Embed Size (px)

Citation preview

Wine Grape Growers Australia

WGGA program report

Murray Darling Swan Hill, Aug 2014

August 2014 Wine Grape Growers Australia Slide 2

Today’s agenda …

1. WGGA’s priorities for 2014-15

2. Detailed discussion on the top priorities

i. Biosecurity

ii. Market access (how your grapes get sold)

iii. Knowledge and information

iv. RD&E

v. Organisational structure

3. Supply and demand going into 2015

August 2014 Wine Grape Growers Australia Slide 3

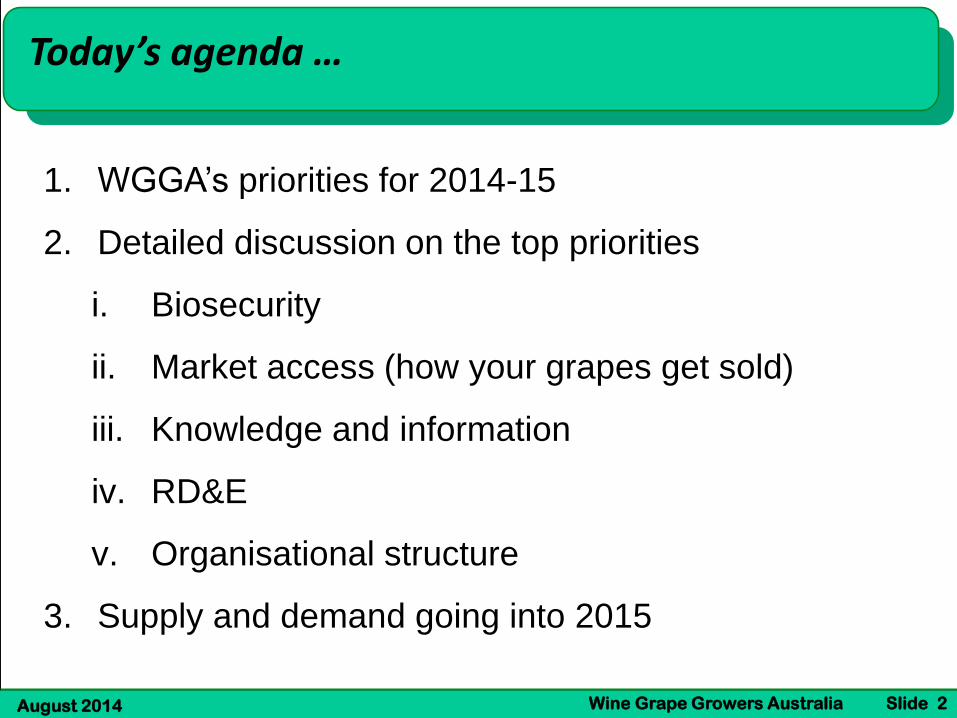

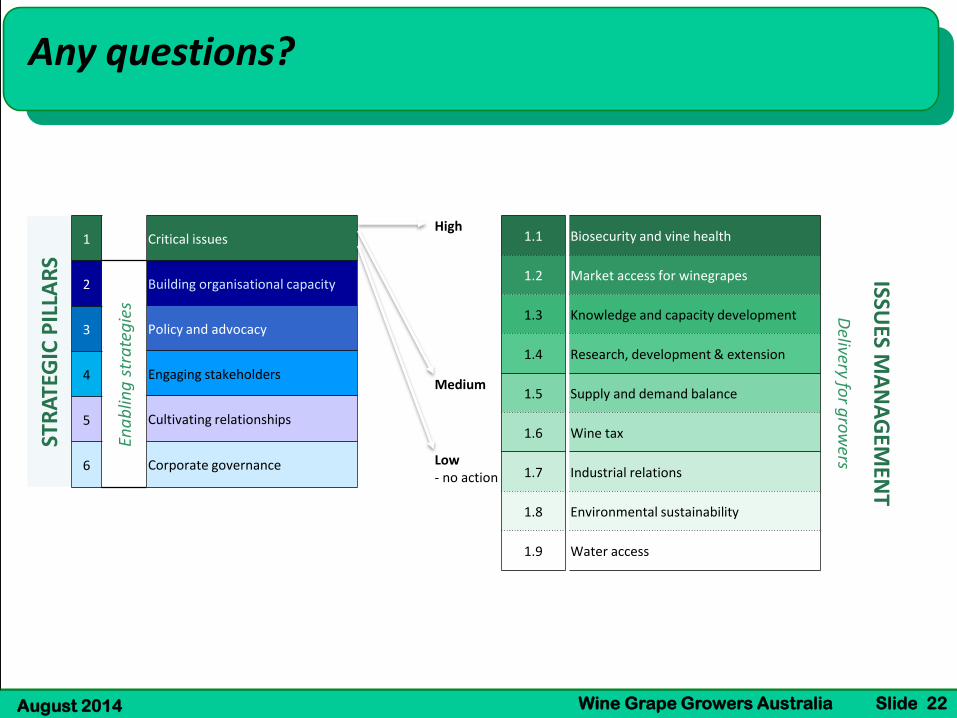

WGGA Strategic Priorities, 2014-15 …ST

RA

TEG

IC P

ILLA

RS

1

2

3

4

5

6

Ena

blin

g s

tra

teg

ies

Critical issues

Building organisational capacity

Policy and advocacy

Engaging stakeholders

Cultivating relationships

Corporate governance

High

Medium

Low - no action

1.1

1.2

1.3

1.4

1.5

1.6

1.7

1.8

1.9

Biosecurity and vine health

Market access for winegrapes

Knowledge and capacity development

Research, development & extension

Supply and demand balance

Wine tax

Industrial relations

Environmental sustainability

Water access

Delivery fo

r gro

wers

ISSUES M

AN

AG

EMEN

T

August 2014 Wine Grape Growers Australia Slide 4

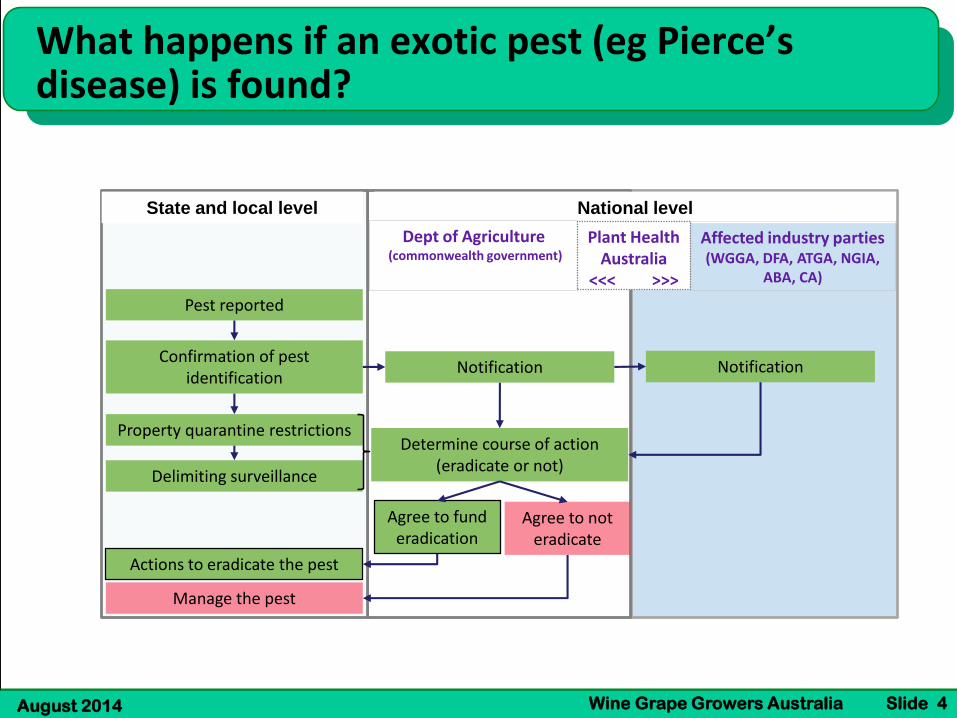

What happens if an exotic pest (eg Pierce’s disease) is found?

Pest reported

Confirmation of pest identification

Notification

Property quarantine restrictions

Delimiting surveillance

Actions to eradicate the pest

Determine course of action (eradicate or not)

Agree to fund eradication

State and local level National level

Dept of Agriculture(commonwealth government)

Affected industry parties (WGGA, DFA, ATGA, NGIA,

ABA, CA)

Notification

Agree to not eradicate

Manage the pest

Plant Health Australia

<<< >>>

August 2014 Wine Grape Growers Australia Slide 5

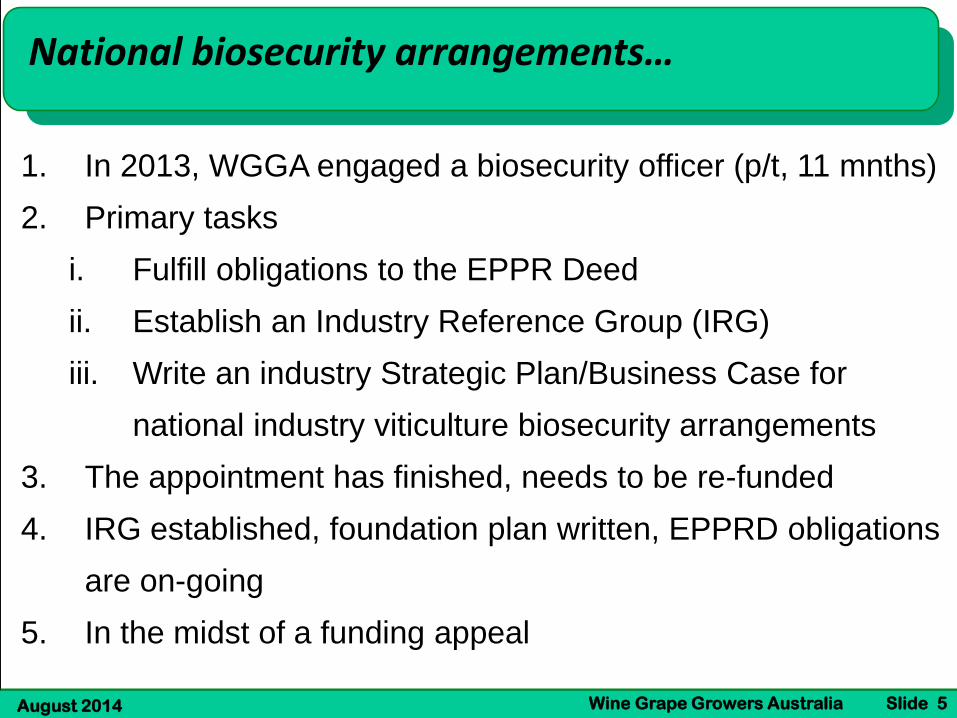

National biosecurity arrangements…

1. In 2013, WGGA engaged a biosecurity officer (p/t, 11 mnths)

2. Primary tasks

i. Fulfill obligations to the EPPR Deed

ii. Establish an Industry Reference Group (IRG)

iii. Write an industry Strategic Plan/Business Case for

national industry viticulture biosecurity arrangements

3. The appointment has finished, needs to be re-funded

4. IRG established, foundation plan written, EPPRD obligations

are on-going

5. In the midst of a funding appeal

August 2014 Wine Grape Growers Australia Slide 6

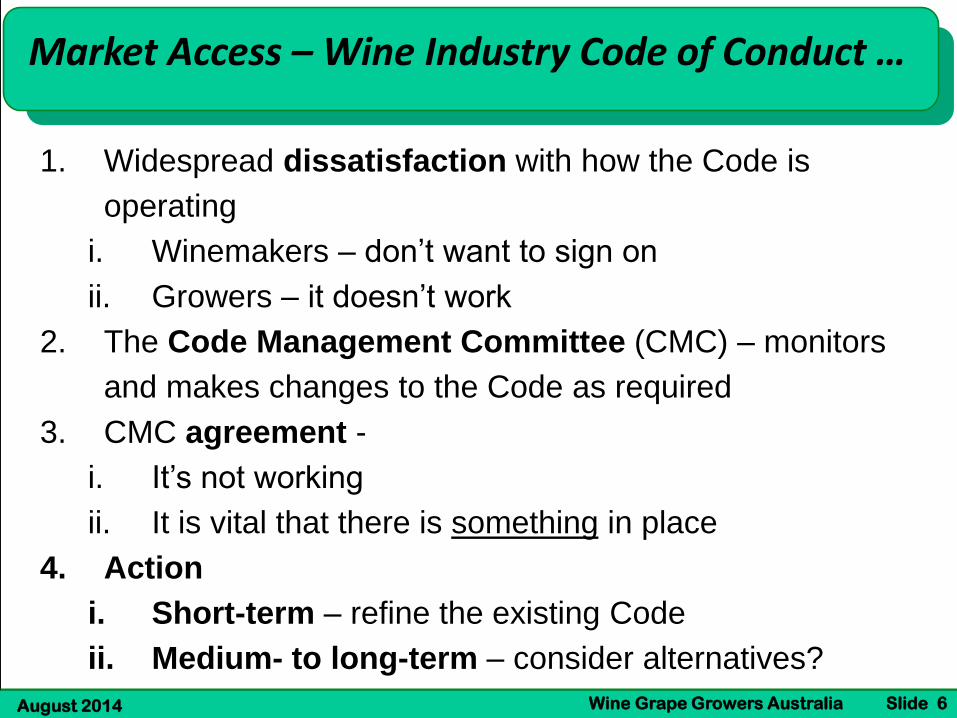

Market Access – Wine Industry Code of Conduct …

1. Widespread dissatisfaction with how the Code is

operating

i. Winemakers – don’t want to sign on

ii. Growers – it doesn’t work

2. The Code Management Committee (CMC) – monitors

and makes changes to the Code as required

3. CMC agreement -

i. It’s not working

ii. It is vital that there is something in place

4. Action

i. Short-term – refine the existing Code

ii. Medium- to long-term – consider alternatives?

August 2014 Wine Grape Growers Australia Slide 7

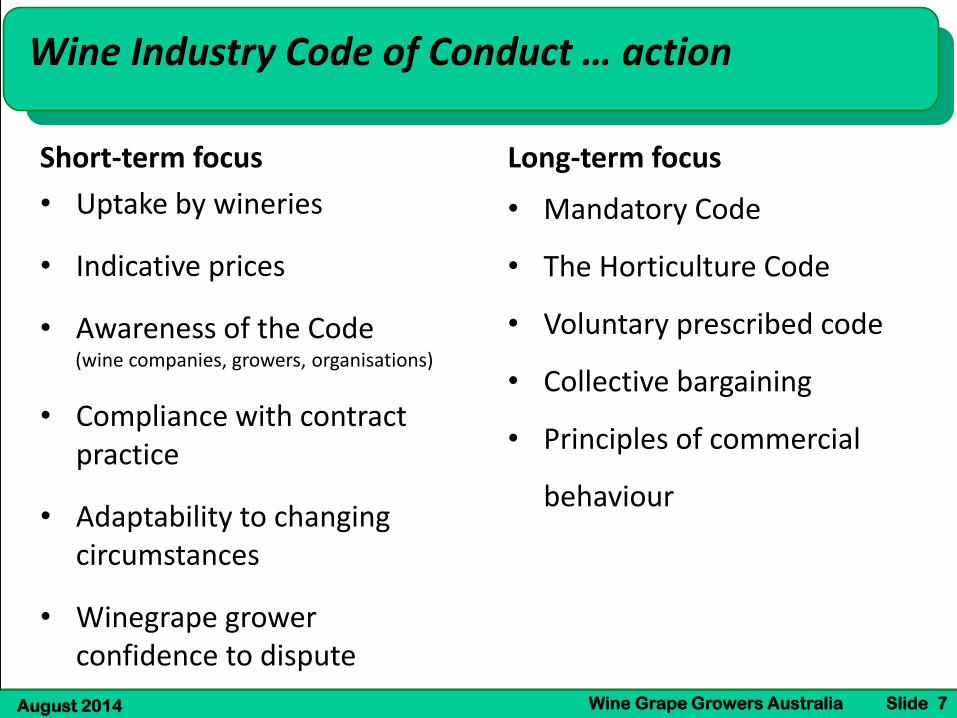

Wine Industry Code of Conduct … action

Short-term focus

• Uptake by wineries

• Indicative prices

• Awareness of the Code(wine companies, growers, organisations)

• Compliance with contract practice

• Adaptability to changing circumstances

• Winegrape grower confidence to dispute

Long-term focus

• Mandatory Code

• The Horticulture Code

• Voluntary prescribed code

• Collective bargaining

• Principles of commercial

behaviour

August 2014 Wine Grape Growers Australia Slide 8

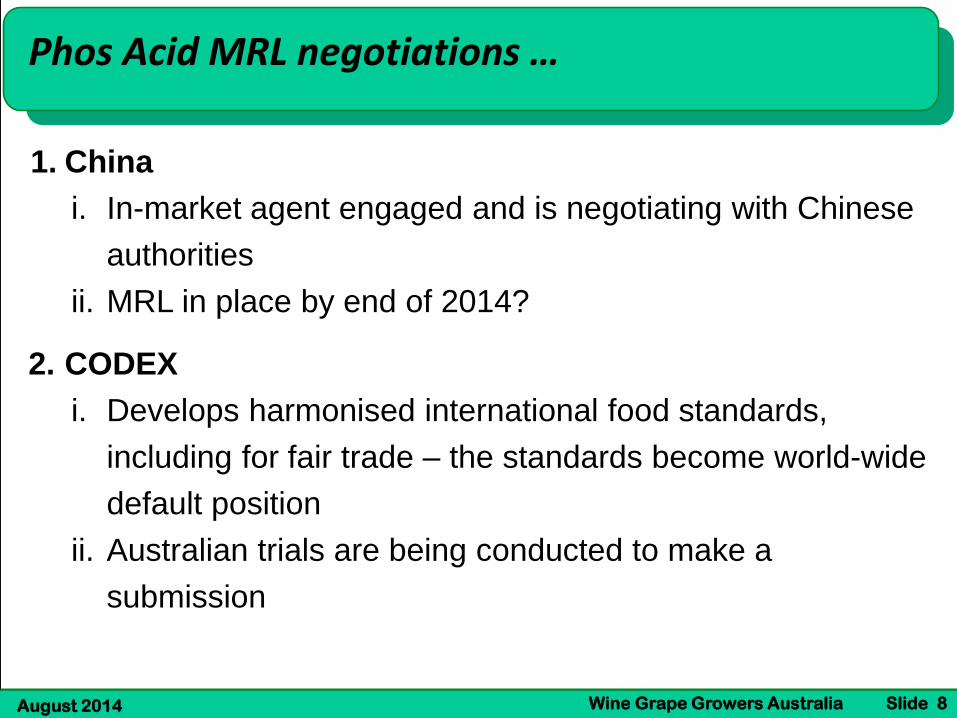

Phos Acid MRL negotiations …

1. China

i. In-market agent engaged and is negotiating with Chinese

authorities

ii. MRL in place by end of 2014?

2. CODEX

i. Develops harmonised international food standards,

including for fair trade – the standards become world-wide

default position

ii. Australian trials are being conducted to make a

submission

August 2014 Wine Grape Growers Australia Slide 9

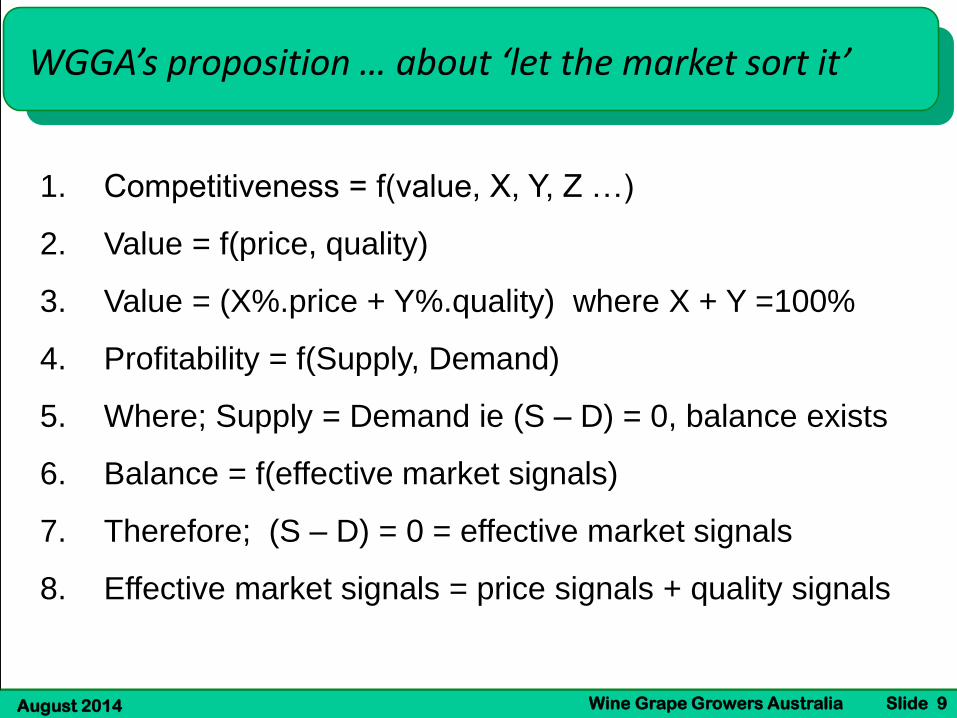

WGGA’s proposition … about ‘let the market sort it’

1. Competitiveness = f(value, X, Y, Z …)

2. Value = f(price, quality)

3. Value = (X%.price + Y%.quality) where X + Y =100%

4. Profitability = f(Supply, Demand)

5. Where; Supply = Demand ie (S – D) = 0, balance exists

6. Balance = f(effective market signals)

7. Therefore; (S – D) = 0 = effective market signals

8. Effective market signals = price signals + quality signals

August 2014 Wine Grape Growers Australia Slide 10

Traditional commercial practices do not provide effective

market signals …

… there are numerous commercial practices in the sector that

prevent the industry adjusting

1. Problems in the vineyard investment dynamic

2. Problems with price determination mechanisms

3. Problems with terms of trade (unfair sharing of risk)

4. Growers are deprived of effective decision-making tools

… it’s about market signals that don’t work to help the market

operate effectively

… it’s about practices that are unfair to growers

August 2014 Wine Grape Growers Australia Slide 11

Market signals for quality …

WFA Expert Review;

“Improving quality … has the potential to help address the oversupply of

commercial grade grapes”

“WGGA … advocated the importance of stronger market signals being sent to

growers through the adoption of objective measurement systems”

“WFA does not support such systems being adopted at the industry level”

“Ultimately, WFA believes that economic forces will continue to be the primary

driver to further adjustments in the market.”

August 2014 Wine Grape Growers Australia Slide 12

0

200

400

600

800

1000

1200

1400

1600

1800

20009

0 -

91

91

-92

92

-93

93

-94

94

-95

95

-96

96

-97

97

-98

98

-99

99

-00

00

-01

01

-02

02

-03

03

-04

04

-05

05

-06

06

-07

07

-08

08

-09

09

-10

10

-11

11

-12

12

-13

13

-14

14

-15

15

-16

16

-17

0

15

30

45

60

75

90

105

120

135

150

Pro

du

ctio

n (

bar

s) t

on

ne

s ‘0

00

Be

arin

g ar

ea

(sh

ade

d b

ackg

rou

nd

)h

ect

are

s ‘0

00

Bearing Area Red White Tonnages left

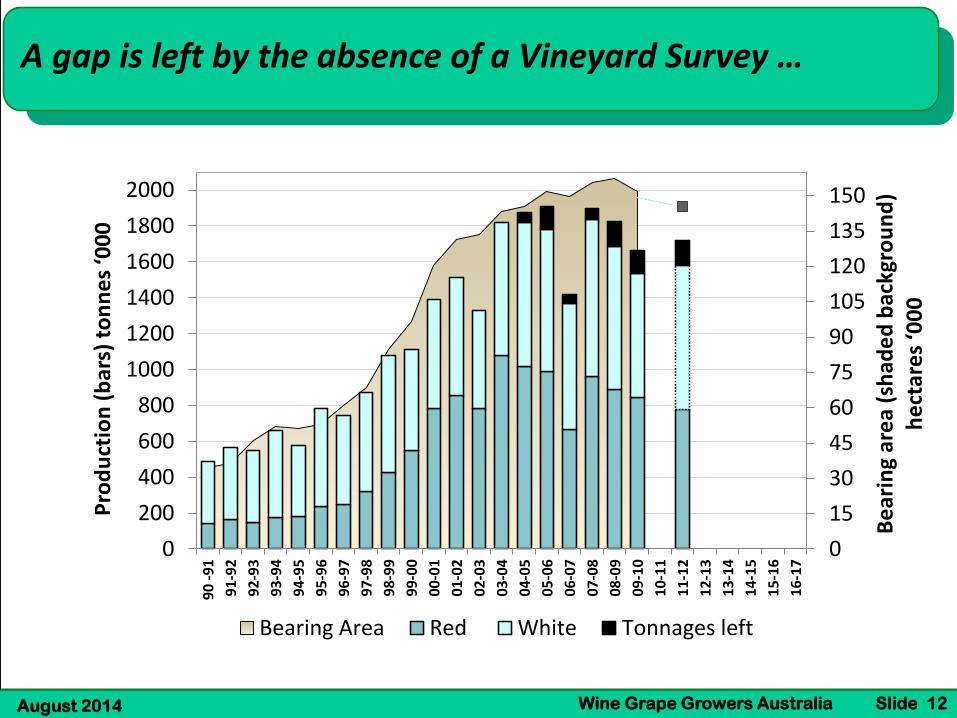

A gap is left by the absence of a Vineyard Survey …

August 2014 Wine Grape Growers Australia Slide 13

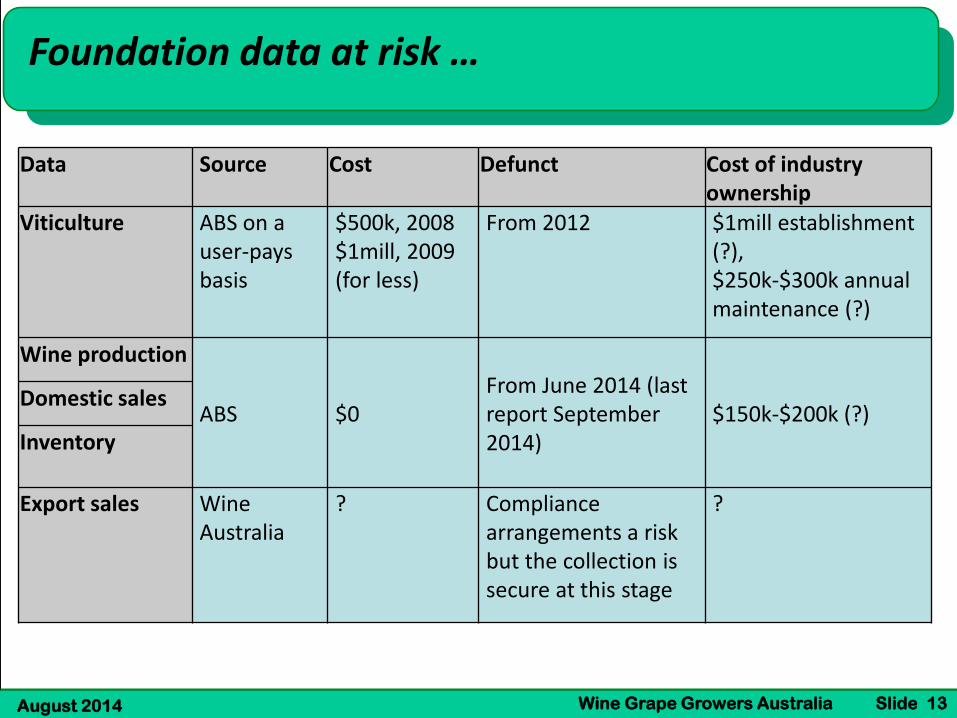

Foundation data at risk …

Data Source Cost Defunct Cost of industry ownership

Viticulture ABS on a user-pays basis

$500k, 2008$1mill, 2009 (for less)

From 2012 $1mill establishment (?), $250k-$300k annual maintenance (?)

Wine production

ABS $0 From June 2014 (last report September 2014)

$150k-$200k (?)Domestic sales

Inventory

Export sales Wine Australia

? Compliance arrangements a risk but the collection is secure at this stage

?

August 2014 Wine Grape Growers Australia Slide 14

Research, Development & Extension …

1. WGGA has a policy – www.wgga.com.au

2. A unified WGGA/WFA RD&E Policy is being scoped

… in a brave new world, industry RD&E (GWRDC) is now

merged with industry marketing/regulation and knowledge

development (Wine Australia Corporation),

… so that all these functions have the same agenda and

strategy.

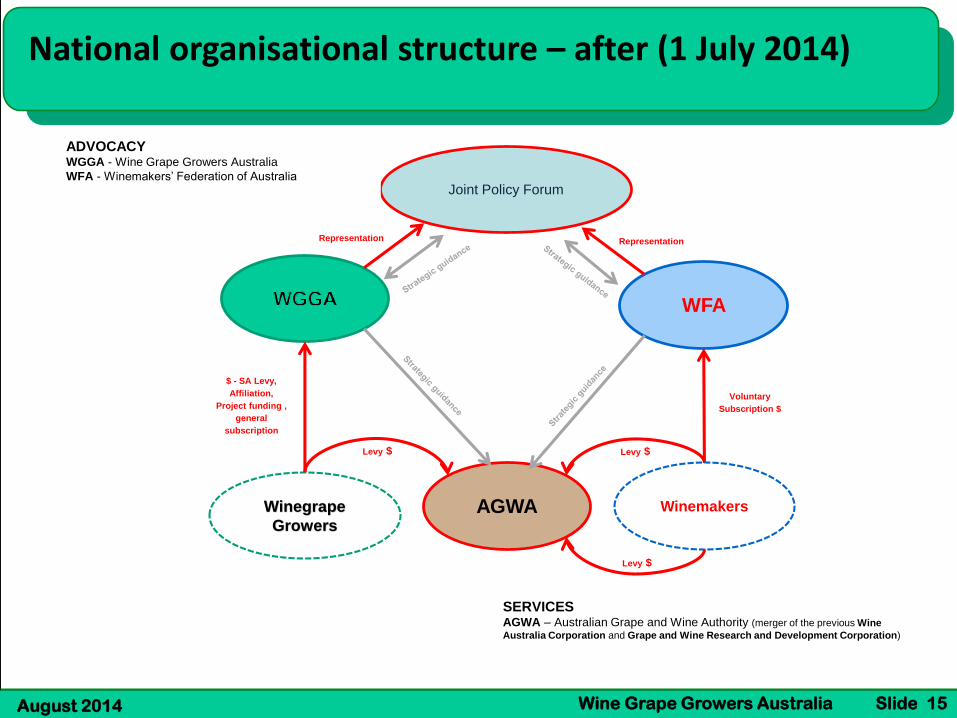

August 2014 Wine Grape Growers Australia Slide 15

AGWA

WFA

$ - SA Levy,

Affiliation,

Project funding ,

general

subscription

Levy $

Levy $ Levy $

WinemakersWinegrape

Growers

Voluntary

Subscription $

SERVICES AGWA – Australian Grape and Wine Authority (merger of the previous Wine

Australia Corporation and Grape and Wine Research and Development Corporation)

Joint Policy Forum

RepresentationRepresentation

ADVOCACYWGGA - Wine Grape Growers Australia

WFA - Winemakers’ Federation of Australia

National organisational structure – after (1 July 2014)

August 2014 Wine Grape Growers Australia Slide 16

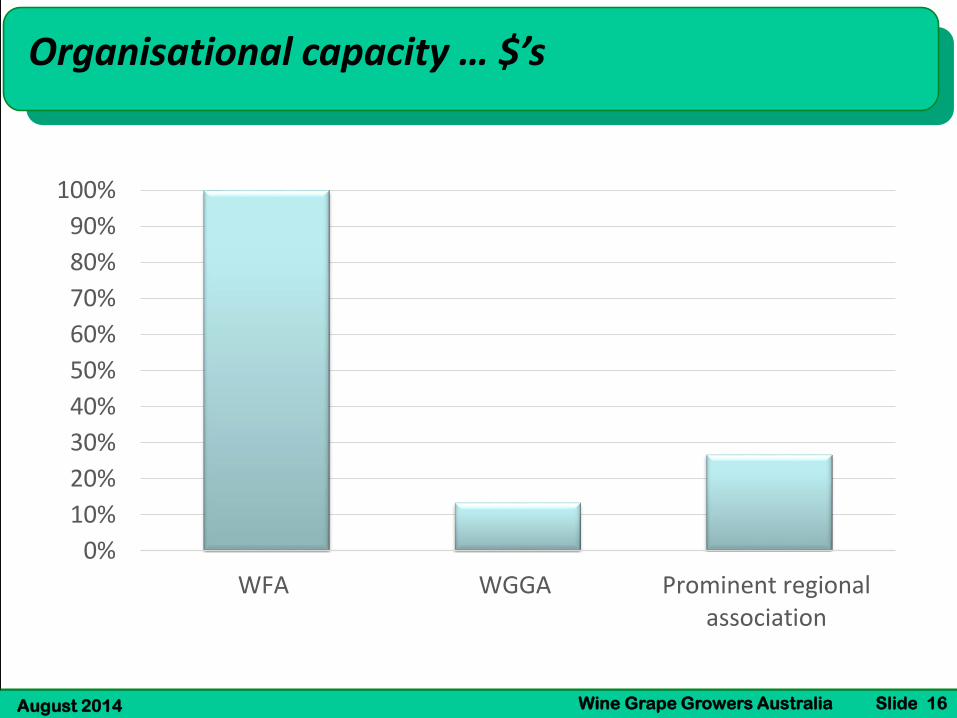

Organisational capacity … $’s

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

WFA WGGA Prominent regionalassociation

August 2014 Wine Grape Growers Australia Slide 17

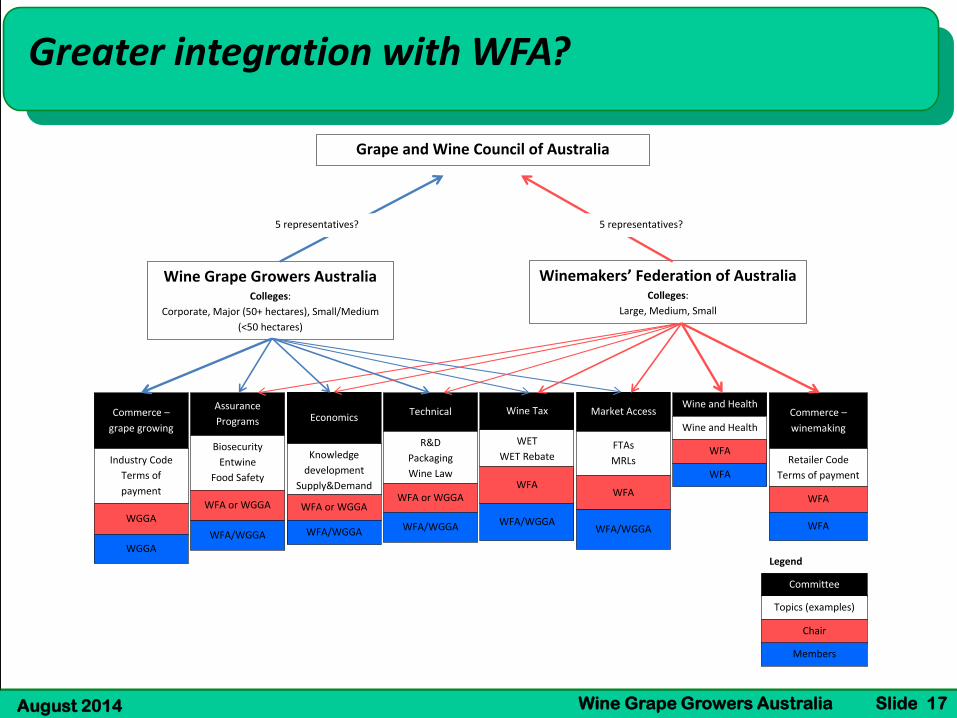

Greater integration with WFA?

Assurance

Programs

Biosecurity

Entwine

Food Safety

WFA or WGGA

WFA/WGGA

Economics

Knowledge

development

Supply&Demand

WFA or WGGA

WFA/WGGA

Technical

R&D

Packaging

Wine Law

WFA or WGGA

WFA/WGGA

Wine Tax

WET

WET Rebate

WFA

WFA/WGGA

Market Access

FTAs

MRLs

WFA

WFA/WGGA

Wine and Health

Wine and Health

WFA

WFA

Commerce –

winemaking

Retailer Code

Terms of payment

WFA

WFA

Commerce –

grape growing

Industry Code

Terms of

payment

WGGA

WGGA

Committee

Topics (examples)

Chair

Members

Legend

Wine Grape Growers Australia Colleges:

Corporate, Major (50+ hectares), Small/Medium

(<50 hectares)

Winemakers’ Federation of Australia Colleges:

Large, Medium, Small

5 representatives? 5 representatives?

Grape and Wine Council of Australia

August 2014 Wine Grape Growers Australia Slide 18

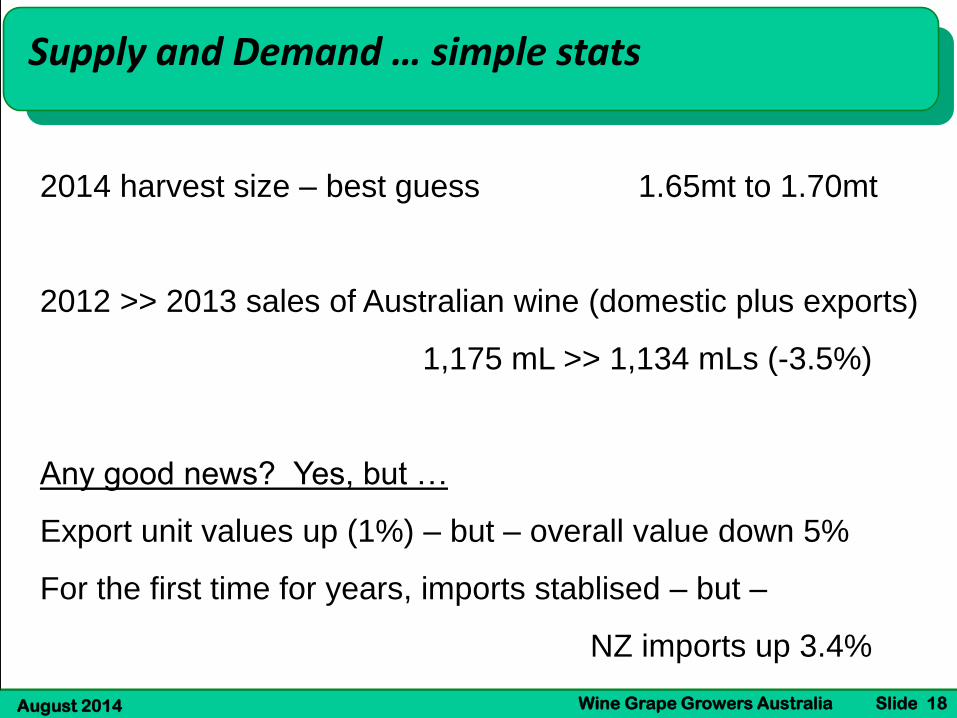

Supply and Demand … simple stats

2014 harvest size – best guess 1.65mt to 1.70mt

2012 >> 2013 sales of Australian wine (domestic plus exports)

1,175 mL >> 1,134 mLs (-3.5%)

Any good news? Yes, but …

Export unit values up (1%) – but – overall value down 5%

For the first time for years, imports stablised – but –

NZ imports up 3.4%

August 2014 Wine Grape Growers Australia Slide 19

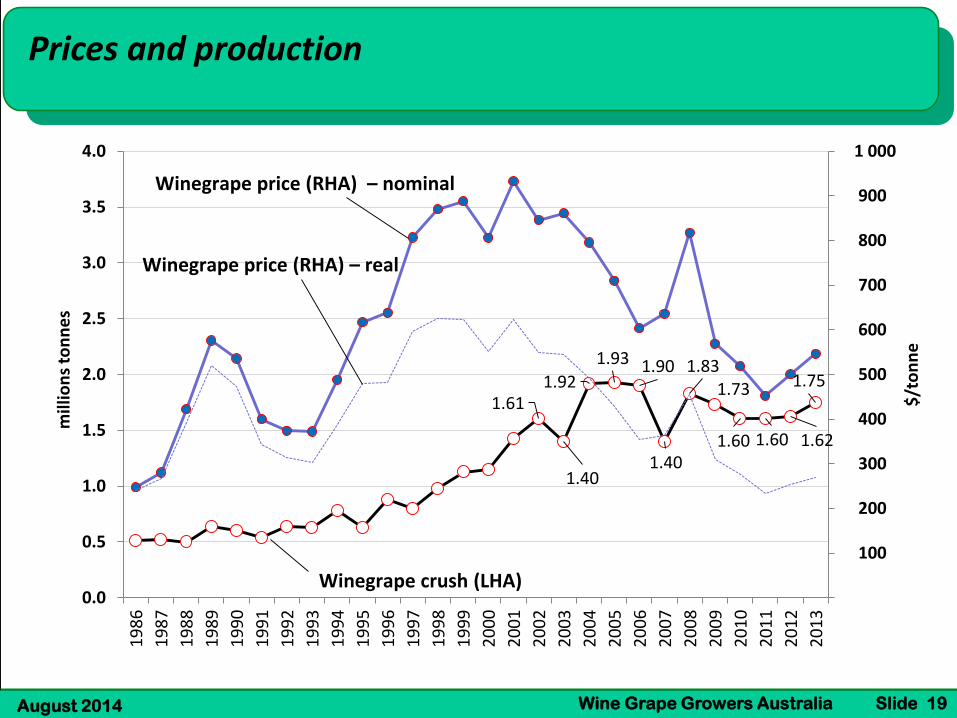

Prices and production

1.61

1.40

1.92

1.93 1.90

1.40

1.831.73

1.60 1.60 1.62

1.75

100

200

300

400

500

600

700

800

900

1 000

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.01

98

6

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

$/t

on

ne

mill

ion

s to

nn

es

Winegrape crush (LHA)

Winegrape price (RHA) – nominal

Winegrape price (RHA) – real

August 2014 Wine Grape Growers Australia Slide 20

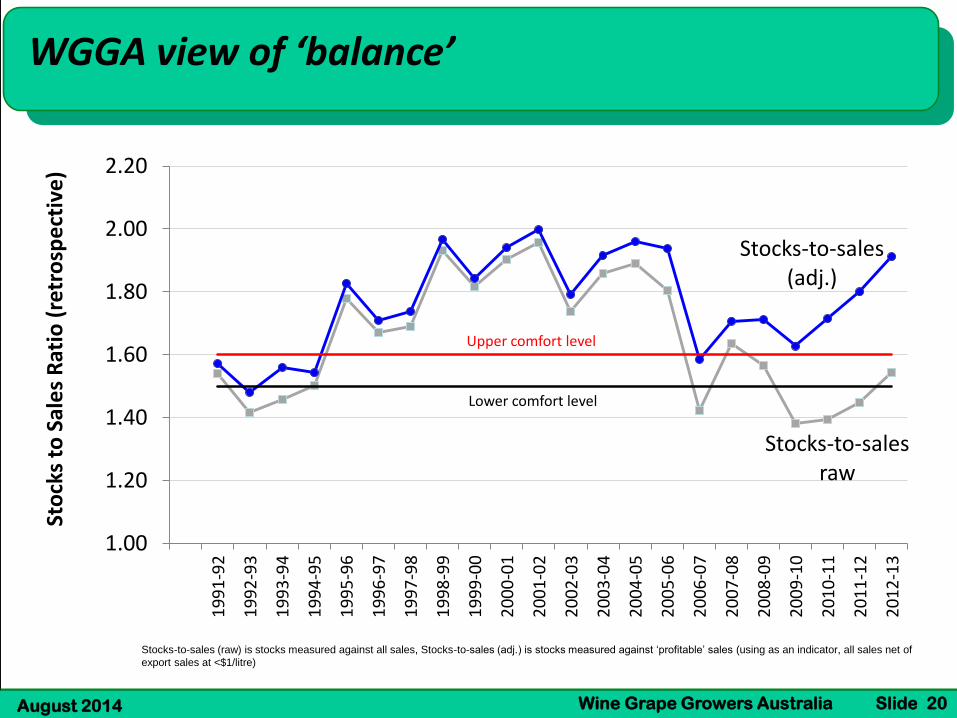

WGGA view of ‘balance’

Stocks-to-sales (raw) is stocks measured against all sales, Stocks-to-sales (adj.) is stocks measured against ‘profitable’ sales (using as an indicator, all sales net of

export sales at <$1/litre)

Stocks-to-sales raw

Stocks-to-sales (adj.)

Upper comfort level

Lower comfort level

1.00

1.20

1.40

1.60

1.80

2.00

2.20

19

91

-92

19

92

-93

19

93

-94

19

94

-95

19

95

-96

19

96

-97

19

97

-98

19

98

-99

19

99

-00

20

00

-01

20

01

-02

20

02

-03

20

03

-04

20

04

-05

20

05

-06

20

06

-07

20

07

-08

20

08

-09

20

09

-10

20

10

-11

20

11

-12

20

12

-13

Sto

cks

to S

ale

s R

atio

(re

tro

spe

ctiv

e)

August 2014 Wine Grape Growers Australia Slide 21

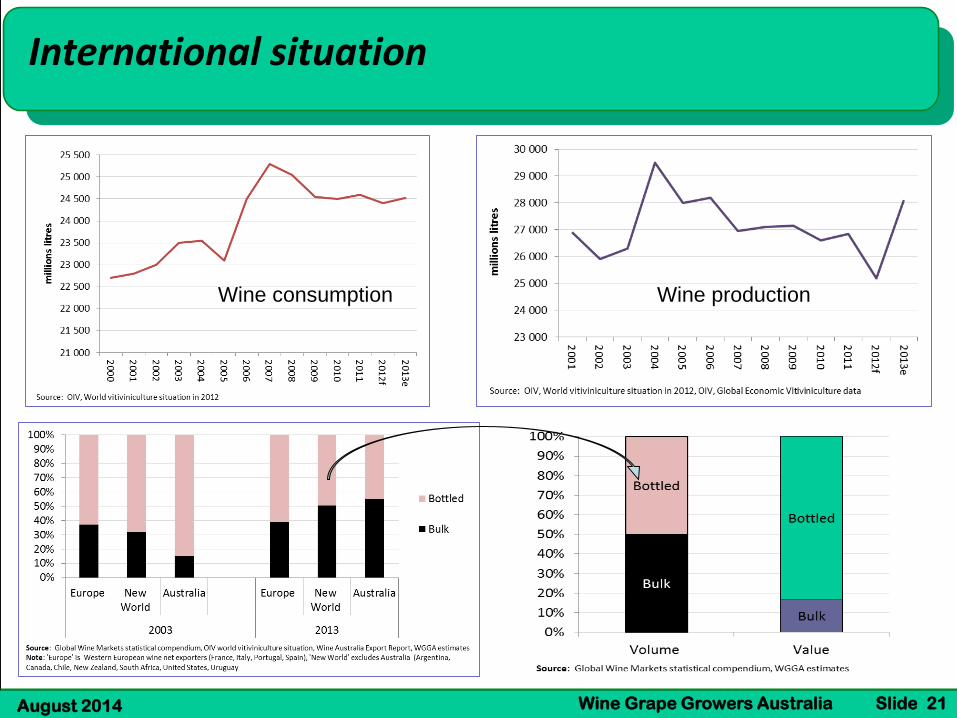

International situation

Wine consumption Wine production

August 2014 Wine Grape Growers Australia Slide 22

Any questions? ST

RA

TEG

IC P

ILLA

RS

1

2

3

4

5

6

Ena

blin

g s

tra

teg

ies

Critical issues

Building organisational capacity

Policy and advocacy

Engaging stakeholders

Cultivating relationships

Corporate governance

High

Medium

Low - no action

1.1

1.2

1.3

1.4

1.5

1.6

1.7

1.8

1.9

Biosecurity and vine health

Market access for winegrapes

Knowledge and capacity development

Research, development & extension

Supply and demand balance

Wine tax

Industrial relations

Environmental sustainability

Water access

Delivery fo

r gro

wers

ISSUES M

AN

AG

EMEN

T