Embed Size (px)

Citation preview

Fiscal Management of Federal Awards

1

Wisconsin Department of Public Instruction

Overview

States’ responsibility to provide fiscal oversight of federal funds that they grant to sub-recipients

2

federal funds that they grant to sub recipients

Federal grants and the requirements have been around for decades

At times LEAs do not comply with certain federal At times LEAs do not comply with certain federal fiscal requirements because they are unaware of them and unaware of the potential loss of funds

Wisconsin Department of Public Instruction

Overview

This training is intended to: Focus on overall fiscal management of the federal

3

Focus on overall fiscal management of the federal funds

This training does not address: All areas of grant management

Specific federal program requirements that accompany every grant

General accounting principles

Wisconsin Department of Public Instruction

What requirements apply t f d l t to federal grants management and where are they found?

Requirements that Apply to Federal Grants

OFFICE OF MANAGEMENT AND BUDGET (OMB)

Established uniform procedures for the

5

Established uniform procedures for the use of federal funds

Wisconsin Department of Public Instruction

Uniform Administrative

6

Uniform Administrative Requirements, Cost Principles and

Audit Requirements for Federal Grants

http://www.gpo.gov/fdsys/pkg/FR-2013-12-26/pdf/2013-30465.pdf

Wisconsin Department of Public Instruction

Requirements that Apply to Federal Grants

7

Office of Management and Budget Circulars

http://www.whitehouse.gov/omb/circulars_default/ OMB Circular A-87 - Cost Principles

OMB Circular A-102 - Common rule

OMB Circular A-133 - Audit State/Local

OMB Circular A-133 - Compliance Supplement

Wisconsin Department of Public Instruction

Requirements that Apply to Federal Grants

Federal Register- official journal of the federal government

8

- official journal of the federal government- contains publications and public notices of government agencies

Code of Federal Regulations (CFR)- Codification of the general and permanent rules Cod ca o o e ge e a a d pe a e u esand regulations published in the federal registerhttp://ecfr.gpoaccess.gov/cgi/t/text/text-idx?sid=b248f3949e2c06c722742aeb38c17562&c=ecfr&tpl=/ecfrbrowse/Title34/34tab_02.tpl

Wisconsin Department of Public Instruction

Requirements that Apply to Federal Grants

Education Department General Administrative Regulations (EDGAR)

9

Regulations (EDGAR)Title 34 (Education), CFR, Parts 74-86 and 97-99http://www2.ed.gov/policy/fund/reg/edgarReg/edgar.html

- regulations for administering discretionary and formula grants awarded by the departmentg y p

Wisconsin Department of Public Instruction

Requirements that Apply to Federal Grants

Administration Office of Management and Budget (OMB) Circular A

10

Office of Management and Budget (OMB) Circular A-102 Common ruleIdentify the administrative systems and procedures

that must be in place to receive, expend, account for and report on the uses of federal funds

34 CFR part 80 incorporates OMB Circular A-10234 CFR part 80 incorporates OMB Circular A 102

EDGAR Title 34 (Education), CFR, Part 80Establishes uniform administrative rules for federal

grants to state, local and Indian tribal governments

Wisconsin Department of Public Instruction

Requirements that Apply to Federal Grants

Management

11

Management EDGAR Title 34 (Education), CFR Part 76 State-

Administered Programs

How funds are to be distributed to LEAs

Program or fiscal conditions that must be met on the state/local level

Wh bli ti dWhen obligations are made

How grant recipients are accountable for fiscal reporting and for the reporting of the program

Wisconsin Department of Public Instruction

Requirements that Apply to Federal Grants

Cost Principles

12

Cost Principles OMB Circular A-87

Identify how federal funds can be expended

Wisconsin Department of Public Instruction

Reform to OMB Circulars

Super-Circular or Omni-CircularSt li i t f 8 OMB Ci l

13

Streamlines requirements from 8 OMB Circulars

Final version issued December 26, 2013

Effective for 2015-16 fiscal school year

Wisconsin Department of Public Instruction

Education Department General Administrative Regulations (EDGAR)

Title 34 CFR Part 80.20

(a)Fiscal control and accounting procedures must be

14

(a)Fiscal control and accounting procedures must be sufficient to: (1) Permit preparation of reports required

(2) Permit tracing of funds to a level of expenditures adequate to establish that such funds have not been used in violation of the applicable standards.

Wisconsin Department of Public Instruction

Education Department General Administrative Regulations (EDGAR)

(b)The financial management systems must meet the following standards:

15

following standards: Financial Reporting

Accounting Records

Internal Control

Budget Control

Allowable Cost

S D t ti Source Documentation

Cash Management

Wisconsin Department of Public Instruction

Education Department General Administrative Regulations (EDGAR)

(c)’An awarding agency may review the adequacy of the financial management system of any applicant

16

the financial management system of any applicant for financial assistance as part of a preaward review or at any time subsequent to award.’

Wisconsin Department of Public Instruction

Financial Reporting

“Accurate, current, and complete di l f th fi i l lt f

17

disclosure of the financial results of financially assisted activities must be made in accordance with the financial reporting requirements of the grant or subgrant ”subgrant.

Wisconsin Department of Public Instruction

Financial Reporting

Individuals who prepare, review and approve reports possess knowledge, skills and abilities necessary

18

possess knowledge, skills and abilities necessary

Written policies and procedures to establish responsibilities and ensure proper monitoring, verification and reporting

Review and approval of reports by appropriate individual prior to submission (separate from p ( ppreparer)

Accounting system set up to provide the financial information as needed for reporting

Wisconsin Department of Public Instruction

Accounting Records

“Grantees and subgrantees must maintain records which adequately identify the

19

records which adequately identify the source and application of funds provided for financially-assisted activities. These records must contain information pertaining to grant or subgrant awards and authorizations, obligations, unobligated balances, assets, liabilities, outlays or expenditures, and income.”

Wisconsin Department of Public Instruction

Accounting Records

The foundation of fiscal management of a federal grant is the grant’s accounting record

20

Common errors LEA does not create an accounting record for each grant and post

expenditures to that account. Rather the LEA just identifies expenditures for grant reimbursement

Expenditures are originally reported to a general account and later reclassified

Accounting records do not integrate and track against the grant’s d b d tapproved budget

Accounting record cannot be used for budget control when expenditures are not posted to the grant as they occur and when they are not tracked against an approved budget

Wisconsin Department of Public Instruction

Accounting Records

An accounting record that incorporates the amount of the award and approved budget At a minimum

21

of the award and approved budget. At a minimum each general area of planned expenditures

Provisions should be made to track expenditures and available balances against each budget line to exercise budget control

An accounting system that provides separate An accounting system that provides separate identification of federal and non-federal transactions and allocation transactions applicable to both

Wisconsin Department of Public Instruction

Accounting Records

Reports provided timely to administration or governance board for review and appropriate

22

governance board for review and appropriate action

Easy access to accurate information on grant expenditures and comparison to grant budget and claims

Recording of expenditures to appropriate account Recording of expenditures to appropriate account when incurred to assist with budget control

Wisconsin Department of Public Instruction

Tracking Expenditures

Wisconsin Uniform Financial Accounting Requirements (WUFAR)

23

q ( ) Used for reporting to DPI Object

Service or commodity acquired Salaries, fringe benefits, purchased services, non-capital objects,

capital objects, insurance and judgments

Function Purpose for which an object is used Purpose for which an object is used Instruction, support services

Project Identify the activity IDEA, Title I, special education state aid

Wisconsin Department of Public Instruction

Accounting Records

Per EDGAR) §76.730 LEA shall keep records that fully show:

24

fully show: Amount of funds under the grant

How the funds will be used

Total cost of the project

Share of the cost provided from other sources

Other records to facilitate an effective audit

Wisconsin Department of Public Instruction

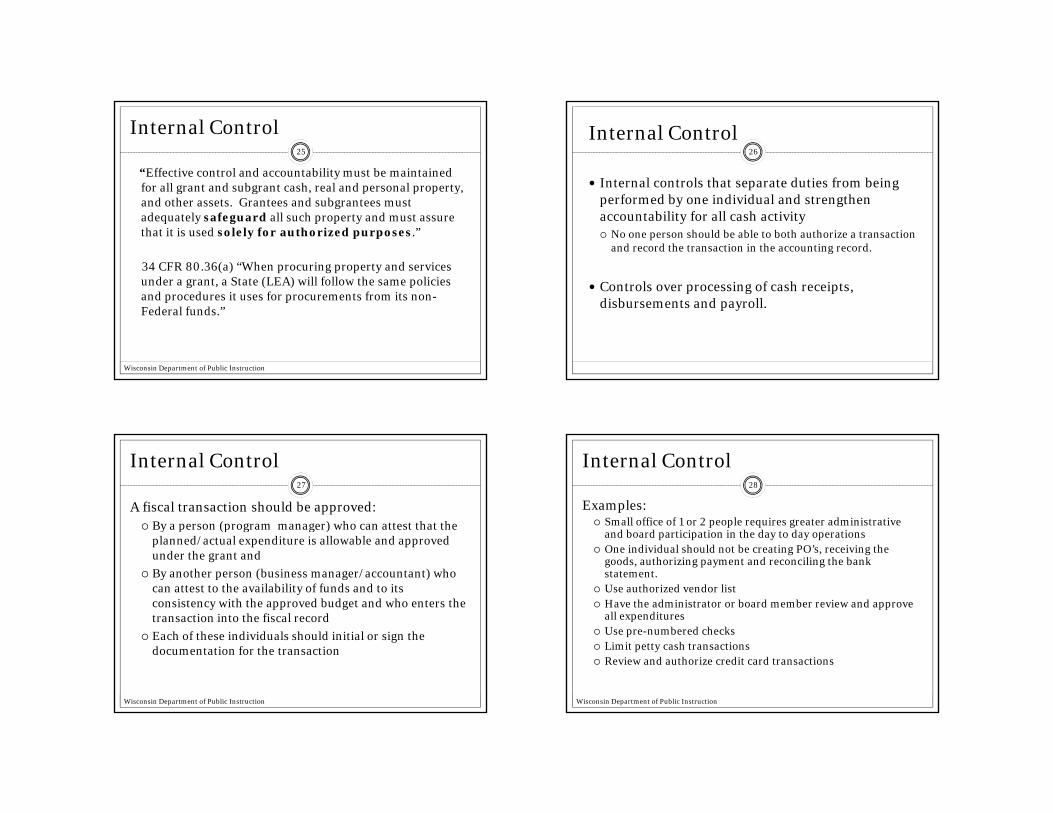

Internal Control

“Effective control and accountability must be maintained for all grant and subgrant cash, real and personal property,

25

g g p p p yand other assets. Grantees and subgrantees must adequately safeguard all such property and must assure that it is used solely for authorized purposes.”

34 CFR 80.36(a) “When procuring property and services under a grant, a State (LEA) will follow the same policies g , ( ) pand procedures it uses for procurements from its non-Federal funds.”

Wisconsin Department of Public Instruction

Internal Control

Internal controls that separate duties from being f d b d d l d h

26

performed by one individual and strengthen accountability for all cash activity No one person should be able to both authorize a transaction

and record the transaction in the accounting record.

Controls over processing of cash receipts Controls over processing of cash receipts, disbursements and payroll.

Internal Control

A fiscal transaction should be approved: By a person (program manager) who can attest that the

27

By a person (program manager) who can attest that the planned/actual expenditure is allowable and approved under the grant and

By another person (business manager/accountant) who can attest to the availability of funds and to its consistency with the approved budget and who enters the transaction into the fiscal recordtransaction into the fiscal record

Each of these individuals should initial or sign the documentation for the transaction

Wisconsin Department of Public Instruction

Internal Control

Examples: Small office of 1 or 2 people requires greater administrative

28

p p q gand board participation in the day to day operations

One individual should not be creating PO’s, receiving the goods, authorizing payment and reconciling the bank statement.

Use authorized vendor list Have the administrator or board member review and approve

all expendituresp Use pre-numbered checks Limit petty cash transactions Review and authorize credit card transactions

Wisconsin Department of Public Instruction

Internal Control

Common errors:

W itt li th t i

29

Written policy that is:Non-existent

Outdated

Not being implemented

Do not document the review of fiscal transactions by two peopleby two people

Do not routinely require approval of or posting of expenditures

Wisconsin Department of Public Instruction

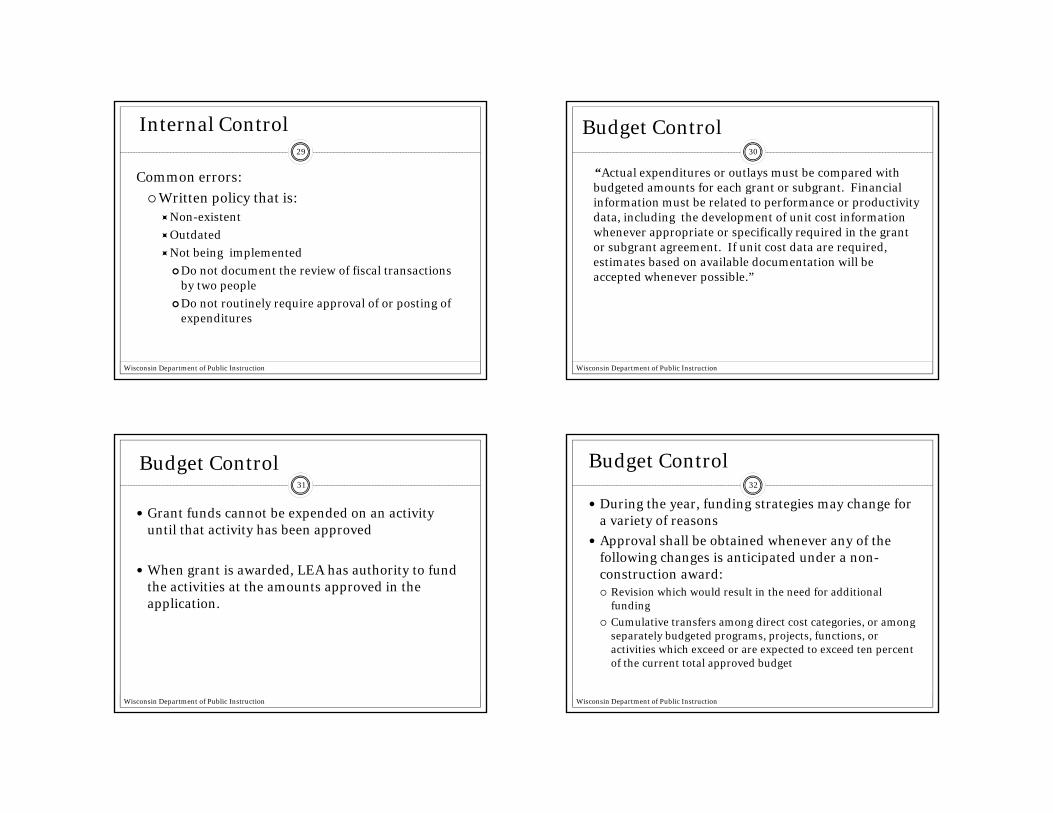

Budget Control

“Actual expenditures or outlays must be compared with budgeted amounts for each grant or subgrant. Financial

30

g g ginformation must be related to performance or productivity data, including the development of unit cost information whenever appropriate or specifically required in the grant or subgrant agreement. If unit cost data are required, estimates based on available documentation will be accepted whenever possible.”

Wisconsin Department of Public Instruction

Budget Control

Grant funds cannot be expended on an activity til th t ti it h b d

31

until that activity has been approved

When grant is awarded, LEA has authority to fund the activities at the amounts approved in the application.

Wisconsin Department of Public Instruction

Budget Control

During the year, funding strategies may change for a variety of reasons

32

y

Approval shall be obtained whenever any of the following changes is anticipated under a non-construction award: Revision which would result in the need for additional

funding

Cumulative transfers among direct cost categories or among Cumulative transfers among direct cost categories, or among separately budgeted programs, projects, functions, or activities which exceed or are expected to exceed ten percent of the current total approved budget

Wisconsin Department of Public Instruction

Budget Control

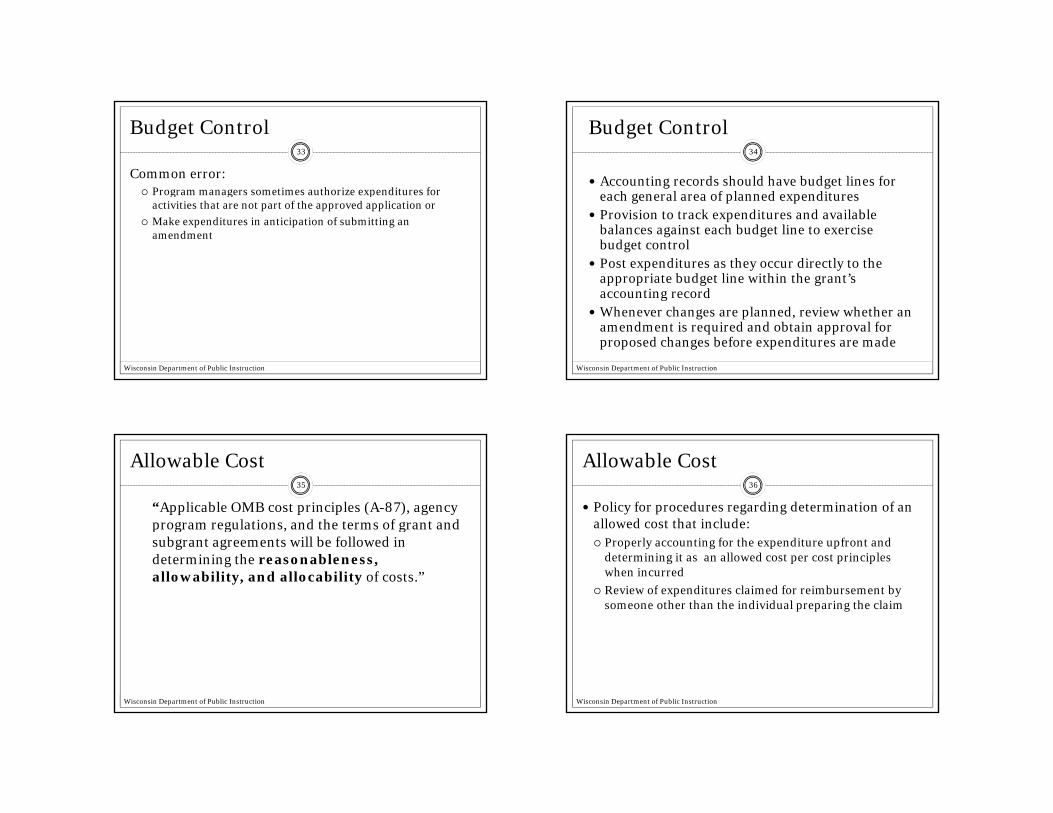

Common error: Program managers sometimes authorize expenditures for

33

Program managers sometimes authorize expenditures for activities that are not part of the approved application or

Make expenditures in anticipation of submitting an amendment

Wisconsin Department of Public Instruction

Budget Control

Accounting records should have budget lines for h l f l d dit

34

each general area of planned expenditures Provision to track expenditures and available

balances against each budget line to exercise budget control

Post expenditures as they occur directly to the appropriate budget line within the grant’s accounting record

Whenever changes are planned, review whether an amendment is required and obtain approval for proposed changes before expenditures are made

Wisconsin Department of Public Instruction

Allowable Cost

“Applicable OMB cost principles (A-87), agency program regulations and the terms of grant and

35

program regulations, and the terms of grant and subgrant agreements will be followed in determining the reasonableness, allowability, and allocability of costs.”

Wisconsin Department of Public Instruction

Allowable Cost

Policy for procedures regarding determination of an allowed cost that include:

36

allowed cost that include: Properly accounting for the expenditure upfront and

determining it as an allowed cost per cost principles when incurred

Review of expenditures claimed for reimbursement by someone other than the individual preparing the claim

Wisconsin Department of Public Instruction

Allowable Cost

Common error: Salaries and Wages - no process in place for time and

37

g p peffort reporting

Employees that are expected to work solely on a single federal award or cost objective supported by periodic certifications that the employee worked solely on that program for period covered by certification

Employees that work on multiple activities or cost objectives supported by personnel activity reports or equivalent documentation

Wisconsin Department of Public Instruction

Source Documentation

“Accounting records must be supported by such source documentation as cancelled checks

38

source documentation as cancelled checks, paid bills, payrolls, time and attendance records, contract and subgrant award documents, etc.”

Wisconsin Department of Public Instruction

Source Documentation

Policies and procedures:Periodic certifications or personnel activity

39

Periodic certifications or personnel activity reports

Adequate source documentation to support amounts and items reported

All goods or services are initiated, approved and paid for through the established disbursement internal controls which should include a purchase order, packing slip if applicable, invoice and school check or electronic transfer

Wisconsin Department of Public Instruction

Cash Management

“Procedures for minimizing the time elapsing between the transfer of funds from the U.S.

40

Treasury and disbursement by grantees and subgrantees must be followed whenever advance payment procedures are used. Grantees must establish reasonable procedures to ensure the receipt of reports on subgrantees’ cash balances and cash disbursements in sufficient time to enable them to prepare complete and accurate cash transactions reports to the awarding agency. When advances…”

Wisconsin Department of Public Instruction

Cash Management

Basic standard – methods and procedures for payment shall minimize the time lapsing between

41

payment shall minimize the time lapsing between the transfer of funds and disbursement by the school

No expenditure may be claimed for reimbursement unless it is obligated

Report expenditures on a timely basis

Wisconsin Department of Public Instruction

EDGAR §76.707When Obligations are MadeIf the obligation is for - The obligation is made -

(a) Acquisition of real or personal property On the date on which the school makes a binding written commitment to acquire the property

42

property.

(b) Personal services by an employee of the school

When the services are performed.

(c) Personal services by a contractor who is not an employee of the school

On the date on which the school makes a binding written commitment to obtain the services

(d) Performance of work other than personal services

On the date on which the school makes a binding written commitment to obtain the work.

(e) Public utility services When the school receives the services

(f) Travel When the travel is taken.

(g) Rental of real or personal property When the school uses the property.

(h) A pre-agreement cost that was properly approved by the State under the cost principles identified in 34 CFR 74.171 and 80.22.

COST REIMBURSED BY A FEDERAL AWARD AND AUDITED UNDER OMB CIRCULAR A-133

43

General Federal Award GuidanceGeneral Federal Award Guidance

http://sms.dpi.wi.gov/sms_fedaids

Wisconsin Department of Public Instruction

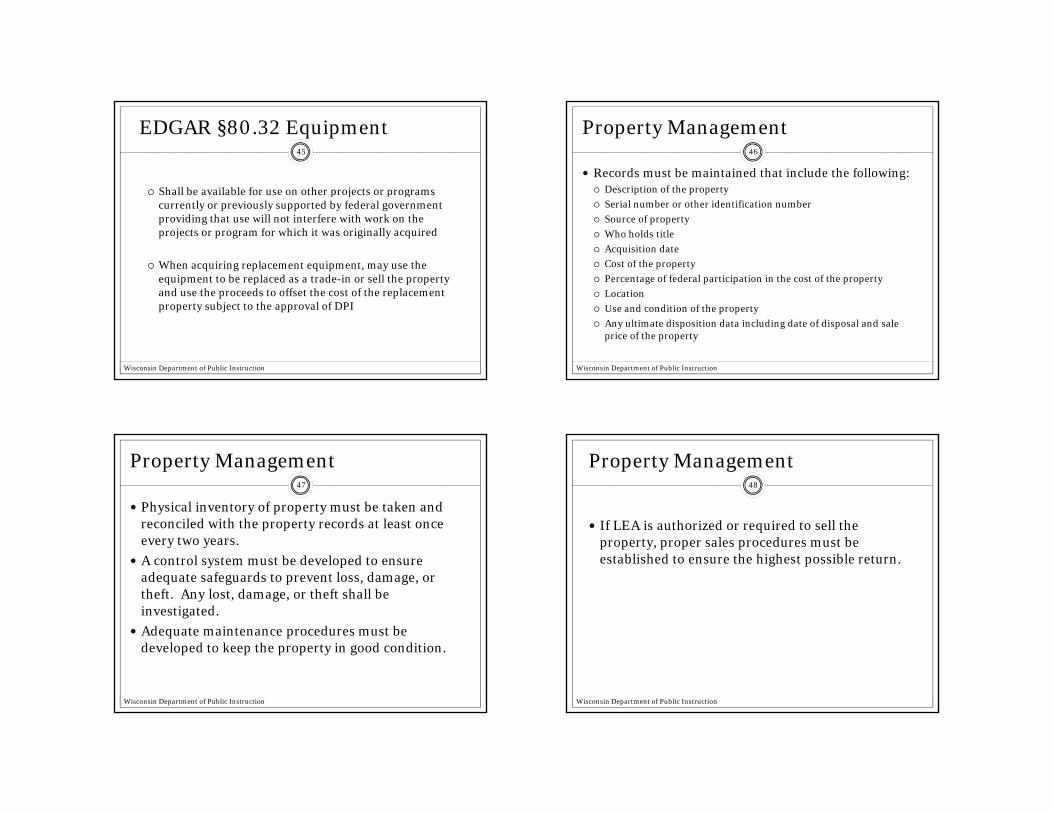

EDGAR §80.32 Equipment

May be used in the program or project for which acquired as

44

long as needed, whether or not the project or program continues to be supported by federal funds

When no longer needed may be used in other activities currently or previously supported by a federal agency

Wisconsin Department of Public Instruction

EDGAR §80.32 Equipment

Shall be available for use on other projects or programs

45

Shall be available for use on other projects or programs currently or previously supported by federal government providing that use will not interfere with work on the projects or program for which it was originally acquired

When acquiring replacement equipment, may use the equipment to be replaced as a trade-in or sell the property and use the proceeds to offset the cost of the replacement property subject to the approval of DPI

Wisconsin Department of Public Instruction

Property Management

Records must be maintained that include the following: Description of the property

46

p p p y

Serial number or other identification number

Source of property

Who holds title

Acquisition date

Cost of the property

Percentage of federal participation in the cost of the property

Location

Use and condition of the property

Any ultimate disposition data including date of disposal and sale price of the property

Wisconsin Department of Public Instruction

Property Management

Physical inventory of property must be taken and reconciled with the property records at least once

47

reconciled with the property records at least once every two years.

A control system must be developed to ensure adequate safeguards to prevent loss, damage, or theft. Any lost, damage, or theft shall be investigated.

Adequate maintenance procedures must be developed to keep the property in good condition.

Wisconsin Department of Public Instruction

Property Management

If LEA is authorized or required to sell the

48

If LEA is authorized or required to sell the property, proper sales procedures must be established to ensure the highest possible return.

Wisconsin Department of Public Instruction

Property Management

When original or replacement equipment acquired under a grant is no longer needed for original project or program or

49

grant is no longer needed for original project or program or for other activities currently or previously supported by a federal agency, disposition of the equipment will be made as follows: 1) Current fair market value < $5,000 may be retained, sold or

disposed of with no further obligation to the federal government.

2) Current fair market value > $5 000 may be retained or sold 2) Current fair market value > $5,000 may be retained or sold and the federal government shall have a right to an amount calculated by multiplying the current market value or proceeds from sale by the federal share of the equipment.

Wisconsin Department of Public Instruction

What happens when your management system does not meet the standards set forth in 34 CFR Part 80 of EDGAR?

•Funds May Be Withheld

•Placed On High Risk

Part 80 of EDGAR? 50

Wisconsin Department of Public Instruction

Review of reports

Comparison of : Financial Annual Report

51

p Source 730, fund 27

Special Education Annual Report Project code 340

IDEA Claims

Comparison to: Source 730 to Claims Source 730 to Claims

Source 730 to 340 project codes

340 project codes to claims

Wisconsin Department of Public Instruction

How can these impact LEA’s Aid and Calculation of MOE?

Understate or overstate the amount of state and

52

local or local expenditures used to determine compliance with MOE

Can result in being paid for a cost by both IDEA and special education state categorical aid

Can result in being underpaid on state categorical g p gaid

Wisconsin Department of Public Instruction

How can the incorrect amount of local expenditures impact MOE?

Fund 27 Fund 27 Report Fund 10 Revenue and Fund 10

Report Fund 27 Revenue

Report Fund 10 Revenue

53

and Fund 10 Expenditure in Fund 27

Revenue in Fund 10

Revenue in Fund 27

Expenditures $500,000 $550,000 $500,000 $500,000

Revenues $400,000 $450,000 $350,000 $450,000

Transfer from Fund 10(Local Expenditures)

$100,000 $100,000 $150,000 $50,000

Review of reports

CEIS

Reported both the revenue and expenditures for CEIS

54

Reported both the revenue and expenditures for CEIS in fund 27.

Reported only the CEIS revenue in fund 27 (no expenditures)

Results

i l d i d h ld b d iCEIS is general education and should be reported in fund 10

Understates local expenditures for MOE

Wisconsin Department of Public Instruction

Review of reports

Indirect:

Reported it on the claims and as revenue in fund 27, but

55

Reported it on the claims and as revenue in fund 27, but did not include a cost in fund 27

Reported indirect cost in fund 27 as a transfer from fund 10 (function 418000)

Result:

d l l di f Understates local expenditures for MOE

Correct

Wisconsin Department of Public Instruction

Review of reports

Claimed or underclaimed 340

Claimed more than what was reported as a 340 project in

56

Claimed more than what was reported as a 340 project in the special education report

Reported more in the 340 project than was in the claims

Results

May be double dipping and overstated local or state and l l di flocal expenditures for MOE

Understated local or state and local expenditures for MOE

Wisconsin Department of Public Instruction

Review of reports

Schoolwide

Reported schoolwide revenue and expenditures in fund

57

Reported schoolwide revenue and expenditures in fund 27

Reported only the schoolwide revenue in fund 27 (not the expenditures)

Results

f l d i i h ld b i f d If general education services should be in fund 10

Understated local expenditures for MOE

Wisconsin Department of Public Instruction

Review of reports

Revenue in source 730

Year end Receivable not reported

58

Year end Receivable not reported

Missing Revenue

Results

Overstated local expenditures for MOE

Overstated local expenditures for MOE

Wisconsin Department of Public Instruction

Review of reports

Variances

Many variances between project 340 and claims

59

Many variances between project 340 and claims

NOT GOOD

Red flag that funds are not tracked appropriately

Could result in incorrect MOE

Could result in over/under state categorical aid

Could result in double dipping

Wisconsin Department of Public Instruction

Questions?60

Wisconsin Department of Public Instruction

Contacts

Kathy Guralski

61

Kathy Guralski

Federal Fiscal Monitoring Consultant

Wisconsin Department of Public Instruction

(608) 267-2947

Wisconsin Department of Public Instruction

Wisconsin Department of Public Instruction June, 2013 Page 1

COST REIMBURSED BY A FEDERAL AWARD

AND AUDITED UNDER OMB CIRCULAR A-133

Definitions

EDGAR - Education Department General Administrative Regulations; regulations for administering

discretionary and formula grants awarded by the US Department of Education.

Liquidation - to liquidate an obligation, the purchased item or service has occurred and payment has been

made to vendor or provider.

Obligation – the amount of orders placed, contracts and subgrants awarded, goods and services received, and

similar transactions during a given period that will require payment by the grantee during the same or a future

period.

OMB – United States Office of Management and Budget; the division of the Executive Office of the President

that prepares and administers the federal budget and improves management in the executive branch.

Obligating Funds EDGAR, Part 76.707, defines the initial period of availability for State-administered programs as July 1 to September

30th. EDGAR, Part 80.23 states that where a funding period is specified, a grantee may charge to the award only costs

resulting from obligations of the funding period unless carryover of unobligated balances is permitted, in which case

the carryover balances may be charged for costs resulting from obligations of the subsequent funding period. The

funding period for an LEA in Wisconsin is July 1 to June 30, so an LEA has until June 30 to obligate funds charged to

a federal award in the current year.

The following table is taken from EDGAR 76.707 regarding when obligations are made for various kinds of property

and services. The obligation needs to be made by June 30 to be a cost in the current year for the federal award.

If the obligation is for - The obligation is made -

(a) Acquisition of real or personal property On the date on which the State or subgrantee makes a

binding written commitment to acquire the property.

(b) Personal services by an employee of the State or

subgrantee

When the services are performed.

(c) Personal services by a contractor who is not an

employee of the State or subgrantee

On the date on which the State or subgrantee makes a

binding written commitment to obtain the services.

(d) Performance of work other than personal

services

On the date on which the State or subgrantee makes a

binding written commitment to obtain the work.

(e) Public utility services When the State or subgrantee receives the services.

(f) Travel When the travel is taken.

(g) Rental of real or personal property When the State or subgrantee uses the property.

(h) A preagreement cost that was properly approved

by the State under the cost principals identified

in 34 CFR 74.171 and 80.22

Liquidating Funds

Per EDGAR, Part 80.23, all obligations incurred within the funding period must be liquidated not later than 90 days

after the end of the funding period (or as specified in a program regulation). Accordingly, for Wisconsin LEAs, an

Wisconsin Department of Public Instruction June, 2013 Page 2

obligation that occurred in the current fiscal year prior to June 30 must be liquidated by September 30 to be charged to

a federal award in the current year.

Reimbursement

Reimbursement of the liquidated expenditure is made upon the filing of a claim with the department. Reimbursement

is not requested until the expenditure has occurred and has been paid for (liquidated). The final claim must be filed by

September 30th for the July 1 to June 30

th funding period just ended.

Recognizing an Expenditure in the General Ledger

Per the Wisconsin Uniform Financial Accounting Requirements, expenditure-driven programs currently reimbursable

are recognized as revenue when the qualifying expenditures have been incurred. Accordingly, an LEA would

recognize for state aid purposes, the expenditure when it has been incurred. The expenditure is incurred when the

related liability is incurred. So that would not be when the obligation is made or when the funds are spent, but rather

when the obligation has been met.

Recognizing an Expenditure for Federal Single Audit

Per OMB Circular A-133, determination of when an award is expended should be based on when the activity related to

the award occurs. Therefore costs are audited in the fiscal year that the actual expenditure or expense transaction

occurred.

Examples

In any given year, a variance can exist between a cost that is claimed for reimbursement on the federal award and the

cost that is reported in the general ledger or in the determination of a federal single audit. Following are examples and

how they would be treated for grant reimbursement, general ledger reporting and single audit purposes.

Grant General

Ledger

Fd-Function/Account-

Srce/Obj-Proj

Single

Audit

1) Summer School

Teacher funded by

Title I dollars

works July 15-30

Service has been

performed

Obligated

and

obligation

met

Subsequent

year

Debit 10E-XXXXXX-

100-14X Expenditure

Credit 10B-811800

Accrued Payroll Payable

Subsequent

year

The Teacher is

paid on August 15

Service has been

paid for

Liquidation Subsequent

year

Debit 10B-811800

Accrued Payroll Payable

Credit 10B-711000 Cash

Claim for

reimbursement

filed on September

30

Claim filed for

reimbursement by

September 30

Reimburse

ment

Subsequ

ent year

Subsequent

year

Debit 10B-715000 Due

from Other Governments

Credit 10R-7XX

Revenue from Federal

Sources

Wisconsin Department of Public Instruction June, 2013 Page 3

Grant General

Ledger

Fd-Function/Account-

Srce/Obj-Proj

Single

Audit

2) Contract is signed

June 28 for

remodeling of a

special education

room, an allowable

cost under the

IDEA grant

Contract is signed

with outside vendor

prior to June 30

Obligated

Work is performed

on August 20

Service performed

after June 30

Obligation

met Subsequent

year

Debit 27E-XXXXXX-

500-34X Expenditure

Credit 27B-811200

Accounts Payable

Subsequent

year

Payment is made

to the contractor

on September 10

Payment for service

made

Liquidation Subsequent

year

Debit 27B-10-811200

Accounts Payable

Credit 27B-711000

Cash

A claim is filed for

reimbursement on

September 30

Claim filed for

reimbursement by

September 30

Reimburse

ment from

current year

grant

Current

year

Subsequent

year

Debit 27B-715000 Due

from Other Governments

Credit 27R-7XX

Revenue from Federal

Sources

3) Textbooks are

ordered on June 15

to be used in the

subsequent school

year and to be

funded with Title I

dollars.

Commitment is

made with outside

vendor prior to June

30

Obligated

The books are

received on June

28

Goods received

prior to June 30

Obligation

met Subsequent

year

Debit 10E-XXXXXX-

400-141 Expenditure

Credit 10B-811200

Accounts Payable

Subsequent

year

Payment is made

to the vendor on

August 1

Payment for goods

made within 90 days

Liquidation Subsequent

year

Debit 10B-811200

Accounts Payable

Credit 10B-711000 Cash

A claim for

reimbursement is

made on

September 30

Claim filed for

reimbursement

Reimburse

ment

Current

year

Subsequent

year

Debit 10B-715000 Due

from Other Governments

Credit 10R-7XX

Revenue from Federal

Sources

4) On May 31, a

Special Education

Teacher signs up

for a conference to

be held in October

and the registration

fee is paid on the

same day.

Commitment is

made and payment

for the services is

made

Obligation

of the

conference

and

Liquidation

of the

registration

fee

Current

year

A claim for

reimbursement is

made on June 30

Claim filed for

reimbursement

Reimburse

ment

Current

year

Wisconsin Department of Public Instruction June, 2013 Page 4

Grant General

Ledger

Fd-Function/Account-

Srce/Obj-Proj

Single

Audit

5) The Special

Education Teacher

attends the

conference on

October 15

Service is performed

after the 90 days

Obligation

is met

Debit 10E-

221300/264400-940

Training Expenditure

Credit 10B-717000

Prepaid Expense

Subsequent

year

Teacher files an

employee expense

report

Subsequent

year

Prepaid Expense

Debit 10E-

221300/264400-342

Training Expenditure

Credit 10B-811200

Accounts Payable

Subsequent

year

The Teacher is

reimbursed for

travel on October

31

Payment for travel is

made after the 90

days

Liquidation Subsequent

year

Debit 10B-811200

Credit 10B-711000 Cash

A claim for

reimbursement is

made on

December 31

Claim filed for

reimbursement

Reimburse

ment

Subsequ

ent year

Subsequent

year

Debit 10B-715000 Due

from Other Governments

Credit 10R-7XX

Revenue from Federal

Sources