Embed Size (px)

Citation preview

Report No. 2235-CO FILE COPYEconomic Position and Prospects of Colombia

c- Ctm A5t(In Two Volumes)

Volume 1: Main Report pr ^,January17,1979 �rbRN TS l,A. & C.Latin America and Caribbean Regional Office iNFORMATION GEMS

FOR OFFICIAL USE ONLY

Document of the World Bank

This document has a restricted distribution and may be ljsed by recipientsonly in the performance of their officiai duties. Its contents may not otherwisebe disclosed without World F:ank authorization

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

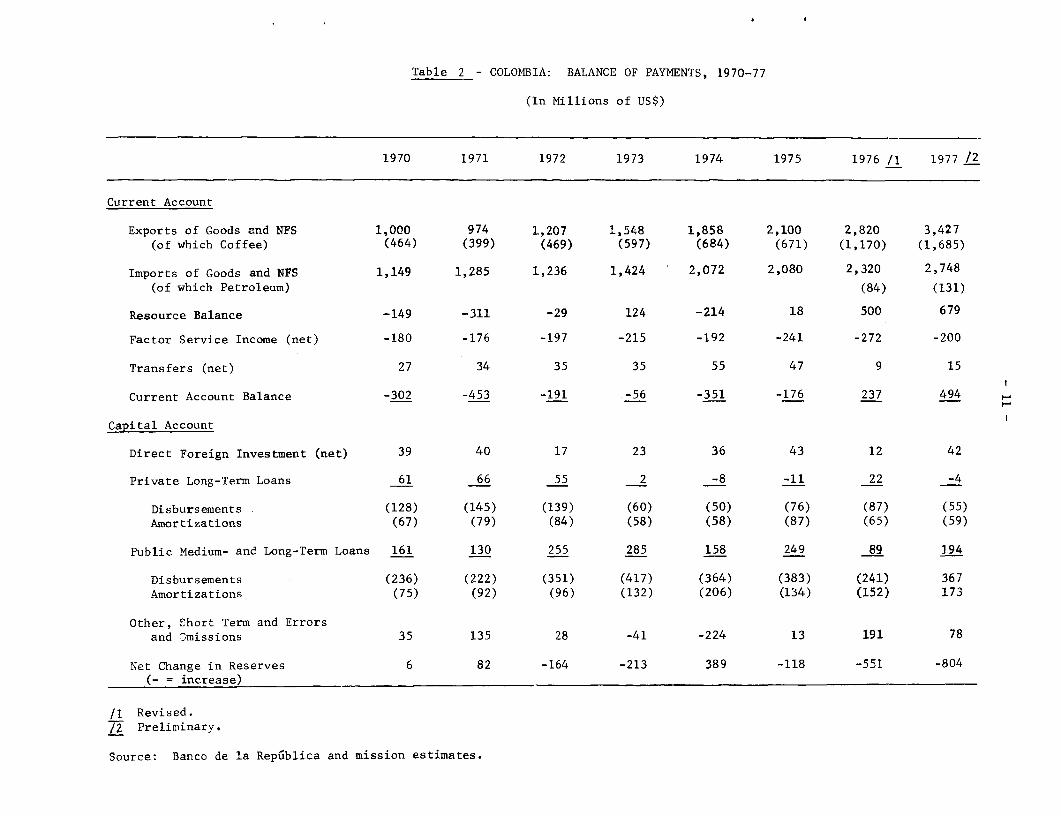

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

Currency Unit: Peso

Exchange Rate Effective December 31, 1978

US$1.00 = Col$41.00Col$1.00 = US$0.0244

Average Exchange Rate (Buling)

1974 1975 1976 1977

US$1.00 = Col$26.08 Col$30.95 Col$35.05 Col$36.998Col$1.00 = US$0.0383 US$0.0323 US$0.0285 US$0.02703

FOR OFFICIAL USE ONLY

This report is based on the findings of an economic mission toColombia during April-May 1978, composed of Messrs. George R. Gebhart (Chiefof Mission), Wolfgang Schohl (General Economist), Pedro Rado (Fiscal Economist,IMF) and Benjamin Sands (Statistical Assistant).

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

ECONOMIC MEMORANDUM ON COLOMBIA

TABLE OF CONTENTS

VOLUME I - THE MAIN REPORT

Page No.

MAP

COUNTRY DATA

SUMMARY AND CONCLUSIONS ............................ i - viii

I. BACKGROUND ............................................. 1

A. Post World War II Growth Patterns ............. 1B. The 1967-74 Period ............................ 2C. The 1974-75 Economic Reforms ................. 4D. The Benefits of Growth ........................ 5

II. RECENT ECONOMIC DEVELOPMENT: THE COFFEE BOOMAND STABILIZATION ................................ 7

A. Introduction ...... ........................ 7B. Growth and Employment: 1976-77 .............. . 8C. The Balance of Payments ..... .................. 10D. Public Finances ...... ......................... 17E. Financial Savings and Credit .................. 27F. Developments in 1978 ............ .. ............ 29

III. DEVELOPMENT STRATEGY AND SECTORAL GROWTH PROSPECTS . 31

A. Development Strategy .31B. Energy .... ....... ........... 36C. Manufacturing .38

IV. GROWTH PROSPECTS AND BALANCE OF PAYMENTS OUTLOOK ... 40

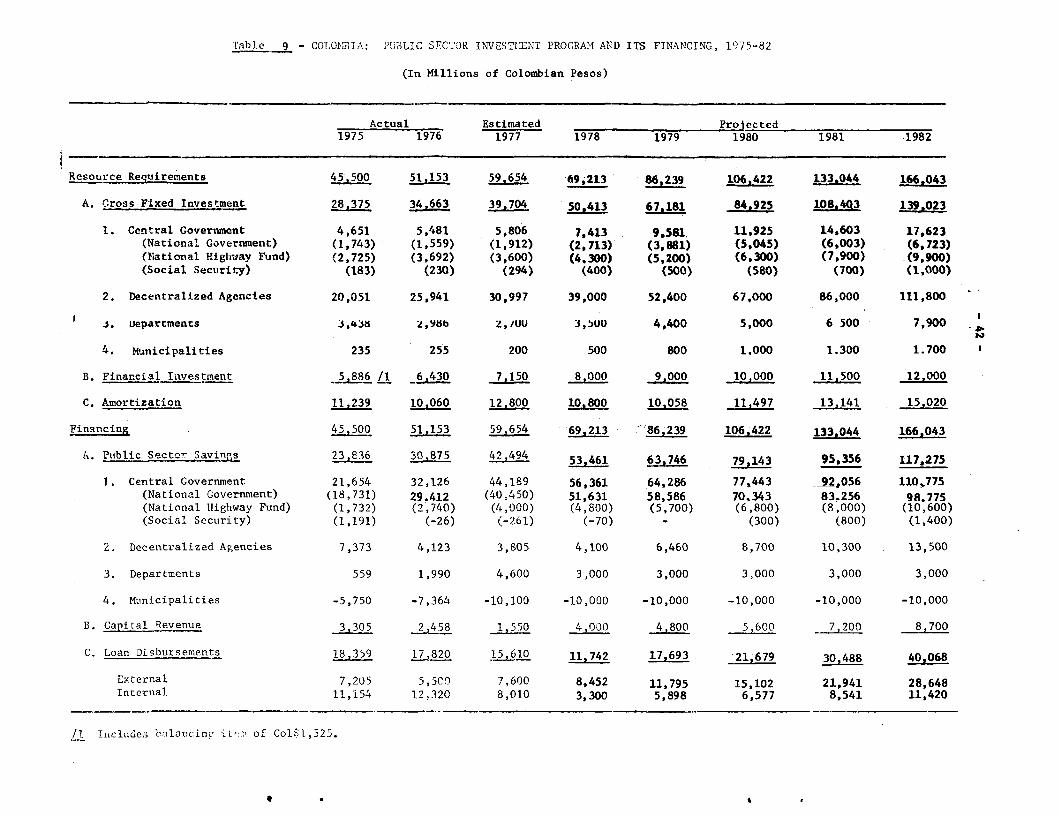

A. Growth Prospects .............. . .... 40B. Public Sector Investment and Its Financing 40C. Balance of Payments Outlook . 43D. External Capital Requirements, Debt Management

and Creditworthiness .46

VOLUME II - STATISTICAL APPENDIX

IBRD-3638R I78 744' 7° 0' OCTO0ER 1976

A r L A N r C/c SOUTH AM

Rioba t

ATLZI0 , ( / t g °

I D-1~~~~~~~~~0

sco A ' e MAGDALENA < COdO408 BX '

0 t~~~~~~~~~~~~~~~TA6B~J~4C1BC hiB BBB -C

< s , c o R D o 6 A ' e / /) i o; o T E \ V ~E N E Z U E L A14

A/ I AENEZUE

%, /. Co !fB 8'' \

t w . _ _ . f S ~~~~~~~A N T A N D ECRJ; J , A R A U C A \. "

tJ <'~~~C H O C O Wr v ., .oP AJ opcsNRE j BOYAr A i 5-' BB *. !'1O) R1SARALDAI / AA OCASANARE

,'o9I~~ CUNDINAMA*CA)

_ Peora ,O' f GOT#

e c ,, fev / M E T A< </.

r4~~~~~~~~~~~~~~~~~~~~~~~ I C A H UILA,_. D

'B a' J' 0

Vlo~rencls~1 o~~ -' -$\\B'

, NARI O - V A L L EES Z

- ~-~CALO U E ~ TOLIMA <. E T A

:- CCI P / YO

.HUILA- IA .

C A . C A+ ^2 A M AZOE S lO

N R I## N 10 V UP E/

__~~~~~~~~ ~~~~~ Aes e a P E R U A-- rB MB ' ' ,.x' Z 6

- t '> CA A M A Z N A

CO LOMBIA'7 E~s~0tM8t .Wv. ~4DOmeRer

- - - - ~~~~~~8MR*8~~~ ~~nI4~~~4I80M & Co~~~~~~rbud@ bormdaq~~~~~~~4

- - M~~~~~~~~~~~M~~~~~POWE~~~~~~~~~BIO8t.~~~~~~~~~~~~~8A / ~ ~ ~ ~ ~ 8

ir 71r'~~~~~~~~~~~

Page 1 of 2 pages

COUNTRY DATA - COLOfIA

AREA 2/ POPULATION DENSITY1,138.9 knr 25.0 million (mid-1977) 22, 0 per km/

Rate of Growth: 2.8% (from 1973 to 1977) 111.0 per k ma/of arable land

POPULATION CHARACTERISTICS (1973) HEALTH (1974)Crude Birth Rate (per 1,000) 33 Population per physician 2230Crude Death Rate (per 1,000) 8 Population per hospital bed 470Infant Mortality (per 1,000 live births) 70

INCOME DISTRIBUTION K1974 DISTRIBUTION OF LAND OWNERSHIP (1971)% of national income, nlug st quintile 54 % owned by top 10% of owners 80.0

lowest quintile 5 % owned by smallest 10% of owners 0.2

ACCESS TO PIPED 'WATER (1974) ACCESS TO ELECTRICITY% of population - urban 73 % of population - urban

- rural 29 - rural

NUTRITION (1972) EDUCATION (1974)Calorie intake as % of requirements 104 Adult literacy rate % 77.6Per capita protein intake (grams per day) 47 Primary school enrollment . 105.0

1/GNP PER CAPITA in 1977 US $710

GROSS NATIONAL PRODUCT IN 1976 ANNUAL RATE OF GROWTH C7.. constant prices)

US $ Min. . 1960-65 1965-70 1973-74 1974-75 1975-76

GNP at Market Pric*s 15,122 100.0 4.5 5.5 6.6 3.6 4.5Gross Domestic Investment 2,956 19.5 1.8 8.1 32.8 -17.4 20.5Grogs National Saving 3,070 20.3 2.1 10.8 18.5 -17.5 48.3Current Account Balance 237 1.6 * 'Exports of Goods, NFS 2 820 18.6 2.1 4.1 -6.1 13.0 34.3Imports of Goods, NFS 2,320 15.3 1.9 10.2 22.6 0.5 11.4

OUTPUT, LABOR FORCE ANDPRODUCTIVITY IN 197^

Value Added Labor Forcer V. A. Per WorkerIlJ$ Mln. % Min. % US $ %

Agriculture 2,812 29.4 2.1 30.9 1,339 81.3Industry 2,522 26.4 1.2 17.6 2,102 127.6Services 4,218 44.2 2.5 36.8 1,687 102.4Unallocated . 14.7

Total/Average 9,552 100.0 6.8 100.0 1,647 100.C

GOVERNMENT FINANCEGeneral Government Central Government

(cole Mln.) 7. of GDP (Co1s Mln.) % of GDP1977 1977 1975-77 1977 1972 _ of 5zGD

Current Receipts 93,974 12.8 13.1 77,874 10.6 10.7Current Expenditure 55,285 7.5 8.1 33,685 4.6 4.9Current Surplus 389689 5.3 5.1 44,189 6.0 5.8Capital Expenditures 8,706 1.2 1.5 5,806 0.8 0.9External Assistance (net) 1,000 0.1 0.4

1/ The Per Capita GNP estimate is calculated by the same conversion technique

as used in the World Atlas. All other conversions to dollars in this table areat the average exchange rate prevailing during the period covered.

2/ Total labor force; unemployed are allocated to sector of their normal occupation. "Unallocated" consistsmainly of unemployed workers seeking their first job.

not availablenot applicable

Page 2 of 2 pages

COUNTRY DATA - COLOMBIA

MONEY, CREDIT and PRICES 1972 1973 1974 1975 1976 1977(Million Col$ outstanding end period)

Money and Quasi Money 44,765 60,177 75,905 100,578 136,068 180,705Bank Credit to Public Sector 7,210 5,665 8,874 11,274 5,169 10,807Bank Credit to Private Sector 56,579 71,907 97,296 119,832 155,375 194,793

(Percentages or Index Numbers)

Money and Quasi Money as 7. of GDP 24.1 24.7 23.1 24.4 25.5 24.6Consumer Price Index (7154-6155 - 100) 573.1 699.0 875.1 1,082.1 1,298.0 1,749.7Annual percentage changes in: 13.8 22.0 25.2 23.7 20.0 34.8

Bank credit to Public Sector -4.8 -21.4 56.6 27.0 -54.2 109.1Bank credit to Private Sector 20.0 27.1 35.3 23.2 29.7 25.4

BALANCE OF PAYMENT' MERCHANDISE EXPORTS (AVERAGE 1975-77) -

1975 1976 1977 US $ Mln %(Millions US $)

Exports of Goods, NFS 2,100 2,820 2,748 Coffee 1,022.7 57.1Imports of Goods, NFS 2.082 2.320 3.427 Other Agriculture 311.9 17.4Resource Gap (deficit = -) 1S 500 679 Manufactured 355.5 19.8

Minerals 21.9 1.2Interest Payments (net) -120 -198 -130 All other commodities 80.4 4.5Workers' Remittances 35 41 44 Total 1,792.4 100,0Other Factor Payments (net) -156 -115 -114Net Transfers 47 9 15 EXTERNAL DEBT. DECEMBER 31. 1977Balance on Current Account -176 237 494

Direct Foreign Investment 43 12 42 US $ MlnNet MLT Borrowing 238 111 190

Disbursement (459) (328) (422) Public debt, incl. guaranteed, totalAimortization (221) (2175 (232) outstanding & Disbursed 2,622Subtotal 360 726

Capital Grants .. .. ., DEBT SERVICE RATIO for 1977 -

Other Capital (net) 1, 1 %Other items n.e.i 13 191 78

Increase in Reserves (+) 118 551 804 Amortization of Public Debt 5.1

Net Interest on Public Debt 3.9Gross Reserves (end year) 2/ 552.6 1,171.5 1,835.6 T 1Net Reserves (end year) 547.3 1,165.9 1,829.6 Total 9.0

RATE OF EXCHANGE IBRD/IDA LENDING, December 31, 1977 (Million US $):

December 31, 197t IBRD IDAUS $ 1.00 = 36.47 I I

Col$ 1.00 = US $0.02742 Outstanding & Disbursed 716.2 22.0

Decener 31 1977Undisbursed 487.9I

USDecember 31,17 Outstanding incl. Undisbursed 1,204.1 22.0

Col$ 1.00 = US $0.02624

1/ Data Refer to Export Registrations.21 Official Reserves.3/ Ratio of Debt Service to Exports of Goods and Nonfactor Services.

not availablenot applicable October 12, 1978

EPD/PRD

SUMMARY AND CONCLUSIONS

Background

1. During the past two decades, Colombia has made substantial progressin the transition from a predominantly rural and agricultural economy madeup of largely self-contained regions to a more integrated urban-industrialeconomy. The productive base of the economy has been widened appreciably, andthere has been substantial diversification of production in both the agricul-tural and industrial sectors. These improvements have been accompanied byrapid growth of nontraditional exports, also by the development of a modernsector relying to a considerable extent on imported inputs. Despite theseadvances, per capita income is still low (US$710 in 1977 1/) and the countryis to a considerable extent undeveloped with a limited modern sector super-imposed on a large, traditional and economically poor base. Moreover, thecountry is still heavily dependent on imports of intermediate and capitalgoods, and on export earnings from coffee. Although some success has beenachieved in recent years in diversifying export products and markets, eventsof the past two years indicate that fluctuations in world coffee prices stillhave a profound effect on the economy.

2. Following strong growth of output and employment in the immediatepost-World War II period, the consequence of rapid import substitution andrising coffee prices, the Colombian economy experienced an extended periodof erratic growth from 1950 to 1966. This was primarily the result of sharpfluctuations in coffee prices and a difficult social and political environment.With mounting balance of payments problems, fiscal difficulties and slowergrowth of employment, it became increasingly clear towards the end of thisperiod that opportunities for additional easy import substitution were ex-hausted and that the proliferation of direct administrative controls overresource allocation was hampering the operating efficiency of the economy.

3. A major reorientation of economic policy was introduced in 1967,designed to increase the availability of foreign exchange, raise domesticsavings and investment rates and improve resource allocation. The cornerstoneof this new strategy was the introduction of periodic adjustments in theexchange rate to provide incentives for expanding noncoffee exports. Majorfiscal, credit and trade policy changes were introduced to support the newexchange rate policy and public sector investment was expanded to provideneeded infrastructure. Led by rapid expansion of noncoffee exports, real GDProse by 6.6X per annum over the 1967-74 period. By 1974, noncoffee exportscomprised 54% of total merchandise exports, up from less than 40% in 1967.Exports of manufactured goods and noncoffee agricultural products respondedfavorably to the new export incentives, producing rapid growth of output inlabor-intensive sectors of the economy. As a consequence, unemployment de-clined and real per capita GDP rose by almost 4% per annum during the1967-74 period.

1/ World Bank Atlas Method.

- ii -

4. Despite improvements in economic efficiency, greater diversifica-tion of exports and strong economic growth, Colombia experienced increasingeconomic difficulties in the mid-1970s. Inflation accelerated, largely becauseof excessive monetary expansion caused by Central Bank financing of growingfiscal deficits and by rapid increases in private sector credit. In 1974,inflation was exacerbated by rising import prices, and the balance of paymentsweakened as a result of slower growth in the industrial countries, risingimport demand, and reduced capital inflows. Measures taken to stabilize theeconomy and a lower investment rate led to slower growth beginning about mid-1974.

5. In response to the country's growing economic problems, extensivefiscal, monetary and trade reforms were introduced beginning in late 1974.As a result of these reforms, the public finances improved sharply in 1975,financial savings expanded and were more evenly distributed among financialinstruments, and resource allocation was improved. Investment failed toincrease however, and while these measures were successful in stabilizing theeconomy, their immediate impact was to dampen economic growth. Consequently,the slowdown which began in 1974 continued through 1975.

Recent Economic Developments

6. During the last two years the Colombian economy has been stronglyaffected by the fourfold increase in the world price of coffee that occurredbetween late 1975 and mid-1977. As a consequence, Colombia's exportearnings from coffee rose from US$671 million in 1975 to nearly US$1.7 billionin 1977 and incomes throughout Colombia's rural areas increased substantially.Government efforts to sterilize the large inflow of foreign exchange reservesand to limit secondary expansion of the money supply were only partiallysuccessful in restraining the growth of aggregate demand. When the supply ofconsumer goods, especially of basic foodstuffs, failed to keep pace with thegrowth in demand, inflation accelerated rapidly; to 44% in the twelve monthsending June 1977 from 17% for the similar period ending June 1976. This un-precedented acceleration in inflation took place when public sector deficitswere low and foreign exchange earnings relatively high. This is differentfrom the usual case. The rise in coffee prices and the policy measures takento offset their inflationary consequences, therefore, had both favorable andunfavorable effects on the economy. Increased foreign exchange reserves,higher tax revenues and expanded employment and incomes in rural areas wereamong the beneficial effects, while much higher inflation, low availability ofinvestment credit, reduced incentives for non-coffee exports and negative realinterest rates leading to inefficiency in resource allocation were among theunfavorable effects.

7. The authorities responded rapidly to the acceleration of inflationby introducing a broad range of fiscal, monetary and trade policies designedto gain control over the explosive increase in prices. Beginning in late1976, reserve requirements were raised, rediscounting at the Central Bank wasreduced and public sector borrowing from the Central Bank was virtuallyeliminated. In early 1977 the authorities temporarily suspended periodicadjustments to the exchange rate, and exporters were required to accept 90-day

- iii -

US dollar-denominated certificates of exchange in lieu of cash payment fortheir exports. A larger proportion of coffee receipts was channeled to theCoffee Federation which agreed to invest these receipts in Central Bank bonds,the proceeds of which were frozen in a special account. Measures were takento liberalize imports, food imports by the state marketing agency, IDEMA, wereincreased sharply, and restrictive fiscal measures were introduced.

8. As a consequence of these measures, a favorable second semesterharvest and a slower rate of accumulation of foreign exchange reserves,inflation declined sharply beginning in July 1977. By the end of the year,the rate of inflation had fallen to 29% as compared to December of the pre-vious year. With inflation subsiding, periodic exchange rate adjustments werereintroduced. With few other exceptions, however, the stabilization policieswere continued in effect throughout the first part of 1978 and for the yearending in November, inflation had fallen to 17%.

9. Despite the domestic stabilization program, real GDP growth in-creased from 3.8% in 1975 to 4.4% and an estimated 5.9%, respectively, inthe subsequent two years. This growth was the direct result of the strongexpansion of domestic demand caused by the rise in incomes of coffee pro-ducers. Output of the industrial and service sectors responded strongly tothe rising demand, while agricultural output, adversely affected by droughtconditions in the interior of the country from early 1976 to mid-1977,showed only small increases in both years. Because strong growth occurredin relatively labor-intensive sectors of the economy, the urban unemploymentrate declined from an average 12% during the first half of the 1970s, toan estimated 8% by the end of 1977. Rural unemployment seems to have declinedalso during this period, although only fragmentary information is available.

10. Colombia experienced its largest overall balance of paymentssurplus of the post war period in 1977, eclipsing by a substantial marginthe previous peak reached in 1976. Export receipts rose by 23% in currentUS dollars and despite strong increases in imports, the current accountsurplus rose to US$494 million, equivalent to 2.5% of GDP. With net capitalinflows at about the same level as in 1976, net official reserves rose tothe equivalent of 11 months' merchandise imports by December 1977. Colombia'strade and exchange rate policies in 1976 and 1977 were largely a function ofthe need to reduce the rate of inflation. In an attempt to offset the disin-centive effects on noncoffee exports of a reduced rate of devaluation of thepeso, tax rebates were increased and export credit was expanded signficantly.Nevertheless, the combination of lower incentives for exports and risinginternal demand resulted in stagnation of noncoffee exports in nominal termsand a reduction in real terms. Consequently, the favorable trend of bothexport product and market diversification, which was characteristic of the1967-74 period, was reversed.

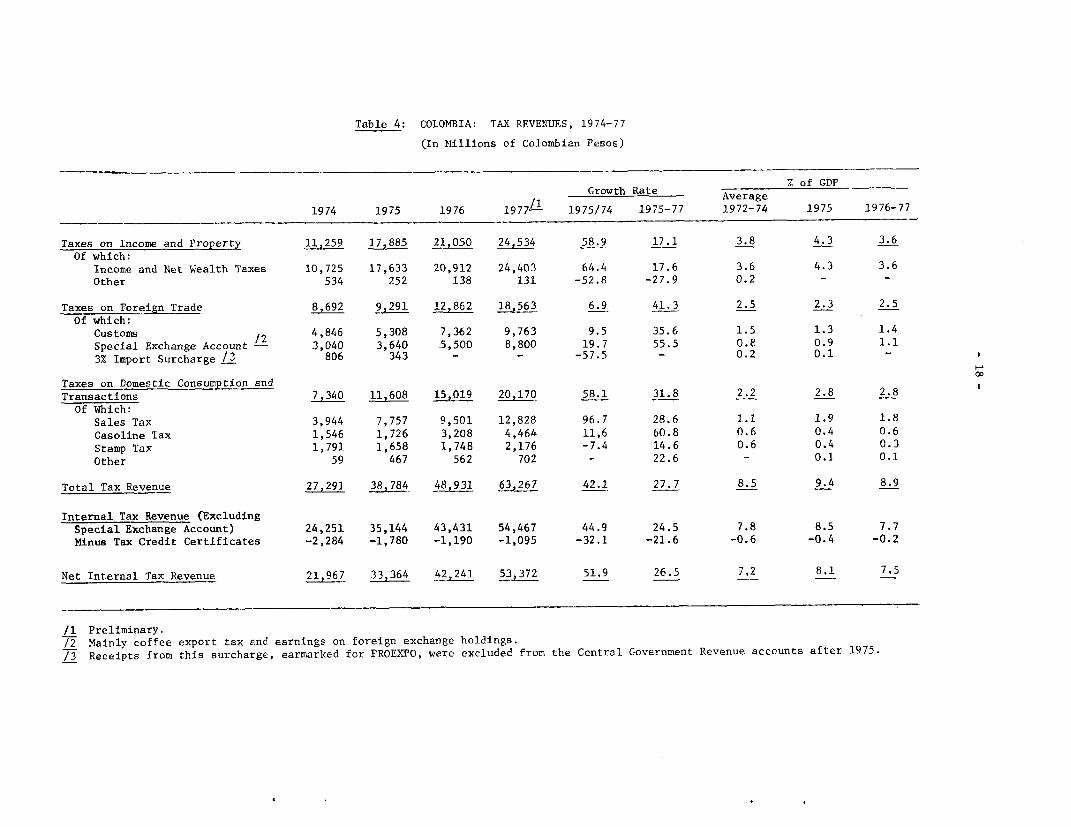

11. Although public sector savings increased substantially in 1976 and1977 as a consequence of the Government's contractionary expenditure policyand increased coffee tax revenues, the capacity of internal taxes to supporthigher levels of public expenditure declined. Modifications of legislationsubsequent to the 1974 reforms reduced the scope and effectiveness of thereform and together with weak tax administration, retarded growth in tax

- iv -

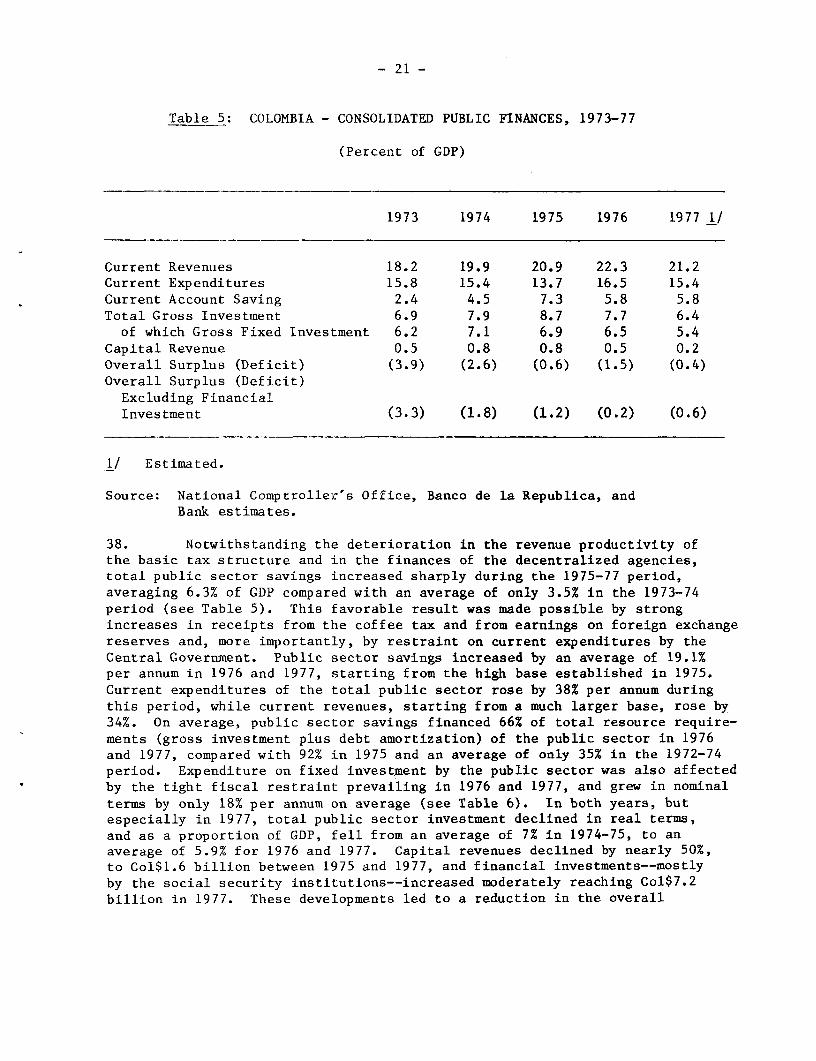

collections. Thus, excluding revenues derived from coffee exports, Colombia'spublic finances deteriorated during this period. As a result of the Govern-ment's restrictive expenditure policy, public investment declined from 6.9% ofGDP in 1975 to an estimated 5.4% in 1977, thereby limiting progress on somesocially significant projects designed to provide increased public servicesto the poorer segments of the population. Public sector savings, however,financed an increasing proportion of public investment in 1976 and 1977, and,at the same time, the country reduced its debt obligations to the Central Bankand repaid in advance some of its more costly loans from external lenders.Future prospects for Colombia's public finances do not appear encouraging.Revenues from the coffee tax are expected to decline as world coffee pricesmove back to their real historic average and the decline in tax buoyancy whichoccurred over the past two years, especially with regard to the income andwealth taxes, may be hard to reverse in the short term. Moreover, thereappears to be only limited room for further reduction in public sector currentexpenditure and public sector investment should be expanded to provide neededsocial and economic infrastructure. Noncoffee tax revenues will probably haveto be the major source of financing for additional investment, and it isexpected that action will be taken to strengthen collections from this source.

12. Fixed investment by the decentralized agencies grew by 24% per annumin nominal terms in 1976 and 1977, representing only a modest increase in realterms. Lower operating surpluses and reduced transfers from the CentralGovernment held down investment by many of these agencies. With their com-binded operating surplus falling to 0.5% of GDP in 1977 from 1.8% in 1975,the deterioration in the finances of the decentralized agencies is a matterof concern since their future investments may have to be cut because of lackof sufficient internally generated savings.

13. Developments in the external sector have continued to exert a stronginfluence on the Colombian economy in 1978. Coffee prices, although graduallyweakening, have remained well above historical levels, and coffee exportvolumes have risen sharply. Thus, the trade account registered a sizeablesurplus during the first half of 1978, despite an apparent rapid increase inimports, and Colombia's balance of payments is expected to register its fourthconsecutive surplus in 1978. Noncoffee exports experienced only slow growthduring the first part of the year, however, probably in large part becauseof the disincentive of an overvalued exchange rate. Food production apparentlyreturned to normal in the first harvest of 1978 as well. Consequently, infla-tion has continued to decline and is not expected to exceed 18% for the year.Income and wealth tax collections in 1978 recovered somewhat from the depressedlevels of 1976 and 1977, and sales and customs taxes and receipts from thespecial exchange account have risen sharply in real terms. Current expendi-tures have also grown rapidly, and public sector savings is expected to beabout the same level as in 1977. A 33% increase in the price of gasoline inOctober 1978 should help improve the finances of Ecopetrol, the State OilCompany. High incomes from coffee, together with further recovery in bothprivate and public investment, should provide the stimulus for continuedstrong growth in real GDP in 1978. A rate of GDP growth somewhat above 6%seems likely.

-v -

Development Strategy

14. The development strategy embodied in the 1975-78 Development Planaimed at accelerating the rate of GDP growth and distributing the benefits ofsuch growth more equitably. This was to be accomplished through policiesdesigned to improve economic efficiency, stimulate public and private invest-ment and expand public services to the poorest half of the population.Substantial progress was made in carrying out this strategy during the pastthree years. However, the dislocations caused by the world recession of1974-75, and the subsequent coffee boom, required more concentration ofeconomic policy on short-term stabilization problems, and some of the longerterm objectives had to be stretched out.

15. The achievement of high economic growth rates in the future willprobably require greater reliance than in the past few years on the noncoffeeexport-led growth strategy followed during the 1967-74 period. This strategyemphasizes the provision of incentives to encourage noncoffee exports, amore active role for the public sector in providing needed infrastructure andsocial services, and increased efficiency and investment in the private sector.As coffee export receipts decline with falling coffee prices, this strategywould relieve the foreign exchange constraint and take up the slack in aggre-gate demand. While the success of this strategy depends in part on favorableeconomic developments in Colombia's major trading partners, domestic policiesmust assure adequate incentives, and the structural bottlenecks to growthwhich have multiplied in recent years must be removed. The most importantof these potential constraints to growth in Colombia is a lack of sufficientenergy, especially of petroleum based products. In the absence of morerapid development of additional energy resources, foreign exchange constraintsand shortages of energy could seriously limit growth by the mid-1980s, if notearlier. Therefore, high priority is expected to continue to be given toavoid any slowdown of growth of the energy sector. In addition, investmentsin transport infrastructure, particularly railroads and highways, shouldreceive priority to eliminate this increasingly serious constraint on growth.With respect to export incentives, the establishment and maintenance of aproper exchange rate will probably be crucial for more rapid growth of non-coffee exports and encouragement of efficient import substitution industries.Fiscal and credit incentives should be used, as necessary, to complementexchange rate incentives and to foster growth of exports of goods in whichColombia has a comparative advantage. In addition, high priority should begiven to the large resource-based projects which have the potential forsubstantially increasing Colombia's exports in the mid to late 1980s, e.g.nickel, coal and gas.

16. The revitalization of public sector investment appears also tobe important for accelerated economic growth in the future. The principaltask in this regard will be to increase public sector saving sufficiently tofinance the higher levels of investment without excessive recourse to CentralBank credit. This will require improvements in tax administrative andpossibly some expansion of the tax base, as well as continued adjustments inthe prices charged for services by the decentralized agencies. Holding downincreases in public sector current expenditures will also be required.

- vi -

17. Energy shortages could become a serious constraint on growth bythe mid-1980s unless efforts to develop alternative sources of energy arestepped up without delay. Although endowed with an abundance of primaryenergy resources, including hydro power, natural gas, coal and most probablyadditional petroleum, past development of Colombia's energy resources hasnot kept pace with energy use. As a consequence, the country became a netimporter of energy (petroleum) in 1976. Major policy changes were intro-duced in the energy sector beginning in mid-1975 as a result of the deter-iorating petroleum balance. Foreign firms were encouraged to enter intoassociation contracts with ECOPETROL (the State Oil Company) to explore foroil in new areas and price incentives were given for new oil and forincremental crude from old fields. A policy of gradual increases in pricesto consumers was adopted, with the self-financing of a substantial portionof the sector's investment requirements as its ultimate goal.

18. Colombia's strategy for dealing with the energy problem is toreduce the country's dependence on petroleum as the major energy source.Hydropower projects are to be executed as rapidly as possible and naturalgas and coal resources are to be developed to substitute for petroleumin generating electricity, and eventually to provide additional exports.These developments are not expected to be sufficient to prevent largeincreases in petroleum imports over the next several years, however, withthese imports projected at over US$600 million by 1982, and about US$900million by 1985. While the total investment requirements of further energydevelopment are still largely unknown, rough estimates indicate that theycould run as high as US$8.0 billion in 1976 prices over the next decade.

19. Increased investment and output in the directly productive sectorsof the economy, especially industry and agriculture, 1/ are crucial for theexport-led development strategy and for expanding employment opportunities.Therefore, measures to stimulate productively in both of these sectors wouldseem to merit high priority. Over the past decade industry has been one ofthe leading growth sectors in the Colombian economy, and at present consti-tutes about 20% of GDP, provides a similar proportion of total employmentand supplies 50% of the country's non-coffee exports. In response todevelopment policies favoring industrial exports, value added in the sectorgrew by over 8% annually in real terms during the 1967-74 period and the valueof manufactured exports increased by 48% annually in nominal terms. Recessionin the industrialized countries and domestic stabilization measures retardedthe sector's growth in 1975, however the growth in domestic demand in 1976 and1977 caused manufacturing value added to recover strongly.

20. A lack of sufficient long term investment resources has limitedexpansion of industrial capacity in recent years. Private sector industrialcredit has been curbed by the restrictive monetary policy pursued by theGovernment. In addition, retained earnings have been squeezed by a high taxburden and by high dividends required to maintain attractive returns onequity. Small- and medium-size firms have been especially hard hit by theshortage of long term funds for investment. Consequently, rollovers of short-

1/ A separate report on Colombia's agricultural sector is in preparation.

- vii -

term credit and high cost credit from the extra-bank market have become majorsources of investment financing for these firms. Lower inflation shouldfacilitate the development of Colombia's capital market and, together withthe lifting of controls over interest rates and credit, could be expected toincrease the availability of investment funds to the private sector.

Growth Prospects and External Capital Requirements

21. Colombia has demonstrated for over a decade that a coherent develop-ment strategy is possible and results in improved output and social welfare.Together with the country's strong resource base and its high level of inter-national reserves, this leads to optimism about the future. Colombia shouldbe able to achieve annual real GDP growth of between 6% and 7% during the1978-82 period. The maintenance of this level of growth will require strongexpansion of noncoffee exports and increases in savings and investment rates.The large unmet needs for infrastructure, social services and additionalsources of energy will mean rapid expansion of public sector investmentduring this period. By 1982, public investment is expected to reach 7% ofGDP, as compared with 5.4% in 1977. About two-thirds of this investment couldbe financed by public sector savings, if improvements are made in tax admin-istration and measures are taken to expand the tax base. Continued upwardadjustments in the prices charged for the goods and services provided by thepublic decentralized agencies would also be required. It is expected thatColombia will follow export promotion policies designed to provide adequateincentives for Colombian exports and to encourage both product and marketdiversification.

22. Greater efforts to increase efficiency and investment in the produc-tive sectors will be needed to complement incentives given to noncoffeeexports. Relaxing controls over interest rates and credit, together withmeasures to stimulate bond and equity issues by the private sector, wouldcontribute to an improved capital market, increased private savings and betterresource allocation. Ongoing and future infrastructure investments by thepublic sector should also facilitate improvements in economic efficiency.

23. Because of the expected continued decline in world coffee prices,accelerating oil imports and the high import content of future investment,the current account of the balance of payments is expected to be in deficitthroughout the early to mid-1980s, despite the strong growth which is assumedfor non-coffee exports. This deficit is projected to average US$466 millionannually during the 1978-82 period, or 1.4% of GDP. Colombia is expected,therefore, still to be a large net importer of capital for some time to come.Its future external resource requirements reflect the need to supplementdomestic savings and to provide increasing amounts of foreign exchange tofinance required imports of capital and intermediate goods. Gross externalcapital requirements are projected at US$4.5 billion between 1978 and 1982, oran annual average of about US$900 million. About half of Colombia's capitalinflow during this period is expected to be provided by official multilateraland bilateral sources, with commercial and financial credits foreseen asbecoming increasingly important.

- viii -

24. Colombia's public external debt repayable in foreign currencyamounted to US$3.6 billion at the end of 1977, of which US$2.6 billion wasdisbursed and outstanding. The capital inflows required during the 1978-82period would raise Colombia's total external debt (disbursed and outstanding)from US$3.1 billion in 1977 to US$5.5 billion in 1982. The public debt serviceratio, which fell during the past two years as export growth accelerated andwas 9.0 at the end of 1977, has increased slightly this year and is expectedto reach 12.3% in 1982. Balance of payments prospects beyond 1982 will dependheavily on the timely development of additional domestic energy sources and onprogress made in executing several large natural resource-based export-orientedprojects currently under preparation. Given the expected continuation ofsound economic and financial management and timely execution of the country'sdevelopment program, it should be possible to prevent the external sector fromagain becoming a constraint on economic growth and to maintain Colombia'screditworthiness for the required external borrowing.

CHAPTER I

BACKGROUND

A. Post World War II Growth Patterns

1. Duri..g the past two decades, Colombia has made substantial progressin the transition from a predominantly rural and agricultural economy madeup of largely self-contained regions, to a more integrated urban-industrialeconomy. The productive base of the economy has been widened appreciably, andthere has been substantial diversification of production in both the agricul-tural and industrial sectors. These improvements have been accompanied byrapid growth of nontraditional exports and by the development of a modernsector relying to a considerable extent on imported inputs. Despite theseadvances, per capita income is still low (US$710 in 1977 1/), and the countryis to a considerable extent undeveloped with a limited modern sector super-imposed on a large, traditional and economically poor base. Moreover, thecountry is still heavily dependent on imports of intermediate and capitalgoods, and on export earnings from coffee. Although some success has beenachieved in recent years in diversifying export products and markets, eventsof the past two years indicate that fluctuations in world coffee prices stillhave a profound effect on the economy.

2. Since the turn of the century, the Colombian economy has beenheavily dependent on export earnings from coffee. During the post WorldWar II period through 1967, proceeds from coffee exports averaged 70% of totalexports. World prices of coffee fluctuated widely during this period and as aconsequence Colombia's coffee earnings have been highly unstable. In thoseperiods in which world coffee prices have been high, there has generally beenan easing of the country's foreign exchange constraint and domestic consump-tion, investment and economic growth have accelerated, resulting in increasedemployment and significant improvements in levels of welfare of most Colombians.There were usually large accumulations of foreign exchange reserves, rapidexpansion of the monetary base, and an acceleration in the inflation rateduring these periods as well. When coffee prices were low, declining aggregatedemand and shortages of foreign exchange usually caused consumption, investmentand economic growth to fall. During these periods, the unemployment rate hasgenerally risen and levels of welfare have fallen.

3. In the late 1960s, the Government attempted to break this dependenceon a single commodity by introducing an export promotion program aimed atstimulating growth of noncoffee exp'orts. The basic components of this programincluded greatly expanded credit and fiscal incentives for noncoffee exportsand improvements in the efficiency of the institutions responsible for exportpromotion. At the same time, periodic adjustments to the exchange rate(crawling peg) were introduced as a further incentive. This effort wassuccessful in expanding noncoffee exports, and, as a consequence, the share of

1/ World Bank Atlas Method.

- 2 -

coffee in total exports declined from 62% in 1966 to 46% in 1974. During thisperiod, considerable diversification of export products and markets tookplace, and the Colombian economy became more resilient to external shocks,including fluctuations in world coffee prices. Nevertheless, the events ofthe past several years--abrupt changes in coffee prices, rapid accumulationof foreign exchange reserves, excessive monetary expansion and acceleratedinflation--indicate that the Colombian economy is still strongly affected byfluctuations in coffee prices and underscore the importance of longer termpolicies directed at reducing the effects of coffee price fluctuations on theeconomy.

4. Following steady growth of output and employment in the immediatepost World War II period, based on import substitution and rising coffeeprices, the Colombian economy from 1950 to 1966 experienced an extendedperiod of erratic growth of GDP, heightened economic instability and risingunemployment. This was in large part of the result of a binding foreignexchange constraint stemming from a secular decline of world coffee prices,exacerbated by trade and exchange rate policies which discouraged the growthof noncoffee exports. Government efforts to stabilize the economy andstimulate economic growth were frustrated by trade and credit policies whichencouraged excess demand for foreign exchange and increased the importintensity of consumption. Investment in fixed assets stagnated as well duringthis period, mainly as a result of shortages of imported capital goods.Consequently, real GDP growth averaged less than 5% per annum between 1950 and1966, and in several years barely exceeded the rate of population growth. Thelack of economic opportunities in the countryside, along with a difficultpolitical and social environment, contributed to a high rate of rural/urbanmigration and increased the social and economic problems of the cities. Thisplaced additional fiscal burdens on the Government, most of which were metthrough increased borrowing, in large part from the Central Bank. In spite ofgrowing economic difficulties, Colombia's development strategy continued toplace a high priority on import substitution. It became increasingly apparentduring this period, however, that the opportunities for easy import substitu-tion were becoming exhausted and that the proliferation of direct administra-tive controls over resource allocation was hampering the operating efficiencyof the economy. It was clear, also, that the country could not rely onthe coffee sector to provide the sustained increases in foreign exchangeearnings required for more rapid growth. It was not, therefore, until a newset of policies substantially altering the country's development strategy wereinstituted, that the basis for accelerated growth was reestablished.

B. The 1967-74 Period

5. Beginning in late 1966, Colombia introduced a new set of economicpolicies directed towards increasing the availability of foreign exchange,raising domestic savings and investment rates and improving resource allocation.The major purpose of the new strategy was to expand and diversify exports byproviding credit, fiscal and exchange rate incentives to noncoffee exporters.Modifications of credit policy focused on increasing the availability andlowering the cost of working capital and investment funds for potentialexport industries, and fiscal policy changes emphasized tax rebates (Certifi-cados de Abono Tributario--CATs) to exporters of most noncoffee items to

increase the return to exporting as compared to selling in the domesticmarket. Credit policy changes were directed towards eliminating the existingexcessive and cumbersome controls over interest rates and credit in order toincrease savings and improve the efficiency of resource allocation. Periodicexchange rate adjustments added a further dimension and widened flexibility tothe Government's export promotion efforts. In addition, significant improve-ments in public administration occurred during this period as several newinstitutions were established to support the export promotion anddiversification effort.

6. As a result of the new economic policies, real GDP increased byan average 6.6% per annum over the 1967-74 period, led by rapid expansionof noncoffee exports. By 1974, these exports comprised 54% of totalmerchandise exports, up from less than 40% in 1967, and only about 25% in1950. Manufactured goods accounted for nearly 50% of the increase innoncoffee exports, growing at 48% per annum in nominal terms between 1967and 1974. The strong growth in manufactured exports was heavily influencedalso by an increased technological sophistication of Colombian industry,acquired in large part through foreign investment. This is illustratedclearly by the increased technological complexity and diversity of thecountry's manufactured exports. In 1974, Colombia exported substantialamounts of chemicals, pharmaceuticals, metal-mechanic products, machineryand electrical equipment, paper based products and glass products, noneof which were exported in 1966. There were strong increases in cotton,sugar, beef and in many other agricultural exports as well. Total noncoffeeagricultural exports expanded by 18% per annum in nominal terms and accountedfor 26% of the increase in noncoffee merchandise exports during the 1967-74period. Expanded research and farm credit contributed strongly to theincreases in agricultural exports and output.

7. In response to the stimulus provided by increased exports, output inthe manufacturing and agricultural sectors rose by an average 8.3% and 4.6%per annum respectively, during the 1967-74 period. Output in the agriculturalsector rose significantly above its historical average growth of about 3%.In both sectors, the composition of output moved increasingly towards export-able goods. As a result of the improved economic climate, investment rosesharply, especially in the directly productive sectors. The average investmentcoefficient (gross fixed investment/GDP) increased to 19.1% during the 1967-74period, from 16.8% for the 1960-66 period. Investment became more efficientas well, with the average ICOR declining to 2.88 from 4.03 in the 1960-66period. The expansion of investment and output generated rapid growth inemployment opportunities, and, although rural/urban migration continued at arapid pace, the unemployment rate declined in each of the four major urbancenters. With the rate of population growth declining, real per capita GDProse by almost 4% annually from 1967 to 1974.

8. Despite the strong growth, increased export diversification, andimprovements in economic efficiency, Colombia experienced increasing economicproblems in the early-1970s. The most serious of these was a sharpacceleration of inflation--to 25% in 1974 from less than 7% in 1970. This wasin part the result of excessive monetary expansion resulting initially fromrapid accumulation of foreign exchange reserves supported by heavy external

-4-

borrowing, and later from Central Bank financing of growing public sectordeficits. Inflationary pressures were exacerbated in 1971 by shortages ofbasic foods caused by excessive rainfall in food producing areas of thecountry and, beginning in late 1973, by higher import prices associated withthe increase in world petroleum prices. Inelasticity of the tax system,rising tax rebates to exporters and inadequate price adjustments by thedecentralized agencies were the major causes of the public sector deficits.The higher inflation was accompanied by a decline in domestic savings andinvestment rates, and, in 1974, by weakening balance of payments and a slow-down in economic growth. Negative real returns on savings, as inflationaccelerated without comparable increases in interest rates, discouragedprivate savings, and weak growth in tax revenues reduced public sectorsavings. Although most of the shortfalls in public savings were covered byincreased external and internal borrowing, especially in 1972 and 1973, publicinvestment spending declined slightly in real terms between 1970 and 1973. In1974, slower economic growth in the industrialized countries reduced thedemand for Colombia's manufactured exports, and, combined with falling coffeeprices, resulted in lower growth of merchandise exports. At the same time, asharp rise in public sector investment and large inventory accumulationscaused imports to accelerate. As a consequence, the trade balance weakenedand the country's foreign exchange reserves fell by US$390 million, to about2.5 months' of merchandise imports by the end of the year.

C. The 1974-75 Economic Reforms

9. In response to the country's growing economic difficulties, exten-sive fiscal, monetary and trade reforms were introduced by the new Governmenttaking power in August 1974. The goals of these reforms were two-fold: (a) tostabilize the economy in the short run by lowering the rate of inflation,reversing the deterioration in the public finances and strengthening the balanceof payments; and (b) to establish a policy framework more conducive to increasedsaving and investment and economic growth. In order to strengthen the publicfinances, a series of measures was introduced aimed at increasing the elasticityand progressivity of the tax system. These measures were based on recommenda-tions of a group of international experts--the Musgrave Commission--which hadearlier undertaken a study of the tax system at the Government's request.Actions taken to reform the financial system were designed to increase privatesavings and ensure their more efficient use. This was to be accomplished byraising maximum allowable interest rates to levels more in line with inflation,and by eliminating distortions in the capital market. These distortions weremainly the result of differential tax treatment of financial instruments andforced investment requirements imposed on financial institutions. Tradepolicy reforms introduced in prior years, which lowered general tariff levelsand reduced cumbersome controls over trade, were reinforced. Taken together,these reforms represented a major reorientation of economic policy with theobjective of increasing the operating efficiency of the economy through greaterreliance on market forces.

10. As a result of these reforms, the public finances improved in 1975,private savings were increased and more evenly distributed among financialinstruments, and the efficiency of resource allocation was improved. Theprogressive lowering of tariffs and reduction in other nontariff barriers to

-5-

trade exposed domestic producers to increased competition from abroad, andprobably induced greater efficiency in local industry. Tax revenues rose by42% in 1975, and, as a share a GDP, increased to 9.4% from 8.3% in 1974.Consequently, public sector savings rose to 5.8% of GDP, from 4.1% theprevious year, covering 67% of total public sector financial requirements(excluding debF amortization) in 1975, in contrast to 47% on average over theprevious three years. More equal and stable returns on different financialinstruments appear to have stabilized financial flows among financialinstitutions, thereby providing a more secure base for the expansion ofcredit. This same factor probably helped to bring about a more efficient useof credit by the various sectors of the economy as well, because of the morebalanced availability of credit. Not all of the distortions in the capitalmarket were eliminated, however. Subsidized credit was still provided tocertain sectors of the economy, and returns on some savings instruments,although improved, remained negative in real terms.

11. The 1974 reforms initially had a contractionary impact on the economy.As a result of this impact and the effects of the deepening world recession,the economic slowdown which began in mid-1974 continued throughout most of1975, and real GDP rose by only 3.8% in real terms that year. The unemploy-ment rate, 1/ which had gradually declined during the 1967-73 period of higheconomic growth, rose in the subsequent two years, reaching a level of 12.5%in 1975, compared with 10% in 1973. Manufactured exports declined by 22% incurrent US dollars in 1975, contributing heavily to the limited growth (1.3%)of industrial output. On the other hand, good weather boosted agriculturaloutput by 6% that year and a strong increase in noncoffee agriculturalexports, combined with a reduction in imports, generated an overall balanceof payments surplus of US$118 million for the year.

D. The Benefits of Growth

12. The growth in employment and incomes that has occurred over the pasttwo decades, along with increased public investment in education, health,nutrition and other public services, has brought widespread benefits to theColombian people. As result of improvements in health and nutrition, thechild mortality rate (one to four years of age) fell from 16 (per thousand)in 1960 to about 9 in 1971, with the infant (less than one year old) mortalityrate declining from 100 to about 70 over the same period. Comparable figuresfor child and infant mortality in the US in 1971 were 0.8 and 22 respectively.Life expectancy increased from 55 years in 1960 to nearly 61 years in 1975.The rapid expansion of health services between 1960 and 1975 is evidenced bythe decline from 2,400 to 2,180 in the ratio of population per physician andfrom 3,540 to 1,920 in the population per nurse (broadly defined) ratio. Thepopulation per hospital bed ratio declined also during this period, from 580to 530. Water and seweage services have been provided to an increasing pro-portion of the population in recent years also, with heavy emphasis on theprovision of services to rural areas. Since 1970, the percent of the ruralpopulation with access to safe water rose from 28% to 33% and the percent

1/ Four largest cities.

- 6 -

with access to sewerage facilities rose from 8% to 13%. It is estimated that86% of the urban population had access to safe water in 1975 and 73% had accessto sewerage facilities.

13. Education services were expanded rapidly during the past severalyears. The primary school enrollment ratio rose from 77 in 1960 to 105 1/ in1975, while the secondary school enrollment ratio tripled, from 12 to 36,during the same period. The pupil-teacher ratio in the primary schoolsdeclined from 38 to 33 between 1960 and 1975, but increased from 11 to 19 atthe secondary school level, reflecting the emphasis on programs to expandprimary school enrollment during this period. The adult literacy rateincreased from 63% to 81% during the fifteen year span 1960-75, indicatinga significant improvement in the general education level of the population.

14. Colombia's population growth declined during the last two decades,from an annual average 3.2% in the 1950s to an estimated average 2.8% p.a.in the 1973-77 period. Most of this decline was the result of a rapid fallin the crude birth rate beginning in the mid-1960s. Average crude birth ratesiri excess of 45.0 per thousand inhabitants in the 1950-64 period gave way torates of 33.1 as measured by the 1973 census data and 31.1 as measured by the1976 National Fertility Survey. A number of factors have been associated withthe lower birth rates, including rising per capita income, rapid rural/urbanmigration, greater economic and educational opportunities for women, andincreased availability and use of family planning methods. Although stillhigh, rural/urban migration has declined somewhat since the early 1960s, andthe urban population growth rate has declined from 6.0% p.a. in the 1950s toabout 4.5% p.a. in the 1973-77 period. Progress made in eliminating thewidespread violence which had occurred in the countryside during the 1950scaused investment, output and employment in agriculture to expand therebyreducing the incentive for migrating to the cities. Also, a selected group ofmedium-size cities serving rapidly growing agricultural hinterlands haveexpanded employment in excess of their labor force growth rate, and attractedmigrants away from the three major urban centers. Approximately 64% of thecurrent population lives in urban centers and there are now 16 cities inColombia with population of over 100,000 persons. While Colombia's populationis not considered excessive relative to the country's resource base, economicgrowth will have to be accelerated in order to expand employment opportunitiesat a pace sufficient to keep up with rapid growth of the labor force.

15. There was some improvement in income distribution in Colombia between1950 and 1970. This appears to have occurred as a consequence of a number offactors, including: reduced population growth, migration of unemployed andunderemployed surplus labor from rural to urban areas, rapid growth of employ-ment in higher productivity jobs in industry and agriculture, and, since 1967,policy efforts to improve the welfare of the poor through employment genera-tion and through increased public investment in health, education, nutritionand urban development. On the other hand, a declining trend in average realwages and in the share of wages and salaries in national income would seem toindicate a worsening of income distribution between 1970 and 1975. In thefollowing two years, however, income distribution may have improved as a conse-quence of the rapid growth of rural incomes associated with the coffee boom.

1/ This ratio exceeds 100 because a number of students enrolled in primaryschool are below or above the official school age.

CHAPTER II

RECENT ECONOMIC DEVELOPMENT: THE COFFEE BOOM AND STABILIZATION

A. Introduction

16. During the last two years the Colombian economy has been stronglyaffected by developments in the external sector. As the result of a seriousfrost in Brazil's major coffee producing area in late 1975, coffee exportsfrom that country declined sharply, triggering a fourfold increase in theworld price of coffee by mid-1977. As a consequence, Colombia's export earningsfrom coffee rose from US$671 million in 1975, to nearly US$1.7 billion in 1977,and incomes throughout Colombia's rural areas increased substantially. Laggingsupply of consumer goods, especially of basic foodstuffs, the production ofwhich was adversely affected by drought conditions in most of the country'sinterior, failed to keep pace with rising demand, and inflation acceleratedfrom 26% in 1976 to 44% in the twelve months ending June 1977. The heavyimpact of declining agricultural production on inflation is clearly visiblein the price increases of basic food items. Food prices rose by 58% in the12 months ending June 1977, and accounted for most of the acceleration in thecost of living during this period. Since inflation in Colombia has generallybeen moderate relative to that experienced by other countries in the region,averaging less than 11% per annum between 1960 and 1970, and seldom exceedingan annual rate of 20%, the magnitude of the acceleration of inflation whichtook place from early 1976 to mid-1977 was unprecedented in the country'srecent history.

17. The authorities responded rapidly by introducing a broad rangeof measures designed to gain control over the explosive increase in prices.Monetary, fiscal, trade and exchange rate policies were increasingly orientedtoward counteracting inflation. Measures were taken to delay the impact ofinternational reserve accumulation on the monetary base, credit was restrictedthrough tighter monetary measures, a policy of fiscal retrenchment wasinstituted, and trade policy was modified to increase imports and curtailexports. Exchange rate adjustments were slowed, and finally temporarilysuspended, in order to discourage exports and increase import payments.Controls over imports were relaxed and food imports were accelerated. Theseactions were highly successful in reducing inflation during the secondhalf of 1977 and in early 1978; however they also had the effect of limitingeconomic growth and reversing some of the gains achieved through the tax andfinancial reforms of 1974. In particular, progress in noncoffee exportexpansion and diversification resulting from the export-led growth strategy ofthe 1967-74 period was temporarily interrupted because of the modifications inexport incentives designed to curb inflation. Moreover, the reductions inpublic sector investment spending slowed progress in carrying out some ofthe Government's high priority social development programs and economicinfrastructure projects.

18. The coffee boom of 1976 and 1977 had a number of favorable effectsas well. The balance of payments registered large surpluses in both yearsand in early 1978, the country's official international reserves rose tonearly one year's merchandise imports, providing a comfortable cushion of

-8-

reserves to support future import requirements. Large receipts from thecoffee export tax boosted public sector revenues, and the public financesshowed an overall surplus (excluding financial investments) for the first timein the post World War II period. Employment expanded more rapidly than thelabor force, reducing the unemployment rate, which, together with the growthof income in ruiral areas, may have led to some improvement in the distributionof income. These same factors may also have slowed the rate of rural/urbanmigration. On balance, the Colombian economy was able to adjust to thedestabilizing effects of the 1974-75 world recession and the subsequent sharpincrese in coffee prices, without serious adverse effects on its long-rungrowth prospects.

B. Growth and Employment: 1976-77

19. Despite attempts by the Government to curb growth of aggregatedemand, the Colombian economy recovered steadily during 1976 and 1977, withreal GDP growth rising from 3.8% in 1975 to 4.4% and 5.9% in 1976 and 1977respectively (see Table 1). The major contributor to growth in these yearswas a strong expansion of incomes and consumption resulting from the rise inworld coffee prices. Gross domestic income rose by about 8% per annum in realterms during the two years, largely as a result of the higher coffee prices.Under the stimulus of increased consumption spending and high capacity

utilization rates in the previous two years, gross investment in fixed assetsis estimated to have increased by about 11% in 1977, after having declined

slightly (0.7% per annum) in 1975 and 1976. The production of manufacturedgoods and commercial and service activities rose by an average 6.8% and 7.6%per annum, respectively, in 1976 and 1977, largely in response to the increaseddemand for consumer goods. While the demand for food increased strongly becauseof the higher incomes, a prolonged drought--beginning in mid-1976 and lastinguntil mid-1977--limited growth of agricultural output in both years, and realvalue added in the sector rose by only 1.5% in 1976 and by an estimated 3.2%in 1977. Shortages of domestic food crops caused IDEMA (the State AgriculturalMarketing Agency) to increase its imports of food to US$112 million in 1977,from only US$58 million in 1976. Coffee output remained constant in 1976,but rose by an estimated 6.7% in 1977, reflecting producers' response to therelatively high world coffee prices over the past few years and the cumulativeeffect of new technology in the industry. Mining sector output is estimatedto have fallen by about 4.5% per annum in 1976-77, largely as a result ofcontinued declines in petroleum production. Construction activity appears tohave increased moderately in 1977, reflecting the climb in investment activity,after having fallen sharply in 1975 (-4.3%) and 1976 (-9.0%).

20. The combination of strong growth in domestic demand for consumergoods, negative real interest rates and high levels of capacity utilizationarising from sluggish investment in the preceeding two years caused a sharprise in private investment demand in 1977. However, the Government's contrac-tionary monetary policies and an inflation-induced high liquidity preferenceon the part of savers resulted in relatively slow growth in the availabilityof long-term credit for investment purposes. This, together with a squeezeon retained earnings brought about by the lack of adjustment of the companyprofits tax for inflation, limited the growth of investment that year.These were the same factors that limited investment in the prior two years,

Table I - COLOMBIA: GROSS DOMESTIC PRODUCT AT FACTOR COST BY SECTOR IN 1970 PRICES, 1970-77

(In Million of 1970 Colombian Pesos)

Growth Rate (Average Annual)1970 1973 1974 1975 1976 1977 /5 1960-70 1970-74 1974-76 1977

Gross Domestic Product at f.c. 119,796.9 147,178.0 156,707.5 163.399.2 170,033.3 180,015.7 5.2 7.0 4.2 5.9

Agriculture /1 34,244.8 39,157.4 41,516.9 44,066.4 44,725.4 46,156.6 3.5 4.9 3.8 3.2

Mining 2,528.0 2,591.7 2,403.8 2,240.7 2,107.9 2,044.7 3.1 1.3 -6.4 -3.0

Manufacturing 20,976.7 27,828.2 29,657.2 30,030.7 32,037.7 34,280.3 6.0 9.0 3.9 8.3

Construction 6,530.0 7,839.2 8,142.4 7,795.9 7,091.8 7,262.0 7.7 5.7 -6.7 2.4

Electricity, Gas and Water 1,787.9 2,473.3 2,615.1 2,753.4 3,073.3 3,205.5 8.8 10.0 8.4 4.3

Transportation and Communication 8,881.1 11,367.5 12,946.5 14,025.3 15,058.8 15,992.4 6.4 9.9 7.8 6.2

Trade /2 20,760.2 26,227.4 28,231.8 29,487.8 31,452.0 34,408.5 6.3 8.0 5.5 9.4

Public Administration andDefense /3 8,283.5 10,529.7 10,775.1 11,189.1 11,385.4 11,692.8 5.5 6.8 2.8 2.7

Other Branches /4 15,804.7 19,163.6 20,418.7 21,749.9 23,101.0 24,972.9 5.5 6.6 6.4 8.1

/1 Includes fishing and hunting and forestry./2 Composed of conmerce and banking, finance and insurance.7 Equals Government services./4 Composed of house rentals and personal services.75 Preliminary estimate.

- 10 -

although investment demand was probably not as buoyant in those years. Small-and medium-scale firms were most seriously affected by the lack of investmentfunds, and, as a result, an increasing concentration of credit and investmentin the larger firms occurred during this period. Foreign investment, mostlyin exploration for oil and other natural resources, rose from US$12 millionin 1976 to an estimated US$42 million in 1977, but still constituted a smallportion (1.5%) of Colombia's total investment. Public sector investment,which was curbed by the Government's contractionary fiscal policies, did notincrease in real terms during the 1976-77 period. By restricting capitaltransfers to the decentralized agencies, which carry out over three-quartersof all public sector investment, the Central Government was able to limitgrowth in their investments to about 5% in real terms.

21. As a result of rapid growth in the labor intensive manufacturingand service sectors of the economy, open unemployment in urban areas ofColombia declined to an estimated 8% in December 1977, as against 9.2% inDecember 1976 and 10.5% in October 1975. 1/ Moreover, labor shortages werereported in several rural areas of the country in 1977, and there is alsoevidence that rural wages increased significantly in real terms over the pastcouple of years. Both of these developments appear consistent with the declinein the rural/urban migration rate and with the slight drop in the participationrate in urban areas that have apparently occurred in recent years.

22. These changes in the rural/urban demand and supply of labor seemto have caused a relative improvement in rural wages in Colombia since 1975.While average real wages in urban areas declined by an estimated 13% duringthe 1976-77 period of high inflation, real wages in rural areas are estimatedto have risen by about the same percentage. The lack of adjustment in publicsector wages, with government encouragement for similar wage restraint by theprivate sector, probably explains the decline in urban real wages. There issome evidence that increases in fringe benefits offset some of the losses inreal base wages in urban areas, but, despite this, the real value of totalremuneration of urban workers has apparently declined. Minimum wages havebeen maintained in real terms since 1974 through periodic adjustments,however these apply to a small proportion of the labor force and are largelyineffective in practice. The higher rural incomes and increased employmentopportunities arising from the coffee boom no doubt contributed stronglyto the increase in real wages in rural areas.

C. The Balance of Payments

23. As a consequence of exceptionally high world coffee prices during1977, Colombia experienced its largest overall balance of payments surplus inthe post World War II period; eclipsing by a substantial margin the previouspeak reached in 1976 (see Table 2). The increase in coffee receipts produceda positive resource balance equivalent to 3.4% of GDP and raised the currentaccount surplus to US$494 million, or 2.5% of GDP, in 1977, from US$237 mil-lion, or 1.6% of GDP in 1976. Drawdowns on foreign loans in 1977 particularlyby the public decentralized agencies, sustained the net inflow of capital at

1/ In the seven largest cities; country-wide employment data are available

only in census years.

Table 2 - COLOMBIA: BALANCE OF PAYMENTS, 1970-77

(In Millions of US$)

1970 1971 1972 1973 1974 1975 1976 /1 1977 /2

Current Account

Exports of Goods and NFS 1,000 974 1,207 1,548 1,858 2,100 2,820 3,427

(of which Coffee) (464) (399) (469) (597) (684) (671) (1,170) (1,685)

Imports of Goods and NFS 1,149 1,285 1,236 1,424 2,072 2,080 2,320 2,748

(of which Petroleum) (84) (131)

Resource Balance -149 -311 -29 124 -214 18 500 679

Factor Service Income (net) -180 -176 -197 -215 -192 -241 -272 -200

Transfers (net) 27 34 35 35 55 47 9 15

Current Account Balance -302 -453 -191 -56 -351 -176 237 494

Capital Account

Direct Foreign Investment (net) 39 40 17 23 36 43 12 42

Private Long-Term Loans 61 66 _55 2 -8 -11 22 -4

Disbursements (128) (145) (139) (60) (50) (76) (87) (55)

Amortizations (67) (79) (84) (58) (58) (87) (65) (59)

Public Medium- and Long-Term Loans 161 130 255 285 158 249 89 194

Disbursements (236) (222) (351) (417) (364) (383) (241) 367

Amortizations (75) (92) (96) (132) (206) (134) (152) 173

Other, Short Term and Errors

and Omissions 35 135 28 -41 -224 13 191 78

Net Change in Reserves 6 82 -164 -213 389 -118 -551 -804

(- = increase)

/1 Revised.

/2 Preliminary.

Source: Banco de la Republica and mission estimates.

- 12 -

about the 1976 levels of US$300 million. Net international reserves of thebanking system rose by an estimated US$804 million for the year, of whichUS$664 million accrued to the Central Bank. Net official reserves reached theunprecedented level of US$1,830 million at year end, equivalent to 11 monthsof merchandise imports.

24. Colombia's total receipts from merchandise exports rose on averageby 28.5% per annum in 1976 and 1977, almost entirely as a consequence of highercoffee prices. Coffee export values rose by 44% in 1977, after having risen byno less than 74% in 1976, while noncoffee export values increased on averageby only 4.2% per annum in the two year period. By 1977, coffee's share intotal goods exports had increased to 60%, from only 40% in 1975. Colombiancoffee fetched an average price of US$2.42/lb in 1977, more than double theaverage 1976 price received and nearly four times the average 1975 price. 1/Coffee export volume, on the other hand, declined by 23% in 1976 and by 15% in1977. The causes of the decline in coffee export volumes during the past twoyears are not entirely clear. The following combination of factors appear tohave been involved. Production declined by 3% in the 1975-76 coffee year(October 1975 to September 1976) and stocks were relatively low, which couldpartially account for the lower exports in 1976 and early 1977. However,production increased by 15% in the following coffee year, and, even allowingfor some rebuilding of stocks, a higher level of exports should have beenfeasible. Also, contraband exports probably increased during this period, asis usual in time of rising coffee prices, diverting some coffee from officiallyregistered marketing channels. Port congestion, caused by large-scale foodimports, may have prevented an acceleration in coffee shipments in 1977, andwith coffee prices on a downward trend beginning in April 1977, importers mayhave held back purchases in anticipation of continued declines in prices.

25. The production of coffee in Colombia has shown an upward trendin the past couple of years, after remaining rather stable at 7-8 million60 kilos bags during the past decade. The major cause of the increaseproduction was the introduction of new technology which substantially raisedthe yield per hectare, without any loss in the quality of the coffee producedor commensurate increase in the cost of production. Largely as a result ofthis new technology, production for the 1977-78 coffee year rose to a record10.6 million bags. Further gains are projected in subsequent years, as the newtechnology is extended to additional coffee areas, with production expected tolevel off at 12-13 million bags in the early 1980s. An increase in productionof this magnitude, given recent trends in world production and consumption,has important implications for current coffee marketing policy and for therole of coffee in the Colombian agricultural sector. Careful considerationneeds to be given to these questions in the context of future economic planning.With domestic consumption at about 1.5 million bags and exports projected at9.0 million bags in 1978, stocks could exceed 6 million bags by year end.This would appear to be well above the level required to guarantee efficientmarketing of coffee.

1/ Average monthly New York price quotations for Colombian coffee soared toUS$3.28/lb by April 1977, following sizeable increases in 1976; declininggradually thereafter to US$2.00/lb by December 1977 and to US$1.91/lbin June 1978. The average annual New York price quotation in 1975 wasUS$0.82/lb.

- 13 -

26. Colombia's coffee export policy was modified in mid-1978. Coffeeexports were accelerated, despite declining prices, in an effort to reduce thelarge stocks accumulated as a result of high production and low sales inprevious months. One advantage of this shift in policy is that any futureinternational coffee agreement will probably base country export quotas onrecent export performance, so that raising exports now would likely guaranteea higher quota for Colombia in any future agreement. With coffee outputexpected to increase rapidly in both Colombia and Brazil, internationalagreements will probably be required to sustain remunerative prices in thefuture. It should be noted, also, that Brazil's coffee output is apparentlybecoming less susceptible to frosts, since a larger proportion of its coffeeis being grown in frost-free areas. Thus, the favorable effect on worldcoffee prices of periodic frosts in Brazil may dimi-tish in the future.

27. In contrast to the large increase in the value of coffee exports,Colombia's noncoffee exports stagnated during the past two years. Therewere sev-ratl reasons for this. Exports of certain food items previoutslyexported in large amounts were prohibited because of supply shortages on thedomestic market, and relatively attractive domestic prices caused the diver-sion of many items from exports to the domestic market. Exports in generalwere hampered by the lowering of export incentives by virtue of slower pesodevaluation and increased protectionist measures in some of Colombia's majortrading partners adversely affected selected export lines, such as textiles.En addition, an apparent sharp increase in smuggling to neighboring countriesof a broad range of Colombian manufacturing and agricultural goods may havediverted a significant amount of exports from the "registered" market.Continued slack demand in some of Colombia's major export markets probablyhindered the growth of exports during this period also.

28. Noncoffee agricultural exports fell sharply in 1976-77, by 6.5%per annum in nominal terms. Decreases were most pronounced for sugar,and cattle and beef exports, while flowers, cotton, bananas and shrimp andshellfish registered significant increases (See Table 3.8, StatisticalAppendix). Sugar exports declined from US$96 million in 1975 to practicallynothing in 1977, when production shortages caused exports to be prohibited.Cattle and beef exports appear to have fallen because of the rebuilding cifherds that had been depleted by heavy sales in previous years. Cotton exports,on the other hand, increased by nearly 17% per annum in current US dollars asa result cf both higher international prices and increased output, and flowerexports rose by 38% due to strong increases in demand.

29. Manufactured exports rose by 12% per annum in nominal terms between1975 and 1977, a very modest increase compared with the large increases(36% per annum) registered in the late 1960s and early 1970s. The diversionof many manufactured goods, which otherwise would have been exported, tomore profitable local markets and a high incidence of unregistered salesin neighboring countries were important causes of the slow growth inmanufactured exports. Also of importance, however, was the reduction inexport incentives during this period. It is estimated that the real effectiveexchange rate, taking account of price and exchange rate movements and

- 14 -

weighted by the non coffee export trade shares of Colombia's major tradingpartners, fell by more than 11% in 1977 and by an estimated 16% since 1975(see Table 3). Although fiscal and credit incentives were increased in thelast two years, they did not rise sufficiently to offset the disincentiveeffects of the lower rate of peso devaluation. The loss of Colombia's sharein the total noncoffee imports of the OECD countries is illustrative of theadverse effects of the decline in export incentives. Since 1975, Colombia'sexports to these countries rose at about one-fourth the rate of the areas'total imports. Moreover, largely as a result of the relatively strong pesodevaluation vis-a-vis some of the European currencies which appreciated withrespect to the US dollar during this period (the peso is tied to the USdollar), the direction of Colombia's export trade changed in favor of thesecountries. An increasing proportion of Colombia's exports are going to theAndean Group countries as well, as a consequence of the reduction in tradebarriers among those countries. Exports of leather and hides, mechanical andelectrical equipment and metallic products increased most rapidly (33%, 29%and 27%, respectively) during this period, while exports of chemicals andpharmaceutical products declined in nominal terms. Exports of all othermanufactured goods either stagnated or grew only modestly in nominal terms.Because world markets for manufactured goods are becoming increasingly competi-tive, it may take Colombian producers some time to regain lost markets onceincentives are right for export expansion.

30. Merchandise imports rose by 23% in current US dollars in 1977,twice as fast as in 1976, reflecting the steep increase in domestic demand,lower production of petroleum and some domestic agricultural goods, and fewerimport restrictions. Registrations of nondurable consumer imports, for themost part foodstuffs to compensate for the poor harvests, increased by anestimated 23%. Fuel imports rose rapidly (56%), reflecting the country'sgrowing dependence on foreign energy sources as a result of declining domesticoil output. Overall, registrations of intermediate goods imports rose by18%. Imports of consumer durables, which were probably most affected by thedecelerating pace of peso devaluation and the expectation of its futureacceleration, increased by an estimated 81% in 1977, while capital goodsimports rose by 22% in current US dollars. The structure of imports since1975, therefore, has shifted towards a greater share of consumer goods intotal imports, mostly at the expense of nonpetroleum intermediate goods.Nevertheless, imports still constitute a relatively small proportion ofColombia's total demand for consumption goods, while a large proportion ofits use of intermediate and capital goods has to be imported. The directionof imports has changed moderately since 1974, with an increasing proportioncoming from the Andean Group countries, Central America and the Caribbean,and a lesser share from Europe. Colombia's other major suppliers managed tomaintain their relative shares during this period.

31. Colombia's trade and exchange rate policies in 1976 and 1977 werelargely a function of the need to reduce the rate of inflation. In orderto slow the rate of international reserve accumulation, the Government loweredthe rate of peso devaluation, reduced import tariffs and nontariff barriersto imports and raised advance import deposit requirements. Beginning inearly 1977, exporters of coffee and most other major export products wererequired to accept dollar-denominated 90-day certificates of exchange in lieu

Table 3: COLOMBIA - Index of Trade Weighted Real Exchange Rate for Non-Coffee

Exports, Selected Countries, 1970-77, June 1978 1/

(1970 - 100)

1970 1971 1972 1973 1974 1975 1976 1977 1978

USA 100.00 100.6 97.3 93.4 90.6 86.8 82.6 73.4 54.7

Venezuela 100.00 101.6 98.6 91.0 87.0 87.1 84.8 78.8 58.6

Ecuador 100.00 88.4 88.2 85.1 85.2 86.2 86.8 82.2 64.9

Peru 100.00 104.0 103.3 95.9 91.6 94.1 81.1 44.3 50.4 un

Germany 100.00 106.5 110.8 119.6 114.2 104.9 108.9 95.1 74.1

Netherlands 100.00 106.2 113.0 118.4 108.7 108.9 100.2 95.8 74.6

United Kingdom 100.00 107.7 107.9 96.4 92.6 95.6 82.3 79.5 63.1

Weighted Average 100.00 103.8 101.5 99.1 95.1 93.0 88.4 77.9 61.1

Source: Bank Staff Estimates

1/ These indicies include an adjustment for certificados de Abono Tributaria (CATS). The countries included inthis index accounted for approximately 64% of the country's total exports in 1975.

16 -