Embed Size (px)

Citation preview

Winds of Change

David Cohen 1

WindsofChange:ForcesImpactingtheFutureoftheForest

Sector

Dr. David CohenUBC

Outline

The Big Picture

Models of Sustainability

Global Forests – Global Trade: A Brief Summary

Drivers of Change in Forestry

David Cohen 2

FourKeyInteractingDrivers

1) Population Growth

2) Economic Power Shift to Developing Regions with their growing middle class

3) Squeeze on world resources, and

4) Growing environmental degradation

David Cohen 3

1)GlobalPopulationGrowth

0

2

4

6

8

10

12

Billion

s of p

eople

2.5 4.1 6.1 7.7 8.7 9.6

Source: Population Reference Bureau 2013David Cohen 4

Winds of Change

David Cohen 2

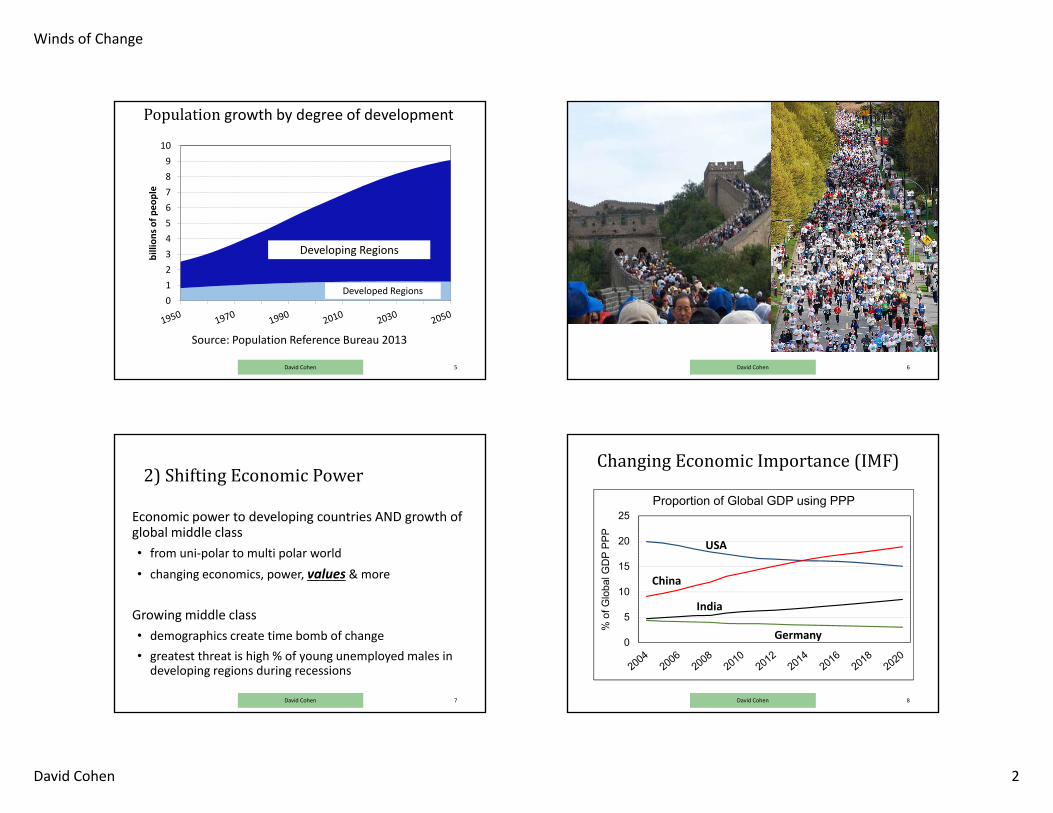

Population growth by degree of development

0123456789

10billion

s of p

eople

Developed Regions

Developing Regions

Source: Population Reference Bureau 2013

David Cohen 5 David Cohen 6

2)ShiftingEconomicPower

Economic power to developing countries AND growth of global middle class• from uni‐polar to multi polar world• changing economics, power, values & more

Growing middle class• demographics create time bomb of change• greatest threat is high % of young unemployed males in developing regions during recessions

David Cohen 7

ChangingEconomicImportance(IMF)

0

5

10

15

20

25

% o

f Glo

bal G

DP

PPP

Proportion of Global GDP using PPP

India

USA

China

Germany

David Cohen 8

Winds of Change

David Cohen 3

ChangingEconomicImportance(IMF)

0

1

2

3

4

% of G

loba

l GDP

Proportion of Global GDP using PPP

Canada

UKIndonesia

David Cohen 9

ThestickysuperpowerTheEconomistOct3,2015Weighted by share of world GDP, trade & exports

GrowingMiddleClass

Globally Middle Class : Extreme Poverty

• Middle class defined as spending of $10‐100/day

• 1 billion people joined 1990‐2010

• Now 2.5 billion (McKinsey: 5 billion by 2022)

• Future drivers of world economic growth

• 1980 – 2015 extreme poverty 47% to 9.6% of world population (<$1.90 per day PPP)

David Cohen 12

BankofCanada:MonthlyCommodityPriceIndexto6/2015

0

500

1,000

1,500

2,000

2,500

3,000

Energy Metals and Minerals Forestry Agriculture

David Cohen 13

Winds of Change

David Cohen 4

BankofCanada:MonthlyCommodityPriceIndexto6/2015

0

500

1,000

1,500

2,000

2,500

3,000

Energy Metals and Minerals Forestry Agriculture

Well managed renewables

flat

Non renewables (metal &

energy) prices doubled

David Cohen 14

3.SqueezeonWorldResources

Leading to high prices and increases in:• Conservation – 3R’s• Eco‐efficiency in business (leaning all operations)• Innovation ‐ resource productivity• Replacing limited non‐renewables with well managed renewables

Paradigm shift this century as sustainability in business becomes opportunity not responsibility

David Cohen 15

UPM Biofore all wood car (2014)

Wood based electronic circuits (2015) http://www.cnbc.com/id/102798585

http://vancouver.housing.ubc.ca/wp‐content/uploads/2017/09/Brock‐Commons‐Tallwood‐House%E2%80%93web.jpg

David Cohen 16

4.Environmentaldegradation:Ecologicalfootprint

Source: Global Footprint Network August 2013http://www.footprintnetwork.org/en/index.php/GFN/page/world_footprint/

David Cohen 19

Winds of Change

David Cohen 5

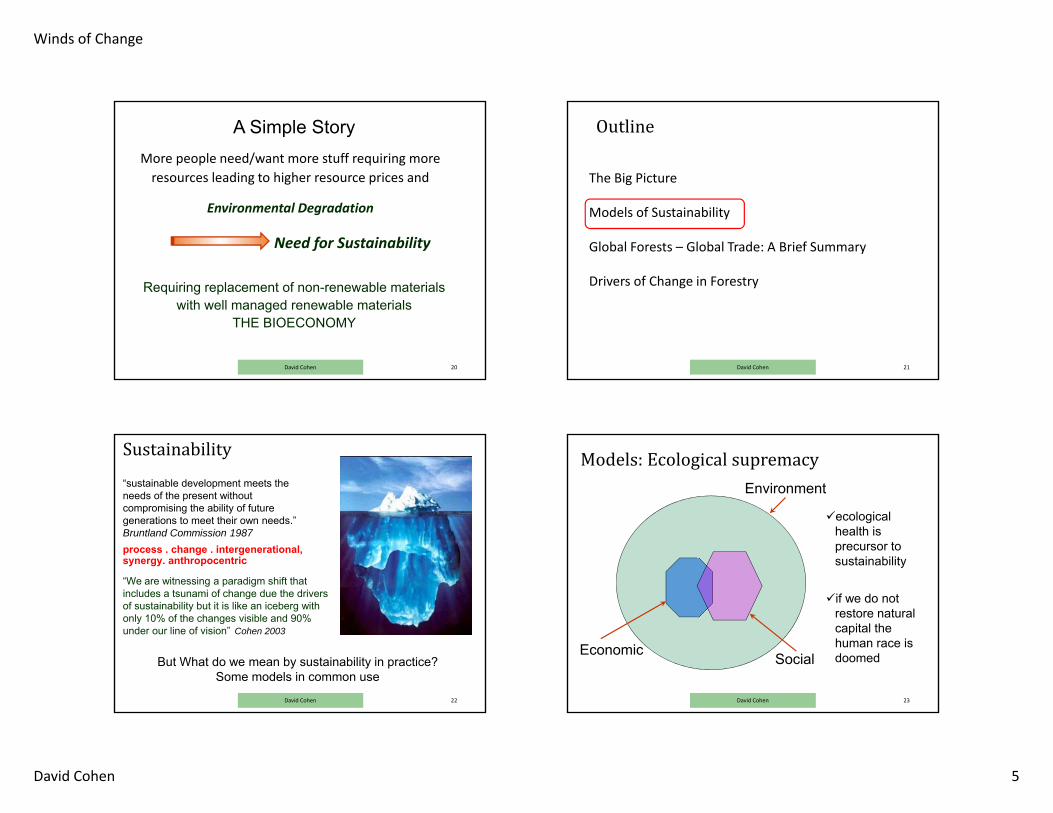

A Simple StoryMore people need/want more stuff requiring moreresources leading to higher resource prices and

Environmental Degradation

Requiring replacement of non-renewable materials with well managed renewable materials

THE BIOECONOMY

Need for Sustainability

David Cohen 20

Outline

The Big Picture

Models of Sustainability

Global Forests – Global Trade: A Brief Summary

Drivers of Change in Forestry

David Cohen 21

Sustainability

“We are witnessing a paradigm shift that includes a tsunami of change due the drivers of sustainability but it is like an iceberg with only 10% of the changes visible and 90% under our line of vision” Cohen 2003

David Cohen 22

“sustainable development meets the needs of the present without compromising the ability of future generations to meet their own needs.” Bruntland Commission 1987process . change . intergenerational, synergy. anthropocentric

But What do we mean by sustainability in practice?Some models in common use

Models:Ecologicalsupremacy

ecological health is precursor to sustainability

if we do not restore natural capital the human race is doomedEconomic

Environment

Social

David Cohen 23

Winds of Change

David Cohen 6

DynamicBalance:mostpopular

Environment

EconomicSocial

Sustainability Models that Reflect Global Reality

Nested Hierarchy

David Cohen 25

NestedHierarchyasfirstproposed

Economy

Society

EnvironmentProposed by Natural Step

Environment is supreme with Economics last (organizational bias)

David Cohen 26

NestedHierarchy:AdaptivemodelThree pillars do not have equal importance BUT:

Different groups have different priorities for pillars.

There is NO “right” hierarchy

Depends on context!

David Cohen 27

Winds of Change

David Cohen 7

Whatisthestory?

All changes point to

SUSTAINABILITY

as key driver for all civil, business, and societal decisions in the future.

Key driver of innovation!

BUT It means different things to different people

David Cohen 28

Outline

The Big Picture

Models of Sustainability

Global Forests – Global Trade: A Brief Summary

Drivers of Change in Forestry

David Cohen 29

This graphic shows some of the countries with the largest forest resources. Those regions highlighted in red show where deforestation has occurred over the past 10 years. Estimates show Indonesia & Brazil account for >75% of global deforestation in most yearsRussia has 1/5th of the world’s forests but produces far less than 1/5th of the worlds wood products. The US & Canada have same forest area BUT the US produces almost twice as many wood products.

Canada–7.7

Source: FRA 2010

USA –7.5

Russia – 20.1

Brazil – 13.0

China –5.1

Indonesia – 2.3

Sweden/Finland – 1.2

David Cohen 30

Forests cover 31% of the worlds land surface or about 4 billion hectares of land. Every continent has some forest cover except for Antarctica. The figure below shows the location of global forest resources in 2010 according to the FAO. Some regions are growing their forest area due to afforestation or planting more areas of tress than are harvested. Some areas are in decline due to land conversion to non forest uses or illegal logging.

area in millions ha: annual % change 2000 ‐ 2010Region#,######

N/C America 7050

S America 864‐8.0

Asia593+4.5

Europe1,005+1.4

Africa674‐3.4

Oceania1

‐1.4

View from Vancouver

David Cohen 31

Winds of Change

David Cohen 8

Global Forest Resources 2010area in millions ha: annual change 2000 ‐ 2010

N/C America 7050

S America 864‐8.0

Asia593+4.5

Europe1,005+1.4

Africa674‐3.4

Oceania191‐1.4

Source: FAO 2000 Yearbook of Forest Products, published in 2002.

Region#,######

View from Toronto

David Cohen 32

Whatisharvested

Harvest of 3.3 – 3.8 billion m3/yr from ~400 billion m3 of trees (0.8% of wood volume) on 4 billion ha of forest land

Subsistence (~50%) vs Industrial (~50%)subsistence and less wood needed to make more products (2015 54% industrial)

Coniferous SW (1/3) vs Non‐coniferous HW (2/3)C (2/3 industrial) vs NC (~2/3 subsistence)

Missing data due to illegal logging and poor reporting =10 ‐ 35% of total volumes

Little change since 1990 25 years

David Cohen 33

Therehasnotbeenmuchchangeisthevolumeofwoodharvestedortheproportionwhichisusedforsubsistenceuseandindustrialuseoverthepast35years.Ittendstovarybasedonhowtheglobaleconomyisfairing.Buttherehasbeenchangesuntermsofsourceofwood.

1,0001,1001,2001,3001,4001,5001,6001,7001,8001,9002,000

Millions of cub

ic m

etres

Annual wood harvests 1980‐2015

for fuel industrial logs

David Cohen 34

Country % 2015 Global Ind. Log Production

% 2000 Global Ind. Log Production

USA 18.3 23.6Russia 9.5 8.2China 8.3 5.3

Canada 8.2 11.2Brazil 7.5 5.4Sweden 3.3 3.2

Indonesia 3.1 2.7

Finland 2.6 2.8

India 2.5 2.3

Germany 2.2 2.9

Chile 2.1 1.4

Poland 1.8 1.4

New Zealand 1.4 1.1

Australia 1.4 1.4

IndustrialLog

Production(20001.6820151.84billionm3) 10%

DeclineinCanada&USGrowthin

China,Russia,Brazil&manyequatorialcountries

David Cohen 35

Winds of Change

David Cohen 9

David Cohen 36

Country % 2015 Log Exports % 2000 Log Exports

Russia 14.9 26.9New Zealand 11.1 5.2USA 9.0 10.4

Canada 4.6 2.5

Ukraine 4.2 0.6

Australia 4.1 1.0

LogExports

Russianexportsduetotax Plantationwood&EasternEurope

LogImports

(6.6‐6.8%oftotal

industriallogharvest2000&2015)

CHINA

Country % 2015 Log Imports % 2000 Log Imports

China 36.1 10.4Germany 7.0 2.7Austria 6.2 6.5Sweden 5.6 8.9Finland 4.6 7.5

Global SW Lumber Production & Exports

David Cohen 37

90

140

190

240

290

340

390

Millions of cum

Exports Production

David Cohen 38

Country % 2015 sawnwood production

% 2000 sawnwood production

USA 17.0 23.7

China 16.4 1.7Canada 10.4 13.1

Russia 7.7 5.2Germany 4.7 4.2

Sweden 4.0 4.2

Brazil 3.4 5.5

Finland 2.4 3.5

Japan 2.1 4.4

Austria 1.9 2.7

Chile 1.9 1.5

SW&HWSawnwoodProduction(2015=452:2000=385millionm3)

• 17%• Shift fromtraditional suppliersto CHINA & Russia

SawnwoodExportsCountry % 2015 Sawnwood Exports % 2000 Sawnwood Exports

Canada 22.9 31.9

Russia 17.7 6.8

Sweden 9.5 9.7

Finland 5.8 7.4

Germany 5.3 3.4

David Cohen 39

SawnwoodExports

SawnwoodImports

(30%oftotal

sawnwoodproductionin2000&2015)

Country % 2015 Sawnwood Imports % 2000 Sawnwood Imports

China 19.9 3.2USA 18.7 30.1UK 4.8 6.9Japan 4.6 8.7Egypt 4.5 1.8

Winds of Change

David Cohen 10

Global Panel Production & Imports

David Cohen 40

050

100150200250300350

Millions of cum

Production Imports

China largest exporter (2.5 times #2) USA, Germany & Japan largest importers

Country % Global Wood Panel Production 2015

% Global Wood Panel Production 2000

China 50.2 9.8USA 8.5 24.5Russia 3.4 2.5Canada 3.2 8.1Germany 3.1 7.5Brazil 2.8 3.1Turkey 2.4 1.3Poland 2.3 2.5Indonesia 1.8 4.9Malaysia 1.7 3.1

WoodPanelProduction(2015– 399;2000‐ 186millionm3)

Chronic under reporting in China

David Cohen 41

David Cohen 42

Country % Global Wood Panel Exports 2015

% Global Wood Panel Exports 2000

China 7.6 1.5Canada 3.9 19.0Germany 3.1 8.1Malaysia 2.7 9.2Russia 2.3 2.5Thailand 2.1 1.5

Exports

WoodPanelExport/import(201581:200057.5millionm3)~30%ofproduction

Imports

Country % Global Wood Panel Imports 2015

% Global Wood Panel Imports 2000

USA 15.1 23.3Germany 6.8 6.8Japan 5.3 10.4Canada 4.2 6.8UK 4.0 5.5

17 countries with 1.0 – 1.7% in 2015

WoodPanels

David Cohen 43

• China; largest producer of MDF, blockboard & plywood

• China uses wood panels for concrete forming & secondary manufacturing

• Chinese production , exports , domestic use grows

• Tendency to overproduce and flood the market before China stops building MDF plants, steel mills, paper plants, etc.

• Before GFC many new OSB plants in NA ready to open new supply easy to add so lid on prices

Winds of Change

David Cohen 11

Chinese Panel Production, Exports & Imports

David Cohen 44

0

20

40

60

80

100

120

140millions of cum

Production

Export

Import

TrendsinPanels

David Cohen 45

• OSB gaining in Europe – entry in Asia China produces > 50% of world supply of MDF

• use of alternative materials for panels Kenaf, strawboard, bamboo board, etc.

• production & exports from China & Brazil

• trade & production of wood panels

• new types of panels e.g. CLT

Pulp

Pulp production has changed substantially between 2000 & 2015. • volume remained almost the same but great increase in

pulp from recycled paper • this now provides almost 1.5 times as much pulp as virgin

wood pulp • reduction in graphic paper use has led to less softwood

pulp use (e.g. in US & Canada) and more use of low cost pulp from eucalyptus plantations in equatorial regions (e.g. Brazil & Uruguay)

• BUT declining paper use results in less paper to recycle

David Cohen 46

Country % Global Production 2015 % Global Production 2000

USA 26.6 33.1

Brazil 9.6 4.2

Canada 9.5 15.3

Sweden 6.3 6.6

Finland 5.6 6.9

China, 5.3 1.9

Japan 4.8 6.6Russia 4.3 3.4

Indonesia 3.6 2.4

Chile 2.8 1.5

WoodPulpProduction(2015– 176;2000=171milliontonnes)

David Cohen 47

Winds of Change

David Cohen 12

Country % Global Wood Pulp Exports 2015

% Global Wood Pulp Exports 2000

Brazil 20.4 7.8Canada 16.8 31.0USA 13.1 15.2Chile 7.5 4.8Sweden 5.9 8.0Indonesia 5.7 3.5

Exports

WoodPulpExports&Imports

2000– 22%2015‐ 34%ofproduction

ImportsCountry % Global Wood Pulp

Imports 015% Global Wood Pulp

Imports 2000China 33.7 7.4USA 9.1 15.8Germany 8.3 9.7Italy 5.9 7.6Korea 3.9 5.1France 3.4 5.7

David Cohen 48

Outline

The Big PictureModels of SustainabilityGlobal Forests – Global Trade: A Brief SummaryDrivers of Change in Forestry• Increased private forest land ownership• Growth of equatorial plantations

• Shifting global timber supply

• Declining paper use• Restricted market access

• Carbon sequestration?

• Crisis in Science

David Cohen 49

IncreasedPrivateOwnershipofForestLandInvestors (e.g. pension plans) seek real assets to

balance stocks and bondsWhy

• To create stable long term cash flows• Long term safe returns• Deflation/inflation hedge• Diversification

Leads to global• Increase in land & house prices

Rapid growth in private equity purchasing forest land from governments (e.g. NZ) and forest companies

50David Cohen

ChangeinPrivateOwnershipofForestLand

David Cohen 51

1990‐2000 2000‐2010 1990‐2010temperate 17.1% 21.0% 41.7%subtropical 5.9% 8.3% 14.7%tropical ‐3.9% 8.2% 3.9%global 8.9% 14.1% 24.2%

• Private forest land ownership increased by 104 million hectares from 1990‐2010

Source: Whitman, Wickramasinghe & Pina, 2015, Forest Ecology and Management 352 (2015) 99‐108.

Winds of Change

David Cohen 13

GrowthofequatorialplantationsHighly managed & subsidized

Trees as agricultural crop

Low cost, fast grown, privately owned, cheap

Technology compensates for weak fibre• e.g. genetic modification, computerized process control,

fertilization, pruning, etc.

Support by NGOs e.g. FSC (intensive vs extensive)

52

SA Eucalyptus harvest has grown to 50 million m3 providing 40% of total SA industrial harvest!

David Cohen

GrowthofPlantedForestAccording to UN FAO (2012) planted forests increased from 1990 – 2010 by 3.6 million ha/year• in developing regions with long growing seasons• 76% were for industrial wood production• Eucalyptus (mostly for pulp) most planted species• China planted greatest area (>60%) followed by Brazil

What about palm plantations? Are they forests?

David Cohen 53

Growthofequatorialplantations

• Most are eucalyptus trees which have short, weak fibres but grow fast compared to NA and EU pulp

• In September 2017 Asia Pulp and Paper paid a very high premium for a pulp mill with expansion option in Brazil

• Paid US$2,810/tonne of pulp capacity which was~70% over recent sales>500% premium over Canfor NBSK production

What could this mean in terms of:competitiveness of northern pulp, relative attractiveness of operating in NA or EUfuture pulp demand, etc.

David Cohen 54

SimplifiedViewofForestPlantations

David Cohen 55

Good for the World

• Rapid growth less land needed natural forest conservation

• Good use of scarce resources• Creates continuous, long term

wood supply• Economically beneficial

Bad for the World

• Biological deserts – NO biodiversity

• Depletes soil / requires fertilization

• Creates hydrological problems

• Monoculture increases pest & disease problems

Winds of Change

David Cohen 14

ShiftingGlobalTimberSupply

Growth in forest volumes (often private) in

• SE USA Pine plantations

• NZ (decline after 2025) Pine plantations

• Australia Plantations

• China plantations Plantations

• Brazil Eucalypts plantations

• Uruguay Eucalypts plantations

• Finland Red & white wood plantations

56David Cohen

DecliningCanadianTimberSupply

BC ‐ substantial declining harvests (more mills will close)Ontario & Quebec – by 2016 all mills that can reopen will do soAlberta – may have room for small increased harvestAtlantic Canada – at or beyond maximum harvest levels

Before US housing starts regain steady state (~1.5 million/yr) Canada has maxed out its lumber production

Does not include impact of fire season of 2017 in western NA

David Cohen 57

DeclineofPaperUse

0

10

20

30

40

50

60

millions of ton

nes NA and EU Graphic Paper Production

USA & Canada

N. & W. Europe

first public access to internet

David Cohen 58

NADemandforNewsprintSource:RBCCapitalMarkets“NewsprintStats”Aug24,2015

David Cohen 59

Winds of Change

David Cohen 15

21st CenturyRecoveredPaperProduction(FAO)

0

50

100

150

200

250

2000 2003 2006 2009 2012 2015

Million tonn

es

How will declining paper use impact this

growth trend?

technology & design keeps increasing % of paper recovered

“urban pulp supply” needs strong virgin

pulp added each time it is recycled

Today almost 60% of all pulp comes from recovered paper

David Cohen 60

MarketAccessRestrictions

US & EU: illegal to use of illegal/unsustainable wood

US Lacey Act Revision 2008• Revised Act to ban trade in illegal animals or plants animal, Great concern to Asian exporters to EU and US

EU’s Forest Law Enforcement, Governance and Trade (FLEGT)• Action plan seeks to use voluntary partnerships with governments to reduce illegal logging & increase legal logging

David Cohen 62

MarketAccessRestrictions

Growing Protectionism• US approval of almost ALL tariff requests by ITC

• Canadian linkage of trade to gender, diversity & labour issues

• Growing use of “environmental imperialism” (which I support due to my personal biases)

• Regulatory bias to home grown SOEs (e.g. China)

David Cohen 63

CarbonSequestration

Flood of Advocacy Research• Showing building with wood sequesters carbon

e.g. tall wood buildings• Showing not harvesting tress sequesters carbon

e.g. communication among trees• Crisis in scientific integrity

David Cohen 64

Winds of Change

David Cohen 16

LooselybasedonCrisisinScience

From “The Rightful Place of Science: Science on the Verge”

by Andrea Saltelli et al.”to improve actual practice in science”

David Cohen 65

Crisisinsciencethreatensitsintegrity:Why?

• “Most published research findings are false” Ionnidis 2005• Unreliability in scientific literature and systematic bias

Boyd 2013• Over 75% of research cannot be reproduced (medical

plus)• Pressure to publish even if findings are not really

significant• Ignoring difference between correlation and causality• Rapid growth of fake papers, journals that publish for

money with no real review, • Promotion based on publishing metrictocracy and not

meritocracy and diversity discrimination

David Cohen 66

• Becomes policy based evidence and not evidence based policy i.e. advocacy science

• Overreliance on dynamic stochastic general models (DSGE) and other modeling techniques:minor changes to basic assumptions and the need for simplification can dramatically change the results climate change and global economic modeling are examples

• Scientific folklore i.e. science can solve any problem given time & money

• “faith based science” so those who disagree become “deniers” and should be punished (David Suzuki)

Crisisinsciencethreatensitsintegrity:Why?“Fallacyofevidencebasedpolicy”

David Cohen 67

Ionnidis, 2005. Why Most Published Research Findings are False, PLoS Med 2(8): e124 doi: 10.1371/journal/pmed. 0020124

Boyd, I. 2013. A standard for policy‐relevant science. Ian Boyd calls for an auditing process to help policy makers to navigate research bias” Nature Comment 501: 160 12 September

David Cohen 68

Winds of Change

David Cohen 17

Outline

The Big PictureModels of SustainabilityGlobal Forests – Global Trade: A Brief SummaryDrivers of Change in Forestry• Increased private forest land ownership• Growth of equatorial plantations

• Shifting global timber supply

• Declining paper use• Restricted market access

• Carbon sequestration?

• Crisis in Science

David Cohen 69