Embed Size (px)

Citation preview

WIRC – Intensive Study Course on Transfer WIRC – Intensive Study Course on Transfer

Pricing

Selection of Methods / Comparables –

Examples/ Case studies

Sanjay Kapadia

05 August 2011

Index

► Indian Transfer Pricing - Concept

► Most Appropriate Method:

► Suggestive Approach on selection of Most Appropriate Method

► Characteristics and requirements of methods used in the process of identifying ALP

► Economic adjustments allowed under various methods

► Selection of comparables

WIRC - Intensive Study Course on Transfer PricingPage 2

► Selection of comparables

► Case studies

► Judicial precedents on methods and comparables

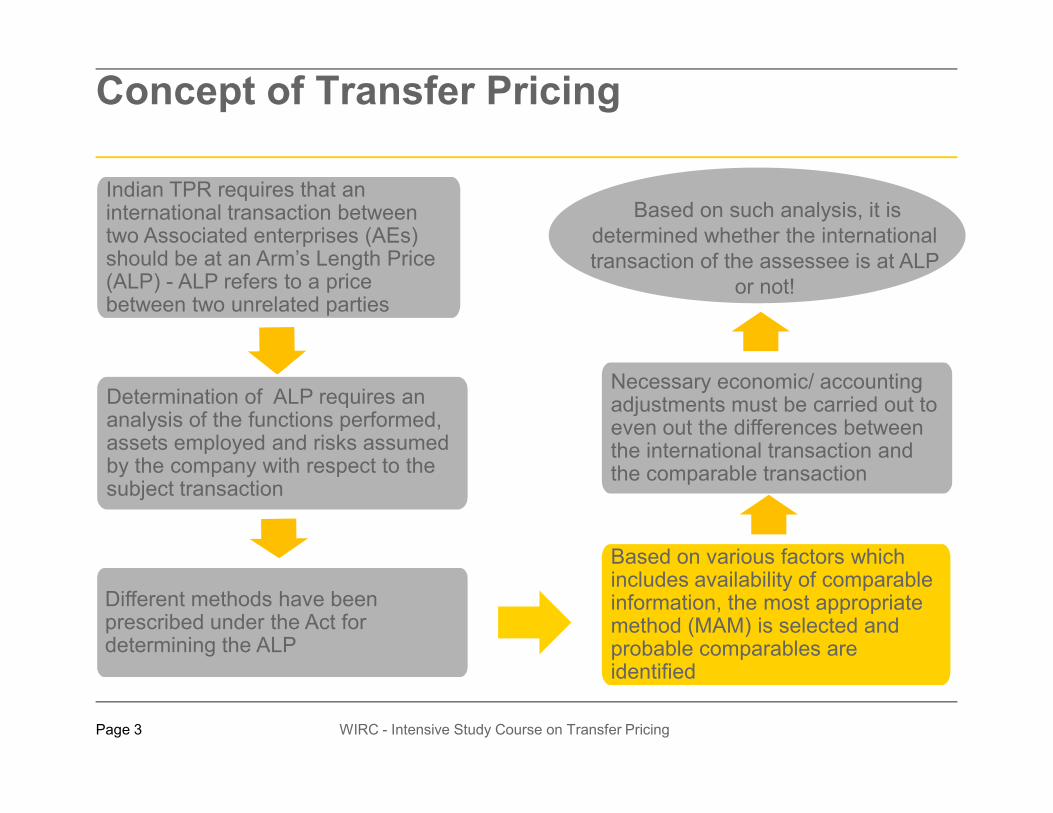

Concept of Transfer Pricing

Indian TPR requires that an international transaction between two Associated enterprises (AEs) should be at an Arm’s Length Price (ALP) - ALP refers to a price between two unrelated parties

Determination of ALP requires an Necessary economic/ accounting adjustments must be carried out to

Based on such analysis, it is determined whether the international transaction of the assessee is at ALP

or not!

WIRC - Intensive Study Course on Transfer PricingPage 3

Determination of ALP requires an analysis of the functions performed, assets employed and risks assumed by the company with respect to the subject transaction

Different methods have been prescribed under the Act for determining the ALP

Based on various factors which includes availability of comparable information, the most appropriate method (MAM) is selected and probable comparables are identified

adjustments must be carried out to even out the differences between the international transaction and the comparable transaction

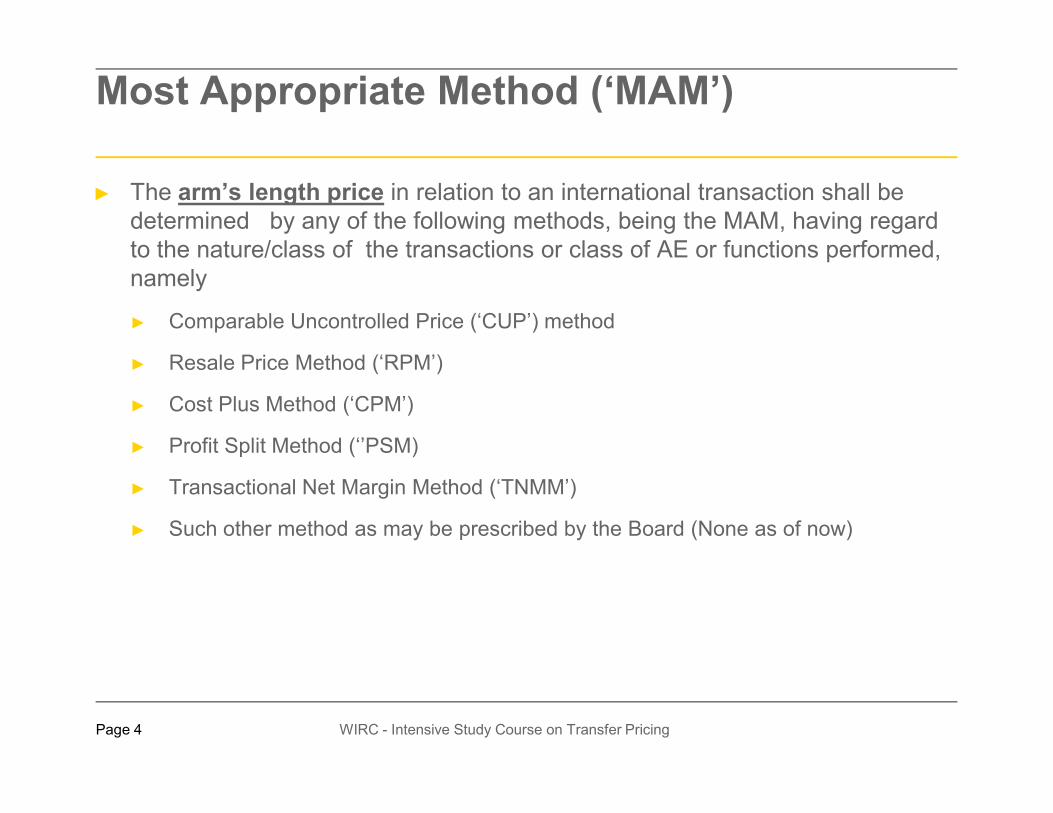

Most Appropriate Method (‘MAM’)

► The arm’s length price in relation to an international transaction shall be determined by any of the following methods, being the MAM, having regard to the nature/class of the transactions or class of AE or functions performed, namely

► Comparable Uncontrolled Price (‘CUP’) method

► Resale Price Method (‘RPM’)

► Cost Plus Method (‘CPM’)

WIRC - Intensive Study Course on Transfer PricingPage 4

► Cost Plus Method (‘CPM’)

► Profit Split Method (‘’PSM)

► Transactional Net Margin Method (‘TNMM’)

► Such other method as may be prescribed by the Board (None as of now)

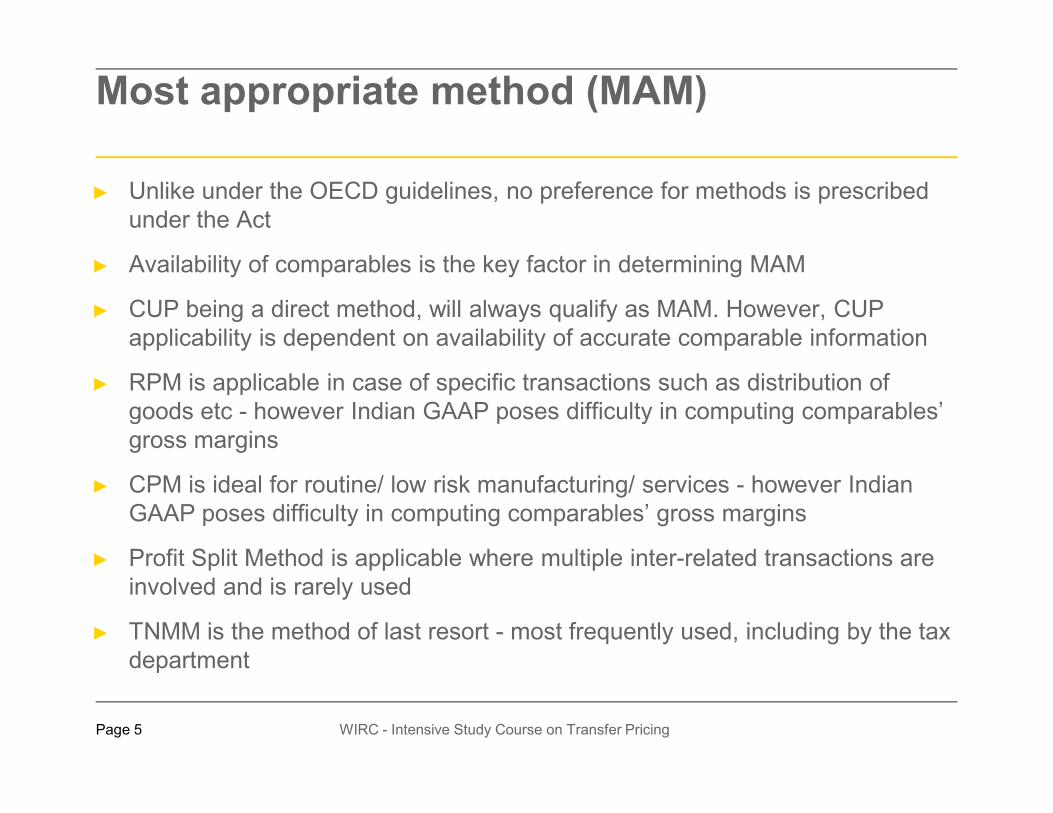

Most appropriate method (MAM)

► Unlike under the OECD guidelines, no preference for methods is prescribed under the Act

► Availability of comparables is the key factor in determining MAM

► CUP being a direct method, will always qualify as MAM. However, CUP applicability is dependent on availability of accurate comparable information

► RPM is applicable in case of specific transactions such as distribution of goods etc - however Indian GAAP poses difficulty in computing comparables’

WIRC - Intensive Study Course on Transfer PricingPage 5

goods etc - however Indian GAAP poses difficulty in computing comparables’ gross margins

► CPM is ideal for routine/ low risk manufacturing/ services - however Indian GAAP poses difficulty in computing comparables’ gross margins

► Profit Split Method is applicable where multiple inter-related transactions are involved and is rarely used

► TNMM is the method of last resort - most frequently used, including by the tax department

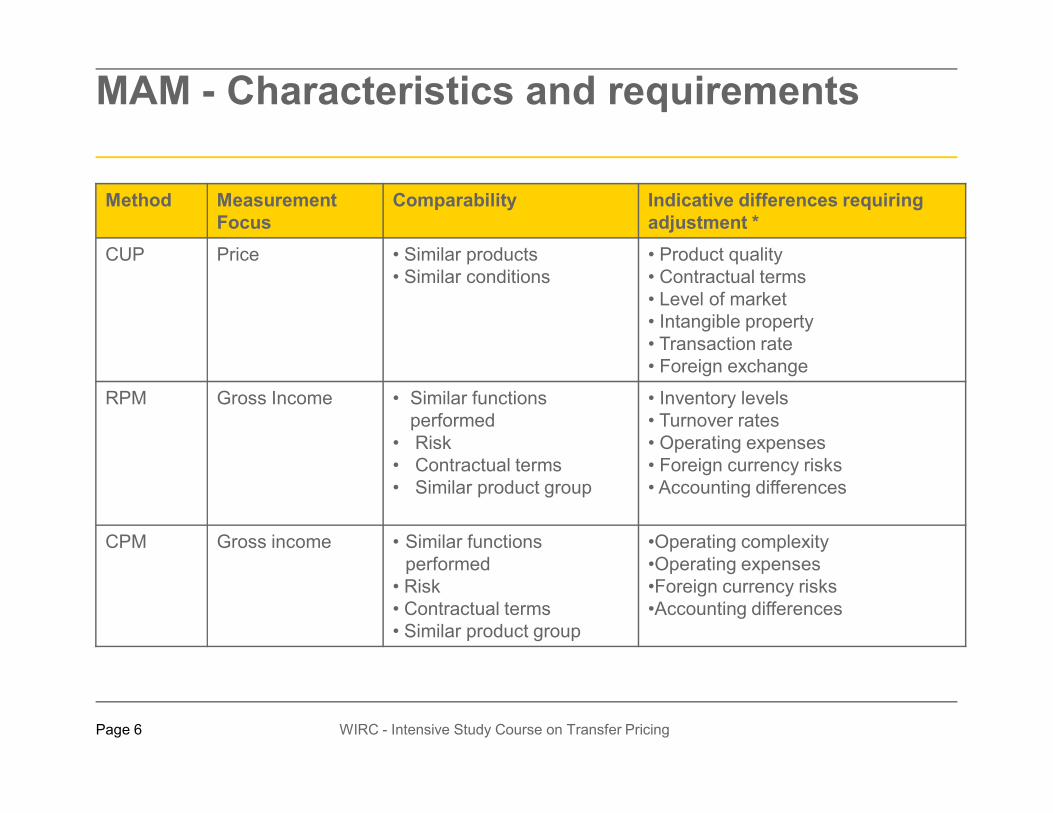

MAM - Characteristics and requirements

Method Measurement

Focus

Comparability Indicative differences requiring

adjustment *

CUP Price • Similar products• Similar conditions

• Product quality• Contractual terms• Level of market• Intangible property• Transaction rate• Foreign exchange

RPM Gross Income • Similar functions • Inventory levels

WIRC - Intensive Study Course on Transfer PricingPage 6

RPM Gross Income • Similar functions performed

• Risk • Contractual terms• Similar product group

• Inventory levels• Turnover rates • Operating expenses• Foreign currency risks• Accounting differences

CPM Gross income • Similar functions performed

• Risk • Contractual terms• Similar product group

•Operating complexity•Operating expenses•Foreign currency risks•Accounting differences

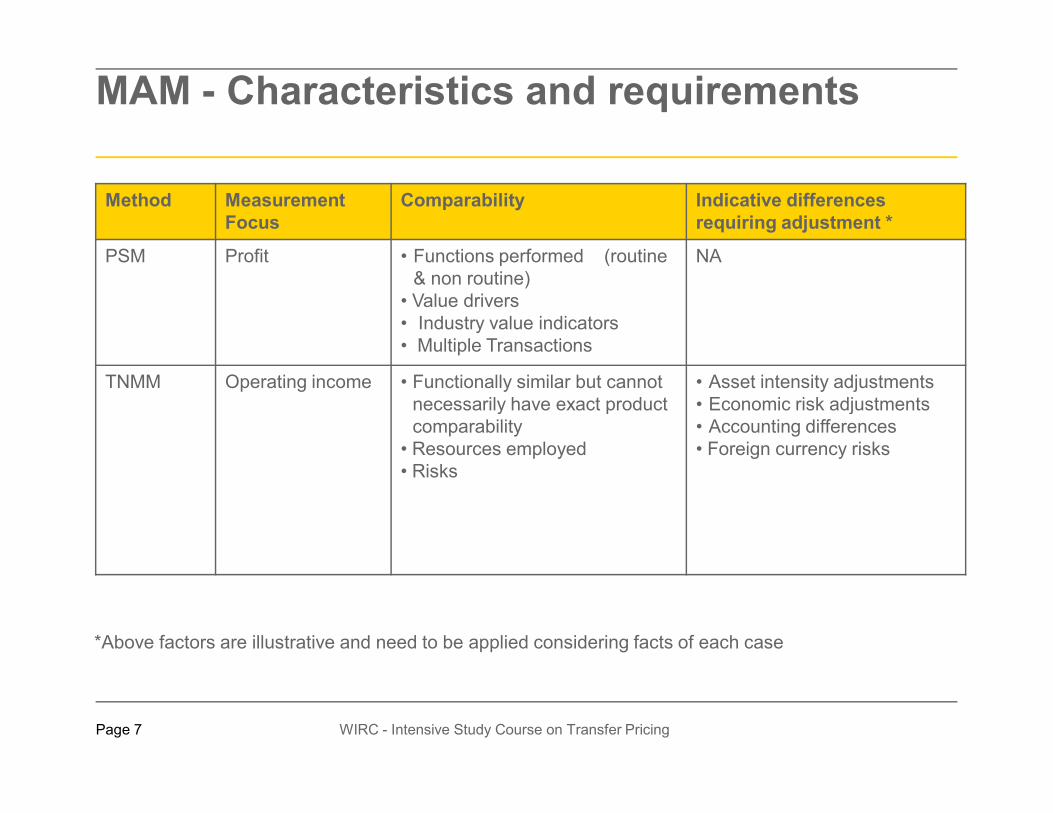

MAM - Characteristics and requirements

Method Measurement

Focus

Comparability Indicative differences

requiring adjustment *

PSM Profit • Functions performed (routine & non routine)

• Value drivers• Industry value indicators• Multiple Transactions

NA

TNMM Operating income • Functionally similar but cannot necessarily have exact product

• Asset intensity adjustments• Economic risk adjustments

WIRC - Intensive Study Course on Transfer PricingPage 7

necessarily have exact product comparability

• Resources employed• Risks

• Economic risk adjustments• Accounting differences• Foreign currency risks

*Above factors are illustrative and need to be applied considering facts of each case

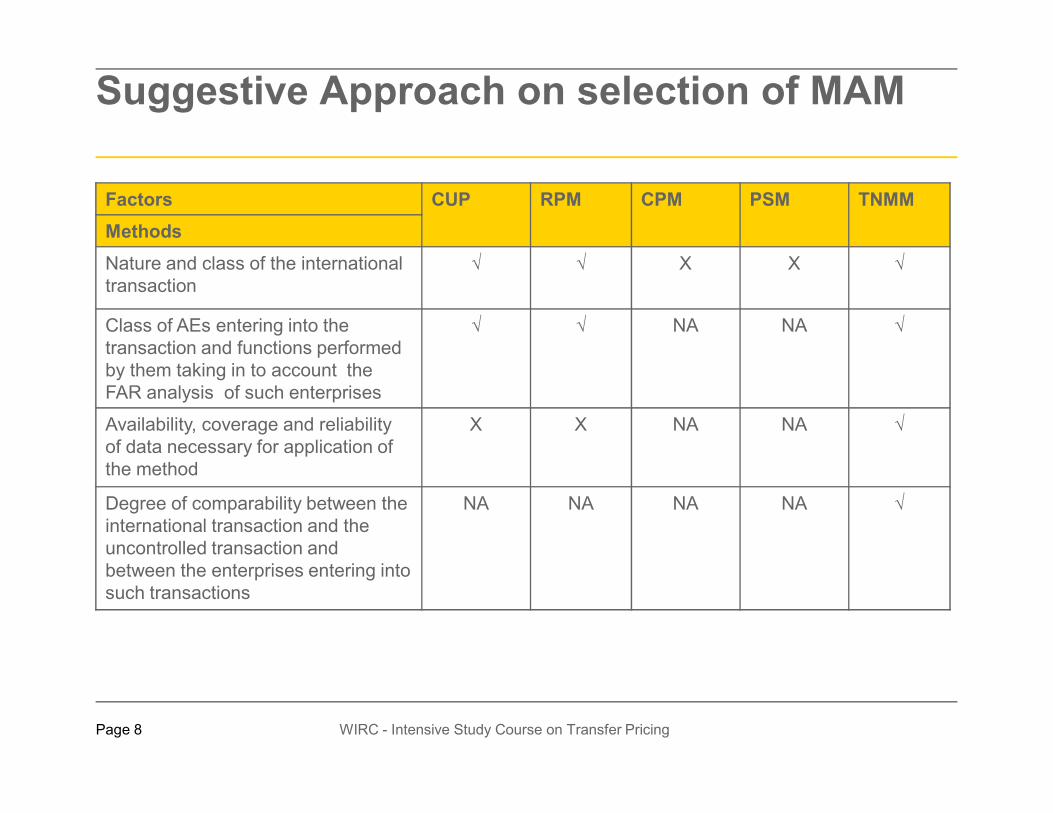

Suggestive Approach on selection of MAM

Factors CUP RPM CPM PSM TNMM

Methods

Nature and class of the internationaltransaction

√ √ X X √

Class of AEs entering into the transaction and functions performed by them taking in to account the FAR analysis of such enterprises

√ √ NA NA √

WIRC - Intensive Study Course on Transfer PricingPage 8

Availability, coverage and reliability of data necessary for application of the method

X X NA NA √

Degree of comparability between the international transaction and the uncontrolled transaction and between the enterprises entering into such transactions

NA NA NA NA √

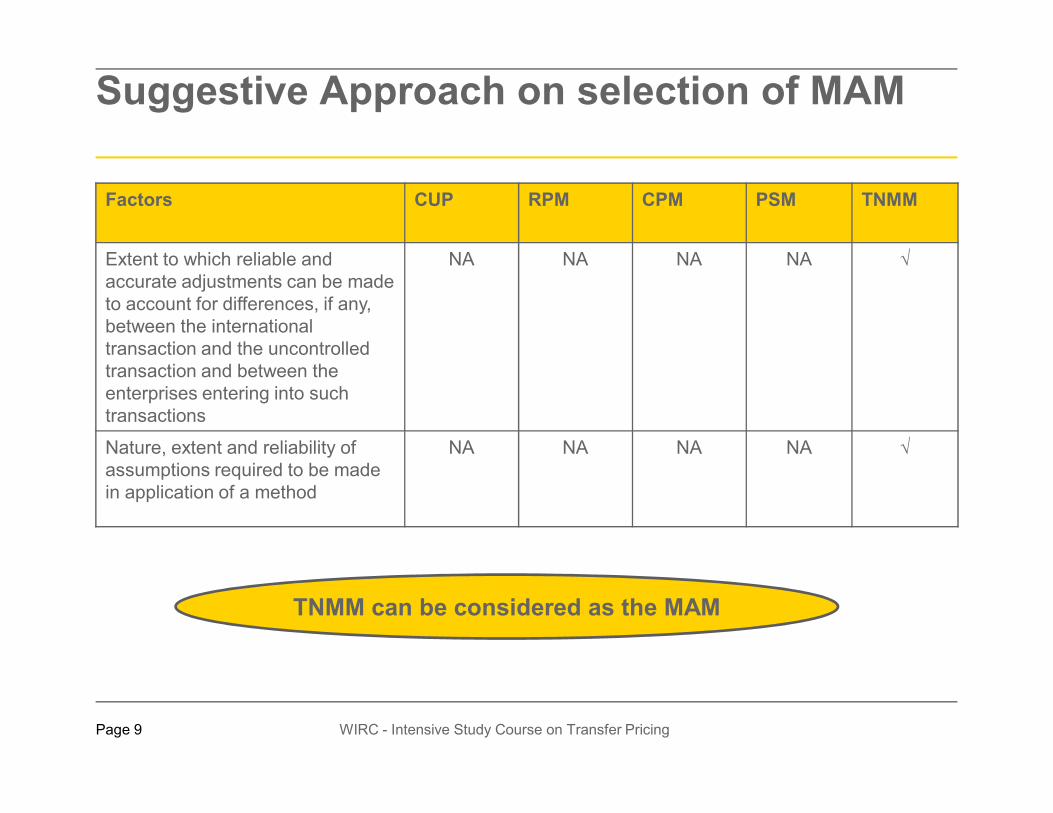

Suggestive Approach on selection of MAM

Factors CUP RPM CPM PSM TNMM

Extent to which reliable and accurate adjustments can be made to account for differences, if any, between the international transaction and the uncontrolled transaction and between the enterprises entering into such transactions

NA NA NA NA √

WIRC - Intensive Study Course on Transfer PricingPage 9

transactions

Nature, extent and reliability ofassumptions required to be made in application of a method

NA NA NA NA √

TNMM can be considered as the MAM

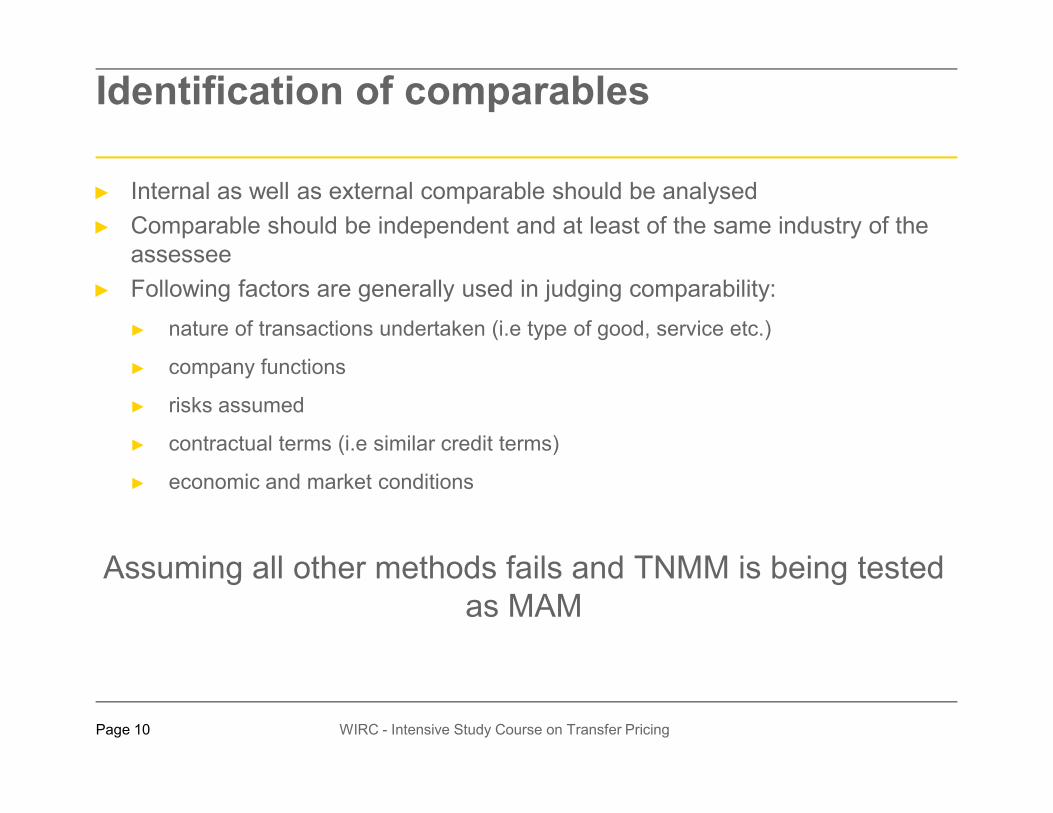

Identification of comparables

► Internal as well as external comparable should be analysed

► Comparable should be independent and at least of the same industry of the assessee

► Following factors are generally used in judging comparability:

► nature of transactions undertaken (i.e type of good, service etc.)

► company functions

► risks assumed

WIRC - Intensive Study Course on Transfer PricingPage 10

► risks assumed

► contractual terms (i.e similar credit terms)

► economic and market conditions

Assuming all other methods fails and TNMM is being tested as MAM

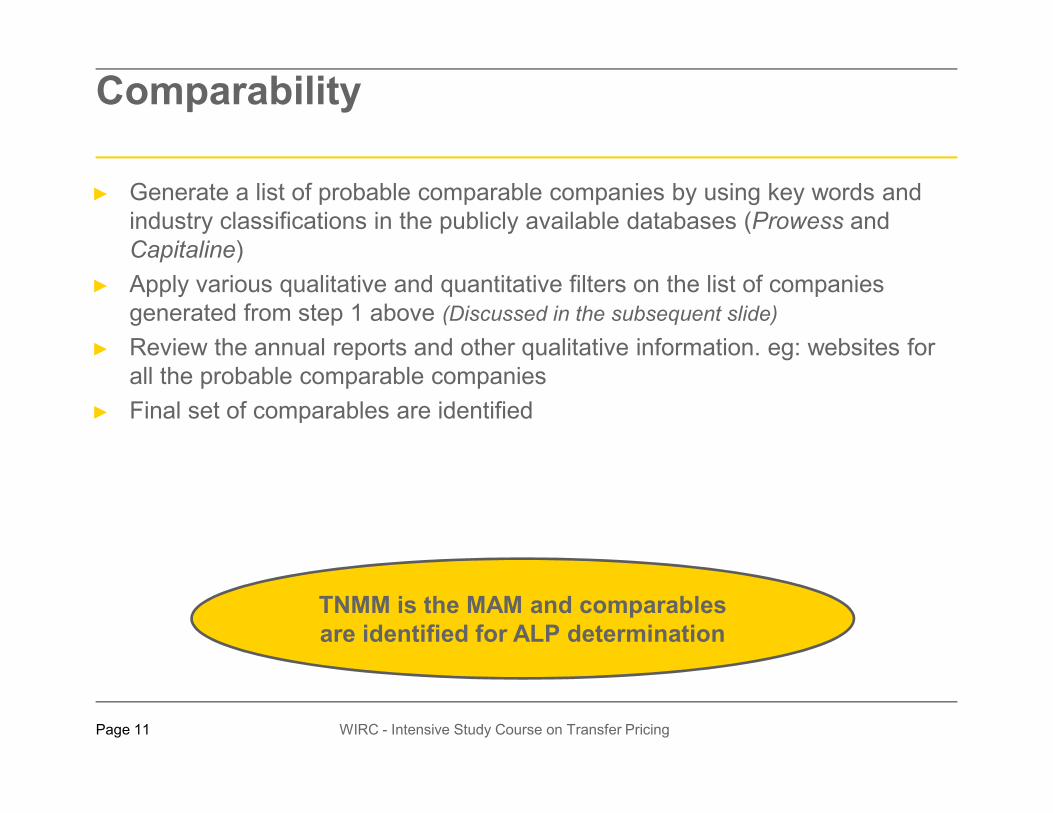

Comparability

► Generate a list of probable comparable companies by using key words and industry classifications in the publicly available databases (Prowess and Capitaline)

► Apply various qualitative and quantitative filters on the list of companies generated from step 1 above (Discussed in the subsequent slide)

► Review the annual reports and other qualitative information. eg: websites for all the probable comparable companies

► Final set of comparables are identified

WIRC - Intensive Study Course on Transfer PricingPage 11

► Final set of comparables are identified

TNMM is the MAM and comparables

are identified for ALP determination

Criteria for selection of comparables

► Analysis of the list of probable comparable companies generated by the databases is undertaken based on the following criterion:

► Insufficient financial data;

► No operations/ Sick companies/ persistent loss makers;

► Functionally different;

► Companies having significant related party transactions;

WIRC - Intensive Study Course on Transfer PricingPage 12

► Companies with exceptional year(s) of operations; and

► Other specific filter such as ‘turnover’, ‘trading income’ etc

ALP Determination

► Once the final set of comparables are arrived at, their operating margin should be computed

► Multiple year data may also be used to capture market cycles and reduce the likelihood of financial results of an anomalous year distorting the arm’s length margin

► If required, any accounting differences should be adjusted

► The Average operating margin of identified comparables are computed (in

WIRC - Intensive Study Course on Transfer PricingPage 13

► The Average operating margin of identified comparables are computed (in case of multiple ALP margins are arrived at) and based on the same, the ALP would be determined

X Inc USAProvision of software development services to X Inc Compensation on basis of costs incurred

Case Study 1 - TP Method

Outside India

WIRC - Intensive Study Course on Transfer PricingPage 14

X Ltd India

► The company does not provide service to third parties

► Pricing policy of companies are more or less influenced by competition but not any industry benchmark

India

Case study 2 - Economic Analysis

ABC Inc

100%

Provision of software development services

Outside India

► Value of services provided by ABC India to its AE, ABC Inc -Rs 50 crore

► Benchmarking is done using External TNMM

► Assessee conducted a search for comparables (as tabulated in the next slide) with the objective of identifying –

WIRC - Intensive Study Course on Transfer PricingPage 15

ABC India

100% subsidiary In India

objective of identifying –

► Independent companies that perform similar functions and

► Operate in broadly similar Markets to that of ABC India’s business profile

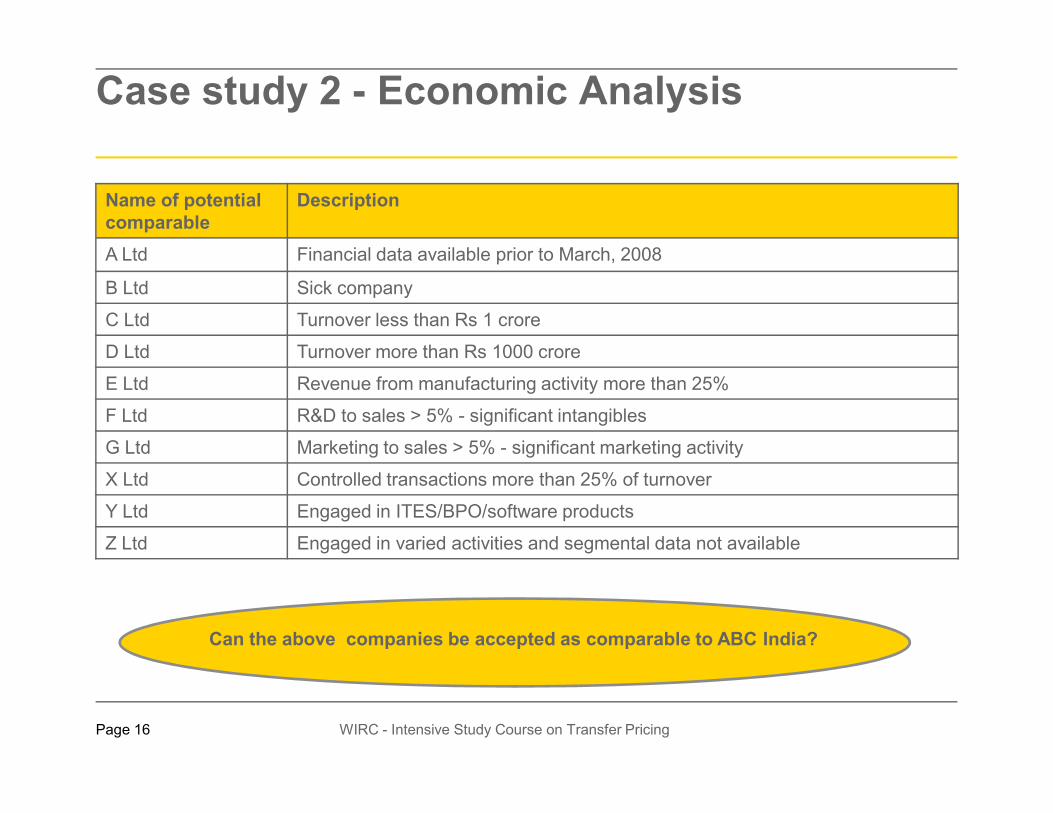

Case study 2 - Economic Analysis

Name of potential

comparable

Description

A Ltd Financial data available prior to March, 2008

B Ltd Sick company

C Ltd Turnover less than Rs 1 crore

D Ltd Turnover more than Rs 1000 crore

E Ltd Revenue from manufacturing activity more than 25%

F Ltd R&D to sales > 5% - significant intangibles

WIRC - Intensive Study Course on Transfer PricingPage 16

F Ltd R&D to sales > 5% - significant intangibles

G Ltd Marketing to sales > 5% - significant marketing activity

X Ltd Controlled transactions more than 25% of turnover

Y Ltd Engaged in ITES/BPO/software products

Z Ltd Engaged in varied activities and segmental data not available

Can the above companies be accepted as comparable to ABC India?

X Inc USA

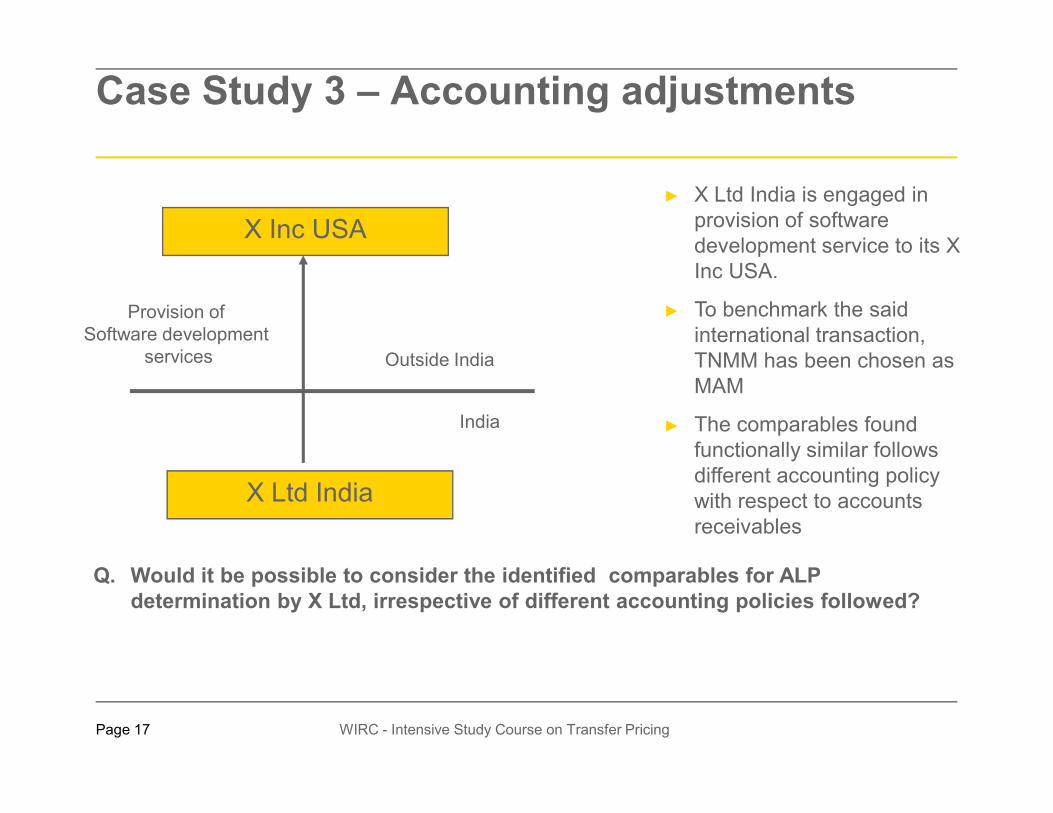

Case Study 3 – Accounting adjustments

Outside India

Provision of Software development

services

► X Ltd India is engaged in provision of software development service to its X Inc USA.

► To benchmark the said international transaction, TNMM has been chosen as MAM

WIRC - Intensive Study Course on Transfer PricingPage 17

X Ltd India

Q. Would it be possible to consider the identified comparables for ALP

determination by X Ltd, irrespective of different accounting policies followed?

India ► The comparables found functionally similar follows different accounting policy with respect to accounts receivables

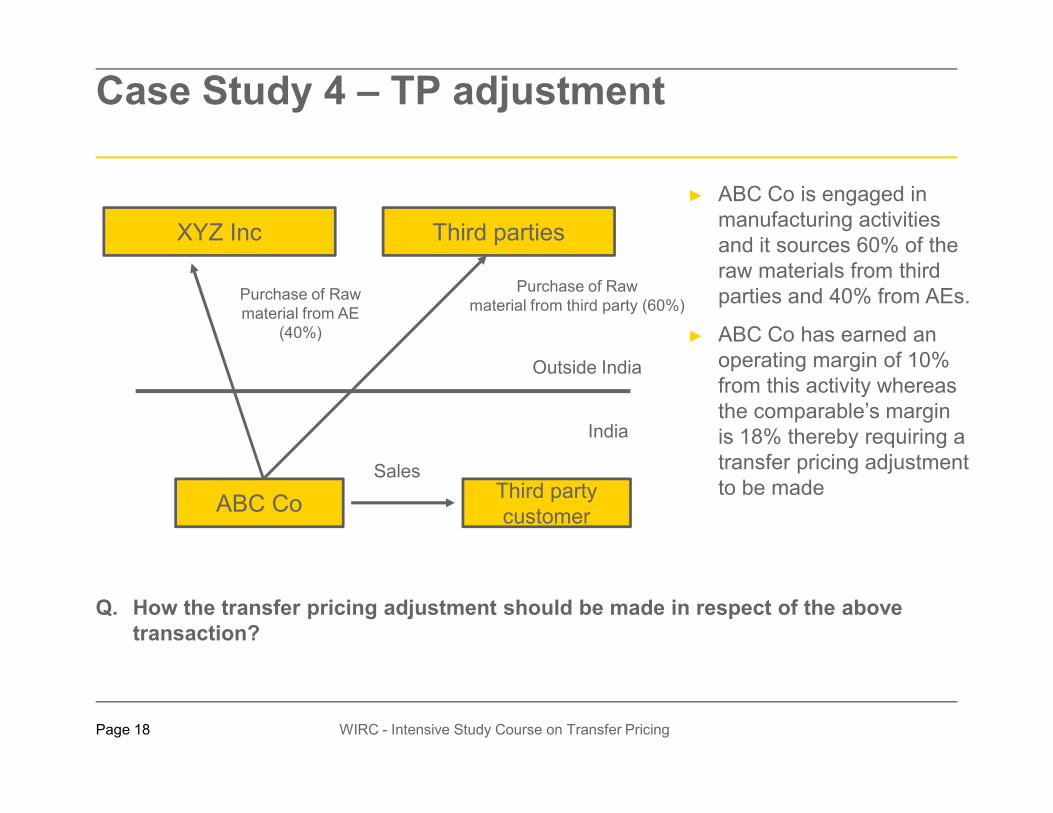

Case Study 4 – TP adjustment

XYZ Inc

Outside India

Purchase of Raw material from AE

(40%)

► ABC Co is engaged in manufacturing activities and it sources 60% of the raw materials from third parties and 40% from AEs.

► ABC Co has earned an operating margin of 10% from this activity whereas the comparable’s margin

Purchase of Raw material from third party (60%)

Third parties

WIRC - Intensive Study Course on Transfer PricingPage 18

Q. How the transfer pricing adjustment should be made in respect of the above

transaction?

ABC Co

Indiathe comparable’s margin is 18% thereby requiring a transfer pricing adjustment to be madeThird party

customer

Sales

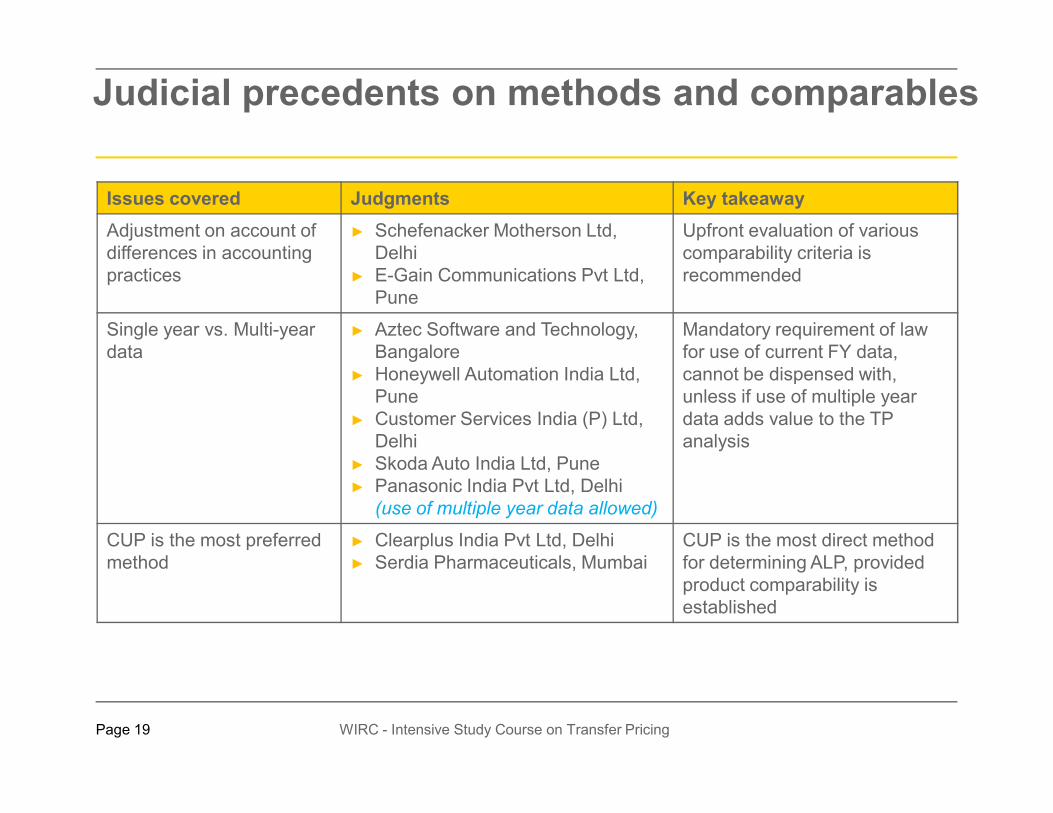

Judicial precedents on methods and comparables

Issues covered Judgments Key takeaway

Adjustment on account of differences in accounting practices

► Schefenacker Motherson Ltd,Delhi

► E-Gain Communications Pvt Ltd,Pune

Upfront evaluation of various comparability criteria is recommended

Single year vs. Multi-yeardata

► Aztec Software and Technology, Bangalore

► Honeywell Automation India Ltd, Pune

Mandatory requirement of law for use of current FY data,cannot be dispensed with, unless if use of multiple year

WIRC - Intensive Study Course on Transfer PricingPage 19

► Customer Services India (P) Ltd, Delhi

► Skoda Auto India Ltd, Pune► Panasonic India Pvt Ltd, Delhi (use of multiple year data allowed)

data adds value to the TP analysis

CUP is the most preferred method

► Clearplus India Pvt Ltd, Delhi► Serdia Pharmaceuticals, Mumbai

CUP is the most direct method for determining ALP, provided product comparability is established

Judicial precedents on methods and comparables

Issues covered Judgments Key takeaway

Applicability of +/-5% range in case of one price

► Perot Systems TSI, Delhi► Essar Steel Ltd, Visakhapatnam

Relief of +/-5% is available only when more than one price is determined by the most appropriate method

Whether +/-5% range is a standard deduction

► Development Consultants Pvt Ltd, Calcutta

► Skoda Auto India Pvt Ltd, Pune► Sony India Pvt Ltd, Delhi

Diverse views on the subject

WIRC - Intensive Study Course on Transfer PricingPage 20

► Sony India Pvt Ltd, Delhi► Philips Software Centre P. Ltd, Bangalore► Schefenacker Motherson Ltd, Delhi► Toshiba India Ltd, Delhi► UE Trade Corporation (India) Pvt Ltd,

Delhi► Cummins India Ltd, Pune► SAP Labs India Pvt Ltd, Bangalore► BASF India Ltd, Mumbai► Technimount Icb Pvt Ltd, Mumbai► Marubeni India Pvt Ltd, Delhi (not allowed)

► Global Vantedge Pvt Ltd, Delhi (not allowed)

Judicial precedents on methods and comparables

Issues covered Judgments Key takeaway

Whether +/-5% benefit is applicable in case ALP is determined using only one method

► ADP Pvt Ltd, Hyderabad (+/-5% benefit not allowed if ALP

determined using one method)

► Electrobug Technologies Ltd, Delhi (+/-5% benefit allowed even if ALP determined using one

method)

Diverse views on the subject

Use of foreign tested ► Development Consultants Pvt Diverse views on the subject –

WIRC - Intensive Study Course on Transfer PricingPage 21

Use of foreign tested party / comparables

► Development Consultants Pvt Ltd, Calcutta (allowed use of foreign tested party)

► Ranbaxy Laboratories Ltd, Delhi (not allowed)

► Global Vantedge Pvt Ltd, Delhi (not allowed)

Diverse views on the subject –further development to be seenGlobally accepted view – Tested party should be the lesser complex entity

Start-up / Idle capacity and working capital adjustment

► Global Vantedge Pvt. Ltd, Delhi► Vertex Customer Services, Delhi► Sony India Pvt Ltd, Delhi► Fiat India Pvt Ltd, Mumbai

All judgments in favour of taxpayers. Upfront evaluation of such adjustments is recommended

Judicial precedents on methods and comparables

Issues covered Judgments Key takeaway

Applicability of turnover filter

► E-Gain Communications Pvt Ltd, Pune

► Indo American Jewellery, Mumbai► Symantec Software Solutions

Private Ltd, Mumbai (rejected use of turnover filter)

► DHL express (India) Pvt Ltd, Mumbai (rejection of companies with turnover < 20% of assessee’s

Diverse views on the subject

WIRC - Intensive Study Course on Transfer PricingPage 22

with turnover < 20% of assessee’s

turnover)

Abnormal/ supernormal profitability of comparables

► Agnity India Technologies Pvt Ltd, Delhi

► Adobe Systems India Pvt Ltd, Delhi► Quark Systems Pvt Ltd, Punjab

and Haryana HC► Sapient Corporation Pvt Ltd, Delhi

Companies earning abnormal profits should not be treated as comparables

Thank you

WIRC - Intensive Study Course on Transfer PricingPage 23

Thank you

The discussions in this presentation are personal views of the speaker and are intended to provide only a general outline of the subjects covered. The presentation should not be regarded as comprehensive or sufficient for making decisions, nor should it be used in place of professional advice, which should always have regard for the particular commercial facts and circumstances. Accordingly, Ernst & Young Private Ltd accepts no responsibility for loss arising from any action taken or not taken by anyone by relying on this presentation.