Embed Size (px)

Citation preview

What The Credit Crunch Has What The Credit Crunch Has Brought to Northern Virginia:Brought to Northern Virginia:The Retail & Real Estate The Retail & Real Estate PerspectivePerspective

Metropolitan Washington Council of GovernmentsMetropolitan Washington Council of Governments

Metropolitan Development Policy CommitteeMetropolitan Development Policy Committee July 8, 2009July 8, 2009

2

Order of Presentation

• Introduction

• Housing

• Consumer Spending

• Retail

• Banking

• Local Government

Why the Research

• Response to information gap: Local perspective on the credit crisis given less attention

• Focus on Northern Virginia– Our view: Regional economy

weakened but better off than other regions, especially close-in areas

• Employment levels higher than national average

• Proximity to Washington, DC• Advantage: relevant data in one place

– Local governments – great asset in the research

• Intention – Data-based trend analysis and

insights for policy making– Audience: local government,

business, thought leaders

2

3

Macroeconomic Adjustment I: Unsustainable Budget Deficit

• Federal government demand for funds rising to record levels– Support of financial and auto industries– Stimulus spending– Rising interest payments and entitlements– Inevitable assistance to certain states running large deficits?

• Financing sources constrained– Competition for the global savings: upward limit on foreign investment in U.S. debt – Rising U.S. savings rate from low level

• One rough estimate: Federal Government on pace to absorb 90% of savings pool

• Federal government competing with corporate, mortgage, consumer borrowers = upward pressure on rates without continued Fed intervention

4

Macroeconomic Adjustment 2:Consumer Behavior Shift

• Consumer spending led economic growth until the recession

• New dynamic: savings rate grows, consumer debt slows

• Consumer spending no longer counted on as dominant economic growth driver– Negative wealth effect– Employment anxiety– Probability of rising aggregate tax levels– Less Available Credit + Shift in Consumer Savings/Debt Attitude = Deleveraged Consumer

5

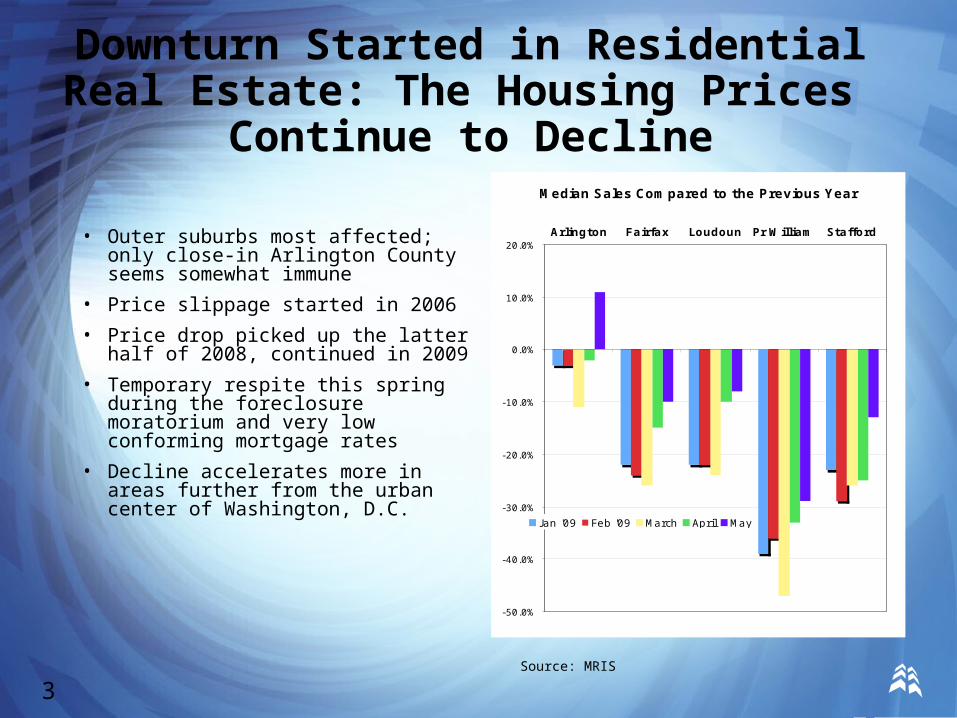

Downturn Started in Residential Real Estate: The Housing Prices

Continue to Decline

• Outer suburbs most affected; only close-in Arlington County seems somewhat immune

• Price slippage started in 2006

• Price drop picked up the latter half of 2008, continued in 2009

• Temporary respite this spring during the foreclosure moratorium and very low conforming mortgage rates

• Decline accelerates more in areas further from the urban center of Washington, D.C.

3Source: MRIS

Median Sales Compared to the Previous Year

-50.0%

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%Arlington Fairfax Loudoun Pr William Stafford

Jan '09 Feb '09 March April May

6

Residential Property Tax Assessments Fall in Line

• Sales prices falling more than anticipated

• Commercial assessments now declining as well.

• Steeper assessment declines on the way?

Notes: Assessments based on most recent county reports as of May 2009 and MRIS for median price change

4

Average Residential Assessment Value Change Compared to Median Price Change -

J an-May 2009

- 40.0%

- 35.0%

- 30.0%

- 25.0%

- 20.0%

- 15.0%

- 10.0%

- 5.0%

0.0%Arlington Fairfax Loudoun Pr William

CY2009 Assessment Change

Median. Sales Price Change J an- May'09

7

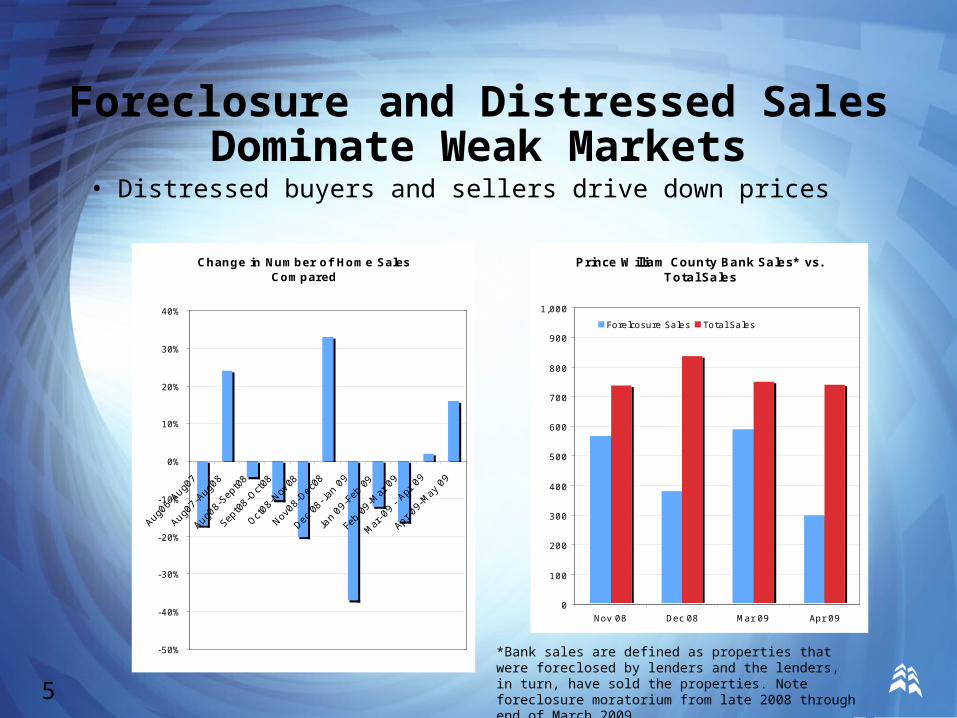

Foreclosure and Distressed Sales Dominate Weak Markets

• Distressed buyers and sellers drive down prices

*Bank sales are defined as properties that were foreclosed by lenders and the lenders, in turn, have sold the properties. Note foreclosure moratorium from late 2008 through end of March 2009.5

Source: MRIS

Change in Number of Home Sales Compared

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

Aug0

6-Au

g07

Aug0

7-Au

g08

Aug0

8-Se

pt08

Sept

08-O

ct08

Oct08

-Nov

08

Nov08

-Dec

08

Dec 0

8-Ja

n 09

Jan

09-F

eb 0

9

Feb

09-M

ar 0

9

Mar

-09

- Ap

r 09

Apr 0

9-May

09

Prince William County Bank Sales* vs. Total Sales

0

100

200

300

400

500

600

700

800

900

1,000

Nov 08 Dec 08 Mar 09 Apr 09

Forelcosure Sales Total Sales

8

Foreclosures and Distressed Properties Rising

• Foreclosures increased significantly since mid-May, following the moratorium

– Incidence of foreclosures especially high in outlying areas: Using Realty Trac data prior to the moratorium effect, foreclosure actions increased from 2006 to 2008 (through October) as % of assessed residential properties

• Fairfax County: 0.2% to 2.6%

• Loudoun County: 0.3% to 3.1%

• Prince William County: 0.5% to 7.6%

• Rising delinquencies and falling prices lead to additional foreclosures and distressed properties

– More than 45% subprime mortgages and 25% Alt-A in Virginia delinquent as of Mar 31 according to CoreLogic data

– Nearly one in five mortgaged properties “upside down” or negative equity as of year-end 2008.

Negative Equity in Virginia - Properties Outstanding

MortgagesNegative Equity

MortgagesNear** Negative

Equity Mortgages Negative Equity ShareNear** Negative

Equity ShareOct '08 1,110,253 177,005 238,414 15.9% 21.5%Dec '08 1,118,334 219,282 280,759 19.6% 25.1%Note: This data only includes properties with a mortgage. Non-mortgaged properties are by definition not included.** Defined as properties within 5% of being in a negative equity position.Source: First American CoreLogic

6

Foreclosures Surging Post-Moratorium

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

5/15/2008 6/11/2009

9

Negative and Near-Negative Equity in Mortgaged Properties by State and Nationally

Year-End 2008

7

State Mortgages

Negative Equity

Mortgages

Near** Negative Equity

Mortgages

Negative Equity Share

Near** Negative Equity Share State Mortgages

Negative Equity

Mortgages

Near** Negative Equity

MortgagesNegative

Equity Share

Near** Negative

Equity Share

Alabama 243,474 20,626 34,934 8.5% 14.3% Nebraska 181,129 30,116 45,079 16.6% 24.9%

Alaska 72,987 9,730 13,379 13.3% 18.3% Nevada 608,374 335,340 359,117 55.1% 59.0%

Arizona 1,283,174 407,604 477,244 31.8% 37.2% New Hampshire 164,082 33,536 44,700 20.4% 27.2%

Arkansas 171,577 28,685 45,496 16.7% 26.5% New Jersey 1,744,333 168,915 227,923 9.7% 13.1%

California 6,452,766 1,901,066 2,174,955 29.5% 33.7% New Mexico 186,500 15,329 21,770 8.2% 11.7%

Colorado 1,048,437 225,074 292,840 21.5% 27.9% New York 1,554,395 73,811 111,765 4.7% 7.2%

Connecticut 682,719 62,260 87,017 9.1% 12.7% North Carolina 1,197,288 134,508 218,655 11.2% 18.3%

Delaware 147,900 16,700 23,617 11.3% 16.0% North Dakota NA NA NA NA NA

Florida 4,245,623 1,284,679 1,479,234 30.3% 34.8% Ohio 1,888,878 435,107 567,344 23.0% 30.0%

Georgia 1,458,185 335,668 470,216 23.0% 32.2% Oklahoma 308,095 33,779 62,323 11.0% 20.2%

Hawaii 202,226 12,627 17,225 6.2% 8.5% Oregon 647,059 57,446 80,632 8.9% 12.5%

Idaho 191,050 26,993 35,292 14.1% 18.5% Pennsylvania 1,407,328 88,274 132,719 6.3% 9.4%

Illinois 2,075,097 236,936 332,261 11.4% 16.0% Rhode Island 205,881 32,357 41,192 15.7% 20.0%

Indiana 408,062 55,004 77,353 13.5% 19.0% South Carolina 459,705 53,770 83,745 11.7% 18.2%

Iowa 210,620 39,194 60,385 18.6% 28.7% South Dakota NA NA NA NA NA

Kansas 200,728 35,212 47,941 17.5% 23.9% Tennessee 728,981 119,442 174,487 16.4% 23.9%

Kentucky 205,813 31,393 49,734 15.3% 24.2% Texas 2,776,017 497,361 677,397 17.9% 24.4%

Louisiana 124,980 16,186 21,849 13.0% 17.5% Utah 418,176 56,763 74,770 13.6% 17.9%

Maine NA NA NA NA NA Vermont NA NA NA NA NA

Maryland 1,308,860 170,849 228,615 13.1% 17.5% Virginia 1,118,334 219,282 280,759 19.6% 25.1%

Massachusetts 1,393,027 151,750 205,524 10.9% 14.8% Washington 1,280,834 125,992 173,891 9.8% 13.6%

Michigan 1,149,588 459,385 549,672 40.0% 47.8% Washington, DC 99,973 14,915 19,216 14.9% 19.2%

Minnesota 442,040 64,643 87,183 14.6% 19.7% West Virginia NA NA NA NA NA

Mississippi NA NA NA NA NA Wisconsin 428,027 69,414 94,991 16.2% 22.2%

Missouri 664,563 100,507 135,161 15.1% 20.3% Wyoming NA NA NA NA NA

Montana 87,671 6,570 9,164 7.5% 10.5% Nation 41,958,989 8,311,496 10,471,519 19.8% 25.0%

* This data only includes properties with a mortgage as of December 2008. Non-mortgaged properties are by definition not included.

** Defined as properties within 5% of being in a negative equity position.

Source: First Americn Core Logic

10

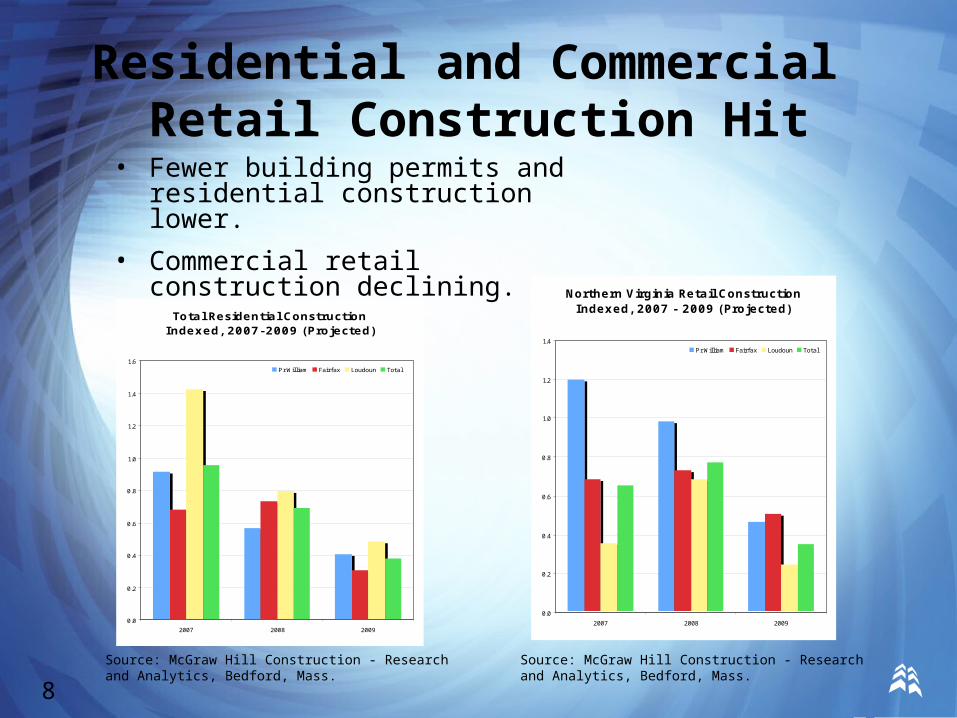

Residential and Commercial Retail Construction Hit

• Fewer building permits and residential construction lower.

• Commercial retail construction declining.

8

Source: McGraw Hill Construction - Research and Analytics, Bedford, Mass.

Source: McGraw Hill Construction - Research and Analytics, Bedford, Mass.

Total Residential Construction Indexed, 2007-2009 (Projected)

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

2007 2008 2009

Pr William Fairfax Loudoun Total2006=1

Northern Virginia Retail Construction Indexed, 2007 - 2009 (Projected)

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

2007 2008 2009

Pr William Fairfax Loudoun Total2006=1

11

Auto Sales: Example of Credit Crunch Effect on Consumer

Spending• Similar to housing, other consumer purchases drop, especially those that are

credit-dependent

• Example: Northern Virginia new auto sales – fall in sales accelerated in latter part of year and early 2009, especially domestic autos. April-May declines slowed by domestic auto dealer inventory liquidation

9Source: Virginia Auto Dealers Association Source: Virginia Auto Dealers Association

Market Share Compared to Year Ago

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

Mar 08 Mar 09

Domestic Imported

Change in Auto Sales Compared to a Year Ago

-60.0%

-50.0%

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

J an 09 Feb 09 Mar 09 Apr 09 May 09

12

Taxable Sales Fall More in Markets Distant from Washington, D.C.

-25.00%

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

ArlingtonCounty

Fairfax County Mannassas

Change in Taxable Sales, 2007-09

Less Consumer Spending Slows Demand For Retail Space

13

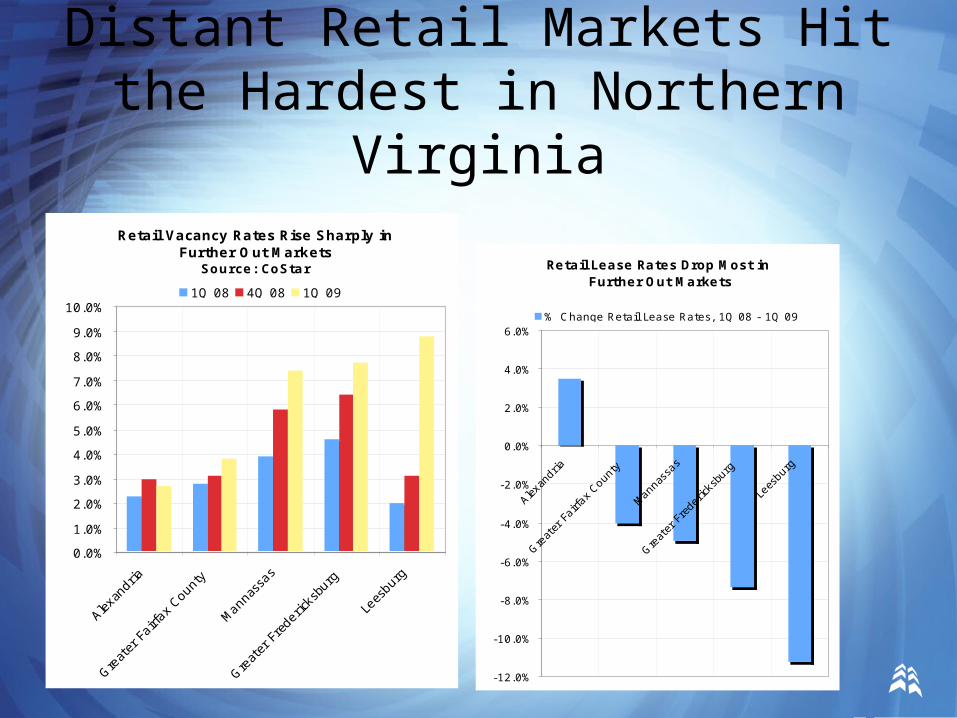

Distant Retail Markets Hit the Hardest in Northern Virginia

Retail Vacancy Rates Rise Sharply in Further Out Markets

Source: CoStar

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

Alexan

dria

Great

er F

airfa

x Cou

nty

Manna

ssas

Great

er F

rede

ricks

burg

Lees

burg

1Q 08 4Q 08 1Q 09

Retail Lease Rates Drop Most in Further Out Markets

-12.0%

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

Alexan

dria

Great

er F

airfa

x Cou

nty

Manna

ssas

Great

er F

rede

ricks

burg

Lees

burg

% Change Retail Lease Rates, 1Q 08 - 1Q 09

14

Distant Retail Markets Also Hit the Hardest Region Wide

Retail Vacancy Rates Rise in Further Out Markets

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

CapitalHill

Beth-ChevyChase

D.C.Metro

Region

St.Mary'sCounty

NorthPrince

GeorgesCounty

1Q 08 1Q 09

15

Economic Downturn Weakens Regional Office Market

Office Vacancy Rates Show Same Pattern, Especially in Further Out Markets

0.0%2.0%4.0%6.0%8.0%

10.0%12.0%14.0%16.0%18.0%20.0%

Alexan

dria

Dulles

Cor

ridor

Downt

own

D.C.

Bethe

sda-

Chevy

Cha

se

North

Prin

ce G

eorg

es C

ount

y

2Q 07 2Q 09

16

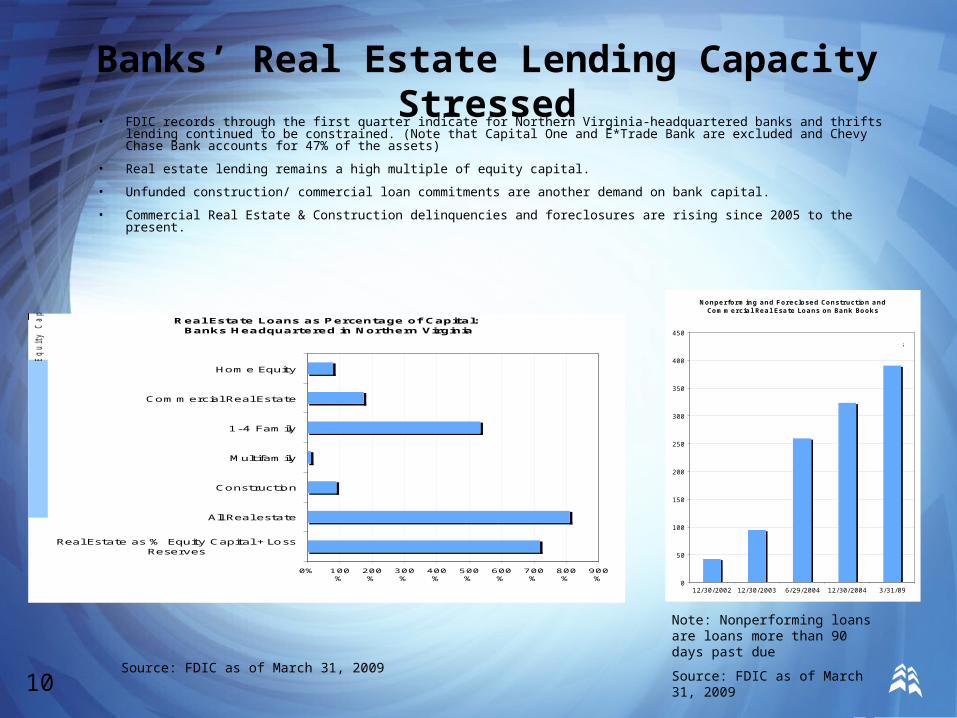

Banks’ Real Estate Lending Capacity Stressed• FDIC records through the first quarter indicate for Northern Virginia-headquartered banks and thrifts lending continued to

be constrained. (Note that Capital One and E*Trade Bank are excluded and Chevy Chase Bank accounts for 47% of the assets)

• Real estate lending remains a high multiple of equity capital.

• Unfunded construction/ commercial loan commitments are another demand on bank capital.

• Commercial Real Estate & Construction delinquencies and foreclosures are rising since 2005 to the present.

10

Note: Nonperforming loans are loans more than 90 days past due

Source: FDIC as of March 31, 2009Source: FDIC as of March 31, 2009

Real Estate Loans as Percentage of Capital: Banks Headquartered in Northern Virginia

0% 100%

200%

300%

400%

500%

600%

700%

800%

900%

Real Estate as % Equity Capital +LossReserves

All Real estate

Construction

Multifamily

1-4 Family

Commercial Real Estate

Home Equity

Rea

l E

sta

te

Lo

an

s a

s a

%

o

f E

qu

ity

C

ap

ita

l

Nonperforming and Foreclosed Construction and Commercial Real Esate Loans on Bank Books

0

50

100

150

200

250

300

350

400

450

12/30/2002 12/30/2003 6/29/2004 12/30/2004 3/31/09

in $ millions

17

Local Government Feels the Heat

• Counties are making plans for budget cuts this fiscal year, in some cases severe

– Bigger cuts this fiscal year (FY ’10)

– Local government revenue base closely tied to real estate

– Recordation taxes lower this fiscal year; some jurisdictions budget increase in FY ’10 assuming more distressed/foreclosure sales

11

Decline in Recordation Taxes: FY 09

-16.0%

-14.0%

-12.0%

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%Fairfax Loudoun

PrinceWilliam

18

Property Taxes – Major Source of Local Government Revenues

• Property taxes, on average, make up over 60 percent of the local revenue base and residential assessments, on average, make up over 70 percent of the property tax base.

12

Tax Rate Percentage Change vs. Average Sales Price Change

- 40.0%

- 30.0%

- 20.0%

- 10.0%

0.0%

10.0%

20.0%

30.0%

Arlington Fairfax Loudoun Prince William

% Increase in Property Tax Rate FY10 Decrease in Avg. Median Sales Price - Jan-May 09

19

Sales Tax Revenues Lower in CY 2008 and 2009

• Sales taxes are another important local government revenue source.• Recession has slowed sales tax revenues and the impact is greater

this year.

13 Source: Commonwealth of Virginia

Sales Tax Declines in Selected Counties

-1.9%

-1.0%

-2.0%

-0.4%

-4.3%

-9.0%

-10.0% -8.0% -6.0% -4.0% -2.0% 0.0%

Prince William

Loudoun

Fairfax

2007 to 2008 J an-Apr '08 to J an-Apr 09 (Average of the Four Months)

20

Summary• Northern Virginia in better economic shape than other regions but credit crunch has

significant effects at the local level – most negative in further out jurisdictions.

• Regional economic deterioration started with residential real estate - still in decline: prices dropping, delinquencies rising - distressed sellers major driver of the market.

• Consumer credit pulled back, cuts retail spending, outlook for commercial retail properties and demand for retail construction.

• Biggest effect on commercial real estate markets furthest away from Washington, DC center.

• Eventual recovery will be from a lower base.

• Local government revenues primarily real estate dependent - downward trend continuing, accelerating in FY 10.

• No easy choices, economic pain - public policy response critical variable.

16