Embed Size (px)

Citation preview

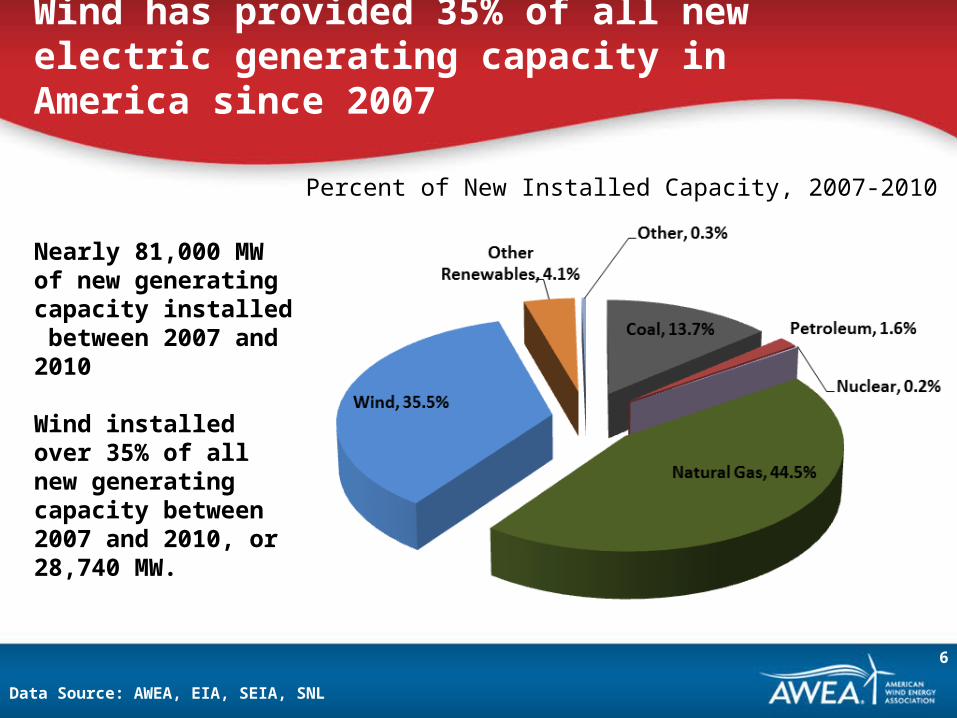

Wind has provided 35% of all new electric generating capacity in America since 2007

Data Source: AWEA, EIA, SEIA, SNL

Nearly 81,000 MW of new generating capacity installed between 2007 and 2010

Wind installed over 35% of all new generating capacity between 2007 and 2010, or 28,740 MW.

Percent of New Installed Capacity, 2007-2010

6

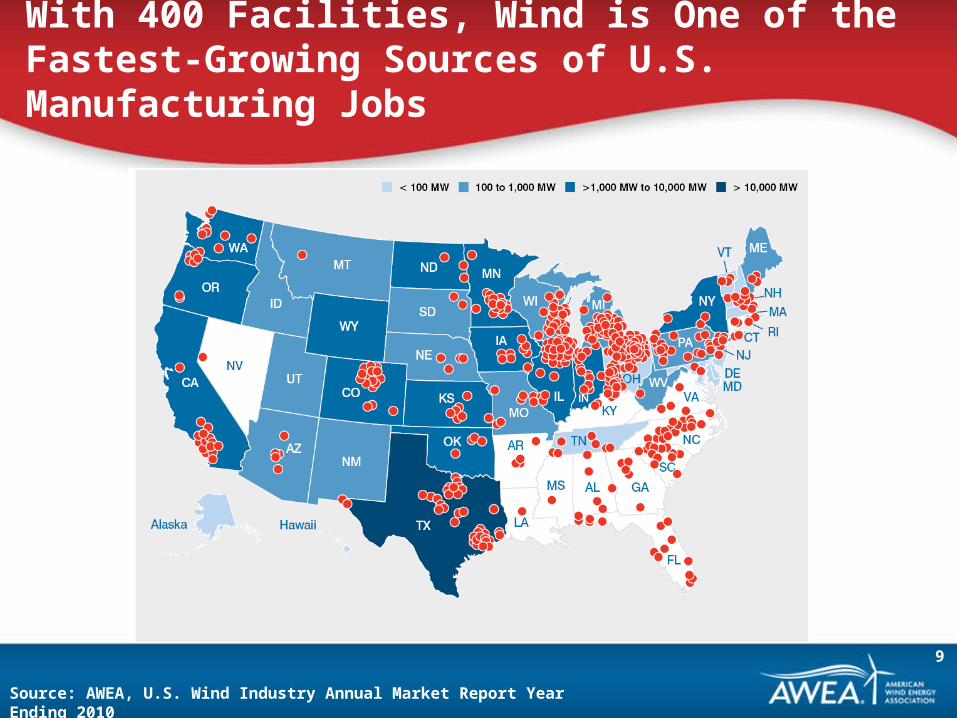

With 400 Facilities, Wind is One of the Fastest-Growing Sources of U.S. Manufacturing Jobs

Source: AWEA, U.S. Wind Industry Annual Market Report Year Ending 2010

9

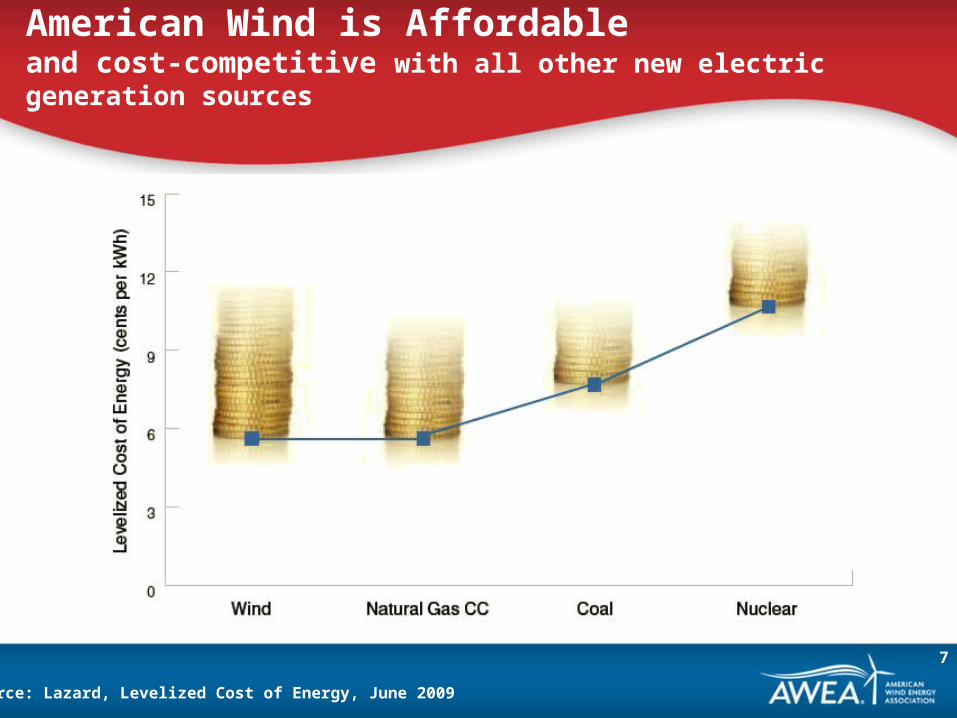

American Wind is Affordableand cost-competitive with all other new electric generation sources

Source: Lazard, Levelized Cost of Energy, June 2009

7

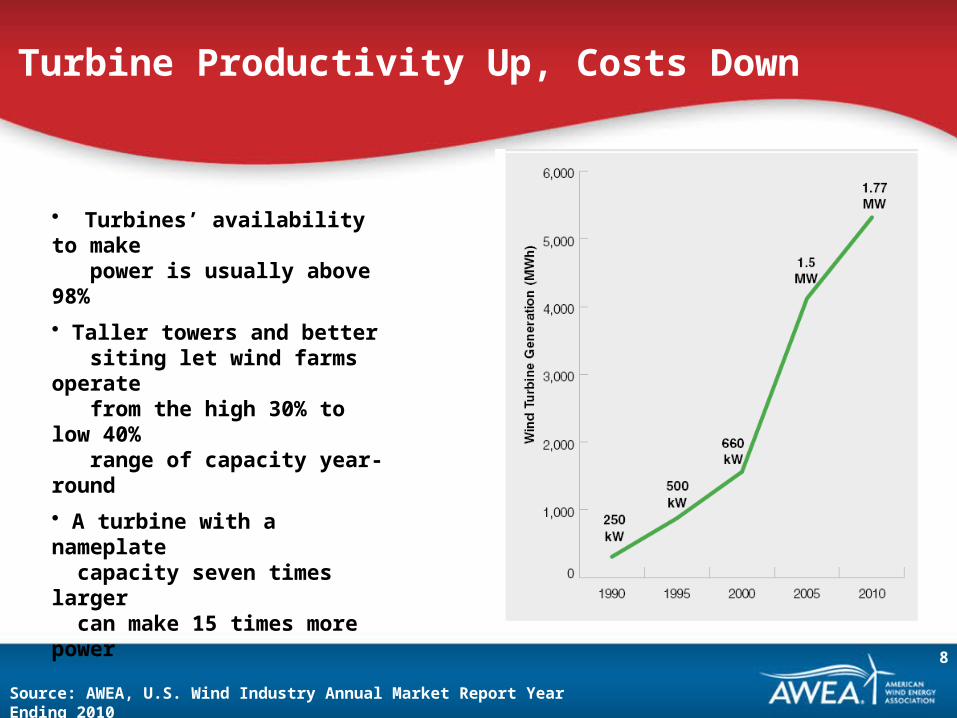

Turbine Productivity Up, Costs Down

Source: AWEA, U.S. Wind Industry Annual Market Report Year Ending 2010

• Turbines’ availability to make power is usually above 98%

• Taller towers and better siting let wind farms operate from the high 30% to low 40% range of capacity year-round

• A turbine with a nameplate capacity seven times larger can make 15 times more power

8

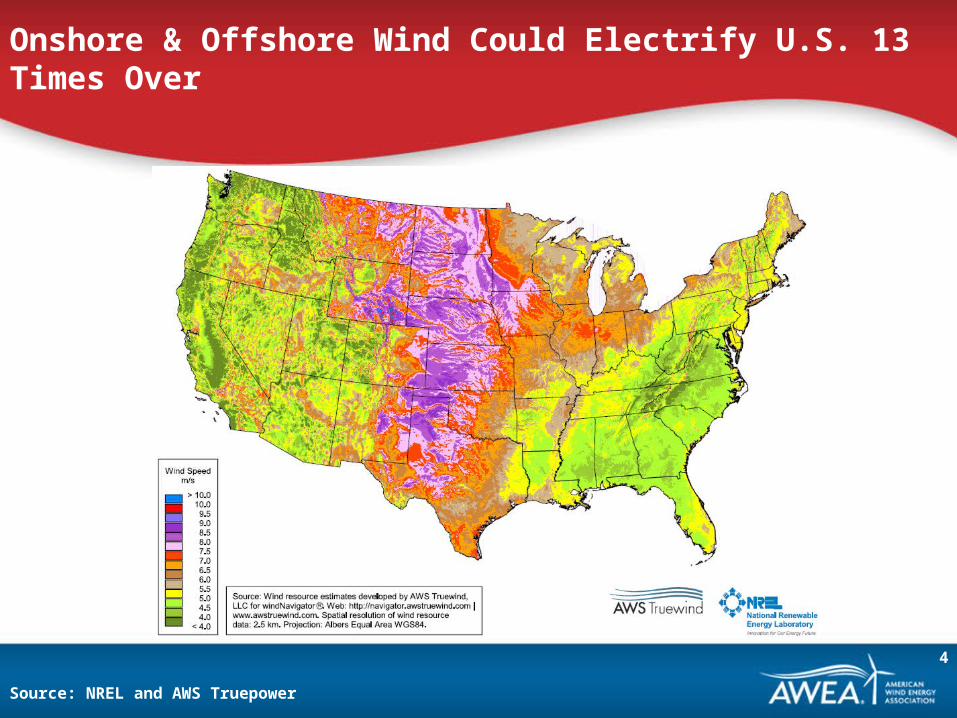

Onshore & Offshore Wind Could Electrify U.S. 13 Times Over

Source: NREL and AWS Truepower

4

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

2026

2028

2030

0

50

100

150

200

250

300

350

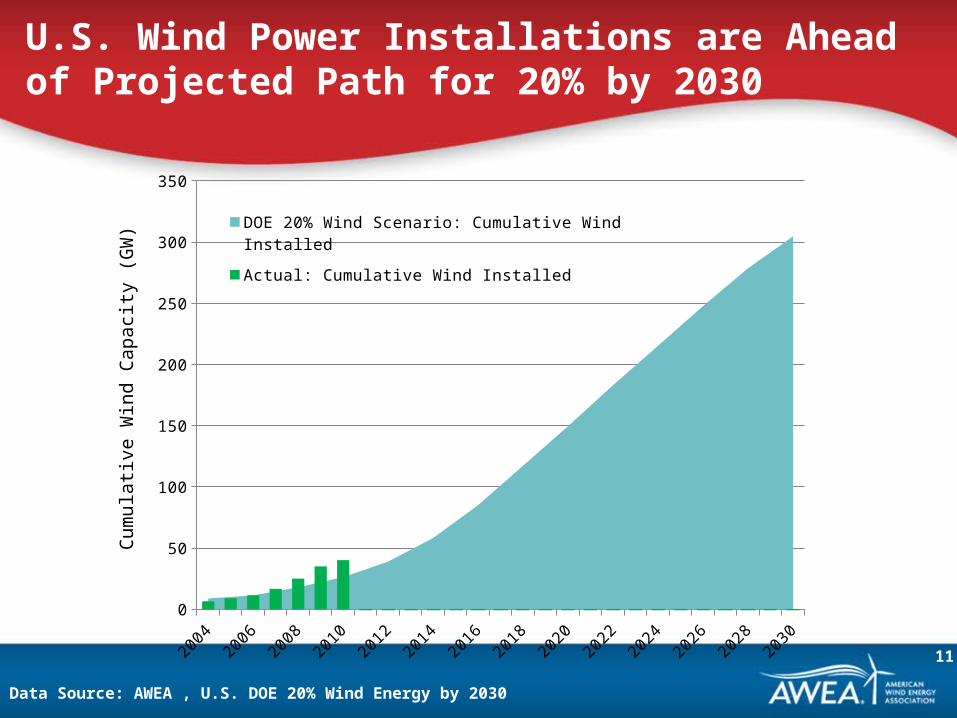

DOE 20% Wind Scenario: Cumulative Wind Installed

Actual: Cumulative Wind Installed

U.S. Wind Power Installations are Ahead of Projected Path for 20% by 2030

Data Source: AWEA , U.S. DOE 20% Wind Energy by 2030

Cum

ula

tive

Win

d C

apac

ity (

GW

)

11

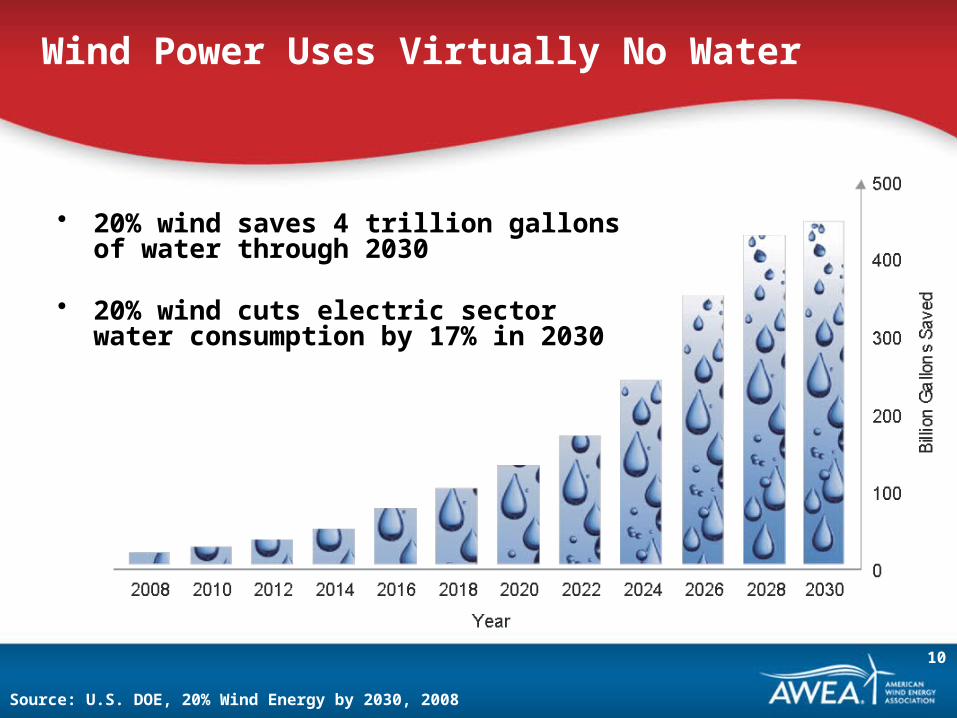

Wind Power Uses Virtually No Water

• 20% wind saves 4 trillion gallons of water through 2030

• 20% wind cuts electric sector water consumption by 17% in 2030

Source: U.S. DOE, 20% Wind Energy by 2030, 2008

10

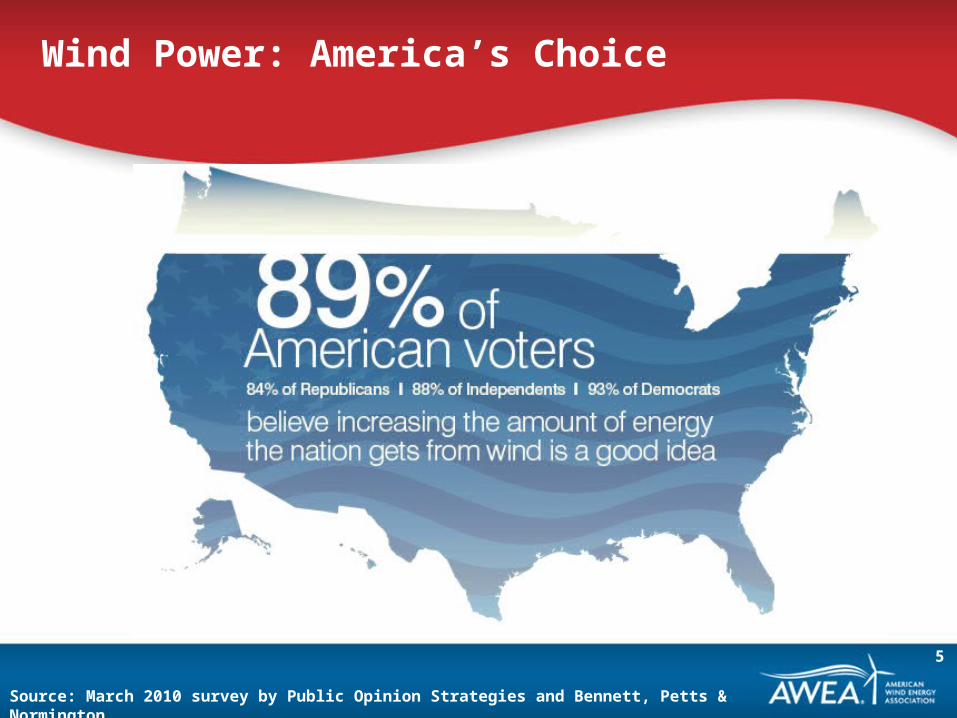

Wind Power: America’s Choice

Source: March 2010 survey by Public Opinion Strategies and Bennett, Petts & Normington

5

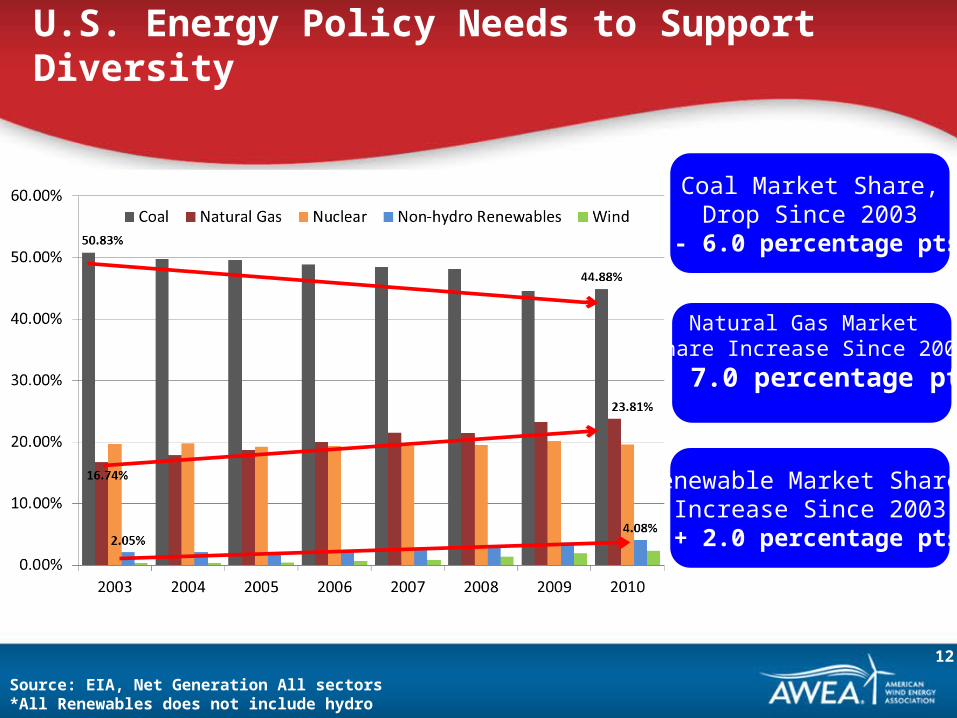

Coal Market Share,Drop Since 2003

- 6.0 percentage pts

Renewable Market Share,Increase Since 2003

+ 2.0 percentage pts

Natural Gas Market Share Increase Since 2003

+ 7.0 percentage pts

Source: EIA, Net Generation All sectors*All Renewables does not include hydro

U.S. Energy Policy Needs to Support Diversity

12

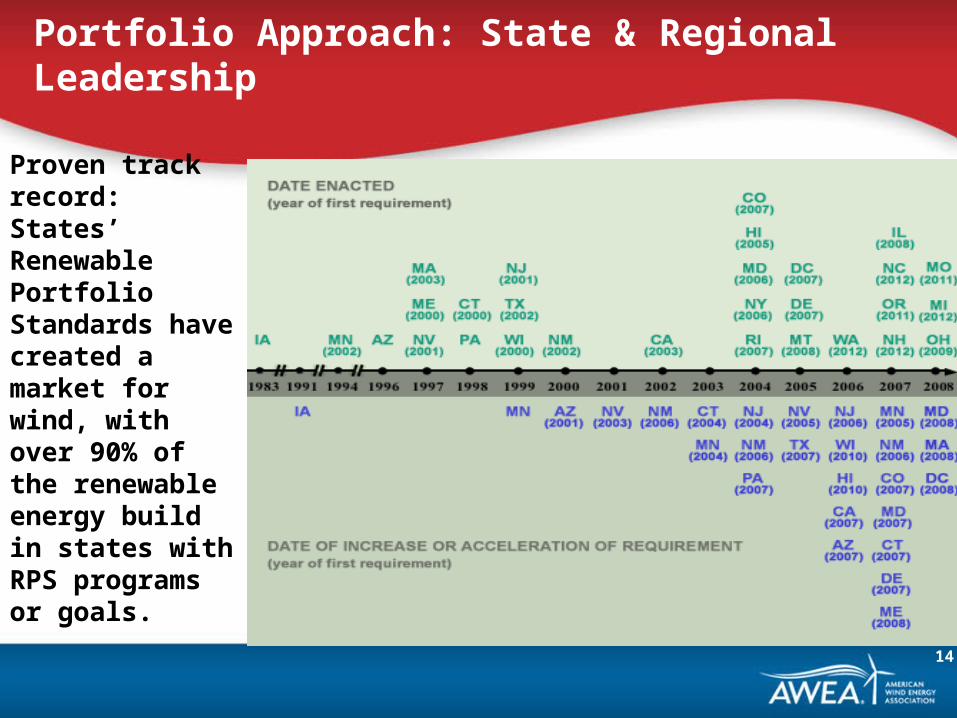

Proven track record: States’ Renewable Portfolio Standards have created a market for wind, with over 90% of the renewable energy build in states with RPS programs or goals.

Portfolio Approach: State & Regional Leadership

14

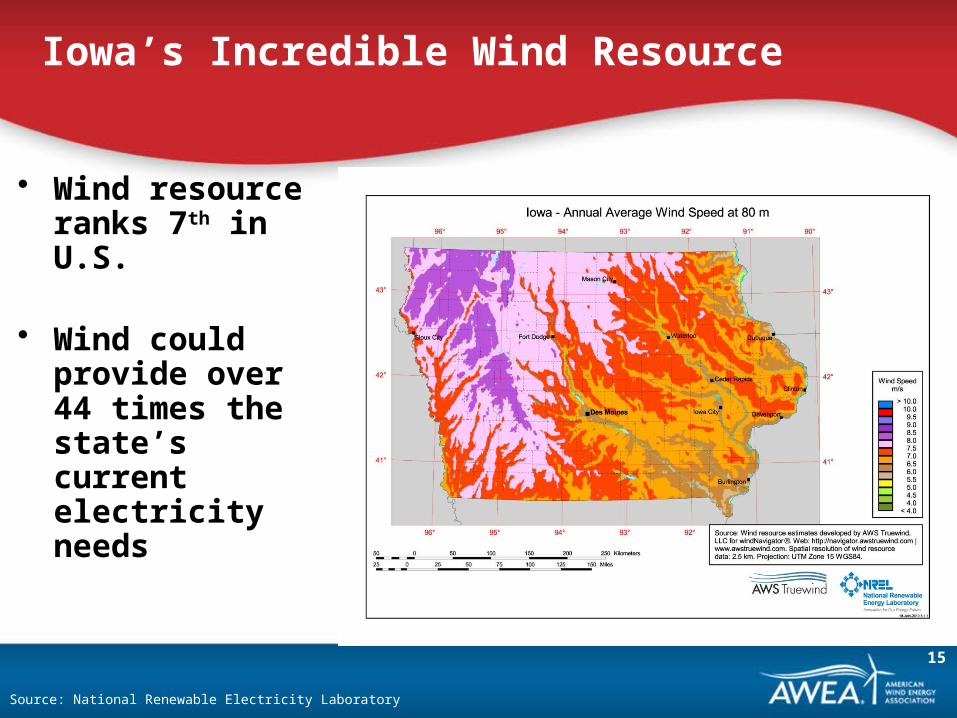

Iowa’s Incredible Wind Resource

• Wind resource ranks 7th in U.S.

• Wind could provide over 44 times the state’s current electricity needs

Source: National Renewable Electricity Laboratory

15

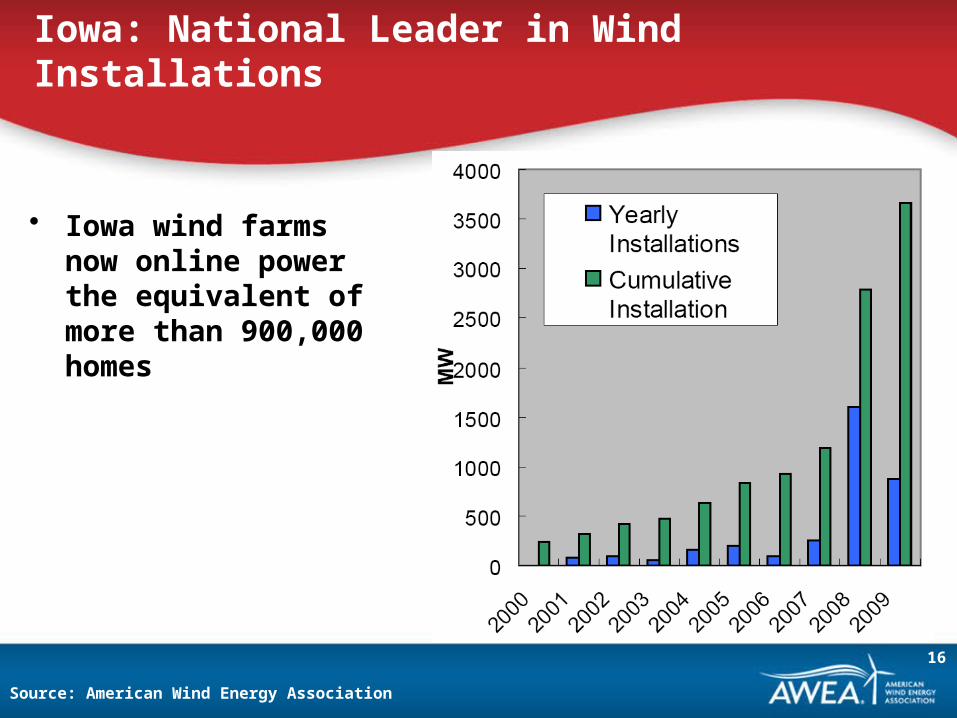

Iowa: National Leader in Wind Installations

• Iowa wind farms now online power the equivalent of more than 900,000 homes

Source: American Wind Energy Association

16

Mandatory RES

Voluntary standard or goal

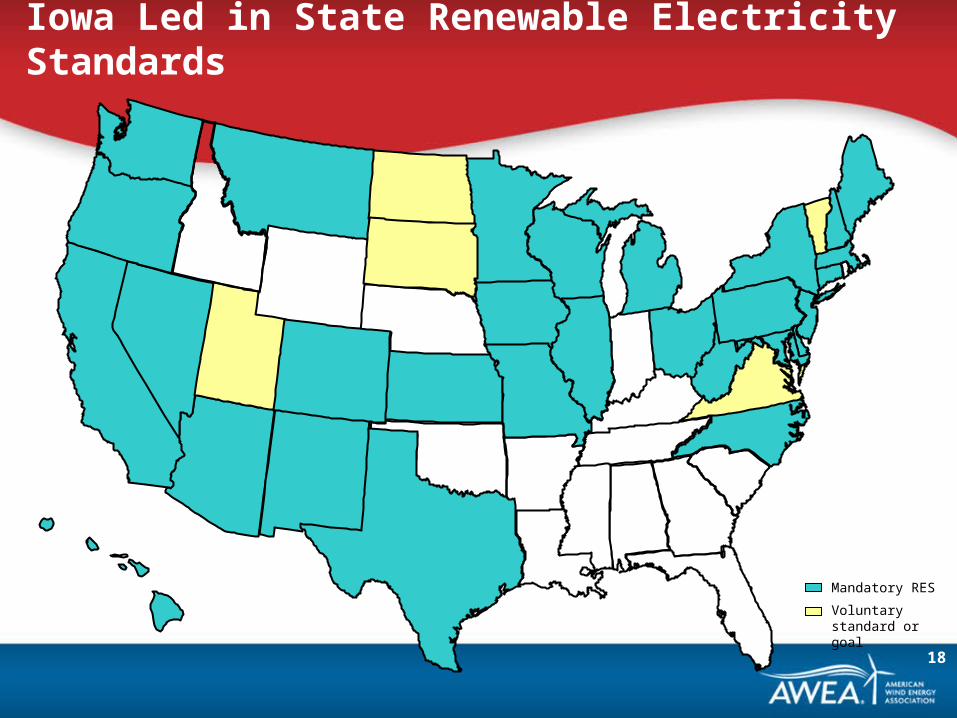

Iowa Led in State Renewable Electricity Standards

18

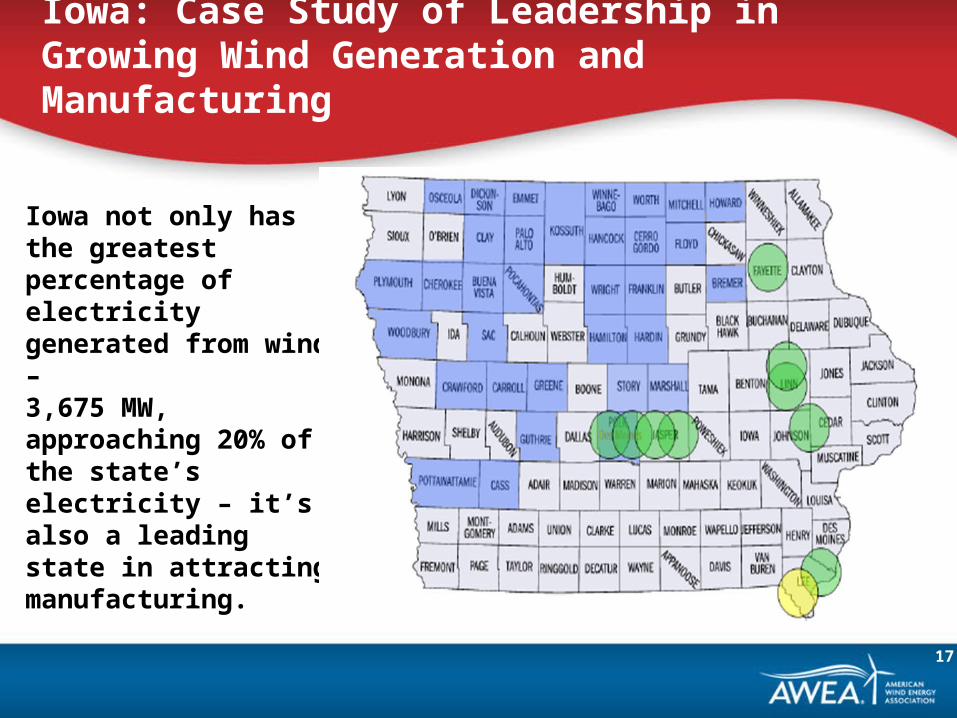

Iowa: Case Study of Leadership in Growing Wind Generation and Manufacturing

Iowa not only has the greatest percentage of electricity generated from wind – 3,675 MW, approaching 20% of the state’s electricity – it’s also a leading state in attracting manufacturing.

17

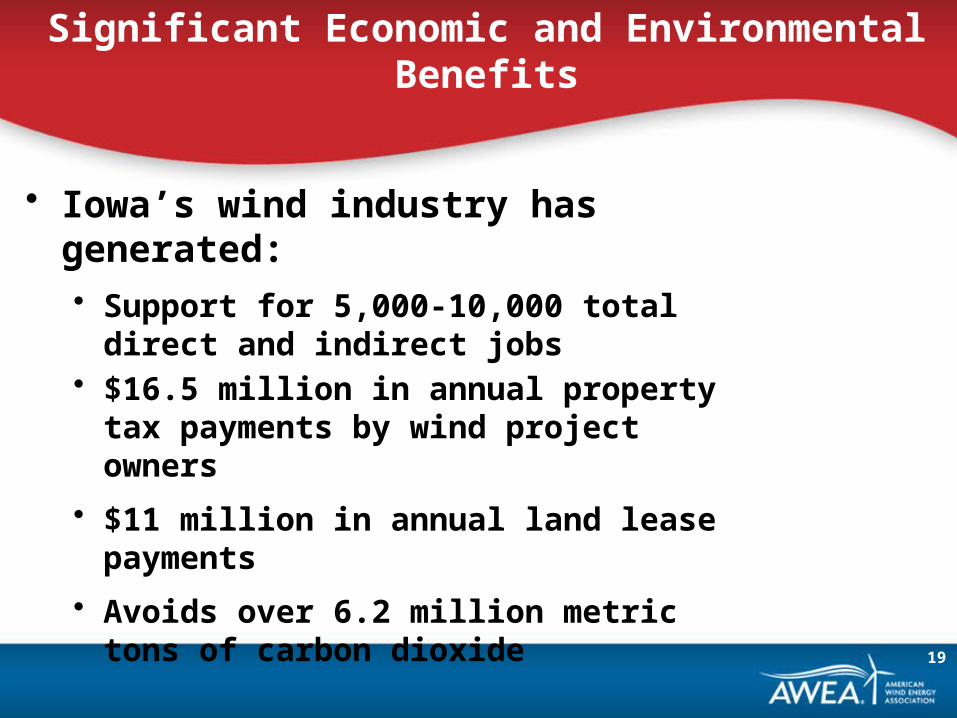

Significant Economic and Environmental Benefits

• Iowa’s wind industry has generated:• Support for 5,000-10,000 total direct and

indirect jobs• $16.5 million in annual property tax

payments by wind project owners

• $11 million in annual land lease payments

• Avoids over 6.2 million metric tons of carbon dioxide

19

Get more information

Sign up to take email actions

Attend one of the fastest-growing U.S. tradeshows: WINDPOWER 2012 Conference & ExhibitionAtlanta, GA | June 3-6, 2012

See www.awea.org for more information and events – covering wind farm siting, transmission, offshore wind, small and community wind, the supply chain, education, operations, and investment.

Remember to sign up to get updates and chances to take action at www.powerofwind.com

Attend one of the fastest-growing U.S. tradeshows

21