Embed Size (px)

Citation preview

1

WORKING PAPER NO: 394

Effect of Payment Mechanisms on the Replacement Time of Durable Products Purchase1

Aruna Divya T Doctoral Student

Marketing Indian Institute of Management Bangalore Bannerghatta Road, Bangalore – 5600 76

Kanchan Mukherjee Associate Professor,

Organizational Behaviour and Human Resource Management Indian Institute of Management Bangalore Bannerghatta Road, Bangalore – 5600 76

Ph: 080-2699 3332 [email protected]

Year of Publication-February 2013

1 This research is work in progress. Please do not quote or cite without permission.

2

Effect of Payment Mechanisms on the Replacement Time of Durable Products

Purchase

Abstract Replacement timing decisions of durable goods have been studied by scholars from both

normative and descriptive perspectives. Normative models are based on the optimization of some

utility based objective function which then suggest an optimal time for replacing a durable good.

On the other hand, studies by behavioral researchers using simulated lab-experiments show that

individuals do not always make optimal replacement decisions but instead exhibit deviations in

systematic ways. For example, individuals were observed to replace old durables at a slower rate

than that predicted by normative models and seemed to anchor on some mental threshold for

making replacement decisions.

The present study adds to the literature on replacement decisions by uncovering systematic

linkages between different payment methods at the time of purchase of durable goods and the

replacement timing of the same. We also explore the psychological processes underlying these

systematic effects. We start by proposing a behavioral model that draws on findings from the

mental accounting, coupling effects and cognitive dissonance literatures to predict that people

who make cash purchases are more likely to replace the durable earlier compared to people who

make the purchase through loans and make EMI payments.

Our arguments are based on how payment methods (cash or EMI) influence the consumption

experiences of durable goods, which ultimately impacts the replacement time. We propose that

the strength of coupling, which is the degree of association between payment and consumption

instances, depends on different payment methods and differentially influences the motivation of

3

individuals to close their mental accounts on one hand and the consumption experiences due to

cognitive dissonance effects on the other.

We conduct two lab and one field experiment to test our model predictions and find support for

the same.

Keywords: Durable Goods, Replacement Decisions, Mental Accounting, Cognitive Dissonance,

Coupling.

4

Introduction:

Manufacturers and retailers of durable products are increasingly trying to incentivize the

consumers by making purchase decisions more attractive. The increasing advent of EMI

(Equated Monthly Installment) based payment for a broad range of durable products like

automobiles, digital cameras, home appliances etc., are a case in point. While the effect of such

payment scheme on the purchase likelihood is intuitive, the effect on the replacement decisions

is a non-trivial question which is worth exploring further.

Since durable products are usually priced higher than the non-durable products, the purchase and

the replacement decisions are an inter-mix of several dynamics of maximizing inter-temporal

utility. Durable Products Replacement Decisions had been extensively explored in the past by

scholars in operations research and economics. It is only recently that behavioral economists and

consumer behaviorists have also started giving a different perspective to this concept (Guiltinan,

2010). Individuals rely on heuristics while making their replacement decisions (Cripps & Meyer,

1994) and are driven by motivating factors like product characteristics (Guiltinan, 2010) and

their own functional attitudes (Grewal, Mehta, & Kardes, 2004). They also mentally track the

benefits of the durable product to evaluate the consumption experience (Okada, 2001).

The process by which individuals mentally track the costs and benefits of consuming a durable

product is moderated by several factors. The present study tries to delve deeper into the process

through which mental accounting takes place and explores the role played by one moderating

factor, i.e., the payment mechanism. The consequences of mental accounting are also studied

with specific focus on the replacement timing decisions.

5

The following sections build up the theoretical foundation for the hypotheses. First, a broad

review of the durable goods literature is presented. The next section narrows down to one aspect

of durable goods i.e., the replacement decisions. The process behind the replacement decisions is

elaborated using concepts from Mental Accounting. Finally, the role of one external factor in

moderating the mental accounting process is explained.

The study also presents the results from a pilot study and proposes the design for follow-up

studies.

Literature Review:

Durable Products: The purchase of a durable product is usually triggered by a need. Studies that

looked at the pre-purchase behavior of durable products primarily highlighted the information-

search related aspects (Westbrook & Fornell, 1979). Durable products usually cost a lot more

than the non-durable products (Grewal, Mehta, & Kardes, 2004), hence consumers indulge in

active information-search to minimize the risks associated with a purchase. Durable products are

characterized by consumption scenarios that extend over long periods of time. Hence, the level

of involvement with the good is expected to be higher. This is the reason why the decision

making process is a combination of psychological and normative aspects.

Consumers are faced with typically two broad decisions during the consumption of any durable

product i.e., whether or not to repair the product (maintenance activity in case of wear and tear)

and when to replace the product. Normative models that looked at modeling these decisions, took

into account few common variables like the costs associated with the activity (either repair or the

cost of new product), the initial purchase price of the currently owned product, the expected re-

sale value of the existing product, and finally, the discounted expected future benefits from the

6

existing and new product (in case of replacement). The decision of when to replace has been

identified using an optimal stopping solution model (Rust, 1987). The model considers a

threshold performance level, which is used as a benchmark to make the replacement decisions.

The replacement decisions in this as well as in other normative models are based solely on the

product performance attributes. The models primarily catered to firm’s replacement decision

making contexts. Individual replacement decisions of durable products were usually considered

as another form of firms’ replacement decisions. In other words, consumers were assumed to act

as perfectly rational economic agents.

Contrary to these assumptions, consumers actually deviated from the normative outcomes and

incorporated several psychological factors in their decision making process (Cripps & Meyer,

1994). Experimental studies proved the existence of under-replacement bias, due to which

individuals did not replace the durable products till a mentally framed time horizon had elapsed.

Beyond such time horizon, individuals showed an increased tendency to replace. Individuals did

not react rationally to the cost-benefit calculations required for a replacement decision, but rather

relied on some heuristics.

Replacement Decisions: Cripps & Meyer (Cripps & Meyer, 1994) identified the deviations from

normative theories exhibited by individuals while making durable products replacement

decisions. Okada (Okada, 2001) moved a step further by analytically incorporating the

behavioral aspects and providing a process oriented approach to the durable products

replacement decisions. A dual-system based utility function was formulated for explaining the

decision making process. The first system corresponds to the normative utility and compares the

costs and benefits of the transaction. On the other hand, the second system captures the mental

accounting aspects of consumption. Mental Accounting refers to the process through which

7

individuals mentally track the costs and benefits of a transaction (Thaler, 1985). In the present

context of durable products, the mental account is opened at the time of making the purchase

payment. The benefits reaped from using the product are posted and the mental account is closed

when the benefits totally compensate for the costs incurred. Okada thus defines the mental

accounting utility as the difference between the initial purchase price of the durable product and

the cumulative enjoyment obtained from using the product. Since the psychological costs of

disposing a product prematurely are very painful, the slope of the mental accounting utility

function is steeper than the normative utility function. Consumers show a resistance to replace

till their mental accounts are closed.

Two assumptions are implicit in the definition of mental accounting utility. The first one is that

the durable product is entirely paid for before its consumption. Although fair, it limits the

generalizability of the formulation. Durable products are usually priced higher than non-durable

products (Grewal, Mehta, & Kardes, 2004), and the method of financing for their purchase varies

from cash, credit cards to term loans. So, the assumption that the payment is fully made before

consuming the product, may not be valid in all cases. Another reason why the assumption needs

to be relaxed is that the mental accounting process differs with varying payment mechanisms.

The second one is that the effect of payment made towards the purchase of the durable product

remains same throughout the consumption period. There is no mechanism to account for the

temporal separation between the payment episode and the various consumption episodes.

Consumers are assumed to have perfect recall and perceive the purchase price of the durable in a

complete objective sense. Studies that adopted mental accounting concepts in explaining inter-

temporal choice and decision making show that the perception of fixed-fee, up-front costs

diminish with time (Gourville & Soman, 1998). In assessing the effect of such payments on

8

subsequent consumption behavior, the temporal distance between them was taken as a moderator

(Prelec & Loewenstein, 1998) (Kamleitner, Cost-Benefit Associations and Financial Behavior,

2009).

Hence, any further attempt to analytically model the mental accounting utility of durable goods

replacement decisions, should take into account the possibility of different payment mechanisms,

the effect of each of them on the mental accounting process and finally, the temporal separation

between the payment instance and the various consumption instances.

Mental Accounting: One of the basic assumptions that underlie all the mental accounting

concepts as well as their applications is that individuals are able to track the payments and

benefits of a transaction and post them accurately to the relevant mental accounts. Termed as

Coupling, it refers to the mapping of benefits and payments of a transaction (Kamleitner,

Coupling : The Implicit Assumption Behind Sunk-Cost Effect and Related Phenomena, 2008).

The concept of Coupling gains special significance in contexts with temporally separated

payments and consumption episodes. Due to the effect of temporal separation, the payment

episodes are buffered by thoughts of consumption and the consumption episodes are dampened

by the thoughts of payment (Prelec & Loewenstein, 1998). The degree of coupling varies

inversely with the temporal distance between the events (Kamleitner, 2009), (Kamleitner, 2008).

Coupling is closely related to another widely studied phenomenon in the domain of mental

accounting, which is the Sunk-Cost Effect. Sunk-Cost Effect refers to the increased levels of

commitment towards a given task after an investment in time or money has already been made

towards that task (Soman & Gourville, 2001), (Gourville & Soman, 1998). Deeper investigations

into the sunk-cost effect led to the finding that sunk-cost effect was valid only when there was

9

coupling between payment and consumption episodes (Kamleitner, 2008). If there was no

coupling, the thoughts of initial investments made towards a task would not be salient and hence

there would not be an escalation in the commitment levels to continue the task.

Some studies have tried to identify the factors that moderate the degree of coupling (Kamleitner,

2008). Broadly speaking, these factors can be grouped into behavioral, situational or

motivational. Situational factors include temporal separation between payment and consumption

events, payment methods and the magnitude of the payment. Few studies have also identified the

possible consequences of coupling (Kamleitner, 2008). Consumption level, re-purchase

likelihood, salience of opportunity costs are some of the consequences. Studies that looked

specifically at the consumption levels concluded that the consumption either increases or

decreases in response to weaker coupling or diminishing sunk-cost effect (Gourville & Soman,

1998), (Prelec & Loewenstein, 1998). Scenarios where the commitment levels decreased with a

decrease in sunk-cost effect include attending a sports-club, pre-paid holiday etc. In other words,

paid-for services were usually characterized by a fall in consumption levels when the sunk-cost

effect vanished. On the other hand, consumption levels increased in scenarios like vacations,

cars, pay-per-usage offers etc. (Prelec & Loewenstein, 1998), (Heath & Fennema, 1996).

Payment Mechanism: Coupling and sunk-cost effect are known to be influenced by the payment

method (Kamleitner, 2008). The salience of the payment influences its degree of association with

the consumption behavior. Several other aspects moderate the effect of different payment

methods on the consumption behavior. Temporal separation and the magnitude of the payment

are two such factors. Payment methods that encourage temporal congruity between payment and

consumption instances increase the consumption levels, due to stronger coupling (Kamleitner,

Cost-Benefit Associations and Financial Behavior, 2009). Term loans are an example which

10

induce tighter coupling. On the other hand, credit cards or up-front payment for benefits that can

be enjoyed at a later point in time, will lead to weaker coupling. The effect of weak coupling on

consumption levels will depend on the nature of the product.

Replacement Timing of Durable Products: The consequences of coupling are expected to include

the consumption levels, re-purchase likelihood and price demanded for disposing the product etc

(Kamleitner, Coupling : The Implicit Assumption Behind Sunk-Cost Effect and Related

Phenomena, 2008). In the context of durable goods consumption, the degree of coupling will

have an effect on the perceived enjoyment derived from the product. The enjoyment derived will

influence the consumption levels. At the time of making a replacement decision, factors like

perceived enjoyment, worthiness of the product for a given usage level and payment paid, and

the future expected benefits that the product can give form the key decision variables. Hence,

there is a chain of effect that percolates from degree of coupling to the final replacement timing

decisions.

Another consequence of the degree of coupling which remains to be tested is the price demanded

on disposing off the product (Kamleitner, Coupling : The Implicit Assumption Behind Sunk-

Cost Effect and Related Phenomena, 2008). The higher the degree of coupling, the higher is the

price demanded.

Studies in the past that looked at replacement timing decisions identified product characteristics

and consumer characteristics as two broad motivating factors (Guiltinan, 2010). Product

characteristics include technological performance, hedonic value, ergonomics, ecological benefit

etc. Consumer characteristics are identified by grouping them into different functional attitudes

like knowledge function, utilitarian, value-expressive and social-adjustive. All the above factors

11

are intrinsic from a marketer’s perspective. They are not amenable to manipulation from external

source. On the other hand, factors like payment mechanism, magnitude of payment etc., are

susceptible to manipulation and hence serve as a strong tool for marketers to influence

consumers’ replacement timing decisions.

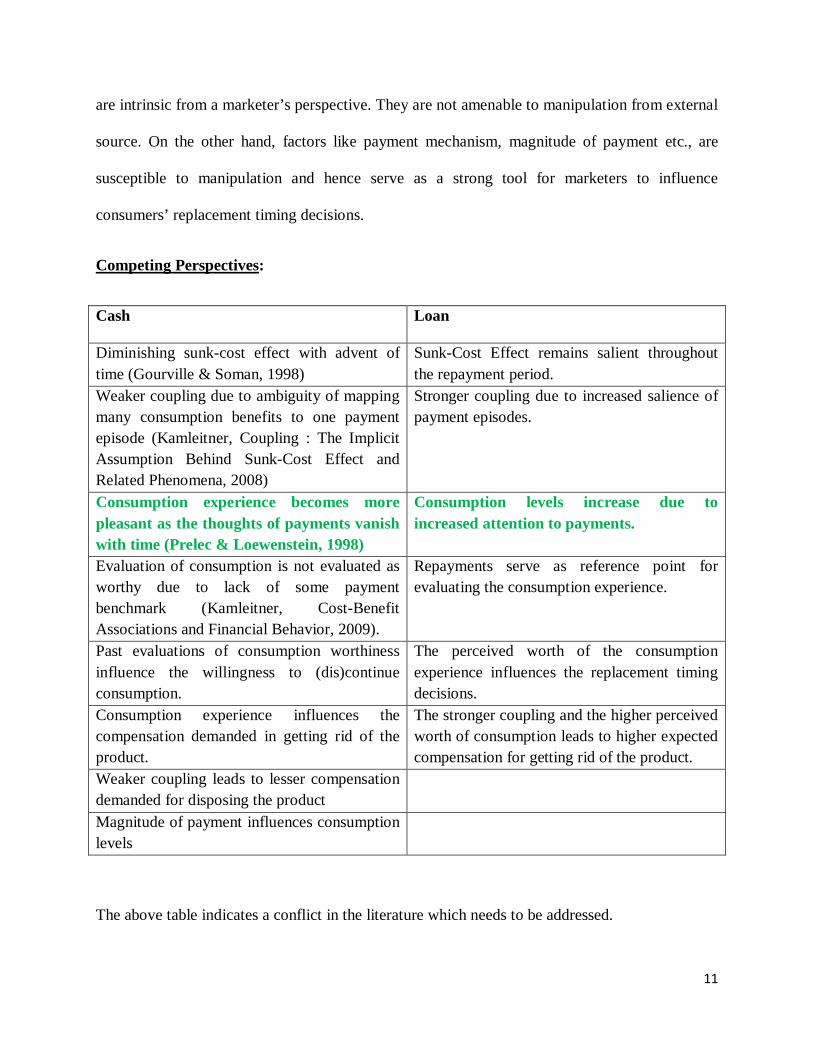

Competing Perspectives:

Cash Loan

Diminishing sunk-cost effect with advent of time (Gourville & Soman, 1998)

Sunk-Cost Effect remains salient throughout the repayment period.

Weaker coupling due to ambiguity of mapping many consumption benefits to one payment episode (Kamleitner, Coupling : The Implicit Assumption Behind Sunk-Cost Effect and Related Phenomena, 2008)

Stronger coupling due to increased salience of payment episodes.

Consumption experience becomes more pleasant as the thoughts of payments vanish with time (Prelec & Loewenstein, 1998)

Consumption levels increase due to increased attention to payments.

Evaluation of consumption is not evaluated as worthy due to lack of some payment benchmark (Kamleitner, Cost-Benefit Associations and Financial Behavior, 2009).

Repayments serve as reference point for evaluating the consumption experience.

Past evaluations of consumption worthiness influence the willingness to (dis)continue consumption.

The perceived worth of the consumption experience influences the replacement timing decisions.

Consumption experience influences the compensation demanded in getting rid of the product.

The stronger coupling and the higher perceived worth of consumption leads to higher expected compensation for getting rid of the product.

Weaker coupling leads to lesser compensation demanded for disposing the product

Magnitude of payment influences consumption levels

The above table indicates a conflict in the literature which needs to be addressed.

12

Research Questions:

The present study tries to answer the question related to how consumers mentally track the

multiple consumption episodes when the payment is an upfront fee versus an installment based

method. Also, how does the complexity of mapping multiple consumption episodes to one

temporally distant payment episode influence the perceived worth of consumption? Will the

reduced ambiguity of mapping payments and consumption benefits translate to different

behavioral outcomes?

Theoretical Background:

Durable goods replacement decisions are dictated by evaluation of consumers’ past experiences.

Consumers evaluate the money’s worth that the product gives and frame their future expectations

accordingly. Hence, a payment mechanism that enables consumers to think more objectively

about the consumption experience and their money’s worth will lead to more positive outcomes.

Durable products financed by cash are characterized by weak coupling due to the ambiguity of

associating multiple consumption benefits to one temporally distanced payment instance. Hence,

the evaluation of consumption experiences is ambiguous. On the other hand, term loans with

repayment schedules spanning over several years serve as a reference point for evaluating the

value of a consumption experience. The attention to the quality of experience is higher due to the

strong coupling between payments and consumption episodes.

Hence, in case of positive experience, consumers experiencing higher degree of coupling will be

willing to continue using the product for a longer time. In contrast, consumers having lower

degree of coupling will not be evaluate the positive experiences as expected. Hence the

replacement time will be shorter.

13

For negative consumption experience, consumers with higher degree of coupling are bound to

feel more painful as they can associate the performance loss with a corresponding payment. Due

to this, the replacement decisions are hastened. This behavior is also expected due to loss

aversion phenomenon. Consumers with a lower degree of coupling do not find the negative

experience as painful as the thoughts of payments are not salient. The replacement length is

longer in this case as compared to the one with higher coupling.

Hypotheses:

H1 – Payment Mechanism influences the replacement time of durable goods.

H1a) – The effect of loan on replacement time is higher than that of cash.

H1b) – The effect of payment mechanism on replacement time is moderated by the quality of

usage experience.

H2) – Payment Mechanism influences the selling price of the product.

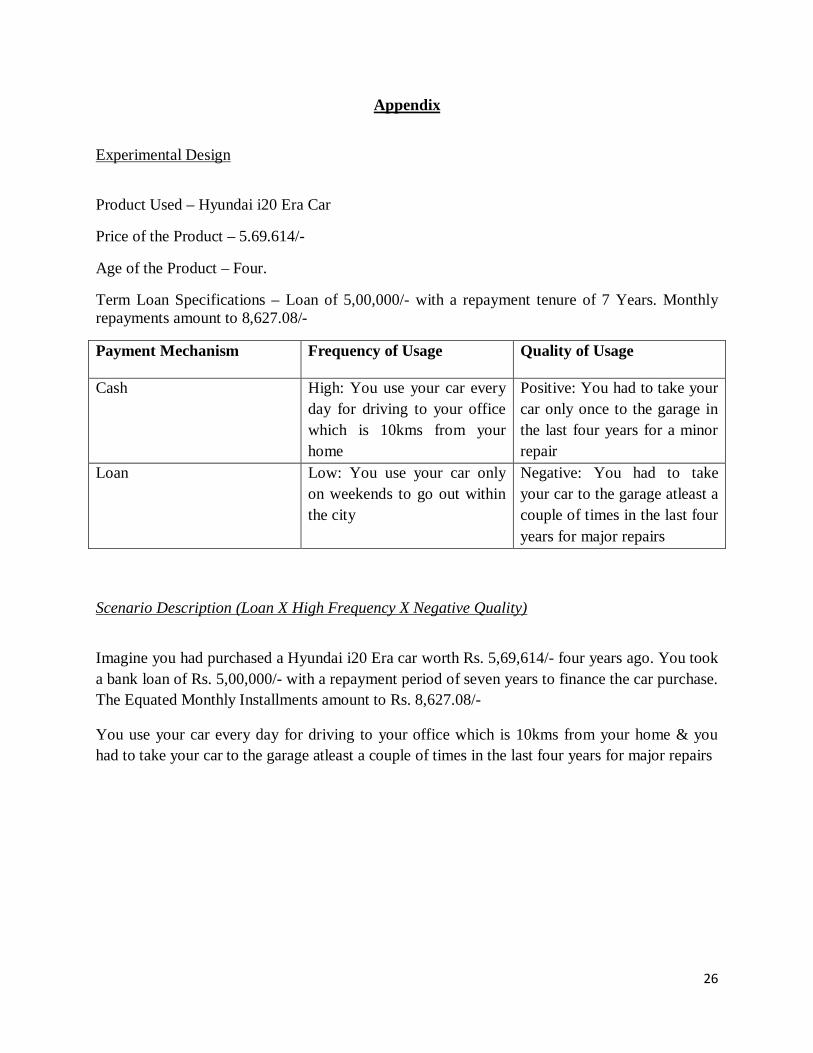

Experimental Design:

Pilot Study – An initial study was conducted to verify the effect of payment mechanism on the

replacement timing decisions. The pilot study was conducted online using Qualtrics for the

questionnaire and Mechanical Turk for getting the respondents. The context of the study was car,

and the respondents were filtered according to their geographical location. Since the car

described in the scenario was priced according to the on-road price in India, respondents were all

Indians by origin. The design was a modification of the one present in Okada’s (Okada, 2001)

paper. The present study used a 2X2X2 (payment mechanism X frequency X quality) between-

subjects design. The payment mechanism was manipulated for cash and term loan conditions.

14

The low and high frequency as well the positive and negative quality of the usage was also

manipulated accordingly. The details of the scenarios are included in the Appendix.

The money’s worth obtained from using the product was measured using a 7-point Likert scale,

with 1 representing “I have obtained a lot of my money’s worth” and 7 representing “I have not

obtained my money’s worth at all”. The expected future enjoyment of continued usage of the

product was also measured using 7 point Likert scale, where 1 represented “I will not get any

enjoyment at all” and 7 represented “I will continue to get a lot of enjoyment”. The replacement

timing decision and the price demanded on replacement was also measured.

Data Analysis:

Descriptive Statistics: The data was initially collected from 468 respondents. Respondents who

failed to respond accurately to the validation questions were deleted from the analysis. The next

level of data screening was done based on other checks put in place within the questionnaire. The

final set of 217 valid responses was finally considered for data analysis. 90 of the respondents

were female. The mean age of the respondents was 28.14 years. Out of the 217, 99 were

graduates, 58 had a masters degree or above, 53 were in college and 7 completed only high

school.

The between-subjects design led to 8 different manipulations. The number of data points for each

manipulation is listed below.

15

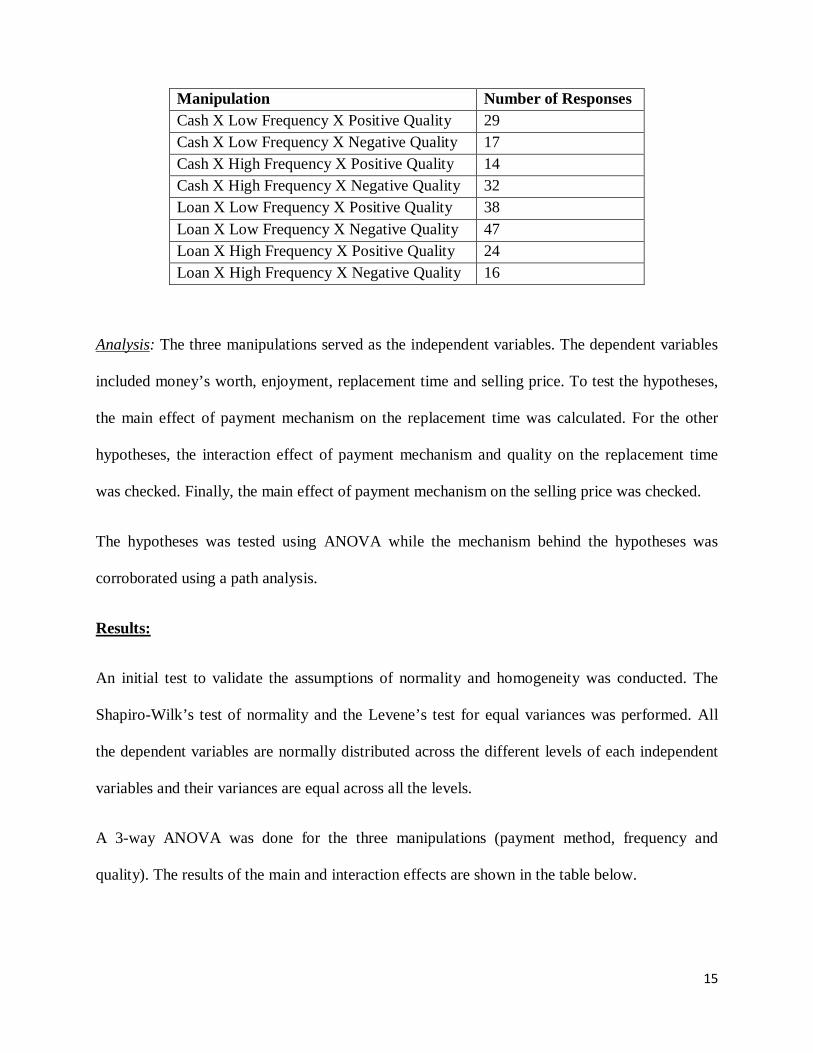

Analysis: The three manipulations served as the independent variables. The dependent variables

included money’s worth, enjoyment, replacement time and selling price. To test the hypotheses,

the main effect of payment mechanism on the replacement time was calculated. For the other

hypotheses, the interaction effect of payment mechanism and quality on the replacement time

was checked. Finally, the main effect of payment mechanism on the selling price was checked.

The hypotheses was tested using ANOVA while the mechanism behind the hypotheses was

corroborated using a path analysis.

Results:

An initial test to validate the assumptions of normality and homogeneity was conducted. The

Shapiro-Wilk’s test of normality and the Levene’s test for equal variances was performed. All

the dependent variables are normally distributed across the different levels of each independent

variables and their variances are equal across all the levels.

A 3-way ANOVA was done for the three manipulations (payment method, frequency and

quality). The results of the main and interaction effects are shown in the table below.

Manipulation Number of Responses Cash X Low Frequency X Positive Quality 29 Cash X Low Frequency X Negative Quality 17 Cash X High Frequency X Positive Quality 14 Cash X High Frequency X Negative Quality 32 Loan X Low Frequency X Positive Quality 38 Loan X Low Frequency X Negative Quality 47 Loan X High Frequency X Positive Quality 24 Loan X High Frequency X Negative Quality 16

16

Table 1 – Three Way ANOVA Results

Independent Variables Dependent Variables

Money’s Worth Expected Future Enjoyment

Replacement in Years Selling Price

Payment Mechanism F(1,209)=5.349, p=.022

F(1,209) = .068, p=.795

F(1,209)=4.810, p=.029

F(1,209) = .349, p=.556

Frequency F(1,209)=1.677, p=.197

F(1,209) = .275, p=.601

F(1,209) = .026, p=.873

F(1,209) = 4.447, p=.036

Quality F(1,209)=7.356, p=.007

F(1,209)=13.384, p=.000

F(1,209)=16.205, p=.000

F(1,209) = 2.719, p=.101

Frequency*Payment Mechanism F(1,209) = .367, p=.545

F(1,209) = .058, p=.810

F(1,209)=1.529, p=.218

F(1,209) = .012, p=.914

Quality*Payment Mechanism F(1,209)=0.000, p=.988

F(1,209) = .05, p=.824

F(1,209) = .023, p=.878

F(1,209) = .790, p=.375

Quality*Frequency F(1,209) = .352, p=.554

F(1,209) = 1.560, p=.213

F(1,209) = .173, p=.678

F(1,209) = 1.474, p=.226

Frequency*Quality*Payment Mechanism F(1,209) = .554, p=.458

F(1,209) = .706, p=.402

F(1,209)=5.608, p=.019

F(1,209) = 3.044, p=.082

The above table proves the main hypothesis of payment mechanism influencing the replacement

timing decisions. The main effect of payment mechanism is significant (p=.029) for replacement

timing as well as for money’s worth (p=-.022). This offers support for H1. The subsequent

hypothesis for the interaction between quality and payment mechanism is not supported by this

data. The last hypothesis regarding the effect of payment mechanism on the selling price is also

not supported by the data (p=.556). The 3-way interaction effect is again significant on the

replacement timing (p=.019). Also, the main effects of quality is significant on money’s worth

(p=.007), expected enjoyment (p=.000) and on replacement timing (p=.000). Although the two-

way interactions are not significant, the three-way interactions came out to be significant.

A simple main-effects was thus conducted to see the underlying cause of the interaction effects.

17

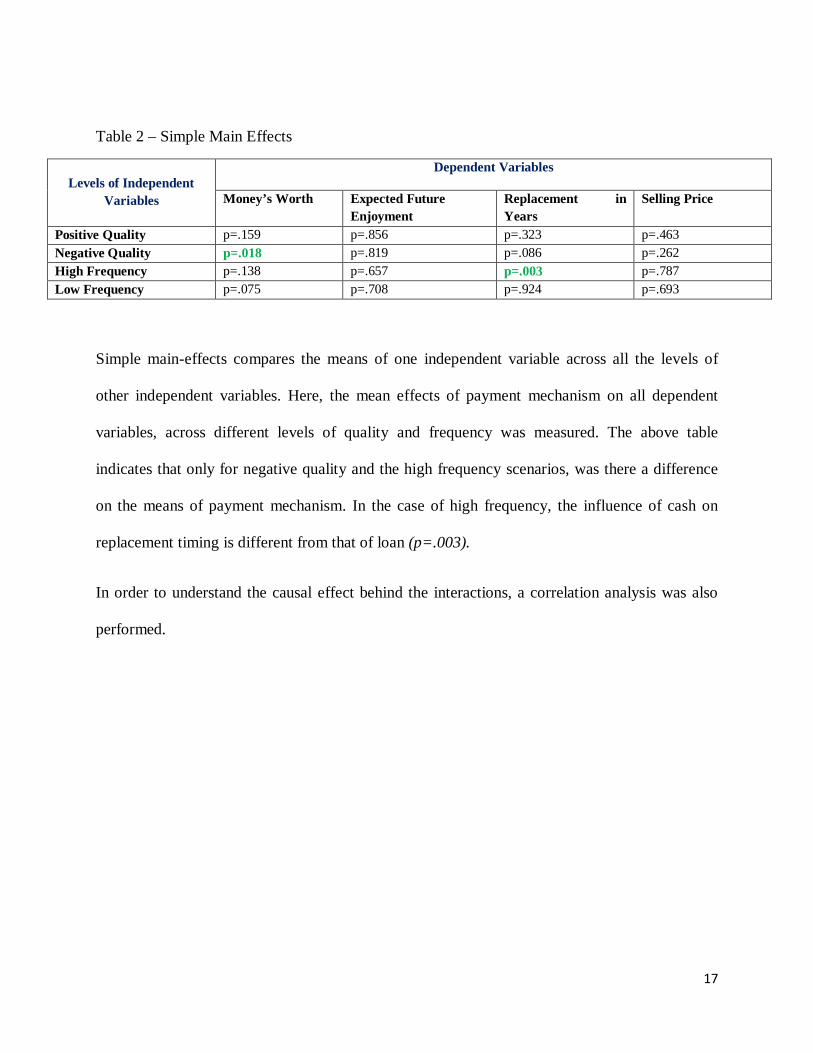

Table 2 – Simple Main Effects

Levels of Independent Variables

Dependent Variables

Money’s Worth Expected Future Enjoyment

Replacement in Years

Selling Price

Positive Quality p=.159 p=.856 p=.323 p=.463 Negative Quality p=.018 p=.819 p=.086 p=.262 High Frequency p=.138 p=.657 p=.003 p=.787 Low Frequency p=.075 p=.708 p=.924 p=.693

Simple main-effects compares the means of one independent variable across all the levels of

other independent variables. Here, the mean effects of payment mechanism on all dependent

variables, across different levels of quality and frequency was measured. The above table

indicates that only for negative quality and the high frequency scenarios, was there a difference

on the means of payment mechanism. In the case of high frequency, the influence of cash on

replacement timing is different from that of loan (p=.003).

In order to understand the causal effect behind the interactions, a correlation analysis was also

performed.

18

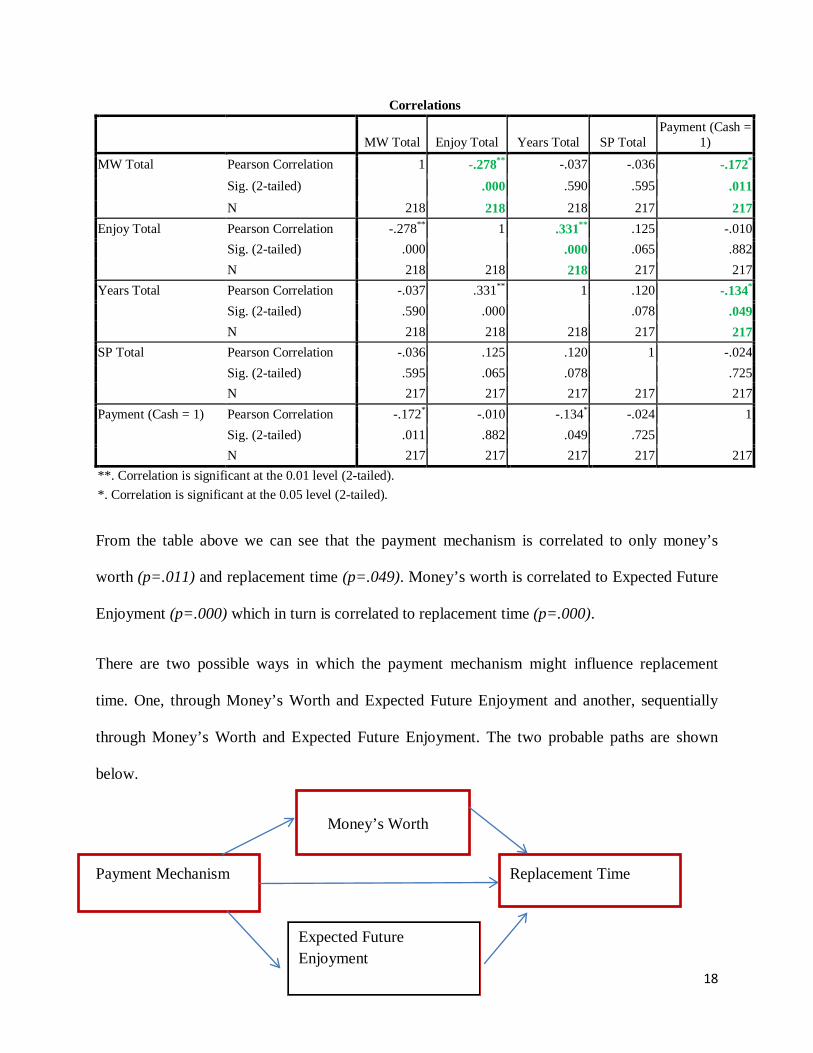

Correlations

MW Total Enjoy Total Years Total SP Total Payment (Cash =

1)

MW Total Pearson Correlation 1 -.278** -.037 -.036 -.172* Sig. (2-tailed) .000 .590 .595 .011 N 218 218 218 217 217

Enjoy Total Pearson Correlation -.278** 1 .331** .125 -.010 Sig. (2-tailed) .000 .000 .065 .882 N 218 218 218 217 217

Years Total Pearson Correlation -.037 .331** 1 .120 -.134* Sig. (2-tailed) .590 .000 .078 .049 N 218 218 218 217 217

SP Total Pearson Correlation -.036 .125 .120 1 -.024 Sig. (2-tailed) .595 .065 .078 .725 N 217 217 217 217 217

Payment (Cash = 1) Pearson Correlation -.172* -.010 -.134* -.024 1 Sig. (2-tailed) .011 .882 .049 .725 N 217 217 217 217 217

**. Correlation is significant at the 0.01 level (2-tailed). *. Correlation is significant at the 0.05 level (2-tailed).

From the table above we can see that the payment mechanism is correlated to only money’s

worth (p=.011) and replacement time (p=.049). Money’s worth is correlated to Expected Future

Enjoyment (p=.000) which in turn is correlated to replacement time (p=.000).

There are two possible ways in which the payment mechanism might influence replacement

time. One, through Money’s Worth and Expected Future Enjoyment and another, sequentially

through Money’s Worth and Expected Future Enjoyment. The two probable paths are shown

below.

Money’s Worth

Payment Mechanism Replacement Time

Expected Future Enjoyment

19

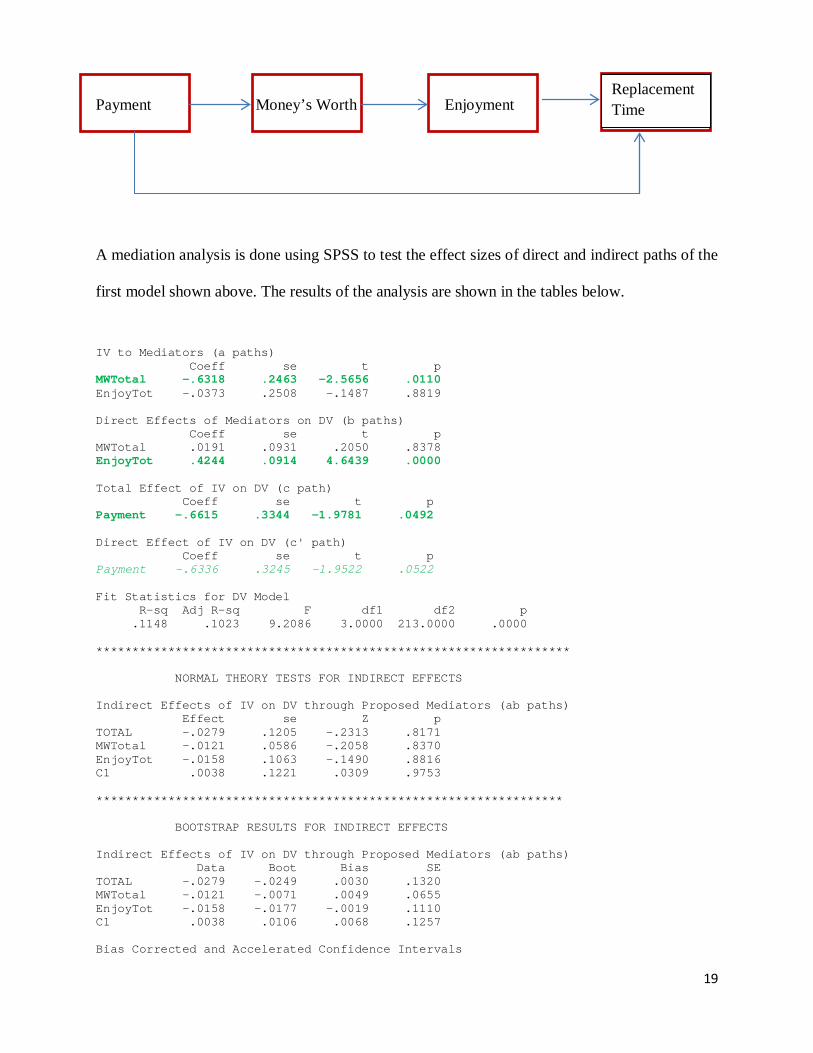

Payment Money’s Worth Enjoyment

A mediation analysis is done using SPSS to test the effect sizes of direct and indirect paths of the

first model shown above. The results of the analysis are shown in the tables below.

IV to Mediators (a paths) Coeff se t p MWTotal -.6318 .2463 -2.5656 .0110 EnjoyTot -.0373 .2508 -.1487 .8819 Direct Effects of Mediators on DV (b paths) Coeff se t p MWTotal .0191 .0931 .2050 .8378 EnjoyTot .4244 .0914 4.6439 .0000 Total Effect of IV on DV (c path) Coeff se t p Payment -.6615 .3344 -1.9781 .0492 Direct Effect of IV on DV (c' path) Coeff se t p Payment -.6336 .3245 -1.9522 .0522 Fit Statistics for DV Model R-sq Adj R-sq F df1 df2 p .1148 .1023 9.2086 3.0000 213.0000 .0000 ****************************************************************** NORMAL THEORY TESTS FOR INDIRECT EFFECTS Indirect Effects of IV on DV through Proposed Mediators (ab paths) Effect se Z p TOTAL -.0279 .1205 -.2313 .8171 MWTotal -.0121 .0586 -.2058 .8370 EnjoyTot -.0158 .1063 -.1490 .8816 C1 .0038 .1221 .0309 .9753 ***************************************************************** BOOTSTRAP RESULTS FOR INDIRECT EFFECTS Indirect Effects of IV on DV through Proposed Mediators (ab paths) Data Boot Bias SE TOTAL -.0279 -.0249 .0030 .1320 MWTotal -.0121 -.0071 .0049 .0655 EnjoyTot -.0158 -.0177 -.0019 .1110 C1 .0038 .0106 .0068 .1257 Bias Corrected and Accelerated Confidence Intervals

Replacement Time

20

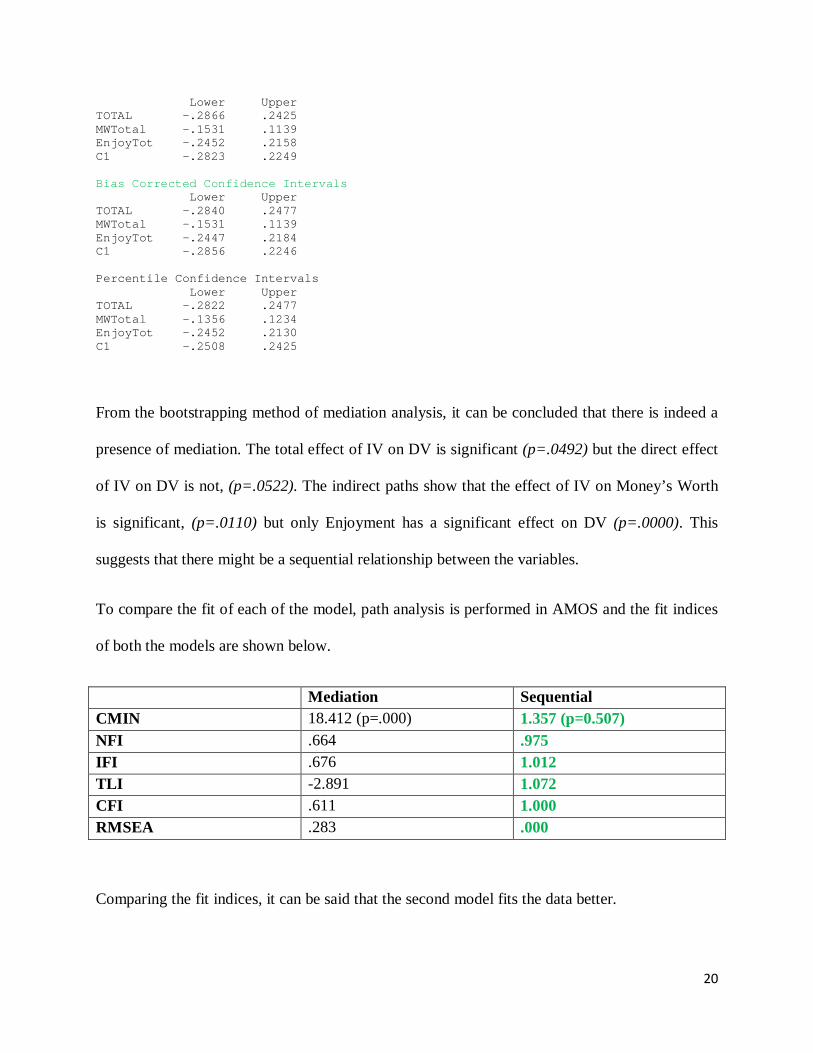

Lower Upper TOTAL -.2866 .2425 MWTotal -.1531 .1139 EnjoyTot -.2452 .2158 C1 -.2823 .2249 Bias Corrected Confidence Intervals Lower Upper TOTAL -.2840 .2477 MWTotal -.1531 .1139 EnjoyTot -.2447 .2184 C1 -.2856 .2246 Percentile Confidence Intervals Lower Upper TOTAL -.2822 .2477 MWTotal -.1356 .1234 EnjoyTot -.2452 .2130 C1 -.2508 .2425

From the bootstrapping method of mediation analysis, it can be concluded that there is indeed a

presence of mediation. The total effect of IV on DV is significant (p=.0492) but the direct effect

of IV on DV is not, (p=.0522). The indirect paths show that the effect of IV on Money’s Worth

is significant, (p=.0110) but only Enjoyment has a significant effect on DV (p=.0000). This

suggests that there might be a sequential relationship between the variables.

To compare the fit of each of the model, path analysis is performed in AMOS and the fit indices

of both the models are shown below.

Mediation Sequential CMIN 18.412 (p=.000) 1.357 (p=0.507) NFI .664 .975 IFI .676 1.012 TLI -2.891 1.072 CFI .611 1.000 RMSEA .283 .000

Comparing the fit indices, it can be said that the second model fits the data better.

21

Hence, it can be explained that the payment mechanism influences the perceived money’s worth

derived out of consuming the product. The expected future enjoyment is an outcome of how

worthy individuals feel was the past consumption experience. The higher the level of future

enjoyment, the more individuals want to continue using the product and hence delay the

replacement decisions. The direct effect of payment mechanism on the replacement timing

decisions can be explained using the concepts of coupling and sunk-cost effect. The tighter the

coupling, the more is the resistance to let go of the product. Hence, individuals in the loan

condition are expected to replace the product at a slower rate in comparison to those in the cash

condition.

The mediation analysis as well as the path analysis did not consider selling price into account as

it was not found to be significantly correlated with any other variable.

Discussion:

The results of the pilot study proved that payment mechanism influences the replacement timing

decisions of durable goods. Although the expected moderating effect of usage quality was not

supported by the data, the hypotheses cannot be dismissed at this stage. The effect of payment

mechanism on the selling price was also not supported by the data.

The payment mechanism influences the replacement timing decision in a two-stage process. The

salience of payment mechanism influences the perceived worth of the consumption experience.

The past usage experiences, influence the expected levels of future enjoyment from using the

product. The future expectations influence the willingness to retain or replace the product.

22

Limitations:

The study suffers from several limitations, which could explain why all the hypotheses are not

supported significantly.

i) The data points in few manipulations was too less to warranty a significant result in

ANOVA (ex: Cash X High X Positive manipulation had only 14 while Loan X High

X Negative manipulation had only 16 data points).

ii) The survey was conducted online and could have led to some confound. The follow-

up studies are proposed to be conducted in a more controlled environment.

iii) The frequency manipulation could have been misconstrued as different perceived

need. To reduce this confound, the frequency manipulation could be quantified in

terms of number of kilometers. In other words, the scenario could read as “you drive

your car every day to your office which is 15Kms away” or “you drive your car every

day to your office which is 5Kms away”.

iv) The quality manipulation does not distinguish starkly between the positive and the

negative cases. There are chances that people might have anchored to some heuristic

which would make even the ‘3 visits to the garage’ to be construed as a neutral

scenario. In order to reduce this, the scenario could read as ‘the car required a lot of

maintenance and you had to take your car to the garage for several times, more than

what is required on average for a car of such make and age’. The explicit mention of

the nature of repairs being more/below the average expected levels of maintenance

for a similar car would increase the salience of both positive and negative quality

scenarios.

23

v) The questions were asked in the sequence where the first one measured Money’s

Worth, followed by Enjoyment, Replacement Time and the last one measured Selling

Price. There could have been some sort of order effects creeping in due to the nature

of the sequence. Hence, randomization of these questions could make the DV

measurements more robust.

vi) The replacement time measured in the study could have been a manifestation of the

term loan tenure. Respondents might have anchored around the remaining time for

repayment before deciding on the replacement timing. In order to reduce this

confound, the next study could have a scenario closer to the completion of repayment

schedule. For example, a scenario with a term loan tenure of 5 years while the car is

4/4.5 years old.

vii) The numbers used in the scenario might have influenced the decision making to some

extent (Price: 5.69.614/- and EMI: 8,627.08/-). The price of the car as well as the

repayment amount could be rounded off to facilitate the decision making process

(Price: 5,70,000/- and EMI: 8,600/-).

Follow-Up Studies:

The next study should incorporate all the above listed modifications. In order to make the

hypotheses more generalizable, the same study could be replicated in different product categories

like cameras. Also, to account for other intrinsic motivating factors like product characteristics

and consumer characteristics, studies should be broadly replicated in utilitarian and hedonic

durable products. Consumers characteristics have to be be accounted for. It has been documented

that tightwads are generally more attentive to the payments (Park & Mowen, 2007), exhibit

24

tighter degree of coupling (Kamleitner, Coupling : The Implicit Assumption Behind Sunk-Cost

Effect and Related Phenomena, 2008) and also differ in their replacement decisions.

Directions for Further Research:

Having established the role played by payment mechanism in the replacement decisions, several

directions for further research emerge. Some of them are listed below.

i) Snob Appeal of Higher Payments: Payments are usually associated with disutility. In

some cases, higher payments lead to higher utility due to the snob-appeal associated

with the same (Kamleitner, Cost-Benefit Associations and Financial Behavior, 2009),

(Koehler & Harvey, 2004). In such contexts, will the payment mechanism that leads

to higher coupling, increase or decrease the consumption levels? This question is

interesting because hedonic products are usually priced at a premium to give a snob-

appeal. In case of hedonic products, consumers are known to prefer a payment

mechanism that pushes the thoughts away from their mind, like in the case of a pre-

paid vacation (Prelec & Loewenstein, 1998). So, this conflicting perspectives offer a

rich avenue worth exploring further.

ii) Evaluability of Different Payment Mechanisms: One reason why different payment

mechanisms lead to different degrees of coupling is the ambiguity associated with

mapping many consumption benefits with a payment incident (Kamleitner, Cost-

Benefit Associations and Financial Behavior, 2009). The lesser the ambiguity, the

more easy it is to evaluate the worth of a consumption instance. Consumption

experience is also influenced by a reference point (Okada, 2001). If individuals are

provided with an external reference point for evaluating the consumption experience,

25

will the payment mechanism still influence the consumption behavior? Which is a

strong moderator – an external reference point or the payment mechanism?

Conclusion:

The study has made a contribution to the broad area of durable goods replacement decisions, by

providing a process-oriented approach. The mental accounting process is influenced directly by

the payment mechanism. This finding is very insightful to marketers who can use the payment

schemes to manipulate and control the replacement decisions. Also, from a firm’s perspective,

the production and planning can be managed according to the expected demand due to product

replacements.

26

Appendix

Experimental Design

Product Used – Hyundai i20 Era Car

Price of the Product – 5.69.614/-

Age of the Product – Four.

Term Loan Specifications – Loan of 5,00,000/- with a repayment tenure of 7 Years. Monthly repayments amount to 8,627.08/-

Payment Mechanism Frequency of Usage Quality of Usage

Cash High: You use your car every day for driving to your office which is 10kms from your home

Positive: You had to take your car only once to the garage in the last four years for a minor repair

Loan Low: You use your car only on weekends to go out within the city

Negative: You had to take your car to the garage atleast a couple of times in the last four years for major repairs

Scenario Description (Loan X High Frequency X Negative Quality)

Imagine you had purchased a Hyundai i20 Era car worth Rs. 5,69,614/- four years ago. You took a bank loan of Rs. 5,00,000/- with a repayment period of seven years to finance the car purchase. The Equated Monthly Installments amount to Rs. 8,627.08/-

You use your car every day for driving to your office which is 10kms from your home & you had to take your car to the garage atleast a couple of times in the last four years for major repairs

27

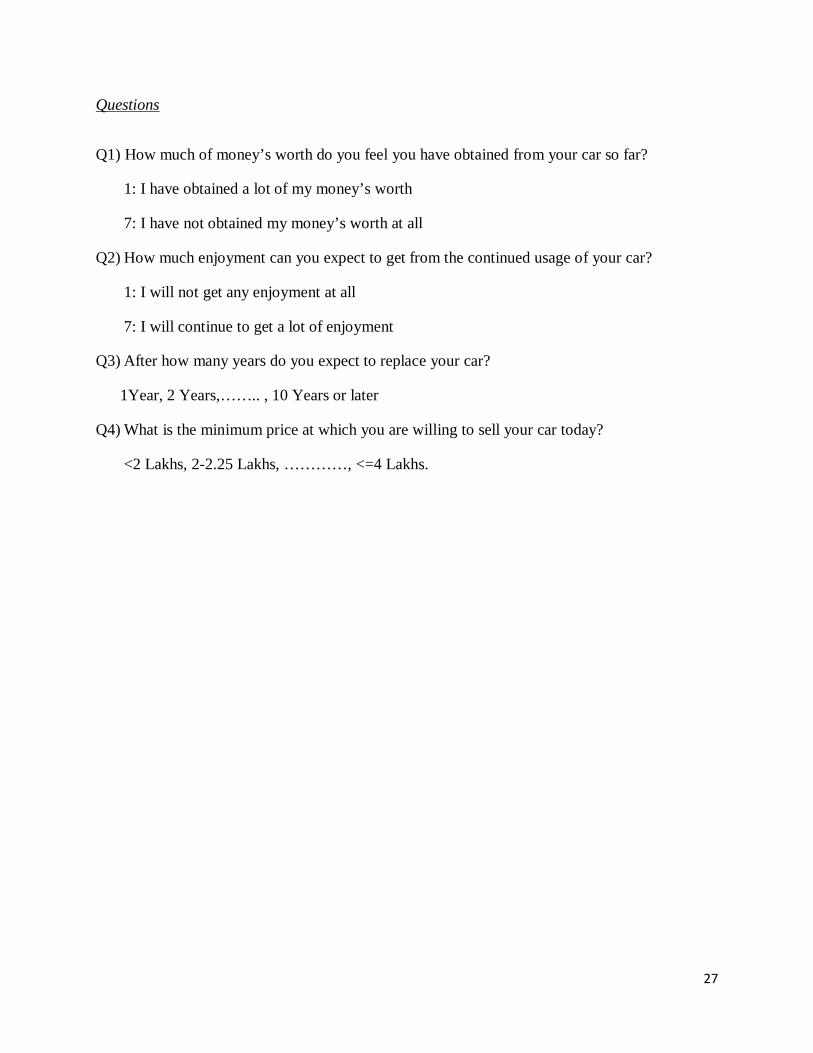

Questions

Q1) How much of money’s worth do you feel you have obtained from your car so far?

1: I have obtained a lot of my money’s worth

7: I have not obtained my money’s worth at all

Q2) How much enjoyment can you expect to get from the continued usage of your car?

1: I will not get any enjoyment at all

7: I will continue to get a lot of enjoyment

Q3) After how many years do you expect to replace your car?

1Year, 2 Years,…….. , 10 Years or later

Q4) What is the minimum price at which you are willing to sell your car today?

<2 Lakhs, 2-2.25 Lakhs, …………, <=4 Lakhs.

28

References

Arkes, H. R., & Blumer, C. (1985). The Psychology of Sunk Cost. Organizational Behavior and Human Decision Processes, 124-140.

Cripps , J. D., & Meyer, R. J. (1994). Heuristics and Biases in Timing the Replacement of Durable Products. Journal of Consumer Research, 304-318.

Gourville, J. T., & Soman, D. (1998). Payment Depreciation: The Behaioral Effects of Temporally Separating Payments from Consumption. Journal of Consumer Research, 160-174.

Grewal, R., Mehta, R., & Kardes, F. R. (2004). The Timing of Repeat Purchases of Consumer Durable Goods: The Role of Functional Bases of Consumer Attitudes. Journal of Marketing Research, 101-115.

Guiltinan, J. (2010). Consumer Durables Replacement Decision-Making: An Overview and Research Agenda. Marketing Letters, 163-174.

Heath, C., & Fennema, M. (1996). Mental Depreciation and Marginal Decision Making . Organizational Behavior and Human Decision Processes, 95-108.

Kamleitner, B. (2008, September). Coupling : The Implicit Assumption Behind Sunk-Cost Effect and Related Phenomena. Centre for Globalization Research.

Kamleitner, B. (2009). Cost-Benefit Associations and Financial Behavior. Applied Psychology, 435-452.

Koehler, D. J., & Harvey, N. (2004). Blackwell Handbook of Judgment and Decision Making. Blackwell Publishing Ltd.

Okada, E. M. (2001). Trade-Ins, Mental Accounting, and Product Replacement Decisions. Journal of Consumer Research, 433-447.

Park, S., & Mowen, J. C. (2007). Replacement Purchase Decisions: On the Effects of Trade-Ins, Hedonic versus Utilitarian Usage Goal, and Tightwadism. Journal of Consumer Behavior, 123-131.

Prelec, D., & Loewenstein, G. (1998). The Red and the Black: Mental Accounting of Savings and Debt. Marketing Science, 4-28.

Rust, J. (1987). Optimal Replacement of GMC Bus Engines: An Empirical Model of Harold Zurcher. Econometrica, 999-1033.

Soman, D., & Gourville, J. T. (2001). Transaction Decoupling : How Price Bundling Affects the Decision to Consume. Journal of Marketing Research, 30-44.

Thaler, R. (1985). Mental Accounting and Consumer Choice. Marketing Science, 199-214.

Westbrook, R. A., & Fornell, C. (1979). Patterns of Information Source Usage Among Durable Goods Buyers. Journal of Marketing Research, 303-312.