Embed Size (px)

Citation preview

Why Trade Agreements Matter: The Case for U.S. Dairy

Sharon SydowOffice of the Chief Economist, USDAGlobal Dairy SymposiumOctober 6, 2016

Photo credit: DATCP

Presentation Overview

•USDA Supply and Demand Outlook for U.S. Dairy

•Structural Change in the U.S. Dairy Sector

•Why Trade Agreements Matter for U.S. Dairy

Office of the Chief Economist

USDA Dairy Market Outlook

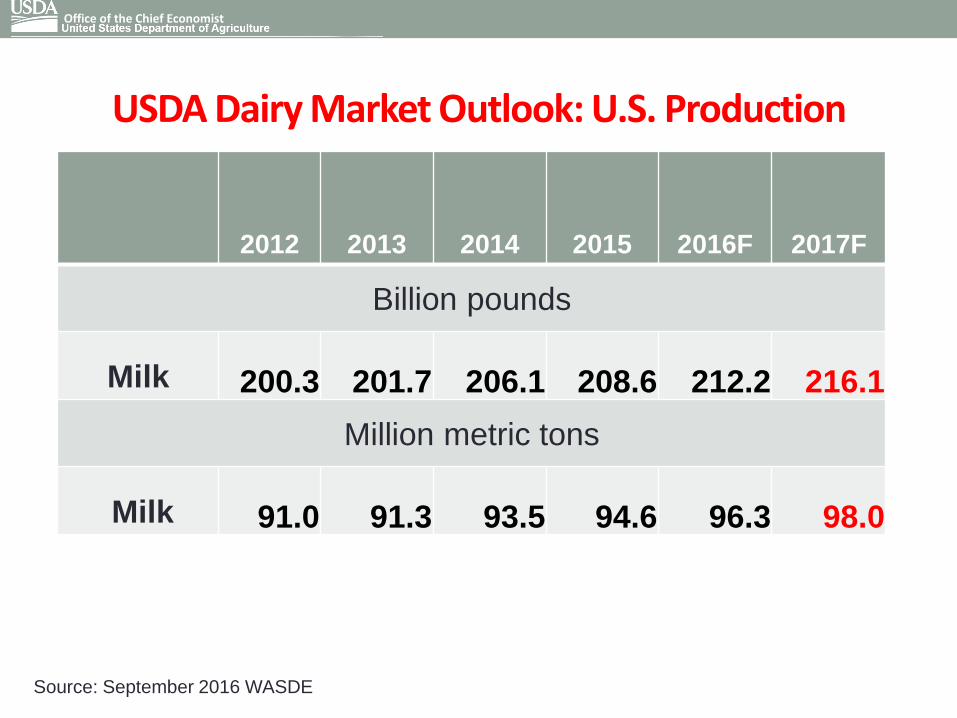

• U.S. milk production in 2016 estimated to increase from 2015. Record production is projected for 2017.

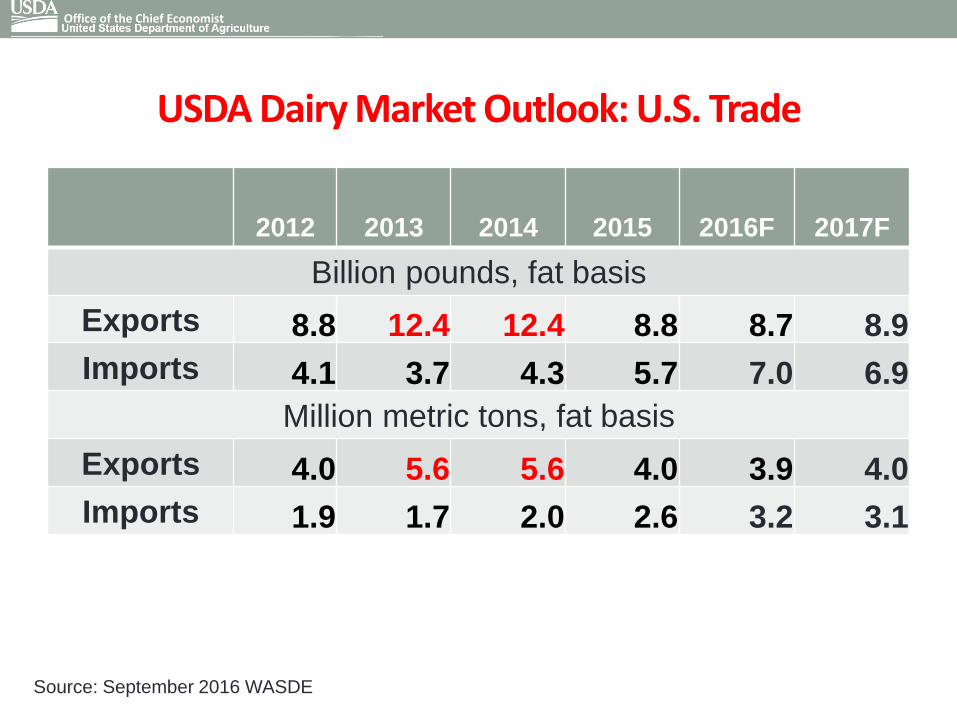

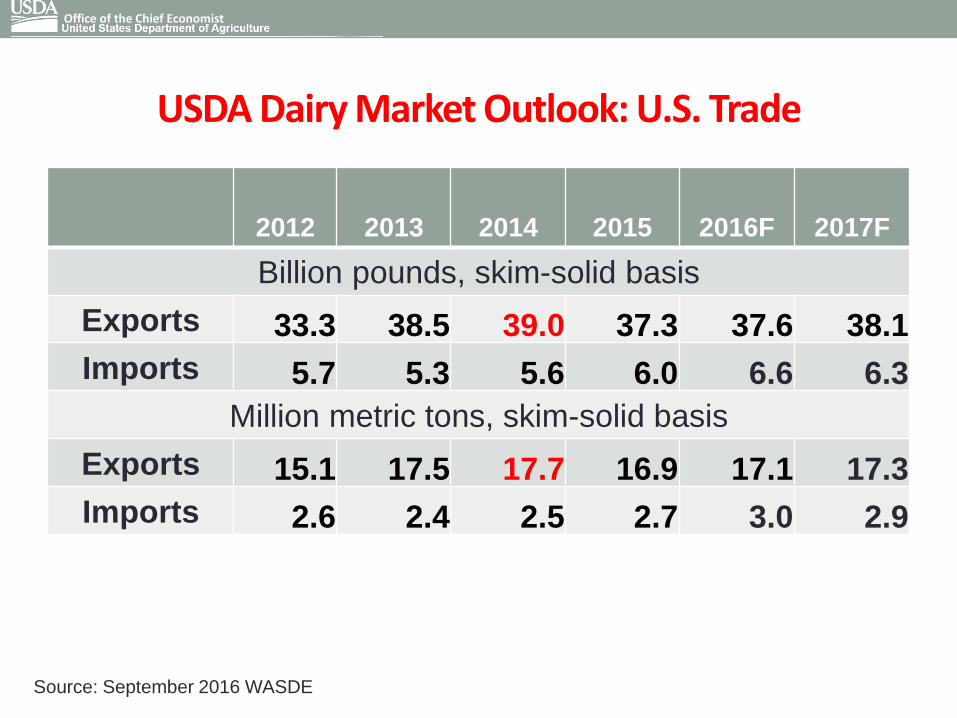

• U.S. dairy exports projected to rebound, while U.S. dairy imports start to decrease slightly.

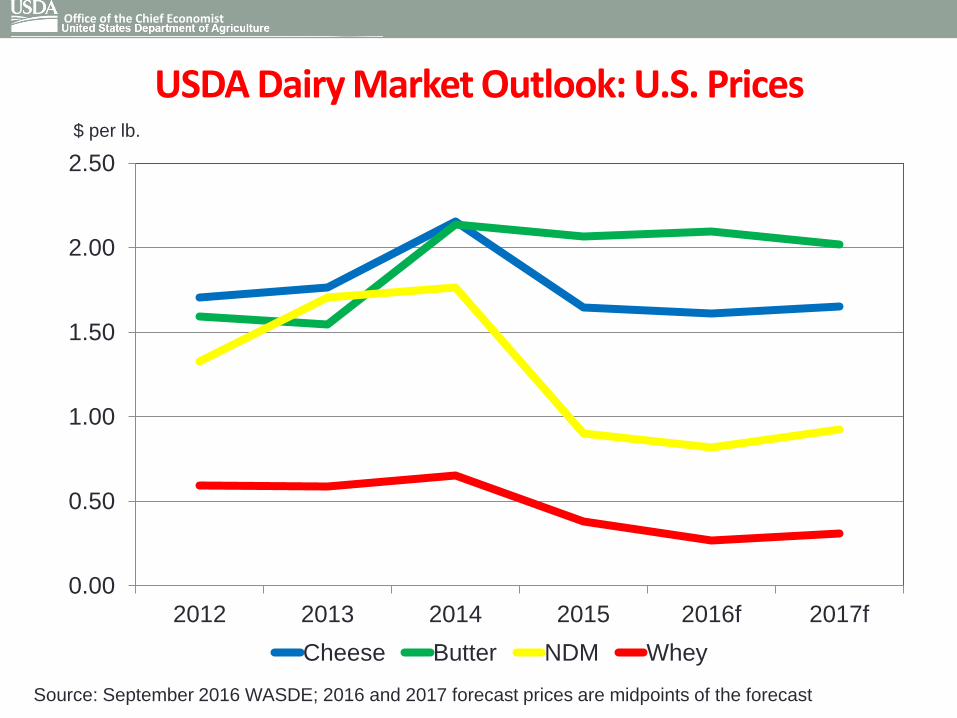

• Some improvement in price forecast for 2017 for cheese, NDM and whey; butter prices projected to decline.

• Ending stocks for 2016 and 2017 reflect relatively high stocks of butter and cheese; 2017 ending stocks projected to decline slightly from 2016 forecast levels (both fat basis and skim-solid basis).

Office of the Chief Economist

USDA Dairy Market Outlook: U.S. Production

Office of the Chief Economist

Source: September 2016 WASDE

2012 2013 2014 2015 2016F 2017F

Billion pounds

Milk 200.3 201.7 206.1 208.6 212.2 216.1

Million metric tons

Milk 91.0 91.3 93.5 94.6 96.3 98.0

USDA Dairy Market Outlook: U.S. Trade

Office of the Chief Economist

Source: September 2016 WASDE

2012 2013 2014 2015 2016F 2017F

Billion pounds, fat basis

Exports 8.8 12.4 12.4 8.8 8.7 8.9

Imports 4.1 3.7 4.3 5.7 7.0 6.9

Million metric tons, fat basis

Exports 4.0 5.6 5.6 4.0 3.9 4.0

Imports 1.9 1.7 2.0 2.6 3.2 3.1

USDA Dairy Market Outlook: U.S. Trade

Office of the Chief Economist

Source: September 2016 WASDE

2012 2013 2014 2015 2016F 2017F

Billion pounds, skim-solid basis

Exports 33.3 38.5 39.0 37.3 37.6 38.1

Imports 5.7 5.3 5.6 6.0 6.6 6.3

Million metric tons, skim-solid basis

Exports 15.1 17.5 17.7 16.9 17.1 17.3

Imports 2.6 2.4 2.5 2.7 3.0 2.9

USDA Dairy Market Outlook: U.S. Prices

0.00

0.50

1.00

1.50

2.00

2.50

2012 2013 2014 2015 2016f 2017f

Cheese Butter NDM Whey

Office of the Chief Economist

Source: September 2016 WASDE; 2016 and 2017 forecast prices are midpoints of the forecast

$ per lb.

U.S. Dairy Sector and Structural Change

• Increased productivity through economies of scale; lower cost of production and improved competitiveness

• Well-developed processing sector known for product innovation

• Shift in U.S. dairy support programs from market price support to margin protection

• Increasingly export-oriented; well positioned to respond to increased overseas demand and new market openings through trade agreements (including FTAs)

Office of the Chief Economist

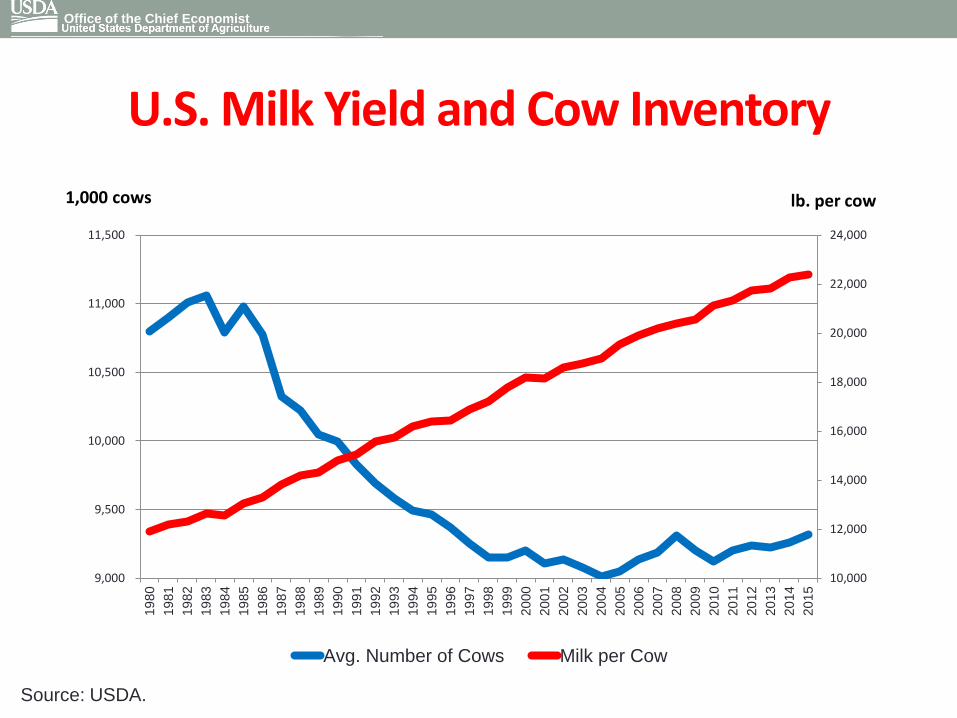

U.S. Milk Yield and Cow Inventory

10,000

12,000

14,000

16,000

18,000

20,000

22,000

24,000

9,000

9,500

10,000

10,500

11,000

11,500

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

Avg. Number of Cows Milk per Cow

1,000 cows lb. per cow

Office of the Chief Economist

Source: USDA.

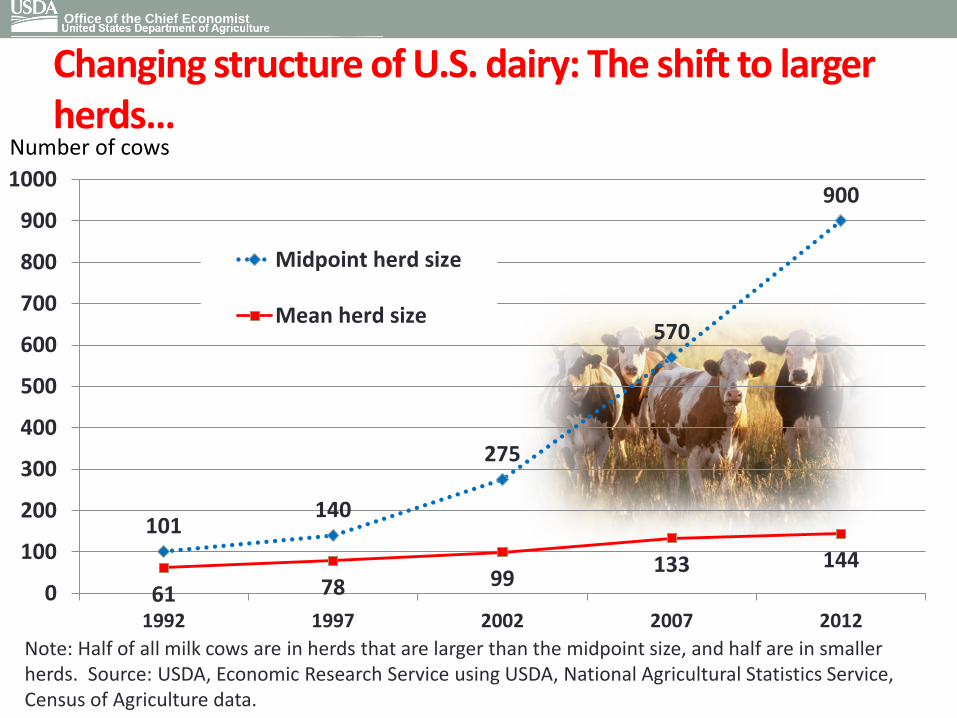

Changing structure of U.S. dairy: The shift to larger herds…

101140

275

570

900

61 78 99133 144

0

100

200

300

400

500

600

700

800

900

1000

1992 1997 2002 2007 2012

Midpoint herd size

Mean herd size

Number of cows

Note: Half of all milk cows are in herds that are larger than the midpoint size, and half are in smaller herds. Source: USDA, Economic Research Service using USDA, National Agricultural Statistics Service, Census of Agriculture data.

Office of the Chief Economist

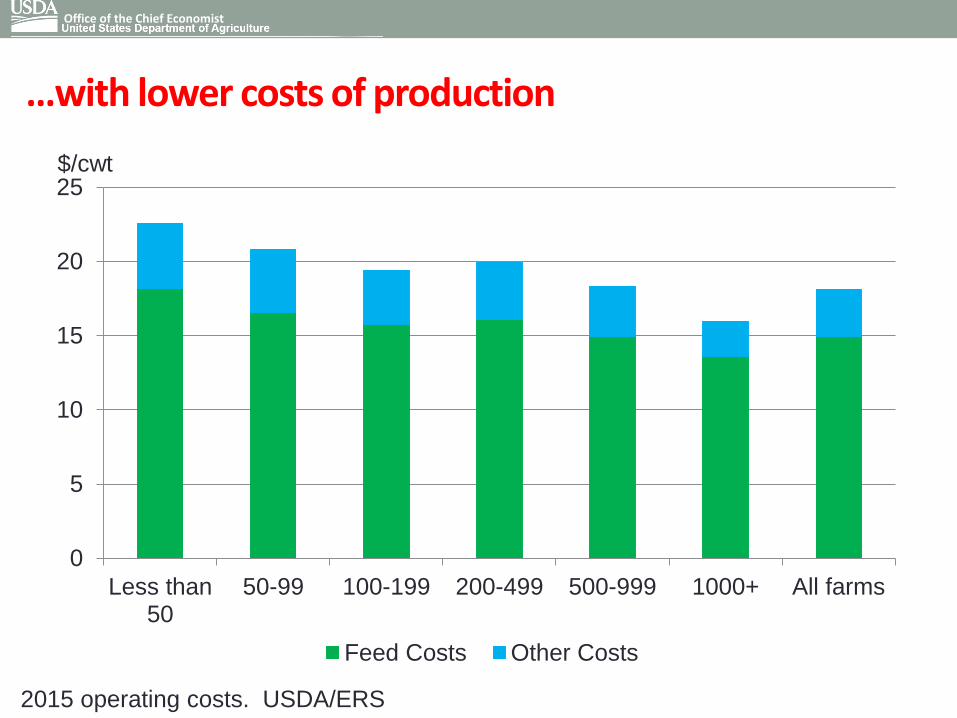

…with lower costs of production

Office of the Chief Economist

0

5

10

15

20

25

Less than50

50-99 100-199 200-499 500-999 1000+ All farms

Feed Costs Other Costs

$/cwt

2015 operating costs. USDA/ERS

Source: Mark W. Stephenson, PhD, University of Wisconsin

Office of the Chief Economist

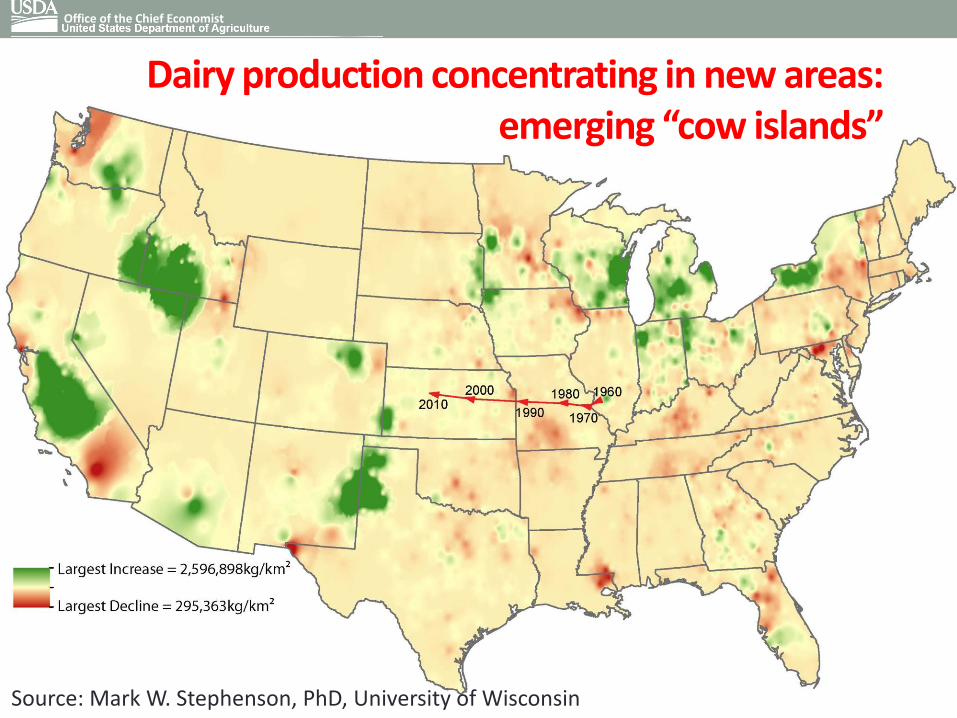

Dairy production concentrating in new areas: emerging “cow islands”

Office of the Chief Economist

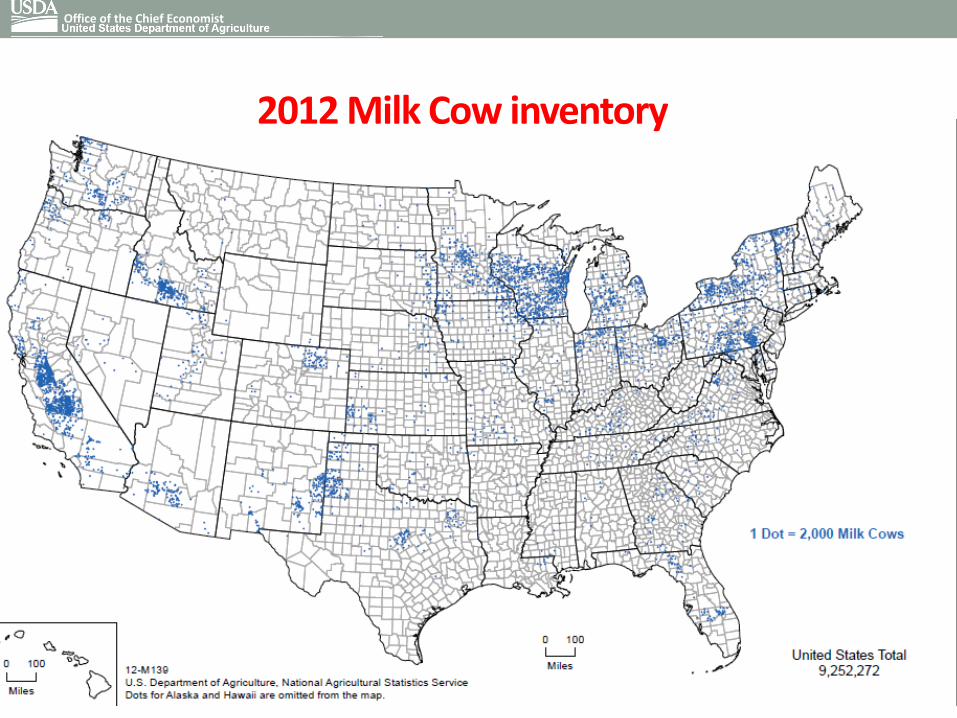

2012 Milk Cow inventory

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

5-Yr CAGR Yield Per Cow US Population Growth

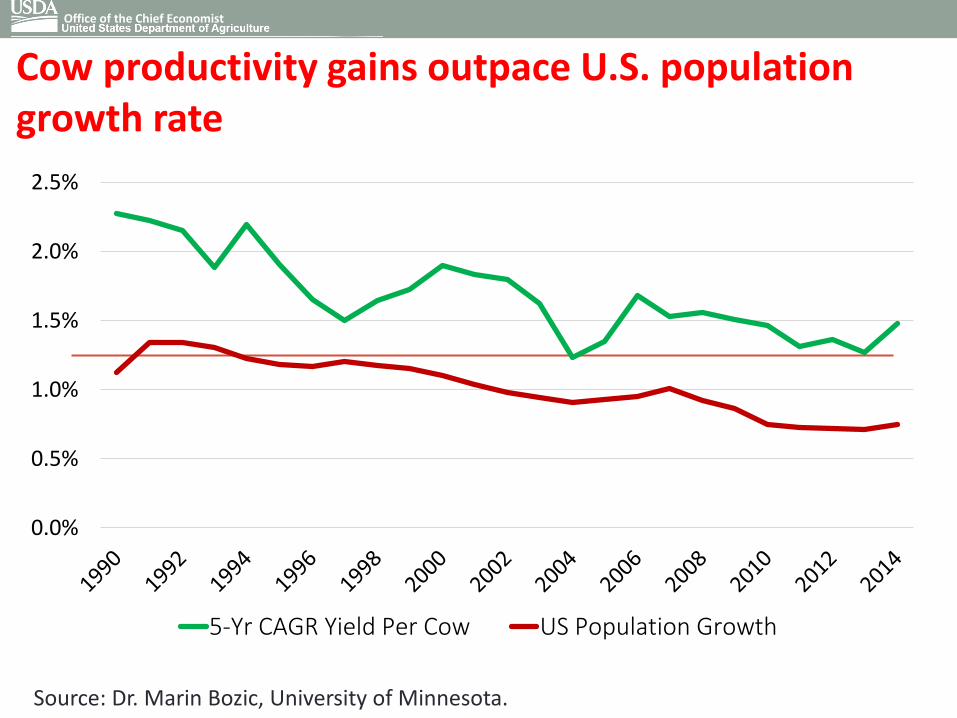

Cow Productivity Gains Outpace U.S. Population Growth Rate

Office of the Chief Economist

Cow productivity gains outpace U.S. population growth rate

Source: Dr. Marin Bozic, University of Minnesota.

Cow Productivity Gains Outpace U.S. Population Growth Rate

Office of the Chief Economist

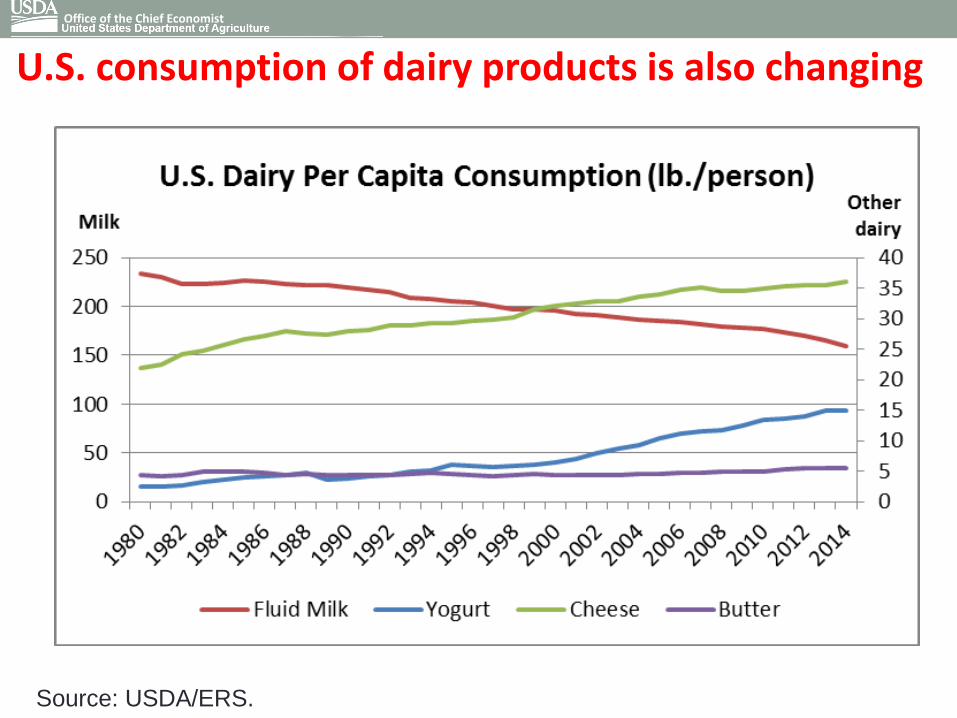

U.S. consumption of dairy products is also changing

Source: USDA/ERS.

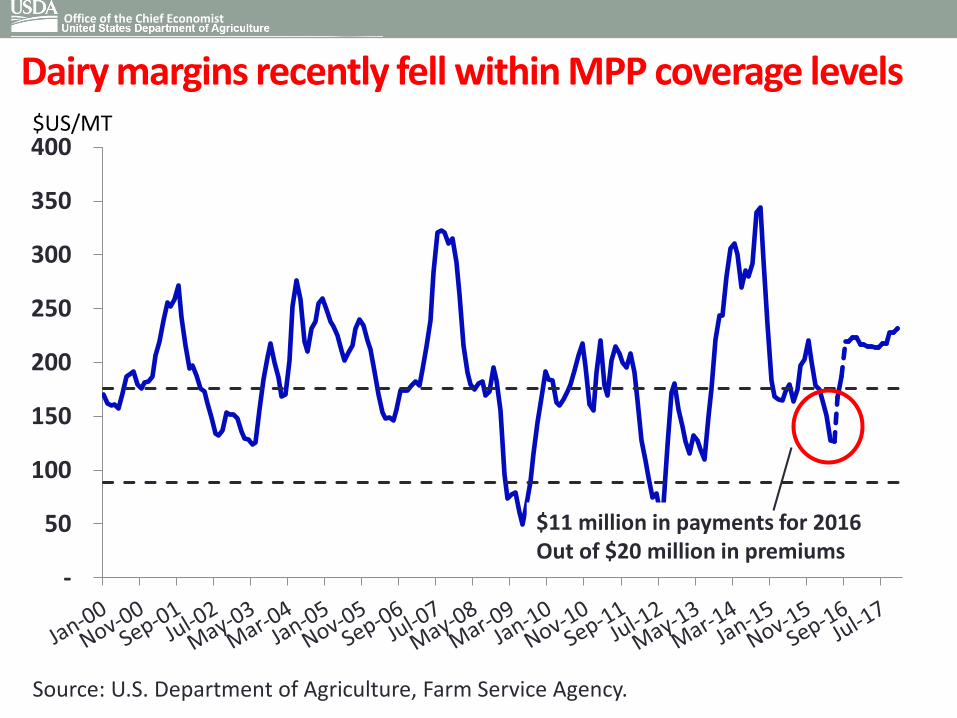

Dairy margins recently fell within MPP coverage levels

-

50

100

150

200

250

300

350

400$US/MT

Office of the Chief Economist

Source: U.S. Department of Agriculture, Farm Service Agency.

$11 million in payments for 2016Out of $20 million in premiums

Office of the Chief Economist

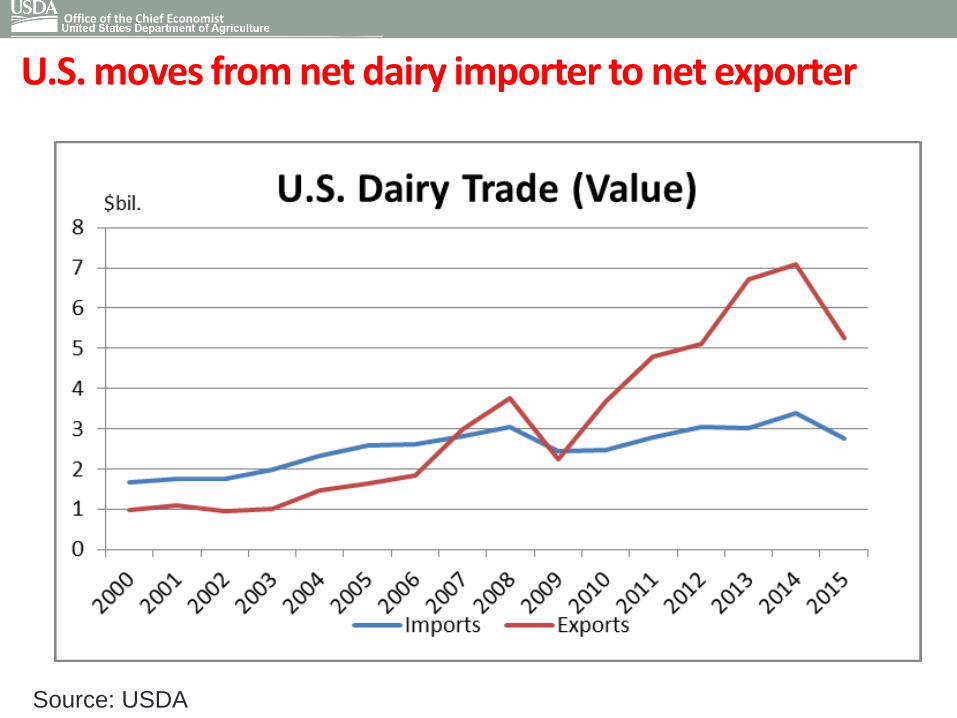

U.S. moves from net dairy importer to net exporter

Office of the Chief Economist

$11 million in payments for 2016Out of $20 million in premiums

Office of the Chief Economist

Source: USDA

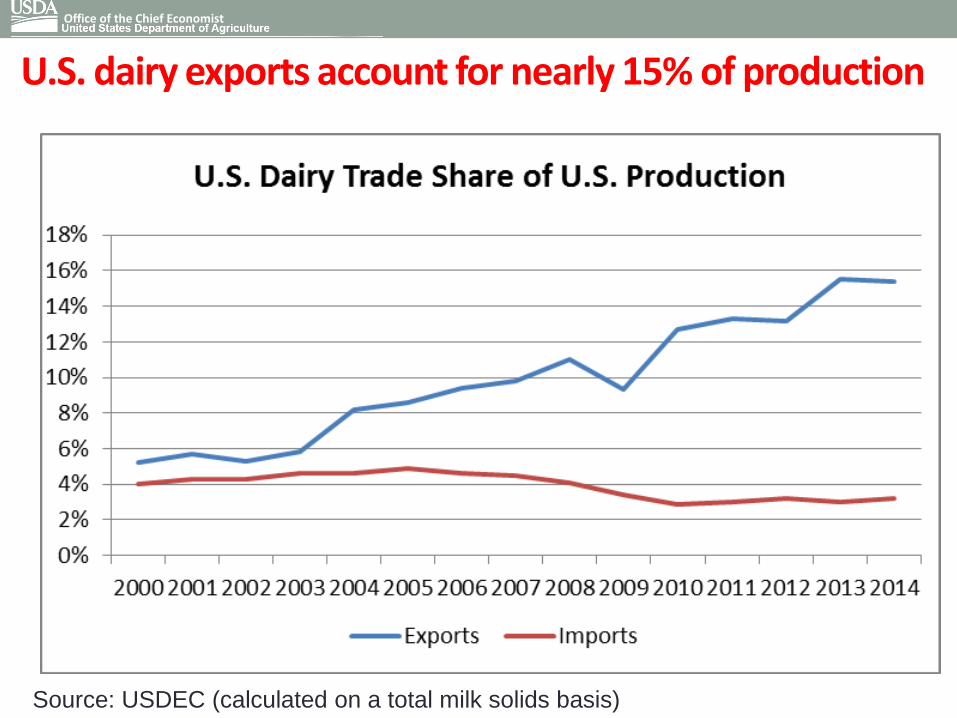

U.S. dairy exports account for nearly 15% of production

Office of the Chief Economist

$11 million in payments for 2016Out of $20 million in premiums

Office of the Chief Economist

Source: USDEC (calculated on a total milk solids basis)

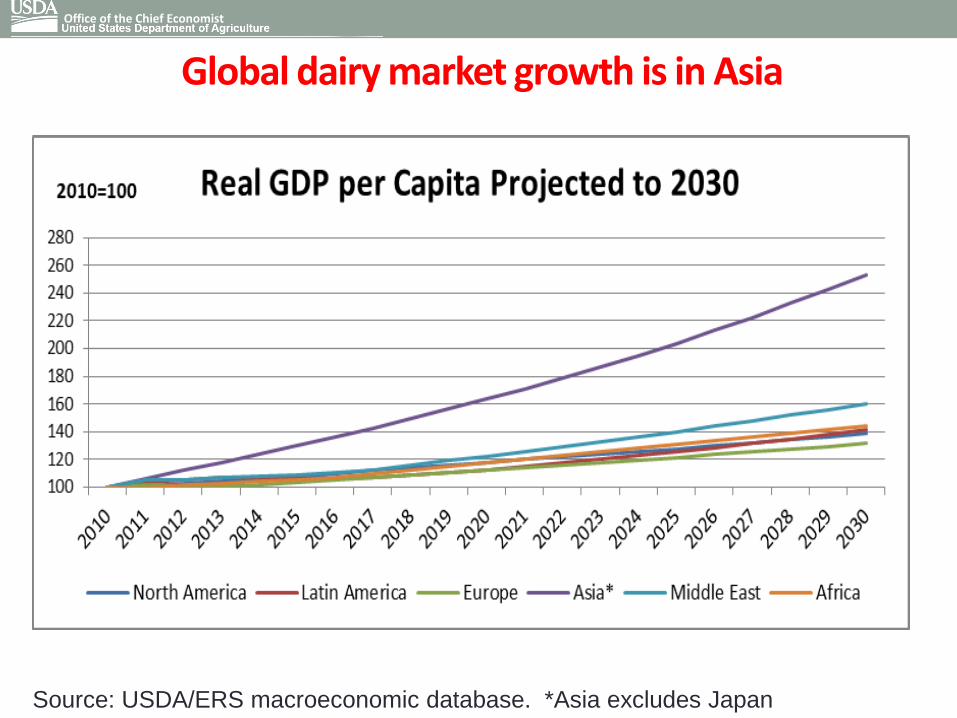

Global dairy market growth is in Asia

Office of the Chief Economist

$11 million in payments for 2016Out of $20 million in premiums

Office of the Chief Economist

Source: USDA/ERS macroeconomic database. *Asia excludes Japan

Why FTAs and Trade Liberalization Matter

• U.S. dairy exports to FTA partners have grown from $476

million in 2000 to $2.8 billion in 2015. The rate of growth

in trade with FTA partners has exceeded that for U.S.

dairy exports to all markets.

• According to NMPF/USDEC, this increased trade from

FTAs helped bring an additional $8.3 billion to the U.S.

dairy industry over 10 years and contributed to higher

U.S. milk prices and incomes during that period.

• Many U.S. FTA partners are developing countries, where

demand growth is expected to be the strongest.

Office of the Chief Economist

Why FTAs and Trade Liberalization Matter

• Most U.S. FTAs are with partners in the Western Hemisphere region.• NAFTA, CAFTA-DR, Colombia, Peru, Panama, Chile

• Australia, South Korea, and Singapore the only U.S. FTAs in Asia-Pacific region

• Other dairy exporters are negotiating (or have implemented) preferential trade agreements in the Asia-Pacific region.

• Not only do these other agreements provide preferential access, they also affect how certain rules are written (SPS, GIs).

Office of the Chief Economist

Gains from Further Liberalization - TPP

• The Trans Pacific Partnership (TPP) was concluded on Oct. 5,

2015 and signed on Feb. 4, 2016.

• The agreement covers 12 countries, many of which are in Asia

and are new FTA partners – Japan, Malaysia, Vietnam, Brunei,

and New Zealand.

• The agreement grants significant new and enhanced market

access into these markets. It also provides new access into

Canada, an existing FTA partner.

• Most tariffs will be eliminated; for sensitive products there will

be longer transitions and some TRQs and limited safeguards

Office of the Chief Economist

Gains from Further Liberalization - TPP

• TPP goes beyond past FTAs to establish strong rules for

trade in agricultural products:

• SPS: enforceable rules

• Geographical Indications (GIs): stronger due process

and transparency disciplines

• Agricultural Biotechnology: first time covered in a FTA

• Organic Agriculture: encourage mutual recognition

Office of the Chief Economist

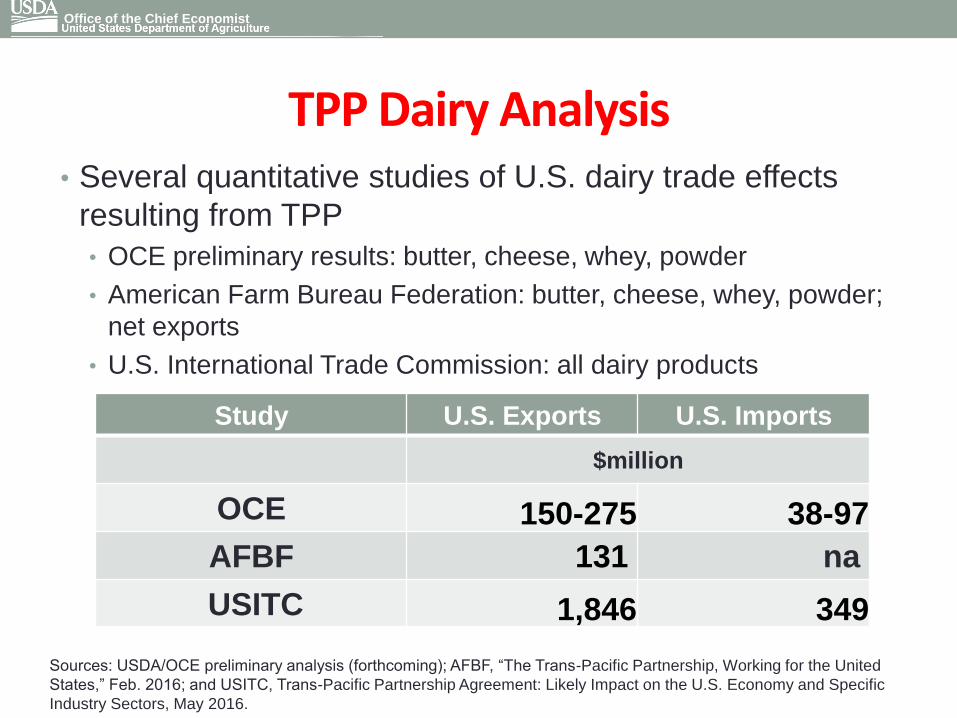

TPP Dairy Analysis• Several quantitative studies of U.S. dairy trade effects

resulting from TPP

• OCE preliminary results: butter, cheese, whey, powder

• American Farm Bureau Federation: butter, cheese, whey, powder;

net exports

• U.S. International Trade Commission: all dairy products

Office of the Chief Economist

Sources: USDA/OCE preliminary analysis (forthcoming); AFBF, “The Trans-Pacific Partnership, Working for the United

States,” Feb. 2016; and USITC, Trans-Pacific Partnership Agreement: Likely Impact on the U.S. Economy and Specific

Industry Sectors, May 2016.

Study U.S. Exports U.S. Imports

$million

OCE 150-275 38-97

AFBF 131 na

USITC 1,846 349

Other Dairy Trade Issues

• SPS/TBT Issues• China (new infant formula regulations)

• Geographical Indications (GIs)• Restrictions on the use of common food names in the EU and other

markets

• Domestic policies and regulations in other

countries that affect trade• Canada’s special milk class pricing system

Office of the Chief Economist