Embed Size (px)

Citation preview

© 2016 Halliburton. All rights reserved.

What will shape the

global supply mix?

Dr. Jonathan Lewis

Senior Vice President, Completion & Production

February 2015

2 © 2016 Halliburton. All rights reserved.

Safe Harbor

The statements in this presentation that are not historical statements, including statements regarding future financial performance and the pending Baker Hughes transaction, are

forward-looking statements within the meaning of the federal securities laws. These statements are subject to numerous risks and uncertainties, many of which are beyond the

company's control, which could cause actual results to differ materially from the results expressed or implied by the statements. These risks and uncertainties include, but are not

limited to: with respect to the Baker Hughes acquisition, the timing to consummate the proposed transaction; the terms, timing and completion of divestitures undertaken to obtain

required regulatory approvals; the conditions to closing of the proposed transaction may not be satisfied or the closing of the proposed transaction otherwise does not occur; the

risk a regulatory approval that may be required for the proposed transaction is not obtained or is obtained subject to conditions that are not anticipated; the diversion of

management time on transaction-related issues; the ultimate timing, outcome and results of integrating the operations of Halliburton and Baker Hughes and the ultimate outcome

of Halliburton’s operating efficiencies applied to Baker Hughes’ products and services; the effects of the business combination of Halliburton and Baker Hughes, including the

combined company’s future financial condition, results of operations, strategy and plans; expected synergies and other benefits from the proposed transaction and the ability of

Halliburton to realize such synergies and other benefits; with respect to the Macondo well incident, final court approval of, and the satisfaction of the conditions in, Halliburton's

September 2014 settlement, including the results of any appeals of rulings in the multi-district litigation; indemnification and insurance matters; with respect to repurchases of

Halliburton common stock, the continuation or suspension of the repurchase program, the amount, the timing and the trading prices of Halliburton common stock, and the

availability and alternative uses of cash; changes in the demand for or price of oil and/or natural gas can be significantly impacted by weakness in the worldwide economy;

consequences of audits and investigations by domestic and foreign government agencies and legislative bodies and related publicity and potential adverse proceedings by such

agencies; protection of intellectual property rights and against cyber attacks; compliance with environmental laws; changes in government regulations and regulatory

requirements, particularly those related to offshore oil and natural gas exploration, radioactive sources, explosives, chemicals, hydraulic fracturing services, and climate-related

initiatives; compliance with laws related to income taxes and assumptions regarding the generation of future taxable income; risks of international operations, including risks

relating to unsettled political conditions, war, the effects of terrorism, foreign exchange rates and controls, international trade and regulatory controls, and doing business with

national oil companies; weather-related issues, including the effects of hurricanes and tropical storms; changes in capital spending by customers; delays or failures by customers

to make payments owed to us; execution of long-term, fixed-price contracts; structural changes in the oil and natural gas industry; maintaining a highly skilled workforce;

availability and cost of raw materials; and integration and success of acquired businesses and operations of joint ventures. Halliburton's Form 10-K for the year ended December

31, 2015, recent Current Reports on Form 8-K, and other Securities and Exchange Commission filings discuss some of the important risk factors identified that may affect

Halliburton's business, results of operations, and financial condition. Halliburton undertakes no obligation to revise or update publicly any forward-looking statements for any

reason.

3 © 2016 Halliburton. All rights reserved.

Agenda

Where Are We?

How Did We Get Here?

Demand Outlook

Key Drivers of Where the Industry

Will Find and Produce Resources

4 © 2016 Halliburton. All rights reserved.

Where We Are

Source: Baker Hughes US Rig Count, through 2/12/16

0.20

0.40

0.60

0.80

1.00

0 25 50 75 100 125 150In

de

xe

d R

ig C

ou

nt

Weeks

1985-88 1997-01 2001-04 2008-11 2014-Curr

-72% -67%

U.S. Rig Count Index

Crude oil at 13-year lows

U.S. rig count down 72%

Capital spend reduced

250,000 energy jobs lost

-57% -72% -43% -52% -67%

5 © 2016 Halliburton. All rights reserved.

How We Got Here

Source: EIA, IHS

0

2

4

6

8

10

12

2010 2011 1Q12 1Q13 1Q14 1Q15 1Q16

OPEC N. America Total Liquids Supply Total Liquids Demand

Mill

ion

ba

rre

ls p

er

da

y

2010-11

Healthy demand growth

following global recession

Incremental Supply and Demand by Source

6 © 2016 Halliburton. All rights reserved.

0

2

4

6

8

10

12

2010 2011 2012 2013 2014 2015 1Q16

OPEC N. America Total Liquids Supply Total Liquids Demand

2010-11

Healthy demand growth

following global recession

2012 -14

N. America production growing

faster than incremental global

demand

How We Got Here

Source: EIA, IHS

Mill

ion

ba

rre

ls p

er

da

y

Incremental Supply and Demand by Source

7 © 2016 Halliburton. All rights reserved.

How We Got Here

0

2

4

6

8

10

12

2010 2011 2012 2013 2014 2015 2016

OPEC N. America Total Liquids Supply Total Liquids Demand

2010-11

Healthy demand growth

following global recession

2012 -14

N. America production growing

faster than incremental global

demand

2015

OPEC increases production to

maintain share

Source: EIA, IHS

Mill

ion

ba

rre

ls p

er

da

y

Incremental Supply and Demand by Source

8 © 2016 Halliburton. All rights reserved.

Is This Downturn Different?

0.90

0.95

1.00

1.05

1.10

1.15

1.20

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1985 1986 1987

WTI Price Global Production

0.90

0.95

1.00

1.05

1.10

1.15

1.20

0.0

0.2

0.4

0.6

0.8

1.0

1.2

2014 2015 2016

WTI Price Global Production

WT

I price in

dex

WT

I price in

dex

Glo

bal p

roductio

n in

dex

Glo

bal p

roductio

n in

dex

1985 - 1987

Oil price only bottomed after OPEC

cut production in 3Q86

2014 – 2016

Lack of meaningful production declines

has weighed on price

Global Production vs. Oil Price

9 © 2016 Halliburton. All rights reserved.

Going Forward – Hydrocarbons Dominate

0

100

200

300

400

500

600

700

2000 2005 2010 2015 2020 2025

Quadrilli

on B

TU

s

Economic Growth

Urbanization

Policy

Technology Developments

Global Energy Demand

Annual growth: 1-2%

2015-2025

CAGR 1-4% ~2% 3-4% 2-3% ~1% 6-9% 0-1%

Oil Gas Coal Nuclear Biomass/

Waste Hydro

Other

Renewables

Source: BP, Exxon Mobil, Statoil, company estimates

10 © 2016 Halliburton. All rights reserved.

Time To Revisit Demand Consensus?

$0

$20

$40

$60

$80

$100

$120

-2%

-1%

0%

1%

2%

3%

4%

5%

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

YOY Change in Oil Demand WTI Price

Annual change in

glo

bal liq

uid

s d

em

and

O

il pric

e, $

/barre

l

1994 – 2004 low-priced oil

Average demand growth:

+1.8% / year

2004-2014 high-priced oil

Average demand growth:

+0.8% / year

Global Demand vs. Oil Price

11 © 2016 Halliburton. All rights reserved.

How Much New Oil Do We Need To Produce?

0

20

40

60

80

100

120

2015 2016 2017 2018 2019 2020

Production Offset decline New Demand

Mill

ion

ba

rre

ls p

er

da

y

* Assumes 1% annual

demand growth

2015 - 2020

19mm barrels of new supply to offset production decline

and meet 1% demand growth

Source: Rystad Energy, Feburary 2016

Global Demand vs. Oil Production

12 © 2016 Halliburton. All rights reserved.

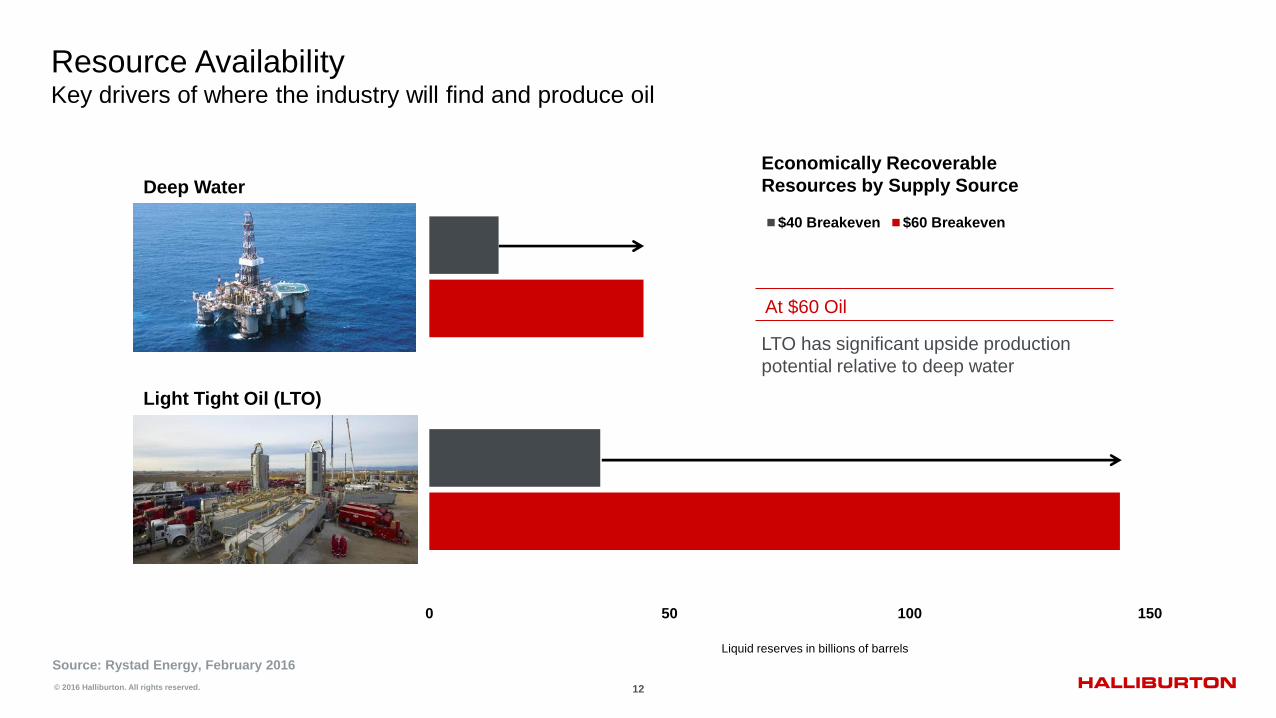

0 50 100 150

$40 Breakeven $60 Breakeven

Liquid reserves in billions of barrels

Resource Availability Key drivers of where the industry will find and produce oil

Source: Rystad Energy, February 2016

At $60 Oil

LTO has significant upside production

potential relative to deep water

Deep Water

Light Tight Oil (LTO)

Economically Recoverable

Resources by Supply Source

13 © 2016 Halliburton. All rights reserved.

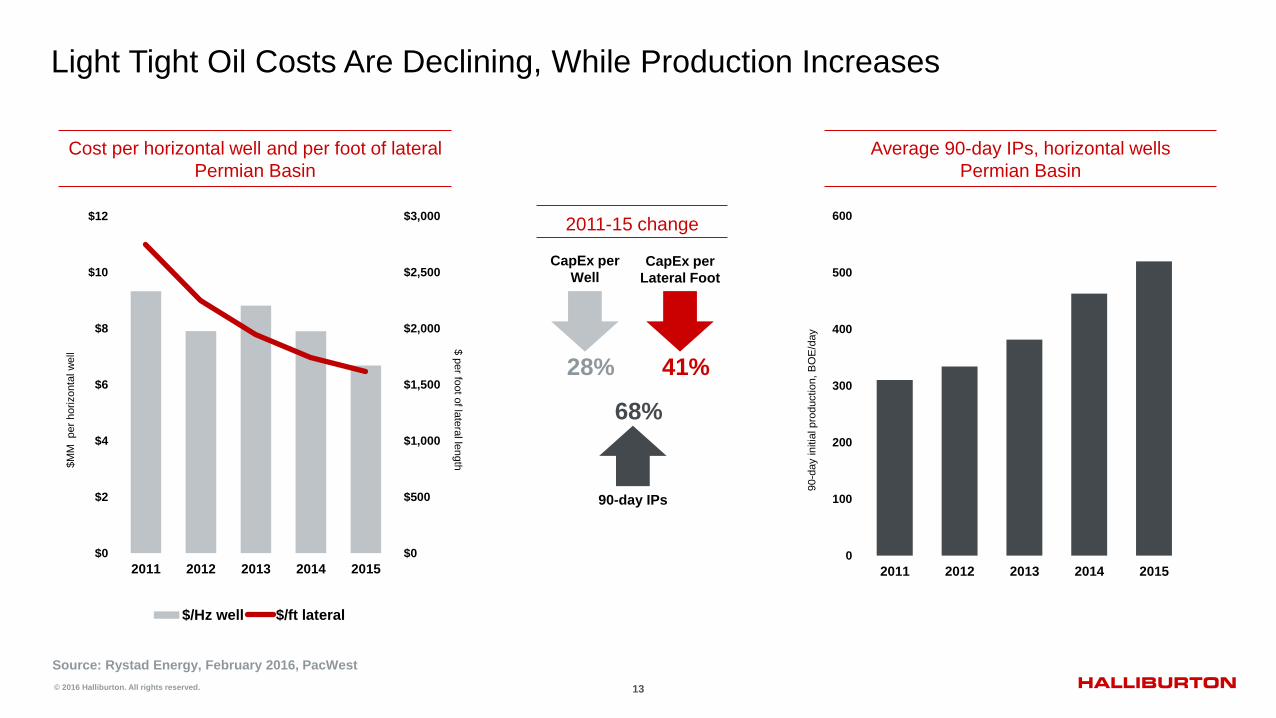

Light Tight Oil Costs Are Declining, While Production Increases $M

M

per

horizonta

l w

ell

90-d

ay in

itia

l pro

ductio

n,

BO

E/d

ay

$ p

er fo

ot o

f late

ral le

ngth

Source: Rystad Energy, February 2016, PacWest

28% 41%

CapEx per

Well CapEx per

Lateral Foot

68%

90-day IPs

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$0

$2

$4

$6

$8

$10

$12

2011 2012 2013 2014 2015

$/Hz well $/ft lateral

0

100

200

300

400

500

600

2011 2012 2013 2014 2015

Cost per horizontal well and per foot of lateral

Permian Basin

Average 90-day IPs, horizontal wells

Permian Basin

2011-15 change

14 © 2016 Halliburton. All rights reserved.

North American LTO Production

0

100

200

300

400

500

600

700

800

900

2010 2011 2012 2013 2014 2015 2016

Bakken Eagle Ford Niobrara PermianN

ew

liq

uid

s p

roductio

n p

er

rig

(th

ousands o

f barr

els

per

day)

+500% +150% +500% +200%

2010-2016

U.S. shale production has not declined at the rate of rig

count, partially driven by increased new barrels per rig

Source: EIA

New barrels per rig

Major U.S. LTO basins

15 © 2016 Halliburton. All rights reserved.

Technologies Enabling North American Shale Efficiency

Harvesting Reserves Stimulation Materials

Frac Design Surface Efficiency Reservoir Insight

16 © 2016 Halliburton. All rights reserved.

$0

$10

$20

$30

$40

$50

$60

$70

$80

2010 2011 2012 2013 2014 2015

LTO vs. Deep Water Breakeven Trends

$0

$10

$20

$30

$40

$50

$60

$70

$80

2010 2011 2012 2013 2014 2015

Bre

ake

ve

n p

rice

, $

pe

r b

arr

el

Bre

ake

ve

n p

rice

, $

pe

r b

arr

el

Source: Rystad Energy, February 2016

Deep Water

Deepwater project breakeven

by approval year

Light Tight Oil

U.S. average wellhead breakeven price

for horizontal wells by spud year

-33%

-9%

17 © 2016 Halliburton. All rights reserved.

0

5

10

15

20

25

<$20 $20-40 $40-60 $60-80 $80-100 >$100

LTO Shelf and Midwater Other Onshore Deep Water Other

Mill

ion

ba

rre

ls p

er

da

y

Light Tight Oil Expected To Be The Largest Source Of New Production in 2020

New Production By Source With Current Breakevens

Source: Rystad Energy, February 2016

19 million bpd of new supply

18 © 2016 Halliburton. All rights reserved.

0

5

10

15

20

25

<$20 $20-40 $40-60 $60-80 $80-100 >$100

LTO Shelf and Midwater Other Onshore Deep Water Other

Mill

ion

ba

rre

ls p

er

da

y

Light Tight Oil Expected To Be The Largest Source Of New Production in 2020

Mill

ion

ba

rre

ls p

er

da

y

New Production By Source With Current Breakevens New Production By Source with Continued Productivity Gains*

Source: Rystad Energy, February 2016

19 million bpd of new supply

0

5

10

15

20

25

<$20 $20-40 $40-60 $60-80 $80-100 >$100

LTO Shelf and Midwater Other Onshore Deep Water Other

19 million bpd of new supply

*Productivity assumptions include:

• 30% total cost reduction for LTO and deepwater from 2015-20

• 40% increase in production from new LTO assets

• 15% increase in production from new deep water assets

19 © 2016 Halliburton. All rights reserved.

![Incorporation of Shape Memory Polymers in Interactive DesignTable 1: Shape Memory Polymer Volumetric Mix Ratios [13] Samples Epon 826 (ml) Jeffamine D-230 (ml) NGDE (ml) T g ( C) 1](https://img.pdfslide.us/doc/110x75/5faaece21fb6cb6fb628c60b/incorporation-of-shape-memory-polymers-in-interactive-design-table-1-shape-memory.jpg)