Embed Size (px)

Citation preview

WORKING DRAFT

Last Modified 19.05.2011 10:06:16 W. Europe Standard Time

Printed 18.05.2011 17:17:00 W. Europe Standard Time

VGI-AAA123-20101217-

May 19th, 2011

CONFIDENTIAL AND PROPRIETARY

Any use of this material without specific permission of McKinsey & Company is strictly prohibited

EyeForTransport

2nd horizontal collaboration

in the supply chain summit

Conference

McKinsey & Company

This presentation aims to inform individual decisions Disclaimer

SOURCE: McKinsey

▪ This presentation aims to provide an objective framework for assessing

horizontal collaboration opportunities in logistics. The outlined ideas for a

formal collaboration of industry players are preliminary. They are based

on the hypothesis such collaboration would enhance overall market

efficiency and benefit consumers/counterparties

▪ Companies and decision-makers need to assess the validity of the

frameworks and arguments individually and take business decisions

individually as appropriate in the specific business context

▪ Such collaboration would very likely have significant legal implications,

e.g., with regards to anti-trust conformity. Companies should assess such

implications individually and take appropriate steps to ensure company

action is in line with the relevant legal framework and regulations

▪ Any use of this material without specific permission of McKinsey &

Company is strictly prohibited

McKinsey & Company

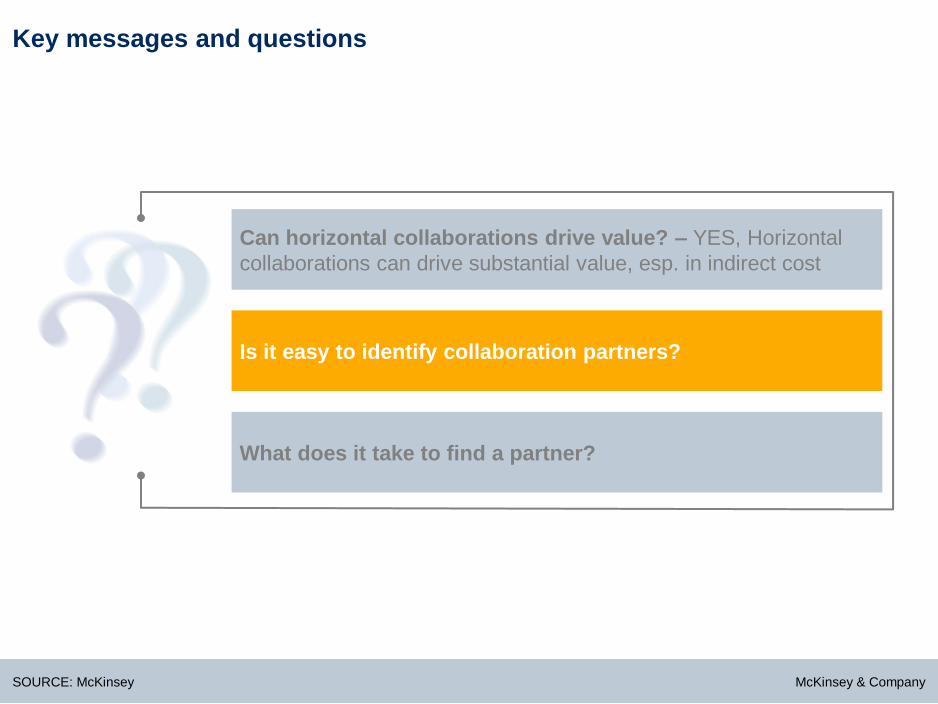

Key messages and questions

Is it easy to identify collaboration partners?

Can horizontal collaborations drive value?

What does it take to find a partner?

SOURCE: McKinsey

McKinsey & Company

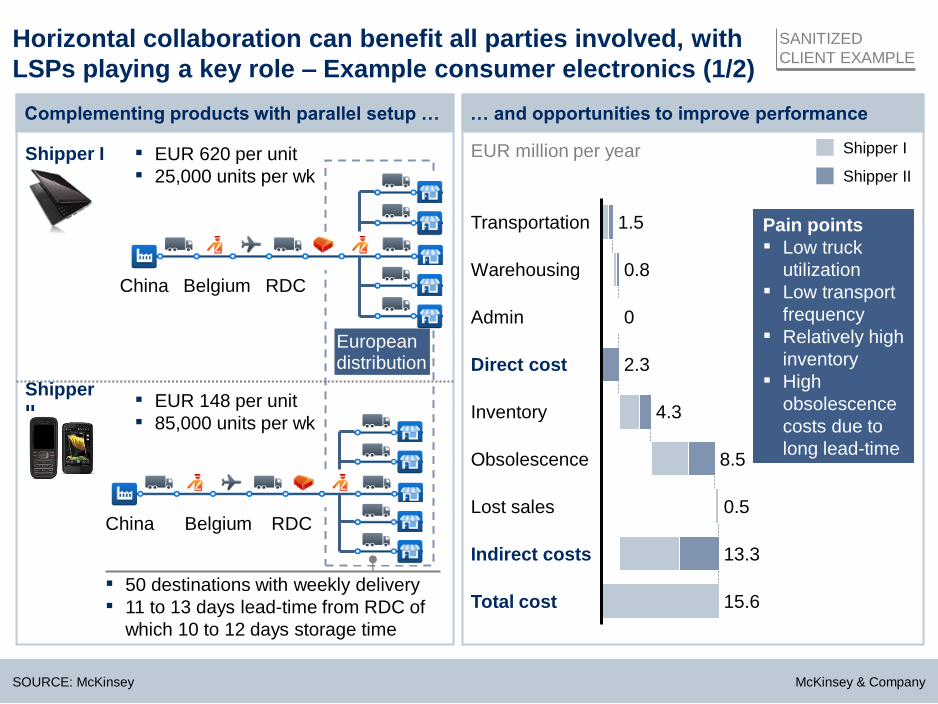

Horizontal collaboration can benefit all parties involved, with

LSPs playing a key role – Example consumer electronics (1/2)

Shipper I

Complementing products with parallel setup … … and opportunities to improve performance

▪ EUR 620 per unit

▪ 25,000 units per wk

China Belgium RDC

Total cost 15.6

Indirect costs 13.3

Lost sales 0.5

Obsolescence 8.5

Inventory 4.3

Direct cost 2.3

Admin 0

Warehousing 0.8

Transportation 1.5

Shipper I

Shipper II

EUR million per year

Shipper

II ▪ EUR 148 per unit

▪ 85,000 units per wk

China Belgium RDC

European distribution

▪ 50 destinations with weekly delivery

▪ 11 to 13 days lead-time from RDC of

which 10 to 12 days storage time

Pain points

▪ Low truck

utilization

▪ Low transport

frequency

▪ Relatively high

inventory

▪ High

obsolescence

costs due to

long lead-time

SANITIZED

CLIENT EXAMPLE

SOURCE: McKinsey

McKinsey & Company

Horizontal collaboration can benefit all parties involved, with

LSPs playing a key role – Example consumer electronics (2/2)

LSP serves Shipper I and II

Total cost 4.5

Indirect costs 4.1

Lost sales 0.3

Obsolescence 2.3

Inventory 1.5

Direct cost 0.4

Admin 0

Warehousing 0

Transportation 0.4

Savings

Shipper I: 30%

Shipper II: 22%

Collaborative set-up improves service level performance resulting in major savings for both parties

Shipper I Shipper II

▪ Lower transport costs due

to higher truck utilization

▪ Double delivery frequency

enabling decrease of

storage time and costs

▪ Optimize inventory levels

enabled by increased

delivery frequency

▪ Reduce obsolescence by

speeding up supply chain

(decrease storage time)

▪ Avoid lost-sales where

possible

Savings

EUR million per year

SANITIZED

CLIENT EXAMPLE

SOURCE: McKinsey

McKinsey & Company

Key messages and questions

Is it easy to identify collaboration partners?

Can horizontal collaborations drive value? – YES, Horizontal

collaborations can drive substantial value, esp. in indirect cost

What does it take to find a partner?

SOURCE: McKinsey

McKinsey & Company

A structured approach can help to maximize the chances

of finding the right collaboration opportunity and partner

Key barriers to horizontal

collaboration

Lack of widespread acceptance

Difficulty to

establish

trust-based

relationships

Difficulty to

finding appro-

priate partner

Fear of information disclosure

No IT

infrastructure/

support

Lack of clarity

who in charge

Designing the solution Building the case Implementation

What could the optimal solution look like?

How best to practically implement?

How best to maintain col-laboration?

I II III

A B A B A B

Typical implementation and

maintenance challenges

mentioned by less than 25%

of respondents

2 - 3 weeks 6 - 8 weeks 12+ weeks Continuous

What is the baseline and the size of the opportunity?

What is your horizontal collaboration model/thrust?

Who are the best partners?

Focus of today’s

discussion

SOURCE: McKinsey

McKinsey & Company

For shippers – 3 major options for collaboration models and

roles within

SOURCE: McKinsey

Convened

collaboration

"Primus inter

pares"

collaboration

"Inter pares"

collaboration

31% of shippers

without own

capabilities to

orchestrate

Critical

mass/

capability

already

reached

Want to

drive

collabora-

tion

Own

ability to

orchestrate

collabora-

tion

Yes Yes

No

No

No

Yes ▪ 23% of shippers who

would act as organiser

High-level decision logic

▪ Envirotainer

▪ Chep

▪ Credit cards

▪ Tall-EX

▪ Cat

Logistics

▪ Carrefour

Example Characteristics

▪ Industry platforms

mostly organized by

neutral party outside

core activity, e.g.,

3PL

▪ Large player with

sufficient critical

scale offer existing

network to smaller

competitors or

complementary

product shippers

▪ Group of players

with subcritical but

typically similar

sized operations

consolidate exist-

ing or set-up new

joined activities

▪ Pharma

Log

McKinsey & Company

Who participated in the survey?

38

25

36

Other

LSP

Shipper

What best describes your current business model?

SOURCE: McKinsey, EFT 2010/2011

28

25

47

2010 survey 2011 survey

McKinsey & Company

2010 survey 2011 survey

The preferred collaboration model changed from inter-pares in 2010 to

convened collaboration in 2011 What best describes in general your preferred collaboration model?, in %

31

16

11

11

18

13

Inter-pares collaboration –

initiator

Inter-pares collaboration –

member

Primus inter-pares

collaboration – primus

Primus-inter-pares

collaboration –member

Convened collaboration –

convener

Convened collaboration –

member

19

6

19

3

25

28

SOURCE: McKinsey, EFT 2010/2011

McKinsey & Company

Especially for inter-pares collaboration agreeing on the collaboration

depth is important

SOURCE: McKinsey

Joint distributor

▪ Owning inventory

▪ Comprehensive logistics

management

Low

Coverage of logistics value chain

High

Low

Inte

nsit

y/n

on

-reve

rsib

ilit

y o

f

co

llab

ora

tio

n c

om

mit

men

t

High

JV/Carve-out into own

logistics service operator

▪ Own assets

▪ Shared information services

(esp. Order management,

forecasting, demand planning)

Joint logistics management

▪ Transport management

▪ Warehouse management

Joint procurement of

commodity services

▪ Esp. Transport

▪ Warehousing

McKinsey & Company

We learned that most participants are interested in joint logistics

management

13

21

48

18

Joint distributor, i.e., owning

inventory, owning operations, …

JV/Carve-out into own

logistics service operator

with own services, shared

information, …

Joint logistics management

(e.g., transport management,

warehouse management, …)

Joint procurement of single

commodity services (esp.

Trucking, warehousing, …)

What best describes your preferred depth of collaboration?, in

%

6

9

53

31

2010 survey 2011 survey

SOURCE: McKinsey, EFT 2010/2011

McKinsey & Company

Identification of partners requires screening from different lenses

SOURCE: McKinsey

Commonality of supply chain lenses (assessing potential for scale advantages

and a positive business case)

Other lenses

Supply chain segment lense ▪ What part of the supply

chain needs to be covered, e.g., inbound, outbound, distribution, reverse?

Geographic overlap lense ▪ What distribution/

warehousing footprint? ▪ What trade-lane set-up?

Supply chain needs lense ▪ What requirements in

terms of speed, reliability and flexibility?

Product characteristics lense ▪ What special handling

requirements? ▪ What licensing/

auditing needs?

Objective lenses ▪ What benefits/

capabilities needs the partner to bring, e.g., volume, skill, market access, financing clout, ..?

Industry conduct lense ▪ Possibility/feasibi-

lity to collaborate with competitors?

KPI lense ▪ Shared success

measures across financial, operational, and consumer-based dimensions?

People lense ▪ Common agenda and

joint willingness to make it happen?

▪ Mutual trust?

McKinsey & Company

2011 survey

The biggest opportunities on inbound lanes are expected from China into

Europe…

…Eastern Europe and Russia

…Africa

…India

…South East Asia (incl. Australia)

… Japan/Korea

… China

…North America

…South America

For which of the following inbound lanes would you expect the best collaboration opportunities, in %

SOURCE: McKinsey, EFT 2011

Into Europe from…

3

3

34

3

6

3

6

42

McKinsey & Company

…and on outbound lanes from Europe into Eastern Europe and Russia For which of the following outbound lanes would you expect the best collaboration opportunities, in %

SOURCE: McKinsey, EFT 2010/2011

2010 survey 2011 survey

2

15

46

15

0

6

2

13

…South America

…North America

…Eastern Europe and Russia

…Africa

…India

…South East Asia (incl. Australia)

… Japan/Korea

… China

From Europe into…

13

25

50

6

0

0

0

6

McKinsey & Company

2010 survey 2011 survey

Overall, best collaboration opportunities in distribution are expected for

Benelux

29

10

10

16

17

3

14

Eastern Europe (Poland,

Czech Rep., …)

South Eastern Europe

(Italy, Greece, Croatia, …)

South-Western Europe

(France, Iberia)

Central (Germany,

Austria, Switzerland)

Benelux

Nordics

UK/Ireland

For which of the following distribution regions would you expect the best collaboration opportunities?, in %

SOURCE: McKinsey, EFT 2010/2011

16

13

22

16

28

0

6

McKinsey & Company

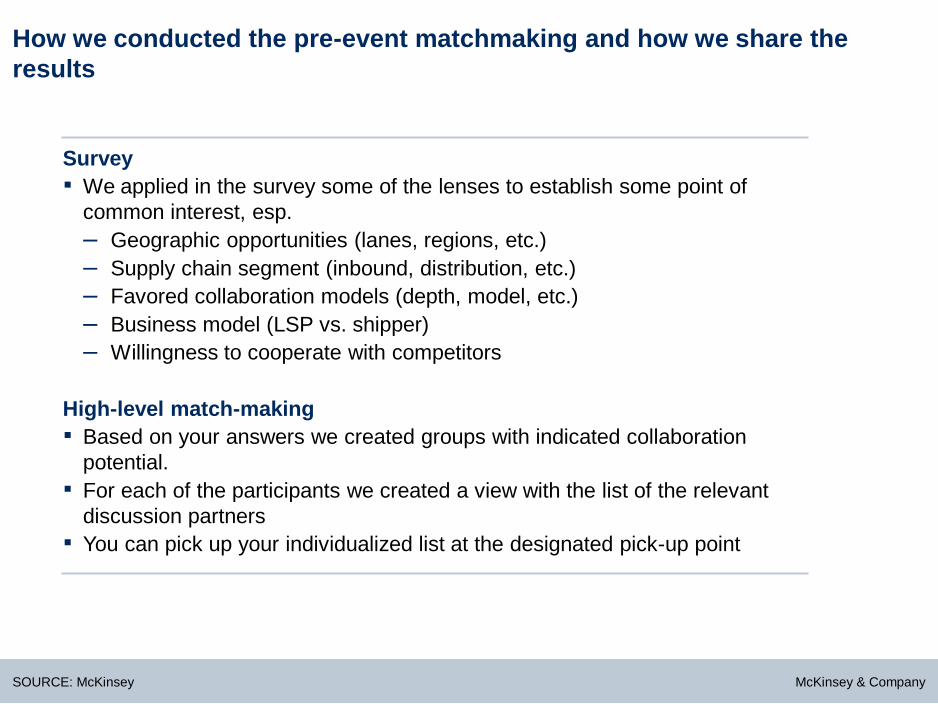

How we conducted the pre-event matchmaking and how we share the

results

SOURCE: McKinsey

Survey

▪ We applied in the survey some of the lenses to establish some point of

common interest, esp.

– Geographic opportunities (lanes, regions, etc.)

– Supply chain segment (inbound, distribution, etc.)

– Favored collaboration models (depth, model, etc.)

– Business model (LSP vs. shipper)

– Willingness to cooperate with competitors

High-level match-making

▪ Based on your answers we created groups with indicated collaboration

potential.

▪ For each of the participants we created a view with the list of the relevant

discussion partners

▪ You can pick up your individualized list at the designated pick-up point

McKinsey & Company

Key messages and questions

Is it easy to identify collaboration partners? – NO, but with a

fact-based systematic approach it can be done with limited effort

Can horizontal collaborations drive value? – YES, Horizontal

collaborations can drive substantial value, esp. in indirect cost

What does it take to find a partner – WELL, Let's find out!

SOURCE: McKinsey

EXAMPLES

McKinsey & Company

The case comprises a setup of shippers and LSPs being active in three

regions with two products

SOURCE: McKinsey

Region North Region South Region West

Case description

▪ The market consists of 3

regions and 2 products

▪ There are 3 shippers active

in this market

▪ 2 LSPs are offering

services in this market

Product A

Product B

1 2 3

1 2

LSP 1

LSP 2

LSP 1

LSP 2

LSP 2 Shipper 1

Shipper 2

LSP 1 Shipper 1

Shipper 1

Shipper 1

Shipper 2

Shipper 3 LSP 1

LSP 2

LSP 1

LSP 2 Shipper 1

Shipper 3

Shipper 1

McKinsey & Company

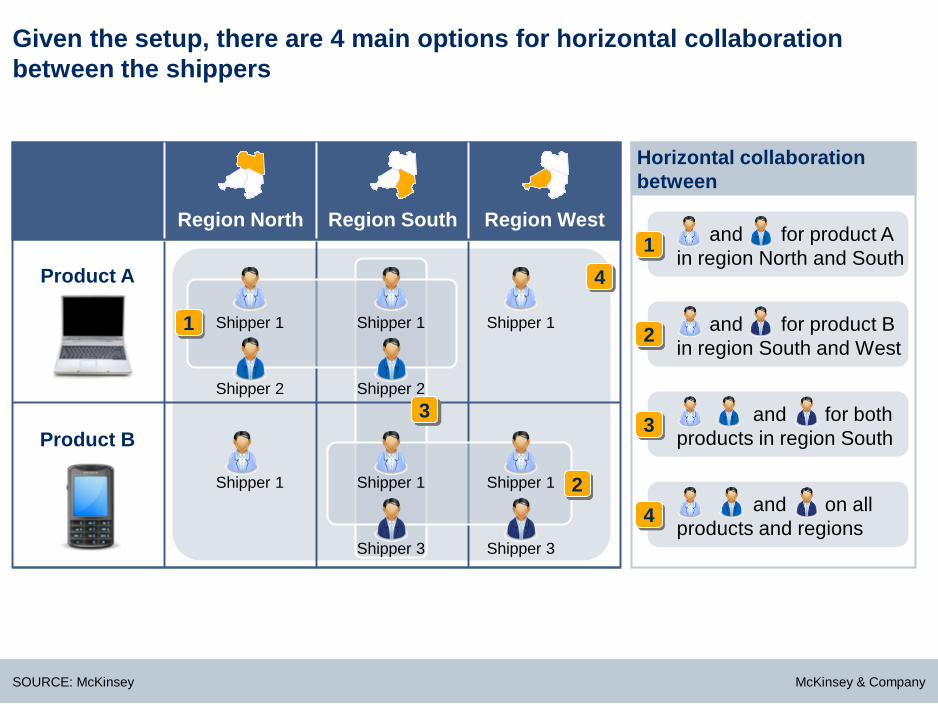

Region North Region South Region West

Given the setup, there are 4 main options for horizontal collaboration

between the shippers

SOURCE: McKinsey

Horizontal collaboration

between

for product A

in region North and South

and 1

for product B

in region South and West

and 2

for both

products in region South

and 3

on all

products and regions

and 4

Product A 4

1

Product B

2

3

Shipper 1

Shipper 2

Shipper 1

Shipper 2

Shipper 1

Shipper 1 Shipper 1

Shipper 3

Shipper 1

Shipper 3

McKinsey & Company

It is your task now to find the collaboration model which creates the

most value

SOURCE: McKinsey

1. Please gather in groups of 5

Each group will receive an envelope with a role

card for each of the players, i.e. three shippers and

two LSPs

Each briefing note contains a negotiation mandate

from your board and some additional information

You have 20 minutes to sign a final agreement

Once you are done, please let us know your results

and place the contracts back into the team

envelope

5.

4.

2.

3.

McKinsey & Company

Collaboration

option

Gain share

for LSP

Contract template horizontal collaboration

SOURCE: McKinsey

LSP partner LSP 1 LSP 2

No Yes – 5%

Gain share

for shipper Equal By volume

Signature

shipper 1

Signature

shipper 2

Signature

shipper 3

Signature

LSP 1

Signature

LSP 2

McKinsey & Company

Contract template price discount

SOURCE: McKinsey

Signature

shipper 1

Signature

shipper 2

Signature

shipper 3

Signature

LSP 1

Signature

LSP 2

Region North Region South Region West

Product A

Product B

Shipper 1

Shipper 2

Shipper 3

Shipper 1

V:

P:

V:

P:

V:

P:

–

V:

P:

V:

P:

V:

P:

V:

P:

V:

P:

–

V:

P:

V:

P:

Fill the results for volume and price1 negotiations and sign the contract V = Volume in units/week

P = Price in USD

1 Current price laptop: USD 0,77; current price mobile phones: USD 0,30

McKinsey & Company

Let‘s see, what you settled for?

SOURCE: McKinsey

Group 1-

Only volume

information

Group 2-

LSP 1

advantage

Group 3-

Full

transparency

Shipper 1 Shipper 2 Shipper 3 LSP 2 LSP 1

Business

case for

shippers

and own

Business

case for

shippers

and own

Own

business

case

Own

business

case

Own

business

case

Business

case for

all

Business

case for

all

Business

case for

all

Own

Business

case

Own

volumes

and costs

Own

volumes

and costs

Own

volumes

and costs

McKinsey & Company

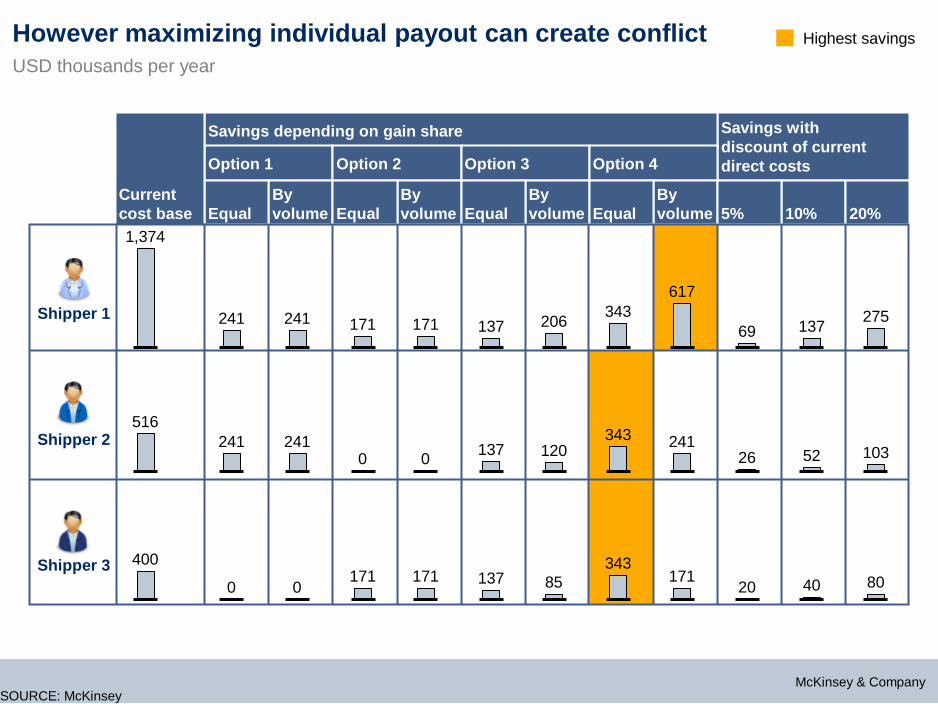

Collaboration amongst all players drives the highest savings

400

300

500

1,000

Total logistics costs savings in USD thsd

SOURCE: McKinsey

McKinsey & Company

All parties involved benefit from horizontal collaboration

Horizontal collaboration model

Transportation 160

196

Admin 1

Warehousing 35

Total cost 1,027

Indirect costs 831

Lost sales 1

Obsolescence 385

Inventory 445

Direct cost

Savings

Shipper I: 45%

Shipper II: 47%

Shipper III: 43%

Collaborative set-up improves service level performance resulting in major savings for all parties

▪ Lower transport costs due

to higher truck utilization

▪ Double delivery frequency

enabling decrease of

storage time and costs

▪ Optimize inventory levels

enabled by increased

delivery frequency

▪ Reduce obsolescence by

speeding up supply chain

(decrease storage time)

▪ Avoid lost-sales where

possible

Savings

EUR thousand per year OPTION 4

Shipper 1

Shipper 2

Shipper 3

SOURCE: McKinsey

McKinsey & Company

Option 2 Option 3 Option 1 Option 4

Savings with

discount of current

direct costs

Savings depending on gain share

Equal

By

volume Equal

By

volume Equal

By

volume Equal

By

volume 5% 10% 20%

Current

cost base

However maximizing individual payout can create conflict

SOURCE: McKinsey

Shipper 1

USD thousands per year

Highest savings

Shipper 2

Shipper 3

1,374

400

516

241

0

241

241

0

241

171

171

0

171

171

0

137

137

137

206

85

120

343

343

343

617

171

241

69

20

26

137

40

52

275

80

103

McKinsey & Company

LSPs need to win collaborations and ideally participate in gain share,

otherwise substantial profit erosion

SOURCE: McKinsey

Profit in USD thousands per year1 Highest savings

Horizontal collaboration

Option 1 Option 2 Option 3 Option 4

Lose

business

Win

horizontal

collaboration

Propose

horizontal

collaboration

12

17

65

8

18

59

10

18

59

0

20

123

Discount on

contract:

15

14

13

5%

10%

15%

1 Current profit USD 16k

McKinsey & Company

Your collaborations

SOURCE: EFT horizontal collaboration survey January 2010; McKinsey analysis

Group 1-

Only volume

information

Value of 500k

Group 2- Only

own savings

potential

Group 3-

Full business

cases

Value of 300k Value of 400k Value of 1000k

1

1

1

1

1

1

1

1

1

1

1

1

1

1

1

1

1

1

1

1

1

1

1

1

w/ LSP 1

w/ LSP 2

McKinsey & Company

PharmLog is a successful industry platform joint venture

SOURCE: PharmLog Web site; McKinsey

Business model

Joint distribution

system of different

pharma companies

1 Low revenue as medication is not owned by Pharmlog; pure logistics revenue

2 Umsatzrendite

3 Depending on collaboration partner (statement PharmLog)

Collaboration partners

▪ Boehringer

Ingelheim

▪ Merck

▪ Novartis

▪ Schering

▪ SmithKline

Beecham

▪ Viatris

▪ Novartis

▪ AWD Pharma

▪ Novo Nordisk

▪ Others (6)

Further users

▪ EUR 30.4 m1

Key data

(2008)

▪ 0.13%2

Profitability

▪ 236

Employees

▪ 4.75 bn

Packages

▪ 20 - 30%3

Savings

6 collaboration

partners and 9

further users

1 distribution

center – up to 1

million packaging

units per day

Revenues

McKinsey & Company

5

20

12

21

13

46

100

54

29

Total cost

Indirect costs

Obsolescence

Inventory

Lost sales

Direct cost

Administration

Warehousing

Transportation

Value creation goes beyond simple direct cost and efficiency gains

SOURCE: McKinsey

Cost items impacted by horizontal

collaboration

Percent of total value (PC hardware example)

Savings

potential Value levers

▪ Merge truckloads

▪ Redesign network

▪ Decrease storage

▪ Increase capacity utilization

▪ Share information

▪ Optimize demand planning

Reduce stock-outs by

increased frequencies

Optimize by higher frequency

and quicker supply chain

Reduce by quicker supply

chain

Additional benefits

▪ Higher revenues through possibility to

service far flung places

▪ Substantially reduced CO2 emissions

McKinsey & Company

Volume information

SOURCE: McKinsey

GROUP 1+2+3

Shippers and LSPs

Average shipment units/week

Product A

Product B

Region South Region West Region North

1,000

5,000

5,000

1,000

1,000

5,000

1,000

1,000

5,000

5,000

Shipper 1

Shipper 2

Shipper 3

Shipper 1

LSP 1

LSP 2

LSP 1

LSP 2

LSP 2

LSP 1 LSP 2 LSP 2

LSP 1 LSP 1

McKinsey & Company

For shippers – Evaluation of collaboration models

SOURCE: McKinsey

Convened

collaboration

▪ Potentially limited transparency on

direct cost efficiency gains (closed

book)

▪ Additional financing of 3PL margin

▪ Little opportunity to influence the

collaboration model/governance

▪ No disclosure of confidential

information to competitors (3PL acts

as neutral intermediary)

▪ Less effort for shipper in organizing

and carrying out collaboration (clear

governance of convener)

▪ No laborious partner search

Co

llab

ora

tive c

om

ple

xit

y

Pros Cons

"Primus inter

pares"

collaboration

▪ Clear alignment on who is in charge

to make collaboration successful

(Primus inter pares)

▪ Potentially large gains for smaller

shippers due to already existent

scale

▪ Little opportunity for smaller shippers

to influence the collaboration model

▪ Potentially limited transparency on

improvements and no guarantee for

"small" shipper to capture the full benefit

▪ High dependency on "primus" for all

smaller shippers to make collaboration

work

▪ Full transparency on cost

improvements

▪ Opportunity to draft fair gain sharing

model providing the full collaboration

benefit to each participant

▪ Disclosure of potentially confident

information to partners

▪ Calls for relatively high expertise on

orchestration and implementation of

collaborations

▪ Buildup of proper governance requires

substantial resources

"Inter pares"

collaboration