Embed Size (px)

Citation preview

8/6/2019 Wind Utility Ownership and Procurement Strategies in the US Wind Sector 8220101

http://slidepdf.com/reader/full/wind-utility-ownership-and-procurement-strategies-in-the-us-wind-sector-8220101 1/12

© 2010 EMERGING ENERGY RESEARCH, LLC.All rights reserved. Reproduction of this publication inany form without prior written permission is strictlyforbidden. The information contained herein is fromsources considered reliable but its accuracy andcompleteness are not warranted, nor are the opinionsand analyses which are based upon i t.

Photo Source

North America WindEnergy Advisory

Market Brief

Utility Ownership

and Procurement Strategies in theUS Wind Sector

ID# NAW 925-100802

2 August 2010

Tim Stephure

+1 617 551 8586

8/6/2019 Wind Utility Ownership and Procurement Strategies in the US Wind Sector 8220101

http://slidepdf.com/reader/full/wind-utility-ownership-and-procurement-strategies-in-the-us-wind-sector-8220101 2/12

Page 2North America Wind Energy Advisory – NAW 925-100802

Utility Ownership and Procurement Strategies in the US Wind Sector

Summary

Utilities are taking an increasingly proactive approach to developing and owning wind assets to diversify theirpower mix

• Approximately 14% of 2009 US wind additions were utility-owned, a slight decrease in percentage terms from 16% in 2008

• In contrast to 2008, when MidAmerican dominated the utility wind ownership market with 73% of utility additions, a diversegroup of 15 utilities contributed to 2009 additions, with continued diversity expected over the near term

• Partnerships with developers and independent power producers (IPPs) have given utilities the experience and confidenceto own, and in some cases develop, wind assets independently

• Falling turbine prices combined with a buyer’s market for some services, including engineering, procurement, and

construction (EPC), has dramatically reduced development risk for some utilities who have chosen to develop their ownwind projects

Power purchase agreement (PPA) market weakness asserts influence on both utility and IPP positioning• Weak PPA demand by utilities nationally is driving wind development to more challenging markets, including California and

New England, where renewable portfolio standard (RPS) supply is significantly below mandated levels

• A slowdown in power demand is delaying PPA contracts as utilities re-evaluate long-term generation requirements andmove more cautiously on renewables procurement

• Slow economic recovery is also driving strong resistance to rate increases, which is further inhibiting wind procurement

Utility willingness to adopt the IPP business model is leading to disputes that have thus far ruled in favor of

utilities

• Western utilities capitalize on strong wind demand in California by inking short-term PPAs, as renewable generation is notneeded over the near term to meet RPS compliance in their home markets

• IPPs focused on turnkey projects including enXco and RES Americas have had to forge new partnerships as their key utilitypartners including MidAmerican and Puget Sound Energy have moved to develop and own wind independently

8/6/2019 Wind Utility Ownership and Procurement Strategies in the US Wind Sector 8220101

http://slidepdf.com/reader/full/wind-utility-ownership-and-procurement-strategies-in-the-us-wind-sector-8220101 3/12

Page 3North America Wind Energy Advisory – NAW 925-100802

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

M W

YE 2009 YE 2008

Utility wind owner

Utility Ownership and Procurement Strategies in the US Wind Sector

Cumulative Wind Ownership Ranking by Owner Type

MidAmerican maintains considerablelead despite slower 2009

• Following a breakout year where

MidAmerican installed over 1 GW ofcapacity, wind installations in 2009were just over 20% of 2008 levels

• MidAmerican subsidiary Pacificorp ledall utilities in 2009 wind additions withover 220 MW of capacity

Increased competition among utility

entrants characterizes 2009

• In contrast to 2008, whenMidAmerican claimed over 73% of all

utility-owned wind, 2009 saw greaterdiversity, with no single entity havingmore than 17% of the annual build

Without a viable merchant option,

IPP’s operations are more greatlyaffected by utility ownership

aspirations

• Top IPP owners of wind powerincluding NextEra, Iberdrola, andInvenergy have had to shift build

strategies in response to utility windownership activity in 2009

Analysis

Note: ‘Utility wind owner’ refers only to capacity owned directly by the utility and does not include capacity owned under IPP subsidiariesSource: IHS Emerging Energy Research

Cumulative Wind Ownership: 2009 vs. 2008

41%

39%

14%

6%

International IPP

Domestic IPP

Domestic Utility

Domestic Developer

9,789MW

While IPPs remain the predominate business model for wind asset ownership, a select group of utilities

have made significant gains in 2009

8/6/2019 Wind Utility Ownership and Procurement Strategies in the US Wind Sector 8220101

http://slidepdf.com/reader/full/wind-utility-ownership-and-procurement-strategies-in-the-us-wind-sector-8220101 4/12

Page 4North America Wind Energy Advisory – NAW 925-100802

Utility Ownership and Procurement Strategies in the US Wind Sector

Utility Wind Ownership Ranking by Owner Type: Year-end 2009

Investor-owned utilities (IOUs) maintain status as primary target for PPAs and lead utility wind

ownership, while a number of rural co-ops are buying utility-scale wind projects

MidAmerican is positioned to

challenge Xcel Energy’s leadingposition through in-house wind

development and ownership• MidAmerican has regulatory approval

to bring 1,001 MW of additional windcapacity online in Iowa by 2012

• Xcel is moving to a more balancedapproach, with over 500 MW of PPAsinked in 2010, as well as plans to ownan additional 351 MW by the end of2011

Rural electric co-ops make impact,

adding large, utility-scale projects• After several years of focusing

primarily on community-scaleprojects, rural electric co-ops arescaling to enhance the economicbenefits of wind power for theircommunities. Several projectsexceeding 100 MW in size wereenergized in 2009, including BasinElectric’s 115.5 Prairie Winds project

and Turlock Irrigation District’s 128.5

MW Windy Point facility; its first forayinto wind ownership

Utility Wind Ownership Ranking by Owner Type: Year-end 2009

Source: IHS Emerging Energy Research

Analysis

0

500

1,000

1,500

2,000

2,500

3,000

3,500

C u m u l a t i v e

I n s t a l l e d / C o n t r a c t e d C a p a c i t y ( M W )

Procured Wind

Owned Wind

Investor Owned Utility

Municipal Utility

Rural Electric Co-op

0 200 400 600 800 1,000 1,200 1,400

Top 10 2009 Utility Wind Ownership Additions (MW)

PacifiCorp (MidAmerican) Alliant EnergyPortland General Electric Turlock Irrigation District

Basin Electric Power Coop Los Angeles Department of Water & PowerOklahoma Gas & Electric Westar EnergyWisconsin Public Service Otter Tail Power Company

8/6/2019 Wind Utility Ownership and Procurement Strategies in the US Wind Sector 8220101

http://slidepdf.com/reader/full/wind-utility-ownership-and-procurement-strategies-in-the-us-wind-sector-8220101 5/12Page 5North America Wind Energy Advisory – NAW 925-100802

Utility ownership’s appeal expanding

regionally

• Although represent in 19 US states,

utility ownership has traditionally beenmost prevalent in the Pacific Northwestand the Midwest. However, statesincluding Oklahoma, Indiana, andWyoming were major rate-based hubsin 2009

Merchant offtake increased in 2009

despite electricity price declines ofover 50% in most of the country

• Bolstered by gas prices averaging

US$8.86/MMBtu in 2008, merchantwind made up nearly one-third of allwind additions in 2008. In 2009,approximately 40% of wind capacitysold power into the merchant marketdespite a more than 50% decline inaverage gas prices

• Texas, the most substantial merchantwind power market in the US, willexperience considerable declines inwind additions over the near term, with

NextEra, a historically Texas-heavydeveloper, having no plans for near-term Texas wind build

Cumulative US Wind Installations by Offtake Type

Utility Ownership and Procurement Strategies in the US Wind Sector

Regional Off-Take Trends

Utility ownership has contributed to a significant drop in PPA demand, which has forced a large group of

generators to sell wind power at unsustainably low prices on the merchant market

Source: IHS Emerging Energy Research

Analysis

Pacific Northwest

California

Desert Southwest

Rocky Mountains

Texas

Midwest

South

Mid-Atlantic

New England

Great Plains

PPA

Utility Owned

Merchant

New York

2,440

29717

2,490

5844

683

4,189

129

5,119

1,816

545

245

5,5092,219

1,600

27

2

63

1,024

1,213

61

1,753

1,539

537

8/6/2019 Wind Utility Ownership and Procurement Strategies in the US Wind Sector 8220101

http://slidepdf.com/reader/full/wind-utility-ownership-and-procurement-strategies-in-the-us-wind-sector-8220101 6/12

Page 6North America Wind Energy Advisory – NAW 925-100802

MidAmerican’s integrated positioningeyed by ownership-focused competitors

• Puget Sound Energy’s move to purchase

its development partner RES America’sstake in the Lower Snake River projectsignals greater comfort in thedevelopment risks associated with windproject development

• Xcel’s move to purchase turnkey projectsfrom its IPP partner enXco in March 2010marks a clear shift from its PPA-focusedstrategy. Xcel has allocated overUS$900 million to purchase 351 MW ofwind capacity through 2011

PG&E leverages its unsatisfied RPSdemand to move toward wind ownership

• PG&E leads the US for projected RPSdemand, making it a key target for IPPsin a tight off-take market. Iberdrola’s

decision to sell its 246 MW Manzanaproject turnkey to PG&E, an out ofcharacter strategy for Iberdrola, reflectsthe utility’s ability to assert its influence inthe market

Analysis

Utility Ownership and Procurement Strategies in the US Wind Sector

Utility Positioning in the US Wind Market

Utilities already established in the ownership segment are increasingly looking toward development to drive down costs, while more risk-averse utilities are sticking with PPA procurement

Source: IHS Emerging Energy Research

Renewable

TransmissionOfftakeOwnershipFinance

Turnkey Ownership

Develop-to-Own Projects with Renewable Transmission

Development

1

3

Utility Example Business Model Comments

1 MidAmerican Develop-to-own

MidAmerican has quickly developed capability across the value chain and

has become a leading player in the industry, and one of very few companies

with experience in each segment

2Xcel,Puget Sound

Energy, Ottertail Power

Partner with established

renewables developer /

IPP to own

Partnering with established renewable IPPs such as enXco, NextEra, andRenewable Energy Systems (RES) has helped mitigate development risks

and has given Puget Sound Energy confidence to move toward developing

projects independently

3 Xcel , PG&E, LADWP Turnkey plant purchase

Utilities able to tap lower costs of capital can take advantage of the benefits

of wind ownership, including lower costs and stronger balance sheet

positioning, without assuming development risk

4AEP, NV Energy, PG&E,

SCE, SDG&ELong-term PPA

The traditional utility role in the wind industry. Regulated utilities facing rate

pressures have slowed their procurement of PPAs after a dramatic drop in

power demand made predicting future renewables needs for RPS

compliance difficult

5National Grid, PECO,

PPL, Northeast utilities

REC purchasing from

utility-scale projects

Limited by transmission or local resources, tapping REC purchase as lowest-

cost option for near-term compliance, mainly focused on short-term needs

6 SDG&E, Xcel, SCE,LADWP Renewable transmissionand storage investment Transmission development and energy storage investments to facilitaterenewables up-take to bolster compliance objectives

REC Purchasing

Partner with Established Renewables Developer / IPP2

Long-Term PPA4

5

U t i l i t y A s s e t O w n

e r s h i p

P r o c u r e m e n t

RE Transmission6

8/6/2019 Wind Utility Ownership and Procurement Strategies in the US Wind Sector 8220101

http://slidepdf.com/reader/full/wind-utility-ownership-and-procurement-strategies-in-the-us-wind-sector-8220101 7/12

Page 7North America Wind Energy Advisory – NAW 925-100802

RFP activity shifting toward load on East

and West coasts

• Difficult wind development conditions have

limited existing RPS-eligible build, whilelarger electricity loads have created ampleunfilled RPS demand in California and NewEngland

Utilities without near-term demandcontinue to issue RFPs for 2015 andbeyond to tap lower wind component

prices

• RFPs by Puget Sound Energy and El PasoElectric Co. are for generation online by

2015 and 2016, reflecting a lack of near-term wind demand

Utilities in Midwest states that have near-

term RPS demand covered are reluctant toattempt to push through additional rate-based wind

• AEP has been forced to reduce its near-term wind procurement expectations dueprimarily to resistance to rate-based wind.On 3 June 2010, the Virginia PUC rejecteda 201 MW PPA that AEP had signed with

Invenergy for the output from the BeechRidge and Grand Ridge projects

• Citing both lack of need and excess cost,Kentucky regulators rejected AEPsubsidiary Kentucky Power’s PPA withNextEra for its 217 MW Lee-DeKalb projectat the proposed price of US$43/MWh

Utility Ownership and Procurement Strategies in the US Wind Sector

RFP Activity Shifts to Load Centers

Source: IHS Emerging Energy Research

2010 Wind RFP Activity Analysis

On 15 February 2010, WEEnergies issued an RFP for up

to 150,000 MWh o f annual

renewable energy including

RECs for up to five-year terms

PSERFP for 1 GW of

generation, including

renewables, due to

be in servic e by 2016

APS is seeking competitive proposals

for 15 MW to 100 MW of wind capacity

located in Arizona though either PPA or

turnkey ownership

MPUC RFP for long-term

con ventional and renewables

with the T&D utilities. Total

capacity not disclosed

• NYPA is seeki ng 25 MW of renewable RECs on behalf of

the Port Authori ty of New York and New Jersey

• NYPA is also seeking bids for up to 500 MW of offshore

wind in the Great Lakes region

PNM is seeking to purchase RECs

equivalent to a minimum of 50,000

MWhs and a maximum of 450,000

MWhs

El Paso Electric Co. is s eeking seekingup to 300 MW of eligi ble supply-side,

including all -in renewable energy, and/or

demand -side resources by 2015

• PPLRFP for up to 850,000 MWh of RECs from

Tier 1 renewables, including wind

• PPLRFP for up 850,000 MWh o f RECs from Tier

1 renewables, in cluding wind

NV Energy RFP for

renewables capacity over 1

MW or the sale of turnkey

facilities of o ver 1 MW

Avista postponed its 24

September 2009 RFP,

including development

of its Reardan wind

proj ect, until 2014 –

2015

•

KCP&L RFP to con struct 100.5 MW Spearville II wind farm, as well as purchase the 32turbines, land rights , and project assets currently under ownership by KCP&L for the

project

• KCP&L is also accepting bids for up to 200 MW of wind capacity via both PPAs or the

sale of turnkey facilities in commercial operation by 1 October 2011

On 8 Apri l 2010,

Nebraska Public PowerDistrict launched an RFP

for wind projects between

50 MW and 300 MW insize

8/6/2019 Wind Utility Ownership and Procurement Strategies in the US Wind Sector 8220101

http://slidepdf.com/reader/full/wind-utility-ownership-and-procurement-strategies-in-the-us-wind-sector-8220101 8/12

Page 8North America Wind Energy Advisory – NAW 925-100802

0

100

200

300

400

500

600

700

800

900

1,000

Tennessee Colorado Vermont Nevada California Nebraska NorthDakota

Wisconsin Hawaii

M W

Utility Ownership and Procurement Strategies in the US Wind Sector

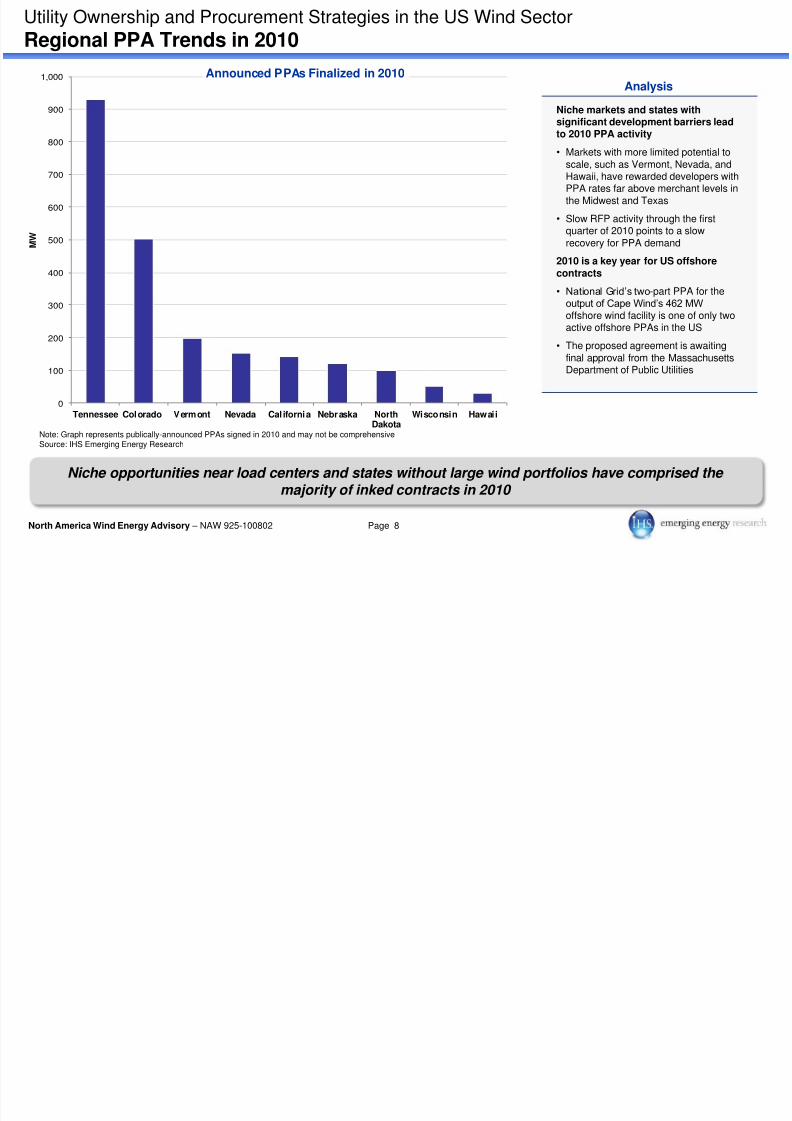

Regional PPA Trends in 2010

Niche markets and states withsignificant development barriers leadto 2010 PPA activity

• Markets with more limited potential toscale, such as Vermont, Nevada, andHawaii, have rewarded developers withPPA rates far above merchant levels inthe Midwest and Texas

• Slow RFP activity through the firstquarter of 2010 points to a slowrecovery for PPA demand

2010 is a key year for US offshore

contracts• National Grid’s two-part PPA for the

output of Cape Wind’s 462 MWoffshore wind facility is one of only twoactive offshore PPAs in the US

• The proposed agreement is awaitingfinal approval from the MassachusettsDepartment of Public Utilities

Niche opportunities near load centers and states without large wind portfolios have comprised the majority of inked contracts in 2010

Note: Graph represents publically-announced PPAs signed in 2010 and may not be comprehensiveSource: IHS Emerging Energy Research

AnalysisAnnounced PPAs Finalized in 2010

8/6/2019 Wind Utility Ownership and Procurement Strategies in the US Wind Sector 8220101

http://slidepdf.com/reader/full/wind-utility-ownership-and-procurement-strategies-in-the-us-wind-sector-8220101 9/12

Page 9North America Wind Energy Advisory – NAW 925-100802

Utility Ownership and Procurement Strategies in the US Wind Sector

2010 PPA Focus Shifts To Niche Markets

Only three of the top 25 utility procurers of wind at year-end 2009 have signed PPAs in 2010

Tennessee Valley Electric Authority leads thecharge in signing PPAs, with over one-thirdof all capacity contracted in 2010

• The government-owned utility has signed over900 MW in 2010 from Midwest-based projectsfrom a variety of developers, includingHorizon, Iberdrola, Invenergy, and CPVRenewable Energy to meet an internally drivenrenewables target

Xcel continues to procure wind via PPA as itgains experience in wind ownership

• Although Xcel has allocated over US$900million to near-term wind ownership, thecompany continues to look to PPAs to

supplement its wind requirements, signing 500MW in 2010

Recent surge in Nebraska PPAs unlikely tomaintain momentum

• Without an RPS mandate and an excess ofbaseload capacity over the near term,Nebraska PPAs from NPPD and OPPD willlikely continue to be sporadic and more aboutsupporting domestic sources than energyneeds. However, recent RFP bids under

US$40/MWh could make wind a valuablecommodity hedge, especially with recentchanges to facilitate power export

Analysis

Note: Includes only publically-announced, finalized PPAsSource: IHS Emerging Energy Research

0

100

200

300

400

500

600

700

800

900

January February March April May

M W

TVA Omaha Public Power District Nebraska Public Power DistrictNV Energy Xcel WE EnergiesBasin Electric Central Vermont Public Service Green Mountain PowerSDG&E HECO

42%

23%

7%

6%

5%

4%

4%

4%2%

2%1%

2,220

MW

U ili O hi d P S i i h US Wi d S

8/6/2019 Wind Utility Ownership and Procurement Strategies in the US Wind Sector 8220101

http://slidepdf.com/reader/full/wind-utility-ownership-and-procurement-strategies-in-the-us-wind-sector-8220101 10/12

Page 10North America Wind Energy Advisory – NAW 925-100802

Utility Ownership and Procurement Strategies in the US Wind Sector

Utilities Front Load Wind Build to Tap California Opportunity

Northwest utilities tap higherCalifornia energy prices until local

RPS compliance takes effect in 2011 –

2012 in Washington and Oregon

• As evidence of utility strategiesconverging with IPPs, five Wyoming,Washington, and Oregon utilities havesigned PPAs with California utilitiesfacing compliance in 2010. The short-term agreements range from threemonths to over three years and allowutility wind owners to benefit from thepricing premium in California versustheir home markets

MidAmerican’s renewables portfoliois estimated to meet 2020 level of RPS

requirement

• The utility’s northwest subsidiary,Pacificorp, is selling over 1 GW ofwind capacity via 14 facilities inWashington, Wyoming, and Oregon.Similarly, Puget Sound Energycontinues to aggressively build andprocure new wind even as the utility

exceeds its 2020 RPS needs

Utilities have successfully imitated the IPP business model to generate profits within their wind portfolio that can mitigate the need for rate increases to meet RPS mandates

Source: IHS Emerging Energy Research

Analysis

Utility Project MW

1 Energy Northwest Nine Canyon, WA 32.2 MW

2 PacifiCorp High Plains, WY 99 MW

3 PacifiCorp McFadden Rid ge, WY 28.5 MW

4 PacifiCorp Combine Hills, OR 41 MW

5 PacifiCorp Foote Creek I, WY 41.4 MW

6 PacifiCorp Glenrock I, WY 99 MW

7 PacifiCorp Glenrock III, WY 39 MW

8 PacifiCorp Goodnoe Hills, WA 94 MW

9 PacifiCorp Leaning Junip er, OR 100.5 MW

10 Paci fi Corp Marengo, WA 140.4 MW

11 Paci fi Corp Marengo II, WA 70.2 MW

12 Paci fi Corp Rock River I, WY 50 MW

13 Paci fi Corp Rolling Hills, WY 99 MW

14 Paci fi Corp Seven Mile Hill I, WY 99 MW

15 Pacifi Corp Seven Mile Hill II, WY 19.5 MW

16Portland GeneralElectric Biglow Canyon, OR 274.9 MW

17 Puget Sound Energy Hopkins Ridge, WA 156.6 MW

18 Puget Sound Energy Wild Horse, WA 272.6 MW

19 Puget Sound Energy Klondike III, OR 50 MW

20 Turlock IrrigationDistrict Tuolumne, WA 136.6 MW

RPS

Demand

19 4

32

6

5

7

8

9

1011

12

131514

16

17

18

201

0 200 400 600 800 1,000 1,200 1,400 1,600 1,800 2,000MW

Utility Owned Wind Actively Selling into California (MW)

WASHINGTON WYOMING OREGON

Utilit O hi d P t St t i i th US Wi d S t

8/6/2019 Wind Utility Ownership and Procurement Strategies in the US Wind Sector 8220101

http://slidepdf.com/reader/full/wind-utility-ownership-and-procurement-strategies-in-the-us-wind-sector-8220101 11/12

Page 11North America Wind Energy Advisory – NAW 925-100802

Utility Ownership and Procurement Strategies in the US Wind Sector

Utilities and IPPs Jostle for Position

Utilities and IPPs that have traditionally worked collaboratively are increasingly competing for market

share, with utilities winning recent cost rulings

1

2

3

4

5

Summary

Puget Sound Energy takes 100% ownership of the 1,432 MW LowerSnake River series of projects, demonstrating its confidence in wind

Iberdrola uncharacteristically sold its 246 MW Manzana project underdevelopment in California for US$900 million. It is the first project thecompany has sold turnkey in the US

NextEra, the largest owner of wind in the US, sold s takes in itsAshtabula and Luverne wind farms to utility Ottertail Power

In December 2009, the Iowa Utilities Board ruled in favor ofMidAmerican to allow the utility to build up to 1 GW of wind by 2012rather than purchase wind from IPPs including NextEra

In January 2010, the Wisconsin PUC rejected Invenergy’s request toonly allow utility WE Energies to build its Glacier Hills wind farmcontingent on the utility executing a PPA for its Ledge wind farm

1

2

5

4

3

IPPs turn to markets with less utility

competition

• Although the Midwest remains a keymarket for NextEra, with 20% ofcapacity additions in 2010 –2011,markets including Canada andCalifornia (which only amount to acombined 12% of existing installations)will make up over 50% over the nexttwo years

• Iberdrola’s near-term portfolio hasshifted significantly to the NortheastUS, while Ontario has become astrategic priority for NextEra andInvenergy

IPPs unable to prove cost savingsargument in rate cases

• Invenergy unsuccessfully argued thatits Ledge Wind project would save ratepayers up to US$50 million over a 30-year PPA versus the cost for WEEnergies to develop its own GlacierHills project

Source: IHS Emerging Energy Research

Key Utility/IPP Interaction in the US Wind Market

Analysis

8/6/2019 Wind Utility Ownership and Procurement Strategies in the US Wind Sector 8220101

http://slidepdf.com/reader/full/wind-utility-ownership-and-procurement-strategies-in-the-us-wind-sector-8220101 12/12

Page 12North America Wind Energy Advisory – NAW 925-100802

IHS Emerging Energy Research

IHS Emerging Energy Research provides analyst-directed advisory services on an annualsubscription basis, providing market intelligence, competitive analysis and strategy advice in

response to the specific needs of our clients. These services provide value-added support of clients’

competitive and market strategies, and are intended to be interactive, offering clients direct access toEER experts.

Advisory service clients receive a stream of market and company briefs, ongoing market data andforecast support, telephone inquiry privileges, and regular analyst briefings. While much of thecontent is syndicated, clients also receive ongoing individual support of market assessment and

strategy development needs.

For more information on EER’s advisory services, please contact:

US Office700 Technology SquareCambridge, Massachusetts, US 02139

Whitney Van HorneSales Support ManagerEmail: [email protected]: +1 617 551 8580Fax: +1 617 551 8481

Spain OfficePaseo de Gracia 47, Planta 2Barcelona, Spain 08007

Paola AlcalaSales Support ManagerEmail: [email protected]: +34 932 726 777Fax: +34 93 467 6754

© 2010 EMERGING ENERGY RESEARCH, LLC. All rights reserved. Reproduction of this publication in any form without prior written permission is strictly forbidden. Theinformation contained herein is from sources considered reliable but its accuracy and completeness are not warranted, nor are the opinions and analyses which are based upon it.