Embed Size (px)

Citation preview

Why Piketty Says r − g Matters for Inequality

Supplementary Lecture Notes “Income and Wealth Distribution”

Benjamin Moll

Princeton

June 1, 2014

1 / 25

These Notes

My version of a hybrid of

1 Section 5.4 of Piketty and Zucman (2014)http://gabriel-zucman.eu/files/PikettyZucman2014HID.pdf

2 Benhabib, Bisin and Zhu (2013)http://www.econ.nyu.edu/user/benhabib/lineartail31.pdf

Warning: high probability of algebra mistakes. If you find one, please email me

2 / 25

These NotesSummary:

• Standard explanation of high observed wealth concentration(e.g. top 1% own 30%): idiosyncratic capital income risk

• In theories with capital income risk, r − g is one maindeterminant of top wealth inequality

• Theory suggests slight modification: r − g − c where c is themarginal propensity to consume out of wealth for rich people

What these notes are not about:

• the aggregate capital-output ratio K/Y : different story(inequality across groups)

• see Piketty and Zucman (2014)

• and critical reviews by Ray and Krusell-Smith:http://www.econ.nyu.edu/user/debraj/Papers/Piketty.pdf

http://aida.wss.yale.edu/smith/piketty1.pdf

3 / 25

Outline

1 Simplest possible case

• Brownian capital income risk

• exogenous MPC

2 Generalizations

• endogenous savings/MPC

• labor income risk

• more general capital income processes

3 Transition dynamics

4 / 25

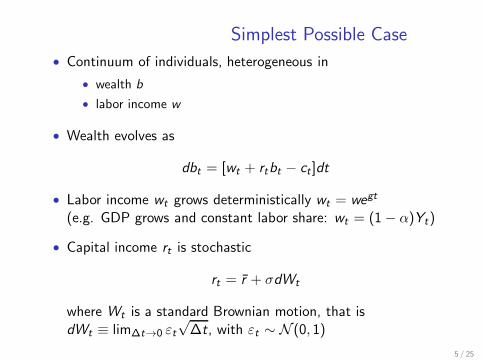

Simplest Possible Case

• Continuum of individuals, heterogeneous in

• wealth b

• labor income w

• Wealth evolves as

dbt = [wt + rtbt − ct ]dt

• Labor income wt grows deterministically wt = wegt

(e.g. GDP grows and constant labor share: wt = (1− α)Yt)

• Capital income rt is stochastic

rt = r + σdWt

where Wt is a standard Brownian motion, that isdWt ≡ lim∆t→0 εt

√∆t, with εt ∼ N (0, 1)

5 / 25

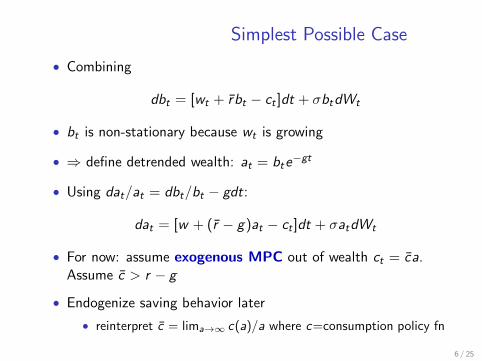

Simplest Possible Case

• Combining

dbt = [wt + r bt − ct ]dt + σbtdWt

• bt is non-stationary because wt is growing

• ⇒ define detrended wealth: at = bte−gt

• Using dat/at = dbt/bt − gdt:

dat = [w + (r − g)at − ct ]dt + σatdWt

• For now: assume exogenous MPC out of wealth ct = ca.Assume c > r − g

• Endogenize saving behavior later

• reinterpret c = lima→∞ c(a)/a where c=consumption policy fn

6 / 25

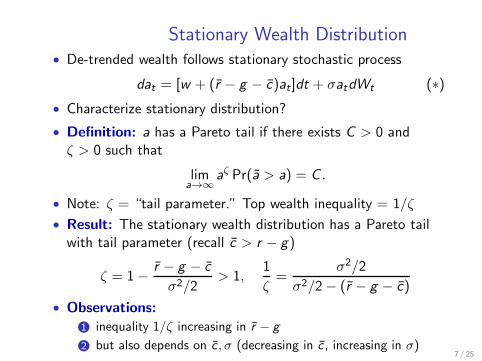

Stationary Wealth Distribution• De-trended wealth follows stationary stochastic process

dat = [w + (r − g − c)at ]dt + σatdWt (∗)• Characterize stationary distribution?

• Definition: a has a Pareto tail if there exists C > 0 andζ > 0 such that

lima→∞

aζ Pr(a > a) = C .

• Note: ζ = “tail parameter.” Top wealth inequality = 1/ζ

• Result: The stationary wealth distribution has a Pareto tailwith tail parameter (recall c > r − g)

ζ = 1− r − g − c

σ2/2> 1,

1

ζ=

σ2/2

σ2/2− (r − g − c)

• Observations:

1 inequality 1/ζ increasing in r − g

2 but also depends on c , σ (decreasing in c , increasing in σ)7 / 25

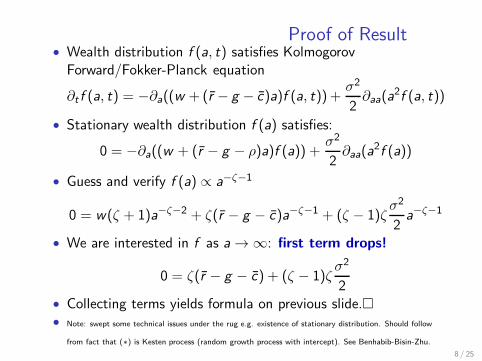

Proof of Result• Wealth distribution f (a, t) satisfies KolmogorovForward/Fokker-Planck equation

∂t f (a, t) = −∂a((w + (r − g − c)a)f (a, t)) +σ2

2∂aa(a

2f (a, t))

• Stationary wealth distribution f (a) satisfies:

0 = −∂a((w + (r − g − ρ)a)f (a)) +σ2

2∂aa(a

2f (a))

• Guess and verify f (a) ∝ a−ζ−1

0 = w(ζ + 1)a−ζ−2 + ζ(r − g − c)a−ζ−1 + (ζ − 1)ζσ2

2a−ζ−1

• We are interested in f as a → ∞: first term drops!

0 = ζ(r − g − c) + (ζ − 1)ζσ2

2• Collecting terms yields formula on previous slide.�• Note: swept some technical issues under the rug e.g. existence of stationary distribution. Should follow

from fact that (∗) is Kesten process (random growth process with intercept). See Benhabib-Bisin-Zhu.

8 / 25

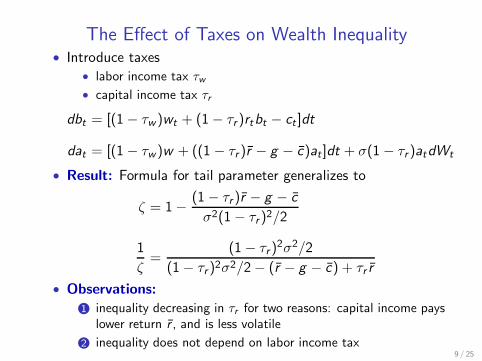

The Effect of Taxes on Wealth Inequality• Introduce taxes

• labor income tax τw• capital income tax τr

dbt = [(1− τw )wt + (1− τr )rtbt − ct ]dt

dat = [(1− τw )w + ((1 − τr )r − g − c)at ]dt + σ(1− τr )atdWt

• Result: Formula for tail parameter generalizes to

ζ = 1− (1− τr )r − g − c

σ2(1− τr )2/2

1

ζ=

(1− τr )2σ2/2

(1− τr )2σ2/2− (r − g − c) + τr r

• Observations:

1 inequality decreasing in τr for two reasons: capital income payslower return r , and is less volatile

2 inequality does not depend on labor income tax9 / 25

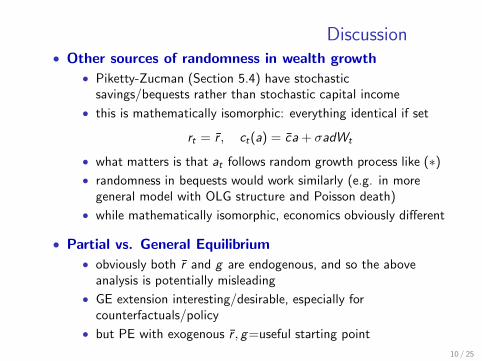

Discussion• Other sources of randomness in wealth growth

• Piketty-Zucman (Section 5.4) have stochasticsavings/bequests rather than stochastic capital income

• this is mathematically isomorphic: everything identical if set

rt = r , ct(a) = ca+ σadWt

• what matters is that at follows random growth process like (∗)• randomness in bequests would work similarly (e.g. in more

general model with OLG structure and Poisson death)

• while mathematically isomorphic, economics obviously different

• Partial vs. General Equilibrium

• obviously both r and g are endogenous, and so the aboveanalysis is potentially misleading

• GE extension interesting/desirable, especially forcounterfactuals/policy

• but PE with exogenous r , g=useful starting point

10 / 25

Generalizations

1 Optimally chosen savings

2 stochastic labor income wt

3 more general process for capital income rt

11 / 25

Optimal Savings + Stochastic wt

• Individuals solve

V (b, w) = max{ct}

E0

∫ ∞

0e−ρtu(ct)dt s.t.

dbt = [wt + rtbt − ct ]dt

dwt = (g + µw (wt))dt + σw (wt)dWt

rt = r + σdWt

bt ≥ 0, (b0, w0) = (b, w )

• Assume CRRA utility

u(c) =c1−γ

1− γ, γ > 0

12 / 25

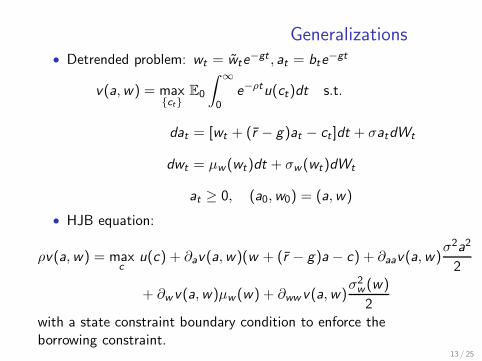

Generalizations• Detrended problem: wt = wte

−gt , at = bte−gt

v(a,w) = max{ct}

E0

∫ ∞

0e−ρtu(ct)dt s.t.

dat = [wt + (r − g)at − ct ]dt + σatdWt

dwt = µw (wt)dt + σw (wt)dWt

at ≥ 0, (a0,w0) = (a,w)

• HJB equation:

ρv(a,w) = maxc

u(c) + ∂av(a,w)(w + (r − g)a − c) + ∂aav(a,w)σ2a2

2

+ ∂wv(a,w)µw (w) + ∂wwv(a,w)σ2w (w)

2with a state constraint boundary condition to enforce theborrowing constraint.

13 / 25

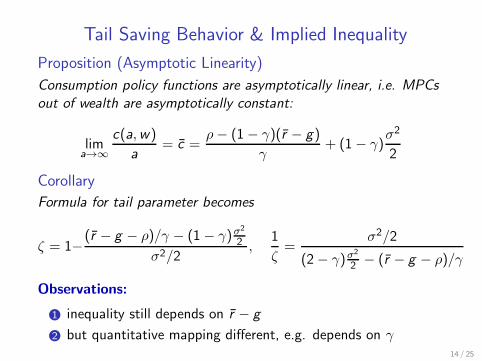

Tail Saving Behavior & Implied Inequality

Proposition (Asymptotic Linearity)

Consumption policy functions are asymptotically linear, i.e. MPCs

out of wealth are asymptotically constant:

lima→∞

c(a,w)

a= c =

ρ− (1− γ)(r − g)

γ+ (1− γ)

σ2

2

Corollary

Formula for tail parameter becomes

ζ = 1−(r − g − ρ)/γ − (1− γ)σ2

2

σ2/2,

1

ζ=

σ2/2

(2− γ)σ2

2 − (r − g − ρ)/γ

Observations:

1 inequality still depends on r − g

2 but quantitative mapping different, e.g. depends on γ14 / 25

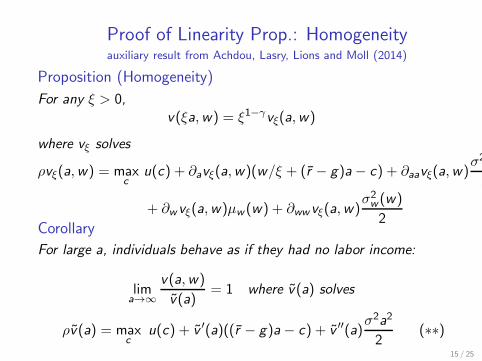

Proof of Linearity Prop.: Homogeneityauxiliary result from Achdou, Lasry, Lions and Moll (2014)

Proposition (Homogeneity)

For any ξ > 0,v(ξa,w) = ξ1−γvξ(a,w)

where vξ solves

ρvξ(a,w) = maxc

u(c) + ∂avξ(a,w)(w/ξ + (r − g)a − c) + ∂aavξ(a,w)σ2

2

+ ∂wvξ(a,w)µw (w) + ∂wwvξ(a,w)σ2w (w)

2Corollary

For large a, individuals behave as if they had no labor income:

lima→∞

v(a,w)

v(a)= 1 where v(a) solves

ρv(a) = maxc

u(c) + v ′(a)((r − g)a − c) + v ′′(a)σ2a2

2(∗∗)

15 / 25

Proof of Linearity Proposition• Next step: find explicit solution for policy function of (∗∗)

ρv(a) =H(v ′(a)) + v ′(a)(r − g)a + v ′′(a)σ2a2

2

H(p) = maxc

u(c)− pc =γ

1− γp

γ−1γ

• Guess and verify v(a) = Ba1−γ , v ′(a) = (1− γ)Ba−γ ,

v ′′(a) = −γ(1−γ)Ba−γ−1, H(v ′(a)) =γ

1− γ((1−γ)B)

γ−1γ a1−γ

ρ = γ((1 − γ)B)−1γ + (1− γ)(r − g)− γ(1− γ)

σ2

2

• from FOC, c(a) = ca, c = ((1 − γ)B)−1/γ and hence

c =ρ− (1− γ)(r − g)

γ+ (1− γ)

σ2

2

• Asymptotic Linearity Proposition follows directly fromHomogeneity Proposition and above.�

16 / 25

Further Generalization: General r Process

• Individuals solve

V (b, w , r) = max{ct}

E0

∫ ∞

0e−ρtu(ct)dt s.t.

dbt = [wt + rtbt − ct ]dt

dwt = (g + µw (wt))dt + σw (wt)dWt

drt = µr (rt))dt + σr (rt)dBt

(b0, w0, r0) = (b, w , r)

• Assume CRRA utility

u(c) =c1−γ

1− γ, γ > 0

17 / 25

Further Generalization: General r Process

• Detrended problem: wt = wte−gt , at = bte

−gt

v(a,w , r) = max{ct}

E0

∫ ∞

0e−ρtu(ct)dt s.t.

dat = [wt + (rt − g)at − ct ]dt

dwt = µw (wt)dt + σw (wt)dWt

drt = µr (rt)dt + σr (rt)dBt

(a0,w0, r0) = (a,w , r)

18 / 25

Tail Saving BehaviorFollowing similar steps as above, one can show:

Corollary

Consumption policy functions are asymptotically linear, i.e. MPCs

out of wealth are asymptotically constant:

lima→∞

c(a,w , r)

a= c(r)

The task is therefore to characterize the stationary distributionf (a,w , r) of the following Kesten-type process:

dat = [wt + (rt − g − c(rt))at ]dt

dwt = µw (wt)dt + σw (wt)dWt

drt = µr (rt)dt + σr (rt)dBt

19 / 25

Stationary Wealth Distribution• Here’s how to do it, based on Gabaix (2010) “On RandomGrowth Processes with Autocorrelated Shocks”

Proposition (Gabaix)

Assume w and r are stationary processes. Then the process for a

has a stationary distribution with a Pareto tail

f (a,w , r) ∼ φ(w , r)a−ζ−1 where the tail parameter ζ satisfies an

eigenvalue problem

0 = ζ(r − g − c(r))e(w , r) + µw (w)∂w e(w , r)] +1

2σ2w (w)∂wwe(w , r)

+ µr (r)∂re(w , r) +1

2σ2r (r)∂rre(w , r) (E)

for some eigenfunction e ≥ 0.

• Need to solve (E) numerically• But can handle very general class of r -processes

20 / 25

Proof• Stationary distribution satisfies

0 =− ∂a[(w + (r − g − c(r))a)f (a,w , r)]

− ∂w [µw (w)f (a,w , r)] +1

2∂ww [σ

2w (w)f (a,w , r)]

− ∂r [µr (r)f (a,w , r)] +1

2∂rr [σ

2r (r)f (a,w , r)]

• Guess f (a,w , r) = φ(w , r)a−ζ−1 and substitute in.

• Divide by a−ζ−1 and use that we’re interested in the tail asa → ∞ and hence w/a drops:

0 =ζ(r − g − c(r))φ(w , r)

− ∂y [µw (w)φ(w , r)] +1

2∂ww [σ

2w (w)φ(w , r)]

− ∂r [µr (r)φ(w , r)] +1

2∂rr [σ

2r (r)φ(w , r)]

• Using KF equation for (w , r), obtain (E).�21 / 25

Transition Dynamics

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1810 1830 1850 1870 1890 1910 1930 1950 1970 1990 2010

Sh

are

of to

p d

ecile

or

pe

rce

ntile

in

to

tal w

ea

lth

!"#$%&'(%)*+%,-&'%.("&/012%3(4$&'%*"(5/4$*&1%346%'*7'(0%*"%8/09:(%&'4"%*"%&'(%!"*&(+%;&4&(6<%

Sources and series: see piketty.pse.ens.fr/capital21c.

Figure 10.6. Wealth inequality: Europe and the U.S., 1810-2010

Top 10% wealth share: Europe

Top 10% wealth share: U.S.

Top 1% wealth share: Europe

Top 1% wealth share: U.S.

22 / 25

Transition Dynamics• So far: only focussed on stationary distributions

• But Piketty’s whole point: world is not stationary (seeFigure on previous slide)

• wants to argue: that’s because rt − gt varies over time

• Most interesting questions require extension to transitiondynamics

• simplest case: characterize f (a, t) satisfying

∂t f (a, t) = −∂a((w +(rt −gt − ct)a)f (a, t))+σ2

2∂aa(a

2f (a, t))

• probably need to go numerical

• Economics should be similar to comparing steady states• inequality depends on rt − gt − ct :

• how much does ct vary over time relative to rt − gt?

• Open question: how fast (or slow) are transitions?• e.g. if rt − gt − ct ↑, how long until inequality ↑?

23 / 25

Richer Models

• Why would capital income be stochastic?

• One answer: entrepreneurship

• Quadrini (1999, 2000)

• Cagetti and DeNardi (2006)

24 / 25

Summary

• Standard explanation of high observed wealth concentration(e.g. top 1% own 30%): idiosyncratic capital income risk

• In theories with capital income risk, r − g is one maindeterminant of top wealth inequality

• does not rely on weird assumptions about saving behavior(instead optimization w/ CRRA utility)

• but theory suggests slight modification: r − g − c

• other factors also potentially important, e.g. σ

• Changes in inequality over time? Open questions:

• speed of transitions?

• relative (quantitative) importance of different factors

• e.g. how much does ct vary over time relative to rt − gt?

25 / 25

![European Journal of Sociology ......6.6 trillion euro value of German real estate in 2008 [Voigtl€ander et al. 2008: i-iv] and 39 percent of private net wealth [Piketty and Zucman](https://img.pdfslide.us/doc/110x75/5f86703189d2e974827225e6/european-journal-of-sociology-66-trillion-euro-value-of-german-real-estate.jpg)