Embed Size (px)

Citation preview

Who owns the value in the agriculture value-chain?

Lindie StroebelGeneral Manager: PMA Southern Africa

July 23, 2018

Read more on PMA

PMA: A global network of note

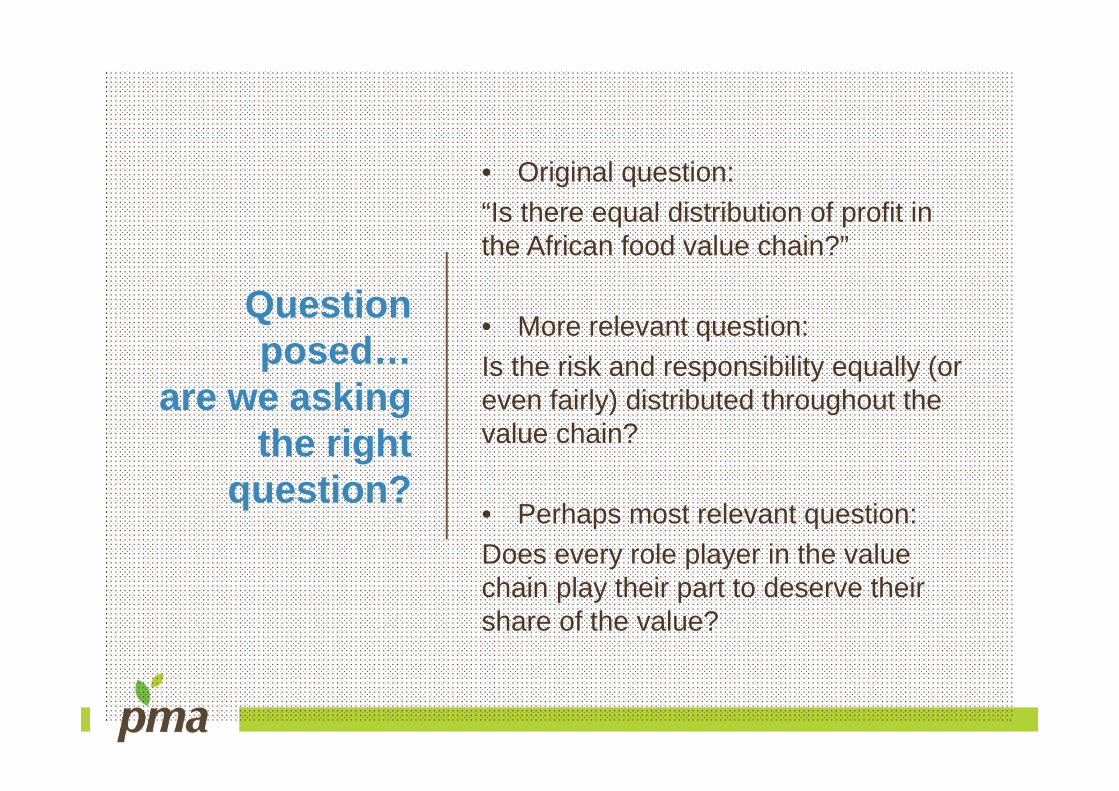

Question posed…

are we asking the right

question?

• Original question: “Is there equal distribution of profit in the African food value chain?”

• More relevant question: Is the risk and responsibility equally (or even fairly) distributed throughout the value chain?

• Perhaps most relevant question:Does every role player in the value chain play their part to deserve their share of the value?

Let me introduce you to Madam Customer

…the blue berries storyBeyond chocolate pudding and gin

Few facts from Euromonitor’sGrocery Retailers in South Africa report

Grocery retailers records current value growth of 9% in 2016 to generate sales of ZAR491.6 billion

Grocery retailers continue to diversify their portfolios in order to remain competitive

Shoprite Holdings Ltd maintains a leading position within grocery retailing with a 22% value share in 2016

Grocery retailers is set to register a 3% value CAGR at constant 2016 prices over the forecast period

Supermarkets accounting for 40% of fresh food sales in SA

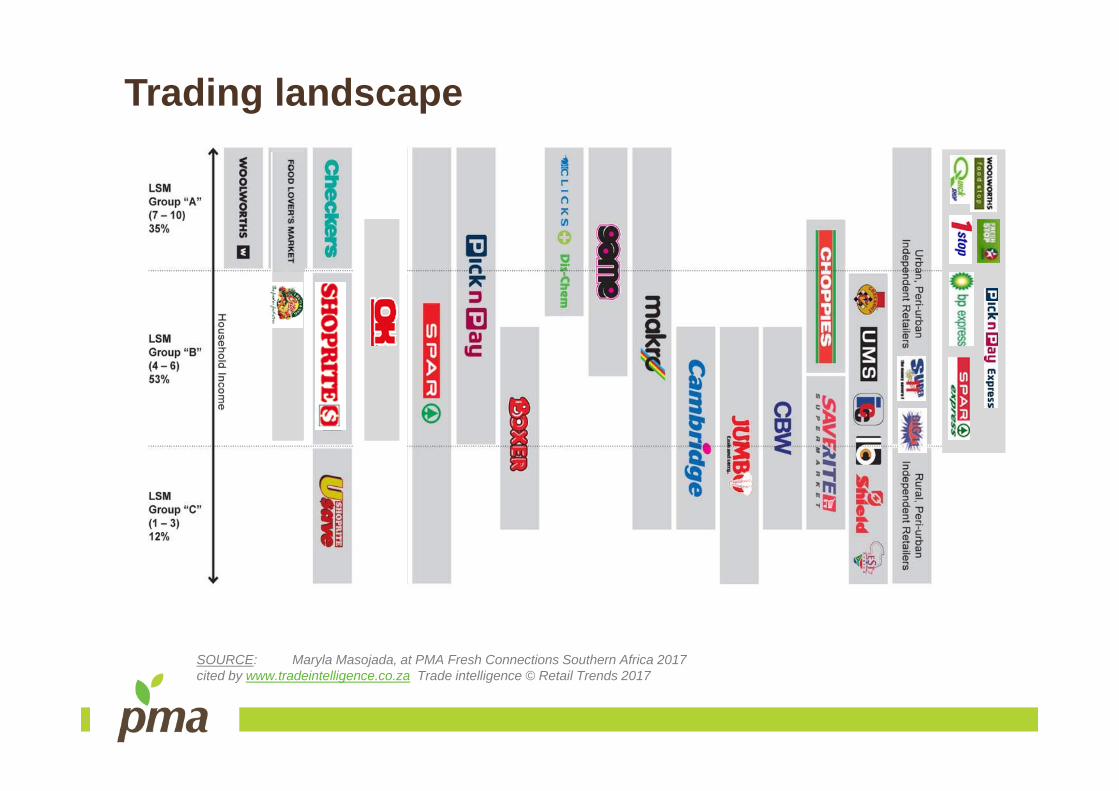

Trading landscape

SOURCE: Maryla Masojada, at PMA Fresh Connections Southern Africa 2017cited by www.tradeintelligence.co.za Trade intelligence © Retail Trends 2017

Trading landscape

Important category to cater for!

SOURCE: Maryla Masojada, at PMA Fresh Connections Southern Africa 2017cited by www.tradeintelligence.co.za Trade intelligence © Retail Trends 2017

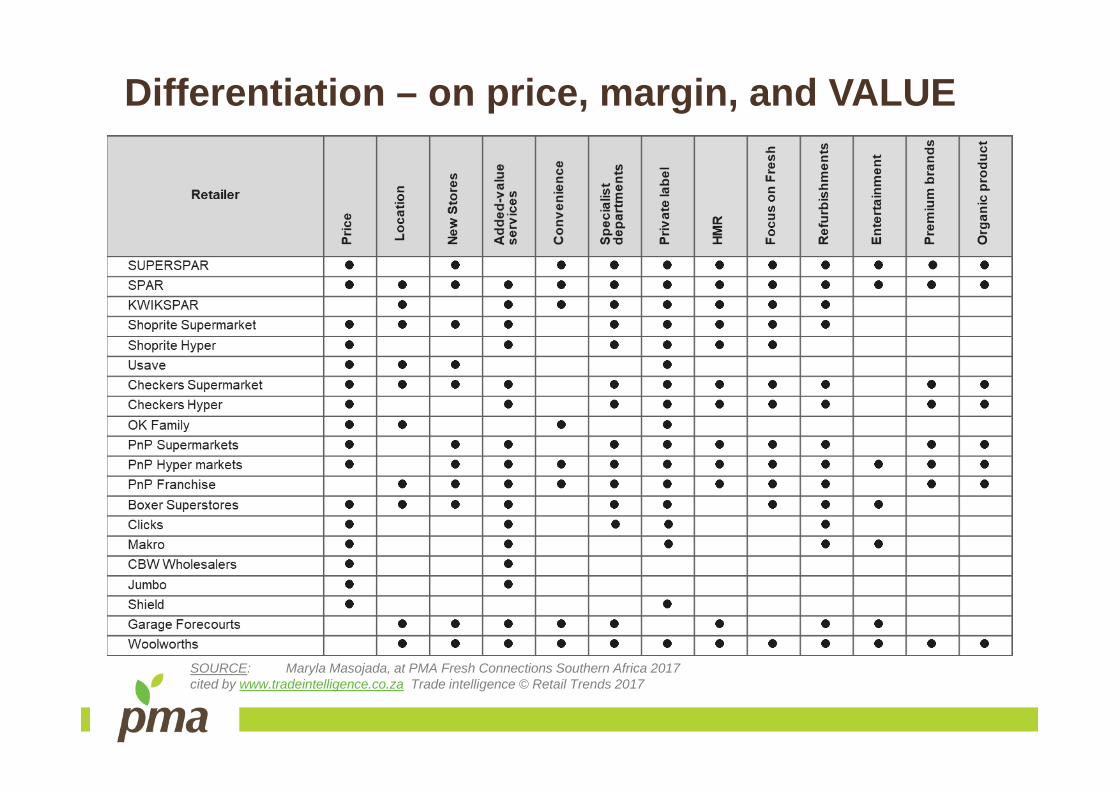

Differentiation – on price, margin, and VALUE

SOURCE: Maryla Masojada, at PMA Fresh Connections Southern Africa 2017cited by www.tradeintelligence.co.za Trade intelligence © Retail Trends 2017

Different market channels to choose from1. Export2. Local & Regional retail3. Commission markets4. Cross-border trade5. Informal markets

Different markets channels reach different consumersDifferent quality expectationDifferent pricing structuresSolution to Food WasteGive producers more options, therefore more negotiation power

Access at: https://www.pma.com/Content/Articles/2018/06/South-African-Markets

Who is really calling the shots?

Claiming your piece of the value

Requirements for better negotiation position

Suppliers who understand individual retailers’ business model and have breadth of capability to deal with these are likely to secure a strong competitive advantage

- Maryla Masojada, Trade Intellgience

- Continuity of Supply - Quality according to spec- Food safety not even a debate- Price always an issue

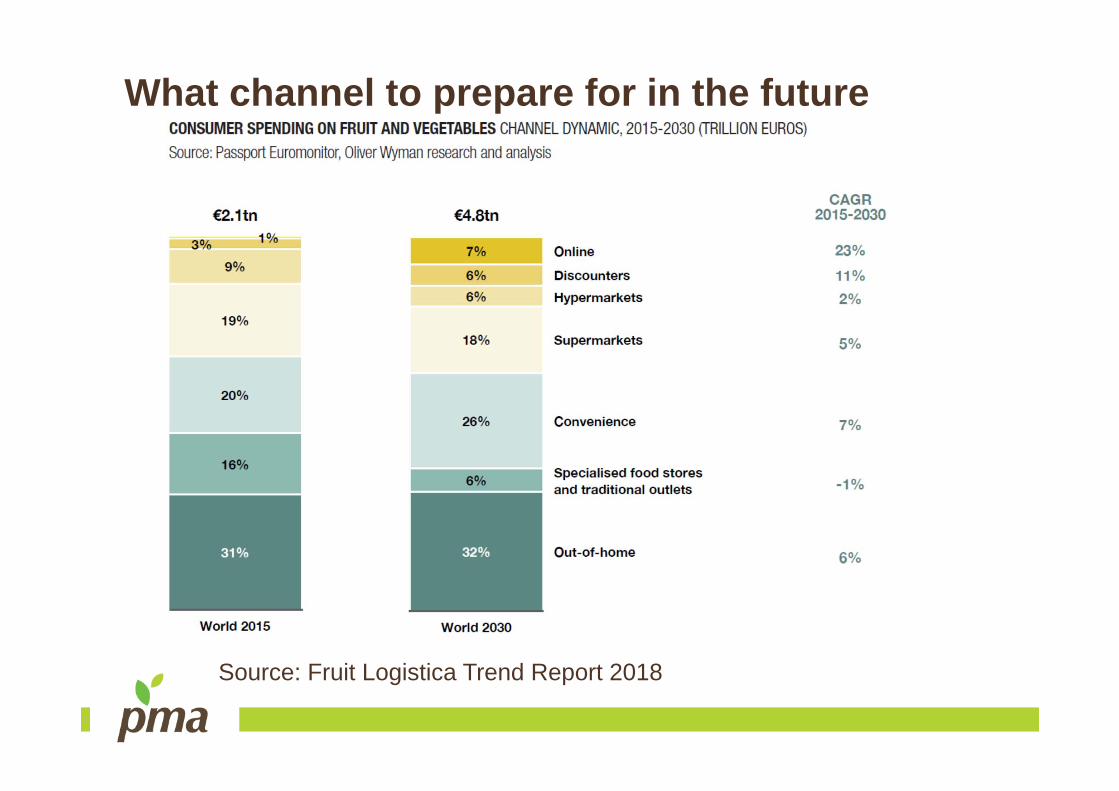

What channel to prepare for in the future

Source: Fruit Logistica Trend Report 2018

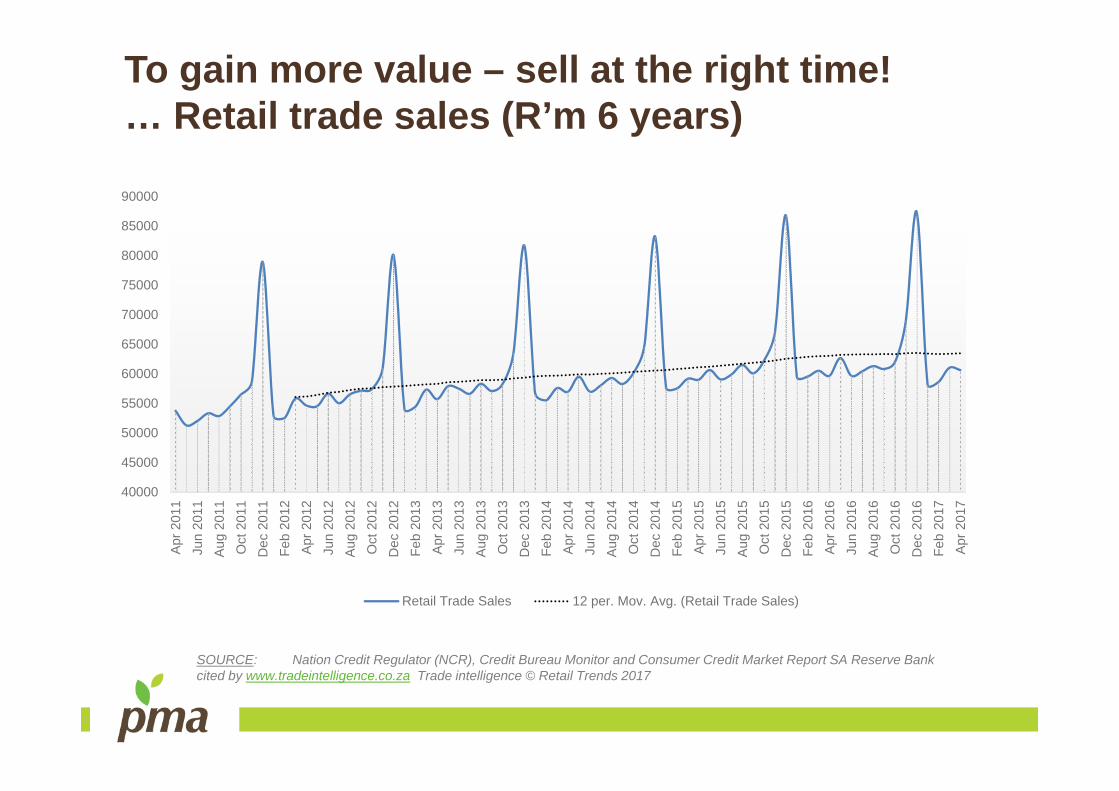

To gain more value – sell at the right time!… Retail trade sales (R’m 6 years)

40000

45000

50000

55000

60000

65000

70000

75000

80000

85000

90000

Apr

201

1

Jun

2011

Aug

201

1

Oct

201

1

Dec

201

1

Feb

201

2

Apr

201

2

Jun

2012

Aug

201

2

Oct

201

2

Dec

201

2

Feb

201

3

Apr

201

3

Jun

2013

Aug

201

3

Oct

201

3

Dec

201

3

Feb

201

4

Apr

201

4

Jun

2014

Aug

201

4

Oct

201

4

Dec

201

4

Feb

201

5

Apr

201

5

Jun

2015

Aug

201

5

Oct

201

5

Dec

201

5

Feb

201

6

Apr

201

6

Jun

2016

Aug

201

6

Oct

201

6

Dec

201

6

Feb

201

7

Apr

201

7

Retail Trade Sales 12 per. Mov. Avg. (Retail Trade Sales)

SOURCE: Nation Credit Regulator (NCR), Credit Bureau Monitor and Consumer Credit Market Report SA Reserve Bank cited by www.tradeintelligence.co.za Trade intelligence © Retail Trends 2017

Requirements to “claim” share of value in future

Source: Fruit Logistica Trend Report 2018

Learn more about retail? Hear it first hand:• Former CEO of Shoprite, Whitey Basson on future of retail in Africa• Panel session with Freshmark (Shoprite), Pick n Pay, SPAR and Food

Lovers Market on Importance of fresh in the future of retail• Panel of Chinese retailers – JD Fresh (JD.com), WinChain

(Yiguo/Alibaba), Frutacloud, Kingo Fruit• Marketing in a digital world• Digital Transformation (and Blockchain)• Local business strategies and market trends

15-16 August 2018CSIR, Pretoria

www.pma.com/FCSouthernAfrica