Embed Size (px)

Citation preview

Document of

The World Bank

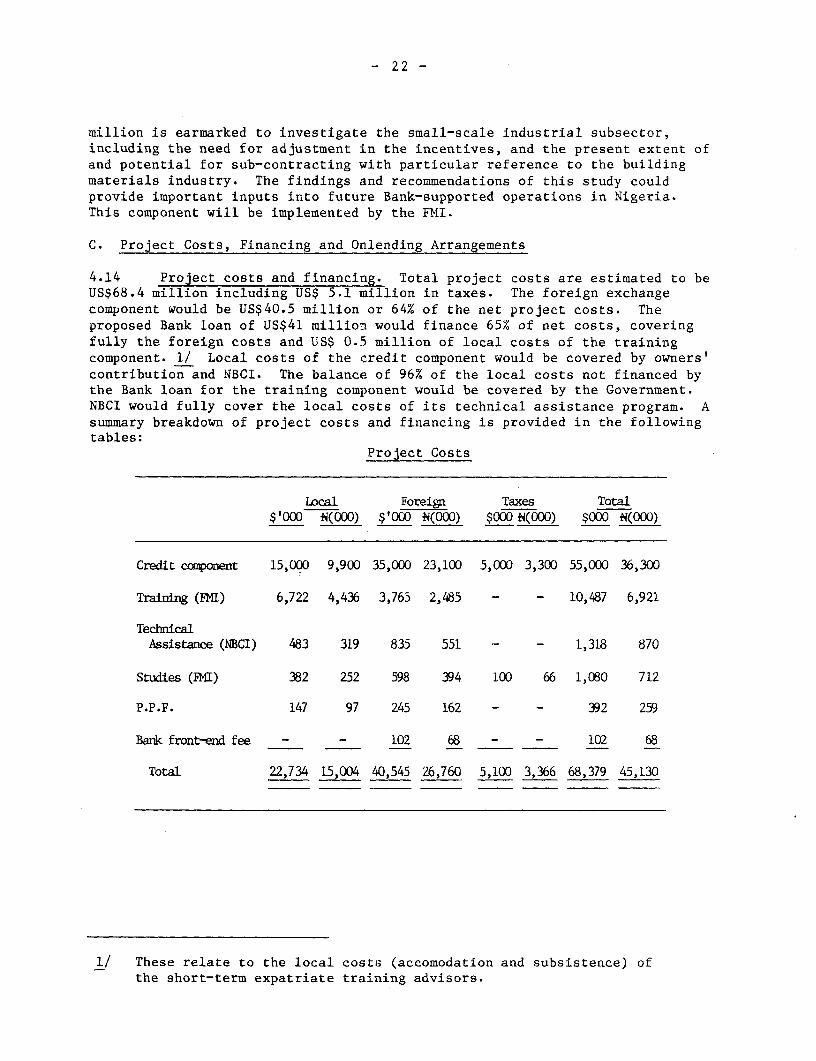

FOR OFFICIAL USE ONLY

Report No. 3597 A-UNI

STAFF APPRAISAL REPORT

NIGERIA

SMALL- AND MEDIUM - SCALE INDUSTRY PROJECT

November 15) 1983

Industrial Development and FinTance DivislonWestern Afri- ca Projects Department

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENT

Currency Unit = NairaUS$1 = N.66Ni = US$1.51

FISCAL YEAR

April 1 - March 31 (until March 31, 1980)April 1 - December 31 (1980 interim)January 1 - December 31 (from January 1, 1981)

ABBREVIATIONS

CBN Central Bank of NigeriaCMD Centre for Management DevelopmentFGN Federal Government of NigeriaFMI Federal Ministry of IndustriesIDC Industrial Development CentreILO International Labour OrganizationNACB Nigerian Agriculture and Cooperative BankNACSSI National Advisory Committee on Small-Scale IndustryNBCI Nigerian Bank for Commerce and IndustryNIDB Nigerian Industrial Development BankSME Small- and Medium-Scale EnterpriseSSID Small-Scale Industries DivisionSSIC Small-Scale Industry Scheme

FOR OFFICIAL USE ONLY

- ii. -

NIGERIA: SMALL- AND MEDIUM-SCALE INDUSTRY

STAFF APPRAISAL REPORT

TABLE OF CONTENTS

Page No.

I. INTRODUCTION ............................................. 1

II. THE SETTING ............................................. 1

A. The Economy ..................................... 1B. The Industrial Sector .......................... 2C. Small- and Medium-Scale Enterprises .... ........ 4D. The Institutional Framework .................... 6E. The Financial Sector ........................... 8

III. NIGERIAN BANK FOR COMMERCE AND INDUSTRY .................. 10

A. The institution ................................. 10B. Operations and finance .......................... 12C. Prospects ...................................... 17

IV. THE PROJECT ...................... ....................... 18

A. Project Background and Objectives .... .......... 18B. Project Description ............................ 19C. Project Costs, Financing and Onlending

Arrangements ................................ 22D. Project Implementation ......................... 24E. Benefits and Risks ............................. 25

V. AGREEMENTS REACHED AND RECOMMENDATIONS .... .............. 26

This report is based on the findings of an appraisal mission to Nigeria inMarch 1981 by Messrs. Hindle, Saleeby and Noel (Bank) and Spiro andCruickshank (consultants), followed by subsequent post-appraisal missions inApril and July 1983 by Mr. Jetha.

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

- iii -

LIST OF ANNEXES

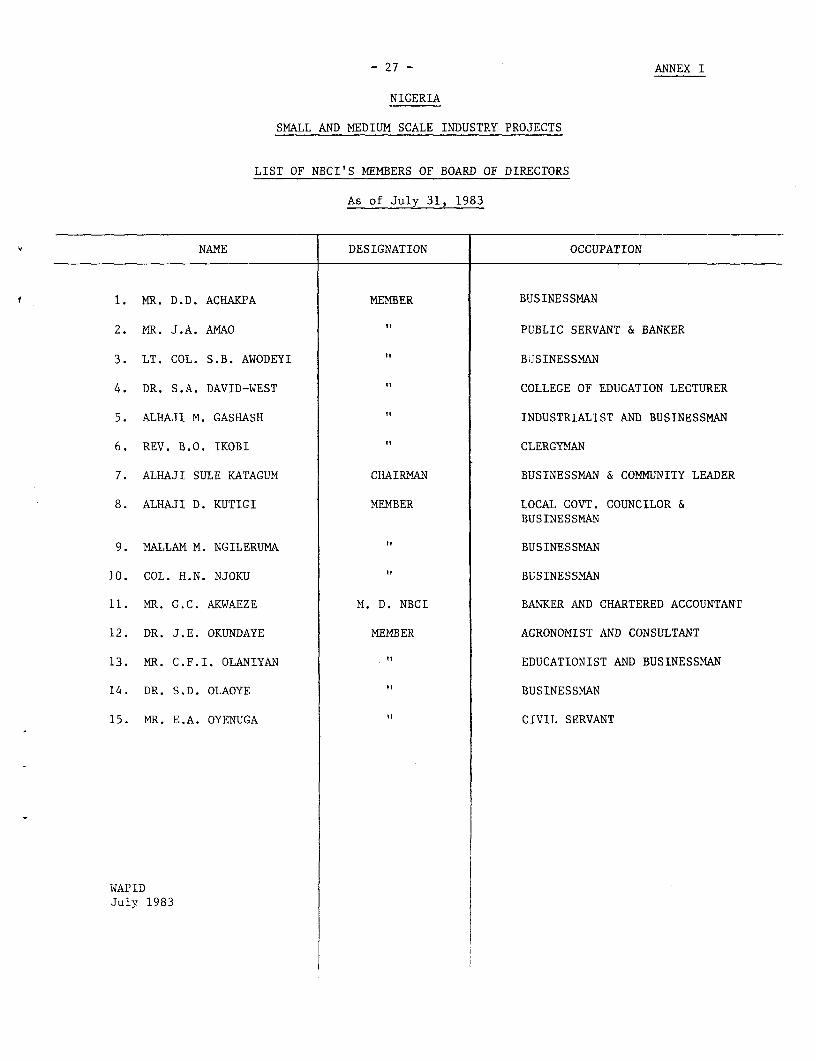

Annex 1 NBCI - List of Members of Board of Directors as ofJuly 31, 1983

Annex II NBCI - Organization ChartAnnex III NBCI - Sectoral Distribution of Approved ProjectsAnnex IV NBCI - Regional Distribution of Approved ProjectsAnnex V NBCI - Comparative Income Statement SummaryAnnex VI NBCI - Comparative Balance SheetAnnex VII NBCI - Resource Position as of December 31, 1982Annex VIII Estimated Schedule of DisbursementsAnnex IX Selected Documents and Data Available in the Project File

I. INTRODUCTION

1.01 This report recommends a Bank loan of US$41 million to the FederalGovernment of Nigeria in support of a program of financial and technicalassistance to Small and Medium Enterprises (SME) in five of the nineteenStates of the Nigerian Federation. The main objective of the project is todevelop in ANigeria a core of trained manpower and an efficient institutionalstructure capable of providing technical services and credit to sound SMEs.To meet this objective, the project would:

(i) provide a line of credit (US$35 million) and a comprehensiveprogram of technical assistance (US$ 1 million) to theNational Bank for Commerce and Industry, the financialintermediary, to strengthen its effectiveness in financialintermediation and to develop its capacity to lend to SMEs;

(ii) assist the Federal MKinistry of Industries (FMI) inestablishing an effective training program for Federalofficers, staff of the Industrial Development Centers (IDCs)and state-level extension workers, thereby developing a localcapability for technical assistance to SMEs (US$4.3 million);and

(iv) finance further sector studies to identify potential areas forSME development, including small Nigerian contractors andbuilding material producers (US$0.6 million).

II. THE SETTING

A. The Economy

2.01 Recent Developments. Although the Nigerian economy grew rapidly inthe years immediately following the quadrupling of oil prices in 1973-74, itis now suffering from effects of the oil syndrome, the current internationaloil glut, and persistent widespread poverty. Real GDP (at factor cost)increased by 6.5% per annum during 1974-77, but experienced an aggregate netdecline of nearly 5% during the succeeding four-year period ending in 1981.Annual domestic price increases soared to nearly 35% in 1975, then moderatedto 12-15% by 1980. The high rate of inflation coupled with an artificiallyhigh value for the Naira had a depressing effect on agriculture and domesticresource-based industries. As a result, the structure of the economy shifteddramatically in favor of construction, trade, and services, as well as oilproduction. Non-oil exports declined in absolute terms and now represent lessthan 5% of total exports. The country's large oil revenues facilitated heavyinvestment and current expenditures. These in turn drove up consumer demandfor imports. As a result, Nigeria has had a surplus on the current account ofits balance of payments in only one year out of the last seven. As world oilmarkets softened in the second half of 1981, the public finances (both federaland state) and the balance of payments were heavily strained and foreignexchange reserves had declined to less than two months of imports by early1983. As the resource constraints heightened, structural inbalances and thevulnerability of the economy became apparent. In the face of thedeteriorating balance-of-payments situation and increasing foreign exchangeshortages, in April 1982, the Government adopted a package of policy measures

-2-

including inter alia increased import duties and quantitative restrictions,cutbacks in public expenditures, increases in interest rates and gasolineprices, ceilings on state governments' external debt and restrictions oncapital transfers abroad. These actions, however, were not adequate in terrasof stabilizing the balance of payments in face of further softening of oilmarkets. In January 1983, additional restrictions were introduced to furtherreduce imports.

B. The Industrial Sector

2.02 Background. Despite a rapid growth rate of about 11% per annum inboth value added and employment during the 1970s, the manufacturing sectorstill represents only about 7% of Nigeria's GDP and 10% of total eraployment.Manufactured exports have fallen to an insignificant level, while importedgoods have taken an increasing share of booming domestic markets in suchimportant products as cement and vegetable oils. The performance of theindustrial sector has been constrained by technical and managerial problems,shortages of domestic raw materials, inadequate infrastructure, competitionfrom smuggled imports, and the greater attractiveness of investmentopportunities other than in manufacturing, as well as the economic recessionand deficiencies in the government policy framework.

2.03 According to the limited data available, gross investment inmanufacturing (in 1975 prices) rose dramatically from about NO.5 billion overthe period 1971-74 to N3.6 billion over 1975-78, of which private investmentaccounted for about N358 million and N2.0 billion respectively. Since then,however, new private investment does not seem to have grown as fast, and mayhave stagnated due in part to the diversion of funds into acquisitions ofexisting assets under the government's indigenization program, as well as ageneral decline in the investment climate. During this period, public sectorinvestment has significantly outpaced the private sector.

2.04 The structure of Nigerian industry remains heavily dominated byconsumer goods (e.g. food and beverages, textiles) which by the late 1970saccounted for 66% of value added and 72% of employment in the industrialsector. Intermediate goods (e.g. metal working, building materials,chemicals) accounted for 26% and 23%, and capital goods, (mostly vehicleassembly) for 8% and 5% of industriLal value added and employment,respectively. There is little reliable data available on the informalmanufacturing sector, but it still predominates in terms of industrialemployment, though its contribution to total output and value added is lessimportant. Consumer goods (particularly food, beverages and textiles)represent two-thirds or more of the value-added, employment and gross privateinvestment in the modern manufacturing sector, with chemicals, metal workingand building materials being the largest intermediate goods industries.Substantial investments in machinery and transportation equipment (mainlyvehicle assembly) have permitted the capital goods subsector to increase itsshare of industrial value added from about 1% to 8.5% during the 1970s. Thelarge public sector investments undertaken in iron and steel, pulp and paper,sugar refining, have yet to go into full commercial operation.

- 3 -

2.05 Manufacturing activity is concentrated in the Lagos area (56% ofinvestment, 43% of employment and 63% of value added in 1976), and to a lesserextent in the Kano-Kaduna region (7% of investment, 21% of employment, and 17%of value added). Mainly as a result of the government's indigenizationpolicies (Decrees of 1972 and 1977), the major share of paid-in share capitalin private sector manufacturing is now held by Nigerians.

2.06 Government Policy. Although the general business environment inNigeria has always been strongly private sector oriented, Government hasgreatly influenced industrial development, both directly and indirectly.Directly, as in many other oil economies, Government has undertaken most ofthe country's investment in large industries of national importance for whichlocal private capital was not available or where ownership was consideredundesirable. Indirectly, private sector investment decisions have beenaffected by a host of government decrees and regulations aimed at promotingand regulating industrial development. This, however, was achieved to alarger extent through increased recourse to tariff and quantitative protectionmeasures, resulting in large distortions in the domestic price structure andin the pattern of industrial investment. Mainly as a result of governmentpolicy, modern industrial development has been biased towards large scalepublic investments in basic industries and private investments in lightconsumer goods and assembly industries, which depend on imported inputs, andrely upon excessive protection and budgetary support. Efficiency,particularly that of public enterprises, is generally low.

2.07 The Government's industrial policy and strategy, as reflected in itsFourth National Development Plan (1981-85), reconfirm the Government'scommitment to industrial development as one of the main pillars of Nigeria'slong-term development. The Government's aim is to develop industries usinglocal raw materials (especially agro-related), strengthen intrasectorallinkages, emphasize manpower and technological development, disperseinvestment regionally, promote export-oriented industries, and stimulatesmall-scale industries. Priority is being given to food processing, textiles,

building materials, engineering, chemicals, electrical equipment, andhousehold durables. Labor intensive industries are also being encouraged. Amore vital role is to be assigned to the private sector, with the role ofGovernment focussed on infrastructure investment, establishment of anappropriate legal and regulatory climate, and investment in heavy projectssuch as steel, fertilizer, LNG, petrochemicals, and cement. Greaterindustrial efficiency and competitiveness is to be promoted through increasedcompetition and improved product quality.

2.08 Bank Group Strategy. On the whole, the Government's broad sectoralobjectives point in the right direction but their realization will require amajor and time-consuming effort on the part of the Government, particularly informulating and implementing the specific policy changes that are needed andestablishing the appropriate administrative mechanisms. The Government hasasked the Bank to assist in this regard. Accordingly, the Bank is undertakinga major program of economic and sector work with the objective of providing abasis for a continuing policy dialogue with the Government on issues affectingthe industrial sector. More specifically, this program aims at making inputsinto current Government efforts at translating its broad industrialdevelopment strategy, described in the preceding paragraph, into concretepolicy changes designed to improve industrial efficiency and encourage greater

- 4 -

private initiative. An Industrial Incentives Report has been comnlet-ed, whichproposes a medium-term program of measures (including adjustmert of exchaangerate and reform of the incentives and protective system) to restructure theincentives system, improve its administration and to streamline the regulatoryframework. This report was discussied with the Government at aninterministerial committee meeting in April, 1983 the outcome of w1hich wasgenerally positive. The Government has already indicated its intention toimplement certain of the report's recommendations (e.g. phasing out of dutyconcessions on imported inputs) and an Industry Technical Assistance Programis under preparation to support these efforts. It is also expected thatnecessary policy changes in relation to trade protection incentives will beaddressed in a possible EFF program currently under discussion between the IMFand the Government, and also a possible SAL envisaged by the Bank. Apreliminary study on Financial Intermediation has been completed, with follow-up work to be undertaken in order, among other things, to (a) identify ordevelop further mechanisms for financial intermediation; and (b) helpformulate mechanisms for the Government to productively invest its oilrevenues. Our sector work program also includes studies (at various stages ofpreparation) on several key subsectors, such as Construction Materials, Agro-Industries, Basic Metals and Engineerings, Petrochemical Industries andIndustrial Infrastructure. These subsector studies also aim at identifyingpromising investment opportunities for Nigeria and developing suitableprojects for Bank Group financing. An in-depth review of the PublicInvestment Program in Manufacturing has recently been prepared and willshortly be discussed with the Government. The recently approved fourth Bankloan to NIDB will reinforce ongoing and future sector policy dialogue betweenthe Government and the Bank while supporting the main objectives of Nigeria'sindustrial strategy by focussing on priority subsectors (e.g. agro-industries,intermediate goods). The proposed Small and Medium Industries loan willcomplement this approach by encouraging employment creation, efficientregional dispersal and strengthening and deepening the financial institutionsand SMI extension service systems.

2.09 Prospects. Nigeria has substantial potential for industrialdevelopment based upon its large domestic market, high per capita income byAfrican standards, substantial agricultural and mineral resources and itssizeable pool of private entrepreneurs. Currently, manufacturing output andinvestment are affected by depressed economic conditions and shortages offoreign exchange for inputs and spares. However, substantial market demandexists for manufactured goods. While stabilization measures are needed in theeconomy in the short-term, these will also need to set in motion necessarystructural changes through increasing incentives to industry andagriculture. Subject to the adoption and implementation of appropriate policymeasures which are the subject of ongoing discussions between the Governmentand the Bank (see para 2.08), significant medium-term prospects exist forindustrial growth.

C. Small- and-Medium-Scale Enterprises

2.10 Background. Despite some survey work carried out in the early 1970sby Nigerian universities and subsequent work by the Bank, knowledge of the SMEsubsector is limited. In 1972 the FGN's official definition of small-scaleenterprises included all firms with machinery and equipment valued at lessthan N150,000 (about US$ 230,000), a definition which has proven too

- 5 -

restrictive in the current Nigerian context especially in view ofinfrastructure constraints and inflation. 1/ Accordingly, small scaleenterprises in recent times are understood to include all those with capitalcosts (excluding land and building) not exceeding N250,000 (US$ 380,000).Likewise, enterprises with capital assets not exceeding N1-1.5 million(US$1.5-2.3 million), though not formally defined as such, are consideredmedium scale enterprises. Attempts made at gaining a better knowledge of SMEin Nigeria have proven elusive, as the sheer size of the country and diversityof small and medium firms has made it difficult to design adequate surveyprograms. Political and social factors have had an important impact on smallbusiness development in Nigeria. First, policy responsibility for small scalebusiness support is shared between federal and state governments, leadingsimultaneously to competition for responsibility and in other cases to mutualneglect. Second, potential entrepreneurs in different geographic areas seemmore or less willing to begin specific businesses, which means that differentstates have different needs and entrepreneurial potential. Certainly theneeds of small businesses are not uniform across Nigeria and vary bylocation. Third, insofar as extension work is an important part of assistanceto small businesses, language constraints apply and virtually necessitatestate directed extension efforts. To deal with such a diverse population ofultimate clients, the project described in this report is a pilot programdesigned to serve primarily five selected States of the Federation. The fivechosen States, selected by FGN, (Cross Rivers, Imo, Niger, Ondo and Plateau)themselves are extraordinarily diverse, but would provide practical experiencein the problems of providing and managing credit and advice to SMlEs inNigeria.

2.11 Profile of Nigerian SMEs. In 1972 the number of modern sector SMEs(defined at that time as those employing fewer than 10 workers) was estimatedat about 90,000. Extrapolating from surveys carried out in the Project'sfive target States, the Bank estimates the number of such firms to be about125,000 now. Regional growth rates both in terms of numbers of firms andsales indicate that numbers of firms may have increased slightly less thanpopulation growth. Clearer evidence is available on the main features ofsmall scale businesses in Nigeria than on their numbers. Tailoring, furnituremaking and baking remain the predominant small enterprises. Automobile repairand metal working are also important. (A recent study by Michigan StateUniversity indicates that in Nigeria, rates of return on tailoring arevirtually nil, but quite high on furniture making, baking and automobilerepairs). Almost 90 percent of small businesses in Nigeria employ two to fivepersons, are highly concentrated in urban areas, are almost exclusively soleproprietorships, depend on their own or relatives' capital, and are promotedby the marginally educated (primary school or below). SMEs in Nigeria areexclusively Nigerian-owned and managed. Little quantitative information isavailable on competition among small, medium and large firms, although

1/ Assuming an annual inflation rate of only 10%, the 1972 figure ofN150,000 would be approximately N350,000 in today's value.

-6-

informal sector firms appear to prcduce for slightly different clienteles.SMEs, although much better distributed throughout the Federation than largeindustries typically have been, seem to be proportionally more numerous in thesouth.

2412 Constraints on SME. Constraints to SME development appear to fall infive categories: i) insufficient properly trained manpower; ii) insufficientSME-oriented capital coupled with inadequate financial intermediation;iii) poor infrastructure support; iv) constrained markets; v) Governmentinertia in providing necessary support. Concerning human skills, there doesnot appear to be a lack of entrepreneurial drive or initiative, as much asthere is a lack of trained technical skills necessary to manage businessgrowth and expansion. Capital insufficiency for small businesses is less aquestion of absolute availability than one of inadequate financialintermediation and the need for priming the pump of domestic liquidity toinduce greater flows to this sector. Infrastructure inadequacy is a pervasiveproblem, but in the case of smaller businesses with limited access to capitalit is especially troublesome, as SHEs are less able to finance their owncaptive water or power supplies. Markets are affected by poor transportfacilities, by uncontrolled imports, or by the parachuting of large scaleenterprises which suddenly absorb the sources of raw materials and flood themarkets of existing SMEs. In contrast to these constraints, the potential forsmall- and medium-scale businesses is sizeable, consumer demand is rising andindustrial growth is seen by government as a cornerstone of futuredevelopment.

2.13 Prospects for SME. Although public stress has been laid on thepromotion of SMEs, practical efforts by the Federal Government have so farbeen limited to designating one federal bank, Nigerian Bank for Commerce andIndustry (NBCI), as lender to SMEs and establishing Industrial DevelopmentCenters (IDCs) to service them (See para 2.15). At the state level, SmallScale Industry Credit Schemes (SSIC; see para 2.23) have had some success inestablishing a core (though insufficient) of trained industrial extensionofficers and a pipeline of projects. These developments, linked to Nigeria'srapid growth and generally dynamic industrial sector, result in fairly brightprospects for SMEs. As an example, in the five target states surveyed forthis project, about 300 small firms with projects totaling about N60 millionappear feasible over the next three years. Of these projects, about 80% havealready reached some advanced stage of preparation. For the longer term, theprospects for Nigerian firms are good as linkages between existing largeenterprises are established and the economy is restructured to emphasizemanufactured goods.

D. The Institutional Framework

2.14 Agencies Assisting SMEs. At the federal level, the focal point forall policies affecting SMEs is the Small-Scale Industries Division (SSID) ofthe Federal Ministry of Industries. As organized, SSID has three divisions:one is the liaison channel with NBCI, one oversees the IDCs, and one handlesadministrative matters. The IDCs are federal agencies, staffed by federalcivil servants. It is Government's intention to establish one in each of thestates. There are also two industrial estates for SMEs, one near Lagos andone in Anambra State. At the state level, within state ministries of Trade,Industry and Cooperatives, each state has its own Small-Scale Industry

-7-

Division. In a purely advisory role, the National Advisory Committee onSmall-Scale Industry (NACSSI) provides advice to state and federal agencies onSME promotion. Finally, outside government the University of Ife's IndustrialDevelopment and Research Unit has established its own small industriesconsultancy service and the ILO supported Centre for Management Development(CMD), is actively engaged in working with SMEs.

2.15 Industrial Development Centers. In 1962, external consultantsfinanced by USAID proposed to Nigeria the establishment of three industrialdevelopment centers (IDCs) in the northern, eastern and western regions. Theobjective of the IDCs is to render on the spot assistance and guidance tosmall industries on process techniques, selection of machinery, training andmanagement. The centers did this through the establishment of commonworkshops, provision of specialized machines, service and testing equipment,libraries and training courses and extension work. In line with theobjectives of the Fourth National Development Plan to provide a center foreach state of the Federation, ten more IDCs have been set up in the recentpast. The remaining six are planned to be established within the next year.The total staff of the IDC system in 1982 was 97 professionals and slightlyover 150 support staff.

2.16 State Ministries of Industries. Although IDCs are the core agenciesresponsible for providing managerial, technical and other assistance to SMEs,the Small Scale industries divisions of the State Ministries also rendersignificant extension services to local enterprises. Through their variousarea offices, the state ministries are often more accessible and betterattuned to local conditions than IDCs and thus, are generally in a betterposition to deal with the problems of smaller entrepreneurs. Areas ofassistance include both pre and post investment activity as well ascounselling on accountancy and management.

2.17 The delivery of assistance to SME has suffered from a number ofproblems. First, because IDCs are perceived as an extension of the FederalMinistry of Industries into the state environment, there is frequently a lackof coordination and cooperation between the IDC and the state ministries.Second, the centers are staffed with federal employees, who often do not speakthe local language and who are inadequately paid. Third, federal financialsupport for operations has been an on again off again proposition depending onthe level of federal resources. Fourth, the current expansion of the IDCsystem from three centers to a nationwide system is putting severe strains onthe existing staff. Despite these problems, the basic concept underlying theIDCs is still sound. Given adequate funding and staffing, carefully detailedoperating procedures, as well as external technical assistance, they should beable to operate as centralized training points for staff from state ministriesin the appraisal, promotion and supervision of small scale businesses.Moreover, they are well placed to act as referral centers for difficulttechnical and managerial problems encountered by state extension officers inthe course of working with small businesses.

-8-

E. The Financial Sector

2.18 Financial Institutions. Nigeria has a relatively well developedfinancial system. In addition to a number of merchant banks, state andfederal development banks, savings banks, mortgage banks and other financialinstitutions, there is an extensive commercial banking network that isincreasingly spreading to smaller cities throughout the 19 states. In 1970,at the end of the civil war, the Central Bank had six branches, while today ithas eleven branches and five currency centers, as well as plans to reach theobjective of one branch in each of the 19 states of the Federation. In 1970,Nigeria had only 14 commercial banks with 273 offices, compared with over 20commercial banks with more than 800 offices at the end of 1982. In the sameinterval, merchant banks have multiplied from one in 1970 to six today.

2.19 Central Bank Policy. The Central Bank of Nigeria (CBN) has been atthe forefront of this growth, emphasizing its developmental role. In the pastdecade, it has had increasing recourse to a wide array of policy instrumentsto foster and direct the growth of the financial sector in Nigeria. Afteractively participating in the promotion of the domestic money and capitalmarkets, the CBN sustained the development of the most important financialinstitutions, among which the Nigerian Industrial Development Bank (NIDB),Nigerian Bank for Commerce and Industry (NBCI) and Nigerian Agriculture andCooperative Bank (NACB). Through the Agricultural Credit Guarantee Fund, itprovides a guarantee to commercial and merchant banks on agricultural creditsup to 75%; and through the Rural Banking Scheme, it requires Nigeriancommercial banks to open 260 new branches throughout the country by the end of1985.

2.20 The CBN regulates the financial sector. It sets ceilings on overallcredit expansion by commercial and merchant banks (currently 30% per annum).It determines minimum shares for preferred sectors in total loans and advancesfrom commercial banks and maximum shares for non-priority sectors. Itrequires a minimum portion (currently 40%) of total loans and advances bymerchant banks to be medium to long-term with maturities of not less thanthree years. It expects banks to maintain a minimum credit allocation of 70%to indigenous borrowers, including 16% to be reserved entirely for small-scaleenterprise. It also monitors the banks' financial position by requiring themto respect certain cash reserve and liquidity ratios.

2.21 Interest Rates. Interest rate guidelines for various financialinstitutions are likewise established by the CBN, subject to periodicrevision. Since the most recent revision in November 1982, these guidelinesprovide for interest rates across sectors ranging from 6 to 13% with a maximumlending rate to industry of 11-1/2% for loans maturing within three years andof 13% for those with longer maturities. Lending rate guidelines for NBCI andNIDB range from 10-1/2% to 13%. NBCI and NIDB, however, are not subject tothe credit ceiling applied on commercial and merchant banks and NBCI has setits rate at 12%, up from between 6-10% previously. Although interest rates inNigeria are still below the rate of inflation, projected at 15% for themedium-term, rates have moved up considerably over the past few years.

-9-

2.22 Lending to SMEs. Despite the existence of a large number offinancial institutions and CBN's guidelines for the banks to allocate a

minimum share of their loans to small scale enterprises, adequateinstitutional credit has not been available to SMEs. Although the Banks

generally meet or sometimes exceed the CBN stipulated 70% allocation to

indigenous borrowers, they have consistently failed to reach the targets inrespect of loans to Nigerian owned small scale enterprises. The industrialdevelopment banks and the state investment companies have mainly lent tomedium- and large-scale enterprises and commercial banks have preferred theestablished and well-known corporate borrowers. As a result, the only

organized form of credit to SSEs has been the SSIC Scheme (see para 2.23).Very little information is available on non-institutional sources of finance,

but a survey of nearly 22,000 SSEs, conducted in the early 1970's by theIndustrial Research and Development Unit of the University of Ife indicated

that the main sources of finance were owner savings and those from relativesor friends. Similarly, little is known about suppliers' credit. In spite ofgovernment efforts to finance SSEs through the SSIC scheme, the generalpicture is still as in many other developing countries: inaccessibility ofinstitutional sources of funds for SSEs which consequently become largely

confined to sources whose methods are relatively simple; these, however,provide mostly short-term financing only, are unreliable and - in the case ofmoneylenders - extremely expensive.

2.23 Small Scale Industry Credit Schemes. With a view to providing

technical and financial assistance for the development of Small Scale Nigerianenterprises in manufacturing, processing and service activities, the SmallScale Industries Credit Scheme (SSIC) was established by the FederalGovernment in the mid-1960's. Relying on matching funds from the states and

the Federal Government, SSICs have been established in all 19 states and aregenerally managed by the State Ministries of Industry, Trade andCooperatives. A loan management committee consisting of state civil servants,representatives of the IDCs and branch managers of local disbursing banksdirect the credit activities of the SSIC. Delivery of technical assistance tothe borrowers, evaluation of their project proposals and collections of theloans are services that IDCs are normally required to provide under thescheme, but, due to IDC staff and resource constraints, these tasks have, inpractice, been increasingly carried out by the State Ministry officials.

2.24 The performance of the scheme has varied considerably from state tostate, although a number of difficulties are common. Despite the fact thatmost of the schemes have screened and approved a large number of loanapplications, actual disbursement of funds has been minimal owing to the factthat both federal and state governments have not been able to meet theirfunding commitments. Moreover, many of the projects ultimately financed havebeen assisted for reasons other than financial or technical viability.Arrears have been extensive and, contrary to original expectations, verylittle, if any, roll over has taken place. In virtually every state, there

have been extensive overcommitments as well as numerous projects on the shelfawaiting approval. The technical capacity of the state civil servants whocarry out the program also varies considerably, although the general level issatisfactory and can be improved with proper training. Finally, the problemof coordinating the state work with IDCs has never really been overcome.Insufficient mobility on the part of both IDC staff and state people,

shortages of experienced staff and communication problems have been very

- 10 -

difficult. Despite these inadequacies, the concept of state basedorganizations for SME promotion is fundamentally sound. What is needed,however, is a consistently available source of credit, training for extensionworkers and acceptable standards of project appraisal. Although creditallocation by the SSICs has been negatively affected by politicalconsiderations and the lack of funds, the industrial officers in the stateministries are frequently the best placed persons to know the needs andenvironment of small local borrowers. The ministries could well therefore,move out of direct financing of projects and focus on the extensionservices. Perhaps to underscore this shift, the Federal Government, in recentyears, has stopped making funds directly available to the states and hasinstead been relying exclusively on NBCI to channel funds for onlending toSSIs within the states.

2.25 Prospects. Demand for credit by Nigerian SMEs is vast, yet, apartfrom limited funds provided through SSICs, little organized form of lending isavailable to them. NBCI, the designated federal financial institution tosupport the growth of indigenous enterprises, has, in the recent past,increased its efforts to satisfy this demand but, lacking the necessarycoverage, experience and resources, its impact so far has not beensignificant. Given the vast size of the country and the diverse needs of theentrepreneurs, an effective credit delivery system in Nigeria appears to beone which would combine apex banking with or without direct lending by NBCIand the bulk of retailing by the commercial and state level banks. However,such a system, under current constraints resulting from institutionalweaknesses in NBCI and the prevailing interest rate structures, which do notallow for a sufficiently attractive spread to retail banks, is not likely tobe accomplished for some time. Bearing these factors in mind, the proposedproject, as a first step in that direction, aims at institutionallystrengthening NBCI and enhancing its role as the principal SME financialintermediary in Nigeria.

III. NIGERIAN BANK FOR COMMERCE AND INDUSTRY (NBCI)

A. The Institution

3.01 Background. The Nigerian Bank for Commerce and Industry (NBCI) wasestablished by Decree 1/ in April 1973, to promote and assist indigenousenterprises in the areas of commerce and industry. Its activities includeequity investments, loans (including short-term advances by its merchantbanking unit), guarantees, underwritings, and merchant banking services. Todate, the bulk of NBCI's activities have been loan and equity financing ofmedium-size Nigerian enterprises, although, with the establishment of branchesin each of the nineteen states of the Federation and through channelling offederal SSIC funds, NBCI has, in recent years, tended to increase the share ofits lending to small scale enterprises.

1/ Now changed to a Legislative Act.

- 11 -

3.02 Capital. NBCI's authorized and paid-in capital is N50 million,represented by 500,000 shares having a par value of N100 each. The Governmentand Central Bank are the sole shareholders of NBCI,subscribing to 60% and 40%of the shares respectively. NBCI has proposed to the Government and CBN, andreceived in principle their approval to increase the share capital to N150million to be achieved by conversion into equity of N60 million of theoutstanding N110 million loans from the Government and fresh subscription ofN40 million by CBN. The conversion from loan to equity of the Government'sshare would not provide any new resources to NBCI, as the funds in questionhave already been received, but it would result in a sizeable saving of

* interest payments and ease NBCI's cash flow.

3.03 Board. Annex I contains a list of NBCI's Board members which, as ofJuly 31, 1983, stood at 15 Directors. NBCI's act does not provide for a fixednumber of Directors, and, except for the Chairman, the Managing Director, andone Director each from the Federal Ministries of Finance, EconomicDevelopment, Trade, Industries and the Central Bank, the Minister ofFinance 1/ may as necessary appoint additional members. NBCI's current Boardis made up largely of experienced businessmen, but the amount of flexibilityprovided by the Charter is unnecessary and agreement was reached duringnegotiations that it would be amended to set a maximum number of members andspecific term of appointment. NBCI's Board decides upon all investments ofN300,000 and over. The Board meets on the average, once every two months.

3.04 Policies, Operating Guidelines and Procedures. Subsequent to on-going discussions between the Bank and NBCI in conjunction with the proposedproject, the basic policies and procedures, outlining NBCI's operating methodsand practices have now been drawn up. Although these still need to becomplemented and further refined in due course, particularly in areas relatingto internal control, financial management, branch operations and loansupervision, they already provide an adequate institutional framework forNBCI's activities. NBCI's policy statement has however not yet been approvedby its Board and this approval would be made a condition of effectiveness forthe proposed loan. NBCI's current policies are generally satisfactory:equity investments in individual companies are limited to 40% of the company'sshare capital, loans are generally restricted to 70% of the total investmentsand NBCI's maximum exposure in any single company is not to exceed 10% ofNBCI's paid-up share capital. Exceptions to these limits may be authorizedon economic grounds for high priority projects, which may require to bepromoted by NBCI itself. Such exceptions are however not expected to benumerous. Procedures with respect to loan appraisal and supervision,disbursements, security requirements, guarantees etc. are likewisesatisfactory and, if applied strictly, should result in markedly improving thestandards of NBCI's operations and, over the long run, the quality of itsportfolio. Compliance with the established procedures is however an arearequiring stricter enforcement and tighter monitoring by NBCI's managementthan in the past.

1/ Now changed to the Minister of Industries.

- 12 -

3.05 Foreign Exchange Risk. Except for a single US$20 million exportcredit from Morgan Grenfell, secured in 1982, all NBCI borrowings aredenominated in Nairas. NBCI's loan agreement, amended following the Bank'srecommendations, passes on the foreign exchange risk on the above credit tothe borrowers. The foreign exchange risk on the proposed Bank loan will beassumed by the Government. Hence NBCI does not currently or prospectivelycarry any exchange risk. However, were NBCI to borrow externally to financethe cost of its projected new head office in Abuja, as initially planned, itwould incur a sizeable exposure to this risk. Assurances were obtained thatfor all such external borrowings, NBCI would take appropriate steps to protectitself against foreign exchange risk.

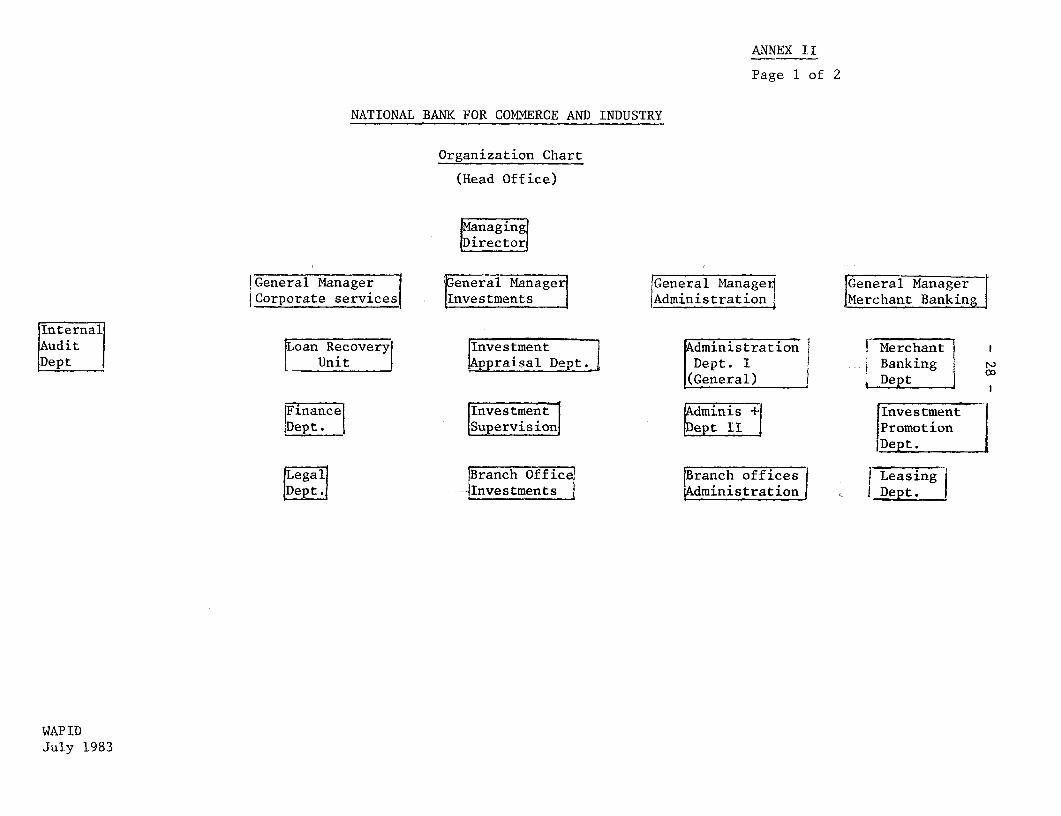

3.06 Organization, Management and Staff. As shown in Annex II, NBCI isorganized into four major Departments (Corporate Services, Investment,Administration and Merchant Banking), each headed by a General Manager.NBCI's senior management is competent and reasonably well trained, but thinlyspread and hampered by lack of experienced professional officers andsufficient support staff. NBCI presently employs over 700 people includingabout 150 in the nineteen branches. NBCI's professional staff numbers about130, most of whom are college graduates, with several having advanced degreesand/or professional qualifications (e.g. MSs, MBAs, CPAs etc.) in economics,business and accounting. About 80 of NBCI's professional staff are engaged inappraisal and supervision activities, of whom eight are trained engineers.Given NBCI's significant involvement with industrial and manufacturingprojects, the volume and scope of its operations, and the weak quality of itsportfolio, there is clearly a neecl to strengthen its technical appraisal andsupervision capability, mainly through provision of advisory services andstaff training. Likewise, assistance is also needed to strengthen NBCI'saccounting and financial systems and procedures as well as its internalcontrol mechanisms. Finally, the recent rapid growth in the number of itsbranch offices (currently one in each of the 19 states in the Federation) hashighlighted the need for setting-up appropriate structures and procedures tobetter monitor, control and evaluate the performance and operations of thesebranches in addition to providing on-the-job training for field officersworking in these branches.

3.07 To meet these various demands, the proposed project provides forfinancing of a comprehensive technical assistance program to NBCI. Theproposed program would consist of provision to NBCI by an experienced bankinginstitution and/or by individual experts, from overseas, of up to96 man/months of advisory services covering a broad spectrum of itsactivities, including project promotion, appraisal and supervision, portfoliomanagement, accounting and financial management, internal control and branchnetwork management. In addition to on-the-job training, selected officers ofNBCI would also benefit from overseas training under the program.

B. Operations and Finance

3.08 Volume of Approvals. as of March 31, 1983, NBCI had approved a totalof 306 projects for commitments amounting to N332.2 million of which equityinvestments in 108 projects accounted for N27 million (8.1%), loans to 290projects accounted for N236.4 million (71.2%) and guarantees to 30 projects

- 13 -

for N 68.5 million 1/. NBCI's annual approvals during the review period havebeen uneven. After reaching a high of N62 million in 1976, annual approvalsdropped for two consecutive years, reaching a low of N7.2 million in 1978,before picking up again to N9.7 million in 1979, N10.4 million in 1980 and N63million in 1981. Approvals dropped again to N26 million in 1982. Annualcommitments during this period have been substantially lower than approvalsaveraging about 48% of annual approvals, owing in part to premature approvals,and also NBCI's limited financial resources during these years. In 1977 and1978, however, commitments were about 50% higher than approvals in each ofthose years, due to a drop in approvals, coupled with substantial carryoverfrom prior years' high approval levels.

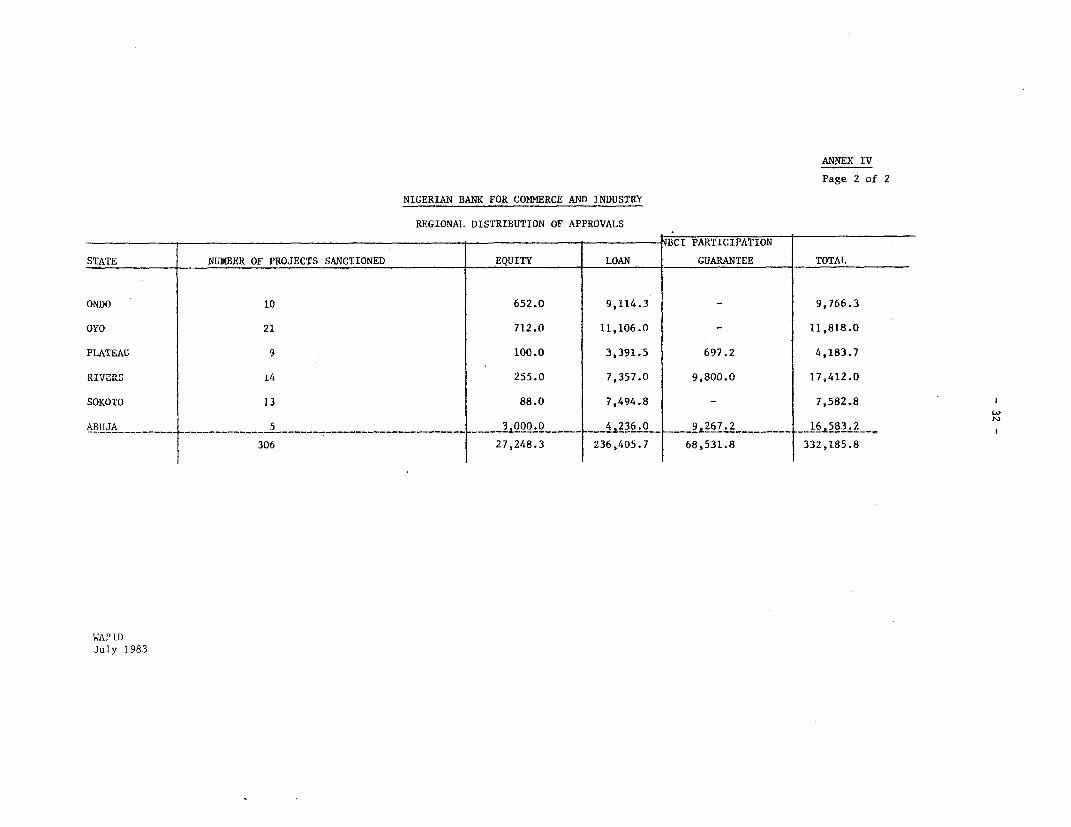

3.09 Sectoral and Regional Distribution of Approvals. NBCI's operations(detailed in Annex III) are multi-sectoral, spanning 14 major areas ofactivities, with non-metallic minerals, food and beverages, hotels and tourismand wood and wood products accounting for the bulk of NBCI's assistance. NBCIhas managed to diversify its portfolio and maintain a balance between varioussub-sectors in terms of its direct lending. Likewise, despite disparities ineconomic potential among the various states, NBCI strives to balance itslending to these states, which in practice is difficult to achieve. Regionaldistribution of N4BCI's approvals as of March 31, 1983 is shown in Annex IV.

3.10 Client Profile. In keeping with its mandate to promote indigenousentrepreneurs, all of NBCI's projects are either wholly of majority Nigerian-owned. As of December 31, 1982, about 60% of NBCI's projects were 100%Nigerian-owned, while the balance were at least 51% Nigerian. In terms ofclient size, the average total cost of NBCI's projects was N2.0 million(approximately USA 3.1 million), while the average size of NBCI's assistancein direct loans was NO.78 million (approximately US$ 1.2 million), and NO.25million (US$0.4 million) in equity investments. Of all the loans approved byNBCI through March 31, 1983, 37.8% in number (and 7.6% in amount) were loansof N250,000 and less, 44.1% in number (and 28.6% in amount) were loans ofbetween N250,000 and N 1 million and the balance (18.1% in number and 63.8% inamount) were loans of N 1 million and more. Within the context of theNigerian economy, NBCI's beneficiaries (81.9% of total approvals in number)have thus been primarily medium- and small-sized projects.

1/ These figures do not include NBCI's approvals of small loans underthe Federal Government SSIC scheme, which it manages since late 1981.Total approvals under this scheme, as of January 31, 1983, amounted toN50.2 million (US$75.8 million) for 1,368 projects.

- 14 -

3.11 Portfolio. As of December 31, 1982, NBCI's outstanding portfolioconsisted of 180 projects amounting to N110.4 million. 1/ Of this amount,-N96.1 million (87%) represented straight loan assistance while the balance ofN14.3 million (13%) represented equity investments. Partly as a result ofunorganized and inadequate investment supervision and recovery efforts, theoverall quality of NBCI's portfolio is poor. Of N96.1 million in loansoutstanding to 180 companies, 96 companies are experiencing difficulties witharrears of N42 million representing NBCI's exposure of about N60.8 million.Thus, based upon available data, it is estimated that, as of December 31,1982, about 63% of NBCI's portfolio was affected by arrears, of which N27.3(65% of total arrears) was over 12 months. As of December 31, 1982, NBCI hadcollected only about N11.3 million in loan repayments out of a total of aboutN53 million due, reflecting a recovery rate of 21%. In terms of geographiclocation, six states account for over 60% of NBCI's arrears (Oyo, CrossRiver, Kaduna, Bendel, Ondo and Anambra). Sectorally, three activitiesaccount for almost 60% of arrears (wood and wood products 14.9%, non metallicminerals 23.6%, and food and beverages 20%).

3.12 NBCI's auditors, D.F. Dafinone & Co., have expressed concern over thehigh level of arrears and reservations as to the adequacy of existingportfolio provisions, which according to NBCI's 1981 accounts stood at aboutN3.2 million, or 3.7% of the total outstanding loans. Accordingly, theauditors have recommended a further increase in the level of provisions forFY1982, in the order of N2 million, to be charged against reserves andoperating results for the year. Though NBCI's arrears situation isunsatisfactory and warrants strong actions by management, the institutionstill remains creditworthy and financially viable, owing to its strong equitybase (N150 million) 2/ which far exceeds existing arrears (or even theoutstanding portfolio), and low level of long-term debts (largely Governmentloans). In order to ensure that adequate and timely measures are henceforthtaken by NBCI's management to improve loan recovery, NBCI's management has,upon the Bank's recommendation, set up a special Loan Recovery Unit andsubmitted to the Bank an acceptable plan of action for this unit, which, interalia, proposes to-

i) implement a comprehensive general accounting and controlsystem (including internal audit) to regularly monitor thestatus of collections;

1/ Exclusive of over 1000 disbursed small loans for N40 million (US$66million) under the FGN SSIC scheme.

2/ This figure is based upon recent agreement in principle by theGovernment to convert into equity N60 million of its existing loans andby the Central Bank to suscribe N40 million in cash into NBCI'sprojected equity increase.

- 15 -

ii) establish proper procedures for billings and follow-upthereof;

iii) reinforce NBCI's efforts to recover past arrears; and

iv) make recommendations to the management, in liaison with thelegal and investment departments, to initiate litigationagainst NBCI's delinquent clients from whom recovery appearsunlikely.

3.13 Profitability. NBCI's audited income statements for the years1977/78 through 1981 along with provisional 1982 accounts are summarized inAnnexes V and VI. They indicate that although there has been a significantincrease in NBCI's gross income over the past five years, (from N3.3 millionin 1977/78 to N15.3 million in 1982), NBCI's operating expenditures, andfinance charges in particular, have grown at a faster rate, resulting in asteady decline in NBCI's net income, which has dropped from a profit of N1.4million in 1977/78 to a deficit of N2.4 million in 1981. Although finalfigures for last year are not yet available, NBCI is expected to record aneven higher deficit in 1982 owing mainly to the need for making additionalprovisions against portfolio losses.

3.14 Several other factors have also contributed to the decline in NBCI'sprofitability. First, the sizeable growth in NBCI's borrowings from thegovernment (N30 million in FY 1979/80 to N142.6 million in 1982), coupled withan increase in the interest rate on these borrowings to 6X from 3% prior to1980, has significantly increased its finance charges. Second, theestablishment of several new branch offices over the past two years, with therequired growth in staff, has resulted in a substantial increase inadministrative expenses. Third, the level of interest rates charged on SMEloans by NBCI, at the government's request, (between 6-8.5%) has not allowedfor a sufficient spread on its resources. Finally, returns to NBCI on itsequity investments have been low, representing less than NO.4 million in 1982on an average portfolio of N14 million.

3.15 The projected conversion into equity of a part of borrowings from thegovernment (see para. 3.02) and the increase, as from beginning of 1983, inNBCI's lending rate to 12% should however bring about a rapid improvement inNBCI's financial performance, and, coupled with more vigilant portfoliomanagement, project supervision and collections, should enable NBCI to restoreits profitability to a satisfactory level.

3.16 Financial Condition. Despite the high level of its arrears, NBCI'sfinancial position can be considered as sound, owing largely to its strongequity base and low level of borrowings. NBCI'S total assets increased morethan threefold from 1977/78 year-end to 1982 year-end. Except for 1979 whenthere was a slight decline in total assets (-9%) from the preceding year,NBCI's total assets have grown at an average annual rate of 40%. The mainfactor for this increase has been the growth in NBCI's portfolio and itsdeposits, resulting from placements of excess liquidity arising from theperiodic injection of additional resources by the Government. The main itemsmaking up NBCI's total assets as of December 31, 1982 were (a) loans andequity investments in projects, 49%, (b) time deposits, 12%; (c) customersliabilities for guarantees, 17%; and (d) cash & bank balances, 8%.

- 16 -

3.17 NBCI's long-term investment portfolio (loans and equity) has averagedaround 60Y of total assets over the past five years, with 1982 figure being49%. After experiencing annual growth of over 50% for both 1977/78 and1978/79, NBCI's total loans and equity portfolio slowed down to a nearstandstill growth of 2% in 1979 and 1980. Since then, however, as a result ofadditional borrowings secured from the Government, the growth has resumed,with a rate of almost 60% in 1982. NBCI's long-term debt to equity (nottaking into account the projected equity increase) has consistently remainedlow, ranging from 0.4 in 1977/78 to 2.6 in 1982. The corresponding ratios oftotal debt to equity were 0.6 and 4.6 respectively. NBCI thus has asubstantial unutilized borrowing capacity, but due to its present weakportfolio and low profitability, NBCI is likely to have difficulties obtaininglong-term loans from the market at this time.

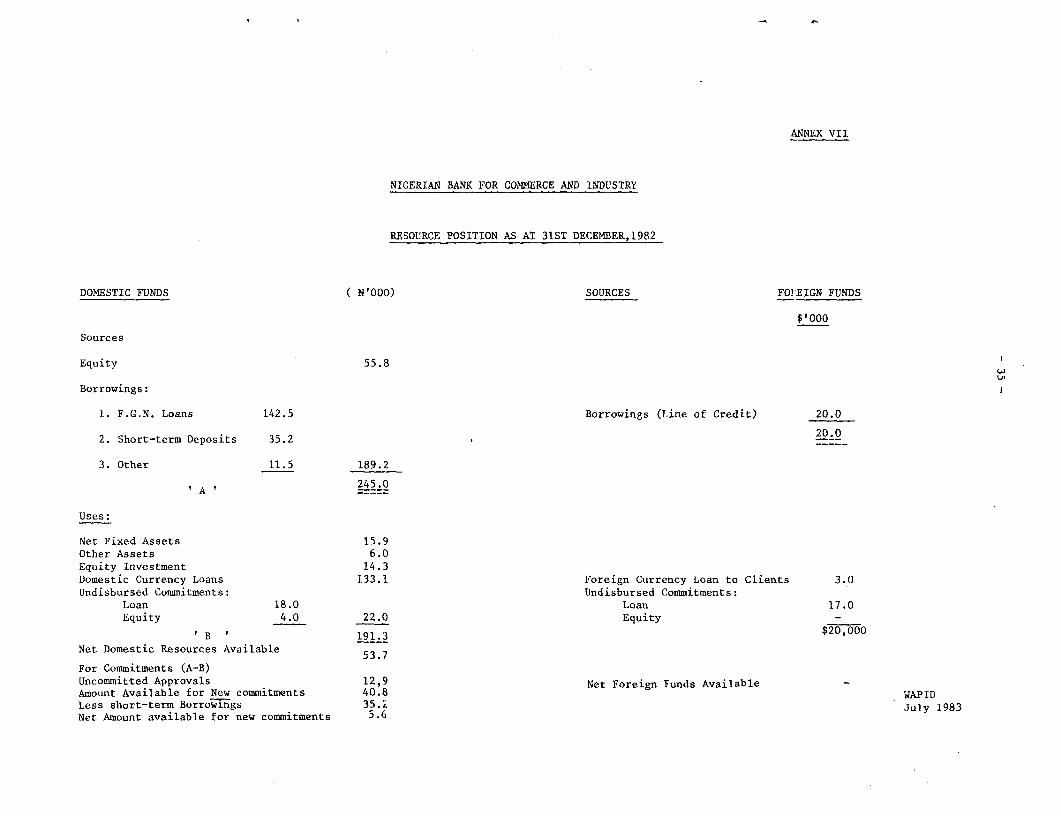

3.18 Resources. As of December 31, 1982, NBCI had a balance of about N5.6million in uncommited local currency resources. Additional N20 million long-term loans were expected to be provided by the Government during 1983, thusbringing the total of available funds for new commitments to N25 million.NBCI's long-term resources as of December 31, 1982, consisted mainly of equityin the amount of N55.8 million (24%), Government loans of N142.5 million (62%)and an export credit from Morgan Grenfell of US$20 million (6%). TheGovernment has recently decided to document properly all loans to NBCI ( whichwas not the case heretofore), and charges an interest rate of 6% p.a. on allloans made available since August 15, 1980, up from 3% on previous loans. 1/Annex VII gives a summary of NBCI's resource position as of December 31, 1982.

3.19 NBCI has had no foreign loans in the past except for the US$20million equivalent export credit from Morgan Grenfell, U.K., and has treatedall its resources, denominated in Nairas, as local currency, though theCentral Bank has provided NBCI with substantial foreign exchange for overseasprocurement. In the future, as Government resources get tighter, NBCI willhave to begin seeking long term loans on the domestic and foreign markets. Ifit is able to preserve its relatively large equity base intact, improve itsefficiency, profitability and portfolio, it might then contemplate making anentry into the market, perhaps with a Government guarantee. With NBCI'spresent large equity base and low cost government loans, there would be enoughcapacity to absorb commercial borrowing rates while keeping down its weightedaverage cost of funds, provided the Government will allow NBCI to chargerealistic interest rates to insure a reasonable spread.

1/ Funds made available to NBCI by the government for small loansunder SSIC scheme (N32.4 million as of December 31, 1982) are interestfree and would continue to remain so, even though NBCI has startedcharging its normal interest rate of 12% on such loans as against 6%previously.

- 17 -

C. Prospects

3.20 Mainly owing to oil revenues, the Nigerian economy in the medium tolong term is expected to resume its rapid growth. Its large market offers agood potential for both consumer and intermediate industrial goods.Furthermore, the Government's commitment to diversify the country's economic

base to reduce the almost total reliance upon oil revenue, should open up newareas of manufacturing activity both for the local and export markets. Todate the major beneficiary of NBCI's direct assistance, in number, has beenmedium to small-scale enterprises, accounting for approvals of about 240projects representing N85 million of NBCI's total direct assistance inaddition to over 1,000 small enterprises assisted under the SSIC scheme. Thissubgroup, which comprises mainly indigenous entrepreneurs, is expected toreceive the greatest boost from the rapidly growing economy and Government'spolicy decision to create a more favorable private investment climate.

3.21 NBCI is endeavoring to overcome its present institutional weaknessesand to develop into an effective development finance institution specializingin assistance to small- and medium-scale enterprises, thus complementing NIDB,the other financial institution operating in the industrial sector, whichconcentrates on larger industrial projects. A major objective of the projectis to assist NBCI in such endeavor. NBCI's present pipeline of projects (250in advanced stages of processing), requiring total NBCI assistance of at leastN200 million, indicates a bright operational outlook for the next two to threeyears. Using past experience, and conservatively assuming that only 40% ofthe present pipeline (100 projects representing assistance of N80 million)would be realized over the next two years, this would still represent averageannual approvals of N40 million, compared with N26 million in 1982 and N60million in 1981. This level of operations, which does not take account ofadditional lending under the SSIC scheme, is attainable by NBCI, particularlygiven the greater recognition by the Government of the potential for SMEs andthe strengthening of the project promotion and assistance capabilities of bothNBCI and the extension service agencies, proposed to be undertaken under thepresent project. Prospects for NBCI lending to SMEs in the five target pilotstates in particular are also good. Approximately 70 projects, costing lessthan Ni million each and requiring total NBCI financing of N26 million (US$ 39million) are currently undergoing processing in the branch offices withinthose states.

3.22 In the past NBCI has not prepared financial or operationalforecasts. Given its weak information base, coupled with some uncertainty inits future equity base, it is not possible to prepare, with any degree ofreliability, a set of forecasts of NBCI's operations and finances at thistime. However, this is one of the areas in which the Bank intends to be ofassistance to NBCI under this project, and by the end of the first year of theprogram, NBCI is expected to be in a position to prepare such forecasts. Inthe meantime however, through Bank's on-going discussions with NBCI, a set ofrough projections has been established, as a working document, subject tosubsequent revision, to provide some tentative indications of NBCI'S financialand operational performance in the near future.

- 18 -

IV. THE PROJECT

A. Project Background and Objectives

4.01 Background. The Bank Group has had a long standing program in theindustrial sector of Nigeria. In 1964 IFC was instrumental in therecapitalization of NIDB and has subsequently participated in 6 investments inNigeria. IFC's 25% shareholding in NIDB was sold to the Government at par in1974 for US$1.4 million. The Bank has approved four lines of credit to NIDBof US$6 million, US$10 million, US$60 million and US$120 million in 1969,1970, 1978 and 1983 respectively. A Project Performance Audit Report on thefirst two lines of credit was circulated on October 10, 1977. The reportconcluded among other points that, while NIDB itself had implemented theproject satisfactorily and had performed efficiently, the Bank's impact on thesector as a whole could have been more extensive. This report, using Nigeriaas one example, recommended the use of primary development banks such as NBCIand NIDB as apex lenders to state, local and commercial banks to stimulate theflow of long-term lending.

4.02 The Bank's first attempt to develop an SME project in Nigeria startedin 1973, when the Bank appraised a nationwide project jointly with UNIDO.Unfortunately, during negotiations the Bank and the Government were unable toagree either on means to implement the proposal or on final lending rates toborrowers, and further consideration of the loan was deferred. Subsequently,during the appraisal of NIDB in January, 1978, the Bank concluded that aneffective approach to industrial development in Nigeria would require anintegrated effort to reach both large and small firms. In practical terms,this means supplementing Bank lending to NIDB, which concentrates on assistingrelatively large industrial projects, with some other lending scheme thatwould benefit enterprises at the lower end of the industrial spectrum. Sincethen work has been carried out in Nigeria to survey the potential of, andconstraints to, SMEs. The proposed project stems from this work.

4.03 Two important considerations underlie the project design. First, thetremendous topographical diversity of Nigeria, reinforced by ethnic andlanguage differences, necessitates a decentralization of an SME credit andtechnical assistance program to the local level. This in turn requires aneffective outreach program for technical advice and credit, which can get toentrepreneurs in their places of work. Second, Nigeria is too big, theproblems of SMEs are too varied and the human constraints too great toimplement a national industrial extension and credit program in one project.Any such program must be phased over a number of years, and be initiallylimited in its geographic scope, and the present project assumes continuedfuture support to the sector by the Government and the Bank. As a firstphase, five states (Cross River, Imo, Niger, Ondo, and Plateau) have beenchosen by the Government as target states for the industrial extension andcredit program proposed under this project.

4.04 Objectives. The basic objective of the project is to develop inNigeria a core of trained manpower and an institutional structure capable ofproviding technical advice and credit to viable SMEs. To meet this objectivethe project would:

- 19 -

i) strengthen NBCI as a financial intermediary and develop itscapacity to lend to small- and medium-scale enterprises;

ii) train federal and state extension workers to improve theireffectiveness in the promotion, appraisal and supervision ofsmall- and medium-scale enterprises; and

(iii) conduct further studies to identify potential areas for small-scale enterprise development and their growth potential inorder to properly plan and focus the eventual expansion of theprogram.

The project is in an important sense a pilot effort, designed to chart the wayfor a future nationwide program. It is designed to provide practicalexperience in the difficulties of assisting SMEs in Nigeria as well asdeveloping a cadre of trained personnel to implement a national program. Theproject would be implemented over a four-year period.

B. Project Description

4.05 Main Features. The project has two major components: (1) a line ofcredit and technical assistance for institutional strengthening of NBCI and(2) a training component for federal and state level extension workers. Inaddition the project includes a small amount of funds to finance furthersector studies of the small- and medium-scale industries in Nigeria, and acomponent to refinance an advance of US$286,500, approved by the Bank underthe Project Preparation Facility, to finance the cost of initial technicalassistance to NBCI and FMI. These components are summarized below:

i) A line of credit to NBCI for financing of sound SMEs in thefive pilot states (US$35 million) and a comprehensive programof technical assistance to strengthen NBCI's effectiveness infinancial intermediation (US$1 million including US$165,000under the PPF);

ii) A US$4.3 million (including US$121,500 under the PPF)component for the Federal Mlinistry of Industries to establishan effective training program for Federal officers, staff ofIDCs and state-level extension workers, thereby developing alocal capability for technical assistance to small and mediumsize entrepreneurs;

iii) A US$0.6 million component for the Federal Ministry ofIndustries to carry out studies on the development of thesmall- and medium- scale industrial subsector, including theneed for adjustments in the investment and export incentivesand the potential for subcontracting by small NAigeriancontractors and building material producers.

Line of Credit to NBCI

4.06 Purpose. The credit component, consisting of a line of credit toNBCI of US$ 35 million, would provide term resources to Nigerian SMEs forfinancing of fixed assets and working capital in sound projects. Eligible

- 20 -

borrowers would be 100% Nigerian owned enterprises whose total assets,including existing and those proposed to be financed under the line, do notexceed Ni million (US$ 1.51 million) 1/. Other general eligibility criteriawould include (a) residency within one of the five pilot states; (b) properbusiness registration and (c) abi:Lity to provide at least 20% of owners'contribution to the total project cost. All projects financed under the lineof credit would need to have a local value added of not less than 35% and aminimum economic rate of return of 10%. Furthermore to ensure that a minimumshare of credit would reach to small scale enterprises and/or labour intensiveprojects, at least 30% of the line of credit would be earmarked forenterprises with total assets I/ not exceeding N300,000 (US$453,000) or forprojects with a cost per job of less than N7,500 (US$11,325) in 1983 constantprices. NBCI would additionally be required to incorporate a capitalintensity analysis in all its subproject appraisal reports. Subloans to berefinanced by NBCI under this line of credit are expected to average aboutUS$0.5 million, which is considerably smaller than the average size (US$2.5million) of subloans from NIDB, the other intermediary chanelling Bank fundsfor the industrial sector.

4.07 Terms and Conditions of Subloans. The line of credit would financeup to 100% of the amount of NBCI subloans subject to a ceiling of 70% of thetotal sub-project cost, the latter coefficient estimated to represent thedirect and indirect foreign exchange content of SME investments in Nigeria.Subloans would carry maturities ranging from a minimum of 4 years to a maximumof 10 years, inclusive of a grace period from 2-4 years. The average maturityof NBCI's loans to sub-borrowers is expected to be 8 years, inclusive of a 3year grace period. All subloans would be denominated in Nairas. The FGNwould assume the exchange risk witihout charging any fee to the sub-borrowers,in view of the lack of sophistication of SMEs and in line with thegovernment's objective of facilitating their access to credit at a reasonablecost.

4.08 Interest Rate. In line with NBCI's rate structure, interest ratesapplied to sub-loans under the line of credit would be at least 12% p.a. Inaddition, there would also be a front end fee of 1.5% and a commitment fee of0.75%. These charges would be adjusted in case of any increases in oradditions to the rates and fees charged by NBCI on its overall lendingoperations. The adequacy of NBCI's interest rate structure would be reviewedannually by the Government, NBCI and the Bank, taking into account the CBNGuidelines, NBCI's average cost of resources and its overall competitiveness.

4.09 Free-Limit. The first three subprojects from each of NBCI's branchesin the five pilot states would require the Bank's review prior to commitment,irrespective of their amount. Thereafter, a free limit of US$150,000 persubloan with an aggregate limit of US$ 10 million would apply. After one fullyear of operation these limits would be reviewed and adjusted as appropriate.

1/ Including working capital but not land.

- 21 -

Technical Assistance to NBCI (US$ 1 million including US$165,000 under thePPF)

4.10 To assist i4BCI in improving its institutional capabilities andparticularly in strengthening its development banking activities in the small-and medium-scale industry sector, the project would finance the foreignexchange cost of a comprehensive technical assistance program to NBCI. Thisassistance, to be provided by a suitable banking institutlon overseas engagedin similar activities and/or experienced individual advisors, would focusmainly on NBCI's small- and medium- scale industry development activities. Itwould concentrate on project lending techniques (e.g. project promotion,appraisal and supervision) while also covering other such areas as branchoperations, accounting, internal control, financial management, portfolioadministration, loan recovery and legal procedures. The program would aim atmanagerial and staff training activities through on-the-job coaching andtraining visits to similar banking institutions overseas. Implementation ofthis program is expected to span over three years and require up to 5 manyears of long term and 3 man years of short-term advisory services in additionto some 45 man/months of overseas training for NBCI staff.

Training of Extension Workers (US$4.3 million including US$121,500 under thePPF)

4.11 The training program (detailed in the project file) consists of about96 manyears of training (about 27 outside Nigeria), covering some 815participants in 63 different training sessions and courses. Although thefocus of the program would be the training of state-level extension workers inthe five pilot states, it would also include personnel of FMI, IDCs, and NBCIbranches. The training program will be administered in several phases brokendown by course content and target group. Where possible, extensive use wouldbe made of local consultants and training facilities.

4.12 Implementation of the training program will be the responsibility ofa project monitoring unit within the Small Scale Industries Division of theFederal Ministry of Industries. This unit, staffed by three full-timeNigerian officials supported by up to 48 man/months of short-term advisoryservices of three expatriate training experts, would design course curricu-a,lead courses, locate local and external training resource persons, arrange fortraining facilities and monitor course participation and attendance. A threeyear program outlining the courses by subject, duration and location has beenformulated. The courses would cover small loan management, investmentappraisal, project implementation and supervision. Courses would be geared tothe needs of specific groups and would be largely carried out in therespective places of work. Staff and facilities of the IDCs, CMD and othersuitable local training institutions would be used to the maximum extentfeasible. Adjustments to the proposed training work program would be made, asnecessary, by the project monitoring unit.

Studies

4.13 In order to lay the groundwork for the eventual expansion coverage ofthe SSE program, of which this project represents the pilot phase, it will benecessary to carry out further studies to identify potential areas for furthersmall-scale entrepreneurial development. Accordingly, an amount of US$0.6

- 22

million is earmarked to investigate the small-scale industrial subsector,including the need for adjustment in the incentives, and the present extent ofand potential for sub-contracting with particular reference to the buildingmaterials industry. The findings and recommendations of this study couldprovide important inputs into future Bank-supported operations in Nigeria.This component will be implemented by the FMI.

C. Project Costs, Financing and Onlending Arrangements

4.14 Project costs and financing. Total project costs are estimated to beUS$68.4 million including US$ 5.1 million in taxes. The foreign exchangecomponent would be US$40.5 million or 64% of the net project costs. Theproposed Bank loan of US$41 million would finance 65% of net costs, coveringfully the foreign costs and US$ 0.5 million of local costs of the trainingcomponent. 1/ Local costs of the credit component would be covered by owners'contribution and NBCI. The balance of 96% of the local costs not financed bythe Bank loan for the training component would be covered by the Government.NBCI would fully cover the local costs of its technical assistance program. Asummary breakdown of project costs and financing is provided in the followingtables:

Project Costs

Local Foreiga Taxes Total$'000 N(000) $'000 N(000) $000 N(000) $000 N(OOO)

Credit component 15,000 9,900 35,000 23,100 5,000 3,300 55,000 36,300

Training (MII) 6,722 4,436 3,765 2,485 - - 10,487 6,921

TechnicalAssistance (NBCI) 483 319 835 551 - - 1,318 870

Studies (FE) 382 252 598 394 100 66 1,080 712

P.P.F. 147 97 245 162 - - 392 259

Bank front-end fee - - 102 68 - - 102 68

Total 22,734 15,004 40,545 26,760 5,100 3,366 68,379 45,130

1/ These relate to the local costs (accomodation and subsistence) ofthe short-term expatriate training advisors.

- 23 -

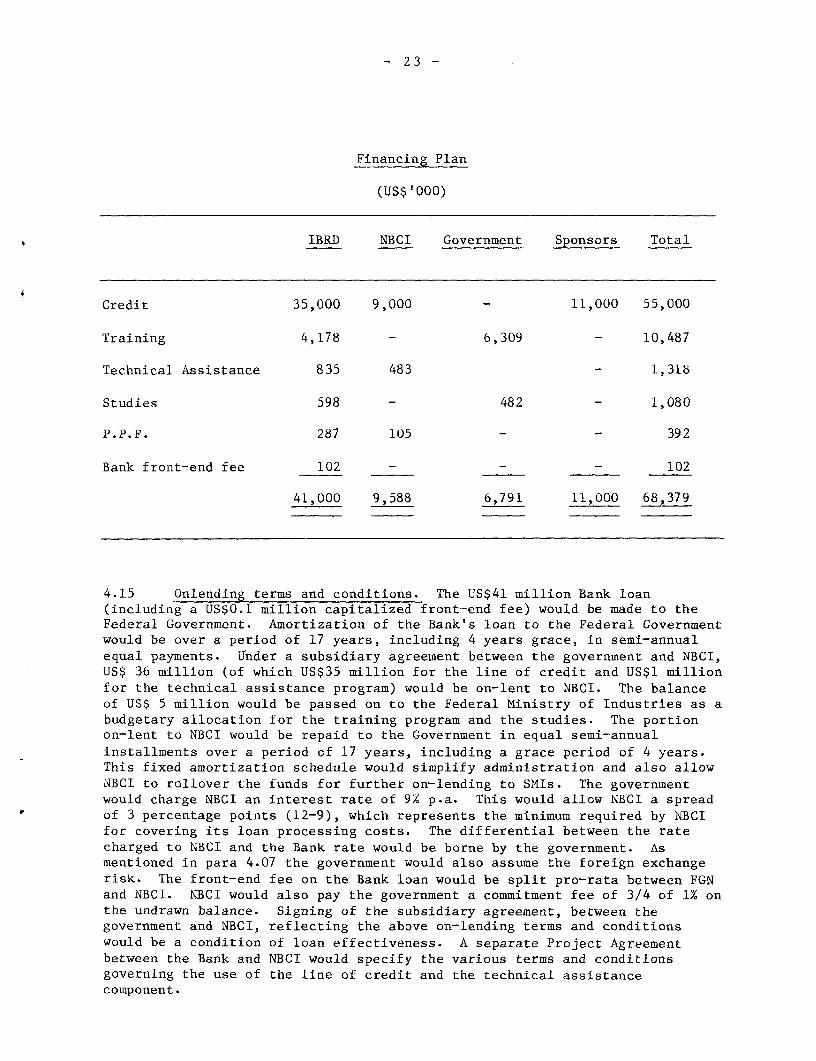

Financing Plan

(US$'000)

IBRD NBCI Government Sponsors Total

Credit 35,000 9,000 - 11,000 55,000

Training 4,178 - 6,309 - 10,487

Technical Assistance 835 483 - 1,318

Studies 598 - 482 - 1,080

P.P.F. 287 105 - - 392

Bank front-end fee 102 - - 102

41,000 9,588 6,791 11,000 68,379

4.15 Onlending terms and conditions. The US$41 million Bank loan(including a US$0.1 million capitalized front-end fee) would be made to theFederal Government. Amortization of the Bank's loan to the Federal Governmentwould be over a period of 17 years, including 4 years grace, in semi-annualequal payments. Under a subsidiary agreement between the government and NBCI,US$ 36 million (of which US$35 million for the line of credit and US$1 millionfor the technical assistance program) would be on-lent to NBCI. The balanceof US$ 5 million would be passed on to the Federal Ministry of Industries as abudgetary allocation for the training program and the studies. The portionon-lent to NBCI would be repaid to the Government in equal semi-annualinstallments over a period of 17 years, including a grace period of 4 years.This fixed amortization schedule would simplify administration and also allowNBCI to rollover the funds for further on-lending to SMIs. The governmentwould charge NBCI an interest rate of 9X p.a. This would allow NBCI a spreadof 3 percentage points (12-9), which represents the minimum required by NBCIfor covering its loan processing costs. The differential between the ratecharged to NBCI and the Bank rate would be borne by the government. Asmentioned in para 4.07 the government would also assume the foreign exchangerisk. The front-end fee on the Bank loan would be split pro-rata between FGNand NBCI. NBCI would also pay the government a commitment fee of 3/4 of 1% onthe undrawn balance. Signing of the subsidiary agreement, between thegovernment and NBCI, reflecting the above on-lending terms and conditionswould be a condition of loan effectiveness. A separate Project Agreementbetween the Bank and NBCI would specify the various terms and conditionsgoverning the use of the line of credit and the technical assistancecomponent.

- 24 -

D. Project Implementation

4.16 Monitoring. As the financial intermediary for the credit component,NBCI will be required to submit to the Bank semi annual reports on itsfinancial and operational activities. These would include standard DFCinformation including financial statements, arrears and resource positions,status of loan collections, operations (approvals, commitments,disbursements), training activities as well as annual and auditors reports.NBCI will also be required to establish and maintain a proper system, withinits branch offices in the pilot states, for collection and recording, ofrelevant data on the sub-projects financed under the line of credit. For thetraining component, FMI would be required to maintain financial recordsacceptable to the Bank and provide the Bank with semi-annual progress reportson the implementation of the training component, including advance plans forthe next six months. FMI would also maintain a tracer system of coursegraduates, in order to monitor the impact of the program and maintain aninventory of course graduates and their acquired skills.

4.17 Procurement. Procurement of equipment and goods under the creditcomponent is not suitable for international competitive bidding given therelatively small size of investments to be financed under the line of credit.NBCI's procurement guidelines are adequate, but have not in the past beenrigorously enforced. For purchases above a certain amount, these guidelinesusually require canvassing from the main sources of supply and comparison ofprice quotations from at least three suppliers. To ensure NBCI's complianceto these guidelines, which are in line with normal DFC practice, the Bank, asa part of project supervision and in addition to the subproject reviewprocess, would require NBCI to maintain detailed information on procurementprocedures followed for each subproject. Such information would beperiodically reviewed by the Bank. Procurement of services for the trainingcomponent, studies and technical assistance to NBCI would be on terms andconditions satisfactory to the Bank.

4.18 Technical Assistance to NBCI and Consultancy Services to FMI. Thequalifications and terms and conditions of employment of the advisors to NBCIand short-term consultants to FMI would be subject to the Bank approval. Atgovernment's and NBCI's request, the Bank is actively assisting in identifyingand selecting these advisors/consultants and would be monitoring theirperformance. Provision has ben made to finance a total of 5 man years of longterm and 7 man/years (including 4 man/years for the training program) ofshort-term advisory services at a total cost of US$2.4 million, includingUS$0.2 million for contingencies, of which foreign costs represent US$1.4million. The average cost of these services is expected to be the equivalentof US$16,500 per man month, local and all other costs included, of whichapproximately 50% would represent reimbursable expenses (housing, travel,transport, relocation etc.)