Embed Size (px)

Citation preview

CDFA: Advancing Development Finance Knowledge, Networks & Innovation www.cdfa.net

CDFA – Stern Brothers Renewable Energy Finance Webcast Series: How Bond Financing is Powering Renewable Energy

The Broadcast will begin at 1:00pm (EDT).

While you’re waiting, mark your calendar for these upcoming CDFA events:

CDFA: Advancing Development Finance Knowledge, Networks & Innovation www.cdfa.net

Katie KramerDirector, Education & ProgramsCouncil of Development Finance AgenciesColumbus, OH

Are you a CDFA Member?

Members receive exclusive access to thousands of resources in the CDFA Online Resource Database. Join today at www.cdfa.net to set‐up your unique login.

How Bond Financing is Powering Renewable Energy

CDFA: Advancing Development Finance Knowledge, Networks & Innovation www.cdfa.net

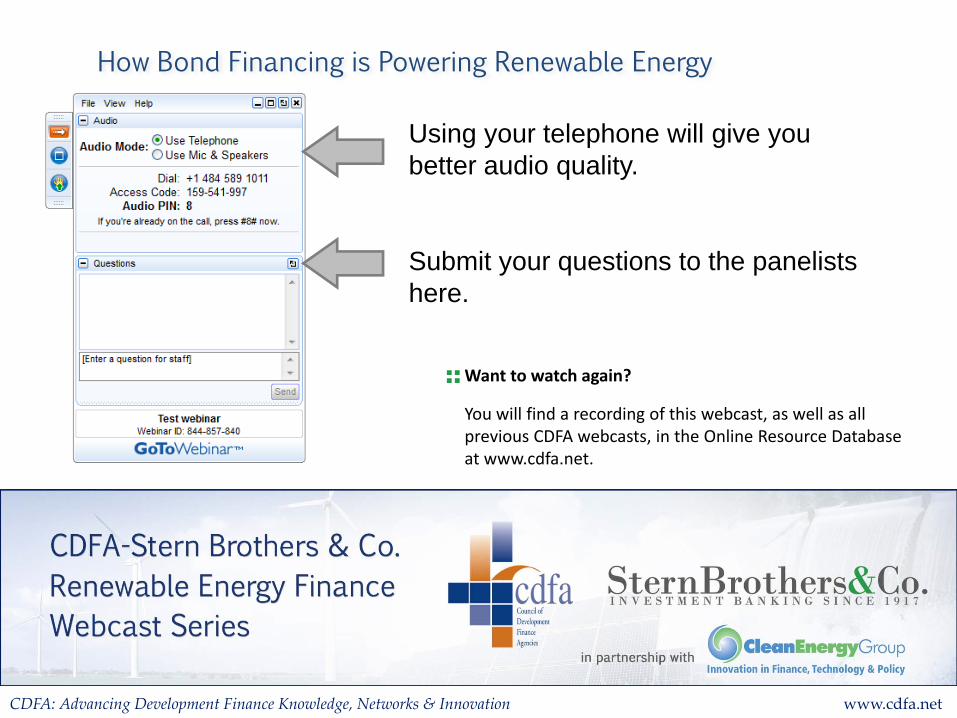

Using your telephone will give you better audio quality.

Submit your questions to the panelists here.

Want to watch again?

You will find a recording of this webcast, as well as all previous CDFA webcasts, in the Online Resource Database at www.cdfa.net.

How Bond Financing is Powering Renewable Energy

CDFA: Advancing Development Finance Knowledge, Networks & Innovation www.cdfa.net

SpeakersLes Krone, ModeratorStern Brothers & Co.

Lew MilfordClean Energy Group

Elizabeth BellisEnergy Programs Consortium

John WangOrrick, Herington & Sutcliffe LLP

Karlynn CoryNational Renewable Energy Laboratory

How Bond Financing is Powering Renewable Energy

CDFA: Advancing Development Finance Knowledge, Networks & Innovation www.cdfa.net

Les KroneManaging DirectorStern Brothers & Co.St. Louis, MO

What are you reading these days?

Your development finance toolbox isn’t complete without a set of CDFA reference guides. CDFA Members save 15% or more on every purchase. Order today at www.cdfa.net.

How Bond Financing is Powering Renewable Energy

CDFA: Advancing Development Finance Knowledge, Networks & Innovation www.cdfa.net

Lewis MilfordPresidentClean Energy GroupMontpelier, VT

Are you a CDFA Member?

Members receive discounts to all CDFA events, including training courses and the National Development Finance Summit. Join today at www.cdfa.net , and start saving.

How Bond Financing is Powering Renewable Energy

CDFA: Advancing Development Finance Knowledge, Networks & Innovation www.cdfa.net

Elizabeth BellisLegal/Tax CounselEnergy Programs ConsortiumBrooklyn, NY

Are you a CDFA Member?

Members receive discounts to all CDFA events, including training courses and the National Development Finance Summit. Join today at www.cdfa.net , and start saving.

How Bond Financing is Powering Renewable Energy

QECBsCDFA Webcast: How Bond Financing is Powering Renewable EnergyMay 3, 2012 1

Disclaimers

Circular 230: This presentation was not intended or written to be used, and it cannot be used by any taxpayer, for the purpose of avoiding penalties that may be imposed on the taxpayer under U.S. Federal tax law.

This presentation is intended to serve as a general introduction to the use of qualified energy conservation bonds to finance renewable energy projects. Nothing contained in this presentation should be construed or relied upon as legal advice.

2

Pleased to meet you

• Energy Programs Consortium (EPC) is a joint venture of NASCSP, representing the state weatherization and community service programs directors; NASEO, representing the state energy policy directors; NARUC, representing the state public service commissioners; and NEADA, representing the state directors of the Low-Income Home Energy Assistance Program.

• The QECB Program began in 2010, when EPC began tracking QECB utilization and talking to issuers about issues, questions, concerns and obstacles encountered along the way.

3

QECB 101

• A qualified energy conservation bond (QECB) is a federally subsidized bond that may be issued for a variety of uses that tend to promote the conservation of energy.

• QECBs are a type of “tax credit bond”. You may be familiar with the more common Build America Bonds.

• Tax credit bonds are subject to many of the same rules as traditional tax-exempt bonds, but the interest is taxable.

• Tax credit bonds can be issued to provide the holder of the bond with a federal tax credit. Until early 2010, QECBs could only be issued this way, and very few of them were issued.

• Some tax credit bonds give issuers the option to receive a direct cash payment from the U.S. Treasury in lieu of providing the bond holders a federal tax credit (sometimes referred to as “direct pay,” “cash pay” or “direct subsidy” bonds). QECBs can now be issued as direct subsidy bonds.

4

QECB Subsidy

• QECB issuers receive a check equal to 70% of the interest on your QECBs OR, if lower than your interest rate, the maximum rate set by Treasury (the “qualified tax credit rate”).

• For example (annualized for simplicity):• Interest rate on your bonds = 5%• Amount issued = $1,000,000• Qualified Tax Credit Rate = 4.5%• Subsidy = 70% * 4.5% * $1,000,000 =$31,500 per year out of $50,000 annual interest

• You can look up the most up to date rate (as well as historical rates) at:• https://www.treasurydirect.gov/GA-SL/SLGS/selectQTCDate.htm.

5

Maturity

• The maximum maturity for tax credit bonds is also set by Treasury periodically.

• Historically, QECB issuers have been allowed 12 to 22 year maturities.

• In the previous example, that would amount to $378,000 (12 years) to $693,000 (22 years) of direct subsidy from the federal government to your jurisdiction.

• The most up-to-date maturity (along with historical maturities) can be found on the tax credit rate lookup page (see slide 6).

• There is currently no cut-off date by which allocations must be used.

6

What kinds of renewable projects can I finance with QECBs?

• You can use your QECBs for a number of “qualified conservation purposes”, including capital expenditures for renewables:

• Rural development including the production of energy from renewable sources

• Certain other renewable energy facilities including wind, closed-loop biomass, open-loop biomass, geothermal or solar energy, small irrigation power, landfill gas, trash, qualified hydropower and marine and hydrokinetic production.

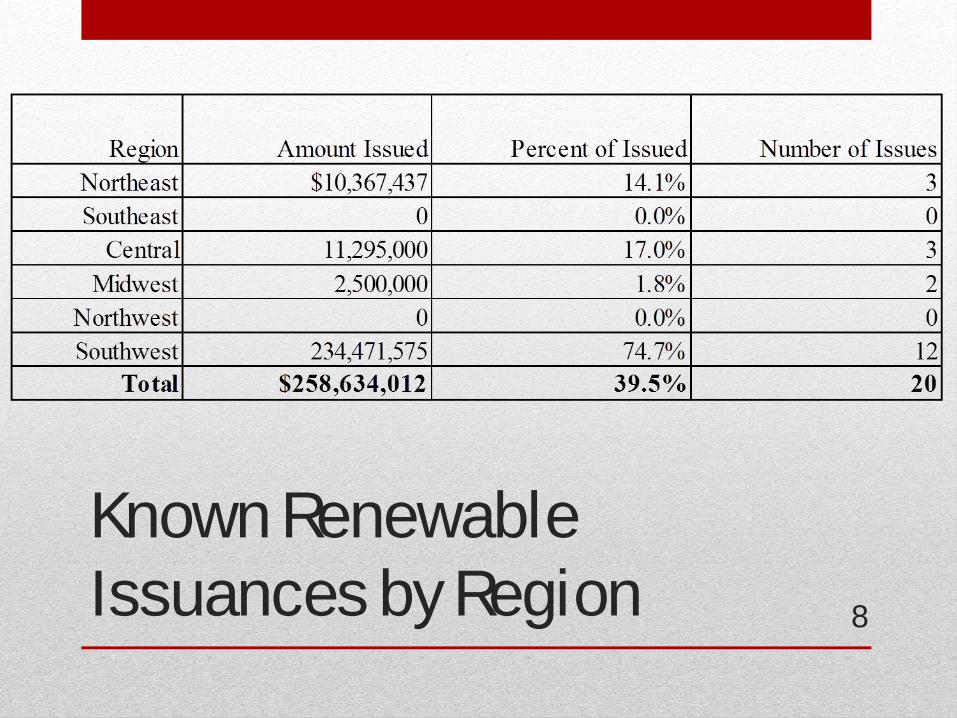

• $260 million of QECBs has been issued for renewable projects, primarily in the Southwest region

• These bonds have funded 20 projects.

7

Known Renewable Issuances by Region 8

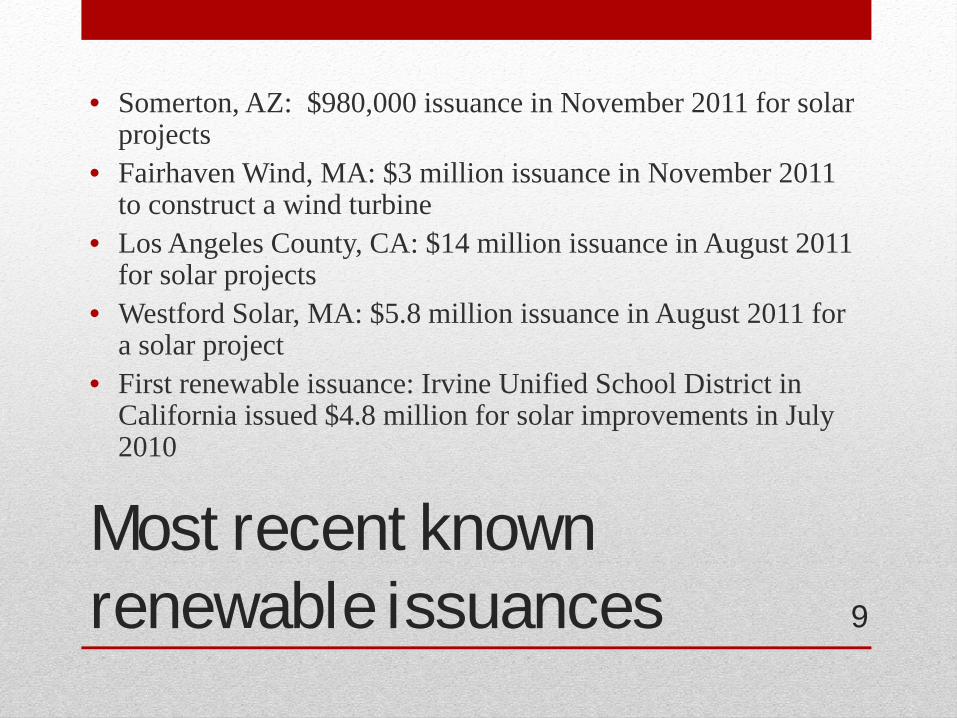

Most recent known renewable issuances

• Somerton, AZ: $980,000 issuance in November 2011 for solar projects

• Fairhaven Wind, MA: $3 million issuance in November 2011 to construct a wind turbine

• Los Angeles County, CA: $14 million issuance in August 2011 for solar projects

• Westford Solar, MA: $5.8 million issuance in August 2011 for a solar project

• First renewable issuance: Irvine Unified School District in California issued $4.8 million for solar improvements in July 2010

9

Example: Large Solar & Wind Issuance

• Issuer: Los Angeles Department of Water & Power• Amount Issued: $131 million• Use of Bond Proceeds:

• Pine Tree Wind Turbine Expansion Project – 10 wind turbines (15MW total added)• Pine Tree Solar Project – PV generator targeted at 10MW at 34.5kV output); will

generate 20 GWh per year• Adelanto Solar Project – PV generator targeted at 10MW at 4.16kV output; will

generate 20 GWh per year

10

Example: Mid-sized Solar for Schools

• Issuer: Lodi Unified School District, CA• Amount Issued: $9.9 million• Use of Proceeds: solar tracking system on available

parking lots and rooftop systems at 8 schools • Offset 77% of school’s electricity usage

11

Example: Small Solar Issuance

• Issuer: Fallbrook Public Utility District, CA• Amount Issued: $3.4 million• Use of Proceeds: Solar panels at wastewater treatment plant• Financed improvements will generate 70 percent of the

treatment plant’s energy needs.

12

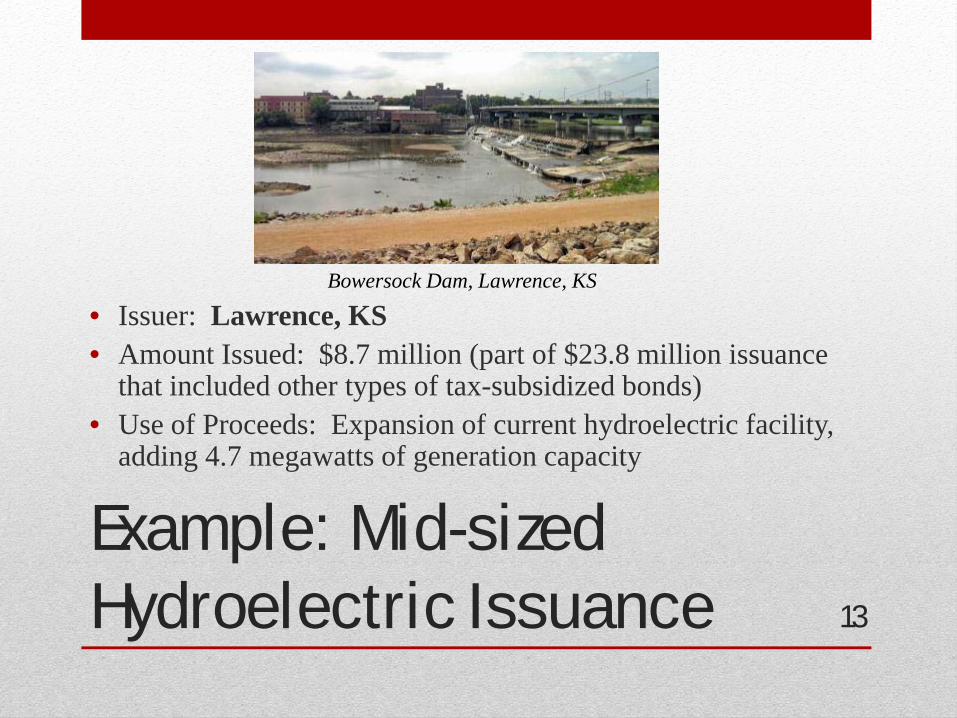

Example: Mid-sized Hydroelectric Issuance

• Issuer: Lawrence, KS• Amount Issued: $8.7 million (part of $23.8 million issuance

that included other types of tax-subsidized bonds)• Use of Proceeds: Expansion of current hydroelectric facility,

adding 4.7 megawatts of generation capacity

13

Bowersock Dam, Lawrence, KS

Example: Small Geothermal for Schools

• Issuer: Hartford School District, WI• Amount Issued: $2.23 million (part of $3.7 million

issuance)• Use of proceeds: Geothermal system for an elementary

school

14

Example: Small Wind Issuance

• Issuer: Scituate, MA• Amount Issued: $1.5 million• Use of Proceeds: One 1500 KW wind turbine

15

How popular are QECBs?

• At least 105 projects in 23 states have been funded with QECBs to date.

• Known bond volume totals $637 million; more bonds may be issued but not yet known (particularly if they were sold through private placement).

16

How do I get started?

• Determine the amount of your jurisdiction’s allocation. • Check the bond rating of the would-be issuer. Issuers with

poor ratings may have difficulty placing their bonds on favorable terms.

• Identify the project or projects desired to be financed. This may be done by issuing a request for applications if there is not already a project in mind.

• Select professionals (legal, financial) and contractors (builders, etc) for the project. This may be done by a competitive bid or RFP process in accordance with state and local requirements.

• Bond counsel should review intended uses for compliance with QECB requirements and assist in drafting documentation.

• Many QECBs (especially smaller issuances) are sold via private placements with banks.

17

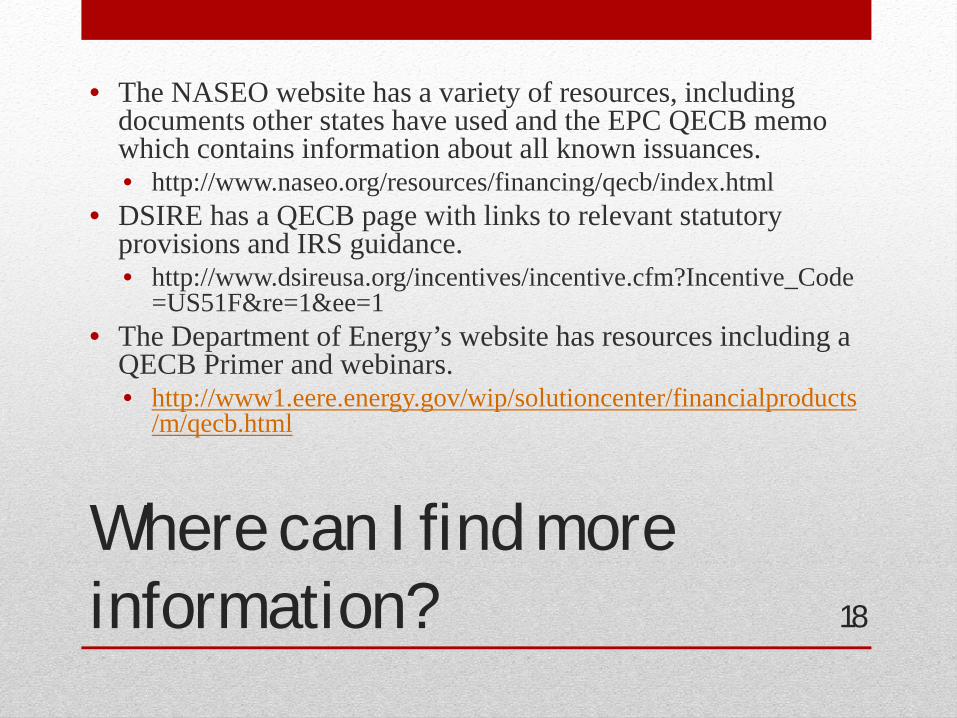

Where can I find more information?

• The NASEO website has a variety of resources, including documents other states have used and the EPC QECB memo which contains information about all known issuances.• http://www.naseo.org/resources/financing/qecb/index.html

• DSIRE has a QECB page with links to relevant statutory provisions and IRS guidance.• http://www.dsireusa.org/incentives/incentive.cfm?Incentive_Code

=US51F&re=1&ee=1• The Department of Energy’s website has resources including a

QECB Primer and webinars.• http://www1.eere.energy.gov/wip/solutioncenter/financialproducts

/m/qecb.html

18

Questions? Please keep in touch.

Elizabeth BellisDirector, QECB Program, Energy Programs ConsortiumEmail: [email protected]: (917) 370-7916

19

CDFA: Advancing Development Finance Knowledge, Networks & Innovation www.cdfa.net

John WangPartnerOrrick, Herington & Sutcliffe LLPSan Francisco, CA

Need assistance with your energy finance programs?

Consider CDFA’s Research & Advisory Services – offering customized and tailored technical assistance for all of your development finance needs. Learn more at www.cdfa.net.

How Bond Financing is Powering Renewable Energy

CDFA-Stern Brothers Renewable Energy Finance Webcast Series: How Bond Financing is Powering Renewable Energy: Certain Tax-Exempt StructuresMay 3, 2012

Presented by John Wang

1

Tax-Exempt Structures

Introduction• Prepay Electricity Power Purchase Agreements (PPAs). Under a Prepay

PPA structure, a municipal owned utility (MOU) as offtaker, enters into a PPA with a special purpose project developer (the “Project Developer”) whereby the Project Developer agrees to construct, own and operate the facility (the “Facility”) and the MOU agrees to prepay for a portion of the output of the Facility to be delivered over time in certain situations. The MOU issues tax exempt municipal bonds to fund the prepayment in a lump sum amount and the Project Developer, in turn, uses such proceeds to fund project costs.

• SWPAB Waste-to-Energy Projects. Certain portions of certain “waste-to-energy” renewable energy projects may qualify for tax-exempt financing under Section 142(a)(6) of the Code, which is available for solid waste disposal facilities. For example, certain facilities may take in municipal waste from city residents and process such waste for ultimate deposit in a landfill. Such processing of solid waste normally produces some form of biogas, such as methane, which can, in turn, be processed to produce a gas that can either power an electric generator onsite or be put into a pipeline for use by a third-party offtaker. Borrowers eligible for this category generally include traditional solid waste companies but also include developers that employ other waste-to-energy technologies.

2

Tax-Exempt Electricity Prepayment Structure

Introduction

• To be distinguished from tax-exempt pre-pay gas transactions

• Project Sponsor (i,.e., a developer or energy company) forms a special purpose power company (the “Project Developer”), which is typically a bankruptcy remote limited liability entity with no material obligations other than the construction, ownership and operation of the Project (the “Project Developer”).

• Project Developer and MOU enter into a Power Purchase Agreement (“PPA”) for the prepayment for a fixed amount of the energy output from the Facility from the Project Developer at a fixed price (the “Prepayment Amount”) to a specified term.

3

Tax-Exempt Electricity Prepayment Structure (cont’d)

• Project Developer finances the construction of the Facility using conventional financing, such conventional financing to be taken out through a combination of tax exempt bond proceeds (discussed below), equity and grant moneys. Such equity investors will be allocated Facility-related investment tax credits, accelerated depreciation and other tax attributes.

• At or around the commercial operation date, the MOU issues tax exempt bonds to fund the Prepayment Amount as a lump sum up front payment to the developer, which may be used by the Project Developer for any purpose, including for reimbursement of the costs of the construction of the Facility.

• The MOU is responsible for repayment of debt service on the bonds. As a result, the MOU’s bonds would be sold and marketed on the credit of the MOU’s utility, not the Facility itself or the Project Developer, thereby reducing or eliminating the need to procure credit enhancement for the bonds depending on the overall credit quality of the MOU’s utility. Therefore, the Prepay PPA structure is a way to provide for significant capital from an MOU offtaker for a large portion of the Facility, while at the same time reducing overall Facility costs through the issuance of municipal debt.

• Project Developer is tax owner of facility, but with no direct active involvement (typically) in the production or delivery of the energy to the MOU. Typically, an operating company will manage the facility pursuant to an O&M agreement.

4

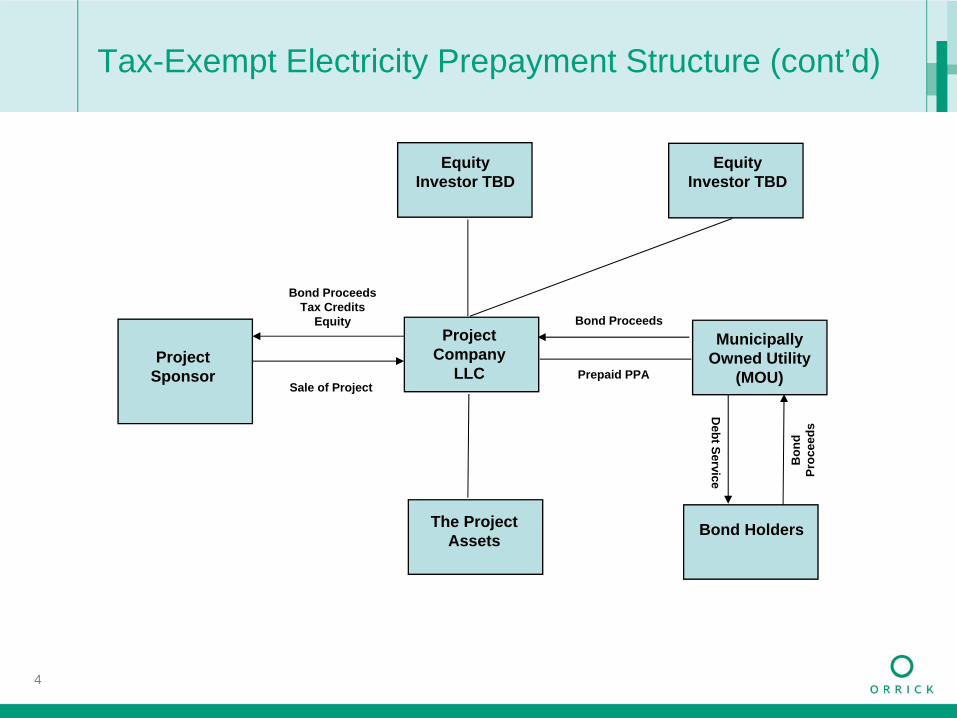

Tax-Exempt Electricity Prepayment Structure (cont’d)

Equity Investor TBD

Equity Investor TBD

Municipally Owned Utility

(MOU)

The Project Assets

Project Sponsor

Project Company

LLC Prepaid PPASale of Project

Bond Proceeds

Bond Holders

Debt Service

Bon

d Pr

ocee

ds

Bond Proceeds Tax Credits

Equity

5

Tax-Exempt Electricity Prepayment Structure (cont’d)

What are the Benefits to the Developer?

• Tax exempt bond proceeds representing the Prepayment Amount provide a significant funding source (can be 50% or more) to a Facility based on the credit and balance sheet of the MOU, not that of the developer, equity owner or project.

• Several tax benefits to the Project Developer under typical PPA structure can be achieved. Equity owners will be entitled to federal tax benefits, withoutreduction due to tax exempt bond financing; these include production tax credits, investment tax credits and accelerated depreciation.

6

Tax-Exempt Electricity Prepayment Structure (cont’d)

Key Municipal Finance Tax Issues on Pre-Pay Structures:

• Bonds must be issued by or on behalf of a municipally owned utility (“MOU”) and use of prepaid energy is limited to retail use through MOU and/or customers in qualified service areas.

• Tax exempt bond proceeds can only be used to make a fixed price prepayment; i.e., fixed payment for fixed amount of energy. Due to variability of amount of energy and O&M costs (which are also passed on to the MOU) a two tiered PPA structured is required.

• Equity must be the "tax" owner of the Facility. Thus, term of PPAs cannot exceed 80% of projects estimated useful life. Tax equity should have some meaningful investment in the project aside from the MOU's Prepayment Account. MOU cannot control plant operations, may not be able to foreclose on the facility in an event of breach by the developer, and MOU may have a purchase option only at FMV at the time of exercise.

7

Tax-Exempt Electricity Prepayment Structure (cont’d)

Key Municipal Finance Tax Issues on Pre-Pay Structures (cont’d): • No portion of Prepayment Amount, once paid to developer, can be reduced or

returned to MOU based on the actions of the MOU.• Tax treatment to Project Developer of lump sum Prepayment Amount should

be analyzed by tax advisors and financial accounts of the equity owners and the Project Developer. There can be ways to defer income inclusion of the Prepayment Amount for tax purposes.

8

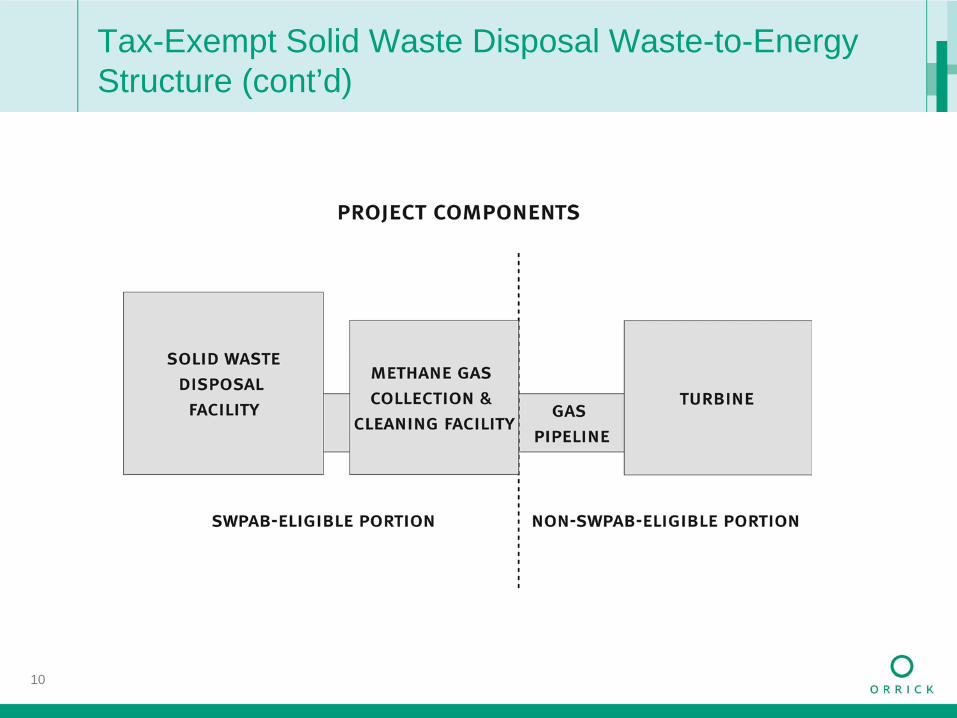

Tax-Exempt Solid Waste Disposal Waste-to-Energy Structure

General• Governmental issuer issues tax-exempt solid waste disposal bonds private

activity bonds (“SWPABs”) on behalf of a private entity borrower (“Borrower”)• Borrower applies proceeds of SWPAB to the portion of waste-to-energy

facilities that qualify portion SWPAB financing, i.e., the portion that constitutes land, buildings, equipment or other property that (i) processes solid waste in a final disposal process, an energy conversion process or a recycling process, (ii) performs a preliminary function to one of the aforementioned processes or (iii) is functionally related and subordinate to a facility described in (i) or (ii).

• Portions of a facility that transfer and or utilize materials after they have been converted from a waste into a useful form do not qualify; for example, in a resource recovery project, once waste has been burned and converted to steam, the part of the facility used to transport the steam or use it to generate electricity is not part of the “solid waste disposal facility.”

9

Tax-Exempt Solid Waste Disposal Waste-to-Energy Structure (cont’d)

• Non-qualifying portion be financed with equity or taxable debt or may qualify for some other form of tax-exempt debt

• This type of financing structure now available for developers and other non-traditional solid waste companies due to recent changes in tax law. Until recently, applicable tax rules required that solid waste have “no market or other value at the place at which it is located” (previously referred to as the so-called “no value rule”). The IRS released final Treasury Regulations that eliminated this requirement in August 2011.

• The following is an illustrative structure for a SWPAB financed waste-to-energy project

10

Tax-Exempt Solid Waste Disposal Waste-to-Energy Structure (cont’d)

CDFA: Advancing Development Finance Knowledge, Networks & Innovation www.cdfa.net

Karlynn CorySenior Energy AnalystNational Renewable Energy LaboratoryGolden, CO

Are you a CDFA Member?

Members receive exclusive access to thousands of resources in the CDFA Online Resource Database. Join today at www.cdfa.net to set‐up your unique login.

How Bond Financing is Powering Renewable Energy

NREL is a national laboratory of the U.S. Department of Energy Office of Energy Efficiency and Renewable Energy operated by the Alliance for Sustainable Energy, LLC

How Bond Financing is Powering Renewable Energy

CDFA-Stern Brothers RE Finance Web Series

Karlynn Cory Strategic Energy Analysis Center

May 3, 2012

How to Combine Bond Financing and PPAs: Key Considerations, Data and Tools

Disclaimer

2

DISCLAIMER AGREEMENT

These information (“Data”) are provided by the National Renewable Energy Laboratory (“NREL”), which is operated by the Alliance for Sustainable Energy LLC (“Alliance”) for the U.S. Department of Energy (the “DOE”).

It is recognized that disclosure of these Data is provided under the following conditions and warnings: (1) these Data have been prepared for reference purposes only; (2) these Data consist of forecasts, estimates or assumptions made on a best-efforts basis, based upon present expectations; and (3) these Data were prepared with existing information and are subject to change without notice.

The names DOE/NREL/ALLIANCE shall not be used in any representation, advertising, publicity or other manner whatsoever to endorse or promote any entity that adopts or uses these Data. DOE/NREL/ALLIANCE shall not provide any support, consulting, training or assistance of any kind with regard to the use of these Data or any updates, revisions or new versions of these Data.

YOU AGREE TO INDEMNIFY DOE/NREL/ALLIANCE, AND ITS AFFILIATES, OFFICERS, AGENTS, AND EMPLOYEES AGAINST ANY CLAIM OR DEMAND, INCLUDING REASONABLE ATTORNEYS' FEES, RELATED TO YOUR USE, RELIANCE, OR ADOPTION OF THESE DATA FOR ANY PURPOSE WHATSOEVER. THESE DATA ARE PROVIDED BY DOE/NREL/ALLIANCE "AS IS" AND ANY EXPRESS OR IMPLIED WARRANTIES, INCLUDING BUT NOT LIMITED TO, THE IMPLIED WARRANTIES OF MERCHANTABILITY AND FITNESS FOR A PARTICULAR PURPOSE ARE EXPRESSLY DISCLAIMED. IN NO EVENT SHALL DOE/NREL/ALLIANCE BE LIABLE FOR ANY SPECIAL, INDIRECT OR CONSEQUENTIAL DAMAGES OR ANY DAMAGES WHATSOEVER, INCLUDING BUT NOT LIMITED TO CLAIMS ASSOCIATED WITH THE LOSS OF DATA OR PROFITS, WHICH MAY RESULT FROM AN ACTION IN CONTRACT, NEGLIGENCE OR OTHER TORTIOUS CLAIM THAT ARISES OUT OF OR IN CONNECTION WITH THE USE OR PERFORMANCE OF THESE DATA.

National Renewable Energy Laboratory Innovation for Our Energy Future

This work was supported by the U.S. Department of Energy under Contract No. DE-AC36-08-GO28308 with the National Renewable Energy Laboratory.

Overview

3

1. RE project financing options for municipalities• Third-party Power Purchase Agreement Financing (aka PPAs)• Focus: How to combine bond financing with PPAs

2. Financing resources available• NREL Data, Tools and Analysis

• Reminder: Tax credits drive much of the market today• Not only for commercial and industrial systems• But also for residential and municipal deployment

4

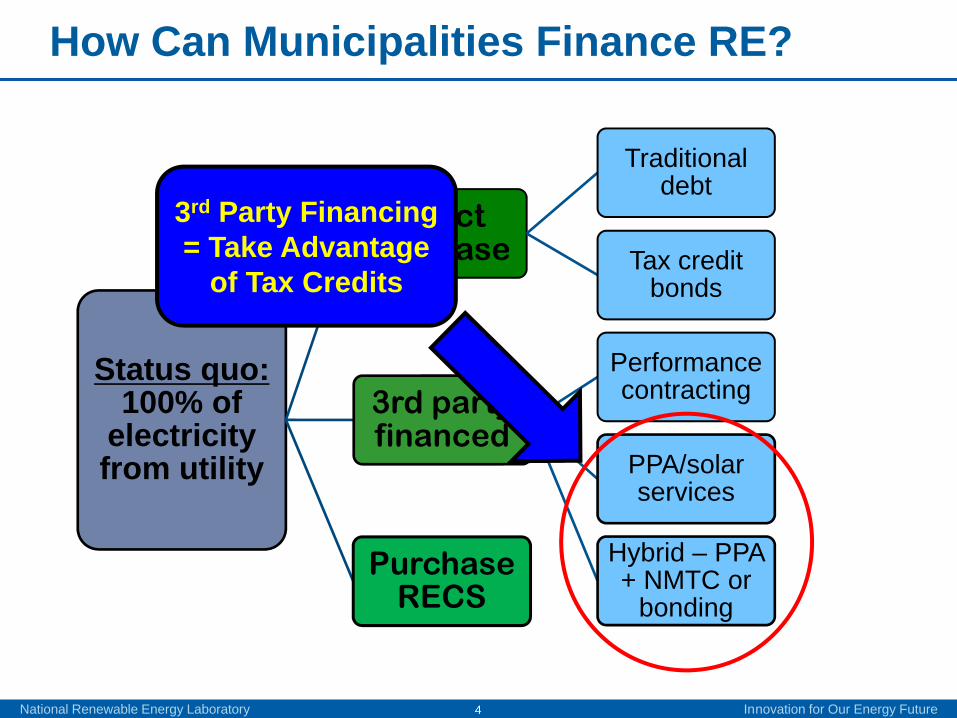

How Can Municipalities Finance RE?

Status quo: 100% of

electricity from utility

Direct purchase

Traditional debt

Tax credit bonds

3rd party financed

Performance contracting

PPA/solar services

Hybrid – PPA + NMTC or

bondingPurchase

RECS

National Renewable Energy Laboratory Innovation for Our Energy Future

3rd Party Financing = Take Advantage

of Tax Credits

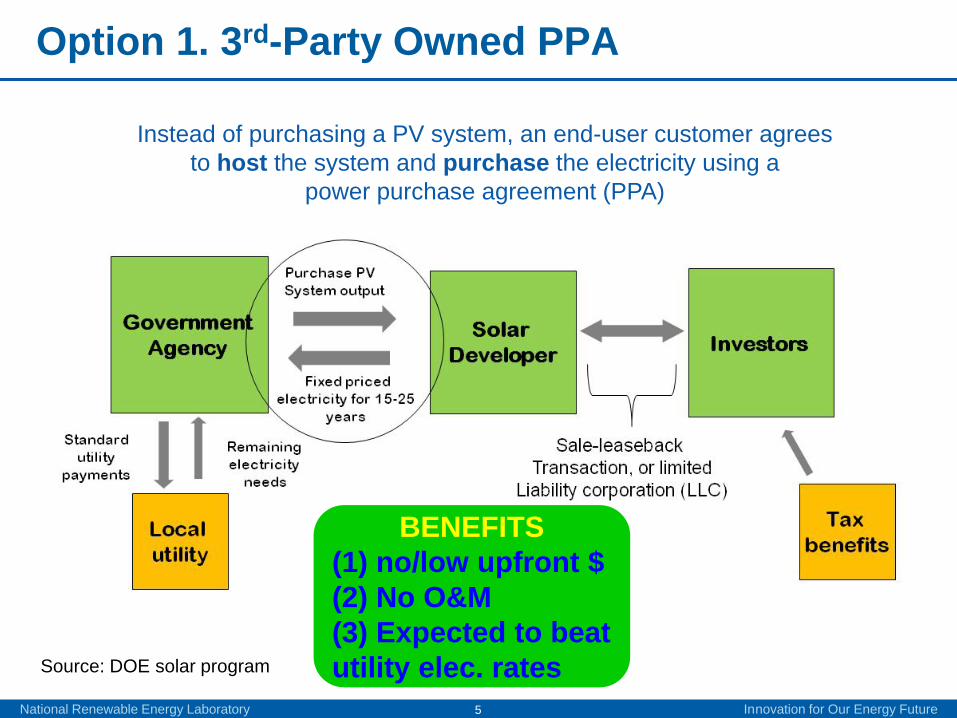

Option 1. 3rd-Party Owned PPA

National Renewable Energy Laboratory Innovation for Our Energy Future5

Source: DOE solar program

Instead of purchasing a PV system, an end-user customer agrees to host the system and purchase the electricity using a

power purchase agreement (PPA)

BENEFITS(1) no/low upfront $(2) No O&M(3) Expected to beat utility elec. rates

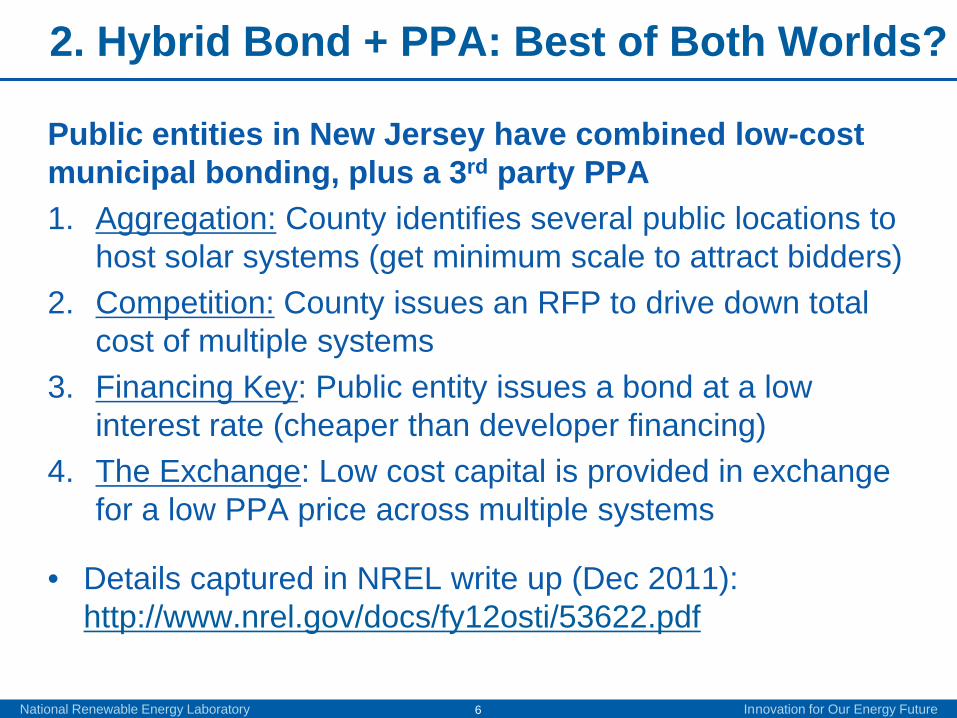

2. Hybrid Bond + PPA: Best of Both Worlds?

Public entities in New Jersey have combined low-cost municipal bonding, plus a 3rd party PPA1. Aggregation: County identifies several public locations to

host solar systems (get minimum scale to attract bidders)2. Competition: County issues an RFP to drive down total

cost of multiple systems3. Financing Key: Public entity issues a bond at a low

interest rate (cheaper than developer financing)4. The Exchange: Low cost capital is provided in exchange

for a low PPA price across multiple systems

• Details captured in NREL write up (Dec 2011): http://www.nrel.gov/docs/fy12osti/53622.pdf

National Renewable Energy Laboratory Innovation for Our Energy Future6

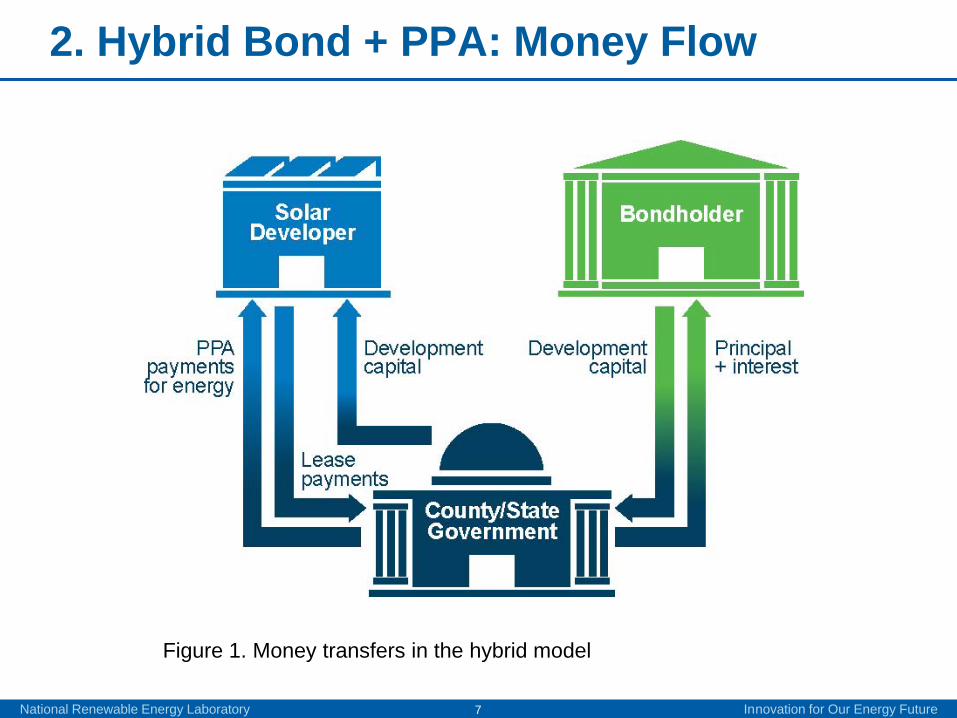

2. Hybrid Bond + PPA: Money Flow

National Renewable Energy Laboratory Innovation for Our Energy Future7

Figure 1. Money transfers in the hybrid model

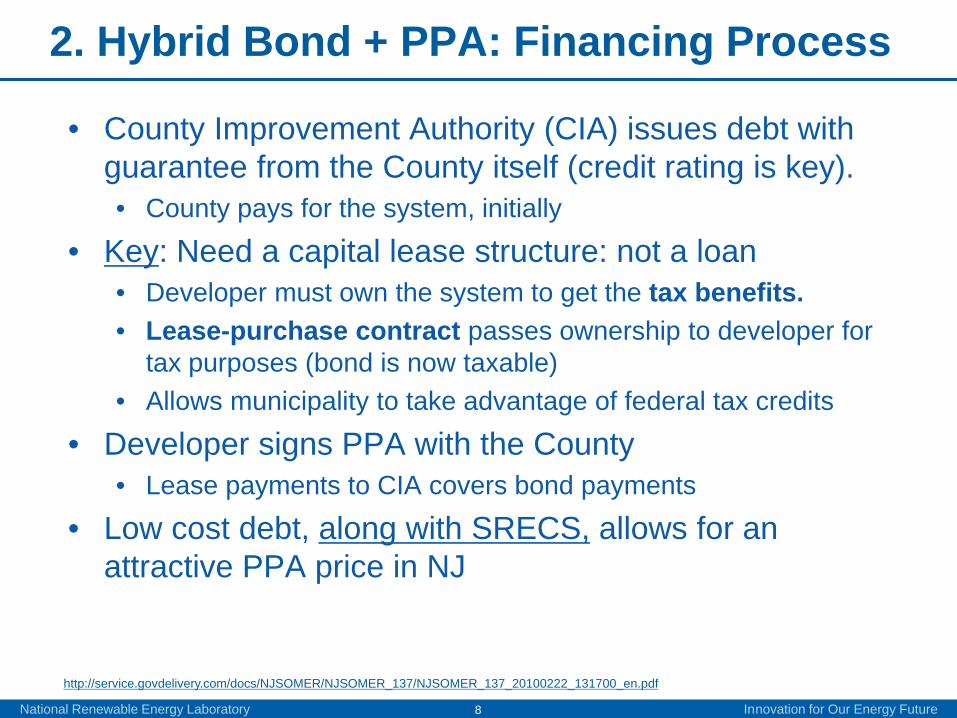

2. Hybrid Bond + PPA: Financing Process

• County Improvement Authority (CIA) issues debt with guarantee from the County itself (credit rating is key).• County pays for the system, initially

• Key: Need a capital lease structure: not a loan• Developer must own the system to get the tax benefits.• Lease-purchase contract passes ownership to developer for

tax purposes (bond is now taxable)• Allows municipality to take advantage of federal tax credits

• Developer signs PPA with the County • Lease payments to CIA covers bond payments

• Low cost debt, along with SRECS, allows for an attractive PPA price in NJ

National Renewable Energy Laboratory Innovation for Our Energy Future8

Source: Somerset County, New Jerseyhttp://service.govdelivery.com/docs/NJSOMER/NJSOMER_137/NJSOMER_137_20100222_131700_en.pdf

National Renewable Energy Laboratory Innovation for Our Energy Future9

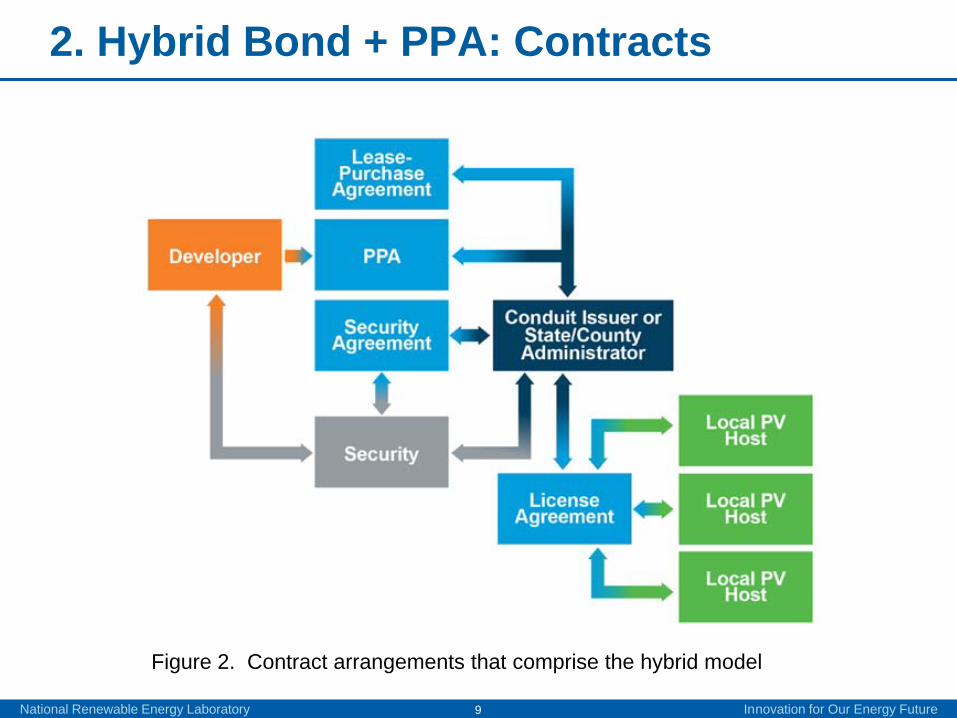

2. Hybrid Bond + PPA: Contracts

Figure 2. Contract arrangements that comprise the hybrid model

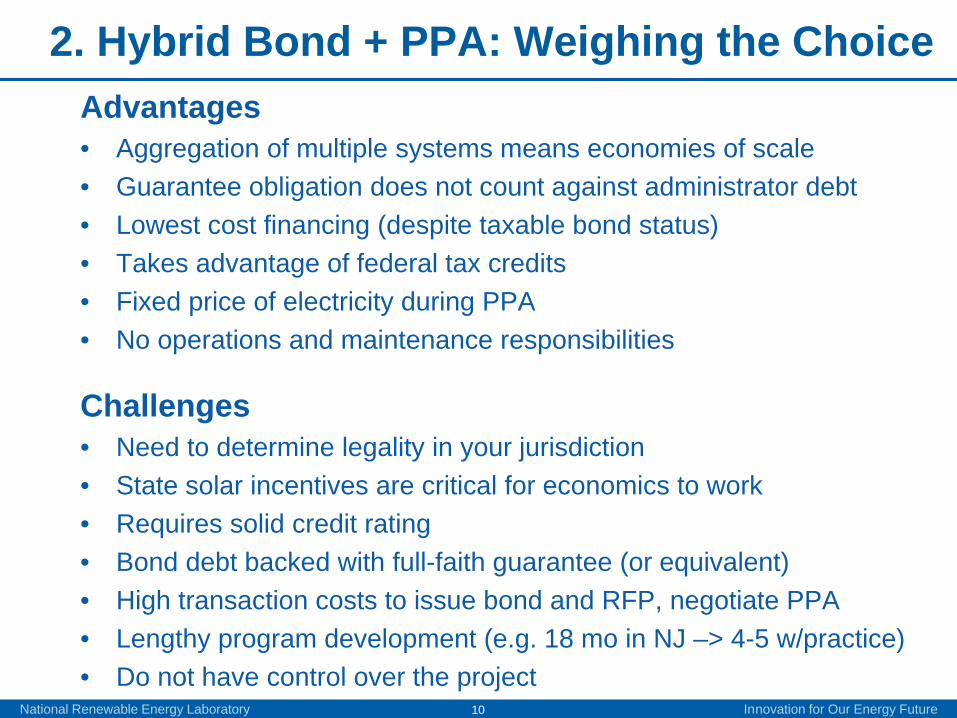

2. Hybrid Bond + PPA: Weighing the ChoiceAdvantages• Aggregation of multiple systems means economies of scale• Guarantee obligation does not count against administrator debt• Lowest cost financing (despite taxable bond status)• Takes advantage of federal tax credits• Fixed price of electricity during PPA• No operations and maintenance responsibilities

Challenges• Need to determine legality in your jurisdiction• State solar incentives are critical for economics to work• Requires solid credit rating• Bond debt backed with full-faith guarantee (or equivalent)• High transaction costs to issue bond and RFP, negotiate PPA• Lengthy program development (e.g. 18 mo in NJ –> 4-5 w/practice)• Do not have control over the project

National Renewable Energy Laboratory Innovation for Our Energy Future10

National Renewable Energy Laboratory Innovation for Our Energy Future11

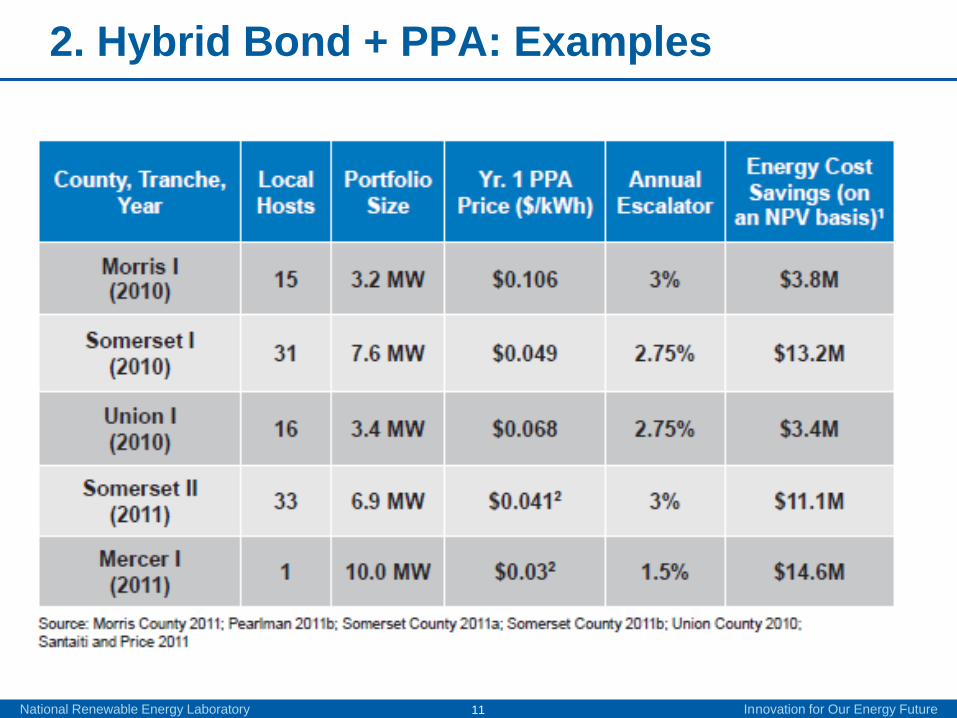

2. Hybrid Bond + PPA: Examples

NATIONAL RENEWABLE ENERGY LABORATORY (Not Peer Reviewed. Do Not Cite)

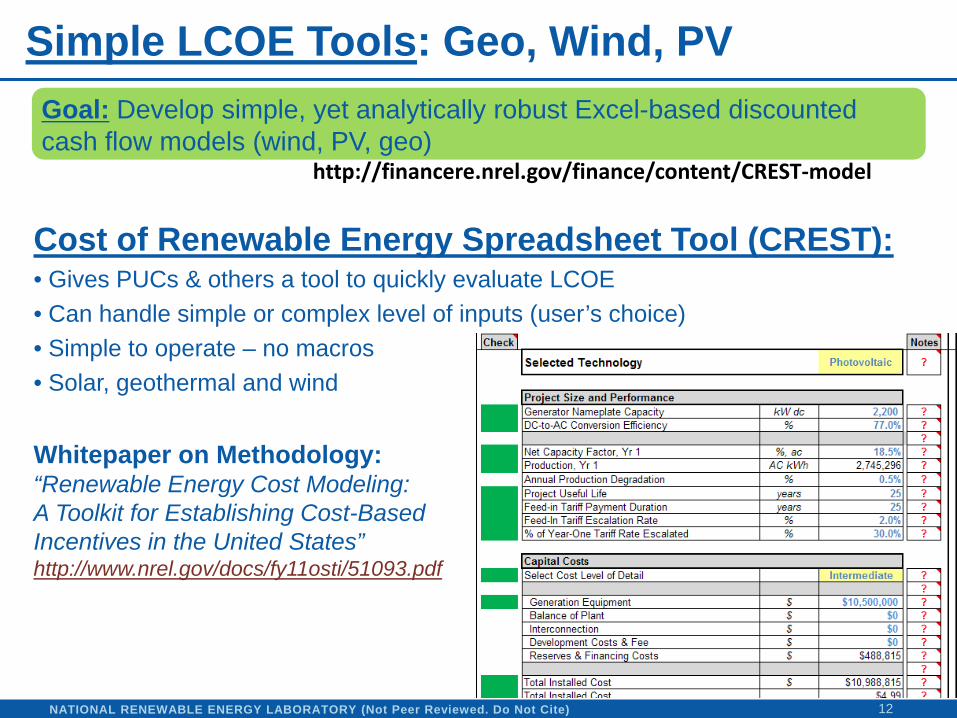

Simple LCOE Tools: Geo, Wind, PV

Cost of Renewable Energy Spreadsheet Tool (CREST):• Gives PUCs & others a tool to quickly evaluate LCOE• Can handle simple or complex level of inputs (user’s choice)• Simple to operate – no macros• Solar, geothermal and wind

Whitepaper on Methodology:“Renewable Energy Cost Modeling: A Toolkit for Establishing Cost-Based Incentives in the United States”http://www.nrel.gov/docs/fy11osti/51093.pdf

Goal: Develop simple, yet analytically robust Excel-based discounted cash flow models (wind, PV, geo)

12

http://financere.nrel.gov/finance/content/CREST‐model

NATIONAL RENEWABLE ENERGY LABORATORY (Not Peer Reviewed. Do Not Cite)

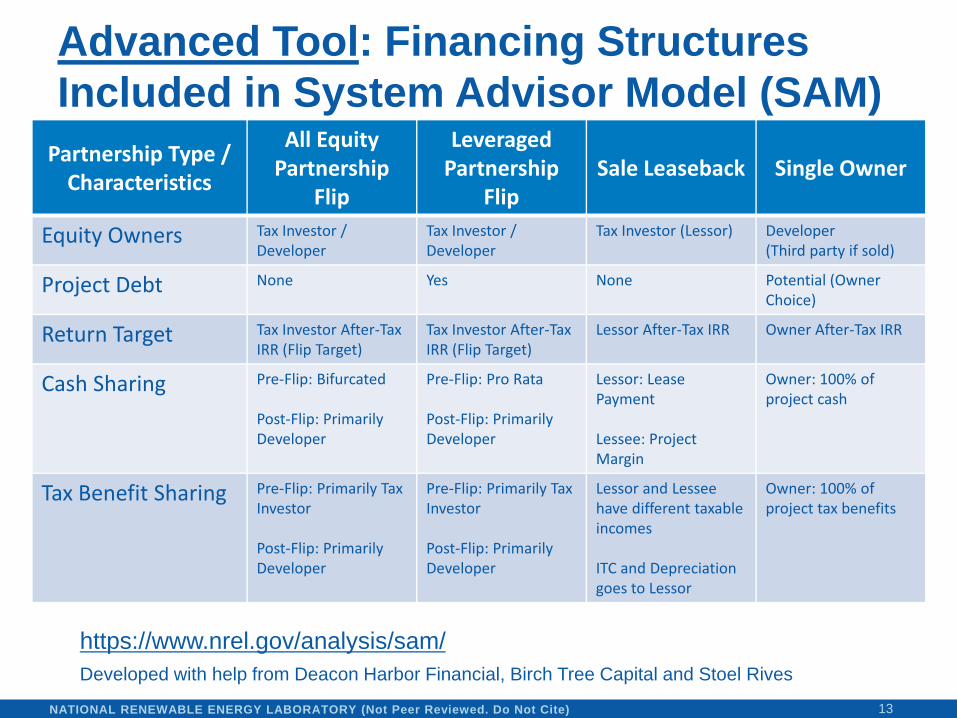

Advanced Tool: Financing Structures Included in System Advisor Model (SAM)

13

Partnership Type / Characteristics

All Equity Partnership

Flip

Leveraged Partnership

FlipSale Leaseback Single Owner

Equity Owners Tax Investor / Developer

Tax Investor / Developer

Tax Investor (Lessor) Developer(Third party if sold)

Project Debt None Yes None Potential (OwnerChoice)

Return Target Tax Investor After‐Tax IRR (Flip Target)

Tax Investor After‐Tax IRR (Flip Target)

Lessor After‐Tax IRR Owner After‐Tax IRR

Cash Sharing Pre‐Flip: Bifurcated

Post‐Flip: Primarily Developer

Pre‐Flip: Pro Rata

Post‐Flip: Primarily Developer

Lessor: Lease Payment

Lessee: Project Margin

Owner: 100% of project cash

Tax Benefit Sharing Pre‐Flip: Primarily Tax Investor

Post‐Flip: Primarily Developer

Pre‐Flip: Primarily Tax Investor

Post‐Flip: Primarily Developer

Lessor and Lessee have different taxable incomes

ITC and Depreciation goes to Lessor

Owner: 100% of project tax benefits

https://www.nrel.gov/analysis/sam/Developed with help from Deacon Harbor Financial, Birch Tree Capital and Stoel Rives

14

http://financeRE.nrel.gov

NATIONAL RENEWABLE ENERGY LABORATORY

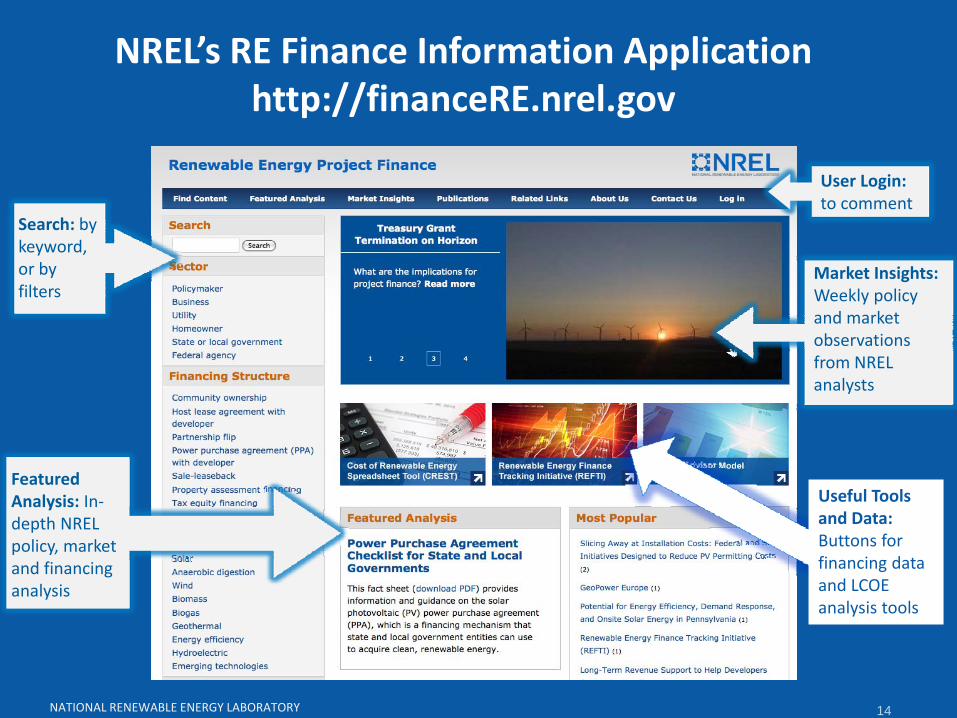

NREL’s RE Finance Information Applicationhttp://financeRE.nrel.gov

Market Insights: Weekly policy and market observations from NREL analysts

Search: by keyword, or by filters

User Login:to comment

Useful Tools and Data: Buttons for financing data and LCOE analysis tools

Featured Analysis: In‐depth NREL policy, market and financing analysis

Karlynn CoryRE Project Finance Analysis Team Lead

http://financeRE.nrel.govP: (303) 384-7464

Leading the Way to a Clean Energy Future

CDFA: Advancing Development Finance Knowledge, Networks & Innovation www.cdfa.net

Audience Questions

Register Today

Early Bird Ratesavailable until June 15, 2012.

CDFA: Advancing Development Finance Knowledge, Networks & Innovation www.cdfa.net

Continue the Conversation #CDFAwebcast

CDFA: Advancing Development Finance Knowledge, Networks & Innovation www.cdfa.net

Innovation Finance WebCourseDaily: 12-5pm (EDT)May 8-9, 2012

Intro Energy Finance CourseWashington, DCJuly 31-August 1, 2012

TIF WeekDaily: 12-5pm (EDT)Intro TIF: Sept. 18-19, 2012Advanced TIF: Sept. 20-21, 2012

Register online at www.cdfa.net

Upcoming Events at CDFA

CDFA: Advancing Development Finance Knowledge, Networks & Innovation www.cdfa.net

CDFA – BNY Mellon Development Finance Webcast SeriesTuesday, May 22, 2012 @ 1:00pm Eastern

CDFA – Stone & Youngberg Tax Increment Finance Webcast SeriesThursday, June 7, 2012 @ 1:00pm Eastern

CDFA – Stern Brothers Renewable Energy Finance Webcast SeriesThursday, September 13, 2012 @ 1:00pm Eastern

Upcoming Webcasts

CDFA: Advancing Development Finance Knowledge, Networks & Innovation www.cdfa.net

Les KroneManaging [email protected]

Katie KramerDirector, Education & [email protected]

Lewis [email protected]

For More Information