Embed Size (px)

Citation preview

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No. P-3640-UNI.

REPORT AND RECOMMENDATION

OF THE

PRESIDENT OF THE WORLD BANK

TO THE EXECUTIVE DIRECTORS

ON A

PROPOSED FERTILIZER LOAN

IN AN AMOUNT EQUIVALENT TO US $250 MILLION

TO THE

FEDERAL GOVERNMENT OF NIGERIA

August 24, 1983

This document has a restr.cted distribution snd may be used by recipients only in the perfurmance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

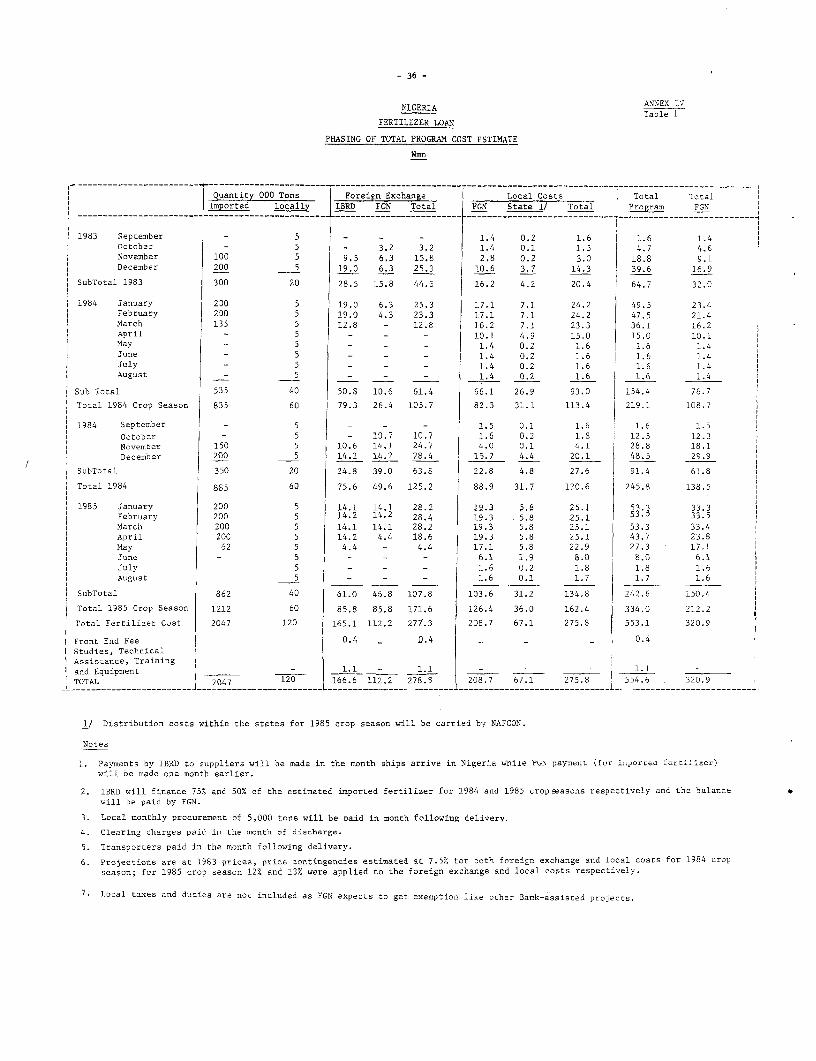

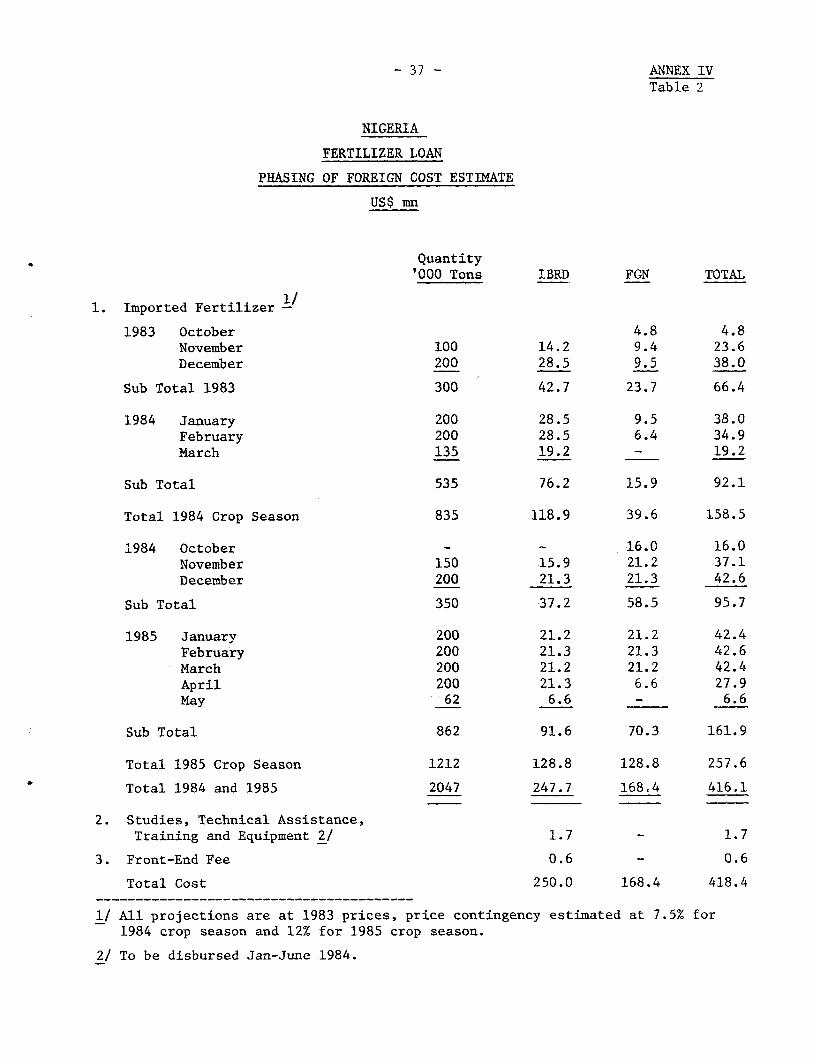

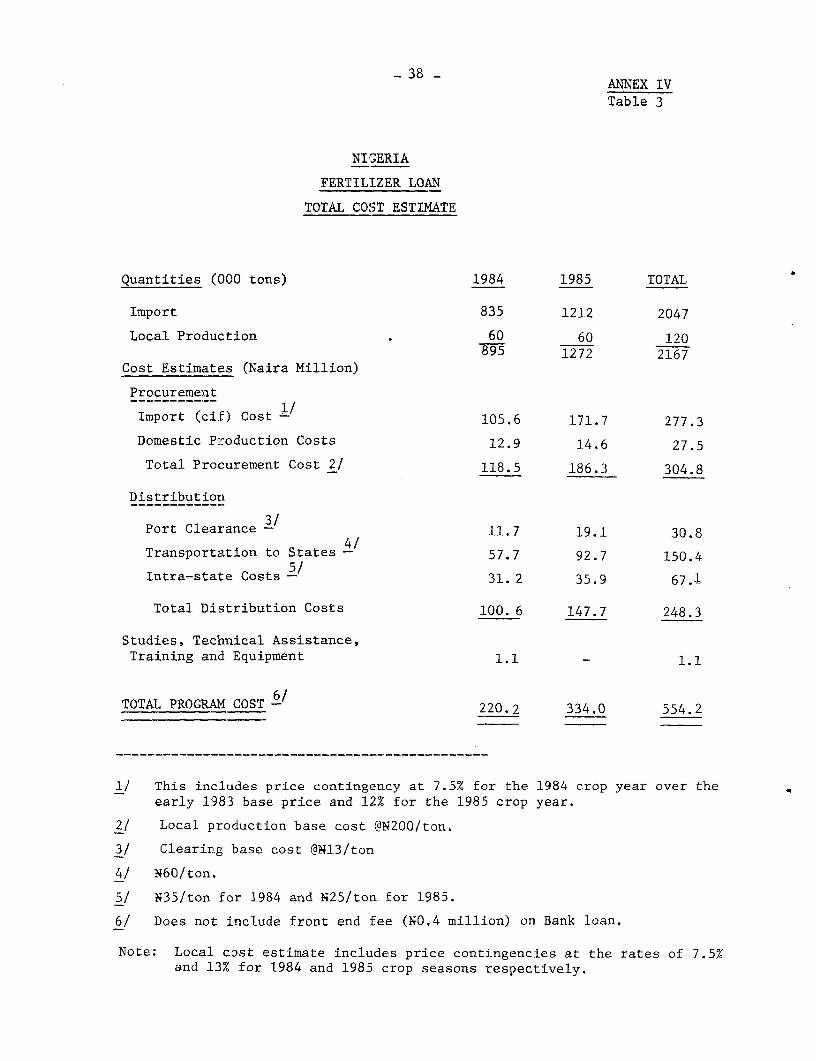

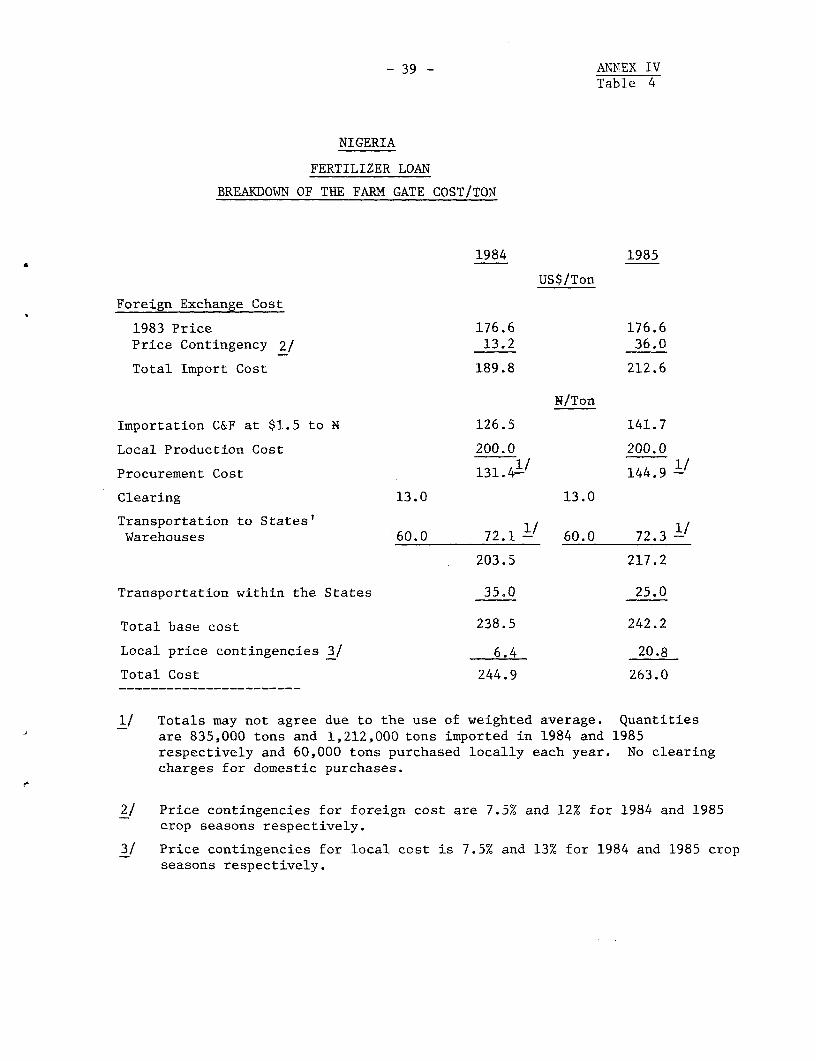

e A

utho

rized

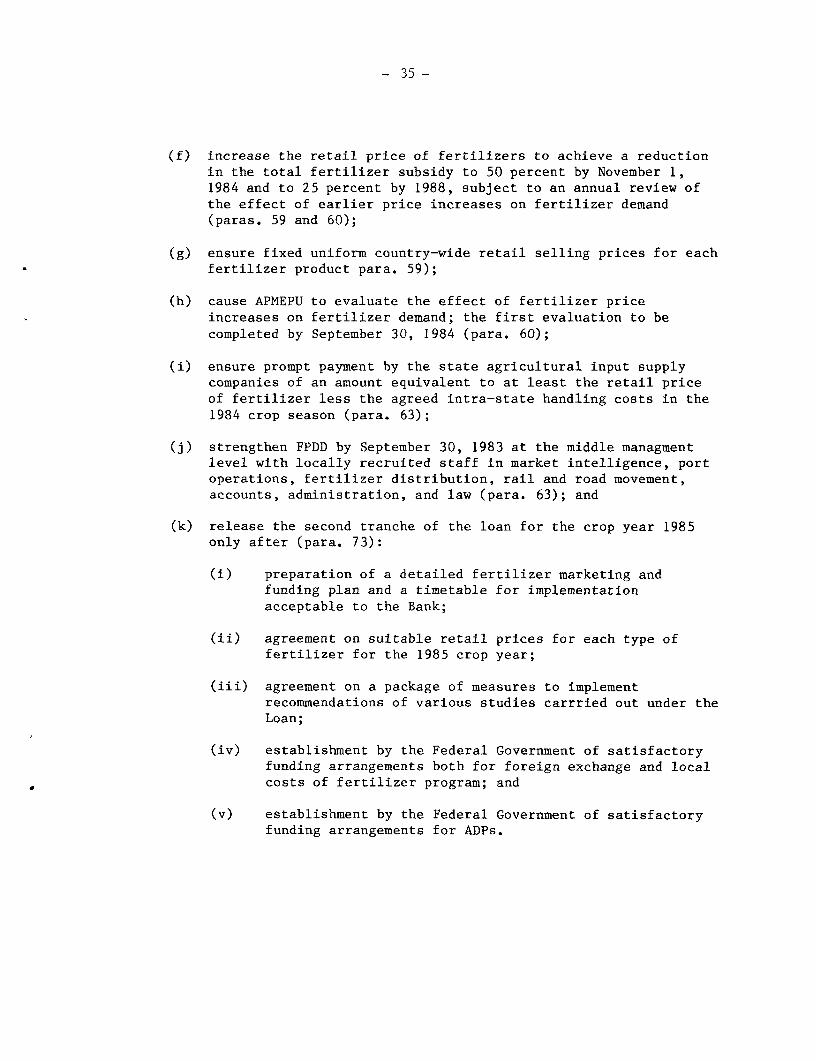

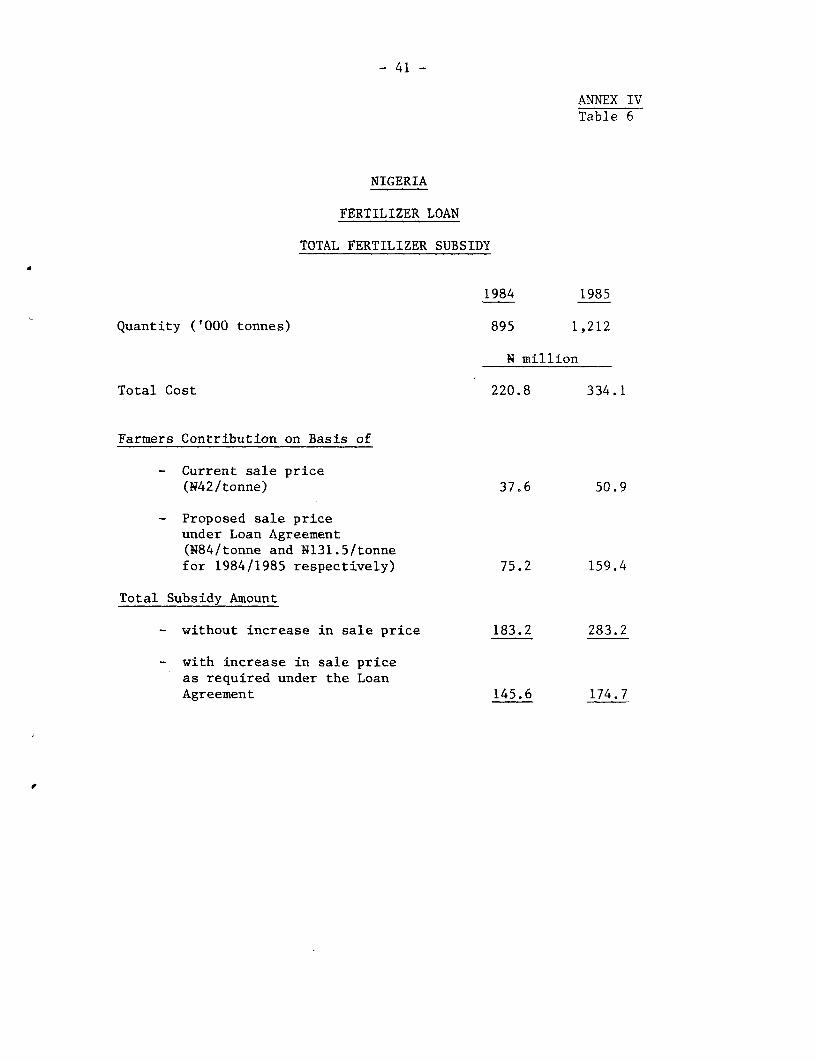

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

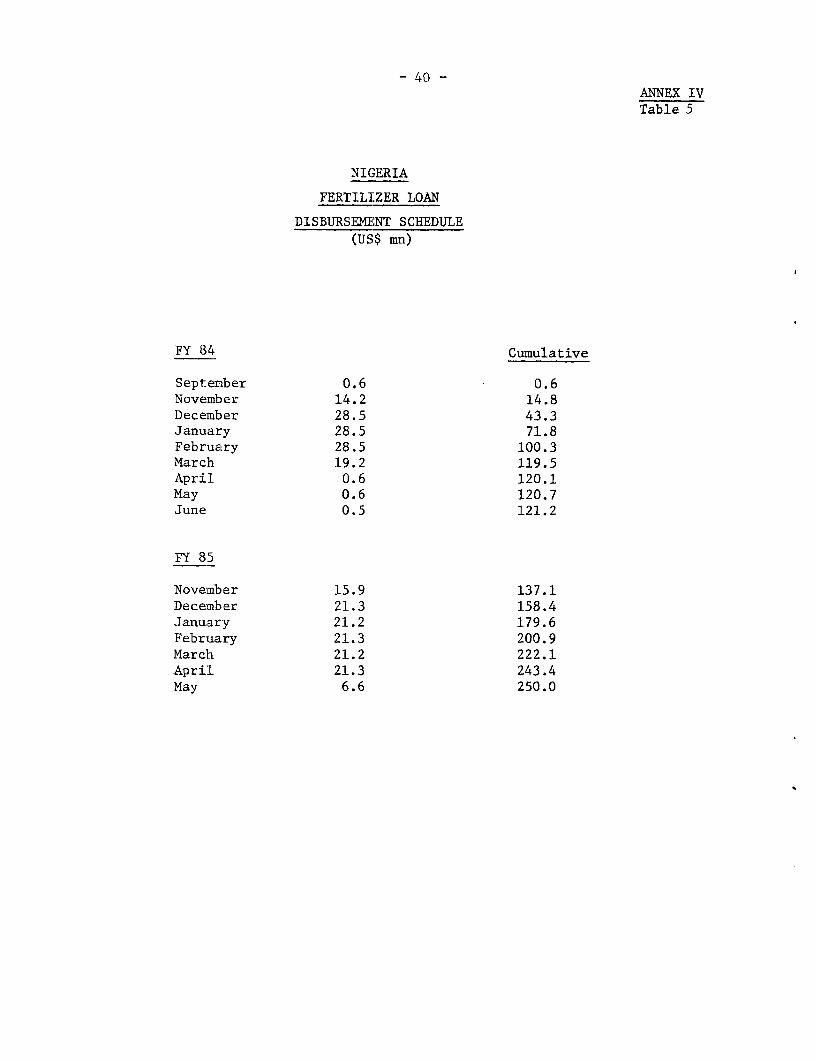

iscl

osur

e A

utho

rized

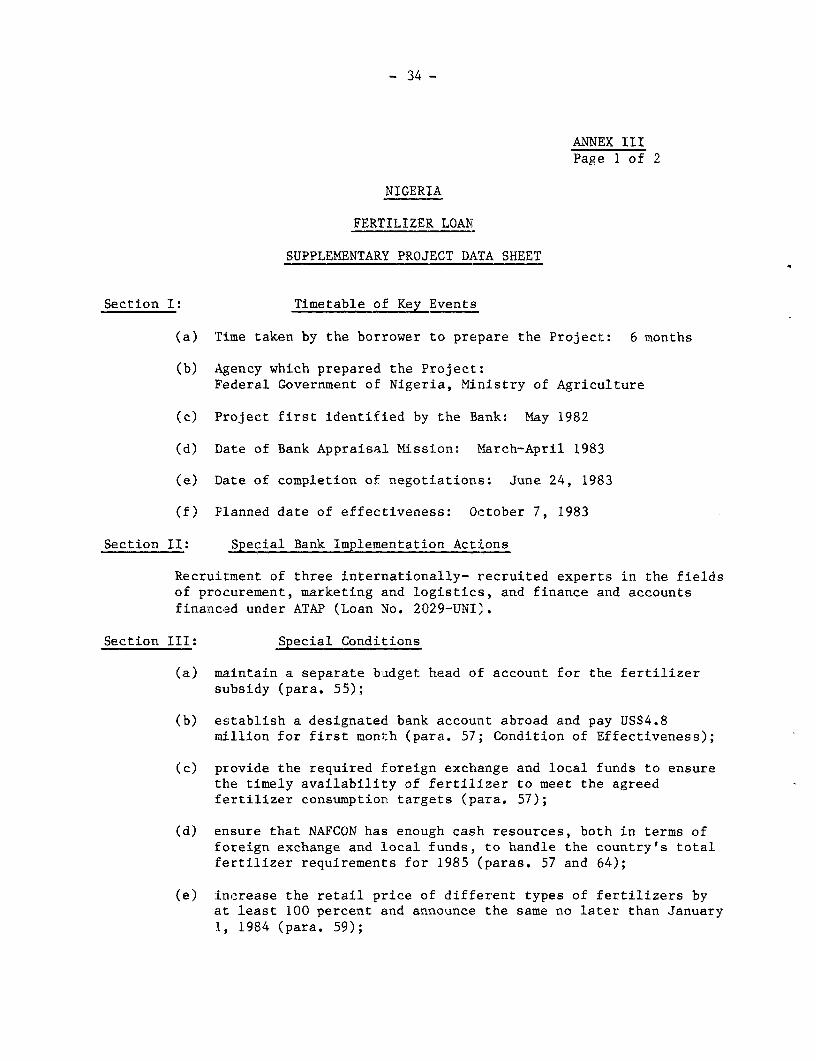

CURRENCY EQUIVALENT

Calendar 1982 May 1983

Currency Unit = Naira (N) Naira (N)US$ = NO.67 NO.71Ni = US$1.49 US$1.41

Used in this Report: Ni = US$1.5

WEIGHTS AND MEASURES

1 metric (m) ton = 0.98 long ton= 1,000 kilograms

1 hectare (ha) 2.47 acres

FISCAL YEAR

January 1 - December 31

ABBREVIATIONS

ADA - Accelerated Development AreaADP - Agricultural Development Project (Bank-assisted)APMEPU - Agricultural Project Monitoring, Evaluation and

Planning Unit, Federal Ministry of AgricultureATAP - Agricultural Technical Assistance Project (Loan No. 2029-UNI)FPDD - Fertilizer Procurement and Distribution Division,

Federal Ministry of AgricultureIFDC - International Fertilizer Development Center, Muscle Shoals, USANAFCON - National Fertilizer Company of NigeriaNPK - Compound fertilizersNSS - National Seed Service

FOR OFFICIAL USE ONLY

NIGERIA

FERTILIZER LOAN

LOAN SUMMARY

Borrower: Federal Republic of Nigeria

Amount: US$250 million, including capitalized front-end fee

Terms: Payable over 17 years, including four years of grace, atstandard variable interest rate.

LoanDescription: The Loan would finance part (nearly 60 percent) of the foreign

exchange cost of importing about 2 million tons of fertilizerrequired by Nigeria for the 1984 and 1985 crop years as well asthe costs of foreign training and communication equipmentrequired for the Fertilizer Procurement and DistributionDivision (FPDD), and studies to assist in the development of anappropriate policy framework. It would contribute to improvingthe fertilizer subsector through an agreed program of phasedreductions in subsidies, commercialization of fertilizer retailbusiness, and changes in procurement and marketing methods. TheLoan would present some risks. First, FPDD may not beadequately staffed and equipped to handle the 1985 cropprogram. To reduce this risk, FPDD's staffing is being upgradedconsiderably. Second, NAFCON may not be ready to assumeresponsibility for fertilizer procurement and distribution forthe 1984 crop year. However, every effort would be made toprepare NAFCON for its task, and the Bank would, if necessary,consider other viable alternatives b,efore the release of thesecond tranche of the Loan. Third, Government may be unable toprovide the requisite counterpart funding. This risk would beminimized through the pro-rata financing of the foreign exchangecost of each shipment by the Bank and the Federal Government; iflocal funds would not be released on time, the second tranche ofthe Loan would be withheld. And finally, the proposedfertilizer price increases may depress fertilizer demand tounacceptable levels. However, this risk would be reviewedannually by the Bank and the Nigerian authorities, andcorrective action could easily be taken.

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

- ii -

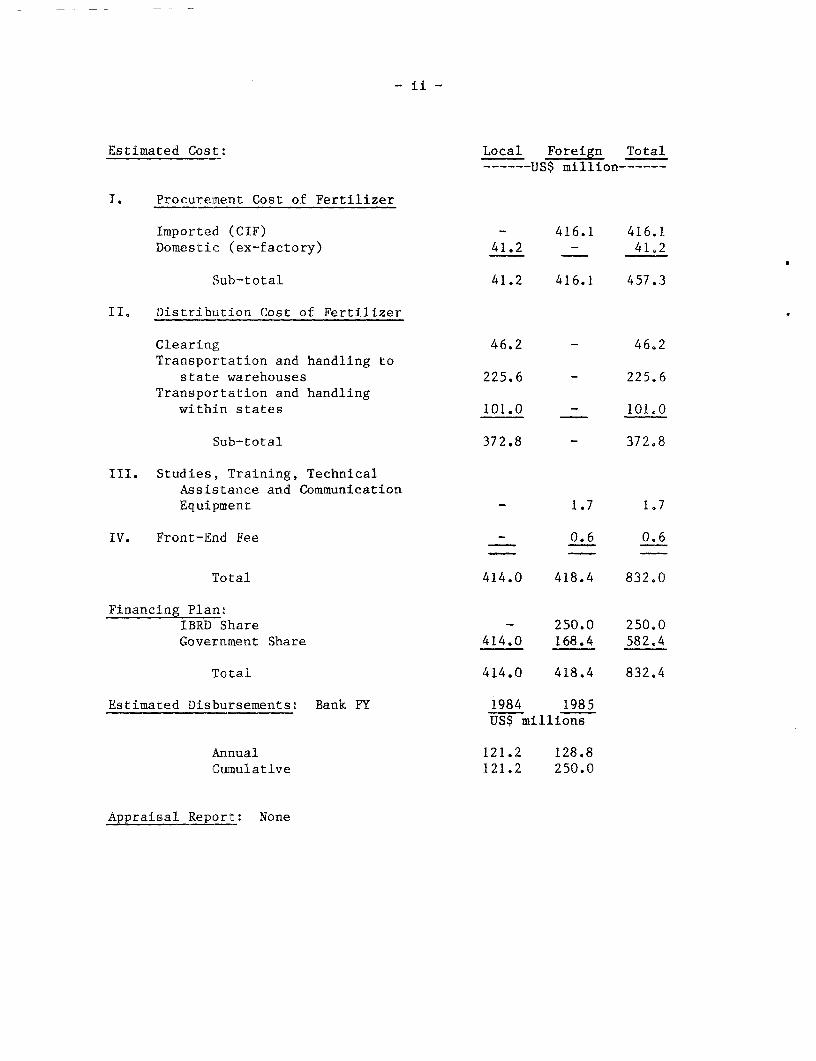

Estimated Cost: Local Foreign Total…-US$ million------

I. Procurement Cost of Fertilizer

Imported (CIF) - 416.1 416.1Domestic (ex-factory) 41.2 - 41,2

Sub-total 41.2 416.1 457.3

II. Distribution Cost of Fertilizer

Clearing 46.2 - 46.2Transportation and handling to

state warehouses 225.6 - 225.6Transportation and handling

within states 101.0 _ 101.0

Sub-total 372.8 - 372e8

III. Studies, Training, TechnicalAssistance and CommunicationEquipment - 1.7 1.7

IV. Front-End Fee - 0.6 0.6

Total 414.0 418.4 832.0

Financing Plan:IBRD Share - 250.0 250e0Government Share 414.0 168.4 582.4

Total 414.0 418.4 832.4

Estimated Disbursements: Bank FY 1984 1985US$ millions

Annual 121.2 128.8Cumulative 121.2 250.0

Appraisal Report: None

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

REPORT AND RECOMMENDATION OF THE PRESIDENTTO THE EXECUTIVE DIRECTORS ON APROPOSED FERTILIZER LOAN TO THE

FEDERAL GOVERNMENT OF NIGERIA

* 1. I submit the following report and recommendations on a proposed loanto the Federal Republic of Nigeria for the equivalent of US$250 million tohelp in the import of requisite quantities of fertilizers for the crop years1984 and 1985 and to assist the Federal Government in improving the managementof the fertilizer subsector. The proposed loan would be amortized over amaximum period of 17 years, including 4 years of grace, with a standardvariable interest rate.

PART I - THE ECONOMY

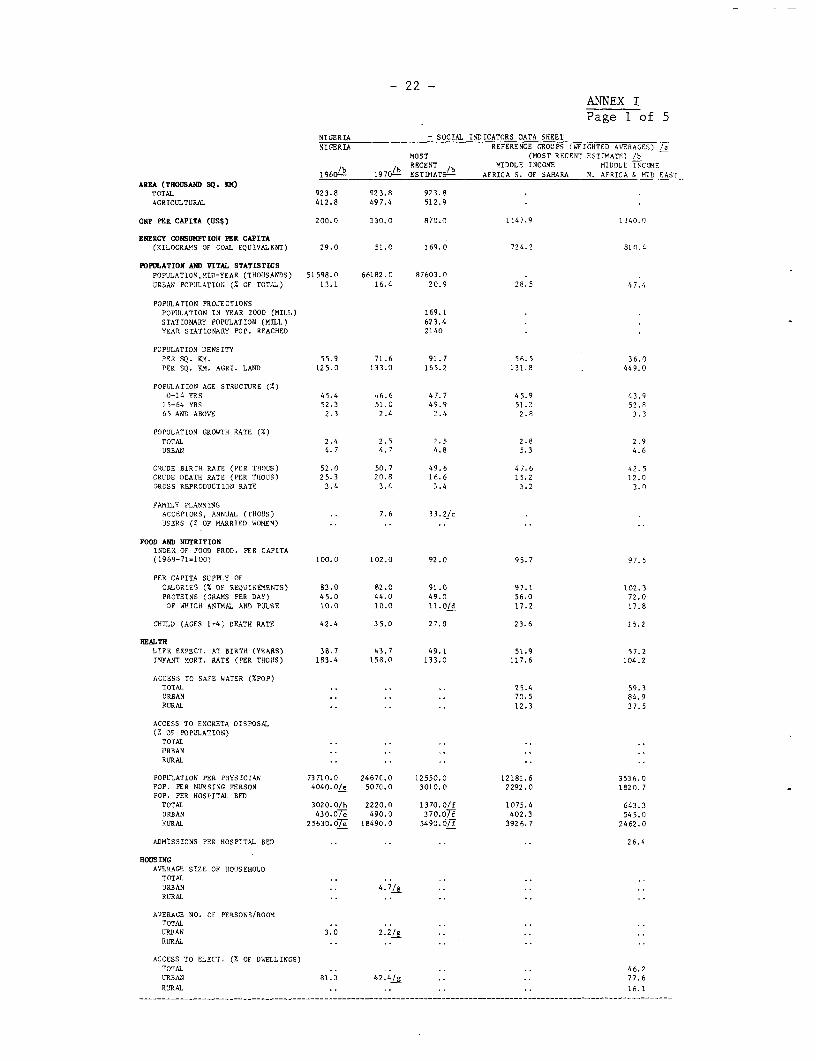

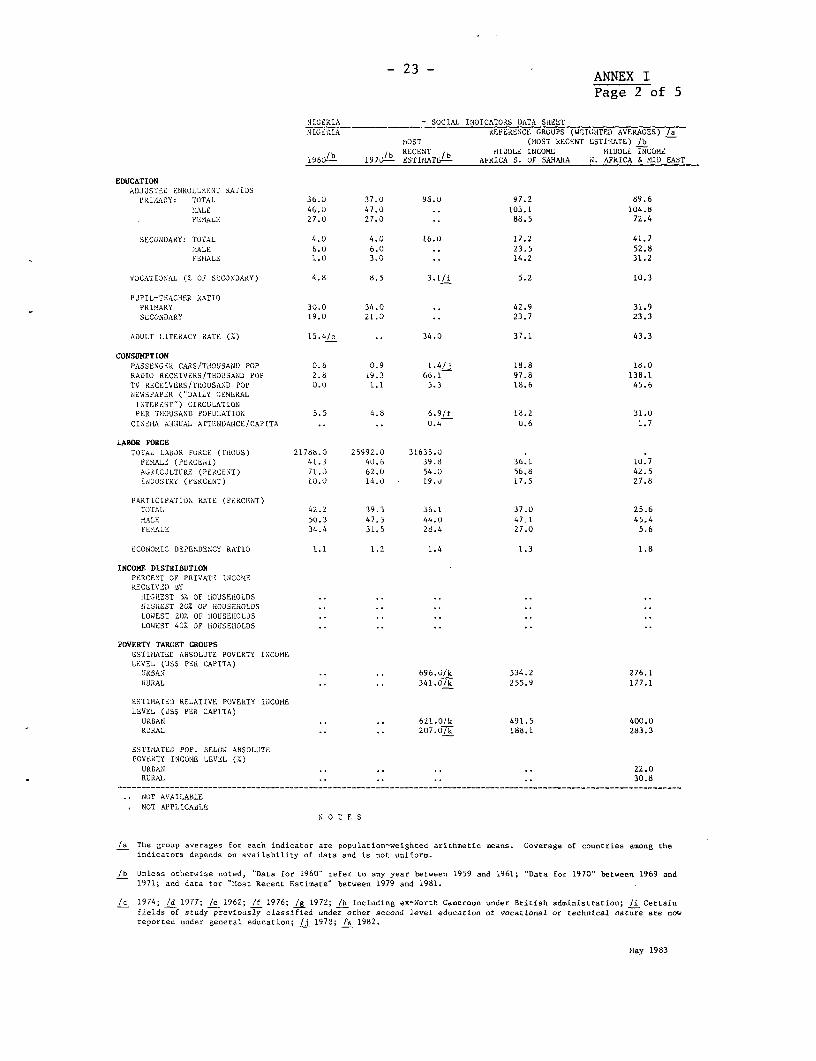

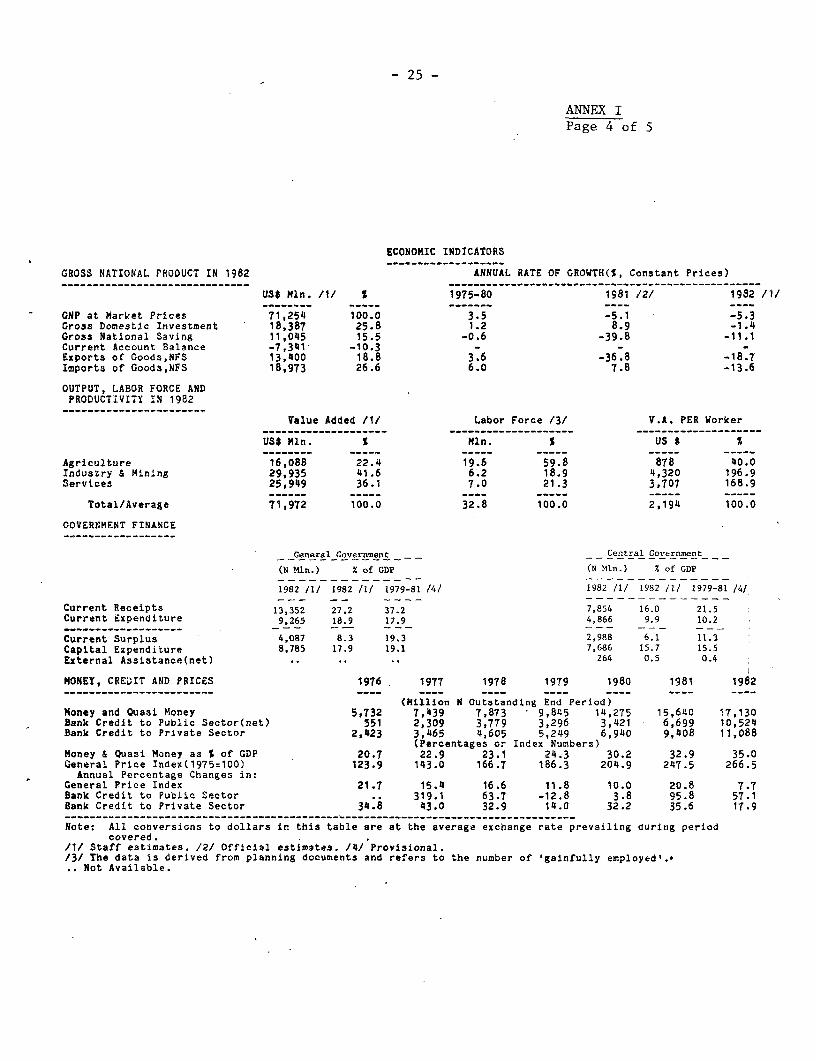

2. An economic mission visited Nigeria in May/June 1982, and a CountryEconomic Report (No. 4506-UNI) will be distributed to the Executive Directorswithin the next few days. Selected social and economic indicators are givenin Annex I.

Background

3. Nigeria, with a population of over 90 million in 1982, is the mostpopulous country in Africa. Among Sub-Saharan Bank members, Nigeria accountedfor about 45 percent of gross output and more than 60 percent of regionalinvestment in 1980. Its GNP per capita is estimated at about US$820 in 1982,which is twice the average for Sub-Saharan Africa. While Nigeria, as a majoroil exporter since the early seventies, enjoyed a substantially improvedresource base from increased oil revenues, it still remains at a very earlystage of development in terms of socio-economic indicators, in which itcompares with other Sub-Saharan countries.

4. Following a civil war and 13 years of military rule, a new federalconstitution was adopted, and an elected civilian government came into powerin 1979. The constitution vests considerable powers in the state and localgovernments, while it maintains a delicate balance between regional autonomyand preservation of national unity. The country seems to have adjusted wellto the new form of government and to civilian rule, and it is holding nationalelections in August 1983.

Macro-economic Developments

5. Nigeria has been undergoing a rapid socio-economic transformationsince the upsurge of oil prices in 1973-74, which dramatically altered thecountry's resource position. During the seventies, Nigeria's developmentstrategy was based on sustaining a high rate of growth and diversifying theeconomy through the resources generated by the oil sector. The principal

-2-

objective of the policies pursued by the Nigerian decision-makers was totranslate the large oil revenues aLccrued - about US$100 billion in currentprices during the 1973-81 period - into investments in economic, social, andphysical infrastructure. While there have been some "non-economic" invest-ments and waste, significant development gains were made in both economic andsocial infrastructure. Transport infrastructure, particularly roads andports, expanded considerably. Power generating capacity tripled, and refiningcapacity more than quadrupled since 1973. Manufacturing grew at an averageannual rate of 12 percent during the 1973-81 period, although there was ahighly distorted investment structure. There aLlso has been a rapid spread ofeducation at aLl levels; in particular, the primary enrollment ratio, whichwas about 35 percent in the early seventies, has more than doubled.

6G Developments have not been as positive in some other areas. Inagriculture, overall output remained virtually stagnant during the 1973-81period, with production of grains increasing at the same rate as thepopulation growth rate, but production of root and export crops decliningsubstantially. Within a decade, Nigeria became a major food importer (US$2billion of imports in 1981). This was caused partly by sudden and rapidgrowth of public expenditures, which outpaced the growth of public revenue,and which, along with a dramatic expansion in domestic demand, resulted inhigh rates of inflation. Inflation, coupled with an appreciating domesticcurrency, pushed up domestic costs of production, thus putting the commodityproducing sectors at a disadvantage vis-a-vis imports and non-traded goods.This encouraged diversion of resources from commodity production to services(including trade and construction). Both agriculture and industry became"high-cost" producers. Trade and iexchange rate policies, which wereformulated in response to frequent swings in oil export earnings, were largelyused to dampen inflationary pressures or ration imports rather than to provideappropriate incentives to domestic production. This was partly due to thefact that, as a result of the fluctuations in the world oil markets and theirimpact on the balance of payments and government revenues, Nigerianpolicymakers have been preoccupied with short-term crisis management. Thishas diverted attention from formulating longer term policies to reduce thecountry's dependence on oil and to strengthen the domestic productive sector.

7. The Fourth Development PLan (1981-85) was prepared in 1980 when theworld oil markets again presented a favorable outlook and, accordingly,reflects an ambitious investment program. It did not envisage, however, thesudden downturn of the world oil MnLrkets in 1981. The sharp decline in oilproduction by about one-third, to 1.43 mbd, changed the short-and mediumi-termprospects for the Nigerian economy significantly. The Government, during mostof 1981, was reluctant to come to grips with the situation and continued tocount, along with most observers of the oil markets, on a quick recovery ofthe oil situation. As the oil market deteriorated further, imports continuedto rise as importers sought to beat the likely impending shortage of foreignexchange. Consequently, the current account balance in 1981 showed a deficitof about US$5.5 billion, which had to be financed by drawing down foreignexchange reserves and external borrowing. By the end of 1981, foreignexchange reserves had declined to US$3.9 billion, almost one-third of thelevel at the end of 1980, and equivalent to only two months of Lmports. Likethe balance of payments, public finances were also strained, since oilrevenues account for more than 80 percent of revenues of the Federal and stategovernments. The Federal Government kept its expenditure level in 1981

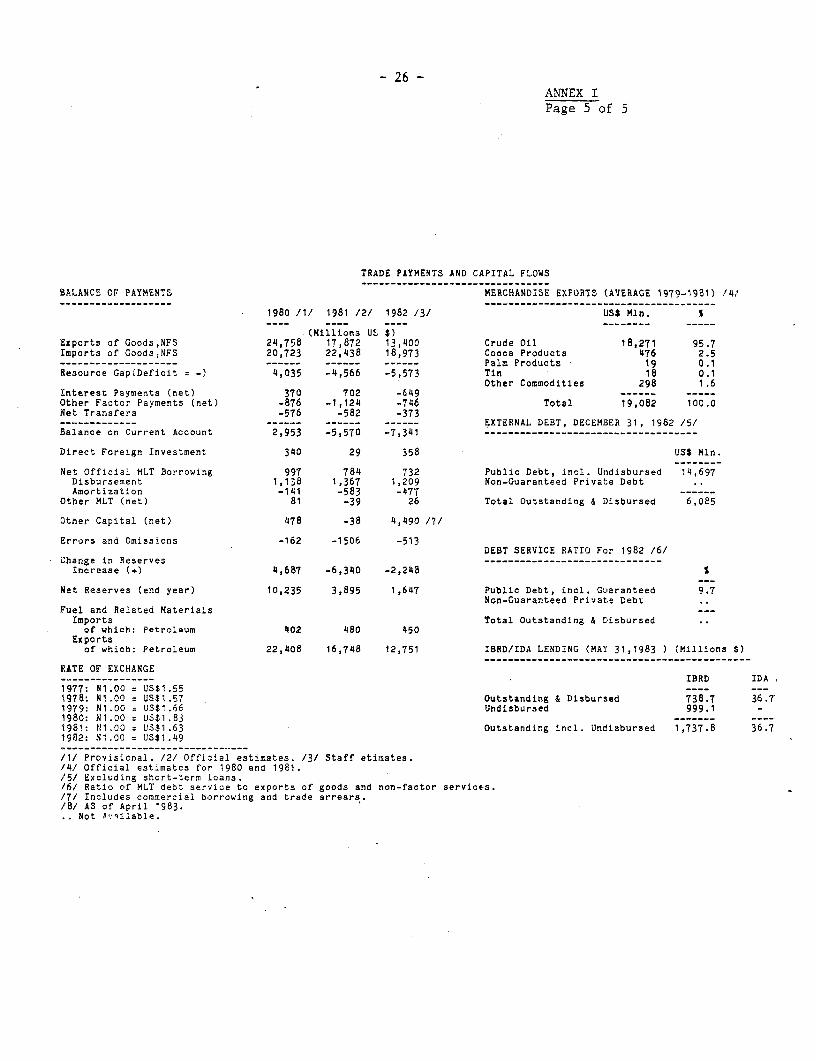

largely intact by deficit financing, amounting to about US$6 billion. Thestate governments, which had increased their spending rapidly, partly as aresult of a shift of responsibilities from the Federal to state governmentsfollowing a change in the revenue allocation formula in 1981, found it moredifficult to cope with the sudden shortfall in revenues, since they hadlimited access to domestic credit. As a result, some state governmentsresorted to borrowing abroad on a substantial scale. By the end of 1981,outstanding external debt (including undisbursed) of the state governments wasabout US$4.5 billion - slightly more than one third of the country's totalexternal debt. Despite the increase in imports and the attempt to maintainthe level of government expenditures, growth in the non-oil sectors declinedconsiderably. Along with the substantial retrenchment in the oil sector, realGDP declined by 5.2 percent in 1981.

8. In 1982, the oil markets continued to be slack, and Nigeria's oiloutput declined further to an annual average level of 1.29 mbd. In the faceof rapidly rising imports in the first few months of 1982 and mounting foreignexchange shortages, the Government, in April 1982, took a series of measures,including: (i) increasing import duties and quantitative restrictions;(ii) import restrictions through introduction of an advance deposit scheme;(iii) tightening customs administration; (iv) cutting back capital expen-ditures about 40 percent including stopping all new projects; (v) increasinggasoline prices 33 percent; (vi) increasing interest rates 2 percent;(vii) placing a $350 million ceiling on each state government's external debt;and (viii) restricting capital transfers abroad. These measures wereprimarily intended to arrest the further deterioration in the domestic andexternal financial situation, although elements such as increases in interestrates and the price of gasoline also reflect the Government's intention toredress widespread price distortions in the economy. In addition to thesemeasures, the Government has pursued an exchange rate policy which resulted ina depreciation of the Naira of 19 percent against the dollar and 5 percentagainst the SDR during the period 1980-82.

9. The various actions have not yet been sufficiently successful inreversing the trend in imports, in part on account of the high level of importapprovals during the first quarter of 1982, prior to the April measures. Thecurrent account deficit is therefore expected to have reached US$7 billion in1982. Because of a further drawdown of foreign exchange reserves of aboutUS$2.3 billion, reserves are estimated to have dropped to about $1.6 billionat the end of 1982. In addition, arrears in payments of short-term tradecredits of about US$3-4 billion accumulated during 1982. Although payments onlonger-term borrowing remained current, this had a sharply adverse effect onthe availability and cost of external borrowing as well as on the continuationof normal trade transactions. The Government has since taken measures toestablish priority categories for systematic payment of these arrears, and hasstarted the process of rescheduling important categories of these tradearrears (para. 12).

10. The Federal Government has generally found it difficult to cope withthe deteriorating financial situation, although the 1982 budget was reducedafter the stabilization measures were announced in April 1982. Budgetary cutswere imposed on capital expenditures, inevitably at a substantial cost toongoing development programs. The financial crisis was particularly acute atthe state level. Some of the state governments were even unable to pay civil

-4-

service salaries5 and had to resort to the Federal Government for loans.ConsequenLly, most of their projects were grossly underfunded, and some had tobe stopped,

11. In its 1983 budget propos.al, the Federal Government adopted aconservative revenue outlook, based on an oil production level of one millior.barrels a day and substantial cutbacks in planned investment expenditures.Certain p-rojects with large foreign exchange requirements, such as thestandard-gauge railroad project, were deferred indefinitely. In January 1983,the Government introduced further import restrictions in the form of licencerequirements and higher tariffs to reduce the level of imports :fromUS$1.3 billion to less than US$900 million a month,

Aqjus tPolcy Issues

12. At present, the Nigerian economy faces two critical issues: first.management of the short-run financial crisis and stabilization of the economy;and second 3 longer-term structural adjustment of the economy by stimulatingproductive sectors, lessening dependence on oil, and generating a widerresource base. Withr regard to the short term, the additional measures thatthe Government took in January 1983 to control imports have helped to arrest afurther deterioration of the external financial situation. However, there nowremains the need to eliminate the external arrears, particularly in view ofthe requirement for substantial external borrowing in the near future.Discussions with major overseas creditor banks resulted in the rescheduling ofthe arrears ow ed to these institutions (for confirmation of letters of credit)of about $1G6 billion accumulated prior to March 31, 1983. Repayments are tobe made over a period of 31 months starting January 1984. As a result of therescheduling agreement, the commercial banks will likely make available toNigeria a revolving trade credit of about US$1.0 billion. The remainingdocumented arrears (estimated at $3.3 billion as of end June 1983) are largelyprivate non-letter-of-credit arrears incurred under "open-account" inter-company import financing. These will also have to be rescheduled, but thearrangements to dio this are likely to be more complex and time-consuming. Tothese documented arrears must be added a backlog of foreign exchange requestsawaiting documentation, The IMF, which has been asked to examinepossibilities of assisting Nigeria through an Extended Fund Facility, istaking the need for such reschedulings into account in putting together afinancing package to meet Nigeria's minimal external financing requirementsfor the period 1984-86.

13. Whaile a rebound in oil revenues would help Nigeria to overcore thecurrent crisis, it will not resolve the structural issues facing theeconomy. More vigorous and consistent policies, beyond the measures taken torestore financial stability, will be needed to bring about structuralchange, The chief requirements comprise: (i) further incentives forefficient export promotion and import substitution, including appropriateexchange rate, tariff, and credit policies; (ii) complementary steps tostrengthen the balance of payments through judicious management of foreaignborrowing and external reserves; (iii) continued control of aggregate demandthrough prudence in monetary, fiscal, and wage policies; (iv) restructuringthe composition of public investment to increase its efficiency; and(v) taking steps such as raising interest rates and improving tax collection,to increase private and public savings and investment. The Government is

- 5 -

currently discussing all of these policy issues with both the IMF and theBank.

Prospects and Financing of Development

14. Although Nigeria's exportable crude oil surpluses are expected to besignificantly reduced well before the turn of the century, the bulk of itsforeign exchange resources will continue to come from the hydrocarbon sectorsduring the next twenty years. This will probably include liquified naturalgas (LNG), for which a major production facility is estimated to come onstream near the end of the decade, and some petrochemical, as well as oil

* exports. To maintain a momentum of growth, major structural changes areneeded for adapting the economy to lower levels of oil export earnings. Inthe short-run, the volume of Nigeria's oil exports is likely to be determinedby the uncertain conditions of the world oil markets rather than by thedeliberate extraction policies of the Government. It is projected that oilproduction would rise to 1.5 mbd in 1986, from its level of 1.29 mbd in 1982.

15. Terms of trade are expected to deteriorate somewhat in the short run,and then to improve beyond 1985. However, gains from terms of trade will notsubstantially alter the longer-run resource picture or the need for structuraladjustment.

16. External borrowing requirements in the short- and long-term will besubstantial in view of slow improvements in oil export revenues, the need toclear payment arrears, and the requirements of major ongoing projects. In1983, the current account deficit of the balance of payments is expected toamount to about US$3 billion (5 percent of GDP) and result in a large overalldeficit of about US$4 billion. The deficit will, in all likelihood, befinanced mostly by additional accumulation of private trade arrears,apparently already incurred. In subsequent years (1984-86), the overalldeficit is likely to remain large. Thus, the balance of payments prospectsfor these years are particularly troublesome. Large claims on foreignexchange earnings are due in 1983-86, essentially on account of trade arrearsand repayment of public guaranteed debt. Even under conservative assumptionswith respect to imports--virtually no change in real imports--borrowingrequirements for the period 1983-86 are estimated at about US$11 billion; evenat this level the investment program would have to be highly constrained.Since the level of reserves is already quite low, further drawdowns cannot beused to finance the deficit as happened in 1981 and 1982. Thus, quickdisbursing external borrowings are needed to fill the gap. Estimates offuture debt service ratios have had to be revised upwards in the light oflower forecasts of oil production and prices and, more importantly, of thearrears. The debt service ratio, which has been quite low until now (around9.6 percent in 1982) is expected to rise to 20 percent in 1983. If alldocumented trade arrears were liquidated during the 1984-86 period on termssimilar to those being rescheduled, the debt service ratio would jump to 35percent in 1984 before declining to 33 percent in 1985 and 27 percent in1986. However, it is likely that the trade arrears would be rescheduled overa longer time period in which case these debt service ratios would be lower.Beyond 1986, the debt service ratios are likely to be 20 percent (with aconservative assumption of oil production of 1.5 mbd) or less. Thus, whilerecognizing that Nigeria has a short-term debt problem, our judgement is thatNigeria is creditworthy for medium- and long-term borrowing provided sound

economic policies are pursued by the Government, Indeed, inc-reased lendingthat would disburse over the next few years, when the debt service ratio issharply increased and thus import capacity sharply reduced, would be a vitalcomponent of the economic reform and recovery program (para. 13)

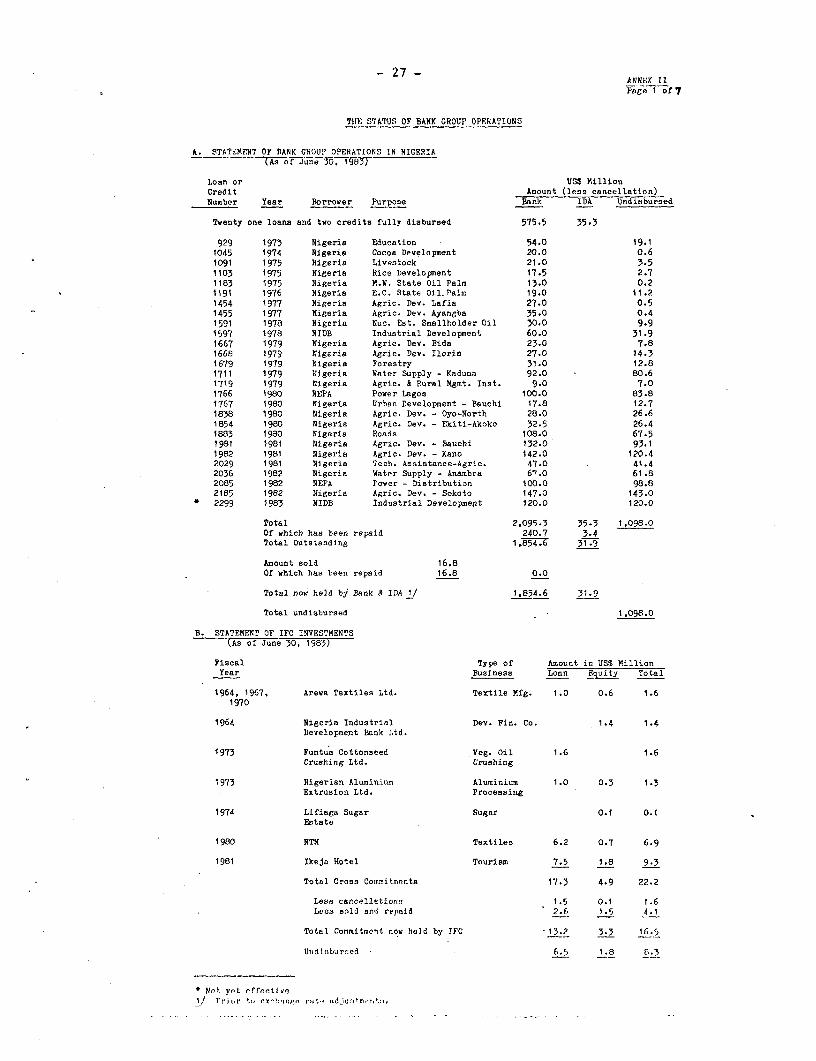

PART II - B NK GROUP OPERATIONIS IN N,IGERIA

1'7. Bank and IDA lending to Nigeria as of June 30, 1983 amounted toUS$2,130.6 million (net of cancellations). The amount of these loans andcredits disbursed as of June 30, 1983 was 'US$1,032.6 million, leaving anundisbursed balance of US$1,098.0 million, Agriculture accounts for about 41percent of total commitments; transport, power, and water supply together forabout 41 percent; and education, industry9 urban, and the post-vrar rehabili-tation loan for the remaining 18 percent. There have been only two IDAcredits to Nigeria, for US$35.3 million; both are fully disbursed. IFC hasmade five loans to borrowers totalling US$1.7.3 millioni, and six equityinvestments totalling US$4.9 million. of these amounts, US$5.7 million havebeen repaid, cancelled, or sold. Annex II contains a summary statement ofBank loans, IDA credits, and IFC investments, as well as rnotes on theexecution of ongoing projects,

18. As a result of the abrupt clieene in earnings from oil, publicrevenues have fallen sharply, causing many of the ongoing projects to run intoserious counterpart funding problems (as indicated in Annex II). This issuei's particularly acute for some of the state-level agricultural projects. TheBank, the Federal Government, and the relevant state governments have takenvarious measures to alleviate the situation. The Bank has agreed to thereallocation of proceeds and revision of disbursement percentages to speed updisbursements, and the Federal Government has established a development loanstock scheme providing supplementary loans for agricultural developmentprojects in the states. As a result, the prospects for state funding of Bank-assisted projects are now brighter.

19e In view of the efforts made by the Nigerian authorities and theserious foreign etxchange constraints projected for the coming years, wepropose to respond positively to a Federal Government request for additionalfinancial and technical assistance. However, such assistance would not befully effective without some changes ini the country's macro-economic andsectoral policy framework, The Bank is therefore considering, as a priority,fast-disbursing assistance aimed at supporting specific macro-economic andsectoral policy initiatives; this includes, in the first instance, thecurrently proposed fertilizer loan,

20. Provided appropriate policy changes are undertaken, an expanded Banklending program would aim primarily at the urgent diversification of Nigeria'seconomy to reduce its excessive dependence upon petroleum as a soilrce offoreign exchange and fiscal revenue. At the same time, the Bank wouldcontinue to support efforts to raise the producti-itv of the lowest incomegroups and thereby diminish the incidence of absolute poverty in Nigeriac Asin recent years, the Bank would continue to provide -major support to agri-culture and rural development, with particular emphasis on institution-building and transfer of technology. These objectives are in line with theFederal Government's priorities under the Fourth Plan, which places con-siderable emphasis on agriculture, and emphasizes thae need to use the proceeds

- 7 -

of the country's oil revenues to increase the productive capacity of theeconomy, and thereby raise the standard of living of its population, parti-cularly the rural poor. The Bank would similarly support efforts to stimulate

a well-balanced and integrated development of Nigeria's industrial sector.This approach would entail a combination of intensive sector work, policydialogue with the Government, as well as Bank assistance for industrialprojects in crucial subsectors.

21. Projects in agriculture and industry together should account for alarge share of Bank lending in the coming two or three years. Effectivesupport for the commodity producing sectors will also require strategicinvestment in production-related infrastructure. There are good opportunitiesfor the Bank to make a significant contribution in energy, water supply, andhighway maintenance. Similarly, there is a strong case for continued lendingfor education. In this context, vocational, technical, and teacher trainingwould be given special emphasis. Finally, the Bank would support the Federaland state governments' efforts to spread the benefits of growth to the socialsectors. It is envisaged that some of the pressing problems of rapid urbani-zation will continue to be addressed through a number of urban developmentprojects focussed on the needs of the urban poor. The Bank is also con-sidering a request from the Federal Government to assist in overcoming thecountry's health problems, and has started a dialogue with the Government onpopulation issues.

22. Although annual disbursements have increased from US$52 million inFY1978 to nearly US$167 million in FY1983, Nigeria's disbursement performancehas lagged behind that of other countries in the region. In the last threeyears, undisbursed balances have progressively increased and now stand at 51percent of the US$2.1 billion in loans and credits approved. One of thereasons for this development is the rapid expansion of the Bank's loanportfolio since 1979 as well as the fact that a number of large loans, withrelatively large, planned disbursements during the early years, were extendedduring this period, mainly for agricultural projects. In many cases, however,disbursements have been slowed by long delays in loan effectiveness andinstitutional and management problems. Recently, the inadequate counterpartfunding of projects by Federal and state governments, resulting from lower oilrevenues, has further slowed disbursements. The disbursement record inagriculture has been mixed. At least until recently, disbursements have beengenerally faster in the case of integrated agricultural development projects,but substantial shortfalls compared to appraisal projections have beenregistered in the tree crop, forestry, and livestock subsectors. Similarly,education and power projects have been particularly slow in disbursing. TheFederal Government, with the assistance of the Bank's Resident Mission, is nowcarefully monitoring loan disbursements with a view to identifying problemsearly and taking corrective action. Also, the Bank has recently agreed to aseries of measures aimed at accelerating disbursements under both ongoing andnew projects (para. 18). These efforts are beginning to show results.

PART III - THE AGRICULTURAL SECTOR

23. Agriculture continues to be the leading non-oil sector in Nigeria,directly supporting about 60 percent of the population, providing 23 percentof GDP, 5 percent of total exports, and 62 percent of non-oil exports. Ofabout 17 million ha of annually cropped land, only 5 percent is irrigated.

The level of production technology is low9 and the traditional rainfed farmingsystems predominate. In recent years, the increasing spread of education anddevelopments in non-agricultural sectors, combined with the drudgery oftraditional agriculture have encouraged the drift of rural youth to urbanareas. The overall effect of all these factors has been that total agri-cultural output remained stagnant cluring the last decade. In particular,production of staples (yam, cassava, sorghum, millet, maize, rice, and wheat)grew at about 1 percent per year, whereas overall food demand is estimated tobe growing at the rate of 3.5 percent per annum., 1/

24. Agricultural production is almost entirely in the hands of small-holders, with the typical unit being a family farm of 2-4 ha. Inadequate useis made of modern inputs, such as fertilizer and improved seeds, and ofmechanized techniques. As a result, yields are very low, and in some caseshave even declined, mainly because of deteriorating soil fertility.

Countr Policiles and Performance

25. Successive governments have emphasized with limited success the needto improve performance in the agricultural sector. In the Third Five-YearDevelopment Plarl (1975-80),the growth rate for agriculture was targeted atfive percent per annum; the estimated actual rate, however, did not exceed onepercent. Annual imports of food rose from about US$300 million in 1974 toover US$2.5 billion in 1981, and agri:icultural exports declined from US$1.5billion in 1973 to nearly US$300 million in 1981. If this trend were tocontinue, it could result in a food deficit in 1'990 of 11 million tons ofgrain equivalent (mtge), about 40 percent of demand, against 2.9 mtge in 1980and 1.2 mtge in 1976.

26. The disappointing performance of the agricultural sector can beattributed in large part to earlier policies which placed strong emphasis onisolated, large-scale irrigation and government-run, intensively mechanizedproduction schemes with generally disappointing production resulits. Littlewas done to develop essential support services for the farming community as awhole, or to develop bottomlands through small- scale, self-help inducedirrigatfon schemes which have the potential of covering 2 millioln ha ascompared to 0.8 million ha in 1978. Despite the declared intentiLons in thePlan, smallholders, who produce over 90 percent of total agricultural output,were not the principal focus of the agricultural strategy. The few governmentsponsored programs for the development of smallholder agriculture sufferedfrom poor management, a shortage of funds, and from being stretched too thinlyin order to cover all states. Against this background, Bank-supported ADPssucceeded in achieving a significant advance in smallholder agriculture.Based on the success of the ADPs and on recognition that past policies topromote agricultural production did nllot achieve their objectives, the FederalGovernment revised its policy to provide maximum support for smallholderproduction in the Fourth National Development Plan (1981-85).

27. The current Development Plan focuses on the smallholder, and aiain toincrease crop productivity through the adoption of available technology of

I/ Nigeria: Fourth National Development Plan, 19381-85, Vol. 1, page 76,

- 9 -

improved seeds as well as the use of scientific inputs like chemical ferti-lizers and pesticides. The Plan envisages simultaneous institutional reformand infrastructural support. The ADP approach of enclave projects hasrecently been extended to cover the entire states of Bauchi, Kano, and Sokoto;a similar project for Kaduna State has been negotiated. The Federal Govern-ment's intention is to progressively extend the ADP approach to the wholecountry. Since manpower and funding constraints prevent immediate replicationof a full-fledged ADP model in all of the 19 states, core components of theADP program are first being introduced in the country as AcceleratedDevelopment Areas (ADAs), now called phased ADPs; these will be upgraded whenthe fiscal and manpower resources improve. Phased ADPs have already beeninitiated in Borno and Gongola States; additional projects are being preparedunder ATAP (Loan 2029-UNI). The Bank has been asked to assist these phasedADPs.

28. While an indepth analysis of three ADPs has shown that ADPs have beensuccessful in achieving an impressive growth rate in agricultural production(over 6 percent per annum in ADPs between 1975 and 1980 against the nationalaverage of 1 percent), the implementation of many ADPs has significantlyslowed down over the past year, largely because of serious local fundingconstraints, particularly of the state governments, occasioned by the steepdownturn in oil revenues. This has led to delays in the expansion ofinfrastructure and agricultural services, as well as gross under-utilizationof project plant, equipment, and expertise. The Bank has worked closelyduring the last several months with the Federal and State Governments, andexplored various avenues to alleviate the ADPs funding problems. As a result,in the context of the proposed fertilizer loan, the Federal Government hasagreed to provide special loans (called development loan stock) in 1983, 1984,and 1985 to assist state governments in meeting their financial obligations tothe ADPs by reducing the states' funding share from about 35 percent to 20percent of project cost. The Bank, on its part, has also taken measures toimprove the flow of loan funds to ADPs (para. 18).

Development Constraints and Potential

29. The technology for enhancing crop yields is available in Nigeria, andhas been demonstrated in ADPs. In particular, extended fertilizer trials inseveral states have shown a highly favorable crop response (i.e. units ofincremental yield per unit of fertilizer nutrient application). For instance,sorghum, a major cereal crop in Nigeria, has shown mean crop response ratesranging between 5.8 and 7.2 in different ecological zones; millet has shown ahigher mean response varying from 6.3 to 18; the maize response has fluctuatedbetween 7.1 and 14.4; and that of groundnut between 9.6 and 17.6. 1/ Theadoption of new technologies is, however, constrained by an inefficient inputsupply system, and inappropriate government policies, mainly regardingsubsidization and agricultural credit.

30. Among farm inputs, fertilizer is the most expensive and most bulky,and its procurement and distribution is the responsibility of Government

1/ Source: Various FAO Reports to the Government of Nigeria between1970 and 1979 on fertilizer programs in different states.

- 10

(paras. 42 and 43). Because of serious inefficiencies in this system,fertilizer use has not been fully esffective desDite a five-fold increase inimports between. 1978 and 1981. There has been considerable wastage and acontinuing mismatch between requirements and supplies in terms of products,timing, and quantities.

31e Substantial subsidies have encouraged -he inefficient use offertilizer, and they have also placed an unsustainable financial burden onGovernment, and absorbed resources which could have been utilized morebeneficially elsewhere in the sector0 The Federal Government has lately beenconcerned about the rising subsidy burden. A subcommittee of the NationalCommittee on Rural Development has examined the pricing and subsidy issue9 andrecommended, inter alia, a phased reduction of subsidies.

32. The distribution of two other inputs, seeds and pesticides, is not soseverely constrained. In the case of seeds, the Federal Governm,ent has takenthe initiative iin creating adequate institutional9 physical, and manpowerinfrastructure, including the issuance of a national seed policy for multi-Dlication of improved seeds, establishment of a National Seed Service (NSS)and of seed processing plants and laboratories, and the organization of aseries of training courses. Seed production is now unidertaken on a few NSSfarms and many state seed multiplication farms. The state seed productionprograms, however, have not been immaune from furnding constraints, nor have theseed quality standards been rigidly adhered' to. Seed pricing and marketingpolicies, as well as linkages between the breeder, foundation, and certifiedseed producers are still unclear. The private sector is becoming involved inthe production of seeds and seed marketing. In the case of pesticides, thepublic and private sectors co-exist, and the retail network is developing tomeet demand. Since some of the pesticides, particularly herbicides, areexpensive, there is an increasing need for farm credit (para. 34).

33. The marketing of food crops is usually done by private traders, andis on the whole fairly competitive. The Federal Government's TechnicalCommittee on Producer Prices determines the guaranteed minimum prices for themajor grain crops every year. These prices are generally much lower than theprevailing market prices; therefore, state intervention through the NigerianGrains Board has seldom been necessary.

34, An emerging constraint relates to agricultural credit. As fertilizersubsidies decline and retail prices rise, farmers' cash requirements will risesignificantly. Increased use of pesticides, including herbicides, to providethe necessary plant protection coverage to safeguard the increased cashMivestments in fertilizers will also have to be financed. Cash is alsorequired to pay for high-cost hired labor which is progressively replacinglow-cost family labor (due to migration from rural to urban areas). Thecredit issue would be addressed through a study unrder the proposed loan (para,54).

35. Feeder roads for the transport of inputs and crops to and fromproduction areas, other infrastructure, and institutional facilities, such asextension 9 research, and marketing need strengthening, These needs are beingadressed under ADPs but, in noi-ADP areas, infrastructural deficiencies still

constitute a problem. They are now expected to receive attention, even thoughlimited, under the proposed phased ADPs (para. 27).

- 11 -

36. Given an appropriate policy framework, adequate institutional andinfrastructure support, and measures to overcome some of the constraintsmentioned above, Nigeria has the potential of achieving significant agri-cultural production increases over the next few years, and fertilizer has amajor role to play.

The Fertilizer Subsector

37. Eleven different types of nitrogenous, phosphatic, and potassicfertilizers are used by Nigerian farmers to increase crop yields. Inaddition, small quantities of micronutrients are also used on deficientsoils. Nigerian farmers are well aware of the benefits of fertilizer use,though efficiency aspects need a greater focus.

38. The Fourth National Development Plan has committed 35 percent of theagriculture sector outlay to the fertilizer subsector to promote intensivefertilizer use as a means of reversing growing food deficits in the country.Of the planned increase of 3.4 million tons of grain equivalent (mtge) by theterminal year (1985) of the Plan, fertilizer is expected to contribute 2.0mtge. To achieve this, the Plan proposes a consumption level of 1.3 milliontons of fertilizers, approximately equal to 430,000 tons of nutrients (16.5 kgper ha) in 1985.

Fertilizer Consumption

39. Reliable fertilizer consumption statistics are not available.However, it appears that Nigeria's fertilizer consumption rose from 0.27 kg ofnutrients per ha in 1970 to about 12 kg in 1981, but declined to 8.5 kg in1982 due to import constraints (para. 44) leaving much unsatisfied demand inan environment of acute shortages. By 1985, this figure would have to rise to16.5 1/ to meet the Plan target of fertilizer consumption. The factors whichfavor increased fertilizer use in Nigeria are: low soil fertility coupledwith low levels of existing plant nutrient use, an assured productionresponse, a favorable benefit-cost ratio, and the heavy dependence of new farmtechnology on increased use of fertilizers.

Domestic Production

40. The first local fertilizer plant, with a designed production capacityof 100,000 tons of single super-phosphate, was set up in the public sector(under the Federal Ministry of Industries) at Kaduna in 1976. Its actualproduction has varied between 20,000 tons and 45,000 tons per year due totechnical and managerial constraints. As a result, its contribution to thenational fertilizer requirements of around a million tons has been ratherlimited.

1/ Some comparable numbers for the year 1979-80 from other countriesare: Ivory Coast 13.5 kg, Morocco 28.9 kg, Algeria 23.1 kg, Libya 23.5kg, Liberia 11.3 kg, Israel 206 kg, Bangladesh 45 kg, South Korea 384kg, Pakistan 52 kg of nutrients per hectare of arable Land. The worldaverage is 77 kg; for Africa, it is 15.6 kg.Source: 1980, FAO Fertilizer Year Book.

- 12 -

41e Nigeria is now planning a major increase in domestic production inthe late 1980s, when a fertilizer complex, the National Fertilizer Company ofNigeria (NAFCON)--a joint venture of the Federal Government and M.W. KelloggCo. of USA--is scheduled to go on stream at Onne, near Port-Harcourt. In theinitial years, NAFCON would be managed by Kellogg. This plant would have aproduction capacity of 1,000 tons of urea and 1,500 tons of different gradesof NPK per day, and is expected to contribute more than 60 percent (in case o-ru-rea 100 percent) to the likely consumption in 1987. However, when this plan-:>goes into production, logistical integration of domestic and irnported ferti-lizer streams and recalculation of costs and subsidies would become an impor-tant task. The Bank has been asked to assist in the financing of the proposedplant; thls request is under consideration.

Procurement and Distribution

42. In 1976-77, the decentralized system of fertilizer imports wasrepiaced by at centralized arrangement under which the full procurement anddistribution cycle was controlled by the Federal Government. This change wasinspired by the Government's desire to gain leverage in the internationalmarket by consolidating the fragmented purchases of individual states and toproperly coordinate the arrival of fertilizer ships to avoid congestion anddelays at Nigerian ports. The Government also introduced a uniform retailselling price for each product throughout the country to overcome the problemof inter-state smuggling caused in the past by differences in retail prices,In effect, the Government took over the responsibility of funding the cif,Liandling, and transportation costs of fertilizer to the states, as well as ofsharing the fertilizer subsidy with the states according to an agreed formula(Federal Government: 50 percent, states: 25 percent, farmers: 25 percent)with reference to the landed cost of fertilizer at the state capitals 1/. Theabove responsibilities, including transport of fertilizers to the states, wereentrusted to a Fertilizer Procurement and Distribution Division (FPDD) createdunder the Federal Ministry of Agriculture.

43. At the state level, fertilizer is generally received by the stateministry of agriculture which arranges for its storage, internal transpor-tation, and retail sale through agro-service centers and local governmentrepresentatives in non-ADP areas; in ADPs, the commercial units or inputsupply companies of the projects sell fertilizers through farm servicecenters. The arrangements for monitoring of stocks, deliveries, sales, and-losses are practically non-existent in non--ADP areas.

/ This arrangement ignored the i-ntra-state storage, transport,handling, and retailing costs which in effect were an additional burdenon the state governments. Moreover, the uniform retail selling price9fix.ed by the Federal Government for the whole country, was not relatedto costs; it remained unchanged for a number of years, while costscontinued to fluctuate. In practice, the farmers' share in the farmgatecost worked out only to about 15 percent.Despite the official cost-sharing formula, the state governments havenot been able to make any contributions in recent years and allrertilizer subsidy payments have therefore, in practice, been made bythe Federal Government.

- 13 -

Major Constraints in the Fertilizer Subsector

44. Funding Constraints. Although the fertilizer sector is an exclusivepreserve of government, its funding has seldom been commensurate with needs.Government budgets must provide for all cash flow requirements for fertilizerimports, handling, transportation, storage, and marketing. In practice, therehas been continual uncertainty about the quantity and timely availability offunds to pay for the imported fertilizers as well as their distribution andmarketing costs. Lately, the budget cuts have become substantial. Thefederal 1983 budget for fertilizers has been cut to N75 million which canfinance the import and distribution of only about 350,000 tons of fertilizersas compared to actual distribution of over one million tons in 1981 and639,000 tons in 1982.

45. Policy Constraints. Two important policy constraints relate topricing and subsidization and fertilizer marketing. With a uniform country-wide retail selling price, government subsidy amounts to about 85 percent oftotal cost and farmers pay only 15 percent. While the effective retailprices, averaging N42 per ton, have remained unchanged in the last few years,the Government's fertilizer imports have risen from a mere 50,000 tons in 1976to one million tons in 1981. The subsidy implications of this quantity havebeen such that the fertilizer imports had to be severely cut. The fertilizerpricing policy has, in fact, become a major impediment to agriculturaldevelopment. On the one hand, fertilizer availability has been severelycurtailed, thereby jeopardizing the success of ADPs and other food productionprograms; on the other hand, very low fertilizer prices, coupled with limitedsupplies, have encouraged fertilizer black marketing at substantially higherprices. Very low retail prices have also encouraged inefficient use andpossible smuggling across the borders. As to the second constraint, thepresent policy of complete government involvement in fertilizer distributionand marketing has made the system both expensive and inefficient. Apart fromincreased efficiencies, the involvement of the private sector and a commercialapproach would relieve the Government of having to budget for total cash flowneeds; only the fertilizer subsidy would have to be provided in governmentbudgets.

46. Organization and Management Constraints. FPDD, which handlesfertilizer importation and distribution to states, does not have theorganizational structure, or the planning system and management methods, tohandle effectively its complex responsibilities arising out of rapidlyincreasing demand from the states. FPDD was studied in detail by a committeeappointed by the President of Nigeria in 1981 (Gebenbichie Committee). Thiscommittee reported that FPDD's structure, strength, and skills wereinadequate, and recommended restructuring and strengthening.

47. The inadequacies of FPDD have increased costs at different stages ofthe fertilizer marketing chain. Poor knowledge about carry-over stocks indifferent states, combined with unplanned despatches to various destinationsfrom the ports, have increased the states' inventory management problems,leading to waste and avoidable losses. FPDD's transportation of fertilizersfrom five ports to 19 states has been predominantly by road, whereas ajudicious multi-modal mix involving road, rail, and inland waterways couldhave resulted in considerable savings. The entire operation is vast and

- 14

complex, and only a carefully drawn up, coordinated import-supply plan, whichtakes note of monthly product requirements of different states, can bringabout a substantial reduction of costs.

48. Distribution problems are further compounded at the state and farmlevel because of poor handling by state and local government functionaries.State retailing costs range between N35 to N69 per ton, when a significantlysmaller distribution margin to the private sector could have done the job moreefficiently.

PART IV - THE LOAN

49. The proposed loan was appraised by a mission which visited Nigeria inMarch - April 1983. This mission was preceded by three missions to discuss indetail Government's fertilizer policies and programs. Senior FederalGovernment officials also visited Washington in December 1982 and April1983. These discussions have contributed to important policy decisions by theGovernment in the fertilizer subsector. Negotiations were held at the Bank inJune 1983; the Nigerian delegation was led by Dr. R. 0. Mowoe of the FederalMinistry of Finance. Further information on the Loan is given in Annexes IIIand IV.

Loan Objectives

50. The Loan has three major objectives. First, to ensure the adequateand timely supply of fertilizer to all Bank-assisted ADPs and other agri-cultural areas for the 1984 and 1985 crop years at a time of acute foreignexchange constraints (para. 16). Second, to assist the Federal Government inrestructuring its fertilizer policy, including pricing, subsidization,procurement, and marketing, to make it an efficient and effective instrumentof agricultural development. And third, to ensure additional FederalGovernment support to states for funding ongoing Bank-assisted ADPs throughimplementation of the development loan stock scheme (para. 28).

Loan Description and Administration

51. The Loan would assist in the financing of about 2.0 million tons offertilizer imports required by Nigerian farmers for the 1984 and 1985 cropyears. Since expenditure on fertilizer imports is incurred several monthsbefore its actual use, foreign exchange expenditures would begin in November1983 for the crop year 1984 and in November 1984 for the crop year 1985.Apart from part of the foreign exchanige cost of fertilizers, the Loan wouldalso finance the cost of studies to develop a fertilizer policy framework, thecost of communication equipment (tele!x and/or radio), and the domestic andoverseas training of key FPDD personnel.

52. The demand for fertilizer is estimated at 895,000 tons (321,200nutrient tons) and 1,272,000 tons (459,205 nutrient tons) in 1984 and 1985,respectively; the indigenous production would contribute 60,000 tons of singlesuperphosphate (10,800 tons of nutrients) in each of these years, and thebalance would therefore have to be imported. The 1985 requirements include asmall buffer of nearly 200,000 tons. These projections, though 10 percentlower than the Plan estimates in nutrient terms (para. 38), are consideredrealistic in view of the present level of fertilizer use and the projected

- 15 -

price increases. The nutrient balance (N:P:K ratio of 3:2:1) proposed for1984 and 1985 is agronomically appropriate, and consistent with past trends.

53. The Director of FPDD would be responsible for administering andmonitoring the program. To this end, FPDD has been strengthened with threeinternationally-recruited experts in the fields of procurement, marketing andlogistics, and finance and accounts, who are being financed under ATAP (LoanNo. 2029-UNI). Taking into account the timing of fertilizer requirements indifferent agro-ecological zones, the capacity of ports and the transportationsystem to handle fertilizers, and also the relative inaccessibility of severalareas during the rainy season, FPDD has planned the arrival of the fertilizershipments between November 1983 to March 1984 for the 1984 crop season. Thisschedule would ensure timely availability of fertilizer to farmers, which isan important objective of Bank assistance. NAFCON would assume responsibilityfor fertilizer procurement and distribution from the 1985 crop season(para. 63).

54. The Loan would also finance the following studies to be completed byJune 1984, so that their recommendations could be considered in determiningthe pricing and marketing arrangements for the 1985 crop season:

i) fertilizer transportation and storage optimization study;

ii) credit plan for short-term crop production loans to farmersand distribution credit for NAFCON, wholesalers, and retailersof fertilizers; and

iii) Legal and regulatory framework for fertilizer subsector e.g.fertilizer specifications, packaging, pricing, qualitycontrol, and registration of dealers.

The terms of reference of these studies were agreed with the FederalGovernment during negotiations.

55. The Federal Government would maintain a separate budget category forfertilizer subsidies to enable a clear assessment of subsidy levels (Section3.06 of the Loan Agreement).

Cost and Financing

56. The total cost of fertilizer imports and internal distribution isestimated at US$833 million (N555 million) of which the foreign exchangecomponent would amount to US$418 million (N279 million) or about 50 percent.A breakdown of cost by major categories is given in the Loan Summary and inAnnex IV (tables 1-4). Allowance has been made for price contingencies forfertilizer imports equal to 7.5 percent for the 1984 crop year and 12 percent

- 16 -

for the 1985 crop year as well as for local costs estimated at 7.5 percent forthe 1984 crop year and 13 percent for the 1985 crop year. 1/

57. The proposed loan of US$250 million (N167 million) would finance 30percent of total costs (60 percent of the cif cost of fertilizer imports, and100 percent of the cost of studies, foreign training, and communicationequipment for FPDD and the front-end fee). The loan would be divided into tctranches reflecting the two crop years. The first tranche would not exceedUS$121.2 million (fertilizer purchases of about: US$119 million and other itemsof about US$2 million); the second tranche of US$128.8 million for the 1985crop year would be applied solely to the purchase of fertilizers. TheNigerian share would amount to US$582.4 million, or 70 percent of total costs(Loan Summary and Annex IV, tables 1 and 2). This comprises 40 percent of theforeign exchange cost of fertilizer and 100 percent of the domestic cost. Theprogram implies Federal Government contributions of N32 million (foreignexchange N15.8 million) in Nigerian fiscal year 1983, N138.5 million (N49.6million) in 1984, and N150.4 million (N46.8 million) in 1985. It was agreedduring negotiations that the Federal Government would (i) import about 835,000tons of fertilizer for 1984 and about 1,212,000 tons for 1985 2/; (ii) makemonthly deposits of their share of foreign exchange costs in a designated bankaccount abroad in accordance with ELn agreed schedule of payments; (iii) ensuresatisfactory arrangements for the full funding of foreign exchange and localcosts of the program. These would, inter alia, enable NAFCON to meet itstotal cash flow needs under the program. The latter point would be acondition of disbursement of the second tranche of loan (Sections 3.07 andSchedule 1, para. 4 of the Loan Agreement), and the first monthly payment ofUS$4.8 million by the Federal Government into its designated bank accountabroad would be a condition of effectiveness of the loan (Section 6.01 of theLoan Agreement).

Policy Environment and Organizational Restructuring

58. In the context of discussions leading up to the proposed Loan , theFederal Government has recently taken a number of decisions to modify itspolicies in the fertilizer subsector, including: (a) to significantly reducesubsidies over the next 5 years; (b) to transfer the responsibility for theimportation and distribution of fertilizer from FPDD to NAFCON; (c) tostrengthen the staffing of FPDD to improve the cost-effectiveness of its 1984operations; (d) to commercialize fertilizer operations and retail business;and (e) to establish a National Fertilizer Technical Committee to guide andcoordinate fertilizer sector programs and policies.

1/ Since fertilizer import contracts are expected to be signed aroundOctober 1983 for the 1984 crop year, price contingencies for six monthsover base costs as of April 1983 have been assumed. Import contractsfor the 1985 crop year are expected to be signed in September-October1984; therefore, price contingencies for one year over base costs as ofOctober 1984 have been assumed.

2/ The balance 60,000 tons (10,800 nutrient tons) is expected to comefrom the domestic plant in each of these two years.

- 17 -

59. During negotiations, the Federal Government has agreed to at leastdouble the retail price of each fertilizer product for the 1984 crop year andreduce fertilizer subsidies to no more than 50 percent of total cost for the1985 crop year and to 25 percent by the 1988 crop year (Section 3.05 (a) ofthe Loan Agreement). This would result in a reduction in subsidies in 1984 ofabout N38 million and in 1985 of about N108 million (Annex IV, table 6). Theannouncement of the revised prices, which would be uniform for the wholecountry (Section 3.08 of the Loan Agreement), would normally take place inearly November, when the fertilizer sale season is over. However, this wouldbe difficult in 1983 as, following the general election, the new Governmentwould only be in position at that time. It has therefore been agreed that thenew prices will be announced no later than January 1, 1984. Agreement on theprices for the 1985 crop year would be a condition of disbursement of thesecond tranche of the Loan (Section 3.05 (b) and Schedule 1, para 4 of theLoan Agreement).

60. While the Federal Government has agreed to raise fertilizer pricesfor the 1985 crop season to reduce the subsidy level to no more than 50percent, the final price would be determined in late-1984 on the basis of ajoint review by Government and the Bank of the effects of the 1984 priceincrease. This review would take into account fertilizer offtake informationfor 1984, as reported by the states, and APMEPU's evaluation of the effect ofthe fertilizer price increase on demand through its modified agronomic surveyfor Bank-assisted ADPs (Section 3.05 (c) of the Loan Agreement).

61. The proposed increases in fertilizer prices in 1983 and 1984 are notlikely to unduly affect the growth in fertilizer consumption because, first,the benefit-cost ratio of fertilizer use will still be favorable, and second,the improved and timely fertilizer availability under the new arrangementswill meet hitherto unsatisfied demand. However, the situation would bemonitored and each announcement of price increase would be preceded by areview of the effect of earlier price increases on demand.

62. The total fertilizer subsidy is also expected to be reduced throughthe implementation of several other cost reduction measures such as fertilizerpurchases through international competitive bidding, greater use of high-analysis fertilizers, more economical inter-modal transportation mix, improvedinventory management, and retailing through private trade channels. Thesavings from international bidding procedures have been taken into account inpreparing the cost estimates; other savings are expected to accrue over theperiod of the loan, particularly for the crop year 1985, following the imple-mentation of the recommendations of the studies financed under the LoanAgreement between the Federal Government and the Bank on the package ofcorrective measures would be a condition of disbursement of the second trancheof the Loan (Section 3.11 (b) and Schedule 1, para. 4 of the Loan Agreement).

63. The Federal Government's decision on the commercialization offertilizer operations is of major importance. Fertilizer importation,distribution, and marketing is now proposed to be entrusted to the newlyestablished commercially-operated NAFCON. The company is presently engaged,inter alia, in recruiting staff for its marketing operations which, prior toits new factory coming on stream in the late eighties, would assume respon-sibility for importing and distributing fertilizers. This is planned for thesecond half of 1984, by which time a network of retailers would have been

- 18 -

appointed, in time for the 1985 season. In the meantime, for the crop year1984, the work of fertilizer importation and distribution will continue to bethe responsibility of FPDD. Although FPDD has recently been strengthenedth-rough the recruitment of three foreign specialists (para. 53), it will befurther strengthened at the middle management level with eight new, localappointments (market intelligence, port operations, fertilizer distribution,-rail and road movement accounts, administration, and law) by September 30,1983 (Section 3.10 (a) of the Loan Agreement). These arrangements, comblnledtwith procurement under international competitive bidding procedures, wouldconstitute the first major step in developing an efficient and cost-effectivefertilizer import and distribution system at the national level. At the statelevel, no significant improvement in the handling and retailing of fertilizeris expected in the first year. However, one important step towards thecommercialization of the process would be that during 1984 the agriculturalinput supply companies or other organizations entrusted with the task ofdistributing and retailing fertilizers in the states would have to makepa,vment to the Federal Government wi,ithin sixty days of the receipt of ferti-lizers of at least the retail price less the agreed in-state distributioncosts 'Section 3.09 of the Loan Agreement).

64, NAFCON has a broad directive to follow the recommendations of IFDC'sFertilizer Marketing Study 1/ in developing organizational and mnarketingplans. The IFDC has proposed the division of the country in 14 distributionzones with storage and transshipment facilities, 100 sales territories, andthe appointment and training of about 30 retailers for each sales territory.NAFCON would continue to use the infrastructure of farm service centers inADPs to retail fertilizers which woluld enable NAFCON to concentrate initiallyon the creation of a retail network in non-ADP areas where the marketingsystem is weak. The study also proposes criteria for the selection ofretailers, and fertilizer promotion through a research and demonstrationprogram, soil testing, organization of farnmer field days, advertising,exhibitions, and radio programs. A detailed marketing and funding plan forthe 1985 crop season and a timetable for implementation will be prepared byNAFCON by June 1984, and agreement between the Goveernment and the Bank on thepreparation of the plan and the timetable for implementation would be acondition for the release of the second tranche of the proposed ILoan (Section3.11 (a) and Schedule 1, para. 4 of the Loan Agreemert).

65. The IFDC study visualizes product ownership by NAFCON to the point ofretail sale. Short-term credit would be required by retailers, commercialunits of ADPs, input supply companies, and NAFCON to finance stocks. Theproposed credit study (para. 54) would address how these needs should be met.

66. After the transfer of the responsibility for fertilizer importationand distribution to NAFCON, FPDD would be restructured to perform non-commercial tasks such as assisting the Federal Government in (i) studyingpolicy issues, e.g., pricing and subsidy, buffer stocks, marketing; (ii)

prepariag 5-year plans for fertilizer consumption and promotion and decidingupon annual consumption targets in consultation wiLth the Green Revolution

.1 Study by International Fertilizer Development Center (MuscleShoals, USA) for the Federal Ministry of Industries in 1980.

- 19 -

Council, NAFCON, and the states; (iii) monitoring fertilizer availabilitythroughout the country; and (iv) creating and enforcing a legal base forfertilizer production, marketing, pricing, and quality control. FPDD wouldalso administer fertilizer subsidy programs and budgets, and monitor the worldfertilizer situation, policies, and trends. These important tasks havehitherto been overshadowed by the priority given to handling the importationand transportation of fertilizers.

Procurement and Disbursement

67. Contracts for fertilizer imports would be provided through inter-national competitive bidding in accordance with Bank guidelines. Equipment,amounting to less than US$0.3 million, would be procured on the basis of localcompetitive bidding following procedures acceptable to the Bank. The servicesof consultants, estimated at about US$1.1 million, would be obtained on termsand conditions acceptable to the Bank, and training, both local and overseas,costing not more than US$0.3 million, would be arranged in consultation withthe Bank.

68. Disbursement of the Bank loan would take place in FY84 and FY85(Annex IV, Table 5). Disbursement would be made against standarddocumentation on the basis of 75 percent and 50 percent of the cif cost offertilizers respectively for 1984 and 1985 crop years and 100 percent of thecost of studies, technical assistance, training, and equipment. Disbursementconditions of the Loan are detailed in para. 73.

Accounts and Audits

69. The accounts and the accounting system of FPDD need strengthening.It would be a primary task of the internationally recruited financialspecialists to do this. The Federal Government would require to keepfinancial records in accordance with sound accounting practices to reflect theoperations and financial position of FPDD and NAFCON. Further, the FederalGovernment would have these accounts audited annually by independent externalauditors acceptable to the Bank.

Justification and Risks

70. The Loan would assist the Federal Government in meeting the demandfor fertilizers at a time of acute foreign exchange constraints. Investmentin fertilizer shows a high return on investment. It is estimated that itwould result in an estimated incremental production of 2 million tons of grainequivalents (mtge) in 1984 and 2.3 mtge in 1985. Even at wholly unsubsidizedfertilizer prices, the economic benefit-cost ratio remains above 2, theaccepted minimum norm for attracting fertilizer use. Since fertilizer use isneutral to scale, and since over 90 percent of Nigerian farmers are small-holders, the distribution of benefits of fertilizer use would be equitable.

71. The loan would also allow the Federal Government to provide, althoughindirectly, additional funding to the ongoing Bank assisted ADPs (para. 28),thereby reducing the states' share to 20 percent of total project cost. Inview of the importance of this issue, the release of the second tranche of theLoan will be subject to the Bank's receiving adequate assurances from the

- 20 -

Federal Government on the funding of the ADPs (Schedule 1, para. 4 of the LoanAgreement).

72. The program does, however, present certain risks. First, FPDD maynot be adequately staffed and equipped to handle the 1984 crop program withconsequent delays and wastage. To reduce this risk, the FPDD is beingstrengthened by additional international and locally recruited staff, andphysical progress will be closely monitored. Second, there is a risk that,despite the required marketing plan, NAFCON will not be ready to assumeresponsibility for fertilizer procurement and distribution in time for the1985 crop year. In such circumstances, the Bank would have to considerwhether alternative and satisfactory arrangements could be made and which,inter alia, would not prevent the release of the second tranche. Third,Government may, in the event, be unable to provide its share of the foreignexchange fundls and the required local currency. The agreement provides thatthe Bank and Nigeria will jointly disburse against fertilizer deliveries on apro-rata basis which should provide a systematic arrangement or an earlywarning of such difficulties. If this were to be a local currency shortfall,thus inhibiting internal distributi'on, the Bank would have no option but towithhold the release of the second tranche funds. Fourth, the projectedincrease in fertilizer prices may lead to an undesirable drop in demand,thereby making it difficult to realize the national food production targets.This risk would be taken care of by the system of guaranteed minimum pricesannually fixed by the Federal Government; additionally, the Loan provides foran annual review of the effects of earlier price increases (para. 60).

PART V - LEGAL INSTRUMENTS

73. The draft Loan Agreement between the Federal Republic of Nigeria andthe Bank and the Recommendation of the Committee provided for in Article III,Section 4 (iii) of the Articles of Agreement are being distributed to theExecutive Directors separately. Special conditions of the Loan are listed inSection III of Annex III. These include the first monthly payment of US$4.8million by the Federal Government into its designated bank account abroad as acondition of effectiveness and the following conditions of disbursement:

(i) Bank disbursements would not exceed US$40 million or extendbeyond January 1, 1984 (whichever is the earlier) in thecircumstances where the Federal Government had not made publicthe prices applying to the 1984 season;

(ii) Limitation of Bank dlisbursement to an aggregate amount ofUS$121.2 million unless:

(a) NAFCON had prepared a satisfactory detailed marketingand funding plan, and agreed with a timetable for itsimplementation;

(b) the Bank and the Federal Government had agreed onretail prices for each type of fertilizer for the 1985crop year, and the Federal Government haci made thispublic;

- 21 -

(c) the Bank and the Federal Government had agreed on apackage of measures to be used to reduce fertilizersubsidies;

(d) the Federal Government had made satisfactoryarrangements for the full funding of the foreignexchange and local costs of the fertilizer program;and

(e) the Federal Government had made satisfactoryarrangements for the adequate funding of ADPs.

74. I am satisfied that the proposed Loan would comply with the Articlesof Agreement of the Bank.

PART VI - RECOMMENDATION

75. I recommend that the Executive Directors approve the proposed loan.

A. W. ClausenPresident

AttachmentsAugust 24, 1983Washington, D.C.

- 22 -ANNEX IPage 1 of 5

NIGERIA - SOCIAL INDICATORS DATA SHEETNIGERIA REFERENCE GROUPS (WEIGHTED AVERAGES) ja

MOST (MOST RECENT ESTIMATE) /b/b /b RECENT MIDDLE INCOME MIDDLE INCQME

1960~- 1970- ESTIMATR-- AFRICA S. OF SAHARA N. AFRICA 6 M7D EASTAREA (THOUSAND SQ. EM)

TOTAL 923.8 923.8 923.8AGRICULTURAL 412.8 4 9 7.4 512.9

GSP PRR CAPITA (0IS$) 200.0 330.0 870.0 1L47.9 1340.0

ENERGY CONSUMPTION PER CAPITA(KILOGRAMS OF COAL EQUIVALENT) 29.0 51.0 169.0 724.2 810.4

POPULATION AND vPTAL STATISTICSPOPULATION,MID-YEAR (THOUSANDS) 51598.0 66182.0 87603.0URBAI POPULATION (I CF TOTAL) 13.1 16.4 20.9 28.5 47.4

POPULATION PROJECTIONSPOPULATION IN YEAR 2000 (MILL) 169.1STATIONARY POPULATION (MILL) 623.4YEAR STATIONARY POP. REACHED 2140

POPULATION DENSITYPER SQ. KM. 55.9 71.6 91.7 56.5 36.0PER SQ. 1KM. AGRI. LANO 125.0 133.0 165.2 131.8 449.0

POPULATION AGE STRUCTURE (Z)0-14 YRS 45.4 46.6 47.7 45.9 43.9

15-64 YRS 52.3 51.0 49.9 51.2 53.865 AND ABOVE 2.3 2.4 2.4 2.8 3.3

POPULATION GROWTH RATE (Z)TOTAL 2.4 2.5 2.5 2.8 2.9URBAN 4.7 4.7 4.8 5.3 4.6

CRUDE BIRTH RATE (PER THOUS) 52.0 50.7 49.6 47.6 42.5CRUDE DEATH RATE (PER THOUS) 25.3 20.8 16.6 15.2 12.0GROSS REPRODUCTION RATE 3.4 3.4 3.4 3.2 3.0

FAMILY PLANNINGACCEPTORS, ANINUAL (THOUS) .. 7.6 33.2/cUSERS (Z OF MARRIED WOMEN) .. ..

FOOD AND NUTRITIONINDEX OF FOOD PROD. PER CAPITA(1969-71-100) 100.0 102.0 92.0 95.7 97.5

PER CAPITA SUPPLY OFCALORIES (7 OF REQUIREMENTS) 83.0 82.0 91.0 97.1 102.3FROTEINS (GRAMS PER DAY) 45.0 44.0 49.0 56.0 72.0OF WHICh ANDIAL AND PFLSE 10.0 10.0 11.0/d 17.2 17.8

CHILD (AGES 1-4) DEATH RATE 42.4 35.0 27.8 23.6 15.2

HEALTHLIFE EXPECT. AT BIRTH (YEARS) 38.7 43.7 49.1 51.9 57.2INFANT MORT. RAIE (PER THOUS) 183.4 158.0 133.0 117.6 104.2

ACCESS TO SA.FE WATER (%POP)TOTAL .. .. .. 25.4 59.3URBAN .. .. .. 70.5 84.9RURAL . 12.3 37.5

ACCESS TO EXCRETA DISPOSAL(% OF POPULATION)

TOTAL .. .. ..URBAN .. ..RURAL .. .. .

POPULATION PER PHYSSCIGN 73710.0 24670.0 12550.0 12181.6 3536.0POP. FER NURSING PERSON 4040.0fe 5071.0 3010.0 2292.0 1820.7POP. PER HOSPITAI. BEDTOTAL 3020.0/h 2220.0 1370.0/f 1075.4 643.3URBAN 430.07e 490.0 370.07 402.3 545.0RURAL 25630.0/e 18490.0 5490.0/f 3926.7 2462.0

ADMISSIONS PER H8)SPITAL BED .. .. .. .. 26.4

NOOSINGAVERAGE SIZE OF HOUSEHOLD

TOTAL .. .. .. .URBAN

4.

7/S ..

RURAL .. .. ..

AVERAGE NO. OF PERSONS/ROOMTOTAL .. .. ..URBAN 3.0 2.2/g .. .RURAL

ACCESS TO ELECT. (Z OF DWELLINGS)TOTAL .. . .. .. 46.2URBAN 81.3

4 2.

4/g .. .. 77. 6

RURAL . . . .. .. 16.1

- 23 A- -23- ~~~~ANNEX IPage 2 of 5

SIGERIA - SOCIAL INDICATORS DATA SHEETN LGERIA REFERENCE GROUPS (WtIGHTED AVERAGES) /a

MOST (MOdST RiECENT ESTIiMATE) /b1960/A 197D~jb RECENT lb MIDDLE INCOMJE MIDDLE INCOftE

0- ESTIMIATE- AFRICA S. OF SAHARA N. AFRICA & MID EAST

EDUCATIONADJUSIED ENROLLAENT VTIUOS

PRIARY; TOTAL 36.0 37.0 98.U 97.2 o9.6NALE 46.0 47.0 .. 103.1 104.8PFE'MALE 27.0 27.0 .. 88.5 72.4

SECONDARY: TOTAL 4.0 4.0 16.0 17.2 41.7MTALE 6.0 6.0 .. 23.5 52.8FEtlALE 1.0 3.0 .. 14.2 31.2

VOCATIONAL (I OF SECONDARY) 4.8 8.5 3.1/i 5.2 10.3

PUPIL-TEACHER RATIOPRItlARY 30.0 34.0 .. 42.9 31.9SECONDARY 19.0 21.0 .. 23.7 23.3

ADULT LITEKACY RATE (N) 15.4/e .. 34.0 37.1 43.3

CONSUMPTIONPASSENGER CARS/TdOUSAND POP 0.6 0.9 1.4/i 18.8 18.0RADIO RECEIVERS/TIOUSAND POP 2.6 19.3 66.1 97.8 138.1TV RECEIVERS/THOUSAND POP 0.0 1.1 5.3 18.6 45.6

UEWSPAPER ("DAILY GENERALINTERCSr") CIRCULATIONPER THOUSAND POPULATION 5.5 4.8 6.9/f 1.2 31.0

CINEMA, AANNUAL ATTENDANCE/CAPITA .. .. 0.4 o.6 1.7

LABOR FORCErOlAL LABOR FURCE (THOUS) 21788.0 25992.0 31635.0

FEMuALL (PEKCENi) 41.3 40.6 39.8 36.1 10.7AGRICULTURE (PERCENT) 71.0 62.0 54.0 56.8 42.5INJOUSIRY (PERCENT) 10.0 14.0 19.0 17.5 27.8

PARIICIPATUIO RATE (PERCENT)TOTAL 42.2 39.3 36.1 37.0 25.6MALE 50.3 47.3 44.0 47-1 45.4FEt'ALE 34.4 31.5 28.4 27.0 5.6

ECONOHIC DEPENDENCY RATIO 1.1 1.2 1.4 1.3 1.8

INCOME DISTRIBUTIONPERCENT OF PRIVATE INCOMERECEIVED BY

HlIGHEST 5% OF lOUSEHOLDS ..

HlUHISsST 20% OF HOUSEHlOLDS ..LOWEST 207 OF HOUSEtHOLDS ..

LOWEST 40% OF HOUSEHOLDS ..

POVERTY TARGET GROUPSESTIMATED ABSOLUTE POVERTY INCOMELEVEL (US$ PER CAPITA)

URBAN .. .. 696.0/k 534.2 276.1RURAL .. .. 341.0)/k 255.9 177.1

ESTIMATED RELATIVE POVERTY ItiCOMELEVEL (USS PER CAP1TA)

URBAN .. .. 621.0/k 491.5 400.0RURAL .. .. 207.o07k 18.1 293.3

ESTIMtATED POP. BELOW ABSOLUTEPOVERTY INCOME LEVEL (N)

URBAN .. .. .. .. 22.0RURAL .. .. .. .. 30.8

.iOT AVAILABLENOT APPLICABLE

N 0 T E S

/a The group averages for each indicator are population-weighted arithmetic means. Coverage of countries among theindicators depends on availability of data and is not uniform.

lb Unless otherwise noted, "Data for 1960" refer to any year between 1959 and 1961; Data for 1970 between 1969 and1971; and data for "Most Recent Estimate" between 1979 and 1981.

/c 1974; /d 1977; /e 1962; /f 1976; /g 1972; /h Including ex-North Cameroon under British administration; /i Certainfields of study previously classified under other second level education of vocational or technical nature are nowreported under general education; /j 1978; /k 1982.

May 1983

-24 - AN'NEX IPage 3 of 5

IIEPINITIONS OP SOCIAL 1iNDIfAT81

Nose I Although the data at draw fro- ore gee"lyjde Itens aIt'll salean reIable, ns Ihudas ontd thatshey waytohroercnuy_op-rble becaus of the 1aco of a-tadardoed def..t-son -d c-ncpta use by dfentcases coltIgtedar.- The dat ar -ntehel-et uo'Lil to

deocribe ardent If sagnlt,cdo i hd mus te-ndo. end -trtrotcosle sajor diff-o-tne

The refornce geouo ars (I the eas ocucsry roup of he subjet totrrrya-d 12) A tuergetup ath --soehat higher a-erge incom shn t co-to group of theeabi ott nuntry (ecept fot'gdgh Inc-oe" hIthoper net seocyohre ''bIddo Itoosshoreir aIlla.and-rIddle fan" Is chsen becaue of es-ogor soco-cfl--ra

atltrs). In he -sfe.e..e gr..up duto t -ergeu oepopulecti _ugtdalhel slefroch Ind ,icato and sb.- only whet -ejoely of the tsohcIgru asdt frIatidnti.Son h cnsg o ontisuno heIdctosdpsd n h nlliteyo an n i o nioelcuInIoth

Otetlsd s eltig ooage f nebnicronnnuho. hes oZ.gs eral y uefu Inp.d tcpahm thivlueo n ncso oasa o h onr oreterasne groups.l -- l I -Pi,lh

Otnu - otalsur aceaea coprsigot area and inlan aes;18,phsco alIeed ePm mdiascoltenertyec.an0 d lilO dao.-eual. erlttn ero-ypaIlatci- le ymobyo euit

Iehas, and rural2) dIolde byebele espesIoIeero heyto -nde

lNP PER CAPITA (All) GNlP per -ale rn ou o as curnen -oeh- Prto-r a-eaIr It publIc en peluabe genres and oe.a.ne nos,.l and

nelculched by __ano --nticn method an laI bath mIss (1971-61 hostel; nohehbituttt cetrs,ioposar srtilh-Iipemnety -rf fed

~1960 1970, an.d 19g; daaIya-oe n hylts oa hac p-ood ing pr-inpallyc oml a

carsaerwooIncude. Or-l hseos,aene,Iecod heath und

ttffto lOtiatiPItyt fIb CafIlo - denual ayperenr coesovyrlon ct reomertoel. yedicid.trussestnotipersenent ly etafted by I phyeitcst (hnb byba a A`el

anI goheie trIcle y) nklgae ol nlaetprcyt pen-lde limited rung of medical tolnls for et-teoa P.rp,e

1960, 1971, and 1980 date.I. Iea hoep,lauls Inlude WliCeprinlalp1/genorl bapaa sd rura

haybao oa ne -ara hoapisls an wedic-l ond eat-tnty coner.

POPULATION all VITAL. STATISTICS Spenialloed hspitssle are Inclded only und-rtrl

TotaEl PopltinMid--yaaj?h-nd ) Is f J.y 1; 1960, 1970, and 198f1 Audwiselon e Bee elld - Treel numbe of adeloi-On boor1 dia-hag-

date. frm opias iided by the -bee of teds.

UrenpoaltrnI erenIf oti oi eI -r1att total pepol.atto;

amngcunrIs i, 1~910, end 1991 dat. anOra... lies o f i-usholdhIpro. e hoahll ou ra,ad rorI

Ponolatien Projecetoor -~~~ h- iNuosn Inset f a glnop of ted idulstof.rlInIng qua-ot-