Embed Size (px)

Citation preview

WORKING CAPITAL MANAGEMENT EFFICIENCY OF SUGAR

FACTORIES IN ANDHRA PRADESH: A CASE STUDY OF SELECT

SUGAR FACTORIES IN CHITTOOR DISTRICT

*Dr .D.VENKATESH

Assistant Professor, Department of Commerce,

Besant Theosophical College, Madanapalle.

**Prof. M.VENKATESWARLU

Professor, Dept. of Commerce, S V University, Tirupati.

ABSTRACT

Sugar cane is an important commercial crop in India. More than 45 million sugar-cane

farmers and large mass of agricultural laborers involved in sugar-cane cultivation and harvesting

are dependent on the performance of sugar industry in India. Management of working capital

performs a very vital part in the performance of firms in sugar industry. Working capital is the

foundation stone of the business. When a business is started, the owners and investors contribute

this capital. The ultimate objective of any firm is to optimize, if not maximize, the wealth of the

shareholders. In order to do this, a firm should earn a suitable return from its operations. In order

to earn sufficient returns, the firm should be able to generate sufficient sales. This requires

adequate investment in current assets because all the sales do not get converted into cash

immediately. The researcher has made an attempt to examine this study focus on working

capital management efficiency of select sugar factories in Chittoor district.

Key Words: Sugar cane, Working Capital, Sufficient Returns and Sugar Factory.

Introduction

Working capital is the foundation stone of the business. When a business is started, the

owners and investors contribute this capital. This capital is then invested in the long term assets

such as land, building, plant and machinery. These fixed assets are of no use unless they are put

to use. The capital, it makes the fixed assets work, is called the working capital. Fixed assets are

like computer hardware, whereas working capital is like computer software. Hardware is dead

without the software; similarly, long-term assets of the business are of no use if there is no

working capital. Working capital is that minimum amount which is always there in a business,

International Journal of Research

Volume VIII, Issue VI, JUNE/2019

ISSN NO:2236-6124

Page No:3599

that is used to meet payments as and when they become due, and is used to avoid technical

insolvency arising out of non-payment of routine bills1.

The ultimate objective of any firm is to optimize, if not maximize, the wealth of the

shareholders. In order to do this, a firm should earn a suitable return from its operations. In order

to earn sufficient returns, the firm should be able to generate sufficient sales. This requires

adequate investment in current assets because all the sales do not get converted into cash

immediately2. The need for working capital arises due to time gap between production and

realization of cash from sales. There is an operating cycle involved in sales and realisation of

cash. There are time gaps in purchase of raw materials and production, production and sales, and

sales and realization of cash.

Objective:

The present study aims to appraise the working capital management efficiency of the

select sugar factories in Chittoor District.

Review of Literature

Dr.R.Gowri (2015), in her article “A Study on Impact of Working Capital Management

on Profitability with Reference to Sugar Companies in Tamil Nadu” analysed that sugar

companies are facing many financial problems. Most of the sugar companies are operationally

viable but are suffering from lack of proper management of working capital. Hence, it is the need

to analyse the impact of working capital management on profitability and improve its firm’s

growth opportunities and return to shareholders. Therefore, the study was made as an attempt to

analyse the impact of WCM on profitability of sugar companies in Tamil Nadu3.

Praveena. S and Mahendran. K. (2013), in their article “Working Capital Management

Efficiency of Sugar Sector in India” found that efficient working capital management was

important for the corporate strategy. Firms try to keep the average level of working capital that

maximizes their value. This study attempted to evaluate the efficiency of working capital

management of sugar sector in India for the period 2007-2012. Instead of employing the

financial ratios, working capital efficiency had been measured in terms of utilization index,

performance index and total efficiency index. Findings of the study indicate that the sugar sector

as a whole was performing well during the study period4.

International Journal of Research

Volume VIII, Issue VI, JUNE/2019

ISSN NO:2236-6124

Page No:3600

Ramachandran and Gopinathan (2012), analysed the relationship between, "Working

Capital Management and Profitability of Sugar Industry in India". There was a significant

positive co-efficient between current ratio and Return on Investment (5.263), Inventory Turnover

Ratio and Return on Investment (1.110) at 5 per cent level. Also there was a significant negative

co-efficient between Quick ratio and Return on Investment (-10.582), Working Capital Turnover

Ratio and Return on Investment (-0.036) at 5 per cent level. Debtors Turnover Ratio recorded

highly significant negative co-efficient (-0.020) at 1 per cent level with Return on Investment.

Creditors Turnover Ratio registered insignificant positive co-efficient 0.014 with profitability.

The overall regression model fit, which was represented by R2, was above 50 per cent (0.51)

which indicated that the sugar industry in India was poised to reap a rich harvest in the season

beginning from October, 2010. The Sugar Corporate firms are over-burdened with surplus

inventories that most of them do not have adequate storage facilities, capacities and cash flow

which have led them to resort to distress sale of sugar which brought down the prices5.

SAMPLE DESIGN

The present study is confined to the study of working capital management efficiency of

select sugar factories in Chittoor district. There are 6 sugar factories in Chittoor district. Out of

these, two factories are in co-operative sector, and four factories are in private sector. Out of

these six sugar factories, three sugar factories are not working i.e., one in private sector and two

in co-operative sector. The researcher has adopted census method and chosen three sugar

factories namely, Prudential Sugar Corporation Limited, Nindra, SNJ Sugars and Products

Limited, S.R.Puram and Suddalagunta Sugars Limited, B.N.Kandriga and all belong to private

sector

Scope and Limitation of the Study

The present study is confined to the working capital management efficiency of select

sugar factories in Chittoor district only. The present study may not be free from limitations. The

figures taken from the annual reports have been rounded off to two decimals of rupees in lakh.

The accuracy of the data depends on the accuracy of the data available in the balance sheet of the

company

International Journal of Research

Volume VIII, Issue VI, JUNE/2019

ISSN NO:2236-6124

Page No:3601

Source of Data Collection

The study is based on the data collected from secondary source only. Both qualitative

and quantitative data relating to the working of sugar factories, cost of production, financial

performance and other related aspects are collected from individual sugar industries, and

regarding their capacity and production etc., the data was collected from journals, annual survey

of the industry and the annual reports of the select sugar factories.

Period of Study

The study is confined to the evaluation of working capital management efficiency of

select sugar factories in Chittoor district only. In the opinion of the researcher, a time span of 10

years is quite reasonable to assess the trend and growth in the effective utilization of resources

and efficiency of financial performance. To exclude abnormalities, the period is fixed for 10

years i.e., from 2006-07 to 2015-16.

Working Capital Analysis

The working capital management efficiency is done with the help of following ratios lime

liquidity and turnover ratios.

Liquidity Ratios:

Liquidity means how quickly you can get your hands on your cash. In simpler terms,

liquidity is to get your money whenever you need it. Liquidity refers to the ability of the firm to

meet the current financial obligations in the short run, usually one year. A firm should ensure

that it does not suffer from lack of liquidity and also it does not carry too much liquidity as this

hampers profitability.

The liquidity ratios measure the ability of a firm to meet its short-term obligations and

reflect the short-term financial strength of a firm. To measure the liquidity of the firm, the

following ratios are commonly used:

Current Ratio

Quick Ratio

Current Ratio

Current ratio represents the relationship between current assets and current liabilities. It

attempts to measure the ability of a firm to meet its current obligations. The standard norm of

International Journal of Research

Volume VIII, Issue VI, JUNE/2019

ISSN NO:2236-6124

Page No:3602

current ratio is 2:1 is ideal for manufacturing firms. The current ratio can be obtained with the

following formula:

Current ratio =Current Assets

Current LiabilitiesX 100

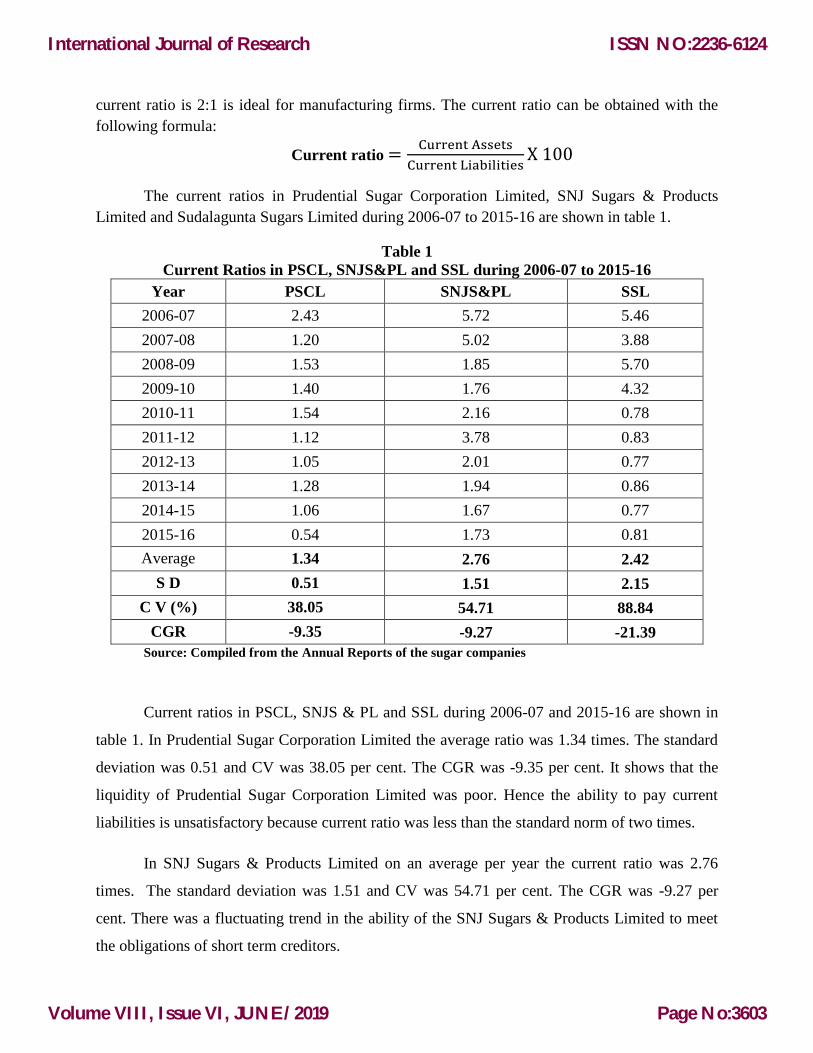

The current ratios in Prudential Sugar Corporation Limited, SNJ Sugars & Products

Limited and Sudalagunta Sugars Limited during 2006-07 to 2015-16 are shown in table 1.

Table 1

Current Ratios in PSCL, SNJS&PL and SSL during 2006-07 to 2015-16

Year PSCL SNJS&PL SSL

2006-07 2.43 5.72 5.46

2007-08 1.20 5.02 3.88

2008-09 1.53 1.85 5.70

2009-10 1.40 1.76 4.32

2010-11 1.54 2.16 0.78

2011-12 1.12 3.78 0.83

2012-13 1.05 2.01 0.77

2013-14 1.28 1.94 0.86

2014-15 1.06 1.67 0.77

2015-16 0.54 1.73 0.81

Average 1.34 2.76 2.42

S D 0.51 1.51 2.15

C V (%) 38.05 54.71 88.84

CGR -9.35 -9.27 -21.39

Source: Compiled from the Annual Reports of the sugar companies

Current ratios in PSCL, SNJS & PL and SSL during 2006-07 and 2015-16 are shown in

table 1. In Prudential Sugar Corporation Limited the average ratio was 1.34 times. The standard

deviation was 0.51 and CV was 38.05 per cent. The CGR was -9.35 per cent. It shows that the

liquidity of Prudential Sugar Corporation Limited was poor. Hence the ability to pay current

liabilities is unsatisfactory because current ratio was less than the standard norm of two times.

In SNJ Sugars & Products Limited on an average per year the current ratio was 2.76

times. The standard deviation was 1.51 and CV was 54.71 per cent. The CGR was -9.27 per

cent. There was a fluctuating trend in the ability of the SNJ Sugars & Products Limited to meet

the obligations of short term creditors.

International Journal of Research

Volume VIII, Issue VI, JUNE/2019

ISSN NO:2236-6124

Page No:3603

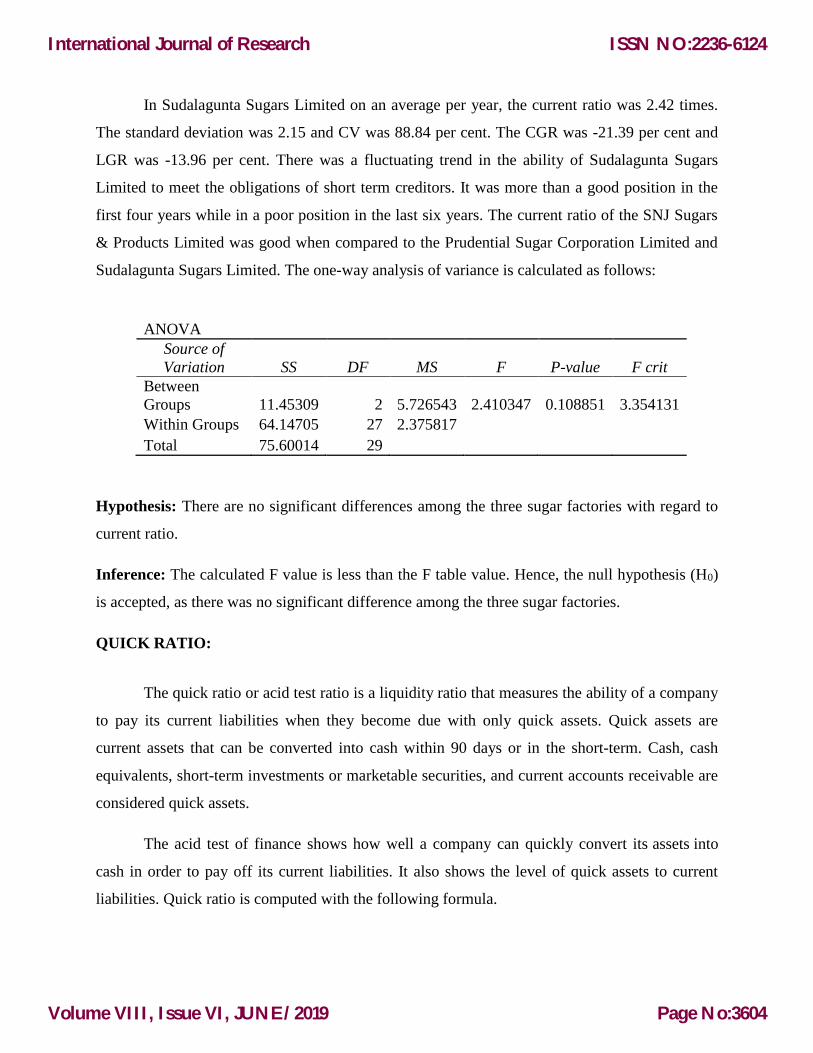

In Sudalagunta Sugars Limited on an average per year, the current ratio was 2.42 times.

The standard deviation was 2.15 and CV was 88.84 per cent. The CGR was -21.39 per cent and

LGR was -13.96 per cent. There was a fluctuating trend in the ability of Sudalagunta Sugars

Limited to meet the obligations of short term creditors. It was more than a good position in the

first four years while in a poor position in the last six years. The current ratio of the SNJ Sugars

& Products Limited was good when compared to the Prudential Sugar Corporation Limited and

Sudalagunta Sugars Limited. The one-way analysis of variance is calculated as follows:

ANOVA

Source of

Variation SS DF MS F P-value F crit

Between

Groups 11.45309 2 5.726543 2.410347 0.108851 3.354131

Within Groups 64.14705 27 2.375817

Total 75.60014 29

Hypothesis: There are no significant differences among the three sugar factories with regard to

current ratio.

Inference: The calculated F value is less than the F table value. Hence, the null hypothesis (H0)

is accepted, as there was no significant difference among the three sugar factories.

QUICK RATIO:

The quick ratio or acid test ratio is a liquidity ratio that measures the ability of a company

to pay its current liabilities when they become due with only quick assets. Quick assets are

current assets that can be converted into cash within 90 days or in the short-term. Cash, cash

equivalents, short-term investments or marketable securities, and current accounts receivable are

considered quick assets.

The acid test of finance shows how well a company can quickly convert its assets into

cash in order to pay off its current liabilities. It also shows the level of quick assets to current

liabilities. Quick ratio is computed with the following formula.

International Journal of Research

Volume VIII, Issue VI, JUNE/2019

ISSN NO:2236-6124

Page No:3604

Quick Ratio = Quick Assets

Current Liabilities

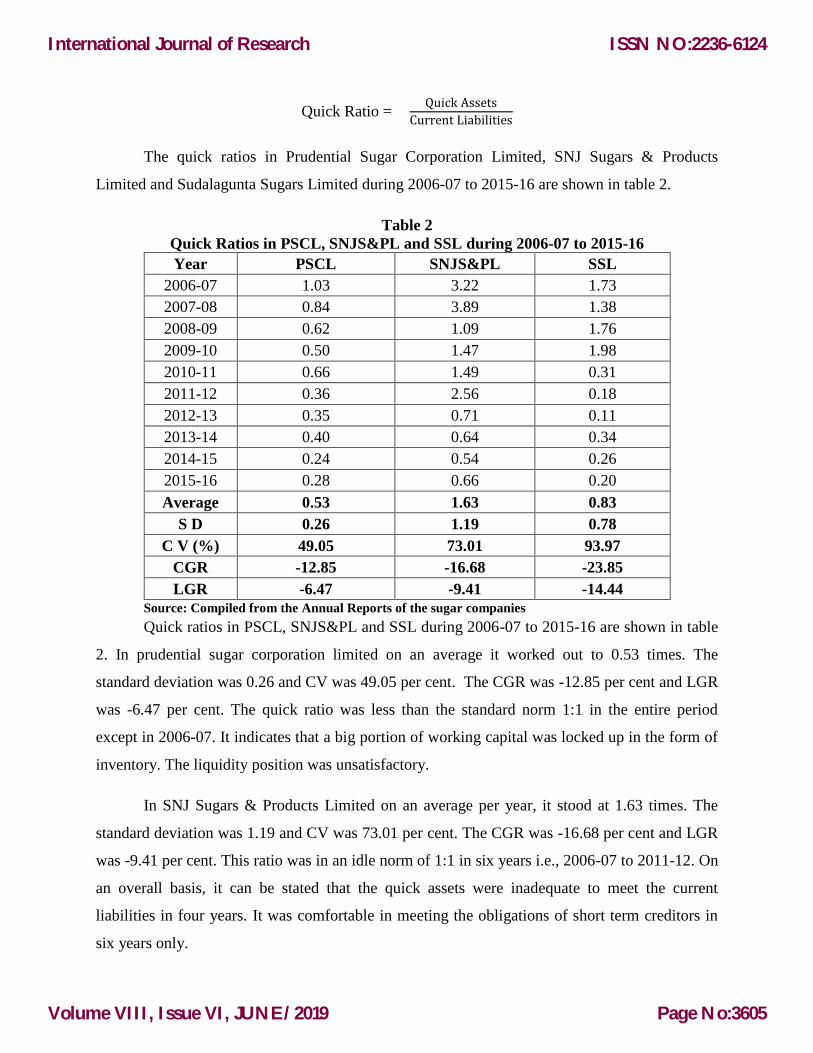

The quick ratios in Prudential Sugar Corporation Limited, SNJ Sugars & Products

Limited and Sudalagunta Sugars Limited during 2006-07 to 2015-16 are shown in table 2.

Table 2

Quick Ratios in PSCL, SNJS&PL and SSL during 2006-07 to 2015-16

Year PSCL SNJS&PL SSL

2006-07 1.03 3.22 1.73

2007-08 0.84 3.89 1.38

2008-09 0.62 1.09 1.76

2009-10 0.50 1.47 1.98

2010-11 0.66 1.49 0.31

2011-12 0.36 2.56 0.18

2012-13 0.35 0.71 0.11

2013-14 0.40 0.64 0.34

2014-15 0.24 0.54 0.26

2015-16 0.28 0.66 0.20

Average 0.53 1.63 0.83

S D 0.26 1.19 0.78

C V (%) 49.05 73.01 93.97

CGR -12.85 -16.68 -23.85

LGR -6.47 -9.41 -14.44

Source: Compiled from the Annual Reports of the sugar companies

Quick ratios in PSCL, SNJS&PL and SSL during 2006-07 to 2015-16 are shown in table

2. In prudential sugar corporation limited on an average it worked out to 0.53 times. The

standard deviation was 0.26 and CV was 49.05 per cent. The CGR was -12.85 per cent and LGR

was -6.47 per cent. The quick ratio was less than the standard norm 1:1 in the entire period

except in 2006-07. It indicates that a big portion of working capital was locked up in the form of

inventory. The liquidity position was unsatisfactory.

In SNJ Sugars & Products Limited on an average per year, it stood at 1.63 times. The

standard deviation was 1.19 and CV was 73.01 per cent. The CGR was -16.68 per cent and LGR

was -9.41 per cent. This ratio was in an idle norm of 1:1 in six years i.e., 2006-07 to 2011-12. On

an overall basis, it can be stated that the quick assets were inadequate to meet the current

liabilities in four years. It was comfortable in meeting the obligations of short term creditors in

six years only.

International Journal of Research

Volume VIII, Issue VI, JUNE/2019

ISSN NO:2236-6124

Page No:3605

In Sudalagunta Sugars Limited on an average per year, it stood at 0.83 times. The

standard deviation was 0.79 and CV was 93.97 per cent. The CGR was -23.85 per cent and LGR

was -14.44 per cent. The idle norm of the ratio was 1:1. The ratio was more than one in the first

four years. For the rest of the period it was less than the one. On an average per year, it worked

out 0.83 times. The liquidity position was unsatisfactory. It indicates that it was not possible for

the Sudalagunta Sugars Limited to meet the current obligations. The one-way analysis of

variance is calculated as follows:

ANOVA

Source of

Variation SS DF MS F P-value F crit

Between

Groups 6.464047 2 3.232023 4.626375 0.01872 3.354131

Within Groups 18.86242 27 0.698608

Total 25.32647 29

Hypothesis: There are no significant differences among the three sugar factories with regard to

quick ratios.

Inference: The calculated F value was greater than F table value. Hence, the null hypothesis

(H0) is rejected.

Turnover Ratios:

Turnover ratios can also be termed as efficiency ratio or performance ratios. Turnover

ratios are represents the relationship between sales and assets. To measure the liquidity of the

firm, the following ratios are commonly used:

Cash to Sales Turnover Ratio

Net Working Capital Turnover Ratio

Cash to Sales Turnover Ratio

This is one of the important ratios employed to control cash. A study of cash to sales ratio

will provide a deep insight into the cash balances held by the sample mills. To examine the

efficiency of cash management, it is useful to know the CSR. A lower CSR indicates poor

liquidity while a high one, sound liquidity. The CSR can be calculated with the help of the

following formula.

International Journal of Research

Volume VIII, Issue VI, JUNE/2019

ISSN NO:2236-6124

Page No:3606

100Cash

Cashto sales ratio XSales

The cash to sales turnover ratios in Prudential Sugar Corporation Limited, SNJ Sugars &

Products Limited and Sudalagunta Sugars Limited during 2006-07 to 2015-16 are shown in table

3.

Table 3

Cash to Sales Turnover Ratio in PSCL, SNJS&PL and SSL during 2006-07 to 2015-16

Year PSCL SNJS&PL SSL

2006-07 1.61 3.86 1.04

2007-08 0.89 5.66 1.37

2008-09 1.27 3.45 1.84

2009-10 1.50 3.21 0.72

2010-11 2.87 1.15 1.58

2011-12 4.40 0.64 0.73

2012-13 1.62 0.31 0.40

2013-14 0.95 0.17 5.36

2014-15 3.65 0.41 2.59

2015-16 3.45 1.93 3.41

Average 2.22 2.08 1.90

S D 1.25 1.87 1.52

C V (%) 56.30 89.90 80.00

CGR 9.71 -22.18 11.23

LGR 11.95 -12.89 15.45

Source: Compiled from the Annual Reports of the sugar companies

Cash to sales turnover ratios in PSCL, SNJS&PL and SSL during 2006-07 to 2015-16 are

shown in table 3. In prudential sugar corporation limited on an average ratio per year was 2.22

per cent. The cash to sales ratio was very low in 2007-08 due to negligible of cash balance and

higher sales relative to rest of the period. As against this, cash to sales turnover ratio was high in

2011-12 due to higher amount of sales as well as cash balances. The standard deviation was 1.25

and CV was 56.30 per cent. The CGR was 9.71 per cent and LGR was 11.95 per cent.

In SNJ Sugars & Products Limited on an average per year it stood at 2.08 per cent. A

poor cash to sales turnover ratio was recorded during 2011-12, 2012-13, 2013-14 and 2014-15

which reveals negligible ratio of cash balances. The standard deviation was 1.87 and CV was

89.90 per cent. The CGR was -22.18 per cent and LGR was -12.89 per cent. It may be concluded

International Journal of Research

Volume VIII, Issue VI, JUNE/2019

ISSN NO:2236-6124

Page No:3607

that the cash to sales turnover ratio was not satisfactory in SNJ Sugars & Products Limited

during the study period.

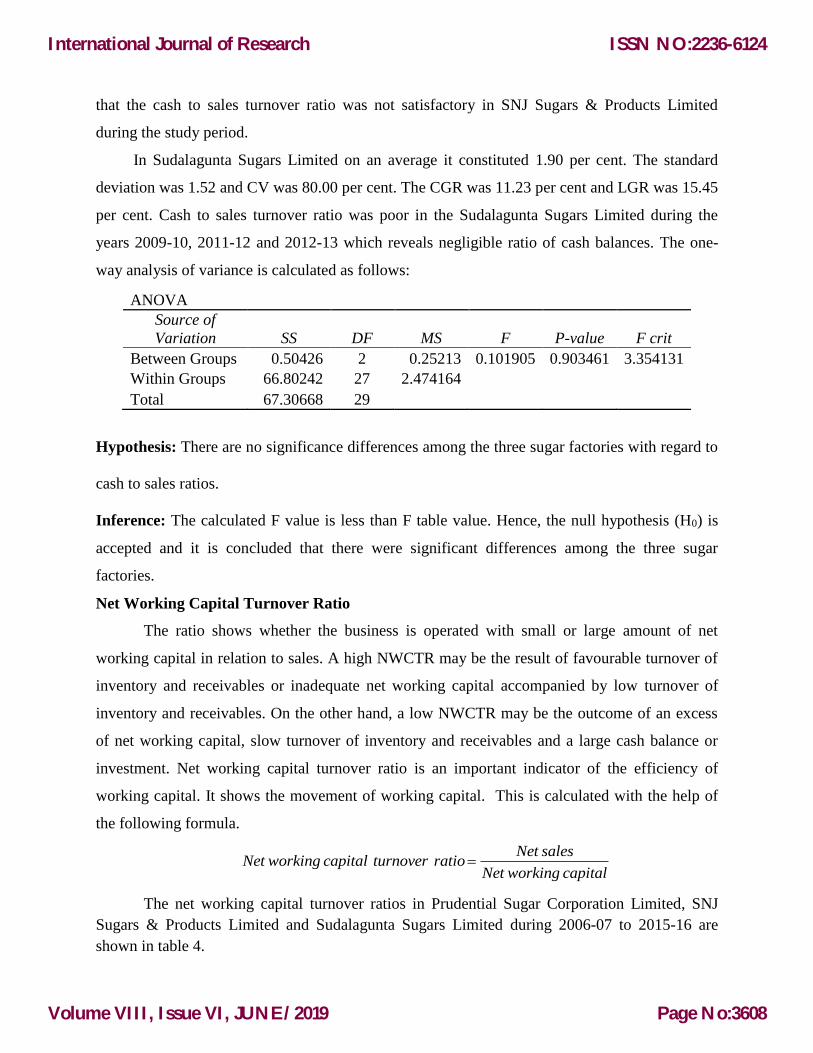

In Sudalagunta Sugars Limited on an average it constituted 1.90 per cent. The standard

deviation was 1.52 and CV was 80.00 per cent. The CGR was 11.23 per cent and LGR was 15.45

per cent. Cash to sales turnover ratio was poor in the Sudalagunta Sugars Limited during the

years 2009-10, 2011-12 and 2012-13 which reveals negligible ratio of cash balances. The one-

way analysis of variance is calculated as follows:

ANOVA

Source of

Variation SS DF MS F P-value F crit

Between Groups 0.50426 2 0.25213 0.101905 0.903461 3.354131

Within Groups 66.80242 27 2.474164

Total 67.30668 29

Hypothesis: There are no significance differences among the three sugar factories with regard to

cash to sales ratios.

Inference: The calculated F value is less than F table value. Hence, the null hypothesis (H0) is

accepted and it is concluded that there were significant differences among the three sugar

factories.

Net Working Capital Turnover Ratio

The ratio shows whether the business is operated with small or large amount of net

working capital in relation to sales. A high NWCTR may be the result of favourable turnover of

inventory and receivables or inadequate net working capital accompanied by low turnover of

inventory and receivables. On the other hand, a low NWCTR may be the outcome of an excess

of net working capital, slow turnover of inventory and receivables and a large cash balance or

investment. Net working capital turnover ratio is an important indicator of the efficiency of

working capital. It shows the movement of working capital. This is calculated with the help of

the following formula.

Net salesNet working capital turnover ratio

Net working capital

The net working capital turnover ratios in Prudential Sugar Corporation Limited, SNJ

Sugars & Products Limited and Sudalagunta Sugars Limited during 2006-07 to 2015-16 are

shown in table 4.

International Journal of Research

Volume VIII, Issue VI, JUNE/2019

ISSN NO:2236-6124

Page No:3608

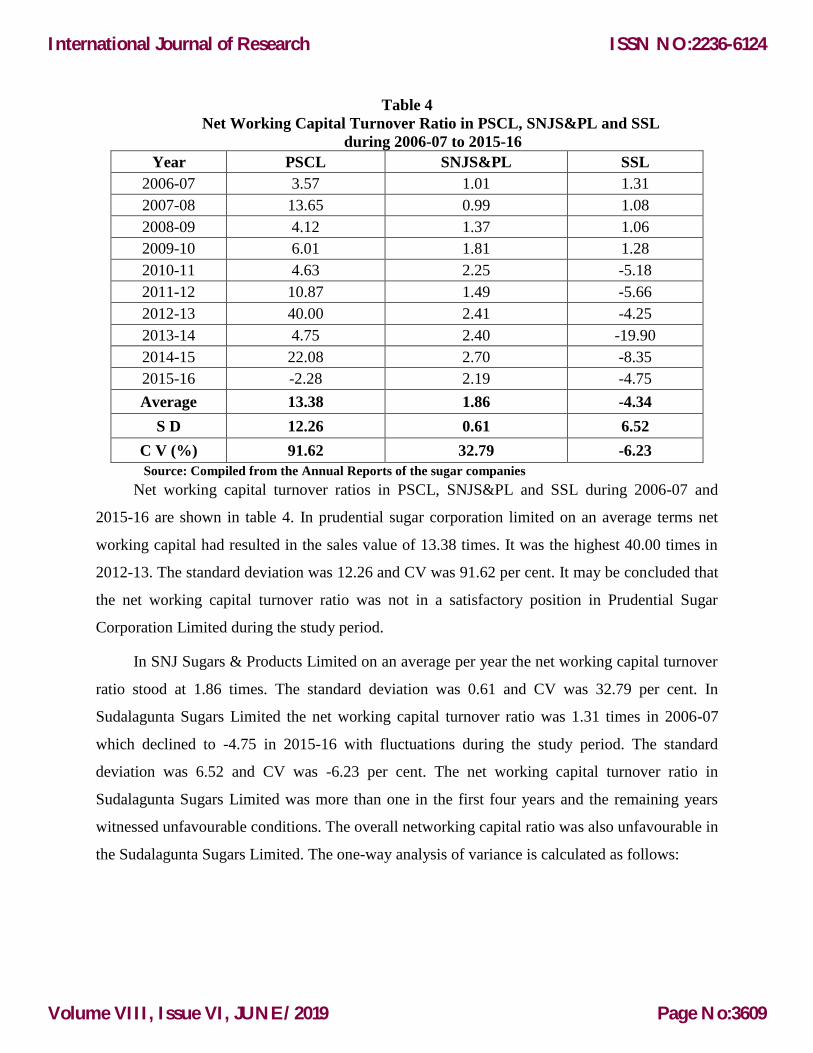

Table 4

Net Working Capital Turnover Ratio in PSCL, SNJS&PL and SSL

during 2006-07 to 2015-16

Year PSCL SNJS&PL SSL

2006-07 3.57 1.01 1.31

2007-08 13.65 0.99 1.08

2008-09 4.12 1.37 1.06

2009-10 6.01 1.81 1.28

2010-11 4.63 2.25 -5.18

2011-12 10.87 1.49 -5.66

2012-13 40.00 2.41 -4.25

2013-14 4.75 2.40 -19.90

2014-15 22.08 2.70 -8.35

2015-16 -2.28 2.19 -4.75

Average 13.38 1.86 -4.34

S D 12.26 0.61 6.52

C V (%) 91.62 32.79 -6.23

Source: Compiled from the Annual Reports of the sugar companies

Net working capital turnover ratios in PSCL, SNJS&PL and SSL during 2006-07 and

2015-16 are shown in table 4. In prudential sugar corporation limited on an average terms net

working capital had resulted in the sales value of 13.38 times. It was the highest 40.00 times in

2012-13. The standard deviation was 12.26 and CV was 91.62 per cent. It may be concluded that

the net working capital turnover ratio was not in a satisfactory position in Prudential Sugar

Corporation Limited during the study period.

In SNJ Sugars & Products Limited on an average per year the net working capital turnover

ratio stood at 1.86 times. The standard deviation was 0.61 and CV was 32.79 per cent. In

Sudalagunta Sugars Limited the net working capital turnover ratio was 1.31 times in 2006-07

which declined to -4.75 in 2015-16 with fluctuations during the study period. The standard

deviation was 6.52 and CV was -6.23 per cent. The net working capital turnover ratio in

Sudalagunta Sugars Limited was more than one in the first four years and the remaining years

witnessed unfavourable conditions. The overall networking capital ratio was also unfavourable in

the Sudalagunta Sugars Limited. The one-way analysis of variance is calculated as follows:

International Journal of Research

Volume VIII, Issue VI, JUNE/2019

ISSN NO:2236-6124

Page No:3609

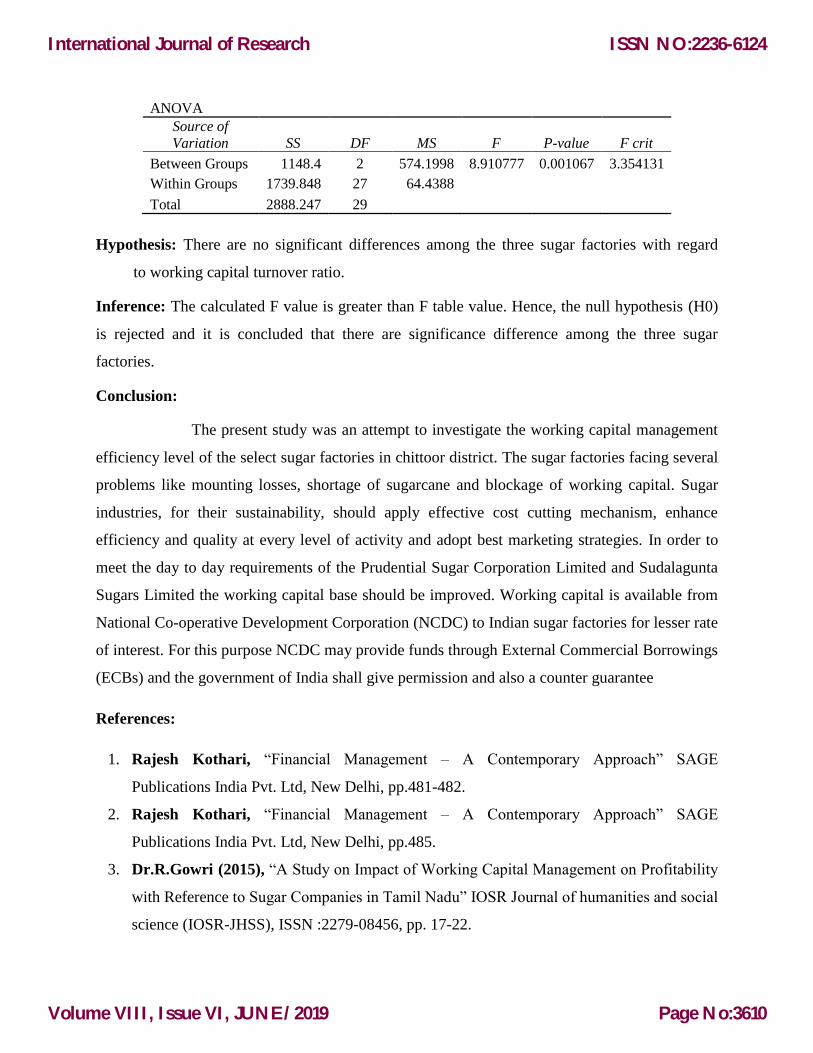

ANOVA

Source of

Variation SS DF MS F P-value F crit

Between Groups 1148.4 2 574.1998 8.910777 0.001067 3.354131

Within Groups 1739.848 27 64.4388

Total 2888.247 29

Hypothesis: There are no significant differences among the three sugar factories with regard

to working capital turnover ratio.

Inference: The calculated F value is greater than F table value. Hence, the null hypothesis (H0)

is rejected and it is concluded that there are significance difference among the three sugar

factories.

Conclusion:

The present study was an attempt to investigate the working capital management

efficiency level of the select sugar factories in chittoor district. The sugar factories facing several

problems like mounting losses, shortage of sugarcane and blockage of working capital. Sugar

industries, for their sustainability, should apply effective cost cutting mechanism, enhance

efficiency and quality at every level of activity and adopt best marketing strategies. In order to

meet the day to day requirements of the Prudential Sugar Corporation Limited and Sudalagunta

Sugars Limited the working capital base should be improved. Working capital is available from

National Co-operative Development Corporation (NCDC) to Indian sugar factories for lesser rate

of interest. For this purpose NCDC may provide funds through External Commercial Borrowings

(ECBs) and the government of India shall give permission and also a counter guarantee

References:

1. Rajesh Kothari, “Financial Management – A Contemporary Approach” SAGE

Publications India Pvt. Ltd, New Delhi, pp.481-482.

2. Rajesh Kothari, “Financial Management – A Contemporary Approach” SAGE

Publications India Pvt. Ltd, New Delhi, pp.485.

3. Dr.R.Gowri (2015), “A Study on Impact of Working Capital Management on Profitability

with Reference to Sugar Companies in Tamil Nadu” IOSR Journal of humanities and social

science (IOSR-JHSS), ISSN :2279-08456, pp. 17-22.

International Journal of Research

Volume VIII, Issue VI, JUNE/2019

ISSN NO:2236-6124

Page No:3610

4. Praveena. S and Mahendran. K. (2013), “Working capital management efficiency of

sugar sector in India”. Agriculture update, Volume 8, issue (3): 425-432.

5. Ramachandran and Gopinathan Radhika, (2012), “Working Capital Management and

Profitability of Sugar Industry in India”, Smart Journal of Business Management, July-

Dec., Vol.8, No.2, 2012, pp.54-55.

International Journal of Research

Volume VIII, Issue VI, JUNE/2019

ISSN NO:2236-6124

Page No:3611