Embed Size (px)

Citation preview

Working on Schedule – II of Companies Act, 2013

©www.enrollmyexperience.com

Major Scripts• Depreciation is charged on Life basis rather than SLM & WDV

method• There will be change in policy if it is calculated on Life basis.• There is a concept of Scrap value as it was in SLM basis, its

treatment.• If the value of assets is still there then it is to be adjusted with the

retained earning.• And those assets which have the value, then they will be treated as

same as written in the act i.e. as per remaining life period.• If any assets has been purchased during the year, then it will be

treated as per pro rata basis.• If there is any asset which cannot be taken jointly into consideration

then they are to be calculated separetly.

©www.enrollmyexperience.com

Explanations

©www.enrollmyexperience.com

Policy that will change

• For change in accounting policy, provision contained in Accounting Standards-5 “NetProfit or Loss for the Period, Prior Period Items and Changes in Accounting Policies” as well as AS-6 “Depreciation Accounting” both are required to be taken into consideration.

What about the scrap value?

• It has clearly written in the act that , “after retaining the residual value, shall be recognised in the opening balance of retained earnings”, so scrap value will be retained as it is, till it is not sold.

• Ordinarily, the residual value of an asset is often insignificant but it should generally be not more than 5% of the original cost of the asset

©www.enrollmyexperience.com

If any assets is purchased during the period?

• As per the act (Note no. 2) “Where, during any financial year, any addition has been made to any asset, or where any asset has been sold, discarded, demolished or destroyed, the depreciation on such assets shall be calculated on a “pro rata basis” from the date of such addition or, as the case may be, up to the date on which such asset has been sold, discarded, demolished or destroyed.”

• It means that the calculation should be made on days basis, not on month or year basis.

If the value of assets is still there then it is to be adjusted with the retained earning

• It has clearly written in the act that , “shall be recognised in the opening balance of retained earnings where the remaining useful life of an asset is nil” and it has also been taken into consideration that if the retained earnings then it will be added to the loss value i.e. increase the loss value. As it is done with current year loss, which is added with the previous year loss.

What about assets having life remaining?

• The assets which have remaining life (as per the schedule) shall be depreciated over the remaining useful life of the asset as per this Schedule

©www.enrollmyexperience.com

For jointly held assets

• As per the Act, “Useful life specified in Part C of the Schedule is for whole of the asset. Where cost of a part of the asset is significant to total cost of the asset and useful life of that part is different from the useful life of the remaining asset, useful life of that significant part shall be determined separately.”

• So, every assets will be calculated seperately via its own nature

Schedule –II has been divided into three Parts as:

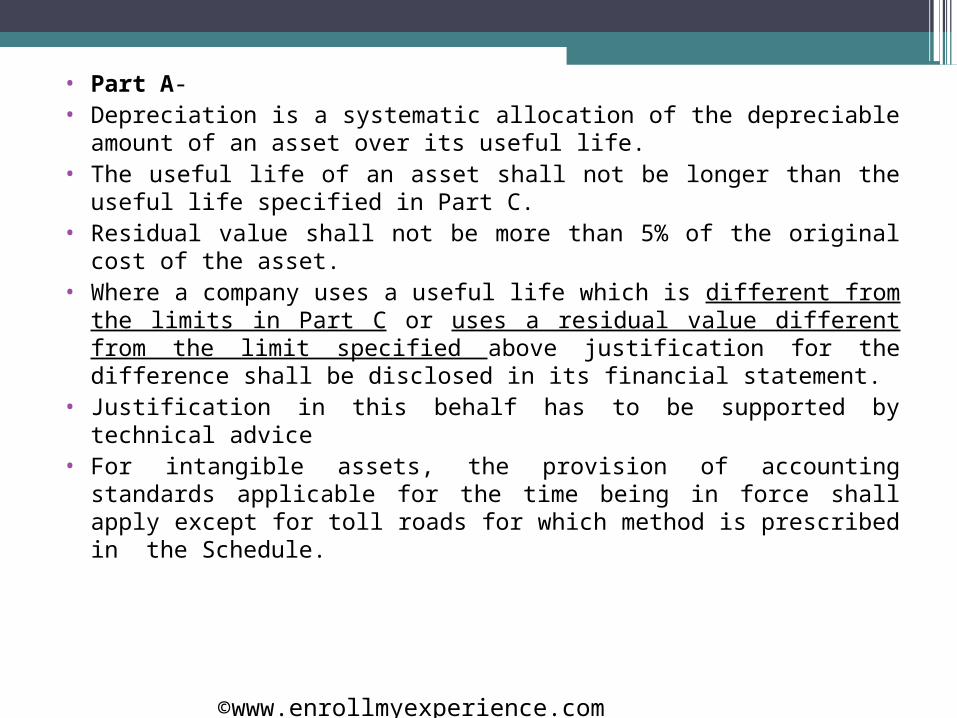

• Part A- • Depreciation is a systematic allocation of the depreciable

amount of an asset over its useful life. • The useful life of an asset shall not be longer than the useful

life specified in Part C.• Residual value shall not be more than 5% of the original cost

of the asset.• Where a company uses a useful life which is different from

the limits in Part C or uses a residual value different from the limit specified above justification for the difference shall be disclosed in its financial statement.

• Justification in this behalf has to be supported by technical advice

• For intangible assets, the provision of accounting standards applicable for the time being in force shall apply except for toll roads for which method is prescribed in the Schedule.

©www.enrollmyexperience.com

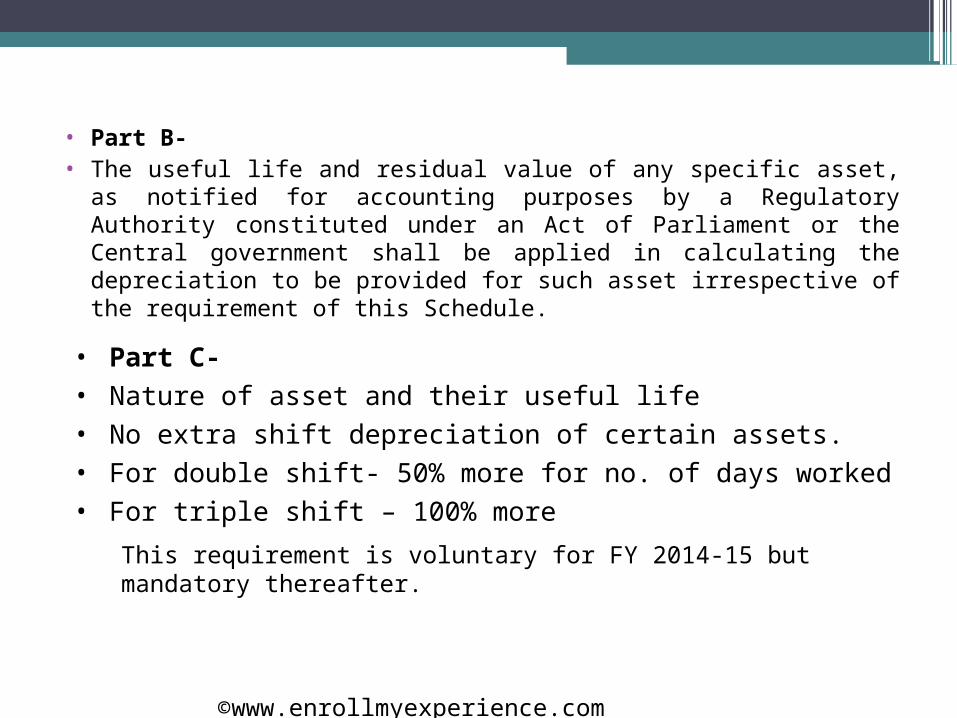

• Part B-• The useful life and residual value of any specific asset, as notified

for accounting purposes by a Regulatory Authority constituted under an Act of Parliament or the Central government shall be applied in calculating the depreciation to be provided for such asset irrespective of the requirement of this Schedule.

• Part C- • Nature of asset and their useful life• No extra shift depreciation of certain assets.• For double shift- 50% more for no. of days worked• For triple shift – 100% more

This requirement is voluntary for FY 2014-15 but mandatory thereafter.

©www.enrollmyexperience.com

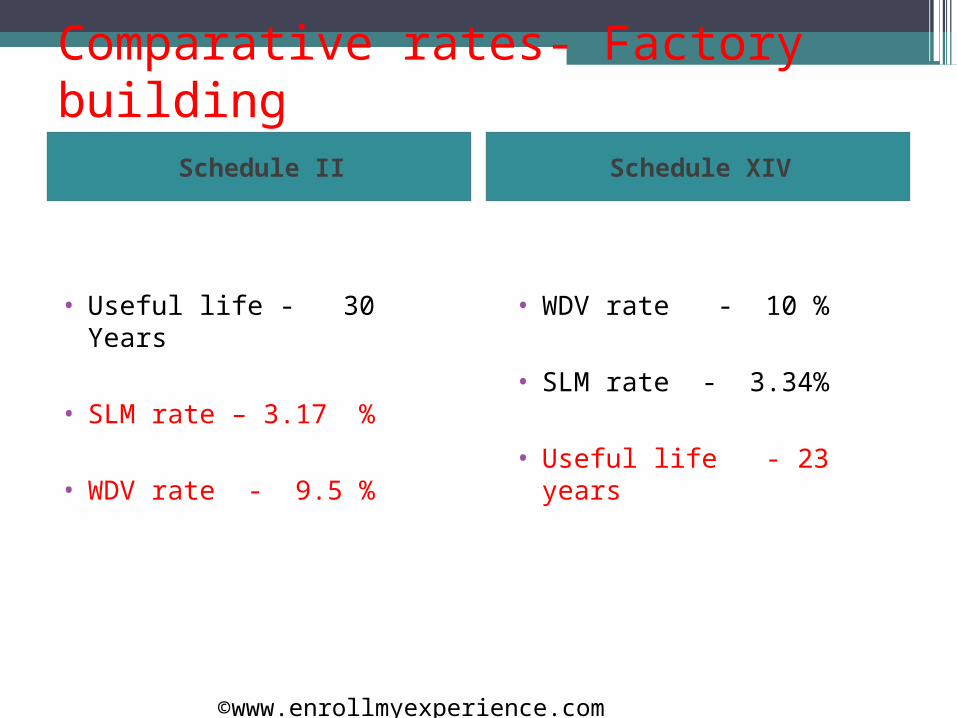

Comparative rates- Factory building

Schedule II Schedule XIV

• Useful life - 30 Years

• SLM rate – 3.17 %

• WDV rate - 9.5 %

• WDV rate - 10 %

• SLM rate - 3.34%

• Useful life - 23 years

©www.enrollmyexperience.com

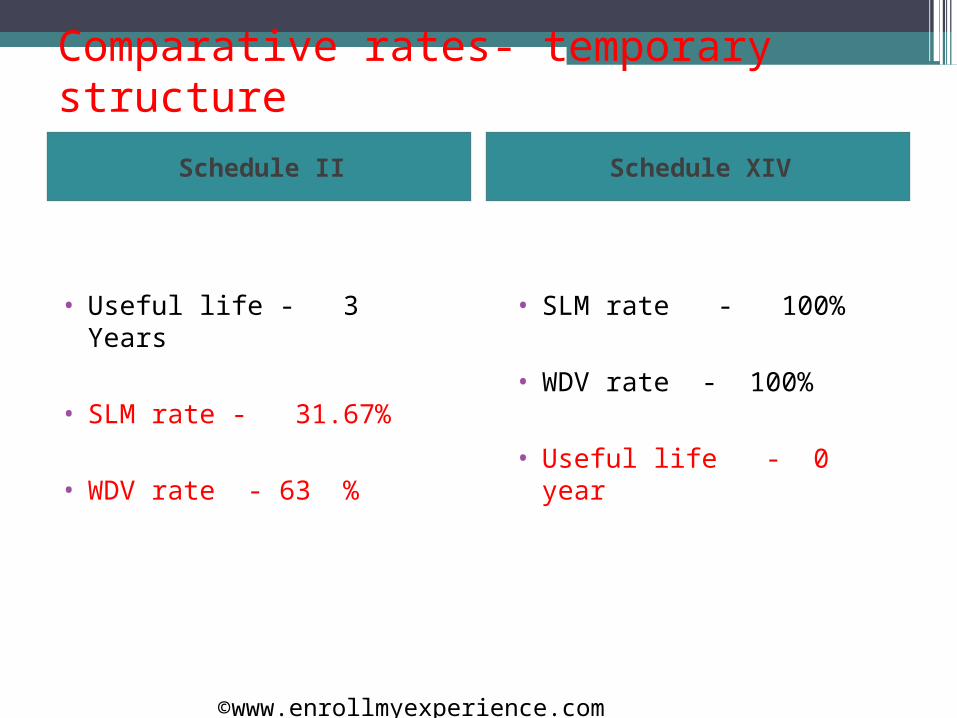

Comparative rates- temporary structure

Schedule II Schedule XIV

• Useful life - 3 Years

• SLM rate - 31.67%

• WDV rate - 63 %

• SLM rate - 100%

• WDV rate - 100%

• Useful life - 0 year

©www.enrollmyexperience.com

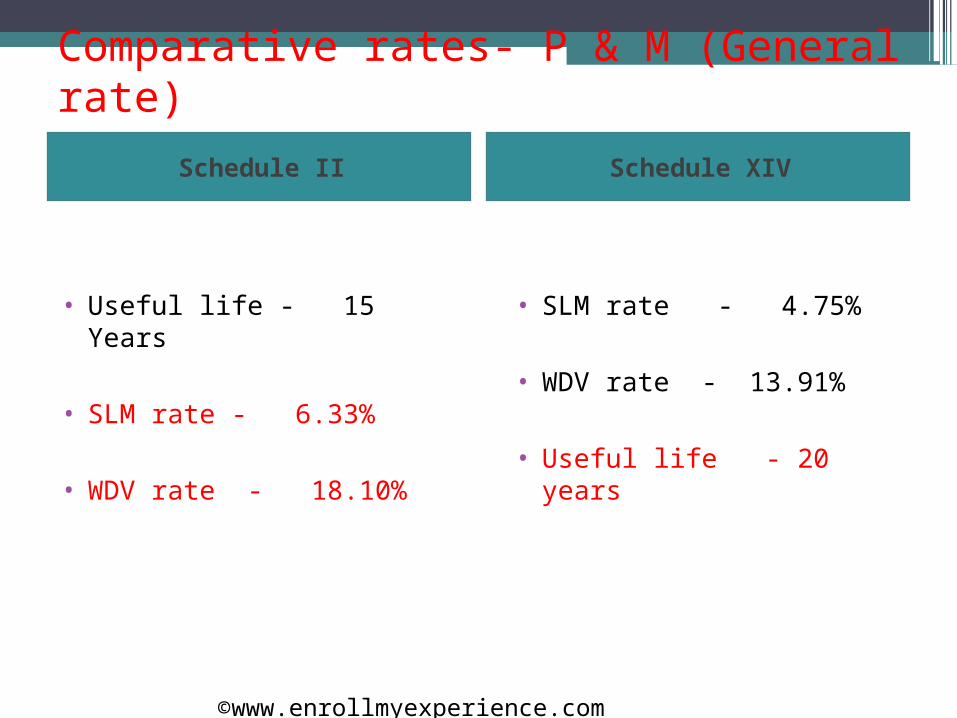

Comparative rates- P & M (General rate)

Schedule II Schedule XIV

• Useful life - 15 Years

• SLM rate - 6.33%

• WDV rate - 18.10%

• SLM rate - 4.75%

• WDV rate - 13.91%

• Useful life - 20 years

©www.enrollmyexperience.com

Some Examples

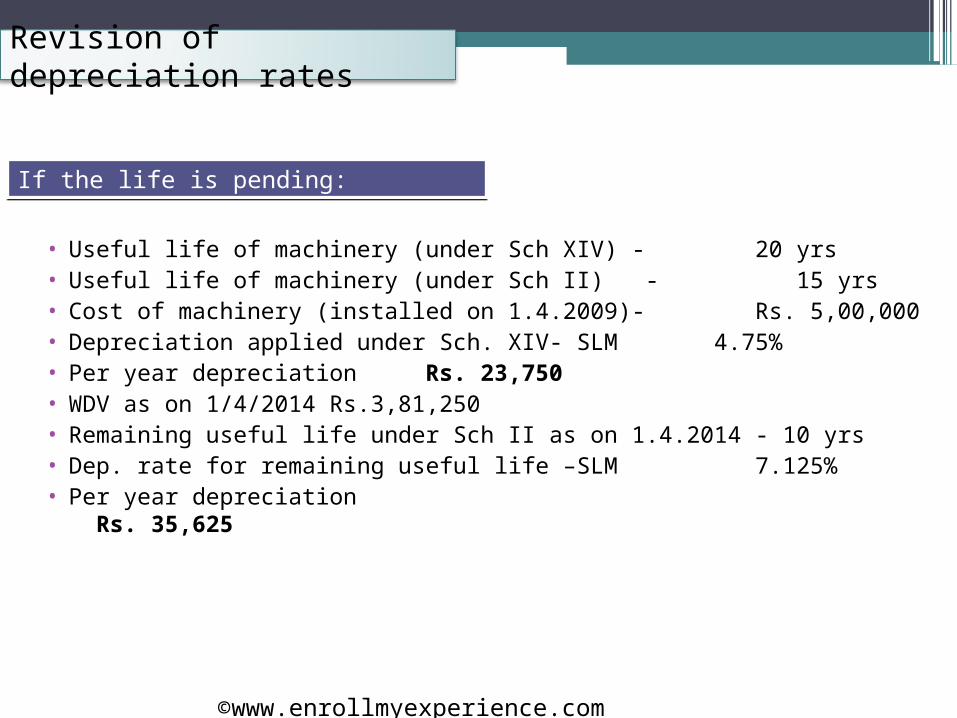

Revision of depreciation rates

• Useful life of machinery (under Sch XIV) - 20 yrs• Useful life of machinery (under Sch II) - 15 yrs• Cost of machinery (installed on 1.4.2009)- Rs. 5,00,000• Depreciation applied under Sch. XIV- SLM 4.75%• Per year depreciation Rs. 23,750• WDV as on 1/4/2014 Rs.3,81,250• Remaining useful life under Sch II as on 1.4.2014 - 10 yrs• Dep. rate for remaining useful life –SLM 7.125%• Per year depreciation Rs. 35,625

If the life is pending:If the life is pending:

©www.enrollmyexperience.com

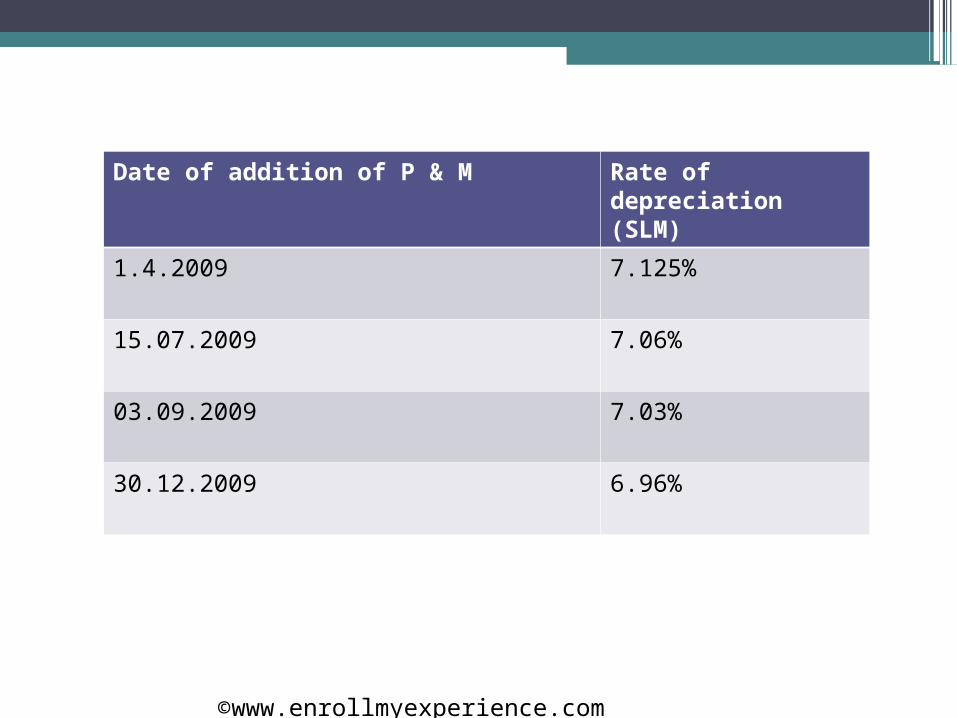

Date of addition of P & M Rate of depreciation(SLM)

1.4.2009 7.125%

15.07.2009 7.06%

03.09.2009 7.03%

30.12.2009 6.96%

©www.enrollmyexperience.com

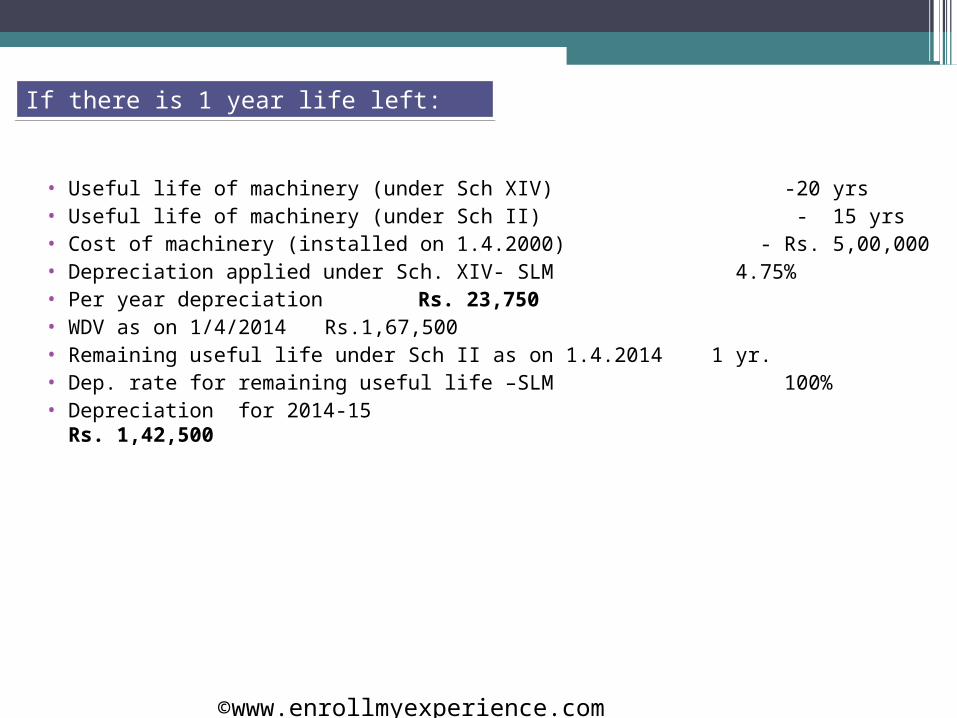

• Useful life of machinery (under Sch XIV) -20 yrs• Useful life of machinery (under Sch II) - 15 yrs• Cost of machinery (installed on 1.4.2000) - Rs. 5,00,000• Depreciation applied under Sch. XIV- SLM 4.75%• Per year depreciation Rs. 23,750• WDV as on 1/4/2014 Rs.1,67,500• Remaining useful life under Sch II as on 1.4.2014 1 yr.• Dep. rate for remaining useful life –SLM 100%• Depreciation for 2014-15 Rs. 1,42,500

If there is 1 year life left:If there is 1 year life left:

©www.enrollmyexperience.com

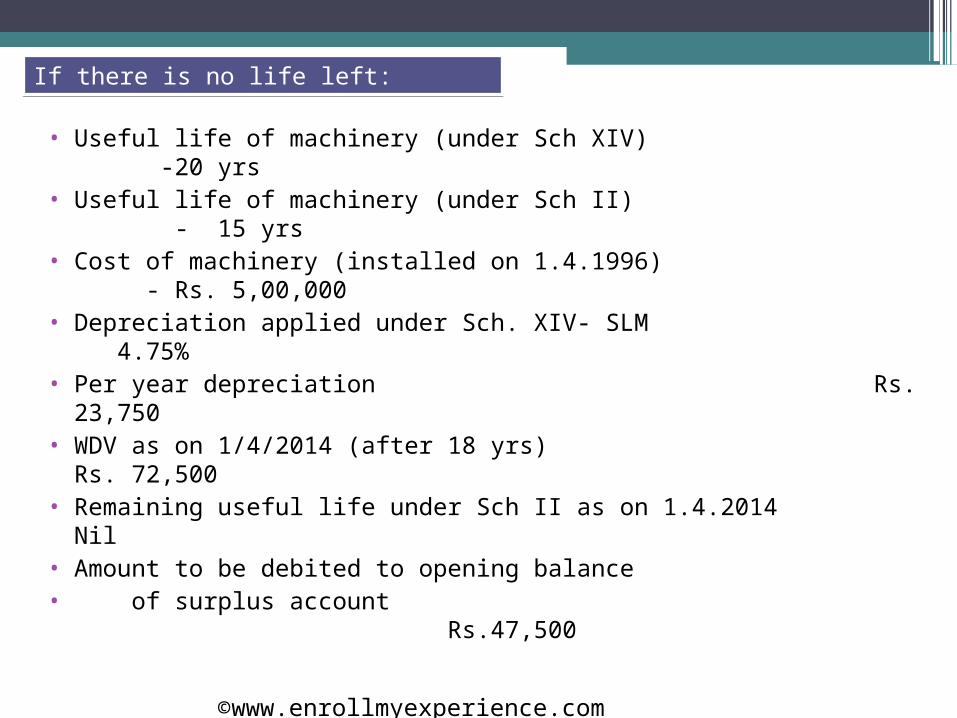

• Useful life of machinery (under Sch XIV) -20 yrs• Useful life of machinery (under Sch II) - 15 yrs• Cost of machinery (installed on 1.4.1996) - Rs. 5,00,000• Depreciation applied under Sch. XIV- SLM 4.75%• Per year depreciation Rs. 23,750• WDV as on 1/4/2014 (after 18 yrs) Rs. 72,500• Remaining useful life under Sch II as on 1.4.2014 Nil• Amount to be debited to opening balance • of surplus account

Rs.47,500

If there is no life left:If there is no life left:

©www.enrollmyexperience.com

![PRIVATE GUARD COMPANIES ACT - PLAClawsofnigeria.placng.org/laws/P30.pdf · in the Schedule to this Act. [Schedule. Form A.] (2) The Minister may, before considering any such application,](https://img.pdfslide.us/doc/110x75/60258527ed67a27ab111fcc7/private-guard-companies-act-in-the-schedule-to-this-act-schedule-form-a-2.jpg)