Embed Size (px)

Citation preview

University of Dundee Service Desk Discussion DocumentPage 1 GM/University of Dundee/SD Discussion Doc v.0.1 02 December 2014

White Paper

IT Service Management Tooling Author: Eddie Potts, Principal IT Service Management Consultant

IT Service Management Tooling – White Paper Page 1

IT Service Management Tools

Market Background ITSM tools can be classified based upon their IT Service Management capabilities and also their integration with IT operations management (ITOM) solutions. In 2014 the estimated value of the proprietary ITSM Tool Market was $1.8 billion and (Granetto, 2015) served by over 400 vendors (ITSM_Portal, 2015). In addition to vendor offerings it is recognised that there are over 85 open source (ITSM_Portal, 2015) and freeware solutions which analysts increasingly recognise as viable options for organisations (Blum, 2015).

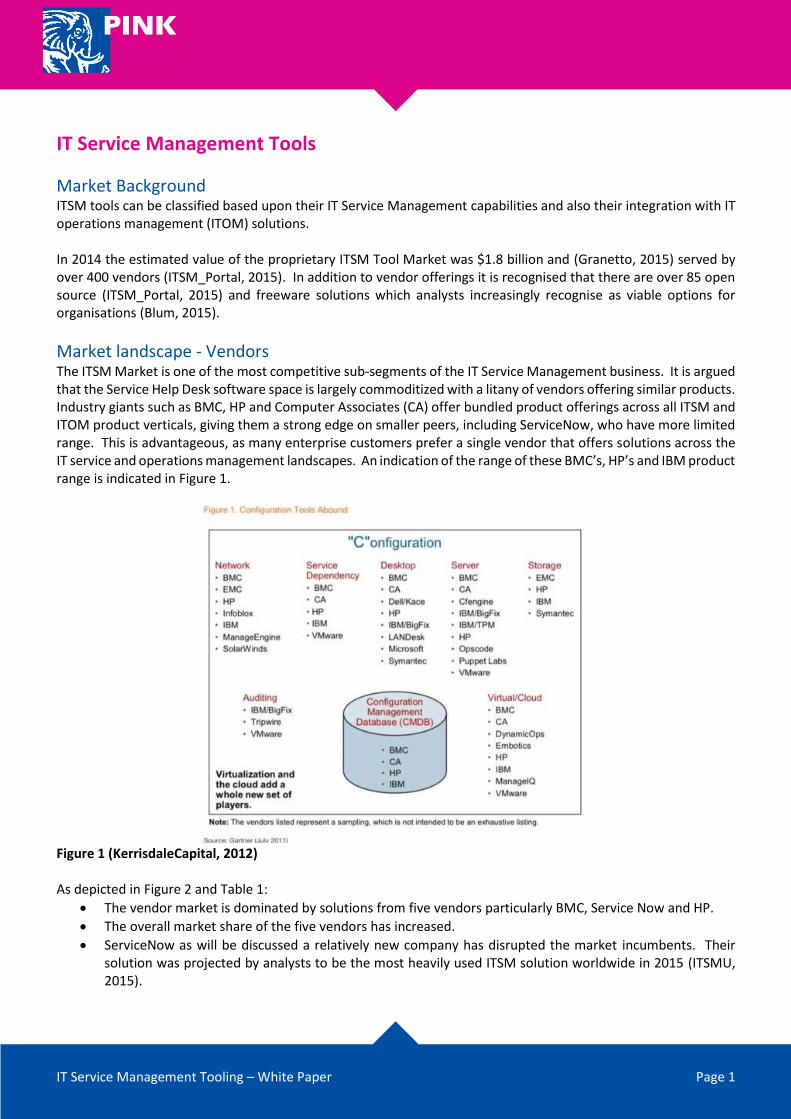

Market landscape - Vendors The ITSM Market is one of the most competitive sub-segments of the IT Service Management business. It is argued that the Service Help Desk software space is largely commoditized with a litany of vendors offering similar products. Industry giants such as BMC, HP and Computer Associates (CA) offer bundled product offerings across all ITSM and ITOM product verticals, giving them a strong edge on smaller peers, including ServiceNow, who have more limited range. This is advantageous, as many enterprise customers prefer a single vendor that offers solutions across the IT service and operations management landscapes. An indication of the range of these BMC’s, HP’s and IBM product range is indicated in Figure 1.

Figure 1 (KerrisdaleCapital, 2012) As depicted in Figure 2 and Table 1:

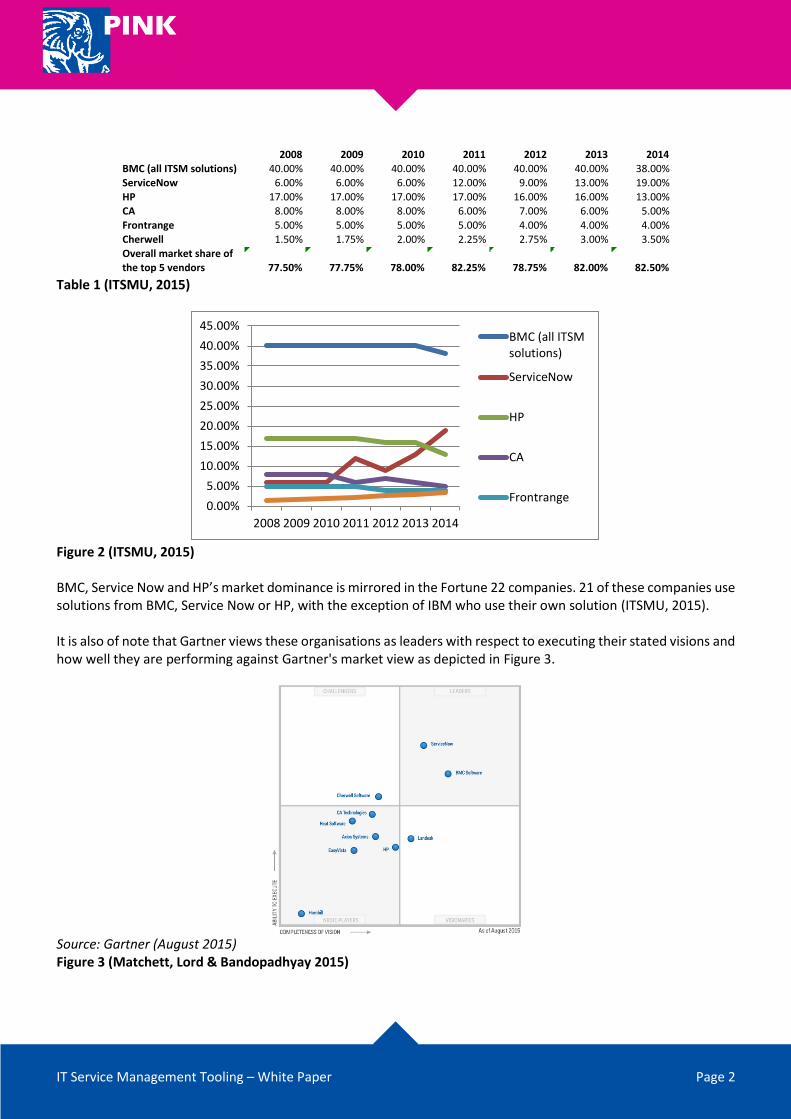

The vendor market is dominated by solutions from five vendors particularly BMC, Service Now and HP.

The overall market share of the five vendors has increased.

ServiceNow as will be discussed a relatively new company has disrupted the market incumbents. Their solution was projected by analysts to be the most heavily used ITSM solution worldwide in 2015 (ITSMU, 2015).

IT Service Management Tooling – White Paper Page 2

Table 1 (ITSMU, 2015)

Figure 2 (ITSMU, 2015) BMC, Service Now and HP’s market dominance is mirrored in the Fortune 22 companies. 21 of these companies use solutions from BMC, Service Now or HP, with the exception of IBM who use their own solution (ITSMU, 2015). It is also of note that Gartner views these organisations as leaders with respect to executing their stated visions and how well they are performing against Gartner's market view as depicted in Figure 3.

Source: Gartner (August 2015) Figure 3 (Matchett, Lord & Bandopadhyay 2015)

2008 2009 2010 2011 2012 2013 2014BMC(allITSMsolutions) 40.00% 40.00% 40.00% 40.00% 40.00% 40.00% 38.00%

ServiceNow 6.00% 6.00% 6.00% 12.00% 9.00% 13.00% 19.00%

HP 17.00% 17.00% 17.00% 17.00% 16.00% 16.00% 13.00%CA 8.00% 8.00% 8.00% 6.00% 7.00% 6.00% 5.00%

Frontrange 5.00% 5.00% 5.00% 5.00% 4.00% 4.00% 4.00%

Cherwell 1.50% 1.75% 2.00% 2.25% 2.75% 3.00% 3.50%

Overallmarketshareofthetop5vendors 77.50% 77.75% 78.00% 82.25% 78.75% 82.00% 82.50%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

2008 2009 2010 2011 2012 2013 2014

BMC (all ITSMsolutions)

ServiceNow

HP

CA

Frontrange

IT Service Management Tooling – White Paper Page 3

Gartner (Jarod et al., 2014) argues that organisations typically replace their ITSM tools every 5 years, although other sources suggest that this may be as low as every three years. Gartner argues that this is because organisations suffer a lack of ITSM improvement road maps, which baseline the current state and outline the people, processes and technology resources required to reach the desired state. Without a road map organisations often purchase tools that have more capabilities and functionality than the organisation is prepared to utilise (thus incurring higher costs) or lack the capabilities or integration abilities needed as the organisation matures its processes. Pink Elephant’s experience strongly supports this assertion together with the related observation that all too often solutions are selected and implemented without sufficient heed to the disparate stakeholders needs within an organisation. There are notable examples of perfectly good Service Management solutions having been poorly implemented and having to be replaced with alternative solutions as stakeholders irreversibly lost faith with the initial solution. Tool vendors are keenly aware of this shortcoming, and are competing aggressively not only to win new business, but also to develop or partner for broader ITSM capabilities and integrations with other ITM functions such as ITSM consultancy. To exemplify Gartner’s observation, in 2012 10% of ServiceNow’s revenue was gained from the provision of such services (KerrisdaleCapital, 2012). Gartner suggests ITSM tools can be classified as basic, intermediate and advanced:

Basic solutions that provide limited ITSM capabilities and limited integration with ITOM solutions.

Intermediate solutions that offer good ITSM capabilities and more range to provide broader ITOM capabilities to integrate with third-party ITOM solutions.

Advanced solutions that offer a full range of ITSM capabilities, and provide broader ITOM functionality or integrate with advanced third-party solutions.

Pink Elephant’s own experience is:

Organisations often procure toolsets that offer more far capability than that is being exploited.

Organisations often possess a “zoo of ITSM products across the organisation”, which are often not integrated and sourced by different vendors.

A key-contributing factor to this is the absence of a coherent ITSM strategy to support the procurement and integration of an optimal solution. In addition to supporting traditional ITSM processes, an increasing trend amongst ITSM vendors is to offer a “Platform as a Service” solutions that support business process such as “joiners, movers and leavers process”. This infers that vendor and tool selections will be increasingly determined by broader business strategy as opposed to just that of IT Service Management. It should also be noted that a prerequisite for Gartner to comprehensively assess a tool is that it should be capable of supporting >5 Service Management processes - which suggests such tools would generally be intermediate or advanced solutions. Whilst Gartner has not comprehensively reviewed solutions that support <5 Service Management processes, they recognise and suggest various solutions that are likely to be appropriate for those organisations operating at a low level of maturity.

Market Landscape - Open Source Solutions In theory, the benefits of using Open Source solutions include:

Significant financial savings.

IT Service Management Tooling – White Paper Page 4

There is no vendor lock-in. For example organisations can easily export data if they decide to migrate to another solution.

Risk reduction in the event of the vendor going out of business or discontinues the product. Conversely there are recognised disadvantages of using Open Source solutions including:

Analysts perceive that few Open Source solutions are considered enterprise grade.

Open Source projects can get discontinued. Even though source code is available for anyone to see, the question is if anyone is ready to pick on a project and continue with development. There are many products in open source world that showed potential, were ahead of similar projects, yet authors decided to abandon the project.

Organisations also need to consider that even though the product may be free, you could easily have additional cost when using it.

It should also be noted that the solutions reviewed by Gartner tend to be those offered by vendors as opposed to being open sourced. Similarly the solutions validated by PinkVERIFY, are generally those nominated by vendors (Pink_Elephant, 2015) although there are exceptions to this rule such as OTRS:ITSM and CITSMART. Clearly this does not mean that quality open source solutions do not exist, only that they are less likely to benchmarked or reviewed by the better-known bodies and schemes such as Gartner, Forrester or PinkVERIFY. However, reviews for such solutions are conducted by respected industry analysts such as ITSMDaily.com (Blum, 2015) and Tech Republic (TechRepublic, 2011). Such tools include, but are not limited to:

Combodo ITOP

OTRS:ITSM

CITSMART

Project Open

OCS Inventory NG

I-doit Note that such reviews do not tend to be benchmarked and therefore more open to subjectivity than those conducted by the likes of Gartner, Forrester and PinkVERIFY.

Product Delivery - Software as a Service Although the outcome is not known to date, in 2012 Gartner's research predicted that 50% of IT organisations would move to Software as a Service (SaaS) solutions by 2015 (KerrisdaleCapital, 2012). The advantages of SaaS include:

Automated software updates.

Remote access through the cloud.

Off-premise database redundancies.

Subscription-based pricing model: Firms pay a subscription fee per month (or year) per user that covers everything needed to operate, including support and maintenance. This model eliminates the capital investment required for on-premise hardware and software licenses.

Forrester surveyed 1,471 North American and European software decision-makers of whom >70% indicated that speed of implementation and deployment was one of the key benefits that drove their SaaS choice. SaaS solutions leave the deployment, maintenance, and ongoing management to the supplier. In the IT Service Management (ITSM) world, this frees up teams to focus on the service automation and service delivery methods that deliver value for their customers.

IT Service Management Tooling – White Paper Page 5

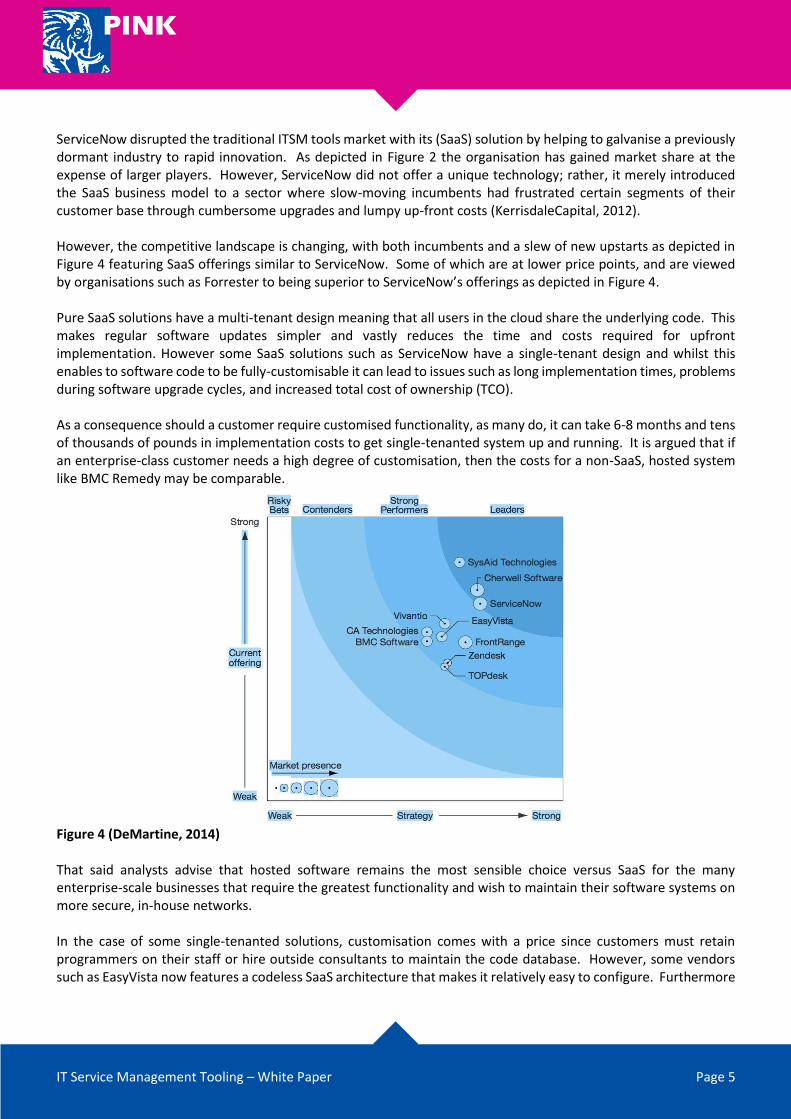

ServiceNow disrupted the traditional ITSM tools market with its (SaaS) solution by helping to galvanise a previously dormant industry to rapid innovation. As depicted in Figure 2 the organisation has gained market share at the expense of larger players. However, ServiceNow did not offer a unique technology; rather, it merely introduced the SaaS business model to a sector where slow-moving incumbents had frustrated certain segments of their customer base through cumbersome upgrades and lumpy up-front costs (KerrisdaleCapital, 2012). However, the competitive landscape is changing, with both incumbents and a slew of new upstarts as depicted in Figure 4 featuring SaaS offerings similar to ServiceNow. Some of which are at lower price points, and are viewed by organisations such as Forrester to being superior to ServiceNow’s offerings as depicted in Figure 4. Pure SaaS solutions have a multi-tenant design meaning that all users in the cloud share the underlying code. This makes regular software updates simpler and vastly reduces the time and costs required for upfront implementation. However some SaaS solutions such as ServiceNow have a single-tenant design and whilst this enables to software code to be fully-customisable it can lead to issues such as long implementation times, problems during software upgrade cycles, and increased total cost of ownership (TCO). As a consequence should a customer require customised functionality, as many do, it can take 6-8 months and tens of thousands of pounds in implementation costs to get single-tenanted system up and running. It is argued that if an enterprise-class customer needs a high degree of customisation, then the costs for a non-SaaS, hosted system like BMC Remedy may be comparable.

Figure 4 (DeMartine, 2014) That said analysts advise that hosted software remains the most sensible choice versus SaaS for the many enterprise-scale businesses that require the greatest functionality and wish to maintain their software systems on more secure, in-house networks. In the case of some single-tenanted solutions, customisation comes with a price since customers must retain programmers on their staff or hire outside consultants to maintain the code database. However, some vendors such as EasyVista now features a codeless SaaS architecture that makes it relatively easy to configure. Furthermore

IT Service Management Tooling – White Paper Page 6

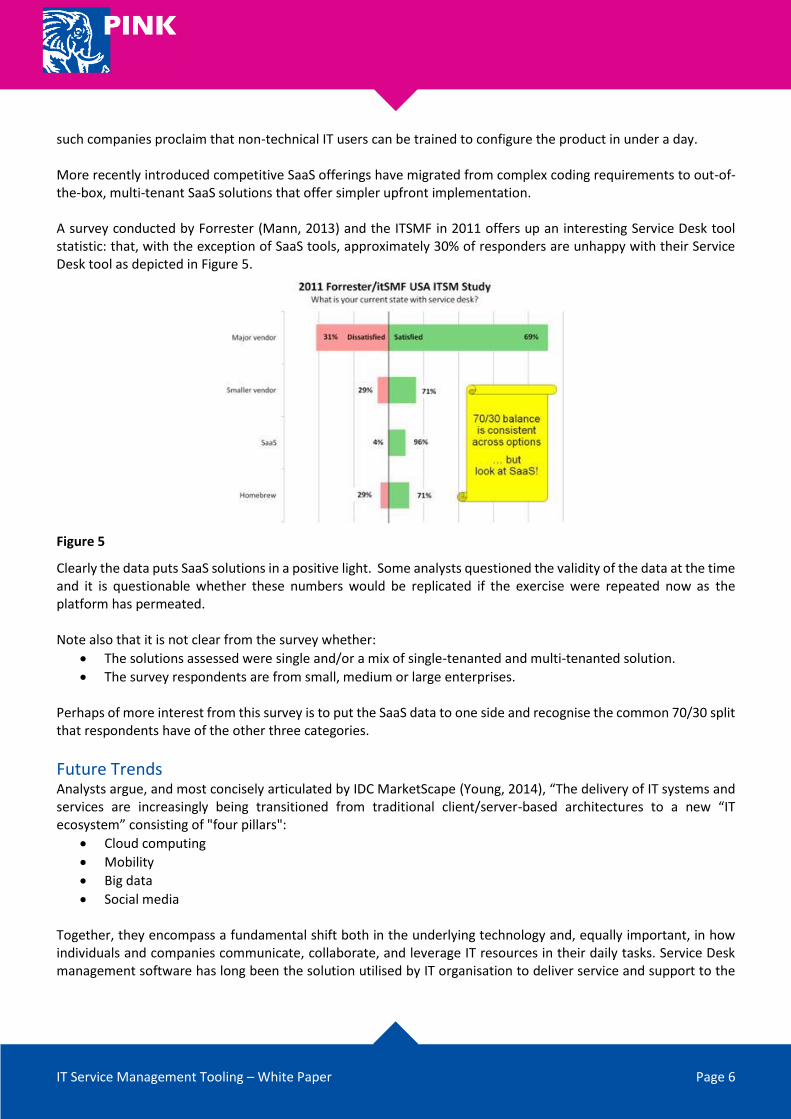

such companies proclaim that non-technical IT users can be trained to configure the product in under a day. More recently introduced competitive SaaS offerings have migrated from complex coding requirements to out-of-the-box, multi-tenant SaaS solutions that offer simpler upfront implementation. A survey conducted by Forrester (Mann, 2013) and the ITSMF in 2011 offers up an interesting Service Desk tool statistic: that, with the exception of SaaS tools, approximately 30% of responders are unhappy with their Service Desk tool as depicted in Figure 5.

Figure 5

Clearly the data puts SaaS solutions in a positive light. Some analysts questioned the validity of the data at the time and it is questionable whether these numbers would be replicated if the exercise were repeated now as the platform has permeated. Note also that it is not clear from the survey whether:

The solutions assessed were single and/or a mix of single-tenanted and multi-tenanted solution.

The survey respondents are from small, medium or large enterprises. Perhaps of more interest from this survey is to put the SaaS data to one side and recognise the common 70/30 split that respondents have of the other three categories.

Future Trends Analysts argue, and most concisely articulated by IDC MarketScape (Young, 2014), “The delivery of IT systems and services are increasingly being transitioned from traditional client/server-based architectures to a new “IT ecosystem” consisting of "four pillars":

Cloud computing

Mobility

Big data

Social media

Together, they encompass a fundamental shift both in the underlying technology and, equally important, in how individuals and companies communicate, collaborate, and leverage IT resources in their daily tasks. Service Desk management software has long been the solution utilised by IT organisation to deliver service and support to the

IT Service Management Tooling – White Paper Page 7

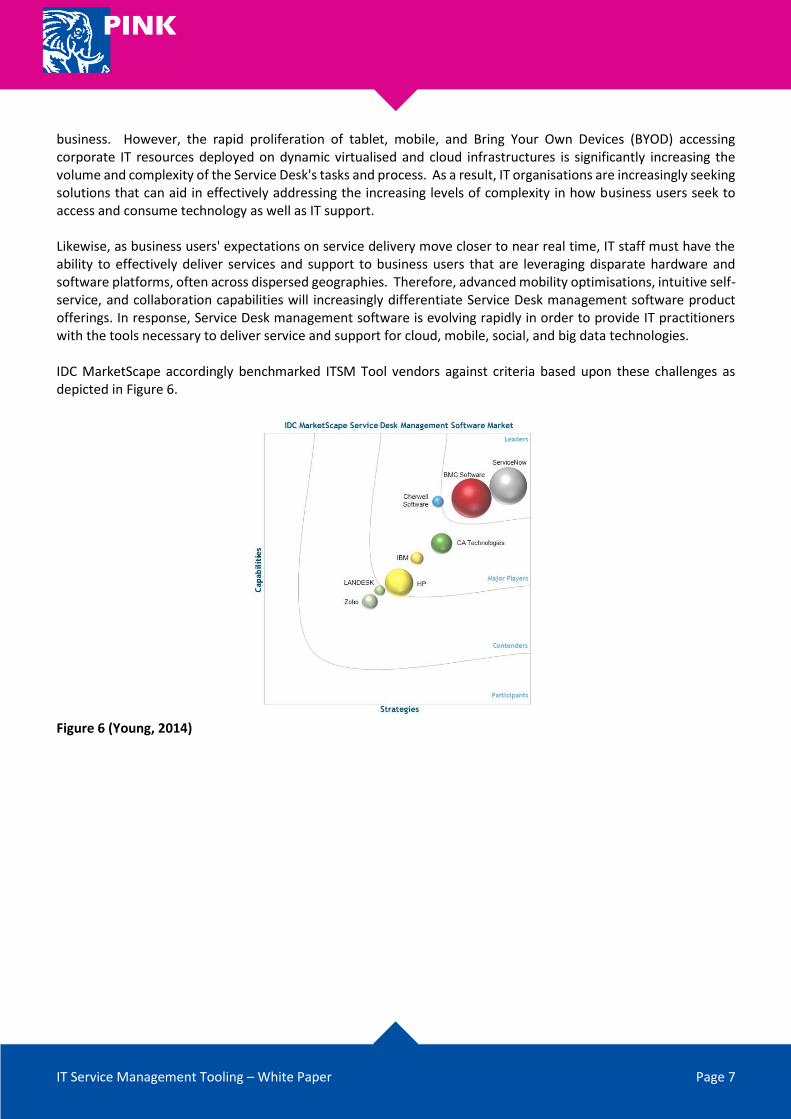

business. However, the rapid proliferation of tablet, mobile, and Bring Your Own Devices (BYOD) accessing corporate IT resources deployed on dynamic virtualised and cloud infrastructures is significantly increasing the volume and complexity of the Service Desk's tasks and process. As a result, IT organisations are increasingly seeking solutions that can aid in effectively addressing the increasing levels of complexity in how business users seek to access and consume technology as well as IT support. Likewise, as business users' expectations on service delivery move closer to near real time, IT staff must have the ability to effectively deliver services and support to business users that are leveraging disparate hardware and software platforms, often across dispersed geographies. Therefore, advanced mobility optimisations, intuitive self-service, and collaboration capabilities will increasingly differentiate Service Desk management software product offerings. In response, Service Desk management software is evolving rapidly in order to provide IT practitioners with the tools necessary to deliver service and support for cloud, mobile, social, and big data technologies. IDC MarketScape accordingly benchmarked ITSM Tool vendors against criteria based upon these challenges as depicted in Figure 6.

Figure 6 (Young, 2014)

Contact Details Pink Elephant EMEA Ltd 9 Castle Street Reading Berkshire RG1 7SB

Telephone: +44 (0) 118 324 0620 Email: [email protected] Twitter: @PinkElephantUK Pink Elephant and its logo, PinkVERIFY, PinkSCAN, PinkATLAS, PinkSELECT, and PinkREADY are either trademarks or registered trademarks of Pink Elephant Inc

Translating Knowledge into Results

www.pinkelephant.co.uk

Pink Worldwide