as machine tools; (ii) stimulate improvement in domestic processing of basic raw materials such as steel; (iii) foster the development of commercial transport activities, particularly haulage of industrial goods; and (iv) generate employment and help develop new engineering teChniques, particularly manufacturing techniques aiming at making the best use of India's labor resources. In 1982, the Government constituted a Subcommittee to prepare a Itperspective Plan for the growth of the automobile industry" coinciding with the Seventh Plan period (1985-90). In drawing up such a plan, the Subcommittee came to recognize that the automotive industrY' was essentially a mass production, volume sensitive industry and therefore had to focus on -strategies and policies which could accelerate growth in the automotive industry. The Subcommittee systematically tackled the basic issues of scale, technology (products and processes), cost reduction, research and development, and export potential in each of the three main vehicle segments, namely passenger cars, commercial vehicles, and two-/three-wheelers. It also included the

-7-

automotive components industry which is a key support to the manufacture of vehicles. In mid-1984, the Subcommittee recommended a new plan for accelerated growth.

1.12 To achieve the strategic objective of accelerating growth and providing for better export prospects, the Subcommittee recommended the introduction of fuel efficient, safer and more cost effective vehicles in the domestic market and the expansion of the domestic market by drastically improving efficiency in the production of such vehicl~s. The Subcommittee also recommended that existing manufacturers upgrade their product/process technology without delay or that new capacities be licensed, and that foreign collaboration be allowed to facilitate technology transfers. Also, the Subcommittee identified a series of technology gaps in the supply of components and manufacturing tools which had to be bridged to enable Indian vehicle manufacturers produce modern vehicles efficiently and to reduce both purchasing and operating costs to the consumer. This strategy was expected to boost domestic demand and, in turn, to enable automotive manufacturers first to install facilities of a sufficient size to control quality and cost, then to expand facilities further to bring production within international standards and eventually compete in export markets. To accelerate the process of modernization across the automotive industry but avoid pricing modern, fuel efficient vehicles out of the market, the Subcommittee advised that concessional tariffs on·imports of CKD passenger car components granted to Maruti Udyog Limited--a 1981 venture between the Covernment and Japan's Suzuki Motor Company--be extended to all impo~ts of components for new fuel-efficient. vehicle~. Unde~lying such recommendations was the recognition by Government officials that continuing protection of domestic manufacturers and Government's controls over the market through capacity/product licensing had prevented the most efficient vehicle manufacturers from tapping successfully two major domestic resources, namely a potentially vast domestic market calling for mass market strategies to overcome the constraint of low individual purchasing power, and a low cost, versatile work force.

1.13 In the 1982-1984 period, there was a major increase in modernization and foreign technical assistance in the two-wheeler, passenger car and light commercial vehicle segments. The modernization wave also touched upon the component industry, but to a much lesser degree. In fact, the significant difference in modernization efforts between vehicles and components manufacturers has been of serious concern to the Government, since the vehicle industry has until recently sourced its bought-out components, which account for a third to half of the value of finished vehicles, locally. Manufacturers of fuelefficient vehicles, introduced aft~r 1983, have relied heavily on component imports. Therefore, the objective of raising domestic production to international standards of quality, reliability and cost which vehicle manufacturers are pursuing in the current modernization pt.ase cannot be achieved without the support of the component industry, unless vehicle manufacturers are allowed to continue importing components. Assuming domestic procurement of parts only when they are manufactured at volume, quality and cost levels closer to international norms can allow domestic vehicles to be produced at a reasonable level of competitiveness. For that matter, Indian automotive component suppliers are

-8-

perceived by both vehicle manufacturers and Government as holding the key to success for the entire automotive industry.

1.14 Efforts to increase efficiency in the component industry could be con-strained by structural deficiencies such as fragmented scales and heterogeneous technologies in the vehicle induscry. At the present stage of development ~f the Indian automotive industry, structural deficiencies of the vehicle segment would almost unavoidably reflect in the component segment. The rest of this chapter provides some insight into the changing profile of India's motor vehicle industry, as it sets the stage for modernization and expansion moves in the component industry. Current performance and prospects of the component industry will be examined in Chapter II.

B. Motor Vehicle Industry Profile

1.15 An Industry under Modernization. Until World War II, India imported all its motor vehicles either complete or in CKD condition (on average 20,000 vehicles a year), most of which were cars. 1/ The first two Indian vehicle manufacturers, Hindustan Motors Limited (HM) and Premier Automobiles Limited (Premier), started in 1942 and 1944 respectively. Local assembly of imported CKD vehicles dominated the market until 1954, when the Government banned assembly acti~ities by foreign companies and promoted local ownership of productive facilities and a very rapid pace of indigenization of parts and components. As a result, six other compa~ies ente~ed the market. One manufactu~ed cars, anoth~r jeeps, two commercial vehicles and the other two, two-wheelers, all initially Under licensing of foreign firms mainly from West Europe. The manufacturing of tractors ~eveloped in the late 1960s under the increased demand stemming from the "Green Revolution4 tt Total vehicle unit production grew rapidly in the 1950s, at a rate of 29% p.a, but slowed down to 11% p.a in the 1960s and 1970s, due to the stagnation of demand for the high-priced vehicles.

1.16 Growth resumed in the late 1970s, with the rapid expansion of two-wheeler demand (particularly for mopeds) stemming from rising fuel costs. The 1970s was also a period of rapid technological change and innovation in world automotive firms which undertook major rationalization and innovation moves to restore competitiveness which had been severely eroded by the manufacturing strength of Japanese manufacturers. To prevent Indian firms from lagging too

1/ Some vehicles were imported after about 1930 by General Motors (GM) and Ford in CKD condition to be assembled in their plants in Bombay, Calcutta and Madras. GM terminated its passenger car, commercial vehicle assembly and battery manufacturing activities in 1954, after 26 years of operations in India. Since 1959, until the late 1970s, GM's main involvement in India has been through a licensing agreement with Hindustan Motors which included manufacture of Bedford trucks. Currently, GM's Japanese affiliate, Isuzu (38%i, has licensed Hindustan Motors to manufacture passenger car engines and complete commercial vehicles in the medium to heavy range.

-9-

much behind a quickly changing automotive world, the Government undertook to liberalize controls over licensing and capacity expansion and access to imported technology (both products and processes). New business ventures and collaborations with Japanese and West European firms to manufacture modern, fuel efficient vehicles mushroomed between 1982 and 1985, fostering the modernization and expansion drive across the sector. In its current transition phase, India's automotive industry counts over 40 vehicle manufacturers, distributed as follows in 1984: