Embed Size (px)

Citation preview

Documewtof

The World Bank

FOIt OFFaCIAL USE ONLY

Rpat No. 11492

PROC COMLLETION REPORT

MOROCCO

FIFTH AND SIXTf AGRICULTORAI CREDIT PROJECTS(LOANS 2367-MOR AND 2731-MOR)

DECEMBE 30, 1992

MICROFICHE COPY

Report No.:11492 MOR Type: (PCR)Title: FIFTH AND SIXTH AGRICULTUfL CRIAuthor: RICE, E.B.Ext.:31755 Room:T9059 Dept.:OEDDI

Agriculture Operations DivisionCountry Department IKiddle East and North Africa Regional Office

Thi doeument has a restricktd disrib*Yo and may be used by recpients only in te pformance ofdir offci dutis Its content may not othwnvse be dicosd wthout World Bank auhorizaion.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EOUIVALENT

Curr Unit Moroccan Drn (Dh)Oh 1.00 5 US$0.12US$1.00 5 Dh 8.5

(Average C abr 1989)

GLOSSARY OF ABREVIATIONS

ADS. African Devlopmet BankAIC AgrltraI Invment CodeCLCA: Caisse Local de Cr4dl AgrkcoeCNCA Caim Nat onale de Crddit AgicoleCRCA Calsse Rgkonafe de CrdiK AgricoleEEC European Economic CommuniyFADES Arab Funds for Economic and Social DevelopmentKW Kredanstat r Wderaubau of the Federal Republic of GenrmaWMARA MlnLtmre de rAgrlcuture et du R6fomne AgraireMIS Managemn Information SysternROE Return on EquityUSAID United Stats Agency for Intrnationa Development

FISCAL YEAR

Janay 1 to December 31

WEIGHTS AND MEASURES

Metric System

FOR OFRCAL USE ONLYTHE V 'UL muN

WasngtcA D.. a43USA

Offlce of Directorz4euralOperations Evaluation

December 30, 1992

MIMORANDUM TO) IntEXEUTIV DIRECMRS AND THERSI

SUBJECT: Project Completion Report on MOROCCOFfth and Sixth Agricultural Credit ProjectsLoans 2367-MOR and 2731-MOR)

Attached is a copy of the report entitled "Project Completion Report on Morocco - Fifth andSixdh Agricultural Credit Projects (Los 2367-MOR and 2731-MOR)' prpared by the Middle Eastand North Africa Regional Office. Part II was prepared by the Borrower.

The projects achieved their primary objectives of financing on-farm investments by small andmedium scale farmers, and of strengthening CNCA as a dovelopment institution CNCA has shownInitiative with innovative programs, including a credit line for women fairmers. Its training programhas attracted international attention On the other hand, at completion of the Sixth Project, muchremained to be done to enhance CNCA's credit recoveries, financial management and resourcemobilization. On balance, both projects are rated as satisfactory and their sustainability as likely. Aseventh project is currently under implementation.

The Project Completion Report is of acceptable quality. An audit is in process.

Attachment

Tlbb doc_un be asa reed dlstbb2n ad may be asy ed Ir *pu ony X tmance of_ dhfoEIcIm due lb onets mab ot ao _hiw be dbdowd whou Wod Bak auRdwf6

FOR OFTICIAL USE ONLY

PROJECT COmPLETnON REPORT

MOROCCO

FIFtH AND SIXH AGRICULTURAL CREDIT PROJECTS(Lans 2367-MOR and 2731-MOR)

TABLE OF CONTENTS

Pare NO.

Preface ............................................................. iEvaluation Summary . ................................................... iii

L PROJECr REVIEW FROM BANK'S PERSPECflVE . . 1A. Introduction . .................................................... 1

Background . .................................................. 1Bankfinanced AgriculturalCredits .................................. 1

B. Project Fomulation .............. ............................... 2Preparation, Apprisd & Negotiations ............................... 2Project Objecives ................ .............................. 3ProjectDescription ............................................. 4

C Project Inplemnentation .............. .............................. SEffectiveness and Start-Up ........................................ S

implementation ................................................ 6Disbursements ................................................. 9Fmancial Perfornance ........................................... 10Compliance with Covenants ....................................... 12Reporting and Auditing .......................................... 14Project Inpact .................................................. 14

D. Conclusions and Lesons Lened .................................... 14

IL PROJECr REVIEW FROM BORROWER'S PERSPECTIVE ..... ........... 16

IIL STATISIICAJL INFODRUATION ......... .......... .................... 211. Projects imetable .............. ................................. 212. Cumulative Estimated and Actual Disbursements ........................ 223. Comparison Between Appraisal and Actual

Disbursements by Category of Disbursement .......................... 234. FIancialRatios . ................................................ 245. Related Bank Loans .............................................. 256. Status of Covenants .............................................. 257. Bank Resources ................. ................................ 26

Map IBRD 19570

This document has a restricted distribution and may be used by recipients only in the performnanceof their official duties. Its contents may not otherwise be disclesed without World Bank authorization.

- i -

PROlECT COMPIErlON REPORT

MOROCCO

FIFTH AND SIXTM AGRICULTURAL CREDIT PROJECTS(Loans 2367-MOR and 2731-MOR)

PREFACE

This is the Project Completion Report for the Fifth and Sixth Agricultural Credit Projects(Loans 2367-MOR and 2731-MOR, respectively) for which loans of US$115.4 million and US$120million, respectively, were approved. The Fifth Agricultural Credit Project was approved onDecember 13, 1983, signed on March 1, 1984 and became effective on May 11, 1984. The originalloan closing date was August 31, 1987, but the loan was fully disbursed on March 17, 1987, severalmonths ahead of schedule. The Sixth Agricultural Credit Project was approved on June 26, 1986,signed on September 17,1986 and became effective on December 10, 1986. The original loan closingdate was March 31, 1990 and the loan was fully disbursed in February 1990, one month ahead ofschedule.

This report was prepared by the Europe, Middle East and North Africa Region, AgriculturalOperations Division in Country Department U on the basis of information available in the Division'sand the Bank's central files: apprasal reports No 4654-MOR, dated November 22, 1983 andNo. 6094-MOR, dated May 28, 1986; supervision reports; correspondence with the Borrower:, andinternal Bank memoranda. The report is also based on the Borrower's Project Completion Reports,translated copies of which can be found in the files CNCA sent a substantial comment on thecombined PAR/PCR package that was submitted to Government in July 1992. Ihe primary letteris incorporated here as Part IL

Y Caisse N ae de CrEdit Agricole - CNCA.

-i-

PROJC COMPMEFION REPOIRT

MOROCCO

FIlTH AND SITH AGRICULTURAL CREl)T PROJECTS(Loans 2367 MOR and 2731-MOR)

EVALUATION SUMMARY

Objecdives

1. The main objectives of the Fifth and the Sixth Agricultural Credit Projects in Morocco wereto improve agricultural production by financing on-farm investments of small and medium fames,improving access of small farmers to agncultural production and strengtheming the status of CNCAas a financial and developmental institution. Mhis was to be done by: (i) emphasizing institutionalcredit penetration in rural, particularly tifed, are; (ii) introducing a new system of appraisa ofcredit needs; and (iii) emphasizing the role of CNCA as an institution which would accommodateepanding demand for credit (paras. 2.07 - 2.08).

Implementaton Experien

2 Except for some initial slowdown in lending due to a major drought in 1983P84, CNCA!'-lending for traditional agricultural activities proceeded smoothbly and disbursements e=ceeded appraisalestimates throughout the life of both projects. Progress was initially somewhat slower for the areasthat were new for CNCA, such as lending for agroindustries and for rural housing, but over the sixyears of both projects ( mid-1984 to early 1990) lending in these areas has also shown considerableprogress and disbursements matched appraisal expectations (paras. 3.03 - 3.07). On institution-building, the progress was predictably slower and overall more mixed. CNCA, the borrower, was ingeneral very receptive to using consultants where necessary, and in taking necessary action in certaininternal improvements. These include setting up agroindustrial units in branch offices in regions withhigh potential (parm. 3.04), and establishing a training program and a monitoring and evaluation unit,both of which functioned and are continuing to function effectively (paras. 3.14 - 3.15).Improvements in the management information system and in accounting procedures were slower tobe introduced (paras. 31.0 - 3.11), and the construction of branch offices and of headquarters showedthe least progress of any of the components (paras. 3.08 - 3.09).

3. Fmancial performance was good, although in the last two years, 1988 and 1989, the return onequity dropped quite sharply (from over 12 percent to 6-7 percent), due mainl to a change to astricter provisioning policy. While the financial ratios look less impressive, in fact they represent aninstitution that is in better financial shape than previously, because of adequate provisioning, as wellas representing a more honest picture of the financial situation than did the past ratios (paras. 3.18 -

- iv -

3.20). Loan recoveries were good compared to many similar agricultural credit institutions in othercountries, although they had dropped progressively from the late 1970s, when they were around 80percent, to 1986 and 1987, when they were below 65 percent. CNCA mounted a serious campaignto improve loan recoveries, and was successful in increasing recoveries to 76 percent for 1988 (paras.3.21 - 3.22). Lending interest rates remained positive in real terms throughout the life of bothprojects (para. 3.24).

4. Compliance with covenants was generally good, and reporting and auditing was satisfactory.CNCA has been audited by qualified international auditors (paras. 3.25 - 3.31).

Result

5. The impact of the two projects has been considerable. CNCA has definitely developed as aninstitution in fundamental and important ways, at the same time that the projects have had an impacton the overall financial framework within which CNCA operates (by looking at CNCA's ability tocompete, both for clients and for its own staff). The projects were successful in channeling resourcesto agriculture and in financing private investments both in this sector and in agroindustry (paras. 3.32- 3.33).

Sustalnabiity

6. To the extent that the projects introduced and supported sounder management practices andencouraged longer term planning (now being carried out under the follow up project), and to theextent that CNCA has introduced better financial management and practices, these projects have hada permanent, and therefore, sustainable, impact on delivery of agricultural credit. In addition, themethod of credit delivery has improved, CNCA has begun to diversify into new areas of profitablelending such as agroindustries and rural housing, and these aspects will better ensure the sustainabilityof CNCA as a profitable institution in a gradually liberalized financial sector.

Findings and Lessons Learned

7. The two projects both have had a positive impact on CNCA's operations and have helped tostrengthen the institution. At the same time, two lessons from these projects, which are perhaps self-evident, but which the Bank tends to lose sight of at appraisal time, are: a) the long-term nature ofinstitution building and the need to have specific, realistic goals and detailed, realistic action plansfor accomplishing these goals (para. 4.02); and b) the use of covenants to ensure specific financialratios should be based on sound accounting practices: in more general terms, the use of covenantson financial ratios cannot substitute for ensuring that an institution is financially self-sufficient(para. 4.03).

PROJECT COMPTON REORT

MOROCCO

FIFMF AND SIXTHI AGRICULTURAL CREDIT PROJECTS(Loas 2367-MOR and 2731-MOR)

PART I PROJECr REVIW FROM BANIKS PERSPEC E

A. INTRODUCrION

Backgoud

1.01 The major objectives of the Moroccan Government for the agricultural sector throughout1980s were to: (i) promote production of stapl fioods, thereby increasing self.sufficiemy, (ii) promoteexports of agricultural products; (iii) create employment opportunities in depressed rural areas,thereby decreasing regional income disparities; and (iv) encourage imestments in processing primaqcommodities which increase the value added of agricultural products At the same time, due tobudgeta,ry constraints, the Go wrment wanted to rely on prnvate sector ivetments and the bankingsstem for financing. The Fifth and the Sixth Agricultual Credit Projects were designed to addressthese objectms by providing credit to farmers and agro-industrial imestors for productive investmentsand by building up the capacity of the agricultural credit institution to deliver and recover creditefficiently.

Bank-flnned Agrictural Crei

1.02 Since 1965 the Bank has supported lending in Morocco for agricultural development througha series of loans and a credit to the Caisse Nationale de Crddit Agricole (CNCA). Four Hlies ofcredit1 have been extended to Morocco in the past with the following two-fold objectives: to buildup CNCA as a viable and effective financial institution and to finance development of the agriculturalsector. The loans and credit have been to a large extent successf in achievng both objectivesOver the years the loans were used for increasingly broader targets and became increasingly flexiblein design initiaDy restricted to the medium and larger farmers (because of differences between theBank and the Government on interest rate policies to small-scale farmers) for specifc imvestments,the loans were gradually used to finace small-scale farmers, rural cooperatives, and agro-industiesfor a broad range of investments.

1.03 During the implementation of the fist four agricultural credit projects, from 1965 through1983, CNCA improved its financial structure and developed into a financially stronger and

Y These were: year loacredit amourntnumter US$ mn

Fis Agrculral Credi Poject 1965 Ln.0433.MOR 10Second Agrcultra Credi Project 1972 Ln.0861-MOR 24

Cr.0338-MOR 10Thid Agrcuu Credit Prwoj 1977 Ln.1361-MOR 35Fourth Agriculu Crdit Proect 1979 Ln.1704-MOR 70

-2-

increasingly autonomous credit institution. Fo example, incases in Iterest rates allowed CNCAto ear a satisatory return on its portfolo; increased autonomy from the Govenmet allowedCNCA to make its own deiios on its lenadg program; improvWed internal systems for credit deliveryand monitring meant that CNCA reahd an ever-larger pportion of the farming population andbad feedback an the more successful initiatve; and increased human resource devepment (traingpr-ams) also improved credit delvery and recovey. On the Bank's insistence, CNCA began to beaudited by an.iernationally recognized audit fine Credit delivery reached .50,000 farmes undertjq Fourth Project compared to 6,000 farmers under the Frst; in 1983, with an estimated populationof famer at about 1.4 mion, this represented over 25 percent of the total number of poteidents. Furthennore, credit recovry remained at one of the highest rates for any agricultural creditinstitution supported by the BanL

1.04 Since most of the focus of previous craedit projects was on specific sub-loan and financial issues,howeve, rather tha on the overal institution, much remained to be done to stengDn CNCA!sinternal structure and systems, such as the planning capacity of CNCA, the accounting andInfomation systems, and the organitioal setup. Since CNCA was operating in a dynamic s.tor,much abo remained to be done to strengthen the lening procedures and resource mobiztionstrategy of CNCA, in order to ao t a growing clientele, and to face the challenge of acompetitive banking evironment.

B. PROJECr FORMUIATION

rp, Appa d Ne

Z01 CNCA prepared the Fifth Agricultural Credit Project, with i iput from Bank staff duringsuperision missos for the Fourth Agricultural Credit Project. Most of the components includedin the preparation were retained by the appraisal mission in Apil 1983. In addition, the apprasalmission paid particular attention to the impact of the interest rate structure on CNCA!s retr onequity, as well as to other aspects of institutional development, such as the need to develop aneffective trai progam for CNCA staff, and to instal a satisfactory data processing system and amaniagement idnmtion system. The Fifth Project differed ftom the previous ones mainly in termsof the provision for financing these elements, a more aggresive lending approach to small-scalefarmers and agro-industres, a training program for CNCA staff and, in general, a greater focus onthe o tional, financial and management issues facing CNCA as a specialzed development bank.

202 Becaue of the concem with the Agrcultual Investment Code (AIC) of Morocco, whi*reglated the pattern of subsidies for on-farm inputs and imvestments and therefore the demand forcredit fot these investments, a condition of negotiations was that the Ministry of Agriculture (MARA)submit terms of reference for a study of the AIC and a short list of consultants, and have issued thenvitations to bid to the consultants on the list. his w done, and negotiations of the Pifth Project

took place in October 1983. The files contain no further mention of this study until October 1985,when Government proposed that studies be caried out to examine only imvestments, as subsidies oninputs were in any case being phased out under an Agricultural Sector Adjustment Loan. MARAultimately proposed that a local consulting firm cr out the study, which was to be financed underanother Bank loan (LoukkIs Rural Development, Loan 1848-MOR). To date the full study has notbeen carried out. Provio were included under the Second Agrcultural Sector Adjustment Loan

-3-

(FY 88) to review a part of the AIC; in the meantime, the King of Morocco has gvein new impeWto the use of the AIC for promoting private investment and Goverment has told Bank missions thatthe AIC should be studied gradually, over a longer tem As the AIC touches vrtualy all aspects ofpublic investments and subsidies for private investments in agriculture, the Bank will need to find aiappropriate forum to deal with it.

2.03 A condition of Board presentation for the Fifth Project was that lending interest rates beineased by an average of two perentage points, which would make the inte e.t rates positive in realterms and bring them in line with lending rates of other commeral bans in Morocco. IbeGowernment did increase the rates by an average of 1.9 percentage points, which the Bank foundacceptable.

2.04 'he identificaion and preparation of the Sixth Agricultural Credit Project were undertakenin 1985 by CNCA with the assistance of Bank missions supeving the Ffth Project. The main issuesnrised during the preparation were: (a) reaching a larger number of farmers; (b) introducingcouwi a new system of credit evaluation; and (c) increasing savings mobilintion. The apprasalmission which was brought forwad by about fie months from the orina plaig so that the loawould be presented to the Board in FY 86, also &oed on: (a) chages needed in the institudonaland legal hamework within which CNCA was functioning (for example, the lack of an effective Boardof Directors to prvide guidance on strateg and policies); (b) the need to establish a medium termplan, a strateg for cmying out that plan, and operational and financial polcies; and (c) settingspecific fiancial targets to ensure the viability of CNCA and the gradual elimnatim of its onyearbonds (paying only 3 percent) which commeial bank were requhied to subscrbe to as an investmentin CNCA.

2.05 Negotiationswere centered aroundvarious fcial covenants on CNCAs financial stucureand interest rate leWs necess to achieve that stuctur In addion, howev, the Goverment

s ll ressted attempts to reduce CNCA's bonds with commercial banks by agreeing only tostudy the scope for reducing the bonds; this issue was pusued furither by the Bank in another forum(see para 328). At negotiations, CNCA did ommmit itself to inresing deposits from the curentlvel of 14 percent of total resources to at least 20 percent (noted in the minutes of negotiaticn, notin the Loan Agreement). The dicussion of the performance with respect to the various financiacovenants is in paras. 327 - 3.29.

2.06 Tle two conditions of Board presentation were: (a) a Manement Commtee be appointedwith powrs conferred on it by CNCAs Board of Diectos, satisfctoy to the Bank; and (b)Government make a first payment, in accord with a schdule of payments agreed at negotiations, forthe foreign exchange losses guaranteed by the Government and already paid by CNCA in advaceon reimbursmnent of Bank loans. These conditins were met and the Sixth Ptojec was presentedto the Board on June 26, 1986.

Project Objecte

2.07 The overall objectives of the Fifth and Sixth Agricudtural Credit Projects were in line with theGovernment objecs and the Bank strategy to assist Morocco in enhancing the impact of credit onagricultural development. Both Projects aimed at (i) improving agricultural producton by financingon-farm ivestments; (ui) improvig access of small farmers to agrcultural credit; and (iii)

-4-

streu thening CNCA's management and financial position. In addition, both Projects emphasizedCNCA's institutional development and, in principle, were to be vehicles for removing subsidies bothto CNCA and its clients (in agriculture as wel as rural housing).

2.08 The FMfth Agricultural Credit Project placed increased emphasis (compared to previousagricultural credit projects) on CNCA's internal development, and st as objectives the installationof an effective management information system and the expansion of CNCA's mobilization ofdomestic savwing The Sixth Project prt specific emphasis on increasig institutional creditpenetration in rural particularly rainfed, areas, in part by introducing a new appraal ystem of creditneeds which had been tested on a smaller scale under a rural development project. The Sixth Projectalso paid particular attention to diversifying CNCA's loan portfolio by encouraging lending in agro-industry and for rural housing, and continued to emphosize institutional development already startedduring the Fifth Agricultural Project.

Project Descrpon

2.09 The PCRs written by CNCA give an accurate description of the major components financedunder the Projects (Section IL1, pages 5-6 for the Fifth Prqject and Section ILI, pages 6-7 for theSixth). The Projects were to finance CNCA's medium and long-term agricultual lending over a six-year period, between 1983/84 and 1988/89, exluding lending to state enterpises. lhe maincomponents to be financed (percentage of total project cost represented by each category is indicatedin parentheses) were as follows:

(a) lending to Small Farmers (44 percent in each project)

(b) lending to Medium and Are Farmes (46 percent and 47 percent in the Fft andSixth Projects, respectively)

(c) lending to Agrarian Reform Cooperatives: (5 percent in the Fift)

(d) lending to Agro-industries: (4 percent in each project)

(e) lending for Construction of Rural Housing: ( 3 percent of the Sixh Project)

(f) CNCA rural branch network: (1 percent and 1.5 percent, respectively). The SixthProject also included financing for the construction of new CNCA headquarter, basedon a satisfactory finandal analysis, done by CNCA, justifying the cost.

(g) Institutional Devlopment. (0.3 percent and 0.2 percent, respectively).

2.10 Total project costs for the Ffth Project were estimated at US$601.9 million of which US$115.4,or 19 percent, were to be financed by the Bank loan, US$135.3 million, or 23 percent, were to comefrom the sub-bonowes, US$43.1 million, or 7 percent, were from Government subsidies forinvestment, US$82 million, or 14 percent, were to come from co-fianciers and US$226.2 mfflln, or38 percent, were CNCAls own resources. The conditions of effectiveness were signig by CNCA of

-5-

the ADB and first KfW loan agreements and satifactory evidence of request by the MoroccanGovernment for the FADES and second KfW loans

211 The total Project costs for the Sixth Ptoject were estimated at US$720 million of whichUS$120 million (17 percnt) were to be financed by the Bank loan, US$212 million (29 percent) wereto come fron sub-borrowers, US$101 million (14 percent) from co-financien and US$288 million (40percent) were CNCAs own resources. For the fist time under the Sixth Project, CNCA was to sharethe foreign exchange losses with the Government in accodance with a formula established by theCGoemrment under the Industrial and Trade Policy Adjustment IX Loan. Since 1986, when the SixthProject became effective, the formula has undergone successive changes to bring it closer to amarket-determined method of sharing foreign exchange risk; under the proposed Fnancial SectorDevelopment Project CNCA, along with other banks, will be paying into an exhange guarantee fundthe difference between the interest rate on its foreign bonrwings and the market-determined rateof resources in the domestic market, plus a 1 percent front-end fee charged to the end-user. BothCNCA and its sub-borowers will therefore be indifferent as to whether the source of the funds isdomestic or foreign.

212 The Fifth line of credit was to be implemented over a period of three years with theanticipated closing date of August 31, 1987 and the Sixth line over a period of three years with theanticipated closing date being March 31, 1990.

2.13 One interesting feature of the financig plan of the Fifth and Sixth Projects is the etent ofWorld Bank exposure to CNCA, which was not mentioned in either report At the time of appraisalof the Fifth Project, in 1983, the total estimated amount of World Bank loans disbursed andoutstanding was almost double that of CNCA's net worth (as reported at the end of CNCA's ficalyear for 1982). Thus was still the case at the time of appraisal of the Sixth Project in 1985 (asreported at the end of CNCA!s fiscal year for 1984)1. Whfle CNCA repayment performance to theBank was at the time of the two appraials unblemished, it would seem that this level of exposurewould have merited some discussion in both cases.

C. PROJECIr IMPLEENTATION

Efftveess ad Start-up

3.01 The Loan Agreement for the Fifth Project was signed on March 1, 1984, became effective onMay 11, 1984. The Loan Agreement for the Sixth Project was signed on September 17, 1986 andbecame effective on December 10, 1986.

This is based on the amot otsdin as o Jun 183 and Jun 1985 (data avaable frm Loan Accountingand Bow SeMvices), respi, compard to the nt woth as d the end of August 1983 and 1985 anfon the balc sheet as presented In te Staff Appraisal Repots), respectively Gn the volume and sped ofd Isements over that period, t figures on ouutnding as of the end of August would show an em gr_eWoad Bank eposr

-6-

3.02 The start-up of the Ffth Project was sdow due to problems relating to the drought. Duringthe fist four months of the Project, total sub-lending was ower than proected at appraisaL WhileCLCAN sub-lending increased by 32 percent, sub-leading decrased substantially (35 percent) forCRCAs- and Headquarters, because the drought caused medium and large famers to postponeivestments. Under the Sixth Project, the rural housng categ of subloans also suffered from slowimplementation in the beginning of the Project for a number of reasons (see para 3.03).

ImplemenltatIon

3.03 CNCA's lendi activities Except for some slowdown early in the Fifth Project due to a majordrought in 1983iB4, most sub-lending for the traditional on-farm investments proceeded at areasonable pace throughout the six years of the two projects Progress was slwer for rural housig,where the demand for credit was slower than expected in the beguming and slowed down further inthe middle of the Sixth Project - from 1986 to mid 1988, and the demand for investments in agro-industries did not grow as quickly as anticipated. For the rural housing component, the low level oflending was attnbuted in part to the imposition by the Minister of Fnance of stricter guarantees forthe mortgages and to the reduction on the subsidies on the interest rate, insisted on by the WorldBank. In fact, it was probably also due to the fact that it was a new area of lending for CNCA, andthe personnel at the branch level were not weJl prepared to handle it. In mid-1988 CNCA made aconcerted effort, howee, to redesig its lending for nural bousing in order to respond to marketdemand and to promote its lending in this area. Thee efforts included both a campaign withinCNCA at the branch level to sensitize the staff, a lowering of the lending rate for loans for low costhousing and an energetic adverting campaign to inform potential borrowers of the creit availability.The efforts were rewarded with increased lending for this component (the amount tripled from 1988to 1989), and final disbursements of the Sixth Loan were close to appraisl estimates (US$6.7 miSlionagainst an appraisal estimate of US$7.0 milion).

3.04 During the Fifth Project, an agro-industrial unit was opened in the CRCA office of Meknes-Fez (a covenant in the Loan Agreement). The unit collected about 50 sub-loan applications andcarried out a sector suvey to assess the area's agro-indusr investment potential and undertake apromotional campaign. During the Sixth Project two more agro-industrial branch offices wereestablished, one each in Casablanca and Agadir. While the pace of demand varied throughout bothprojects, the overall trend in sub-lending for this subcategory was upward, fom DH 30 milion in1983/84 to DH 44 milion by 198687 and thereafer x upward, to DR 163 millon in 1988 andDR 134 mllion in 1989. In the ,-d, disbursements matched appraisl expectatios in both the Fifthand the Sixth Projecs This was probably attributable to the patticular effort made by CNCA in thisarea.

3.05 In the Fifth Project, dibursements for CLCAsubkus somewhat exceeded appraisal estimatesand in the Sixdh Project the same was true for investments in greenhouses financed by CRCAs andHeadquarters Because of the loe coincidence of appraisal estimates and actual disbursementsacross a number of sub-loan categories (see the Borrowers PCRs, pp. 6-7 and 8-9 for the Ffth and

i CLCa Caisso local de crdd agrcolb, seAVg smar fames; CRCA = Ca s. rmonl de crd agco,sw lmr m flamn

-7-

Sixth Projects, respectively), CNCA may have exercised some discretion in determining to which ofits man lenders it would submit dbursement aim

3.06 Under the Fifth Poject disburements against subloanS for Agrarian Reform Cooperativesaccounted for only 59 percent of appraisal estimates The reasons given for the shortfall were thesame as those during the Fourth Agricultural Project: (i) some of the existing cooperatives were inarrears ith payments and hence were ineligible for additional borrowg and (ii) establishment ofnew cooperatives was suspended in 1980, pending a full review of Government's policy towards thisAgrarian Reform sector. This component was absent from the Sixth Project.

3.07 In general, the use of the World Bank loans to finace CNCA!s subloans has proceededquickly and smoothly. Ihere have been temporazy setbacks due to drought or to start up difficultieswhen lending in a new area has been involved, but CNCA has proved itself to be a higWy effectveorganization in terms of credit delivery and an efficient client in terms of the use of the Loan fundsSlower progress has been made, predictably enough, on the mstitutional development components

3.08 Construction an reabiltto of branch Under both projects, the use of the loansfor financing construction and rehabilitation of CNCAls branch offices lagged well behind appraisalestimates This seems to be due to a combination of: (a) overestimating the speed at which CNCAcoud expand from a purely logisdcal point of viev, (b) an unfortunate choice of contractors in somecases; (c) a priori control exerised by Government over CNCA!s budget expenditure; and (d) theneed to have prior World Bank approval for reladvely small investments (under the Fifth Projectprior approval was required for any onstruton costing more than US$300,000 and under the Sixththe limit was inidally US$400,000 until it was raised in mid-1988 to US$700,000, partly in an effortto expedite the program of network expansion). Towards the end of the Sixth Project, a superviionmission rcommended that a separate dqetment or service be put in charge of the construction andrehabilitation program, to avoid the dflution of responsibDities and lack of attention that hadcharacterized it up until then. By the end of both projects only a small fraction of the Loan proceeds(16 percent and 6 percent, respectvely) had been used. In an attempt to accelerate this program andin the contedt of supervision of the follow up project (National Agricultural Credit Project, Lowa3088-MOR), the Bank has recently recommended a posteriori control by Government of CNCA!sbudgetary expenditures.

3.09 Construction of new headquarters (Sixth Project). Although CNCA moved quickly in 1985and early 1986 to preselect contractors for the new headquarters, whose justification, financing anddesign had all been approvWed under the Sixth Project, CNCA decided in 1987 that the site designatedin Rabat for construction was ultimately unsuitable, and that with an upcoming change in the focusand functions of CNCA, the organiational structure of CNCA would change considerably, and thattherefore the design of the headquarters had to be rethought. As a result, nothing was done on theheadquarters for over a year; in 1988 CNCA was again ready to construct and began to seek a newsite in Rabat. Mhis took some time, and by the end of the Sixtbh Project, CNCA had obtained a siteand had a new design ready for tendering. As a result, at the end of the Sixth Loan, only 2 percentof the Loan category had been used. Fnancing for part of the cost of headquarters was included inthe follow-up prqect.

-8-

3.10 Consultants' Srices and Management Inform,aton vtr Under the Fifth Project CNCAwas to improve its MIS in two phases lTe fiMst phase, consisting of a review of the accountingsytem, was carried out by January 1985 by an internationally recruwted consuting firm Te second

phase, the design and implementation of a comprehensive electronic data proesing system (EDP),including purchase and instalation of equipment, was to be carried out by a locally recruited firmworking with the firm that had done the first phase. Disagreement between the former CNCAmanagement and the internationaly ecruited fim on disclosure of information and decentralizationof MIS resulted in the termination of the contract.

3.11 A new partnership was formed in 1985 between the local fim and a different foreign firm butlittle progress was made until after the arrival of new CNCA management in 1987. At the end ofthe Fifth loan about 60 percent of the categoly consultants' services and nothing of the category forcomputer equipment had been used. The focus of the new effort was on reorganizing CINCA,establishing medium and long-term planning focussed on deposit mobilization and agricultural lending,and then installing a decentralied EDP system through mni-computers in the branch network, andtraining of accounts and loan officers in the use of microcomputers. The report submitted in mid-1988 was not acceptable to CNCA because it was found to be incomplete in seveal areas, and it wasdecided not to pursue the issues ith the same consultants; no further work was done on planningunder the Sixth Project. Because of the delays in getting this work started, at the end of the SixthProject only about 17 percent of estimated disbursements for consulting services had been used andno purchases had been made on computer equipment (and hence no disbursements). Efforts alongthese lines have been pursued under the follow up project by requiring CNCA to provide a policystatement defining its medium term objectives (which CNCA has done) and to improve itsorganiation, MIS and accounting.

3.12 Management Committee and CNCA's Long-tem S . Under both the Fifth and SixthProjects CNCA was to develop a medium term plan and a strategy for carying out that plan, but itwas only under the Sixth Project that arrangements were formalized in terms of conditionality (forBoard presentation). An external Management Committee was set up, comprsed of seniorrepresentatives of various Ministries, to determine CNCA's policies and strategy. After newmanagement was appointed to CNCA in 1987, this concept of an external committee to determineCNCA's long-term planning was considered superfluous to the proper functioning of the Board ofDirectos Te Bank and CNCA agreed to disband the Management Committee in 1988 in favorof strengthening the Board of Directors instead to enable it to carny out the normal and appropriateBoard functions of strategy, policy mabing, overal supervision and development of CNCA's intemalmanagerial capacity. In addition, consultants were to be relied on to help the management toarticulate the longer-term planning to present to the Board for approval.

3.13 Banking Activities Development. The Fifth and the Sixdh Projects were also to formulate amedium term plan for the development of CNCA's banking activities with special emphasis on thepromotion and development of savings deposits. This aspect of institutional development was ofcontinuous concem to appraisal and supervision missions, because of the importance for CNCA toincrease its domestic resource base and to rely less on external sources of fuding. During the FifthProject, CNCA linked resource moblization to an improved information system. As a result, thedelays in implementing the MIS meant that no work was done on it. During the Sixth Project, withthe arrival of new management, this became a higher priority, but was still associated with developing

-9g

a long term plan and strategy for CNCA's future, and implementation invohled developingprocedures, staff training, and a concerted promotional campaign. While some progress was madeon this, in that domestic deposits grew from Dh 715 million in 1984 to 1,751 million in 1989, liabilitiesgrew faster, so that as a proportion of total liabilities (excluding equity), deposits shrank from 19percent to about 16 percent over this same period (the minutes of negotiations for the Sixth Projectspecified a target for deposits of 20 percent of total resources)0'. This remains a priority under thefollow up project.Y

3.14 Training Program. Throughout both projects, training took on increasing importance andbecame a regular feature of employment in CNCA. Given the lack of attention often given totraining, this is a considerable achievement. Under the Fifth Project, CNCA was required under theLoan Agreement to produce a training program, which it did by planning a program on: (i) new creditand banking procedures; (ii) use of newly computerized system; and (iii) project anabsis of largerprojects for a Limited number of staff According to the files, CNCA did carry out a 30-week internaltraining program on a part of this program which covered general accounting and the use ofmicrocomputers, benefitting about 430 professionals. Under the Sixth Project, the training programsin various activities (agro-industries, loan rcoveries, accounting, computer system, bankdng activities)were prepared and carried out for continuous in-service training. CNCA currently has an active in-service training program covering many areas of CNCA!s banking activities. Later supervision reports(from 1988 onwards) pointed out the need to coordinate CNCA's training program wnth the long-term planning and strategy being put in place.

3.15 Moitoring and Evaluation. As stipulated in the Loan Agreement under the Fifth Project, amonitoring and evaluation (M and E) unit was created in CNCA in May 1984 and becameoperational in 1985. Based on farm surveys, the unit: (a) monitored the use of CNCA funds bybeneficiaries; (b) calculated at least financial benefits of subloans; whether the unit also calculatedcosts and benefits in economic terms is not clear; (c) surveyed current and potential CNCA customersfor their views on present lendmg procedures, organization and lending potential and Umits. The firstsurvey was carried out in 1985. About 5 percent of medium and long-term clients were surveyed inthe North West regions and the results of the survey indicated that the objectives set under the creditline were generally being achieved. It was decided that M and E services would be extended to otherareas of the country and a computer managed data bank would be established to increase theusefulness of feedback information for CNCA's lending activities. This is being continued on anational scale under the follow-up project.

Disbursements

3.16 Unlike most Bank projects, throughout most of the life of both projects, disbursements* exceeded appraisal estimates (Annex 1, Tables 1 and 2) They were both fully disbursed and final

E n equity is Included, ftn deposts decreased from 16.3% in 1984 to 14.7% in 1989.

Y Another aspect constraining deposit mobilization was the fact that CNCA has not been allowed to mobUiizedeposks in urban areas, this being the domain of the commerci banks. This issue was not fiubl discussed untlthe follow up prolect and is now being dealt wfith under the Financiai Sector Development Project

- 10-

disbursements took place m both cases ahead of original closing dates The actual and estimateddisbursements for both Project periods, over time and by category of disbursements, are in Annexes1 and 2, respectively. Under the Fifth Project, retroactive financing was allowed for US$11 milion(10 percent of total loan amount) and disbursement percentags were increased twice. The Bankaccepted the requests on the grounds that because of delays in Loan effectiveness, cofinancing fundshad been used and were now exhausted, demand for farm investment was higher than expected dueto Government liberalzation measures, certain categories (computer equipment and technicalassistance) were not being used because of initial difficulties with consultants, and the funds forcompletion of activities under these categories were provided for under the Sixth Project. Under theSixth Project retroactive financing was also included for US$12 million (10 percent of total loanamount).

3.17 On the request of CNCA management and the Ministry of Fnance, a Special Account wascreated in July 1985 (Fifth Project). The account was kept in Dirhams which was an exception tonormal Bank practice; it was allowed because the funds credited to the CNCA account representedthe Dirham equivalent of foreign curreny already spent to pay for imported agricultural equipmentpurched by project beneficiaries and because CNCA did not assume the foreign exchange riskunder the Fifth Project. Under the Sixth Project, provisions were included for a Special Acowunt andthe authorized amount was later doubled in size on the request of the CNCA. In spite of this, theSpecia Account under the Sixth Project was never actually established because in the event CNCAwas able to pre-finance the expenditures

Financal PerformIace

3.18 Over the six fiscal years of the two projects (1983/84-89), the financial position of CNCAcontinued to be generaly satisfactory. During this time, CNCA's role continued to grow rapidly asthe principal financial institution to provide funds to the agricultural sector and the only one financingsmall farmers' credit needs From 1984 to 1989, CNCA's total assets increased almost three-fold fromDIH 4.4 billion to DH 11.9 billion (while cumulative inflation was 43 percent for the same period,varying from 87 percent to 2.7 percent per year, assets in real terms virtually doubled). This growthwas financed primarily through long-term lending by external agencies, whfle domestic resourcemobilization was lower than expected (see par. 3.13).

3.19 In spite of the statements and figures in CNCA's PCR showing that CNCA had respected allthe financial covenants (up through 1987; figures are not available in CNCAWs PCR for 1988 and1989), this report found that it was mixed. Calculations and ratios are in Annex 3. Under bothProjects, the liquidity ratio was to remain at or above 1.2. Between 1985 and 1987 it was slightlybelow 1.1. Since 1988 it has been above 1.5. Under the Fifth Project the (long-term) debt to equityratio was to be no greater than 6:1. It was above this figure for 1985 and 1986. Under the SixthProject the ratio was increased to &1 and CNCA was able to stay within this limit for 1987 - 1989.Fnally, the Fifth Project specified in the appraisal report and reflected in the legal documents(Supplemental Letter) that the return on equity (ROE) was to be at east 10 percent for 1985 and12 percent thereafter. Under the Sixth Project, the appraisal report specified, as did a covenant inthe Loan Agreement, that the ROE was to be at least 12 percent. In fact, CNCA's ROE wascomfortably above 12 percent until 1988, when it dropped to about 6 percent (as loan loss provisions

- 11 -

increased considerably, thereby reducing net income, and CNCA profits became taxable), and 1989,when it was 7.4 percent.

3.20 In spite of the high rates of return eamed in 1985 - 1987, however, an audit of CNCA by aninternationally e ized auditing firm in 1986 questioned the adequacy of the provisions given theloan portfolio. In 1987, CNCA agreed to study careflly its provisioning policy, and the result wasa change to a much stricter approach which was announced in a policy statement in 1989 and maderetroactive to 1988 As early as mid-1988, it was predicted by World Bank missions that the returnon equity would decrease as a result of this. Net income (before tax) did indeed drop considerably,from about DH 87 mfllion in 1987 to DH 52 million in 1988 CNCA has further improvements tomake in its accounting practices, such as the introduction of a policy on non-accrual of interest onpast due loans, and this, combined with the recent reforms on provisioning policy and theintroduction of a corporate income tax that increases the incentive to reduce net income (CNCAdoes not distribute dividends), means that there is likely to be a more modest return on equity in thefuture, but a sounder financial structure. CNCA has nevertheless set itself a target (speiled out inits policy statement) of achieving a return on equity at least equal to the domestic inflation rate, andthis is an entirely reasonable objective.

3.21 L c . CNCA loan recoveries during the project implementation perods were goodcompared to other agriultural credit banks in both developing and industrialized countries.However, due to unfavorable weather conditions, there was a gradual decline in recoveryperformance; the rate fell from 80 percent during the Fourth Agricultural Credit Project (1979-82)to some 65-70 percent between 1983 and 1985, and eventually to below 65 percent in 1986 and 1987.During the Fifth Project, around 1985, some rescheduling became possible with extemal funds fromEEC (US$20 M), the USAID (US$13.5 M) and CNCA's own resources (US$7 M); loans wererescheduled over a ten year period to accommodate about 70 percent of CNCAs arreams Of this,EEC and USAID contnbutions were used to assist small farmers with less than DH 6,000 of fiscalincome.

3.22 As a result of the declining trend in recovery rates, CNCA made a concerted effort towardsthe middle of the Sixth Project (in 1988) to improve them, piaril by sensitzing CNCA staff tofollow up on reimbursements. In addition, CNCA changed its fical year in 1988, to run from Januaryto December and thus coincide better with the lending cycle (with an end of the fiscal year formerlyin August, loan recovenes looked quite lovr, by December they had usually increased appreciably).Loan recoveries improved in 1988 to 76 percent, and remained at that level in 1989 and 1990 (75percent and 76 percent, respetively).

3.23 In summary on the financial performance, it is important to distinguish CNCA's financial healthand soundness of accountig practices from its ability to meet the financial covenants of World BankLoan Agreements. Particularly under the Sixth Project, CNCA made important progress in improvingits provisioning policies, as well as undertakng a concerted effort to increase loan recoveries As aresult, it is a stronger financial institution today than when it was showing a 12 percent or 13 percentROE. Tis argues for focussing on policies and procedures as well as on financial ratios to ensurelonger term financial health.

- 12-

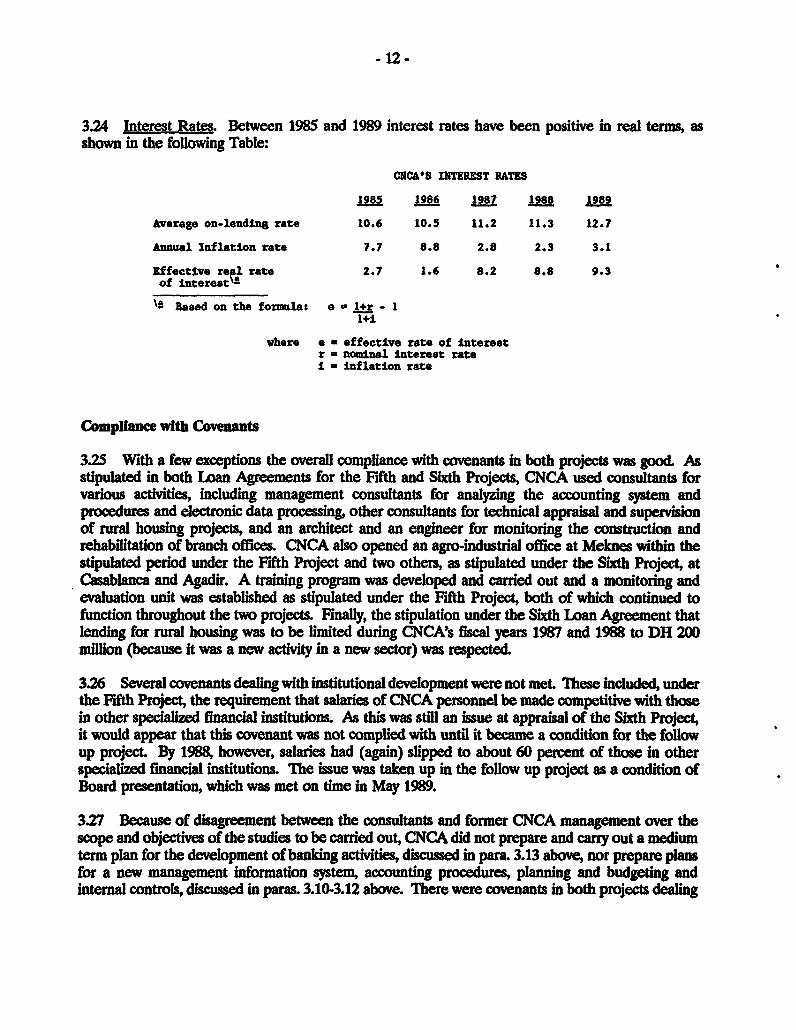

3.24 Interest Rates. Between 1985 and 1989 interest rates have been positive in real terms, asshown in the following Table:

CNCA'S INTEREST RATES

1985 1986 1987 1988 1989

Average on-lenditg rate 10.6 10.5 11.2 11.3 12.7

Annual Inflation rate 7.7 8.8 2.8 2.3 3.1

Effective re 4 rate 2.7 1.6 8.2 8.8 9.3of interest '

'l Based on the fomd as e - l+r - 11+i

where e a effective rate of interestr - nominal Interest ratei - inflation rate

CompLHnce with Cove=na

32S With a few exceptions the overall compliance with covenants in both projects was good. Asstipulated in both Loan Agreements for the Fifth and Sixth Projects, CNCA used consultants forvarious acthivties, including management consultants for analyzing the accounting system andprocedus and electronic data processing, other consultants for technical appraial and supervisionof rural housing projects, and an architect and an engineer for monitoring the construction andrehabilitation of branch offices CNCA also opened an agro-industrial office at Mecknes wthin thestipulated period under the Fifth Project and two others, as stipulated under the Sixth Project, atCasablanca and Agadir. A training program was developed and carried out and a monitoring andevaluation unit was established as stipulated under the Fifth Project, both of which continued tofunction throughout the two projects. Fmally, the stipulation under the Sicth Loan Agreement thatlending for rural housing was to be limited during CNCA's fiscal years 1987 and 1988 to DR 200million (because it was a new activity in a new sector) was respected.

3.26 Several covenants dealing with institutional development were not met These included, underthe Fifth Project, the requirement that salaries of CNCA personnel be made competitive with thosein other specialized financial institutions. As this was still an issue at appraisal of the Sixth Project,it would appear that this covenant was not complied with until it became a condition for the followup project By 1988, however, salaries had (again) slipped to about 60 percent of those in otherspecialized finandal institutions. The issue was taken up in the follow up project as a condition ofBoard presentation, which was met on time in May 1989.

3.27 Because of disagreement between the consultants and former CNCA management over thescope and objectives of the studies to be carried out, CNCA did not prepare and carny out a mediumterm plan for the development of banking activities, discussed in param 3.13 above, nor prepare plansfor a new management information system, accounting procedures, planning and budgeting andinternal controls, discussed in paras 3.10-3.12 above. There were covenants in both projects dealing

- 13 -

with these issues. Finally, under the Sixth Project, the Management Committee that was to take anactive role in determining many organizational and operational issues never fulfilled its function asdiscussed in para. 3.12 and this idea was ultimately abandoned (and the Loan Agreement amendedaccordingly).

3.28 Compliance with Financial Covenants. As discussed in para. 3.19, compliance with thecovenants on financial ratios was mixed, although CNCAs fnancial performance should be consideredgenerally good. In addition, CNCA and the Government did keep interest rates positive in real terms(para. 3.24), as specified under the Sixth Loan Agreement. There were other financial covenantswhich were either girt met or not monitored. For example, under the both the Fifth and the SixthProjects, CNCA's lending or other financial participation for any one investment was limited to 20percent of CNCKs equity. While external auditors presumably would have flagged any particularproblem in this area, there is no mention in the files that this covenant was ever monitored by theBank. CNCA was to ensure that full costs of operating CLCAs, the branches serving the poorerclients, were covered by the lending interest rates. There is no specific mention in the files as towhether this was accomplished, although CNCA did develop an accounting system that allowed it toaccount for CLCAs' operations separately.

3.29 The covenant in the Sixth Loan Agreement (Section 4.10) regarding one-year bonds was notcomplied with; CNCA was to complete a study by June 30, 1987 on the scope for gradual eliminationof CNCA bonds to which commercial banks were required to subscnrbe at below market rates. Theintention was to encourage CNCA to mobilize other domestic resources to replace the bonds. AsCNCA did not make significant progress on mobilizing other domestic resources for reasons discussedin para. 3.13, CNCA did not carny out the study. The Bank has continued to press for reduction inthe obligatory subscription to these bonds; with the gradual liberalization of the banling system, theBank has made new proposals for all spealized financial institutions, including CNCA, under theproposed financial sector development loan. In addition, CNCA was to establish and maintain aseparate account to which it would credit each year an amount equal to 1 percent of its outstandingbonds for covering losses resulting from the failure of its borrowers to repay their loans because ofnatural calamities. This account was created to ensure adequate loan loss provision pending thedevelopment of improved general financial policies, but upon CNCA's request the Bank agreed tochange this requirement as being an inappropriate way to deal with the issue (the Loan Agreementwas amended accordingly). Under the follow up project, CNCA has adopted significantly improvedloan loss provisioning policies and procedures (see para. 3.20) and the establishment of a Guaranteefund for natural disasters is currently under study.

3.30 Compliance with Guarantee Agreements. Most of the covenants of both GuaranteeAgreements concerned ensuring that CNCA would be able to honor its commitments under "%e LoanAgreements (for example, on interest rates or salary structure). To the extent that CNCA met itsconditions, it can be said that Government compliance was also satisfactory. One area which wasproblematic throughout both projects concerns Government obligation to reimburse CNCA in atimely manner for its share of the foreign exchange losses incurred on foreign debt reimbursementsthat CNCA paid on behalf of Government. While Government did settle its 1986 and 1987 foreignexchange arrears to CNCA in July 1988 with five-year Treasury bonds at 6 percent and its 1988arrears in a similar way in April 1989, this has created problems of liquidity for CNCA.

-14 -

Rqportig ad Auditing

331 CNCA submitted to the Bank regular semi-annual reports including detailed data on its lendingactivities by category and maturity, credit recovery, financial situation, and progress achieved in theimplementation of its institution building activities. External audit reports were prepared by aqualified independent priate auditor and were submitted to the Bank annually and in a timelyfashion.

Project Impact

3.32 The Fifth Project proposed to improve the living standards of about 580,000 farm families andcreate some 78,600 manyears of rural employment. Under the Sixth Project around 520,000 familieswere projected to be direct beneficiaries and about 50,600 man-years of rural employment would becreated. It is not clear from the fMies why CNCA expected a decrease in the number of its borrowersbetween the Ffth and the Sxth Loans. However, neither CNCA's own PCRs nor project filesprovide information as to the impact of these projects in terms of the number of beneficiaries andemployment. According to the follow-up project, about W85,000' farmers had been reached by1987; this represents an increase of 30 percent over the estimated 450,000 clients reached in 1982.

333 On the institutional side, the impact of the two projects has been considerable. Combined withnew and more receptive management, CNCA has evolved considerably in terms of its internalprocedures, accounting practices, organizational structure, recognition of the need for long termplanning and strategy, training prgrams; in terms of its actvities, it has considerably expanded thewope of its lending to cover agro-industres and ruraa housing and is continuing to explore otherareas for lending under the follow-up project. Continual Bank presence and intervention should takeat least part of the credit for these developments.

D. CONCLUSIONS AND LESSONS LEARNED

4.01 Overall, the Fifth and the Sixth Projects were successful both in terms of delvering credit toan impressive number and proportion of the agricultural population, at unsubsidized interest rates,and in terms of progress made in the development of a specialized financial institution. While someof the specific covenants were not met, CNCA was, at the end of the two projects, institutionalstronger in financial and managerial terms than it had been at the beginning.

4.02 CNCA"s overall record is good, and from 1984 to 1987, progress was made on: (a) introducinga management information system and improving the accounting procedures to show a more accuratepicture of the financial situation; (b) introducing and expanding internal training which had directresults in, among other things, improvnmg credit delivesy in new areas and in loan recovery; (c)beginning the process of decentralization, which increased efficiency, and (d) improving the lendingcriteria so as to facilitate credit delivery and reach a larger number of farmers In most areas,however, these developments were slower than expected until around end-1987 and in some areas,little progress was made. These include direct deposit mobilization and constructon of new branches.

d' Includt women farmers and aitisans and cint reahed though Agrarin Reform CooPeraiesand ORMVA.

The limited success of these components can be attributed to: (a) their ambitious and long-termnature; (b) lack of a wel defined plan of implementation; and (c) administrative constraints imposedby Government. These activities are now being undertaken (with increasing success with respect todeposit mobilization) during the follow-up National Agricultural Credit Project.

4.03 Measuring CNCA!s financial situation only in terms of the ratios used during the two projects,it appears that its profitability, for example, worsened, as CNCA's return on equity dropped from 12-13 percent to 6-7 percent. CNCA had, however, improved its financial management and changed itsaccounting practices so that CNCA now has in place more prudent accounting pracdtes and thefinancial statements reflect a more soundly managed institution (in particular, there is more adequateprovisioning for loan losses than in the past). One of the lessons of this exercise is that definingfinancial ratios in legal documents without also having good financial management and accountngpractices is not very useful for ensuring financial health and long-term viability.

4.04 Although CNCA has grown rapidly into one of the largest and most important financilinstitutions in Morocco, both its management and its structure must be modernized in order tocontinue to operate effectively in the future and to evolve towards fullservice banking. By the endof 1987, CNCA had grown rapidly (with a clientele numbering over 700,000), and was suffering fromthe consequences of this rapid growth CNCA now must face the challenge of servicing an ever-increasing clientele in an increasingly competitive financial sector environment, and is responding toit by introducing reforms following the decision to transform CNCA into a universal banL Thesemajor institutional reforms are currently being carried out under the National Agricultural CreditProject (Loan 3088-MOR).

4.05 In many respects, CNCA continues to be a successful example of an agricultural credit banLTbis accomplishment, due in part to continued Bank assistance as weU as to excellent leaderipwithin CNCA itself and to Government support in certain areas, and in spite of the restrictions underwhich it has operated, should not be underestimated. It is currently one of the few examples ofsuccessful agricultural credit institutions with which the Bank is associated. CNCA has in the pastenjoyed justifiable grants and concessionaire funds, which are not available to other banks that donot work in agriculture, for rescheduling loans in arrears due to bad weather; CNCA has alsoobtained a portion (12-13 percent in 1986/87) of its resources at below-market cost. These resourceshave enabled CNCA to undertake the costly and risky business of senvng small farmers under adverseclimatic conditions. CNCA has simflarly operated under considerable constraints, such as a prioricontrol and an interdiction on mobilizing deposits in urban areas. Now that CNCA is on reasonablysound footing, the Bank, the Moroccan Govenment and CNCA are moving towards establishing anundistorted, competitive financial sector environment and are in the prooess of removing the existingdistortions in the farm credit system. It is important to recognize, however, the special conditionsprevaiing in agricultural lending, which make it imperative to provide some sort of financial safetynet to either farmers or to the financial institution(s) lending to farmers (provided, of course, thatsuch a safety net is transparent). The success of CNCA to date is testimony to this fact.

- 16 -

PART Un PROJECT REVIEW FROM BORROWER'S PERSPECTIVE

In addition to the two PCRs prepared by CNCA, retained in Bank files, CNCA submitted asubstantial comment on the PARJPCR package sent to< Government in uiy 1992. The CNCAcomment includes a primaty letter, included here, and an annex, which refers to PAR paragraphs andis attached to the PAR but not included here. In the following letter, reference on the first page toparagraphs numbers and the Subsidy Dependence Index are also directed at the PAR.

- 17 -

TRANSLATION

KINGDOM OF MOROCCOCREDIT AGRICOLE

gneral Director

N 547/92/DG Rabat, October 1, 1992

Mr. Graham Donaldson, ChiefOperations Evaluation DepartmentInternational Bank forReconstrction and Development1818 H Street N.W.Washington DC 20433

U.SA

Dear Mr. Donaldson:

In reply to your letter of July 22, 1922 enclosing the preliminary evaluation report onthe fifth and sixth Agricultural Credit projects, I am sending you herewith my remarks on the contentsof that document.

I should like first of all to congratulate the team of experts who produced the evaluationin question on the fine quality of the work and the distinct highlighting of the development prospectsfor Credit Agricole in spite of the particularly difficult situation which beset the 1991-1992 crop year.

The first group of my comments has to do with the congruence of the figures: thatsubject is addressed in a detailed note attached to this letter.

In examining the conclusions of the report, I shall confine my remarks to the topics offinancial results (4.3), the settlement of arrears (4.9), the exchange risk (4.11) and, finally, the futureof Credit Agricole (4.15)

1. Financial Performance

Before tackling this subject, I think it is important to note that the CNCA had, at theappropriate time, already conveyed to the experts responsible for the evaluation the limitations ofthe Jacob Yaron model for calculating the degree of dependence on subsidies. Since very little time

-18-

was available for the experts to apply the model to Credit Agricole, it had been decided to take thisquestion up with the model's author himself in the course of July 1992.

While awaiting the adaptation of the Subsidy Dependence Index (SDI) to the specificcase of CNCA (since Mr. Jacob Yamn was unable to keep the July appointment because of otherengagements), judgment on the subsidy amoun.s estimated by the esaluation mission (see paragraph3.17) should be reserved.

Moreover, as noted in the report, Credit Agricole today as in a more solid financialposition than in the past, thans to a stronger policy for setting up reserves for bad debts-one thatis better able to cope with the risks facing the agricultural sector. It should be noted in thisconnection that our external auditors have-for the first time-stated that the reserves set up in 1990were adequate, taking into account the risks inherent in the agricultural sector.

In my opinion, however, strengthening of this financial structure is not achieved solelyby raising interest rates, but also-and most importantly-by the establishment of a guarantee fund asinsurance against natural disasters in order to protect the institution from other than banking risks.

2 The Settlement of Past Due Accounts

The mission was able to observe the importance the CNCA assigns to the settlement ofoverdue fincial obligations and the impressive efforts expended by Credit Agricole to resolve thatsituation. It was also in this context, and due to the drought experienced in the 1991-92 crop year-the adverse impact of which had been noted by the experts-that steps were taken to clean up thearrears situation and ease the farmers' debt burden.

To that end, it was decided to cancel the late payment charges for debtors who pay theamounts owed within the allotted period, and to grant rescheduled loans to the farmers who pay offpart of their dues.

I should like to point out, along the same lines, that the statistics presented by theCNCA reflect the account ledgers; and that inconsistencies noted by the evaluation mission stem froma oonfusion between the recvery rate on current maturities for the fiscal year and the rate on allaccounts payable, including those for earlier coliection periods.

Generally speaking the results posted as a result of the 1985 rescheduling have beensatisfactory, when the region in question has experienced successful crop years in the wake of thatoperation.

The analysis of previous overdue accounts should have taken into account the regionalconcentration of such arrears. Three regions (the east, Haouz and the south) were chronically besetby disasters throughout the 1980s and at the start of the 90s, and they account for more than 70%of the entire CNCA arrearages. This is why the development of Credit Agricole in those regionsmust include more widely diversified activities and risks, as well as the establishment of a guaranteefund for protection against natural disasters.

-19-

3. Mtem for Cveraue of Exchane Risk

According to the simulation exercises conducted, application of the new exchange riskcoverage system to external loans contracted by the CNCA will boost the interest rate by three tofour points This increase would jeopardize the profitability of the projects financed, and it willundoubtedly have an adverse effect on loan recoveries.

While awaiting the implementation of specific financial mechansms to cover exchangerislcs, it is eminently desirable to continue using the exchange coverage system negotiated in May1989, (which was approved by the World Bank), for the new lines of credit that the CNCA hopes tomobilize in 1993.

4. The Future of Credit Agricole

Originally a financial institution specializing in funding for agrculture, the CNCA hasnow begun to diversify its activities so that it wil gradually become a universal bank for service to therural community and, eventually, a bank that is able to provide its customers with all categories ofbanking services.

That long and difficult process calls for an evolution strategy tailored to the country'sspecific needs as well as to its economic and social situation.

The efforts deployed since 1987 are aimed at strengthening the institution's financialstructure, cleaning up previous arrears, diversiing financing to spread the risks; actively attractsavings deposits; strenw then the branch network; enhance the reliability of management control tools;and imest in the training of Credit Agricole's managers, professional staff and agents.

Tbis new strategy also calls for instituting basic reforms needed to meet the competition,which has become increasingly evident since the departitioning decreed by the monetary authoritiesin 1991.

What are those necessary reforms?

* Frst and foremost, revision of the text of the law governing Credit Agricole to adaptit to the reality of the nationwide financial sector reform and the changes in thenational economy.

* In addition, the establishment of a Guarantee Fund to cover Natural Disasters.

* And finally, completion of the reforms currently in progress, covering administrative,accounting and data processing procedures, implementation of a mamagementinformation system, and upgrading of the services offered by the Credit Agricole.

Only when all of these prerequisites have been met and Credit Agricole's public servicerole as the source of financing for small farmers has been established-with all the associated

- 20 -

implication in regard to the mobilization of stable concessional resources-only then can wecontemplate the participation of commercial banks in the development of rural financial markets.

Tbere you have some observations I wanted to contnbute to the important evaluationreport which reviews almost eight years of Credit Agricole activity (1983-1990).

To conclude, I would like once more to assure you of the need to take into account andsupport the strategy now being implemented to mobilize the means required for its complete success,without undue haste, in the knowledge that the most important mission of Credit Agricole will ahvwaysbe to make an effective contribution to improve living conditions for farmers and the rural populationby sponsoring productive and profitable investments.

Thank you again for your cooperation and for the World Bank's ongoing assistance toCredit Agricole.

Please accept. Sir, the assurances of my highest consideration.

M. Rachid Haddaoui,Director General

-21 -

PART mI: STATISTICAL INFORMATION

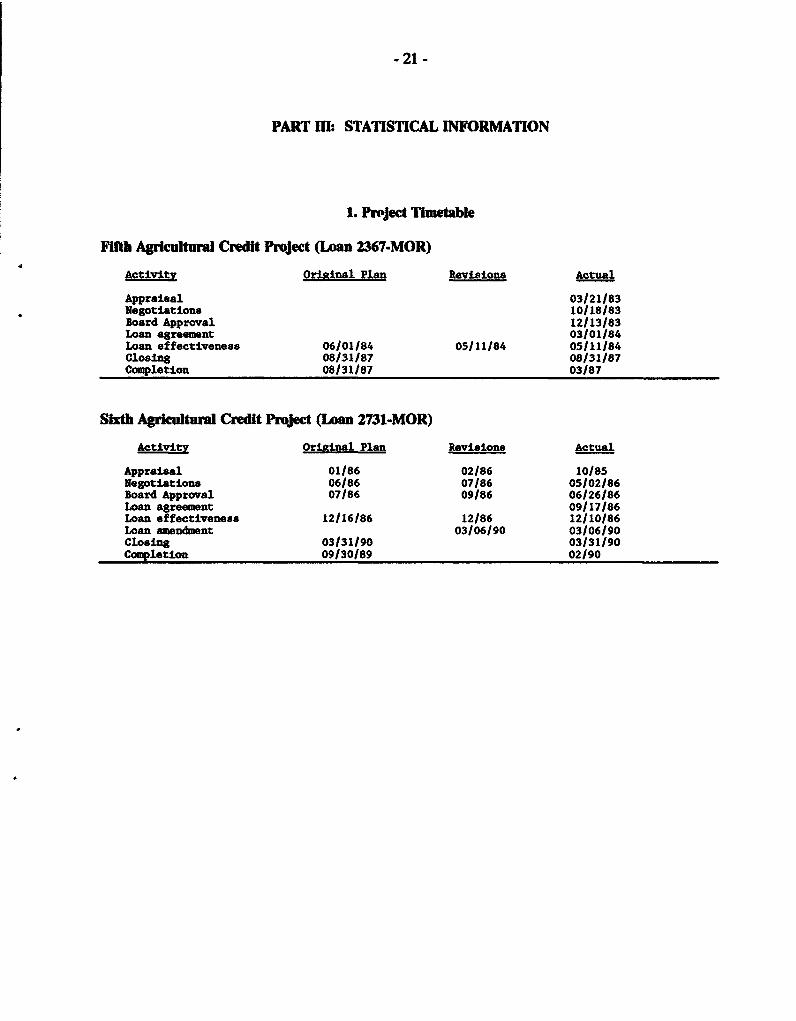

1. Prject Timetable

ifth Agricultural Credit Project (Loan 2367-MOR)

Activitv Orilinal Plan Revisions Actual

Appraisal 03/21/83Negotiations 10/18/83Board Approval 12/13/83Loan agreement 03/01/84Loan effectiveness 06/01/84 05/11/84 05/11/84Closing 08/31/87 08/31/87Completion 08/31/87 03/87

Sixth Agricultural Credit Project (Loan 2731-MOR)

Activity Ori-inal Plan Revisions Actual

Appraisal 01/86 02/86 10/85Negotiations 06/86 07/86 05/02/86Board Approval 07/86 09/86 06/26/86Loan agreement 09/17/86Loan effectiveness 12/16/86 12/86 12/10/86Loan amendment 03/06/90 03106/90Closing 03/31/90 03/31/90Completion 09/30/89 02/90

-22-

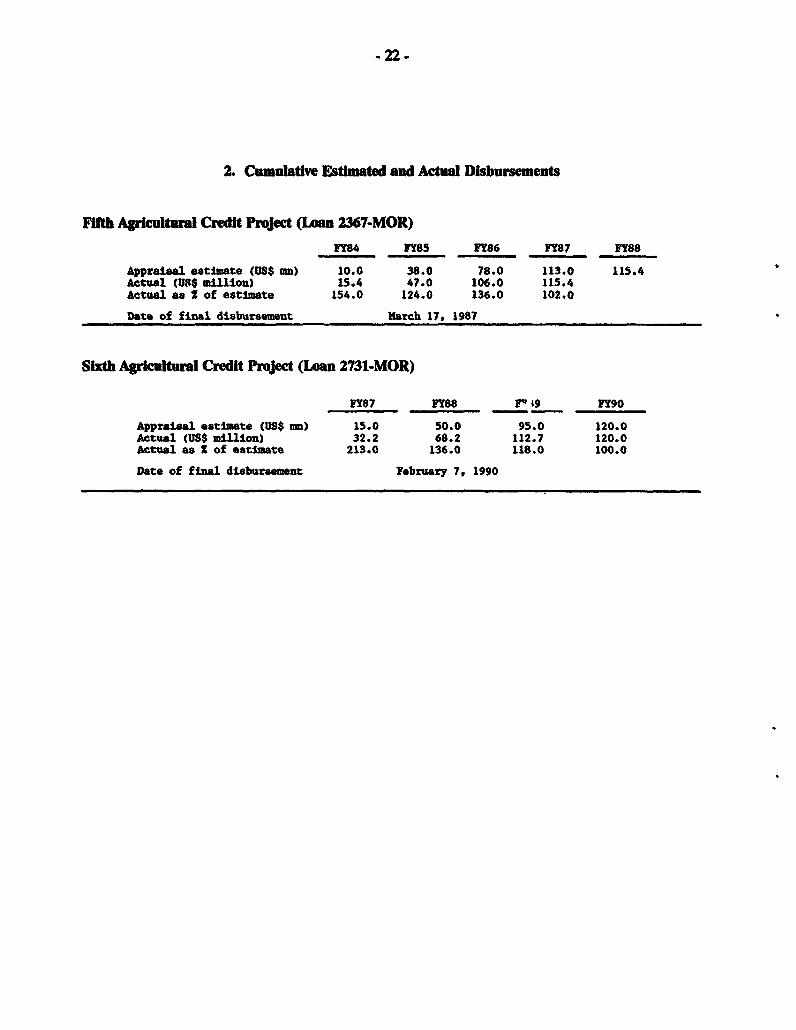

2. CumulatIve Estlmated and Actual Disbursements

Fifth Ariculturl Credit Project (Loa 2M7-MOR)

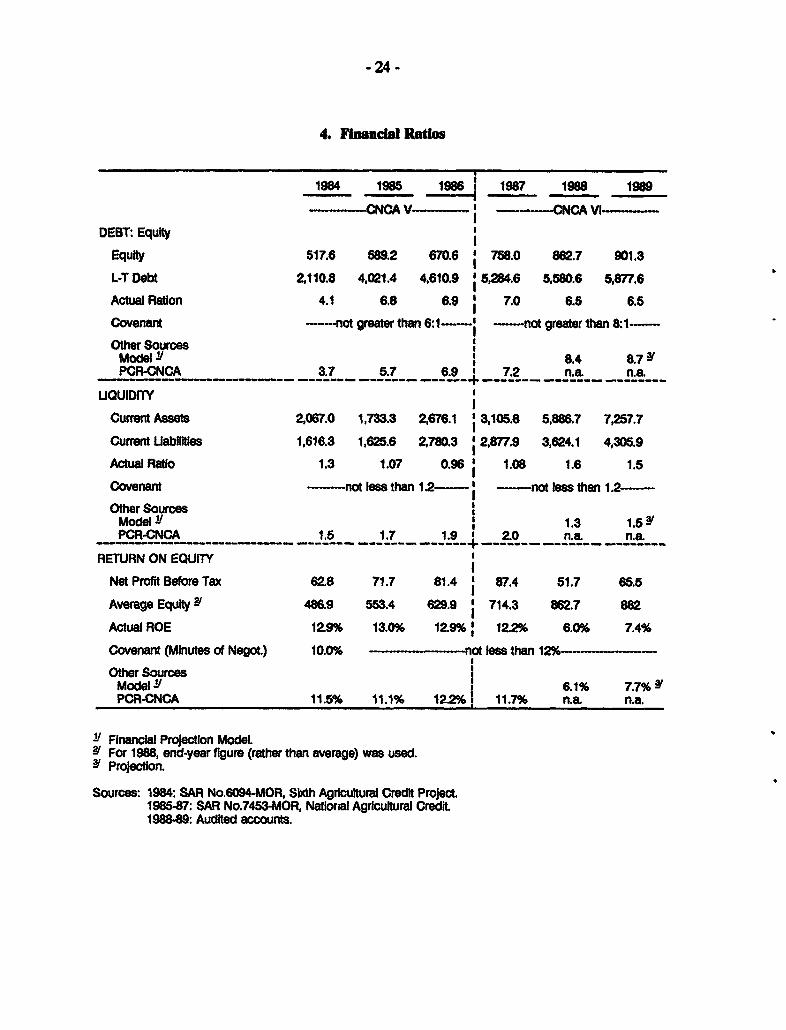

FY84 FY85 FY86 FY87 FY88

Appraisal estimate (US$ mn) 10.0 38.0 78.0 113.0 115.4Actual (USS milioa) 15.4 47.0 106.0 115.4Actual as 2 of estimate 154.0 124.0 136.0 102.0

Date of final disbursement March 17, 1987

Sixth Agricultural Credit Project (Loan 2731-MOR)

FY87 FY88 F" i9 FY90

Appraisal estimate (U$ n) 15.0 50.0 95.0 120.0Actual (US$ mlllion) 32.2 68.2 112.7 120.0Actual as 2 of estimate 213.0 136.0 118.0 100.0

Date of finl disburseent February 7, 1990

-23-

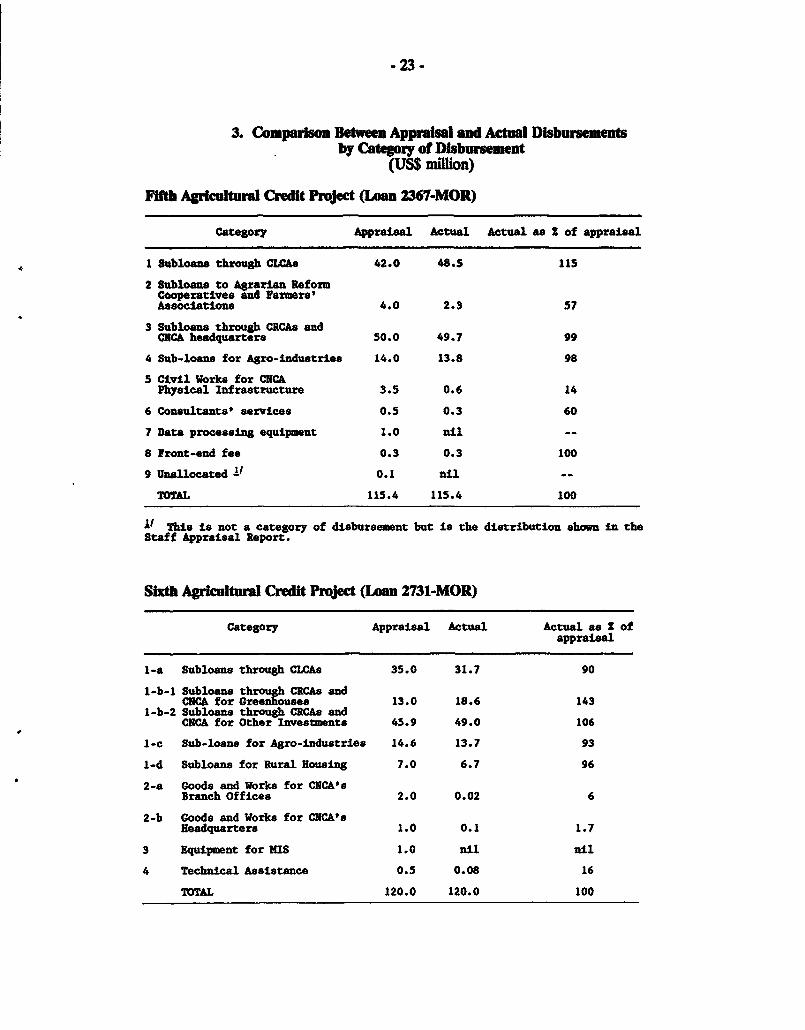

3. Compaison Beween Appisal and Actual Disbursemeby Categoiy of Dbumsement

(US$ million)

Fth Agriculurl Ceit Project (Loan 2367-MOR)

Category Appraisal Actual Actual as 2 of appraisal

4 1 Subloans through CLCAs 42.0 48.5 115

2 Subloans to Agrarian RefonmCooperatives and Narmers'Associations 4.0 2.3 57

3 Subloans through CRCAs andCRCA headquarters 50.0 49.7 99

4 Sub-loans for Agro-industries 14.0 13.8 98

5 Civil Works for CNCAPhysical Infrastructure 3.5 0.6 14

6 Consultants' services 0.5 0.3 60

7 Data processing equipment 1.0 nil --

8 Front-end fee 0.3 0.3 100

9 Unallocated -/ 0.1 nil --

TOTAL 115.4 115.4 100

11 This is not a category of disbursement but is the distribution shown in theStaff Appraisal Report.

Sit Agriultul Credit Prjecd (Lan 2731-MOR)

Category Appraisal Actual Actual as ofappraisal

I-a Subloans through CLCAs 35.0 31.7 90

1-b-i Subloans through CRCAs andCNCA for Greenhouses 13.0 18.6 143

1-b-2 Subloans through CRCAs andCNCA for Other Investments 45.9 49.0 106

1-c Sub-loans for Agro-industries 14.6 13.7 93

1-d Subloans for Rural Housing 7.0 6.7 96

2-a Goods and Works for CNCA'sBranch Offices 2.0 0.02 6

2-b Goods and Works for CNCA'sHeadquarters 1.0 0.1 1.7

3 Equipment for HIS 1.0 nil nil

4 Technical Assistance 0.5 0.08 16

TOTAL 120.0 120.0 100

-24-

4. FIancal Ratlos

1984 1985 19861 1987 1988 1989

-CNCA V- -CNCA Vli-

DEBT: Equity

Equity 517.6 589.2 670.6 ' 758.0 862.7 901.3

L-T Debt 2110.8 4,021.4 4,610.9 '5,284.6 5,58.6 5,877.6

Actual Ration 4.1 6.8 6.9 ' 7.0 6.5 6.5

Covenant -o greater than 6:1 - not greater than 8:1-

Other SourcesModel " 6 84 &7YPCR-OCA 3.7 57 6.9 7.2 n.a n.ae

UQUIDiTY

Current Assets 2,067.0 1,733.3 2676.1 '3,105.8 5,886.7 7,257.7

Current Labiiitles 1,616.3 1,625.6 2780.3 '2877.9 3,624.1 4,305.9

Actual Ratio 1.3 1.07 0.96 ' 1.08 1.6 1.5

Covenant -not less than 12-' -not iess than 1.2-

Other SourcesModel ia / 1.3 1,5PCR-CNCA 1.5 1.7 1.9 i 2.0 n.a. n.a

RETURN ON EQUITY

Net Profit Before Tax 62.8 71.7 81.4 0 87.4 51.7 65.5

Average Equity Y 486.9 553.4 629.9 ' 714.3 862.7 882

Actual ROE 129% 13.0% 12.9%' 12.2% 6.0% 7.4%

Covenant (Minutes of Negot.) 10.0% oo t less than 12% -

Other SourcesModel1' a 6.1% 7.7%PCR-CNCA 11.5% 11.1% 122% 1 11.7% n.a. n.a.

1' Financial Projection Model.Y For 1988, end-year figure (rather than average) was used.W Projection.

Sources: 1984: SAR No.6094-MOR, Sbth Agricultural Credit Project1985-87: SAR No.7453-MOR, Natioral Agricultural Credit1988-89: Audited accounts.

-25-

5. Relad ak Laos

Fifth Agicult l Credit Projwct (Lan 2367-MOR)Borrower Cadse. Rationale de Cr4dit Agricole (CNCA)

Ulme 1Sxth Aaricultural Credit ProjectLoan number 2731-HO!Amount USS120 millionDate Board Approval 06126/86

Sih Agiulura Credit Project (Lon 2731-MOR)Borrower Caisse National de CrEdit Agricole (CNCA)

Rsme on fPro ect National Agricultural Credit ProjectLoan Number 3088-10RAmount US$190 minlionDate Board Approval 06/14189

i Status of C(veants

Fif Ag ultural Credit Pojct (Loan 2367-MOR)Sixh Agrkculu Credit Project (Loa 2731-MOR)

See PMR pam 325-330.

-26 -

7. Bank Resources

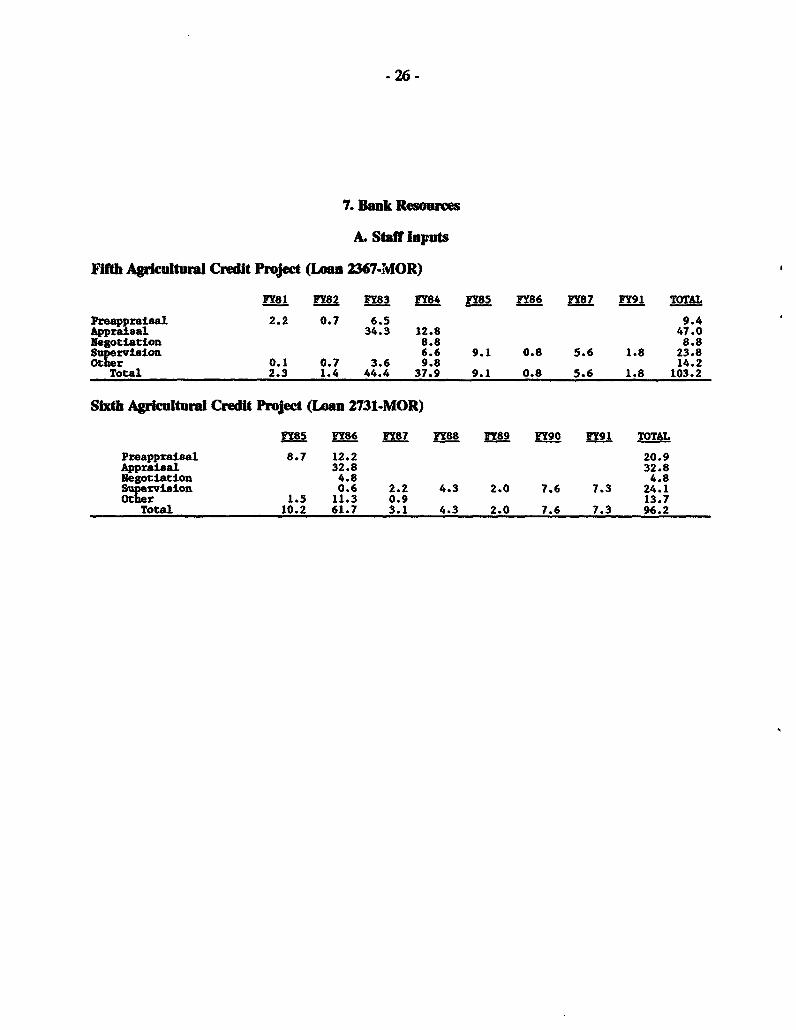

A. Staff Inputs

Ffh Ariutura Credit Project (a 2367-MOR)

FY81 PY82 FY83 FY84 FY85 FY86 FY87 FY91 TOTAL

Prgappraisa1 2.2 0.7 6.5 9.4Appraisal 34.3 12.8 47.0Negotiation 8.8 8.88 rvision 6.6 9.1 0.8 5.6 1.8 23.8Other 0.1 0.7 3.6 9.8 14.2

Total 2.3 1.4 44.4 37.9 9.1 0.8 5.6 1.8 103.2

Sih Apricultural Credit Project (L1n 2731-MOR)

PY85 YY86 FY87 FY88 FY89 FYgo pY91 TOTAL

Preappraisal 8.7 12.2 20.9Appraisal 32.8 32.8Negotiation 4.8 4.8Su ervision 0.6 2.2 4.3 2.0 7.6 7.3 24.1uther 1.5 11.3 0.9 13.7

Total 10.2 61.7 3.1 4.3 2.0 7.6 7.3 96.2

-27 -

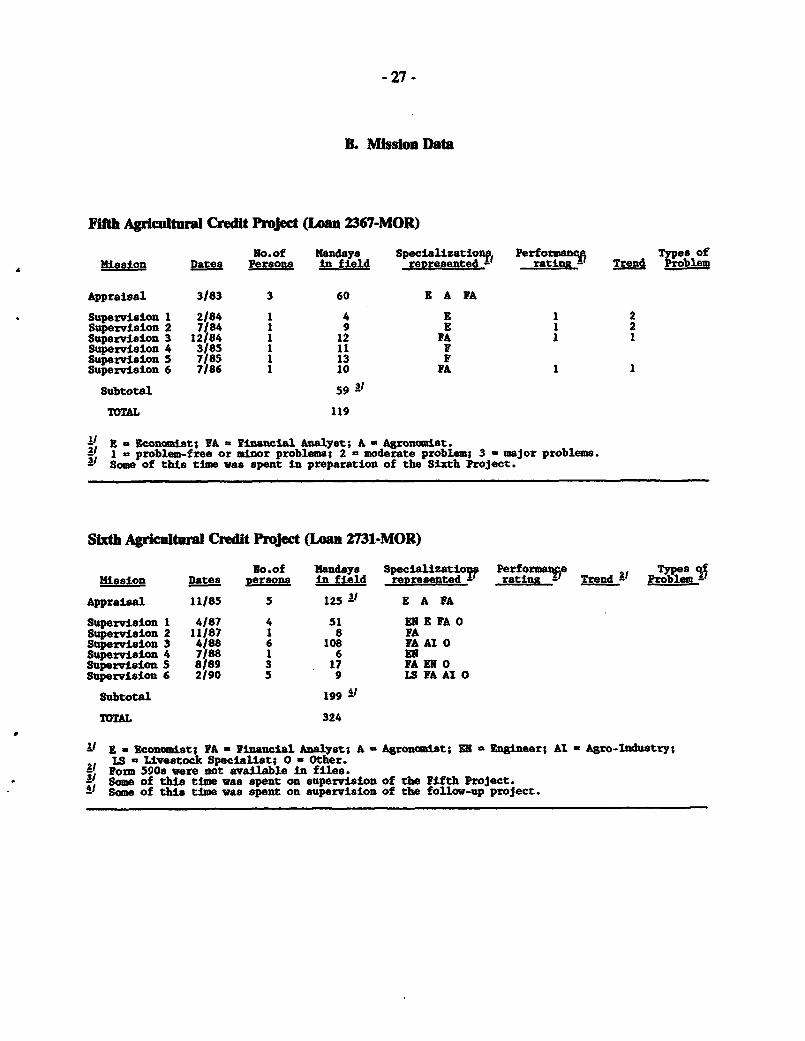

B. Missio Data

Fifth Agrkultu Credit Project (Loan 2367-MOR)

No .of Mandays Specializatiopl, Performanc Tes ofPiosion Dates Persons in field _represented ratin. Trend Proble

Appraisal 3183 3 60 B A PA

Supervision 1 2/84 1 4 E 1 2Supervision 2 7184 1 9 B 1 2Supervision 3 12/84 1 12 PA I ISupervision 4 3/85 1 11 PSupervision 5 7/85 1 13 FSupervision 6 7/86 1 10 PA

Subtotal 59 3

TOTAL 119

I u Economist; PA - Financial Analyst; A Agronumist.1 problem-free or minor problems; 2 = moderate problem- 3 major problems.

I Some of this time Was spent in preparation of the Sixth Project.

Sixth Agrltun Credit PJject (L4an 2731-MOR)

No.of Mandays Specialisatiou Performsn e Types cMission Dates persons in field reVresented O ratina - Trend ' Problem -

Appraisal 11/85 5 125 I E A FA

Supervision 1 4/87 4 51 EN E FA 0Supervision 2 11/87 1 8 PASupervision 3 4/88 6 108 PA Al 0Supervision 4 7/88 1 6 ENSupervision 5 8/89 3 17 FA EN 0Supervision 6 2/90 5 9 LS PA AIO

Subtotal 199

TOTAL 324

1I Economist; PA - Financial Analyst; A k Agronomist; EN * Engineer; Al Agro-Induetry;LS - Livestock Specialist; 0 - Other.Form 590s were not available in files.Some of this time was spent on supervision of the Fifth Project.

- Some of this time was spent on supervision of the follow-up project.

MOROCCO/C4ARO -SIXTH AGRICULTURAL vRfIED #P1imT -- odtterranean 5e.,

SIXI#ME PROJET OE CRADD(7AeflhCOI4 . A.,.

BRANCH NETWORK OF THE DNAPT ONAV IT4MIKJRASAU DE IA CAI55 NA(Ar,aA HMoA.

"6(: NUrMMO4/R1f0D^ N E MAt -, m*-. t

CRCA'4O) ALGERIA* CLCA 090 *S-b L J1 ;

-600- ind )im 47j r ndu*) n,' '-

Afw~ws o^ie ,o * (W J *CRCA~~~~~~~~~~~~~~~~~~~~~~~S

002

Avmgt, a em¢ 34frocfio /x 4#

8.00+~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~0

'0-0 / f /f'( *J<tr-.~1

AutinaI capit I 0 * )

S : ¢ <- :'. -u - r t 5 1~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~'-

., A T z t/ > C

R3iei32 .

.* -tk ( }NDv . . A W f