Embed Size (px)

Citation preview

Who moved my benefits?

The Future of Employment-based Benefit Programs

What we know

Over the past 12

years employment

based overage has

dropped 10

percentage points

68%

1999

58%

2011

Data: US Census Bureau

What we know

In the 30 years from

1980 thru 2010 there

was a 10x increase

in employer group

medical costs

$2600B

2010

$256B

1980

Data: US Dept. HHS

What we know

In the 7 years from

2005 thru 2012 there

was an increase of

$3,500 in employer

group medical costs

per employee

$10K

2012

$7K

2005

Data: Mercer

Factors causing cost inflation

• Availability and growth of expensive medical procedures

• Availability and growth of expensive prescription drugs

• Employee longevity in active workforce

• Self-funded plans have seen continued unpredictability in catastrophic claims

Financial incentives

• Employees have responded to incentives to take

better care of themselves

• 2012 saw the smallest increase in group medical

coverage in 15 years

• An average increase of 4.1%

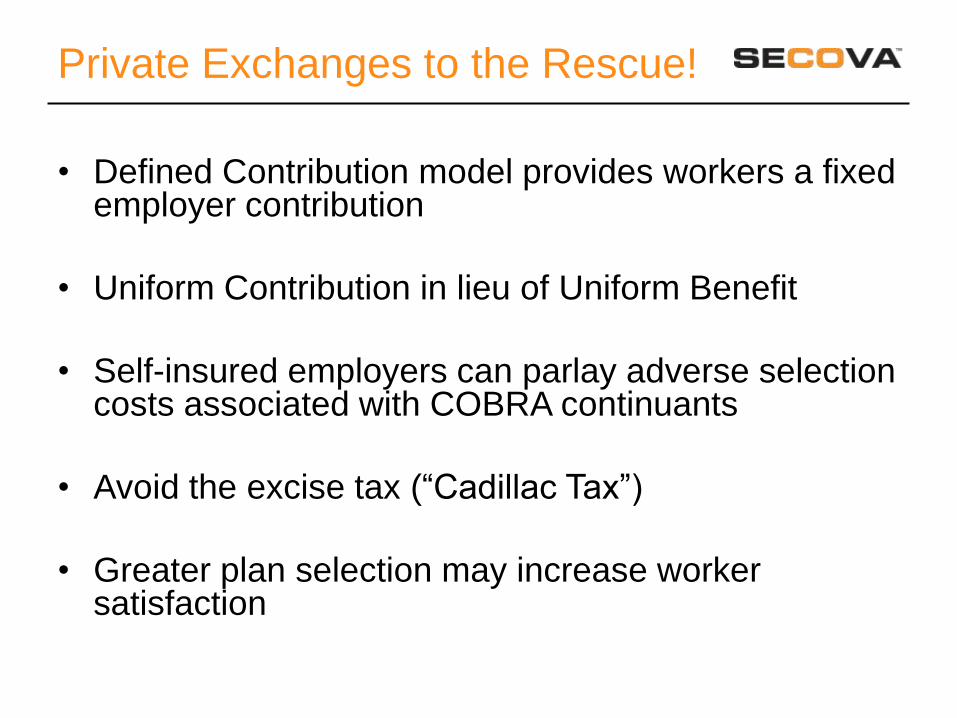

Private Exchanges to the Rescue!

• Defined Contribution model provides workers a fixed employer contribution

• Uniform Contribution in lieu of Uniform Benefit

• Self-insured employers can parlay adverse selection costs associated with COBRA continuants

• Avoid the excise tax (“Cadillac Tax”)

• Greater plan selection may increase worker satisfaction

Have we been here before?

• Managed competition first described in the late 70s by Alain Enthoven

• Defined Contribution health plans were broadly discussed over a decade ago – “DC Health”

• Over 62% of health-care leaders predicted DC Health would takeover employment-based coverage in 1998

• Interest waned – confusion, tax-free benefits, worker retention

Employee Perspective

Traditional Offering

• Continuity in health plans offered and access to providers

• Reduced perceived value of benefit offering given increased OOP costs

• Singular and consistent experience with enrolling in all benefit types

Private Exchange

• Possibly different carrier and plan mix than what was previously offered

• Reduced perceived value of benefit offering given increased OOP costs

• Mixed enrollment experience with medical plans enrolled on exchange platform while other plans may require use of another platform

Employer Perspective

Traditional Offering

• ERISA-based plan offering retains certain tax benefits

• Reduced perceived value of benefit offering given increased OOP costs

• Singular and consistent experience with enrolling in all benefit types

Private Exchange

• Defined Contribution based offering may adversely impact tax exposure

• Reduced perceived value of benefit offering given increased OOP costs

• Mixed enrollment experience with medical plans enrolled on exchange platform while other plans may require use of another platform

Employers will still…

• Need to decide whether they want to have

involvement in plan selection

• Determine adverse selection implications (risk

adj, exchange open to all employers, min

underwriting provisions)

Employers will still…

• Need to answer whether their contributions will

float with inflation

• Need to provide tools to help works avoid plan

choice overload

• Consider varying contributions by geographic

location

Other Considerations

• Workers depend on employer plan selection

because they lack confidence (7/10)

• Employers may be better positioned to deploy

group purchasing efficiencies

• Insurers respond to the collective voice and

check book of an employer

Sources

• Alain Enthoven, New England Journal of Medicine, March 1978a

• 1998 CIGNA/BenefitAccess National Survey

• Paul Fronstin, EBRI, Private Health Insurance Exchanges and Defined

Contribution Health Plans

• Peter Orzag, Bloomberg, Defined Contributions Define Health-Care Future,

December 2011

• PriceWaterhouseCoopers, HealthCast, 1999

• US Census Bureau,

http://www.census.gov/hhes/www/hlthins/data/historical/HIB_tables.html