Embed Size (px)

Citation preview

Wind Energy UpdateMarch 2017

Maf SmithDeputy Chief Executive

About RenewableUK

• UK’s leading renewable energy trade association, founded in 1978.• 400 wind, wave and tidal members.• Influence policy development and represent sector in media.• Involve members via Forums and Working Groups• Lead organiser of conferences, exhibitions, trade delegations,

workshops and seminars.• Providing industry intelligence via Project Intelligence and on-line

Intelligence Hub

• We work across the four Governments of the UK, with offices in London, Cardiff and Belfast, and a close partnership with our sister organisation Scottish Renewables in Glasgow

2

Project Intelligence & online Hub

• Data used in this presentation comes from RenewableUK’s

– Offshore Wind Project Intelligence with Global Offshore analysis– Onshore Wind Project Intelligence with UK Onshore analysis– Marine Energy Project Intelligence with UK wave and tidal analysis

• ReneawbleUK’s new online Project Intelligence Hub is also searchable on contract and project basis, tracking market to date and forecasting ahead

3

Introduction

• Contribution of wind energy today

• Onshore wind intelligence & outlook

• Offshore wind intelligence & outlook

• The emerging policy landscape

Wind Energy key facts and figures

• Renewable electricity is now delivering 25% of GB power needs

• Wind delivering 11.5% of GB power needs, and now outperforming coal power.

Onshore Wind

• Onshore wind now demonstrably the cheapest option for new power generation, with rapid cost reduction

• Onshore wind also enjoys high UK content –currently at 67% - and high local content

RenewableUK (2015)

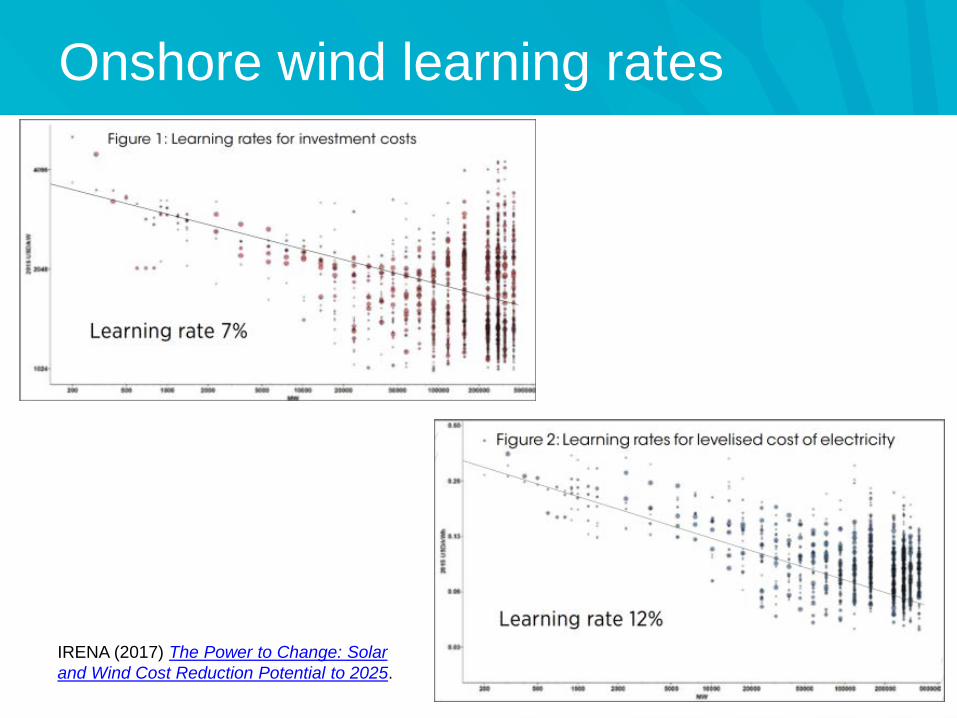

Onshore wind learning rates

IRENA (2017) The Power to Change: Solar and Wind Cost Reduction Potential to 2025.

Onshore’s onward march

• “Wind and solar keep getting cheaper. While already competitive in a number of countries today without policy support, the cost of onshore wind is expected to drop 41% by 2040.

• “As new wind and solar capacity is added worldwide, generation using these technologies rises ninefold to 10,591TWh by 2040, and to 30% of the global total, from 5% in 2015.

• “By 2040, Germany, Mexico, the UK and Australia all have average wind and solar penetration of more than 50%.

Bloomberg New Energy Finance (2016) New Energy Outlook

Onshore delivery

Onshore delivery

Source: RenewableUK Onshore Wind Project Intelligence

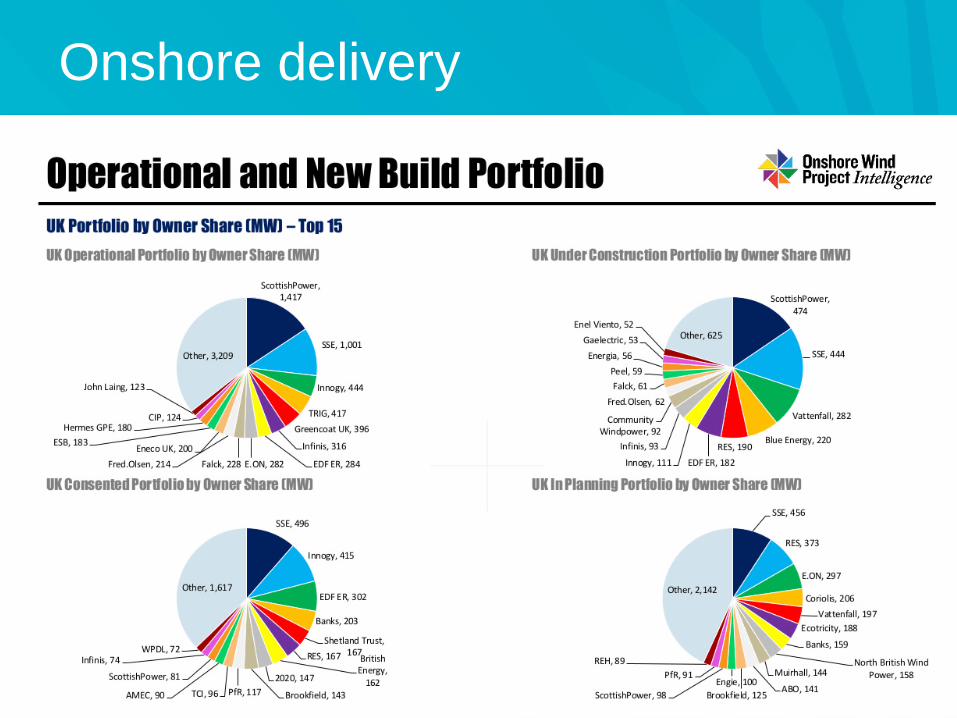

Onshore delivery

Source: RenewableUK Onshore Wind Project Intelligence

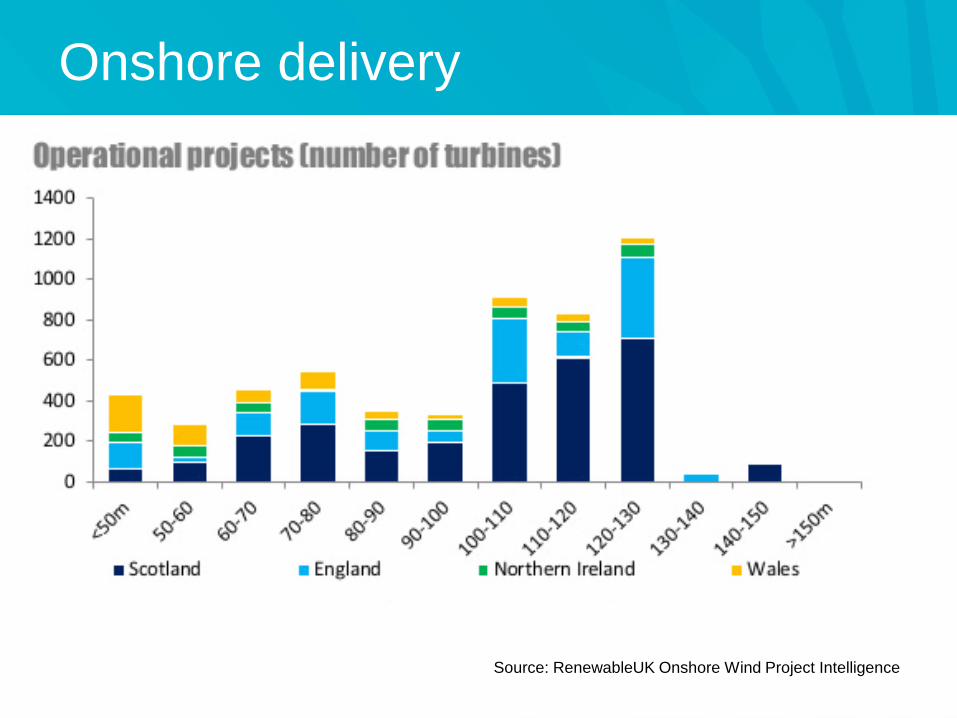

Onshore delivery

Source: RenewableUK Onshore Wind Project Intelligence

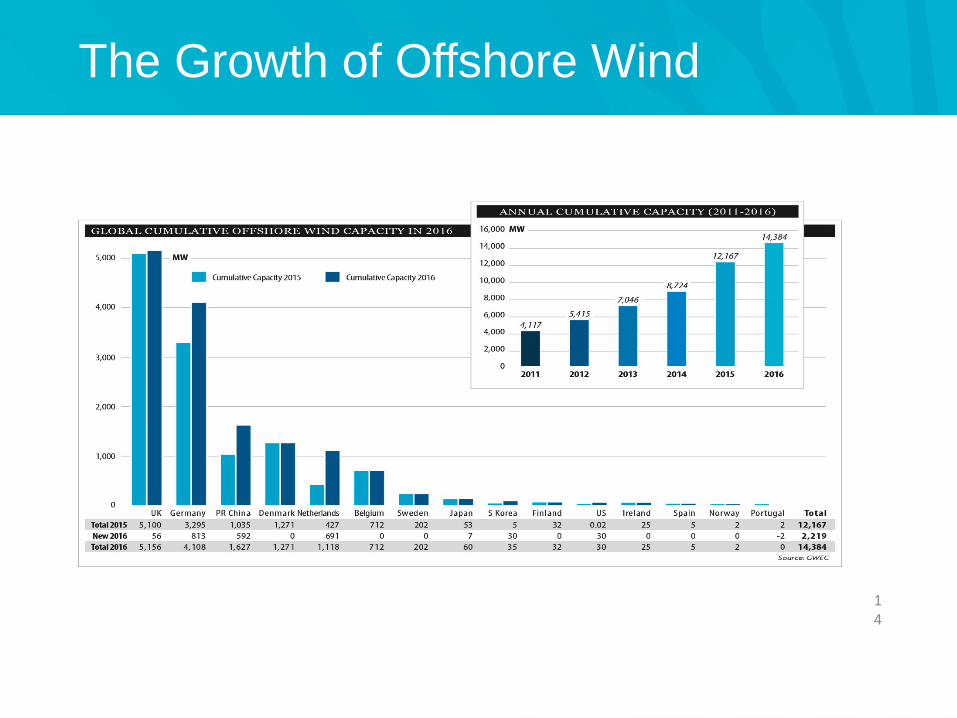

The Growth of Offshore Wind

14

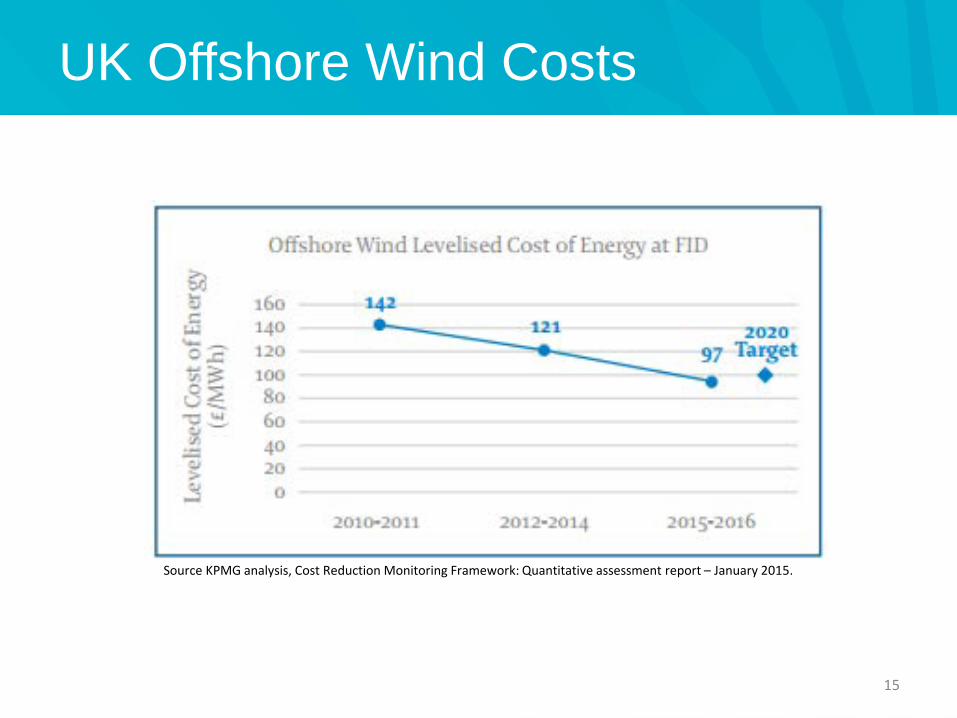

UK Offshore Wind Costs

15

Source KPMG analysis, Cost Reduction Monitoring Framework: Quantitative assessment report – January 2015.

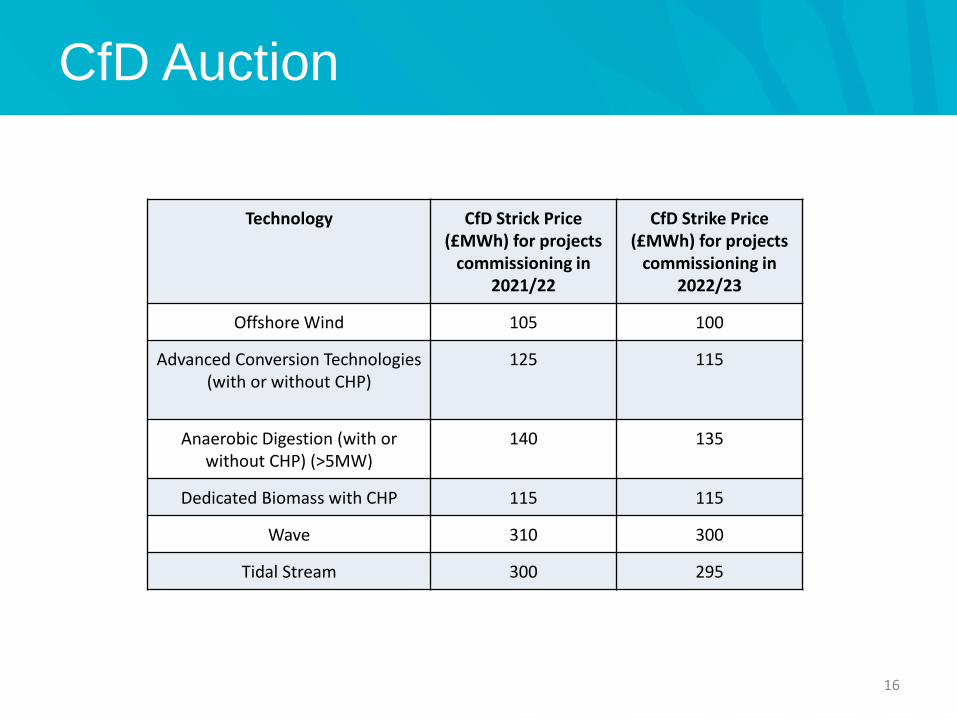

CfD Auction

16

Technology CfD Strick Price (£MWh) for projects

commissioning in 2021/22

CfD Strike Price (£MWh) for projects

commissioning in 2022/23

Offshore Wind 105 100

Advanced Conversion Technologies (with or without CHP)

125 115

Anaerobic Digestion (with or without CHP) (>5MW)

140 135

Dedicated Biomass with CHP 115 115

Wave 310 300

Tidal Stream 300 295

European Offshore Wind Costs

17

Opportunities in Offshore Wind

18

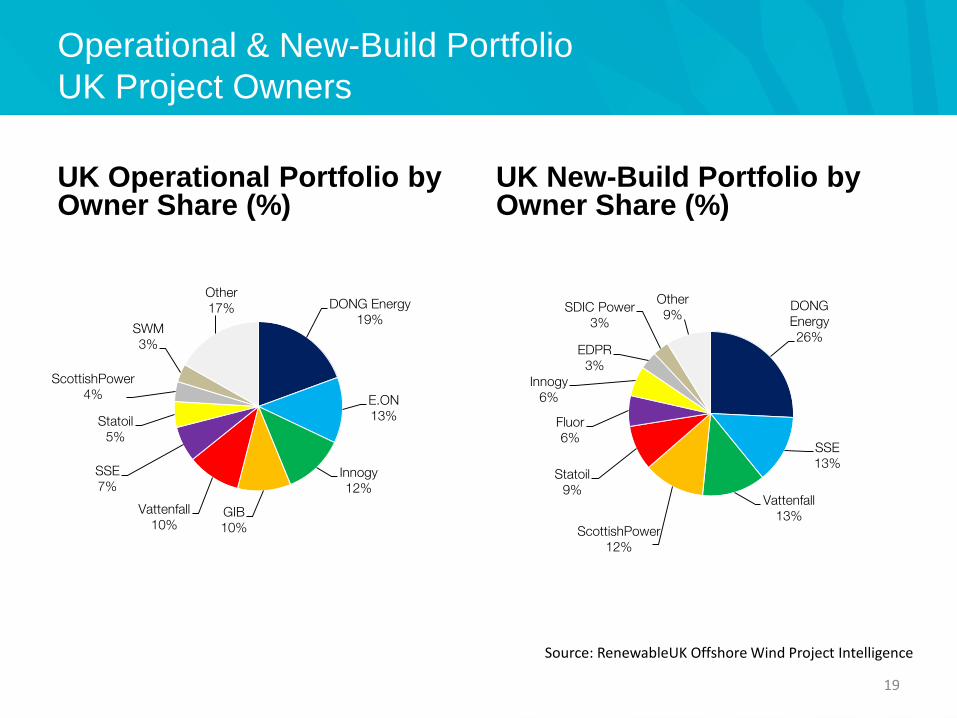

Operational & New-Build Portfolio UK Project Owners

UK Operational Portfolio by Owner Share (%)

UK New-Build Portfolio by Owner Share (%)

19

DONG Energy19%

E.ON13%

Innogy12%

GIB10%

Vattenfall10%

SSE7%

Statoil5%

ScottishPower4%

SWM3%

Other17% DONG

Energy26%

SSE13%

Vattenfall13%

ScottishPower12%

Statoil9%

Fluor6%

Innogy6%

EDPR3%

SDIC Power3%

Other9%

Source: RenewableUK Offshore Wind Project Intelligence

Operational & New-Build Portfolio – Europe

Europe Operational Portfolio by Country (MW)

Europe New-Build Portfolio by Country (MW)

20

5,098

3,283 518 01,271 712 255

0

2,000

4,000

6,000

8,000

10,000

12,000

29,388

21,234 4,100 2,988 1,776 1,355 3,305

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Source: RenewableUK Offshore Wind Project Intelligence

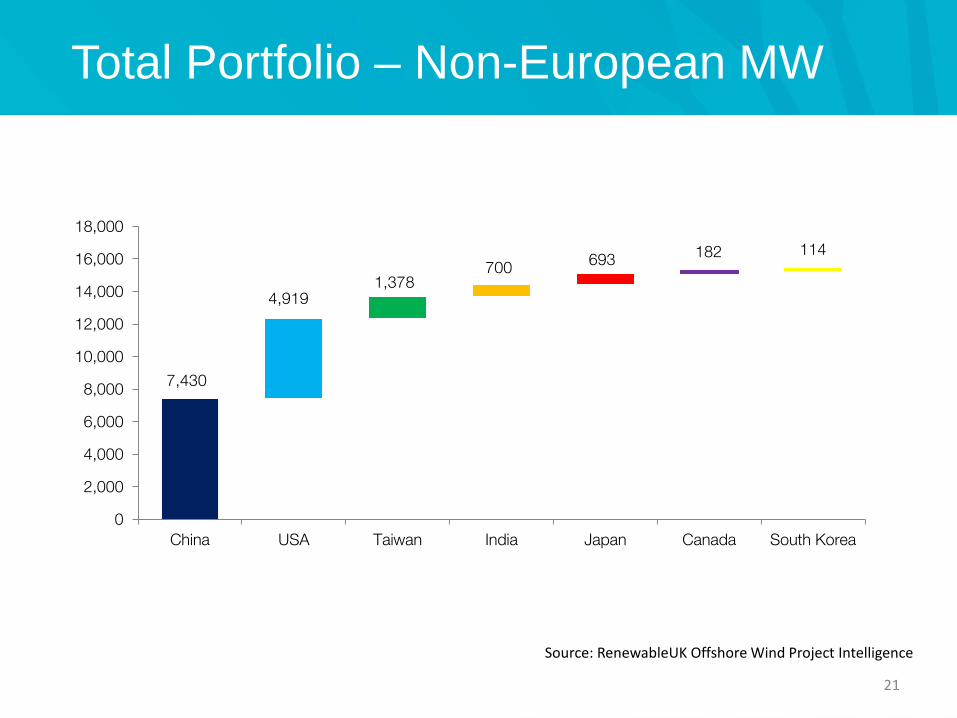

Total Portfolio – Non-European MW

21

7,430

4,9191,378

700 693 182 114

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

China USA Taiwan India Japan Canada South Korea

Source: RenewableUK Offshore Wind Project Intelligence

Commissioning Forecast – Europe

22

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

UK Germany Netherlands France Denmark Belgium Other Cumulative

Source: RenewableUK Offshore Wind Project Intelligence

In Conclusion

• The future progress of wind energy is seen as inevitable within global market

• UK Government focus is on Industrial Strategy, securing economic opportunities of low carbon generation, while keeping costs down for energy consumers. Wind plays well to both these requirements.

• Onshore wind costs now rival those of traditional alternatives, while avoiding carbon impacts and fuel imports

– UK Government committed to end subsidy and changed English planning laws. – Future schemes will be built without subsidy, but there is strong political support for

this in Scotland, with interest in Wales and NI– High UK content and shift of market to Scotland

• Offshore wind costs now competitive with new nuclear and in-line to be competitive with new gas in mid 2020s

– Sector has a strong pipeline and expectations around delivery of UK supply chain and ongoing cost reduction

– Supply chain investments means UK content increasing rapidly, with investments focused in coastal and manufacturing communities

In Conclusion

• The future progress of wind energy is seen as inevitable within global market

• UK Government focus is on Industrial Strategy, securing economic opportunities of low carbon generation, while keeping costs down for energy consumers. Wind plays well to both these requirements.

• Onshore wind costs now rival those of traditional alternatives, while avoiding carbon impacts and fuel imports

– UK Government committed to end subsidy and changed English planning laws. – Future schemes will be built without subsidy, but there is strong political support for

this in Scotland, with interest in Wales and NI– High UK content and shift of market to Scotland

• Offshore wind costs now competitive with new nuclear and in-line to be competitive with new gas in mid 2020s

– Sector has a strong pipeline and expectations around delivery of UK supply chain and ongoing cost reduction

– Supply chain investments means UK content increasing rapidly, with investments focused in coastal and manufacturing communities

In Conclusion

• The future progress of wind energy is seen as inevitable within global market

• UK Government focus is on Industrial Strategy, securing economic opportunities of low carbon generation, while keeping costs down for energy consumers. Wind plays well to both these requirements.

• Onshore wind costs now rival those of traditional alternatives, while avoiding carbon impacts and fuel imports

– UK Government committed to end subsidy and changed English planning laws. – Future schemes will be built without subsidy, but there is strong political support for

this in Scotland, with interest in Wales and NI– High UK content and shift of market to Scotland

• Offshore wind costs now competitive with new nuclear and in-line to be competitive with new gas in mid 2020s

– Sector has a strong pipeline and expectations around delivery of UK supply chain and ongoing cost reduction

– Supply chain investments means UK content increasing rapidly, with investments focused in coastal and manufacturing communities

In Conclusion

• The future progress of wind energy is seen as inevitable within global market

• UK Government focus is on Industrial Strategy, securing economic opportunities of low carbon generation, while keeping costs down for energy consumers. Wind plays well to both these requirements.

• Onshore wind costs now rival those of traditional alternatives, while avoiding carbon impacts and fuel imports

– UK Government committed to end subsidy and changed English planning laws. – Future schemes will be built without subsidy, but there is strong political support for

this in Scotland, with interest in Wales and NI– High UK content and shift of market to Scotland

• Offshore wind costs now competitive with new nuclear and in-line to be competitive with new gas in mid 2020s

– Sector has a strong pipeline and expectations around delivery of UK supply chain and ongoing cost reduction

– Supply chain investments means UK content increasing rapidly, with investments focused in coastal and manufacturing communities