Embed Size (px)

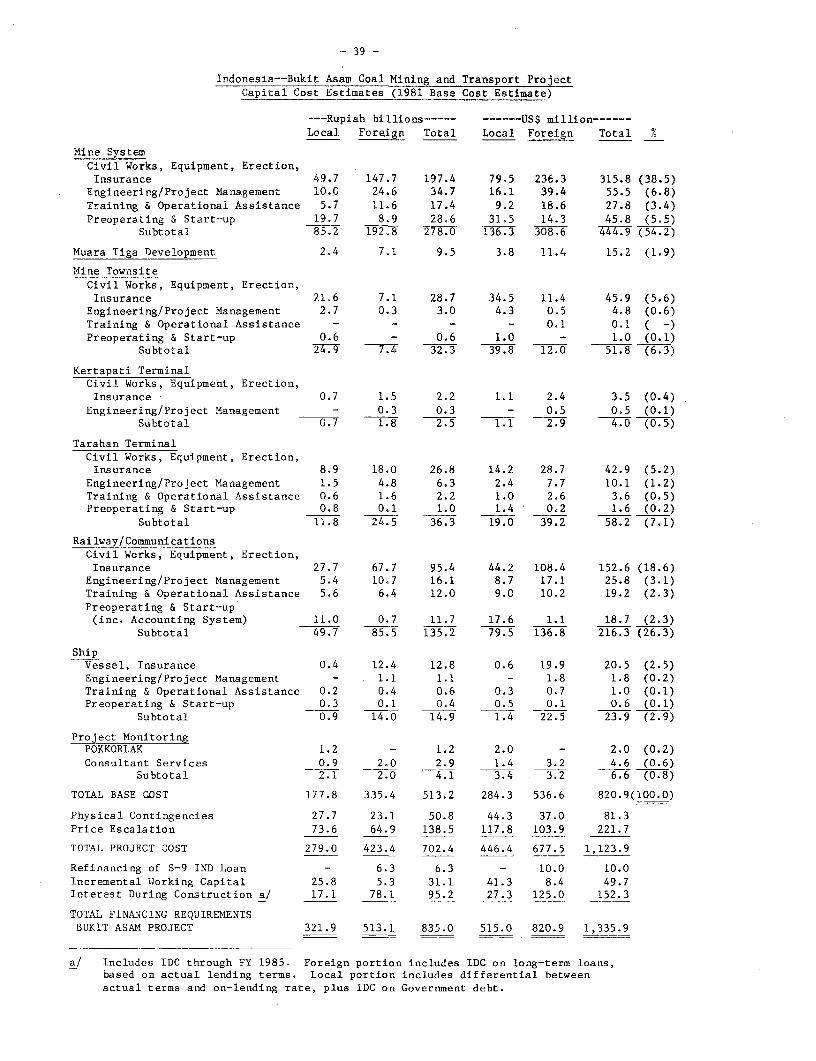

Citation preview

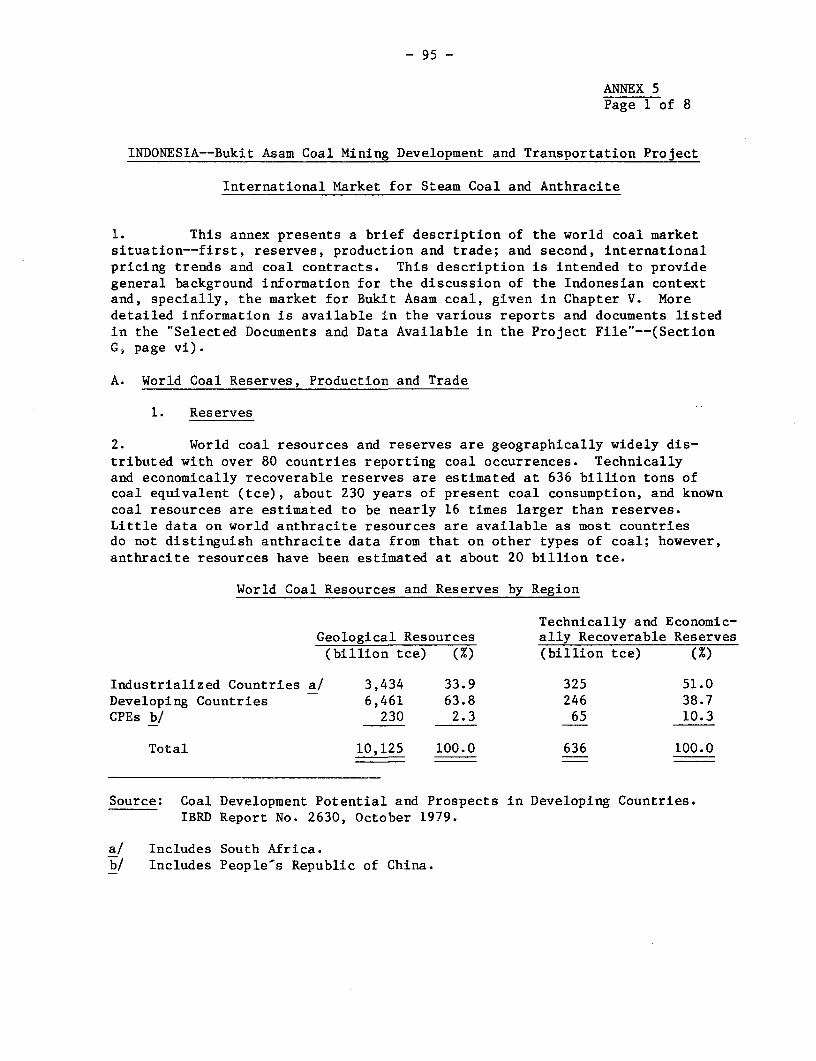

Document of

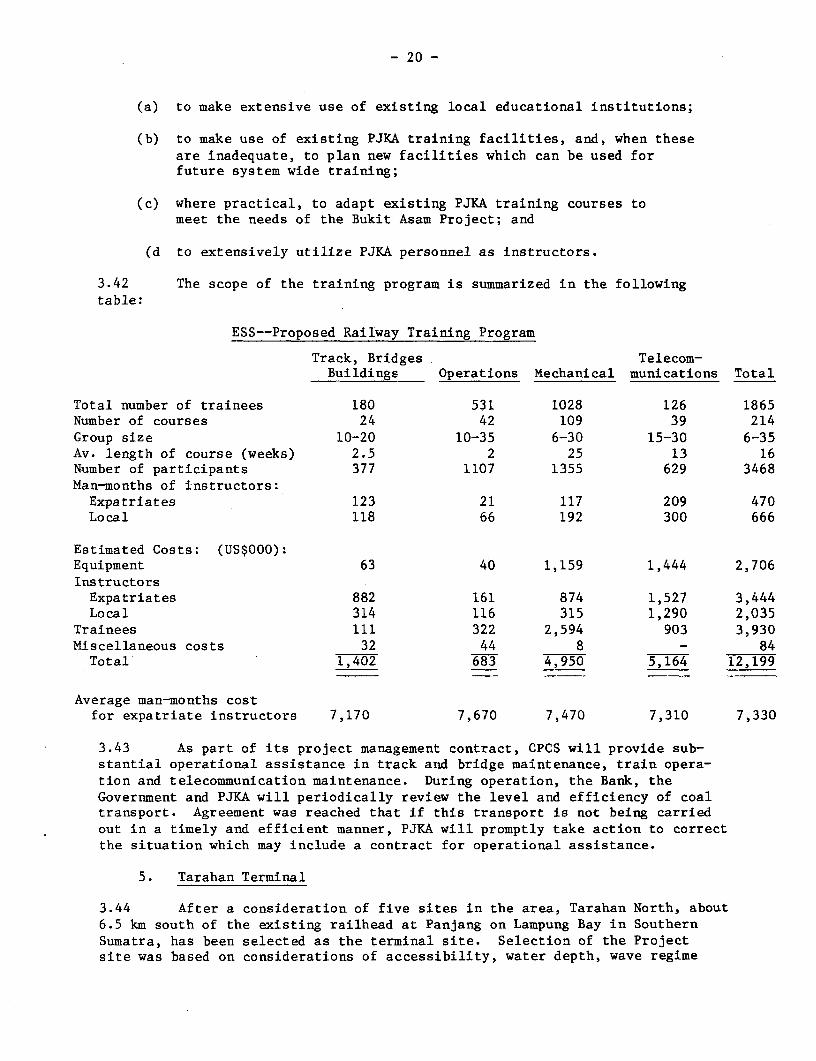

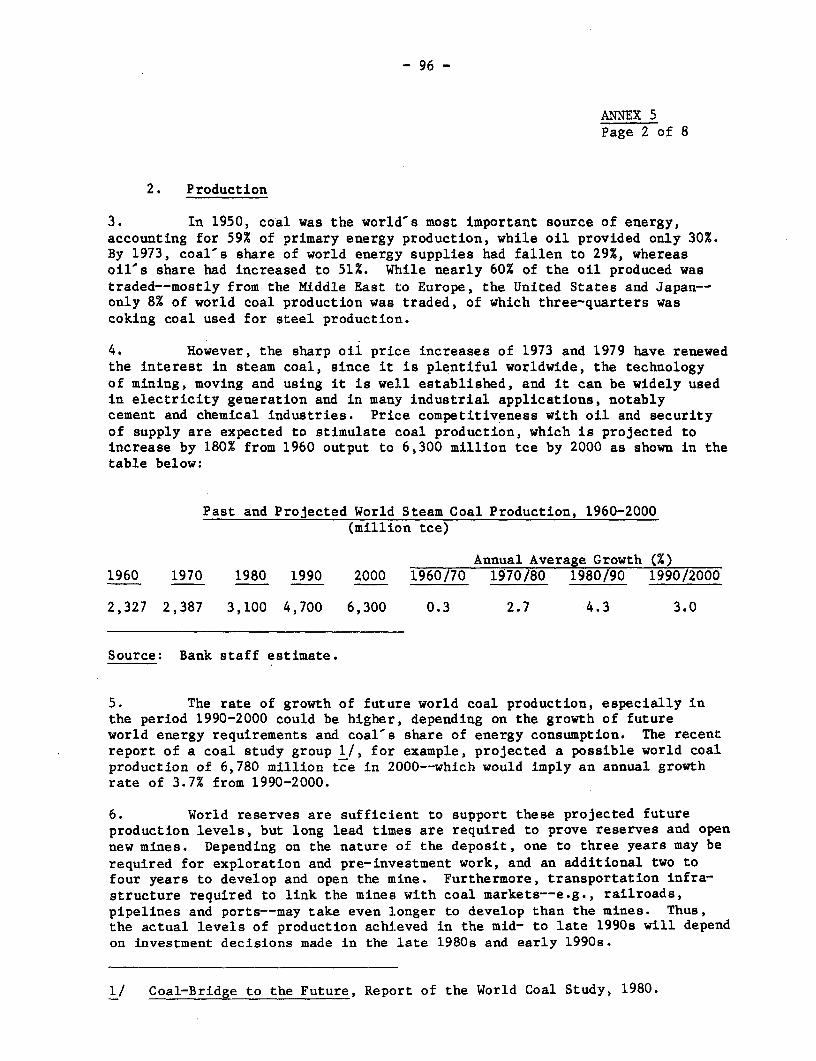

The World Bank

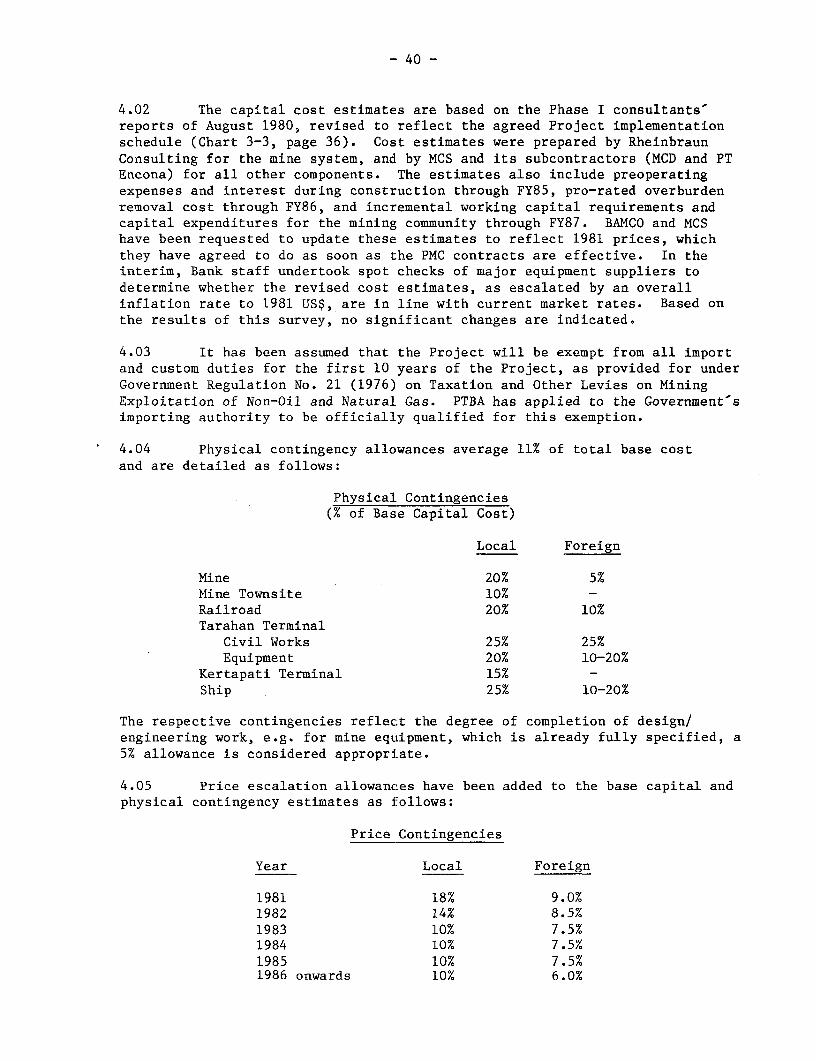

FOR OFFICIAL USE ONLY

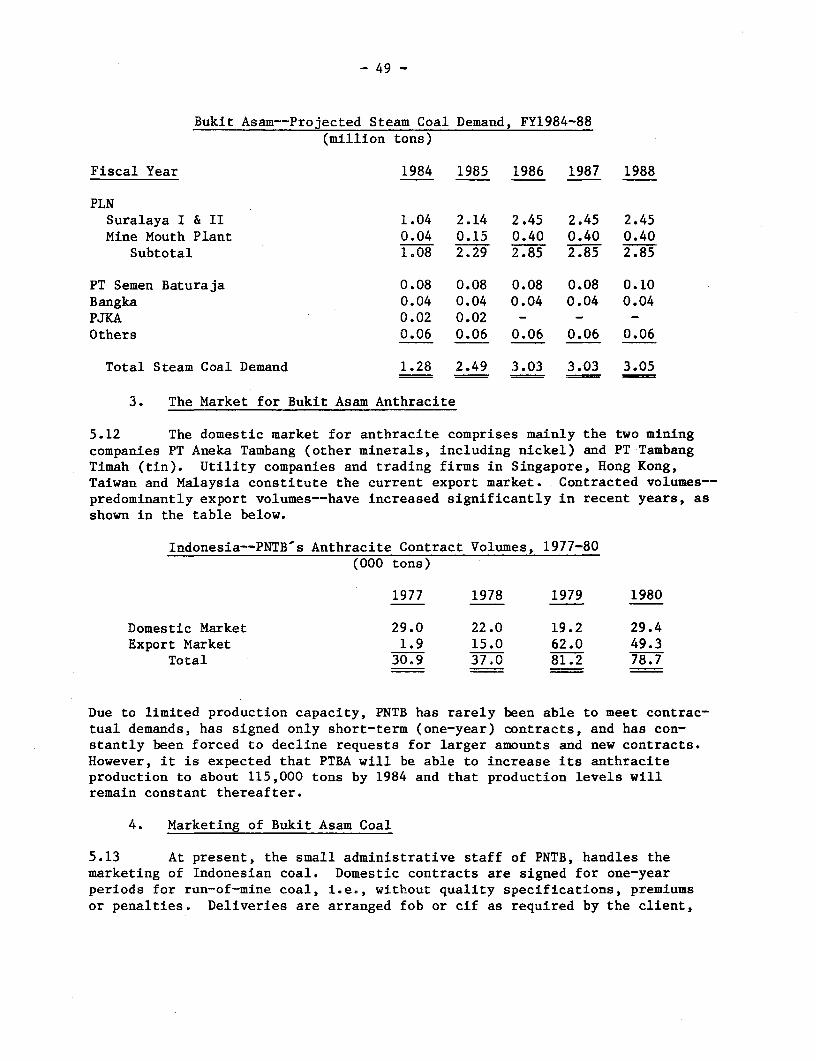

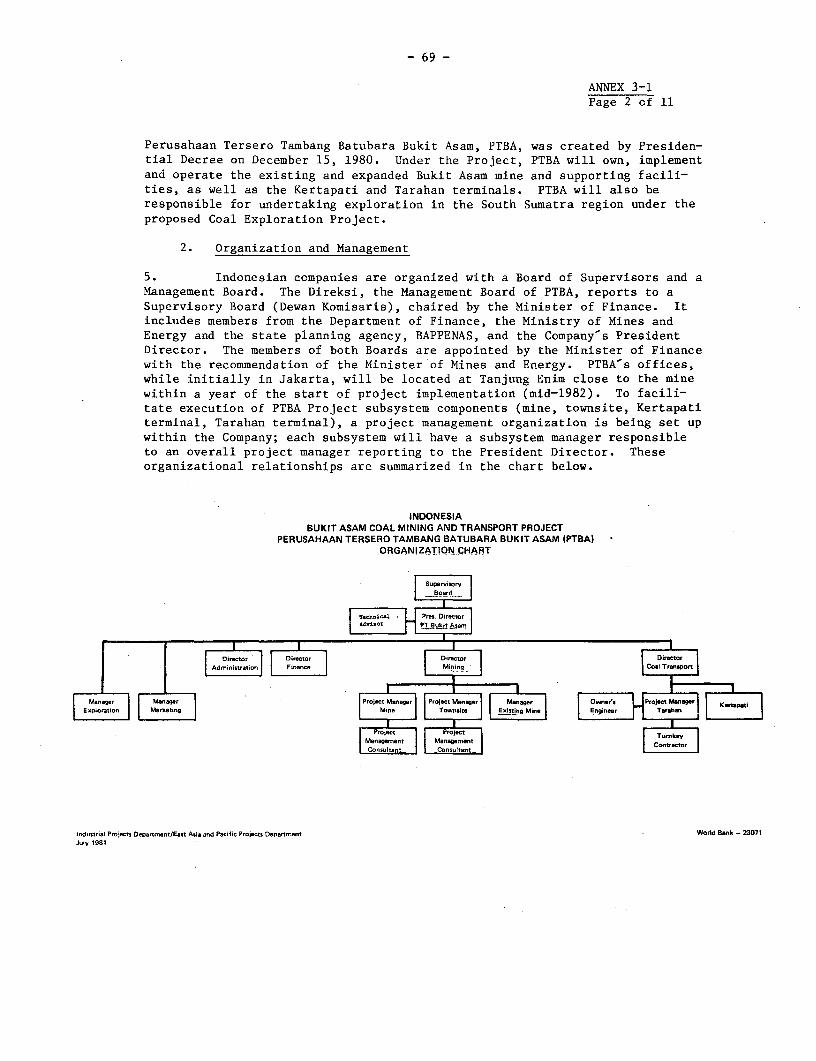

Report No. 3581-IND

STAFF APPRAISAL REPORT

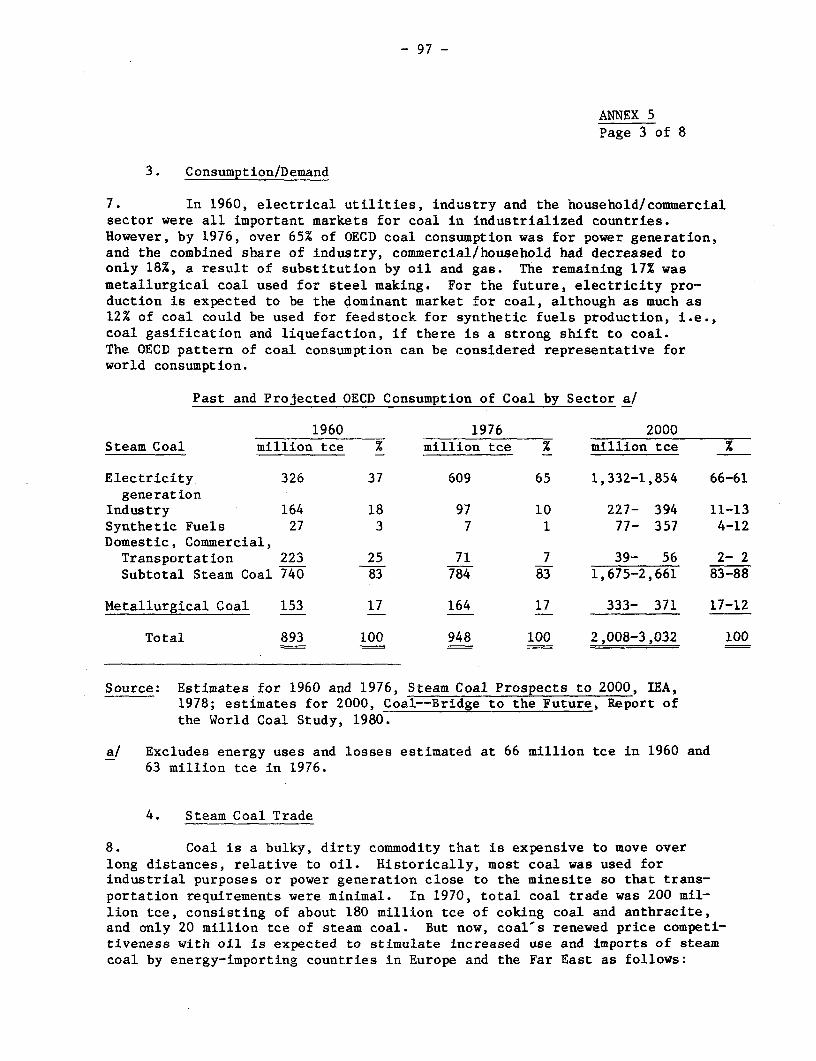

INDONESIA

BUKIT ASAM COAL MINING DEVELOPMENT AND TRANSPORTATION PROJECT

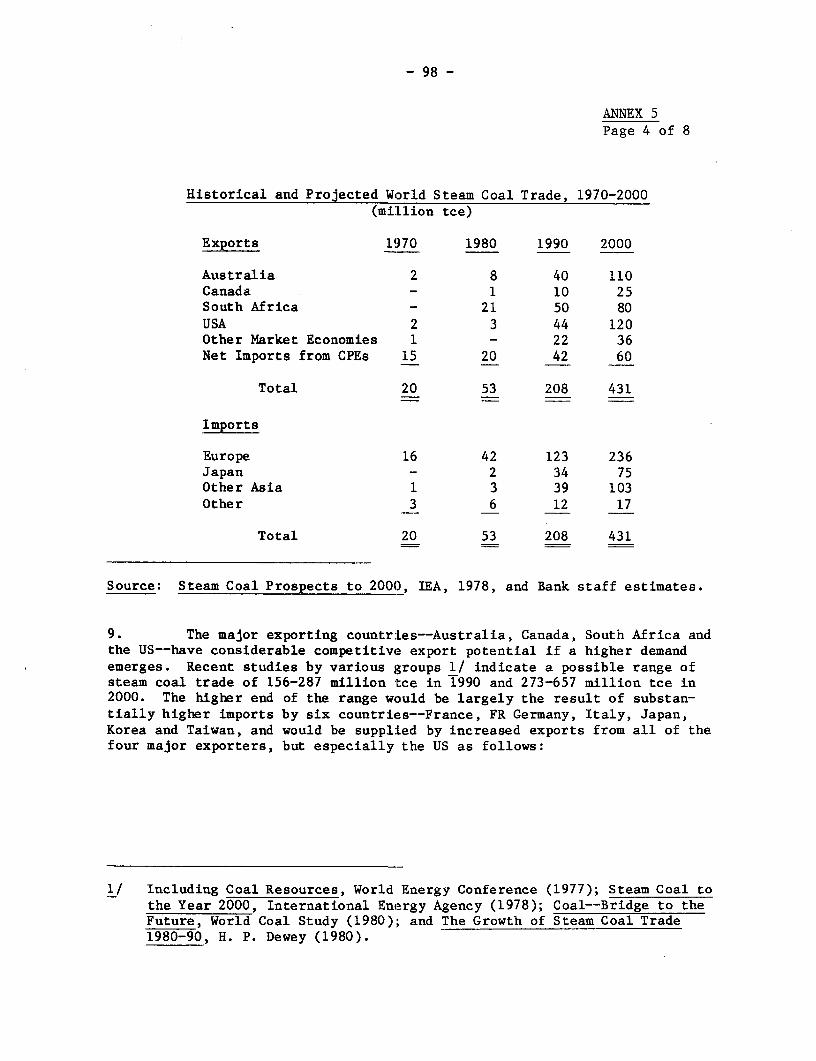

December 9, 1981

Industrial Projects DepartmentEast Asia & Pacific Projects Department

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

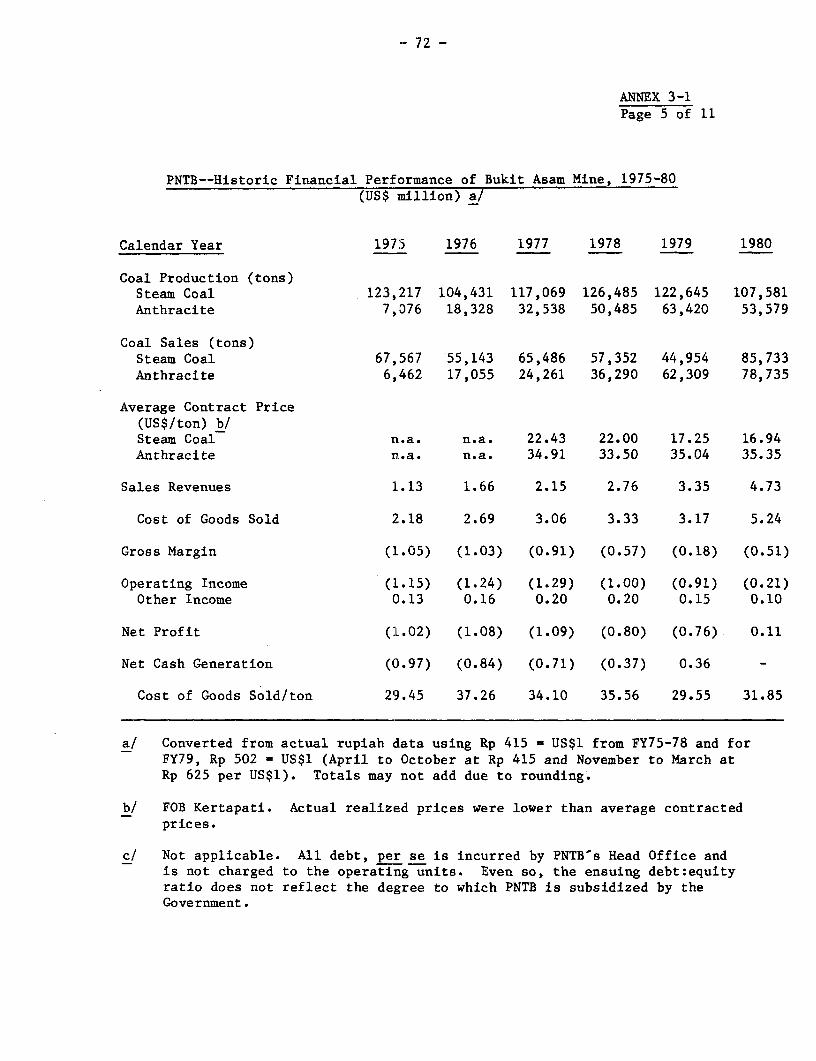

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

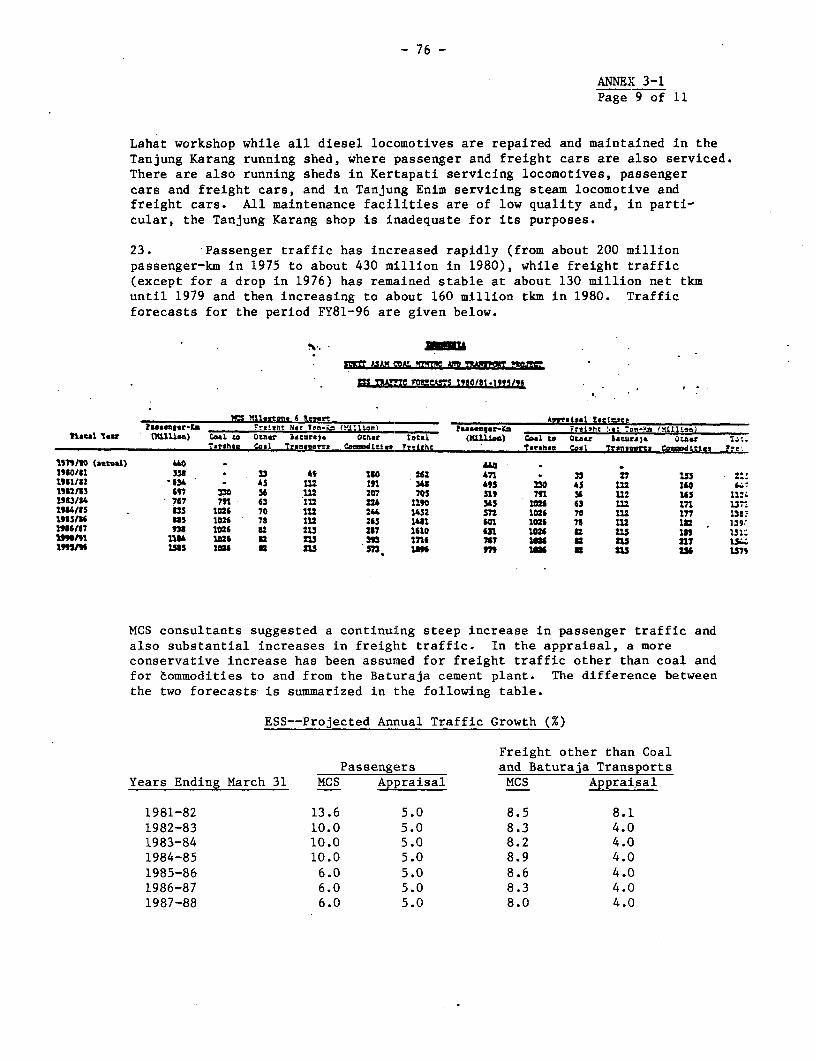

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

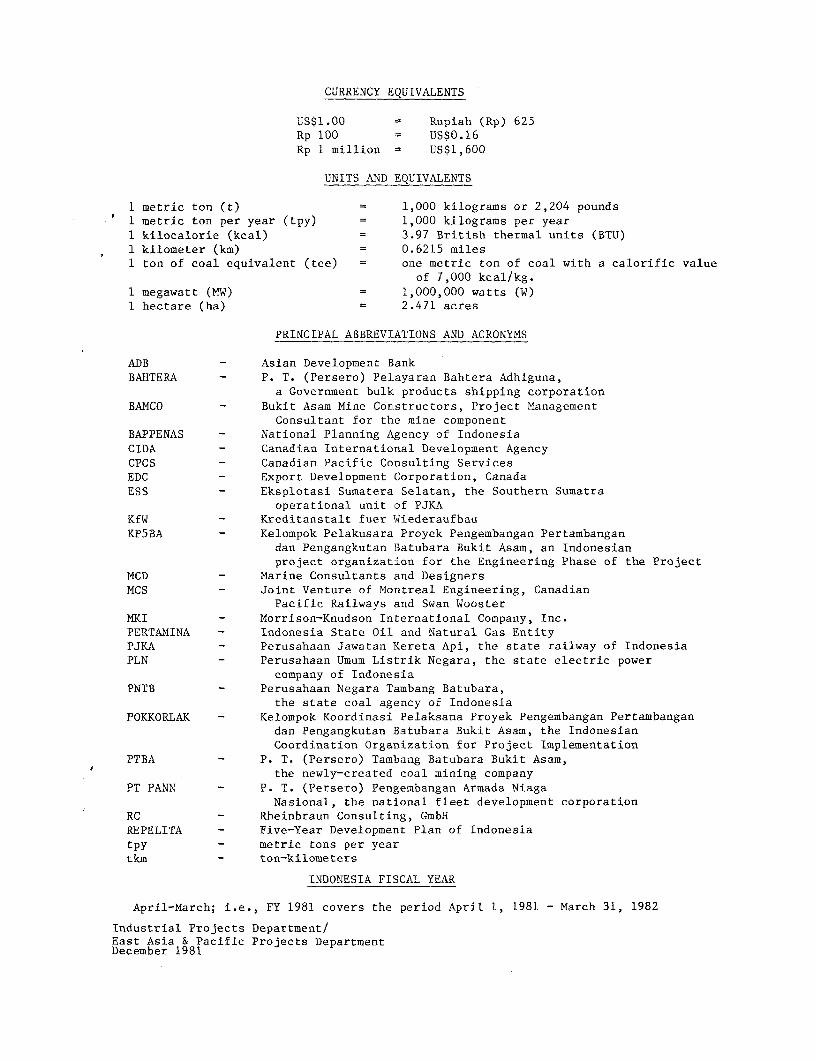

CURRENCY EQUIVALENTS

US$1.00 Rupiah (Rp) 625Rp 100 US$0.16Rp 1 million = US$1,600

UNITS AND EQUIVALENTS

1 metric ton (t) = 1,000 kilograms or 2,204 pounds1 metric ton per year (tpy) 1,000 kilograms per year1 kilocalorie (kcal) = 3.97 British thermal units (BTU)1 kilometer (km) = 0.6215 miles1 ton of coal equivalent (tce) = one metric ton of coal with a calorific value

of 7,000 kcal/kg.1 megawatt (MW) = 1,000,000 watts (W)1 hectare (ha) = 2.471 acres

PRINCIPAL ABBREVIATIONS AND ACRONYMS

ADB - Asian Development Bank

BAHTERA - P. T. (Persero) Pelayaran Bahtera Adhiguna,a Government bulk products shipping corporation

BAMCO - Bukit Asam Mine Constructors, Project ManagementConsultant for the mine component

BAPPENAS - National Planning Agency of IndonesiaCIDA - Canadian International Development AgencyCPCS - Canadian Pacific Consulting ServicesEDC - Export Development Corporation, CanadaESS - Eksplotasi Sumatera Selatan, the Southern Sumatra

operational unit of PJKAKfW - Kreditanstalt fuer WiederaufbauKP5BA - Kelompok Pelakusara Proyek Pengembangan Pertambangan

dan Pengangkutan Batubara Bukit Asam, an Indonesianproject organization for the Engineering Phase of the Project

MCD - Marine Consultants and DesignersMCS - Joint Venture of Montreal Engineering, Canadian

Pacific Railways and Swan WoosterMKI - Morrison-Knudson International Company, Inc.PERTAMINA - Indonesia State Oil and Natural Gas EntityPJKA - Perusahaan Jawatan Kereta Api, the state railway of IndonesiaPLN - Perusahaan Umum Listrik Negara, the state electric power

company of IndonesiaPNTB - Perusahaan Negara Tambang Batubara,

the state coal agency of IndonesiaPOKKORLAK - Kelompok Koordinasi Pelaksana Proyek Pengembangan Pertambangan

dan Pengangkutan Batubara Bukit Asam, the IndonesianCoordination Organization for Project Implementation

PTBA - P. T. (Persero) Tambang Batubara Bukit Asam,the newly-created coal mining company

PT PANN - P. T. (Persero) Pengembangan Armada NiagaNasional, the national fleet development corporation

RC - Rheinbraun Consulting, GmbHREPELITA - Five-Year Development Plan of Indonesiatpy - metric tons per yeartkm - ton-kilometers

INDONESIA FISCAL YEAR

April-March; i.e., FY 1981 covers the period April 1, 1981 - March 31, 1982

Industrial Projects Department/East Asia & Pacific Projects DepartmentDecember 1981

INDONESIA FOR OFFICIAL USE ONLY

BUKIT ASAM COAL MINING DEVELOPMENT AND TRANSPORTATION PROJECT

STAFF APPRAISAL REPORT

Table of Contents

Page No.

I. INTRODUCTION .............................................. 1

II. THE PROJECT SECTORS ........................................ 1

A. Energy Resources, Consumption and Sector Strategy .... 11. Development Strategy ............................. 22. Institutional Framework ......................... 23. Oil ............................................. 24. Natural Gas ..................................... 35. Hydro ........................................... 36. Geothermal ...................................... 37. Coal ............................................ 3

B. The Power Sector ..................................... 5.1. PLN and The Role of the Sector in the Economy ... 52. PLN's Development Plan, including Suralaya

Power Generation ................................ 6C. The Transport Sector ..... ....................... 7

1. General ......................................... 72. Railways ........................................ 83. Maritime ........................................ 8

III. THE PROJECT ................................................ 9

A. Project Objectives ................................... 9B. Project Formulation ................................... 10

1. The Suralaya Power Scheme ....................... 102. Bukit Asam Coal Deposit ......................... 103. Project Preparation - Bukit Asam Engineering Loan 114. Major Design Alternatives ....................... 12

C. Project Description ............. .. .................. 131. Bukit Asam Mine ................................. 132. Muara Tiga Mine ................................. 173. Mining Community ................................ 174. Railway and Communications System .... ........... 185. Tarahan Terminal ................................ 206. The Ship ........................................ 227. Kertapati Terminal .............................. 238. Environmental Considerations ..... ............... 249. Coal Exploration Program ........................ 25

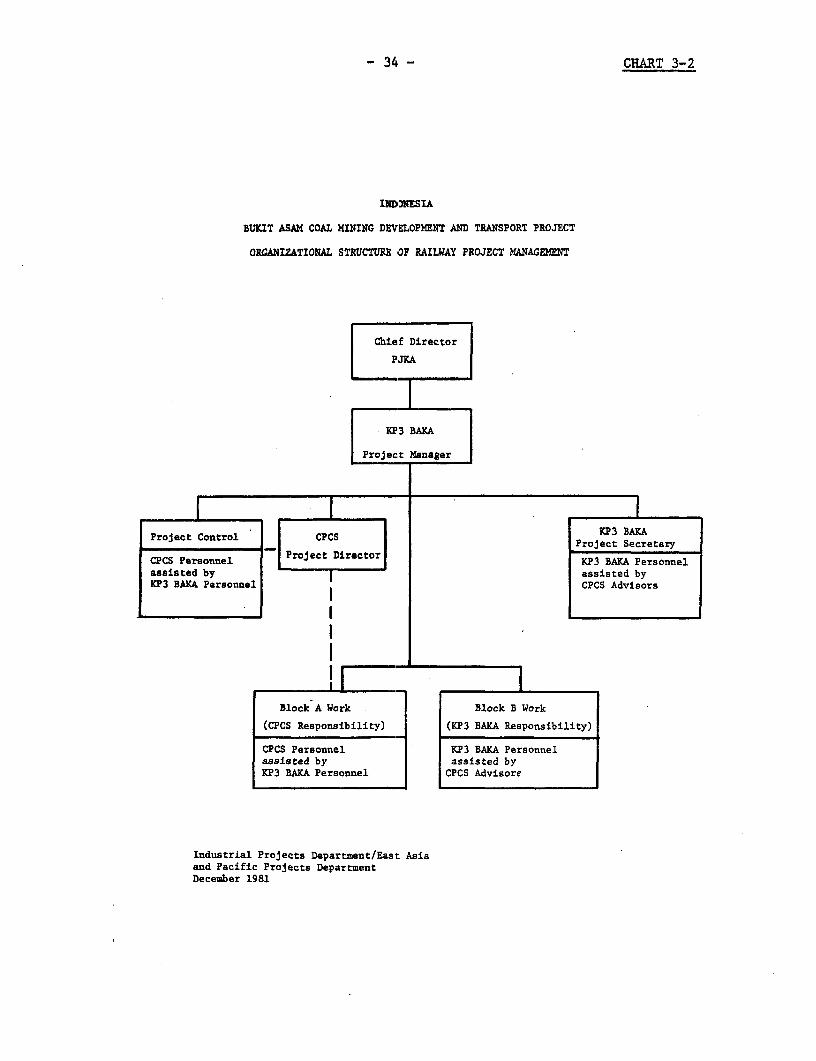

D. Project Execution and Implementation , .. . . 261. Executing Entities .............................. 262. Overall Project Coordination ..... ............... 313. Project Management and Operational Assistance

for Project Components .......................... 314. Project Implementation Schedule .... ............. 35

This report was prepared by Messrs. B. Stenberg and E. P. Rodriguez and Mrs. J.Wright of the Industrial Projects Department; and Messrs. G. Bain, E. Ohlundand L. Siegel of the Transport Division, East Asia and Pacific ProjectsDepartment.

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

-. ii. -

Page No.

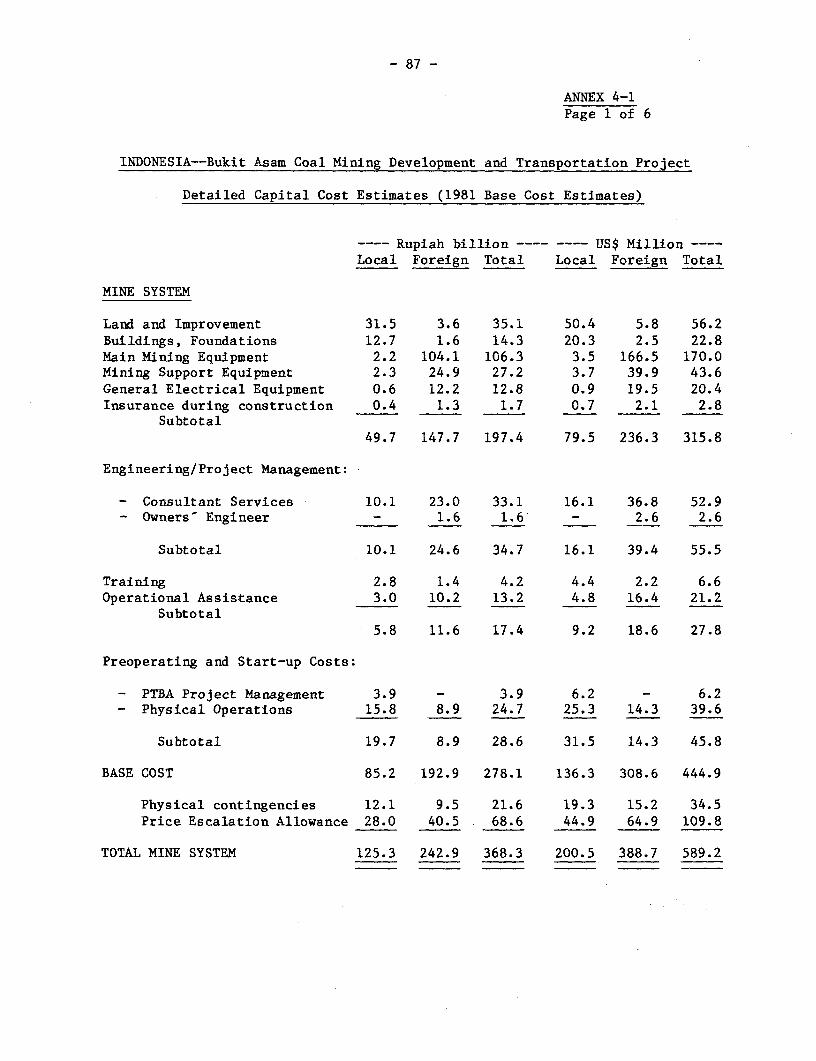

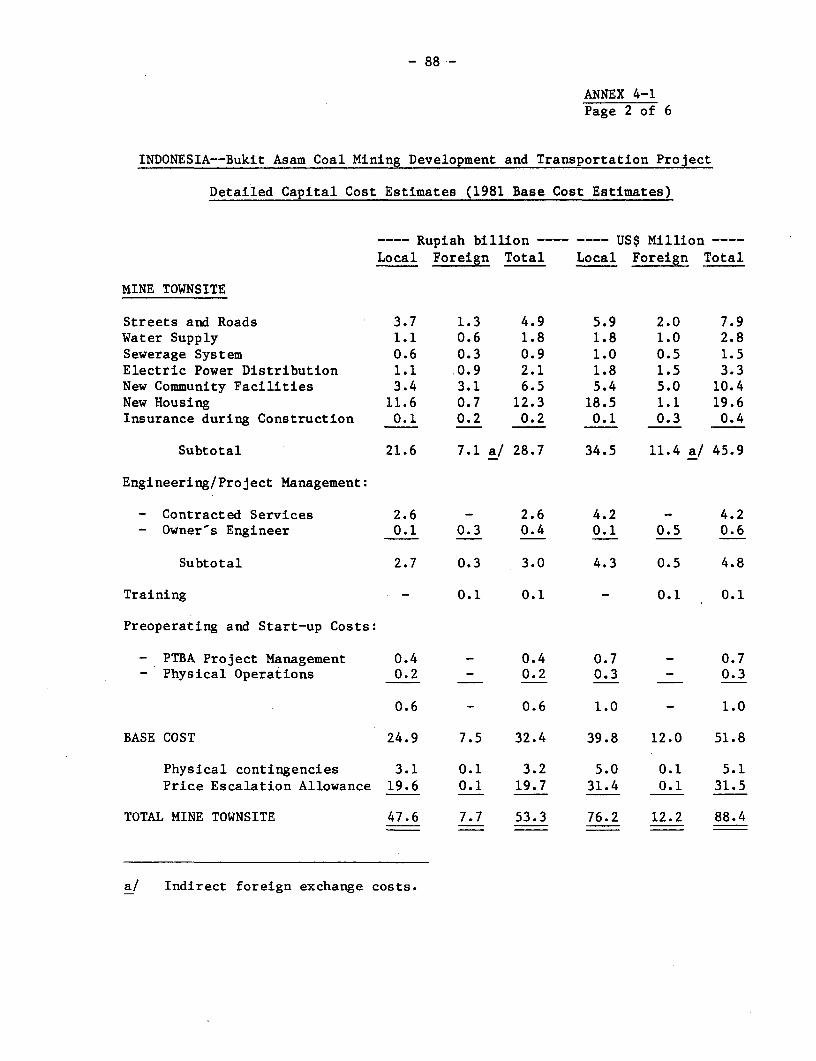

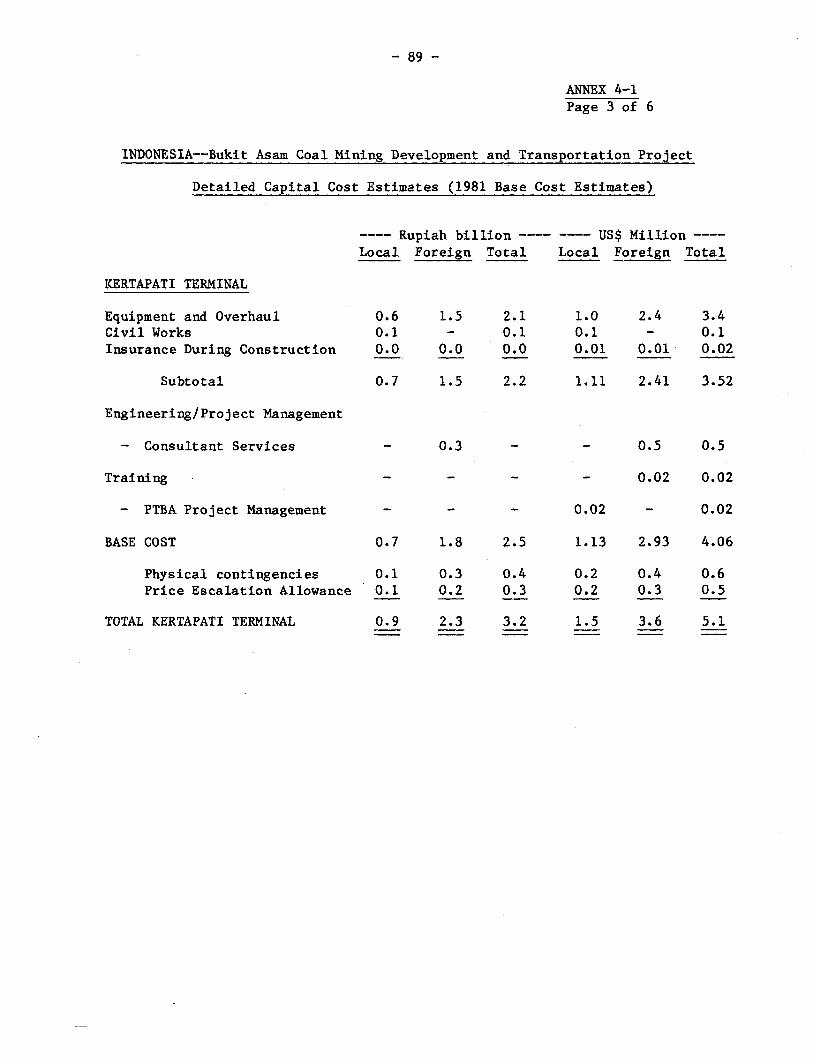

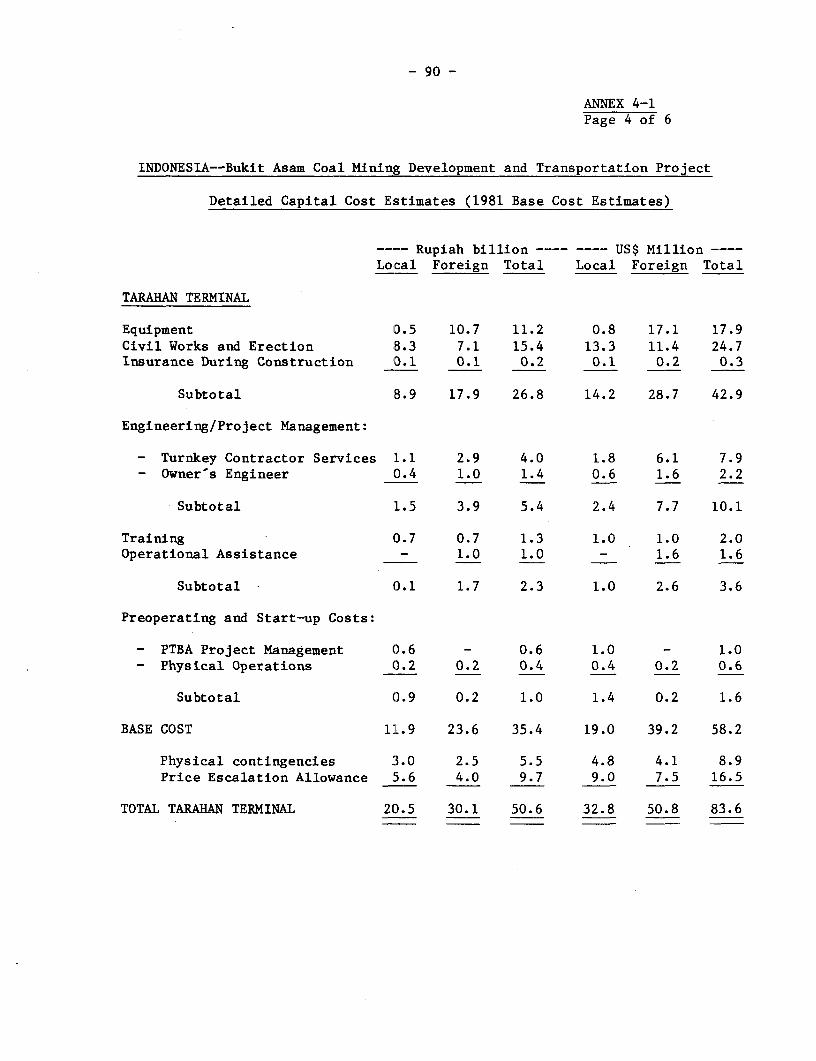

IV. CAPITAL COSTS, FINANCING AND PROCUREMENT ....... .. .......... 38

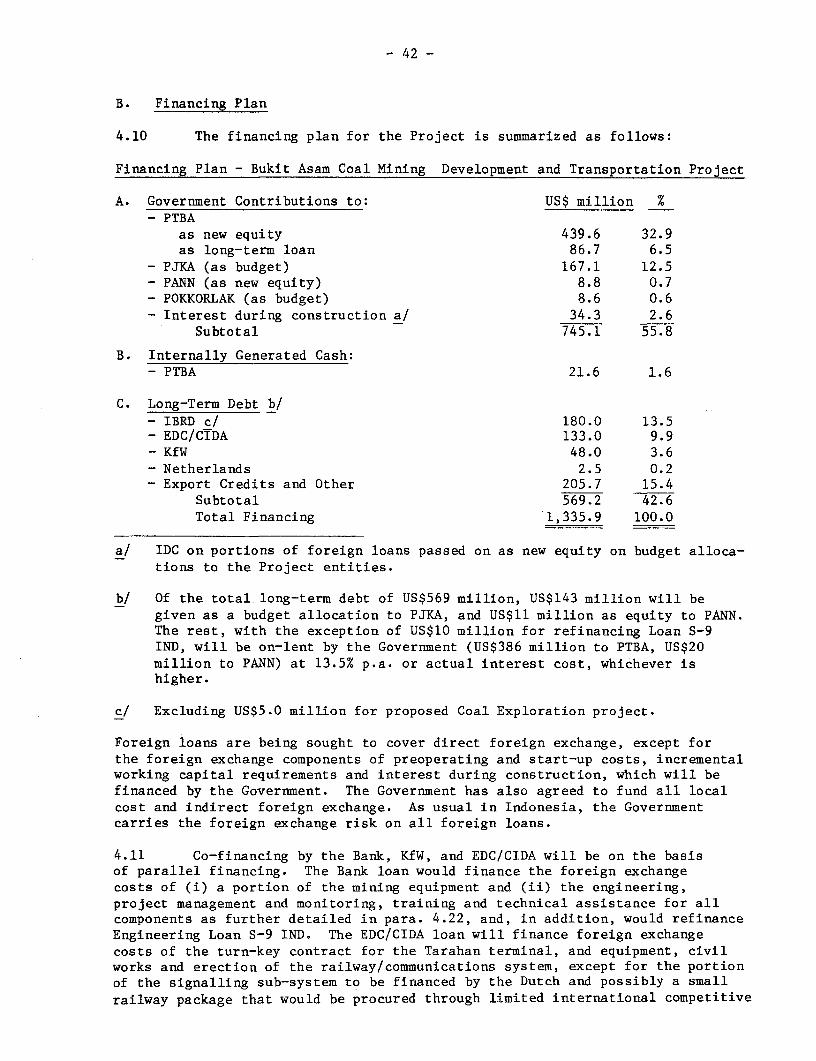

A. Capital Costs ...... ................................... 38B. Financing Plan .... ...................... 42C. Procurement ................ .......................... 44D. Allocation and Disbursement of the Bank Loan.. 45

V. THE MARKET FOR INDONESIAN STEAM COAL AND ANTHRACITE 46

A. World Market Situation and Prospect .46B. The Market and MarketJing of Indonesian Coal ... 48

1. Demand/Supply Prospects . .. 482. The Market for Bukit Asam Steam Coal . .48

3. The Market for Bukit Asam Anthracite . .494. Marketing of Bukit Asam Coal. 495. Coal Pricing Pol:Lcy . .50

VI. FINANCIAL ANALYSIS ... 52

A. Contractual Arrangements . . .52B. PT Bukit Asam ... 53

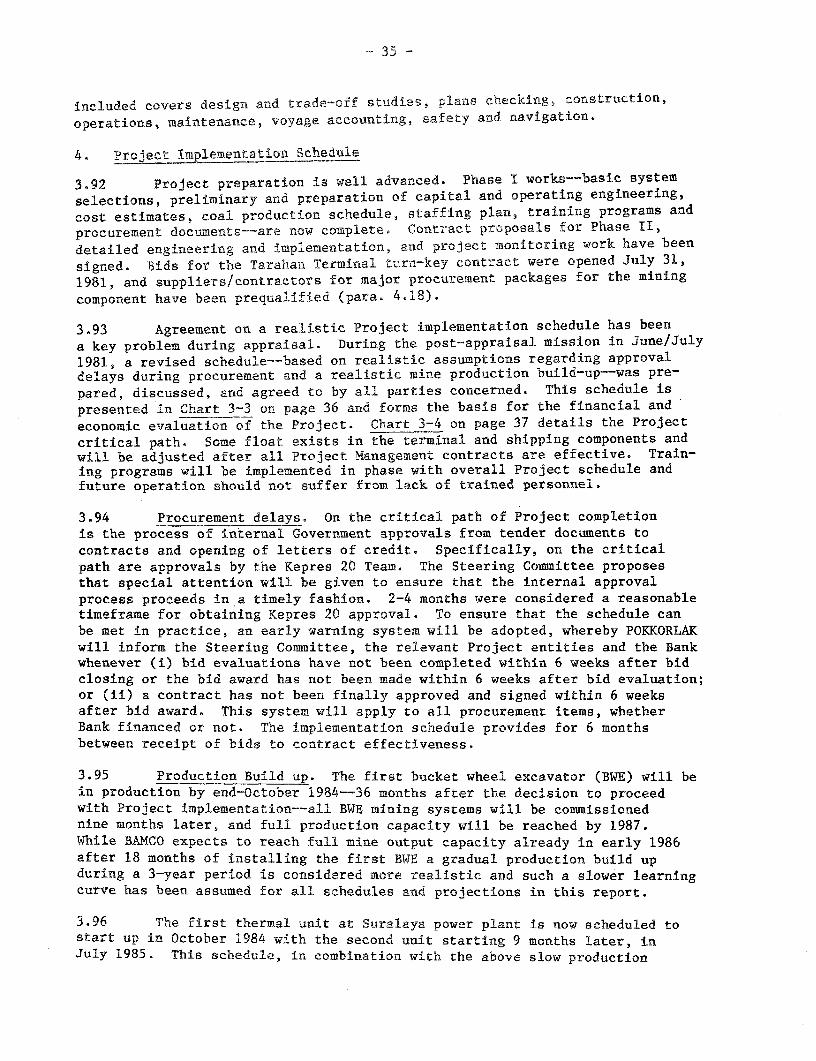

1. Coal Pricing and Revenue Projections . .532. Operating Costs .. 543. Financial Projections .. 56

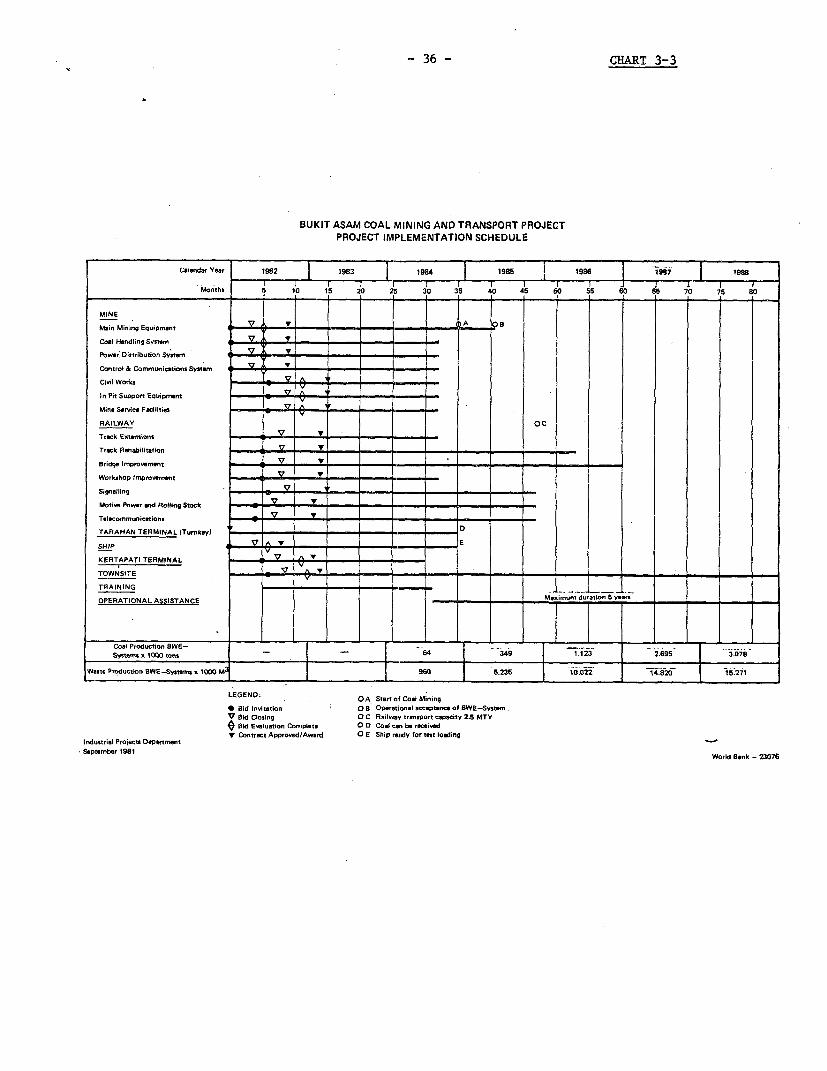

C. PJKA-ESS ... 58D. Financial Rates of Return and Sensitivity Tests 59E. Major Risks ... 61

VII. ECONOMIC ANALYSIS .62

A. Economic Rate of Return .. 62B. Foreign Exchange Benefits . .63C. Institution Building. 63D. Employment and Other Social Benefits . .64

VIII. AGREEMENTS REACHED AND RECOMMENDATIONS .64

- iii -

CHARTS

3-1 Overall Project Implementation Organization3-2 Organizational Structure of Railway Project Management3-3 Project Implementation Schedule3-4 Project Critical Path Schedule

ANNEXES

3-1 The Project Entities - Detailed Description3-2 Muara Tiga - Detailed Description3-3 Railway Component - Detailed Organization Chart for Project Management3-4 PT PANN - Past Financial Results

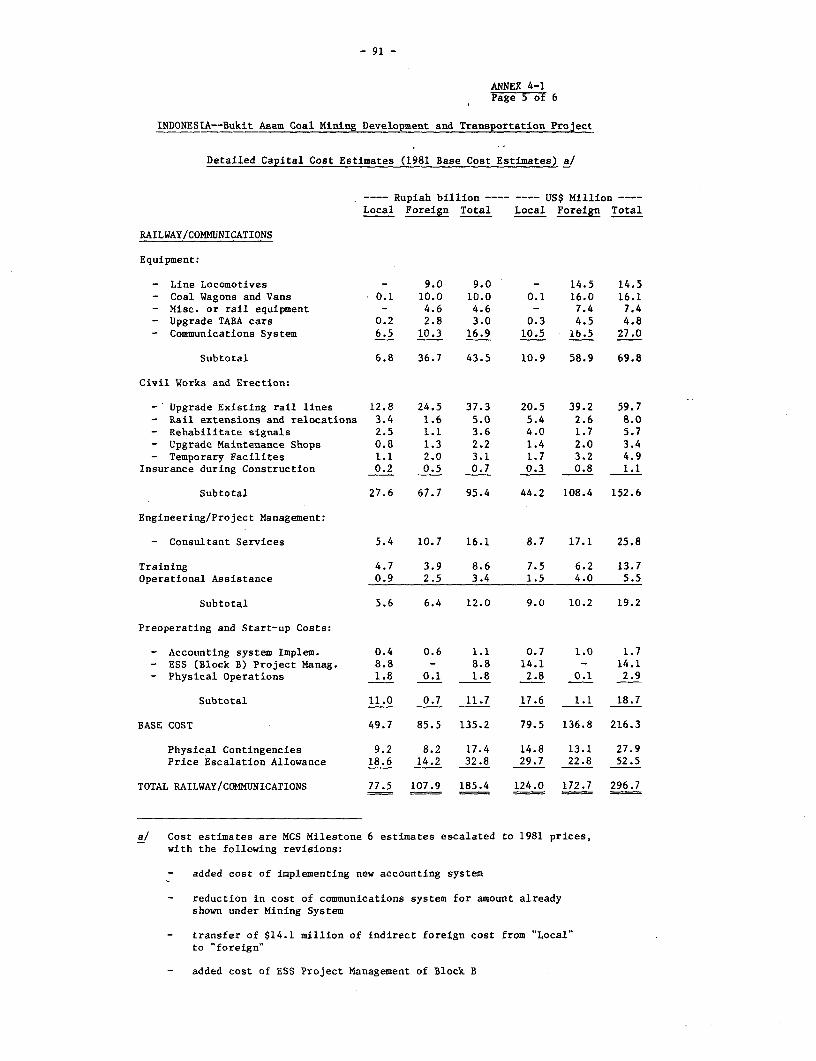

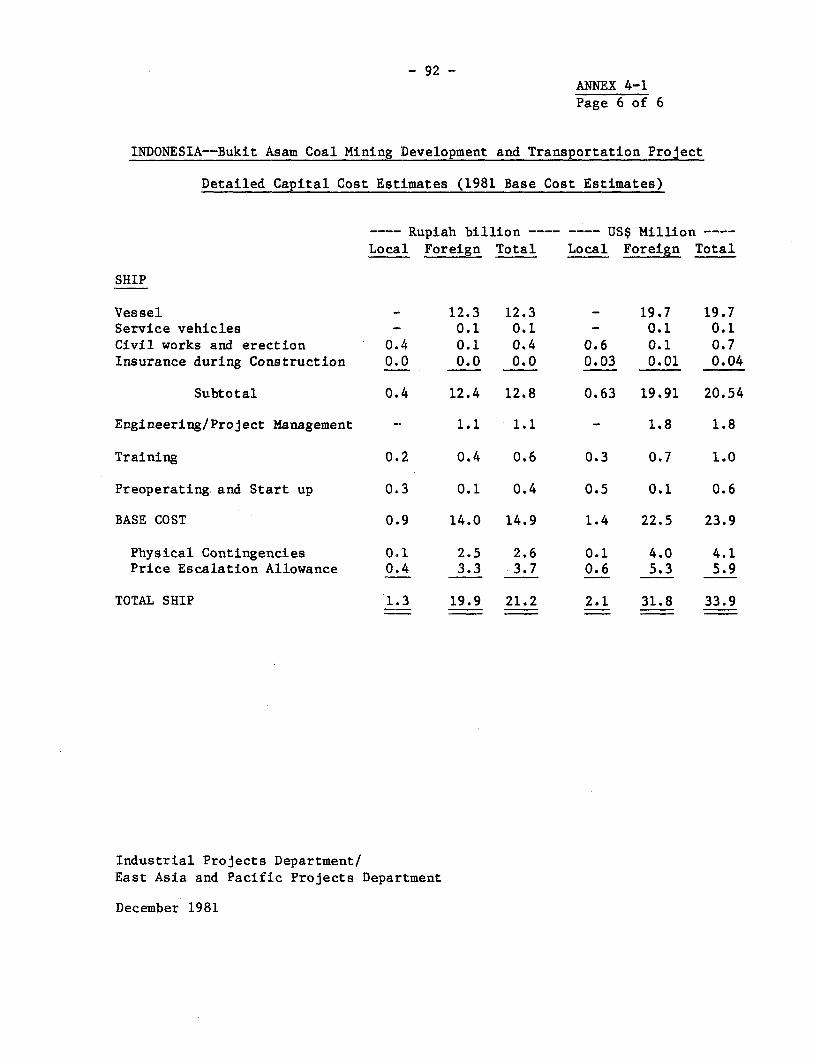

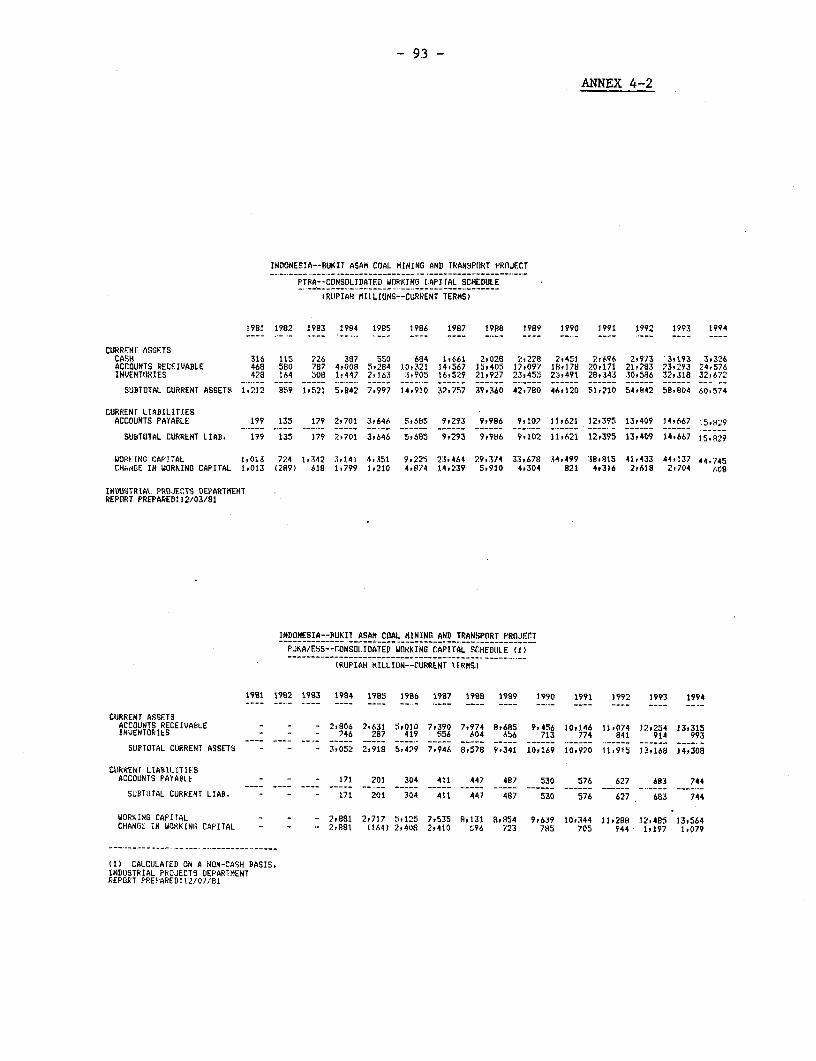

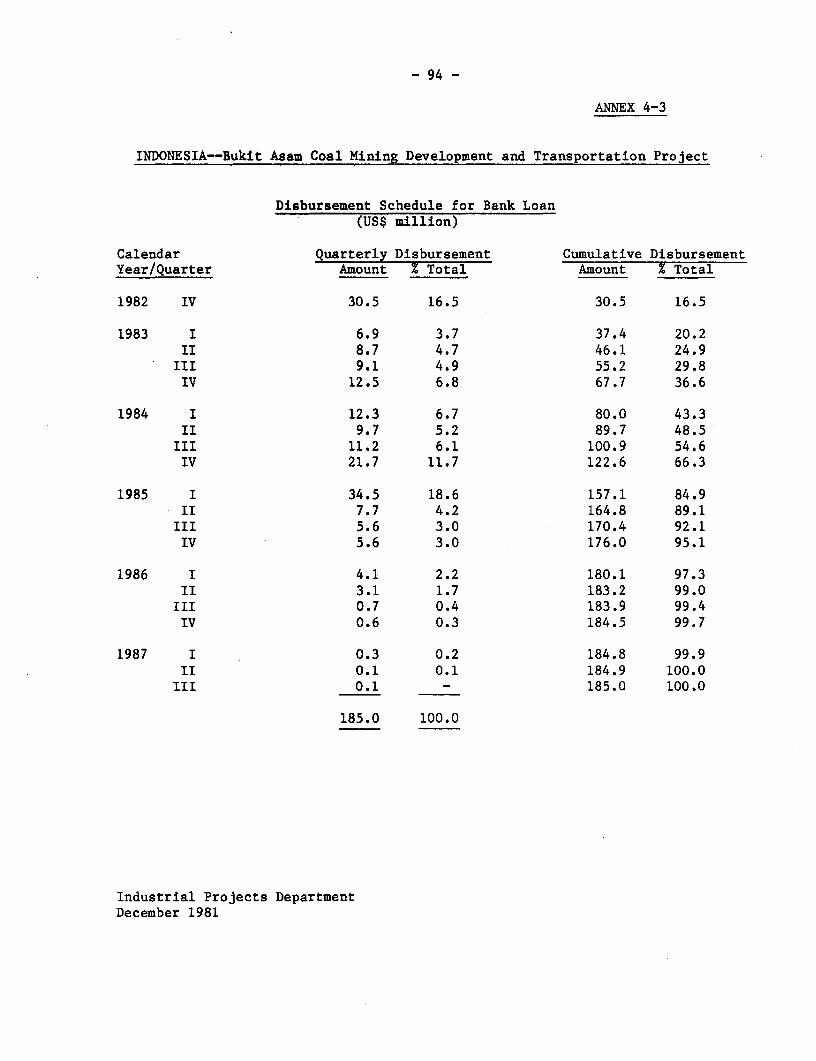

4-1 Detailed Capital Cost Estimates (by Component)4-2 Consolidated Working Capital Schedules--PTBA and PJKA/ESS4-3 Disbursement Schedule for Bank Loan

5 International Market for Steam Coal and Anthracite

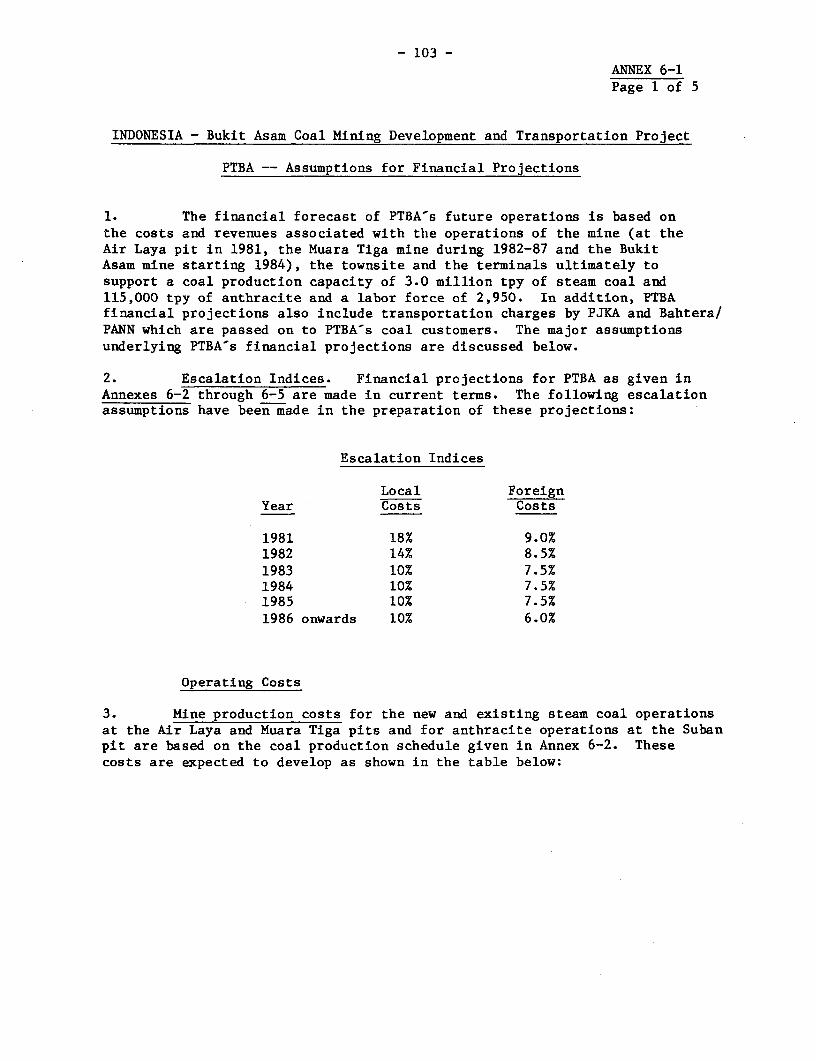

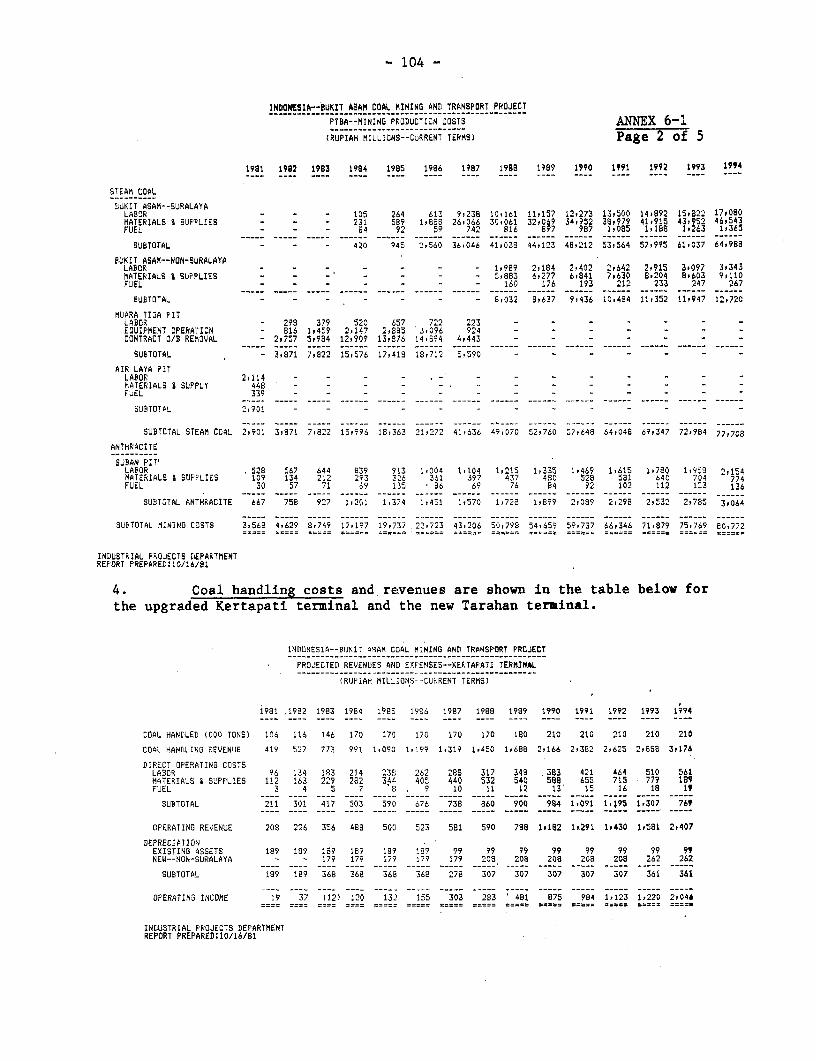

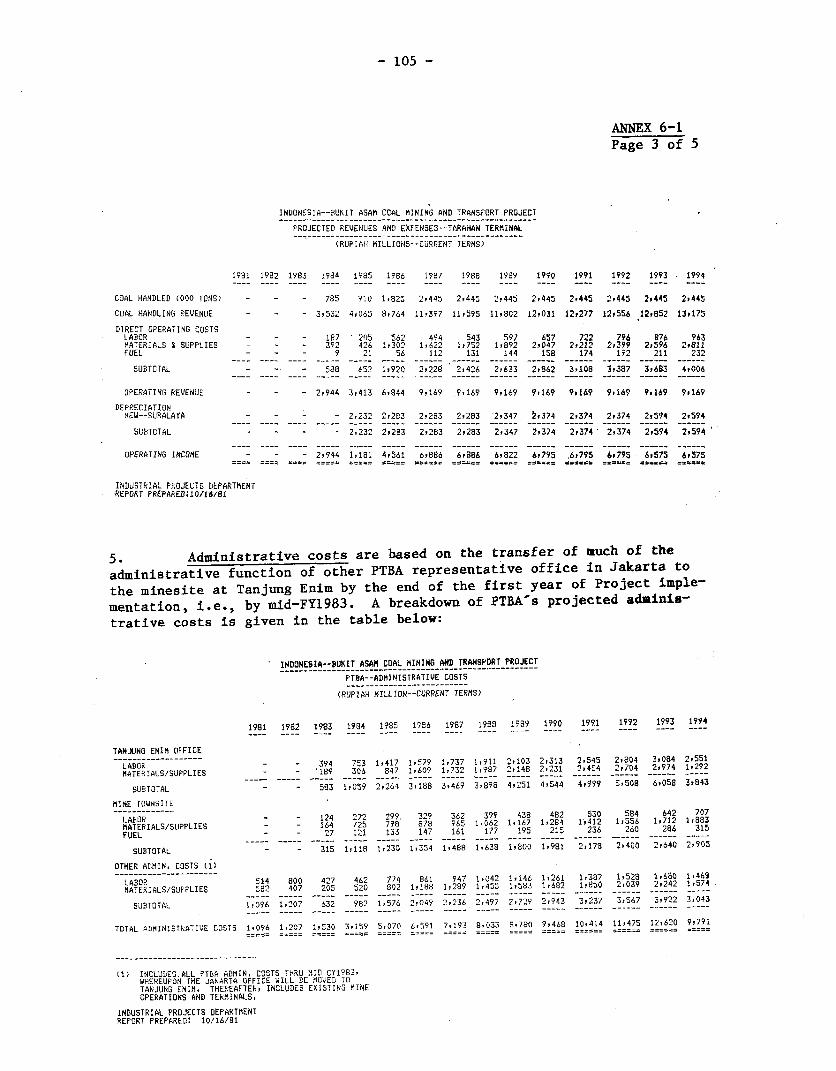

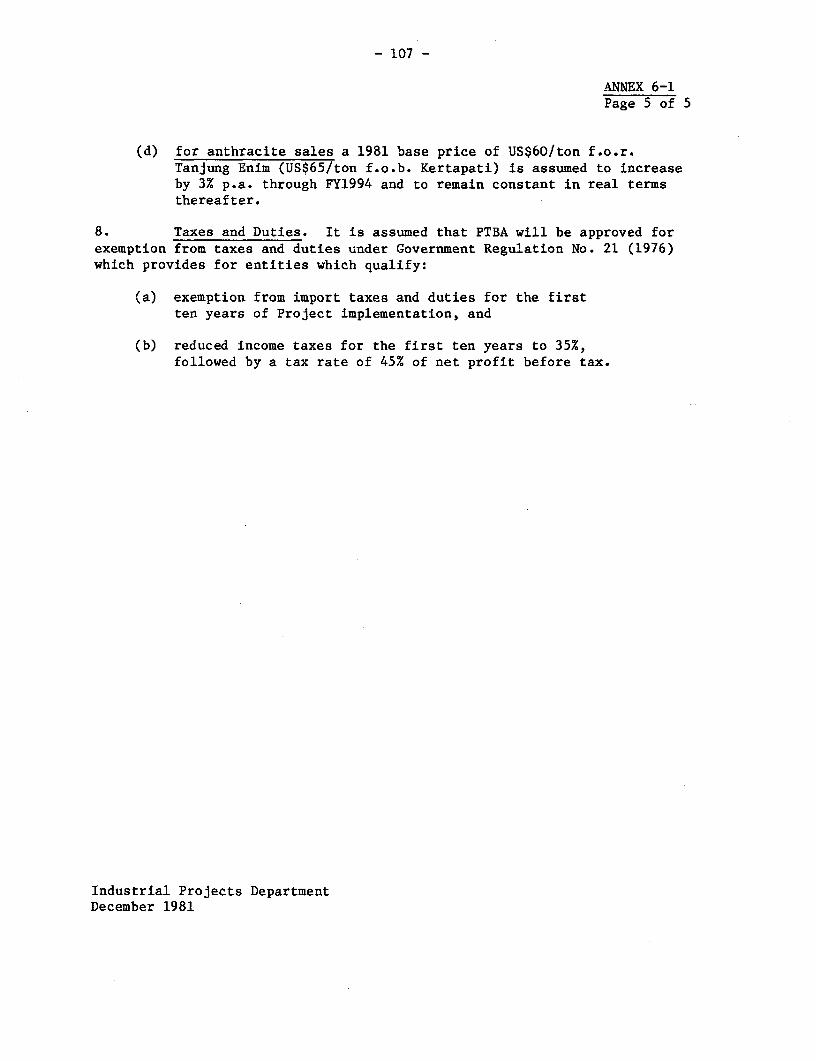

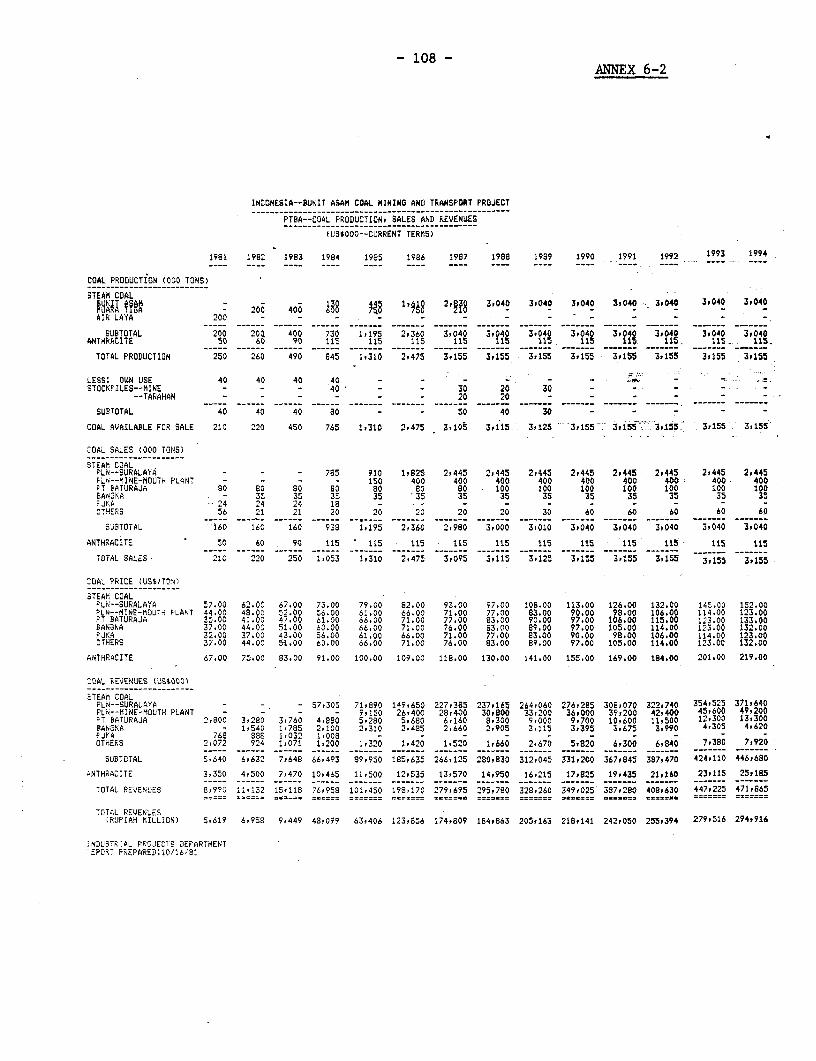

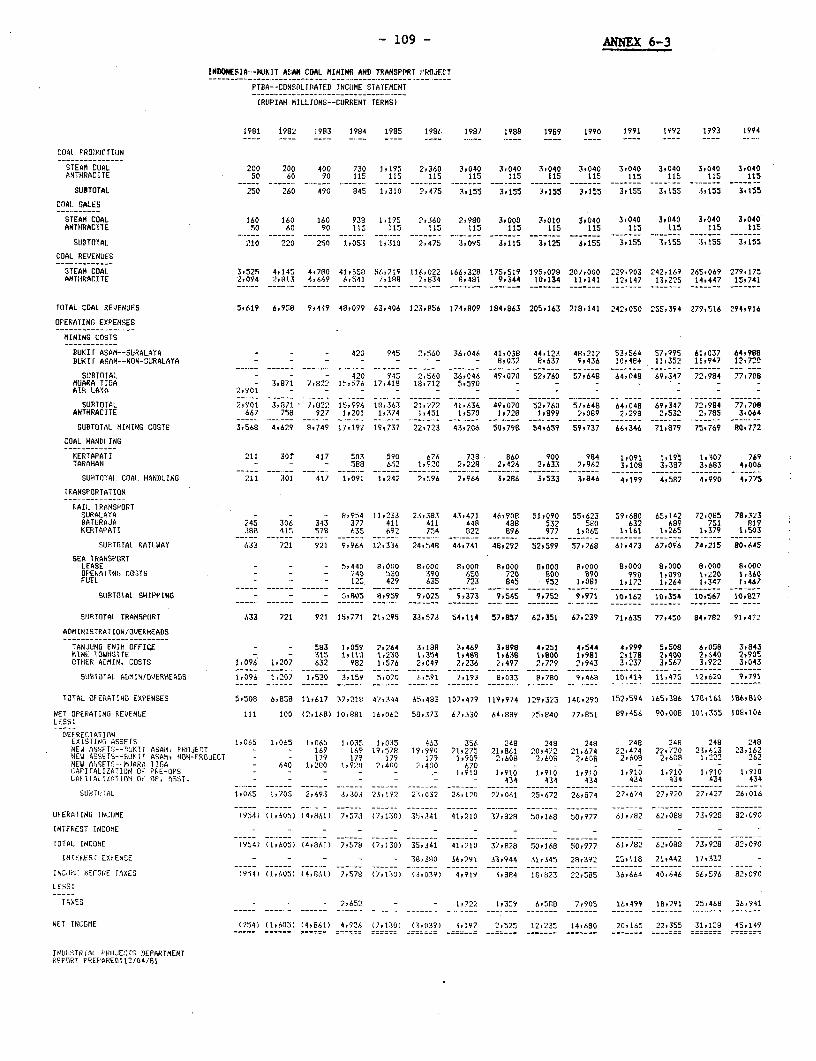

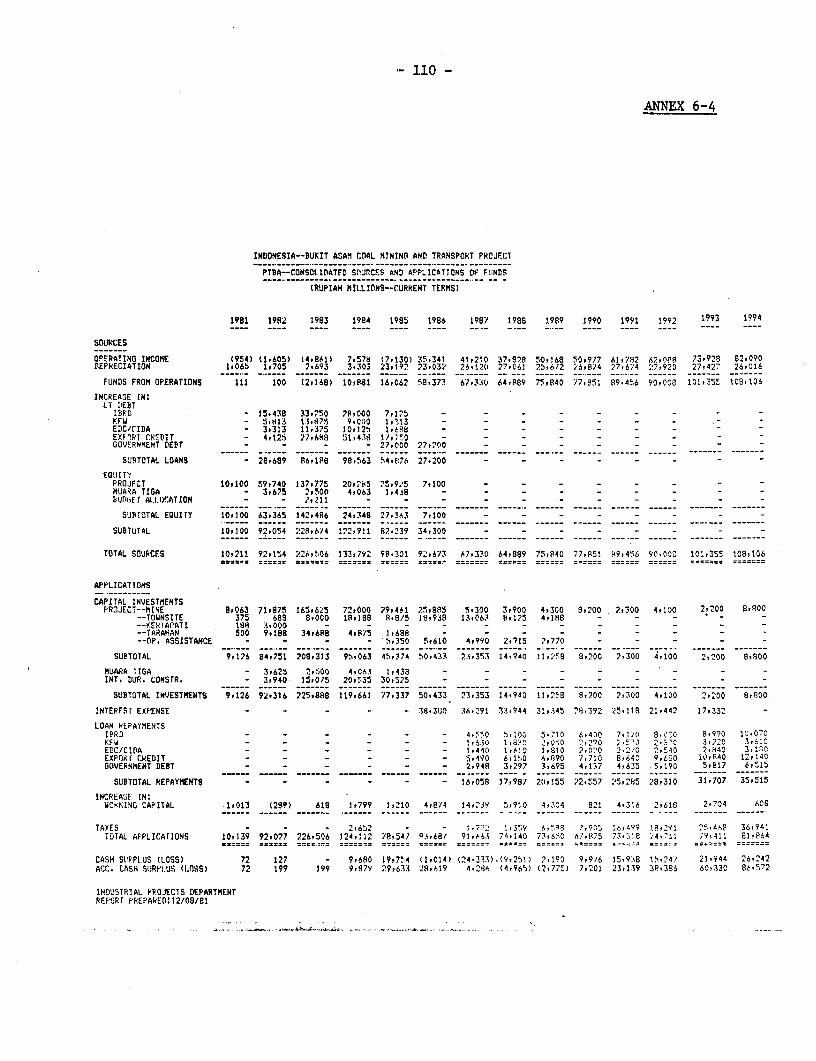

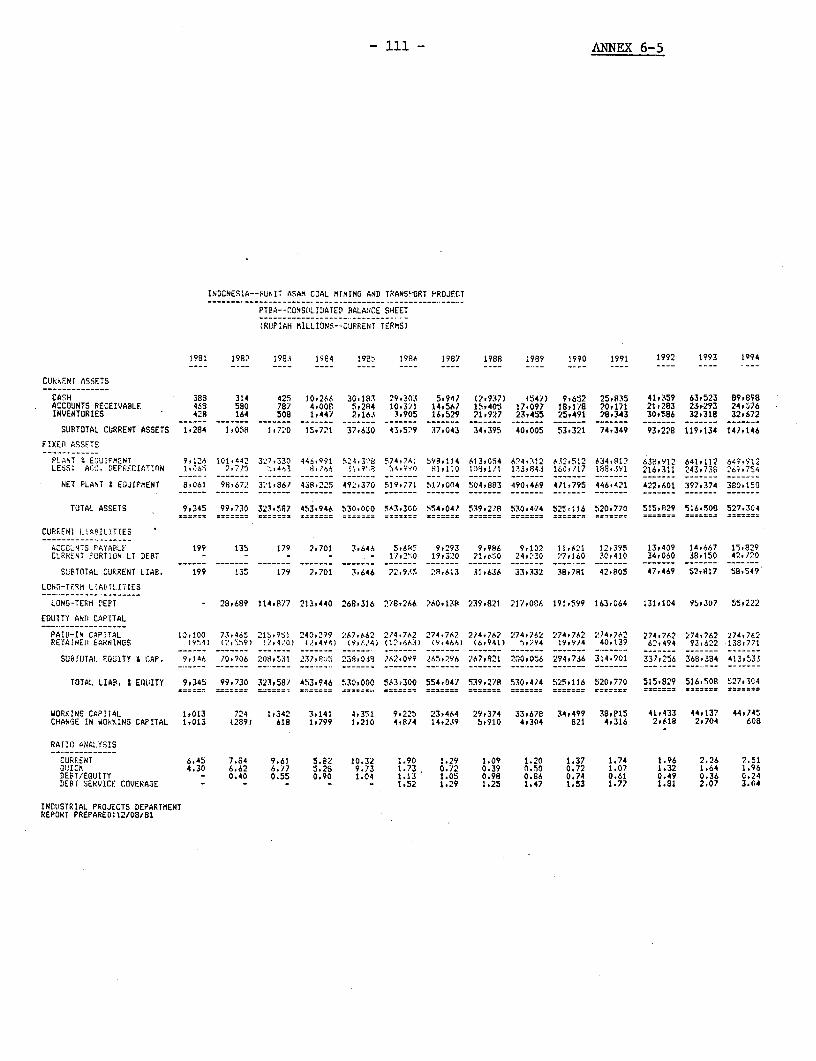

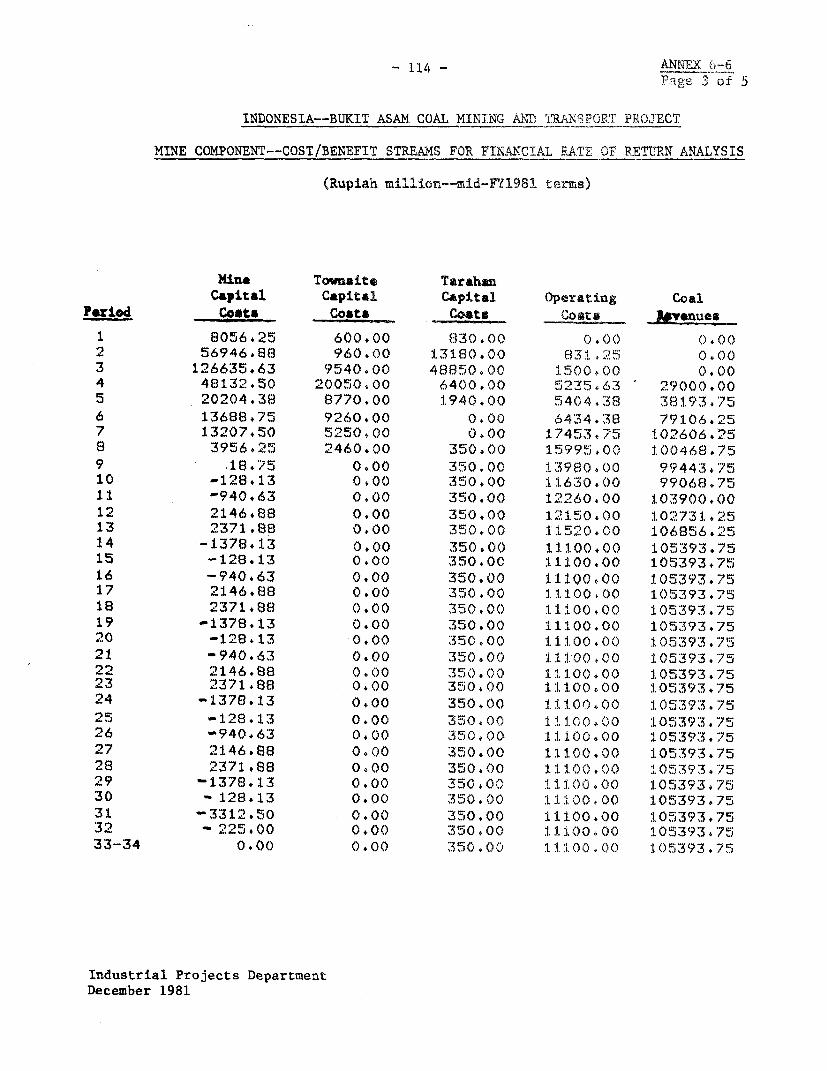

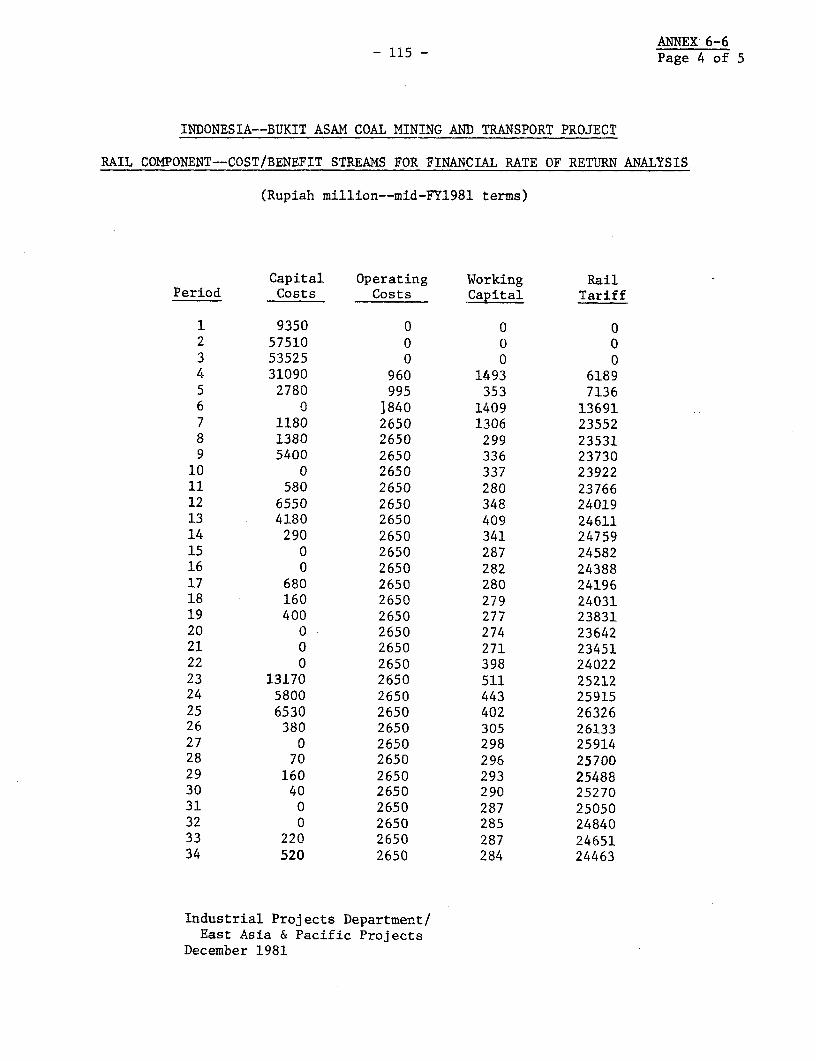

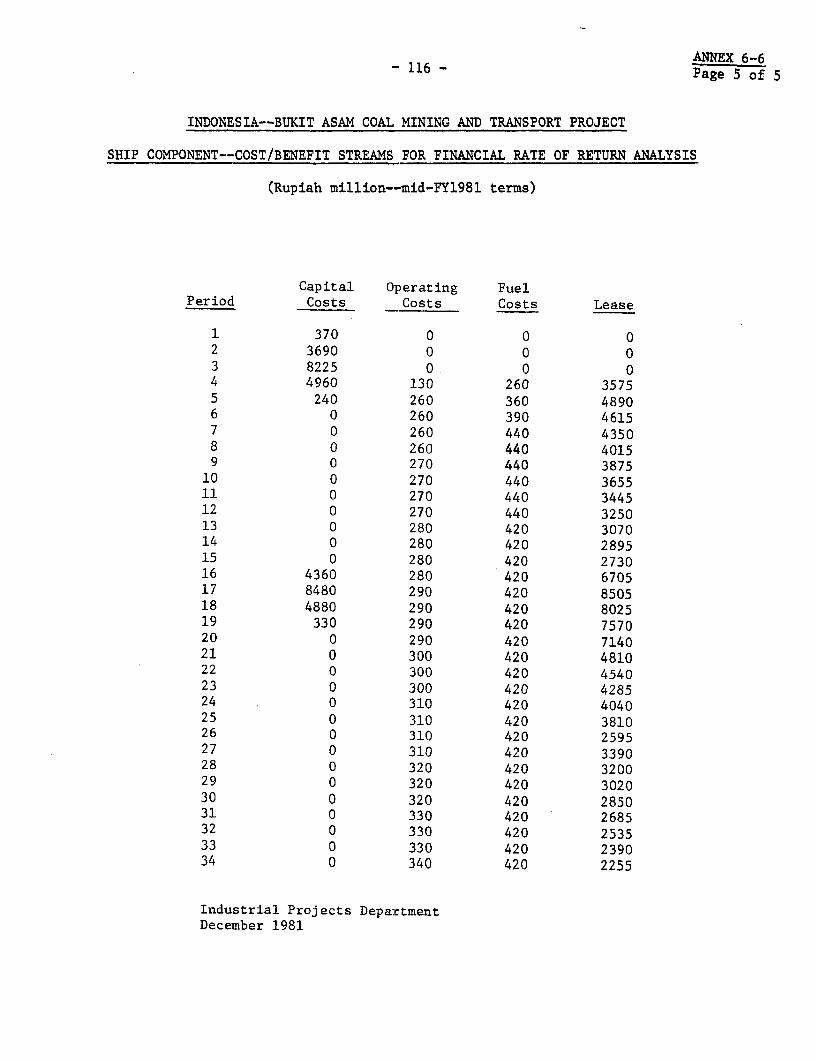

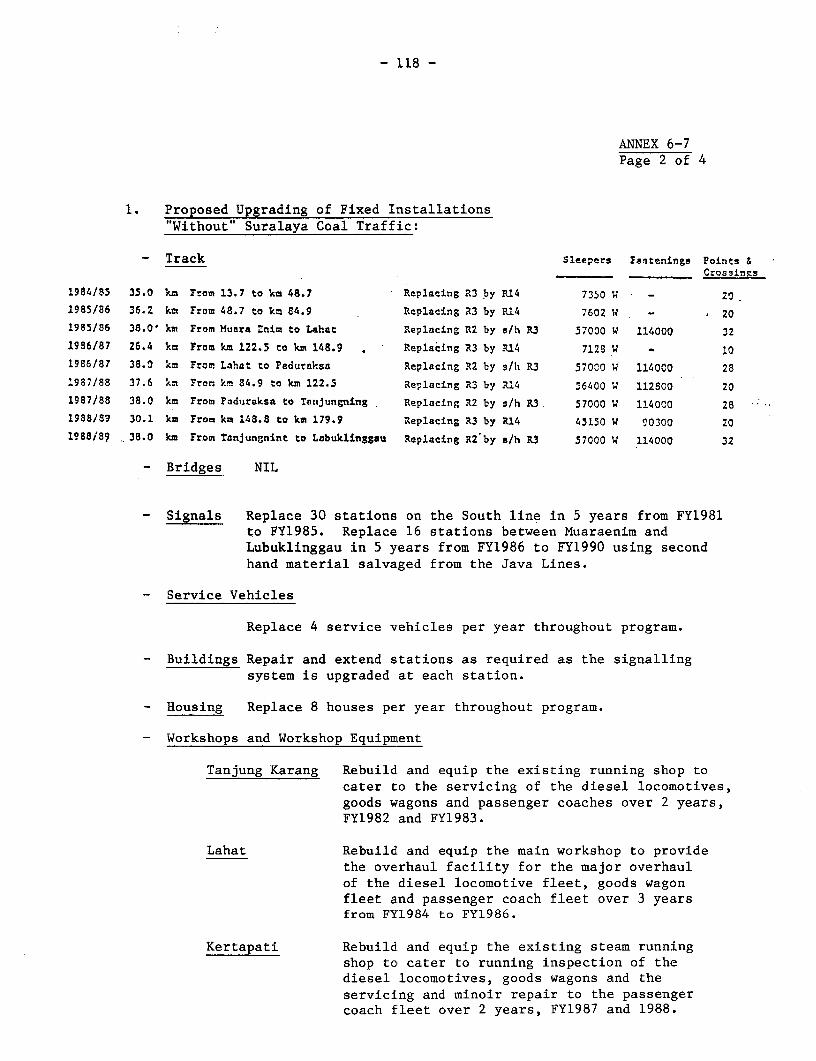

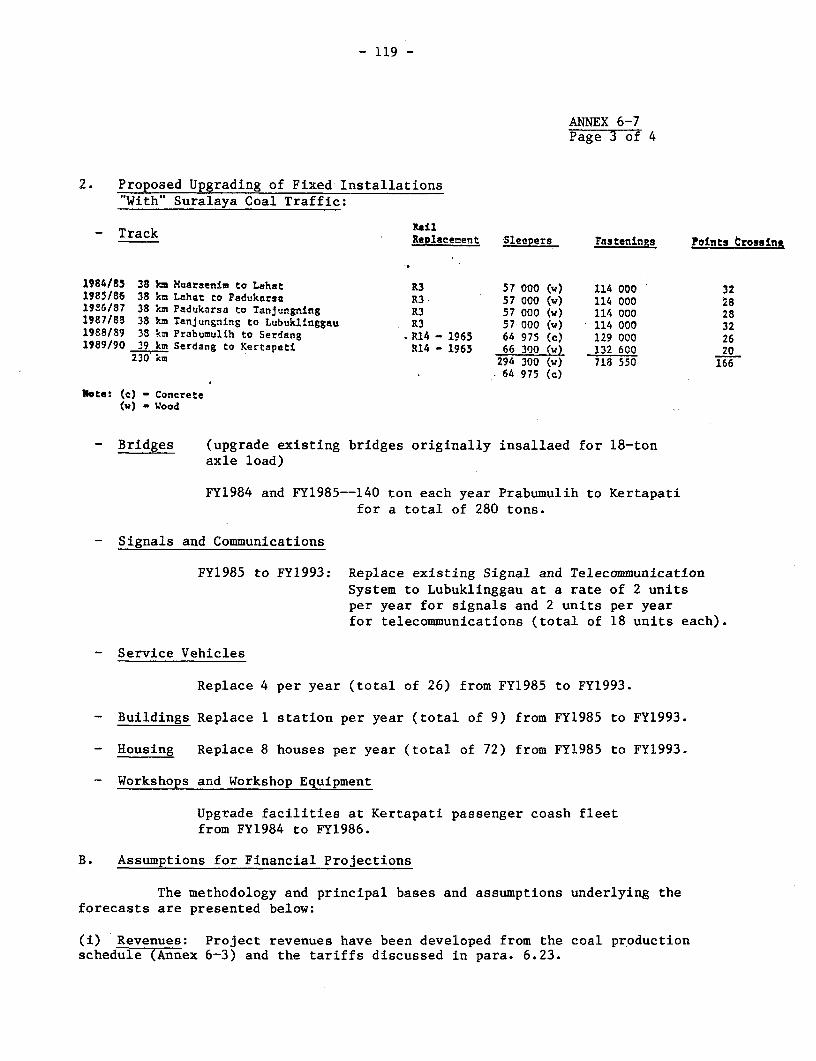

6-1 PTBA--Assumptions for Financial Projections6-2 PTBA--Coal Production, Sales and Revenues, FY1981-946-3 PTBA-Consolidated Income Statement, FY1981-946-4 PTBA--Consolidated Sources and Application of Funds, 1981-946-5 PTBA--Consolidated Balance Sheet, FY 1981-946-6 Financial Rate of Return -- Assumptions and Calculation6-7 Railway Component: Assumptions for Financial and Economic

Rates of Return7 Economic Rate of Return--Assumptions and Calculation

MAP

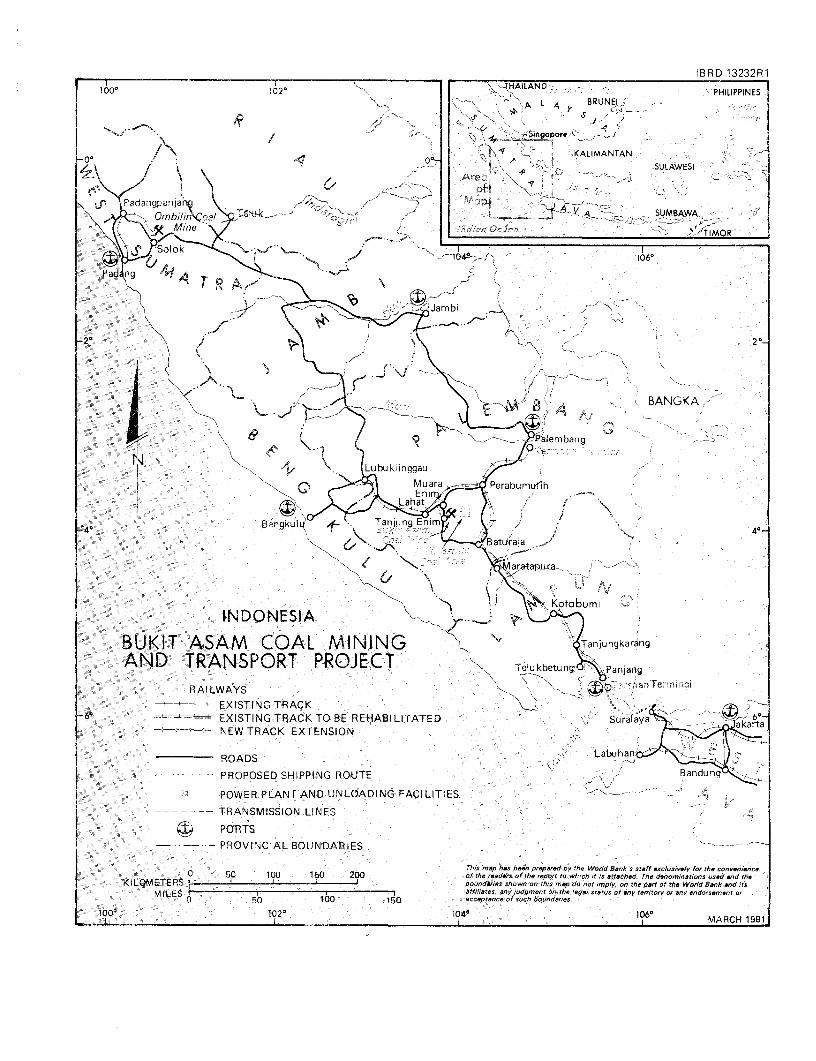

IBRD No. 13232R-1 - Indonesia and Project Location

- iv -

SELECTED DOCUMENTS AND DATA AVAILABLE IN THE PROJECT FILE

Reference Title, Date and Authors

A. General 1. Milestone 3 - Selected Systems ReportOctober 1979 by MCS Consultants

2. Milestone 3 - Selected Systems Report-AddendumNovember 1979 by MCS Consultants

3. Milestone 3 - Selected Systems Report-AddendumNo. 2 Cost Review ExerciseTerminal and Shipping System for5 mtpy Training, January 1980 byMCS Consultants

4. Milestone 6 - Final Report for Phase IJuly-August 1980 by MCSConsultants

B. Mine 1. Re-evaluation of Cost Estimation of AB-StudyJanuary 1980 by Rheinbraun Consulting

2. Milestone 6 - Coal Mine SystemJuly 1980 by RheinbraunConsulting

3. Milestone 5 Report - Accounting SystemsMay 1980 by PT PamintoriConsultants

C. Townsite 1. Planning of Workers Settlement for Bukit AsamCoal Mining Plant by the Center of PlanningStudies, Institute of Technology, Bandung,Indonesia

D. Terminals 1. Tarahan Terminal Prequalification ReportJune 1980 by MCS Cconsultants

2. Tarahan Terminal Tender Documentsby MCS Consultants

E. Railway 1. Selective Railway Operating Statistics for ESS 1973-80prepared by PJKA 1981

2. INDONESIA: Bukit Asam Coal Project - Selection ofTransport Route, April 23, 1981, AEPTR

3. INDONESIA: Bukit Asam Coal Project - Selection ofAxle Load, AEPTR

v

Reference Title, Date and Authors

F. Shipping 1. Marine Transportation Alternatives -Preliminary June 20, 1979, by MarineConsultant and Designers

2. Transportation Study of 4 mtpy SeaTransportation and Suralaya Terminal,November 1979 by MCS Consultants

3. Study of Five Marine TransportationAlternatives Selected from June 1979.Milestone 3 Report, September 7, 1979,by Marine Consultants and Designers

4. Survey of Bulk Carriers for use asSubstitutes for Specialized Self-Unloader,January 8, 1980, by Marine Consultants andDesigners

5. Survey of Bulk Carriers to Carry 40,000 CDWTof Coal for Use as Substitutes for SpecializedSelf-Unloader, Undated, by Marine Consultantsand Designers

6. Bukit Asam Coal Transport Study1976 by E. G. Frankel

7. Appraisal of PT Bahtera AdhigunaDecember 19, 1980 by PT PANN

8. Indonesia: Bukit Asam Project--Selectionof Transport Route, Office Memoranda

G. International Coal Market

1. Coal Resources, World Energy Conference (1977)

2. Steam Coal to the Year 2000, International Energy Agency (1978)

3. Coal--Bridge to the Future, World Coal Study (1980)

4. The Growth of Steam Coal Trade 1980-90, H.P. Drewry (1980)

5. 1981 Coking Coal Manual (Including Thermal Coal and Anthracite),Tex (1981)

6. An Analysis of Current and Projected Coal Import Requirementsof Major Prospective Consuming Countries for Australiam Steamingand Coking Coal (Draft Report, 1981)

- vi -

Reference Title, Date and Authors

7. Interim Report of the Interagency Coal Export Task Force, USDepartment of Energy (January, 1981)

8. International Coal Trade, The Markets, The Prospects, Coal Weekand Coal Week International (1981)

9. Coal Export Strategy Study, OECD (1979)

10. The Outlook for Coal ... Promises, Promises, The Energy Bureau (1980)

11. World Steam Coal Service, Z:Lnder Neris (1981)

12. Symposium on World Coal Prospects, United Nations (1979)

H. Contracts (Proposals and/or Agreements)

1. Mine: BAMCO Project Management ContractBechtel Teclnical Assistance Service Contract

2. Townsite: PT Encona Project Management Contract

3. Railway: CPCS Project Management/OperationalAssistance Contract

4. Tarahan Terminal: MCS Owner's Engineer Contract

5. Ship: MCD Engineering Contract

6. Project Monitoring: MCS Monitoring Group Contract

I. Detailed Cost/Benefit Streams for the Rate of Return Calculation

I. INTRODUCTION

1.01 The Government of Indonesia has requested a Bank loan of US$185million equivalent to finance a portion of the foreign exchange component fora coal mining development and transport project. The proposed Project wouldproduce about 3.0 million tons of coal per year from the Bukit Asam mine atTanjung Enim in South Sumatra of which 2.4 million tons per year (tpy) would betransported by railway and sea to the Suralaya electric power station on WestJava, 1/ 0.4 million tpy supplied to a mine mouth power plant and the remaining0.2 million tpy used by local cement plants and other domestic users. TheProject would be executed by three Government-owned companies: P. T. (Persero)Tambang Batubara Bukit Asam (PTBA--a Government-owned coal mining company),Perusahaan Jawatan Kereta Api (PJKA--the State Railway) and P. T. (Persero)Pengembangan Armada Niaga Nasional (PT PANN--the national shipping developmentcorporation). In addition, Bank financing is made available under the Projectto initiate and fund the first tranche for a US$45 million expanded coalexploration program in South Sumatra and Kalimantan. The Project forms part ofIndonesia-s national development strategy to diversify the country's largelymono-energy economy by increasing the use of coal and other oil substitutes inthe energy sector. The mining/transport Project was prepared under a Bank-financed Engineering loan (Loan S-9 IND--US$10.0 million, signed on May 19,1978).

1.02 The mine and railway components of the Project were appraised inOctober 1980 by Messrs. L. H. Cash (Chief), B. Stenberg, and E. Rodriguezof IPD; Messrs. E. Ohlund and L. Seigel of AEPTR; and Mr. C. Wardell (Con-sultant). The shipping component was appraised by Mr. G. Bain of AEPTR inDecember 1980. A post-appraisal mission consisting of Messrs B. Stenberg(Mission leader), E. Ohlund, E. Rodriguez and J.-C. Crochet and Mrs. J.Wright was carried out in June/July 1981. Loan negotiations were held inWashington in November, 1981.

II. THE PROJECT SECTORS

A. Energy Resources, Consumption and Sector Strategy

2.01 Indonesia is endowed with abundant energy resources and has as yetunderdeveloped natural gas, coal, hydroelectric power and geothermal resources.Prior to independence in 1945, the country relied to a large extent on coaland hydroelectric energy for its commercial energy; subsequently, the avail-ability and exploitation of indigenous oil have led Indonesia to develop apetroleum-based energy sector rather than to exploit other available energyresources. Recently, however, with the greatly increased opportunity cost ofusing indigenous oil, the Government has formulated a strategy of developingalternative energy sources.

1/ Suralaya power generation development is being financed under Ln 1708-IND (the Eighth Power Project, signed June 1, 1979--US$180 million),and Ln 1872-IND (the Ninth Power Project, signed June 13, 1980--US$250million).

- 2-

1. Development Strategy

2.02 The basic policy objectives of the Government in the energy sector,as broadly outlined in Repelita III are: (i) intensification of energyresource development and expansion of processing facilities; (ii) gradualshift from a mono-energy to a poly-energy economy (primarily based on coal andnatural gas); (iii) improved efficiency of conversion and utilization; and(iv) expansion of research programs. While Repelita III recognizes therole of energy pricing and fiscal policy in regulating and directing energyconsumption as well as in stimulating exploration and development of energysources, specific policy measures designed to meet these needs are not con-tained in the Plan. Detailed demand projections and costing of alternativedevelopment strategies are also lacking. The Bank is carrying out an inten-sive dialogue with the Government on these matters on the basis of an energyassessment report dated August 1981.

2. Institutional Framework

2.03 In May 1978, as part of a general reorganization of Government depart-ments, the Ministry of Mines and Energy (MME) was established to coordinateall activities in the energy sector. The Ministry has overall responsibilityfor mining, oil, natural gas and electricity. It controls the state enter-prises responsible for the execution of Government policies in the respectiveenergy sub-sectors: the oil and natural gas entity (PERTAMINA); the coalagency, PNTB; and the public power utility, PLN. To facilitate coordinationof energy planning and policy, the Government also established an Interdepart-mental Technical Committee on Energy Resources and charged it with developingenergy plans and policies; the Chairman and Vice-Chairman of the latterCommittee are the MME's Directors-General of Oil and Gas and of ElectricPower, respectively. The Ministry further formed a Permanent Committee forEnergy Studies to assess energy technologies, deal with day-to-day energyproblems and prepare long-term projections for demand and supply. Recentlya ministerial-level National Energy Board was formed, with the Minister ofMines and Energy as Chairman, to review the proposals of the Technical Commit-tee, to establish the Government's energy policy and to give specific implemen-tation instructions to the ministries concerned.

3. Oil

2.04 Total oil reserves are estimated at about 50 billion barrels,but reserves in the proven category have remained at 10-15 billion barrelssince 1970. Since January 1978, the Government has introduced importantincentives that have spurred exploration by concession holders. As a result,production, currently about 1.6 million barrels per day, is expected toincrease to about 1.8 million per day in five years. On the other hand,domestic consumption of oil--which equalled about 20% of Indonesia's crude oilproduction in 1979--will continue to increase such that the net exportablesurplus, in absolute terms, is not expected to grow and may even decline.This is an important factor behind the Government's decision to adopt a policyof developing other indigenous energy sources such as natural gas, hydro-electricity, geothermal steam and coal for internal consumption.

-3-

4. Natural Gas

2.05 Natural gas reserves are about 34 trillion ft , of which 5 tril-lion ft represent gas associated iith oil production. Current domesticconsumption is about 80 billion ft per year. Pipelines have recently beenlaid to major industries such as steel and fertilizer factories and consumptionis expected to increase at about 15% annually during the next five years.Following agreement with Japan a few years ago, exports of natural gas inliquid form (LNG) have begun. A study of natural gas utilization fundedunder Credit 451-IND 1/ will help determine both the potential usage ofnatural gas in Indonesia and the amount of resources available.

5. Hydro

2.06 The country has a hydroelectric potential of nearly 31,000 MW, ofwhich only about 2% is being used. The Government proposes to develop over1,000 MW of hydroelectric generating capacity in Java by 1987. In particular,the 700 MW Saguling hydropower project was identified in the Java SystemDevelopment Study funded by Credit 399-IND. 2/ This project is now beingimplemented under the Tenth Power Project. Detailed engineering and designfor the next hydropower project in Java, the Cirata project, also constitutesa part of the Tenth Power Project. Development of the Asahan River in NorthSumatra, with a capacity of 600 MW, for use by an aluminum smelter is also inprogress. Rapid development of other hydro resources is constrained by thelack of demand for electricity in islands having large hydroelectric potential(Irian Jaya, Kalimantan, Sulawesi). Investigations of potential sites in thepopulous islands (Java, Sumatra) are being accelerated.

6. Geothermal

2.07 Indonesia has substantial geothermal energy potential and about 900MW of generating capacity have already been proven. The fields are close tothe main population centers in Java and Sulawesi. A 30 MW plant with a futureplanned capacity of 90 MW is being constructed by the state electricitygenerating organization (PLN) at Kamojung in West Java. A further projectsponsored by Pertamina with an initial estimated capacity of 110 MW in GunungSalak, West Java, is being considered by IFC.

7. Coal

2.08 Reserves. Hundreds of coal occurrences are known to exist on theislands of Sumatra, Kalimantan, Sulawesi, Java, Timor and in Irian Jaya.Substantial exploration work, however, has only been undertaken in Sumatrawhere about 80% of all of Indonesia's geological coal resources are estimated

1/ Fourth Technical Assistance Project, Credit 451-IND, signed January 2,1974--US$5.0 million.

2/ West Java Thermal Power Project (Power III), approved June 1973--US$46 million.

- 4 -

to be. Due to different criteria used in estimates made by different sourcesand the scarcity of reliable exploraltion data, resource figures vary consider-ably and none of these can be considered to be reliable. The official WEC 1/figure is 3,723 million tce 2/ (equa:L to about 6,515 million tons, assuming aheating value of 4,000 kcal/Tg) whilea the Ministry of Mines and Energy quotesa figure of 17,200 million tce, the majority being lignitic coal. Provenreserves can be estimated at some 225 million tons in Sumatra (Ombilin,Bukit Asam and North West Bangko). All other coal-bearing areas in Indonesiamust be classified as terra incognita with respect to reliable reserve figures.Nevertheless judged by its geologicaL formations, the country's coal resourcepotential is substantial.

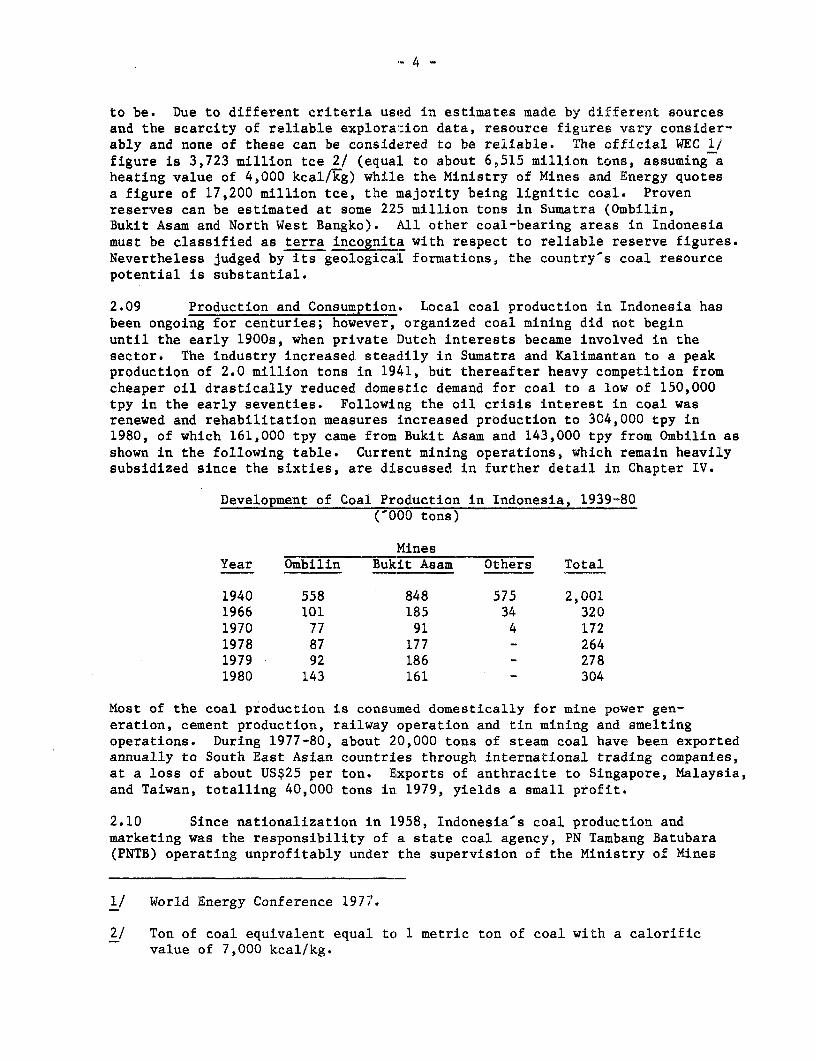

2.09 Production and Consumption. Local coal production in Indonesia hasbeen ongoing for centuries; however, organized coal mining did not beginuntil the early 1900s, when private Dutch interests became involved in thesector. The industry increased steadlily in Sumatra and Kalimantan to a peakproduction of 2.0 million tons in 1941, but thereafter heavy competition fromcheaper oil drastically reduced domestic demand for coal to a low of 150,000tpy in the early seventies. Following the oil crisis interest in coal wasrenewed and rehabilitation measures increased production to 304,000 tpy in1980, of which 161,000 tpy came from Bukit Asam and 143,000 tpy from Ombilin asshown in the following table. Current mining operations, which remain heavilysubsidized since the sixties, are discussed in further detail in Chapter IV.

Development of Coal Production in Indonesia, 1939-80('000 tons)

MinesYear Ombilin Bukit Asam Others Total

1940 558 848 575 2,0011966 101 185 34 3201970 77 91 4 1721978 87 177 - 2641979 92 186 - 2781980 143 161 - 304

Most of the coal production is consumed domestically for mine power gen-eration, cement production, railway operation and tin mining and smeltingoperations. During 1977-80, about 20,000 tons of steam coal have been exportedannually to South East Asian countries through international trading companies,at a loss of about US$25 per ton. Exports of anthracite to Singapore, Malaysia,and Taiwan, totalling 40,000 tons in 1979, yields a small profit.

2.10 Since nationalization in 1958, Indonesia's coal production andmarketing was the responsibility of a state coal agency, PN Tambang Batubara(PNTB) operating unprofitably under the supervision of the Ministry of Mines

1/ World Energy Conference 1977.

2| Ton of coal equivalent equal to 1 metric ton of coal with a calorificvalue of 7,000 kcal/kg.

- 5 -

and Energy (Annex 3-1, paras. 1-15). A new company, PT Tambang Batubara BukitAsam (PTBA), was created in December 1980, to implement the proposed Projectand carry out exploration in the Bukit Asam area, leaving PNTB to operate theOmbilin mine and pursue exploration and pre-investment work in other areas;To fulfill these mandates, the organization, staff and financial resources ofboth PTBA and PNTB will have to be substantially strengthened.

2.11 Development Plans. In 1976, a Presidential Instruction that aimedat the maximum possible utilization of coal for future domestic electric powergeneration and industrial usage was issued (paras. 2.01-2.02). Repelita III(i.e., the Third Five-Year Plan) gives first priority to the development of amore balanced domestic energy production, encouraging the development of coalfor internal consumption wherever technically and economically feasible.To date, efforts to do so have resulted in (i) the proposed Bukit Asam mineexpansion/Suralaya power plant project; (ii) coal reserve exploration in theOmbilin basin, and ini:iation of a US$100 million rehabilitation program forthe Ombilin mines to increase output to 500,000 tpy primarily for regionalcement and power plant consumption, and (iii) an invitation to foreign companiesto explore and exploit the coal deposits in Kalimantan for export and domesticconsumption. PNTB has been negotiating production sharing agreements with ARGO,UTAH, Rio Tinto, AGIP and CONSOL to undertake coal exploration and eventualdevelopment in Kalimantan, four of these were signed in mid-1981. Thesecontracts allow the foreign partners 5 years to undertake exploration andfeasibility studies prior to an investment decision followed by a minimum of3 years to bring a mine in production. Thus, under realistic assumptionscoal from Kalimantan cannot be expected to be available in significantquantities before 1990. While the production sharing contracts are designedfor export, PNTB has reserved its right to buy all output at market prices.

2.12 As domestic demand for coal is estimated to reach about 10 milliontpy by 1990, it is now urgent to accelerate coal exploration and pre-investmentwork for a number of well-known promising areas in Sumatra. These areas hadbeen explored during the 1974-78 period by Shell Mijnbouw, a Dutch subsidiaryof Shell, under a production sharing agreement with PNTB. After spending aboutUS$50 million and establishing about 100 million tons of measured reserves and500 million tons of indicated reserves, Shell returned the concession. It hadbecome apparent that coal quality and mining/transport cost to Japan could notcompete with Australian and South African coal. The Government unsuccessfullyrequested Shell to consider mining coal for domestic consumption.

2.13 A Bank mission visited Indonesia in June 1981 to explore with theGovernment its plans to intensify coal exploration and preinvestment work andthe institution building which would be required in order to execute an accele-rated coal exploration production program with emphasis on the former Shellconcession in South Sumatra and promising areas in Kalimantan not covered byproduction sharing agreements with private partners. As a result of thesediscussions, the scope of work for a comprehensive Coal Exploration Programwas identified, which the Bank appraised in late October 1981. Thisprogram will require US$45 million for detailed exploration and feasibilitystudy work in South Sumatra and preliminary exploration in Kalimantan. Detailsare given in paras. 3.59-3.61.

B. The Power Sector

1. PLN and the Role of the Sector in the Economy

2.14 Institutionally, the power sector consists of the DirectorateGeneral of Electric Power, in the Ministry of Mines and Energy, and PLN,

which is statutorily responsible for all public sector power generation,transmission and distribution and some municipal franchises. PLN came intobeing in 1961 when three Dutch-owned electricity utility companies werenationalized, but commenced effective operations only in 1972, when its newcharter gave it legal status as an autonomous entity with exclusive responsi-bility for electricity supply in the country and when adequate foreignfinancing became available for its expansion programs. 1/ Through 1976,captive power plants--largely linked to industrial enterprises--grew rapidly,but since then PLN has begun to fulfill its role as the main electricitysupplier. PLN's decision to reduce its excessive connection charges has beena major factor in this development. In FY1979, PLN's KWh (kilowatt hour)sales registered a 21.6% increase, the most significant annual increase sofar, and PLN expects to sustain an average annual growth rate of about 20%through FY1986. Hence the share of captive generation, which is presentlyabout 40% in the total market, is expected to decline to about 25% by FY1986.

2.15 Despite PLN's progress since 1976, the per capita consumption ofelectricity in Indonesia as a whole is still extremely low at about 76 KWhin FY1981, compared to other Asian countries. Indonesia-s population has lowaccess to electricity due to a lack of distribution systems and generatingfacilities. Only about 6% of households are connected in the country andthis figure varies from 9.6% in Java, 5.0% in Kalimantan, 4.3% in Sumatra,4.2% in Sulawesi; 4.6% in Irian Jaya, to 2-3% in the other islands.

2. PLN's Development Plan, including Suralaya Power Generation

2.16 General. PLN has prepared a development plan for power in Indonesiathat envisages an increase in installed generating capacity from about2,000 MW in FY1979 to over 7,300 MW in FY1987. Consistent with the overallGovernment policy of expansion and diversification, the objectives of PLN'sdevelopment plan are to: (i) optimize energy resources utilization bysubstituting use of oil by coal, hydro and geothermal resources for powergeneration, and by reducing the use of fuel-inefficient installations; (ii)realize economies of scale through larger-sized installations; (iii) achieveoperational economy by coordinating the utilization of plants through inter-connected operations; and (iv) provide acceptable standards on reliability ofsupply. PLN-s estimated investment for generation, transmission and distri-bution to meet the development plan from FY1980 to FY1989 is US$11.0 billionequivalent, in end-1979 prices, with a foreign exchange component of US$7.0billion equivalent. The expenditure is planned to be phased over a nine-yearperiod, increasing from US$0.6 billion in FY1980 to an average of US$1.5billion in FY1987 and thereafter. The Government has made appropriatebudgetary provisions in Repelita III to cover the period up to FY1984.

2.17 The investment program covers the country according to two geogra-phically divided plans: one for the island of Java and another for territoriesoutside Java. Except for Sulawesi and Bali, PLN's development plan for theterritories outside Java is still being formulated and Java continues to be

1/ The Association and the Bank have made ten credits and loans for powergeneration and transmission to Indonesia since 1968, amounting toUS$1,389 million in total.

- 7 -

the focus of power sector development in Indonesia. In FY1979, Java, with 63%of Indonesia's population (85 million out of 135 million), accounted for 80%of PLN's electricity sales. PLN plans to increase installed generatingcapacity in Java from 1,547 MW in FY1979 to 4,609 MW by FY1987, an annualgrowth rate of 14.6%, while generating capacity in all other territories isplanned to increase from 622 MW to 2,740 MW over the same period (19.4%annually).

2.18 Suralaya Power Generation. The Suralaya power generation project,at the western tip of Java, plays a key role in PLN's overall development planfor Java. The Suralaya power plant is planned to have an ultimate installedgenerating capacity of 3,100 MW, consisting of 4 x 400 MW and 3 x 500 MWunits. In line with Government policy, the Suralaya power plant will usecoal. The first stage of development consists of the installation of: (i)2 x 400 MW dual-fired (coal-oil) thermal generating sets (Suralaya I and II);(ii) facilities for coal reception, handling and storage, ash disposal,cooling seawater intake and discharge facilities, and fresh water supply;and (iii) associated extra high voltage (EHV) transmission works of 500 KVcapacity over 725 circuit-kms. This stage is being implemented in two phases,one for each unit, which are covered by Bank Loans 1708-IND and 1872-IND(para. 1.01), respectively, and co-financed with ADB and export financingsources. The subsequent stages would extend the EHV network to Surabaya inEast Java, and eventually increase capacity to 3,100 MW.

2.19 In parallel, the Government is developing the Bukit Asam coal mineunder the proposed Project in order to supply 2.4 million tons of coal annuallyto Suralaya I and II, now scheduled to come on stream in October 1984 andJuly 1985, respectively. It later plans to expand coal production levels inSouth Sumatra and Kalimantan to supply about 12.0 million tons of coal annuallywhen the Suralaya power plant reaches its ultimate capacity of 3,100 MW. Thisobjective is reflected in the Government's effort to initiate pre-investmentwork for a second or third coal mine in South Sumatra (see para. 2.13),and to provide for the appropriate basic infrastructure under the Project.

C. The Transport Sector

1. General

2.20 Road transport accounts for the majority of all passenger andfreight (except oil) movements in Indonesia; Java, which comprises only 7%of Indonesia's land area, accounts for 35% of all roads. However, othermodes do compete with and/or substitute for road transport in many places,including railways, river traffic, aviation and even pipelines. Inter-islandshipping is important given Indonesia's archipelago nature. Between 1972 and1978, passenger and freight traffic on scheduled airlines increased by nearly20% per year. Railways and shipping are becoming carriers of bulk commoditiesas Indonesia is expanding plantation crops (such as palm oil), building newindustries (such as fertilizer and cement), and planning expansion of miningactivities, particularly coal. Thus, transport modes are becoming morespecialized.

-8-

2. Railways

2.21 Railways are mainly confirLed to two islands: about 4,700 km oftrack on Java and 2,000 km on Sumatra. The railways suffered from the declinein exports in the 1950s and 1960s and were allowed to deteriorate. Limitedrehabilitation took place under the First Five-Year Plan (1969/70-1973/74);and, as a result, freight traffic increased to over 1,100 million ton-kilometers(tkm) in 1974. It declined again to a low of about 700 million tkm in 1976,but has thereafter gone back up to about 1,100 million tkm in 1979. Passengertraffic grew only slightly from 1974-76 but has since grown more rapidlyand reached about 5,600 million passenger-kms in 1979.

2.22 The railways' disappointing performance up to 1976 reflects a numberof factors, including delays in rehabilitation of its assets and in improvingits operations, excessive numbers of personnel, and weaknesses in the competi-tive position of some services, particularly on Java. The comprehensiveprogram of modernization and rehabilitation that formed the basis of theBank's Railway Project 1/ was not carried out in accordance with the originalschedule. Nevertheless, some improvements in operations have been seenrecently. A Development Plan for the 1979-88 period emphasizes the marketingof rail services based on realistic traffic projections, improved maintenanceof permanent way and rolling stock, and operation of larger and more reliabletrains. The railway will continiue to play an important economic role inspecific areas and services, such as long-distance movements of passengersand bulk commodities on Java, and transport of coal in South Sumatra.

3. Maritime

2.23 About two-thirds of the deadweight tonnage of the Indonesian domes-tic shipping fleet has been used in the petroleum trade. Another quartercorresponds to the ships used by companies in the Regular Liner Services(RLS) that carry about half of the inter-island seaborne dry cargo movemeris.Much of the remainder of the fleet is specialized vessels for offshore oiloperations and for carrying commodities such as salt, fertilizer and lumber.Rehabilitation of part of the RLS was carried out under the First ShippingProject. 2/ Provision of additional and some replacement vessels is underwayunder a Second Shipping Project. 3/ Studies leading to preparation of anintegrated maritime project are being financed under the Second Shipping Loanand will include ships, small port improvement, training, and provision ofshipping services to remote areas. In addition, the initial design of shipsfor this proposed Project is also being financed from the Second Shipping Loan.

2.24 The country has about 300 registered ports scattered over thearchipelago, but only a few ports handle the bulk of the traffic. In 1974,

1/ First Railway Project. Loan 1005-IND, signed June 14, 1974--US$48million. For past PJKA project implementation performance see ProjectPerformance Audit Report, March, 1981.

2/ First Shipping Project. Credit 318-IND, signed June 28, 1972--US$8.5 million.

3/ Second Shipping Project. Credit 1250-IND, signed May 20, 1976--US$54.0 million.

- 9 -

only 16 ports each handled more than 0.5 million tons of domestic and foreigntraffic, and eight of these were primarily petroleum or lumber ports.

2.25 The Government has been emphasizing port rehabilitation works andimproved port operations to overcome serious congestion under the FirstFive-Year Plan. Longer-term expansion needs were also studied in a series ofmaster plans and port loans by the Bank Group and other lenders. 1/ Portprojects have also included continued technical assistance and other measuresto improve customs procedures and port management, particularly cargo handling,maintenance and accounting. It is anticipated that further expansion of theTanjung Priok port will be undertaken under Repelita III as a component ofthe maritime project now under preparation (para. 2.23) and provision forengineering this expansion, and for other project preparation activities, isincluded in a forthcoming National Fertilizer Distribution Project.

III. THE PROJECT

A. Project Objectives

3.01 Growth of domestic demand for oil in Indonesia is now outpacingincreases in oil production, and oil exports are showing a declining trend.Urgent steps must therefore be taken to increase levels of investment in thedevelopment of other energy sources in order to ensure continued and, ifpossible, increased petroleum export earnings. Through the PresidentialInstruction issued in 1976, Indonesia is now committed to an increased use ofcoal as a substitute for oil in order to maximize export earnings from oil.The Presidential Budget Speech in 1977 reinforced this commitment by statingthat coal would be used in thermal power generation wherever possible and eco-nomically justified.

3.02 The Project is a first step in this direction and it will:

(a) raise the current production capacity of the Bukit Asammine of about 150,000 tons of coal per year to about 3 mil-lion tpy, predominantly to feed the first two units of theSuralaya power plant development in West Java; and

(b) initiate an accelerated coal exploration program in Indonesia.The exploration program would delineate additional coalreserves and provide the Government with a series of pre-feasibility and feasibility studies that would facilitateand accelerate development of two to three new mines in SouthSumatra. These mines would provide coal for thermal power gene-ration, first, for the next phase of the Suralaya power plantdevelopment scheduled for commissioning in 1988/89, and, second,for the Tuban power plant development in East Java scheduled for1990/91.

1/ Tanjung Priok Port Project. Loan 1337-IND, US$32.0 million.

-10 -

B. Project Formulation

1. The Suralaya Power Scheme

3.03 The Suralaya Power Scheme waLs identified by the comprehensiveJava System Development Study, financed through Credit 399-IND 1/ and carriedout by Preece, Carden and Rider (UK) in 1975-76. It will ultimately havean installed electrical generating capacity of 3,100 MW. The scheme hasbeen subdivided to reduce annual financing commitments; Stage I and II,for a combined 800 MW, are now being implemented under Loans 1708-IND and1872-IND, respectively. 2/ In order to enhance phasing with coal development,the thermal units are designed to burn oil and/or coal (dual-fired).

3.04 The selection of the Suralaya site in West Java was thoroughlyreviewed by the Japanese in feasibility studies prepared in 1977. MONENCOof Canada in another feasibility study for which Loan 1127-IND 3/ providedfinancing, confirmed that the Suralaya site is the most feasible location,both technically and economically. Among the major technical constraints forthe plant to be at or near the Bukit Asam mine site was the fact that sufficientcooling water for the first phase of the Suralaya Power Plant Development,800 MW, was not available, not to mention the ultimate plant with a capacity of3,100 MW. Having the plant located on. the sea-coast of Sumatra, where of coursesufficient cooling water is available, would not only require rail transport ofthe coal but also a transmission cable across the Sunda Strait to Java, inaddition to the 500 KV lines required to connect it with Jakarta and CentralJava distribution grids. A submerged cable across the Sunda Strait, in lieu ofsea transport of coal across the Strait was found to be a much more expensiveproposition, apart from the question of the reliability of the submarine cableand its effect on the total system operation, considering the possible seismicactivities in the area.

2. Bukit Asam Coal Deposit

3.05 In 1976, the Bank was requested by the Indonesian Government toassist with the preparation of a project to mine and transport coal froman expanded Bukit Asam mine in South Sumatra to the Suralaya Power Develop-ment. Initially, about 2.5 million tons of coal annually were envisaged,thus substituting for about 9 million barrels of oil per year. The Bukit Asamcoal field was at that time, and still is, the best-explored coal deposit inIndonesia with reserves of coal, suitable for power generation and otherindustrial usage, in excess of 100 million tons--more than sufficient toprovide coal to the first stages of the Suralaya Scheme for at least 30 years.The choice by the Indonesian Government to study a possible expansion ofthe Bukit Asam mine to meet increasing domestic coal demands was appropriate,

1/ Third Power Project. Credit 399-IND, signed June 22, 1973--US$46 million.

2/ Eighth Power Project. Ln 1708-IND, signed June 1, 1979--U$180 million, and Ninth Power Project, signed June 13, 1980--US$250 million.

3/ Fourth Power Project. Loan 1127-IND, signed June 17, 1975--US$41million.

11 -

particularly in light of the potential for additional coal development in thearea, as indicated by Shell Mijnbouw's of the Netherlands substantial explora-tion program in South Sumatra in the mid-l970s.

3. Project Preparation - Bukit Asam Engineering Loan

3.06 In 1976-77, the Government of Indonesia undertook a number ofstudies to define the coal reserves more precisely and to select the idealmine and transport configuration for the Bukit Asam mine expansion. How-ever, major issues relating to the determination of coal reserves and coalquality variations, the selection of mining system, the preparation of amining plan and the selection of an optimal transport configuration were yetunresolved. Consequently, it was agreed with the Indonesian Government, thatadditional work was required to resolve these issues and to prepare compre-hensive optimization and feasibility studies. This work was financed underEngineering Loan S-9 IND (signed May 9, 1978, US$10.0 million) and the finalfeasibility report, the Milestone 6 Report, was submitted in July-August 1980.

3.07 Under that Engineering Loan, consulting contracts were signed withMCS Consultants (a joint venture of Montreal Engineering Company, Ltd.;Canadian Pacific Consulting Services, Ltd.; and Swan Wooster EngineeringCompany, Ltd. of Canada) for overall Project analysis and for detailedstudies on the railway, terminal and townsite components. Engineeringstudies and cost estimates on the mine system were subcontracted by MCS toRheinbraun Consulting GmbH (FR Germany) and marine systems studies and designwere subcontracted to Marine Consultants and Designers (MCD) of USA/Canada.About 10% of civil engineering work and the review of the accounting set-up were subcontracted locally to IEC (Indonesian Engineering Consortium)and PT Pamintori, respectively. Bechtel (US) was technical advisor forKP5BA, the Indonesian Project Management Organization. After initial delaysin signing contracts, KP5BA implemented this phase of the Project on time,effectively coordinating the work with the various Government entitiesinvolved (PNTB, the State Coal Agency; PJKA, the State Railway; and PANN,the national fleet development corporation).

3.08 In addition to defining the technical, institutional and cost aspectsof the Project components, the Project analysis included (i) a general assess-ment of existing training facilities and the personnel situation in Indonesia,particularly in South Sumatra, (ii) definition of general training and personnelrequirements and, consequently, (iii) recommendation of training programs (paras.3.24-3.28, 3.41-3.43, 3.49-3.50, 3.55, 3.78, 3.80 and 3.84) that are consideredadequate by the Government and the Bank.

3.09 As Project preparation progressed, the Government decided with Bankstaff agreement that execution of the various project subsystems, and theirownership and operation, would be the responsibility of the respective Govern-ment entities (PTBA, PJKA, PANN/Bahtera), instead of creating a super agencyfor the purpose. This approach is justified as the Project is seen as a firststage of a series of coal development and related infrastructure projects andthus, strengthening of functional entities is of vital long-term importance.However, when adopting such a decentralized framework, overall coordination ofthe different Project components becomes critical and is addressed in detailbelow (paras. 3.81-3.82).

- 12 -

4. Major Design Alternatives

3.10 Mining System. The major task during mine engineering was to selectthe optimal open pit mining system taking into consideration the specificconditions at Bukit Asam. Overburden material/coal characteristics, incombination with prevailing difficult climatic condition, had major impacts onthe system selection. Four alternatives--combining shovels, rigid frame aswell as articulated trucks, scrapers, bucket wheel excavators (BWE), conveyorbelts and waste material spreaders in different configurations--were evaluatedtechnically and economically. The Government selected a BWE mining systemwith the Bank approving the choice. The BWE system was considered to be lessvulnerable to the climatic conditions, had a levelized 1/ operating cost/tonof coal that was about 9% less than the second best alternative, and equalinitial capital costs. Other factors in favor of the BWE system are: (i)some of the current personnel in the mine are familiar with BWE operations(the mine was operated 1957-75 with the BWE mining method), and (ii) the BWEmining system will not require the heavy periodical reinvestment (every 5-6years), that is characteristic of truck and shovel systems.

3.11 Railway route selection. In the selection of the appropriatetransport configuration, two alternative route systems were considered:(a) the Eastern route by rail to Kertapati and then by barge from Palembangvia the Musi River and by sea to Suralaya, and (b) the Southern route by railto Panjang and then by ship across the Sunda Strait to Suralaya. In examiningthese alternatives, both the initial 2.5 million tpy and the planned 5.6million tpy capacities were considered. After a thorough study of the capitaland operating cost estimates as well as the risks inherent to each route, thestaff endorsed the Government's decision to proceed with the Southern routefor the Project. In particular, although the economic cost/benefit analysispoints to the Eastern route at a 2.5 million tpy capacity, the Southern routeis favored when larger coal volumes are considered, as are projected to resultfrom the coal exploration program and subsequent mine developments in SouthSumatra by 1988. In either case the quantifiable advantage/disadvantage arewithin the margin of error of the underlying cost estimates. As the degree ofconfidence associated with cost estimates for the Eastern route is considerablyless (within 15-25%) than that for the Southern route (within 10-15%), due tothe substantial difference in the amount of engineering undertaken on the tworoutes, the desirability of the Southern route is most likely underestimated.This analysis is documented in the Project file.

3.12 Apart from pure cost considerations, the arguments for the Southernroute are reinforced by uncertainties about navigation in the Musi riverand the length of the Eastern sea route. It has been assumed that rivernavigation is feasible without complication or further cost, but this un-proven assumption would have to be verified. Also, with a 560 km sea journeyfor barges, there is a greater risk of loss of equipment or navigationaldelays on the Eastern route than for the Southern route where the sea routeis only 100 km.

1/ Levelized cost is equal to the present value of the costs divided by thepresent value of the physical benefits and is used for comparison ofalternatives only.

13

3.13 Axle load decisior. Iwo track standard alternatives, one allowing18-ton axle load and the other 13 tons, were examined. The analysis (in theProject File) leads to the choice of the 18-ton axle load alternative, whichdoes require strengthening of bridges but, on the other hand, would reduceinvestments in motive power and rolling stock and operating costs.

C. Project Description

1. Bukit Asam Mine

3.14 The mining component of the Project consists of an expansion of theexisting coal mine at Bukit Asam. Based on the known average heating value of5,200 kcal/kg for Bukit Asam coal, the first phase of the Suralaya power plantdevelopment (Suralaya Units I and II) will require about 2.4 million tpy. Anadditional 400,000 tpy will be required for a new 2 x 65 MW coal-fired powerplant to be built adjacent to the mine. Including the demand of other currentconsumers of Bukit Asam steam coal a total mine output of 3.0 million tpy isenvisaged. A minor tonnage (115,000 tons) of anthracite will also be mined inthe future from the southern part of the deposit. As sufficient small-scalemining equipment exists at Bukit Asam, this operation is not part of theProject.

3.15 Coal reserves amounting to 124 million tons have been proven in thefour A and B seams (technically, the Al, A2, B1 and B2 seams) in the so-calledTABA concession. Additional coal reserves are available in the underlying Cseam but neither the quantity nor the quality is presently classifiable asproven reserves. The mineable reserves in the A and B seams are sufficientto supply Suralaya Units I and II for 30 years. To improve current knowledgeof coal quality in the A and B seams, and to prove the potential reserves inthe C seam, further drilling will be undertaken as part of the Project. Adecision to mine the C seam can be postponed until 1997, when a decision onback-filling of overburden material into the pit must be made.

3.16 The mine will consist of an open pit operation employing a bucketwheel excavator (BWE) mining system. A BWE system is a device for efficientbulk handling; and, when topography and physical overburden and coal character-istics allow its application, as is the case for this mine, the system issuperior to any other mining system in terms of productivity and costs.Annual coal production of 3.0 million tons will require overburden removalduring the first 5 years of Bukit Asam operations of about 17 million bankcubic meters per year. Overburden removal requirements for the remaining 25years of the mine life will average about 9 million bank cubic meters peryear. It is envisaged that five bucket wheel excavators are required, eachcapable of excavating 4 million bank cubic meters of material (coal andoverburden) annually. Both coal and waste are to be transported from themining face by means of belt wagons and an extensive (30 km) belt conveyorsystem to either the coal crushing facilities or the waste dumps. At thewaste dumps, two spreaders with a capacity of 5,000 tph each will dump thewaste according to a carefully worked out waste disposal plan, in order toreduce the risk of dumpslides and to minimize the environmental impact.Additional land outside the existing concession boundary will be required forthe waste dump, and land acquisition is in progress. The coal will be conveyedto stockpiles with a total capacity of 250,000 tons in the vicinity of a trainloading station. The stockpiled coal will be reclaimed, loaded on conveyorbelts and transported to the train loading station.

- 14 -

3.17 Due to the relatively few mining faces and the fact that a majorpart of the belt conveyor system consists of installations that have to befixed in their proper locations from the very start-up of the mine, a detailedmining plan covering the lifetime of the mine had to be worked out. Deviationsfrom such a plan could delay coal release and prevent the mine from supplyingcoal at the required rate. However, the layout of the mine will allow forcertain flexibility since equipment movement between different mining benchesis possible, and adequate stockpiles will enable the mine to cope with antici-pated production disturbances caused by local conditions such as heavy rains.

3.18 Based on statistics covering a 30-year period, the average annualprecipitation in the area is 3,147 mm with an average of 162 days per yearwith rainfall. Even during the dry season, the number of days per month withsome rainfall averages 8. Consequently, a substantial effort has been made bythe consultants when engineering and designing the final pit slopes, thedrainage systems and pump-station capacities in order to prevent the floodingof working areas and slope failures. Slopes in the mine are designed with aslope angle of 17 degrees, which is considered to be a safe slope. Theoverall waste dump slopes are 8 degrees, which is equal to the slope angles ofexisting stable waste dumps with similar material. The possible effect of-seismic activity in the area has also been considered when planning the openpit as well as designing the buildings for support facilities.

3.19 Scheduled working hours are calculated on a 7-day week and 3-shiftday basis, less 11 National Holidays and one shift each Friday (Moslemholiday). The effective operating hours are the scheduled working hours lesstime lost due to scheduled maintenance (1 shift per week), bad weather (heavyrainfall) general maintenance and repair (breakdowns) conveyor shifting/equip-ment maneuvering and an allowance for unexpected standstills in the rathercomplicated BWE-conveyor-spreader systems. Of scheduled working hours, 47%equal to 3,800 hours per year, has been used when calculating equipmentcapacities and required mine output. The effective operating hours areconsidered to be conservative and a certain spare capacity is available.

3.20 In addition to the basic mine layout described above, the miningcomponent includes:

(i) construction of access and service roads, preparation of benches anddrainage ditches, levelling of waste dumps and in-pit cleaning by afleet of track dozers, rubber-tired loaders, road graders, trucksand scrapers;

(ii) provision of cranes, trucks and pick-ups for speedy response toequipment breakdowns and routine preventive maintenance by workshoppersonnel;

(iii) construction of a new workshop with facilities such as a weldingshop, vulcanization shop, mechanical shop, machine shop, electricalshop and equipment service bays;

(iv) construction of a new warehouse, including an outdoor storage area;

(v) construction of an office building for maintenance and minesupervisors, including a training center at the mine (the existing

- 15 -

office will be renovated and administrative and planningpersonnel will be housed there);

(vi) construction of two overhead 30-kV high-tension power lines fromthe boundary of the mining area to a number of substations anddistribution points. From there, a distribution network will bebuilt to supply power to all electrical equipment facilities.Some switchgear and transformers will be mobile and follow theadvance of the mining faces. Total installed drive power will beabout 40 MW; and

(vii) installation of a communications system, radio and telephone,to facilitate proper supervision and maintenance/repair withinthe mining area. A center for centralized control and supervisionof the BWE and conveyor operations will be established.

3.21 French bilateral financing has been arranged for the constructionof a 2 x 65 MW mine mouth power plant (MMP) and a 150-kV transmission line toPalembang, to be engineered and constructed by Sofrelec, a French consultingfirm. Though not part of the Project, this MMP will supply electricity forthe mine as well as be a user of coal, amounting to 400,000 tpy by FY1985,when the MMP is expected to be completed. Until then, PLN is responsible forinterim power supply (IPS) to the mine during the initial period of operation(para. 3.99).

3.22 About 2,950 people, consisting of 2,780 laborers, 35 junior staffand administrative personnel and 35 senior staff, such as engineers andmanagement personnel, will be required to operate the mine by the end of1986 (one year after mine start-up). PTBA currently-employs about 1,250people in Bukit Asam; the balance of 1,700 new employees will be recruited,primarily from South Sumatra. A survey made by MCS (para. 3.08) has indicatedthat there is a large supply of candidates available to fill lower-levelskilled and semi-skilled jobs in the technical areas required for this Project.Because PTBA is an independent entity it is anticipated that it will be ableto recruit graduate engineers and other entities have had no problems inrecruiting and relocating engineers to Sumatra provided satisfactory salaries,housing and other fringe benefits are available. As part of the Project PTBAwill provide competitive salaries and other benefits and should therefore beable to attract and retain required personnel.

3.23 Because of the substantial number of new recruits and the need tointroduce new skills as well as upgrade the skills of existing employees atall levels, the Project includes a significant training component for PTBA.The objectives of the program are two-fold: (i) to improve and strengthenPTBA's management, mine operations, and maintenance activities and (ii) toprovide for efficient overall operations in the future. Although certaintraining facilities and courses are available, no significant training hasbeen undertaken in recent years due to lack of funds and materials. Nation-ally, graduates are few from the formal technical training available atthe Senior High School level where courses in mechanical and electricalengineering are offered, and most of the graduates have received no practicaltraining at all due to lack of facilities. Informal training on the job,although existing, cannot close the gap and meet the skill requirement of theindustry.

-- 16 -

3.24 A three-year training program, starting in 1982, will be undertakenin PTBA by the Project Management Consultants. BAMCO (discussed in detail inpara. 3.841). This will prepare new and current personnel to supervise overallmine operations and to operate and miaintain the bucket wheel system. It isestimated that some 2,000 employees (1,500 new employees and 500 currentemployees) will require some type of training in Indonesia. This local train-ing program will focus on approximately 100 individual skill areas includingboth managerial and technical requirements, and will be accomplished by meansof: (i) specialized training programs consisting of classroom instruction (ina new training center to be constructed at the minesite), student workshop andon-the-job training; (ii) maintenance and operator training by equipment sup-pliers during erection and initial operation; and (iii) other training, interalia, mine safety and blasting technics) in existing Indonesian institutions.

3.25 In the implementation of this Program, BAMCO, under its contract,will develop both classroom and on-the-job training materials, equipmentmanuals, performance standards, course objectives, training schedules, andevaluation criteria, with a view towards enabling Bukit Asam staff to be self-sufficient in operating and maintaining the mine and in providing training toall levels of future mineworkers. The precise content and number of classesto be offered will be further defined once BAMCO has fully assessed thesignificant strengths and weaknesses of the readily available pool of manpowernear Tanjung Enim. This work, which will be included in BAMCO's inceptionreport, is expected to be completed in January 1982, according to the BAMCO con-tract, at which time it will be subaitted to the Bank for review and approval.

3.26 In addition to local training, under the program twelve carefullyselected senior mine personnel will be sent to Germany for intensive trainingat the Rheinbraun Training Center and the Brown Coal Mining School to acquireskills in mining engineering, mine planning, mechanical and electrical engineer-ing, dewatering technics and surveying. The six-month program consists of216 hours of classroom teaching and 672 hours of on-the-job training. Thecurriculum has been reviewed by the Bank and found adequate. The trainedindividuals will be expected to stay with PTBA for a minimum of 5 years aftertraining.

3.27 BAMCO is well qualified to undertake this training program, havingsuccessfully done so in other mining projects elsewhere in developing coun-tries (e.g., India, Turkey). The total cost of the training program is esti-mated to be US$6.6 million (US$4.4 million local and US$2.2 million foreign,including 184 man-months of expatriate staff at an average cost of US$11,700per man-month). A new training center will be established, consisting of 5classrooms, electrical and mechanical shops (in total about 1,750 squaremeters) at a cost of US$972,000 (of which equipment costs are US$261,000).

3.28 Operational assistance during the initial years of mine operationwill be provided by BAMCO through a local counterpart staffing system contract,covering, inter alia, mine planning, mine supervision and maintenance planningand supervision. BAMCO is obligated to provide operational assistance underthe present contracts. A detailed proposal is to be submitted for Bank review12 months before operational acceptance of the mine system and a contracticceptable to the Bank should be eiEfective prior to the mine subsystemacceptance (para. 3.85).

-17 -

2. Muara Tiga Mine

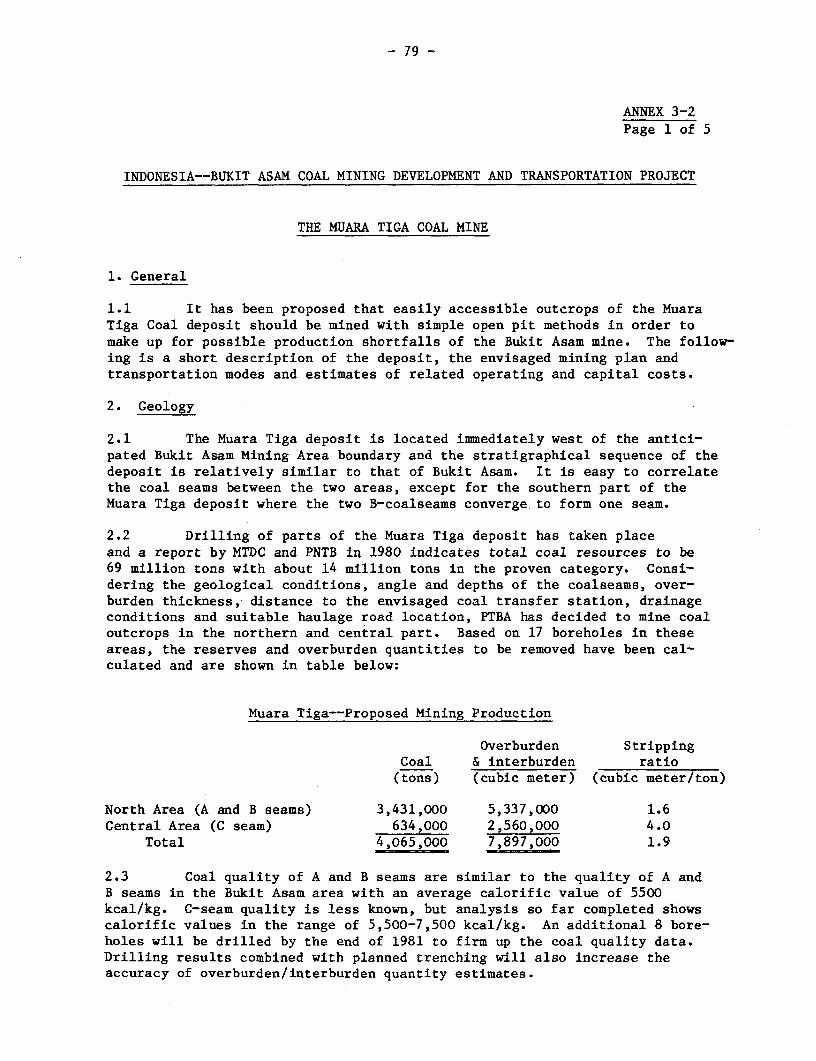

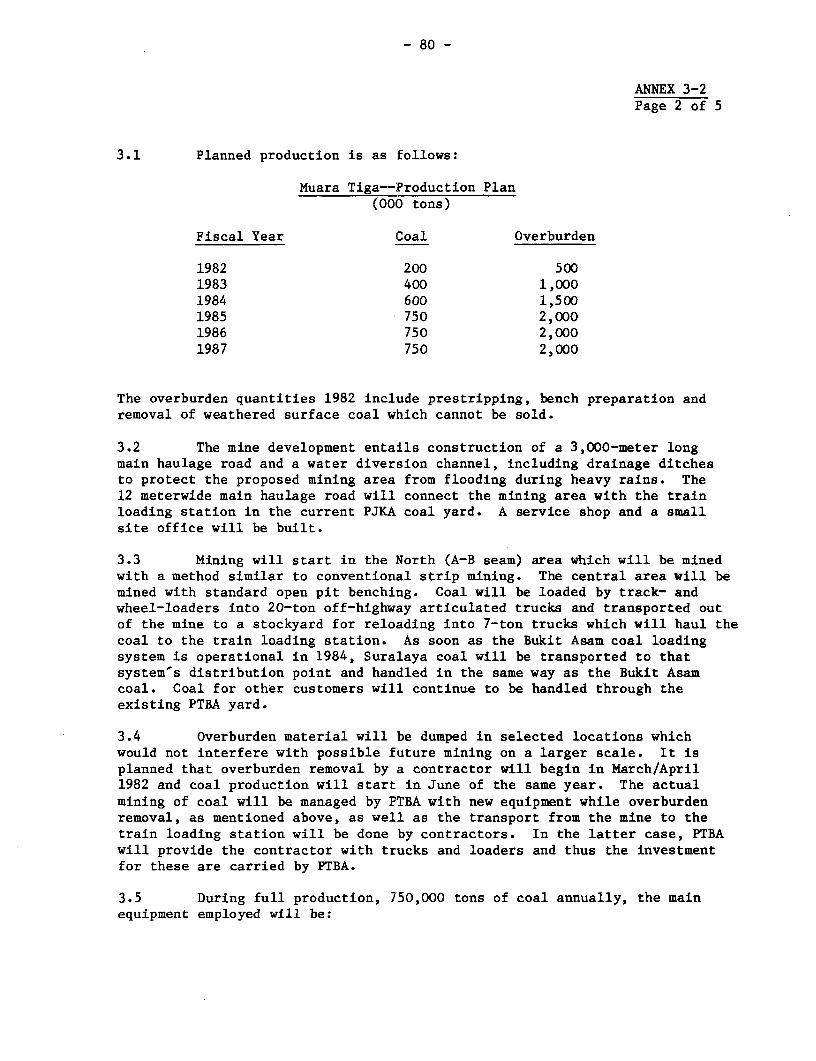

3.29 In addition to the principal mine development described in paras.3.14-3.28 above, the project consists of the development of the small MuaraTiga deposit located immediately west of the proposed Bukit Asam mine. TheMuara Tiga mine will during the period 1982-1987 replace steam coal productionfrom the currently operated Air Laya mine (which will be closed down) as wellas make up for possible production shortfalls from the Bukit Asam mine duringthe initial years of operation (para. 3.96). Annex 3-2 gives a description ofthe deposit, the envisaged mining plan and transportation modes and estimatesof related operating and capital costs.

3.30 The mine development entails construction of a 3,000-meter longmain haulage road and a water diversion channel, including drainage ditchesto protect the proposed mining area from flooding during heavy rains. The12 meterwide main haulage road will connect the mining area with the trainloading station in the current PTBA coal yard. A service shop and a smallsite office will be built.

3.31 Mining will start in the North (A-B seam outcrops) area whichwill be mined with a method similar to conventional strip mining. The centralarea will be mined with standard open pit benching. Coal will be loaded bytrack- and wheel-loaders into 20-ton off-highway articulated trucks and trans-ported out of the mine to a stockyard for reloading into 7-ton trucks whichwill haul the coal to the train loading station. As soon as the Bukit Asamcoal loading system is operational in 1984, Suralaya coal will be transportedto that system's distribution point and handled in the same way as the BukitAsam coal. Coal for other customers will continue to be handled through theexisting PTBA yard. Overburden material will be dumped in selected locationswhich would not interfere with possible future mining on a larger scale.

3. Mining Community

3.32 PTBA today owns about 1,300 houses in the community of Tanjung Enim.About 300 of those are occupied by retired employees. Considering the rela-tively poor condition of existing houses (1,200 out of 1,300 houses arejudged to be inhabitable by 1985), it is, at present, estimated that about2,500 new houses, ranging in size from 40 to 100 square meters, and dormitoriesfor abour 300 people are required over an 8-year period. It is also envisagedthat roads, drainage and electrical distribution system including street lightsfor the new residential areas will be constructed. A water supply systemincluding main lines, a water purification plant and pumping facilities, aswell as new sewerage facilities, will be built. Service facilities, includinga new hospital (200 beds), a new school (1,000 students), and new recreationalfacilities (club house and cinema, sports field, tennis courts), will beconstructed. The existing swimming pool will be renovated. Additional spacewill be reserved for religious facilities and small-scale commercial activities.

3.33 It is recognized, by PTBA as well as by the Bank, that the size andproposed standards of the townsite expansion, as presently envisaged, might beexcessive. Also the impact of the Project on urban areas along the rail routeand at the terminal requires further analysis. As first priority, therefore,PTBA in collaboration with the Indonesian authorities responsible for regionaland urban development and using appropriate consultants will:

- 18 -

(i) estimate the potential growth of associated industrial andcommercial activity in the communities assocated with therail and terminals; and undertake an urban impact study todeal with the potential problem of squatters in Tanjung Enimand along the rail/terminal areas;

(ii) propose appropriate institutional and administrativearrangements for integrating the PTBA financed houses andinfrastructure in the existing towns;

(iii) clarify the responsibilities for payment of capital andrecurrent costs for the mining town and establish chargesfor services rendered, and

(iv) in light of the results of these studies, review the scopeand design of the mining community.

Specifically, it was agreed during negotiations that PTBA will carry out orcommission a detailed urban impact situdy for Tanjung Enim to be carried outbefore the mining community layout is finalized. The implementation schedule(Chart 3-3) on page 37 allows for an additional 6 months to complete thispreparatory work, which is considered adequate.

4. Railway and Communications System

3.34 The railway component of the Project includes the following mainphysical elements:

(a) upgrading of track and bridges on the existing 405 km TanjungEnim-Muara Enim-Perabumulih-Panjang section to allow 18-tonaxle loads (para. 3.14);

(b) construction of a new 800-m rail line from the existing railway linenear Tanjung Enim to the mine site train loading station and a new6.5-km rail line from the existing line at Panjang to the terminalsite at Tarahan North;

(c) provision of new sidings and extension of existing sidings atstations needed for running 40-car coal trains;

(d) upgrading of the signalling system;

(e) provision of 15 new 1,500--hp diesel locomotives, 264 coal wagons andtwo auxiliary cranes and rehabilitation of 135 existing coal wagons;

(f) extension of motive power and rolling stock repair facilities; and

(g) establishment of the telecommunication system needed to linkthe mine, railway, terminals and shipping functions andthe internal system needed for the railway.

In addition to these, a railway traiLning program will be undertaken, asdescribed in para. 3.38.

- 19

3.35 The upgrading of track includes: (i) about 178 km of track renewalwith 54 kg/m rails and concrete sleepers; (ii) about 71 km of rail renewalwith 42.5 kg/m rails and replacement of defective sleepers; (iii) increasingof the number of 3sleepers per km from 1,500 to 1,666; and (iv) ballast renewal(about 500,000 m ).

3.36 The bridge rehabilitation program includes: (i) replacement of 71steel spans (2-20 m) with reinforced spans; (ii) rep'lacement of 8 steel spans(25-60 m) with steel-concrete spans; (iii) reinforcement of 72 steel spans(12-60 m); and (iv) repair of piers and abutments.

3.37 The railway extensions include earth works, bridges and otherstructure and track. The upgrading of signalling includes completion of anon-going program for installation of a mechanical signalling system, includinginterlocking on the entire Tanjung Enim-Panjang section.

3.38 The new locomotives will be ballasted to 18-ton axle loads andequipped with dynamic braking and multiple unit control. The coal wagons fortransport of Suralaya coal will be of solid-bottom type, equipped with arotary coupler at one end for rotary dumping at the terminal and carry anet load of 52 tons.

3.39 The additional railroad equipment required to handle the 2.5 milliontpy of coal for Suralaya will not warrant construction of new servicing andmaintenance facilities. Repair facilities will be established in the existingworkshop at Lahat and the inspection and running maintenance will be per-formed in the existing shed in Tanjung Karang. The workshop at Lahat, whichpresently is equipped to service and overhaul steam locomotives and to over-haul all types of wagons, will be remodelled to do all heavy repairs andoverhaul works on motive power and rolling stock. The Tanjung Karang shed,which despite inadequate facilities is presently overhauling and servicingdiesel locomotives and servicing passenger and freight cars, will be remodelledto carry out proper servicing of motive power and rolling stock.

3.40 The proposed telecommunication system consists of: (i) a UHFterrestial point-to-point radio relay system running from Lahat to Kertapatiand from Perabumulih to Tanjung Karang, principally adjacent to the PJKA railline. From Tanjung Karang it is extended to Radja Basa on the southerntip of Sumatra and to Suralaya on Java; (ii) a telephone system consisting of afully integrated network of electronic private automatic branch exchanges(EPABX) at ten places with access to the Perumtel network at six places;(iii) a trackside communication network for PJKA consisting of a dispatcher tostation system, a point-to-train radio system and a station-to-station system;(iv) a message-switching network, including external telex connections, toprovide communications between PJKA central office in Kertapati and sixteenPJKA points plus the Tarahan and Suralaya terminals; and (v) VHF radio systemsfor internal radio communications for the mine, railway terminals and ship-to-shore. Operation of the system will be the responsibility of PJKA and PTBA.

3.41 The railway training program that will be undertaken by CanadianPacific Consulting Services (CPCS), which will provide managerial and technicalservices to PJKA throughout the project implementation period (para. 3.91),will be related to the movement of coal and the skills and personnel requiredto perform this, however, other traffic will to some extent benefit from theimproved skills. The training plans are based on the following basic principles:

- 20 -

(a) to make extensive use of existing local educational institutions;

(b) to make use of existing PJKA training facilities, and, when theseare inadequate, to plan new facilities which can be used forfuture system wide training;

(c) where practical, to adapt existing PJKA training courses tomeet the needs of the Bukit Asam Project; and

(d to extensively utilize PJKA personnel as instructors.

3.42 The scope of the training program is summarized in the followingtable:

ESS--Proposed Railway Training Program

Track, Bridges Telecom-Buildings Operations Mechanical munications Total

Total number of trainees 180 531 1028 126 1865Number of courses 24 42 109 39 214Group size 10-20 10-35 6-30 15-30 6-35Av. length of course (weeks) 2.5 2 25 13 16Number of participants 377 1107 1355 629 3468Man-months of instructors:Expatriates 123 21 117 209 470Local 118 66 192 300 666

Estimated Costs: (US$000):Equipment 63 40 1,159 1,444 2,706InstructorsExpatriates 882 161 874 1,527 3,444Local 314 116 315 1,290 2,035

Trainees 111 322 2,594 903 3,930Miscellaneous costs 32 44 8 - 84Total 1,402 683 4,950 5,164 12,199

Average man-months costfor expatriate instructors 7,170 7,670 7,470 7,310 7,330

3.43 As part of its project management contract, CPCS will provide sub-stantial operational assistance in track and bridge maintenance, train opera-tion and telecommunication maintenance. During operation, the Bank, theGovernment and PJKA will periodically review the level and efficiency of coaltransport. Agreement was reached that if this transport is not being carriedout in a timely and efficient manner, PJKA will promptly take action to correctthe situation which may include a contract for operational assistance.

5. Tarahan Terminal

3.44 After a consideration of five sites in the area, Tarahan North, about6.5 km south of the existing railhead at Panjang on Lampung Bay in SouthernSumatra, has been selected as the terminal site. Selection of the Projectsite was based on considerations of accessibility, water depth, wave regime

- 21 -

and wind direction. The present site is on a natural beach, underlain withcoral, lying between an existing road and the water. With a realignment ofthe road, already underway, sufficient land and beach area can be reserved forthe terminal without affecting the village of Sorampok which is on the landside of that part of the road not subject to realignment. Steep cliffs behindthe village constrain the area, determine the route to be followed by the road,and provide a flat plain on which the future extension of the railway fromPanjang must be located. The site is bounded on the north by land owned by awood processing plant.

3.45 While the terminal has been designed for an initial volume of 2.5 mil-lion tpy, the railway facilities, in the form of loop track, are sufficient toprovide space to handle future volumes of up to 12.0 million tpy. The initialworks will, however, be sufficient only for the initial volume. Adequate soiltests have been undertaken on land and at the pier site to ensure that thesite is acceptable. Areas of sand adequate for the preparation of the sitehave been located nearby, and hydrographic studies have not revealed anynavigational problems. Topographical studies have also been completed.

3.46 The terminal's design consists of a railway car dumper with an un-loading capacity of 3,000 tph. Coal reception and take-away conveyor facilities,with a capacity of 3,200 tph, will crush the coal; and conveyor belts anda fixed stacker will stockpile the crushed coal above two reclaim hopperslocated at ground level. The stockpile will have 15,000 tons of activestorage and 45,000 tons of compacted storage. These amounts are derived froma system-wide stockpile optimization study. Provision is made at the primarycrusher to direct future larger volumes of coal (e.g., for later stages of theSuralaya or Tuban power developments) to much larger stockpiling facilities,to be served by mobile stackers or combined stacker/reclaimers. When thisexpansion takes place, the facilities proposed for the 2.5 tpy volume willbecome the emergency stacking and reclaiming system.

3.47 Coal will be reclaimed from the stockpile for ship loading bya combination of gravity flow through the reclaim hoppers and flow createdby three large bulldozers pushing coal to the reclaim hoppers. This systemis expected to provide, over the average distance the bulldozers will operate,a coal flow at a peak rate of about 2,000 tph, sufficient to load ships at anaverage of 1,150 tph. This method of coal reclaim is used for ship loading ina number of coal terminals in other parts of the world, one of which has beeninspected by Bank staff, and is expected to be satisfactory.

3.48 Reclaimed coal will be sent by conveyor belts to secondary coalcrushing facilities consisting of, initially, three units each of 1,100 tphcapacity (two operational, one stand-by). After secondary crushing, the coalwill be sent to the travelling ship loader, which is designed to load theProject ship at an average rate of 1,150 tph. Provision is made for theshiploader to load at a future average rate of 2,000 tph, so that only minoralterations will need to be made when the volume rises above 2.5 million tpy.The coal loading pier, aligned to the underwater contours so as to permitapproach of a loaded Project ship from either direction, will stand in 12 m ofwater. While the Project ship will require only 7 m of water, the possibilitycan arise that, in the event of damage to the ship, emergency ships would haveto be used. After a survey was made of the world fleet of ships carryingtheir own coal unloading gear, it was decided that provision should be made

- 22 -

for the 12 m depth sufficient to accommodate up to a 40,000 dwt ship thatwould be loaded fully with 30,000 tons of coal.