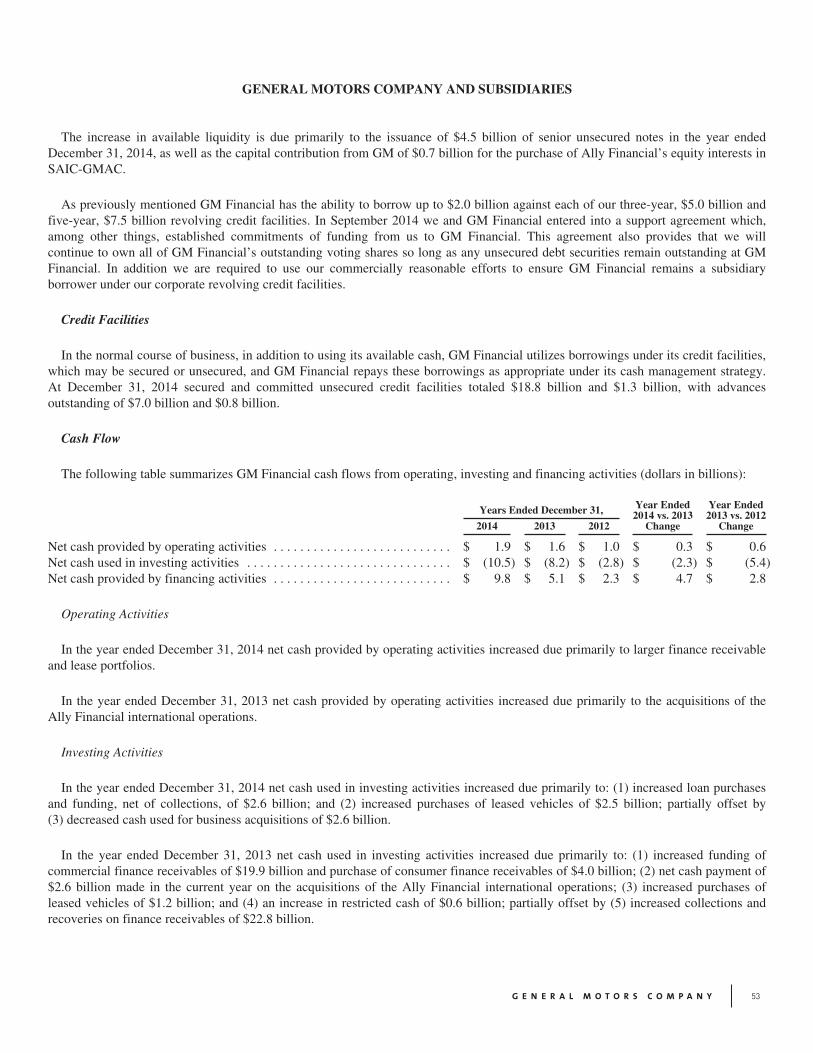

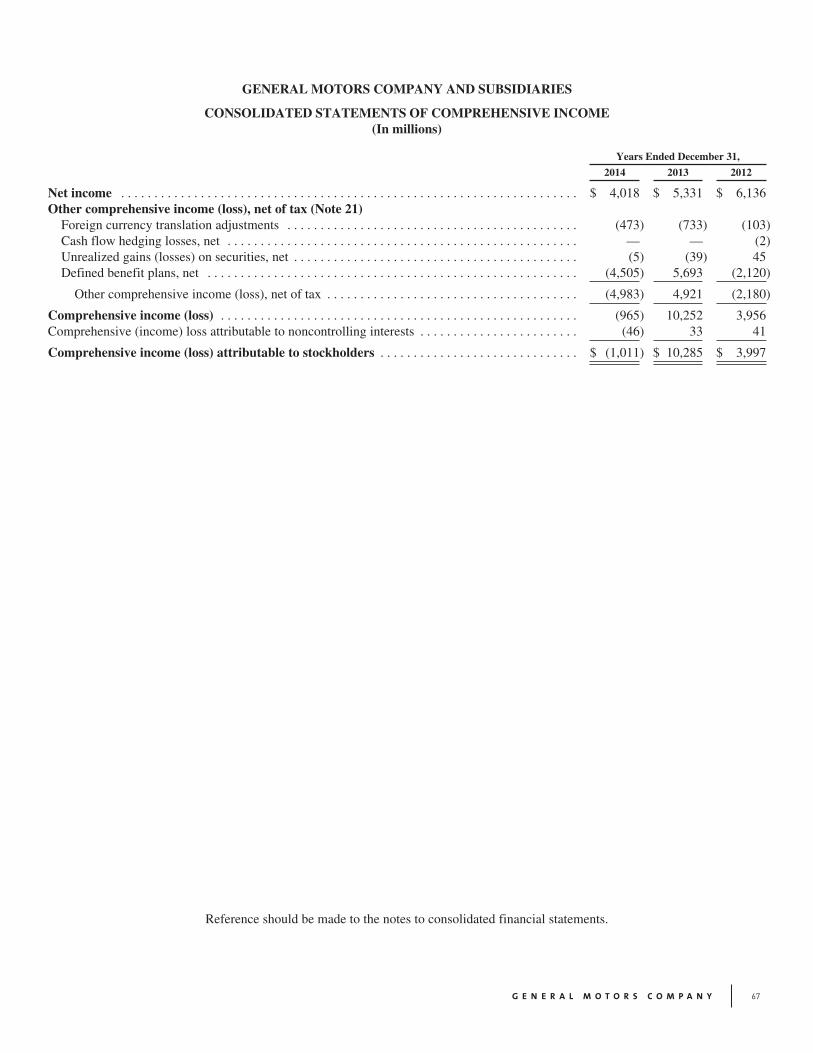

Embed Size (px)

Citation preview

2 0 1 4 A N N U A L R E P O R T

With the all-new 2015 COLO RADO , Chevrolet has reinvented the midsize pickup and earned recognition as Motor Trend’s 2015 Truck of the Year.

3

CUSTOMERS AT THE CENTER

At today’s GM, we put the customer at the center of everything

we do … customers like Bailey, who’s featured on our cover.

Her passion is riding and caring for her horses, Allegra and

Karma. She also loves her 2015 Chevrolet Colorado. But you

don’t have to take our word for it …

“To me, horseback riding isn’t just a hobby. It’s a lifestyle —

one I’ve loved for as long as I can remember. And I love

the way my Colorado fits that lifestyle. It’s eye-catching.

It’s dependable. And the four-wheel drive makes Chicago

snowstorms seem like any other day. It has space for

passengers, but it also gives me plenty of space for horse

supplies. Most importantly, I’m able to tow my ‘girls.’

“Chevys run in my family. My dad has a ’66 Corvette Stingray

and a 2002 Camaro — both red — and he’s always said he

wanted me to be a Chevy girl. And when I was little, my

trainer had an old Chevy and I can still remember to this

day telling my parents that someday I’d own one. Now I do!

“I’ve worked hard and earned everything I’ve got. I always

have … it’s how my folks raised me. And so have my horses.

More than once over the years, Allegra has fought back

from injuries and we’ve won competitions together.”

All around the world, we take pride in creating vehicles that

fit people’s lives … that meet their needs … that take them

where they want to go.

And it starts with putting customers at the center of it all,

working hard to earn their loyalty. For life.

4

LEADING THE WAY

The spirit of innovation and a passion for performance

are at the heart of every Chevrolet. For the customer, that

means our cars, trucks and crossovers combine engaging

performance, world-class safety features, head-turning

designs and purposeful technology — all while offering

great value.

From Detroit to São Paulo … from Los Angeles to New Delhi

to Shanghai and beyond … Chevrolet offers customers a

vehicle that meets their lifestyle — everything from the

Chevy Spark minicar and the best-selling Cruze midsize

sedan, to the longest-lasting, most dependable Chevy

Silverado full-size pickup and the iconic Corvette Stingray.

Chevy achieved nearly 4.8 million global sales and earned

more awards than any other manufacturer in 2014. And

our product lineup will become even fresher in 2015 as

the brand launches several key new vehicles — including

Camaro, Malibu, Spark and Volt.

Meanwhile, we’re continuing to build on the global success

of vehicles like the Trax, which is winning over customers in

the fast-growing small SUV market in China and the United

States. Or the Onix subcompact, which has the highest

resale value in Brazil, according to an AutoInforme survey.

In market after market, all around the world, Chevrolet is

a brand powered by design and innovation for the everyday

consumer. Whether it’s integrating Siri into our small cars,

or the corner-step rear bumper on Colorado, we’re leading

the way in giving our customers solutions that make their

lives better.

5

The all-new 2 0 1 5 CHEVROLET TRAX isn’t just any small SUV. With an array of street-smart features and technologies, it’s a new breed of SUV designed especially for city life.

6

The 2015 CADI L L AC CT S — pictured here against the Shanghai skyline — is just one of the models leading Cadillac’s rebirth as a true global luxury brand.

7

INSPIRING PASSION AND LOYALTY

We see it over and over again: Customers

who buy our brands car after car … from a

first car for college … to a crossover for toting

a growing family … to a luxury model that’s a

well-earned reward for career goals achieved.

And we’re determined to keep it that way.

Consider, for example, the Cadillac brand.

Over the years, it represented the very pinnacle

of American automotive achievement. The

word “Cadillac” itself became a synonym for

the highest standard in class, regardless of

industry or product category.

In today’s changing marketplace, Cadillac

is reclaiming that standard, as it undergoes

a global transformation. We’re challenging

our competitors head-on, with cars that can

beat their very best. These are vehicles at

the forefront of performance and technology

... bristling with expressive designs and

exhilarating driving dynamics.

Nowhere is that more true than in China.

It’s now our second-largest market, and

growing fast. Our assembly plant in China

began producing its second model, the ATS-L,

in 2014 and we expect a second China plant

to come online in 2015.

Meanwhile, Cadillac continues to launch

exciting new models, like its new top-of-the-

range car, the 2016 Cadillac CT6. In addition

to using advanced techniques for lighter weight

and more efficient performance, this new luxury

sedan will also deliver new technologies that

enhance safety and connectivity.

Around the world, this is a brand — 112-years-

young — that’s reinventing itself. And it’s just

one example of our commitment to deliver

brands that inspire passion and loyalty.

The word “Cadillac” itself has become a synonym for the highest standard in class, regardless of industry or product category.

8

SUCCESS BUILT ON QUALITY

AND EXCELLENCE

Earning customers for life begins with an intense focus

on those customers … from designers and engineers who

listen and respond to their feedback on their car, truck or

crossover, and seek their input in focus groups on future

vehicles … to production workers who always have the

customer in mind in their zero-defect mentality and their

passion to build the best vehicles we’ve ever offered.

That’s part of the spirit behind GM’s resurgence in Europe,

where our Opel/Vauxhall team is launching a major product

offensive that aims to deliver 27 new models and 17 new

engines by 2018. It’s being led by models like the Opel Corsa

and ADAM, which are attracting a large and loyal following —

and earning award after award in the process. Meanwhile,

the brand-new Karl subcompact is generating quite a buzz.

We’re backing this growing success with an aggressive,

multibillion dollar investment program, including a

245 million euro investment to prepare Opel’s assembly

plant in Rüsselsheim, Germany, to produce a new flagship

SUV. We’ll invest more than a half-billion euro in engine

and transmission plants in Rüsselsheim and Kaiserslautern,

Germany, and Tychy, Poland, enabling Opel/Vauxhall to

provide even more fuel-efficient engines and transmissions

for customers throughout Europe.

And that’s just one example of our commitment to invest

in our products … our people … our future.

9

At Opel/Vauxhall, the commitment and craftsmanship of employees like Gero and his team are taking hold. For the second year in a row, we’ve grown market share — actually increasing our share in more than 12 different markets.

10

The built-in 4G LTE connection in the 2014 BUICK E NCORE offers drivers advances in a wide range of in-vehicle communications and entertainment capabilities.

11

A TASTE OF TOMORROW ... TODAY

Across all our brands, as we work to develop new vehicle

technologies, we’re imagining a world where cars never crash

… where they communicate with each other, with the roads

beneath them, and with the world around them … where our

cars actually do the driving. It’s all part of our vision of how

the future of transportation will change our customers’ lives.

But some elements of that future are already here. We

offer the most vehicles with 4G LTE connectivity by OnStar

that turns your car into your most powerful and interactive

mobile device. That includes an available built-in Wi-Fi

hotspot that keeps you and your passengers seamlessly

connected to people, music, news, movies and more. It

gives your passengers the freedom to recreate their world

inside your vehicle while you navigate the world beyond it.

And with such active safety technologies as adaptive cruise

control, side blind zone warning and automatic park assist,

we’re making the driving experience easier and more

enjoyable, while making it much safer.

Meanwhile, we’re continuing to expand the frontiers of clean,

sustainable electric vehicle technology with new models

like the next-generation Chevy Volt and an all-new next-

generation electric vehicle based on the Bolt EV concept.

For us, it’s all about translating breakthrough technologies

into vehicles and experiences people love.

12

STRENGTHENING OUR COMMUNITIES

Building cars people love is just part of what

we do at GM. We also build relationships that

reach out into the communities where we live

and work. GM, our employee team and the

General Motors Foundation are on the front

lines of our efforts to make those communities

better — from our United Way partnership

to providing scholarships and mentoring

students, to building houses and refurbishing

schools through our plant city grant program,

to educating parents on child safety through

our work with Safe Kids Worldwide.

And we’re doing it on a global scale. As the

founding sponsor of the One World Play Project,

Chevrolet is committed to providing 1.5 million

ultra-durable footballs (soccer balls) to youth

in war-stricken zones, refugee camps, disaster

areas and other underprivileged communities

around the world.

GM China is working to reduce vehicle-

related child injuries and raise public

awareness of child safety in and around

vehicles with the recent launch of Safe Kids

China. To date 13,000 children and their

families have benefited from the program.

As part of our commitment to STEM education,

GM is a founding sponsor of the FIRST®

Robotics Competition (FRC®), supporting

hundreds of teams and thousands of students

around the world. In Mexico, for example,

GM employees mentor seven teams, and our

company sponsors part of the competition

in which all 39 Mexican teams participate.

Meanwhile, GM India has joined with some

local schools to help support the basic

educational needs of children in underprivileged

communities, and we’re also actively involved

in promoting child vehicle safety awareness.

In Colombia, GM South America’s Pacto Motor

program provides young adults from families

with the most serious financial need the

technical and vocational education and training

for a career in automotive service and repair.

From the cars we design and build to the

customers we serve to the community needs

we meet, we are all in with giving our best each

and every day. You’ll see in the following pages

what our spirit and determination accomplished

in a pivotal year for our company.

13

Children in Myanmar experience the power of play, courtesy of Chevrolet’s One World Play Project. Photo: OWPP/Sonderman

14

General Motors Chief Executive Officer Mary T. Barra with the advanced-technology luxury sedan, the all-new 2016 CADILLAC CT6 — fresh from its global debut at the 2015 New York Auto Show.

15

TO OUR STOCKHOLDERS

2014 was a defining year for GM.

The extraordinary challenges we faced with the ignition switch recall and additional

recalls were the ultimate test of our team and our priorities. As we faced these

challenges, we demonstrated our recently refined core values. We confronted our

problems and acknowledged our shortcomings. It was a very difficult year in many

ways, but we are a stronger company because of the way we responded to the crisis.

As the situation unfolded, we were guided

by two principles. First, do the right thing

for those who were affected by the switch

failures; and second, accept responsibility

for our mistakes and commit to doing

everything within our power to prevent

this problem from ever happening again.

In a global meeting with all GM employees last

June, I told them I never want anyone in the

company to put what happened behind them.

This experience must be permanently etched

in our memories because we never want it to

happen again. To fulfill this promise, we made

a public commitment to become the industry

leader in safety. We have made progress on this

promise, but understand there is more to do.

The demands of the recalls were significant.

At the same time, we felt strongly that we

couldn’t use this situation as an excuse for

a disappointing year financially. Successful

businesses find a way to perform, regardless

of the challenges they face. Our performance

wasn’t perfect, but we delivered solid returns.

As I reflect on this past year, I am most proud of

the men and women of General Motors. Under

difficult circumstances, they demonstrated their

character, determination, and commitment to

our customers.

Earlier this year, Consumer Reports named the 2 014 BUICK REGAL its top sports sedan, as Buick set its second consecutive annual global sales record. Sales in 2014 reached nearly 1.2 million vehicles, including more than 900,000 in China.

16

In 2014, we earned net income to common

stockholders of $2.8 billion, including recall-

related costs. Absent special items, net income

would have been $5.2 billion. Turning to EBIT-

adjusted results, we earned $6.5 billion, which

included $2.8 billion in recall-related expenses.

Net revenue increased by about $500 million

to $155.9 billion. Our adjusted automotive free

cash flow was $3.1 billion. These results are

important because this is the first year since

2010 that the company met its target for core

operating financial performance.

The results of 2014 are illustrative of what GM

can do as we become more sharply focused.

Among the year’s many highlights:

• Our China joint ventures delivered record

sales, market share and earnings.

• In North America, through the end of 2014

we delivered six consecutive quarters, year

over year, of improved core operating EBIT-

adjusted margins. Market share held steady

despite the impact of recalls.

• In Europe, Opel/Vauxhall enjoyed its second

consecutive year of sales and share growth.

• In South America, we posted a small

loss, but even as conditions became more

challenging, the team finished the year

with three consecutive, quarter to quarter,

improved EBIT-adjusted results.

• GM Financial continues to contribute to

solid earnings.

Looking to 2015 and beyond, we have made

company-wide changes so we are more attuned

to the needs and expectations of customers.

We are more united as a leadership team in

our purpose and direction. And we are putting

concrete strategies and plans in place that will

help us achieve our goal of becoming the most

valued automotive company.

2015 OP EL C ORSA

17

I believe we will see more changes in the

automotive sector in the next five years

than we have seen in the last 50. We are

on the verge of a revolution in personal

transportation. Vehicles will become

dramatically safer, more fuel efficient and

cleaner than anyone thought possible even

a few years ago. The impact on the industry,

communities around the globe and hundreds

of millions of consumers will be profound.

I have been in this industry my entire career

and this is by far the most exciting time I have

experienced. The competition is fierce. The

technological advances are dramatic and

regulatory changes are far reaching. But the

opportunity to build the next generation of cars,

trucks and crossovers that will improve millions

of lives is incredibly motivating to all of us at

GM. Our mission at GM is to be the industry

leader in this era of transformative change.

As we add the latest technology to vehicles, we

will remain focused on our customers. We want

to earn customers for life. We want customers

to know that they can count on GM for industry

leading quality, safety and reliability, as well as

for translating breakthrough technologies into

vehicles and experiences that they love. Most

importantly, we want customers to know that,

in partnership with our dealers, they will be

valued and respected throughout their entire

ownership experience.

Accountability is the foundation for any

organization’s success. A company, like an

individual, becomes known for whether or

not it keeps its word. More than anything

else, we want people to know that GM can

be counted on to act with integrity, to keep

its commitments and honor its relationships

with all stakeholders. Financially, we will

work to make prudent investments for the

future while delivering strong results in the

short term. We will continue to expand our

efforts to strengthen our brands and better

serve the needs and desires of our customers.

One great example of our ability to lead is

the new Chevrolet Colorado and GMC Canyon

midsized pickups. Many industry experts

believed the midsized truck segment was

dead. It had shrunk significantly over the last

decade or so, and most manufacturers had

dropped out of the segment.

Yet after listening carefully to customers,

and relying on our own instincts, we saw an

opportunity. We concluded there was demand

for an all-new, midsized truck, and we put a

plan in place to meet this need. It was not an

easy call, but it was the right one. The trucks

The competition is fierce. Our mission at GM is to be the industry leader in this era of transformative change.

18

have received rave reviews and numerous

awards, including Motor Trend’s Truck of the

Year and Autoweek’s Best of the Best Truck.

We have 10 distinct brands around the globe

and we are working to strengthen each of

them to inspire passion and loyalty in the

markets they serve.

A critical component of GM’s business plan is

to restore Cadillac to a position of leadership

in the global luxury segment. We took a

significant step late last year by establishing

Cadillac as a separate business inside General

Motors. The brand experienced a 5 percent

sales increase in 2014, led by a 47 percent

increase in sales in China and the resounding

success of the new Escalade.

The luxury segment is an important part of

the auto business today, and it’s going to be

even more important over the next decade.

By 2020, the luxury segment is expected to

expand globally by 35 percent or more. To take

advantage of this rising tide of sales, we are

investing heavily in new product for Cadillac.

Over the next five years, we intend to launch

eight new models, several of which will be new

segments for the brand.

Another element of our strategy for Cadillac is

to position the brand as the flagship for industry

leading technology. In the 2017 model year, we

plan to introduce vehicle-to-vehicle connectivity

and Super Cruise, a GM developed system

that allows drivers in certain circumstances

to operate the vehicle without touching the

steering wheel or pedals.

It will take time to see results, but we have

confidence that, as we execute our strategy,

Cadillac sales will grow over the next few years.

Chevrolet performed well in 2014, with sales up

4 percent in the U.S. The new Silverado, Tahoe

and Suburban had great sales momentum and

they each gained market share. Chevrolet also

had record sales in China, and it retained its

market leadership in South America.

With more than 70 million customers around

the world, Chevrolet is one of the best

positioned auto brands in the industry. Our

challenge is to better leverage Chevrolet’s

extraordinary assets so it can continue to

grow in the U.S., while expanding rapidly in

China, Brazil and other developing markets.

An example of Chevrolet’s potential is the

all-new Trax, a small crossover that competes

in one of the fastest-growing segments in the

To take advantage of this rising tide of sales, we are investing heavily in new product for Cadillac. Over the next five years, we intend to launch eight new models, several of which will be new segments for the brand.

19

U.S. and China. Following the Trax, we have a

full pipeline of strong new products launching

over the next 12 months. Starting late this year,

we will launch new versions of the Malibu and

Equinox, which compete in two of the world’s

largest vehicle segments. All-new versions

of the Spark, Volt and Camaro will also make

their debuts.

Opel/Vauxhall continues to execute its plan

for growth and profitability. With successful

products such as Mokka and ADAM, Opel/

Vauxhall delivered sales of nearly 1.1 million

last year. This was the second year in a row

Opel/Vauxhall gained market share. To keep

our momentum going, we launched the fifth

generation of the Corsa in early 2015. The

new Karl small car and Astra will follow later

this year. Astra and Corsa represent about

half of Opel/Vauxhall’s volume.

Rebuilding Opel has taken resolve, discipline

and a lot of hard work. We believe we have

the right plan, a strong leadership team and a

company-wide commitment to Opel’s future.

Buick continues to be a style leader and a

core component of our growth strategy in

China. With sales of nearly 1.2 million in 2014,

including more than 900,000 in China, Buick is

a great example of how GM’s global scale can

be leveraged to produce value for stockholders.

Buick is also a great example of the quality

of our vehicles and the strength of our dealer

network. Consumer rating organizations, such

as J.D. Power and Associates and Consumer

Reports, consistently rank Buick among the

top automotive brands for reliability and

dealer service.

The GMC brand is defined as Professional

Grade — a commitment to premium materials,

purposeful design and advanced technology in

every vehicle. We are enhancing our marketing

efforts and exploring a number of ways to

further expand GMC’s product offerings. Going

The all-new 2 0 1 6 CHEVY MALIBU

20

The all-new 2016 BUICK E NVISION

forward, we will continue to invest in the brand

because of GMC’s strong brand identity and

growth potential.

GM Financial is another critical part of our

growth strategy. As we expand our ability to

offer customers financing and leasing, it is an

important resource for fulfilling our ambition of

earning lifetime relationships with customers.

GM Financial currently operates in 19 countries

that account for approximately 80 percent of

GM’s sales. Now that it is the exclusive lease

provider for Chevrolet, Buick, GMC and Cadillac,

GM Financial’s growth and profitability should

increase substantially.

Across all of our brands, we are leading the

industry in connectivity. Our commitment to

offer 4G LTE and OnStar on a global basis is

creating a significant competitive advantage

for GM. In North America, we installed 4G LTE

on more than 30 models — 16 Chevrolet,

4 Buick, 6 GMC and 5 Cadillac — by far the most

in the industry. Our service includes a built-

in Wi-Fi hot spot capable of connecting up to

seven devices. It also enhances the connection

to OnStar, making it the best in-vehicle safety

system available from any manufacturer.

We are accelerating the integration of OnStar

and 4G LTE in China and Europe as well.

OnStar launched in China in 2009, and today

it is the largest telematics provider in the

country with more than 850,000 subscribers.

Later this year we expect to begin offering

4G LTE on select Cadillac models in China.

Opel/Vauxhall will launch OnStar with 4G LTE

capabilities in 13 European markets this year,

with no additional roaming charges. OnStar will

be available across the Opel/Vauxhall car range,

and interactions with our advisors, in-vehicle

voice prompts, the radio display and mobile

app will be in the customers’ chosen language.

21

With these services, we are making sure our

customers have more than just a great vehicle,

they have a great ownership experience.

The electrification of the automobile is an

important part of our future as well. On this

front, we are making rapid and dramatic

progress. Consumers have purchased more

than 75,000 Volts, and we know two things from

their collective experience. First, owners love

the vehicle. The Volt’s customer satisfaction

ratings are among the highest in the industry.

Second, they rarely buy gasoline. The typical

Volt customer is averaging about 100 miles per

gallon, which translates to a fill-up about once

a month.

Building on our experience with the first

generation Volt, we revealed a second-

generation model and a new electric concept

car at the North American International Auto

Show in January. The concept vehicle, known as

the Bolt EV, is an all-electric vehicle that will go

200 miles on a charge and cost roughly $30,000.

Following a positive response from consumers,

we recently confirmed we will build the car in

our Orion Assembly facility near Detroit.

As we consider the progress of the last few

years, we believe we are on track to meet

our 2016 financial targets, which include

10 percent EBIT-adjusted margins in North

America, profitability in Europe, sustained

strong margins in China and continued

progress in emerging markets.

In addition, in February we announced our

intent to increase the second quarter dividend

on our common stock by 20 percent to 36 cents

per share. And, in March we announced a

capital allocation framework that provides

for reinvestment in the business, maintains

an investment grade balance sheet and

anticipates the return of all available free cash

flow to stockholders, including a $5-billion

share buyback.

During 2015, we expect to sell more than

1,000 new vehicles per hour, 24 hours a day.

This adds up to nearly 10 million vehicles, the

most in our history. I look at this extraordinary

volume as 10 million opportunities to prove

what kind of company we are. I believe we

are stronger than we were a year ago. I also

believe we will continue to gain strength this

year and in the years ahead.

Respectfully,

MARY T. BARRAChief Executive Officer

April 24, 2015

Today’s Chevy Volt customers average about 100 miles per gallon, which should be even better with the all-new 2 0 1 6 CHEVROLET VOLT .

22

FINANCIAL CONTENTS

21 Vehicle Sales and Net Revenue

22 Board and Management Team

24 Reconciliation of Non-GAAP Measures

27 Market for Registrant’s Common Equity and Related Stockholder Matters

28 Selected Financial Data

29 Management’s Discussion and Analysis of Financial Condition and Results of Operations

59 Quantitative and Qualitative Disclosures About Market Risk

66 Financial Statements and Supplementary Data

66 Consolidated Income Statements

67 Consolidated Statements of Comprehensive Income

68 Consolidated Balance Sheets

69 Consolidated Statements of Cash Flows

70 Consolidated Statements of Equity

71 Notes to Consolidated Financial Statements

134 Disclosure Controls and Procedures

HIGHLIGHTS

Source: Bloomberg

CUMULATIVE VALUE OF $100 INVESTMENT THROUGH DECEMBER 31, 2014

11/18/2010 2010 2011 2012 2013 2014

$100 $111.70 $ 61.42 $ 87.36 $123.85 $109.51

$100 $106.94 $109.20 $126.68 $167.71 $190.66

$100 $104.10 $ 87.40 $108.68 $144.26 $138.00

General Motors Company

Dow Jones Automobiles & Parts Titans 30 Index

S&P 500 Stock Index

WORLDWIDE NET SALES & REVENUE

$156B

NET INCOME ATTRIBUTABLE TO COMMON STOCKHOLDERS

$2.8B

$1.65DILUTED EARNINGS PER COMMON SHARE

COMPARISON OF CUMULATIVE TOTAL RETURN

$ 200

$ 180

$ 160

$ 140

$ 120

$ 100

$ 80

$ 60

$ 40

NOV 2010

DEC2010

DEC2011

DEC2012

DEC2013

DEC2014

23

VEHICLE SALES AND NET REVENUE

(in millions, except units per share & employment) 2013 2014

VEHICLE SALES, INCLUDING JOINT VENTURES - (OOO’S UNITS)

GMNA 3,234 3,413

GME 1,393 1,256

GMIO 4,058 4,378

GMSA 1,037 878

Worldwide Vehicle Sales 9,722 9,925

FINANCIAL RESULTS

Worldwide Net Sales & Revenue $ 155,427 $ 155,929

Earnings Before Interest and Income Taxes - Adjusted* $ 8,578 $ 6,494

Net Income Attributable to Common Stockholders $ 3,770 $ 2,804

Diluted Earnings Per Common Share $ 2.38 $ 1.65

AUTOMOTIVE LIQUIDITY & KEY OBLIGATIONS

AVAILABLE AUTOMOTIVE LIQUIDITYCash and Marketable Securities $ 27,919 $ 25,202

Credit Facilities 10,404 12,026

Total Available Automotive Liquidity $ 38,323 $ 37,228

KEY AUTOMOTIVE OBLIGATIONSDebt $ 7,137 $ 9,410

Underfunded U.S. Pension 7,314 10,901

Total Automotive Obligations $ 14,451 $ 20,311

ADJUSTED AUTOMOTIVE FREE CASH FLOW

Operating Cash Flow $ 11,021 $ 10,132

Less: Capital Expenditures (7,549 (7,039

Adjustments 225 53

Adjusted Automotive Free Cash Flow $ 3,697 $ 3,146

EMPLOYMENT - YEAR END (000’S)

GMNA 109 110

GME 37 37

GMIO 36 33

GMSA 31 29

GM Financial 6 7

Worldwide Employment 219 216

*Includes GM Financial on an Earnings Before Tax (EBT)-adjusted basis

))

24

BOARD OF DIRECTORS As of April 1, 2015

Beginning on left:

KATHRYN MARINELLOSenior Advisor, Ares Management LLC, Joined Board 07/10/09

JOSEPH ASHTONRetired Vice President, United Auto Workers, Joined Board 08/11/14

CAROL STEPHENSONRetired Dean, Ivey Business School, Univ. of Western Ontario, Joined Board 07/24/09

ERROLL DAVIS Retired, Superintendent for Atlanta Public Schools, Joined Board 07/10/09

THEODORE SOLSOChairman of the Board, General Motors Company and Retired Chairman and Chief Executive Officer, Cummins Inc., Joined Board 06/12/12

MARY BARRAChief Executive Officer, General Motors Company, Joined Board 01/15/14

MICHAEL MULLENRetired Chairman, Joint Chiefs of StaffJoined Board 02/01/13

JAMES MULVARetired Chairman and Chief Executive Officer, ConocoPhillips, Joined Board 06/12/12

THOMAS SCHOEWERetired Executive Vice President and Chief Financial Officer, Wal-Mart Stores, Inc., Joined Board 11/14/11

PATRICIA RUSSOFormer Chief Executive Officer, Alcatel-Lucent S.A., Joined Board 07/24/09

STEPHEN GIRSKYPresident, S. J. Girsky & Company, Joined Board 07/10/09

Not Pictured:

E. NEVILLE ISDELLRetired Chairman and Chief Executive Officer, The Coca-Cola Company, Joined Board 07/10/09

LINDA GOODENRetired Executive Vice President, Information Systems & Global Solutions, Lockheed Martin CorporationJoined Board 02/05/15

Above: The General Motors Board of

Directors enjoyed a preview of the

CHEVROLET BOLT EV CONCEPT CAR,

as it debuted at the 2015 North American

International Auto Show in Detroit. Based

on an equally enthusiastic response from

consumers, GM has committed to build

a production version at its Orion, Mich.,

assembly facility. The next generation

electric vehicle based on the Bolt EV

concept will have more than 200 miles

of range — translating to more trips to

work, school or the market on a single

charge. The Bolt EV concept is a true

game-changer. It’s a more affordable

pure electric option — an EV for everyone.

And it’s packed with the kind of innovation

that raises the bar for electric vehicles

around the globe.

25

MANAGEMENT TEAM As of April 1, 2015

MARY BARRAChief Executive Officer

DAN AMMANNPresident

JAIME ARDILAExecutive Vice President & President, South America

ALAN BATEYExecutive Vice President & President, North America

DAN BERCESenior Vice President & President and Chief Executive Officer, GM Financial

ALICIA BOLER-DAVISSenior Vice President, Global Connected Customer Experience

TONY CERVONESenior Vice President, Global Communications

JIM DELUCAExecutive Vice President, Global Manufacturing

JOHAN DE NYSSCHENExecutive Vice President & President, Cadillac

BOB FERGUSONSenior Vice President, Global Public Policy

CRAIG GLIDDENExecutive Vice President & General Counsel

STEFAN JACOBYExecutive Vice President & President, GM International

GRACE LIEBLEINVice President, Global Quality

VICTORIA MCINNISVice President, Tax and Audit

RANDY MOTTSenior Vice President, Global Information Technology & Chief Information Officer

KARL-THOMAS NEUMANNExecutive Vice President & President, EuropeChairman of the Management Board of Opel Group GmbH

JOHN QUATTRONESenior Vice President, Global Human Resources

NIHARIKA TASKAR RAMDEVVice President, Finance & Treasurer

MARK REUSSExecutive Vice President, Global Product Development, Purchasing & Supply Chain

BOB SHROSBREEActing Secretary

CHUCK STEVENSExecutive Vice President & Chief Financial Officer

TOM TIMKOVice President, Controller & Chief Accounting Officer

MATT TSIENExecutive Vice President & President, GM China

ED WELBURNVice President, Global Design

26

GENERAL MOTORS COMPANY AND SUBSIDIARIES RECONCILIATION OF NON-GAAP MEASURES The accompanying Letter to Stockholders includes earnings before interest and taxes adjusted for special items (EBIT-adjusted) and Adjusted

automotive free cash flow which are not prepared in accordance with Accounting Principles Generally Accepted in the United States of America (U.S.

GAAP) and have not been audited or reviewed by GM’s independent auditors. EBIT-adjusted and Adjusted automotive free cash flow are considered

non-GAAP measures.

Management believes these non-GAAP measures provide meaningful supplemental information regarding GM’s operating results and liquidity

because they exclude amounts that management does not consider when assessing and measuring operational and financial performance.

Management believes these measures allow it to readily view operating trends, perform analytical comparisons and benchmark performance

between periods and among geographic regions. GM believes these non-GAAP measures are useful in allowing for greater transparency of GM’s

core operations and they are therefore used by management in its financial and operational decision-making.

While management believes that these non-GAAP measures provide useful information, they are not operating measures under U.S. GAAP, and

there are limitations associated with their use. GM’s calculation of these non-GAAP measures may not be completely comparable to similarly titled

measures of other companies due to potential differences between companies in their method of calculation. As a result, the use of these non-GAAP

measures has limitations and should not be considered in isolation from, or as a substitute for, other measures such as Net income or Net income

attributable to common stockholders. Due to these limitations, these non-GAAP measures are used as a supplement to U.S. GAAP measures.

The following table summarizes the reconciliation of EBIT-adjusted to its most comparable U.S. GAAP measure (dollars in millions):

(a) GM’s automotive operations’ interest income and interest expense are recorded centrally in Corporate.

(b) GM Financial amounts represent income before income taxes.

In the year ended December 31, 2013, adjustments to automotive free cash flow included the following:

• Accrued interest on the prepayment of the Health Care Trust notes of $154 million;

• Pension contributions of $71 million related to the previously announced annuitization of the U.S. salaried pension plan.

In the year ended December 31, 2014, adjustments to automotive free cash flow included the following:

• Pension contributions of $53 million related to the previously announced annuitization of the U.S. salaried pension plan.

In the year ended December 31, 2013, special items for EBIT-adjusted included the following:

• Impairment charges of property and intangible assets of $774 million in GMIO;• Costs related to our plans to cease mainstream distribution of Chevrolet brand

in Europe of $621 million in GMIO, and $15 million in GM Financial;• Gain related to reversal of GM Korea wage litigation accrual of $577 million in

GMIO;• Gain on sale of equity investment in Ally Financial of $483 million in Corporate;

• Goodwill impairment charges of $442 million in GMIO;• Venezuela currency devaluation loss of $162 million in GMSA;• Gain on sale of equity investment in PSA of $152 million in GME;• Noncontrolling interests related to redemption of the GM Korea mandatorily

redeemable preferred shares of $67 million in GMIO;• Pension settlement charges of $56 million in GMNA;• Charges related to PSA product development agreement of $49 million

in GMNA; and• Income related to various insurance recoveries of $35 million.

In the year ended December 31, 2014, special items for EBIT-adjusted included the following:

• Catch-up adjustment related to the change in estimate for recall campaigns of $874 million in GMNA;

• Venezuela currency devaluation loss of $419 million in GMSA;• Charge related to the funding of the ignition switch recall compensation

program of $400 million in Corporate;• Asset impairment charges in Russian subsidiaries of $245 million in GME;• Asset impairment charges in Thailand subsidiary of $158 million in GMIO;• Goodwill impairment charges of $120 million in GMSA;• Charges related to flood damage, net of insurance recoveries,

of $101 million in GMNA; and• Other charges of $10 million.

2013 2014

OPERATING SEGMENTS

GMNA(a) $ 7,461 $ 6,603

GME(a) (869 (1,369

GMIO(a) 1,255 1,222

GMSA(a) 327 (180

GM Financial(b) 898 803

Total operating segments(b) 9,072 7,079

Corporate and eliminations (494 (585

EBIT-ADJUSTED (B) 8,578 6,494

Special items (805 (2,327

Automotive interest income 246 211

Automotive interest expense (334 (403

Gain (loss) on extinguishment of debt (212 202

Net income (loss) attributable to noncontrolling interests (15 69

Income Before Income Taxes $ 7,458 $ 4,246

) )

)

) )

) )

) )

)

)

GMIO;

GENERAL MOTORS COMPANY AND SUBSIDIARIES

Market Information

Shares of our common stock have been publicly traded since November 18, 2010 when our common stock was listed and begantrading on the New York Stock Exchange and the Toronto Stock Exchange. The following table summarizes the quarterly priceranges of our common stock based on high and low prices from intraday trades on the New York Stock Exchange, the principalmarket on which the stock is traded:

Years Ended December 31,

2014 2013

High Low High Low

First quarter . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 41.06 $ 33.57 $ 30.68 $ 26.19Second quarter . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 37.18 $ 31.70 $ 35.49 $ 27.11Third quarter . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 38.15 $ 31.67 $ 37.97 $ 33.41Fourth quarter . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 35.45 $ 28.82 $ 41.85 $ 33.92

Holders

At January 28, 2015 we had a total of 1.6 billion issued and outstanding shares of common stock held by 420 holders of record.

Dividends

Since our formation, we had not paid any dividends on our common stock through the year ended December 31, 2013. Beginning inthe first quarter of 2014 our Board of Directors declared, and we paid, quarterly dividends on common stock in the amount of $0.30per share. It is anticipated that dividends on our common stock will continue to be declared and paid quarterly. However our paymentof dividends in the future, if any, will be determined by our Board of Directors and will be paid out of funds legally available for thatpurpose. Our payment of dividends in the future will depend on business conditions, our financial condition, earnings, liquidity andcapital requirements and other factors.

* * * * * * *

27

GENERAL MOTORS COMPANY AND SUBSIDIARIES

Selected Financial Data

Selected financial data is summarized in the following table (dollars in millions except per share amounts):

At and for the Years Ended December 31,

2014 2013 2012 2011 2010

Income Statement Data:Total net sales and revenue . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 155,929 $ 155,427 $ 152,256 $ 150,276 $ 135,592Income from continuing operations (a) . . . . . . . . . . . . . . . . . . . . . . . . $ 4,018 $ 5,331 $ 6,136 $ 9,287 $ 6,503Net income attributable to stockholders . . . . . . . . . . . . . . . . . . . . . . . $ 3,949 $ 5,346 $ 6,188 $ 9,190 $ 6,172Net income attributable to common stockholders (b) . . . . . . . . . . . . . $ 2,804 $ 3,770 $ 4,859 $ 7,585 $ 4,668Basic earnings per common share (c) . . . . . . . . . . . . . . . . . . . . . . . . . $ 1.75 $ 2.71 $ 3.10 $ 4.94 $ 3.11Diluted earnings per common share (c) . . . . . . . . . . . . . . . . . . . . . . . . $ 1.65 $ 2.38 $ 2.92 $ 4.58 $ 2.89Dividends declared per common share . . . . . . . . . . . . . . . . . . . . . . . . $ 1.20 $ — $ — $ — $ —Balance Sheet Data:Total assets (d) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 177,677 $ 166,344 $ 149,422 $ 144,603 $ 138,898Automotive notes and loans payable . . . . . . . . . . . . . . . . . . . . . . . . . . $ 9,410 $ 7,137 $ 5,172 $ 5,295 $ 4,630GM Financial notes and loans payable (d) . . . . . . . . . . . . . . . . . . . . . $ 37,431 $ 29,046 $ 10,878 $ 8,538 $ 7,032Series A Preferred Stock (b) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ — $ 3,109 $ 5,536 $ 5,536 $ 5,536Series B Preferred Stock (e) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ — $ 4,855 $ 4,855 $ 4,855Equity (f) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 36,024 $ 43,174 $ 37,000 $ 38,991 $ 37,159

(a) In the year ended December 31, 2014 we recorded charges of approximately $2.9 billion in Automotive cost of sales related to recall campaignsand courtesy transportation, a catch-up adjustment of $0.9 billion recorded in the three months ended June 30, 2014 related to the change inestimate for recall campaigns and a charge of $0.4 billion related to the ignition switch recall compensation program. In the year endedDecember 31, 2012 we recorded Goodwill impairment charges of $27.1 billion, the reversal of deferred tax valuation allowances of $36.3billion in the U.S. and Canada, pension settlement charges of $2.7 billion and General Motors Europe (GME) long-lived asset impairmentcharges of $5.5 billion.

(b) In December 2014 we redeemed all of the remaining shares of our Series A Preferred Stock for $3.9 billion, which reduced Net incomeattributable to common stockholders by $0.8 billion. In September 2013 we purchased 120 million shares of our Series A Preferred Stock heldby the UAW Retiree Medical Benefits Trust (New VEBA) for $3.2 billion, which reduced Net income attributable to common stockholders by$0.8 billion.

(c) In the years ended December 31, 2012 and 2011 we used the two-class method for calculating earnings per share as the Series B Preferred Stockwas a participating security. Refer to Note 22 to our consolidated financial statements for additional detail.

(d) General Motors Financial Company, Inc. (GM Financial) acquired Ally Financial Inc.’s (Ally Financial) international operations in Europe andLatin America in the year ended December 31, 2013.

(e) In December 2013 all of our Series B Preferred Stock automatically converted into 137 million shares of our common stock.(f) In December 2012 we purchased 200 million shares of our common stock for a total of $5.5 billion, which directly reduced stockholder’s equity

by $5.1 billion and we recorded a charge to earnings of $0.4 billion.

* * * * * * *

28

GENERAL MOTORS COMPANY AND SUBSIDIARIES

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Basis of Presentation

This Management’s Discussion and Analysis of Financial Condition and Results of Operations (MD&A) should be read inconjunction with the accompanying consolidated financial statements.

In the three months ended March 31, 2014 we changed our managerial and financial reporting structure to reclassify the results ofour Russian subsidiaries previously reported in our General Motors International Operations (GMIO) segment to our GME segment.We have retrospectively revised the segment presentation for all periods presented.

Non-GAAP Measures

Management uses earnings before interest and taxes (EBIT)-adjusted to review the operating results of our automotive segmentsbecause it excludes interest income, interest expense and income taxes and includes certain additional adjustments. GM Financial usesincome before income taxes-adjusted because management believes interest income and interest expense are part of operating resultswhen assessing and measuring the operational and financial performance of the segment. Examples of adjustments to EBIT and GMFinancial’s income before income taxes include certain impairment charges related to goodwill, other long-lived assets andinvestments; certain gains or losses on the settlement/extinguishment of obligations; and gains or losses on the sale of non-coreinvestments. Refer to Note 25 to our consolidated financial statements for our reconciliation of these non-GAAP measures to the mostdirectly comparable financial measure under U.S. GAAP.

Management uses adjusted free cash flow to review the liquidity of our automotive operations. We measure adjusted free cash flow ascash flow from operations less capital expenditures adjusted for management actions, primarily related to strengthening our balance sheet,such as accrued interest on prepayments of debt and voluntary contributions to employee benefit plans. Refer to the “Liquidity” section ofMD&A for our reconciliation of this non-GAAP measure to the most directly comparable financial measure under U.S. GAAP.

Management uses these non-GAAP measures in its financial and operational decision making processes, for internal reporting andas part of its forecasting and budgeting processes as they provide additional transparency of our core operations. These measuresallow management to view operating trends, perform analytical comparisons and benchmark performance between periods and amonggeographic regions.

Our calculation of these non-GAAP measures may not be comparable to similarly titled measures of other companies due topotential differences between companies in the method of calculation. As a result the use of these non-GAAP measures has limitationsand should not be considered in isolation from, or as a substitute for, related U.S. GAAP measures.

Overview

Our strategic plan includes several major initiatives that we anticipate will help us achieve 9% to 10% margins on an EBIT-adjustedbasis (EBIT-adjusted margins, calculated as EBIT-adjusted divided by Net sales and revenue) by early next decade: (1) earncustomers for life by developing a strong product pipeline, leading the industry in quality and safety and delivering on ourcommitments; (2) lead the industry in product design, with our light-weighting and mixed material body structures and in leadingedge technology, including the launch of 4G LTE in China and expansion of OnStar, LLC to Europe; (3) grow our brands, particularlythe Cadillac brand in the U.S. and China; (4) continue our growth in China; (5) continue our growth of GM Financial as our captiveautomotive financing company; and (6) deliver core operating efficiencies by institutionalizing Operational Excellence. Our financialtargets include the following:

• Expected EBIT-adjusted and EBIT-adjusted margins improving in all automotive segments in 2015 due primarily to thefollowing anticipated trends: (1) an approximately 3% increase in global industry vehicle sales; (2) improved mix of full-sizeSport Utility Vehicles (SUVs) and full-size pick-up trucks; and (3) lower overall restructuring costs; partially offset by(4) higher marketing and engineering costs; and (5) unfavorable foreign currency effects;

29

GENERAL MOTORS COMPANY AND SUBSIDIARIES

• Anticipated adjusted automotive free cash flow will be relatively flat in 2015 compared to 2014;

• Forecasted consolidated EBIT-adjusted margins of 9% to 10% by the 2020s;

• Expected EBIT-adjusted margins of 10% in General Motors North America (GMNA) in 2016, which we anticipate will bedriven by product launches, disciplined pricing and a focus on fixed costs;

• An anticipated return to profitability in GME in 2016 driven by investments in our product portfolio, a revised brand strategyand reducing material, development and production costs assuming Europe does not suffer another recession;

• Expected continued improvement of our results in GMIO (excluding the results of our China joint ventures (China JVs))through our emerging market product portfolio, improvements in brand strategy and dealer networks, cost structure andsourcing over the medium term;

• Continued strong net income margins at our China JVs, with plans to invest approximately $14 billion in China through 2018and increase vehicle sales volumes by nearly 40% by 2018;

• Expected continued improvement of our core operations in General Motors South America (GMSA) through product launchesand material and logistics optimization, with a long-term objective of single digit EBIT-adjusted margins; and

• An anticipated increase of GM Financial’s support of the sale of new GM vehicles around the world through a comprehensivesuite of financing products, including continuing on the path towards full global captive capability.

Automotive Summary and Outlook

Our consolidated Net income decreased from $5.3 billion to $4.0 billion. Notwithstanding this decrease we had strong financialresults in 2014 excluding the impact of recall campaign and courtesy transportation charges. Performance of GMNA met ourexpectations, while GME and GMIO outperformed our expectations. However, we experienced weaker performance in GMSA due tothe challenging environment in Venezuela, Brazil and Argentina.

As more fully described in the “GM North America” section of MD&A we recorded charges of approximately $2.9 billion inAutomotive cost of sales relating to recall campaigns and courtesy transportation in the year ended December 31, 2014, of which over86% was recorded in GMNA.

In the three months ended June 30, 2014 we announced the creation of a compensation program (the Program) to compensateaccident victims who died or suffered physical injury (or their families) as a result of a faulty ignition switch related to the 2.6 millionvehicles recalled under the Ignition Switch Recall. Refer to the “GM North America” section of MD&A for additional information onthe Ignition Switch Recall. It is important to our company that we reach everyone through this Program who has been impacted. TheProgram is being administered by an independent program administrator. The independent administrator has established a protocolthat defines the eligibility requirements to participate in the Program. There is no cap on the amount of payments that can be made toclaimants under the Program.

In the three months ended June 30, 2014 we recorded $0.4 billion in Automotive selling, general and administrative expense inCorporate which represents our best estimate of amounts that may be paid under the Program. The amount was treated as anadjustment for EBIT-adjusted reporting purposes. However, it is reasonably possible that the liability could exceed our recordedamount by approximately $0.2 billion. The most significant estimates affecting the amount recorded include the number ofparticipants that have eligible claims related to death and physical injury, which also contemplates the severity of injury, the length ofhospital stays and related compensation amounts and the number of people who actually elect to participate in the Program. Ourestimate is subject to significant uncertainties, as programs of this nature are highly unusual and each eligible claim will have a uniqueunderlying fact pattern. While we do not anticipate material changes to our current estimate, it is possible that material changes could

30

GENERAL MOTORS COMPANY AND SUBSIDIARIES

occur if actual eligible claims and the related compensation amounts differ from this estimate. The Program accepted claims fromAugust 1, 2014 through January 31, 2015. Payments to eligible claimants began in the fourth quarter 2014 and will continue throughthe first half of 2015. Accident victims (or their families) could choose not to participate in the Program and pursue litigation againstus. At January 30, 2015 the Program has received 3,810 claims and the independent program administrator has determined 128 claimsto be eligible for payment under the Program. Remaining claims are either under review, deficient awaiting further documentation ordeemed ineligible. Based on currently available information we believe our accrual at December 31, 2014 is adequate to cover theestimated costs under the Program. At January 30, 2015 we have paid $93 million to eligible claimants under the Program. Accidentvictims that accept a payment under the Program agree to settle all claims against GM related to the accident.

We analyze the results of our automotive business through our four geographically-based segments:

GMNA

Automotive industry volume has continued to grow in North America. In 2014 U.S. industry light vehicle sales for the calendaryear were 16.5 million units, up from 15.6 million units in 2013. In January 2015 we announced that we expect 2015 industry lightvehicle sales to be between 16.5 and 17.0 million units.

In the year ended December 31, 2014 our U.S. retail vehicle sales increased at a rate approximately 0.7 percentage points less thanindustry sales. As a result, our U.S. market share decreased by 0.1 percentage points. U.S. market share for both Chevrolet andCadillac decreased, while GMC and Buick increased.

GMNA continued to generate increases in average transaction prices (ATP) in U.S. According to J.D. Power PIN estimates, in theyear ended December 31, 2014 we achieved record ATP in the U.S. on the strength of new products such as large pick-ups and SUVs.Contributing to the record ATP, our U.S. incentive spending as a percentage of ATP increased by 0.1 percentage points, whileindustry spending increased by 0.4 percentage points compared to the prior year.

The first deliveries of the new 2015 Chevrolet Colorado and GMC Canyon mid-size pick-ups occurred in September 2014. Wehave announced plans to add a third shift at our Wentzville, Mo. assembly plant in early 2015 to meet expected demand for both mid-size pick-ups and full-size vans.

Customer safety and satisfaction were the major reasons for the recall of approximately 36 million vehicles announced during 2014.These recalls included: (1) approximately 2.6 million vehicles to repair ignition switches that could result in a loss of electrical powerunder certain circumstances that may prevent front airbags from deploying in the event of a crash (accident victims who died orsuffered physical injury associated with these vehicles (or their families) may be eligible to participate in a compensation program, asmore fully described in Note 17 to our consolidated financial statements) and to fix ignition lock cylinders that could allow removal ofthe ignition key while the engine is running, leading to possible rollaway or crash; (2) approximately 1.9 million vehicles to replaceeither the power steering motor, the steering column, the power steering motor control unit or a combination of the steering columnand the power steering motor control unit as the electric power steering could fail under certain circumstances; (3) approximately1.3 million vehicles prone to non-deployment of the side impact restraints if vehicles are not serviced when the Service Air Bagwarning light is illuminated; (4) approximately 2.7 million vehicles to modify the brake lamp wiring harness that could have corrosiondevelop due to micro-vibration; (5) approximately 1.5 million vehicles to replace front safety lap belt cables that could fatigue andseparate over time; (6) approximately 1.4 million vehicles to replace the shift cable that could wear out over time resulting inmismatches of the gear position indicated by the shift lever; (7) approximately 12.1 million vehicles to rework or replace ignition keysbecause the ignition switch may move out of the “run” position which may impact power steering and power braking and, dependingon timing of the key movement relative to the activation of the sensing algorithm of a crash event, may result in airbags notdeploying; (8) approximately 1.1 million vehicles to repair a loose battery cable that could impact vehicle warning systems;(9) approximately 0.7 million vehicles to repair ignition mechanisms where the ignition key could be pulled out while the vehicle is inthe run position; (10) approximately 0.6 million vehicles to replace the wave plate in all vehicles with 6T70 and 6T75 transmissionswhich could crack under certain circumstances; and (11) approximately 10.1 million vehicles for other matters. In the three and sixmonths ended June 30, 2014 we recorded charges of approximately $1.1 billion and $2.4 billion primarily for the estimated costs of

31

GENERAL MOTORS COMPANY AND SUBSIDIARIES

parts and labor to repair these vehicles and for courtesy transportation. The cost of the vehicles recalled in the six months endedDecember 31, 2014 were comprehended in the June 30, 2014 catch-up adjustment of $0.9 billion associated with a change in estimatefor previously sold vehicles. Refer to Note 1 and Note 13 to our consolidated financial statements for more detail related to the catch-up adjustment. Total Net sales and revenue for GMNA have increased for the year ended December 31, 2014 as compared to prioryear by 6.4%. It is difficult to determine the impact, if any, on current or future Net sales and revenue due to our recent recall activity.Of the approximately 36 million vehicles subject to recall, approximately 63% of the vehicles and 65% of the costs involve vehicleswe no longer produce or sell. We began repairing vehicles in early April 2014 and we have produced sufficient parts to have theability to repair all vehicles impacted by the Ignition Switch Recall. Refer to the “GM North America” section of MD&A foradditional information on all of the recalls we announced in 2014.

In the year ending December 31, 2015 we expect an increase in EBIT-adjusted and EBIT-adjusted margins due primarily to: (1) aslight increase in U.S. industry vehicle sales; and (2) full year production of full-size SUVs; partially offset by (3) increasedengineering and marketing costs.

The International Union, United Automobile, Aerospace and Agriculture Implement Workers of America (UAW) contract weentered into in September 2011 expires in September 2015.

GME

The automotive industry conditions in Europe remain challenging due to economic uncertainty resulting from weak gross domesticgrowth, high unemployment and vehicle production overcapacity. Despite such conditions, automotive industry sales to retail andfleet customers began to improve in the three months ended December 31, 2013 compared to the corresponding period in 2012. Thistrend continued in 2014 with industry sales to retail and fleet customers of 19 million vehicles representing a 1.8% increase comparedto the corresponding period in 2013.

Our European operations are benefiting from this trend and continue to show signs of improvement underscored by furtherimprovement in our Opel and Vauxhall market share in the year ended December 31, 2014, which builds on our first market shareincrease in 14 years in 2013. This market share increase was partially driven by the success of the recently launched Opel Mokka.

We continue to implement various strategic actions to strengthen our operations and increase our competitiveness. The key actionsinclude investments in our product portfolio including the next generation Opel Astra and Corsa, a revised brand strategy andreducing material, development and production costs, including restructuring activities. The success of these actions will depend on acombination of our ability to execute and external factors which are outside of our control.

We continue to assess additional strategic actions across the region as a result of significant volume pricing and foreign exchangepressures in certain markets, which may result in additional restructuring or rationalization actions. These actions, if implemented,may result in impairment and other charges. The determination of the amount of these charges is subject to significant uncertainty andhighly dependent on finalization of our strategic assessments.

Our restructuring activities include our effort to rationalize our manufacturing footprint in GME whereby we reached agreementwith the labor union in Germany to terminate all vehicle and transmission production at our Bochum, Germany facility at the end of2014. Affected employees are eligible for a voluntary restructuring separation program. Restructuring charges were recordedprimarily through the end of 2014. Refer to Note 19 to our consolidated financial statements for additional information.

In the year ended December 31, 2014 we performed a strategic assessment of our Russian operations as a result of a significantdeterioration in sales volumes due to challenging market conditions and deterioration in the Russian Ruble. Our review indicated thatthe existing long-lived assets and certain investments in our Russian operations were not recoverable. As a result we recordedimpairment charges of $0.2 billion in Automotive cost of sales which was treated as an adjustment for EBIT-adjusted reportingpurposes. Industry and economic conditions in Russia remain volatile and we continue to evaluate and execute various strategicactions to improve our operations in a difficult environment.

32

GENERAL MOTORS COMPANY AND SUBSIDIARIES

We expect the European automotive industry to continue to moderately improve and we expect to be profitable in GME in 2016.

In the year ending December 31, 2015 we expect an increase in EBIT-adjusted and EBIT-adjusted margins due primarily to:(1) lower restructuring costs; partially offset by (2) higher engineering, marketing and depreciation and amortization cost.

GMIO

We are addressing many of the challenges in our GMIO operations and continue to strategically assess the manner in which weoperate in certain countries within GMIO. In 2013 we announced the withdrawal of the Chevrolet brand from Western and CentralEurope and the ceasing of manufacturing and significant reduction of engineering operations in Australia by 2017 and incurredimpairment and other charges in 2013 and 2014. We continue to execute these plans and within the financial impact that we projected.As we continue to assess our performance throughout the region, additional restructuring and rationalization actions may be requiredand may be material.

In the three months ended December 31, 2014 due to a significant decrease in domestic sales driven by political unrest and a lack ofconsumer confidence domestically as well as ongoing weakness and trade challenges in several export markets we performed arecoverability test of our real and personal property assets in our Thailand operations. As a result we recorded impairment charges of$0.2 billion in Automotive cost of sales which was treated as an adjustment for EBIT-adjusted reporting purposes.

To address the significant industry, market share, pricing and foreign exchange pressures in the region, we continue to focus onproduct portfolio enhancements, manufacturing footprint rationalization, increased local sourcing of parts, cost structure reductions, aswell as brand and dealer network improvements which we expect to favorably impact the region over the medium term. However,with the significant reduction in wholesale volumes and forward pricing pressures, we tested certain long-lived assets for impairmentand additional testing may occur in the near term. Determining whether long-lived assets need to be tested for impairment, whetherrecorded amounts are recoverable and the estimate of impairment and other charges, if any, is subject to significant uncertainty andhighly dependent on finalization of our strategic assessments.

In the year ending December 31, 2015 we expect an increase in EBIT-adjusted and EBIT-adjusted margins due primarily to:(1) improved profitability at our China JVs; (2) a flat to slight increase in industry vehicle sales; (3) improved product mix in theMiddle East; and (4) improved cost performance; partially offset by (5) higher restructuring costs.

In China we are expecting an increase in industry vehicle sales with a modest increase in market share coupled with new vehiclelaunches and a full year of the 2014 launches.

GMSA

In the three months ended March 31, 2014 we recorded devaluation charges of $0.4 billion related to a change in the exchange ratewe use for remeasuring our Venezuelan subsidiaries’ non-U.S. Dollar denominated monetary assets and liabilities from the Venezuelaofficial exchange rate to the rate determined by an auction process conducted by Venezuela’s Complementary System of ForeignCurrency Administration (SICAD I). In addition to currency controls already in place the Venezuelan government announced pricingcontrols that, taken with other initiatives, require us to closely monitor and consider our ability to maintain a controlling financialinterest in our Venezuelan subsidiaries. Refer to the “GM South America” section of MD&A for additional information.

In the year ended December 31, 2014 we recorded a net gain on extinguishment of debt of $0.2 billion primarily related toprepayment of unsecured debt in Brazil.

Based on the results of our annual goodwill impairment tests we recorded goodwill impairment charges of $0.1 billion in the yearended December 31, 2014 which was treated as an adjustment for EBIT-adjusted reporting purposes.

33

GENERAL MOTORS COMPANY AND SUBSIDIARIES

In the year ending December 31, 2015 we expect an increase in EBIT-adjusted and EBIT-adjusted margins due primarily to: (1) aslight improvement in market share primarily in Brazil; (2) improved product and country mix; and (3) improved pricing; partiallyoffset by (4) higher marketing, labor, material and logistics costs. Continued foreign currency volatility will also affect our results in2015.

Corporate

On December 31, 2014 we redeemed all of our shares of Series A Preferred Stock outstanding at a redemption price equal to theaggregate liquidation amount, including accumulated dividends, of $3.9 billion. The difference of $0.8 billion between the carryingamount and the consideration paid was recorded as a reduction to Net income attributable to common stockholders.

At December 31, 2014 our European businesses had deferred tax asset valuation allowances of $4.9 billion. As a result of thechanges in our European operating structure and improving financial performance in certain jurisdictions, we are experiencingpositive evidence trends in certain operations. If these operations generate profits and taxable income in the future, it is reasonablypossible our conclusion regarding the need for full valuation allowances could change, resulting in the reversal of significant portionsof the valuation allowances. In the quarter in which significant valuation allowances are reversed, we will record a material tax benefitreflecting the reversal, which could result in lower than expected or negative effective tax rate for both the quarter and full year.

Automotive Financing — GM Financial Summary and Outlook

GM Financial is currently seeking to expand its prime lending programs in North America and anticipates that prime lending willbecome an increasing percentage of the consumer portfolio balance over time. We believe that offering a comprehensive suite offinancing products will generate incremental sales of our vehicles, drive incremental GM Financial earnings and help support oursales throughout economic cycles. GM Financial completed the acquisitions of Ally Financial’s automotive finance and financialservices businesses in Europe and Latin America during 2013. On January 2, 2015 GM Financial completed its acquisition of AllyFinancial’s 40% equity interest in SAIC-GMAC Automotive Finance Company Limited (SAIC-GMAC) in China. The aggregatepurchase price was approximately $1.0 billion, subject to certain post-closing adjustments. Also on January 2, 2015 GM Financialsold a 5% equity interest in SAIC-GMAC to Shanghai Automotive Group Finance Company Ltd. (SAICFC), a current shareholder ofSAIC-GMAC, for proceeds of approximately $120 million, subject to certain post-closing adjustments. As a result of thesetransactions GM indirectly owns 45% of SAIC-GMAC.

In January 2015 we announced GM Financial will become the exclusive U.S. lease provider for Buick-GMC dealers in February2015 and is targeting March 2015 for Cadillac dealers. U.S. lease exclusivity with Chevrolet dealers is under consideration.

In the year ending December 31, 2015 we expect income before income taxes-adjusted to remain consistent with 2014 because ournear-term financial results will be impacted by additional provisions on loan losses and interest expense resulting from the growth ofthe business.

Consolidated Results

We review changes in our results of operations under four categories: volume, mix, price and other. Volume measures the impact ofchanges in wholesale vehicle volumes driven by industry volume, market share and changes in dealer stock levels. Mix measures theimpact of changes to the regional portfolio due to product, model, trim, country and option penetration in current year wholesalevehicle volumes. Price measures the impact of changes related to Manufacturer’s Suggested Retail Price and various sales allowances.Other includes primarily: (1) material and freight; (2) costs including manufacturing, engineering, advertising, administrative andselling and policy and warranty expense; (3) foreign exchange; and (4) non-vehicle related automotive revenues and costs as well asequity income or loss from our nonconsolidated affiliates.

34

GENERAL MOTORS COMPANY AND SUBSIDIARIES

Total Net Sales and Revenue

Years Ended December 31, Variance Due To

2014 2013Favorable/

(Unfavorable) % Volume Mix Price Other

(Dollars in millions) (Dollars in billions)

GMNA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $101,199 $ 95,099 $ 6,100 6.4% $ 1.3 $ 1.2 $ 3.4 $ 0.3GME . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22,235 21,962 273 1.2% $ 0.2 $ 0.7 $ — $ (0.5)GMIO . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14,392 18,411 (4,019) (21.8)% $ (4.6) $ 0.4 $ 0.7 $ (0.4)GMSA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13,115 16,478 (3,363) (20.4)% $ (2.4) $ 0.1 $ 1.1 $ (2.1)Corporate and eliminations . . . . . . . . . . . . . . . . 151 142 9 6.3% $ —

Automotive . . . . . . . . . . . . . . . . . . . . . . . . . . . . 151,092 152,092 (1,000) (0.7)% $ (5.6) $ 2.3 $ 5.1 $ (2.8)GM Financial . . . . . . . . . . . . . . . . . . . . . . . . . . . 4,837 3,335 1,502 45.0% $ 1.5

Total net sales and revenue . . . . . . . . . . . . . . . . $155,929 $155,427 $ 502 0.3% $ (5.6) $ 2.3 $ 5.1 $ (1.3)

Years Ended December 31, Variance Due To

2013 2012Favorable/

(Unfavorable) % Volume Mix Price Other

(Dollars in millions) (Dollars in billions)

GMNA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 95,099 $ 89,910 $ 5,189 5.8% $ 1.7 $ 1.3 $ 1.9 $ 0.3GME . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21,962 23,055 (1,093) (4.7)% $ (1.1) $ — $ (0.2) $ 0.2GMIO . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18,411 20,588 (2,177) (10.6)% $ (0.8) $ (0.2) $ (0.5) $ (0.7)GMSA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16,478 16,700 (222) (1.3)% $ — $ 0.6 $ 0.9 $ (1.7)Corporate and eliminations . . . . . . . . . . . . . . . . 142 42 100 n.m. $ 0.1

Automotive . . . . . . . . . . . . . . . . . . . . . . . . . . . . 152,092 150,295 1,797 1.2% $ (0.2) $ 1.7 $ 2.2 $ (1.9)GM Financial . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,335 1,961 1,374 70.1% $ 1.4

Total net sales and revenue . . . . . . . . . . . . . . . . $155,427 $152,256 $ 3,171 2.1% $ (0.2) $ 1.7 $ 2.2 $ (0.5)

n.m. = not meaningful

Refer to the regional sections of the MD&A for additional information.

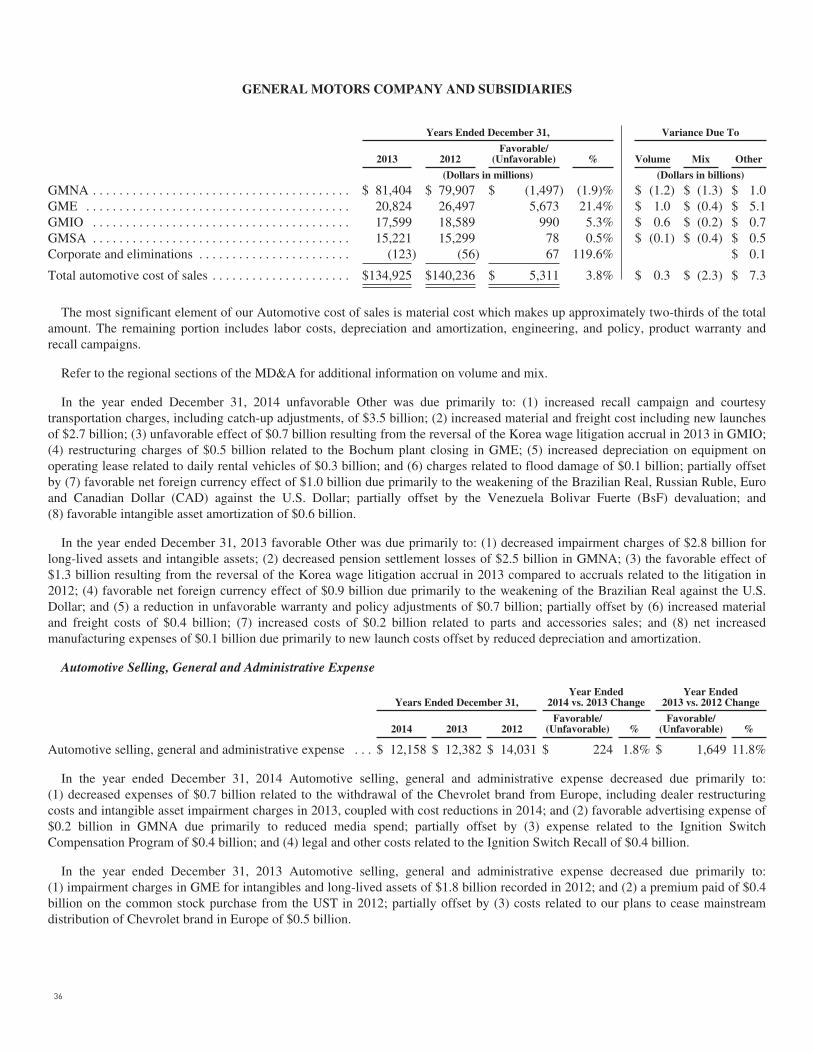

Automotive Cost of Sales

Years Ended December 31, Variance Due To

2014 2013Favorable/

(Unfavorable) % Volume Mix Other

(Dollars in millions) (Dollars in billions)

GMNA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 89,371 $ 81,404 $ (7,967) (9.8)% $ (0.8) $ (0.9) $ (6.2)GME . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21,712 20,824 (888) (4.3)% $ (0.1) $ (0.5) $ (0.3)GMIO . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14,009 17,599 3,590 20.4% $ 3.7 $ (0.5) $ 0.4GMSA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12,736 15,221 2,485 16.3% $ 1.9 $ (0.2) $ 0.8Corporate and eliminations . . . . . . . . . . . . . . . . . . . . . . . . 254 (123) (377) n.m. $ (0.4)

Total automotive cost of sales . . . . . . . . . . . . . . . . . . . . . $138,082 $134,925 $ (3,157) (2.3)% $ 4.7 $ (2.0) $ (5.8)

n.m. = not meaningful

35

GENERAL MOTORS COMPANY AND SUBSIDIARIES

Years Ended December 31, Variance Due To

2013 2012Favorable/

(Unfavorable) % Volume Mix Other

(Dollars in millions) (Dollars in billions)

GMNA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 81,404 $ 79,907 $ (1,497) (1.9)% $ (1.2) $ (1.3) $ 1.0GME . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20,824 26,497 5,673 21.4% $ 1.0 $ (0.4) $ 5.1GMIO . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17,599 18,589 990 5.3% $ 0.6 $ (0.2) $ 0.7GMSA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15,221 15,299 78 0.5% $ (0.1) $ (0.4) $ 0.5Corporate and eliminations . . . . . . . . . . . . . . . . . . . . . . . (123) (56) 67 119.6% $ 0.1

Total automotive cost of sales . . . . . . . . . . . . . . . . . . . . . $134,925 $140,236 $ 5,311 3.8% $ 0.3 $ (2.3) $ 7.3

The most significant element of our Automotive cost of sales is material cost which makes up approximately two-thirds of the totalamount. The remaining portion includes labor costs, depreciation and amortization, engineering, and policy, product warranty andrecall campaigns.

Refer to the regional sections of the MD&A for additional information on volume and mix.

In the year ended December 31, 2014 unfavorable Other was due primarily to: (1) increased recall campaign and courtesytransportation charges, including catch-up adjustments, of $3.5 billion; (2) increased material and freight cost including new launchesof $2.7 billion; (3) unfavorable effect of $0.7 billion resulting from the reversal of the Korea wage litigation accrual in 2013 in GMIO;(4) restructuring charges of $0.5 billion related to the Bochum plant closing in GME; (5) increased depreciation on equipment onoperating lease related to daily rental vehicles of $0.3 billion; and (6) charges related to flood damage of $0.1 billion; partially offsetby (7) favorable net foreign currency effect of $1.0 billion due primarily to the weakening of the Brazilian Real, Russian Ruble, Euroand Canadian Dollar (CAD) against the U.S. Dollar; partially offset by the Venezuela Bolivar Fuerte (BsF) devaluation; and(8) favorable intangible asset amortization of $0.6 billion.